2017 FULL YEAR RESULTS - SEGRO

56

2017 FULL YEAR RESULTS 16 FEBRUARY 2018

Transcript of 2017 FULL YEAR RESULTS - SEGRO

2017 FULL YEAR RESULTS16 FEBRUARY 2018

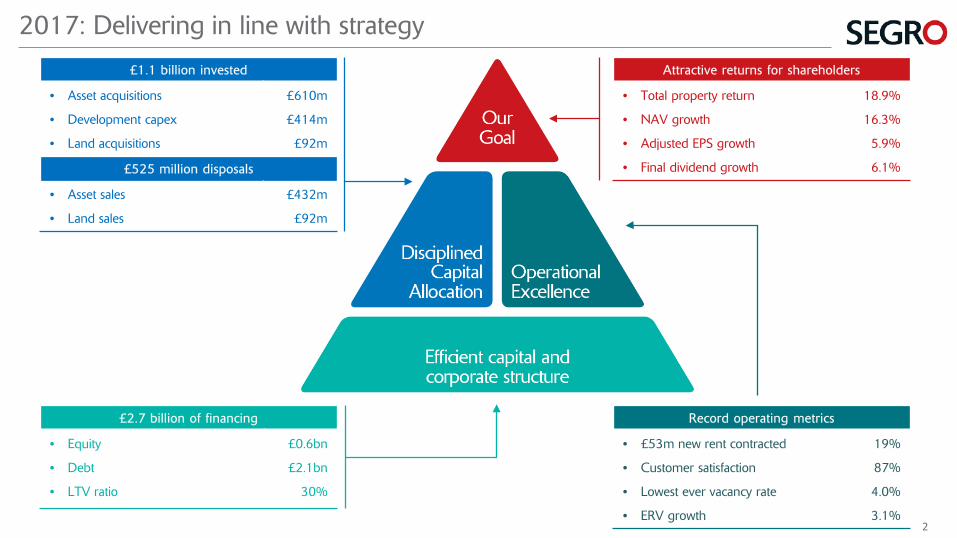

2017: Delivering in line with strategy

Attractive returns for shareholders

• Total property return

• NAV growth

• Adjusted EPS growth

• Final dividend growth

18.9%

16.3%

5.9%

6.1%

Record operating metrics

• £53m new rent contracted

• Customer satisfaction

• Lowest ever vacancy rate

• ERV growth

19%

87%

4.0%

3.1%

£1.1 billion invested

• Asset acquisitions

• Development capex

• Land acquisitions

£610m

£414m

£92m

£525 million disposals

• Asset sales

• Land sales

£432m

£92m

£2.7 billion of financing

• Equity

• Debt

• LTV ratio

£0.6bn

£2.1bn

30%

2

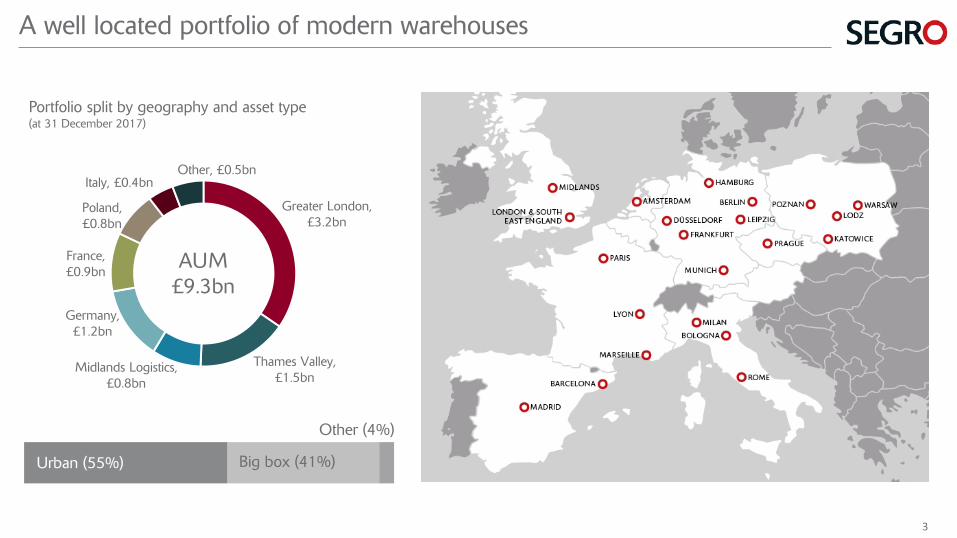

Greater London, £3.2bn

Thames Valley, £1.5bn

Midlands Logistics, £0.8bn

Germany, £1.2bn

France, £0.9bn

Poland, £0.8bn

Italy, £0.4bnOther, £0.5bn

A well located portfolio of modern warehouses

AUM£9.3bn

Urban (55%) Big box (41%)

Other (4%)

Portfolio split by geography and asset type(at 31 December 2017)

3

OneExpress, Vailog Interporto Bologna

Strong momentum going into 2018

Supportive market with structural drivers

Further rental income growth potential

Profitable development pipeline

Strong balance sheet

4

2017: Another year of delivery

Strong financial results and significantly improved capital structure

Disciplined capital allocation improving portfolio scale and quality

Operational excellence delivers strong operating and development performance

Significant growth opportunities within our control

SEGRO Park Düsseldorf-Sud

5

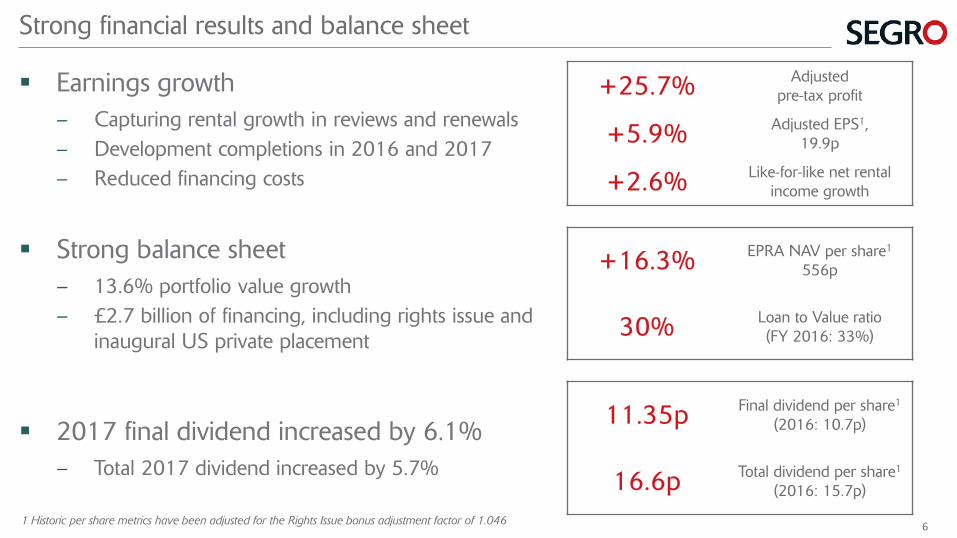

Strong financial results and balance sheet

Earnings growth– Capturing rental growth in reviews and renewals– Development completions in 2016 and 2017– Reduced financing costs

+25.7% Adjustedpre-tax profit

+5.9% Adjusted EPS1, 19.9p

+2.6% Like-for-like net rental income growth

Strong balance sheet– 13.6% portfolio value growth– £2.7 billion of financing, including rights issue and

inaugural US private placement

+16.3% EPRA NAV per share1

556p

30% Loan to Value ratio(FY 2016: 33%)

2017 final dividend increased by 6.1%– Total 2017 dividend increased by 5.7%

11.35p Final dividend per share1

(2016: 10.7p)

16.6p Total dividend per share1

(2016: 15.7p)

1 Historic per share metrics have been adjusted for the Rights Issue bonus adjustment factor of 1.046 6

2016

net

rent

al in

com

e

Disp

osal

s

Acq

uisit

ions

Like

-for-

like

NRI

Com

plet

edde

velo

pmen

ts

Take

-bac

ks fo

rde

velo

pmen

t

Oth

er

Cur

renc

y

2017

net

rent

al in

com

e

Pro

form

a 20

17(s

ee s

lide

35)

£(18.8)m

£19.9m

£20.4m

£(1.5)m£4.5m

£(1.8)m

£5.9m

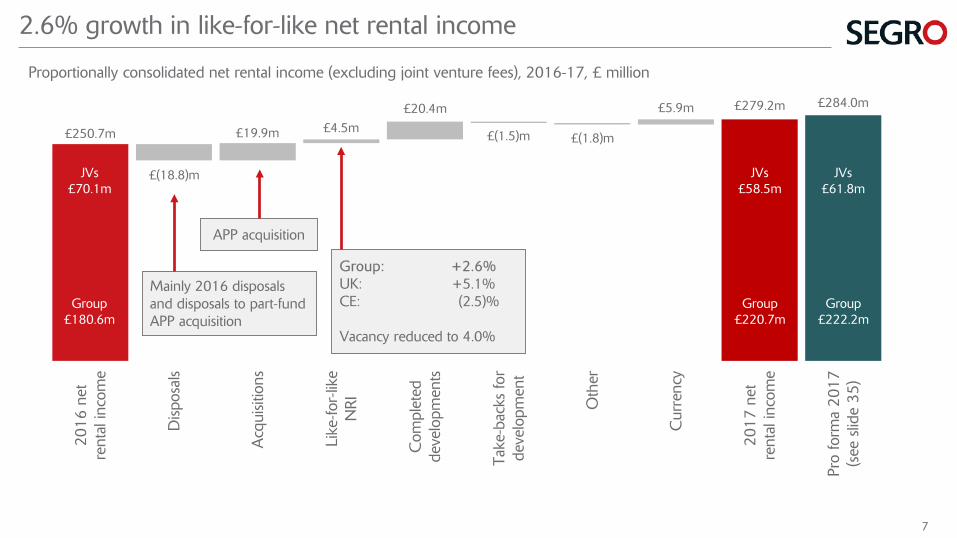

£250.7m

£279.2m

2.6% growth in like-for-like net rental income

Proportionally consolidated net rental income (excluding joint venture fees), 2016-17, £ million

Mainly 2016 disposals and disposals to part-fund APP acquisition

Group: +2.6%UK: +5.1%CE: (2.5)%

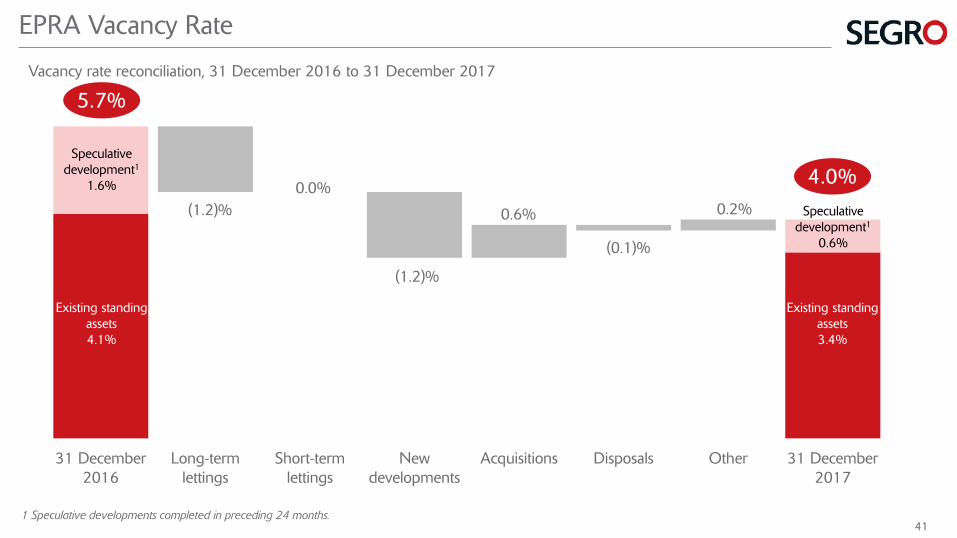

Vacancy reduced to 4.0%

APP acquisition

Group£220.7m

JVs£70.1m

Group£180.6m

JVs£58.5m

Group£222.2m

JVs£61.8m

£284.0m

7

1 Net property rental income less administrative expenses, net interest expenses and taxation

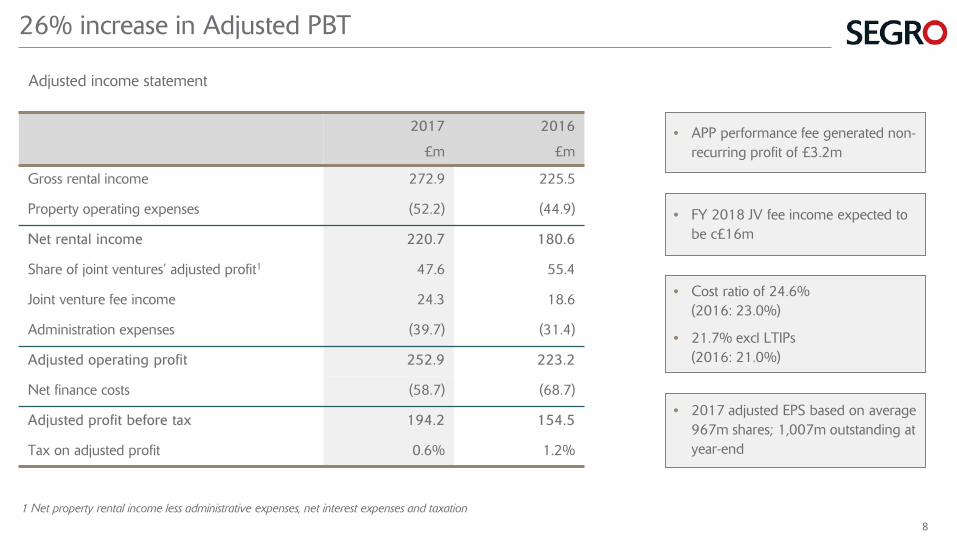

26% increase in Adjusted PBT

Adjusted income statement

2017

£m

2016

£m

Gross rental income 272.9 225.5

Property operating expenses (52.2) (44.9)

