Languages

Pages

Legal

PRM CONSULTING GROUP, INC • 3206 TOWER OAKS BOULEVARD, SUITE 400 • ROCKVILLE, MD 20852 • 301.951.5104

Statewide Health Care Study:

Review of Findings

So What’s Next?

Date: March 11, 2016

Presented to: PASBO

Background

Senate Resolution 250 directed a study of

the feasibility and cost effectiveness of

merging public school district health

plans.

2

The study included medical, dental, vision, and prescription drug benefits and addresses eleven areas:

SR 250 Had 11 Study Areas

3

1. Analysis of the specific health benefits, policies and contracts provided by at least 50 percent of the school entities throughout the Commonwealth

2. Cost of current benefits for the next five years

3. Cost of current school employee contribution or average per employee.

4. Impact on PSERS and SERS

5. Comparison of coverage with average taxpayer in the relevant region.

6. Regionalization versus one health care plan.

7. Cost savings realized with consortia

8. Administrative, staffing, and technology costs associated with forming mergers.

9. Comparison of school employees with Commonwealth employees

10. Cost of least used benefits by school employees

11. Cost impact of Health Care Reform (PPACA)

Today I’ll focus on the findings from these 6

4

1. Analysis of the specific health benefits, policies and contracts provided by at least 50 percent of the school entities throughout the Commonwealth

2. Cost of current school employee contribution or average per employee

3. Comparison of coverage with average taxpayer in the relevant region

4. Comparison of school employees with Commonwealth employees

5. Regionalization versus savings from one state-wide health care plan

6. Cost impact of Health Care Reform (PPACA)

Following set of slides provide the findings on 1. and 2.

Analysis of School Health Benefit Plans

Information was gathered from a variety of sources, including school districts,

health care consortia, health insurance companies and interviews with key

stakeholders.

5

Data Provided

• The survey was administered to all 500 school districts

• Respondents provided copies of their CBAs, SPDs and health plan rates

• 27 of the 37 Consortia provided claims data for last 5 years

PA-taxpayer health insurance information

from:

• Aetna

• Capital Blue Cross

• Geisinger Health System

• Highmark Blue Cross Blue Shield

• Independence Blue Cross

Stakeholder interviews

• PEBTF

• PASBO

• PSEA

• PAIU

• PSERS

• SERS

• Philadelphia Federation of Teachers H&W Fund

• Department of Education

• State Board of Education

• Governor’s Office of Administration

• Pennsylvania Association of Health Underwriters

Survey Respondents

6

269 (54%) schools submitted responses

Key Findings

Most school districts obtain coverage through a consortium

Over 85% of schools participate in one of 37 Consortia

Consortia have experienced below average healthcare cost trends

Some are implementing novel cost-saving programs

7

Key Findings

8

25%

18%

4%5%

48%

EE only

EE + Spouse

EE + Child

EE + Children

EE + Family

88%

50%43%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Medical Dental Vision

Employee Contributions Required

$128

$106

$57

$0 $20 $40 $60 $80 $100 $120 $140

EE + Family

EE + Spouse

EE only

Average Monthly Medical Contribution

Key Findings

9

38%

57%

60%

85%

86%

86%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Grandfathered Plan

Dental coverage is self-insured

Vision coverage is self-insured

Medical coverage is self-insured

School districts participating in a consortium

Prescription Drugs included w/ Medical Plan

Medical Plan Designs

10

Percentiles 10% 25% Median 75% 90%

Summary across all plans, including plans with no deductibles

Individual coverage cost-sharing

In-Network Deductible $- $- $100 $350 $1,300

Out of Network Deductible $200 $250 $400 $700 $1,500

In Network Out-of-Pocket maximum $515 $1,888 $6,350 $6,350 unlimited

In Network Coinsurance 100% 100% 100% 100% 100%

Out of Network Coinsurance 100% 80% 80% 80% 70%

Summary across only plans with deductibles

In-Network Deductible $100 $231 $350 $713 $1,300

Out of Network Deductible $200 $250 $450 $700 $1,500

In Network Out-of-Pocket maximum $515 $1,888 $6,350 $6,350unlimite

d

Medical Plan Designs

11

Percentiles 10% 25% Median 75% 90%

Summary across all plans, including plans with no copays

Office Visits

Primary Care Physician $- $- $10 $20 $20Specialist $- $10 $20 $25 $30Emergency Room $- $- $35 $75 $100Routine Lab $- $- $- $- $10

