ACCT 2302 Fundamentals of Accounting II Spring 2011 Lecture 5 Professor Jeff Yu.

27

ACCT 2302 Fundamentals of Accounting II Spring 2011 Lecture 5 Professor Jeff Yu

-

Upload

edwin-elwin-reeves -

Category

Documents

-

view

214 -

download

0

Transcript of ACCT 2302 Fundamentals of Accounting II Spring 2011 Lecture 5 Professor Jeff Yu.

ACCT 2302

Fundamentals of Accounting II

Spring 2011

Lecture 5

Professor Jeff Yu

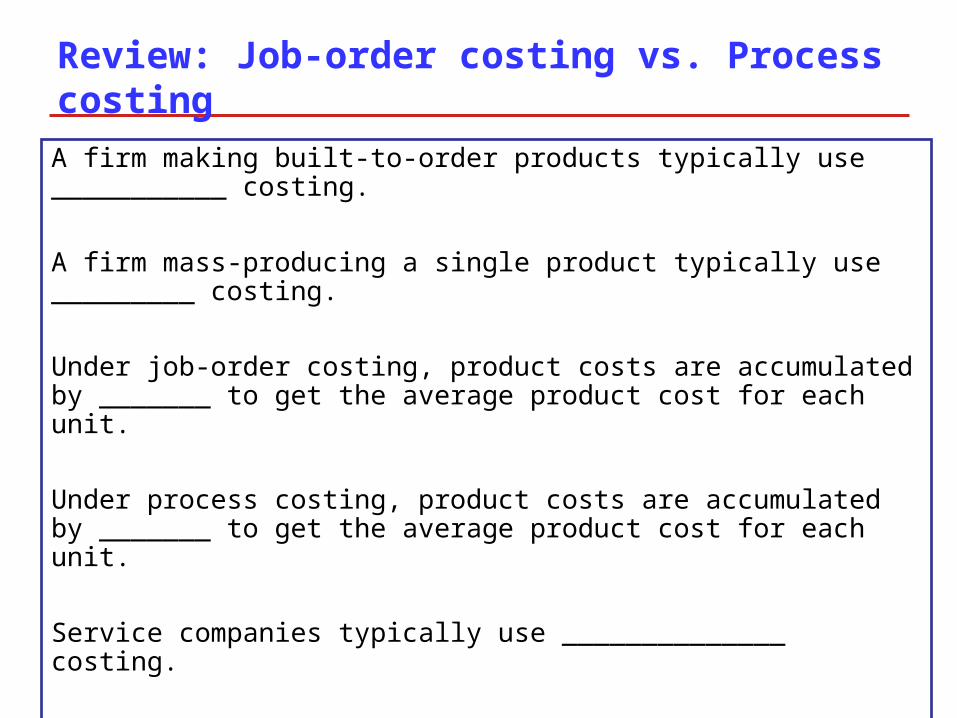

Review: Job-order costing vs. Process costing

A firm making built-to-order products typically use ___________ costing.

A firm mass-producing a single product typically use _________ costing.

Under job-order costing, product costs are accumulated by _______ to get the average product cost for each unit.

Under process costing, product costs are accumulated by _______ to get the average product cost for each unit.

Service companies typically use ______________ costing.

Both job-order costing and process costing are _______ costing systems.

Manufacturing overhead is applied (allocated) to individual jobs (work-in-process) based on a ___________ rate (POHR).

Review: MOH Application in job-order costing

POHR = Estimated total MOH cost / __________ total activity level

Applied MOH = POHR * ________ activity level

_______ MOH - Applied MOH

At the ________ of the period, calculate:

________ the period, calculate:

At the _______ of the period, calculate:

to determine whether MOH was underapplied or overapplied.

Review: Job-Order Costing

1. If Applied MOH>Actual MOH, then MOH is ________ for the period.

If Applied MOH<Actual MOH, then MOH is __________ for the period.