Net rental income 220.7 180.6

Share of joint ventures’ adjusted profit1 47.6 55.4

Joint venture fee income 24.3 18.6

Administration expenses (39.7) (31.4)

Adjusted operating profit 252.9 223.2

Net finance costs (58.7) (68.7)

Adjusted profit before tax 194.2 154.5

Tax on adjusted profit 0.6% 1.2%

• APP performance fee generated non-recurring profit of £3.2m

• Cost ratio of 24.6%(2016: 23.0%)

• 21.7% excl LTIPs(2016: 21.0%)

• 2017 adjusted EPS based on average 967m shares; 1,007m outstanding at year-end

• FY 2018 JV fee income expected to be c£16m

8

31 December2016

2017Adjusted EPS

Dividends Realised andunrealised gains

Net impact offinancing activity

Exchange rate andother

31 December2017

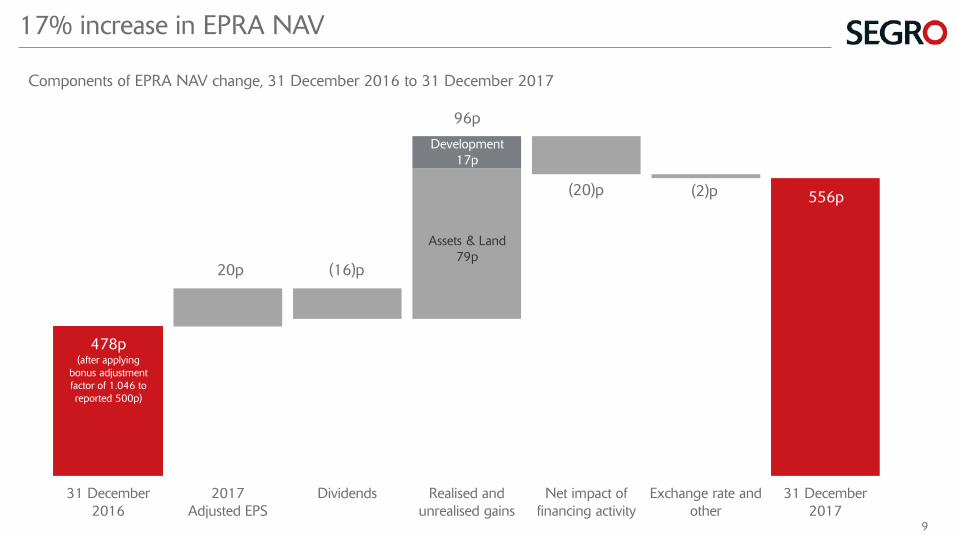

17% increase in EPRA NAV

Components of EPRA NAV change, 31 December 2016 to 31 December 2017

(16)p20p

96p

(20)p 556p

478p(after applying

bonus adjustment factor of 1.046 to reported 500p)

(2)p

Assets & Land79p

Development17p

9

£0m

£200m

£400m

£600m

£800m

£1,000m

Total London Slough Midlands BigBox

Germany France Poland Italy

+17.6%

+8.1%

+1.4% +2.9%+13.2%

+15.8%

+7.5%+10.3%

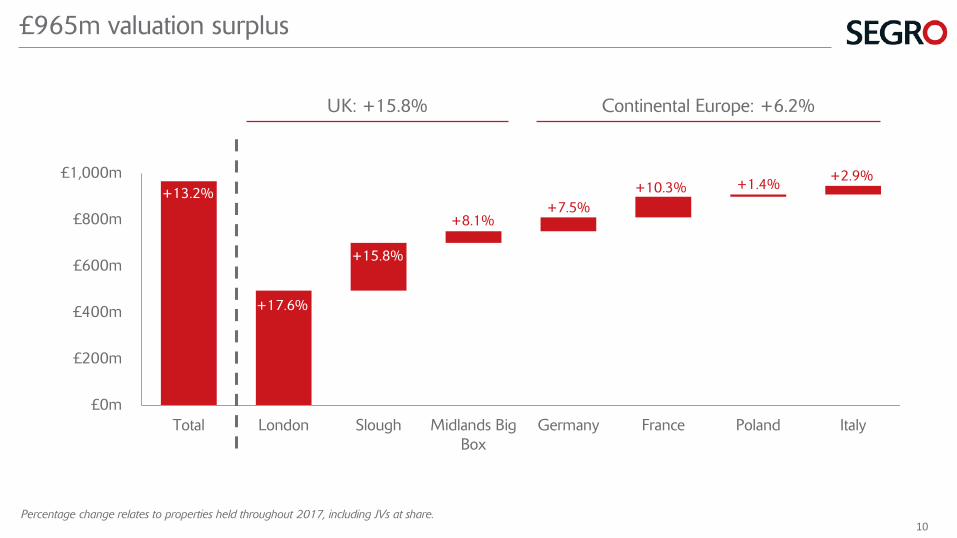

Percentage change relates to properties held throughout 2017, including JVs at share.

£965m valuation surplus

UK: +15.8% Continental Europe: +6.2%

10

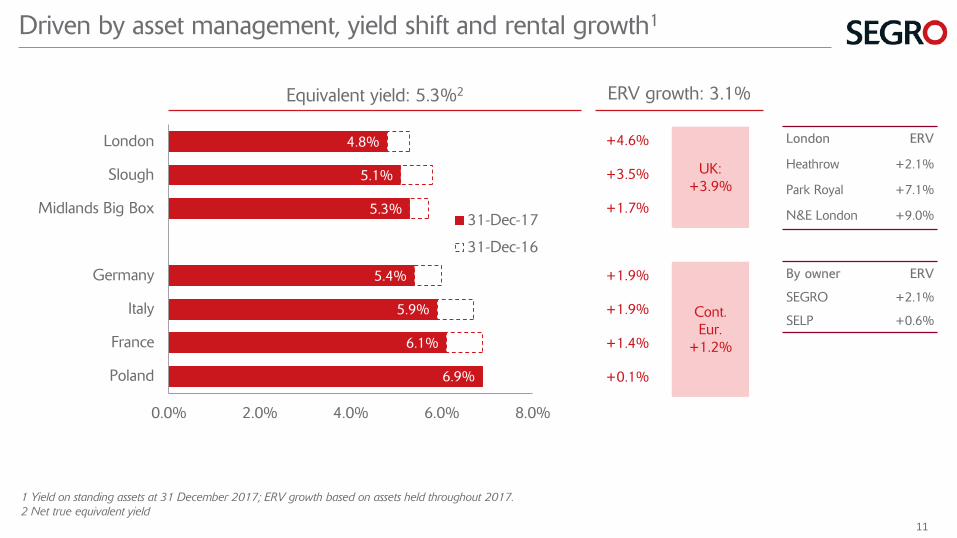

6.9%

6.1%

5.9%

5.4%

5.3%

5.1%

4.8%

0.0% 2.0% 4.0% 6.0% 8.0%

Poland

France

Italy

Germany

Midlands Big Box

Slough

London

31-Dec-17

31-Dec-16

1 Yield on standing assets at 31 December 2017; ERV growth based on assets held throughout 2017.2 Net true equivalent yield

Driven by asset management, yield shift and rental growth1

+4.6%

UK: +3.9%

+3.5%

+1.7%

+1.9%

Cont.Eur.

+1.2%

+1.9%

+1.4%

+0.1%

Equivalent yield: 5.3%2 ERV growth: 3.1%

By owner ERV

SEGRO +2.1%

SELP +0.6%

London ERV

Heathrow +2.1%

Park Royal +7.1%

N&E London +9.0%

11

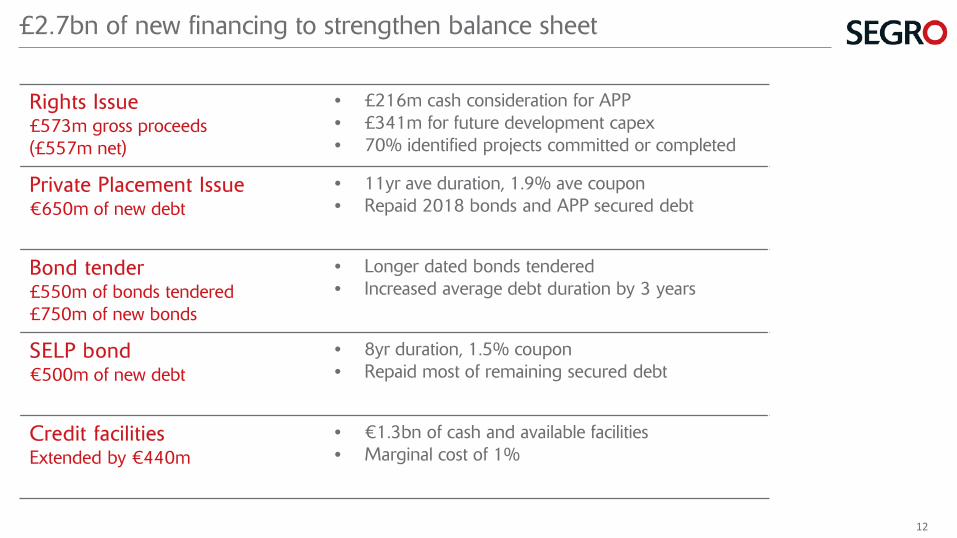

£2.7bn of new financing to strengthen balance sheet

Rights Issue£573m gross proceeds(£557m net)

• £216m cash consideration for APP• £341m for future development capex• 70% identified projects committed or completed

Private Placement Issue€650m of new debt

• 11yr ave duration, 1.9% ave coupon• Repaid 2018 bonds and APP secured debt

Bond tender£550m of bonds tendered£750m of new bonds

• Longer dated bonds tendered• Increased average debt duration by 3 years

SELP bond€500m of new debt

• 8yr duration, 1.5% coupon• Repaid most of remaining secured debt

Credit facilitiesExtended by €440m

• €1.3bn of cash and available facilities• Marginal cost of 1%

12

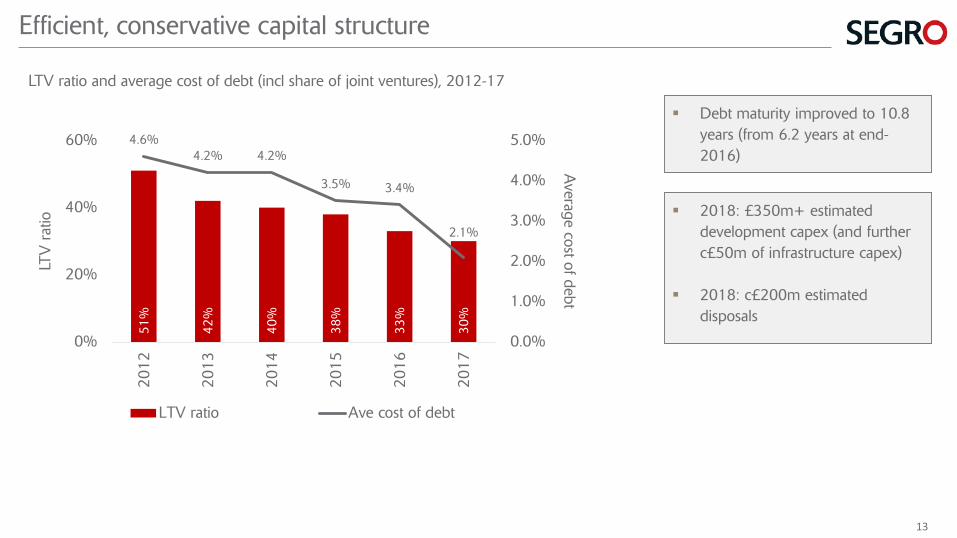

2018: £350m+ estimated development capex (and further c£50m of infrastructure capex)

2018: c£200m estimated disposals

Efficient, conservative capital structure

LTV ratio and average cost of debt (incl share of joint ventures), 2012-17

51%

42%

40%

38%

33%

30%

4.6%4.2% 4.2%

3.5% 3.4%

2.1%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

0%

20%

40%

60%20

12

2013

2014

2015

2016

2017

Average cost of debt

LTV

rat

io

LTV ratio Ave cost of debt

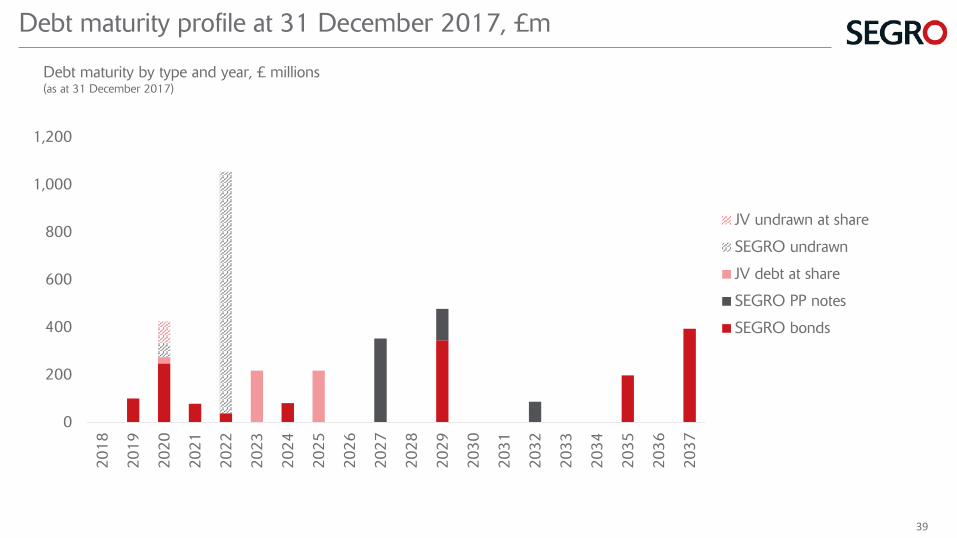

Debt maturity improved to 10.8 years (from 6.2 years at end-2016)