Radiology $- $- $- $- $10Summary across only those plans with copays

Office Visits

Primary Care Physician $10 $10 $15 $20 $25

Specialist $10 $15 $20 $25 $30

Emergency Room $25 $35 $50 $100 $100

Routine Lab $10 $10 $15 $20 $21

Radiology $10 $10 $15 $20 $26

Hospital and Outpatient Copays

Hospital In Network Per Admission $22 $38 $100 $250 $365

Hospital In Network Per Day Copay $75 $75 $75 $88 $150

Outpatient In Network Copay $13 $20 $30 $75 $100

Prescription Drug Plan Designs

12

Percentiles 10% 25% Median 75% 90%

Summary across only those plans using copays

Retail

Generic Copay $5 $5 $8 $10 $10

Brand Formulary Copay $10 $15 $20 $30 $35

Brand Non-Formulary Copay $15 $25 $35 $50 $60

Specialty Copay $15 $25 $35 $50 $70

Mail Order

MO Generic Copay $7 $10 $12 $20 $20

MO Brand Formulary Copay $20 $25 $40 $50 $70

MO Brand Non-Formulary Copay $20 $35 $60 $90 $110

Prescription Drug Plan Designs

13

Percentiles 10% 25% Median 75% 90%

Summary across only those plans using coinsurance

Retail Generic 18% 20% 20% 20% 20%

Retail Brand Formulary 20% 20% 20% 20% 25%

Retail Brand Non-Formulary 20% 20% 20% 20% 40%

MO Generic 18% 20% 20% 20% 20%

MO Brand Formulary 20% 20% 20% 20% 22%

MO Brand Non-Formulary 20% 20% 20% 20% 40%

Health Plan Actuarial Values

14

Definition – the estimated percentage of a typical policyholder’s healthcare

bills that the plan is expected to pay. The smaller the member’s out-of-

pocket costs the larger the plan’s actuarial value.

Under PPACA, employer plans must have a minimum actuarial value of 60%

to avoid an employer penalty.

On the healthcare exchanges, to facilitate comparison shopping, healthcare

plans must have an actuarial value that fits one of four metal tiers:

Platinum = 90%

Gold = 80%

Silver = 70%

Bronze = 60%

Individual plan AV’s can be no more than +2% or -2% from these values to

be eligible for the Exchanges.