2. What is the journal entry to apply MOH to jobs during the period?

3. What is the adjusting journal entry to close the overapplied (underapplied) MOH to CGS at the end of the period?

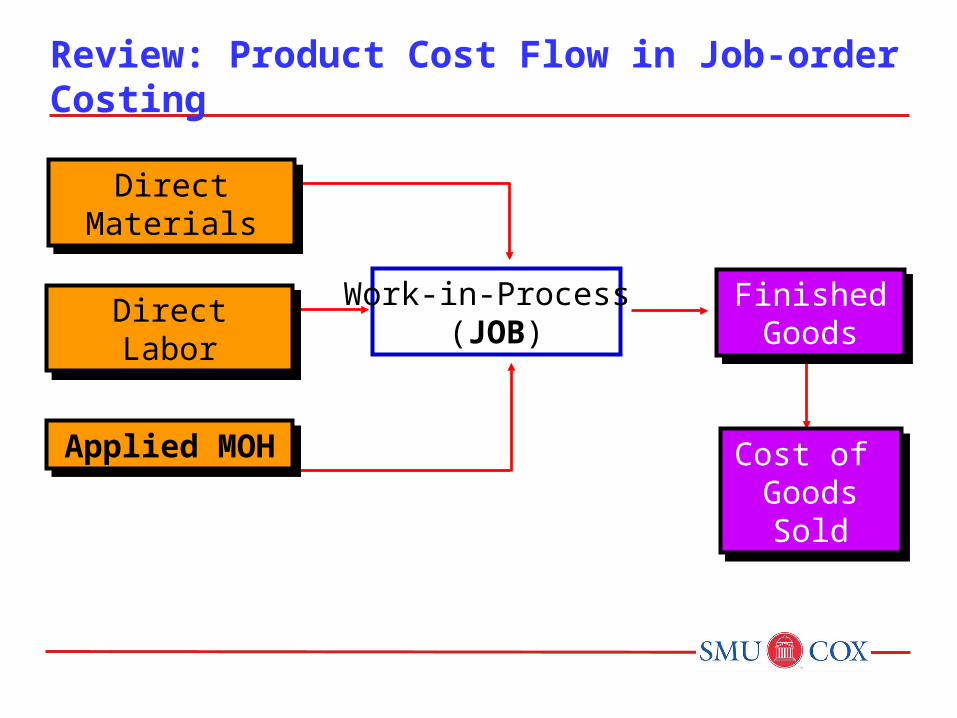

Review: Product Cost Flow in Job-order Costing

FinishedGoods

FinishedGoods

Cost of GoodsSold

Cost of GoodsSold

Direct LaborDirect Labor

Applied MOH

Applied MOH

Direct MaterialsDirect

Materials

Work-in-Process (JOB)

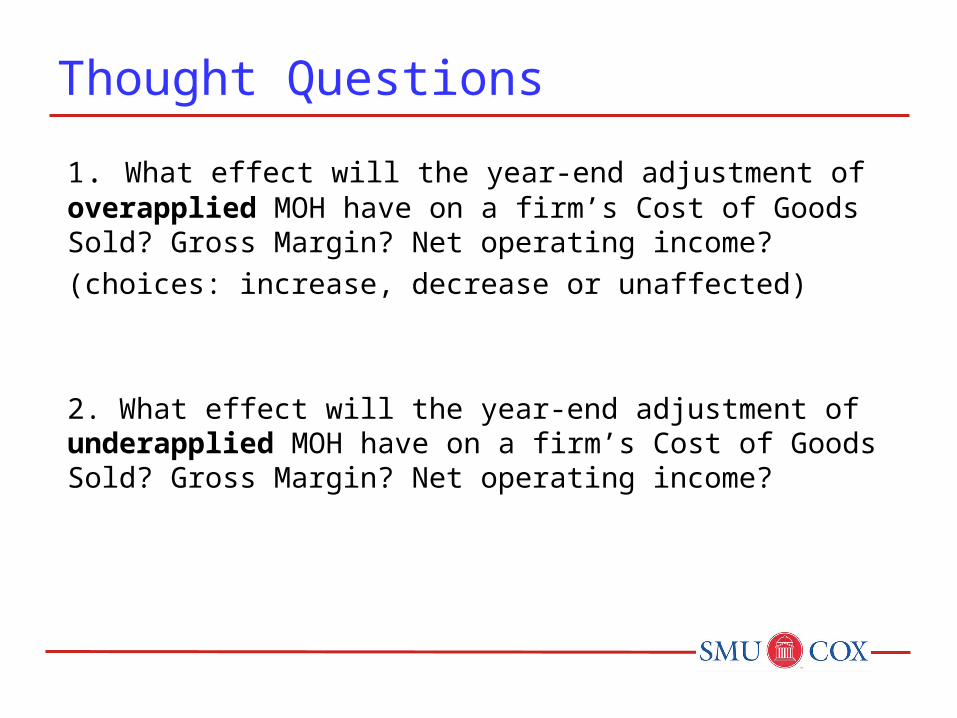

Thought Questions

1. What effect will the year-end adjustment of overapplied MOH have on a firm’s Cost of Goods Sold? Gross Margin? Net operating income?

