Languages

Pages

Legal

Forex 2018

www.matrixtrade.com Page 1 of 20

INTRODUCTIONTheoutlookfortheforeignexchangemarketin2018is,likeanymarket,dependentontheinteractionandtrendsofFITS(fundamentals,intermarketrelationships,technicalandsentiment).ThisinteractionexplainswhycurrenciescanandfrequentlymoveawayfromtheirtraditionallysignificantinterestdifferentialsintheshorttoneartermastheEurohasdonesinceJuly.ItcertainlyexplainswhysomecurrenciesliketheCHFseemtoignoretheirpurchasingpowerparity(PPP)forprolongedperiods.Italsoaccountsfortheunderestimationof,oncetheoreticallyimportant,tradeflowseventhoughthecurrencyofthecountrywiththelargestcurrentaccountdeficits,theUnitedStates,wasamongst2017’sworstperformers.ItalsocruciallyexplainswhytheUSDhaslostitsriskstatus(correlationtoSPX)in2017.HowacombinationofthefourFITSpillarsmanifestsitselfcontributesto,butalsodependson,volatilityandthereforeclarity(VC).Movementsinvolatile(particularlyfundamental)trendstendtobeclearerthanconsolidationmarkets,atleastinretrospect.Althoughanyofthesefactorscanbeobscuredintheforexmarketascurrenciesareexpressedintermsofanothercurrency(orbasketegDXY),whenoneoftheFITSofanymarketisdominantittendstosupersedeallothers.Sterling’ssentimentdrivenBrexitcollapseinJune2016stillcastsalongshadowovertheCablemarketandindeedtheUKeconomy.TheFundamentalprospectofTrumpflationarygrowthdrovetheUSDhigheragainstmostothercurrenciesinto2017.Incontrasttotheequitymarkets,itwasthenreversedevenagainsttheBrexitbeleagueredGBPformostoftheyearpartlybecauseUSinflationdidnotrisetotheextenteithertheFedortraders’anticipated.ThisoverestimationwasalsocompoundedbyTrump’swishforaweakerdollarcombinedwithpoliticaluncertaintyathomeandabroad.Addingtothedollar’swoes,wasthe‘Sintrapact’inJunethatsawaco-ordinatedsteptowardstighteningbytheECB,theBoEandtheBoC,andpavedthewayforallthreebanksmakinghawkishpolicychangeslaterintheyear.ThemainbeneficiarywastheEuro.TheECBwasnotablysluggishinannouncingthetaperingofitsquantitativeeasingprogrammeeventhoughtheEuropeaneconomycontinuedtorecoverandshruggedoffpoliticalconcernssurroundingBrexitandFrench/GermanelectionsandevenCatalonia.WhereasthepersistentcampaignoftheSNBhasensuredprolongedCHFweaknessagainsttheEuroandstabilityversusthesimilarlyweakDollar.Despiteboutsoftwo-wayBrexitinspiredvolatility,Sterlingremainedstabletostrongthroughouttheyear.Ourtheory,thatuncertaintyaboutuncertaintycreatesinertiauntilitisresolvedeitherway,hasbeenborneout.WhenBrexitnewshasn’tbeenforthcomingasurprisinglyresilienteconomyandinflationoutlookhashelpedmaintaintheGBPUSDupdrift.Aself-correctingirony:Sterlingweaknesshadpushedinflationupto3.1%inturnhelpingthePoundtorecover.Intermarketrelationshipsforcurrencieshave,attimes,borderedonthebizarre.Thethreemainlinks(interestratesandtherelatedcommoditiesandriskappetite/aversionwithstocks)havevacillatedandvariedaspartofageneralmarketcorrelationbreakdown.10yearUSyieldshaveremainedrangeboundarounda2.3%pivotallyearandwhiletheFedhasraisedthreetimesnowtheFederalFundsRatesitsinthe1.25-1.5%range.ClearlythemarketisstillscepticalaboutsustainedinflationandtowardstheendoftheyeartheoutgoingFedChair,JanetYellen,admittedshefoundthelowinflationa‘mystery’,aclearbreakfromthepreviousmessageitwas‘transitory’.

