Languages

Pages

Legal

www.worldbank.org/id www.worldbank.org/indonesia

Indonesia Economic Quarterly: December 2011

Enhancing Preparedness, Ensuring Resilience

Shubham Chaudhuri Indonesia Lead Economist

World Bank

December 14, 2011 Jakarta, Indonesia

2

Outline

What I’ll be talking about

Developments in the last quarter: more of the same

Global economic outlook continues to deteriorate

Financial markets continue to be volatile

The real economy remains little affected, thus far

Looking forward: enhancing preparedness to ensure resilience

How the global economy might evolve: baseline as well as more adverse

scenarios

Fiscal measures to enhance preparedness: the 2012 budget

Ensuring financial sector stability

Structural reforms to ensure resilience

Revitalized manufacturing sector key to resilience and medium-term growth

A decade of slow recovery

Constraints on growth

Renewed opportunities for growth

Developments in the last quarter: more of the same

Source: Bloomberg, Consensus Economics

-1

0

1

2

3

4

5

-1

0

1

2

3

4

5

2011 2012 2011 2012 2011 2012 2011 2012

US Euro area Japan Indonesia's MTP

Mar-11 Jun-11 Sep-11 Nov-11

Percent Percent

4

Global economic outlook continues to deteriorate…

Growth projections for selected economies

…with lower growth projections for Indonesia’s trading partners

International Stock Markets

Note: Updated to December 9th 2011 Source: CEIC 5

Financial markets continue to be volatile…

Equity markets have fallen in Indonesia and across EMEs…

-0.5

-5.7 -6.7

-9.6 -10.3

-12.4

-14.4 -16.2

-20

-15

-10

-5

0

5

-20

-15

-10

-5

0

5

BRA PHP MYS THA IDN IND CHN SGP

From 1 Aug 2011

From 30 Dec 2010

Percent Percent

Note: Updated December 9th 2011 Sources: CEIC and World Bank

5

6

7

8

9

10

75

80

85

90

95

100

Aug-11 Sep-11 Oct-11 Nov-11 Dec-11

JCI equity (LHS)

IDR 000 per USD (RHS)

5-yr IDR government

bond yield (RHS)

1 Aug 2011=100 Percent; 000 IDR per USD

6

Financial markets continue to be volatile…

Indonesia’s asset prices have been affected

Note: Updated December 9th 2011 Sources: CEIC and World Bank

5

10

15

20

25

0

50

100

150

200

Jun-08 Aug-09 Oct-10 Dec-11

JCI equity (LHS)

IDR 000 per USD (RHS)

5-yr domestic gov. bond yield

(RHS)

2 June 2008=100 Percent; 000 IDR per USD

7

Financial markets continue to be volatile…

…but the volatility has not reached the levels of late 2008

After strong capital inflows over 2010 and the first half of 2011, Indonesia remains

vulnerable to portfolio outflows, as seen in Q3 2011

Source: BI

-8

-4

0

4

8

12

16

-8

-4

0

4

8

12

16

Sep-08 Sep-09 Sep-10 Sep-11

Net direct investment Net portfolio

Net other capital Current account

Overall balance

USD billion USD billion

8

Deteriorating global economic outlook and financial market volatility

…was reflected in Q3 Balance of Payments…

Note: * For short-term external debt by remaining maturity and update for “Nov 2011’ is Sept 2011 data Sources: BI, KSEI, CEIC and World Bank

Sensitivities to investor sentiment remain …as non-resident asset holdings have increased

9

0 25 50 75 100 125 150 175

Total FX Reserves

Short-term external debt*

Non-resident equity holdings

Non-resident local gov. securities holdings

Non-resident SBI holdings

Sep 2008

May 2010

July 2011

Nov 2011

USD billion

10

…but the real economy continues with strength

Source: BPS

Domestic drivers of growth have been robust

0

2

4

6

8

0

1

2

3

4

Sep-04 Jun-06 Mar-08 Dec-09 Sep-11

Percent Percent

QoQ seas. adjust (LHS)

Year on year (RHS)