13

Strong financial results and balance sheet

Growing earnings

Strong balance sheet

2017 final dividend increased by 6%

BidFood, Slough Trading Estate

14

2017: Another year of delivery

Strong financial results and significantly improved capital structure

Disciplined capital allocation improving portfolio scale and quality

Operational excellence delivers strong operating and development performance

Significant growth opportunities within our control

Camden Town Brewery, Navigation Park

15

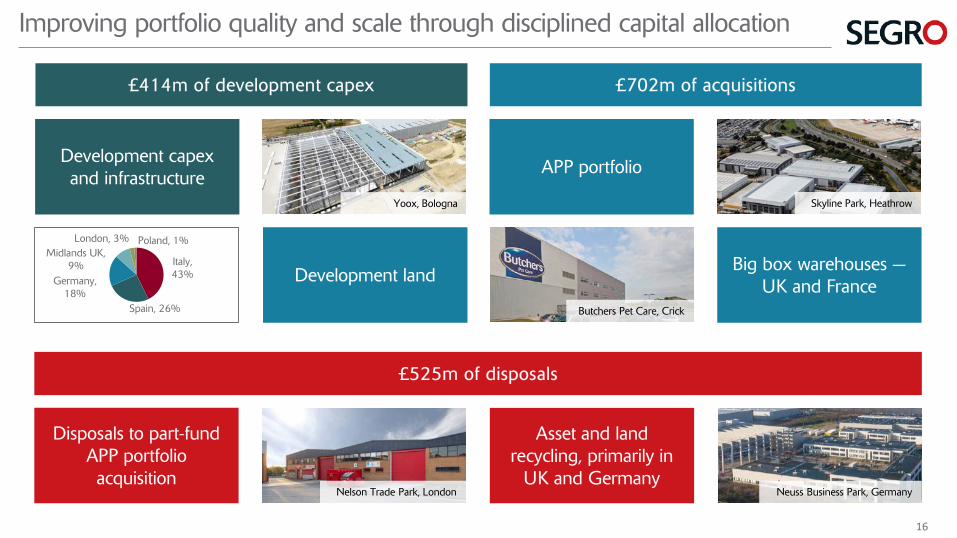

Improving portfolio quality and scale through disciplined capital allocation

£525m of disposals

£702m of acquisitions

Disposals to part-fund APP portfolio acquisition

Nelson Trade Park, London

Asset and land recycling, primarily in

UK and GermanyNeuss Business Park, Germany

APP portfolio

Skyline Park, Heathrow

Big box warehouses —UK and France

Butchers Pet Care, Crick

Development landItaly, 43%

Spain, 26%

Germany, 18%

Midlands UK, 9%

London, 3% Poland, 1%

£414m of development capex

Development capex and infrastructure

Yoox, Bologna

16

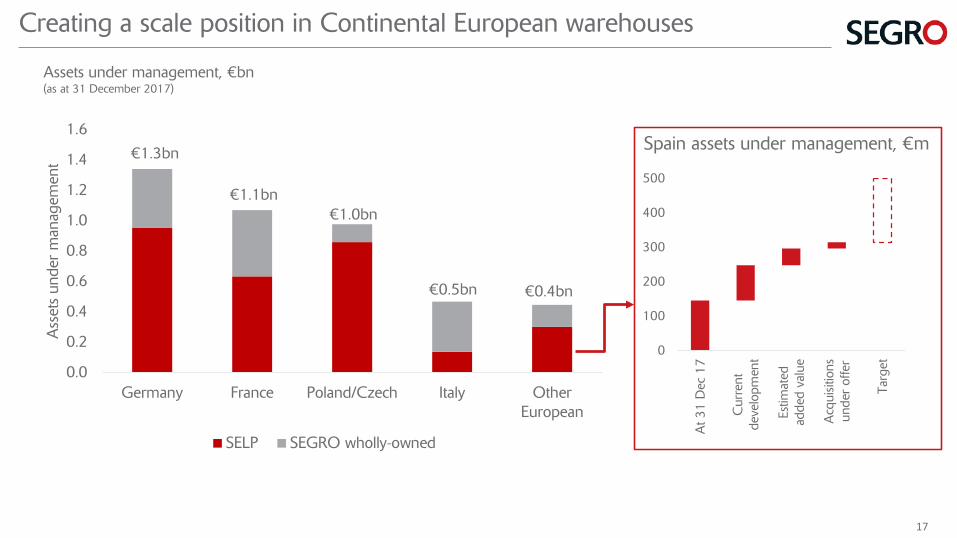

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Germany France Poland/Czech Italy OtherEuropean

Ass

ets

unde

r m

anag

emen

t

SELP SEGRO wholly-owned

€1.3bn

€1.1bn€1.0bn

€0.4bn€0.5bn

Creating a scale position in Continental European warehouses

0

100

200

300

400

500

At 3

1 D

ec 1

7

Cur

rent

deve

lopm

ent

Estim

ated

adde

d va

lue

Acq

uisit

ions

unde

r of

fer

Targ

et

Spain assets under management, €m

Assets under management, €bn(as at 31 December 2017)

17

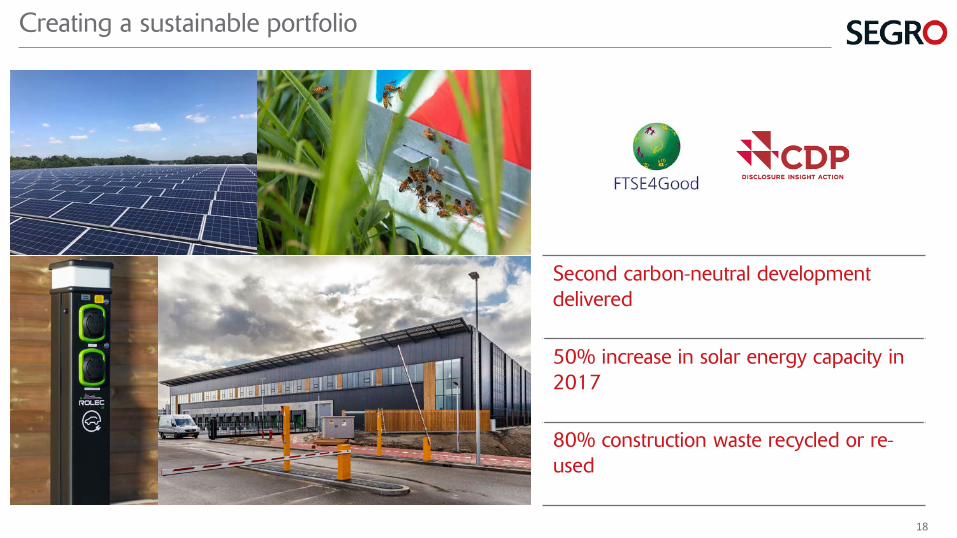

Creating a sustainable portfolio

Second carbon-neutral development delivered

50% increase in solar energy capacity in 2017

80% construction waste recycled or re-used

18

2017: Another year of delivery

Strong financial results and significantly improved capital structure

Disciplined capital allocation improving portfolio scale and quality

Operational excellence delivers strong operating and development performance

Significant growth opportunities within our control

XPO Logistics, SEGRO Logistics Park Bondouffle

19

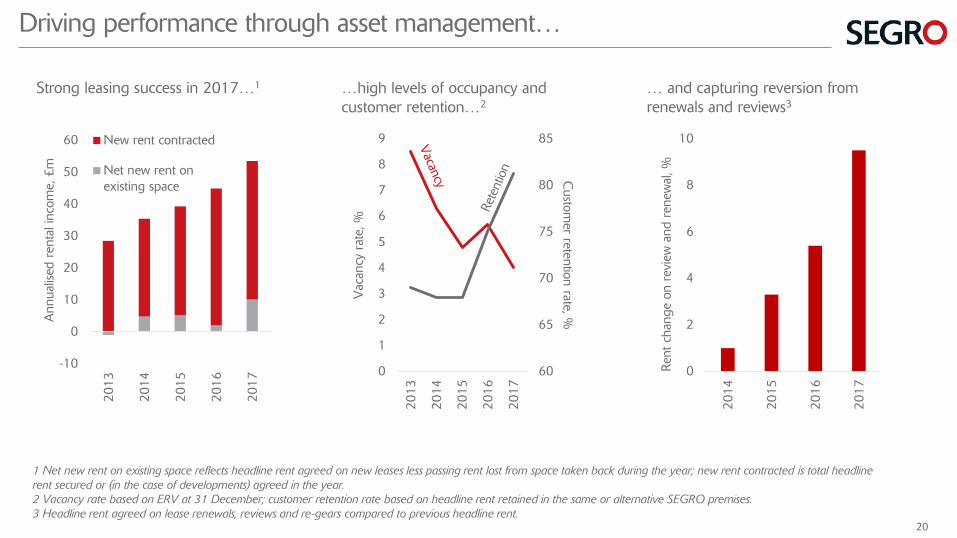

Driving performance through asset management…

-10

0

10

20

30

40

50

60

2013

2014

2015

2016

2017

Ann

ualis

ed r

enta

l inc

ome,

£m

New rent contracted

Net new rent onexisting space

60

65

70

75

80

85

0

1

2

3

4

5

6

7

8

9

2013

2014

2015

2016

2017

Custom

er retention rate, %

Vac

ancy

rat

e, %

0

2

4

6

8

10

2014

2015

2016

2017

Rent

cha

nge

on r

evie

w a

nd r

enew

al, %

Strong leasing success in 2017…1 …high levels of occupancy and customer retention…2

… and capturing reversion from renewals and reviews3

1 Net new rent on existing space reflects headline rent agreed on new leases less passing rent lost from space taken back during the year; new rent contracted is total headline rent secured or (in the case of developments) agreed in the year.2 Vacancy rate based on ERV at 31 December; customer retention rate based on headline rent retained in the same or alternative SEGRO premises.3 Headline rent agreed on lease renewals, reviews and re-gears compared to previous headline rent.

20

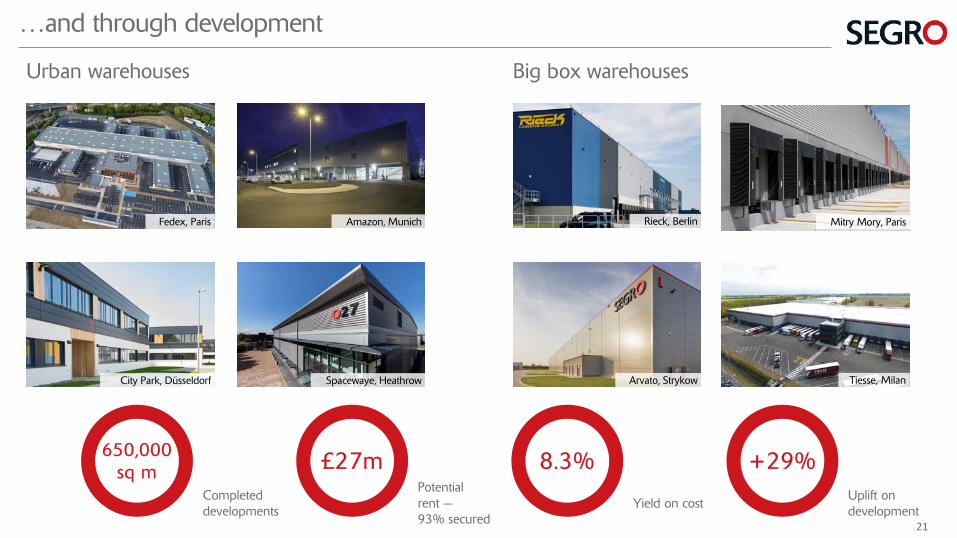

Big box warehousesUrban warehouses

…and through development

Mitry Mory, ParisFedex, Paris Amazon, Munich

City Park, Düsseldorf

Rieck, Berlin

Arvato, Strykow Tiesse, MilanSpacewaye, Heathrow

650,000sq m

Completed developments

£27mPotential rent —93% secured

8.3%

Yield on cost

+29%Uplift on development

21

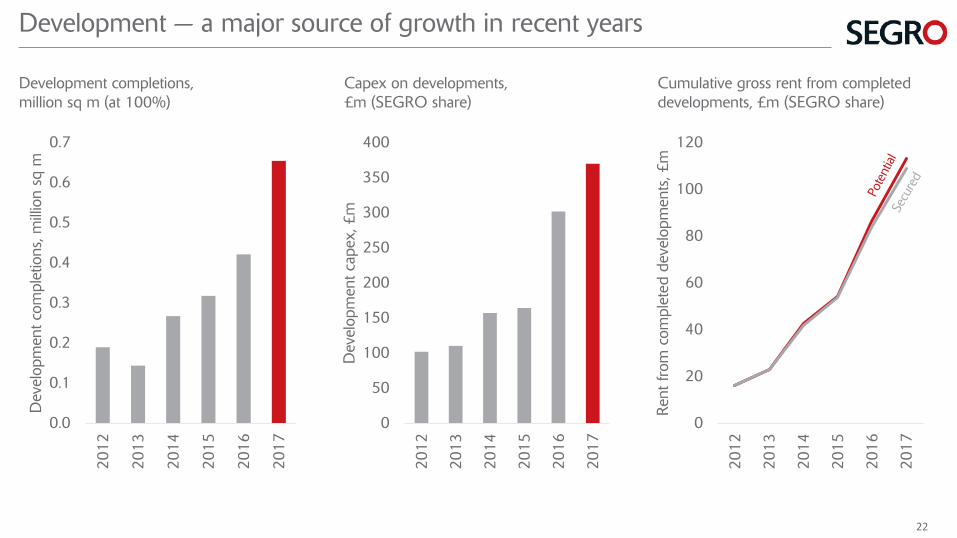

0

50

100

150

200

250

300

350

400

2012

2013

2014

2015

2016

2017

Dev

elop

men

t cap

ex, £

m

Development — a major source of growth in recent years

Development completions, million sq m (at 100%)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

