Languages

Pages

Legal

Transformation of Wireline Access Networks Requires Smarter Solutions

OvumOvumTMT intelligence |

Sponsored by

Ovum survey identifies key challenges and solutions

2 TMT intelligence informa © 2016 Ovum. All rights reserved.

Summary.............................................................. 3

Key highlights ..................................................3

Access network transformations are under way ...................................................... 4

QoE is a key competitive differentiator ..........4

Next-gen technologies are fueling bandwidth upgrades .......................................5

Wireline access network transformation ............ 6

Challenges throughout the transformation stages .............................................................6

Planning stage .................................................6

Implementation ...............................................7

Operations and management .........................9

Use of partners will increase .............................. 9

Usage expected to increase sharply for ongoing network management, optimization, QoE, and analytics ....................9

Recommendations for service providers .......... 11

Solve challenges externally and internally ................................................11

Appendix ............................................................ 12

Methodology ..................................................12

Further reading .............................................13

Contents About the authors

© Copyright Ovum 2016. All rights reserved.

The contents of this product are protected by international copyright laws, database rights and other intellectual property rights. The owner of these rights is Informa Telecoms and Media Limited, our affiliates or other third party licensors. All product and company names and logos contained within or appearing on this product are the trademarks, service marks or trading names of their respective owners, including Informa Telecoms and Media Limited. This product may not be copied, reproduced, distributed or transmitted in any form or by any means without the prior permission of Informa Telecoms and Media Limited.Whilst reasonable efforts have been made to ensure that the information and content of this product was correct as at the date of first publication, neither Informa Telecoms and Media Limited nor any person engaged or employed by Informa Telecoms and Media Limited accepts any liability for any errors, omissions or other inaccuracies. Readers should independently verify any facts and figures as no liability can be accepted in this regard - readers assume full responsibility and risk accordingly for their use of such information and content.Any views and/or opinions expressed in this product by individual authors or contributors are their personal views and/or opinions and do not necessarily reflect the views and/or opinions of Informa Telecoms and Media Limited.

Julie Kunstler

Julie Kunstler has over 25 years of experience in the communications components, equipment, and software industry. She is responsible for Ovum’s coverage of the wireline broadband access component, equipment, and software markets, closely following technology developments and subsequent effects on the vendor ecosystem. Julie is paying close attention to SDN/NFV and its impact on wireline broadband access.

Julie has worked as an executive, investor, and board member for communications companies. Having served in these numerous roles, Julie understands what it takes for new communications technologies to be deployed in large numbers and across multiple geographies. Julie brings her knowledge of the pressure on telcos to offer bandwidth-hungry applications along with the margin requirements of component vendors. Julie is a regular participant at industry events around the globe.

Kamalini Ganguly

Kamalini is a senior analyst with Ovum’s Service Provider & Markets practice, which provides an industry perspective across the fixed, mobile, and integrated telecoms marketplace. Looking towards the strategic horizon, the team assesses the challenges facing service providers and advises on how they will evolve and how they should respond.

Specifically, Kamalini tracks and analyzes the global fixed voice and broadband market, overseeing the forecast for DSL, cable, and FTTH/B broadband subscriptions for more than 67 countries. She provides a perspective on the future outlook for the fixed voice and broadband business and the changing role of service providers in the ecosystem. She examines the business case for the path to next-generation broadband, including best-practice commercialization strategies across fiber, copper, and Wi-Fi. She also advises service providers on the evolution of their fixed network and competitive bundling and pricing strategies.

3TMT intelligence informa© 2016 Ovum. All rights reserved.

SummaryKey highlightsQoE (quality of experience) is the primary driver for wireline access network transformations. Competitive pressures are forcing service providers to compete on service bundles and downstream speeds. Capex/opex savings are taking a backseat to subscriber requirements for bandwidth and services.

For this report, Ovum interviewed 50 wireline access network service providers around the world to understand their priorities for network transformations, along with their challenges and use of support partners. The service providers included both telco and cable operators.

Key findings across the 50 service providers include:•NetworkupgradesarebeingdrivenbybandwidthupgradestoimproveQoE.Customerchurniscostly

and wireline access service providers are operating in increasingly competitive environments, including competition from OTT services.

•Whilenetworktransformationcostisaconcern,itisnotakeydriveratthistime.Thefocusisonsubscribers – both residential and business – and the ability to offer services faster, including cloud-based service provisioning.

•Networktransformationpresentsseveralchallenges,suchaschoosingthebesttechnologystrategyandunderstanding its impact on future upgrades, identifying new revenue opportunities, and meeting rollout targets and network optimization goals. Many of the cited challenges can be mitigated through enhanced vendor relationships, improved tools, and targeting internal talent gaps.

•Serviceprovidersexpecttoincreasetheiralreadysignificantusageofpartners,suchasnetworkequipment vendors and IT services vendors. However, growth will be strongest for telecom software vendors and business/management consultants.

Key findings segmented by service provider type and region:•Integratedserviceproviders,thosewithbothwirelineandwirelessnetworks,consistentlyratedtheir

challenges higher than service providers that are wireline only. Even though the survey focused on wireline access transformation, the challenges are more complex when supporting and transforming different types of networks at the same time.

•Cableoperatorsoftenratedchallengesdifferentlythanthetelcooperators.Forexample,theycitedgreater challenges around making the business case for transformation. Conversely, cable operators rated a number of implementation challenges lower than their telco counterparts, such as lack of accurate databases.

•Asia-Pacific'sserviceprovidersratedconcernsregardingtheimpactoftechnologychoicesonfutureupgrades lower than service providers in other regions, possibly reflecting the prevalence of national broadbandplansinChina,Australia,NewZealand,andSingapore.Oftenthesenationalbroadbandplansset technology upgrade directions and provide funding, diminishing the concerns facing individual service providers.