(choices: increase, decrease or unaffected)

2. What effect will the year-end adjustment of underapplied MOH have on a firm’s Cost of Goods Sold? Gross Margin? Net operating income?

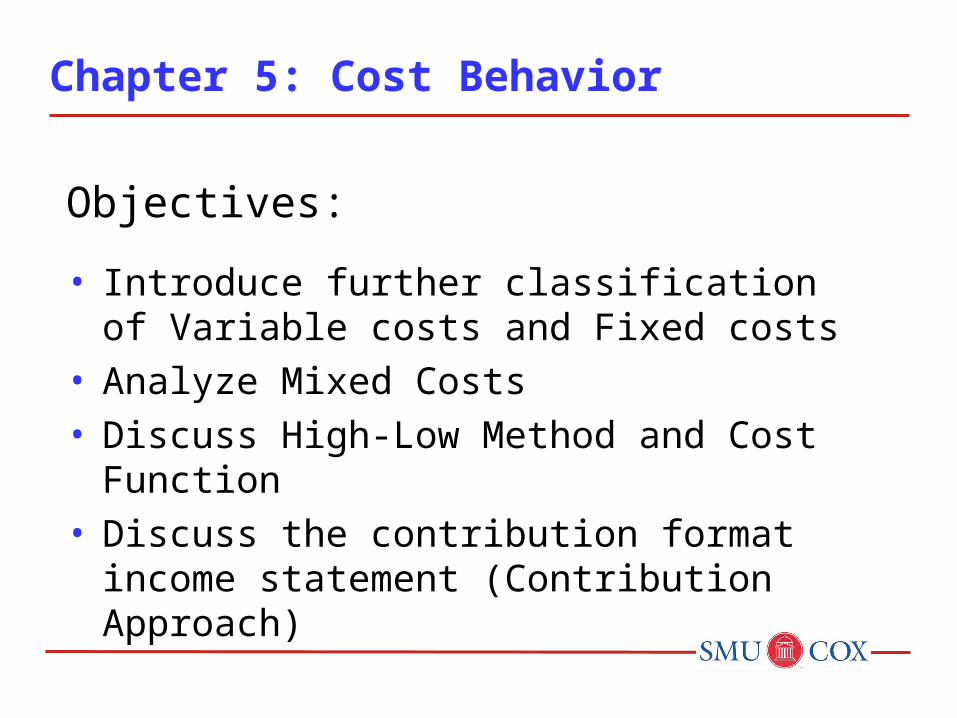

Objectives:

• Introduce further classification of Variable costs and Fixed costs

• Analyze Mixed Costs• Discuss High-Low Method and Cost Function• Discuss the contribution format income

statement (Contribution Approach)

Chapter 5: Cost Behavior

Review: The Activity Base (Cost Driver)

A measure of what causes the incurrence of a variable cost

A measure of what causes the incurrence of a variable cost

Unitsproduce

d

Unitsproduce

d

Miles drivenMiles driven

Labor hoursLabor hours

Machine hours

Machine hours

RelevantRange

A straight line closely

approximates a curvilinear variable cost

line within the relevant range.

A straight line closely

approximates a curvilinear variable cost

line within the relevant range.

Activity

Tota

l C

ost

Economist’sCurvilinear

Cost Function

Review: Relevant Range

Accountant’s Straight-Line Approximation

(constant unit variable cost)

Review: Cost Behavior

In Total Per Unit

Variable Cost

Fixed Cost

Within the Relevant Range, how will each of the followingcost change as activity level increases (decreases)?

Units Produced

DM

Cost

True Variable Cost

For example, Direct Material is typically a true variable cost because the amount used during a period will vary in direct proportion to the level of production activity.

Step-Variable Cost

Costs increase or decrease only in response to fairly wide changes in activity.