2012

2013

2014

2015

2016

2017

Dev

elop

men

t com

plet

ions

, mill

ion

sq m

0

20

40

60

80

100

120

2012

2013

2014

2015

2016

2017

Rent

from

com

plet

ed d

evel

opm

ents

, £m

Capex on developments, £m (SEGRO share)

Cumulative gross rent from completed developments, £m (SEGRO share)

22

2017: Another year of delivery

Strong financial results and significantly improved capital structure

Disciplined capital allocation improving portfolio scale and quality

Operational excellence delivers strong operating and development performance

Significant growth opportunities within our control

SEGRO Business Park Zeran, Warsaw

23

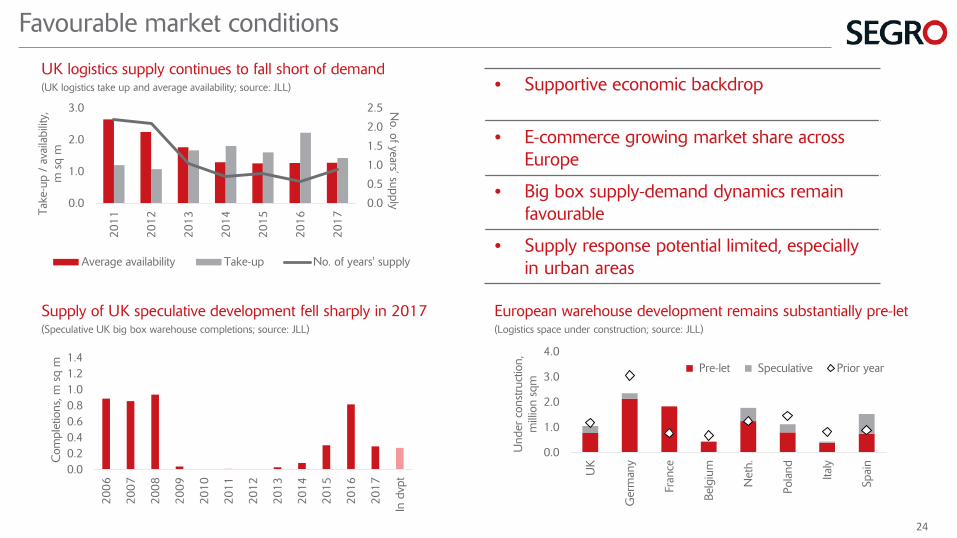

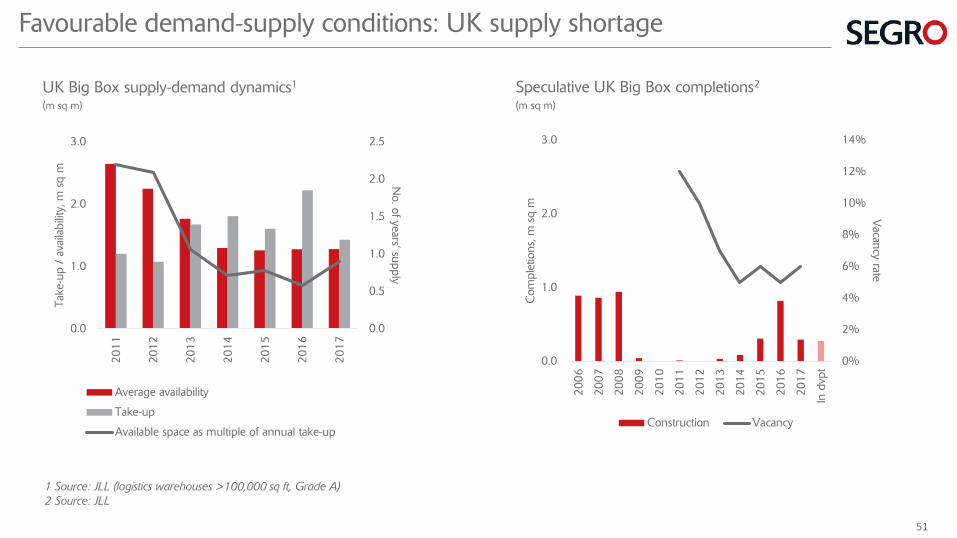

UK logistics supply continues to fall short of demand(UK logistics take up and average availability; source: JLL)

Favourable market conditions

Supply of UK speculative development fell sharply in 2017(Speculative UK big box warehouse completions; source: JLL)

0.00.20.40.60.81.01.21.4

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

In d

vpt

Com

plet

ions

, m s

q m

0.0

0.5

1.0

1.5

2.0

2.5

0.0

1.0

2.0

3.020

11

2012

2013

2014

2015

2016

2017

No. of years’ supply

Take

-up

/ av

aila

bilit

y,m

sq

m

Average availability Take-up No. of years' supply

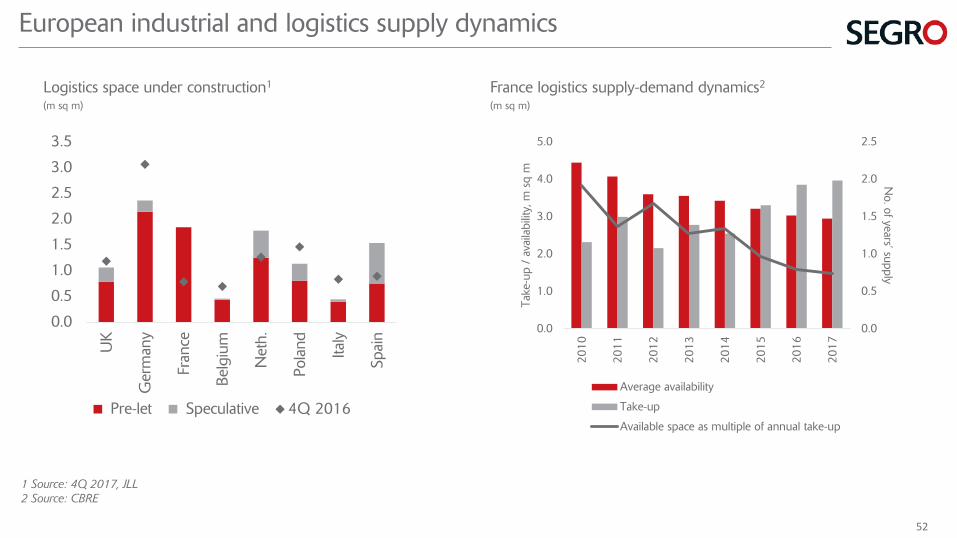

European warehouse development remains substantially pre-let(Logistics space under construction; source: JLL)

• Supportive economic backdrop

• E-commerce growing market share across Europe

• Big box supply-demand dynamics remain favourable

• Supply response potential limited, especially in urban areas

0.0

1.0

2.0

3.0

4.0

UK

Ger

man

y

Fran

ce

Belg

ium

Net

h.

Pola

nd Italy

Spai

n

Und

er c

onst

ruct

ion,

m

illio

n sq

m

Pre-let Speculative Prior year

24

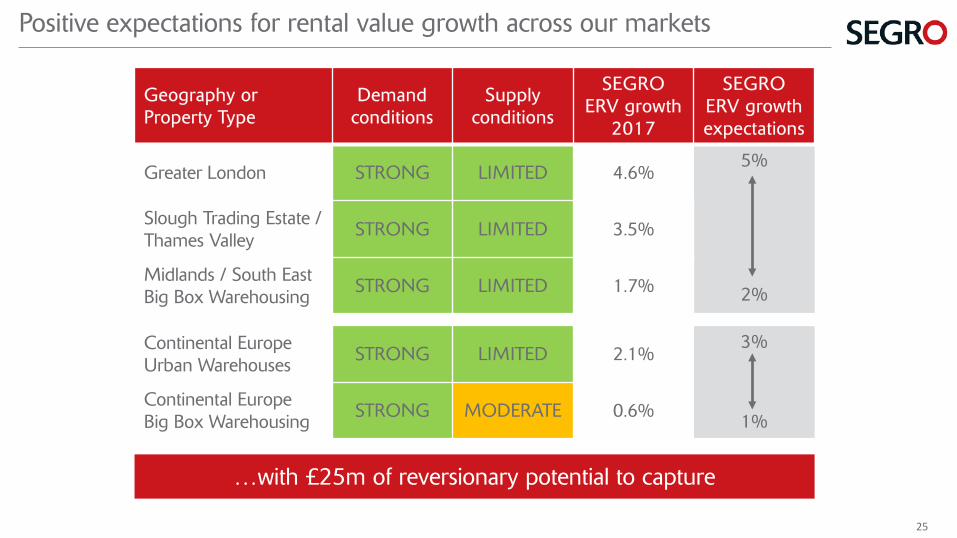

Geography or Property Type

Demand conditions

Supply conditions

SEGROERV growth

2017

SEGROERV growth expectations

Greater London STRONG LIMITED 4.6%5%

2%

Slough Trading Estate / Thames Valley STRONG LIMITED 3.5%

Midlands / South East Big Box Warehousing STRONG LIMITED 1.7%

Continental Europe Urban Warehouses STRONG LIMITED 2.1%

3%

1%Continental Europe Big Box Warehousing STRONG MODERATE 0.6%

Positive expectations for rental value growth across our markets

…with £25m of reversionary potential to capture

25

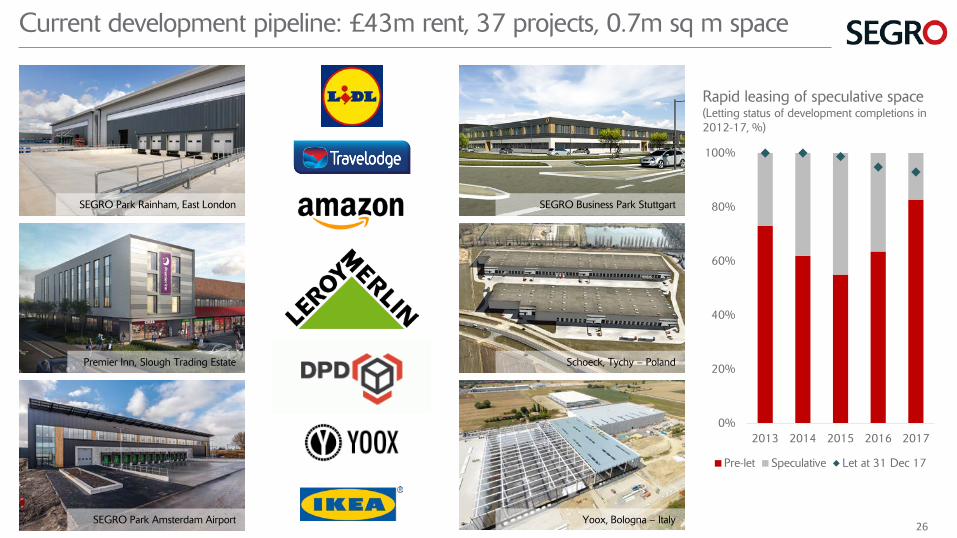

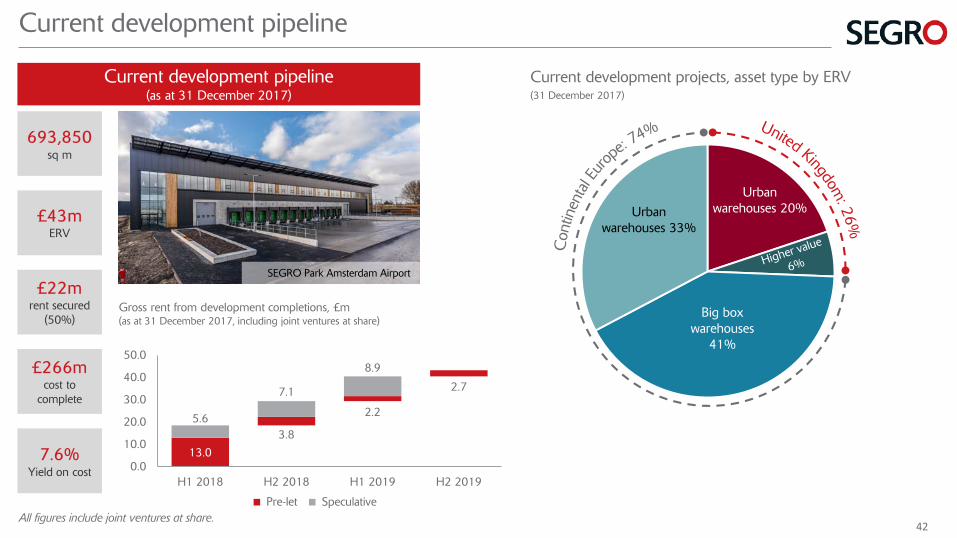

Current development pipeline: £43m rent, 37 projects, 0.7m sq m space

Premier Inn, Slough Trading Estate

SEGRO Park Rainham, East London

SEGRO Park Amsterdam Airport

SEGRO Business Park Stuttgart

Schoeck, Tychy – Poland

Yoox, Bologna – Italy

0%

20%

40%

60%

80%

100%

2013 2014 2015 2016 2017

Pre-let Speculative Let at 31 Dec 17

Rapid leasing of speculative space(Letting status of development completions in 2012-17, %)