Yielddrivencurrencymovesthencanbeexplainedpartlybyachangeintheyieldcurvebutmorebyuncorrelatedmovementsinothercountries’bondmarkets.Formuchoftheyearcertaincurrencypairshavecorrelatedstronglywithinterestrates.EURUSDgrippedits10yearyieldspreadforthefirstsixmonthsuntiltheJuly20thECBmeeting

Forex 2018

www.matrixtrade.com Page 2 of 20

butthereaftercontinuedtorallywhileitsdifferentialdowntrendedfortherestoftheyear.Basedon10yearinterestyieldsaloneEURUSDshouldhaveclosedtheyear900pipslower!Thankfullywechosetoignorethis.USDCADhasbeentiedtoitsfallingdifferentialallyearwithanydivergenceprovingmomentaryandoftenflaggingareversalinthecurrencyasitcamebackinline.SomeofthatdivergenceisduetoOilinCanada’scasebutthatinturnhasledtoanassociatedmovementintheCanadianbondmarket.ThedelayedreactionhasoftencounterintuitivelyseentheCanadianDollarmoveintheoppositedirectiontoOil.Similarly,theAussiehasbeenbuffetedbycommoditymovementbuttypicallywithatimelag.Its4.2%yearendsqueezecanmainlybeattributedtoGold’srecoveryratherthanonlya11basispointdifferentialreboundeventhoughthisstartedearlierinNovember.PoliticsratherthanmilkhasbeenthemaindriveroftheKiwi’swhipsawtrendsandsawNZDrampwhileitsdifferentialcollapsedinDecember.Whatisnormallyseenasayield/riskappetitecurrencyhasignoredstockmarketsformuchof2017.Butthemostinterestingbreakdownincorrelationhasbeentheapparentendofthe11yearbondbetweenUSDJPYandtheNikkei,whichweflaggedaspossiblyourboldestcurrencypredictionof2017,andapreconditionofanendtodeflation.AlthoughthiscaninpartbeattributedtoUSDJPY’smorepowerfulcorrelationto10yearyields,itreflectsamoregeneralbreakdownintraditionalcurrencyriskappetite/aversionrelationships.Therootcauseofthecurrencydisconnect,webelieveisthedisintegrationoftheriskstatusoftheworld’sreservecurrency,theUSD.Attheendof2017theDollarIndexclosed10.55%lowerandtheS&P20.6%higher.Thelasttimewesawsuchaninversionwasatthestartofthestockbullmarketin2009(duetoQuantitativeEasing).2010sawthemslowlybutsurelycomebackinlinebeforebothralliedfortheensuing6years.Theconsequenceof2017’sbreakdownhasbeenvariedandarguablybizarre.Thosecurrencypairsthathavestucktotheirinterestratedifferentialshavetradedastheywouldinriskaversionmodeiestocksfalling.TheprimeexampleswouldbeEURUSDstrengthandAUDweaknesshenceEURAUDstrength.Howeverothersafe-haven/riskaversionpairssuchasEURCHFandJPYcrosseshaverallieddivergingfromtheirdifferentialsinthelastsixmonthsandreflectingstockstrength.TraditionalTechnicalAnalysisofforeignexchangehasbeenunderminedbytheweaknessinthemarket’sglue.Potentiallysignificantbreakshavefrequentlyprovedfalseatleastintheshortertermwithcurrenciesrollingbackintotheirrange.Onceuponatimewecouldhaveblamedthisonvegatradingbyoptionsdesks.Butthistimeitissymptomaticofabrokenmarket.TheAustralianDollarisprobablytheprimeexamplein2017totheextentyoualmosthadtowaitforafalsebreakbeforeitreversed.Similarly,thesequenceofpotentiallyabortivebearishEURUSDHeadandShoulderspatternshasironicallybeenausefulguidetonursingabullishtrade.2017hasprobablysetarecordforredrawntrendlinesandresurrectedthe‘thirdtrendlineisagoodone’maxim.Althoughwearegenerallynotfansofdailyorweeklyclosebasedanalysisthishasprovedasaferandtruerguideforgenuinebreaksformuchof2017.Theproliferationofwedgesisalsotestimonytoamarketthatistryingtotrendbutbroughtbackbyoppositemovementsinotherrelatedmarkets.WhenmarketsbehavelikethisitnormallysuggeststheyarebeinginfluencedbylargerflowsinothercurrenciesoftenwhereoneoftheFITSismoredominant.Forewarnedisforearmed.Therearetwopowerfultechnicaltemplatesforthecurrentforexmarket.USstockmarketshavefollowedaslower(delayed)butconsequentlymoreaggressiveversionoftheir1987blowout.AswehaveseentheForexmarketbehavedoddlybutthereforeverymuchlikeitdidin1987without,asyetthedramaticriskaversionfinaleassociatedwiththe1987stockcrash.Althoughtheforexoutlookfor2018wouldseemtobegthequestionofwhetherindices(andthereforesafehaven/riskaversionpairs)willturn,wearefortunatethatmanycurrencies(notablytheUSDandparticularlyEURUSD,AUDUSDandGBPUSD)arealsofollowingverysimilarpriceactionin2002-2003–aperiodwherestockswereflattodownbeforealargerrecovery.Inotherwords,therearetemplatesfortheforexmarketthatarenotentirelydependenton(althoughinfluencedby)whatthestockmarketsdo.

