Languages

Pages

Legal

Making Financial Services Accessible

and Affordable to Women

MBA. Phan Cử Nhân – May 2015

Contents

Part I - General Introduction on VBSP

Part II - Making Financial Services Accessible

and Affordable to Women

Part III - Achievement

Part I

General Introduction

on VBSP

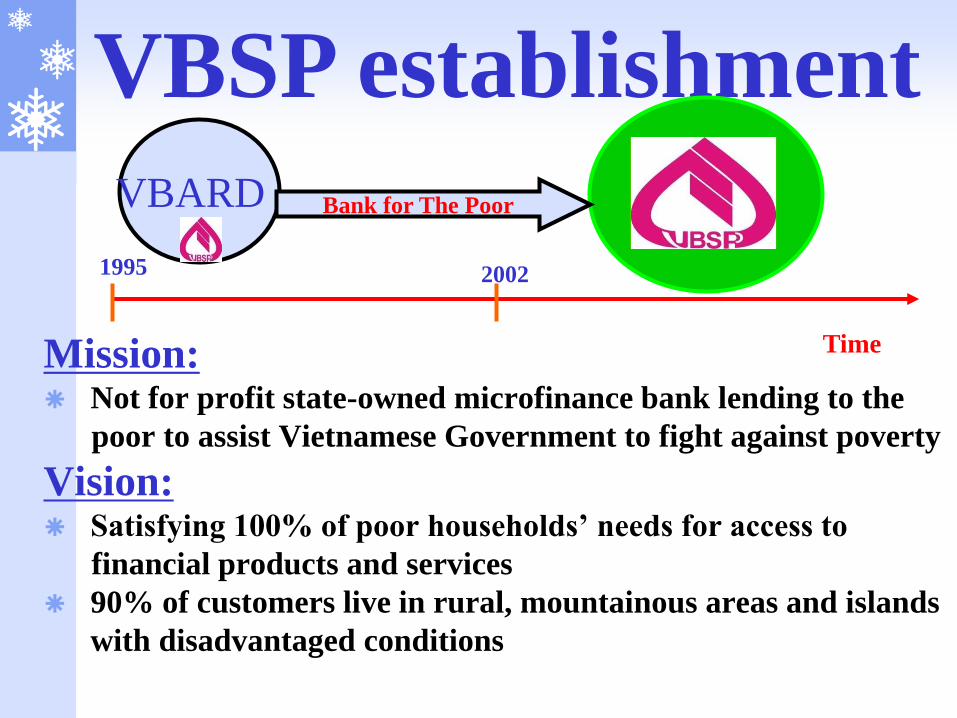

VBARD

2002

Time

VBSP establishment

Bank for The Poor

1995

Mission: Not for profit state-owned microfinance bank lending to the

poor to assist Vietnamese Government to fight against poverty

Vision: Satisfying 100% of poor households’ needs for access to

financial products and services

90% of customers live in rural, mountainous areas and islands

with disadvantaged conditions

Part II

Making Financial

Services Accessible

and Affordable to

Women

Credit Programs also aiming women

Target

Clients

Job Creation program

Disadvantaged students

Poor Households

Business & production households living in

specially disadvantaged areas and communes

Others (Entrusted by donors or mandated

by the Government)

