©2014 Genworth Financial, Inc. All rights reserved. What is MI? Understanding the Basics of...

53

©2014 Genworth Financial, Inc. All rights reserved. What is MI? Understanding the Basics of Mortgage Insurance August 2014

-

Upload

gabrielle-fritter -

Category

Documents

-

view

218 -

download

1

Transcript of ©2014 Genworth Financial, Inc. All rights reserved. What is MI? Understanding the Basics of...

©2014 Genworth Financial, Inc. All rights reserved.

What is MI?Understanding the Basics of Mortgage Insurance

August 2014

What is MI – The BasicsWho Does Mortgage Insurance Insure?

– Insures the LENDER not the borrower– MI required on conventional loans sold to Fannie Mae or Freddie Mac when *LTV

is greater than 80%– FHA and VA loans are insured by HUD or the Veteran’s Administration– Different types of MI products are available– Investors/Lenders restrict the “type” of MI they allow– Every MI rate is filed as required by applicable state law– Genworth is an approved MI provider by Fannie Mae and Freddie Mac– MI is not life or credit life insurance

August 2014 - What is MI?

*LTV is calculated by dividing the loan amount by lesser of the sales price or appraised value for a purchase or for a refinance use the loan amount divided by the appraised value

2

How MI HelpsBorrower Benefits

– Less than 20% down– Average homebuyer can take up to 10 years to save the 20% down– MI can be cancelled in certain cases

• MI is always cancelable by Lender but Investors may have certain requirements when it can be cancelled

• Homeowners Protection Act requires that MI must be cancelled at 78%LTV unless Investor has parameters around defaulted situations

– Tax deductible *– Affordable – Homeowner Assistance

*For further information about the deductability of MI seek a tax professional

3August 2014 - What is MI?

MI ProductsGenworth Mortgage Insurance Products

– Borrower paid Monthly and Zero Monthly (BPMI)– Borrower paid Standard Annual (Paid Monthly by borrower - remitted annually)– Borrower paid level Annual– Borrower or Lender Paid Split Premium– Borrower paid Single Premium/Non-Refundable– Lender Paid Single Premium Non-Refundable (LPMI)

Genworth Offers Many Types of Mortgage Insurance Products But Investors Dictate What Type of MI They Will Allow

4August 2014 - What is MI?

5

mi.genworth.com/RatesAndGuidelines/RateCards

August 2014 - What is MI?

Product: Borrower Paid Monthly (BPMI)

6

Lender Benefits– Premium does not count against qualified mortgage (QM) points & fees1

– Simple to process and explain to borrower… payment embedded in PITI– Commonly accepted – no investor restrictions– Easier processing & lower monthly payments than FHA loans

1Per the CFPB’s ATR/QM Small Entity Compliance Guide, monthly or annual PMI premiums are excluded from Points and Fees. The language can be found on page 38 of the guide which says the following:

“Private mortgage insurance (PMI) premiums: Exclude monthly or annual PMI premiums. You may also exclude up-front PMI premiums if the premium is refundable on a prorated basis and a refund is automatically issued upon loan satisfaction.”

August 2014 - What is MI?

Borrower Paid Zero Monthly Premium

7

Example of $150,000 loan amount, 90% LTVOwner occupied, fixed rate, single family & FICO score ≥ 760

August 2014 - What is MI?

Product: Standard Annual

8

Lender Benefits• Premium does not count against qualified mortgage (QM) points & fees1

• Provide borrowers more ways to pay for MI• Easier processing & lower monthly payments than FHA loans

1Per the CFPB’s ATR/QM Small Entity Compliance Guide, monthly or annual PMI premiums are excluded from Points and Fees. The language can be found on page 38 of the guide which says the following:“Private mortgage insurance (PMI) premiums: Exclude monthly or annual PMI premiums. You may also exclude up-front PMI premiums if the premium is refundable on a prorated basis and a refund is automatically issued upon loan satisfaction.”

August 2014 - What is MI?

Standard Annual Premium

9

Example of $150,000 loan amount, 90% LTVOwner occupied, fixed rate, single family & FICO score ≥ 760

August 2014 - What is MI?

Product: Split PremiumSplit Premium MI

– Is a payment option that features lower monthly rates combined with an upfront premium due at closing.

Borrower Paid– Non-refundable (must meet QM test) or Refundable (note: lender paid split is non-refundable)

Renewal Premiums– For Constant Renewals:

• The renewal premium rate is applied to the original loan balance for years 2 through 10.• For years 11 through term, the rate is reduced to 0.20% or remains the same if the rate is less than 0.20%.• Premium adjustments do not apply to the 11th year rate through term.

