Languages

Pages

Legal

0

Nordic Region

P7S1 Group Capital Markets Day

Munich, October 5, 2011

1

P7S1 Nordics is a leading pan-Nordic TV and radio operator

Source: P7S1 Nordics

Radio

14

FTA

75Revenues

rec. EBITDA

Region

104

398

EUR millions, 2010

1 Adjusted external financials

DENMARK SWEDEN FINLANDNORWAY

FINLANDNORWAY

SWEDENDENMARK

rec. EBITDA- margin

90

323

28% 18% 26%

2

Nordic region – experienced management team

Tomas JansonCFO Nordic RegionCFO Sweden TV

• 13 years of in-depth knowledge of Swedish TV market; appointed Nordic CFO in 2009

• Part of the P7S1 growth story in Sweden from 2001 to 2005

1321Henrik RavnCEO Nordic RegionCEO Denmark

• Pioneer in Danish commercial TV• Successfully turned around P7S1 in

Denmark and launched five Danish TV channels

Jonas SjögrenCEO Sweden/Finland

• Successfully launched Kanal 9; led Kanal 5 to best media sales house award 2005/06

• As CEO Finland responsible for building Finnish TV business

11 Harald S. StrømmeCEO Norway

• Key to launch and formation of TV2; built the leading advertising agency in Norway

• Successfully turned around P7S1 Norway and launched hit channel MAX in 2010

25

Source: P7S1 Nordics

Years of broadcasting experienceX

3

The Nordic Region investment highlights

24The partner of choice in a highly

competitive distribution landscape 3

The challenger with superior growth and profitability1Highly attractive

growth markets

Clear path towards additional value creation

Source: P7S1 Nordics

4

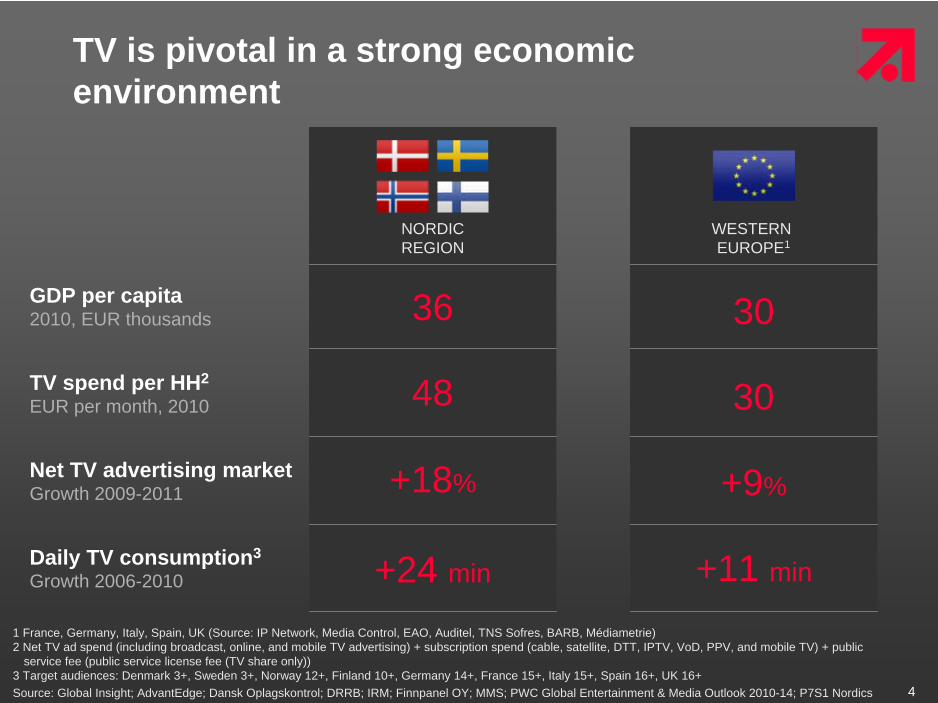

TV is pivotal in a strong economic environment

+9%+18%

+11 min+24 min

3048

3036GDP per capita 2010, EUR thousands

Net TV advertising market Growth 2009-2011

TV spend per HH2

EUR per month, 2010

Daily TV consumption3

Growth 2006-2010

WESTERN EUROPE1

NORDIC REGION

Source: Global Insight; AdvantEdge; Dansk Oplagskontrol; DRRB; IRM; Finnpanel OY; MMS; PWC Global Entertainment & Media Outlook 2010-14; P7S1 Nordics