4 TMT intelligence informa © 2016 Ovum. All rights reserved.

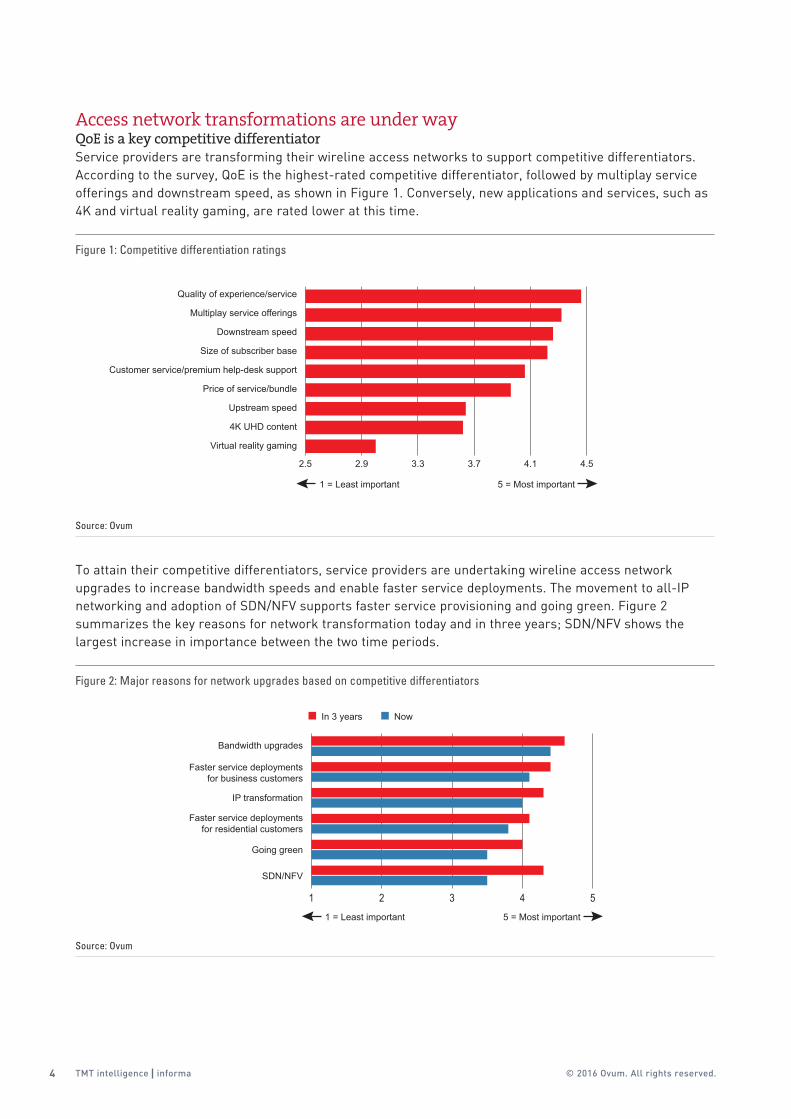

Access network transformations are under wayQoE is a key competitive differentiatorService providers are transforming their wireline access networks to support competitive differentiators. Accordingtothesurvey,QoEisthehighest-ratedcompetitivedifferentiator,followedbymultiplayserviceofferings and downstream speed, as shown in Figure 1. Conversely, new applications and services, such as 4K and virtual reality gaming, are rated lower at this time.

To attain their competitive differentiators, service providers are undertaking wireline access network upgrades to increase bandwidth speeds and enable faster service deployments. The movement to all-IP networking and adoption of SDN/NFV supports faster service provisioning and going green. Figure 2 summarizes the key reasons for network transformation today and in three years; SDN/NFV shows the largest increase in importance between the two time periods.

1 = Least important 5 = Most important

Quality of experience/service

Multiplay service offerings

Downstream speed

Size of subscriber base

Customer service/premium help-desk support

Price of service/bundle

Upstream speed

4K UHD content

Virtual reality gaming

2.5 2.9 3.3 3.7 4.1 4.5

Figure 1: Competitive differentiation ratings

Source: Ovum

In 3 years

Bandwidth upgrades

Faster service deploymentsfor business customers

IP transformation

Faster service deploymentsfor residential customers

Going green

SDN/NFV

1 = Least important 5 = Most important

Now

1 2 3 4 5

Figure 2: Major reasons for network upgrades based on competitive differentiators

Source: Ovum

5TMT intelligence informa© 2016 Ovum. All rights reserved.

