Risperdal Lawsuit Loan Funding - Risperdal Lawsuit Settlements

Upload

northdecoderCategory

view

221download

0

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 1/45

Empower the Taxpayer Complaint – page 1

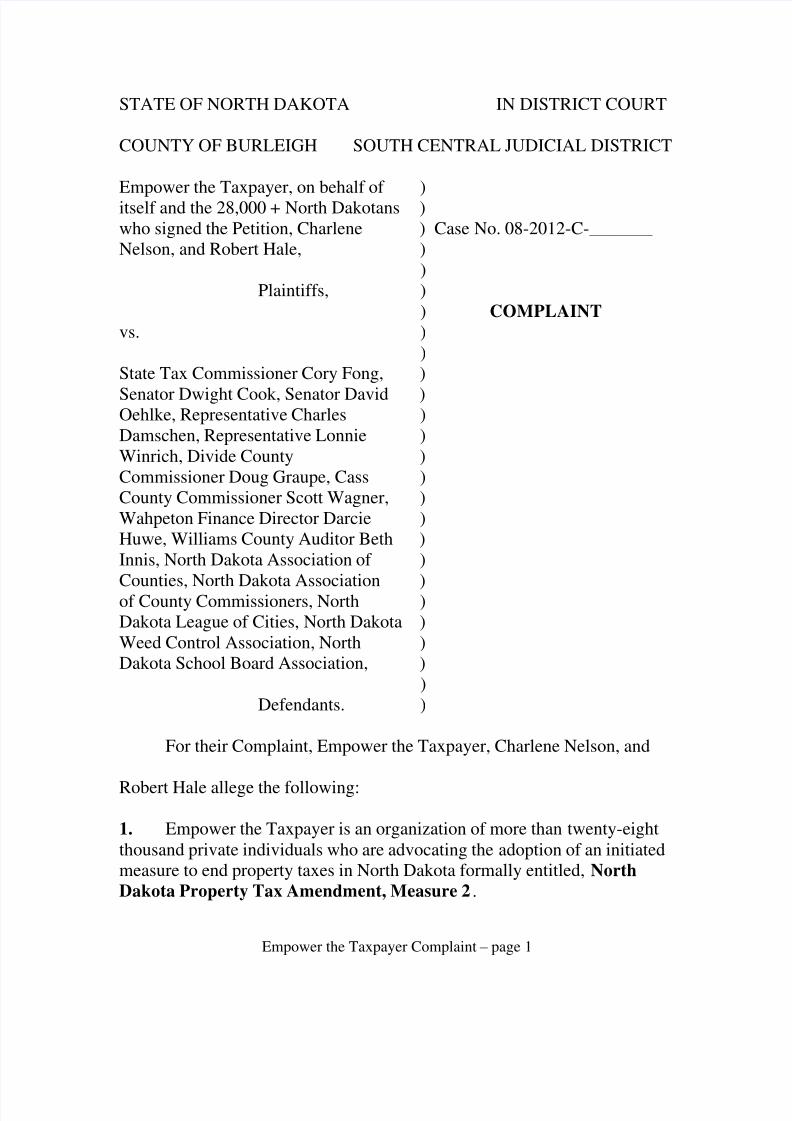

STATE OF NORTH DAKOTA IN DISTRICT COURT

COUNTY OF BURLEIGH SOUTH CENTRAL JUDICIAL DISTRICT

Empower the Taxpayer, on behalf of )itself and the 28,000 + North Dakotans )who signed the Petition, Charlene ) Case No. 08-2012-C-_______Nelson, and Robert Hale, )

)Plaintiffs, )

) COMPLAINTvs. )

)State Tax Commissioner Cory Fong, )

Senator Dwight Cook, Senator David )Oehlke, Representative Charles )Damschen, Representative Lonnie )Winrich, Divide County )Commissioner Doug Graupe, Cass )County Commissioner Scott Wagner, )Wahpeton Finance Director Darcie )Huwe, Williams County Auditor Beth )Innis, North Dakota Association of )Counties, North Dakota Association )of County Commissioners, North )Dakota League of Cities, North Dakota )Weed Control Association, North )Dakota School Board Association, )

)Defendants. )

For their Complaint, Empower the Taxpayer, Charlene Nelson, and

Robert Hale allege the following:

1. Empower the Taxpayer is an organization of more than twenty-eightthousand private individuals who are advocating the adoption of an initiatedmeasure to end property taxes in North Dakota formally entitled, NorthDakota Property Tax Amendment, Measure 2.

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 2/45

Empower the Taxpayer Complaint – page 2

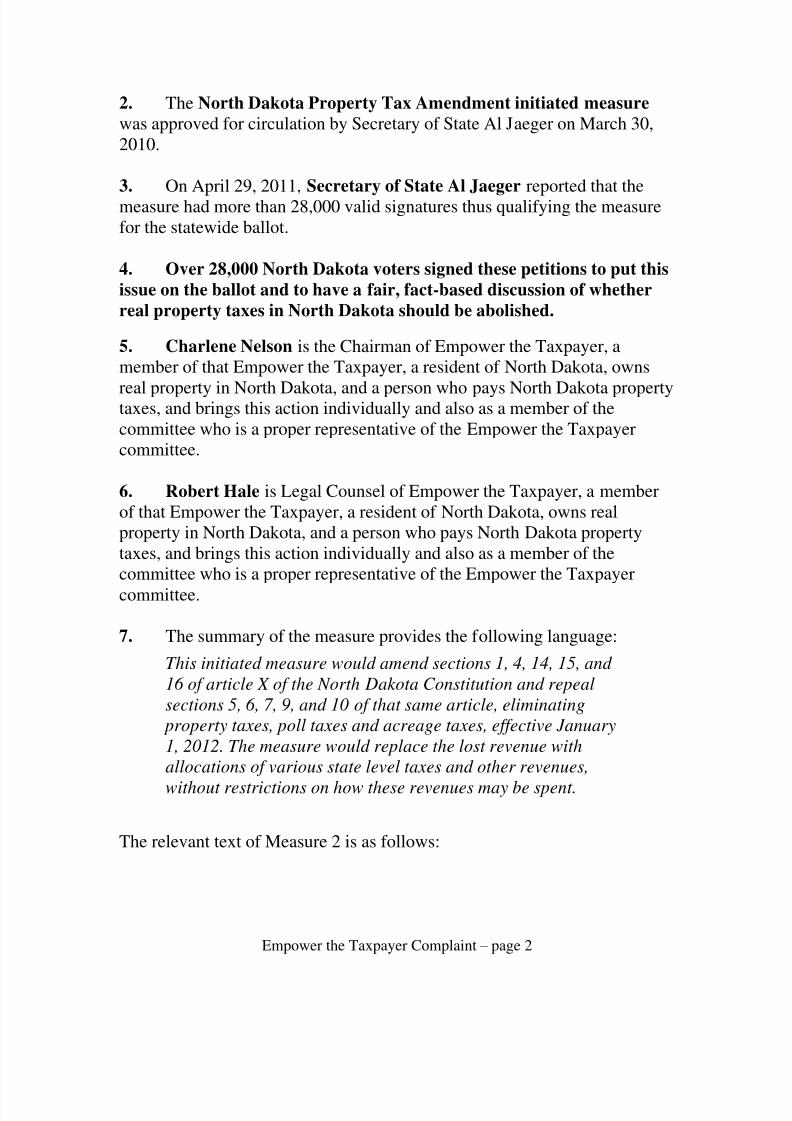

2. The North Dakota Property Tax Amendment initiated measurewas approved for circulation by Secretary of State Al Jaeger on March 30,2010.

3. On April 29, 2011, Secretary of State Al Jaeger reported that themeasure had more than 28,000 valid signatures thus qualifying the measurefor the statewide ballot.

4. Over 28,000 North Dakota voters signed these petitions to put thisissue on the ballot and to have a fair, fact-based discussion of whetherreal property taxes in North Dakota should be abolished.

5. Charlene Nelson is the Chairman of Empower the Taxpayer, amember of that Empower the Taxpayer, a resident of North Dakota, owns

real property in North Dakota, and a person who pays North Dakota propertytaxes, and brings this action individually and also as a member of thecommittee who is a proper representative of the Empower the Taxpayercommittee.

6. Robert Hale is Legal Counsel of Empower the Taxpayer, a memberof that Empower the Taxpayer, a resident of North Dakota, owns realproperty in North Dakota, and a person who pays North Dakota propertytaxes, and brings this action individually and also as a member of thecommittee who is a proper representative of the Empower the Taxpayer

committee.

7. The summary of the measure provides the following language:

This initiated measure would amend sections 1, 4, 14, 15, and

16 of article X of the North Dakota Constitution and repeal

sections 5, 6, 7, 9, and 10 of that same article, eliminating

property taxes, poll taxes and acreage taxes, effective January

1, 2012. The measure would replace the lost revenue with

allocations of various state level taxes and other revenues,

without restrictions on how these revenues may be spent.

