Forex 2018 - Matrix · EURUSD gripped its 10 year yield spread for the first six months until the...

20

Forex 2018 www.matrixtrade.com Page 1 of 20 INTRODUCTION The outlook for the foreign exchange market in 2018 is, like any market, dependent on the interaction and trends of FITS (fundamentals, intermarket relationships, technical and sentiment). This interaction explains why currencies can and frequently move away from their traditionally significant interest differentials in the short to near term as the Euro has done since July. It certainly explains why some currencies like the CHF seem to ignore their purchasing power parity (PPP) for prolonged periods. It also accounts for the underestimation of, once theoretically important, trade flows even though the currency of the country with the largest current account deficits, the United States, was amongst 2017’s worst performers. It also crucially explains why the USD has lost its risk status (correlation to SPX) in 2017. How a combination of the four FITS pillars manifests itself contributes to, but also depends on, volatility and therefore clarity (VC). Movements in volatile (particularly fundamental) trends tend to be clearer than consolidation markets, at least in retrospect. Although any of these factors can be obscured in the forex market as currencies are expressed in terms of another currency (or basket eg DXY), when one of the FITS of any market is dominant it tends to supersede all others. Sterling’s sentiment driven Brexit collapse in June 2016 still casts a long shadow over the Cable market and indeed the UK economy. The Fundamental prospect of Trumpflationary growth drove the USD higher against most other currencies into 2017. In contrast to the equity markets, it was then reversed even against the Brexit beleaguered GBP for most of the year partly because US inflation did not rise to the extent either the Fed or traders’ anticipated. This overestimation was also compounded by Trump’s wish for a weaker dollar combined with political uncertainty at home and abroad. Adding to the dollar’s woes, was the ‘Sintra pact’ in June that saw a co-ordinated step towards tightening by the ECB, the BoE and the BoC, and paved the way for all three banks making hawkish policy changes later in the year. The main beneficiary was the Euro. The ECB was notably sluggish in announcing the tapering of its quantitative easing programme even though the European economy continued to recover and shrugged off political concerns surrounding Brexit and French/German elections and even Catalonia. Whereas the persistent campaign of the SNB has ensured prolonged CHF weakness against the Euro and stability versus the similarly weak Dollar. Despite bouts of two-way Brexit inspired volatility, Sterling remained stable to strong throughout the year. Our theory, that uncertainty about uncertainty creates inertia until it is resolved either way, has been borne out. When Brexit news hasn’t been forthcoming a surprisingly resilient economy and inflation outlook has helped maintain the GBPUSD updrift. A self-correcting irony: Sterling weakness had pushed inflation up to 3.1% in turn helping the Pound to recover. Intermarket relationships for currencies have, at times, bordered on the bizarre. The three main links (interest rates and the related commodities and risk appetite/aversion with stocks) have vacillated and varied as part of a general market correlation break down. 10 year US yields have remained range bound around a 2.3% pivot all year and while the Fed has raised three times now the Federal Funds Rate sits in the 1.25-1.5% range. Clearly the market is still sceptical about sustained inflation and towards the end of the year the outgoing Fed Chair, Janet Yellen, admitted she found the low inflation a ‘mystery’, a clear break from the previous message it was ‘transitory’. Yield driven currency moves then can be explained partly by a change in the yield curve but more by uncorrelated movements in other countries’ bond markets. For much of the year certain currency pairs have correlated strongly with interest rates. EURUSD gripped its 10 year yield spread for the first six months until the July 20th ECB meeting

Transcript of Forex 2018 - Matrix · EURUSD gripped its 10 year yield spread for the first six months until the...