Volume

Cost

Activity

Cost

Total cost remainsconstant within anarrow range of

activity

Total cost increases to a new higher cost for the next

higher range of activity

Step-Variable Cost

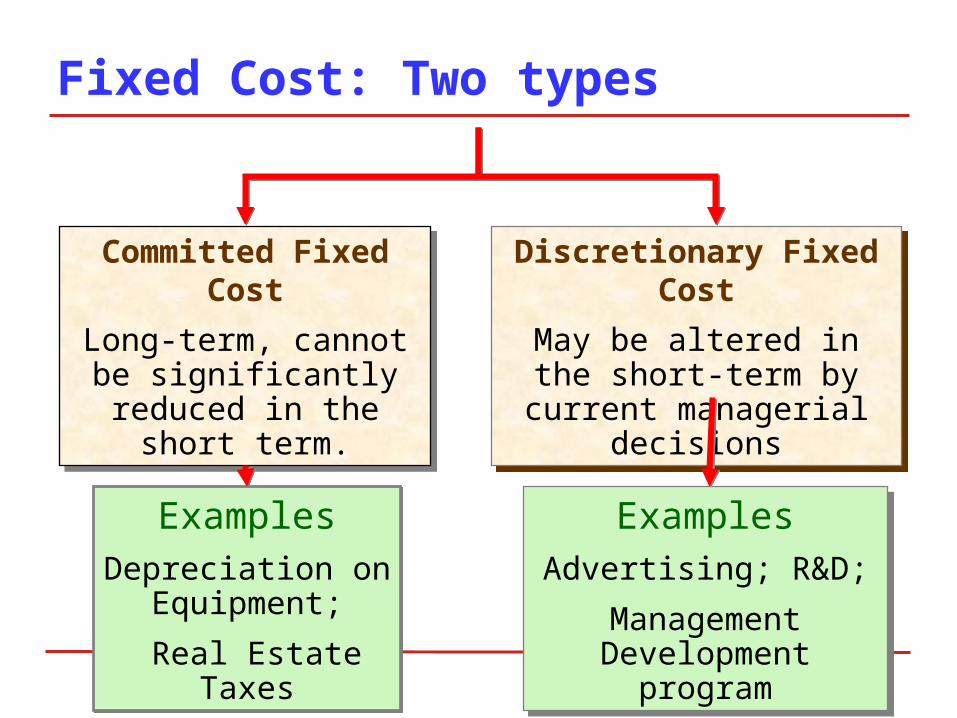

ExamplesAdvertising; R&D;

Management Development

program

ExamplesAdvertising; R&D;

Management Development

program

ExamplesDepreciation on

Equipment;

Real Estate Taxes

ExamplesDepreciation on

Equipment;

Real Estate Taxes

Fixed Cost: Two types

Discretionary Fixed Cost

May be altered in the short-term by current managerial decisions

Discretionary Fixed Cost

May be altered in the short-term by current managerial decisions

Committed Fixed Cost

Long-term, cannot be significantly reduced

in the short term.

Committed Fixed Cost

Long-term, cannot be significantly reduced

in the short term.

Fixed Monthly

Utility Charge

Variable Cost based on the

usage

Activity (Kilowatt Hours)