The relevant text of Measure 2 is as follows:

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 3/45

Empower the Taxpayer Complaint – page 3

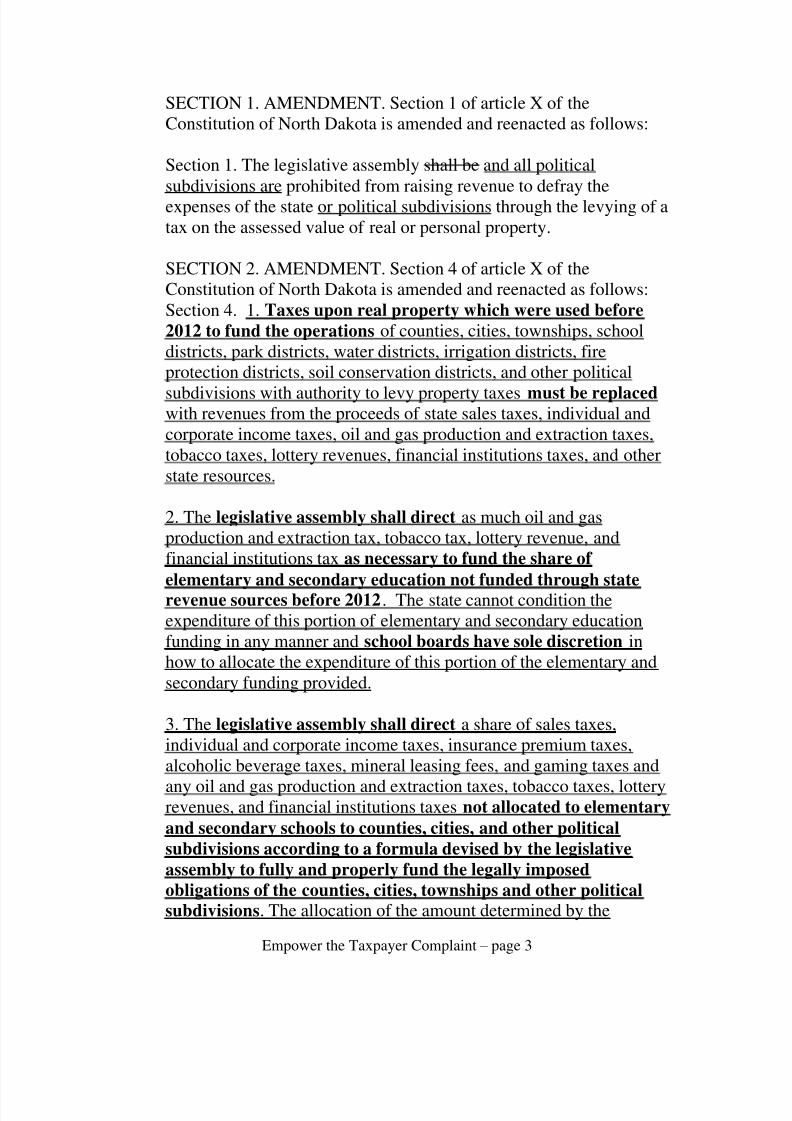

SECTION 1. AMENDMENT. Section 1 of article X of theConstitution of North Dakota is amended and reenacted as follows:

Section 1. The legislative assembly shall be and all politicalsubdivisions are prohibited from raising revenue to defray theexpenses of the state or political subdivisions through the levying of atax on the assessed value of real or personal property.

SECTION 2. AMENDMENT. Section 4 of article X of theConstitution of North Dakota is amended and reenacted as follows:Section 4. 1. Taxes upon real property which were used before2012 to fund the operations of counties, cities, townships, schooldistricts, park districts, water districts, irrigation districts, fireprotection districts, soil conservation districts, and other political

subdivisions with authority to levy property taxes must be replaced with revenues from the proceeds of state sales taxes, individual andcorporate income taxes, oil and gas production and extraction taxes,tobacco taxes, lottery revenues, financial institutions taxes, and otherstate resources.

2. The legislative assembly shall direct as much oil and gasproduction and extraction tax, tobacco tax, lottery revenue, andfinancial institutions tax as necessary to fund the share of elementary and secondary education not funded through staterevenue sources before 2012. The state cannot condition theexpenditure of this portion of elementary and secondary educationfunding in any manner and school boards have sole discretion inhow to allocate the expenditure of this portion of the elementary andsecondary funding provided.

3. The legislative assembly shall direct a share of sales taxes,individual and corporate income taxes, insurance premium taxes,alcoholic beverage taxes, mineral leasing fees, and gaming taxes and

any oil and gas production and extraction taxes, tobacco taxes, lotteryrevenues, and financial institutions taxes not allocated to elementaryand secondary schools to counties, cities, and other politicalsubdivisions according to a formula devised by the legislativeassembly to fully and properly fund the legally imposedobligations of the counties, cities, townships and other politicalsubdivisions. The allocation of the amount determined by the

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 4/45

Empower the Taxpayer Complaint – page 4

legislative assembly must be provided to the governing bodies of counties, cities, townships, and other political subdivisions. Howcounties, cities, townships, and other political subdivisions choose toallocate the expenditures of this revenue is at the sole direction of thegoverning bodies of counties, cities, townships, and other politicalsubdivisions.

Underlines in Original, bold added. The complete Measure 2 isprovided as ATTACHMENT 1.

I. The Truth – What Measure 2 Says and What it is About

8. The Real Effect of Measure 2: No One’s House can be Taken by

the Government for Failure to Pay a Tax to the Government.

Empower the Taxpayer and 28,000 plus North Dakota voters initiatedMeasure 2, the measure to eliminate property taxes to:a. Allow citizens to ACTUALLY own their home and not have to

perpetually pay “rent” to the government or face having the

government foreclose and take our home.

b. End an abusive, complex, expensive, and broken tax mechanism that

benefits special interests while penalizing those who are not

politically connected.

c. Stimulate true economic development diversifying North Dakota’s

economy and creating private sector jobs.

9. Measure 2: A Thoroughly and Well-Reasoned MeasureSome of the opponents listed above assert that Measure 2 is, “A poorlyconceived idea.” This is simply untrue.

Point 1: Assistance by Legislative Council in Drafting Measure TheMeasure, like many such measures submitted to the people of NorthDakota by the Legislature, received input and was drafted byprofessionals and lawyers of the Legislative Council.

Point 2: Prior Study and Detailed Review by Proponents In additionto Legislative Council input, the proponents of the Measure spentconsiderable time studying property taxes and the issues that need to beaddressed in the Measure and other issues that will come up upon itspassage. The proponents actually wrote and published a book going over

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 5/45

Empower the Taxpayer Complaint – page 5

all of these issues.1 The reviews of the book, and statements made insupport of Measure 2 in the book, demonstrate professional opinionsfrom well-qualified persons relating to the value and actual impact of implementation of Measure 2.

Point 3: Proponents Commissioned a Fiscal Impact Study by anEntity Used by the State for Just such Studies In addition, theproponents actually commissioned a study by Beacon Hill, an entity thatthe State of North Dakota hires to do financial impact studies for theState. According to the Beacon Hill study, the fiscal impact of Measure2 will be it will actually save money, more than would have been broughtin via property taxes.

10. Measure 2: Enhancing Local Control , Not Taking it Away Some

of the opponents listed above assert that Measure 2 takes away local controland provides for all decision-making to occur in Bismarck. The opposite istrue.

Point 1: The Measure Specifically Provides for the Funding of Counties, Cities, Townships, and Other Political Subdivisions andAllocates “Sole Direction” to Local Authorities on How to Distributethose Funds The Measure specifically provides that any local entityoperations previously funded through property taxes “must be replacedwith revenues from the proceeds of state sales taxes, individual andcorporate income taxes, oil and gas production and extraction taxes,tobacco taxes, lottery revenues, financial institutions taxes, and otherstate resources.” The Measure specifically provides that these politicalsubdivisions are granted “sole direction” in how to allocate those funds.The state’s only control is the development of a state- wide formulawhich will be used to determine the amount certain to fully and properlyfund what political subdivisions will receive.

Point 2: The Legislature is Obligated to Fund Elementary and

Secondary Education and Prohibits the State from Conditioning theExpenditure of this Money by Providing for “Sole Discretion” by

School Boards in Distribution and Expenditure of those Funds TheMeasure specifically requires funding of elementary and secondary

1 Hale, Narloch, & Nelson, PROPERTY TAX REVOLUTION (2012). The book isattached as ATTACHMENT 6.

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 6/45

Empower the Taxpayer Complaint – page 6

education, and specifically provides that the state cannot condition theexpenditure of these monies and must provide school boards with “solediscretion” in how to allocate the expenditure of these school funds.

Point 3: The Legislature is Obligated to “Fully and Properly Fund

the Legally Imposed Obligations” of those Local Governments Whatever legally imposed obligations that local governments have(roads, fire department, police, water, sewer, etc.) must be properlyfunded by the state, but once the money is sent to the local governmentsthat entity has sole direction in how those funds are spent. The stateconstitution lists numerous legally imposed obligations, including thefollowing:

Article 7, Section 8 of the North Dakota Constitution provides that

each county “shall provide for law enforcement, administrative andfiscal services, recording and registration services, educationalservices, and any other governmental services or functions as maybe provided by law.”

Article 8, Section 1 of the North Dakota Constitution provides that“the legislative assembly shall make provision for theestablishment and maintenance of a system of public schoolswhich shall be open to all children of the state of North Dakota and

free from sectarian control.”

Article 8, Section 2 of the North Dakota Constitution provides that“[t]he legislative assembly shall provide for a uniform system of free public schools throughout the state, beginning with theprimary and extending through all grades up to and includingschools of higher education, except that the legislative assemblymay authorize tuition, fees and service charges to assist in thefinancing of public schools of higher education.”

And of course, the legislature through the laws it passes places uponpolitical subdivisions and entities numerous requirements and legallyimposed obligations.

Point 4: The Legislative Council Issued a Memo that Describes theTrue Effects of Measure 2 In November of 2011 the LegislativeCouncil staff issued a memo which clearly indicates that numerous laws

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 7/45

Empower the Taxpayer Complaint – page 7

and funding sources are not effected one bit by Measure 2. This ten-pagememo is attached as ATTACHMENT 2.

Point 5: Local Control is Given back to the Local Governments – Presently, all decisions relating to Property Taxes is Done by theState by the State Deciding the Mills that can be Assessed The statelegislature gives each political subdivision/district authority to impose amill levy against the properties within its geographical area. A “mill” isone-hundredth of a cent. The local political entity is permitted to levymills only as authorized by the state legislature. Control over the processis strictly regulated. The North Dakota Century Code has 32 pages thatoutline the mandates, limitations, and authority the political subdivisionsof North Dakota must follow when imposing property taxes. The Codespecifies in minute detail what political subdivisions can and cannot do

regarding imposing, collecting, and expending property taxes. Countiesare limited to imposition of 23 mills per dollar for general or specialcounty purposes, but they may impose more levies for 38 additionalpurposes. Thus, most and arguably ALL of the control over propertytaxes presently rests with the legislature and not the local governingbodies.

11. Measure 2: Services to the Public will Not be Reduced

Point 1: Streets, Roads, Fire Departments, Police, and All OtherTraditional Public Serves Are Required To Be Funded Measure 2specifically provides that whatever amount local governments previouslyreceived through property taxes must be replaced by the stategovernment, while actually requiring real autonomy and local control asto the spending of those funds. The subdivisions will be receiving thesame amount of money and will be in a position to fund whatever itpreviously funded, including all traditional services.

Point 2: As noted above, Article 7, Section 8 of the North Dakota

Constitution provides that each county “shall provide for lawenforcement, administrative and fiscal services, recording andregistration services, educational services, and any other governmentalservices or functions as may be provided by law.”