Forex 2018

www.matrixtrade.com Page 1 of 20

INTRODUCTIONTheoutlookfortheforeignexchangemarketin2018is,likeanymarket,dependentontheinteractionandtrendsofFITS(fundamentals,intermarketrelationships,technicalandsentiment).ThisinteractionexplainswhycurrenciescanandfrequentlymoveawayfromtheirtraditionallysignificantinterestdifferentialsintheshorttoneartermastheEurohasdonesinceJuly.ItcertainlyexplainswhysomecurrenciesliketheCHFseemtoignoretheirpurchasingpowerparity(PPP)forprolongedperiods.Italsoaccountsfortheunderestimationof,oncetheoreticallyimportant,tradeflowseventhoughthecurrencyofthecountrywiththelargestcurrentaccountdeficits,theUnitedStates,wasamongst2017’sworstperformers.ItalsocruciallyexplainswhytheUSDhaslostitsriskstatus(correlationtoSPX)in2017.HowacombinationofthefourFITSpillarsmanifestsitselfcontributesto,butalsodependson,volatilityandthereforeclarity(VC).Movementsinvolatile(particularlyfundamental)trendstendtobeclearerthanconsolidationmarkets,atleastinretrospect.Althoughanyofthesefactorscanbeobscuredintheforexmarketascurrenciesareexpressedintermsofanothercurrency(orbasketegDXY),whenoneoftheFITSofanymarketisdominantittendstosupersedeallothers.Sterling’ssentimentdrivenBrexitcollapseinJune2016stillcastsalongshadowovertheCablemarketandindeedtheUKeconomy.TheFundamentalprospectofTrumpflationarygrowthdrovetheUSDhigheragainstmostothercurrenciesinto2017.Incontrasttotheequitymarkets,itwasthenreversedevenagainsttheBrexitbeleagueredGBPformostoftheyearpartlybecauseUSinflationdidnotrisetotheextenteithertheFedortraders’anticipated.ThisoverestimationwasalsocompoundedbyTrump’swishforaweakerdollarcombinedwithpoliticaluncertaintyathomeandabroad.Addingtothedollar’swoes,wasthe‘Sintrapact’inJunethatsawaco-ordinatedsteptowardstighteningbytheECB,theBoEandtheBoC,andpavedthewayforallthreebanksmakinghawkishpolicychangeslaterintheyear.ThemainbeneficiarywastheEuro.TheECBwasnotablysluggishinannouncingthetaperingofitsquantitativeeasingprogrammeeventhoughtheEuropeaneconomycontinuedtorecoverandshruggedoffpoliticalconcernssurroundingBrexitandFrench/GermanelectionsandevenCatalonia.WhereasthepersistentcampaignoftheSNBhasensuredprolongedCHFweaknessagainsttheEuroandstabilityversusthesimilarlyweakDollar.Despiteboutsoftwo-wayBrexitinspiredvolatility,Sterlingremainedstabletostrongthroughouttheyear.Ourtheory,thatuncertaintyaboutuncertaintycreatesinertiauntilitisresolvedeitherway,hasbeenborneout.WhenBrexitnewshasn’tbeenforthcomingasurprisinglyresilienteconomyandinflationoutlookhashelpedmaintaintheGBPUSDupdrift.Aself-correctingirony:Sterlingweaknesshadpushedinflationupto3.1%inturnhelpingthePoundtorecover.Intermarketrelationshipsforcurrencieshave,attimes,borderedonthebizarre.Thethreemainlinks(interestratesandtherelatedcommoditiesandriskappetite/aversionwithstocks)havevacillatedandvariedaspartofageneralmarketcorrelationbreakdown.10yearUSyieldshaveremainedrangeboundarounda2.3%pivotallyearandwhiletheFedhasraisedthreetimesnowtheFederalFundsRatesitsinthe1.25-1.5%range.ClearlythemarketisstillscepticalaboutsustainedinflationandtowardstheendoftheyeartheoutgoingFedChair,JanetYellen,admittedshefoundthelowinflationa‘mystery’,aclearbreakfromthepreviousmessageitwas‘transitory’.

Yielddrivencurrencymovesthencanbeexplainedpartlybyachangeintheyieldcurvebutmorebyuncorrelatedmovementsinothercountries’bondmarkets.Formuchoftheyearcertaincurrencypairshavecorrelatedstronglywithinterestrates.EURUSDgrippedits10yearyieldspreadforthefirstsixmonthsuntiltheJuly20thECBmeeting