Migrant workers

Safe water supply & rural sanitation

Housing purpose at flooded areas

Business & production units with drug-detoxified

employees

Specially disadvantaged ethnic minority households

Traders doing business in disadvantaged areas

Near poor Households

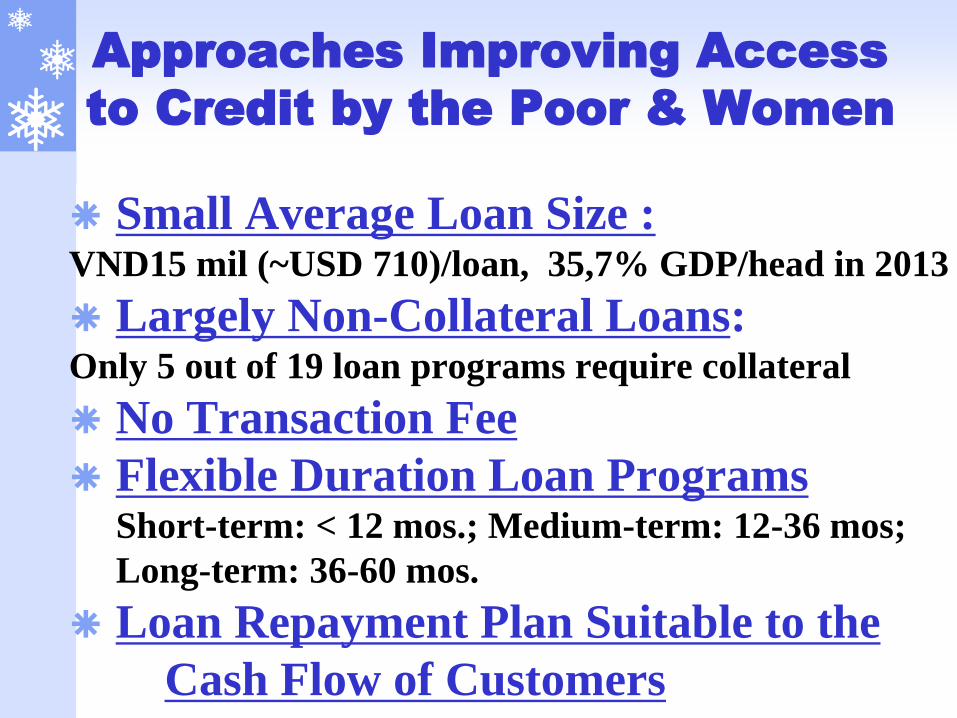

Approaches Improving Access

to Credit by the Poor & Women

Small Average Loan Size : VND15 mil (~USD 710)/loan, 35,7% GDP/head in 2013

Largely Non-Collateral Loans: Only 5 out of 19 loan programs require collateral

No Transaction Fee

Flexible Duration Loan Programs Short-term: < 12 mos.; Medium-term: 12-36 mos;

Long-term: 36-60 mos.

Loan Repayment Plan Suitable to the

Cash Flow of Customers

Saving Services

In 2009, VBSP has launched a new savings model :

"To mobilize savings from poor communities

through savings and credit groups ( SCGs) ".

In particular, the poor deposit savings with a small

amount atleast VND 1,000 (5cent) which creates

the awareness for the poor and women to spend

their savings to make up their own capitals and get

familiarity with financial services.