1 France, Germany, Italy, Spain, UK (Source: IP Network, Media Control, EAO, Auditel, TNS Sofres, BARB, Médiametrie)2 Net TV ad spend (including broadcast, online, and mobile TV advertising) + subscription spend (cable, satellite, DTT, IPTV, VoD, PPV, and mobile TV) + public

service fee (public service license fee (TV share only))3 Target audiences: Denmark 3+, Sweden 3+, Norway 12+, Finland 10+, Germany 14+, France 15+, Italy 15+, Spain 16+, UK 16+

5

3

4

3

2

5

3

3

2

Advertising is shifting from print to broadcasting

Source: AdvantEdge; Dansk Oplagskontrol; DRRB; IRM; Finnpanel OY; P7S1 Nordics

Share of media in net advertising market Percent

Print TV

20112008

17

24

17

22

24

19

23

1851

47

61

52

49

57

42

42

Radio

FINLAND

NORWAY

SWEDEN

DENMARK

6

Strong growth in all Nordic TV markets Expectations Nordic TV ad markets 2011

2010 YTD Rest of 2011 2011 ESweden (MSEK) 5.198 2.430 3.417 5.847Index 118 116 110 113Denmark (MDKK) 2.256 1.317 1.330 2.707Index 110 122 118 120Norway (MNOK) 3.061 2.036 1.369 3.405Index 110 114 107 111Finland (M€) 266 149 144 293Index 112 114 106 110Source: MediAid (Group M). YTD: DK & Nor: Jan‐July, Fin: Jan‐Jun, Swe: Jan‐May

7

Strong growth in all Nordic radio markets Expectations Nordic radio ad markets 2011

2010 YTD Rest of 2011 2011 ESweden (MSEK) 688 308 450 758Index 110 117 106 110Denmark (MDKK) 232 197 116 313Index 107 149 117 135Norway (MNOK) 563 368 232 600Index 112 109 105 107Finland (M€) 52 30 32 62Index 104 117 122 120Source: MediAid (Group M). YTD: DK & Nor: Jan‐July, Fin: Jan‐Jun, Swe: Jan‐May

8

Synergies – Strong pan-Nordic radio portfolio complements TV challenger position

1 Based on advertising shares 2010

Position in radio market1

Source: P7S1 Nordics

DENMARK SWEDEN FINLANDNORWAY

9

Audience – Strong growth trajectory

Source: Advantedge; Finnpanel OY; MMS/AGB Nielsen; P7S1 Nordics

FINLAND

NORWAY

SWEDEN

DENMARK

1 Full day, commercial shares; Denmark: 15-50 years, Sweden and Finland: 15-59 years, Norway: 12-44 years

P7S1 audience share1

30.0%22.5%

6.5%2.3%

21.0%21.7%

17.0%14.3%

2008 2011E

10

Monetization – P7S1 Nordics is turning audience shares into advertising revenues

Source: Advantedge; Finnpanel OY; MMS/AGB Nielsen; P7S1 Nordics

FINLAND

NORWAY

SWEDEN

DENMARK

P7S1 Nordics net TV advertising market share

19.1%

N/A

17.7%

10.8%

24.3%

2.6%

16.5%

15.3%

2008 2011E

11

Carriage revenues – Partner of choice in highly competitive distribution landscape

Source: P7S1 Nordics

~20% p.a.

Cable

DTT

Satellite (DTH)

IPTV & others

Increase in P7S1 carriage revenues 2008 – 2011E

P7S1 distribution partners SWEDENDENMARK NORWAY

12Source: Advantedge; Finnpanel OY; MMS/AGB Nielsen; P7S1 Nordics

1 Full day, commercial shares; Denmark: 15-50 years, Sweden: 15-59 years, Norway: 12-44 years, Finland: 15-59 years 2 Share for Q3 20113 Combined audience share with The Voice TV

Jan 2009Launch date

Target audience

2.94.0

6.236.1

5.12

Feb 2007 Sep 2008Nov 2010 Sep 2007

Distribution – 5 successful channel launches in 4 years

Audience share1

2010, percent

15-50 30-59 15-4412-4412-44

DENMARK SWEDEN FINLANDNORWAY

13

Carriage Denmark – Channel positioning favored by distributors and advertisers

Note: Bubble size = audience share 1 TV2 is still in public hands but treated like a commercial stationSource: TNS-Gallup; Advantedge; P7S1 Nordics

Target group structure and audience sharesNational universe, 15 - 50 years, Mon-Sun, all day, full year 2010

