Languages

Pages

Legal

COMM 324 --- W. Suo Slide 1Slide 1

Market EfficiencyMarket Efficiency&&AnomaliesAnomalies

COMM 324 --- W. Suo Slide 2Slide 2

Random Walk - stock price change unpredictably Actually stock prices follow a positive trend

Expected price is positive over time Positive trend and random around the trend

Random Walk and Stock Prices

Security Prices

Time

COMM 324 --- W. Suo Slide 3Slide 3

Why do stock prices change?

Why are price changes random? Prices react to information Flow of information is random

Random Price Changes

COMM 324 --- W. Suo Slide 4Slide 4

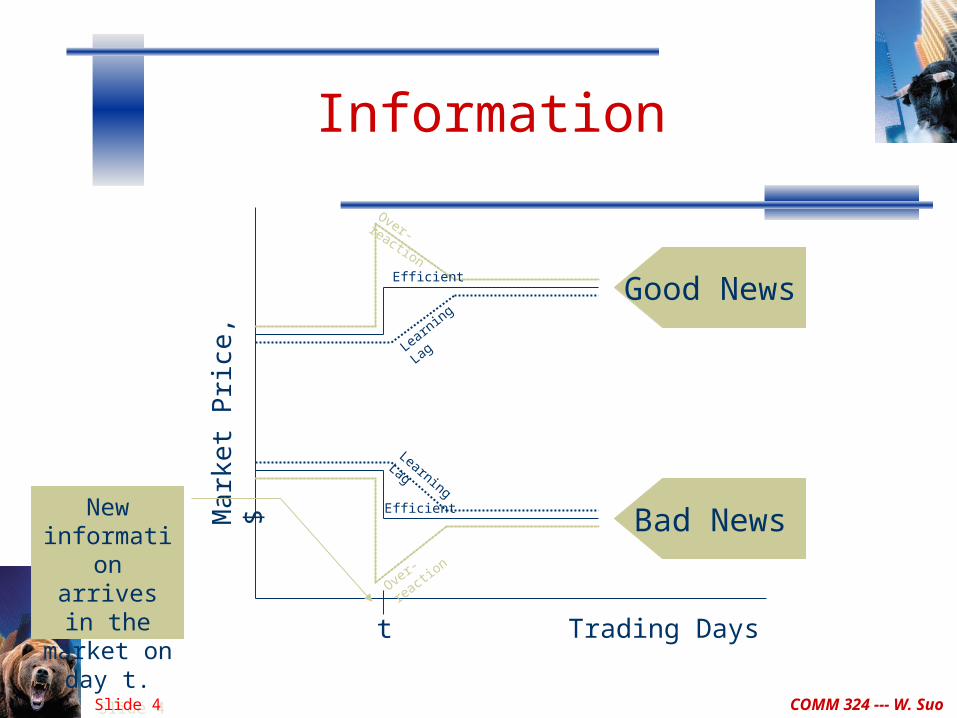

Information

Trading Days

Mar

ket P

rice

, $

t

Over-reaction

Efficient

Learning Lag

Over-rea

ction

Efficient

Learning LagNew

information arrives in the

market on day t.

Bad News

Good News

COMM 324 --- W. Suo Slide 5Slide 5

Basic question: Do security prices reflect information ?

Why look at market efficiency Implications for business and corporate finance Implications for investment

Forms of efficient market hypothesis Weak Semi-strong Strong

Efficient Market Hypothesis (EMH)

COMM 324 --- W. Suo Slide 6Slide 6

Types of Stock Analysis Fundamental Analysis

Using economic and accounting information to predict stock prices Semi strong form efficiency & fundamental analysis

Technical Analysis Using prices and volume information to predict future prices Weak form efficiency & technical analysis

Active Management Security analysis Timing

Passive Management Buy and Hold Index Funds

Even if the market is efficient a role exists for portfolio management Diversification Appropriate risk level Tax considerations

Implications of Efficiency for Active or Passive Management

COMM 324 --- W. Suo Slide 7Slide 7

Event studies Assessing performance of professional managers Testing some trading rule

Empirical Tests of Market Efficiency

COMM 324 --- W. Suo Slide 8Slide 8

Evidence SupportingWeakly Efficient Hypothesis

Is it possible that security prices do not reflect all historical information? Which is easy to obtain and cheap

Technicians focus on past security prices Look for meaningful trends in historical security prices Attempt to extract predictions from whatever patterns

they find

COMM 324 --- W. Suo Slide 9Slide 9

Filter Rules

An X% filter is a mechanical trading rule If a security’s price rises by at least X%, buy and hold until the price

peaks and falls by at least X% When price decreases from a peak level by X%, liquidate long

position and sell short Hold short position until price reaches a low point and then begins

to rise If (when) the price rises above X%, cover the short position and go

long

COMM 324 --- W. Suo Slide 10Slide 10

Using a 10% Filter Rule to Trade a Security

COMM 324 --- W. Suo Slide 11Slide 11

Filter Rules

Different filter rules can be testing by changing the X value If stock prices fluctuate randomly, filter rules should not

outperform randomly chosen stocks Filters ranging from .05% to 50% have been tested In general, filter rules generate large commissions

(especially those with small X values) After deducting for commissions, filter rules do not outperform

naïve buy-and-hold strategy Some filters result in large net losses after deducting commissions

COMM 324 --- W. Suo Slide 12Slide 12

Serial Correlation Tests

Serial correlation (autocorrelation) tests should be able to determine if security prices move in trends or reversals

Measures the correlation coefficient in a series of numbers with lagged values in the same series

Lags of any length can be used

Stock prices exhibit a long-run upward trend of about 6.6% a year in the U.S.