Lender Benefits– Provide borrowers more ways to pay for MI (greater buying power options to structure loans)– Qualify more borrowers (seller contributions/concessions)– Easier processing & lower monthly payments than FHA loans

10August 2014 - What is MI?

BP Non-Refundable Split Premium Plan #1

11

Example of $150,000 loan amount, 90% LTV, Premium Option Plan 1; Owner occupied, fixed rate, single family & FICO score ≥ 760

August 2014 - What is MI?

BP Non-Refundable Split Premium Plan #2

12

Example of $150,000 loan amount, 90% LTV, Premium Option Plan 2; Owner occupied, fixed rate, single family & FICO score ≥ 760

August 2014 - What is MI?

BP Non-Refundable Split Premium Plan #3

13

Example of $150,000 loan amount, 90% LTV, Premium Option Plan 3; Owner occupied, fixed rate, single family & FICO score ≥ 760

August 2014 - What is MI?

Additional BP Non-Refundable Split Premium Plans

14August 2014 - What is MI?

BP Non-Refundable Split Plans 1-4

15August 2014 - What is MI?

LP Non-Refundable Split Premium Plan #1

Pd by Lender through Rate

Example shows rate increased by .5%

16August 2014 - What is MI?

Product: SinglesBorrower Paid

– Provides coverage until the loan amortizes to 78% of the original value, unless previously cancelled. (Must meet QM test)

Lender Paid– Single premium lender paid options one–time premium coverage for the life of the loan.– Non-refundable only– See secondary for pricing

Lender Benefits– Qualify more borrowers– Reduce expenses – underwrite & process one loan– LPMI: premium does not count against qualified mortgage (QM) points & fees

17

Reminder: For BPMI non-refundable, the borrower may still get a refund if cancelled subject to HPA.

August 2014 - What is MI?

Refundable Single Premium

18

Example of $150,000 loan amountOwner occupied, fixed rate, single family & FICO score ≥ 760

August 2014 - What is MI?

Coverage and ExposureCoverage – Percentage of risk the MI company has

– Fannie Mae and Freddie Mac have coverage requirements– Most investors follow Fannie/Freddie guidelines for MI coverage – Lenders must ensure the required MI coverage is in force on the loan to deliver it

Exposure – The amount of risk the lender has– Most investors follow “exposure” requirements of Fannie Mae and Freddie Mac – Determining “exposure” is not part of the credit underwriting of the mortgage– Ensuring proper MI coverage is!

19August 2014 - What is MI?

Required MI Coverage Fannie Mae/Freddie Mac determine the required MI coverage

– Coverage requirements are based on LTV and amortization term/product type– In exchange for premiums, mortgage insurers reduce lender exposure to risk of

losses due to borrower default– Example

• 30 year fixed rate, 95% LTV loan (see highlighted area below)• Required Coverage is 30%

– Genworth would cover losses in the event of default up to 30% of the loan balance (plus allowable or “claimable” foreclosure costs)

– Lender’s original exposure is reduced to 67% LTV (95% x 70%)

20August 2014 - What is MI?

Required MI Coverage Let’s put numbers into the formula

– Appraisal Value/Sales Price $100,000– Loan amount: $95,000 or 95% LTV ($95,000/$100,000 = 95%)– Lender requires and MI provider will ensure 30% of the loan amount (which is

the standard MI coverage for Fannie Mae and Freddie Mac) • $95,000 x 30% = $28,500• Exposure is calculated by taking loan amount minus the covered loan amount ($95,000

- $28,500 = $66,500) and dividing by the value of $100,000• Lender exposure will be $66,500/$100,000 or 67%

21August 2014 - What is MI?

How is Maximum MI Coverage Calculated?

Unpaid Insured Loan Balance: $176,000Plus Allowable Foreclosure Costs: $ 18,000Total Outstanding Balance/Costs: $194,000Percentage of Coverage: 30%Maximum Coverage: ($194,000 X 30% $ 58,200)

MI Provider will pay the lender lesser of the maximum coverage or actual claim amount

22August 2014 - What is MI?

Calculation of Payment Claim to Lender

Total Outstanding Balance Costs: $194,000Less Pre-Foreclosure Sale Proceeds: $175,000Loss After Sale of Property: $ 19,000Payment due Lender in this case: $ 19,000*

*Genworth would pay the lesser of Maximum Claim Amount of $58,200 plus allowable foreclosure costs or Actual loss of $19,000 in this case.

23August 2014 - What is MI?

