Languages

Pages

Legal

Restructuring & Rollovers

redchip lawyers

Level 8, 100 Skyring Terrace | Newstead QLD 4006

Locked Bag 2 | Fortitude Valley QLD 4006

T +61 7 3223 6100 | F +61 7 3223 6199 | E [email protected]

www.redchip.com.au

March 2015

redchip lawyers | Restructuring & Rollovers | page i

Table of Contents

RESTRUCTURE OF SME BUSINESS .............................................................................................................. 1 1. INTRODUCTION ................................................................................................................................. 1 2. INDIVIDUALS/TRUSTEE/PARTNERSHIP CONVERSION TO A COMPANY STRUCTURE................................. 2 3. PRACTICAL EXAMPLE TRANSFER OF ASSETS – SUBDIVISION 122-B .................................................... 7 4. COMPANY STRUCTURE ...................................................................................................................15 5. CONVERSION OF A UNIT TRUST TO A COMPANY ...............................................................................22 PART IVA ITAA 1936 CASE STUDY ..........................................................................................................26 1. TRACK AND ORS V COMMISSIONER OF TAXATION - WHY PART IVA ITAA 1936 NEEDS TO BE

CONSIDERED ..................................................................................................................................26 2. BROADER ANALYSIS OF PART IVA ITAA 1936 .................................................................................36 GENERAL TAX UPDATES ...........................................................................................................................39 1. EMPLOYEE SHARE SCHEMES – DRAFT LEGISLATION RELEASED .......................................................39 2. LIMITED RECOURSE BORROWING ARRANGEMENTS – PROPOSED “LOOK-THROUGH” TAX TREATMENT 42 3. THE ENFORCEMENT OF SMSF ADMINISTRATIVE PENALTIES – THE ATO SPEAKS ..............................44

redchip lawyers | Restructuring & Rollovers | page 1

Restructure of SME Business

Presenter: Brian Richards, Specialist Tax Consultant, redchip lawyers

1. Introduction

There are many reasons and circumstances that cause questions being asked about the

commercial and taxation effectiveness of the taxpayer’s business structure at various points

of time:

(a) Are my enduring business assets protected from unexpected and significant risk

events?

(b) Are my private assets safe from business risk?

(c) Does my structure facilitate business expansion and geographic opportunities?

(d) Do I have the flexibility to determine how to deal with distributions of income and

capital?

(e) Can I deal expediently with any change of ownership of my business and its assets?

(f) Does my current business structure expose me to taxation complexity or risk?

(g) Am I paying the “right” amount of tax?

(h) Will I be able to access all or any of the present taxation concessions available to a

small business?

(i) Can I provide continuity for my business through intergenerational change or my

death?

It is the adviser’s ongoing task to ensure that the above questions are considered and acted

upon at the appropriate time. Making changes at a time when there is a tax event often

complicates the type and nature of advices that can appropriately be provided. Ultimately,

the end result of the responses to these questions might require a restructure of the

business or its assets in whole or in part.

Having regard to the myriad situations, there are various methods that are available to

achieve the restructure. In many circumstances a combination of methods might achieve the

commercial and taxation objectives of the client.

One of the essential issues for the adviser is to understand the longer term business

strategy of the client. Some of the above questions require a clear understanding of the

future and how to best facilitate the taxation and commercial implications of the future

business strategy.

Within the context of the above, when contemplating structure change, the use of various

CGT rollovers provided by Division 122, 124, 125 and 126 of the Income Tax Assessment

Act 1997 (Cth) (ITAA 1997) can achieve immediate taxation benefits but note that if the

longer term business strategy is for a client exit, then the ensuring that the benefits of

accessing the Division 152 ITAA 1997 concessions at the exit time must be considered in

the immediate context. That is:

(a) Whether the various rollover provisions are chosen in the first instance to preserve

CGT status and avoid any immediate taxation consequences; and

redchip lawyers | Restructuring & Rollovers | page 2

(b) What are the particular taxation issues that arise as a consequence of using any of the

rollover provisions?

For example access to Subdivision 152-B ITAA 1997 is time “sensitive” in that subdivision is

dependent on ownership of the asset for at least 15 years. With regard to Subdivision 152-

B, all of the rollover types create a new asset. The various rollover provisions do not,

however, negatively impact the timing issues for Division 115 ITAA 1997, as it does include

some grandfathering provisions. These issues are significant when considering restructuring

and/or changes in ownership.

As a general rule with any restructuring advices, the following taxation matters need to be

considered, at both the entity level and the stakeholder level:

(a) Those provisions of the ITAA that apply to revenue assets – trading stock, depreciable

assets, and debtors;

(b) Those provisions of the ITAA that apply to capital gains tax, including the various CGT

rollovers and CGT concessions;

(c) GST implications of the transfers of assets and interests; and

(d) Transfer Duty implications.

Importantly there is also the critical need to be cognisant of the associated commercial and

legal matters to reinforce the taxation decisions. Taxation should never be the driver of a

business transaction – commercial and family outcomes and objectives must lead any

restructuring analysis.

In this paper, we will examine various practical situations and discuss the taxation

implications and alternative methods to restructure. The discussion will consider:

(a) Conversion of business structure

(b) Trust to company

(c) Formation of a corporate group

(d) Mum & Dad to trust as a shareholder – how and consequences

As a general observation for the following discussion, there is no one or correct method to

achieve the desired outcome!

2. Individuals/Trustee/Partnership Conversion to a Company Structure

2.1 Introduction

With regard to the circumstances that involve an individual, a partnership or a trustee the ITAA

1997 provides for CGT relief where the transferor taxpayer transfers CGT assets to a company

subject to meeting specific conditions. The statutory requirements and consequences of one

form of rollover – Division 122 ITAA 1997, separates the type of taxpayer as follows:

(a) Subdivision 122-A ITAA 1997 applies to an individual and/or a trustee; and

(b) Subdivision 122-B ITAA 1997 applies to a partnership.

redchip lawyers | Restructuring & Rollovers | page 3

Fundamentally the requirements and consequences of both subdivisions are the same, albeit

with a partnership, all partners have to agree to the rollover election.

2.2 Application of Subdivision 122-A/B Rollover Option

Whereas generally the rollover relief is applied when there is a transfer of the ownership of an

asset (CGT Event A1), the provision has broader application than that. Consider the following

section which outlines the introductory provision if the taxpayer is either an individual or a

trustee of a trust:

Section 122-15 Disposal or creation of assets--wholly-owned company

If you are an individual or a trustee, you can choose to obtain a roll-over if one of the

*CGT events (the trigger event) specified in this table happens involving you and a

company in the circumstances set out in sections 122-20 to 122- 35.

Relevant *CGT events

Event No. What you do

A1 *Dispose of a CGT asset, or all the assets of a business, to the

company

D1 Create contractual or other rights in the company

D2 Grant an option to the company

D3 Grant the company a right to income from mining

F1 Grant a lease to the company, or renew or extend a lease

These extended CGT events are an important planning tool if the taxpayer is contemplating the

splitting of asset ownership from income generation, for example by transferring the income

earning capacity of the asset by leasing, licensing or otherwise creating some rights to the use

of the asset without transferring the ownership of the asset.

Note that the same opportunities arise in relation to a CGT asset of a partnership pursuant to

Subdivision 122-B (discussed below).

2.3 Division 122 – The Threshold Elements

As with any of the CGT rollover provisions, it is essential to ensure that the taxpayer

comprehends and then satisfies all of the specific elements of the section. A careful noting of

what conditions need to be satisfied is mandatory.

(a) Individual or trustee as the transferor taxpayer

Section 122-20 ITAA 1997 details the elements that an individual/trustee must satisfy

to access the rollover concession:

(i) Shares must be the only consideration, albeit the company can assume liabilities

related to the assets;

(ii) Shares must not be redeemable shares;

(iii) The market value of the shares must be substantially the same as the market

value of the assets transferred.

The section stipulates (bolding my emphasis):

redchip lawyers | Restructuring & Rollovers | page 4

Section 122-20

What you receive for the trigger event

(1) The consideration you receive for the trigger event happening must

be only:

(a) *shares in the company; or

(b) for a *disposal of a *CGT asset, or all the assets of a

business, to the company (a disposal case )--shares in the

company and the company undertaking to discharge one or

more liabilities in respect of the asset or assets of the

*business (as appropriate).

Note: There are rules for working out what are the liabilities in respect of an

asset: see section 122-37.

(2) The *shares cannot be *redeemable shares.

(3) The *market value of the *shares you receive for the trigger event

happening must be substantially the same as:

(a) for a disposal case--the market value of the asset or assets

you disposed of, less any liabilities the company undertakes

to discharge in respect of the asset or assets (as appropriate);

or

(b) for another trigger event (a creation case )--the market value

of the CGT asset created in the company (the created asset ).

(4) In working out if the requirement in paragraph (3)(a) is satisfied, if the

*market value of the *shares is different to what it would otherwise be

only because of the possibility of liabilities attaching to the asset or

assets, disregard the difference.

Note: The company may have to pay income tax if an amount is included in

its assessable income because of a CGT event happening to an asset

you disposed of, or it may have a liability because of accrued leave

entitlements of employees. The market value of the shares will reflect

these contingent liabilities.

(b) Partners – transferor taxpayers

The CGT provisions reflect in many respects the general law as it applies to a

partnership and treats a partner as having a separate interest in the partnership assets

(108-5 ITAA 1997) and this is reinforced by section 106-5 ITAA 1997 which provides:

Partnerships

(1) Any *capital gain or *capital loss from a *CGT event happening in

relation to a partnership or one of its *CGT assets is made by the

partners individually.

redchip lawyers | Restructuring & Rollovers | page 5

Each partner's gain or loss is calculated by reference to the

partnership agreement, or partnership law if there is no agreement.

Example 1: A partnership creates contractual rights in another entity

(CGT event D1). Each partner's capital gain or loss is calculated by

allocating an appropriate share of the capital proceeds from the event

and the incidental costs that relate to the event (according to the

partnership agreement, or partnership law if there is no agreement).

Example 2: Helen and Clare set up a business in partnership. Helen

contributes a block of land to the partnership capital. Their partnership

agreement recognises that Helen has a 75% interest in the land and

Clare 25%. The agreement is silent as to their interests in other assets

and profit sharing.

When the land is sold, Helen's capital gain or loss will be determined

on the basis of her 75% interest. For other partnership assets, Helen's

gain or loss will be determined on the basis of her 50% interest (under

the relevant Partnership Act).

(2) Each partner has a separate *cost base and *reduced cost base for

the partner's interest in each *CGT asset of the partnership.

Given the taxation context of a partner vis a vis the partnership, it is to be noted that

when considering the taxation implications involving a partnership restructure, the use

of Division 122 ITAA 1997 has some subtle issues.

First it will be noted that as with an individual or a trustee, the rollover provision

applies to various CGT Events, not only the transfer of ownership arrangement but

also the creation arrangement.