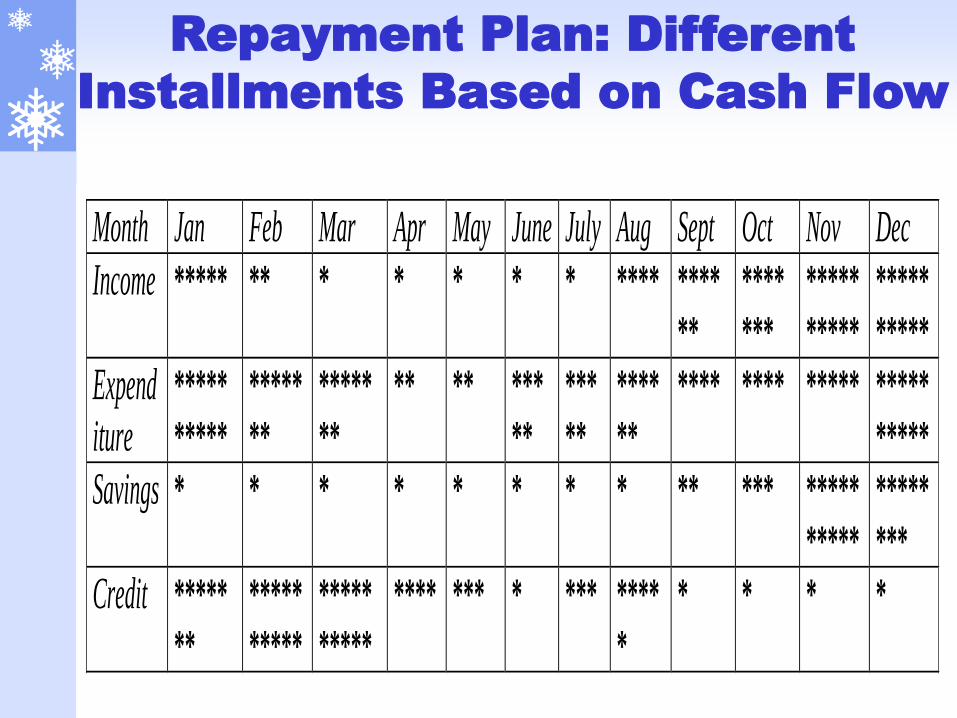

Repayment Plan: Different

Installments Based on Cash Flow

Month Jan Feb Mar Apr May June July Aug Sept Oct Nov Dec

Income ***** ** * * * * * **** ****

**

****

***

*****

*****

*****

*****

Expend

iture *****

*****

*****

**

*****

**

** ** ***

**

***

**

****

**

**** **** ***** *****

*****

Savings * * * * * * * * ** *** *****

*****

*****

***

Credit *****

**

*****

*****

*****

*****

**** *** * *** ****

*

* * * *

Service Outreach to reduce

mobility constraints.

63 Provincial and Municipal Branches

626 District Transaction Offices

196,931 Savings & Credit Groups

at Communes/Wards

10,904 Fixed Date Transaction Points at

Communes/Wards

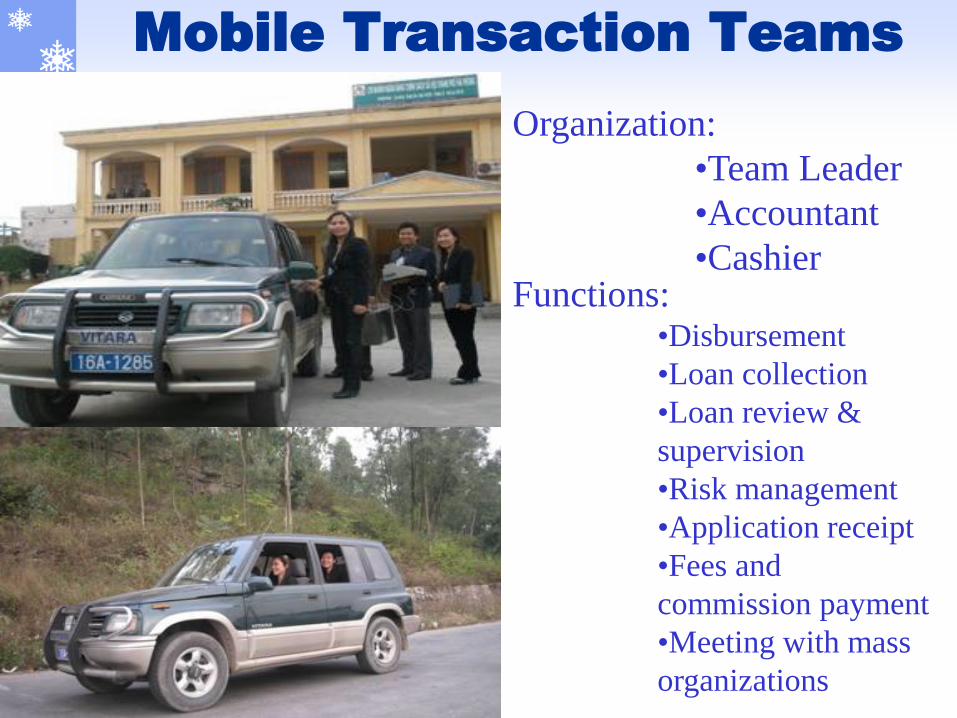

Mobile Transaction Teams

Forming

Savings and Credit Groups

•30-60 members

•10-15 members

(mountainous)