12. Measure 2: Will Not Affect Bonds, Bonding Powers, or SpecialAssessments

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 8/45

Empower the Taxpayer Complaint – page 8

Point 1: Local Governments may Still Issue Bonds Such bondswould be secured by other means, such as Sales Tax or Other TaxRevenues. Leg. Council Memo page 9.

Point 2: Special Assessments may Still be Used. Special assessmentswould be based not on the value of the property but on the just proportionof the total cost of the work not exceeding the benefit. Leg. CouncilMemo page 5.

13. Will Not Affect Oil and Gas Taxes, or Coal Conversion orSeverance Taxes

Point 1: Measure 2 will Not Affect Oil and Gas Taxes These are

separate taxes entirely. Neither gross production nor extraction taxwould be effected by Measure 2. Leg. Council Memo page 5.

Point 2: Coal Conversion and Coal Severance Taxes Will not beAffected. Coal conversion tax is not based on the assessed value of property; coal severance tax is based on a specified number of cents perton. Leg. Memo page 5.

Point 3: Oil and Gas Revenues are Here to Stay for a Long Time Lynn Helms, director of the North Dakota Oil and Gas Division,estimated in April of 2010 that there are about 4 billion barrels of recoverable oil in North Dakota. The most conservative estimatesprovide for at least 30 more years of oil and gas production; otherestimates are as high as 90 to 120 years.

Point 4: Oil Companies will not be Able to Use Measure 2 Oil andgas taxes are entirely separate and have nothing to do with Measure 2.There is no Basis for Asserting that coal, oil and gas productioncompanies may seek favorable treatment regarding these taxes through

the court system.

14. Measure 2: Will Not Create a Tax Shift – Not Necessarily orAutomatically

Point 1: According to the Only Economic Study Conducted on theEffects of Measure 2, Measure 2 will Result in Saving Money Beacon

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 9/45

Empower the Taxpayer Complaint – page 9

Hill Institute, a Boston-based research firm that the ND Department of Commerce uses to evaluate its many economic development programs,has concluded that Measure 2 will create 11,000 new jobs, increasedisposable income by 3.24% or nearly $900 per capita; the study predictsa 34.6% surge in business investments in new private-sector businesses,new jobs, and better wages, all of which will increase tax revenues – notdecrease them.

Point 2: Any Loss of Revenue that Does Happen can Easily beReplaced by Other Revenues Any loss of revenue can be replacedwithout increases in any tax rates because North Dakota sales and incometax collections are, without increases in their rates, generating dramaticincreases in revenue. These increases are coming from additionaleconomic activity. Measure 2 will drive those revenues considerably

higher. Further, elimination of property taxes will result in a directsavings of between $30 million and $50 million due to elimination of thehigh costs to administer and collect of property taxes.

Point 3: Any Loss of Revenue Could be Offset by Reducing the Size(or at least the Growth) of Government The legislature has the optionof reducing or eliminating special-interest spending, bringing stateexpenditures into line with private-sector spending, and/or allocating

North Dakota’s natural-resources to fund what is now funded withproperty taxes.

15. Measure 2: Will Actually Result in a Real Tax Cut

Point 1: The Cost of Government Will be Lessened As shown by theBeacon Hill analysis, the net result of Measure 2 is an increase inrevenues, not a decrease. Further, the expense of a complicated propertytax system will be gone.

16. Measure 2: Provides Resident and Non-Resident Property

Owners Relief, and is Fair to Both

Point 1: The 86% Resident Property Owners will Receive the TrueBenefit of Measure 2 While it is true that the 14% of non-residentproperty owners will no longer have to pay property taxes, the opponentsfail to mention that the 86% of resident property owners will not have topay property taxes either. Both resident and non-resident property owners

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 10/45

Empower the Taxpayer Complaint – page 10

will, for the first time in North Dakota history, be secure in the ownershipof their property and never have to worry about losing it to governmentfor failure to pay property tax.

Point 2: The Present Payment of Property Taxes by Non-Residentsis Not Fair The reality is that the non-resident property owners are beingforced to pay for schools, and other services that they do not use.

Point 3: Non-Resident Property Owners will Still Have to Pay Taxesrelating to the use of Their Property For those non-resident propertyowners who use the land as a business or a home would pay their fairshare by payment of income taxes on any income received and salestaxes on any goods they purchase. Tenants of non-resident ownedproperty would be paying the cost of the services the properties they

lease/rent use. All property will pay its fair share. Currently, between 30and 40% of all real property in North Dakota is exempt from propertytax. These properties do not pay their fair share.

17. Measure 2: Will not Bankrupt Cities and CountiesSome of the opponents listed above have asserted the Measure 2 willbankrupt cities and counties on January 1, 2013. This is not true.

Point 1: Measure 2 Specifically Provides that Cities and CountiesMust Fully and Properly be Funded The Measure specificallyprovides that any local entity operations previously funded through

property taxes “must be replaced with revenues from the proceeds of state sales taxes, individual and corporate income taxes, oil and gasproduction and extraction taxes, tobacco taxes, lottery revenues,financial institutions taxes, and other state resources.” As aconstitutional mandate the legislature must fully and properly fundthese obligations before it funds optional, discretionary and specialinterest expenditures.

Point 2: Local Governments have Means Other Than PropertyTaxes to Obtain Revenues Local governments will still be able toreceive revenues from special assessments, local option sales tax;charter city and counties have additional revenue options as well, suchas sales taxes, use taxes, income taxes, gross receipt taxes, and manyother charges and fees allowed by law. Roads are funded by the gas

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 11/45

Empower the Taxpayer Complaint – page 11

tax and are revenue funded; water and sewer are funded by operatingcosts charged to the persons receiving the services.

Point 3: Bankrupting Local Governments isn’t even a Possibility Measure 2 specifically requires the Legislature to replace the propertytax money that otherwise would have been received from propertytaxes. The Legislature may have to cut discretionary spending, butnot the replacement funding to local governments.

18. Measure 2: Will Not Create “Considerable” Litigation

Point 1: Measure 2 is Specific in All Necessary Details and Non-Specific Where it Needs to Be Many constitutional provisions have tohave some vagueness in order to be flexible to the situation, some of

which is intentional (such as reasonable searches and seizures).

Point 2: Measure 2 Specifically Requires Local Control, andFunding for Local Governments Measure 2 contains, as much aspossible, detailed and clear constitutional requirements; some items haveto be left to the legislature to implement, such as the formula that will beused to replace the revenues needed to fund operations previously fundedthrough property taxes. On the other hand, Measure 2 specificallyrequires that local control as to spending those funds is left to the solediscretion and/or direction of the local entity.

19. North Dakota Will Not Become Subject to Public Approbation

Point 1: Mr. Traynor’s assertion that “Passage of Measure 2 will make North Dakota a laughing stock” is nothing more than a baseless scaretactic.

II. Violations of the Corrupt Practices Act, Chapter 16.1

20. Demonstrated Violations of Chapter 16.1-10 by Public Officialsand Publicly Funded Entities The opponents to Measure 2 are ignoring allof the steps taken and information prepared relating to a very carefullydrafted Measure; they are blatantly and intentionally issuing falsehoodsregarding:

local control,

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 12/45

Empower the Taxpayer Complaint – page 12

bankrupting cities and counties,

inability to pay back bonds,

the creation of considerable litigation,

negative effects on oil and gas taxes and income derived

therefrom, asserting a tax increase or tax shift when the only study conducted

shows a net tax decrease,

asserting city and counties will go broke or be unable to provideservices, and

creating an unfair advantage to non-residents agricultural propertyowners.

As shown above, each of these assertions are baseless, constitute theissuance of false and misleading information based not on facts but scaretactics. Those persons who are doing so as public officials or using publicmonies are all in violation of Chapter 16.1-10. These persons and entitiesare also attempting to sway persons in regards to the upcoming vote, also indirect violation of Chapter 16.1-10.

21. North Dakota law at Chapter 16.1-10 prohibits certain conductdefined as corrupt practices and specifically prohibits elected officials andpublic organization, as well as any organization that derives its funding fromstate or political subdivisions funds, from advocating “for or against or otherwise reflect a position on the adoption or rejection of the ballot

question” and specifically prohibits political statements or politicaladvertisements a from knowingly, or with reckless disregard for its truth orfalsity, publishing any political advertisement or news release that containsany assertion, representation, or statement of fact, which is untrue,deceptive, or misleading on behalf of or in opposition to any “initiatedmeasure, referred measure, constitutional amendment, or any other issue,question, or proposal on an election ballot.”

22. Section 16.1-10-02 provides at subdivision 1 that “[n]o personmay use any property belonging to or leased by, or any service which isprovided to or carried on by, either directly or by contract, the state or anyagency, department, bureau, board, commission, or political subdivisionthereof, for any political purpose.”

23. Section 16.1-10-02 further provides at subdivision 2 (a) thedefinition of “political purposes” as prohibiting “any activity undertaken in

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 13/45

Empower the Taxpayer Complaint – page 13

support of or in opposition to a statewide initiated or referred measure, aconstitutional amendment or measure, a political subdivision ballot measure,or the election or nomination of a candidate to public office and includesusing ‘vote for’, ‘oppose’, or any similar support or opposition language inany advertisement whether the activity is undertaken by a candidate, apolitical committee, a political party, or any person. In the period thirty daysbefore a primary election and sixty days before a special or general election,‘political purpose’ also means any activity in which a candidate's name,office, district, or any term meaning the same as ‘incumbent’ or ‘challenger’ is used in support of or in opposition to the election or nomination of acandidate to public office. The term does not include activities undertaken inthe performance of public office or a position taken in any bona fide newsstory, commentary, or editorial. Factual information may be presentedregarding a ballot question solely for the purpose of educating voters if the

information does not advocate for or against or otherwise reflect a positionon the adoption or rejection of the ballot question.”

24. Section 16.1-10-02 further provides at subdivision 2 (a) thedefinition of "Property" includes motor vehicles, telephones, typewriters,adding machines, postage or postage meters, funds of money, and buildings.However, nothing in this section may be construed to prohibit any candidate,political party, committee, or organization from using any public buildingfor such political meetings as may be required by law, or to prohibit suchcandidate, party, committee, or organization from hiring the use of anypublic building for any political purpose if such lease or hiring is otherwisepermitted by law.