Average (LHS)*

GDP growth,

11

…but the real economy continues with strength…

Source: BPS

QoQ growth contributions

Domestic drivers of growth have been robust

-2

0

2

4

-2

0

2

4

Sep-08 Mar-09 Sep-09 Mar-10 Sep-10 Mar-11 Sep-11 Discrepancy Net Exports Investment

Gov cons. Private cons. GDP

Percent Percent

Source: BI

125

200

275

350

65

85

105

125

Oct-08 Oct-09 Oct-10 Oct-11

Index Index

BI Retail sales (RHS)

BI Consumer Survey Index (LHS)

…and consumer sentiment remains upbeat…

12

Looking ahead: how the global economy might evolve

Continuing turmoil

Continued turmoil in financial markets Growth slowdown in US and Europe Commodity prices moderate

Higher Lower

Higher

Lower

Likelihood of scenario

Severity of impact and risks

for Indonesia

Full-blown financial crisis

Global financial markets stall (similar to 2008 Q4) Large-scale disruptive capital outflows from EMEs

Lehman-like triggering

event

Hard landing in BRICs

Severe global slowdown

More pronounced and protracted global growth slowdown Sharper fall in commodity prices

Soft landing in BRICs

Return of 2009

Global growth slowdown with swifter recovery in large EMEs

14

Continuing turmoil

Continued turmoil in financial markets Growth slowdown in US and Europe Commodity prices moderate

Higher Lower

Higher

Lower

Likelihood of scenario

Severity of impact and risks

for Indonesia

Stable transition to the “new normal”

Financial market volatility dissipates Growth in high-income economies moves gradually to long-term, lower trend levels EME growth robust

Credible and effective resolution to fiscal

and banking problems in high income

economies

15

Note: 2011 and 2012 are projections. Real ratio of investment to GDP. Terms of trade series is constructed by World Bank from monthly trade data Source: CEIC and World Bank staff projections

Previous

outcomes

Scenario 1:

baseline

Scenario 2:

possible

Scenario 3:

less likely

Ongoing

international

financial

turmoil

Global

financial crisis

and 2009-like

outcome

Severe global

slowdown

2008

2009 2010 2011 2012 2011 2012 2011 2012

Indonesian GDP

growth (percent) 6.0 4.6 6.1 6.4 6.2 6.3 5.5 6.3 4.1

Scenario assumptions:

Investment/GDP ratio

(percent) 23.7 23.4 24.0 24.5 25.3 24.5 24.5 24.5 23.6

Major trading partner

GDP growth (percent) 2.0 -1.4 6.8 3.3 3.5 3.2 2.0 3.0 -1.8

Terms of trade growth

(percent) -18.1 -4.2 5.3 10.0 0.0 8.0 -15 7.0 -30.0

The impact of the global scenarios …could be sizeable but solid growth is likely

16

Note: Data to November 2011 Source: WB

International USD commodity prices (Jan 2005=100)

50

100

150

200

250

300

350

50

100

150

200

250

300

350

Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Energy

Non-energy

Index (Jan 2005=100)

Dashed lines are Nov 2011

forecasts

Index (Jan 2005=100)

17

Commodity prices have fallen in recent months…

…but remain high from a historical perspective

Potential impact of external demand shocks

Limited trade exposures to EU and US directly...

Notes: * 2009 trade shares. EA-5 comprises Korea, Singapore, Malaysia, Thailand and the Philippines Blue indicates export share from 5 to 10 percent and pink above 10 percent Source: World Integrated Trade Solution (WITS)

Exports to:

