ACCT 2302 Fundamentals of Accounting II Spring 2011 Lecture 6 Professor Jeff Yu.

19

ACCT 2302 Fundamentals of Accounting II Spring 2011 Lecture 6 Professor Jeff Yu

-

Upload

sharon-richard -

Category

Documents

-

view

222 -

download

0

Transcript of ACCT 2302 Fundamentals of Accounting II Spring 2011 Lecture 6 Professor Jeff Yu.

ACCT 2302

Fundamentals of Accounting II

Spring 2011

Lecture 6

Professor Jeff Yu

Review: Cost Behavior

True Variable Cost (a=0, b>0)Total cost: Y=bX, increases with XUnit cost: Y/X=b, constant

Fixed Cost (a>0, b=0)Total cost: Y=a, constantUnit cost: Y/X=a/X, decreases with X

Mixed Cost (a>0, b>0)Total cost: Y=a+bX, increases with XUnit cost: Y/X=a/X + b, decreases with activity level X.

(1) Select the highest- & the lowest- activity levels: Xh, Xl

(2) Fit a line through the two data points: (Xh, Yh), (Xl, Yl)

Yh =a + bXh b=(Yh - Yl)/(Xh - Xl)

Yl =a + bXl a= ?

The slope of the line: b = Variable Cost per unit

The intercept of the line: a = Total Fixed Cost

Review: Cost Function & High-low Method

Cost Function: Y = a + bX

Used primarily forexternal reporting

Used primarily for Managerial Decision making

The Contribution Format Income Statement

Total Unit

Sales 100,000$ 50$

Less: Variable costs 60,000 30

Contribution margin 40,000$ 20$

Less: Fixed costs 30,000

Net income 10,000$

The contribution format emphasizes cost behavior. Contribution Margin (CM) covers fixed costsand then contributes to net operating income.

The Contribution Format Income Statement

Q: Prepare a contribution margin format income statement for August.

Example

July AugustSales in units 11,000 10,000Sales $165,000 $150,000Cost of goods sold 72,600 66,000Gross margin 92,400 84,000Selling and administrative expenses:Rent 12,000 12,000Sales commissions 13,200 12,000Maintenance expenses 13,500 13,000Clerical expense 16,000 15,000

Total S&A expense 54,700 52,000Net operating income $ 37,700 $ 32,000

Comparative income statements for Boggs Co. for the last two months are presented below (assume all costs are either fixed, true variable or mixed):

The 2010 income statement for Janna Company is as follows:

Sales $1,600,000Less: Cost of goods sold $1,200,000Gross Margin $ 400,000Less: Selling expenses $ 196,000 Administrative expenses $ 98,000Net Income $ 106,000

The price of the product is $50 per unit and CGS is entirely variable. Variable selling expenses are $5.5 per unit. The remaining selling expenses are fixed. Variable administrative expenses are 2% of CGS. The remaining administrative expenses are fixed.

Q: (1) What is the contribution margin for year 2010? (2) Let X be the number of units sold, what is the cost function for total S&A expenses?

Practice Problem

Break-even point is the amount of units needed to be sold to make the company’s revenues equal to expenses (NOI = 0).

Sales $250,000 Less: Variable Expenses 150,000 Contribution Margin $100,000 Less: Fixed Expenses 100,000 Net Operating Income 0