25. Section 16.1-10-02 further provides at subdivision 2 (a) thedefinition of "Services" includes the use of employees during regularworking hours for which such employees have not taken annual or sick leaveor other compensatory leave.

26. Section 16.1-10-04 prohibits the distribution of false

information in political advertisements or news release and provides asfollows:

16.1-10-04. Publication of false information in politicaladvertisements - Penalty. A person is guilty of a class Amisdemeanor if that person knowingly, or with reckless disregard forits truth or falsity, publishes any political advertisement or news

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 14/45

Empower the Taxpayer Complaint – page 14

release that contains any assertion, representation, or statement of fact,including information concerning a candidate's prior public record,which is untrue, deceptive, or misleading, whether on behalf of or inopposition to any candidate for public office, initiated measure,referred measure, constitutional amendment, or any other issue,question, or proposal on an election ballot, and whether thepublication is by radio, television, newspaper, pamphlet, folder,display cards, signs, posters, billboard advertisements, websites,electronic transmission, or by any other public means. This sectiondoes not apply to a newspaper, television or radio station, or other commercial medium that is not the source of the politicaladvertisement or news release.

27. Chapter 16.1-10, relating to public officials advocating a

position on initiated measures, was passed with the specific intent that publicofficials who advocate a position on an initiated measure are committing acorrupt practice in violation of the law. This legislation was passed for thespecific purpose of preventing public officials from using public funds ortheir public position to taint the initiative measure process by advocating orpresenting false or misleading information to the detriment of the publicmaking a decision, as shown by the legislative history.2 The LegislativeHistory is attached as ATTACHMENT 3.

2 Dustin Gawrylow: . . . There shouldn’t be any city telling the citizens how to vote.

It is a far cry from advocating it; taxpayers shouldn’t be fighting their own money.

Even if it passes the minority of the voters has had the tax dollars used against theirinterest and that is just morally objectionable. Page 2Under current law government property or services should not be used foradvocacy. Using taxpayer dollars to campaign or persuade people is not an effectiveuse of government time. Page 3Robert Harmes: I am here on my own behalf. I am looking at the amendments thatSenator Cook raised. Current law says that you can’t use public resources forpolitical purposes. But you can use public resources to educate the public. Theamendment would confirm the Attorney General’s opinion that you can educate the

public. In 1989 Governor Sinner at the time and Senator Lipps flew around the state of North Dakota trying to tell the public about the impact of the 1989 referrals. Bismarck school board within the last few years took to advocating to life the cap on the mill levy.Again, they can educate the public but they were doing so to sway their vote. Thelaw says that you can’t use it for political purposes but you can use it to educate; for instance I see the potential for an agency to bring info before the legislature and it fails.They could then use state resources to get a measure passed and do so under the veil

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 15/45

Empower the Taxpayer Complaint – page 15

III. Violations of Existing Attorney General Opinions

28. Attorney General Opinion 2009-L-11 specifically providesthat “that a state agency or entity may not use state funds or resources toadvocate for or against a ballot measure, absent a constitutional or statutory

provision permitting it.”

of educating the public. If there is a bona fide interest in educating the public then thereare ways to genuinely educate the public: have both sides be present and state their case.Page 16Rep. Kim Koppelman: . . . The key is an official of government or an agency of government should not be using your tax dollars to convince you how to vote. It hasnothing to do with what the public can do when they come into a public building oranything like that.Rep. Vicky Steiner: Can I explain a little bit what the thinking is on this bill? The intent

of this bill is really about a statewide initiated measure where you have state officeholders . . . using state funds to say don’t vote for this. I agree with Rep. Winrich inthe fact that in theory people should know that is the law because we do have that incurrent law. Sometimes we will put things in to make things even more clear. Itclarifies that if there is an initiated measure, you can’t use state resources to say vote

no or vote yes. Pages 25-26Vice Chairman Randy Boehning: How does this affect the League of Cities,Association of Counties, and the School Boards Association?John Bjornson: I haven’t looked at that, but I don’t believe it is intended to address – weare talking about the use of state and political subdivision resources. Those

organizations have dues paid to them to participate. They are not state orgovernmental organizations. They are groups that provide assistance to thegovernments themselves. I don’t think this would affect them.Vice Chairman Randy Boehning: I would assume most or all of the money that theyrun on is tax dollars that are paid through dues. Technically, wouldn’t that be tax

dollars? John Bjornson: I don’t know if I can really answer that. I know from our standpoint wepay dues to the National Conference of State Legislatures and NCSL represents thestates. Part of their function is to represent the states before the Congress. If a policyposition is taken by NCSL to oppose something they believe is going to affect the statesand the Congress, they do it. The money that is paid as dues or even contracting with

another entity doesn’t stay public funds once it turns into the hands of the outside entitygenerally. This could seem to be like open records and open meetings. If you rememberabout 15 years ago, when GNDA was publishing their magazine and the question wasasked if whether the state’s contribution for the magazine was just support of theorganization or if it was for exchange for a service. In this case I think it was probablyexchange for a service so those records probably weren’t open to the public. We can finda lot of scenarios that raise questions and are gray areas.Page 32

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 16/45

Empower the Taxpayer Complaint – page 16

Emphasis added. Notice that the AG Opinion prohibits the use of publicfunds to advocate for or against a ballot measure by a state agency OR aentity; the language implies that any entity that receives any public fundsmay not violate the provisions of Chapter 16.1-10.] This most recentopinion is very instructive to the issues at hand:

One leading case has held that a state official lacks authority toexpend public funds to support a state bond issue enhancing state andlocal facilities because, absent clear and explicit legislativeauthorization, a public agency may not expend public funds topromote a position in an election campaign. “A fundamental

precept of this nation’s democratic electoral process is that the

government may not ‘take sides’ in election contests or bestow an

unfair advantage on one of several competing factions.” (Footnote4 and 5 omitted.)

Page 2.. . .

In addition, a trivial or de minimis use of public funds or resourceswould likely not be determined by the courts to constitute a violationof the law.8 Thus, to the extent an expenditure of state funds orresources would be used only to educate the voters through a fairpresentation of the facts about a pending ballot measure, noviolation would occur.

Page 3.

29. Attorney General Opinion 2004-L-55 specifically provides that“while a school district may provide the public with neutral factualinformation, it may not, absent a statute, expend public funds to advocateschool board’s position on a ballot measure.” Attorney General Opinion

2009-L-11, note 1.

The words used by the Attorney General in 2004-L-55 apply equally well tothe situation present in this case:

Likewise, in this instance, while a fact-finder could conceivablyreach a different conclusion, it appears to me that a fair-

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 17/45

Empower the Taxpayer Complaint – page 17

minded reading of the flyer in the context in which it wasdistributed was to promote defeat of the measure and not toprovide a fair and balanced presentation of the issues. Seenote 1 above. The flyer mentioned that similar measureshave failed twice in the past; it predicted significant staff and teacher layoffs and impacts on class size and possibleconsolidation or closure of smaller schools. The flyer alsoargued school programs, courses, teaching materials, andbuilding maintenance would be adversely affected. It alsodownplayed potential property tax savings “compared tothe potential long-term impact on property values if schoolquality in the community is compromised.” Whileundoubtedly the passage of the ballot measure would have hadserious fiscal effects for the school district’s budget and

programs, the flyer could have been drafted in a more fair andbalanced manner.

30. Attorney General Opinion 2002-L-61 specifically provides that“county commission newspaper insert went beyond fair presentation of factsrelating to a pending ballot measure on whether to construct a newcourthouse to advocacy by the county for passage of the bond issue;expenditure of public funds for the newspaper insert advocating the county’sposition was inappropriate and unlawful.” Attorney General Opinion 2009-L-11, note 1.

The words used by the Attorney General in 2004-L-55 apply equally well tothe situation present in this case:

Although a fact-finder conceivably could reach a contraryconclusion, it is apparent to me that no fair minded readingof the newspaper insert could lead to a conclusion otherthan the overall intent and purpose of the newspaper insertwas to promote passage of the bond issue, and not to

provide a fair and balanced presentation of the issues beforethe voters. In my opinion the newspaper insert went beyond afair presentation of facts to advocacy by the county for passageof the bond issue for a new courthouse. The expenditure of public funds for the newspaper insert in such a manner isinappropriate and unlawful.

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 18/45

Empower the Taxpayer Complaint – page 18

31. Each Attorney General Opinion is issued pursuant to N.D.C.C. § 54-12-01 and governs the actions of public officials. Where a public official oran entity supported in part or in full by public funds violates an attorneygeneral opinion, he or she or the entity should be held jointly liable and berequired to pay personally any costs associated with correcting thatviolation, including attorney fees.

IV. Applicable Law – Declaratory Judgment and Injunctive Relief

32. Chapter 32-23 of the North Dakota Century Code allows the DistrictCourt to enter declaratory judgment in regards to legal issues. The sectionrelating to the power of the district court to issue declaratory judgments issection 32-23-01, which provides as follows:

32-23-01. Court of record may enter a declaratory judgment. Acourt of record within its jurisdiction shall have power to declarerights, status, and other legal relations whether or not further relief isor could be claimed. No action or proceeding shall be open toobjection on the ground that a declaratory judgment or decree isprayed for. The declaration may be either affirmative or negative inform and effect, and such declaration shall have the force and effect of a final judgment or decree.

33. Chapter 32-06 of the North Dakota Century Code allows the DistrictCourt to enter declaratory judgment in regards to legal issues. The sectionrelating to the power of the district court to issue declaratory judgments isSection 32-06-01 and Section 32-06-02, which provide as follows:

32-06-01. Injunction by order.An injunction by order may be made by the court in which an action isbrought, or by a judge thereof, in the cases provided in section 32-06-02, and, when made by a judge, may be enforced as the order of thecourt.

32-06-02. Injunction - In what cases granted.An injunction may be granted in any of the following cases:1. When it shall appear by the complaint that the plaintiff is entitled tothe relief demanded, and such relief, or any part thereof, consists inrestraining the commission or continuance of some act, the

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 19/45

Empower the Taxpayer Complaint – page 19

commission or continuance of which during the litigation wouldproduce injury to the plaintiff.2. When, during the litigation, it shall appear that the defendant isdoing or threatening, or is about to do, or is procuring or suffering,some act to be done in violation of the plaintiff's rights respecting thesubject of the action and tending to render the judgment ineffectual, atemporary injunction may be granted to restrain such act.3. When, during the pendency of an action, it shall appear by affidavitthat the defendant threatens, or is about to remove or dispose of thedefendant's property, with intent to defraud the defendant's creditors, atemporary injunction may be granted to restrain such removal ordisposition.