Forex 2018

www.matrixtrade.com Page 2 of 20

butthereaftercontinuedtorallywhileitsdifferentialdowntrendedfortherestoftheyear.Basedon10yearinterestyieldsaloneEURUSDshouldhaveclosedtheyear900pipslower!Thankfullywechosetoignorethis.USDCADhasbeentiedtoitsfallingdifferentialallyearwithanydivergenceprovingmomentaryandoftenflaggingareversalinthecurrencyasitcamebackinline.SomeofthatdivergenceisduetoOilinCanada’scasebutthatinturnhasledtoanassociatedmovementintheCanadianbondmarket.ThedelayedreactionhasoftencounterintuitivelyseentheCanadianDollarmoveintheoppositedirectiontoOil.Similarly,theAussiehasbeenbuffetedbycommoditymovementbuttypicallywithatimelag.Its4.2%yearendsqueezecanmainlybeattributedtoGold’srecoveryratherthanonlya11basispointdifferentialreboundeventhoughthisstartedearlierinNovember.PoliticsratherthanmilkhasbeenthemaindriveroftheKiwi’swhipsawtrendsandsawNZDrampwhileitsdifferentialcollapsedinDecember.Whatisnormallyseenasayield/riskappetitecurrencyhasignoredstockmarketsformuchof2017.Butthemostinterestingbreakdownincorrelationhasbeentheapparentendofthe11yearbondbetweenUSDJPYandtheNikkei,whichweflaggedaspossiblyourboldestcurrencypredictionof2017,andapreconditionofanendtodeflation.AlthoughthiscaninpartbeattributedtoUSDJPY’smorepowerfulcorrelationto10yearyields,itreflectsamoregeneralbreakdownintraditionalcurrencyriskappetite/aversionrelationships.Therootcauseofthecurrencydisconnect,webelieveisthedisintegrationoftheriskstatusoftheworld’sreservecurrency,theUSD.Attheendof2017theDollarIndexclosed10.55%lowerandtheS&P20.6%higher.Thelasttimewesawsuchaninversionwasatthestartofthestockbullmarketin2009(duetoQuantitativeEasing).2010sawthemslowlybutsurelycomebackinlinebeforebothralliedfortheensuing6years.Theconsequenceof2017’sbreakdownhasbeenvariedandarguablybizarre.Thosecurrencypairsthathavestucktotheirinterestratedifferentialshavetradedastheywouldinriskaversionmodeiestocksfalling.TheprimeexampleswouldbeEURUSDstrengthandAUDweaknesshenceEURAUDstrength.Howeverothersafe-haven/riskaversionpairssuchasEURCHFandJPYcrosseshaverallieddivergingfromtheirdifferentialsinthelastsixmonthsandreflectingstockstrength.TraditionalTechnicalAnalysisofforeignexchangehasbeenunderminedbytheweaknessinthemarket’sglue.Potentiallysignificantbreakshavefrequentlyprovedfalseatleastintheshortertermwithcurrenciesrollingbackintotheirrange.Onceuponatimewecouldhaveblamedthisonvegatradingbyoptionsdesks.Butthistimeitissymptomaticofabrokenmarket.TheAustralianDollarisprobablytheprimeexamplein2017totheextentyoualmosthadtowaitforafalsebreakbeforeitreversed.Similarly,thesequenceofpotentiallyabortivebearishEURUSDHeadandShoulderspatternshasironicallybeenausefulguidetonursingabullishtrade.2017hasprobablysetarecordforredrawntrendlinesandresurrectedthe‘thirdtrendlineisagoodone’maxim.Althoughwearegenerallynotfansofdailyorweeklyclosebasedanalysisthishasprovedasaferandtruerguideforgenuinebreaksformuchof2017.Theproliferationofwedgesisalsotestimonytoamarketthatistryingtotrendbutbroughtbackbyoppositemovementsinotherrelatedmarkets.WhenmarketsbehavelikethisitnormallysuggeststheyarebeinginfluencedbylargerflowsinothercurrenciesoftenwhereoneoftheFITSismoredominant.Forewarnedisforearmed.Therearetwopowerfultechnicaltemplatesforthecurrentforexmarket.USstockmarketshavefollowedaslower(delayed)butconsequentlymoreaggressiveversionoftheir1987blowout.AswehaveseentheForexmarketbehavedoddlybutthereforeverymuchlikeitdidin1987without,asyetthedramaticriskaversionfinaleassociatedwiththe1987stockcrash.Althoughtheforexoutlookfor2018wouldseemtobegthequestionofwhetherindices(andthereforesafehaven/riskaversionpairs)willturn,wearefortunatethatmanycurrencies(notablytheUSDandparticularlyEURUSD,AUDUSDandGBPUSD)arealsofollowingverysimilarpriceactionin2002-2003–aperiodwherestockswereflattodownbeforealargerrecovery.Inotherwords,therearetemplatesfortheforexmarketthatarenotentirelydependenton(althoughinfluencedby)whatthestockmarketsdo.