TV3 dk

TV3+

TV3 PULS

DR 2 TV 2 Zulu

TV 2 NEWS

TV 2 Sport

TV 2 Charlie

TV 2 FILM

TV 2DR 1

MTV dk

Discovery dk

DENMARK

Commercial

PSB

P7S1

MTG

Other

DR

TV21

Fe- male

Male

YoungOld

14

Nordics: Carriage fees drive strong revenue growth

FTA carriageand other

FTAadvertising

Radio69

75

2010

398

69

210

2009

335

170

113

2008

355

197

9791

RevenuesEUR millions

2008-2010 CAGR

4.2%

2.0%

13.5%

Source: P7S1 Nordics

15

0 20 40 60

30

20

10

0

P7S1 Nordics carriage fee share of total FTA revenues 2010

Percent

Norway

Sweden

Denmark

P7S1 Nordics EBITDA margins Percent - 2010

40

Distribution model earns high margins and stable revenues

• Predictable carriage revenues with significant future growth potential

• Carriage revenues allow for very strong EBITDA margins

• Danish "mini-pay" model successful through partnership with cable and DTH platforms

Source: P7S1 Nordics

Bubble size represents EUR 10 million of carriage revenue contribution; No carriage fees in Finland

16

Growth through transfer of Danish model across the Nordics

1

3

4

Source: P7S1 Nordics

2

1 Estimate based on total EBITDA development Norway (2008-2011B)

+150%

Realized EBITDA growth in Norway through transfer of Danish model1

• 4 channels • Dedicated target audiences

(young F, young M, general)• Football on• Strategic alliances with

distributors ("partner of choice")

DENMARK

• 4 channels • Dedicated target audiences

(young F, young M, general)• Football on• Increase in EBITDA margin

NORWAY

17

18

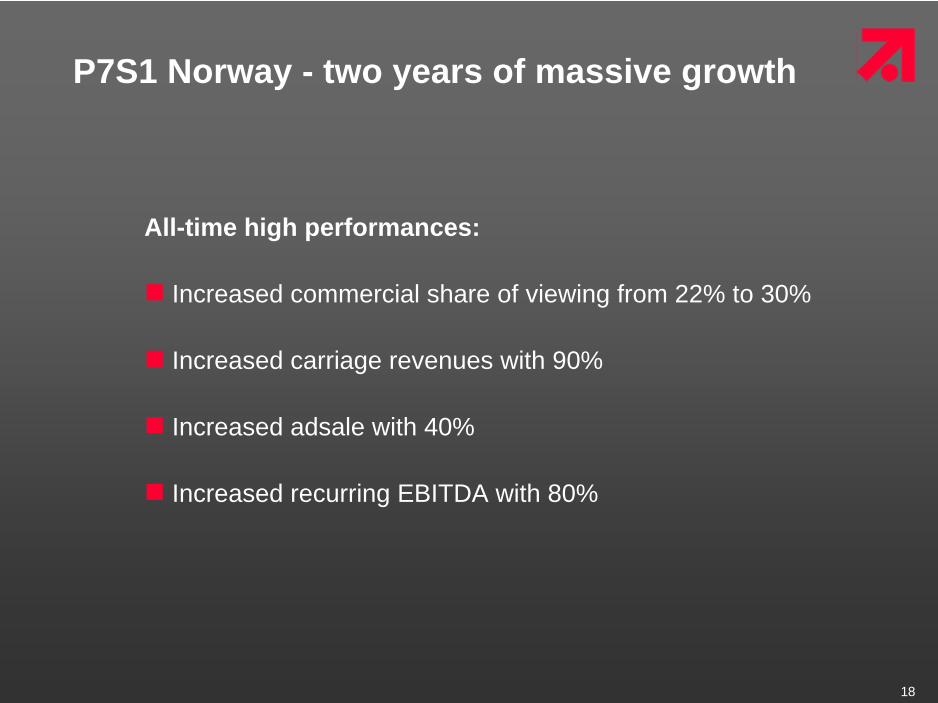

P7S1 Norway - two years of massive growth

All-time high performances:

Increased commercial share of viewing from 22% to 30%

Increased carriage revenues with 90%

Increased adsale with 40%

Increased recurring EBITDA with 80%

19

Key success factors

Optimized channel portfolio• Repositioning of TVNorge to broad entertainment• Consolidation of female channel FEM• Launch of male channel MAX on November 1st, 2010

Win-win approach to carriage revenues• Danish model of dual revenue streams• Telenor partnership

99% hitrate on local productions• Strong pipeline and production skills• Timeslot analysis• Flexibility in scheduling

20

Norway – competitive landscape

Source: TNS-Gallup; Advantedge; P7S1 NordicsNote: Bubble size = audience share

Fe- male

Male

YoungOld

Viasat 4

TV3 no

TV 2 no

NRK1

NRK3

TV 2 Zebra

Target group structure and audience sharesNational universe, 12 - 44 years, Mon-Sun, all day, full year 2010

