Valuation: Packet 2 Relative Valuation, Asset-based valuation and Private Company Valuation

1/21/2021

1

Business Valuation Essentials For Attorneys

Evan M. Levine, ChFCNainesh Shah, CFA

22

1

2

1/21/2021

2

3

4

…What’s the Question?

3

4

1/21/2021

3

Overview• Why?

• Purpose• Premise• Level• Standards

• How?• Qualitative and Quantitative Analysis

• When?• Impact of subsequent events on a valuation• COVID -19

5

Overview• What?

• Approaches and Methods

• discounts and premiums to business value

• Report Writing

• Who?

• Professional Organizations

• IRS

• Courts: Legal Cases

6

5

6

1/21/2021

4

7

Purpose for Business Valuation• Tax valuations

• ESOP• Succession planning

• M&A : Merger and acquisition• Selling or buying of a business• Employee buy-in situations

• Financial Accounting• Goodwill assessments• Intellectual property valuations

• Litigation• Shareholder dispute resolution• Insurance claims or settlements• Divorce

8

7

8

1/21/2021

5

Premise of Value1. Going concern

2. Assets Valuation

3. Liquidation

• orderly

• forced

9

Levels of Value• Minority v. Control

• Marketable v. Non-Marketable

10

9

10

1/21/2021

6

Standards of Value a) Fair market valueb) Fair valuec) Investment (strategic) valued) Intrinsic (fundamental) value

IRS Revenue Ruling 59-60 • Issued in 1959• Regarded as the single most important piece of

valuation literature• Outlined methods and factors to be used in valuing

closely held businesses• Involved itself with Estate and Gift Taxes• Provided for a series of valuation formulas or methods

11

IRS Revenue Ruling 59-60:“The price at which the property would change hands between a willing buyer and a willing seller, when the former is not under any compulsion to buy and the latter is not under any compulsion to sell, both parties having reasonable knowledge of relevant facts.”

12

11

12

1/21/2021

7

13

• Qualitative Analysis• Quantitative Analysis

14

13

14

1/21/2021

8

Qualitative Analysis• Economic Environment

• Industry background

• Company background

15

Economic Environment• Macro-environment

• National

• Regional & Metropolitan

• International elements

16

15

16

1/21/2021

9

Industry Background1. Economic data

2. Industry Information

• Structure

• Trends

• Life cycle

• Seasonality

17

Company Background1. Site visit and discussions with management

2. History and nature

3. Economic data

• cost structure

• pricing power

• margin analysis

4. SWOT analysis

18

17

18

1/21/2021

10

19

Quantitative Analysis • Financial statements

1. Source

• audited/reviewed/compiled/tax returns/internal

2. Number of years to obtain

3. Common size

4. Trend analysis

5. Ratios

6. Comparative analysis

a) Specific company

b) Industry averages

20

19

20

1/21/2021

11

Adjustments to Financial Statements

1. Normalizing

a) Control v. non-control

b) Discretionary

c) Reasonable compensation analysis

d) Extraordinary/non-recurring

2. Operating v. non-operating items

3. Off-balance sheet and unrecorded items

21

Benefits Streams and Selection

1. Appropriate time periods

2. Appropriate income/cash flow

3. Growth assumptions

4. Pass-through entities

• tax effecting of the benefit stream

22

21

22

1/21/2021

12

23

Defining the Engagement • Valuation date and its importance

• Known and Knowable

• COVID-19

24

23

24

1/21/2021

13

25

Valuation ApproachesA. Income approach

B. Market approach

C. Asset Approach

26

25

26

1/21/2021

14

Income Approach1. General theory

2. Defining applicable income/cash flow

3. Sources of data

4. Capitalization/discount rates

27

Income Approach Commonly used methods:

a) Capitalized cash flow method (CCF)

• Gordon Growth Model (constant growth model)

b) Discounted cash flow method (DCF),

• Gordon Growth Model (two stage model)