Thus, some positive serial correlation is found But, technical analysts focus on short-term trends

COMM 324 --- W. Suo Slide 13Slide 13

Serial Correlation Tests

Do daily or weekly price change trends exist and, if so, can they be used to earning a trading profit after commission?

Many studies have failed to detect statistically significant serial correlations on a daily, weekly or monthly basis

Scientific evidence supporting weak form efficiency Some conflicting evidence exists

DeBondt & Thaler (1985) find evidence of long-term stock price overreaction and negative serial correlation for individual stocks

Lo & MacKinlay (1988) found positive serial correlation for a diversified portfolio of stocks

Conrad & Kaul (1993) suggest that the above results are due to statistical measurement errors

COMM 324 --- W. Suo Slide 14Slide 14

Runs Tests

A “runs” test can be performed to determine if irregular trends occur in price changes

A run occurs when the changes between consecutive numbers switch direction

A series of random numbers is expected to generate a certain amount of positive, negative or zero runs

By comparing the actual number of runs to the expected number, we can determine if a non-random number of runs occurred

Results suggest that actual number of runs do not differ statistically from the number of expected runs

COMM 324 --- W. Suo Slide 15Slide 15

Anomalies in Weakly Efficient Hypothesis

Day-of-the-Week Effects the stock market tends to fall on Mondays and rise the rest of the week

Holiday effect Returns on the day before holiday weekends are 9 – 13 times higher than the average

daily return About 1/3 of the average stock’s annual return was earned in pre-holiday trading days

Friday to Monday Negative (positive) returns on a Friday are usually followed by large

negative (positive) returns on Monday The large commissions paid (relative to the small positive daily returns) will

more than offset the potential benefit of this knowledge January Effect

average stock’s return in January is more than 5 times the mean monthly return A large part of the typical stock’s annual return is generated during January

This is a larger anomaly than the day-of-the-week effects Can yield net trading profits after deducting transaction costs

Buy stocks before Christmas and sell at the end of January

COMM 324 --- W. Suo Slide 16Slide 16

1. Examine prices and returns over time

Tests of Semi-Strong Efficiency: Event Studies

0 +t-t

Announcement Date

COMM 324 --- W. Suo Slide 17Slide 17

2. Returns are adjusted to determine if they are abnormalMarket Model approach

a. Rt = a + bRmt + et

(Expected Return)b. Excess Return = (Actual - Expected)

et = Actual - (at + btRmt)

How Tests Are Structured (cont’d)

COMM 324 --- W. Suo Slide 18Slide 18

Stock Splits and Stock Dividends

Neither of these events change the total value of the firm or investor’s wealth

If security markets are efficient, the firm’s market capitalization should not be impacted by a stock split or stock dividend

In the long-run, stock splits and stock dividends do not seem to impact

The liquidity of the split stocks The market value of the firm Investors’ returns

If an investor can correctly predict which companies are going to split, it may be possible to earn excess returns

Studies involving stock splits and stock dividends appear to support the semi-strong efficient market hypothesis

COMM 324 --- W. Suo Slide 19Slide 19

Anomaly: Size Effect

Research shows that small company stocks earned higher rates of return than large company stocks, on average

Size based on market capitalization Found that small cap stocks were also riskier, but even after

adjusting for risk the size effect remained Even after adjusting for the impact of infrequent price

changes the size effect remained

COMM 324 --- W. Suo Slide 20Slide 20

Growth-Value Anomaly

Semi-strong form of EMH suggests that money managers who use a particular management style should not consistently outperform managers using another management style Value managers Growth manager Value stock investors have historically outperformed

growth stock investors on a risk-adjusted basis over extended periods of time

Constitutes an anomaly to the semi-strong form of efficient market hypothesis

COMM 324 --- W. Suo Slide 21Slide 21

Equity Premium Puzzle

Rewards for bearing risk appear too excessive Possible causes:

Unanticipated capital gains Survivorship bias

Survivorship bias also creates the appearance of abnormal returns in market efficiency studies

COMM 324 --- W. Suo Slide 22Slide 22

The Paradox

Grossman and Stiglitz In a world where it cost money to analyze securities,

analysts will be able to identify mispriced securities

Investors will do just as well using passive investment strategy where they simply but the securities in a particular index and hold unto those investments

Top Related