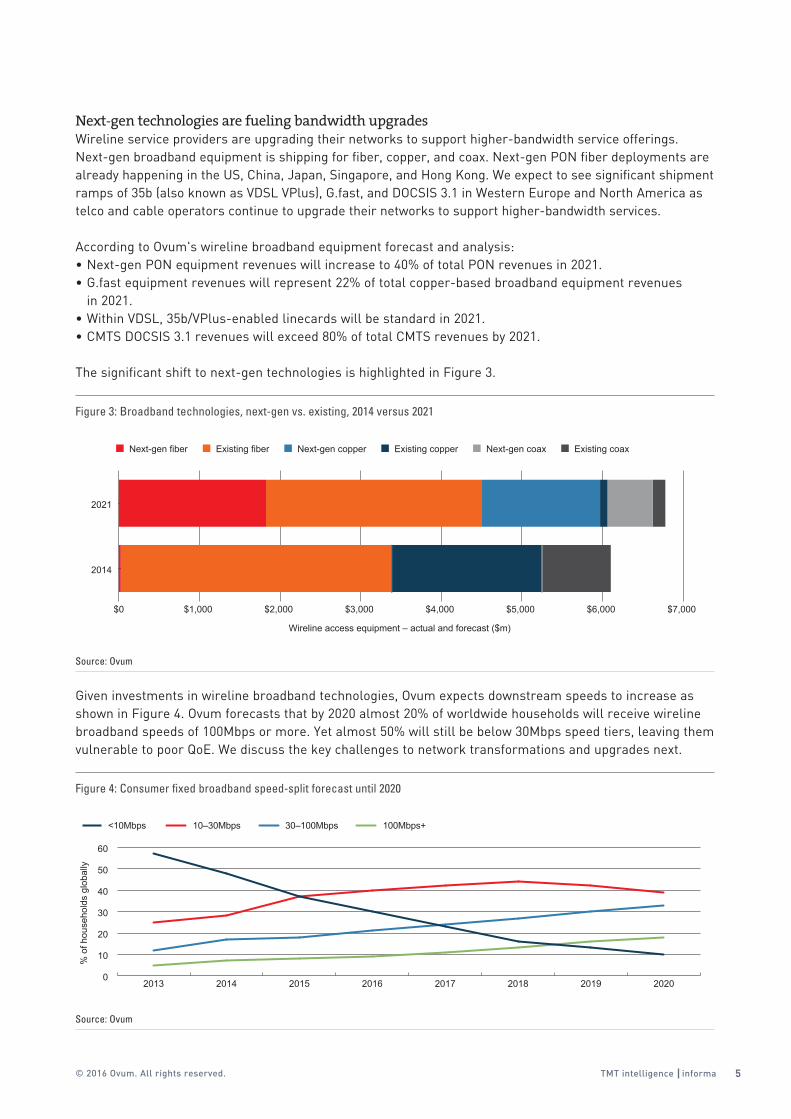

Next-gen technologies are fueling bandwidth upgrades Wireline service providers are upgrading their networks to support higher-bandwidth service offerings. Next-gen broadband equipment is shipping for fiber, copper, and coax. Next-gen PON fiber deployments are already happening in the US, China, Japan, Singapore, and Hong Kong. We expect to see significant shipment rampsof35b(alsoknownasVDSLVPlus),G.fast,andDOCSIS3.1inWesternEuropeandNorthAmericaastelco and cable operators continue to upgrade their networks to support higher-bandwidth services.

AccordingtoOvum'swirelinebroadbandequipmentforecastandanalysis:•Next-genPONequipmentrevenueswillincreaseto40%oftotalPONrevenuesin2021.•G.fastequipmentrevenueswillrepresent22%oftotalcopper-basedbroadbandequipmentrevenues

in 2021.•WithinVDSL,35b/VPlus-enabledlinecardswillbestandardin2021.•CMTSDOCSIS3.1revenueswillexceed80%oftotalCMTSrevenuesby2021.

The significant shift to next-gen technologies is highlighted in Figure 3.

Given investments in wireline broadband technologies, Ovum expects downstream speeds to increase as showninFigure4.Ovumforecaststhatby2020almost20%ofworldwidehouseholdswillreceivewirelinebroadbandspeedsof100Mbpsormore.Yetalmost50%willstillbebelow30Mbpsspeedtiers,leavingthemvulnerable to poor QoE. We discuss the key challenges to network transformations and upgrades next.

Wireline access equipment – actual and forecast ($m)

$0 $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 $7,000

2014

2021

Next-gen fiber Existing fiber Next-gen copper Existing copper Next-gen coax Existing coax