Forex 2018

www.matrixtrade.com Page 3 of 20

TherearemanyotherweakerprecedentsforthistypeofmarketwhereintermarketandtechnicalfactorshaveunderperformedbuttheyarenormallyseenattheendorindeedstartofamajorglobaltrendwhereSentimenthasbecomethemaindrivingforce.ExtremesentimentinamajormarketsuchasUSindiceswillinevitablyspilloverintootherrelatedmarketsduetostockrelatedflowsandstockassociatedsentiment.TraderswillsellCHFandJPYinordertofundpurchaseofhigheryieldingcurrencies/assetsbutalsobecausethoseloweryieldingcurrenciesareweak.Thiscomplicatessentimentanalysisofforeignexchangeascurrencyflowsarenolongerisolated;thatistheyincreasinglycontainanadditionalstockoryieldrelatedelement.AmarketsuchastheEURmayappearoverlybullishbutnewentrantsmaycomeinandbuysignificantamountstransformingamarketthatmayindeedbelongtoonethatisnetshortbutstillbullish.ThisadditionallongtermfundbuyingisprobablythemainreasonforthegrowinggapbetweenEURUSDanditsinterestdifferentialoverthelastsixmonths.Theironyandaninterestingfeaturefor2018isthatshouldstocksturn,ratherthanprovokealiquidationofthelongEURUSDtrade,itcouldexaggeratetheuptrend.Asaconsequence,forexsentimenthasbeenconfusedformuchoftheyear.Itisnaturaltoseektrendandquickly.Butayearoffalsebreaks,slowtrendsorconsolidationshasseencurrenciestakeoutweakpositionsleavingthemarketoverlylongorshortandthereforeretracebeforeresumingthepattern.2017maywellgodownastheyearoftheForexcynicorthehesitantCentralBank.Despitemomentsofastutepresentation,theECBhasfailedtograspthesentimentoftheForexmarket.TheyexpressedconcernonanumberofoccasionsabouttheappreciationoftheEuroandseeminglydelayedthelongoverdueTaperasaresult.AndyetthisdelayhasitselffedEurostrengthdenyingthemarketitsfavorite‘buytherumorsellthefact’.Theoutlookfor2018thereforedependspartlyonwhetherthesetrendsinFITScontinueandthereforewhetherUSinflationandinterestrates/yieldswillnotriseasmuchaselsewhere.Toappreciatewhatmayhappenin2018requiresanunderstandingofwhereeachcountrysitswithinitseconomiccyclecomparedtoothersbutalsotheattitudeofCentralBanksandtheirrespectivepolicies.CertainlytheUShasbeenattheforefrontofeconomicgrowth.ItisnotclearwhethersubduedUSinflationreflectseitheralessthanrobusteconomyoranecommerceinspiredchangeinthenatureofinflation.ButeitherwayanhistoricallyslowUStighteningphasehasencouragedcentralbankselsewheretofollowsuitandditheranddelay.Thisnotonlyrisksashiftinrelativeinflationratesandconsequentlyyieldsbutmaywellservetoperpetuatetrendstheywishtoavoid.Twotrendswedoexpecttoseein2018:Firstly,justasstocksexceededevenouraggressivelybullishtargetsfor2017,theForexmarkethasthepotentialtoregainvolatilityandexceedmanyexpectations.Secondly,justlike2010theForexmarketshouldslowlybutsurelycomebacktogetherin2018—hopefullymakingmarketseasiertotradeandcertainlytounderstand.