Second, and what must be carefully noted, is that section 122-125 ITAA 1997 requires

all of the partners to agree to the rollover (do not underestimate the practical difficulties

this might cause!)

Section 122-125 Disposal or creation of assets--wholly-owned company

All of the partners in a partnership can choose to obtain a roll-over if one of the * CGT

events (the trigger event) specified in this table happens involving the partners and a

company in the circumstances set out in sections 122-130 to 122-140.

Relevant * CGT events

Event No. What the partners do

A1 * Dispose of their interests in a * CGT asset of the partnership, or all the assets of a business carried on by the partnership, to the company

D1 Create contractual or other rights in the company

D2 Grant an option to the company

D3 Grant the company a right to income from mining

F1 Grant a lease to the company, or renew or extend a lease

redchip lawyers | Restructuring & Rollovers | page 6

Shares issued in sole consideration for the grant of

the licence.

Example – Asset creation rollover for partners

By way of example, assume a business partnership operates a successful professional

business and has created substantial goodwill and brand value. The partners are concerned

with risk exposure of the business and the nature of the business activities and wish to isolate

the trading risk by operating via a company.

The options the partners have are:

(a) Sell the entire partnership business or targeted assets and use whatever CGT

concessions are available;

(b) Use Subdivision 122-B ITAA 1997 to rollover the business; or

(c) Grant a goodwill licence to a company and use subdivision 122-B to transfer the

income generation to the company.

Subject to any Part IVA ITAA 1936 issues, the advantages of alternative (c) above include:

(d) Preserving the ownership of the asset;

(e) Preserving the CGT status of the asset;

(f) Avoiding potential Transfer Duty issues;

(g) Isolating the risk and providing asset protection by instituting termination entitlements

(contractual terms).

In this way, the subdivision can be applied to facilitate the following “creation” case:

The next step – the partner’s “move” to deal with newly acquired asset:

Whilst the above facilitates the “transference” of the direct interest in the asset, what is

particularly relevant is the requirement that the partners, subsequent to the rollover, must own

the interests in the company. This might satisfy the immediate tax consequences however it

does not negate entirely the asset protection risks nor maximise the taxation flexibility in

relation to the business income that is prudent.

As an aside and in the context of the above strategy, the ATO’s current stipulation that any

restructure of a “no goodwill” professional practice cannot be extended to an incorporated

practice unless the shareholders are individuals (TD 2011/26) merges conveniently with the

practical outcome of the rollover. As to whether this is commercially appropriate is a separate

issue.

Subject to any adverse transfer duty implications (there are no GST implications as any

interest in a partnership is a financial supply), the preliminary rollover to a company structure

pursuant to Subdivision 122-B ITAA 1997 might represent the first step in the restructure of an

redchip lawyers | Restructuring & Rollovers | page 7

individual partners newly acquired shares in the transferee company. That is the partner might

contemplate a subsequent transfer of the “partner” shareholder’s interest in the incorporated

entity to a family trust, for example.

Subject to the proportionate interest the partner holds (noting that a 20% interest is the relevant

threshold for Division 152 ITAA 1997), both Division 115 and Division 152 ITAA 1997 could be

available to negate any taxation consequences of the restructure. Further, there would be no

GST or transfer duty implications for the second tranche of transactions.

3. Practical Example Transfer of Assets – Subdivision 122-B

The above example illustrates the potential utility of the Division 122 ITAA 1997 CGT rollover,

the following practical examples illustrates some of the nuances of the rollover and identify

some of the subtleties of the provision.

From the outset it must be emphasised that the rollover provisions deal with relief from CGT. If

the transaction involves a revenue asset, these rollover provisions merely defer the CGT

component of any gain. If there is any revenue gain attributable to the transaction, you need to

consider the transaction in the context of that revenue provision. Division 70 ITAA 1997

(trading stock) and Division 40 ITAA 1997 (depreciable assets) are two common examples.

When considering a restructure of a business or a business asset, the use of the rollover

provision is often compared to the use of the concessional CGT provisions (i.e. Division 115

and Division 152 ITAA 1997). There are many variables to consider, however hopefully the

following example illustrates some of the situational circumstances that will influence the use of

the rollover concessions.

3.1 Facts

(a) Mr A & Mrs A have operated a small engineering business for 10 years.

(b) The business is very profitable but the nature of the business has a level of commercial

risk associated with the installation of its product into client’s machinery and

manufacturing processes.

(c) One of the reasons for the success of the business is its ability to continue to innovate.

A substantial amount of expenditure is incurred in research & development

expenditure. The business owns a number of valuable patents.

(d) The business has a market value of $ 4 million consisting of the following assets:

Cost Base Market Value

(i) Patents nil $1 million

(ii) Depreciable Plant (WDV) $200,000 $500,000

(iii) Trading Stock (at cost) $300,000 $300,000

(iv) Debtors $225,000 $200,000

(v) Goodwill nil $2 million

(e) Mrs & Mrs A have limited other assets.

redchip lawyers | Restructuring & Rollovers | page 8

3.2 Issues

If Mr & Mrs A wish to conduct their business in a company, what are the best methods to

achieve this objective?

3.3 Conversion Options

Sell all or some of the assets to a company(s); or

Rollover all or some of the assets; or

Some combination of the above.

(a) Sale Option

First consider the implications of selling the specific assets owned by Mr & Mrs A to the

company:

(i) Taxation characteristics of the assets

(A) Patents:

Fully assessable pursuant to Division 40 ITAA 1997 as a patent

is a depreciable asset (section 40-30 ITAA 1997);

Subject to Transfer Duty if sold together with other business

assets.

(B) Depreciable Assets:

The amount in excess of the written down value is assessable

pursuant to Division 40 ITAA 1997.

(C) Debtors:

There will be no direct taxation consequences of the transfer of

debtors, however the company will not be entitled to claim any

bad debt deduction (section 25-35 ITAA 1997).

(D) Goodwill:

The sale would generate a capital gain of $2 million;

Mr & Mrs A would entitled to reduce the gain by $1M by applying

the Division 115 ITAA 1997 discount;

Mr & Mrs A would be entitled to further reduce the net gain by

applying Subdivision 152-C ITAA 1997 ($500,000) and perhaps

applying Subdivision 152-D in respect of the balance (the latter

requires a cash contribution into a complying superannuation

fund unless they are over 55 years of age).

(ii) Taxation implications on the disposal of the assets

It is highly unlikely that Mr & Mrs A would accept the sale of the entire assets

having regard to the significant income tax liability related to the disposal of the

patent and the depreciable assets, notwithstanding any cost base uplift.

redchip lawyers | Restructuring & Rollovers | page 9

They need to have a company to conduct the R & D activities to maximise the

tax concessions available for their ongoing innovation, but care needs to be

exercised to ensure that the entity claiming R & D owns the IP and enjoys the

economic benefits associated with the R & D.

They might decide to only transfer the goodwill and claim the CGT concessions

to eliminate any tax and at the same time reset the cost base of the goodwill.

(b) Rollover Option

As the A Family conducts their business as a partnership, they can elect to apply

Subdivision 122-B ITAA 1997 to achieve the transfer of the business to a company, if

the consideration for the transfer of assets is satisfied by the issue of non-redeemable

shares (plus assumption of liabilities that are related to the transferred assets).

Assume for the purposes of this example, the company issues 4 million $1 shares as

the consideration for the transfer (Note: it does not matter how many shares are

issued, the primary requirement is that the shares issued is approximately the same as

the market value of the assets transferred, that is 100 shares can be issued and the

requirements will be satisfied).

Pursuant to Subdivision 122-B ITAA 1997, all of the partners (Mr A & Mrs A) must

jointly agree to apply this subdivision; with the consequence being they are then able

to disregard any CGT implications on the transfer of CGT assets.

Section 122-130 Rollover conditions

What the partners receive for the trigger event

(1) The consideration the partners receive must be only:

(c) *shares in the company; or

(d) for a *disposal of their interests in a *CGT asset, or in all the

assets of a business, to the company (a disposal case )--

shares in the company and the company undertaking to

discharge one or more liabilities in respect of their interests.

Note: There are rules for working out what are the liabilities in respect

of an interest in an asset: see section 122-145.

(2) The *shares cannot be *redeemable shares.

(3) The *market value of the *shares each partner receives for the trigger

event happening must be substantially the same as:

(a) for a disposal case--the market value of the interests in the

asset or assets the partner disposed of, less any liabilities the

company undertakes to discharge in respect of the interests in

the asset or assets (as appropriate); or

redchip lawyers | Restructuring & Rollovers | page 10

(b) for another trigger event (a creation case )--the market value

of what would have been the partner's interest in the * CGT

asset created in the company (the created asset ) if it were an

asset of the partnership.

(4) In working out if the requirement in paragraph (3)(a) is satisfied, if the *

market value of the *shares is different to what it would otherwise be

only because of the possibility of liabilities attaching to the asset or

assets, disregard the difference.

Note: The company may have to pay income tax if an amount is

included in its assessable income because of a CGT event happening

to an asset a partner disposed of, or it may have a liability because of

accrued leave entitlements of employees. The market value of the

shares will reflect these contingent liabilities.

The consequences of the rollover need to be considered from the perspective of the

shareholder transferor and the company transferee.

(c) Consequences for partners as transferors of the assets

The taxation implications for partners when they transfer their interests in the

partnership assets

The taxation consequences for the partners when choosing the rollover relief is

dependent on the nature of the asset and the acquisition date of the asset (i.e. whether

the asset was a pre-CGT asset).

There are three categories of assets that we generally need to consider:

(i) General CGT assets (section 108-5 ITAA 1997 defines the term “CGT asset”);

(ii) Division 70 ITAA 1997 – trading stock; and

(iii) Division 40 ITAA 1997 – depreciable assets.

When the Subdivision 122-B ITAA 1997 rollover is applied, the partners are able to:

(i) disregard the CGT gain as a consequence of the rollover pursuant to section

122-170 ITAA 1997;

(ii) defer the balancing adjustment pursuant to section 40-340 ITAA 1997

(discussed below).

But they cannot disregard the Division 70 ITAA 1997 issues (trading stock).

If all of the assets are being transferred in conjunction with the rollover, it is important

to consider the ramifications of “precluded assets”. In this regard section 40-340 ITAA

1997 is relevant to the taxation implications of the rollover. Section 40-340 ITAA 1997

provides that there is an automatic rollover where all of the assets of the partnership

are transferred:

Section 40-340 Roll-over relief

Automatic roll-over relief

redchip lawyers | Restructuring & Rollovers | page 11

(1) There is roll-over relief if:

(a) there is a *balancing adjustment event because an entity (the

transferor ) disposes of a *depreciating asset in an income

year to another entity (the transferee ); and

(b) the disposal involves a *CGT event; and

(c) the conditions in an item in this table are satisfied

Item 2 Disposal of asset by partnership to wholly-owned company

The transferor is a partnership, the property is partnership property

and the partners are able to choose a roll-over under Subdivision 122-

B for the disposal by the partners of the *CGT assets consisting of

their interests in property.

