ATTORNEYS’ TITLE INSURANCE FUND, INC. · bank, trust Company, broker, ... ATTORNEYS’ TITLE...

26

REPORT ON EXAMINATION OF ATTORNEYS’ TITLE INSURANCE FUND, INC. ORLANDO, FLORIDA AS OF DECEMBER 31, 2006 BY THE OFFICE OF INSURANCE REGULATION

Transcript of ATTORNEYS’ TITLE INSURANCE FUND, INC. · bank, trust Company, broker, ... ATTORNEYS’ TITLE...

REPORT ON EXAMINATION

OF

ATTORNEYS’ TITLE INSURANCE FUND, INC.

ORLANDO, FLORIDA

AS OF

DECEMBER 31, 2006

BY THE OFFICE OF INSURANCE REGULATION

TABLE OF CONTENTS LETTER OF TRANSMITTAL..........................................................................................................-

SCOPE OF EXAMINATION...................................................................................................... 1 STATUS OF ADVERSE FINDINGS FROM PRIOR EXAMINATION ....................................................... 2

HISTORY ...................................................................................................................................... 4 GENERAL ..................................................................................................................................... 4 CAPITAL STOCK ........................................................................................................................... 4 PROFITABILITY OF COMPANY ...................................................................................................... 5 DIVIDENDS TO STOCKHOLDERS ................................................................................................... 5 MANAGEMENT............................................................................................................................. 5 CONFLICT OF INTEREST PROCEDURE............................................................................................ 8 CORPORATE RECORDS ................................................................................................................. 8 ACQUISITIONS, MERGERS, DISPOSALS, DISSOLUTIONS, AND PURCHASE OR SALES THROUGH REINSURANCE.............................................................................................................................. 8 SURPLUS DEBENTURES ................................................................................................................ 8

AFFILIATED COMPANIES ...................................................................................................... 9

ORGANIZATIONAL CHART ................................................................................................. 10 TAX ALLOCATION AGREEMENT................................................................................................. 11

FIDELITY BOND AND OTHER INSURANCE..................................................................... 11

PENSION, STOCK OWNERSHIP AND INSURANCE PLANS .......................................... 12

STATUTORY DEPOSITS......................................................................................................... 12

INSURANCE PRODUCTS AND RELATED PRACTICES.................................................. 12 TERRITORY ................................................................................................................................ 13 TREATMENT OF POLICYHOLDERS............................................................................................... 13

REINSURANCE ......................................................................................................................... 14

ASSUMED................................................................................................................................... 14 CEDED ....................................................................................................................................... 14

ACCOUNTS AND RECORDS.................................................................................................. 14 CUSTODIAL AGREEMENT ........................................................................................................... 15

FINANCIAL STATEMENTS PER EXAMINATION............................................................ 15 ASSETS ...................................................................................................................................... 16 LIABILITIES, SURPLUS AND OTHER FUNDS ................................................................................ 17 STATEMENT OF INCOME............................................................................................................. 18

COMMENTS ON FINANCIAL STATEMENTS.................................................................... 19 LIABILITIES................................................................................................................................ 19

COMPARATIVE ANALYSIS OF CHANGES IN SURPLUS............................................... 20

SUMMARY OF FINDINGS ...................................................................................................... 21

CONCLUSION ........................................................................................................................... 22

Tallahassee, Florida August 19, 2007 Honorable Kevin M. McCarty Secretary, Southeastern Zone, NAIC Commissioner of Insurance Regulation Office of Insurance Regulation 200 E. Gaines Street Tallahassee, Florida 32399-0326 Honorable Jim Poolman Secretary, Midwestern Zone, NAIC Commissioner North Dakota Dept. of Insurance 600 E. Blvd. Bismarck, North Dakota 58505-0320 Honorable Alfred W. Gross Chairman Financial Condition (E) Committee State Corporation Commission Bureau of Insurance Commonwealth of Virginia PO Box 1157 Richmond, Virginia 23218 Dear Sirs and Madam: Pursuant to your instructions, in compliance with Section 624.316, Florida Statutes, and in accordance with the practices and procedures promulgated by the National Association of Insurance Commissioners (NAIC), we have conducted an examination of December 31, 2006, of the financial condition and corporate affairs of:

ATTORNEYS’ TITLE INSURANCE FUND, INC. 6545 CORPORATE CENTRE BOULEVARD

ORLANDO, FLORIDA 32822 Hereinafter referred to as the “Company”. Such report of examination is herewith respectfully submitted.

1

SCOPE OF EXAMINATION

This examination covered the period of January 1, 2002 through December 31, 2006. The

Company was last examined by representatives of the Florida Office of Insurance Regulation

(Office) as of December 31, 2001. This examination commenced, with planning at the Office, on

June 11, 2007, to June 15, 2007. The fieldwork commenced on June 18, 2007, and was

concluded as of December 19, 2007.

This financial examination was an association examination conducted in accordance with the

Financial Condition Examiners Handbook, Accounting Practices and Procedures Manual and

annual statement instructions promulgated by the NAIC as adopted by Rules 69O-137.001(4) and

69O-138.001, Florida Administrative Code, with due regard to the statutory requirements of the

insurance laws and rules of the State of Florida.

In this examination, emphasis was directed to the quality, value and integrity of the statement of

assets and the determination of liabilities, as those balances affect the financial solvency of the

Company as of December 31, 2006. Transactions subsequent to year-end 2006 were reviewed

where relevant and deemed significant to the Company’s financial condition.

The examination included a review of the corporate records and other selected records deemed

pertinent to the Company’s operations and practices. In addition, the NAIC IRIS ratio reports, the

A.M. Best Report, the Company’s independent audit reports and certain work papers prepared by

the Company’s independent certified public accountant (CPA) and other reports as considered

necessary were reviewed and utilized where applicable within the scope of this examination.