Actuarial Values of School Health Plans

15

Actuarial Value Percent of SchoolHealth Plans

Platinum plus Over 92% 71%

Platinum 88% to 92% 14%

Gold plus >82% and <88% 14%

Gold 78% to 82% 1%

Silver plus >72% and <78% 1%

Silver 68% to 72% 0%

Bronze & bronze plus >60% and <68% 0%

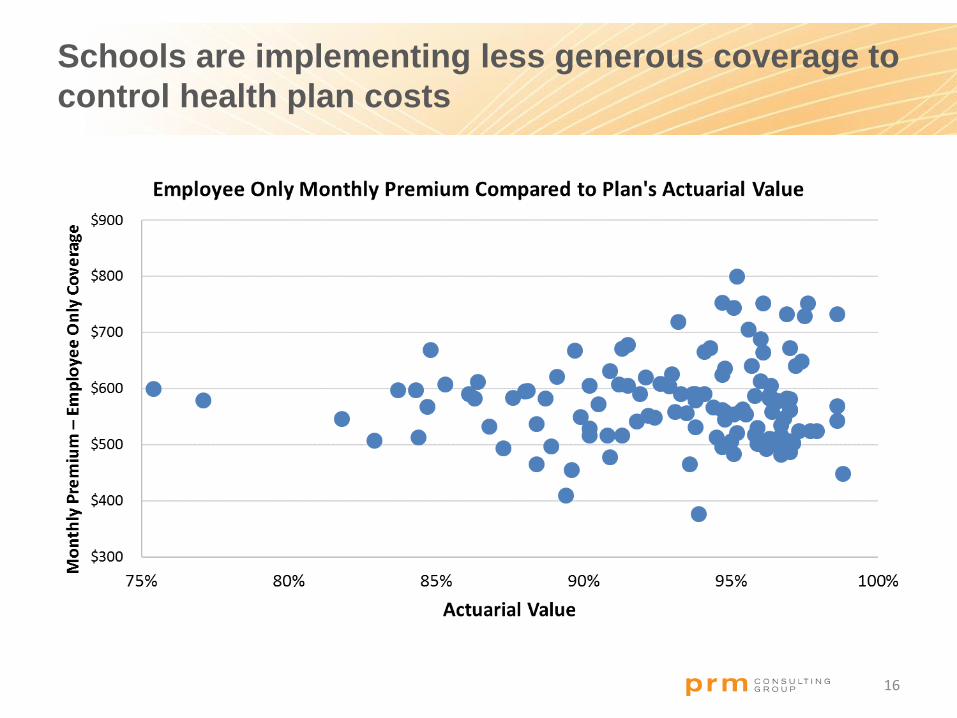

85% of SD’s have health plans with an actuarial value of 90% or more, with

over 70% more generous than is permitted for a plan to be marketed on the

Exchanges.

Schools are implementing less generous coverage to

control health plan costs

16

Healthcare costs varied substantially among consortia.

The largest consortium (ACSHIC) had the lowest cost.