V. Allegations Relating To Corrupt Practices

34. Tax Commissioner Cory Fong is presently taking sides regardingMeasure 2 and distributing a false and misleading document entitled, Impact

of Measure 2: Abolishing Property Taxes by North Dakota Office of StateTax Commissioner, Cory Fong, Tax Commissioner. This document isattached as ATTACHMENT 4.

This document is filled with false and misleading information and clearlyadvocates a position, all in violation of Chapter 16.1 of the North DakotaCentury Code and the Attorney General Legal Opinions quoted above.

Point 1: Commissioner Fong has Already Admitted that the TaxDepartment does not Have Econometric Modeling Capabilities and isNot in a Position to Access, Determine, or Otherwise Evaluate “Any

Potential Benefits” of Measure 2 and Has no Intention to Engage inAny Expertise to Do So

“Kathy Strombeck, Director of Research & Education for the TaxDepartment, will report to the committee that we do not haveeconometric modeling capabilities here within the department. Kathy

will provide a little background information on the modelingcapabilities that we do have --- models which are useful for estimatingthe direct (static) revenue consequences of tax rate changes and otherdirect changes from proposed legislation. Dynamic estimates --- suchas estimating any potential benefits associated with possible propertytax reductions or elimination --- are beyond the scope of our in-house

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 20/45

Empower the Taxpayer Complaint – page 20

models. At this time, the Tax Department does not plan tocommission an econometric study on this topic.”

Commissioner Fong email to Robert Hale 10-31-12 113:37 am.

Point 2: 3-Legged Stool False and Misleading On page 4 of the TaxCommissioner’s presentation, he describes the “3-Legged Stool” of

North Dakota’s state tax system, consisting of Sales/Use Taxes, IncomeTaxes, and Property Taxes. This statement alone is false andmisleading: North Dakota has more than 20 other taxes or revenuesources not mentioned, such as motor vehicle excise tax ($121 Million),department collections ($66 Million), insurance premium tax ($64Million), cigarette and tobacco tax ($44 Million),interest income ($42Million), oil extraction tax ($38 Million), coal conversion tax ($38Million), oil and gas gross production tax ($32 Million), mineral leasing

fees ($16 Million), gaming tax ($16 Million), wholesale liquor tax (14Million), lottery tax ($1 Million), Business privilege tax ($6 Million)[allfigures bases on 2009 – 2011 Biennium). The total of the other revenuesNOT MENTIONED by Commissioner Fong is more than a half a billiondollars! Measure 2 itself mentions seven other revenue sources, pluc“other state resources.”

Point 3: Commissioner Fong Incorrectly Lists 2010 Property TaxCollections that Would be Required to be Replaced by Measure 2 as$816.2 Million When the Real Number is $667 Million.Commissioner Fong lists $816.2 million as the amount of property taxescollected in 2010, but this number is wrong, the Commissioner knows itis wrong, and is intentionally misleading because Commissioner Fongfails to subtract from that number special assessments that will remainafter Measure 2 passes.3 According to the Tax Department’s own staff,the amount of 2010 property taxes that would not be collected if Measure

3In 2010, property taxes and special assessments totaled $816,215,832.63. Of this total,

$94,227,588.97 were special taxes and special assessments that would not have beenimpacted by Measure 2 ($11,822, Special Taxes; $70,293,379.73, special assessments-cities; $12,110,967.45, special assessments-rural). An additional $45,370,645.23 werecentrally assessed ($8,544,7551.03 for railroads; $12,602,183.43 for electricity, gas, andheating; and $24,223,710.77 for pipelines.) None of these will be impacted by Measure 2,either.

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 21/45

Empower the Taxpayer Complaint – page 21

2 was in effect is $667,617,598.43.4 The use of $816 instead of $667 isan intentional overstatement of more than 22%.

Point 4: Commissioner Fong Asserts a Tax Shift if Property Taxesare Abolished As stated above, the ONLY study done in regards to theeffect of Measure 2 (done by an entity regularly used by the state) itself concluded that Measure 2 will create 11,000 new jobs, increasedisposable income by 3.24% or nearly $900 per capita; the study predictsa 34.6% surge in business investments in new private-sector businesses,new jobs, and better wages, all of which will increase tax revenues – notdecrease them.

Point 5: There Will not be a “Tax Shift” because measure 2

Requires the Legislature to Replace the Funds At page 5 of

Commissioner Fong’s presentation he asserts that there will have to be atax shift. This is false. The Measure specifically provides that any localentity operations previously funded through property taxes “must bereplaced with revenues from the proceeds of state sales taxes, individualand corporate income taxes, oil and gas production and extraction taxes,tobacco taxes, lottery revenues, financial institutions taxes, and otherstate resources.” The money will be replaced.

Point 6: Commissioner Fong’s Assertions as to the Increases in

Individual Income Tax Rates And Sales Tax Rate is Baseless and aScare Tactic At page 7 of Commissioner Fong’s presentation, withoutany foundation at all, he asserts that “the lost revenue would have to bereplaced” when in reality the revenue is replaced by the terms of Measure 2; he also fails to note that the Legislature would have theoption of reducing other non-local expenditures instead of insistingthat government spending continue at its same or higher levels; theassertion that Individual Income Tax rates would increase 279% of 2011rates is baseless and an obvious scare tactic. On page 8 he repeats that“the lost revenue would need to be replaced” and again without any

4 The total amount of property taxes that will need to be replaced initially is$667,617,598.43, less the cost of collection, according to data presented June 22, 2011,by the State Supervisor of Assessments and Director of the Property Tax Division of theOffice of State Tax Commissioner to the Legislative Property Tax Measure ReviewCommittee.

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 22/45

Empower the Taxpayer Complaint – page 22

foundation asserts that the “Sales tax rate would double” from 5% to10%.

Commissioner Fong is taking a position, presenting false and misleadinginformation, and distributing a presentation that is not a fair or neutralpresentation of facts; he is doing all of this using public monies and hispublic office. He is blatantly violating Chapter 16.1-10 and all of theAttorney General Opinions quoted above.

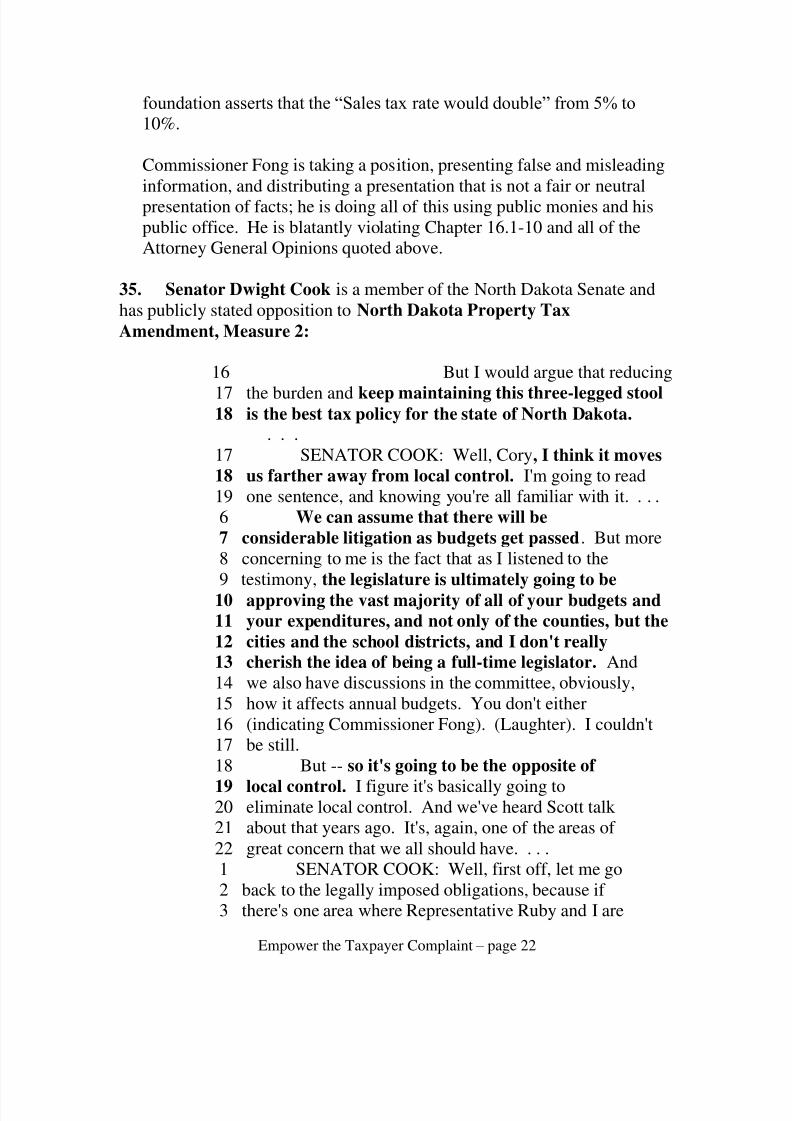

35. Senator Dwight Cook is a member of the North Dakota Senate andhas publicly stated opposition to North Dakota Property TaxAmendment, Measure 2:

16 But I would argue that reducing

17 the burden and keep maintaining this three-legged stool18 is the best tax policy for the state of North Dakota.