(2) In applying an item in the table in subsection (1), disregard the

following so far as they relate to the *depreciating asset you disposed

of:

(a) an exemption in Division 118 (which contains the general

exemptions from CGT); and

(b) subsection 122-25(3) (which excludes certain assets from roll-

over relief under Subdivision 122-A); and

(c) subsection 124-870(5) (which excludes certain assets from

roll-over relief under Subdivision 124-N).

The effect of the roll-over relief provision is to defer the balancing adjustment until the

next balancing adjustment event for which there is no roll-over relief and to allow the

transferee to claim deductions for the depreciating asset which has been transferred

as if the asset continued to be held by the transferor. However, importantly, the

rollover is dependent on all of the assets being transferred pursuant to the Subdivision

122-A or Subdivision 122-B ITAA 1997 rollover.

This is evidenced by the section’s stipulation that certain assets are disregarded for

the purposes of the rollover in certain circumstances (sub-section 122-135(3) ITAA

1997):

redchip lawyers | Restructuring & Rollovers | page 12

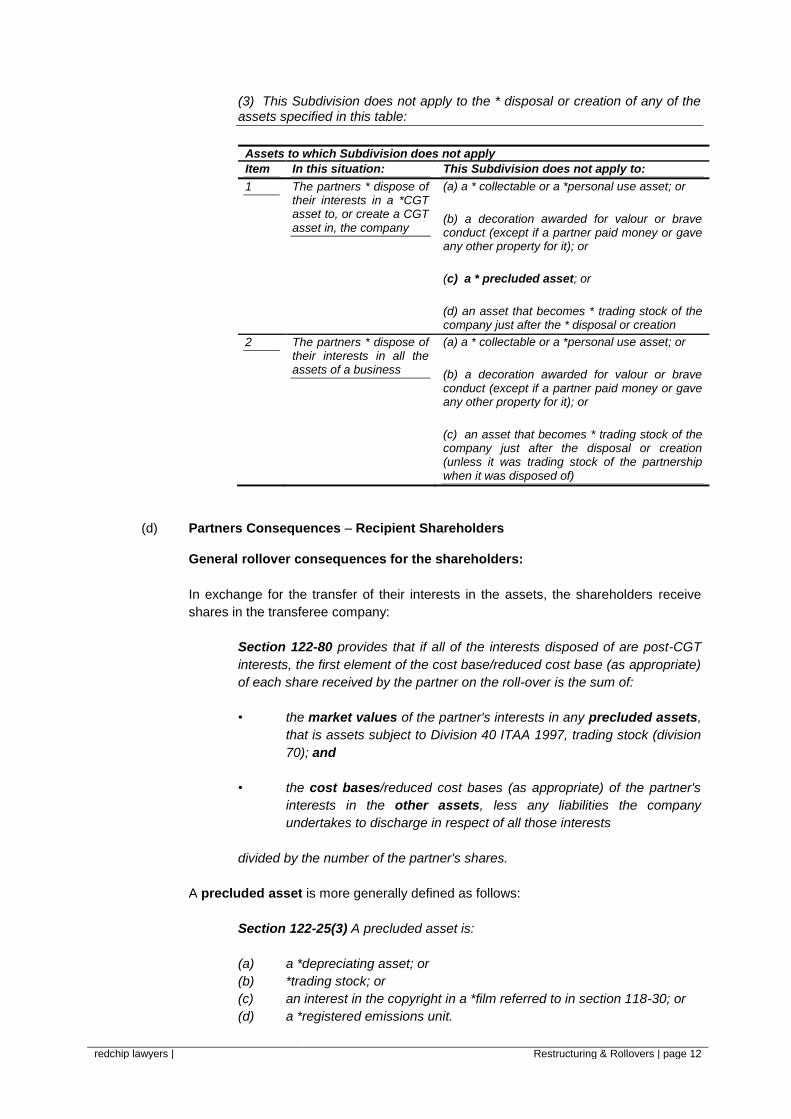

(3) This Subdivision does not apply to the * disposal or creation of any of the assets specified in this table:

Assets to which Subdivision does not apply

Item In this situation: This Subdivision does not apply to:

1 The partners * dispose of their interests in a *CGT asset to, or create a CGT asset in, the company

(a) a * collectable or a *personal use asset; or

(b) a decoration awarded for valour or brave conduct (except if a partner paid money or gave any other property for it); or

(c) a * precluded asset; or

(d) an asset that becomes * trading stock of the company just after the * disposal or creation

2 The partners * dispose of their interests in all the assets of a business

(a) a * collectable or a *personal use asset; or

(b) a decoration awarded for valour or brave conduct (except if a partner paid money or gave any other property for it); or

(c) an asset that becomes * trading stock of the company just after the disposal or creation (unless it was trading stock of the partnership when it was disposed of)

(d) Partners Consequences – Recipient Shareholders

General rollover consequences for the shareholders:

In exchange for the transfer of their interests in the assets, the shareholders receive

shares in the transferee company:

Section 122-80 provides that if all of the interests disposed of are post-CGT

interests, the first element of the cost base/reduced cost base (as appropriate)

of each share received by the partner on the roll-over is the sum of:

• the market values of the partner's interests in any precluded assets,

that is assets subject to Division 40 ITAA 1997, trading stock (division

70); and

• the cost bases/reduced cost bases (as appropriate) of the partner's

interests in the other assets, less any liabilities the company

undertakes to discharge in respect of all those interests

divided by the number of the partner's shares.

A precluded asset is more generally defined as follows:

Section 122-25(3) A precluded asset is:

(a) a *depreciating asset; or

(b) *trading stock; or

(c) an interest in the copyright in a *film referred to in section 118-30; or

(d) a *registered emissions unit.

redchip lawyers | Restructuring & Rollovers | page 13

If, however, all of the assets of the business are transferred, precluded assets and

trading stock are included as part of the rollover and any CGT consequences are

disregarded.

The consequence of the cost base rules for the shares is that any unrealised gain

attributable to the precluded assets is “protected” from tax. The potential tax liability is

shifted to the company.

Example

Based on the application of the above statute and applying it to our facts, Mr & Mrs A

receive 4 million shares which will have a cost base (for the purposes of future CGT

transactions) equal to:

(i) Cost base of assets transferred:

Goodwill nil

Debtors $225,000 $225,000

(ii) Market value of precluded assets

Patents $1,000,000

Depreciable plant $500,000

Trading stock $300,000 $1,800,000

Total cost base of the shares $2,025,000

(e) Company Consequences

Pursuant to section 122-200 ITAA 1997, where the partners dispose of an asset to a

wholly-owned company and all of the partners’ interests are post-CGT interests:

(i) The cost base of the asset in the company will be the asset’s cost

base/reduced cost base (as appropriate) when it was disposed of (s122-200(2)

ITAA 1997);

(ii) However this does not apply to a precluded asset (s122-200(1) ITAA 1997) —

a capital gain or loss from a precluded asset can be disregarded (Subdivision

118-A ITAA 1997); and

(iii) Note the relevance of the CGT rollover if depreciating assets are included in

the rollover (section 40-345 ITAA 1997).

The CGT rollover legislation provides:

Section 122-200(1) There are these consequences for the company in a

disposal case if the partners choose to obtain a roll-over. They are relevant for

interests in each *CGT asset (except a *precluded asset) that the partners

*disposed of to the company.

Section 122-200(2) If all of the partners’ interests in an asset were *acquired

on or after 20 September 1985:

redchip lawyers | Restructuring & Rollovers | page 14

(a) the first element of the asset’s *cost base (in the hands of the

company) is the sum of the cost bases of the partners’ interests in the

asset when it was disposed of; and

(b) the first element of the asset’s *reduced cost base (in the hands of the

company) is the sum of the reduced cost bases of the partners’

interests in the asset when it was disposed of.

Where a depreciable asset is included (a “precluded asset”) and the rollover provisions

are applicable, the Division 40 ITAA 1997 implications are provided by section 40-345

ITAA 1997:

40-345(1) Section 40-285 does not apply to the *balancing adjustment event

for the transferor.

40-345(2) The transferee can deduct the decline in value of the *depreciating

asset using the same method and *effective life (or *remaining effective life if

that method is the *prime cost method) that the transferor was using.

That is:

(i) The transferor has no revenue gain pursuant to Division 40 ITAA 1997;

(ii) The transferor has no CGT gain pursuant to Subdivision 122 ITAA 1997; and

(iii) The transferee company inherits the written down value of the transferor for

the purposes of the company’s future Division 40 ITAA 1997 deductions.

Example

The company is deemed to have acquired the assets transferred at a cost base

pursuant to sections 122-200 & 40-345 ITAA 1997:

(i) Assets dealt with in accordance with section 122-200 ITAA 1997:

Goodwill nil

Debtors $225,000

(ii) Assets dealt with in accordance with section 40-345 ITAA 1997

Patents nil

Depreciable plant $200,000

(iii) Assets dealt with in accordance with section 70-90

Trading stock $300,000

A Practical Accounting Issue

One of the more practical risk issues for advisers is the accounting treatment of the

transfer vis a vis the taxation implications. For example, using the above example and

assuming that the company issues 4 million $1 shares, the accounting would be:

Dr Assets 4,000,000

Cr Issued capital 4,000,000

redchip lawyers | Restructuring & Rollovers | page 15

However, for example, the goodwill has a tax cost base of nil but a cost in the

accounting records of $2m.

Note: Ensure that the company and the shareholder records note the taxation cost

base!!