17

An

nu

al

Co

st

Number of Covered Lives

Next we’ll compare how the school health

plans compare to the average tax payer

18

3. Comparison of coverage with average taxpayer in the relevant region

Average Taxpayer Coverage

19

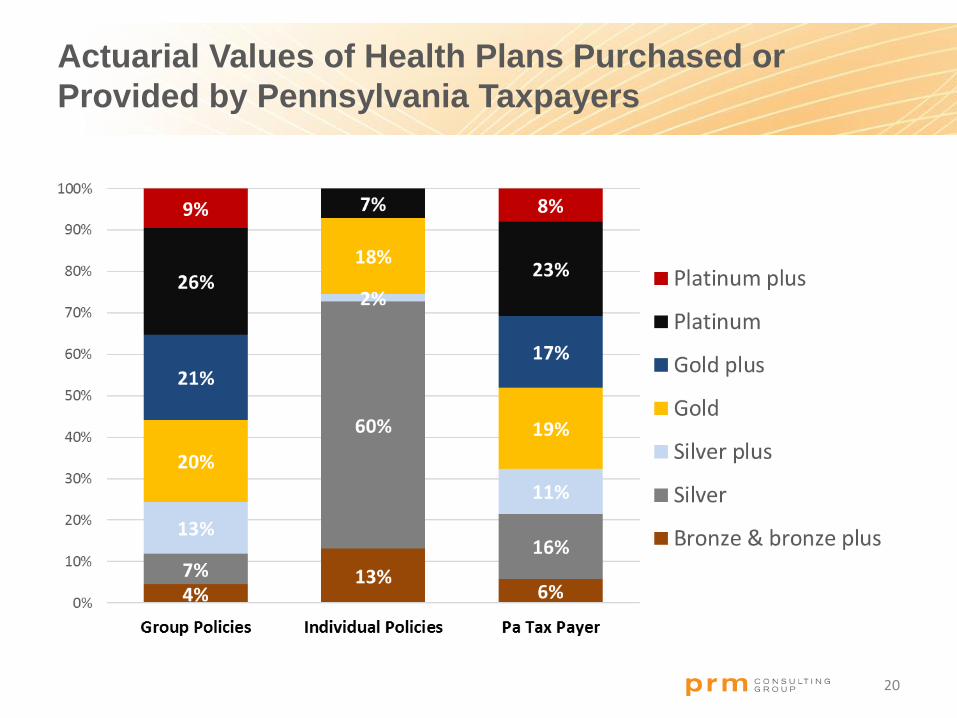

Health Plan Coverage Level Actuarial Value Group PoliciesIndividual

PoliciesTotal

Platinum plus Above 92% 223,409 - 223,409

Platinum 88% to 92% 605,974 31,772 637,746

Gold plus 82.1% to 87.9% 486,272 43 486,315

Gold 78% to 82% 464,245 81,296 545,541

Silver plus 72.1% to 77.9% 296,712 8,632 305,344

Silver 68% to 72% 174,118 265,607 439,725

Bronze & bronze plus 60% to 67.9% 104,570 58,484 163,054

Total 2,355,300 445,834 2,801,134

Average Actuarial Value 82.9% 72.7% 81.3%

Actuarial Values of Health Plans Purchased or

Provided by Pennsylvania Taxpayers

20

Comparison of Actuarial Values of Pa Tax Payer

Coverage with School Health Plans

21

Comparison of Actuarial Values of Health Plans of Pa

Tax Payers by Region

22

85.4% 85.2%83.4%

80.7%

60%

65%

70%

75%

80%

85%

90%

Western Northeastern Central Southeastern

Group Policies

73.7%75.9%

73.7%71.1%

60%

65%

70%

75%

80%

85%

90%

Western Northeastern Central Southeastern

Individual Policies

Group policies are more generous in the Western and Northeastern parts of

the Commonwealth. For both Group and Individual policies, less generous

plans are purchased or provided in the Southeastern area. This may be a

consequence of the higher cost of healthcare in Philadelphia and

surrounding suburbs.

Comparison of School Employee Benefits

to State Employee Benefits

23

4. Comparison of school employees with Commonwealth employees

School & State Employees

Plan Design Comparison

24

In-Network Out-of-Network / Non-Network Providers

Plan Feature/Benefit School Median Plan

State PPO Plan

School Median Plan State PPO Plan

Deductible—Individual $ 300 None $ 750 $400

—Family $500 None $1,500 $400 per person

Member Coinsurance 20% 0% 20% 30%

Out-of-pocket limit—Individual $1,300 $6,600 $3,000 $1,900

—Family $1,500 $13,200 $6,000 $3,000 excluding deductible

Hospital inpatient (member pays) 100% 100% 20% 30%

Outpatient care (member pays) 20% $15 20% 40%

Emergency room $85 $50 $50

Urgent care facility 20%

Office visit—Primary care (member pays) 20% $15 $25 30%

—Specialist (member pays) 20% $25 $40 30%

School & State Employees

Plan Design Comparison

25

In-Network

Plan Feature/Benefit School Median Plan State PPO Plan

Retail copays

Generic drugs $7 $10

Formulary $12 $18 +

Non-Formulary $20 $36

Mail Order Copays

Generic drugs $5 $15

Formulary $20 $27 +

Non-Formulary $30 $54

+ Plus pay the difference between the cost of the generic and the brand drug.

Median School Health Plan State PPO Plan

Actuarial Value 95% 96%

Comparison of School Employee Benefits to State

Employee Benefits – Dental Benefits

26

School Dental Benefits State

Percent Paid by Plan 100% 80% to 90% 60% to 75% 50%Schools Average

PEBTF

Preventive Services 96% 3% 1% 0% 98% 100%

Basic Restorative Services 83% 14% 3% 0% 95% 90%

Major Restorative Services 21% 29% 6% 44% 66% 60%

Maximum benefit $1,215 $1,000

Average deductible $27 $50

Most, but not all, schools provide dental coverage. Almost all (96 percent) of school districts cover

preventive services at 100 percent. Most (83 percent) school districts cover basic restorative services at

100 percent. Only 21 percent of school districts cover major restorative services at 100 percent, with

the most common level at 50 percent.