Exports from: CHN EU IND IDN JPN KOR MYS SGP US

China (CHN) – 16.4 2.6 1.4 7.7 4.4 1.5 2.1 18.0

EU 8.4 – 2.6 0.5 3.2 2.1 0.8 1.8 18.0

India* (IND) 5.9 20.4 – 1.7 1.8 2.1 2.0 3.8 10.8

Indonesia (IDN) 9.9 8.6 6.3 – 16.3 8.0 5.9 8.7 9.1

Japan (JPN) 19.4 12.2 1.2 2.1 – 8.1 2.3 3.3 15.6

Korea, Rep.* (KOR) 23.9 11.9 2.2 1.7 6.0 – 2.1 3.7 10.4

Malaysia (MYS) 12.6 10.5 3.3 2.8 10.4 0.0 – 13.4 9.5

Singapore* (SGP) 7.5 10.0 3.8 9.4 4.7 4.1 11.0 – 6.5

US 7.2 20.0 1.5 0.5 4.7 3.0 1.1 2.3 –

East Asia-5 14.2 11.4 2.8 4.5 7.5 1.7 5.3 4.9 9.3

Share of total merchandise exports in 2010, percent

18

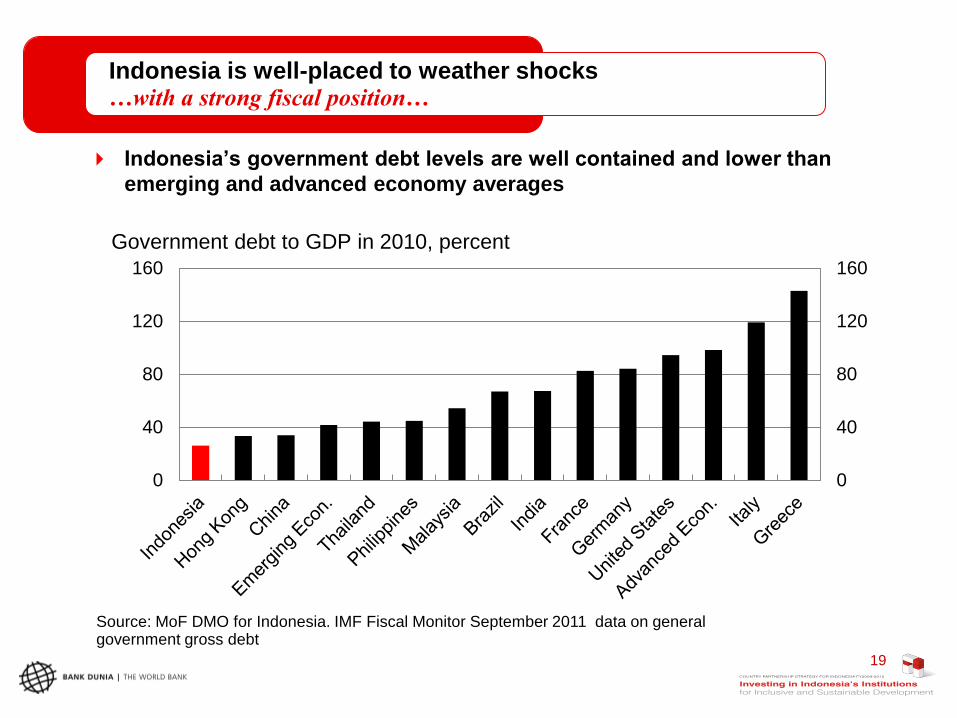

Source: MoF DMO for Indonesia. IMF Fiscal Monitor September 2011 data on general government gross debt

Indonesia’s government debt levels are well contained and lower than

emerging and advanced economy averages

0

40

80

120

160

0

40

80

120

160

Government debt to GDP in 2010, percent

Indonesia is well-placed to weather shocks …with a strong fiscal position…

19

Sources and notes: IMF Public Debt database plus IMF Fiscal Monitor, BPS and GoI-MoF.

But, Indonesia is well-placed to weather shocks …and a remarkable record of debt reduction…

20

Source: MoF. IMF Fiscal Monitor September 2011 (data for 2010), World Bank estimates

Indonesia’s fiscal balance has space to respond to a crisis and is better

placed than most emerging and advanced economies

-12

-8

-4

0

-12

-8

-4

0

2010 fiscal balance as percent of GDP

But, Indonesia is well-placed to weather shocks …and relatively low fiscal deficit

21

Looking ahead: enhancing preparedness to ensure resilience

23 Sources: Budget outcomes, APBN, and APBN-P

Budget Table (IDR trillion)