26

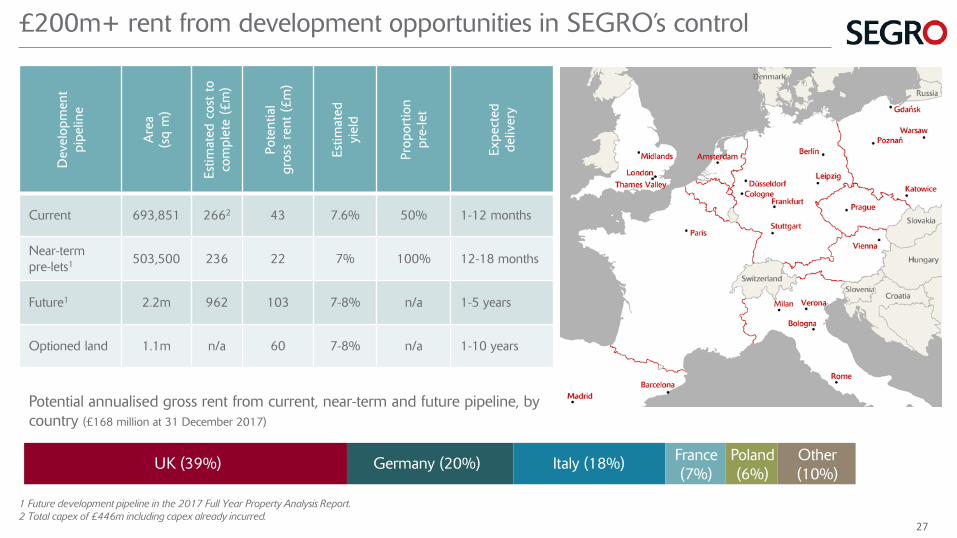

£200m+ rent from development opportunities in SEGRO’s control

1 Future development pipeline in the 2017 Full Year Property Analysis Report.2 Total capex of £446m including capex already incurred.

Dev

elop

men

t pi

pelin

e

Are

a (s

q m

)

Estim

ated

cos

t to

co

mpl

ete

(£m

)

Pote

ntia

l gr

oss

rent

(£m

)

Estim

ated

yi

eld

Prop

ortio

n

pre-

let

Expe

cted

de

liver

y

Current 693,851 2662 43 7.6% 50% 1-12 months

Near-termpre-lets1 503,500 236 22 7% 100% 12-18 months

Future1 2.2m 962 103 7-8% n/a 1-5 years

Optioned land 1.1m n/a 60 7-8% n/a 1-10 years

UK (39%) Germany (20%) Italy (18%) France(7%)

Poland(6%)

Potential annualised gross rent from current, near-term and future pipeline, by country (£168 million at 31 December 2017)

Other(10%)

27

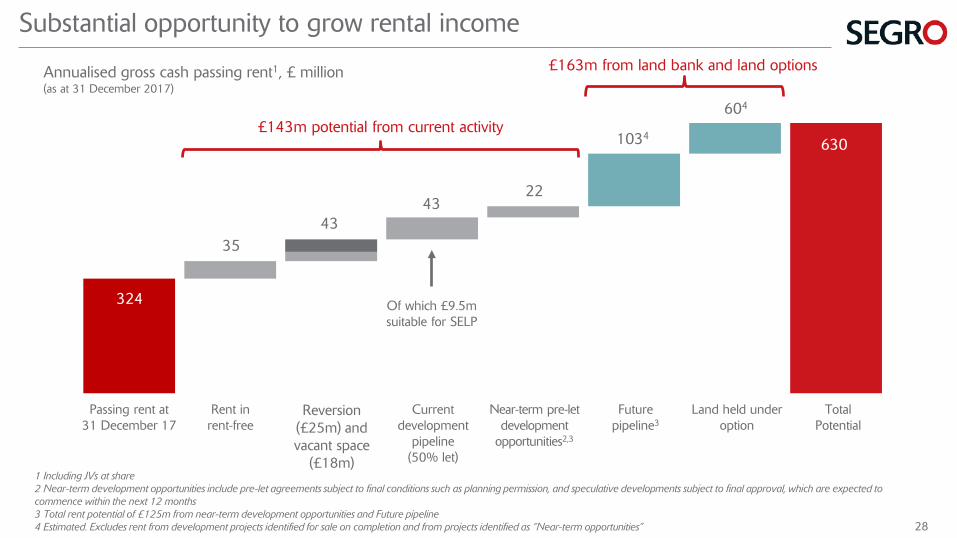

324

35

4322

384

388.8

Annualised gross cash passing rent1, £ million(as at 31 December 2017)

1 Including JVs at share2 Near-term development opportunities include pre-let agreements subject to final conditions such as planning permission, and speculative developments subject to final approval, which are expected to commence within the next 12 months3 Total rent potential of £125m from near-term development opportunities and Future pipeline 4 Estimated. Excludes rent from development projects identified for sale on completion and from projects identified as “Near-term opportunities”

43

Passing rent at31 December 17

Rent in rent-free

Reversion (£25m) and vacant space

(£18m)

Current development

pipeline(50% let)

Near-term pre-letdevelopment

opportunities2,3

Futurepipeline3

Land held under option

TotalPotential

Substantial opportunity to grow rental income

1034

604

£143m potential from current activity

£163m from land bank and land options

630

Of which £9.5m suitable for SELP

28

Strong momentum going into 2018

Supportive market with structural drivers

Further rental income growth potential

Profitable development pipeline

Strong balance sheet

SEGRO Logistics Park Ingolstadt

29

2017 FULL YEAR RESULTS

Q&A

APPENDIX IPORTFOLIO AND FINANCIAL DATA

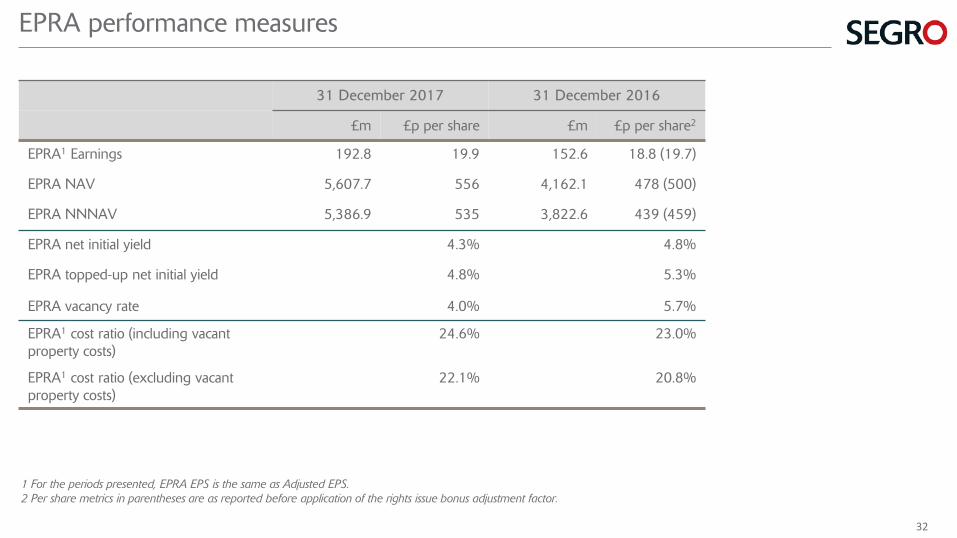

31 December 2017 31 December 2016

£m £p per share £m £p per share2

EPRA1 Earnings 192.8 19.9 152.6 18.8 (19.7)

EPRA NAV 5,607.7 556 4,162.1 478 (500)

EPRA NNNAV 5,386.9 535 3,822.6 439 (459)

EPRA net initial yield 4.3% 4.8%

EPRA topped-up net initial yield 4.8% 5.3%

EPRA vacancy rate 4.0% 5.7%

EPRA1 cost ratio (including vacant property costs)

24.6% 23.0%

EPRA1 cost ratio (excluding vacant property costs)

22.1% 20.8%

1 For the periods presented, EPRA EPS is the same as Adjusted EPS.2 Per share metrics in parentheses are as reported before application of the rights issue bonus adjustment factor.

EPRA performance measures

32

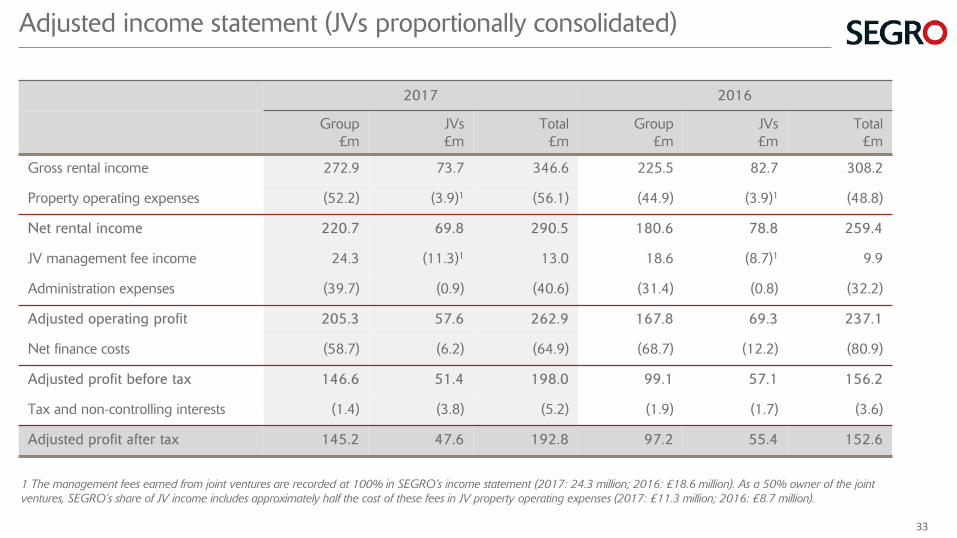

2017 2016

Group£m

JVs£m

Total£m

Group£m

JVs£m

Total£m

Gross rental income 272.9 73.7 346.6 225.5 82.7 308.2

Property operating expenses (52.2) (3.9)1 (56.1) (44.9) (3.9)1 (48.8)

Net rental income 220.7 69.8 290.5 180.6 78.8 259.4

JV management fee income 24.3 (11.3)1 13.0 18.6 (8.7)1 9.9

Administration expenses (39.7) (0.9) (40.6) (31.4) (0.8) (32.2)

Adjusted operating profit 205.3 57.6 262.9 167.8 69.3 237.1

Net finance costs (58.7) (6.2) (64.9) (68.7) (12.2) (80.9)

Adjusted profit before tax 146.6 51.4 198.0 99.1 57.1 156.2

Tax and non-controlling interests (1.4) (3.8) (5.2) (1.9) (1.7) (3.6)

Adjusted profit after tax 145.2 47.6 192.8 97.2 55.4 152.6

Adjusted income statement (JVs proportionally consolidated)

1 The management fees earned from joint ventures are recorded at 100% in SEGRO’s income statement (2017: 24.3 million; 2016: £18.6 million). As a 50% owner of the joint ventures, SEGRO’s share of JV income includes approximately half the cost of these fees in JV property operating expenses (2017: £11.3 million; 2016: £8.7 million).