Comparison of School Employee Benefits to State

Employee Benefits – Vision Benefits

PEBTF Participating Provider Non-Participating Provider

Yearly vision examination 100% covered Allowance of up to $28

Glaucoma test 100% covered Allowance of up to $3

LensesStandard glass/plastic

are covered in full

Single vision: $15Bifocals: $24.50

Ex-Bifocals: $26.50Trifocals: $31.00Aphakic: $60.00

Frames – up to $20Covered in full up to a

maximum of $20 $20.00

Frames – above $20 80% covered $20.00

27

Comparison of School Employee Benefits to State

Employee Benefits – Vision Benefits

28

Vision Coverages School District Plans PEBTF

25th Percentile Median 75th Percentile

Vision exam-amount plan pays (where not 100%) $30 $39 $58.75 $28

Standard single lenses amount plan pays 24 30 60 15

Bifocal lenses-amount plan pays 36 40 73 24.50

Trifocal lenses-amount plan pays 46 60 94 31

Frames-amount plan pays 24 55 62 20

Medically necessary contact lenses-amount plan pays 70 160 250

Elective contact lenses-amount plan pays 73.50 80 125

Comparison of school employees with Commonwealth

employees – average annual employee premiums

29PEBTF cost based on salary of $55,450

Almost finished – lets review the potential

cost-savings from mergers

30

5. Regionalization versus savings from one state-wide health care plan

State-wide Pharmacy Benefit Program

Pharmacy benefits carved out from each medical plan.

Three or four benefit levels – to minimize copay differences moving from

current design to the state-wide program.

Each school district (or Consortium) could choose the benefit level(s) they

want for the first year of operation. School districts could move to one of the

alternative designs at open enrollment.

Single PBM to administer the program. PBM selected through a

competitive bidding process.

Could also include member choice from among 3 networks – with savings

passed on to participants.

31

Pharmacy Benefits – Current Benefit Levels

Schools Pharmacy Copays PEBTF KFF

10th MEDIAN 90th

Retail Generic Copay $5 $8 $10 $10 $11

Retail Brand Formulary Copay $10 $20 $35 $18 $31

Retail Brand Non-Formulary Copay $15 $35 $60 $36 $54

Retail Specialty $15 $35 $70 $36 $93

32

Smaller variation in pharmacy plan design across schools than in medical

Median plan design comparable to the PEBTF plan

90th percentile plan design comparable to private sector (KFF)

Only 14% of SDs have carved out prescription drugs

Opportunity to capitalize on bulk purchasing power if pharmacy is carved out of

all healthcare plans and competitively bid with 3-4 plan designs

State-wide Pharmacy Benefit Program

Straw man plan designs

Superior High Standard Basic

Generic $5 $10 $10 $10

Preferred brand $10 $20 $35 20% ($25 min. and $75 max.)

Non-preferred brand $15 $35 $60 50% ($50 min. and $100 max.)

Specialty $25 $40 $75 50% ($50 min. and $100 max.)

Mail Order 90 day supply at equivalent of 2 copays rather than 3

33

Network Choices

Broad PBM’s full network of pharmacies

Performance PBM’s performance network

Performance plus PBM’s performance network plus maintenance drugs must be purchased through mail-order.