Cancellation** Guidelines

AutomaticLTV < 78%

Borrower Request to Lender

LTV < 80% LTV< 75%Yrs 2-5

LTV < 80%After yr 5

a

b

Original Value

Appreciated Value

a

a b

Cancellation Guidelines*

**Other Restrictions May Apply

Loan Servicer/Investor dictate when MI can be cancelled except for the case of automatic termination at 78%LTV of the “Original Value”

*Policies for One Unit Primary Residence/Second Home Properties

24August 2014 - What is MI?

MI cannot be cancelled without authorization from the Servicer– HPA (Homeowners Protection Act) law went into effect on July 29, 1999

• Applies to single family residential loans closed on or after July 29, 1999

– Cancellation at 80% or LTV• Borrower may request to cancel MI when the loan reaches 80% of the original property

value based on the initial amortization schedule or actual balance (in the event of curtailment).

– Automatic Termination at 78% LTV• Servicers must cancel MI when the LTV reaches 78% based on the initial amortization

schedule.*

Cancellation Guidelines*

* Additional requirements/restrictions may apply - check with the loan servicer for requirements

25August 2014 - What is MI?

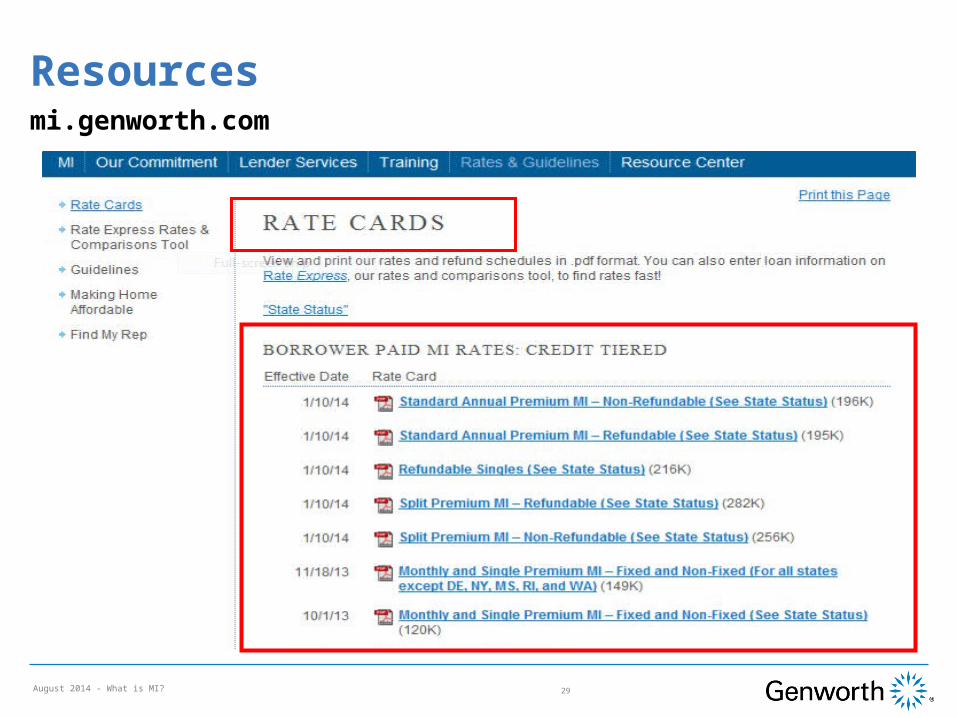

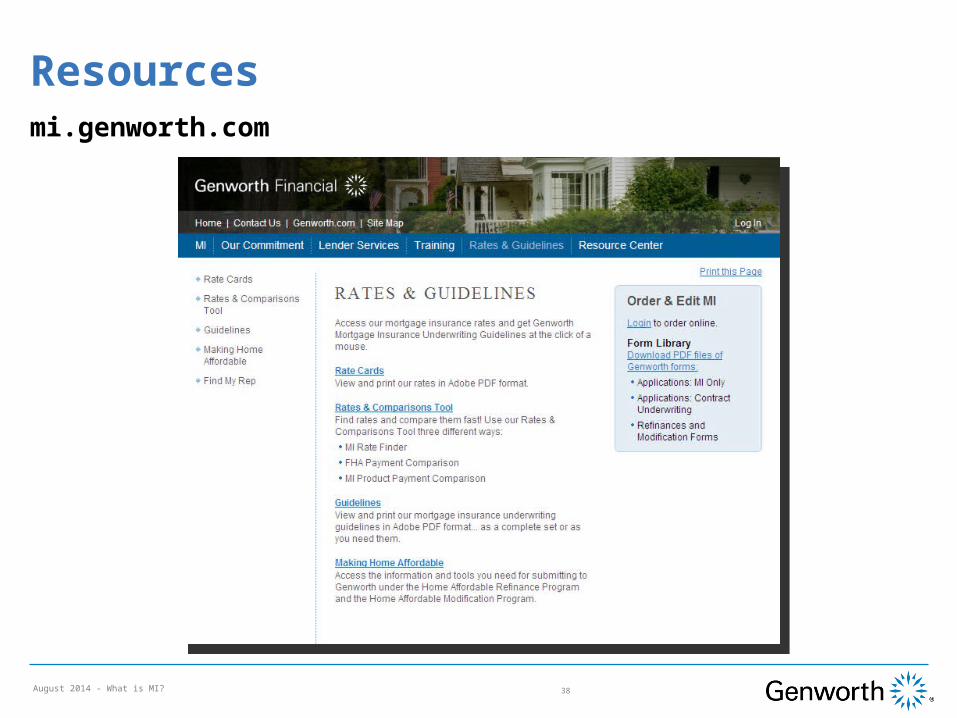

ResourcesGenworth Rate CardsQualified Mortgage (QM) InfoRate Express℠ Tool and Mobile App Genworth Underwriting Guidelines

26August 2014 - What is MI?

Resourcesmi.genworth.com

27August 2014 - What is MI?

Resourcesmi.genworth.com

28August 2014 - What is MI?

Resourcesmi.genworth.com

29August 2014 - What is MI?

Qualified Mortgage (QM) Info

30August 2014 - What is MI?

31August 2014 - What is MI?

Product Positioning and Points & Fees Considerations

Product positioning and marketing is focused on products that have limited to no implementation and Points and Fees impacts for customers.

August 2014 - What is MI? 32

Mobile App

33August 2014 - What is MI?

####

34August 2014 - What is MI?

Genworth Rate ExpressNo User ID or password required

– Contact your Genworth Account Rep for more information or with any loan scenario.

35August 2014 - What is MI?

$150,000 loan, 4.00% 95% LTV with 30% coverage 720 score, BPMI

Genworth Rate Express

36August 2014 - What is MI?

Genworth Rate Express

37August 2014 - What is MI?

Resourcesmi.genworth.com

38August 2014 - What is MI?

Genworth Guidelines

39August 2014 - What is MI?

40August 2014 - What is MI?