Forex 2018

www.matrixtrade.com Page 4 of 20

EURUSD

LongEURUSDwasourprojectedhighlightforthelatterpartof2017andcouldwellbeforthenext4years.In2016wehighlightedlongEURUSDwouldbetheForexTradeof2017basedonthePandora’sBoxAnalogywehavefollowedformuchofthisdecade.ThisandthesimilarleadingGold(WashingtonGoldagreement)priceactionin1999arguedtheEurowassettingabasewithinarepeatingpatterninarisingwedgedatingbackto1985(whenitwas$-Deutschmark).Thissuggesteditwouldeventuallysecureanotherrunatthehighsonceitregainedweeklydowntrendnowat1.2636.Italsoprojectedaninterimconsolidationbase16yearsafterthepreviousconsolidationbase(thatwasalso16yearsafterthe1985low).Furthermore,itforecastthat,oncetheEurobroketheeffective1.1550consolidationhighthiswouldbemaintainedina218-weekuptrend–amajorbullmarket–thatcharacteristicallyabortedabearishHead&Shoulders.Althoughthemarginalnewlowto1.0340atthestartof2017wasslightlyoutofsynch,EURUSDsubsequentlyproveditwasstillfollowingthispatternandthereforeanuptrenddrivenbyeconomicresurgenceinEurope,acatchupwiththeUSandarelativefirmlyofyields.IndeedthisyieldviewissupportedbythelongtermMatrixcurrencyfractal(where3monthforwardsareleadingtheEURUSDhigher-seebelow).WethereforeremainbullishtheEuropotentiallyforabreakof1.2635toconfirmatleast1.3710-1.40.Thetimingofanyupwardaccelerationandthereforelikelyhighfor2018dependspartlyonthestructureoftherally(andpossiblystockdisinvestmentfromtheUS)andtheextenttowhichtheItalianelectionsearlyMarchwillserveasabrake(NotetheFrenchElectionsin2017initiallyslowedtheuptrendbutthengaveitlaterimpetus).Withanoutstandingsixmonthtargetfrom2017of1.2340wemayhavetotolerateaperiodof1.1550-1.2635consolidationbeforetheuptrendcangathermomentumeventhoughhistoryfavorsacontinueduptren

Alossof1.1550wouldsuggest1.11inadeepercorrectionbutonlyabreakofthe1.0340lowabortsthislong-termpatternforanaggressivespikesubparity.

Forex 2018

www.matrixtrade.com Page 5 of 20

USDJPY

Thereissurprisinglylittlechangeinourviewfrom2017asUSDJPYhasspent43weeksofthelastyearina107.35-114.70rangeandthereforesitsneatlybutperhapsdisappointinginapotentialconsolidationtop.Contextisimportanttounderstandingwhatthisrepresents.Withina20-year75-145prolongedconsolidationthe50yenUSDJPYrallyfollowingthe2011earthquakeshouldrepresentthefirstlegofanotherrunatthe145high.The50%pullbackto99.10waseasilyenoughindistancetosatisfythecorrection.

Althoughitisthereforeeasytobelievethecurrentimpulsiverecoveryisaresumptionofthatuptrend,bothoursofarsuccessfulEarthquaketemplateandaverysimilarimpulsiverecoveryin2000suggestthiscouldbetheearlystagesofatleastprolongedconsolidationinthe100-125rangeifnotapotentiallylargeralbeitcorrectivedecline.ThelongerUSDJPYcanstaybelowideally114.70nowbutmoresignificantly125.80thennotonlycanweexpectareturnto99.15butpossiblybreakingdownto94.75(61.8%)even87.40(76.4%)inapossiblecontinuedreflationinspireddisconnectwiththeNikkei.Itisthereforeonlyafteralongerand/ordeepercorrectionthatwecanseeUSDJPYbreakthe125.80highalthougharallythrough114.70and118.90wouldincreasetheprobabilityofaprematuretest/break.

Forex 2018

www.matrixtrade.com Page 6 of 20

GBPUSD

GBPUSDstandsoutasthecurrencypairwiththegreatestpotentialtosurprisewithaBrexitunwindin2018,particularlyafterapossibleperiodofgeneralSterlingweaknessatthestartoftheyear.Followingwhatappearstobeapossiblycompletethreeleggeddeclinefromthe2.11602007high,theFatFingerspiketo1.1815(possiblylower)marksapotentialbasefromarecoverybackthroughthepreBrexitreferendumlowsof1.3653-1.3833initiallybackto1.4320(50%butwithpotentialforareturntothepreBrexithighof1.50(61.8%)andpotentialdownchannelresistance.Inthisrespectacontinuedsimilaritytothe2001-2007uptrendisinstructive.Soalthoughwecouldtoleratefurtherconsolidationbelow1.3654eventotheextentofspikingbelow1.30to1.2775-1.2815,whileGBPUSDisabove1.25thentherewillremainawindowtoresumeapotentialsixyearuptrend.AsurprisingthumbsupforBrexit?!