The 2012 budget is consistent with the baseline scenario of resilience…

…and targets a budget deficit of 1.5% of GDP

2008 2009 2010 2011 2012

Actual

Audited

Actual

Audited

Actual

Audited APBN-P APBN

A. State Revenues and Grants 982 849 995 1,170 1,311

I. Domestic Revenues 979 847 992 1,165 1,311

1. Tax Revenues 659 620 723 879 1,033

2. Non Tax Revenues 321 227 269 287 278

B. Expenditures 986 937 1,042 1,321 1,435

I. Central Government

Expenditure 693 629 697 908 953

K/L spending 299 358 395 548 591

Capital Expenditure 73 76 80 141 168

Non-K/L Spending 394 271 303 360 361

Interest Payments 88 94 88 107 122

II. Transfers to Region 292 309 345 413 470

Surplus/Deficit -4 -89 -47 -151 -124

Deficit (% of GDP) -0.1 -1.6 -0.7 -2.1 -1.5

24

…but the 2012 budget also has measures to enhance crisis preparedness

2012 Budget introduces new measures which support stability

• Bond stabilization framework: number of actions to stabilize the government bond market in the event of a sudden reversal in capital flows or shocks

• buying back bonds in secondary markets by using allocated budget funds or other sources such as the Government’s un-spent fiscal balance (SAL) and the buy-back of bonds by SOEs under coordination of the Minister for SOEs

• Article 43: measures that allow GoI to respond rapidly to a crisis, subject to parliamentary approval, which is required within 24 hours:

• increase bond issuance

• seek alternative financing sources from bilateral and multilateral creditors

Budget financing

• Article 43: measures that allow GoI to respond rapidly to a crisis, subject to parliamentary approval, which is required within 24 hours:

• carry out expenditures that have not been budgeted

• use un-spent fiscal balance (SAL)

Fiscal measures

Any contingent plan for fiscal stimulus must address budget execution…

Sources: MoF and World Bank

Actual spending (by Nov) of revised budget

…which remains a challenge

0

20

40

60

80

100

0

20

40

60

80

100

Personnel Material Capital Energy Subsidy

Social exp

Total Central

Govt

Transfers

2008 2009 2010 2011

Percent Percent

25

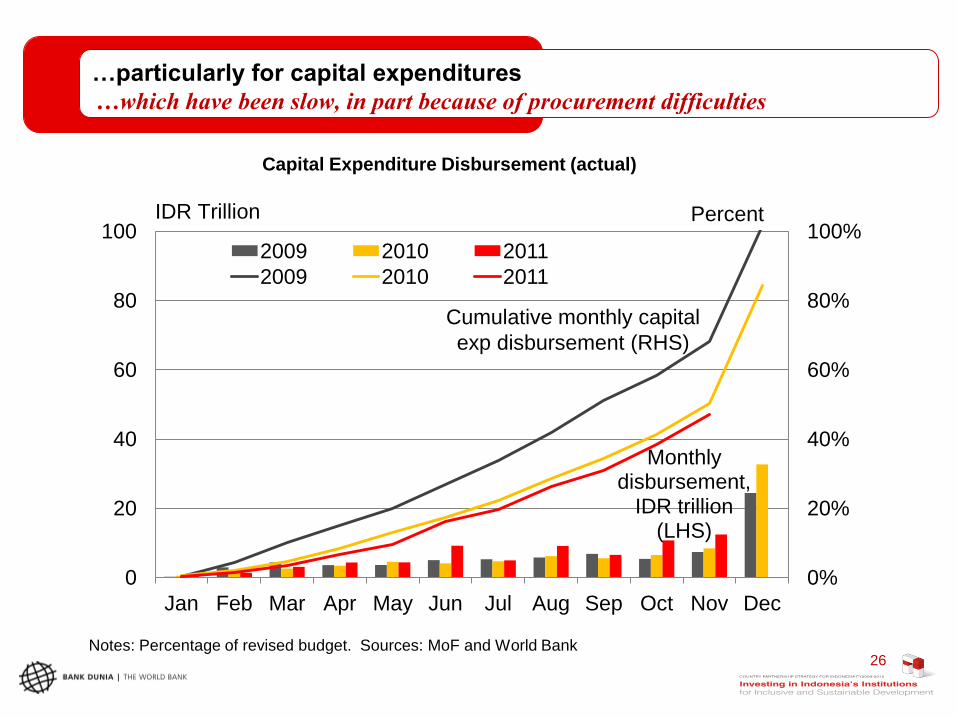

…particularly for capital expenditures

Notes: Percentage of revised budget. Sources: MoF and World Bank

Capital Expenditure Disbursement (actual)