Forex 2018

www.matrixtrade.com Page 3 of 20

TherearemanyotherweakerprecedentsforthistypeofmarketwhereintermarketandtechnicalfactorshaveunderperformedbuttheyarenormallyseenattheendorindeedstartofamajorglobaltrendwhereSentimenthasbecomethemaindrivingforce.ExtremesentimentinamajormarketsuchasUSindiceswillinevitablyspilloverintootherrelatedmarketsduetostockrelatedflowsandstockassociatedsentiment.TraderswillsellCHFandJPYinordertofundpurchaseofhigheryieldingcurrencies/assetsbutalsobecausethoseloweryieldingcurrenciesareweak.Thiscomplicatessentimentanalysisofforeignexchangeascurrencyflowsarenolongerisolated;thatistheyincreasinglycontainanadditionalstockoryieldrelatedelement.AmarketsuchastheEURmayappearoverlybullishbutnewentrantsmaycomeinandbuysignificantamountstransformingamarketthatmayindeedbelongtoonethatisnetshortbutstillbullish.ThisadditionallongtermfundbuyingisprobablythemainreasonforthegrowinggapbetweenEURUSDanditsinterestdifferentialoverthelastsixmonths.Theironyandaninterestingfeaturefor2018isthatshouldstocksturn,ratherthanprovokealiquidationofthelongEURUSDtrade,itcouldexaggeratetheuptrend.Asaconsequence,forexsentimenthasbeenconfusedformuchoftheyear.Itisnaturaltoseektrendandquickly.Butayearoffalsebreaks,slowtrendsorconsolidationshasseencurrenciestakeoutweakpositionsleavingthemarketoverlylongorshortandthereforeretracebeforeresumingthepattern.2017maywellgodownastheyearoftheForexcynicorthehesitantCentralBank.Despitemomentsofastutepresentation,theECBhasfailedtograspthesentimentoftheForexmarket.TheyexpressedconcernonanumberofoccasionsabouttheappreciationoftheEuroandseeminglydelayedthelongoverdueTaperasaresult.AndyetthisdelayhasitselffedEurostrengthdenyingthemarketitsfavorite‘buytherumorsellthefact’.Theoutlookfor2018thereforedependspartlyonwhetherthesetrendsinFITScontinueandthereforewhetherUSinflationandinterestrates/yieldswillnotriseasmuchaselsewhere.Toappreciatewhatmayhappenin2018requiresanunderstandingofwhereeachcountrysitswithinitseconomiccyclecomparedtoothersbutalsotheattitudeofCentralBanksandtheirrespectivepolicies.CertainlytheUShasbeenattheforefrontofeconomicgrowth.ItisnotclearwhethersubduedUSinflationreflectseitheralessthanrobusteconomyoranecommerceinspiredchangeinthenatureofinflation.ButeitherwayanhistoricallyslowUStighteningphasehasencouragedcentralbankselsewheretofollowsuitandditheranddelay.Thisnotonlyrisksashiftinrelativeinflationratesandconsequentlyyieldsbutmaywellservetoperpetuatetrendstheywishtoavoid.Twotrendswedoexpecttoseein2018:Firstly,justasstocksexceededevenouraggressivelybullishtargetsfor2017,theForexmarkethasthepotentialtoregainvolatilityandexceedmanyexpectations.Secondly,justlike2010theForexmarketshouldslowlybutsurelycomebacktogetherin2018—hopefullymakingmarketseasiertotradeandcertainlytounderstand.