Tota

l U

tilit

y

Cost

X

Y

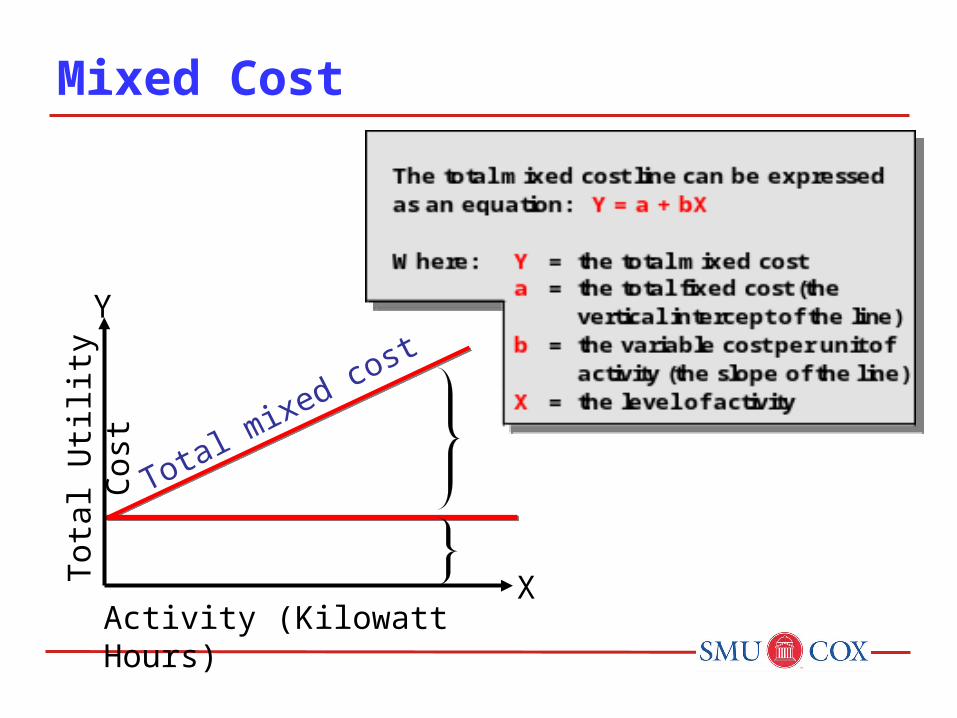

A mixed cost has both fixed and variablecomponents. Consider the example of utility cost.

Mixed Cost

Total mixed cost

Activity (Kilowatt Hours)

Tota

l U

tilit

y

Cost

X

Y

Mixed Cost

Total mixed cost

Mixed Cost Example

TXU charges a fixed monthly fee of $20 plus $0.1 per kilowatt hour. In March you used 2,000 kilowatt hours.

Q: 1) What is the amount of your electricity bill for March?

2) What is the average cost per kilowatt hours for March?

3) What will be the average cost per kilowatt hours for April if you only use 1,000 kilowatt hours?

Practice…Hospital Costs

True variable, step variable, mixed, discretionary fixed or committed fixed?

• Spending on medical student internship• Nursing supervisor salaries – supervisor needed for

every 10 nursing personnel• Operating costs of x-ray equipment ($95,000 per year

plus $3 per film)• Insurance for all full time employees

Y = a + bX

Total Cost Activity Level(Cost Driver)

Variable Cost per Unit Total Fixed Costs

Cost Function

Q: what can we say about a and b for each of the costs below1)True variable cost; 2) Fixed Cost; 3) Mixed Cost

For each of the costs below, please specify whether it is a Fixed Cost, True Variable Cost, Mixed Cost, or Step Variable Cost?

Example

Activity Level within relevant range

100 Units 200 Units 250 Units

Cost A $200 $400 $500

Cost B $350 $550 $650

Cost C $300 $300 $600

Cost D $150 $150 $150

(1) Choose the two data points with the highest- and the lowest- activity level: (XH, YH), (XL,YL)

(2) Set up the equations: YH = a + b XH

YL = a + b XL

(3) Solve the equation for “a” (total fixed cost) and “b” (VC per unit):

b = (YH-YL)/(XH-XL)