Figure 3: Broadband technologies, next-gen vs. existing, 2014 versus 2021

Source: Ovum

<10Mbps

% o

f hou

seho

lds

glob

ally

10–30Mbps 30–100Mbps 100Mbps+

0

10

20

30

40

50

60

20202019201820172016201520142013

Figure 4: Consumer fixed broadband speed-split forecast until 2020

Source: Ovum

6 TMT intelligence informa © 2016 Ovum. All rights reserved.

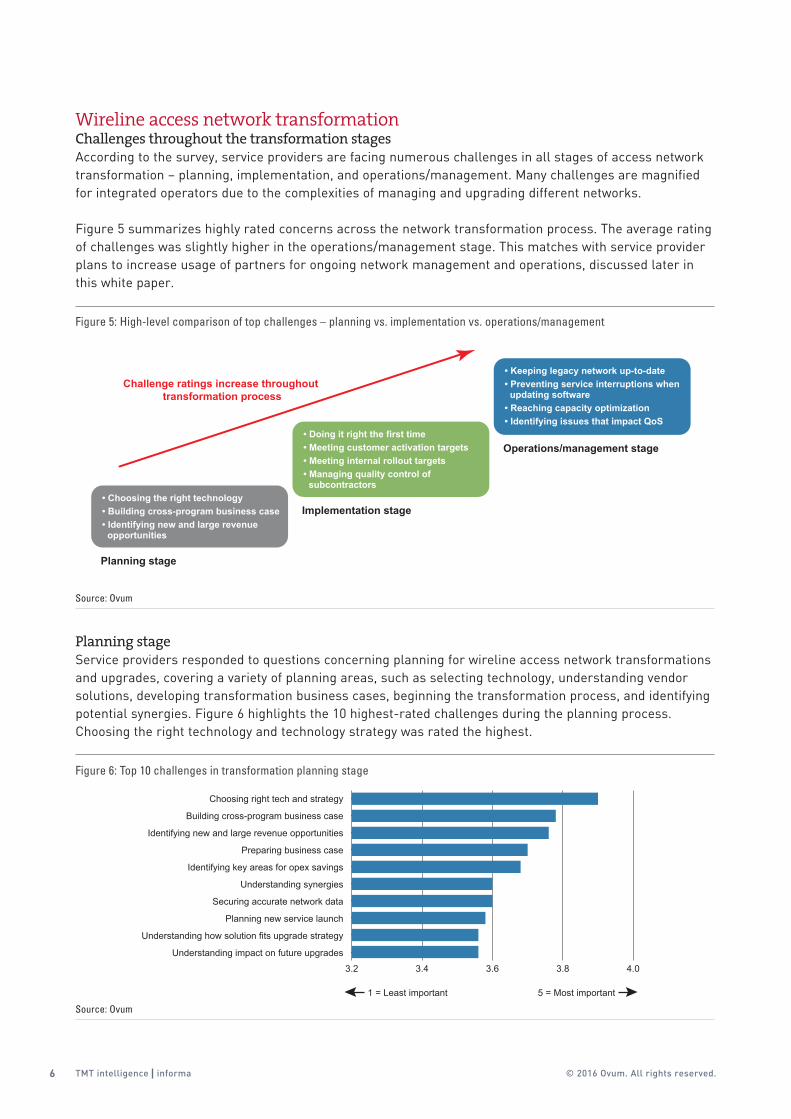

Wireline access network transformationChallenges throughout the transformation stages Accordingtothesurvey,serviceprovidersarefacingnumerouschallengesinallstagesofaccessnetworktransformation – planning, implementation, and operations/management. Many challenges are magnified for integrated operators due to the complexities of managing and upgrading different networks.

Figure 5 summarizes highly rated concerns across the network transformation process. The average rating of challenges was slightly higher in the operations/management stage. This matches with service provider plans to increase usage of partners for ongoing network management and operations, discussed later in this white paper.

Planning stageService providers responded to questions concerning planning for wireline access network transformations and upgrades, covering a variety of planning areas, such as selecting technology, understanding vendor solutions, developing transformation business cases, beginning the transformation process, and identifying potential synergies. Figure 6 highlights the 10 highest-rated challenges during the planning process. Choosing the right technology and technology strategy was rated the highest.

Planning stage

Challenge ratings increase throughout transformation process

• Choosing the right technology• Building cross-program business case• Identifying new and large revenue opportunities

Implementation stage

• Doing it right the first time• Meeting customer activation targets• Meeting internal rollout targets• Managing quality control of subcontractors

Operations/management stage

• Keeping legacy network up-to-date• Preventing service interruptions when updating software• Reaching capacity optimization• Identifying issues that impact QoS

Figure 5: High-level comparison of top challenges – planning vs. implementation vs. operations/management

Source: Ovum

Choosing right tech and strategy

Building cross-program business case

Identifying new and large revenue opportunities

Preparing business case

Identifying key areas for opex savings

Understanding synergies

Securing accurate network data

Planning new service launch

Understanding how solution fits upgrade strategy

Understanding impact on future upgrades

1 = Least important 5 = Most important

3.2 3.4 3.6 3.8 4.0

Figure 6: Top 10 challenges in transformation planning stage

Source: Ovum

7TMT intelligence informa© 2016 Ovum. All rights reserved.

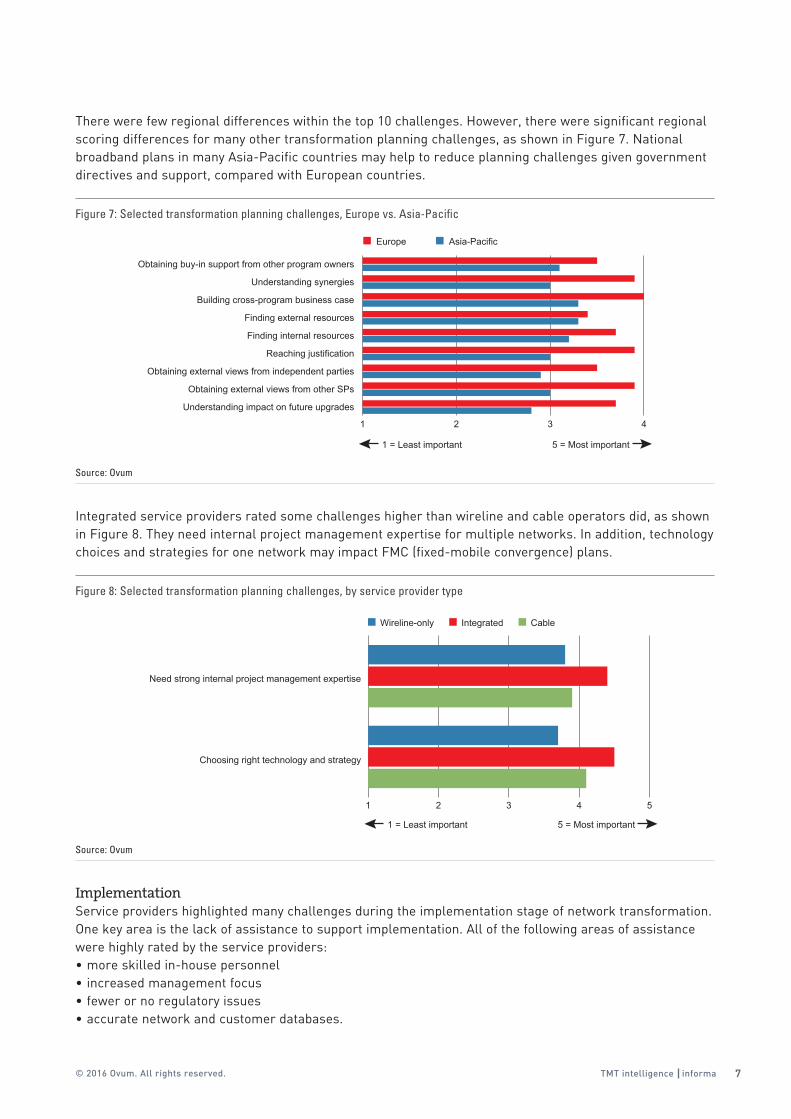

There were few regional differences within the top 10 challenges. However, there were significant regional scoring differences for many other transformation planning challenges, as shown in Figure 7. National broadbandplansinmanyAsia-Pacificcountriesmayhelptoreduceplanningchallengesgivengovernmentdirectives and support, compared with European countries.