. . .17 SENATOR COOK: Well, Cory, I think it moves18 us farther away from local control. I'm going to read 19 one sentence, and knowing you're all familiar with it. . . .6 We can assume that there will be7 considerable litigation as budgets get passed. But more 8 concerning to me is the fact that as I listened to the9 testimony, the legislature is ultimately going to be

10 approving the vast majority of all of your budgets and11 your expenditures, and not only of the counties, but the12 cities and the school districts, and I don't really13 cherish the idea of being a full-time legislator. And 14 we also have discussions in the committee, obviously,15 how it affects annual budgets. You don't either16 (indicating Commissioner Fong). (Laughter). I couldn't17 be still.18 But -- so it's going to be the opposite of

19 local control. I figure it's basically going to20 eliminate local control. And we've heard Scott talk 21 about that years ago. It's, again, one of the areas of 22 great concern that we all should have. . . .1 SENATOR COOK: Well, first off, let me go2 back to the legally imposed obligations, because if 3 there's one area where Representative Ruby and I are

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 23/45

Empower the Taxpayer Complaint – page 23

4 going to agree it's the statement that he made that this5 is very general and ambiguous. Where we're going to6 disagree is the consequences. 7 Folks, this is going into the constitution.8 This general and ambiguous language is going to go into9 the constitution. It doesn't matter what he thinks; it

10 doesn't matter what I think or what you think. When you11 come with a budget and the legislature says -- or when 12 we give you some money, we give you a budget and you13 say, "That isn't enough for our legally-imposed14 obligations; we disagree with you," ultimately it is15 through litigation; it is the Court that is going to16 over years determine the meaning of "legally imposed17 obligations."

18 I said at the beginning, "tax shift,19 litigation and uncertainty."22 . . . we23 will live in a world of uncertainty and nothing will24 bring the wheels to a halt quicker than that type of 25 uncertainty. So it is the consequences of this general1 and ambiguous language that I fear the most.

North Dakota Association of Counties Conference, Forum on ProposedConstitutional Amendment to Abolish Property Taxes Measure 2, RamkotaHotel, Bismarck, North Dakota, Transcript at page 8, lines 16-18, ; page18, lines 17-19, page 19, lines 6-22, page 29 lines 1-19, page 29 lines 22-25 to page 30 line 1 (October 17, 2011)(emphasis added).

Senator Cook is taking a position, presenting false and misleadinginformation, and issuing a presentation that is not a fair or neutralpresentation of facts; he is blatantly violating Chapter 16.1-10 and all of theAttorney General Opinions quoted above. Senator Cook voted in favor of SB 2327in which the following additional language was added to 16.1-10-

02(2)(a):“Factual information may be presented regarding a ballot questionsolely for the purpose of educating voters if the information does notadvocate for or against or otherwise reflect a position on the adoptionor rejection of the ballot question.”

2011 Senate Journal 1486.

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 24/45

Empower the Taxpayer Complaint – page 24

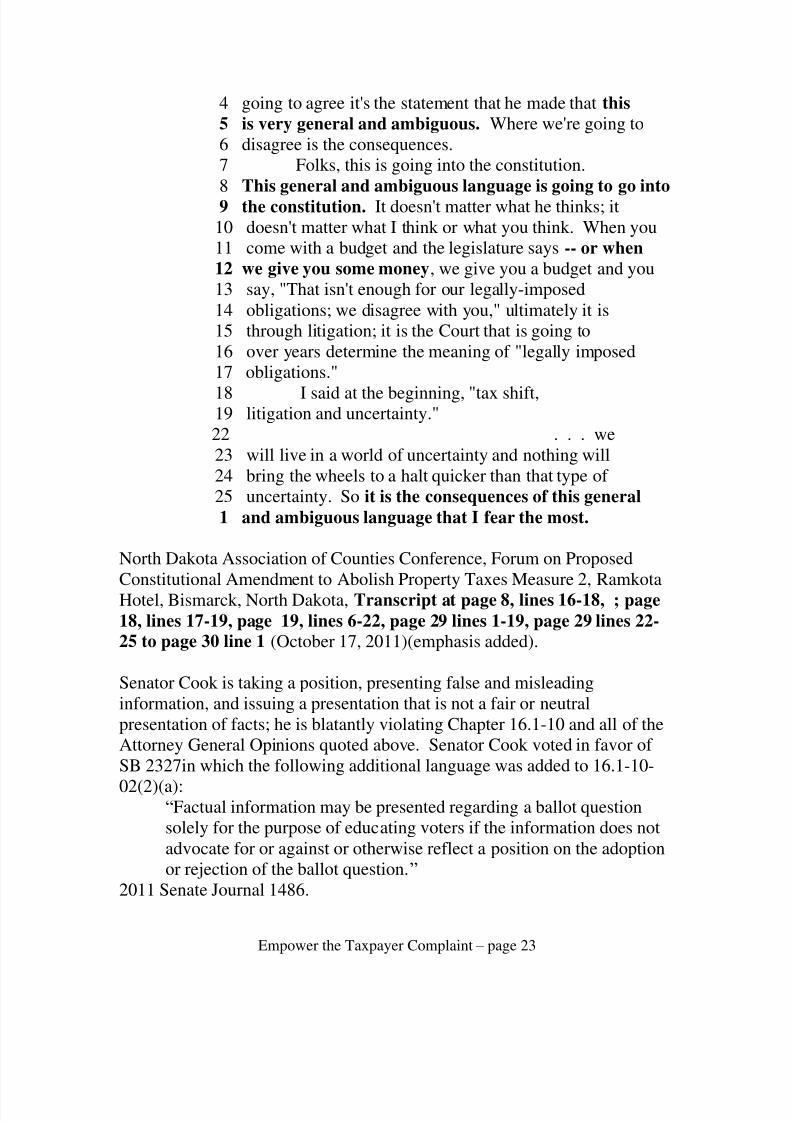

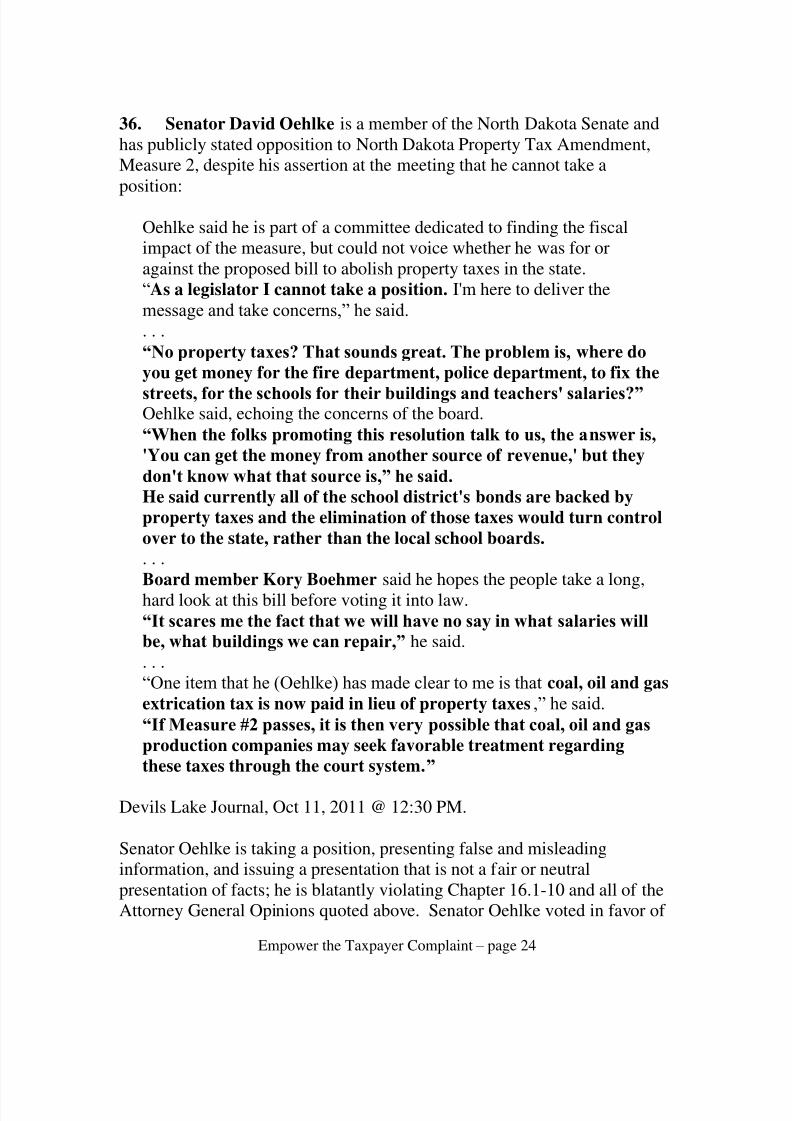

36. Senator David Oehlke is a member of the North Dakota Senate andhas publicly stated opposition to North Dakota Property Tax Amendment,Measure 2, despite his assertion at the meeting that he cannot take aposition:

Oehlke said he is part of a committee dedicated to finding the fiscalimpact of the measure, but could not voice whether he was for oragainst the proposed bill to abolish property taxes in the state.“As a legislator I cannot take a position. I'm here to deliver themessage and take concerns,” he said.. . .“No property taxes? That sounds great. The problem is, where doyou get money for the fire department, police department, to fix the

streets, for the schools for their buildings and teachers' salaries?” Oehlke said, echoing the concerns of the board.“When the folks promoting this resolution talk to us, the answer is,'You can get the money from another source of revenue,' but theydon't know what that source is,” he said. He said currently all of the school district's bonds are backed byproperty taxes and the elimination of those taxes would turn controlover to the state, rather than the local school boards.. . .Board member Kory Boehmer said he hopes the people take a long,hard look at this bill before voting it into law.“It scares me the fact that we will have no say in what salaries will

be, what buildings we can repair,” he said.. . .“One item that he (Oehlke) has made clear to me is that coal, oil and gasextrication tax is now paid in lieu of property taxes,” he said.“If Measure #2 passes, it is then very possible that coal, oil and gas

production companies may seek favorable treatment regardingthese taxes through the court system.”

Devils Lake Journal, Oct 11, 2011 @ 12:30 PM.

Senator Oehlke is taking a position, presenting false and misleadinginformation, and issuing a presentation that is not a fair or neutralpresentation of facts; he is blatantly violating Chapter 16.1-10 and all of theAttorney General Opinions quoted above. Senator Oehlke voted in favor of

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 25/45

Empower the Taxpayer Complaint – page 25

SB 2327in which the following additional language was added to 16.1-10-02(2)(a):

“Factual information may be presented regarding a ballot questionsolely for the purpose of educating voters if the information does notadvocate for or against or otherwise reflect a position on the adoptionor rejection of the ballot question.”