…which have been slow, in part because of procurement difficulties

Monthly disbursement,

IDR trillion (LHS)

0%

20%

40%

60%

80%

100%

0

20

40

60

80

100

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2009 2010 2011

2009 2010 2011

IDR Trillion

Percent

Cumulative monthly capital

exp disbursement (RHS)

26

Fiscal measures to ensure resilience: redirecting public expenditures

Sources: MoF

Budget expenditures

…which are skewed towards energy subsidies

0

1

2

3

4

5

0

1

2

3

4

5

2008 2009 2010 2011 2012

Energy subsidy Capital exp Social exp

Percent of GDP Percent of GDP

27

The budget deficit is projected to fall in 2012

Sources: MoF and World Bank

Budget balance

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

2008 2009 2010 2011 2012

APBN APBN-P Actual World Bank Projection

Percent of GDP Percent of GDP

28

Policies to enhance preparedness to ensure resilience

Robust contingency planning is critical

29

Currently, under the baseline scenario, no need for immediate emergency measures…

…in fact important to avoid policy missteps and hasty measures that might send the

wrong signal in a fragile market environment

But critical to prepare for more adverse crisis scenarios by:

revisiting and rehearsing financial crisis management protocols, and putting in place

needed financial stability regulations

considering contingent budget financing to support critical public expenditures

preparing contingent plans for fiscal stimulus measures to support growth

preparing contingent plans for social assistance measures to cushion poor and low-

income households adversely affected by economic shocks

…and also important to continue to push forward on key structural reforms

To enhance long-term growth prospects AND support investor confidence

To improve domestic competitiveness to help in adjustment to appreciation with likely

resumption of capital inflows over the medium-term

Policies to enhance preparedness to ensure resilience

Structural reforms to maintain and enhance competitiveness

30

Manufacturing sector, perhaps more than any other, is likely to come under stress in the

event of a global economic slowdown

Manufacturing sector, in the last decade, has experienced a growth recession…

…and though there are signs of a pick-up, will be particularly important to take steps to

enhance the competitiveness of the manufacturing sector so as to enable it to contribute to

both growth and high value-added job creation

Key to both ensuring the near-term resilience and to sustainably enhancing the medium-

term competitiveness of the manufacturing sector is:

addressing infrastructure bottlenecks

reducing regulatory uncertainty and burden

Short-term measures that do not address the underlying structural impediments to the

competitiveness of Indonesia’s manufacturing sector are unlikely to lead to sustained

Revitalizing and enhancing the competitiveness of the

Indonesian manufacturing sector

Sjamsu Rahardja Indonesia Senior Trade Economist

World Bank

32

Impact on employment creation and additional source for formal jobs

Staff estimates from Sakernas

Employment cross-elasticities to growth in

manufacturing activities 1990-2009

-0.53

0.65

1.13

0.42

0.59

-1.0

-0.5

0.0

0.5

1.0

1.5 90%

82%

69%

47%

44%

23%

10%

Finance

Public Sector

Manufacturing

Trade and Transport

Construction and Utilities

Others

Agriculture and Mining

Formal jobs across sectors (August 2010)

Indonesia’s manufacturing sector has experienced a slow recovery in

the 2000’s...