Forex 2018

www.matrixtrade.com Page 4 of 20

EURUSD

LongEURUSDwasourprojectedhighlightforthelatterpartof2017andcouldwellbeforthenext4years.In2016wehighlightedlongEURUSDwouldbetheForexTradeof2017basedonthePandora’sBoxAnalogywehavefollowedformuchofthisdecade.ThisandthesimilarleadingGold(WashingtonGoldagreement)priceactionin1999arguedtheEurowassettingabasewithinarepeatingpatterninarisingwedgedatingbackto1985(whenitwas$-Deutschmark).Thissuggesteditwouldeventuallysecureanotherrunatthehighsonceitregainedweeklydowntrendnowat1.2636.Italsoprojectedaninterimconsolidationbase16yearsafterthepreviousconsolidationbase(thatwasalso16yearsafterthe1985low).Furthermore,itforecastthat,oncetheEurobroketheeffective1.1550consolidationhighthiswouldbemaintainedina218-weekuptrend–amajorbullmarket–thatcharacteristicallyabortedabearishHead&Shoulders.Althoughthemarginalnewlowto1.0340atthestartof2017wasslightlyoutofsynch,EURUSDsubsequentlyproveditwasstillfollowingthispatternandthereforeanuptrenddrivenbyeconomicresurgenceinEurope,acatchupwiththeUSandarelativefirmlyofyields.IndeedthisyieldviewissupportedbythelongtermMatrixcurrencyfractal(where3monthforwardsareleadingtheEURUSDhigher-seebelow).WethereforeremainbullishtheEuropotentiallyforabreakof1.2635toconfirmatleast1.3710-1.40.Thetimingofanyupwardaccelerationandthereforelikelyhighfor2018dependspartlyonthestructureoftherally(andpossiblystockdisinvestmentfromtheUS)andtheextenttowhichtheItalianelectionsearlyMarchwillserveasabrake(NotetheFrenchElectionsin2017initiallyslowedtheuptrendbutthengaveitlaterimpetus).Withanoutstandingsixmonthtargetfrom2017of1.2340wemayhavetotolerateaperiodof1.1550-1.2635consolidationbeforetheuptrendcangathermomentumeventhoughhistoryfavorsacontinueduptren

Alossof1.1550wouldsuggest1.11inadeepercorrectionbutonlyabreakofthe1.0340lowabortsthislong-termpatternforanaggressivespikesubparity.

Forex 2018

www.matrixtrade.com Page 5 of 20

USDJPY

Thereissurprisinglylittlechangeinourviewfrom2017asUSDJPYhasspent43weeksofthelastyearina107.35-114.70rangeandthereforesitsneatlybutperhapsdisappointinginapotentialconsolidationtop.Contextisimportanttounderstandingwhatthisrepresents.Withina20-year75-145prolongedconsolidationthe50yenUSDJPYrallyfollowingthe2011earthquakeshouldrepresentthefirstlegofanotherrunatthe145high.The50%pullbackto99.10waseasilyenoughindistancetosatisfythecorrection.

Althoughitisthereforeeasytobelievethecurrentimpulsiverecoveryisaresumptionofthatuptrend,bothoursofarsuccessfulEarthquaketemplateandaverysimilarimpulsiverecoveryin2000suggestthiscouldbetheearlystagesofatleastprolongedconsolidationinthe100-125rangeifnotapotentiallylargeralbeitcorrectivedecline.ThelongerUSDJPYcanstaybelowideally114.70nowbutmoresignificantly125.80thennotonlycanweexpectareturnto99.15butpossiblybreakingdownto94.75(61.8%)even87.40(76.4%)inapossiblecontinuedreflationinspireddisconnectwiththeNikkei.Itisthereforeonlyafteralongerand/ordeepercorrectionthatwecanseeUSDJPYbreakthe125.80highalthougharallythrough114.70and118.90wouldincreasetheprobabilityofaprematuretest/break.

Forex 2018

www.matrixtrade.com Page 6 of 20

GBPUSD

GBPUSDstandsoutasthecurrencypairwiththegreatestpotentialtosurprisewithaBrexitunwindin2018,particularlyafterapossibleperiodofgeneralSterlingweaknessatthestartoftheyear.Followingwhatappearstobeapossiblycompletethreeleggeddeclinefromthe2.11602007high,theFatFingerspiketo1.1815(possiblylower)marksapotentialbasefromarecoverybackthroughthepreBrexitreferendumlowsof1.3653-1.3833initiallybackto1.4320(50%butwithpotentialforareturntothepreBrexithighof1.50(61.8%)andpotentialdownchannelresistance.Inthisrespectacontinuedsimilaritytothe2001-2007uptrendisinstructive.Soalthoughwecouldtoleratefurtherconsolidationbelow1.3654eventotheextentofspikingbelow1.30to1.2775-1.2815,whileGBPUSDisabove1.25thentherewillremainawindowtoresumeapotentialsixyearuptrend.AsurprisingthumbsupforBrexit?!

Forex 2018

www.matrixtrade.com Page 7 of 20

EURGBP

EURGBPremainswithininalongertermuptrendreflectinginherentweaknessthatpredatesBrexit.