Commercial

PSB

P7S1

MTG

NRK

Egmont

21

Channel portfolio - Norway

0.0% 0.0% 0.0% 0.0% 0.1% 0.3% 0.3% 0.2% 0.3% 0.3% 0.1% 0.0%

0.0% 0.0% 0.0% 0.0% 0.2% 0.6% 0.4% 0.3% 0.4% 0.4% 0.1% 0.0%

0.0% 0.0% 0.0% 0.0% 0.4% 0.9% 0.7% 0.7% 0.8% 0.5% 0.1% 0.0%

0.0% 0.0% 0.0% 0.0% 0.3% 1.2% 1.5% 2.1% 1.6% 0.6% 0.1% 0.0%

0.0% 0.0% 0.0% 0.0% 0.3% 2.6% 6.1% 4.6% 1.9% 0.8% 0.1% 0.0%

0.0% 0.0% 0.0% 0.0% 0.4% 2.8% 10.7% 7.5% 1.9% 0.7% 0.1% 0.0%

0.0% 0.0% 0.0% 0.0% 0.6% 2.7% 7.8% 3.5% 1.8% 0.5% 0.2% 0.1%

0.0% 0.0% 0.0% 0.0% 0.4% 1.7% 2.5% 1.3% 1.0% 0.4% 0.2% 0.1%

0.0% 0.0% 0.0% 0.0% 0.1% 1.1% 2.5% 0.7% 0.6% 0.3% 0.2% 0.1%

0.0% 0.0% 0.0% 0.0% 0.0% 1.0% 2.1% 0.6% 0.3% 0.2% 0.2% 0.1%

0.0% 0.0% 0.0% 0.0% 0.0% 0.4% 1.3% 0.5% 0.2% 0.2% 0.2% 0.1%

0.0% 0.0% 0.0% 0.0% 0.0% 0.2% 0.5% 0.4% 0.2% 0.1% 0.1% 0.1%

0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1%

0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.1% 0.1% 0.1% 0.1% 0.0%

Gross spend per demographic Percent

Source: CIM/GfK Audimetrie; P7S1 Nordics

~1% ~2% ~3% ~4% ~5% ~6%<0.5%

Age

% female

85

80

75

70

40

35

30

25

20

15

65

60

55

50

45

YoungOld

Advertisers' sweet spot

71%29%

36%64%

58%42%

22

P7S1 Norway Share of Viewing (SoV)C

omm

erci

al s

hare

of v

iew

ing

(in p

erce

nt),

12-4

4

Source: P7S1 Nordics

23

P7S1 Norway Share of Viewing (SoV)C

omm

erci

al s

hare

of v

iew

ing

(in p

erce

nt),

12-4

4

P7S1 vs. MTG

Source: P7S1 NordicsNote: Adjusted for terror attack in Norway

24

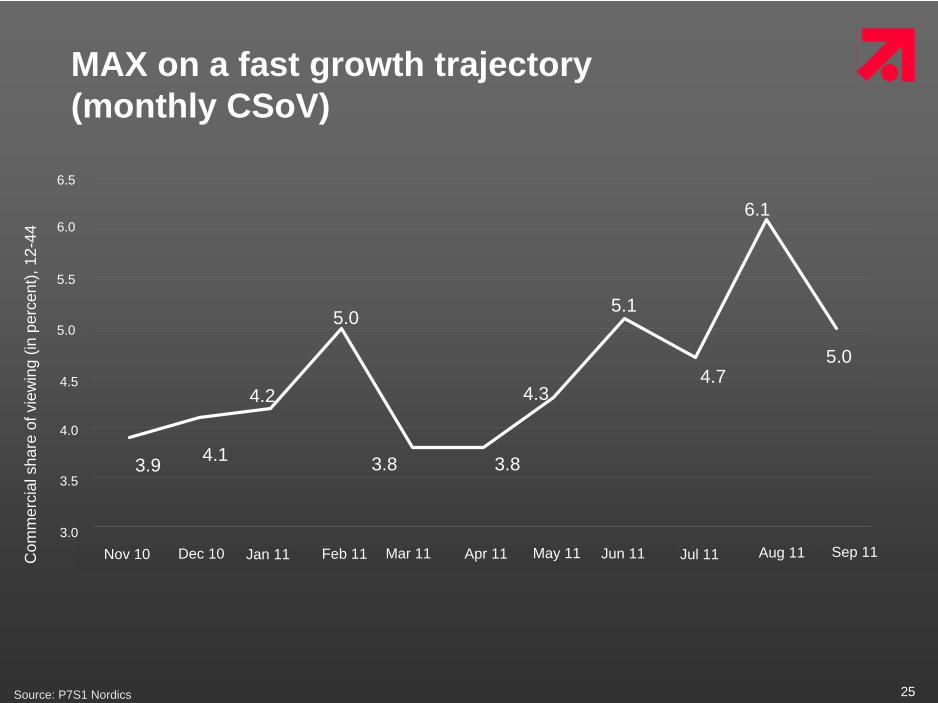

MAX - key programming highlights

Heavily male programming and some famous light-house brands Norwegian elite series football, one match a week Very strict programming grid