Sources: BPS, World Bank WDI and World Bank staff calculations

Growth rate of real GDP and Manufacturing

0

2

4

6

8

10

12

14

16

0

2

4

6

8

10

12

14

16

1990

1991

1992

1993

1994

1995

1996

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

GDP

Non-Oil and Gas Manufacturing

Pre 1997-98 crisis

Post 1997-98 crisis

Percent Percent

Manufacturing real growth

33

…except for transport equipment, output growth in all manufacturing

sub-sectors has declined

Note: FBT is food, beverages and tobacco. Cement & minerals include only non-metal minerals

Sources: BPS and World Bank staff calculations

Average annual growth

-5

0

5

10

15

20

-5

0

5

10

15

20

1993-96 2001-10 Percent Percent

34

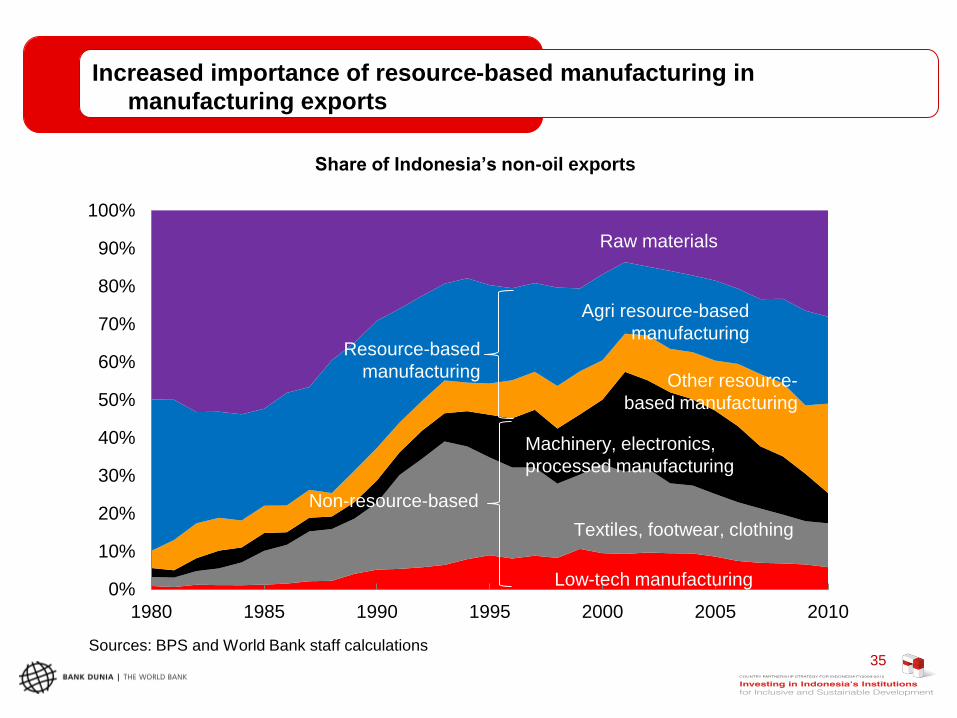

Increased importance of resource-based manufacturing in

manufacturing exports

Sources: BPS and World Bank staff calculations

Share of Indonesia’s non-oil exports

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1980 1985 1990 1995 2000 2005 2010

Machinery, electronics,

processed manufacturing

Textiles, footwear, clothing

Low-tech manufacturing

Non-resource-based

Resource-based

manufacturing

Raw materials

Agri resource-based

manufacturing

Other resource-

based manufacturing

35

What factors explain Indonesia’s recent manufacturing sector

performance?

The major constraints on business vary across the type of firms within

Indonesia’s manufacturing sector

Sources: World Bank Enterprise Survey (2009) and World Bank staff calculations

Percentage of firms within each group reporting the following issues as severe or

major constraints for businesses

0

10

20

30

40

0

10

20

30

40

Large firms Small firms Exporting firms

Percent Percent

37

38

Indonesia’s manufacturing exports face relatively high cost of logistics

World Bank Logistics Performance Indicators

Comparisons of speed and costs of logistics

1.4

2.6

1.7

5.4

2.8

5.0

2.6

2,225

397 500

701

341

1,238

302

-

500

1,000

1,500

2,000

2,500

-

1.0

2.0

3.0

4.0

5.0

6.0

Bangladesh China Vietnam Indonesia Malaysia Philippines Thailand

Lead time import for port/airport, median case (days)