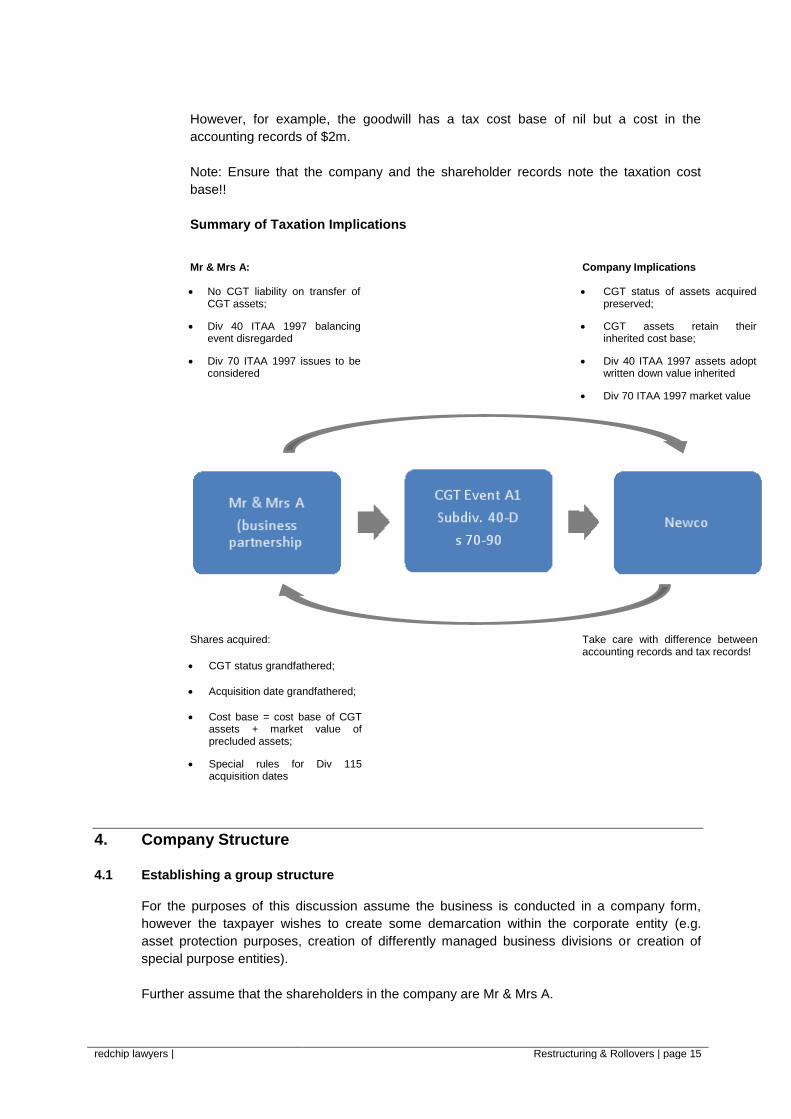

Summary of Taxation Implications

Mr & Mrs A: Company Implications

No CGT liability on transfer of CGT assets;

CGT status of assets acquired preserved;

Div 40 ITAA 1997 balancing event disregarded

CGT assets retain their inherited cost base;

Div 70 ITAA 1997 issues to be considered

Div 40 ITAA 1997 assets adopt written down value inherited

Div 70 ITAA 1997 market value

4. Company Structure

4.1 Establishing a group structure

For the purposes of this discussion assume the business is conducted in a company form,

however the taxpayer wishes to create some demarcation within the corporate entity (e.g.

asset protection purposes, creation of differently managed business divisions or creation of

special purpose entities).

Further assume that the shareholders in the company are Mr & Mrs A.

Shares acquired: Take care with difference between accounting records and tax records!

CGT status grandfathered;

Acquisition date grandfathered;

Cost base = cost base of CGT assets + market value of precluded assets;

Special rules for Div 115 acquisition dates

redchip lawyers | Restructuring & Rollovers | page 16

4.2 Strategy 1 – Use Rollover Provisions to Interpose a New Holding Company

This strategy uses the new business restructure rules in Division 615 ITAA 1997 to create a

holding company subsidiary structure.

[Note] Unit trust conversion:

Division 615 ITAA 1997 also applies to the either the interposition of a holding company or

exchanging units in a unit trust for shares in a new company.

It is possible to convert a unit trust structure to a company structure by using Subdivision 124-

N ITAA 1997 – all assets must be transferred to the company and the trust must come to an

end within 6 months.

A feature of Division 615 ITAA 1997 is that there is, inter alia:

(a) A retention of CGT status;

(b) No cost base uplift;

(c) No transfer duty or GST issues.

Subsequent to the above restructure steps, the head company can then elect to form a tax

consolidated group and then restructure asset ownership using the “single entity” rule to

mitigate any tax consequences of transfer of assets within the group.

Diagrammatically:

Step 1 – Starting Structure Matters to Consider

Note:

The same result can be achieved by using Subdivision 124-M ITAA 1997 if there is only one shareholder

Step 2 – Insert Holding Company

Shareholders of Trading Co transfer their shares to Hold Co in exchange for shares in Hold Co

redchip lawyers | Restructuring & Rollovers | page 17

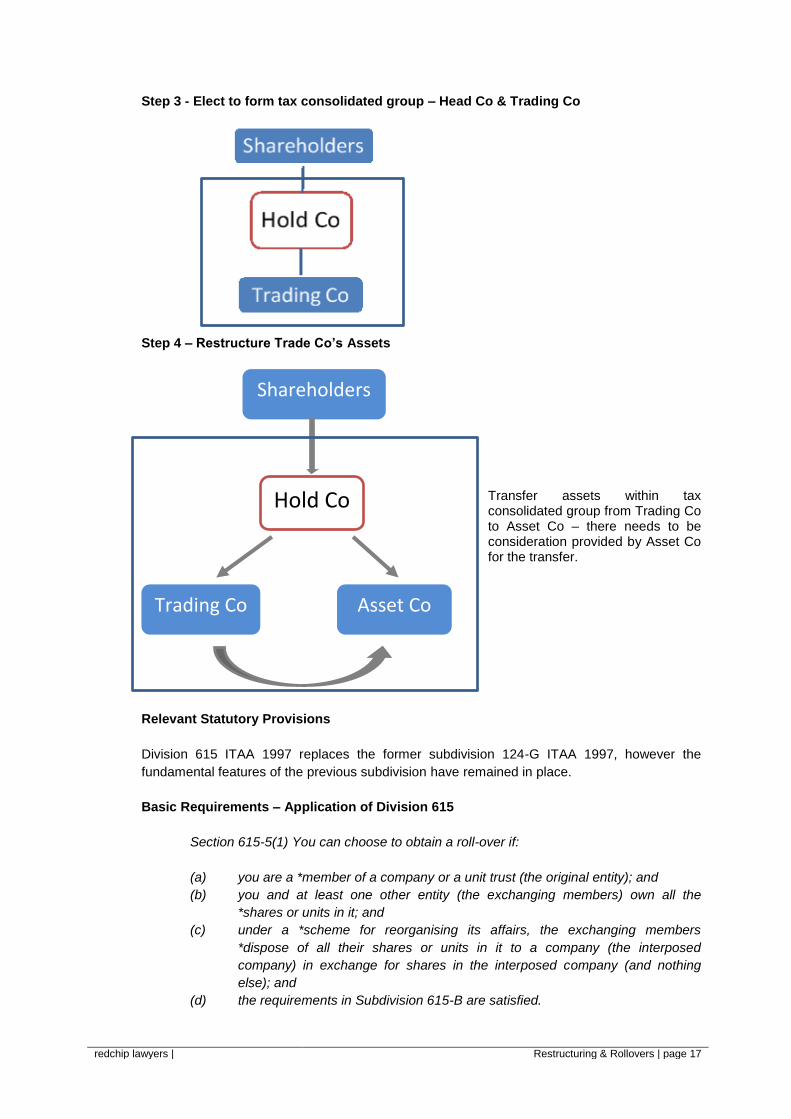

Step 3 - Elect to form tax consolidated group – Head Co & Trading Co

Step 4 – Restructure Trade Co’s Assets

Transfer assets within tax consolidated group from Trading Co to Asset Co – there needs to be consideration provided by Asset Co for the transfer.

Relevant Statutory Provisions

Division 615 ITAA 1997 replaces the former subdivision 124-G ITAA 1997, however the

fundamental features of the previous subdivision have remained in place.

Basic Requirements – Application of Division 615

Section 615-5(1) You can choose to obtain a roll-over if:

(a) you are a *member of a company or a unit trust (the original entity); and

(b) you and at least one other entity (the exchanging members) own all the

*shares or units in it; and

(c) under a *scheme for reorganising its affairs, the exchanging members

*dispose of all their shares or units in it to a company (the interposed

company) in exchange for shares in the interposed company (and nothing

else); and

(d) the requirements in Subdivision 615-B are satisfied.

Shareholders

Hold Co

Trading Co Asset Co

redchip lawyers | Restructuring & Rollovers | page 18

This particular rollover provision requires the following principal features:

(a) At least two shareholders in the original company (it can also apply to a unit holder in a

unit trust); and

(b) There is an exchange of shares in one company for shares in another company with

no change in relevant interests or value.

Note: If there is only one shareholder consider the use of Subdivision 124-M ITAA 1997 “scrip

for scrip” rollover as an alternative.

The Subdivision 615-B ITAA 1997 requirements are:

(a) The interposed company must own all of the shares in the original company

immediately after the exchange (section 615-15 ITAA 1997);

(b) The exchanging shareholders must own all of the shares in the interposed entity

immediately after the exchange, with no change in proportionality or market value in

exchanged interests (section 615-20 ITAA 1997);

(c) The shares issued in the interposed company must not be redeemable shares (section

615-25 ITAA 1997); and

(d) The interposed entity must make the choice to apply the rollover concession.

Taxation Consequences:

Shareholder

The consequences of the Division 615 ITAA 1997 rollover for the shareholders in the original

company are outlined in section 615-40 ITAA 1997:

Section 615-40 The consequences set out in Subdivision 124-A also apply to a roll-

over under this Division as if that roll-over were a roll-over covered by Division 124

(about replacement-asset roll-overs).

Note:

Those consequences generally involve:

(a) disregarding a capital gain or capital loss you make from the disposal,

redemption or cancellation of your shares or units in the original entity; and

(b) working out the first element of the cost base of each of your new shares in

the interposed entity by reference to the cost bases of your shares or units in

the original entity.

Interposed Entity

The consequences for the interposed company are outlined by section 615-65 ITAA 1997:

Pre CGT shares in original company

615-65(2) A number of the *shares or units that the interposed company owns in the

original entity (immediately after the completion time) are taken to have been *acquired

redchip lawyers | Restructuring & Rollovers | page 19

before 20 September 1985 if any of the original entity’s assets as at the completion

time were acquired by it before that day.

615-65(3) That number (worked out as at the completion time) is the greatest possible

whole number that (when expressed as a percentage of all the *shares or units) does

not exceed:

(a) the *market value of the original entity’s assets that it *acquired before 20

September 1985; less

(b) its liabilities (if any) in respect of those assets;

expressed as a percentage of the market value of all the original entity’s assets less all

of its liabilities.

Post CGT shares in the original company

615-65(4) The first element of the *cost base of the interposed company’s *shares or

units in the original entity that are not taken to have been *acquired before 20

September 1985 is:

(i) the total of the cost bases (as at the completion time) of the original

entity’s assets that it acquired on or after that day; less

(ii) its liabilities (if any) in respect of those assets.

The first element of the *reduced cost base of those shares or units is worked out

similarly.

615-65(5) A liability of the original entity that is not a liability in respect of a specific

asset or assets of the original entity is taken to be a liability in respect of all the assets

of the original entity.

Note:

An example is a bank overdraft.