2

This report of examination is confined to financial statements and comments on matters that

involve departures from laws, regulations or rules, or which are deemed to require special

explanation or description.

Based on the review of the Company’s control environment and the materiality level set for this

examination, reliance was placed on work performed by the Company’s CPAs, after verifying the

statutory requirements, for the following accounts:

Federal and Foreign Income Taxes Agents’ Balances – Premiums not collected

Status of Adverse Findings from Prior Examination

The following is a summary of significant adverse findings contained in the Office’s prior

examination report as of December 31, 2001, along with resulting action taken by the Company

in connection therewith.

Securities Custodian

Morgan Stanley Dean Witter, a broker, had custody of securities for the Company. The broker was

not an authorized custodian in accordance with Rule 69O-143.042 and 69O-143.041(2), Florida

Administrative Code. Resolution: The recent amendment to Section 628.511(2)(c), Florida

Statutes provided an updated definition of a custodian. Custodian means a national bank, state

bank, trust Company, broker, or dealer that participated in a clearing corporation. The broker who

has custody of the Company securities is now an acceptable custodian.

Reporting of Security Trades

In the 2001 annual statement, the Company incorrectly recorded the amount of $1,003,978 as due

from the broker for four stocks not traded or settled until late January and February of 2002. This

3

was not only inaccurate recording but also resulted in an $118,007 overstatement of Company

assets on the 2001 annual statement. Resolution: The Company recognized the problem and

correctly recorded the security trades on subsequent annual statements.

Custody Agreement

The Company’s custody agreement with First Union National Bank did not meet all of the

requirements of Rule 69O-143.042, Florida Administrative Code. Resolution: First Union

National Bank was merged into Wachovia Bank. The Company had a corrected custody

agreement with Wachovia Bank.

Escrow Accounts

The Company had a checking account with SunTrust and an associated 001 sweep account. The

account had a December 31, 2001 balance of $16,822,686, of which $2,256 was identified as

Company funds. This account did not segregate funds held for others as required by SSAP No. 1.

The associated sweep account earned $64,024 of interest in 2001 that was retained by the

Company. This was in violation of Rule 69O-186.008(3), Florida Administrative Code, which

requires that escrow funds received not be deposited in an interest – bearing account without the

written consent of the buyer and seller. Resolution: The Company submitted a new escrow

agreement to the Office. The Office subsequently approved the new agreement.

Review of 1998 Examination Report

The Company’s board of directors meeting minutes did not reflect a review of the 1998 report of

examination by the Office. Resolution: The Company presented the report of examination at the

2002 annual board of directors meeting and noted its review in the board of director minutes.

4

HISTORY

General

The Company was incorporated in Florida on November 21, 1985, under the laws of the State of

Florida, as a stock title insurer and commenced business on January 1, 1986, as Attorneys’ Title

Insurance Fund, Inc.

The Company’s parent was created as a business trust on March 22, 1947, under the name of

Lawyers’ Title Guaranty Fund. On July 1, 1982, its name was changed to Attorneys’ Title

Insurance Fund. The trust was owned by members consisting of attorneys.

On January 1, 1986, Attorneys’ Title Insurance Fund merged its operations and transferred its

assets and liabilities into the Company in exchange for all of the Company’s 1,000,000 shares of

Class A voting stock.

The Company was authorized to transact title insurance coverage in the State of Florida on

December 31, 2006.

Capital Stock

As of December 31, 2006, the Company’s capitalization was as follows:

Number of authorized common (A) capital shares 10,000,000 Number of shares common (A) issued and outstanding 2,000,000 Number of authorized common (B) capital shares 5,000,000 Number of shares common (B) issued and outstanding 0 Total common capital stock $2,000,000 Par value per share $1.00

Control of the Company was maintained by its parent, Attorneys’ Title Insurance Fund, which

owned 100% of the stock issued by the Company.