= change in cost / change in activity

a = YL – b*XL

Estimate Cost Function: the High-low Method

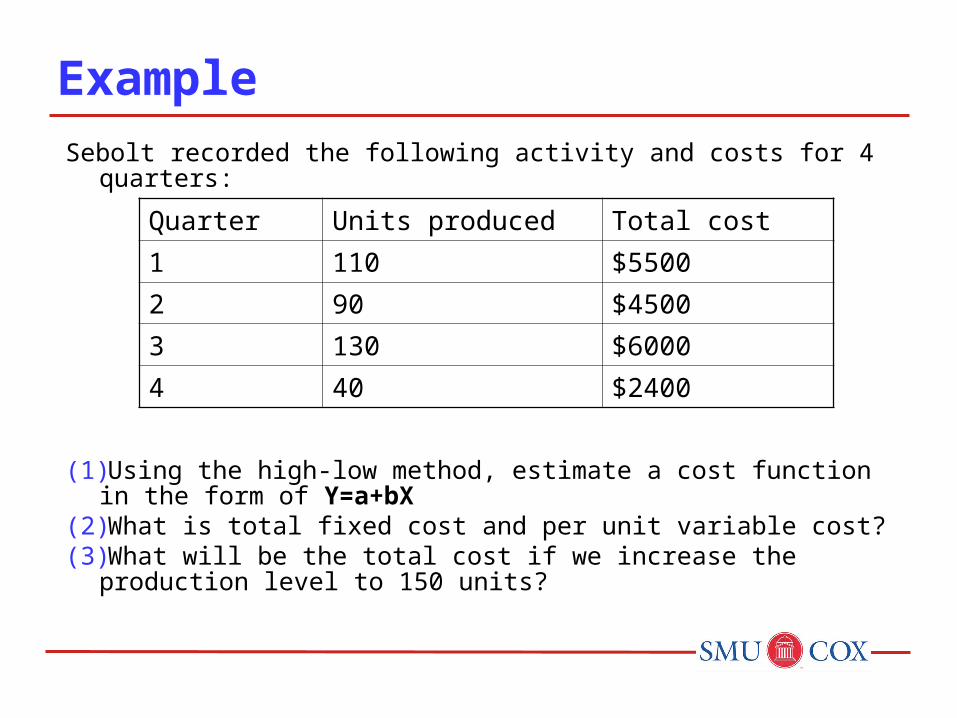

Sebolt recorded the following activity and costs for 4 quarters:

(1)Using the high-low method, estimate a cost function in the form of Y=a+bX

(2)What is total fixed cost and per unit variable cost?(3)What will be the total cost if we increase the production level to 150

units?

Example

Quarter Units produced Total cost

1 110 $55002 90 $45003 130 $60004 40 $2400

For Next Class

Complete assigned readings We will finish Chapter 5 with the contribution

format income statement, and start Chapter 6: CVP analysis

Attempt the assigned HW problems We will work on a lot of problems next class!

Homework Problem 1

Neptune Rental operates a boat rental service and its relevant range is 5,000 to 8,000 hours of operating time.When the boats were operated for 6,000 hours, Neptune’s total costs were $192,000, among which $168,000 was total fixed cost.

Q: If it is estimated that on Saturday the boats will be operated for 8,000 hours, what will be the estimated average cost per hour?

Q: Identify each of the expenses above as either fixed, true variable or mixed (assume there is no step variable cost).

Homework Problem 2

July AugustSales in units 11,000 10,000Sales $165,000 $150,000Cost of goods sold 72,600 66,000Gross margin 92,400 84,000Selling and administrative expenses:Rent 12,000 12,000Sales commissions 13,200 12,000Maintenance expenses 13,500 13,000Clerical expense 16,000 15,000

Total selling and administrative expense 54,700 52,000

Net operating income $ 37,700 $ 32,000

Comparative income statements for Boggs Co. for the last two months are presented below.

Bakeman Corporation has provided the following production and average cost data for two levels (highest and lowest) of monthly production volume. The company produces a single product.

Homework Problem 3

2,000 units 3,000 unitsAverage DM cost

$36.10 per unit $36.10 per unitAverage DL cost

$48.00 per unit $48.00 per unitAverage MOH cost $51.00 per unit $40.90 per unit

Q: 1) Identify the cost behavior of DM, DL and MOH as fixed, true variable or mixed.

2) What is the best estimate of Variable MOH cost per unit? 3) What is the cost function for total manufacturing cost?

Golden Co’s MOH costs consists of utilities (true variable), supervisory salaries (fixed) and maintenance (mixed). At 40,000 machine hours, the breakdown of overhead costs are $52,000 for utilities, $60,000 for supervisory salaries and $58,200 for maintenance.

(1)How much of the $241,600 MOH cost in June was maintenance cost?(2)Use high-low method to estimate cost function of maintenance cost.(3)Use high-low method to estimate cost function of total MOH cost.

Homework Problem 4

Month Machine Hours Total MOH cost

March 50,000 $194,000

April 40,000 $170,200

May 60,000 $217,800

June 70,000 $241,600

![C SYLLABUS [FALL 2016] 3315 - University of Texas …...decision-making. Prerequisites: Principles of Managerial Accounting (ACCT 2302) HE UNIVERSITY OF TEXAS AT YLER COLLEGE OF BUSINESS](https://static.fdocuments.us/doc/165x107/5f11bb4f6c1ee863876830f3/c-syllabus-fall-2016-3315-university-of-texas-decision-making-prerequisites.jpg)