615-65(6) If a liability is in respect of 2 or more assets, the proportion of the liability

that is in respect of any one of those assets is equal to:

The *market value of the asset

Total market value of all the assets that the liability is in respect of

4.3 Strategy 2 - Utilise the Division 152 Concessions to Obtain a Cost Base Uplift and Then

Consolidate

Cost Uplifting Strategy

Using the same facts as before:

(a) The shares in the target entity are owned by Mr & Mrs A equally;

(b) The acquisition of the shares was a consequence of the previous subdivision 122-B

rollover (the shares will have a cost base of $2.025 million); and

(c) The shareholders can satisfy the $6M Maximum Net Asset Value Test (“MNAV”).

redchip lawyers | Restructuring & Rollovers | page 20

With these facts and assumptions based on a tax planning motive, the strategy would include

the following steps:

(a) Mr & Mrs A establish a newly private company (“Newco”) with shares issued in the

company held by a discretionary trusts (should elect to be a family trust);

(b) Newco acquires the shares from Mr & Mrs A for full consideration being the market

value of the shares ($4 million). The consideration will be effected by vendor financing

in the first instance;

(c) Mr & Mrs A have a capital gain of $1.975 million which can be reduced by:

(i) Division 115 ITAA 1997 – as the shares have been held for more than 12

months – $987,500 reduction;

(ii) The Division 152 ITAA 1997 concessions if the shares are active assets (refer

to section 152-40(3) ITAA 1997 – if 80% of the company’s assets are active,

the shares will be active) – the shares will be active in this instance;

(iii) Mr & Mrs A can utilise Subdivision 152-C ITAA 1997 - $493,750 reduction; and

(iv) Mr & Mrs A can utilise Subdivision 152-D ITAA 1997 if they contribute

$493,750 into superannuation (i.e. $246,875 each) or alternatively apply

Subdivision 152-E ITAA 1997 and defer the contribution time by two years

(CGT Event J5 will occur).

(d) Newco wholly owns all of the shares and accordingly can form a consolidated group.

Newco has paid $4 million for the shares in the target entity. The cost to acquire the

membership interests (i.e. the shares) of $4 million will be the ACA (section 705-60

ITAA 1997) which is then allocated over the assets in the target entity;

(e) The ACA is allocated over the various assets which will result in the cost base of the IP

being reset at $1 million and depreciable plant at $500,000; and

(f) Newco borrows $493,750 either immediately or upon the happening of CGT J5 Event

and repays some part of the vendor finance to be used by Mr & Mrs A to contribute to

superannuation (noting the timing periods that must be satisfied to access the

Subdivision 152-D ITAA 1997).

The above strategy provides a much better outcome for Mr & Mrs A.

4.4 The Versatility of Division 615 ITAA 1997

The CGT rollover provisions in Division 615 ITAA 1997 are a versatile tool for restructuring

your client’s affairs in instances which are more complex that the above simple example of Mr

& Mrs A.

Although the rollover is typically applied to facilitate a tax-free interposition of a holding

company between shareholders and a specific company, the provisions can also be used to

amalgamate multiple companies under a single holding company.

Consider the following scenario recently illustrated in redchip’s recent Tax Bulletin written by

Mark Lowis:

redchip lawyers | Restructuring & Rollovers | page 21

(a) Stephen holds 60% of the ordinary shares in Trading Co Pty Ltd, IP Company Pty and

Staff Pty Ltd.

(b) Marty owns 40% of the ordinary shares in the corresponding companies.

(c) Stephen and Marty incorporate Holding Co Pty Ltd, issuing shares to themselves.

(d) Holding Co Pty Ltd agrees to issue shares in Holding Co Pty Ltd to Stephen and Marty

to bring them up to their 60/40 proportions in exchange for Stephen and Marty’s shares

in all three companies.

(e) Stephen and Marty now hold all of the shares in Holding Co Pty Ltd in their original

proportions.

(f) Trading Co Pty Ltd, IP Company Pty Ltd and Staff Pty Ltd are now wholly owned

subsidiaries of Holding Co Pty Ltd.

Before

After

This strategy may be particularly useful where a client with multiple corporate structures would

be better served by centralising their ultimate shareholding (e.g. administrative burden, costs).

If applied correctly, Stephen and Marty’s shares in Holding Co Pty Ltd will acquire an averaged

cost CGT base equivalent to the cost bases of the shares exchanged – thereby rolling over any

CGT liability which would have otherwise arisen.

The provisions strategy fundamentally requires:

(a) That there are more than one shareholder in each of the companies;

redchip lawyers | Restructuring & Rollovers | page 22

(b) That the proportional shareholdings in each of the original companies before the

interposition occurs are identical, and

(c) That the proportionate market value of the shareholdings for each shareholder are the

same as the original companies

A summary of the Commissioner of Taxation’s views and his endorsement of this particular

strategy and many others can be found within Taxation Ruling TR 97/18. Principally the

notion embraced by the Commissioner (albeit in relation to an earlier version of Division 615

ITAA 1997):

10. It is readily observed that if there is a reorganisation of the affairs of a wholly

owned group/conglomerate by reconfiguring the group under two main operating

companies, there occur changes in cross holdings between each related company but

no change in the overall economic ownership of the underlying assets within the

group. This type of arrangement is common commercial practice and not offensive to

the roll-over provisions of section 160ZZO.

5. Conversion of a Unit Trust to a Company

Finally, the ITAA 1997 provides an opportunity to convert a unit trust into a company.

Subdivision 124-N ITAA 1997 is essentially a more sophisticated version of Subdivision 122-A

1997. Whilst Subdivision 122-A ITAA 1997 allows assets held by a trust to be transferred to a

company where the consideration provided by the transferee is shares in the company, the

trust becomes a shareholder.

Subdivision 124-N ITAA 1997, however, has a multi-faceted rollover for a unit trust (not a

discretionary trust):

(a) Assets of the unit trust are transferred to a company;

(b) The unit holders are entitled to shares in the company, without any change in the

market value or proportionate interest in the company; and

(c) The unit trust is vested within a 6 month period of the first CGT event attributable to the

restructure (otherwise CGT Event J4 will apply).

Ultimately what Subdivision 124-N ITAA 1997 provides is:

(a) A new company can be established to hold the assets of the unit trust;

(b) The unit holders interests are converted to a shareholding interest in the transferee

company; and

(c) The trust ceases to exist.

Whilst this subdivision provides CGT relief, there are transfer duty issues to consider.

Statute (Subdivision 124-N ITAA 1997)

Section 124.855 ITAA 1997 provides the broad parameters:

(1) A roll-over may be available for a restructuring (a trust restructure) if:

redchip lawyers | Restructuring & Rollovers | page 23

(a) a trust, or 2 or more trusts, (the transferor) *dispose of all of their

*CGT assets to a company limited by * shares (the transferee); and

(b) CGT event E4 is capable of applying to all of the units and interests in

the transferor; and

(c) the requirements in section 124-860 are met.

Note: A roll-over is not available for a restructure undertaken by a discretionary

trust.

(2) For 2 or more transferors, units and interests in each transferor must be

owned in the same proportions by the same beneficiaries.

Matthew and Jaclyn each own 50% of the units in the Spring Unit Trust and

the Dale Unit trust. All of the assets of both trusts are disposed of to Jonathon

Pty Ltd. A roll-over for a trust restructure is available if the other requirements

of this Subdivision are met.

More particularly, the specific requirements to access the concessions are outlined in section

124-860 ITAA 1997:

Requirements for roll-over

(1) All of the *CGT assets owned by the transferor must be disposed of to the

transferee during the *trust restructuring period. However, ignore any CGT

assets retained by the transferor to pay existing or expected debts of the

transferor.

(2) The trust restructuring period for a trust restructure:

(a) starts just before the first *CGT asset is *disposed of to the transferee

under the trust restructure, which must happen on or after 11

November 1999; and

(b) ends when the last CGT asset of the transferor is disposed of to the

transferee.

(3) The transferee must not be an *exempt entity.

(4) The transferee must be a company that:

(a) has never carried on commercial activities; and

(b) has no *CGT assets, other than any or all of the following:

(i) small amounts of cash or debt;

(ii) its rights under an *arrangement, if (collectively) those rights

only facilitate the transfer of assets to the transferee from the

transferor; and

(c) has no losses of any kind.

Example: It could be a shelf company.

redchip lawyers | Restructuring & Rollovers | page 24

(5) Subsection (4) does not apply to a transferee that is the trustee of the

transferor.

(6) Just after the end of the *trust restructuring period:

(a) each entity that owned interests in a transferor just before the start of

the trust restructuring period must own replacement interests in the

transferee in the same proportion as it owned those interests in that

transferor; and

(b) the *market value of the replacement interests each of those entities

owns in the transferee must be at least substantially the same as the

market value of the interests it owned in the transferor or transferors

just before the start of the trust restructuring period.

Note 1: Any assets in the company just before the start of the trust

restructuring period may affect the ability of owners of units or

interests to comply with paragraph (6)(b).

Note 2: See section 124-20 if an entity uses an interest sale facility.

(7) For the purposes of subsection (6), ignore any *shares in the transferee that:

(a) just before the start of the *trust restructuring period, were owned by

entities who together owned no more than 5 shares; and

(b) just after the end of that period, represented such a low percentage of

the total *market value of all the shares that it is reasonable to treat

other entities as if they owned all the shares in the transferee.

Example: To continue the example in subsection 124- 855(2), assume that Jonathon

Pty Ltd was a shelf company organised for Matthew and Jaclyn by their solicitor,

Indira.

Indira owned the 2 shares in Jonathon Pty Ltd before the trust restructuring period.

The company issues Matthew and Jaclyn 5,000 shares each.

In these circumstances, it is reasonable to treat Matthew and Jaclyn as if they owned

all the shares in Jonathon Pty Ltd.

In summary the consequences of choosing the rollover are:

(a) Section 124-870 ITAA 1997 - the taxpayer can choose the application of the roll-over in

relation to their units (or interests in a trust) where they exchange their trust interests

for shares. The taxation consequences are provided by subdivision 124-A ITAA 1997.

Note:

(i) The effect of the roll-over may be reversed if the transferor does not cease to

exist within 6 months: see section 104-195.

(ii) There are limits on non-resident unitholders)

redchip lawyers | Restructuring & Rollovers | page 25

(b) Section 124-875 ITAA 1997 provides that:

(i) any CGT gain attributable to the exchange of trust interests to shares is

disregarded;

(ii) Cost base of the transferor is “inherited” by the transferee; and

(iii) Pre-CGT assets retain their status.

redchip lawyers | Restructuring & Rollovers | page 26

Part IVA ITAA 1936 Case Study

Presenter: Mark Lowis, Associate, redchip lawyers

1. Track and Ors V Commissioner of Taxation - Why Part IVA ITAA 1936

Needs To Be Considered

The recent decision of Track and Ors v Commissioner of Taxation [2015] AATA 45

(Track’s Case) is a timely reminder of the serious impact that Part IVA of the Income Tax

Assessment Act 1936 (Cth) (ITAA 1936) can have on restructures.