5

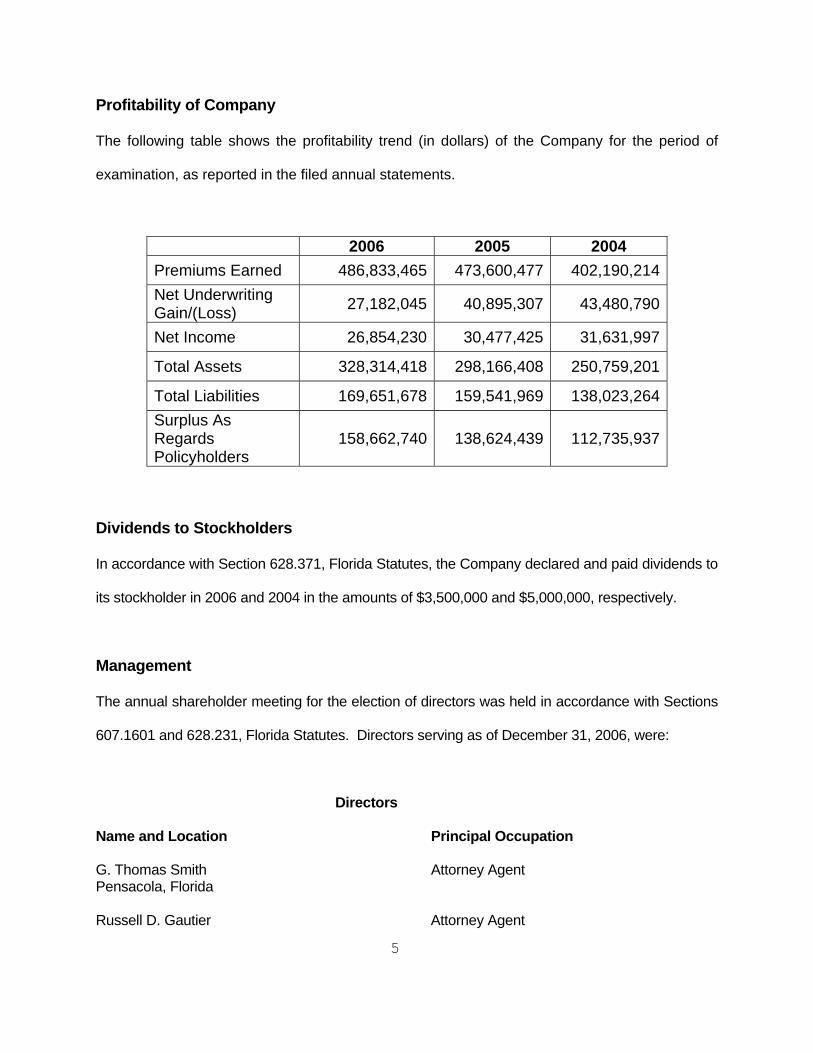

Profitability of Company

The following table shows the profitability trend (in dollars) of the Company for the period of

examination, as reported in the filed annual statements.

2006 2005 2004 Premiums Earned 486,833,465 473,600,477 402,190,214Net Underwriting Gain/(Loss) 27,182,045 40,895,307 43,480,790

Net Income 26,854,230 30,477,425 31,631,997

Total Assets 328,314,418 298,166,408 250,759,201

Total Liabilities 169,651,678 159,541,969 138,023,264Surplus As Regards Policyholders

158,662,740 138,624,439 112,735,937

Dividends to Stockholders

In accordance with Section 628.371, Florida Statutes, the Company declared and paid dividends to

its stockholder in 2006 and 2004 in the amounts of $3,500,000 and $5,000,000, respectively.

Management

The annual shareholder meeting for the election of directors was held in accordance with Sections

607.1601 and 628.231, Florida Statutes. Directors serving as of December 31, 2006, were:

Directors

Name and Location Principal Occupation

G. Thomas Smith Attorney Agent Pensacola, Florida Russell D. Gautier Attorney Agent

6

Tallahassee, Florida

Michael S. Smith Attorney Agent Perry, Florida

Duane C. Romanello Attorney Agent Jacksonville, Florida

Del G. Potter Attorney Agent Mt. Dora, Florida Julius J. Zschau Attorney Agent Clearwater, Florida Michael A. Pyle Attorney Agent Ormond Beach, Florida Melissa J. Murphy Attorney Agent, Chairman Gainesville, Florida Victor E. Woodman Attorney Agent Winter Park, Florida George T. Dunlap, III Attorney Agent Bartow, Florida Richard W. Lyons Attorney Agent Miami, Florida James L. Ritchey Attorney Agent Sarasota, Florida Stephen H. Reynolds Attorney Agent Tampa, Florida Stephen L. Mackey Attorney Agent Boca Raton, Florida Charles S. Isler, III Attorney Agent Panama City, Florida Thomas D. Wright Attorney Agent Marathon, Florida George R. Maraitis Attorney Agent Ft. Lauderdale, Florida Jerry W. Allender Attorney Agent Titusville, Florida

7

Richard J. Dungey Attorney Agent Stuart, Florida Peter J. Gravina Attorney Agent Ft. Myers, Florida

The Board of Directors in accordance with the Company’s bylaws appointed the following senior

officers:

Senior Officers

Name Title

Charles James Kovaleski President Robert Norwood Gay, III Secretary Jimmy Roger Jones Treasurer Michael Roy Hammond Senior Vice President Barbara Gwen Geier Senior Vice President Sharon Kay Priest Senior Vice President Jeannie Lynn Calabrese Senior Vice President Louis Brent Guttman, III Vice President Sue Ellen Foreman Vice President William Theodore Conner Vice President Patricia Pearl Jones Vice President George Robert Arnold Vice President Matthew Allen Lewis Assistant Vice President The Company’s board appointed several internal committees in accordance with Section

607.0825, Florida Statutes. Following are the principal internal board committees and their

members as of December 31, 2006:

Executive Committee Audit Committee Investment Committee

Russell Gautier1 Thomas Smith 1 Jerry Allender 1 Charles Isler Jerry Allender Russell Gautier George Moraitis George Moraitis Charles Isler Melissa Murphy Stephen Reynolds Richard Lyons Del Potter James Ritchey George Moraitis Stephen Reynolds Michael Smith Del Potter

Thomas Wright Thomas Wright Thomas Smith

Julius Zschau Victor Woodman

8

1 Chairman

Conflict of Interest Procedure

The Company adopted a policy statement requiring annual disclosure of conflicts of interest in

accordance with the NAIC Financial Condition Examiners Handbook. No exceptions were noted

during this examination period.

Corporate Records

The recorded minutes of the shareholder, Board of Directors, and certain internal committees

were reviewed for the period under examination. The recorded minutes of the Board

adequately documented its meetings and approval of Company transactions and events in

accordance with Section 607.1601, Florida Statutes, including the authorization of investments

as required by Section 625.304, Florida Statutes.

Acquisitions, Mergers, Disposals, Dissolutions, and Purchase or Sales through

Reinsurance

The Company did not have any acquisitions, mergers, disposals, dissolutions, purchases or sales

through reinsurance during the period January 1, 2002 to December 31, 2006.

Surplus Debentures

The Company did not have any surplus debentures as December 31, 2006.

9

AFFILIATED COMPANIES

The Company was a member of an insurance holding company system as defined by Rule

69O-143.045(3), Florida Administrative Code. The latest holding company registration

statement was filed with the State of Florida on February 17, 2007, as required by Section

628.801, Florida Statutes, and Rule 69O-143.046, Florida Administrative Code.