c) Dividend paying capacity

28

27

28

1/21/2021

15

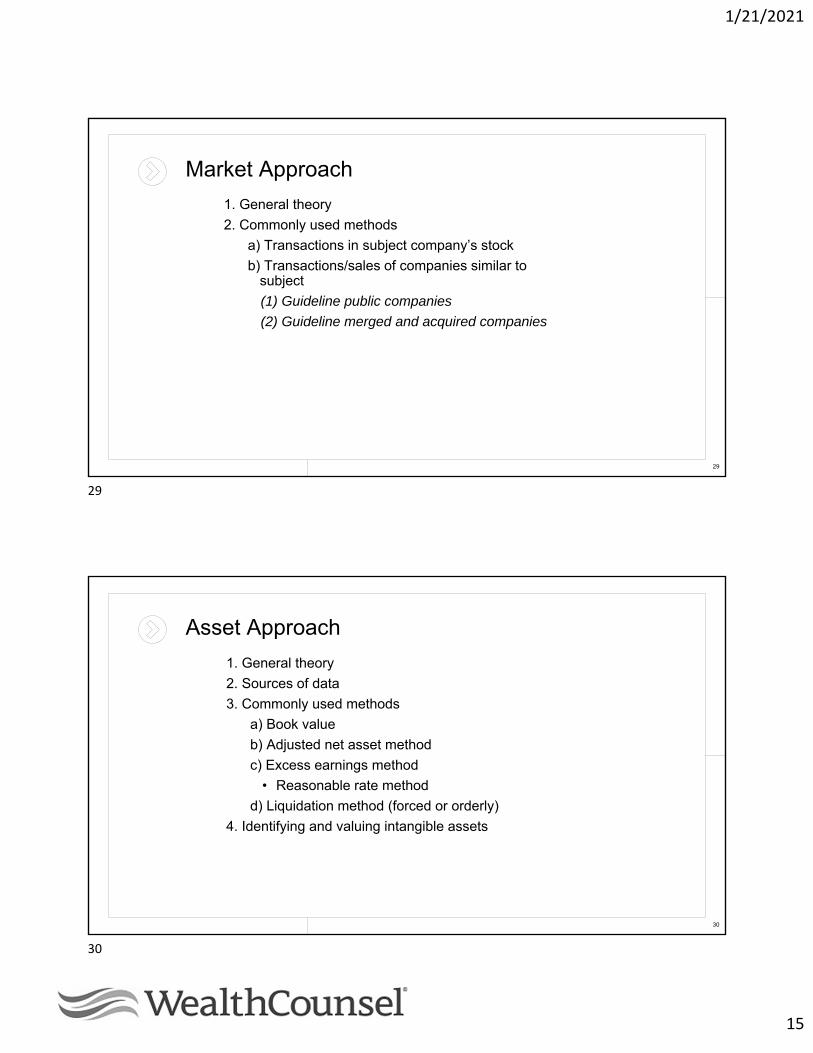

Market Approach

1. General theory

2. Commonly used methods

a) Transactions in subject company’s stock

b) Transactions/sales of companies similar tosubject

(1) Guideline public companies

(2) Guideline merged and acquired companies

29

Asset Approach

1. General theory

2. Sources of data

3. Commonly used methods

a) Book value

b) Adjusted net asset method

c) Excess earnings method

• Reasonable rate method

d) Liquidation method (forced or orderly)

4. Identifying and valuing intangible assets

30

29

30

1/21/2021

16

Sanity Checks1. General theory

2. Sources of data

3. Commonly used methods

a) Industry formulas (“Rules of Thumb”)

b) Justification of purchase

4. Reconciliation of indicated values

31

Discounts, Premiums, and other Adjustments

32

31

32

1/21/2021

17

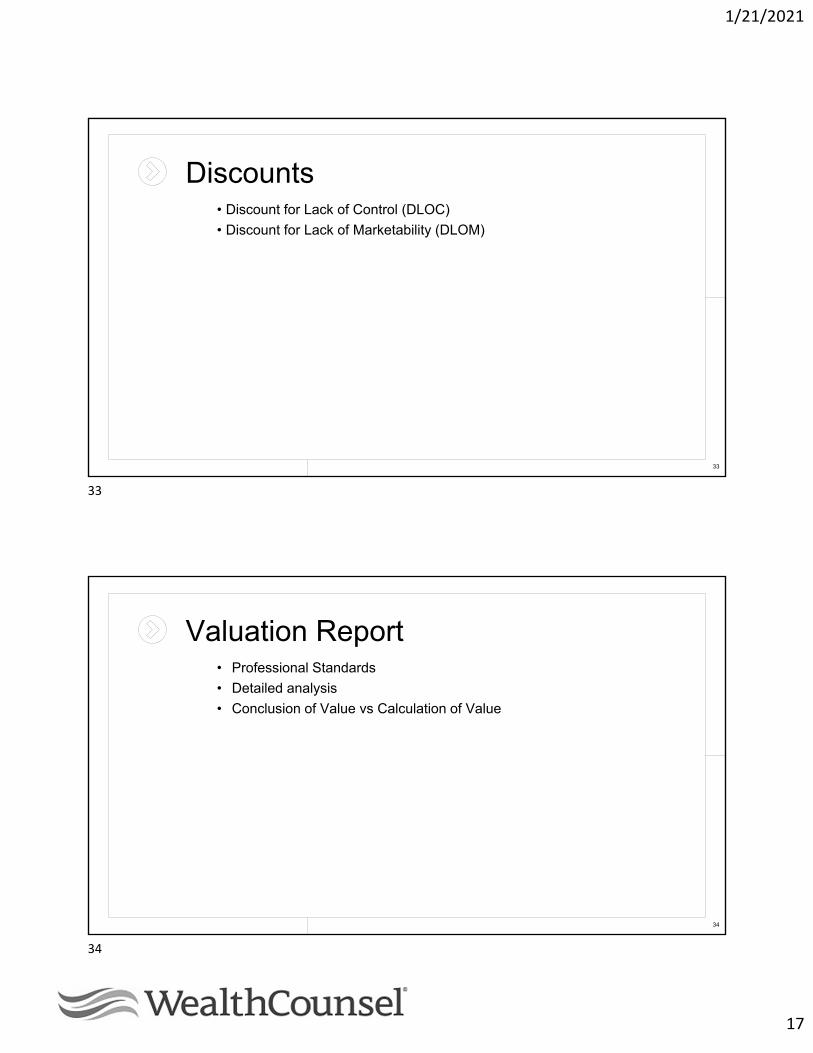

Discounts• Discount for Lack of Control (DLOC)

• Discount for Lack of Marketability (DLOM)

33

Valuation Report• Professional Standards

• Detailed analysis

• Conclusion of Value vs Calculation of Value

34

33

34

1/21/2021

18

35

Groups Involved in the Valuation Space

• Professional Organizations

• AICPA

• NACVA

• ASA

• IBA

• Regulators

• Courts

• DATABASE PROVIDERS

• APPRAISERS

36

35

36

1/21/2021

19

Valuation Report

• Professional Standards

• Detailed analysis

• Conclusion of Value vs. Calculation of Value

37

…..Re-cap

38

37

38

1/21/2021

20

For More Information Contact:

Evan Levine

516-240-6161

www.completeadvisors.com

40

41

Questions?

41

40

41