The case comprised eight applications to the Administrative Appeals Tribunal (AAT) regarding

amended assessments issued by the Commissioner for capital gains made by the trustee of a

hybrid unit trust when it sold business assets for over $8M in July 2005.

The case is particularly interesting within the context of our seminar and offers an opportunity

to reflect upon our roles as advisers when a restructure is proposed and how that restructure is

to be carried out.

1.1 Facts

The primary facts in Track’s Case are relatively complex. It will be useful to recount them

chronologically, highlighting the various changes to the business structure as they took place.

Michael Track (Michael) and Arnold Track (Arnold) started a cane harvester repair and

operations business in or around 1988. The brothers were fitters by trade and as their repair

business grew, they developed an expertise in fabricating parts for harvesters.

This business was conducted by Track Bros Pty Ltd.

Their growing interest and expertise in plastic fabrication lead them to investigate rotational

plastic moulding methods. After a while, the business of manufacturing and selling plastic

moulded tanks became lucrative.

By the mid 1990’s the Track brothers wished to expand the business by bringing in additional

management and investment. Mr James Patrick (James), a long term employee of Track Bros

Pty Ltd invested in the business. Mr Carter Ford (Carter), the manager of the trading bank

where Track Bros Pty Ltd conducted its accounts also invested in the business.

Michael, Arnold, James and Carter where the “Principals” in this new venture of manufacturing

plastic water tanks.

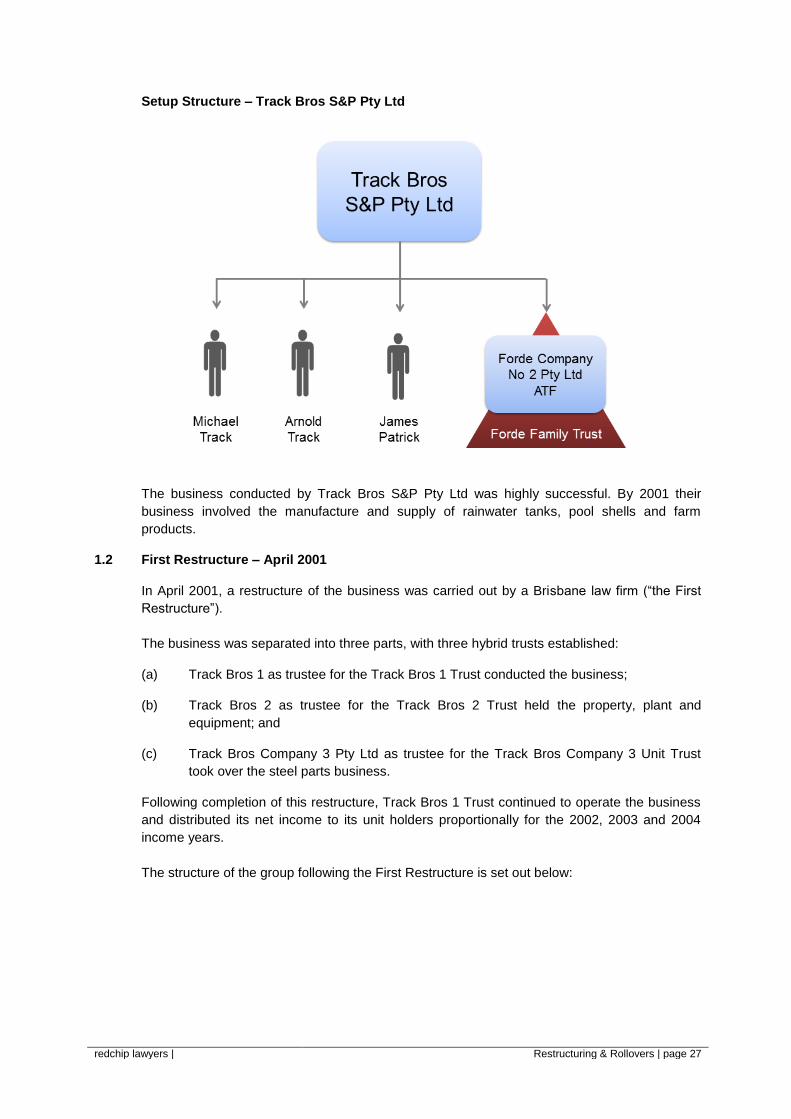

In 1996, the structure of this new venture was as follows: -

redchip lawyers | Restructuring & Rollovers | page 27

Setup Structure – Track Bros S&P Pty Ltd

The business conducted by Track Bros S&P Pty Ltd was highly successful. By 2001 their

business involved the manufacture and supply of rainwater tanks, pool shells and farm

products.

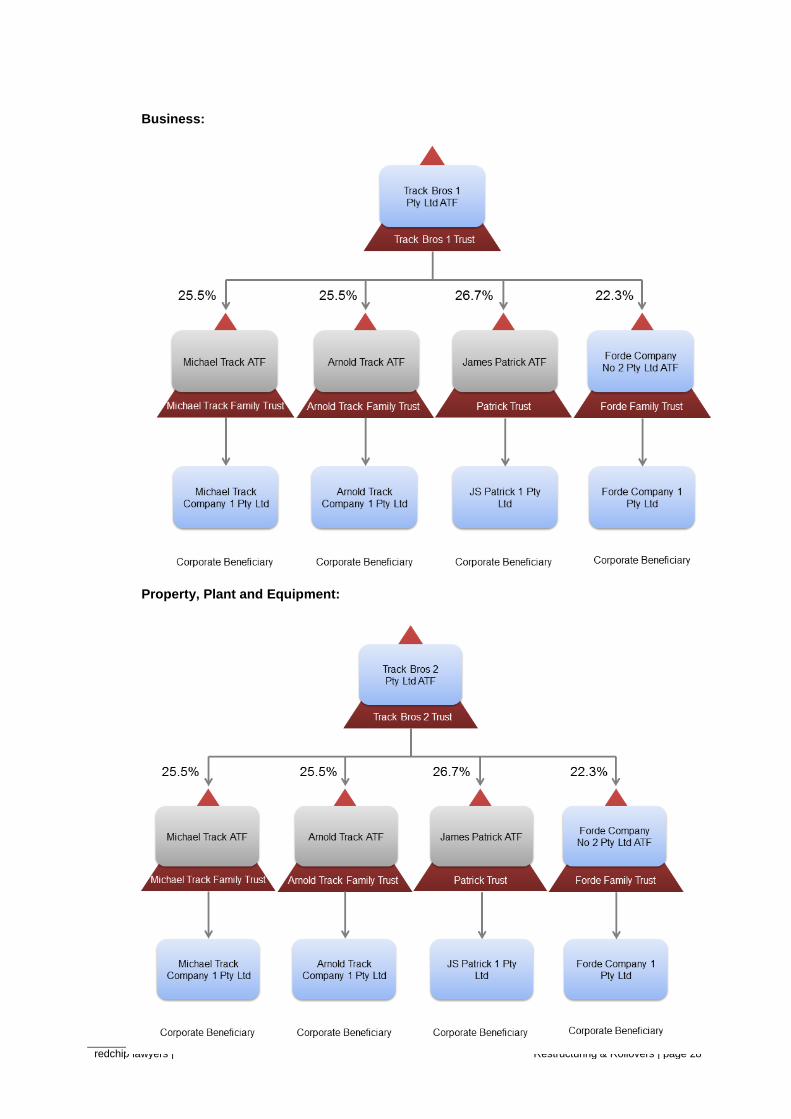

1.2 First Restructure – April 2001

In April 2001, a restructure of the business was carried out by a Brisbane law firm (“the First

Restructure”).

The business was separated into three parts, with three hybrid trusts established:

(a) Track Bros 1 as trustee for the Track Bros 1 Trust conducted the business;

(b) Track Bros 2 as trustee for the Track Bros 2 Trust held the property, plant and

equipment; and

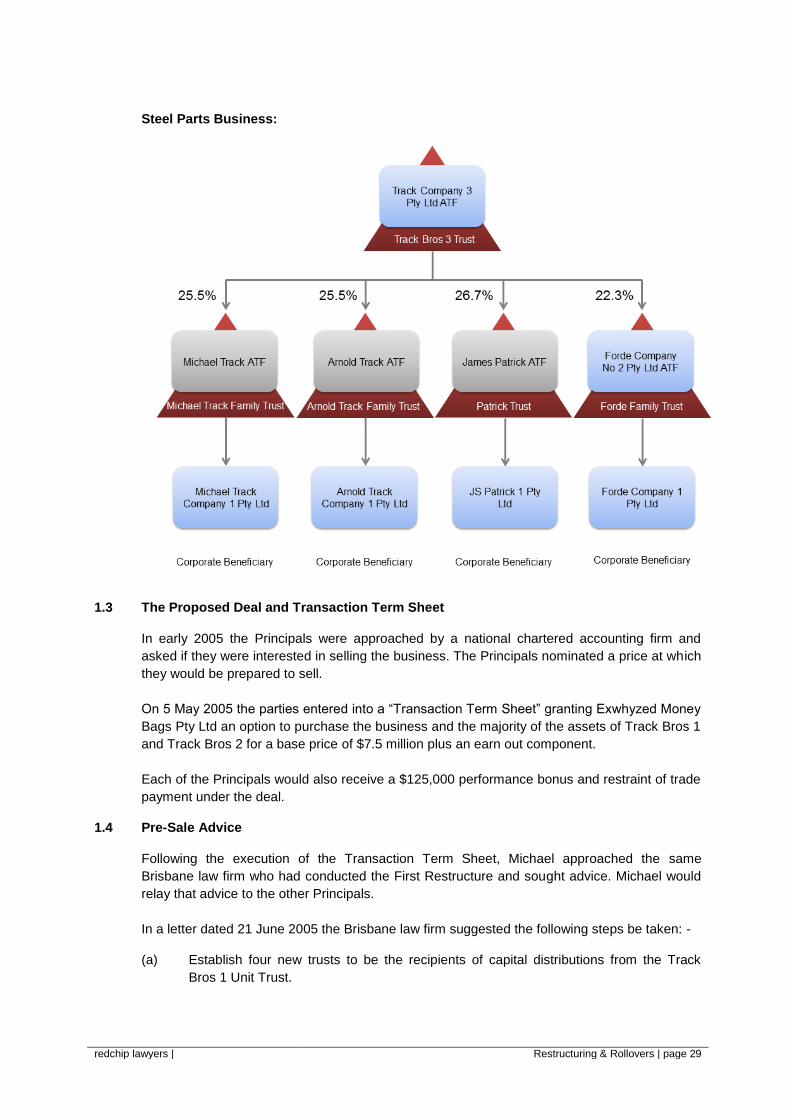

(c) Track Bros Company 3 Pty Ltd as trustee for the Track Bros Company 3 Unit Trust

took over the steel parts business.

Following completion of this restructure, Track Bros 1 Trust continued to operate the business

and distributed its net income to its unit holders proportionally for the 2002, 2003 and 2004

income years.