Avg charge (US$) for 40-foot container (import + export) (right axis)

39

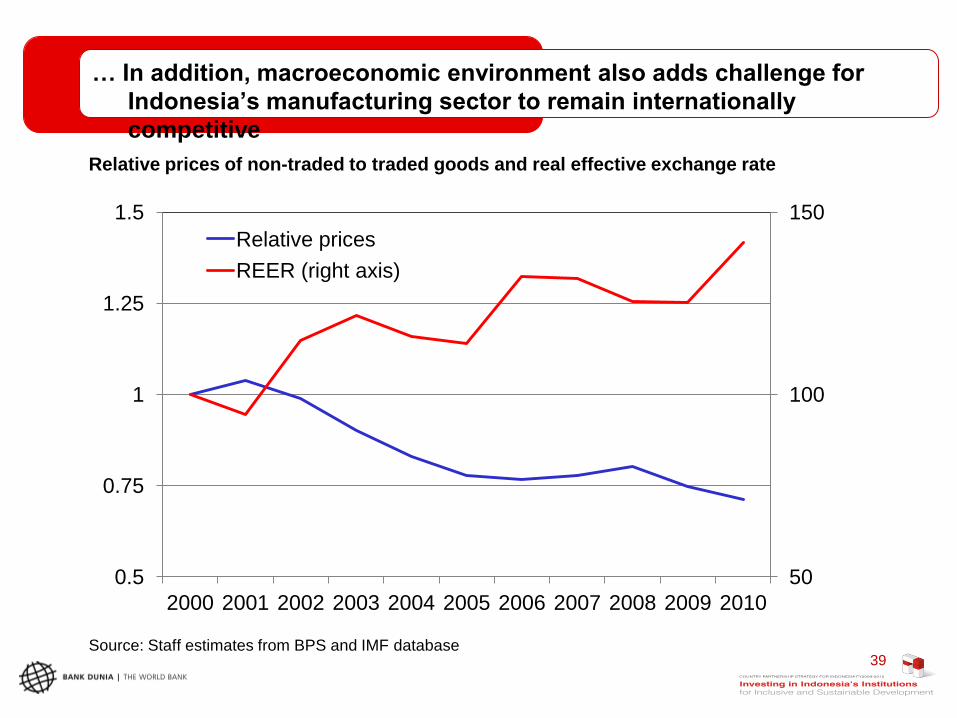

… In addition, macroeconomic environment also adds challenge for

Indonesia’s manufacturing sector to remain internationally

competitive

Source: Staff estimates from BPS and IMF database

Relative prices of non-traded to traded goods and real effective exchange rate

50

100

150

0.5

0.75

1

1.25

1.5

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Relative prices

REER (right axis)

Are we seeing renewed opportunities for Indonesia’s manufacturing

sector?

Manufacturing activities have shown strong recovery in recent

quarters…

Sources: BPS and World Bank staff calculations

-20

-10

0

10

20

30

40

-4

-2

0

2

4

6

8

Sep-07 Sep-08 Sep-09 Sep-10 Sep-11

Manufacturing production index (LHS)

Domestic demand (LHS)

Investment in machinery (RHS)

Percent Percent

41

Manufacturing activities in Indonesia are also likely to be boosted from

investment from firms that are relocating to Indonesia

60

75

90

105

120

135

150

60

75

90

105

120

135

150

2000 2005 2006 2007 2008 2009 2010

China

Indonesia

Vietnam

unit labor cost index, USD, 2005=100

42

• Actions to strengthen coordination and coherence in government policies

•Actions to improve efficiency in production process and capacity expansion

•Efforts to enhance capacity to innovate

•Efforts to develop financial sector to support manufacture operations

• Improvement in cost competitiveness

•Establishing core for value-based competitiveness

•Reducing opportunity costs for investing in manufacturing sector

One possible framework to sustain momentum for growth in

Indonesian manufacturing sector

www.worldbank.org/id www.worldbank.org/indonesia

Indonesia Economic Quarterly: December 2011

Enhancing Preparedness, Ensuring Resilience

December 14, 2011 Jakarta, Indonesia

Top Related