Integrated service providers rated some challenges higher than wireline and cable operators did, as shown inFigure8.Theyneedinternalprojectmanagementexpertiseformultiplenetworks.Inaddition,technologychoices and strategies for one network may impact FMC (fixed-mobile convergence) plans.

ImplementationService providers highlighted many challenges during the implementation stage of network transformation. Onekeyareaisthelackofassistancetosupportimplementation.Allofthefollowingareasofassistancewere highly rated by the service providers:•moreskilledin-housepersonnel•increasedmanagementfocus•fewerornoregulatoryissues•accuratenetworkandcustomerdatabases.

Europe Asia-Pacific

1 2 3 4

Obtaining buy-in support from other program owners

Understanding synergies

Building cross-program business case

Finding external resources

Finding internal resources

Reaching justification

Obtaining external views from independent parties

Obtaining external views from other SPs

Understanding impact on future upgrades

1 = Least important 5 = Most important

Figure 7: Selected transformation planning challenges, Europe vs. Asia-Pacific

Source: Ovum

Integrated Cable

1 2 3 4 5

Wireline-only

Need strong internal project management expertise

Choosing right technology and strategy

1 = Least important 5 = Most important

Figure 8: Selected transformation planning challenges, by service provider type

Source: Ovum

8 TMT intelligence informa © 2016 Ovum. All rights reserved.

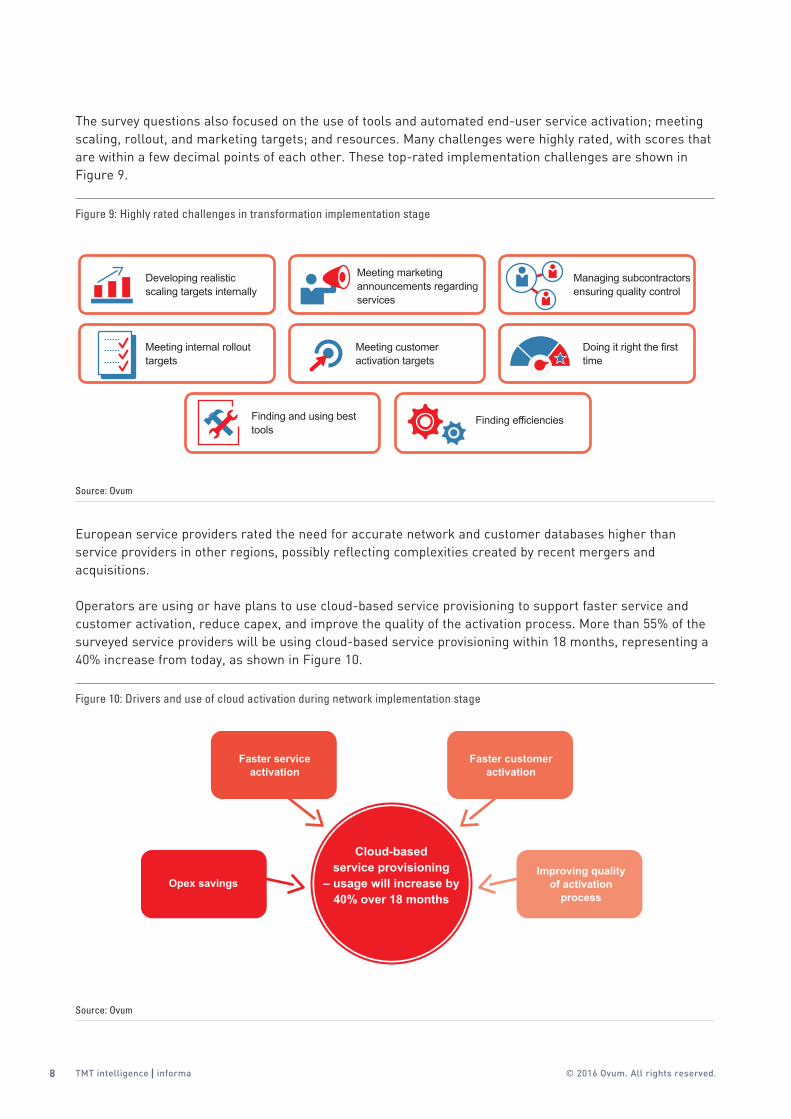

The survey questions also focused on the use of tools and automated end-user service activation; meeting scaling, rollout, and marketing targets; and resources. Many challenges were highly rated, with scores that are within a few decimal points of each other. These top-rated implementation challenges are shown in Figure 9.

European service providers rated the need for accurate network and customer databases higher than service providers in other regions, possibly reflecting complexities created by recent mergers and acquisitions.

Operators are using or have plans to use cloud-based service provisioning to support faster service and customeractivation,reducecapex,andimprovethequalityoftheactivationprocess.Morethan55%ofthesurveyedserviceproviderswillbeusingcloud-basedserviceprovisioningwithin18months,representinga40%increasefromtoday,asshowninFigure10.

Developing realistic scaling targets internally

Meeting internal rollout targets

Finding and using best tools

Meeting marketing announcements regarding services

Meeting customer activation targets

Finding efficiencies

Managing subcontractors ensuring quality control

Doing it right the first time

Figure 9: Highly rated challenges in transformation implementation stage

Source: Ovum

Cloud-based service provisioning

– usage will increase by 40% over 18 months

Opex savings

Faster service activation

Faster customer activation

Improving quality of activation

process

Figure 10: Drivers and use of cloud activation during network implementation stage

Source: Ovum

9TMT intelligence informa© 2016 Ovum. All rights reserved.