Chapter 6: CVP Analysis

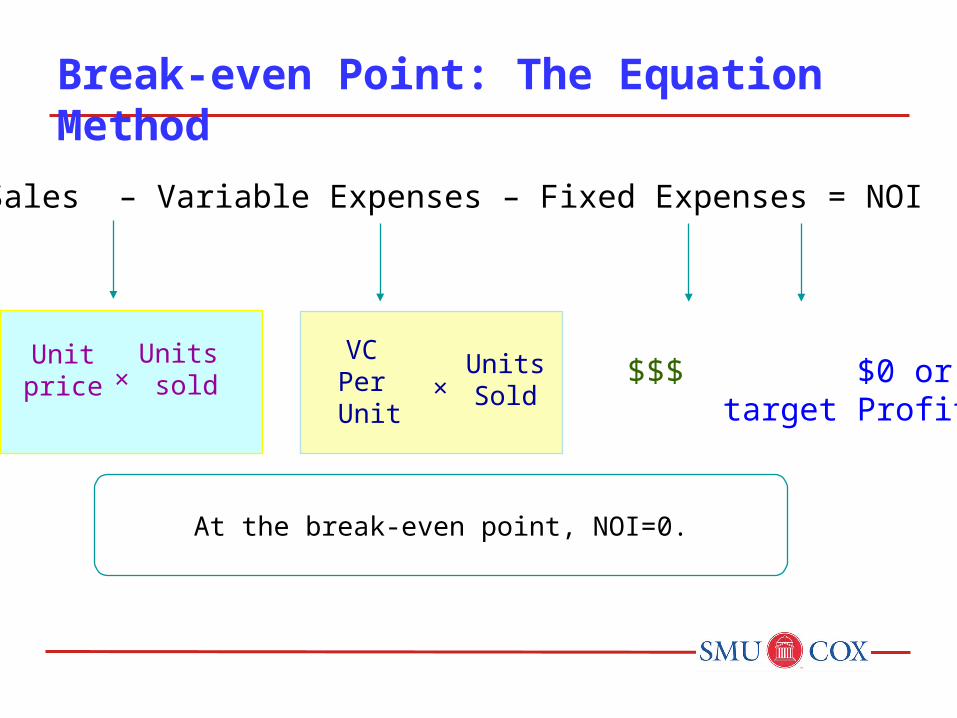

Sales – Variable Expenses – Fixed Expenses = NOI

Unitprice

Units sold×

VC Per Unit

UnitsSold×

At the break-even point, NOI=0.

$$$ $0 or target Profit

Break-even Point: The Equation Method

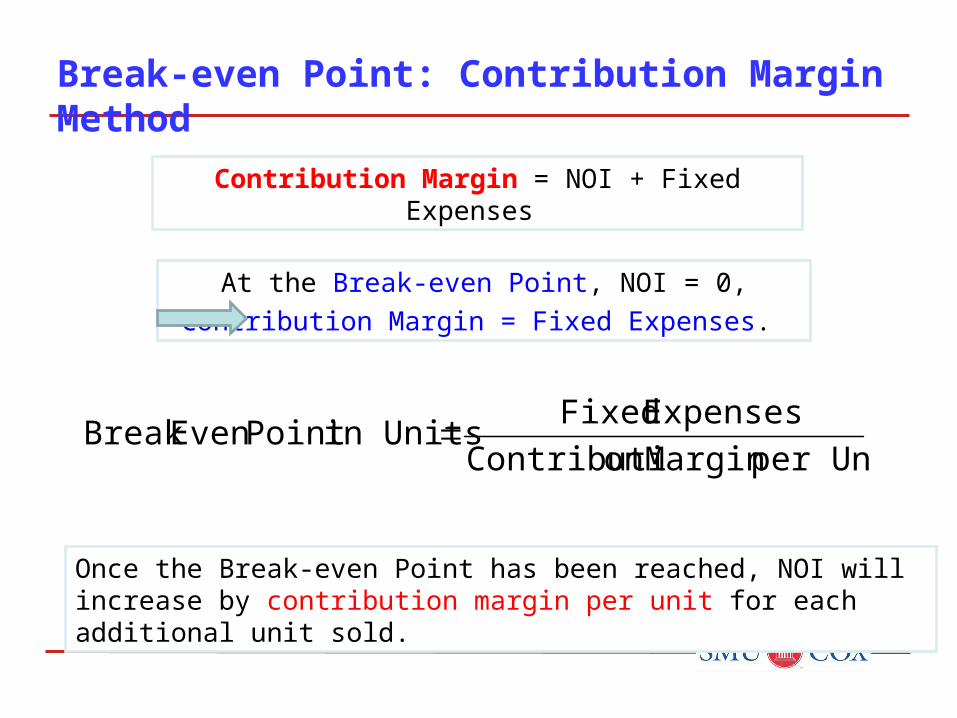

Contribution Margin = NOI + Fixed Expenses

Once the Break-even Point has been reached, NOI will increase by contribution margin per unit for each additional unit sold.

At the Break-even Point, NOI = 0,

Contribution Margin = Fixed Expenses.

Break-even Point: Contribution Margin Method

per UnitMargin on Contributi

Expenses Fixedin UnitsPoint Even Break

Total Per Unit PercentSales (500 scooters) 250,000$ Less: variable expensesContribution margin

Less: fixed expenses 80,000 Net Operating Income 20,000$

Total Per Unit PercentSales (500 scooters) 250,000$ Less: variable expensesContribution margin

Less: fixed expenses 80,000 Net Operating Income 20,000$

Consider Razor Inc, a scooter manufacturer. For each additional scooter sold, Razor Inc. generates $200 in contribution margin.

Example

Q: calculate the break-even point in units for Razor Inc.

We can calculate the break-even point in sales dollars rather than in units using the Contribution-Margin (CM) ratio.

Sales

CMRatio CM

Ratio CM

Expenses FixedDollars Sales in Point Even Break

Break Even Point in Sales Dollars

What is the break-even point in Sales Dollars for Razor Inc.?