10

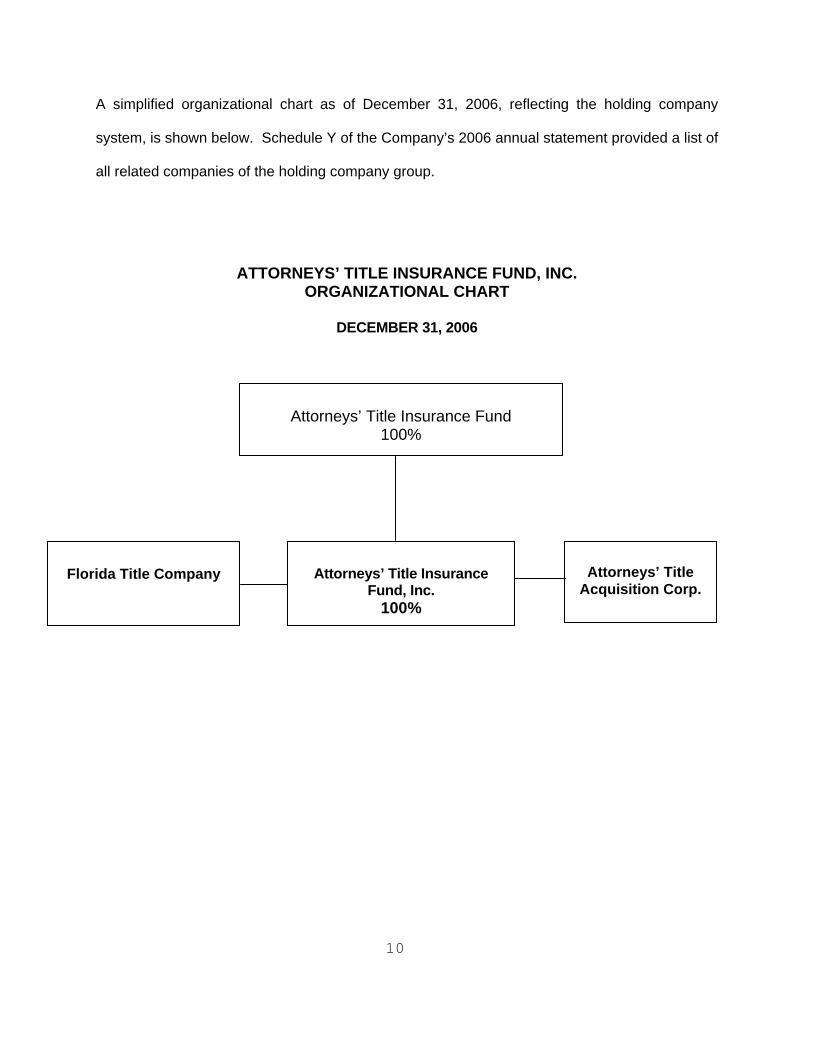

A simplified organizational chart as of December 31, 2006, reflecting the holding company

system, is shown below. Schedule Y of the Company’s 2006 annual statement provided a list of

all related companies of the holding company group.

ATTORNEYS’ TITLE INSURANCE FUND, INC. ORGANIZATIONAL CHART

DECEMBER 31, 2006

Attorneys’ Title

Acquisition Corp.

Attorneys’ Title Insurance Fund

100%

Attorneys’ Title Insurance

Fund, Inc. 100%

Florida Title Company

11

The following agreements were in effect between the Company and its affiliates:

Tax Allocation Agreement

The Company, along with its parent and affiliates, filed a consolidated federal income tax return.

On December 31, 2006, the method of allocation was apportioned among the members of the

affiliated group in accordance with the ratio that the portion of the consolidated income attributable

to each member of the group having taxable income bears to the consolidated taxable income.

Under the percentage method an additional amount shall be allocated to each member of the

group equal to 100% of the excess, if any, of the separate return tax liability for such member for

the tax year and credited to the members that had items of income, deduction, credit, and so forth

to which any difference was attributable.

FIDELITY BOND AND OTHER INSURANCE

The Company maintained fidelity bond coverage up to $7,500,000 with a deductible of $50,000,

which adequately covered the suggested minimum amount of coverage for the Company as

recommended by the NAIC.

The Company carried the following insurance coverage during the period covered by the

examination: Commercial application, general liability, flood, commercial application pollution

liability, Directors Officers, inland marine, automobile umbrella excess liability, boiler & machinery,

and workers compensation.