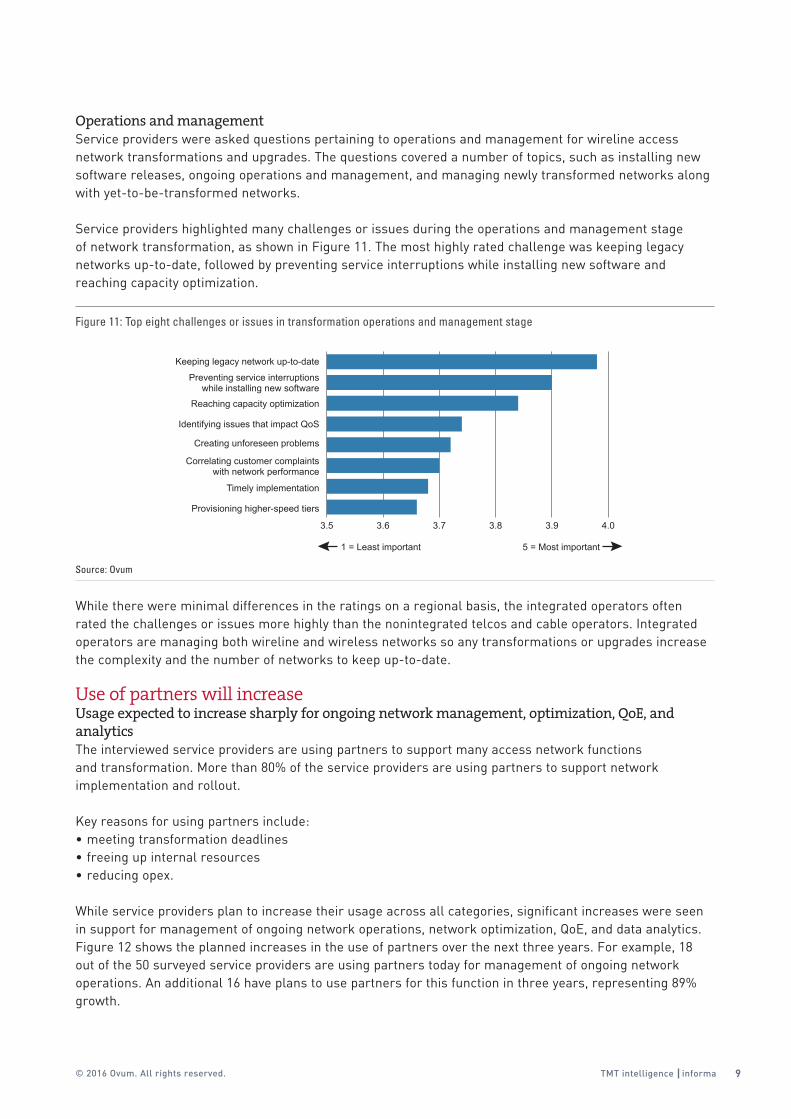

Operations and managementService providers were asked questions pertaining to operations and management for wireline access network transformations and upgrades. The questions covered a number of topics, such as installing new software releases, ongoing operations and management, and managing newly transformed networks along with yet-to-be-transformed networks.

Service providers highlighted many challenges or issues during the operations and management stage of network transformation, as shown in Figure 11. The most highly rated challenge was keeping legacy networks up-to-date, followed by preventing service interruptions while installing new software and reaching capacity optimization.

While there were minimal differences in the ratings on a regional basis, the integrated operators often rated the challenges or issues more highly than the nonintegrated telcos and cable operators. Integrated operators are managing both wireline and wireless networks so any transformations or upgrades increase the complexity and the number of networks to keep up-to-date.