25

Nov 10 dec.10 Jan 11 Feb 11 Mrz 11 Apr 11 may.11 Jun 11 Jul 11 Aug 11 Sep 11

MAX on a fast growth trajectory (monthly CSoV)

Com

mer

cial

sha

re o

f vie

win

g (in

per

cent

), 12

-44

Source: P7S1 Nordics

3.9 4.1

4.2

5.0

3.8 3.8

4.3

5.1

4.7

6.1

5.0

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

Nov 10 Dec 10 Jan 11 Feb 11 Mar 11 Apr 11 May 11 Jun 11 Jul 11 Aug 11 Sep 11

26

6.1

4.14.1

3.1

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

Viasat 4 Discovery TV 2 Zebra MAX

Com

mer

cial

sha

re o

f vie

win

g (in

per

cent

), 12

-44

MAX already #2 among male channels Digital universe, men 12-44 years

Source: P7S1 Nordics

7.0

6.0

5.0

4.0

3.0

2.0

1.0

0.0

27

MAX – fastest new launch in years

4.0

2.5

1.5

4.3

3.3

2.3

4.4

3.02.8

5.1

4.4 4.4

0.0

1.0

2.0

3.0

4.0

5.0

6.0Q4 2010 Q1 2011 Q2 2011 Q3 2011

Com

mer

cial

sha

re o

f vie

win

g, 1

2-44

Source: P7S1 Nordics

MAX TV2 Bliss EM (2007/-08)

28

Carriage revenues: The Telenor

example

Five year partnership, and a new win-win approach

Telenor wins:• DTH exclusivity for MAX• A distinctive offering to male subscribers, with football• A key content partner to a new VOD/WEB-TV platform

P7S1 wins:• Increased carriage revenues for channel portfolio• Secured penetration and PVR-position for MAX• Muscle to acquire premier Norwegian football rights• Increased negotiating power towards rest of distribution market• A strong VOD/WEB-TV partnership with strong marketing presence

Source: P7S1 Nordics

29

Carriage revenues (NOK m)

Source: P7S1 Nordics

30

Nordic region: High growth potential going forward

TV/radio

Cost synergies

Source: P7S1 Nordics

Ad sale & distribution

Online & diversification

• Well established challenger position secures high potential to grow share of viewing and share of money

• Potential to grow regional sales in Sweden• Export Danish distribution model to rest of region and

cooperate with main distributors

• Build pan Nordic online and diversification strategy to take advantage of high growth markets

• Implement radio in TV organisations in each country to secure cost synergies and more efficient sales and back office organisations

• Secure more pan Nordic synergies within playout, programming, online and diversification

Nordic revenue growth potential of high mid single digit CAGR until 2015

31

This presentation contains "forward looking statements" regarding ProSiebenSat.1 Media AG ("ProSiebenSat.1 AG"), its subsidiaries/affiliates and/or ProSiebenSat.1 Group as a whole (all hereinafter collectively referred to as “P7S1 Group”), including opinions, estimates and projections regarding P7S1 Group's financial position, business strategy, plans and objectives of management and future operations and including opinions, estimates and projections regarding the markets in which it presently operates or in which it expects to operate in the future. Such forward looking statements involve known and unknown risks, uncertainties and other important factors that could cause the actual results, performance or achievements of P7S1 Group to be materially different from future results, performance or achievements expressed or implied by such forward looking statements. These forward looking statements speak only as of the date of this presentation and are based on numerous assumptions which may or may not prove to be correct.

No representation or warranty, express or implied, is made by ProSiebenSat.1, its subsidiaries/affiliates or P7S1 Group as a whole with respect to the fairness, completeness, correctness, reasonableness or accuracy of any information and opinions contained herein. The information in this presentation is subject to change without notice, it may be incomplete or condensed, and it may not contain all material information concerning P7S1 Group. ProSiebenSat.1 and its subsidiaries/affiliates undertake no obligation to publicly update or revise any forward looking statements or other information stated herein, whether as a result of new information, future events or otherwise.

Disclaimer

Top Related