Followingaclearlycorrectivesevenyearretracementfrom0.9800to0.6945theimpulsiverecoverytotheFatFingerhighof0.9365(followingsimilarpriceactiontotheUK’sexitfromtheERMin1992)shouldrepresentthefirstofathree-leggedmoveinarisingwedgetoa1.0577equalitytarget.However,that24centuptrendneedstobecorrected.SoalthoughEURGBPhassettledintoaBrexituncertaintystasisina0.8300-0.9365rangethisshouldeventuallygivewaytoadeepercorrectionin2017toacurrent0.8245(c=a)equalitytargetprobablyanideal0.814850%anevenaslowas0.0.786061.8%?Oncethecurrent0.83consolidationisspikedandregainedEURGBPwillbeinapositiontobreak0.9365tochallengethe0.98high.ThiscorrectiveconsolidationphaseissupportedbytheremarkablyaccurateMatrixCurrencyFractal(3monthEURGBPforward)thatdiscountedtheLeavescenariowhenthereferendumwascalledinFebruary2016.

Forex 2018

www.matrixtrade.com Page 8 of 20

USDCAD

Withinanobviousandbroad0.90-1.60longtermrange,USDCADremainswithinanoilandinterestratedrivendowntrendtoatleast1.1410(61.8%)andprobably1.1035likelychannelsupportandthesamesizeofthepreviousdecline.Despitethepersistenceofthenotdissimilar2008-2011downwardratchetitisnosurprisetofindtheselloffrom1.4690takingtheformadecliningwedge.SOalthoughthisallowsaperiodofapproximate1.20-1.30equilibriumconsolidationralliesshouldcontinuetofadeinthe1.29-1.31regionforaneventualbreakdownthrough1.1915tothenextobjectiveat1.1540(c=a)

Forex 2018

www.matrixtrade.com Page 9 of 20

AUDUSD

AUDUSDcontinueswithinasteadyupwardratchetfromthe0.6835lowthatmaintainsa2001-2004inspiredwindowtoaccelerateatsomepointthroughthepivotal0.8430-0.8660toatleast0.945561.8%.AlthoughthisrecoveryappearslaboredandthereforepossiblycorrectiveitistypicalofoneofAussie’sfavoriteformations:theleadingdiagonalorwedge.Thereforeeventhoughthissuggestsapotentialspikeonlyof0.8160in2018possiblyfailingbelow0.8430,weexpectanapproximate75-84rangeformuchoftheyeartocreateabasefromwhichtogatherupwardmomentum.Althoughalossof75wouldappearatoddswiththe2002templateonlyalossof0.7140threatenstobreakthe0.6830lowdownto60.