33

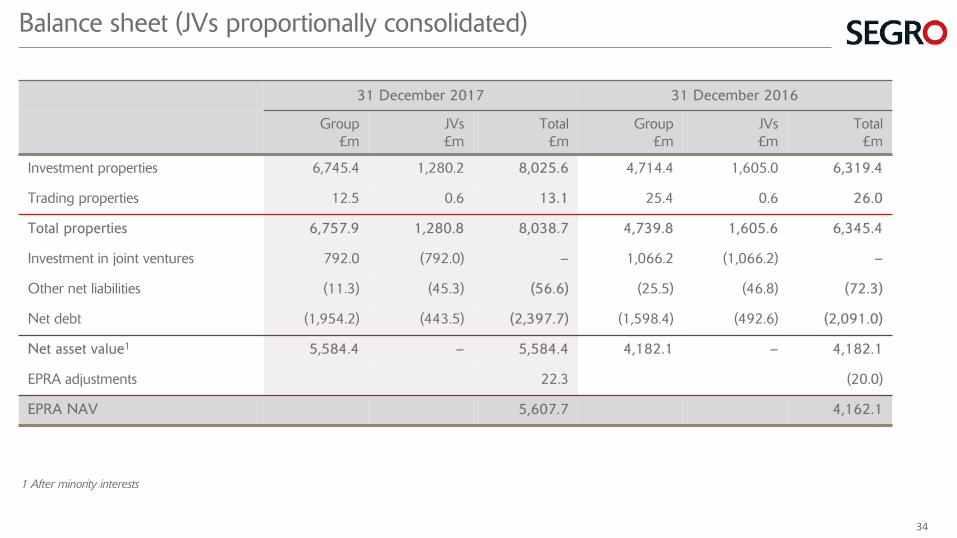

31 December 2017 31 December 2016

Group£m

JVs£m

Total£m

Group£m

JVs£m

Total£m

Investment properties 6,745.4 1,280.2 8,025.6 4,714.4 1,605.0 6,319.4

Trading properties 12.5 0.6 13.1 25.4 0.6 26.0

Total properties 6,757.9 1,280.8 8,038.7 4,739.8 1,605.6 6,345.4

Investment in joint ventures 792.0 (792.0) – 1,066.2 (1,066.2) –

Other net liabilities (11.3) (45.3) (56.6) (25.5) (46.8) (72.3)

Net debt (1,954.2) (443.5) (2,397.7) (1,598.4) (492.6) (2,091.0)

Net asset value1 5,584.4 – 5,584.4 4,182.1 – 4,182.1

EPRA adjustments 22.3 (20.0)

EPRA NAV 5,607.7 4,162.1

1 After minority interests

Balance sheet (JVs proportionally consolidated)

34

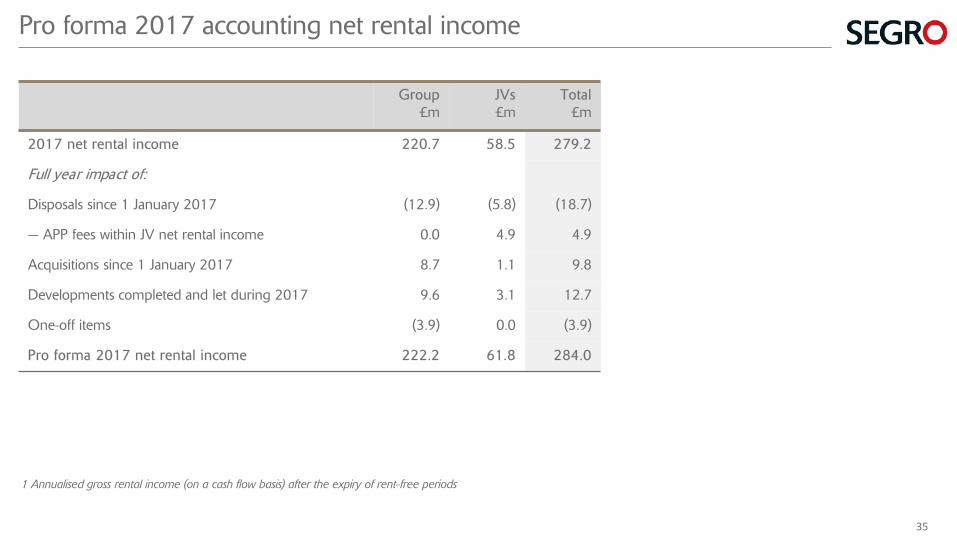

1 Annualised gross rental income (on a cash flow basis) after the expiry of rent-free periods

Group£m

JVs£m

Total£m

2017 net rental income 220.7 58.5 279.2

Full year impact of:

Disposals since 1 January 2017 (12.9) (5.8) (18.7)

— APP fees within JV net rental income 0.0 4.9 4.9

Acquisitions since 1 January 2017 8.7 1.1 9.8

Developments completed and let during 2017 9.6 3.1 12.7

One-off items (3.9) 0.0 (3.9)

Pro forma 2017 net rental income 222.2 61.8 284.0

Pro forma 2017 accounting net rental income

35

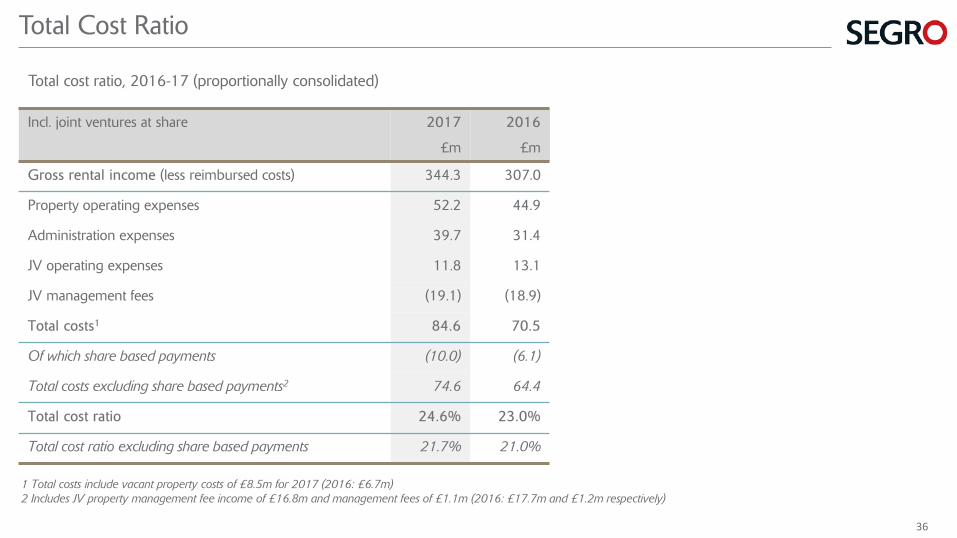

1 Total costs include vacant property costs of £8.5m for 2017 (2016: £6.7m)2 Includes JV property management fee income of £16.8m and management fees of £1.1m (2016: £17.7m and £1.2m respectively)

Incl. joint ventures at share 2017

£m

2016

£m

Gross rental income (less reimbursed costs) 344.3 307.0

Property operating expenses 52.2 44.9

Administration expenses 39.7 31.4

JV operating expenses 11.8 13.1

JV management fees (19.1) (18.9)

Total costs1 84.6 70.5

Of which share based payments (10.0) (6.1)

Total costs excluding share based payments2 74.6 64.4

Total cost ratio 24.6% 23.0%

Total cost ratio excluding share based payments 21.7% 21.0%

Total Cost Ratio

Total cost ratio, 2016-17 (proportionally consolidated)

36

2017 2016

Group£m

JVs£m

Total£m

Group£m

JVs£m

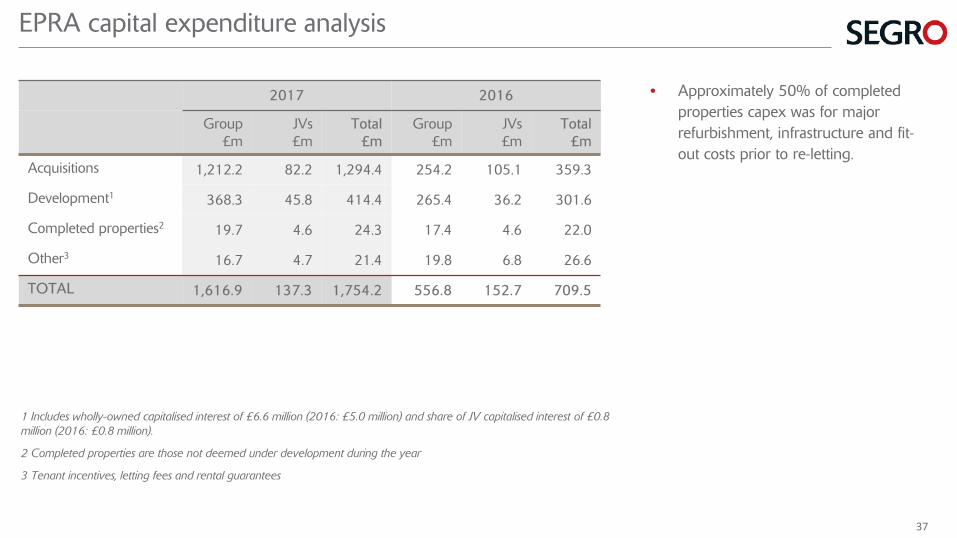

Total£m

Acquisitions 1,212.2 82.2 1,294.4 254.2 105.1 359.3

Development1 368.3 45.8 414.4 265.4 36.2 301.6

Completed properties2 19.7 4.6 24.3 17.4 4.6 22.0

Other3 16.7 4.7 21.4 19.8 6.8 26.6

TOTAL 1,616.9 137.3 1,754.2 556.8 152.7 709.5

1 Includes wholly-owned capitalised interest of £6.6 million (2016: £5.0 million) and share of JV capitalised interest of £0.8 million (2016: £0.8 million).

2 Completed properties are those not deemed under development during the year

3 Tenant incentives, letting fees and rental guarantees

• Approximately 50% of completed properties capex was for major refurbishment, infrastructure and fit-out costs prior to re-letting.

EPRA capital expenditure analysis

37

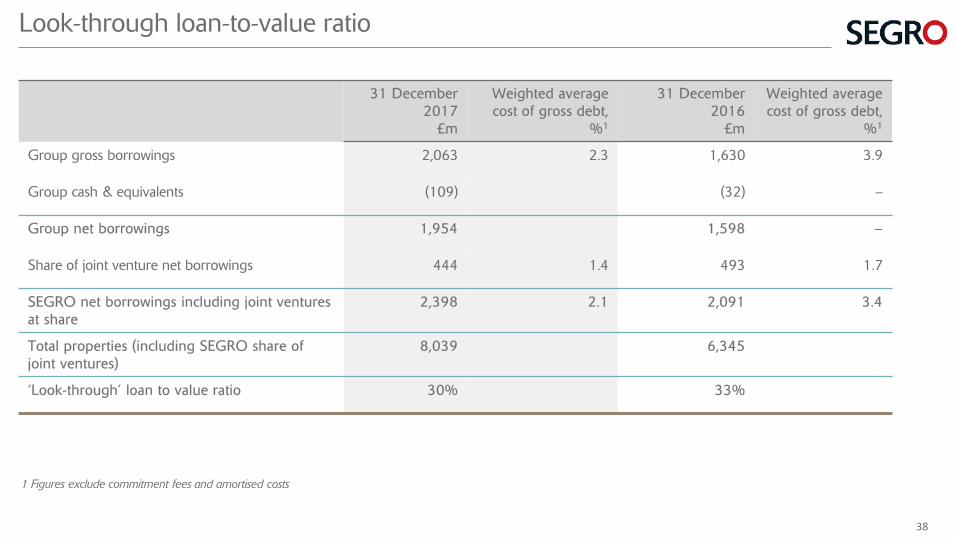

31 December 2017

£m

Weighted average cost of gross debt,

%1

31 December 2016

£m

Weighted average cost of gross debt,

%1

Group gross borrowings 2,063 2.3 1,630 3.9

Group cash & equivalents (109) (32) –

Group net borrowings 1,954 1,598 –

Share of joint venture net borrowings 444 1.4 493 1.7

SEGRO net borrowings including joint ventures at share

2,398 2.1 2,091 3.4

Total properties (including SEGRO share of joint ventures)

8,039 6,345

‘Look-through’ loan to value ratio 30% 33%

1 Figures exclude commitment fees and amortised costs

Look-through loan-to-value ratio

38

Debt maturity profile at 31 December 2017, £m

0

200

400

600

800

1,000

1,200

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

JV undrawn at share

SEGRO undrawn

JV debt at share

SEGRO PP notes

SEGRO bonds

Debt maturity by type and year, £ millions(as at 31 December 2017)

39

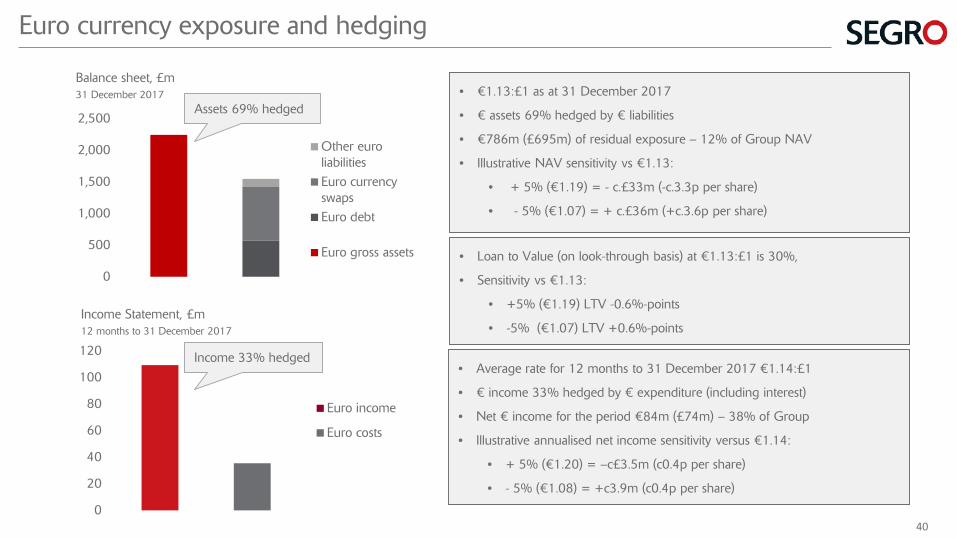

• €1.13:£1 as at 31 December 2017

• € assets 69% hedged by € liabilities

• €786m (£695m) of residual exposure – 12% of Group NAV

• Illustrative NAV sensitivity vs €1.13:

• + 5% (€1.19) = - c.£33m (-c.3.3p per share)

• - 5% (€1.07) = + c.£36m (+c.3.6p per share)

• Loan to Value (on look-through basis) at €1.13:£1 is 30%,

• Sensitivity vs €1.13:

• +5% (€1.19) LTV -0.6%-points

• -5% (€1.07) LTV +0.6%-points

• Average rate for 12 months to 31 December 2017 €1.14:£1

• € income 33% hedged by € expenditure (including interest)

• Net € income for the period €84m (£74m) – 38% of Group

• Illustrative annualised net income sensitivity versus €1.14:

• + 5% (€1.20) = –c£3.5m (c0.4p per share)

• - 5% (€1.08) = +c3.9m (c0.4p per share)

0

500

1,000

1,500

2,000

2,500

Other euroliabilitiesEuro currencyswapsEuro debt

Euro gross assets

0

20

40

60

80

100

120

Euro income

Euro costs

Balance sheet, £m31 December 2017

Income Statement, £m12 months to 31 December 2017

Assets 69% hedged

Income 33% hedged

Euro currency exposure and hedging

40

31 December2016

Long-termlettings

Short-termlettings

Newdevelopments

Acquisitions Disposals Other 31 December2017

Speculative development1

0.6%

Speculative development1

1.6%

0.6%

(1.2)%

5.7%

0.2%0.0%

1 Speculative developments completed in preceding 24 months.

Existing standing assets4.1%

Existing standing assets3.4%

(1.2)%

4.0%

EPRA Vacancy Rate

(0.1)%

Vacancy rate reconciliation, 31 December 2016 to 31 December 2017

41

Current development pipeline

Current development pipeline(as at 31 December 2017)

693,850sq m

£43m ERV

£22mrent secured

(50%)

£266m cost to

complete

7.6%Yield on cost

Current development projects, asset type by ERV(31 December 2017)

Urbanwarehouses 20%

Big box warehouses

41%

Urbanwarehouses 33%

Gross rent from development completions, £m(as at 31 December 2017, including joint ventures at share)

13.03.8

2.2

2.7

5.6

7.1

8.9

0.0

10.0

20.0

30.0

40.0

50.0

H1 2018 H2 2018 H1 2019 H2 2019

Pre-let SpeculativeAll figures include joint ventures at share.