12

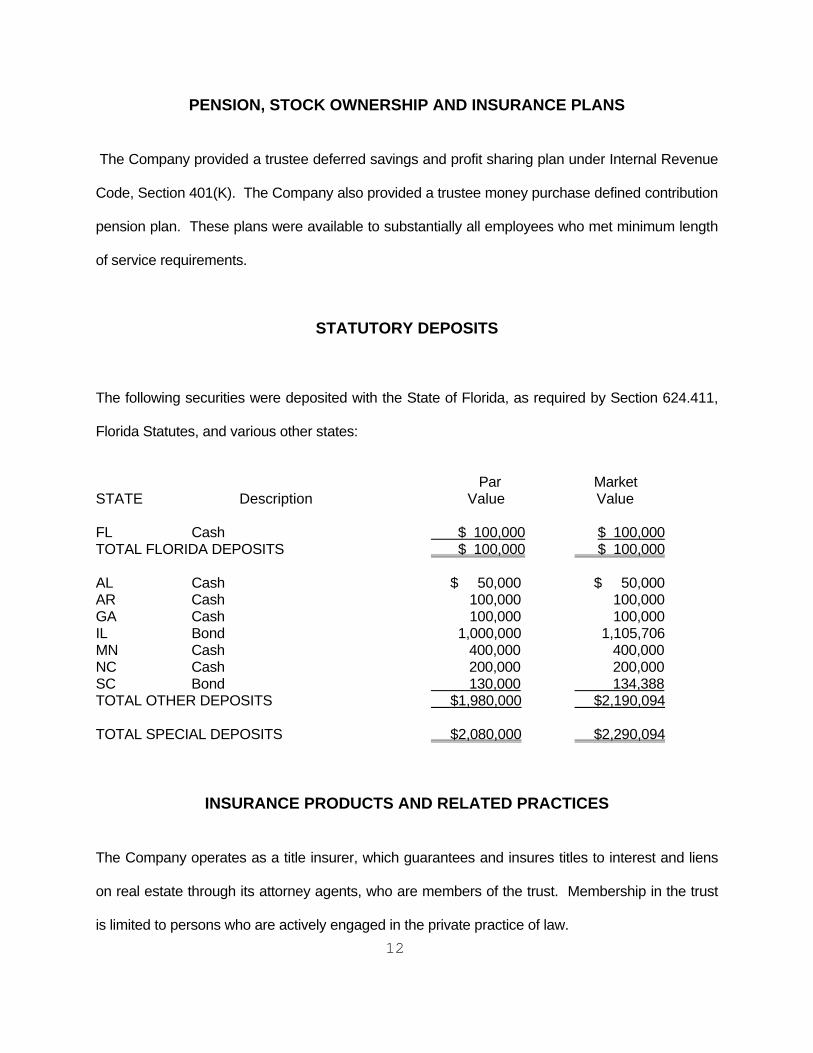

PENSION, STOCK OWNERSHIP AND INSURANCE PLANS

The Company provided a trustee deferred savings and profit sharing plan under Internal Revenue

Code, Section 401(K). The Company also provided a trustee money purchase defined contribution

pension plan. These plans were available to substantially all employees who met minimum length

of service requirements.

STATUTORY DEPOSITS

The following securities were deposited with the State of Florida, as required by Section 624.411,

Florida Statutes, and various other states:

Par Market STATE Description Value Value FL Cash $ 100,000 $ 100,000 TOTAL FLORIDA DEPOSITS $ 100,000 $ 100,000 AL Cash $ 50,000 $ 50,000 AR Cash 100,000 100,000 GA Cash 100,000 100,000 IL Bond 1,000,000 1,105,706 MN Cash 400,000 400,000 NC Cash 200,000 200,000 SC Bond 130,000 134,388 TOTAL OTHER DEPOSITS $1,980,000 $2,190,094 TOTAL SPECIAL DEPOSITS $2,080,000 $2,290,094

INSURANCE PRODUCTS AND RELATED PRACTICES

The Company operates as a title insurer, which guarantees and insures titles to interest and liens

on real estate through its attorney agents, who are members of the trust. Membership in the trust

is limited to persons who are actively engaged in the private practice of law.

13

A title insurance policy comes in two forms, 1) an “owners policy”, which protects the interests of

the buyer, and 2) a “lender’s policy”, which protects the interests of the mortgage lender of the

property. Mortgage lenders require the borrowers to obtain a lender’s title insurance policy, which

provides an opinion of the condition of the lender’s interest in the title. A reasonable search and

examination of the title must be conducted before a title insurance policy may be issued. A title

insurance policy is required by Section 627.7845, Florida Statutes.

Title insurance coverage is for past defects that were in place at the time the property was sold,

which did not become noticed until after the property was transferred to the new owner.

Title search and abstract work are related title services that generate revenue from title plants. The

Company provides title information necessary to perform the title search and examination of the

title through the utilization of the title plants owned by the Company.

Territory

The Company was authorized to transact insurance in the following states and territories:

Florida Illinois Minnesota Georgia Indiana North Dakota Arkansas Maryland South Carolina Alabama Michigan North Carolina Puerto Rico

Treatment of Policyholders

The Company established procedures for handling written complaints in accordance with Section

626.9541(1) (j), Florida Statutes.

14

The Company maintained a claims procedure manual that included detailed procedures for

handling each type of claim in accordance with Section 626.9541(1)(i) 3a, Florida Statutes.

REINSURANCE

The reinsurance agreements reviewed complied with NAIC standards with respect to the standard

insolvency clause, arbitration clause, transfer of risk, reporting and settlement information

deadlines.

Assumed

The Company assumed risk on an excess of loss basis, and a facultative basis. The entity's

maximum liability was $3,210,000 on a single policy. The reinsurer's maximum coverage was

$25,000,000 per policy. The Company had Excess of Loss of 90% of insured's liability excess

of $3,000,000. All amounts greater than $30,000,000 were reinsured on a facultative policy.

Ceded

The Company ceded risk on a quota share and excess of loss basis to Old Republic National

Title Insurance Company. The Company retained risk for the first $3,000,000, then 30% up to

$10,000,000. Old Republic National Title Insurance Company assumed all risk above

$10,000,000 to $30,000,000 maximum.

ACCOUNTS AND RECORDS

The Company maintained its principal operational offices in Orlando, Florida, where this

examination was conducted.

15

An independent CPA audited the Company’s statutory basis financial statements annually for the

years 2002 to 2006, in accordance with Section 624.424(8), Florida Statutes. Supporting work

papers were prepared by the CPA as required by Rule 69O-137.002, Florida Administrative Code.

The Company’s accounting records were maintained on a computerized system. The Company’s

balance sheet accounts were verified with the line items of the annual statement submitted to the

Office.

The Company and non-affiliates had the following agreements:

Custodial Agreement

The Company had custodial agreements with Wachovia Bank and Morgan Stanley/Dean Witter.

The agreements were in compliance with Rule 69O-143.042, Florida Administrative Code.