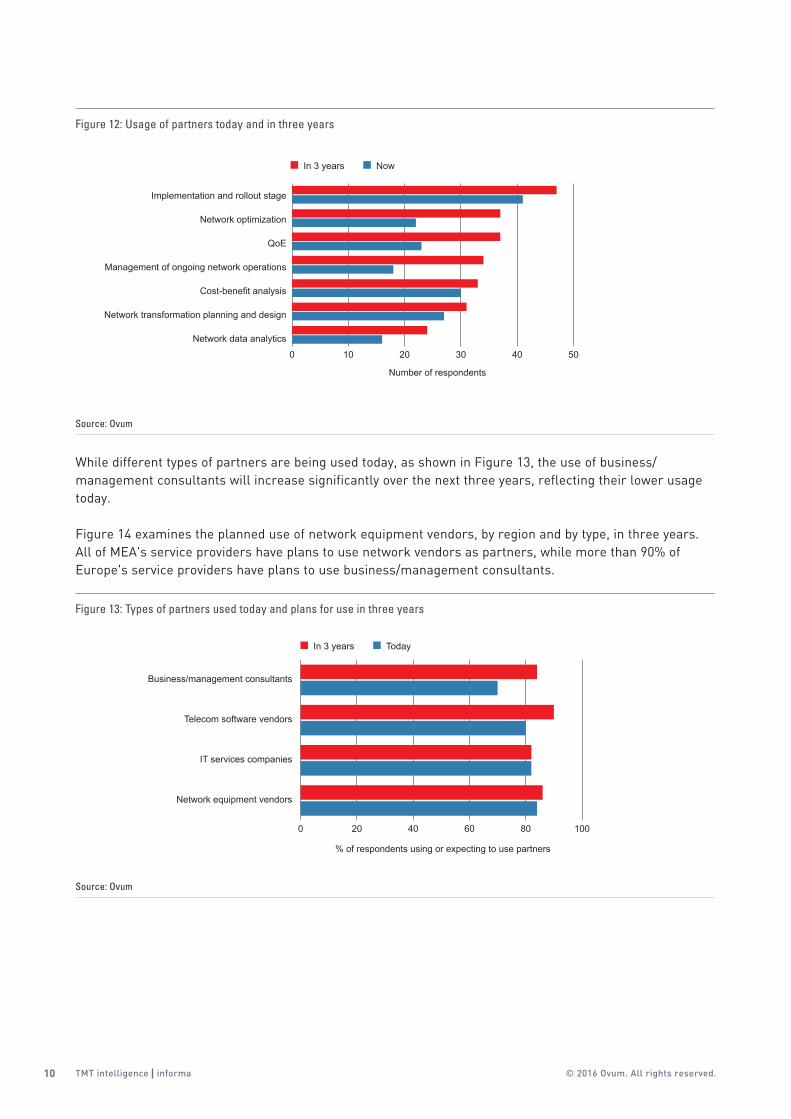

Use of partners will increaseUsage expected to increase sharply for ongoing network management, optimization, QoE, and analytics The interviewed service providers are using partners to support many access network functions andtransformation.Morethan80%oftheserviceprovidersareusingpartnerstosupportnetworkimplementation and rollout.

Key reasons for using partners include:•meetingtransformationdeadlines•freeingupinternalresources•reducingopex.

While service providers plan to increase their usage across all categories, significant increases were seen in support for management of ongoing network operations, network optimization, QoE, and data analytics. Figure12showstheplannedincreasesintheuseofpartnersoverthenextthreeyears.Forexample,18out of the 50 surveyed service providers are using partners today for management of ongoing network operations.Anadditional16haveplanstousepartnersforthisfunctioninthreeyears,representing89%growth.

Provisioning higher-speed tiers

Timely implementation

Correlating customer complaintswith network performance

Creating unforeseen problems

Identifying issues that impact QoS

Reaching capacity optimization

Preventing service interruptionswhile installing new software

Keeping legacy network up-to-date

1 = Least important 5 = Most important

3.5 3.6 3.7 3.8 3.9 4.0

Figure 11: Top eight challenges or issues in transformation operations and management stage

Source: Ovum

10 TMT intelligence informa © 2016 Ovum. All rights reserved.

While different types of partners are being used today, as shown in Figure 13, the use of business/management consultants will increase significantly over the next three years, reflecting their lower usage today.

Figure 14 examines the planned use of network equipment vendors, by region and by type, in three years. AllofMEA'sserviceprovidershaveplanstousenetworkvendorsaspartners,whilemorethan90%ofEurope'sserviceprovidershaveplanstousebusiness/managementconsultants.

Number of respondents

0 10 20 30 40 50

Network data analytics

Network transformation planning and design

Cost-benefit analysis

Management of ongoing network operations

QoE

Network optimization

Implementation and rollout stage

In 3 years Now

Figure 12: Usage of partners today and in three years

Source: Ovum

In 3 years

% of respondents using or expecting to use partners

Today

0 20 40 60 80 100

Business/management consultants

Telecom software vendors

IT services companies

Network equipment vendors

Figure 13: Types of partners used today and plans for use in three years

Source: Ovum

11TMT intelligence informa© 2016 Ovum. All rights reserved.

By type of service provider, integrated operators represent the highest partner usage group today and remain the highest usage group in three years, as shown in Figure 15. This is not surprising given their high ratings of challenges throughout the stages of network transformation.

Recommendations for service providersSolve challenges externally and internallyService providers need to work more closely with vendors to solve selected challenges. For example, vendors can provide additional resources concerning:•technologychoicesandtheirimpactonfutureupgrades•productreadiness•casestudymodelsandidentifyingpotentialareasofopexsavings•supportforfasternetworkbuildandrollout•solutionsforfasterserviceandcustomeractivation•toolssupportingnetworkoptimization•assistanceforkeepinglegacynetworksup-to-datewhilemigrating•supportforhigh-qualitynetworksoftwareupgrades•improvedQoE-monitoringtoolsandmodels.

% o

f res

pond

ents

usi

ng p

artn

ers

Asia-Pacific Europe Americas MEA

0102030405060708090

100

Business/management consultantsSoftware vendorsIT services companiesNetwork equipment vendors

Figure 14: Use of partners in three years – by partner type, by region

Source: Ovum

% o

f res

pond

ents

usi

ng p

artn

ers

Now In 3 years

53

0102030405060708090

Cable operatorTelco - integratedTelco - wireline only

7161

83

5565

Figure 15: Overall use of partners today and in three years, by type of service provider

Source: Ovum

12 TMT intelligence informa © 2016 Ovum. All rights reserved.

Service providers need to increase in-house expertise in selected areas, such as:•projectmanagementskillsforallstagesofnetworktransformation•managementofpartners–thisbecomesmoreimportantgivenplanstoincreaseusageofpartners.

Since many service providers have noncompetitive peers, they can share information on their use of tools, solutions, and partners to support network transformation planning, implementation, and management.