2011 Senate Journal 1486.

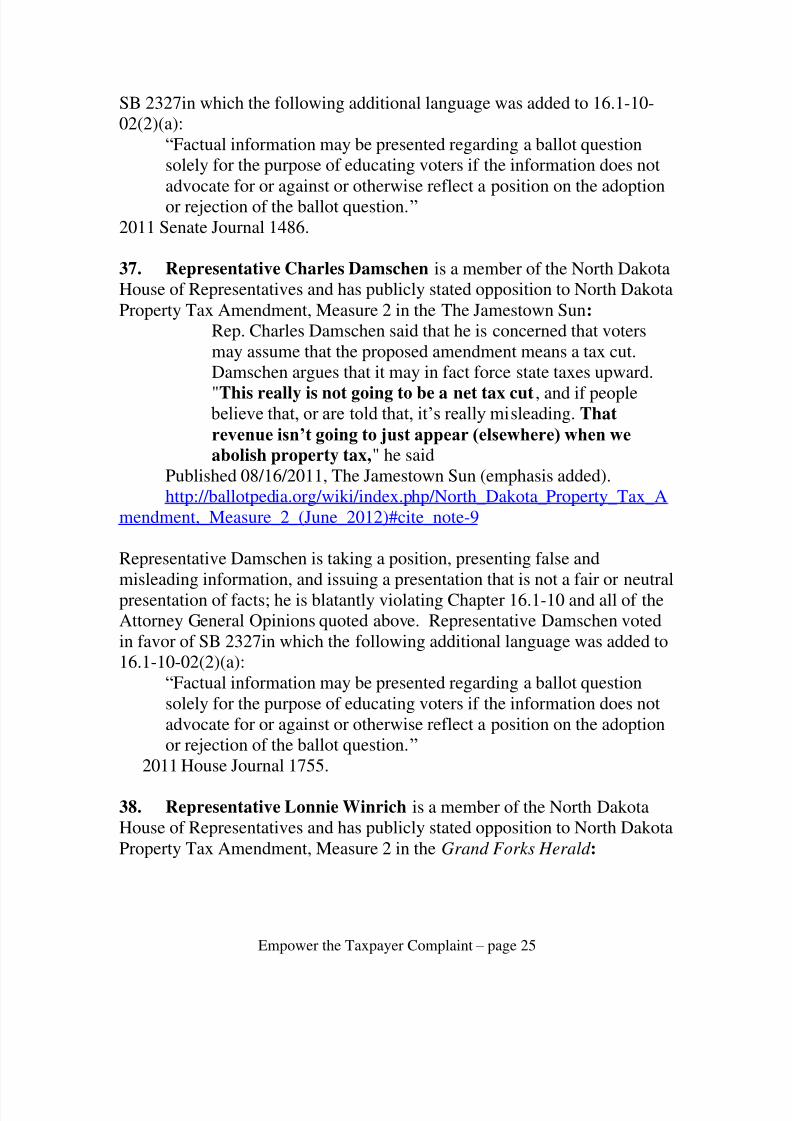

37. Representative Charles Damschen is a member of the North DakotaHouse of Representatives and has publicly stated opposition to North DakotaProperty Tax Amendment, Measure 2 in the The Jamestown Sun:

Rep. Charles Damschen said that he is concerned that votersmay assume that the proposed amendment means a tax cut.Damschen argues that it may in fact force state taxes upward.

"This really is not going to be a net tax cut, and if people believe that, or are told that, it’s really misleading. Thatrevenue isn’t going to just appear (elsewhere) when we

abolish property tax," he saidPublished 08/16/2011, The Jamestown Sun (emphasis added).http://ballotpedia.org/wiki/index.php/North_Dakota_Property_Tax_A

mendment,_Measure_2_(June_2012)#cite_note-9

Representative Damschen is taking a position, presenting false andmisleading information, and issuing a presentation that is not a fair or neutralpresentation of facts; he is blatantly violating Chapter 16.1-10 and all of theAttorney General Opinions quoted above. Representative Damschen votedin favor of SB 2327in which the following additional language was added to16.1-10-02(2)(a):

“Factual information may be presented regarding a ballot questionsolely for the purpose of educating voters if the information does notadvocate for or against or otherwise reflect a position on the adoptionor rejection of the ballot question.”

2011 House Journal 1755.

38. Representative Lonnie Winrich is a member of the North DakotaHouse of Representatives and has publicly stated opposition to North DakotaProperty Tax Amendment, Measure 2 in the Grand Forks Herald :

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 26/45

Empower the Taxpayer Complaint – page 26

Winrich provided copies of a 10- page memo written by the legislature’sstaff attorney lining out some of the problems some see in the measure’swording. . . .The measure prohibits the “levying” of property tax on its effective date. Since property taxes typically are levied by local governments in the year

before the tax revenue is spent, it’s not entirely clear what the measure’seffect would be, Winrich said. It also raises questions about counties, cities, school districts and park districts borrowing money, through issuing bonds for, say, capitalimprovements, based on expected property tax collections over five or 10years or more.Some interpret state law on such bonding decisions as effectively levyingthe needed property taxes for the duration of the bond payments, Winrichsaid. How Measure 2 would be interpreted in light of such bonding issues

isn’t clear, he said.. . .The state tax department reported that property tax receipts in 2010,including payments made in lieu of property taxes by such nonprofitentities as wildlife management groups, totaled $720 million and areexpected to total about $800 million this year.Other revenue sources will need to be found to replace that money if Measure 2 passes, Winrich said.Deb Nelson, Grand Forks County auditor, said the impact actually wouldbe larger than that, because about 15 percent of the total property taxcollections each year in North Dakota come from property owners thatlive out of state.That would mean that state residents would not only have to make up forthe property taxes by some other means, such as sales taxes, they wouldalso have to pay more to make up for the $120 million that can’t becollected from out-of-state property-owners.David Waterman, a Grand Forks business owner, said he supportedMeasure 2, which makes sense when the state has a surplus from taxes onoil production.

“Property taxes are one of the most regressive taxes, because they hit theelderly, those who live on fixed incomes,” he said. “And when they can’t

pay their property taxes, they lose their property and get evicted.” Waterman asked Winrich, “Do you think all the problems you see in thismeasure are insurmountable?” “No, I don’t,” Winrich said. . . .

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 27/45

Empower the Taxpayer Complaint – page 27

Reach Lee at (701) 780-1237; (800) 477-6572, ext. 237; or send email to

Published 01/11/2012, Grand Forks Herald (emphasis added).

Representative Winrich is providing false information, mischaracterizing theLegislative Council report, and misleading the public.

Point 1: In regards to levying of property taxes, as clearly indicatedin the staff report, any further levying would be prospective; and anyprevious levies would be valid.

Point 2: As to public entities borrowing money, RepresentativeWinrich fails to note that the Legislative staff memo clearly indicates

that bonding can continue, but the governmental entity will need touse a different funding source to secure the bonds, such as sales tax orspecial assessments.

Point 3: As to the effect on bonds already in place, the legislativereport clearly indicates that such an interpretation is not likely; themore likely interpretation is that the levy actually occurred “before theeffective date of the measure and that the obligation continues afterthe effective date of the measure.” Legislative staff report page 3.The report provides almost a whole page demonstrating that thepossible interpretation raised by Representative Winrich is not likelyand indeed is basically rejected by the staff report. Nonetheless,Representative Winrich raises this possible interpretation withoutindicating the interpretation was rejected by the Report he justdistributed. Such misleading statements and mischaracterization is aviolation of Chapter 16.1-10.

Point 4: As to the need to find other revenue sources, RepresentativeWinrich fails to mention other revenue sources or the possibility of

not having to “find” additional money: As to the local governments,the state is require to replace the money; in addition, the state mayhave more than enough additional revenues to do just that; forexample, discretionary spending can be reduced; additional revenuesmay come in due to the increase in revenues from increased economicdevelopment that exists in the state – without any rate changes.

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 28/45

Empower the Taxpayer Complaint – page 28

Point 5: As to Deb Nelson’s statement that the impact is higher dueto non-residents, this is false and misleading. If the figures listedabove include ALL property taxes, then how can the non-payment of those same taxes by non-residents increase the amount needed? Italso ignores the benefit to North Dakotans: 86% of the property taxesare being paid by them!Point 5: As to the insurmountability of the alleged problems, the staff report makes it clear that any of the perceived problems are indeedNOT insurmountable, and many of the perceived problems are notproblems at all. It should be noted that Measure 2 was drafted by theLegislative Council staff, and the report is from a member of thatstaff.

Representative Winrich is taking a position, presenting false and misleading

information, and issuing a presentation that is not a fair or neutralpresentation of facts; he is blatantly violating Chapter 16.1-10 and all of theAttorney General Opinions quoted above. Representative Winrich votedagainst SB 2327; it is nonetheless the law. House Journal 1755.

39. Divide County Commissioner Doug Graupe and North DakotaCounty Commissioners Association (NDCCA) President, in an articletitled, “Keep it Local,” published in the North Dakota CountyCommissioners Association’s publication, stated the following:

“I just returned from a state commissioner board meeting. At thatmeeting we spent a considerable amount of time discussing Measure2. Several months ago our board asked Mark and Terry to form acoalition with the League of Cities, School Boards Association andany other groups impacted by the passage of this measure. I feel thatwe need to educate the people of our state about the probable impactthe successful passage of this measure would have. With education Iam confident the voters will defeat the measure as I said in my lastcolumn. I am opposed to measure 2. I think our slogan should be

“Keep It Local”. After all we are the government closest to thepeople. Every county is unique and our local citizens should be thedecision makers. The proponents of this measure seem to becomfortable that spending decisions for local government will bemade in Bismarck.

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 29/45

Empower the Taxpayer Complaint – page 29

“Two examples of local decision-making in our county are: Weformed a Divide County Hospital District that provides a levy tosupport our hospital and asked the voters of the county if we shouldincrease the Farm to Market levy from 10 mills to 20 mills. It wasapproved with approximately 2/3 voting in favor. These twodecisions made by local taxpayers would not be possible if Measure 2passes.

Point 1: As discussed above, local control is guaranteed through thespecific language of Measure 2.Point 2: Special assessments and the issuance of general obligationbonds remains after the passage of Measure 2, as clearly shown in theLegislative Council staff memo at pages 5 & 9. CommissionerGraupe’s statement that under Measure to there would be no way to

fund those projects is absolutely false.

40. Cass County Commissioner Scott Wagner has publicly statedopposition to North Dakota Property Tax Amendment, Measure 2:

22 My fear is we will not lower the cost of 23 government with this measure. We will either shift the24 cost to the state, and if there's not the capacity to25 raise that revenue, you have state and local government1 fighting for the same pool of money. . . . If this4 passes, property taxes will be decided by the state.5 And how do you reconcile what that does -- flipping6 representative government upside down, on its head?