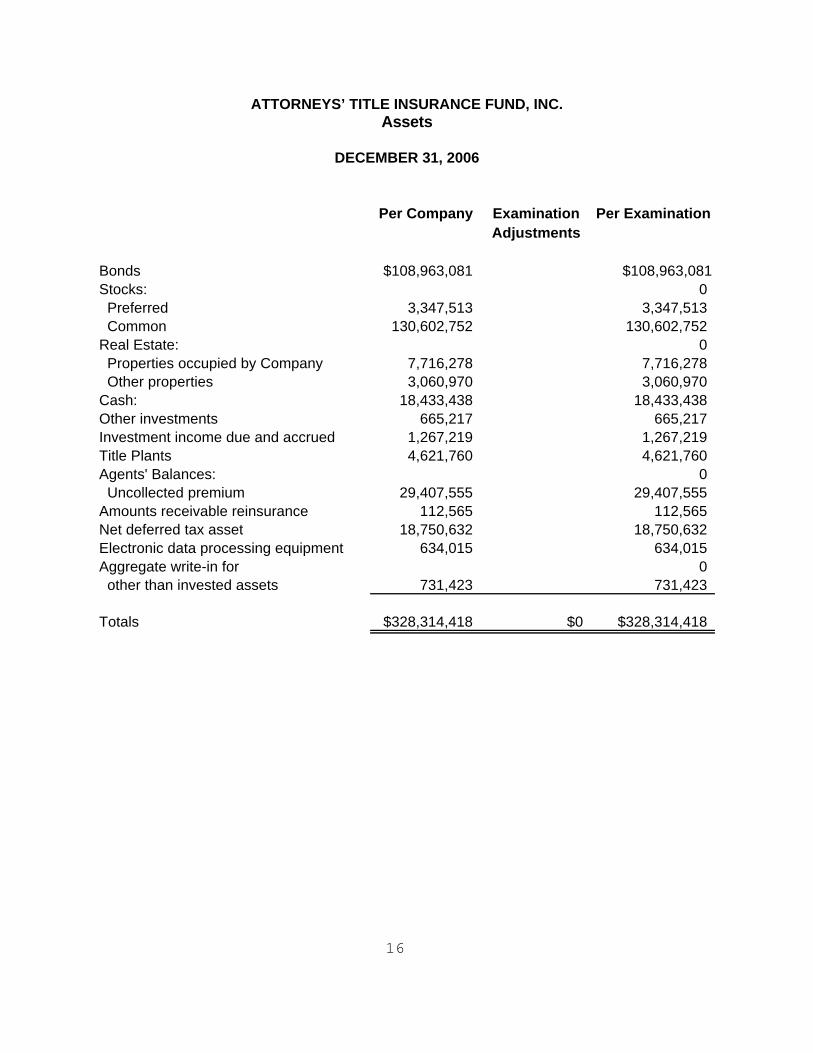

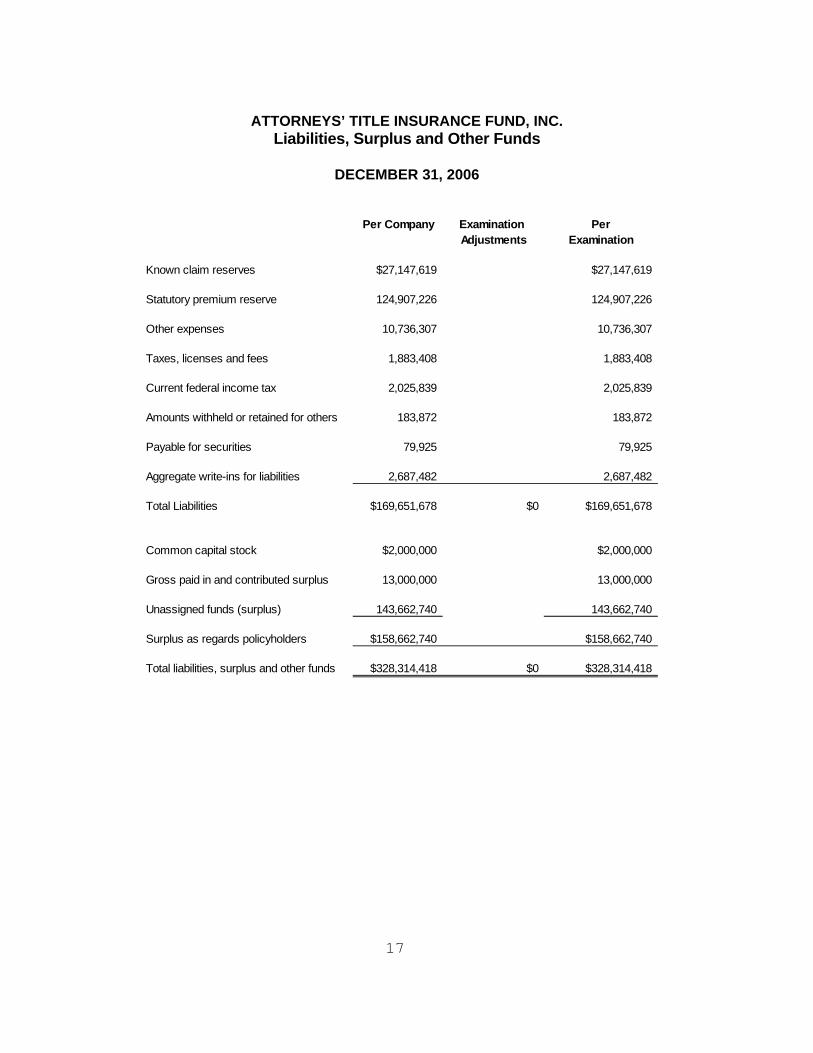

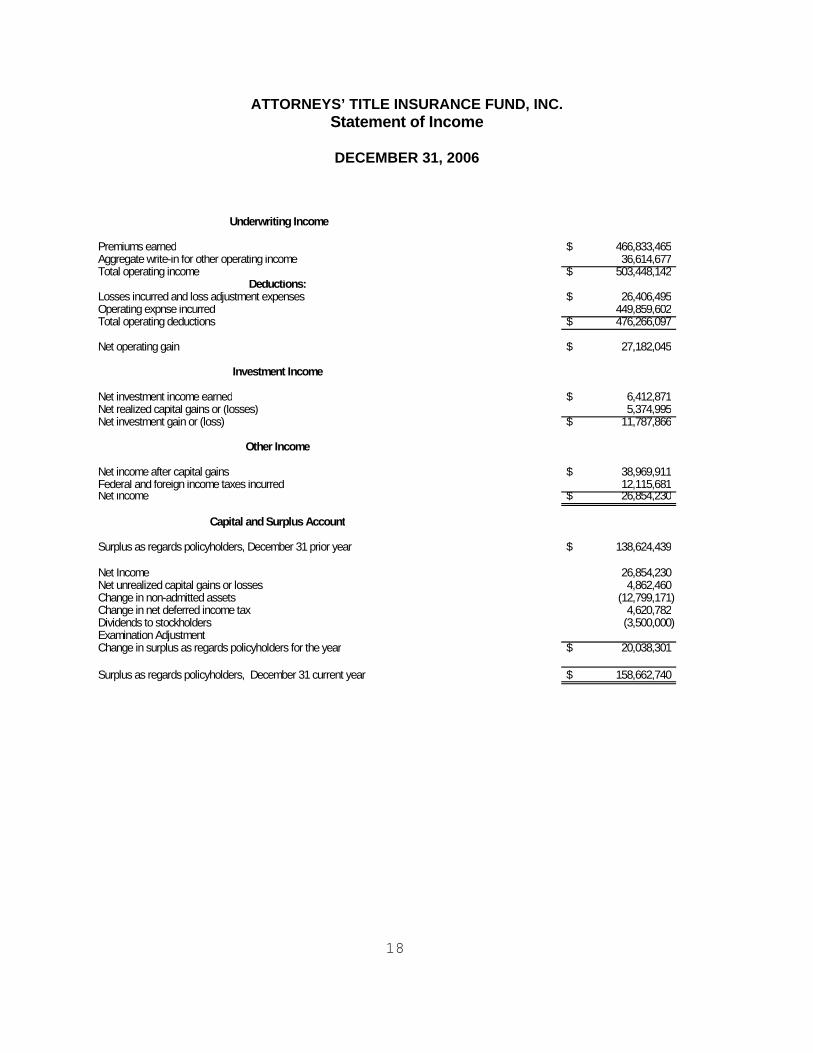

FINANCIAL STATEMENTS PER EXAMINATION

The following pages contain financial statements showing the Company’s financial position as of

December 31, 2006, and the results of its operations for the year then ended as determined by this

examination. Adjustments made as a result of the examination are noted in the section of this

report captioned, “Comparative Analysis of Changes in Surplus.”

16

ATTORNEYS’ TITLE INSURANCE FUND, INC. Assets

DECEMBER 31, 2006

Per Company Examination Per ExaminationAdjustments

Bonds $108,963,081 $108,963,081Stocks: 0 Preferred 3,347,513 3,347,513 Common 130,602,752 130,602,752Real Estate: 0 Properties occupied by Company 7,716,278 7,716,278 Other properties 3,060,970 3,060,970Cash: 18,433,438 18,433,438Other investments 665,217 665,217Investment income due and accrued 1,267,219 1,267,219Title Plants 4,621,760 4,621,760Agents' Balances: 0 Uncollected premium 29,407,555 29,407,555Amounts receivable reinsurance 112,565 112,565Net deferred tax asset 18,750,632 18,750,632Electronic data processing equipment 634,015 634,015Aggregate write-in for 0 other than invested assets 731,423 731,423

Totals $328,314,418 $0 $328,314,418

17

ATTORNEYS’ TITLE INSURANCE FUND, INC.

Liabilities, Surplus and Other Funds

DECEMBER 31, 2006

Per Company Examination PerAdjustments Examination

Known claim reserves $27,147,619 $27,147,619

Statutory premium reserve 124,907,226 124,907,226

Other expenses 10,736,307 10,736,307

Taxes, licenses and fees 1,883,408 1,883,408

Current federal income tax 2,025,839 2,025,839

Amounts withheld or retained for others 183,872 183,872

Payable for securities 79,925 79,925

Aggregate write-ins for liabilities 2,687,482 2,687,482