The structure of the group following the First Restructure is set out below:

redchip lawyers | Restructuring & Rollovers | page 28

Business:

Property, Plant and Equipment:

redchip lawyers | Restructuring & Rollovers | page 29

Steel Parts Business:

1.3 The Proposed Deal and Transaction Term Sheet

In early 2005 the Principals were approached by a national chartered accounting firm and

asked if they were interested in selling the business. The Principals nominated a price at which

they would be prepared to sell.

On 5 May 2005 the parties entered into a “Transaction Term Sheet” granting Exwhyzed Money

Bags Pty Ltd an option to purchase the business and the majority of the assets of Track Bros 1

and Track Bros 2 for a base price of $7.5 million plus an earn out component.

Each of the Principals would also receive a $125,000 performance bonus and restraint of trade

payment under the deal.

1.4 Pre-Sale Advice

Following the execution of the Transaction Term Sheet, Michael approached the same

Brisbane law firm who had conducted the First Restructure and sought advice. Michael would

relay that advice to the other Principals.

In a letter dated 21 June 2005 the Brisbane law firm suggested the following steps be taken: -

(a) Establish four new trusts to be the recipients of capital distributions from the Track

Bros 1 Unit Trust.

redchip lawyers | Restructuring & Rollovers | page 30

(b) Track Bros 1 Unit Trust make proportional distributions to the new trust (equal to the

cash, term deposits and loans owing by entities such as the trustee of Track Bros 2

Unit Trust).

(c) Have the related entities repay the loans and amounts owing to Track Bros 1 Unit

Trust.

(d) Have the new Trusts loan back funds to Track Bros 1 Unit Trust under security.

1.5 The Second Restructure

The parties adopted the advice and the following actions were carried out: -

(a) Four new “protection” trusts were established for the benefit of each of the Principals

(see below);

(b) Track Bros 1 redeemed call deposit in its name and deposited the proceeds of

$1,002,660.37 into its bank account;

(c) In partial satisfaction of the resolution to make the “discretionary distribution”, cheques

totalling $1,000,000 were drawn in favour of each of the protection trusts as follows: -

(i) Michael Track Protection Trust $255,000;

(ii) Arnold Track Protection Trust $255,000;

(iii) JS Patrick Protection Trust $267,000;

(iv) Ford Protection Trust $223,000.

redchip lawyers | Restructuring & Rollovers | page 31

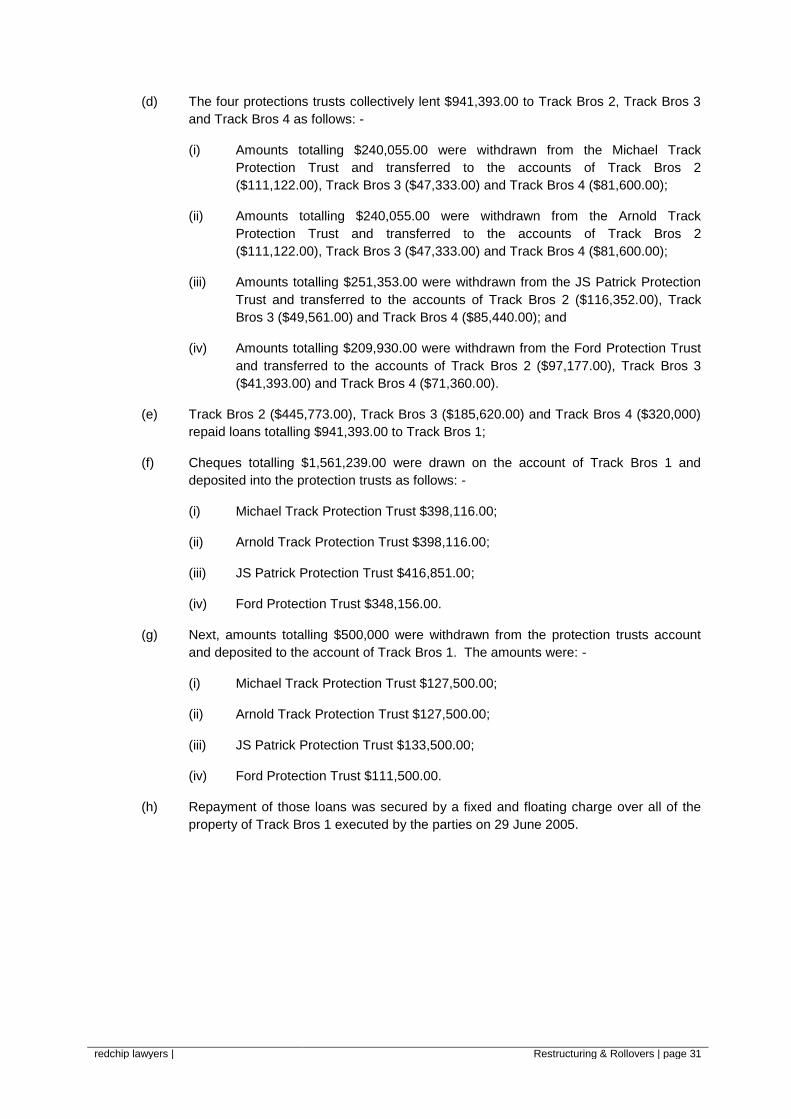

(d) The four protections trusts collectively lent $941,393.00 to Track Bros 2, Track Bros 3

and Track Bros 4 as follows: -

(i) Amounts totalling $240,055.00 were withdrawn from the Michael Track

Protection Trust and transferred to the accounts of Track Bros 2

($111,122.00), Track Bros 3 ($47,333.00) and Track Bros 4 ($81,600.00);

(ii) Amounts totalling $240,055.00 were withdrawn from the Arnold Track

Protection Trust and transferred to the accounts of Track Bros 2

($111,122.00), Track Bros 3 ($47,333.00) and Track Bros 4 ($81,600.00);

(iii) Amounts totalling $251,353.00 were withdrawn from the JS Patrick Protection

Trust and transferred to the accounts of Track Bros 2 ($116,352.00), Track

Bros 3 ($49,561.00) and Track Bros 4 ($85,440.00); and

(iv) Amounts totalling $209,930.00 were withdrawn from the Ford Protection Trust

and transferred to the accounts of Track Bros 2 ($97,177.00), Track Bros 3

($41,393.00) and Track Bros 4 ($71,360.00).

(e) Track Bros 2 ($445,773.00), Track Bros 3 ($185,620.00) and Track Bros 4 ($320,000)

repaid loans totalling $941,393.00 to Track Bros 1;

(f) Cheques totalling $1,561,239.00 were drawn on the account of Track Bros 1 and

deposited into the protection trusts as follows: -

(i) Michael Track Protection Trust $398,116.00;

(ii) Arnold Track Protection Trust $398,116.00;

(iii) JS Patrick Protection Trust $416,851.00;

(iv) Ford Protection Trust $348,156.00.

(g) Next, amounts totalling $500,000 were withdrawn from the protection trusts account

and deposited to the account of Track Bros 1. The amounts were: -

(i) Michael Track Protection Trust $127,500.00;

(ii) Arnold Track Protection Trust $127,500.00;

(iii) JS Patrick Protection Trust $133,500.00;

(iv) Ford Protection Trust $111,500.00.

(h) Repayment of those loans was secured by a fixed and floating charge over all of the

property of Track Bros 1 executed by the parties on 29 June 2005.

redchip lawyers | Restructuring & Rollovers | page 32

1.6 The Purchase of the Business Assets

The option granted by the Transaction Term Sheet was not exercised within the required time,

however, the parties remain prepared to contract.

On 1 July 2005 Track Bros 1 and Track Bros 2 as vendors, entered into a Business Sale

Agreement with Oz Fluid Systems Pty Ltd for the sale of the tank manufacturing business and

associated plant and equipment. Each of the Principals were party to the Deed, and they

undertook particular obligations including binding themselves to restraint of trade clauses and

assuming personal liability for some continuing product liability.

The purchase price was $8,000,000.00 plus or minus an adjustment amount.

The net proceeds of sale ($8,159,808.20) were credited to the bank account to Track Bros 1 on

8 July 2005.

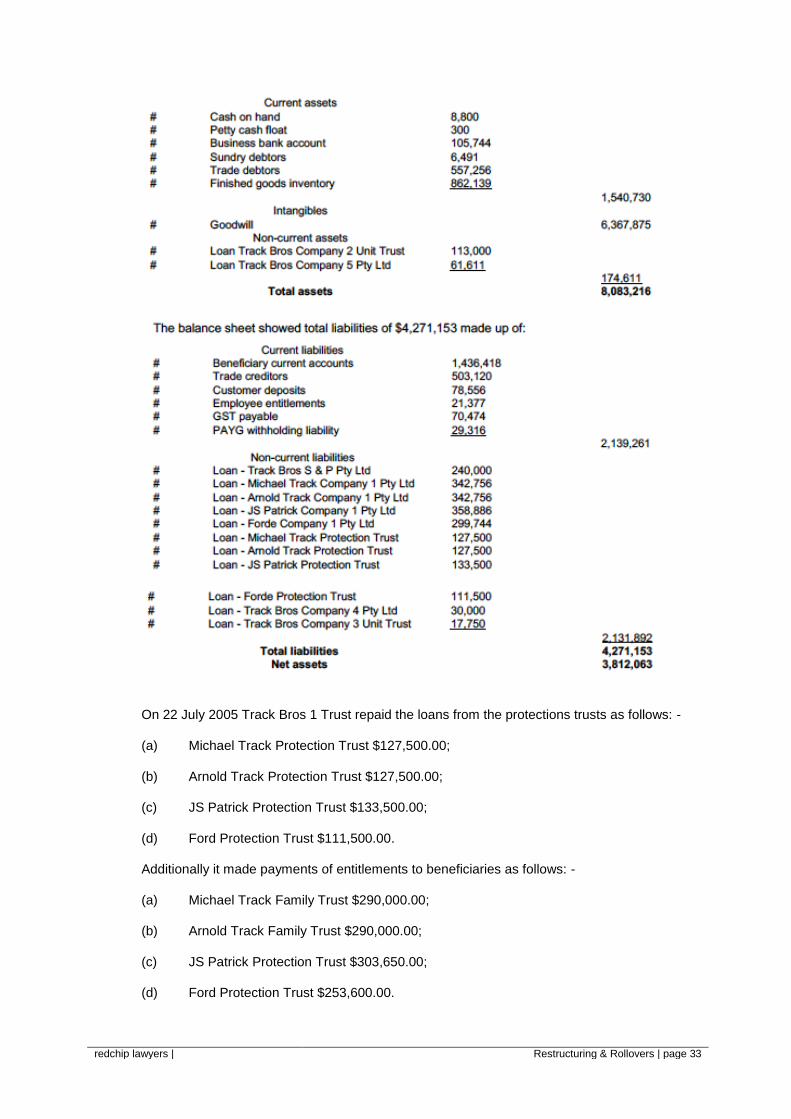

Immediately prior to the sale the net value of the assets of Track Bros 1 Trust were recorded

as $3,812,063.00.