. . .3 Once again, what I think this measure4 inevitably will do, it will pit state and local spending5 priorities against one another for a narrow amount of 6 revenue given the needs, and the locally elected7 officials that have been elected by the citizens to meet8 those needs don't have a vote. What we become is

9 nothing more than elected lobbyists.10 Now, that's not going to help and that's not11 going to give more control to the citizens.

North Dakota Association of Counties Conference, Forum on ProposedConstitutional Amendment to Abolish Property Taxes Measure 2, RamkotaHotel, Bismarck, North Dakota, Transcript at page 13 line 22 to page 14line 6, page 23, lines 3-11 (October 17, 2011).

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 30/45

Empower the Taxpayer Complaint – page 30

41. Wahpeton Finance Director Darcie Huwe has publicly statedopposition to North Dakota Property Tax Amendment, Measure 2:

"This will be monumental. Property tax is one way for local

governments to kind of control their destiny, with their ability to raisebulk revenue to provide local services. And if we lose that ability ordiminish that ability to raise local revenue that provides local services,I think you end up with a disconnect between funding and priorities."If property taxes were eliminated as a source of revenue, localgovernments would have to depend on the state to replace the source,said Huwe. "In what form and how would it come and would it be thesame amount and what would control how much that amount wouldbe... a lot of big unknowns that aren't necessarily defined in theproposed legislation," she said.The Daily News May 19, 2010http://www.wahpetondailynews.com/articles/2010/05/19/news/doc4bf 441b16cde9310714586.txt

42. Williams County Auditor Beth Innis has publicly stated oppositionto North Dakota Property Tax Amendment, Measure 2:

Williams County Auditor Beth Innis said eliminating property taxeswould have a serious impact on the services provided to thepublic.

Innis said abolishing the taxes would most likely require a sharpincrease in either sales tax or income tax to compensate for therevenue loss. She explained that this would impact people withlow or fixed incomes, or if they receive different tax breaks suchas the homestead credit. If a way to make up the lost revenueweren’t put into place, Innis said people would have to make cuts

in essential services.“What part of government do you want to eliminate? County, citygovernment, townships, schools, are funded in part by this. Yourlibraries, airport, fire districts, vector districts. What don’t you

need?” said Innis. Williston Herald May 24, 2010http://www.willistonherald.com/articles/2010/05/24/news/doc4bfaaa470c855721961830.txt

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 31/45

Empower the Taxpayer Complaint – page 31

43. The North Dakota Association of Counties5 is a group of all 53North Dakota counties which pay and use public funds to be a member of that organization and has publicly stated opposition to North DakotaProperty Tax Amendment, Measure 2 by adopting Resolution 2011-05at its recent annual meeting:

2011-05. Property Tax Elimination Measure. An amendment to the

North Dakota Constitution has been proposed to eliminate all property

taxes in North Dakota. This amendment would require the State

Legislature to replace the lost revenue for “legal obligations”, but

does not guarantee the Legislature will fund all current services and

the increasing costs of local government. As existing State revenues

are insufficient to meet the current and future funding needs of local

government, this measure mandates increases in State taxes – adoubling of the current sales tax rate, a tripling of personal &

corporate income tax, or some combination of these would be

needed. The amendment does not address payments in lieu of property

taxes paid by a variety of public and private entities and it does not

address the existing bonded indebtedness of local governments where

payment is obligated against property tax receipts; creating a situation

of inevitable litigation. Additionally, the amendment would

dramatically shift the responsibility for funding local services away

from locally elected officials to the statewide legislative body. While

this Association supports the use of increased state revenues to reduce

the property tax burden, this Association opposes the passage of the

constitutional amendment to eliminate property taxes as currently

proposed.

http://www.ndaco.org/?id=457&page=Resolutions

5The ND Association of Counties asserts on its webpage in reference to Measure 2 that

unlike the counties themselves, it can use the public monies submitted by the counties asdues and represent all the counties and nonetheless state a position on Measure 2:

“Remember, although as an organization, it's fully acceptable for NDACo and NDCCA to take up positions

and pass resolutions, but as county officials, be careful that your resources are used for information only, not"campaigning." http://www.ndaco.org/?id=1

The individual public officials cannot, by joining in doing a joint illegal act with otherpublic officials, create legality by the individuals acting in concert and in a group to dothat which is illegal.

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 32/45

Empower the Taxpayer Complaint – page 32

44. The North Dakota Association of County Commissioners is agroup of North Dakota county commissioners which pay and use publicfunds to be a member of that organization and has publicly stated oppositionto North Dakota Property Tax Amendment, Measure 2 by adoptingResolution 2011-05 at its recent annual meeting:

2011-05. Property Tax Elimination Measure. An amendment to theNorth Dakota Constitution has been proposed to eliminate all propertytaxes in North Dakota. This amendment would require the StateLegislature to replace the lost revenue for “legal obligations”, butdoes not guarantee the Legislature will fund all current services andthe increasing costs of local government. As existing State revenuesare insufficient to meet the current and future funding needs of local

government, this measure mandates increases in State taxes – adoubling of the current sales tax rate, a tripling of personal &corporate income tax, or some combination of these would beneeded. The amendment does not address payments in lieu of propertytaxes paid by a variety of public and private entities and it does notaddress the existing bonded indebtedness of local governments wherepayment is obligated against property tax receipts; creating a situationof inevitable litigation. Additionally, the amendment woulddramatically shift the responsibility for funding local services awayfrom locally elected officials to the statewide legislative body. Whilethis Association supports the use of increased state revenues to reducethe property tax burden, this Association opposes the passage of theconstitutional amendment to eliminate property taxes as currentlyproposed.

http://www.ndcca.org/?id=13

45. In addition to taking a position on Measure 2, the North DakotaAssociation of Counties, an entity that receives funding in whole or in partfrom public entities and therefore receives public funds, employs Mark

Johnson as its Executive Director and Terry Traynor as its deputy Directorfor Policy; the The North Dakota County Commissioners Associationemploys Mark Johnson separately, listing him as its Executive Director andSecretary to the Board. The North Dakota Association of Counties

publishes “County News” and has taken a position against Measure 2. In theJanuary/February 2012 issue of their paper “County News”, NDACoExecutive Director Mark Johnson stated the following:

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 33/45

Empower the Taxpayer Complaint – page 33

Even if it stays quiet outside this winter, we have plenty of activity tomaintain our focus. As you know, both associations passedresolutions opposing Measure 2, which would abolish propertytaxes. Our staff has been asked to work with schools, cities,townships and other local government entities to form a united frontto combat this very bad idea. We have met several times with theseorganizations, and you will be happy to hear that the businesscommunity has embraced this effort as well. In fact, they are taking aleadership position. They know that an unfair burden will shift ontoincome and corporate taxes, and will hit local businesses hardest,as out-of-state businesses quit paying property taxes.

We all need to inform ourselves and citizens of the true consequences

of abolishing property taxes. We are building a section on ourwebsite (www.ndaco.org) to address measure 2 issues. And don’t letanyone intimidate you about expressing your opinion. You can’tspend money from your county budget to campaign against Measure2, but you can and should speak to your local news, media, civicclubs and anyone else who will listen. There may be much to dislikeabout property taxes, but this measure does nothing to replace themwith any kind of local control, and that’s not good.

If we work together, we can put this poorly conceived idea torest. My best wishes to you for a successful new year.

46. The North Dakota Association of Counties publishes “County News” and has taken a position against Measure 2. In the January/February2012 issue of their paper “County News” Divide County CommissionerDoug Graupe, North Dakota County Commissioners Association(NDCCA) President published in the North Dakota CountyCommissioners Association’s newsletter, stated the following:

“I just returned from a state commissioner board meeting. At thatmeeting we spent a considerable amount of time discussing Measure2. Several months ago our board asked Mark and Terry to form acoalition with the League of Cities, School Boards Association andany other groups impacted by the passage of this measure. I feel thatwe need to educate the people of our state about the probable impactthe successful passage of this measure would have. With education I

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 34/45

Empower the Taxpayer Complaint – page 34

am confident the voters will defeat the measure as I said in mylast column. I am opposed to measure 2. I think our sloganshould be “Keep It Local”. After all we are the government closestto the people. Every county is unique and our local citizens should bethe decision makers. The proponents of this measure seem to becomfortable that spending decisions for local government will bemade in Bismarck.

“Two example of local decision-making in our county are: We formeda Divide County Hospital District that provides a levy to support ourhospital and asked the voters of the county if we should increase theFarm to Market levy from 10 mills to 20 mills. It was approved withapproximately 2/3 voting in favor. These two decisions made bylocal taxpayers would not be possible if Measure 2 passes.

47. The “County NEWS – serving county government for 39 years,” isthe official in-house organ for this government funded organization, theNorth Dakota Association of Counties. This organization is funded by duespaid by counties with taxpayer money. For example Ward County paysmore than $20,000 each year for membership. County dues for 2011 were$449,100 up from $421,424 in 2010. While prohibited by NDCC 16.1 fromtaking positions on ballot measures, either supporting or opposing it is clearNDACo and its sister (or is it brother) organization NDCCA believe this law(which as passed during the 2011 legislative session and signed by thegovernor into law) does not apply to them.

48. The North Dakota League of Cities is a group of North Dakotacities which pay and use public funds to be a member of that organizationand has publicly stated opposition to North Dakota Property TaxAmendment, Measure 2.

On January 3, 2012, the League of Cities appeared before the KiwanisClub in Minot to address Measure 2 (of course, Empower the

Taxpayer was not invited to speak and provide factual informationand answer questions). The presentation was covered by KXMC andcan be watched athttp://www.kxnet.com/story/16438839/measure-two This was the written report done by KXMC on the matter:

8/3/2019 Abolish Property Taxes Lawsuit

http://slidepdf.com/reader/full/abolish-property-taxes-lawsuit 35/45

Empower the Taxpayer Complaint – page 35

Would you like to get rid of your property tax bill?The June primary ballot in North Dakota will have a

measure that would eliminate property tax from the state.But the North Dakota League of Cities says if

Measure Two passes - and property taxes go away - it wouldbe devastating to towns across the state.