Total Liabilities $169,651,678 $0 $169,651,678

Common capital stock $2,000,000 $2,000,000

Gross paid in and contributed surplus 13,000,000 13,000,000

Unassigned funds (surplus) 143,662,740 143,662,740

Surplus as regards policyholders $158,662,740 $158,662,740

Total liabilities, surplus and other funds $328,314,418 $0 $328,314,418

18

ATTORNEYS’ TITLE INSURANCE FUND, INC. Statement of Income

DECEMBER 31, 2006

Underwriting Income

Premiums earned 466,833,465$ Aggregate write-in for other operating income 36,614,677Total operating income 503,448,142$

Deductions:Losses incurred and loss adjustment expenses 26,406,495$ Operating expnse incurred 449,859,602Total operating deductions 476,266,097$

Net operating gain 27,182,045$

Investment Income

Net investment income earned 6,412,871$ Net realized capital gains or (losses) 5,374,995Net investment gain or (loss) 11,787,866$

Other Income

Net income after capital gains 38,969,911$ Federal and foreign income taxes incurred 12,115,681Net income 26,854,230$

Capital and Surplus Account

Surplus as regards policyholders, December 31 prior year 138,624,439$

Net Income 26,854,230Net unrealized capital gains or losses 4,862,460Change in non-admitted assets (12,799,171)Change in net deferred income tax 4,620,782Dividends to stockholders (3,500,000)Examination AdjustmentChange in surplus as regards policyholders for the year 20,038,301$

Surplus as regards policyholders, December 31 current year 158,662,740$

19

COMMENTS ON FINANCIAL STATEMENTS

Liabilities

Losses $27,147,619 An outside actuarial firm appointed by the Board of Directors, rendered an opinion that the

amounts carried in the balance sheet as of December 31, 2006, make a reasonable provision for

all unpaid loss and loss expense obligations of the Company under the terms of its policies and

agreements.