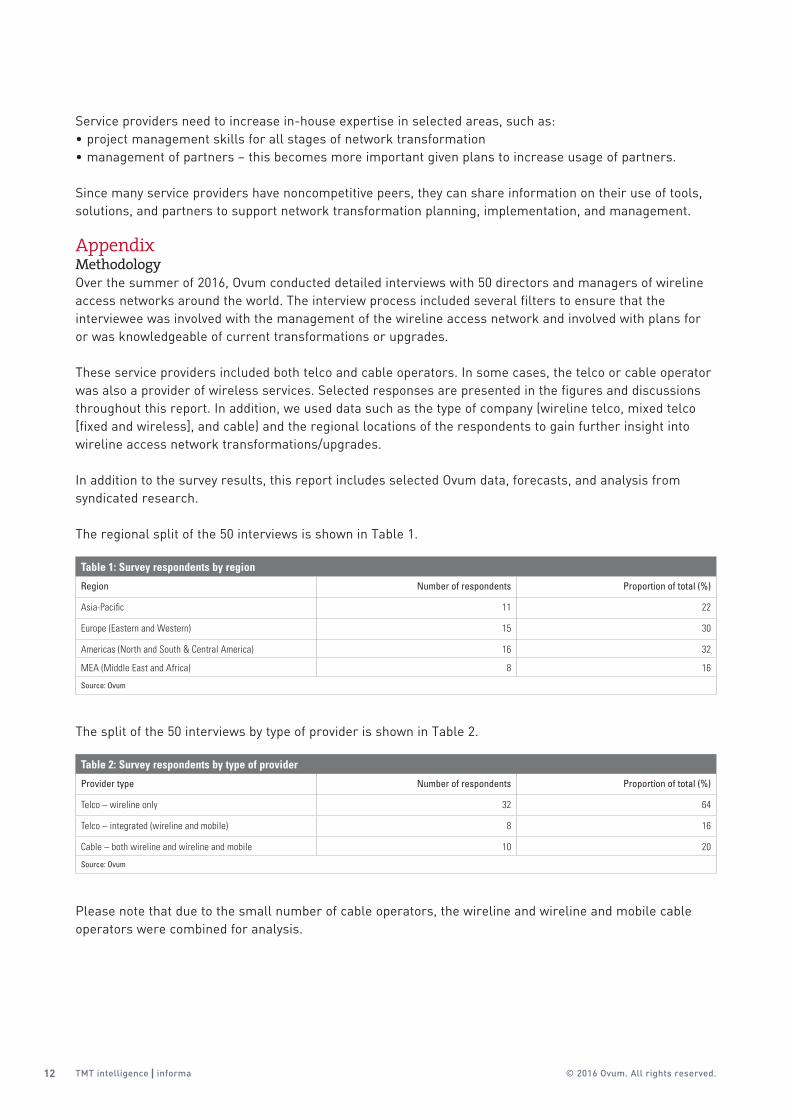

AppendixMethodologyOver the summer of 2016, Ovum conducted detailed interviews with 50 directors and managers of wireline access networks around the world. The interview process included several filters to ensure that the interviewee was involved with the management of the wireline access network and involved with plans for or was knowledgeable of current transformations or upgrades.

These service providers included both telco and cable operators. In some cases, the telco or cable operator was also a provider of wireless services. Selected responses are presented in the figures and discussions throughout this report. In addition, we used data such as the type of company (wireline telco, mixed telco [fixed and wireless], and cable) and the regional locations of the respondents to gain further insight into wireline access network transformations/upgrades.

In addition to the survey results, this report includes selected Ovum data, forecasts, and analysis from syndicated research.

The regional split of the 50 interviews is shown in Table 1.

The split of the 50 interviews by type of provider is shown in Table 2.

Please note that due to the small number of cable operators, the wireline and wireline and mobile cable operators were combined for analysis.

Table 1: Survey respondents by region

Region Number of respondents Proportion of total (%)

Asia-Pacific 11 22

Europe (Eastern and Western) 15 30

Americas (North and South & Central America) 16 32

MEA (Middle East and Africa) 8 16

Source: Ovum

Table 2: Survey respondents by type of provider

Provider type Number of respondents Proportion of total (%)

Telco – wireline only 32 64

Telco – integrated (wireline and mobile) 8 16

Cable – both wireline and wireline and mobile 10 20

Source: Ovum

13TMT intelligence informa© 2016 Ovum. All rights reserved.

Further reading

Market Share Report: 2Q16 FTTx, DSL, and CMTS, TE0006-001283(September2016)

Market Share Spreadsheet: 2Q16 FTTx, DSL + G.fast, and CMTS (Revenues), TE0006-001279(August2016)

Market Share Spreadsheet: 2Q16 FTTx, DSL + G.fast, and CMTS (Units), TE0006-001278(August2016)

Broadband Bundle Subscription Forecast: 2015–20, TE0009-001515 (March 2016)

Consumer Broadband Subscription and Revenue Forecast: 2015–20, TE0003-000903 (February 2016)

"Take-up of high-speed broadband is set to accelerate," TE0003-000905 (February 2016)

"Broadband access equipment market to remain strong in 2016," TE0006-001191 (February 2016)

Broadband Access Equipment Forecast (PON, xDSL, CMTS): 2015–21, TE0006-001186(February2016)

Telecom Network Services Evolution: Supporting CSP Transformation, TE0006-001184(January2016)

Vendor Telecom Network Services Forecasts: 2015–20, TE0006-001178(January2016)

2016 Trends to Watch: Wireline Broadband Access, TE0006-001143 (December 2015)

Implementing Customer Interaction Analytics to Manage Customer Complaints, IT0012-000140 (October 2015)

Service Provider PSTN Migration, TE0009-001449(August2015)

Global Fixed Industry Survey: 2015, TE0009-001431 (May 2015)

ABOUT OVUMOvumisaleadingglobaltechnologyresearchandadvisoryfirm.Throughits180analystsworldwideitoffersexpertanalysisandstrategicinsightacrosstheIT,telecoms,andmediaindustries.Foundedin1985,Ovumhasoneofthemostexperienced analyst teams in the industry and is a respected source of guidance for technology business leaders, CIOs, vendors, service providers, and regulators looking for comprehensive, accurate and insightful market data, research and consulting. With 23 offices across six continents, Ovum offers a truly global perspective on technology and media markets and provides thousands of clients with insight including workflow tools, forecasts, surveys, market assessments, technologyauditsandopinion.In2012,OvumwasjointlynamedGlobalAnalystFirmoftheYearbytheIIAR.

For more details on Ovum and how we can help your company identify future trends and opportunities, please contact us at [email protected] or visit www.ovum.com.TohearmorefromouranalystteamjoinourAnalystCommunitygroup on LinkedIn www.ovum.com/linkedin and follow us on Twitter www.twitter.com/OvumTelecoms.

OvumOvumTMT intelligence |

Top Related