Forex 2018

www.matrixtrade.com Page 7 of 20

EURGBP

EURGBPremainswithininalongertermuptrendreflectinginherentweaknessthatpredatesBrexit.

Followingaclearlycorrectivesevenyearretracementfrom0.9800to0.6945theimpulsiverecoverytotheFatFingerhighof0.9365(followingsimilarpriceactiontotheUK’sexitfromtheERMin1992)shouldrepresentthefirstofathree-leggedmoveinarisingwedgetoa1.0577equalitytarget.However,that24centuptrendneedstobecorrected.SoalthoughEURGBPhassettledintoaBrexituncertaintystasisina0.8300-0.9365rangethisshouldeventuallygivewaytoadeepercorrectionin2017toacurrent0.8245(c=a)equalitytargetprobablyanideal0.814850%anevenaslowas0.0.786061.8%?Oncethecurrent0.83consolidationisspikedandregainedEURGBPwillbeinapositiontobreak0.9365tochallengethe0.98high.ThiscorrectiveconsolidationphaseissupportedbytheremarkablyaccurateMatrixCurrencyFractal(3monthEURGBPforward)thatdiscountedtheLeavescenariowhenthereferendumwascalledinFebruary2016.

Forex 2018

www.matrixtrade.com Page 8 of 20

USDCAD

Withinanobviousandbroad0.90-1.60longtermrange,USDCADremainswithinanoilandinterestratedrivendowntrendtoatleast1.1410(61.8%)andprobably1.1035likelychannelsupportandthesamesizeofthepreviousdecline.Despitethepersistenceofthenotdissimilar2008-2011downwardratchetitisnosurprisetofindtheselloffrom1.4690takingtheformadecliningwedge.SOalthoughthisallowsaperiodofapproximate1.20-1.30equilibriumconsolidationralliesshouldcontinuetofadeinthe1.29-1.31regionforaneventualbreakdownthrough1.1915tothenextobjectiveat1.1540(c=a)

Forex 2018

www.matrixtrade.com Page 9 of 20

AUDUSD

AUDUSDcontinueswithinasteadyupwardratchetfromthe0.6835lowthatmaintainsa2001-2004inspiredwindowtoaccelerateatsomepointthroughthepivotal0.8430-0.8660toatleast0.945561.8%.AlthoughthisrecoveryappearslaboredandthereforepossiblycorrectiveitistypicalofoneofAussie’sfavoriteformations:theleadingdiagonalorwedge.Thereforeeventhoughthissuggestsapotentialspikeonlyof0.8160in2018possiblyfailingbelow0.8430,weexpectanapproximate75-84rangeformuchoftheyeartocreateabasefromwhichtogatherupwardmomentum.Althoughalossof75wouldappearatoddswiththe2002templateonlyalossof0.7140threatenstobreakthe0.6830lowdownto60.