Kay Kufera, FCAS, MAAA of Veris Consulting, LLC, an outside actuarial firm contracted by the

Office, reviewed work papers provided by the Company and was in concurrence with this opinion.

A comparative analysis of changes in surplus is shown below.

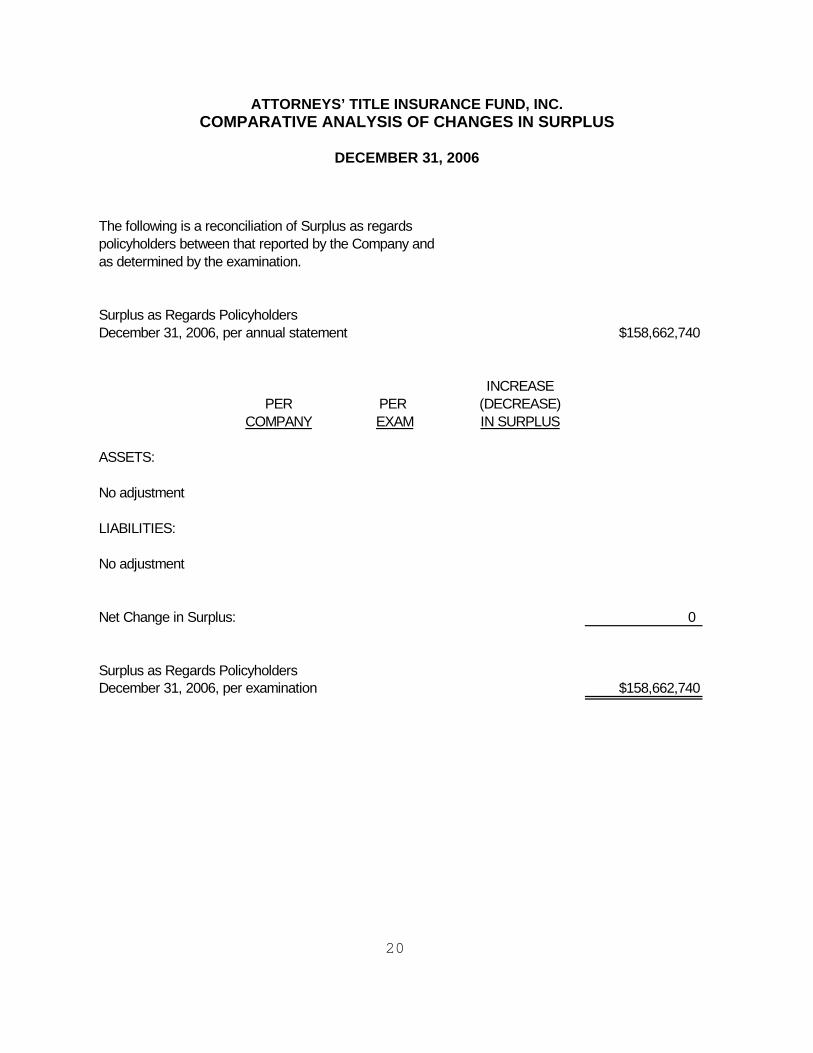

20

ATTORNEYS’ TITLE INSURANCE FUND, INC. COMPARATIVE ANALYSIS OF CHANGES IN SURPLUS

DECEMBER 31, 2006 The following is a reconciliation of Surplus as regardspolicyholders between that reported by the Company andas determined by the examination.

Surplus as Regards PolicyholdersDecember 31, 2006, per annual statement $158,662,740

INCREASEPER PER (DECREASE)

COMPANY EXAM IN SURPLUS

ASSETS:

No adjustment

LIABILITIES:

No adjustment

Net Change in Surplus: 0

Surplus as Regards PolicyholdersDecember 31, 2006, per examination $158,662,740

21

SUMMARY OF FINDINGS

Compliance with previous directives

The Company has taken the necessary actions to comply with the comments made in the 2001

examination report issued by the Office.

Current examination comments and corrective action

The Company did not have any items that needed corrective actions taken.

22

CONCLUSION

The insurance examination practices and procedures as promulgated by the NAIC have been

followed in ascertaining the financial condition of Attorneys’ Title Insurance Fund, Inc. as of

December 31, 2006, consistent with the insurance laws of the State of Florida.

Per examination findings, the Company’s Surplus as regards policyholders was $158,662,740,

in compliance with Section 624.408, Florida Statutes.

In addition to the undersigned, Kethessa Carpenter, CPA, Financial Examiner/Analyst

Supervisor, Owen Anderson, Financial Examiner/Analyst II, and Samita Lamsal, Financial

Examiner/Analyst II participated in the examination. We also recognize the participation of Kay

Kufera, FCAS, MAAA of Veris Consulting, LLC in the examination.

Respectfully submitted,

___________________________ James D. Collins Reinsurance/Financial Specialist Florida Office of Insurance Regulation Mary James, CFE Financial Administrator Florida Office of Insurance Regulation