Genworth Guidelines

41August 2014 - What is MI?

42

Genworth Mortgage Insurance National Eligibility and Guidelines

Genworth Guidelines

42August 2014 - What is MI?

Genworth GuidelinesRemember Simply Underwrite

Genworth Guidelines Must Be Followed Regardless Of Lender/Investor Negotiated Variances Or Exceptions

43August 2014 - What is MI?

Simply UnderwriteSM

44August 2014 - What is MI?

Simply UnderwriteSM

45August 2014 - What is MI?

MI Ordering Options

Genworth Underwrite Genworth’s Delegated Underwriting

46August 2014 - What is MI?

MI Ordering Options

47August 2014 - What is MI?

Application for Genworth MI

48August 2014 - What is MI?

Sample Genworth MI Commitment/Certificate

49August 2014 - What is MI?

Genworth ActionCenter®

http://www.mortgageinsurance.genworth.com/

50August 2014 - What is MI?

For additional information on MI underwriting, MI servicing, premium billing, technical assistance and general inquires contact the Genworth ActionCenter.800 [email protected]

mi.genworth.com/LenderServices/UnderwritingGenworth Underwriting Resources

51August 2014 - What is MI?

Additional Resources

GENWORTH RESOURCES

Action Center: 800 444.5664

Your Local Genworth Underwriting Manager

Your Genworth Account Executive or Manager

52August 2014 - What is MI?

Genworth Mortgage Insurance is happy to provide you with these training materials. While we strive for accuracy, we also know that any discussion of laws and their application to particular facts is subject to individual interpretation, change, and other uncertainties. Our training is not intended as legal advice, and is not a substitute for advice of counsel. You should always check with your own legal advisors for interpretations of legal and compliance principles applicable to your business.

GENWORTH EXPRESSLY DISCLAIMS ANY AND ALL WARRANTIES, EXPRESS OR IMPLIED, INCLUDING WITHOUT LIMITATION WARRANTIES OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE, WITH RESPECT TO THESE MATERIALS AND THE RELATED TRAINING. IN NO EVENT SHALL GENWORTH BE LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, PUNITIVE, OR CONSEQUENTIAL DAMAGES OF ANY KIND WHATSOEVER WITH RESPECT TO THE TRAINING AND THE MATERIALS.

Legal Disclaimer

Desktop Underwriter ® or DU® are registered trademarks of Fannie MaeLoan Prospector ® or LP ® are registered trademarks of Freddie MacExcel® is a registered trademark of Genworth

53August 2014 - What is MI?