Management Board:

•Group Head

•Deputy Head

•Group Charter

•Outsourcing contract

by the VBSP

•Facilitating the

loan management

and savings

•Commission based

activities

Introduction of VBSP’s lending programs

Choosing target clients

Self-selecting borrowers

Collecting interest, savings

Supervising the loan

Supporting activities

Role of Women Organizations

Savings & Credit Groups

100 % of communes

reached by VBSP

Fixed Date Transaction Points

3km<

>3km

Mobile Transaction Teams

Organization:

•Team Leader

•Accountant

•Cashier Functions:

•Disbursement

•Loan collection

•Loan review &

supervision

•Risk management

•Application receipt

•Fees and

commission payment

•Meeting with mass

organizations

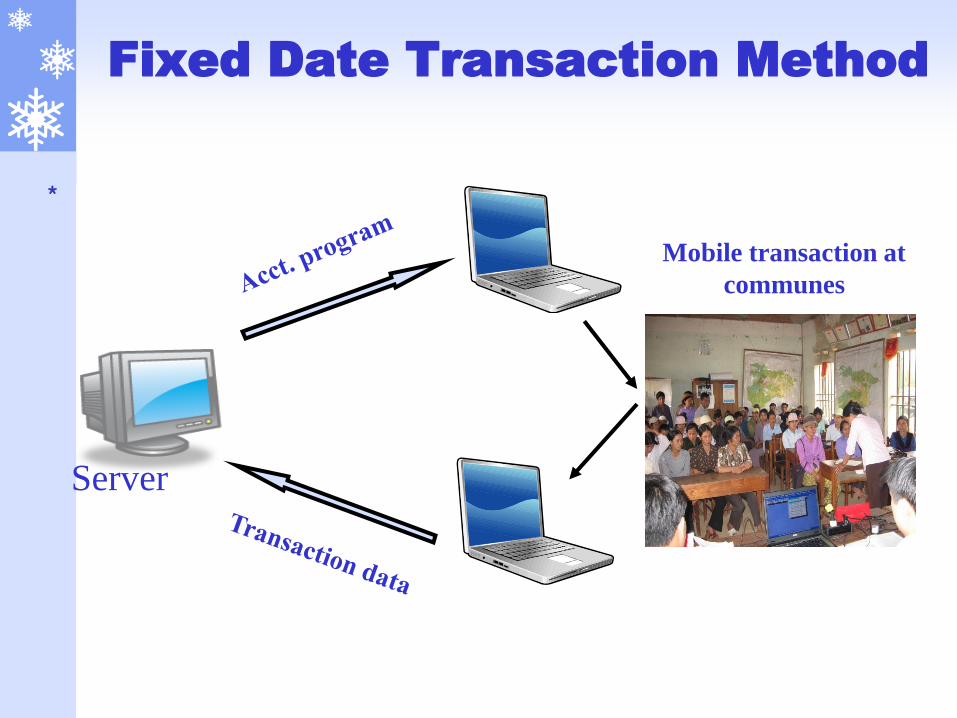

Fixed Date Transaction Method

*

Mobile transaction at

communes

Server

Part III

ACHIEVEMENTS

Knowledge Transfer

Collaboration with state agency in agriculture

extension, business models, know-how to members of

saving and credit groups including women

Economic Impact on Women

2002-2014

Outstanding loan to Women: VND

52,000bil ($2.2 Bil) – 44% of total

Savings of women: VND 1,800 bil

( $90 mil) - 50% of total

2.8 million women households

borrowing -40% of total

Non-performing loan: 0.4%

Providing small loans, technical assistance and

targeted service outreach,VBSP makes

financial products and services accessible and

affordable to the poor and women.

VBSP contributes to raising women’s

status financially and socially so that the

disadvantaged women can develop themselves

and have greater roles in their communities.

Women’s Economic and

Social Empowerment

Impact on Women…

Top Related