CM = Fixed Expensesat the break-even point

Target Profit: CM Approach

Original formula:

Target profit modification:

per Unit CM

Expenses Fixedin UnitsPoint Even Break

per Unit CM

ProfitTarget Expenses FixedProfitTarget attain tosales Units

We can determine the number of scooters that Razor must sell to earn a target profit of $100,000 by slightly modifying the break-even point formula:

Sales revenue – Variable expenses – Fixed expenses = NOI

($500 × X) ($300 × X)– – $80,000 = $100,000

($200X) = $180,000

X = 900 units

Target Profit: Equation Approach

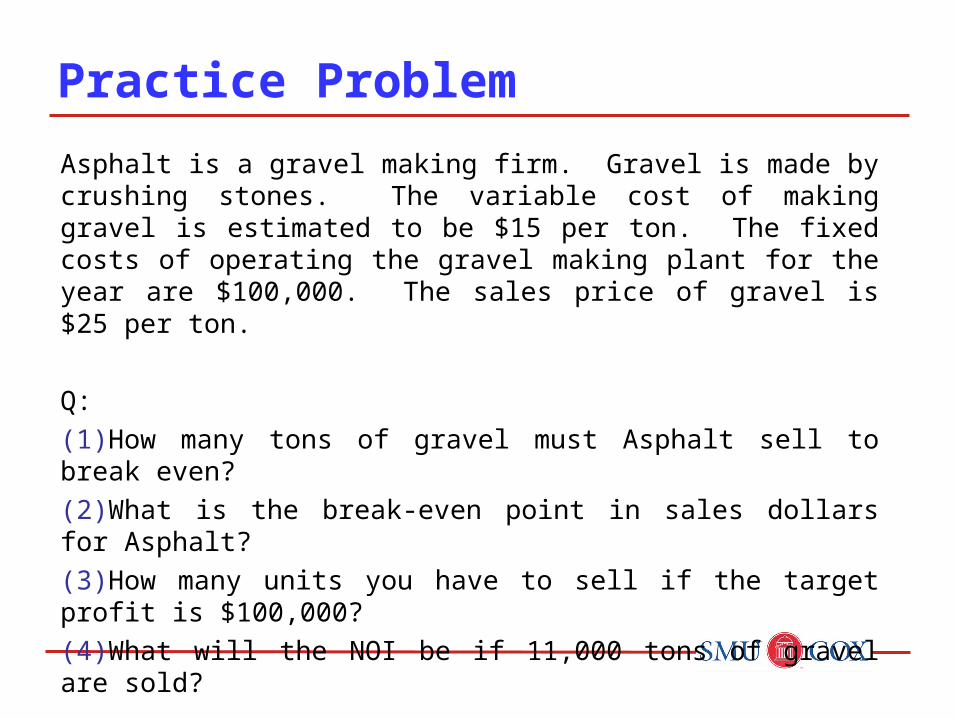

Asphalt is a gravel making firm. Gravel is made by crushing stones. The variable cost of making gravel is estimated to be $15 per ton. The fixed costs of operating the gravel making plant for the year are $100,000. The sales price of gravel is $25 per ton.

Q:

(1)How many tons of gravel must Asphalt sell to break even?

(2)What is the break-even point in sales dollars for Asphalt?

(3)How many units you have to sell if the target profit is $100,000?

(4)What will the NOI be if 11,000 tons of gravel are sold?

Practice Problem

For Next Class

Continue covering Chapter 6. Complete assigned readings. Attempt the assigned HW problems.

Homework Problem 1

Units Sold Unit Price

VC per unit

CM per unit

Total CM Total fixed costs

NOI

120,000 $30 $720,000 $640,000

100,000 $6 $4 $320,000

80,000 $9 $160,000 $40,000

Fill in the blanks of the following table:

In 2010, Voltar Co. sold 20,000 units of a special telephone at $60 each, variable expenses were $900,000 and fixed expenses were $240,000.

Q:(1) Compute its CM ratio and variable expense ratio.

(2) Compute its break-even point in units and sales dollars.

(3) How many units have to be sold to earn a profit of $90,000 in 2011?

Homework Problem 2

Air Safety Systems manufactures a component used in aircraft radar systems. The firm’s fixed costs are $4,000,000 per year. The variable cost per unit is $2,000 and the sales price is $3,000 per component. The company sold 5,000 components in 2010.

Q: (1) What is the breakeven point in units? (2) What is the breakeven point in units if fixed costs increase 10%? (3) What if sales price and VC per unit both decrease 10%, while other things remain unchanged?

The sales manager believes that reducing sales price to $2,500 per unit will increase the sales volume to 7,500 components. (4) What will the new break-even point in units be? Should the change be made?

Homework Problem 3