Forex 2018

www.matrixtrade.com Page 10 of 20

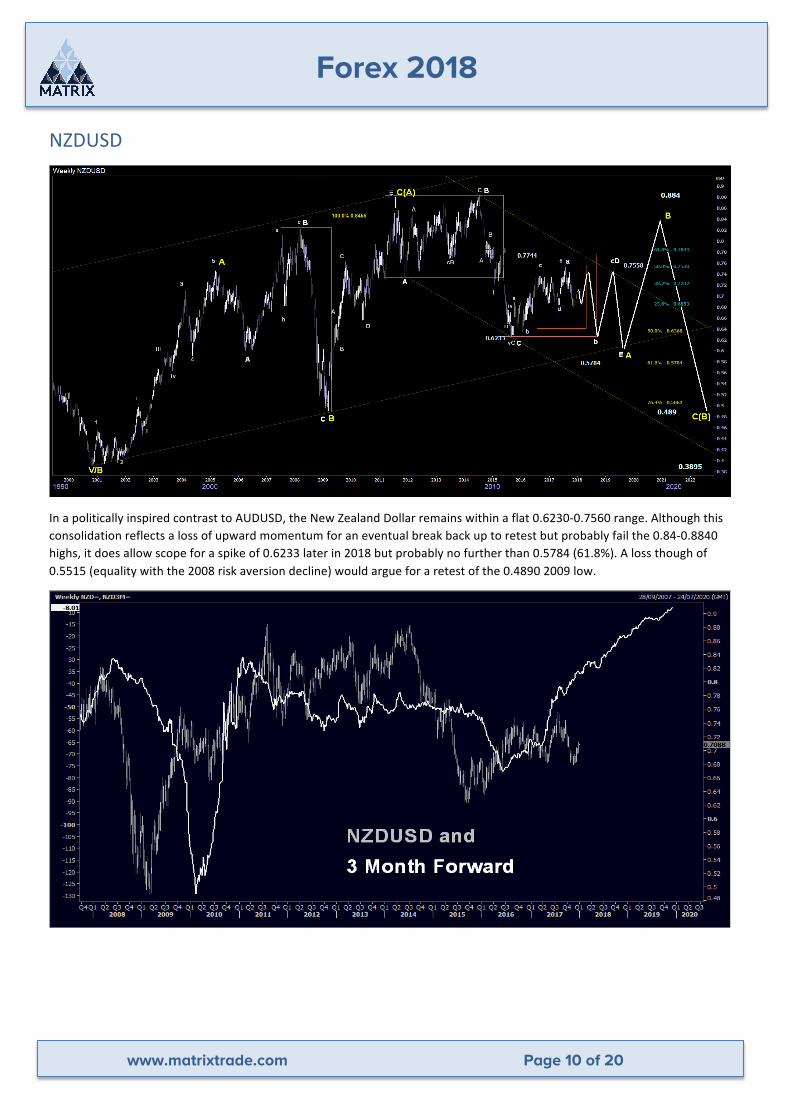

NZDUSD

InapoliticallyinspiredcontrasttoAUDUSD,theNewZealandDollarremainswithinaflat0.6230-0.7560range.Althoughthisconsolidationreflectsalossofupwardmomentumforaneventualbreakbackuptoretestbutprobablyfailthe0.84-0.8840highs,itdoesallowscopeforaspikeof0.6233laterin2018butprobablynofurtherthan0.5784(61.8%).Alossthoughof0.5515(equalitywiththe2008riskaversiondecline)wouldargueforaretestofthe0.48902009low.

Forex 2018

www.matrixtrade.com Page 11 of 20

APPENDICESHerewepresentcharts(inalphabeticalorder)forcrosspairsderivedfromtheUSDprimaries.

AUDCAD

AUDCHF

Forex 2018

www.matrixtrade.com Page 12 of 20

AUDJPY

AUDNZD

Forex 2018

www.matrixtrade.com Page 13 of 20

CHFJPY

DXY

Forex 2018

www.matrixtrade.com Page 14 of 20

EURAUD

EURCAD

Forex 2018

www.matrixtrade.com Page 15 of 20

EURCHF

EURJPY

Forex 2018

www.matrixtrade.com Page 16 of 20

EURNZD

GBPAUD

Forex 2018

www.matrixtrade.com Page 17 of 20

GBPCAD

GBPCHF

Forex 2018

www.matrixtrade.com Page 18 of 20

GBPJPY

GBPNZD

Forex 2018

www.matrixtrade.com Page 19 of 20

NZDJPY

USDCHF

Forex 2018

www.matrixtrade.com Page 20 of 20

DISCLAIMER:

MatrixTrade.commakesnowarrantiesorguaranteesinrespectofitscontent.Alltheinformationcontainedinthisnoteisprovidedasgeneralcommentaryanddoesnotconstituteinvestmentadviceorrecommendation.MatrixTrade.comwillnotacceptliabilityforanylosseswhichmayarisedirectlyorindirectlyfromuseoforrelianceonsuchinformation.

Youareadvisedtoconductyourownresearchbeforemakingadecision.Tradingfinancialinstrumentscarriesahighlevelofrisk,andmaynotbesuitableforallinvestors.Beforedecidingtoinvestinanyfinancialinstrumentyoushouldcarefullyconsideryourinvestmentobjectives,levelofexperience,andriskappetite.Youshouldbeawareofalltherisksassociatedtradingfinancialinstruments,andseekadvicefromanindependentfinancialadvisorifyouhaveanydoubts.Pastperformanceisnoguaranteeoffuturegains.

Inparticularspreadbetting,CFDsandFXareleveragedproductsandcarryahigherlevelofrisktoyourcapital.Itispossibletolosemorethanyourinitialinvestment,requiringfurtherpayments.

AllthematerialinthisdocumentistheintellectualpropertyofMatrixMarketsLimited,tradingasMatrixtrade.com,andmaynotbereproducedwithoutpriorpermissionandacknowledgement.

MatrixTrade.comprovideshigh-qualityandaccurateresearchinthepublicstockandcurrencymarketsviaasubscriptionwebsite.Furtherinformationisavailableonourwebsite.

Top Related