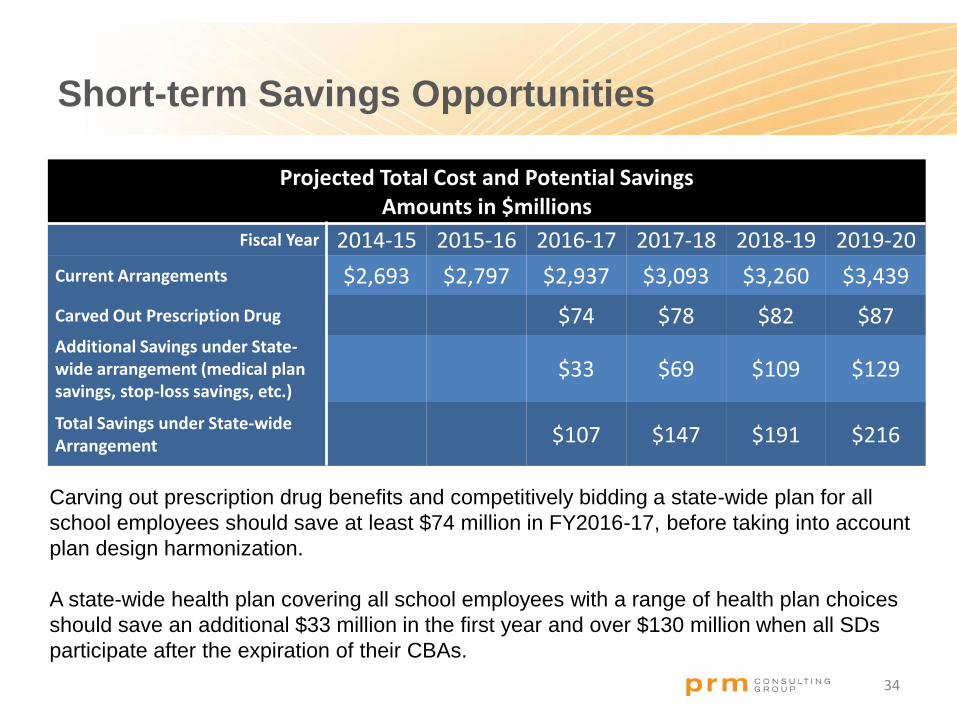

Short-term Savings Opportunities

Projected Total Cost and Potential Savings Amounts in $millions

Fiscal Year 2014-15 2015-16 2016-17 2017-18 2018-19 2019-20

Current Arrangements $2,693 $2,797 $2,937 $3,093 $3,260 $3,439

Carved Out Prescription Drug $74 $78 $82 $87Additional Savings under State-wide arrangement (medical plan savings, stop-loss savings, etc.)

$33 $69 $109 $129

Total Savings under State-wide Arrangement $107 $147 $191 $216

34

Carving out prescription drug benefits and competitively bidding a state-wide plan for all

school employees should save at least $74 million in FY2016-17, before taking into account

plan design harmonization.

A state-wide health plan covering all school employees with a range of health plan choices

should save an additional $33 million in the first year and over $130 million when all SDs

participate after the expiration of their CBAs.

Lastly, we identified an opportunity to

mitigate costs from PPACA

35

6. Cost impact of Health Care Reform (PPACA)

Longer-term Savings Opportunities

36

Healthcare Reform added an Excise Tax on high-cost health plans. The tax is

40% of the excess of the cost above a threshold of $10,200 for self-only

coverage and $27,500 for “other than self-only coverage”. Implementation date

of 2018 has been postponed to 2020, with the likelihood of more plans hitting

the threshold in the first year of operation.

If SDs participated in a multiemployer plan, the threshold is $27,500 (indexed)

for all employees, which has the effect of reducing the amount of the tax. The

savings are significant as illustrated in the table below (projected cost in 2027)

of $2,500 per employee – about 6% of the premium cost.

Threshold Cost Excess Tax Employees Total tax

Self $12,309 $16,823 $4,514 $1,806 30 $54,168

Other $33,187 $45,355 $12,168 $4,867 70 $340,704

Total single employer $394,872

Multiemployer $33,187 $36,796 $3,609 $1,444 100 $144,360

Savings if SDs participate in a multiemployer plan $250,512

Next Steps

Establish a statewide pharmacy program but who leads:

PEBTF? PSERS-HOP? PSEA?

Regional health plan:

Merging of “small” consortia

Merging of “high cost” consortia to avoid/defer Cadillac Tax

Implementing best practices:

Cost effective plan design options

Narrow networks

Contribution policies

Statewide health plan

Would likely need to be legislated, rather than voluntary to be

successful

37

Questions?

I would be happy to answer any questions you may have now, or after the

conference

Adam Reese FSA, FCA, MAAA

(301) 951.5107

38

Top Related