SEGRO Park Amsterdam Airport

42

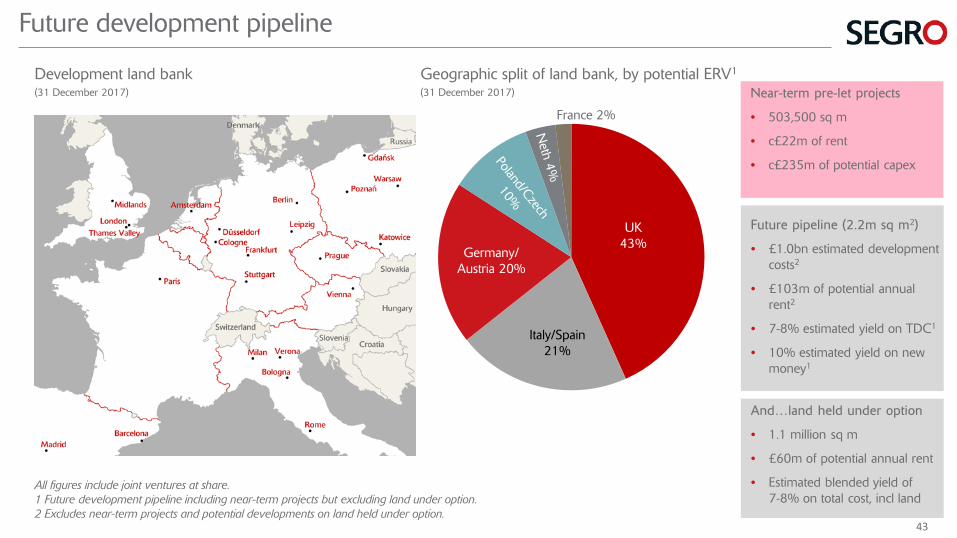

All figures include joint ventures at share.1 Future development pipeline including near-term projects but excluding land under option.2 Excludes near-term projects and potential developments on land held under option.

Germany/Austria 20%

UK43%

Italy/Spain21%

France 2%

Geographic split of land bank, by potential ERV1

(31 December 2017)

Development land bank(31 December 2017)

Future pipeline (2.2m sq m2)

• £1.0bn estimated development costs2

• £103m of potential annual rent2

• 7-8% estimated yield on TDC1

• 10% estimated yield on new money1

Future development pipeline

And…land held under option

• 1.1 million sq m

• £60m of potential annual rent

• Estimated blended yield of 7-8% on total cost, incl land

Near-term pre-let projects

• 503,500 sq m

• c£22m of rent

• c£235m of potential capex

43

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

0

100

200

300

400

500

600

2011

2012

2013

2014

2015

2016

2017

Land

ban

k va

lue,

£m

Alternative use

Future development pipeline

Long-term and residual land bank

As % of portfolio (right hand scale)

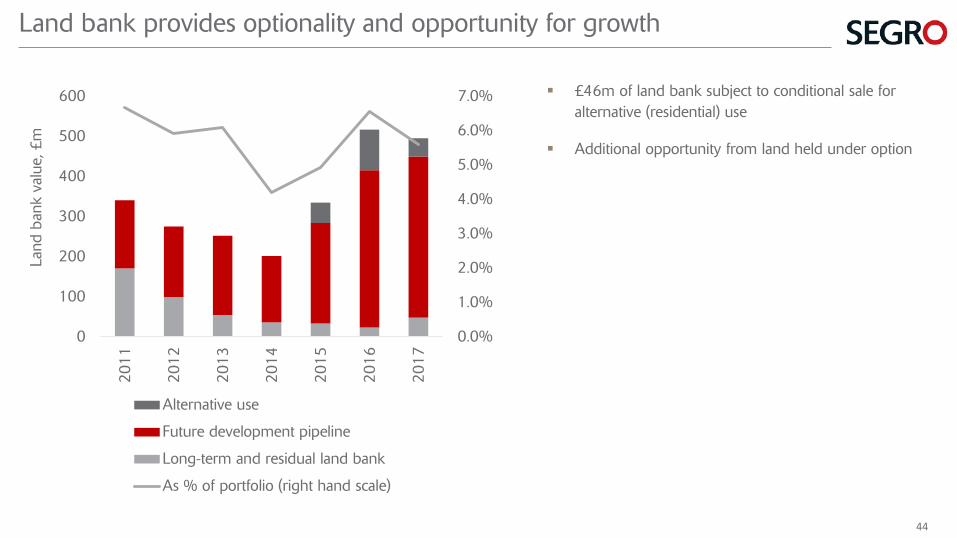

£46m of land bank subject to conditional sale for alternative (residential) use

Additional opportunity from land held under option

Land bank provides optionality and opportunity for growth

44

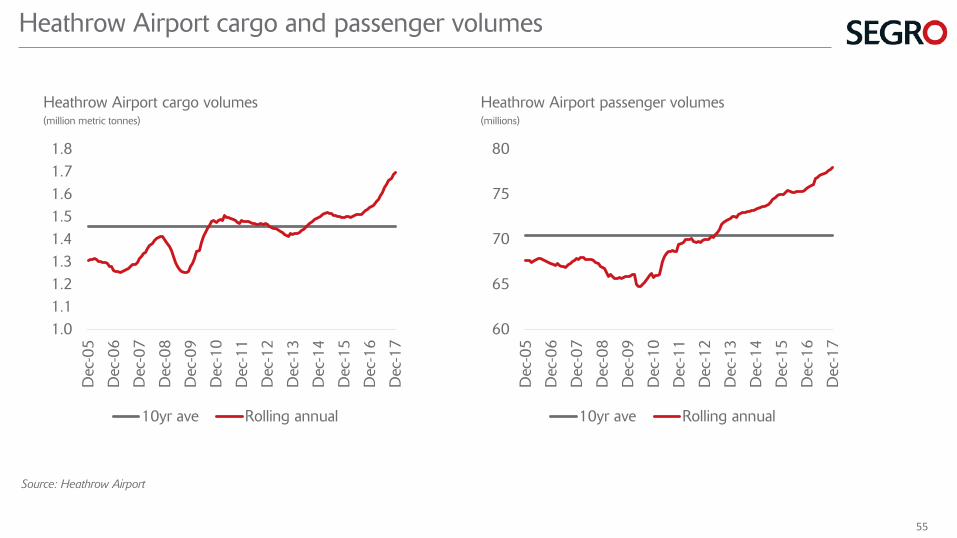

Heathrow Cargo Area

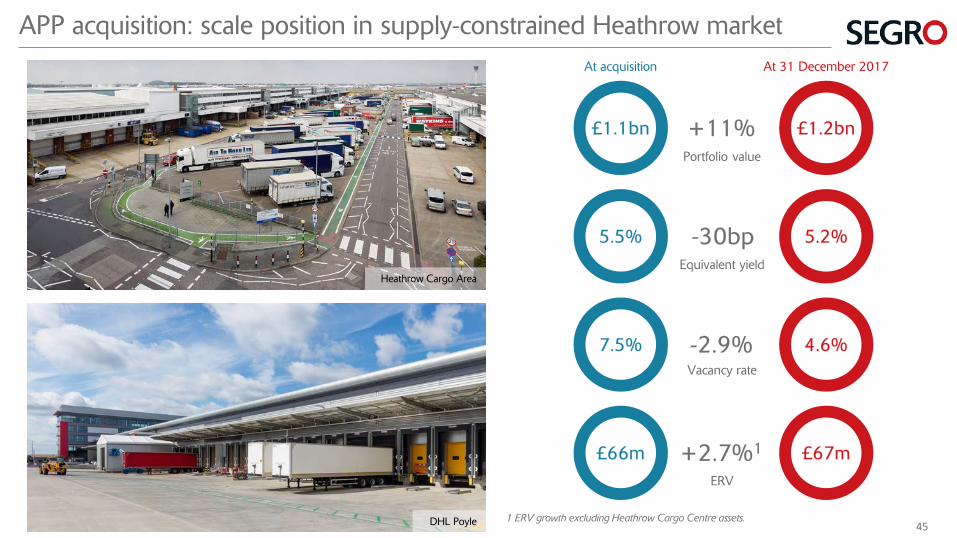

APP acquisition: scale position in supply-constrained Heathrow market

1 ERV growth excluding Heathrow Cargo Centre assets.

£1.1bnPortfolio value

£1.2bn+11%

5.5%Equivalent yield

5.2%-30bp

7.5%Vacancy rate

4.6%-2.9%

£66mERV

£67m+2.7%1

At acquisition At 31 December 2017

DHL Poyle 45

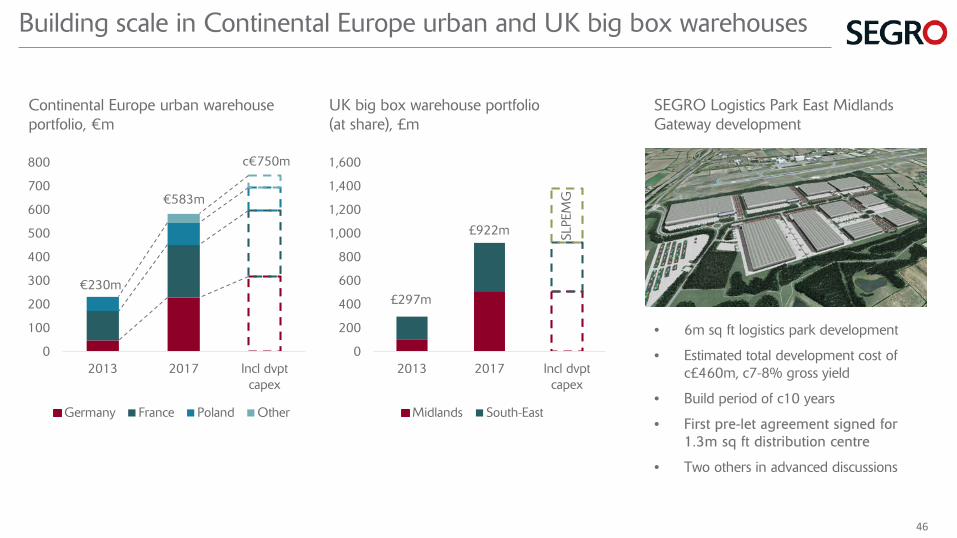

Building scale in Continental Europe urban and UK big box warehouses

• 6m sq ft logistics park development

• Estimated total development cost of c£460m, c7-8% gross yield

• Build period of c10 years

• First pre-let agreement signed for 1.3m sq ft distribution centre

• Two others in advanced discussions

0

100

200

300

400

500

600

700

800

2013 2017 Incl dvptcapex

Germany France Poland Other

€230m

€583m

c€750m

Continental Europe urban warehouse portfolio, €m

0

200

400

600

800

1,000

1,200

1,400

1,600

2013 2017 Incl dvptcapex

Midlands South-East

£297m

£922m SLPE

MG

UK big box warehouse portfolio(at share), £m

SEGRO Logistics Park East Midlands Gateway development

46

APPENDIX IIMARKET DATA

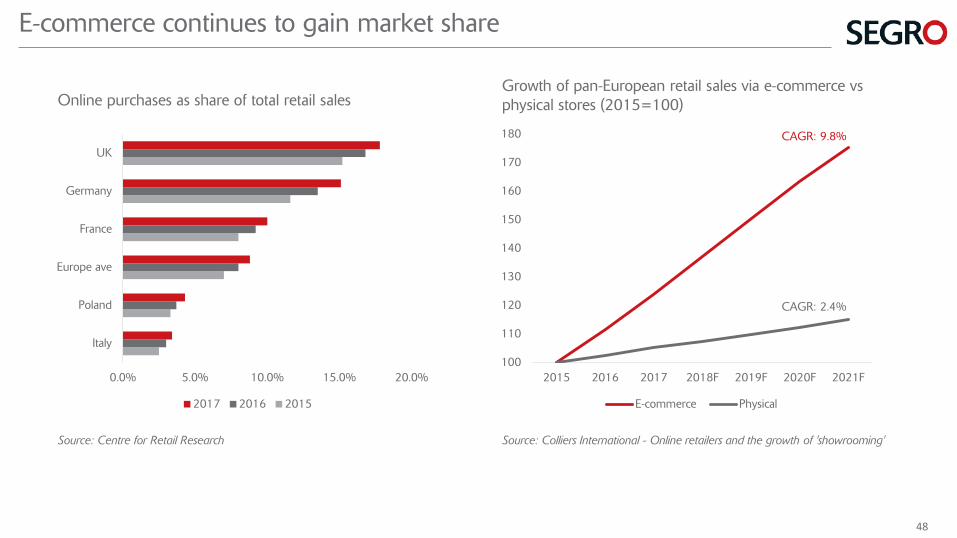

E-commerce continues to gain market share

0.0% 5.0% 10.0% 15.0% 20.0%

Italy

Poland

Europe ave

France

Germany

UK

2017 2016 2015

Online purchases as share of total retail sales

Source: Centre for Retail Research

100

110

120

130

140

150

160

170

180

2015 2016 2017 2018F 2019F 2020F 2021F

E-commerce Physical

CAGR: 2.4%

CAGR: 9.8%

Growth of pan-European retail sales via e-commerce vs physical stores (2015=100)