The balance sheet for Track Bros 1 at 30 June 2005 (the day before the CGT event) is set out

below:

redchip lawyers | Restructuring & Rollovers | page 33

On 22 July 2005 Track Bros 1 Trust repaid the loans from the protections trusts as follows: -

(a) Michael Track Protection Trust $127,500.00;

(b) Arnold Track Protection Trust $127,500.00;

(c) JS Patrick Protection Trust $133,500.00;

(d) Ford Protection Trust $111,500.00.

Additionally it made payments of entitlements to beneficiaries as follows: -

(a) Michael Track Family Trust $290,000.00;

(b) Arnold Track Family Trust $290,000.00;

(c) JS Patrick Protection Trust $303,650.00;

(d) Ford Protection Trust $253,600.00.

redchip lawyers | Restructuring & Rollovers | page 34

1.7 Tax Returns and Amended Assessments

On 15 June 2006 Track Bros 1 Trust paid eligible termination payments (ETPs) of $500,000 to

James and Carter.

Track Bros 1 as trustee for Track Bros 1 Trust reported a net income of $146,652 and net

capital gain of $460,101 in its 2005/2006 tax return. The net capital gain was calculated by

reducing the gross capital gain of $5.8m by the Division 115 ITAA 1997 50% discount,

Subdivision 152-C ITAA 1997 50% Active Asset reduction and the Subdivision 152-D ITAA

1997 $1M ETP paid.

The Commissioner determined that Part IVA ITAA 1936 applied and he issued amended

assessments to all eight taxpayers increasing their taxable incomes in accordance with their

unit holdings and imposing scheme shortfall penalties of 50%.

The taxpayers all objected to the amended assessments, the objections were disallowed, and

the taxpayers applied to the AAT.

1.8 Contentious Issues

There were two main issues in contention:

(a) Was Track Bros 1 eligible for the small business CGT concessions provided for by

Subdivision 152-C and 152-B of ITAA 1997?

(b) Do the anti-avoidance provisions contained in Part IVA ITAA 1936 operate to cancel

tax benefits obtained in connection with the scheme?

The first issue turned on whether Track Bros 1 satisfied the maximum net asset value (MNAV)

test which itself turned upon whether certain liabilities of Track Bros 1 were “related to” assets

of that trust.

The Commissioner contended that the scheme had the object of enabling access to the small

business CGT concessions by reducing the trust’s assets and increasing its liabilities to ensure

that the trust’s net assets at the time of sale were less than $5M.

Furthermore, it was argued that had the arrangements not been entered into, Track Bros 1

would have been assessed on the entire capital gain, which it would reasonably have

distributed to the family trusts, who would then have distributed it to their beneficiaries in the

same fashion as previous years.

Track Bros 1 had lodged its 2006 trust return on the footing that it satisfied the MNAV test.

However, the taxpayers argued that:

(a) Track Bros 1 did not satisfy the MNAV test as certain categories of the trust’s liabilities

were not “related to” its assets. On this reasoning, there was no tax benefit evident on

the Commissioner’s alternative postulate as Track Bros failed the MNAV test either

way.

(b) the Commissioner’s alternative postulate was unreasonable as, had the arrangements

not been implemented, no asset protection would have been achieved.

redchip lawyers | Restructuring & Rollovers | page 35

(c) it was not reasonable to assume that the capital gain would have been distributed by

the family trusts to any corporate beneficiaries given that those beneficiaries could not

access the general 50% CGT discount.

The Commissioner later conceded at the hearing that the amended assessments pertaining to

the second and eighth taxpayers were made outside of the time limits permitted and that those

objection decisions should thus be set aside.

The taxpayers accepted that the arrangements satisfied the definition of a “scheme” for Part

IVA ITAA 1936.

1.9 Decision

It was held by Deputy President Hack that:

(a) The relevant liabilities (including unpaid present entitlements) were “related to” the

CGT assets of the trust. Whilst both parties relied on the decision of Bell v

Commissioner of Taxation [2013] FCA 1042 (Bell’s Case) that case was

distinguishable from the current case on the basis that it was not clear in this instance

that the cash represented the borrowing to fund the capital distributions made.

(b) The taxpayers failed to prove that Track Bros 1 did not satisfy the MNAV test –

therefore, the arrangements carried out to satisfy the MNAV test were effective.

(c) The taxpayers failed to explain as to how any of the steps in the scheme effected asset

protection and their evidence supporting a need for asset protection was unconvincing.

(d) The complexity of the scheme pointed to the purpose of obtaining a tax benefit, and

the timing of the distributions pointed to the purpose of meeting the CGT concession

threshold.

(e) The scheme was entered into for the purpose of obtaining a tax benefit – Track Bros

1’s capital gain was reduced from $2,920,202 to $460,101.

(f) The distribution of trust income in prior years from Track Bros 1 was not a reliable

indicator of how capital gains would have been distributed. In circumstances where

corporate beneficiaries were not able to access the discount, it was not reasonable to

expect that any of the distributions from Track Bros 1 to the family trusts would have

been distributed to corporate beneficiaries. This was reinforced by the distributions that

actually took place. None of the corporate beneficiaries received a tax benefit and so

Part IVA ITAA 1936 did not apply to them.

(g) In respect to the individual beneficiaries, it was reasonable to postulate that the

distributions would have been made on the basis of the resolutions purportedly

prepared by the directors in 2006. Unlike the corporate beneficiaries, the natural

person beneficiaries did receive a tax benefit, which was cancelled by operation of Part

IVA ITAA 1936.

(h) In regard to penalties, the taxpayers’ position was not arguable. The transactions were

motivated by a desire to avoid tax, not protect assets. The scheme was not

“reasonably arguable”.

A transcript of Track’s Case (including a comprehensive account of the facts and arguments)

can be found at http://www.austlii.edu.au/au/cases/cth/AATA/2015/45.html.

redchip lawyers | Restructuring & Rollovers | page 36

1.10 Additional Aspects

There are some curiosities arising from the decision which are worthy of note:

(a) The AAT confirmed the emerging view since Bell’s Case that unpaid present

entitlements were liabilities for the purposes of the MNAV test, however, there was

discussion on the matter.

(b) The Commissioner did not take issue with the UPE being recorded in the accounts as

“loans” and did not level his well-worn arguments regarding the characterisation of

UPE. It is presumed that the Commissioner did not wish to support the striking down of

the liabilities – to do so would lend support to the taxpayer’s argument that they would

not have satisfied the MNAV test anyway (despite that argument being ultimately

rejected by the AAT).

(c) The AAT took a common sense approach in determining where the distributions of

capital gains would be made. As discussed above, the AAT found that, based on the

taxpayer’s assertions, in circumstances where corporate beneficiaries were not able to

access the discount, it was not reasonable to expect that any of the distributions would

have been made to corporate beneficiaries – the Track brothers would have taken

advice in this regard. The AAT found that this was reinforced by the distributions that

actually took place.

2. Broader Analysis of Part IVA ITAA 1936

2.1 Evolution of Framework

The central thrust of Part IVA ITAA 1936 is to strike down “blatant, artificial or contrived

arrangements” but not to not “cast unnecessary inhibitions on normal commercial transactions

by which taxpayers legitimately take advantage of opportunities available for the arrangement

of their affairs” (Second Reading Speech, Income Tax Laws Amendment Bill 1981).

This general anti-avoidance framework has been the Commissioner’s “go-to” weapon for many

years. Between 2007 and 2012, around 80 Part IVA ITAA 1936 cases were initiated by the

ATO.

The Commissioner was successful in applying Part IVA ITAA 1936 in those cases where he

demonstrated that the commercial viability of the scheme, as compared to a reasonable

alternative, is dependent on the tax outcome. Furthermore, the Commissioner was successful

where aspects of the scheme were not capable of commercial explanation.

However, the Commissioner began to lose ground where he attempted to apply Part IVA ITAA

1936 to certain internal group restructures1 or whenever there was a disparity between the

economic and tax outcomes of a scheme.2 Between 2010 and 2012, taxpayers were

successful in nine of the 15 Part IVA court cases. In several of these cases3 the Commissioner

failed to even establish that a “tax benefit” had arisen as each time the taxpayer demonstrated

that, but for the identified scheme, it would have done nothing or would have done something

that produced a tax outcome at least as favourable as the one achieved under the scheme.

1 See RCI Pty Ltd v FCT [2011] FCAFC 104; FCT v News Australia Holdings Pty Ltd [2010] FCAFC 78.

2 See AXA Asia Pacific Holdings Pty Ltd v FCT [2009] FCA 1427; FCT v BHP Billiton Finance Ltd [2010] FCAFC 25; FCT v

Ashwick (Qld) [2011] FCAFC 49. 3 See AXA Asia Pacific Holdings Pty Ltd v FCT [2009] FCA 1427, RCI Pty Ltd v FCT [2011] FCAFC 104; FCT v Futuris [2012]

FCAFC 32.

redchip lawyers | Restructuring & Rollovers | page 37

In an effort to overcome these difficulties, the Government enacted amendments to the regime

in February 2013.

Section 177CB ITAA 1936 now provides greater scope for the Commissioner to establish a tax

benefit by assessing the “alternative postulate” and deciding what would have, or might

reasonably be expected to have happened if the scheme had not been entered into or carried

out.

2.2 General Requirements – Part IVA

A comprehensive account of the Part IVA ITAA 1936 framework is outside the scope of this

paper. However, it is useful to recount the general high-level requirements.

There are three general elements to the operation of Part IVA ITAA 1936:

(a) Was there a “scheme”? (s177A(a) ITAA 1936) – which, given the broad definition, is

almost satisfied in any circumstances that Part IVA ITAA 1936 is raised.

(b) Was there a “tax benefit”? (s177CB ITAA 1936) – Generally speaking, the

Commissioner must compare his “alternative postulate” with the substance of what

actually took place from the taxpayer’s point of view.

The process to be followed by the Commissioner is:

(i) To identify a reasonable alternative to the scheme, but the alternative must

comprise only the event events or circumstances that actually happened or

existed (other than those that form part of the scheme) - the “Annihilation

Approach”; and

(ii) Consider an alternative postulate which is based on a reasonable construction

of what the taxpayer might have done if the scheme was not entered into –

the “Reconstruction Approach”

In determining a reasonable alternative postulate, the Commissioner must have

particular regard to the substance of the scheme and any result or consequence of it

for the taxpayer that is or would be achieved by the scheme (other than a result to the

operation of the Act). This essentially means that the alternative postulate formulated

must achieve the same commercial outcome for the taxpayer as the scheme.

The taxpayer is not be able to argue that the alternative postulate is not reasonable

because of the income tax costs of that postulate.