Forex 2018

www.matrixtrade.com Page 10 of 20

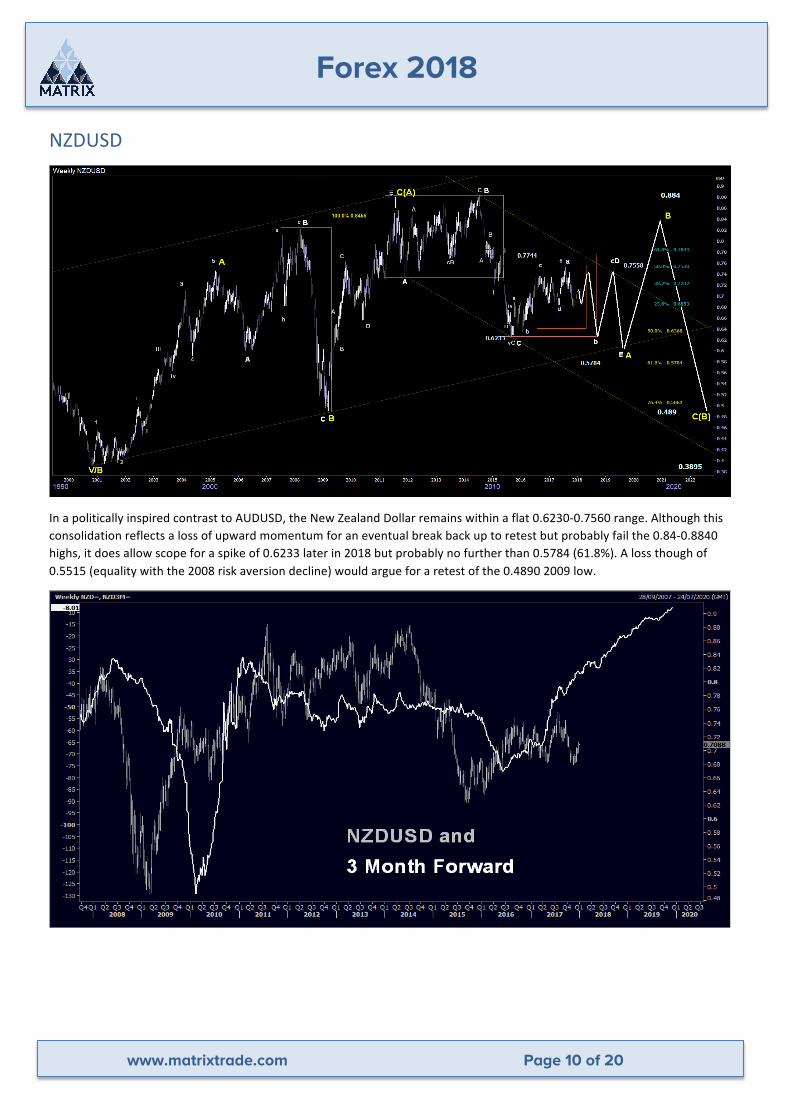

NZDUSD

InapoliticallyinspiredcontrasttoAUDUSD,theNewZealandDollarremainswithinaflat0.6230-0.7560range.Althoughthisconsolidationreflectsalossofupwardmomentumforaneventualbreakbackuptoretestbutprobablyfailthe0.84-0.8840highs,itdoesallowscopeforaspikeof0.6233laterin2018butprobablynofurtherthan0.5784(61.8%).Alossthoughof0.5515(equalitywiththe2008riskaversiondecline)wouldargueforaretestofthe0.48902009low.

Forex 2018

www.matrixtrade.com Page 11 of 20

APPENDICESHerewepresentcharts(inalphabeticalorder)forcrosspairsderivedfromtheUSDprimaries.

AUDCAD

AUDCHF

Forex 2018

www.matrixtrade.com Page 12 of 20

AUDJPY

AUDNZD

Forex 2018

www.matrixtrade.com Page 13 of 20

CHFJPY

DXY

Forex 2018

www.matrixtrade.com Page 14 of 20

EURAUD

EURCAD

Forex 2018

www.matrixtrade.com Page 15 of 20

EURCHF

EURJPY

Forex 2018

www.matrixtrade.com Page 16 of 20

EURNZD

GBPAUD

Forex 2018

www.matrixtrade.com Page 17 of 20

GBPCAD

GBPCHF

Forex 2018

www.matrixtrade.com Page 18 of 20

GBPJPY

GBPNZD

Forex 2018

www.matrixtrade.com Page 19 of 20

NZDJPY

USDCHF

Forex 2018

www.matrixtrade.com Page 20 of 20

DISCLAIMER:

MatrixTrade.commakesnowarrantiesorguaranteesinrespectofitscontent.Alltheinformationcontainedinthisnoteisprovidedasgeneralcommentaryanddoesnotconstituteinvestmentadviceorrecommendation.MatrixTrade.comwillnotacceptliabilityforanylosseswhichmayarisedirectlyorindirectlyfromuseoforrelianceonsuchinformation.

Youareadvisedtoconductyourownresearchbeforemakingadecision.Tradingfinancialinstrumentscarriesahighlevelofrisk,andmaynotbesuitableforallinvestors.Beforedecidingtoinvestinanyfinancialinstrumentyoushouldcarefullyconsideryourinvestmentobjectives,levelofexperience,andriskappetite.Youshouldbeawareofalltherisksassociatedtradingfinancialinstruments,andseekadvicefromanindependentfinancialadvisorifyouhaveanydoubts.Pastperformanceisnoguaranteeoffuturegains.

Inparticularspreadbetting,CFDsandFXareleveragedproductsandcarryahigherlevelofrisktoyourcapital.Itispossibletolosemorethanyourinitialinvestment,requiringfurtherpayments.

AllthematerialinthisdocumentistheintellectualpropertyofMatrixMarketsLimited,tradingasMatrixtrade.com,andmaynotbereproducedwithoutpriorpermissionandacknowledgement.

MatrixTrade.comprovideshigh-qualityandaccurateresearchinthepublicstockandcurrencymarketsviaasubscriptionwebsite.Furtherinformationisavailableonourwebsite.