Source: Colliers International - Online retailers and the growth of 'showrooming'

48

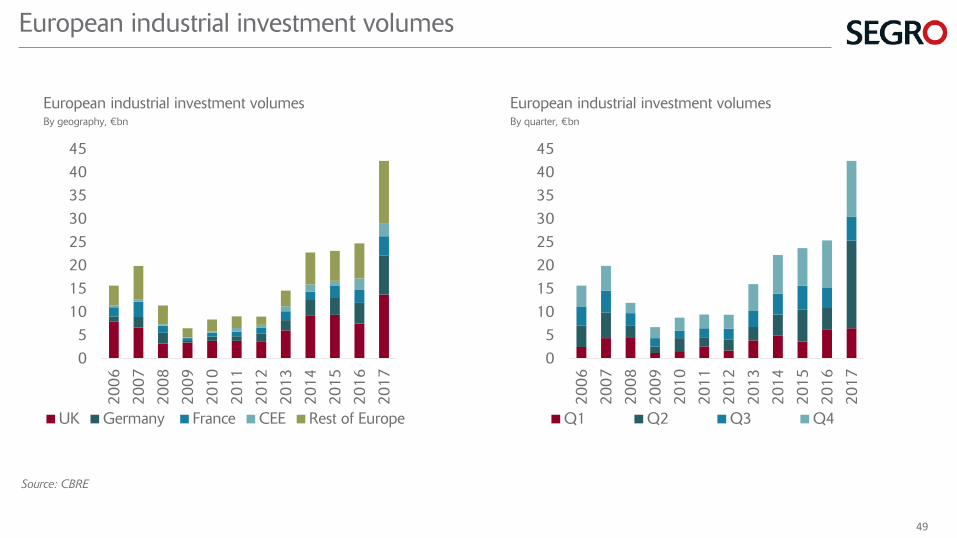

05

1015202530354045

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

UK Germany France CEE Rest of Europe

05

1015202530354045

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Q1 Q2 Q3 Q4

European industrial investment volumesBy geography, €bn

European industrial investment volumesBy quarter, €bn

Source: CBRE

European industrial investment volumes

49

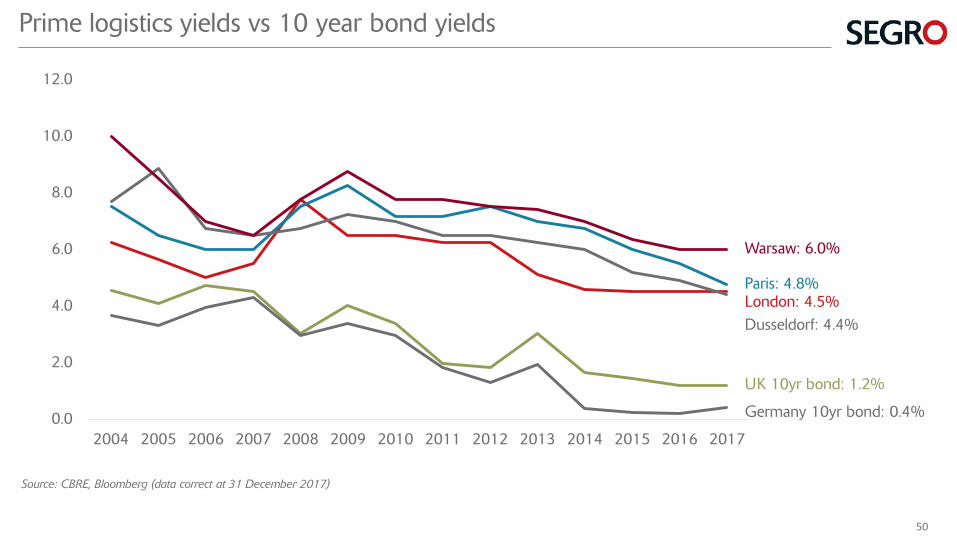

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Warsaw: 6.0%

Paris: 4.8%

Dusseldorf: 4.4%London: 4.5%

UK 10yr bond: 1.2%

Germany 10yr bond: 0.4%

Source: CBRE, Bloomberg (data correct at 31 December 2017)

Prime logistics yields vs 10 year bond yields

50

0.0

0.5

1.0

1.5

2.0

2.5

0.0

1.0

2.0

3.0

2011

2012

2013

2014

2015

2016

2017

No. of years’ supply

Take

-up

/ av

aila

bilit

y, m

sq

m

Average availability

Take-up

Available space as multiple of annual take-up

UK Big Box supply-demand dynamics1

(m sq m)

1 Source: JLL (logistics warehouses >100,000 sq ft, Grade A)2 Source: JLL

Speculative UK Big Box completions2

(m sq m)

0%

2%

4%

6%

8%

10%

12%

14%

0.0

1.0

2.0

3.0

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

In d

vpt

Vacancy rate

Com

plet

ions

, m s

q m

Construction Vacancy

Favourable demand-supply conditions: UK supply shortage

51

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

UK

Ger

man

y

Fran

ce

Belg

ium

Net

h.

Pola

nd Italy

Spai

n

Pre-let Speculative 4Q 2016

Logistics space under construction1

(m sq m)

1 Source: 4Q 2017, JLL2 Source: CBRE

European industrial and logistics supply dynamics

0.0

0.5

1.0

1.5

2.0

2.5

0.0

1.0

2.0

3.0

4.0

5.0

2010

2011

2012

2013

2014

2015

2016

2017

No. of years’ supply

Take

-up

/ av

aila

bilit

y, m

sq

m

Average availability

Take-up

Available space as multiple of annual take-up

France logistics supply-demand dynamics2

(m sq m)

52

0.0

1.0

2.0

3.020

07

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

New Second hand

Take-up of warehouse space >100,000 sq ft – UK1

(m sq m)

1 Source: JLL2 Source: CBRE3 Source: BNP Paribas Real Estate

0.01.02.03.04.05.0

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

0.0

2.0

4.0

6.0

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Net demand Lease renewals

Take-up of warehouse space >5,000 sq m – France2

(m sq m)

Take-up of warehouse space – Poland1

(m sq m)

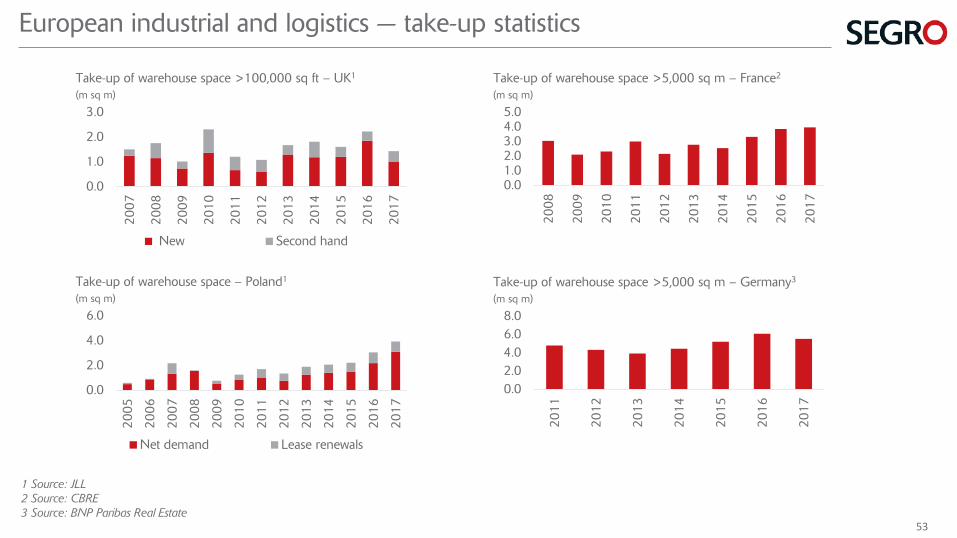

European industrial and logistics — take-up statistics

0.02.04.06.08.0

2011

2012

2013

2014

2015

2016

2017

Take-up of warehouse space >5,000 sq m – Germany3

(m sq m)

53

0.0

1.0

2.0

3.020

10

2011

2012

2013

2014

2015

2016

2017

New / Early Marketed Second hand

Availability of Grade A warehouse space >100,000 sq ft– UK1

(m sq m)

1 Source: JLL2 Source: CBRE

0.01.02.03.04.05.0

2009

2010

2011

2012

2013

2014

2015

2016

2017

0.0%

5.0%

10.0%

15.0%

0.0

1.0

2.0

2011

2012

2013

2014

2015

2016

2017

Pre-let Speculative Vacancy (RHS)

Availability of warehouse space >5,000 sq m – France2

(m sq m)

Warehouse space under construction and vacancy rate – Poland1

(m sq m)

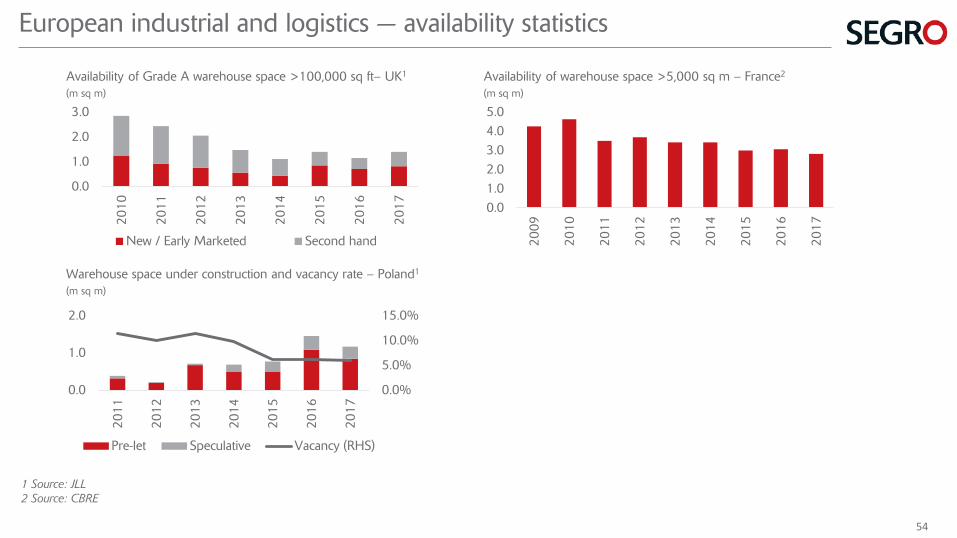

European industrial and logistics — availability statistics

54

1.01.11.21.31.41.51.61.71.8

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Dec

-16

Dec

-17

10yr ave Rolling annual

Heathrow Airport cargo volumes(million metric tonnes)

Source: Heathrow Airport

60

65

70

75

80

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Dec

-16

Dec

-17

10yr ave Rolling annual

Heathrow Airport passenger volumes(millions)

Heathrow Airport cargo and passenger volumes

55

This document has been prepared by SEGRO plc (‘SEGRO’) solely for use at the presentation of SEGRO’s results announcement in respect of the year ended 31

December 2017. For the purposes of this disclaimer, “Presentation” shall mean this document, the oral presentation of the slides by SEGRO and related question-and-

answer session and any materials distributed at, or in connection with, that presentation.

This Presentation does not constitute or form part of and should not be construed as, an offer to sell or issue, or the solicitation of an offer to buy or acquire, SEGRO’s

securities in any jurisdiction or an inducement to enter into investment activity. No part of this Presentation, nor the fact of its distribution, should form the basis of, or be

relied on in connection with, any contract or commitment or investment decision whatsoever.

This Presentation may contain certain forward-looking statements with respect to SEGRO’s expectations and plans, strategy, management’s objectives, future

performance, costs, revenues and other trend information. These statements and forecasts involve risk and uncertainty because they relate to events and depend upon

circumstances that may occur in the future. There are a number of factors which could cause actual results or developments to differ materially from those expressed or

implied by these forward looking statements and forecasts. The statements have been made with reference to forecast price changes, economic conditions and the

current regulatory environment. Any forward-looking statement is based on information available to SEGRO as at the date of the statement. SEGRO does not undertake

any obligation to revise or update any forward-looking statement to reflect any change in SEGRO’s expectations or events, conditions or circumstances on which any

such statement is based.

Nothing in this Presentation should be construed as a profit forecast. Past share performance cannot be relied on as a guide to future performance.

Forward-looking statements and Disclaimer

56