Languages

Pages

Legal

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

IFTA – DUAL FUEL VEHICLE TAX REPORTING

August 14, 2014Pittsburgh, PA

Presented by

DUAL FUEL WORKING GROUP

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

Overview• A Quick Recap on Dual Fuel Vehicles • Conversion Issue for LNG – Diesel gallon equivalents– Short-Track Ballot #05-2014

• New Fuel Types for the Clearinghouse– For reporting between jurisdictions

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

Dual FuelWorking Group

IFTA:Hugh Hughson (BC) Dawn Lietz (NV) Paul Bernander (WI)Garry Hinkley (MI)Tim Ford (CA) Chuck Ulm (MD)Industry: Robert Pitcher (ATA) Gary Bennion (Con-Way)FTA:Cindy Anders-Robb IFTA, Inc. Advisors:Lonette Turner Amanda Koeller

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

Dual Fuel Vehicles - 101

• Dual fuel vehicles can use two fuels at the same time (i.e., diesel and natural gas)

• Two types of natural gas are being used:• Compressed Natural Gas (CNG)

• Stored as a gas in high-pressure tanks (e.g., 3,000 to 3,600 psi) • Often sold as a gaseous measure (e.g., ft3 or m3)

• Liquefied Natural Gas (LNG):• Stored as a super-cooled liquid (e.g., -260°F or -170°C)• Almost always sold as a liquid measure (e.g., gallons or liters) or by

weight

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

Dual Fuel Vehicles - 101

• Expect:• At least 5% of long haul vehicles will be

dual fuel within the next 5 years• LNG will be used more for since the

energy content comparable to gasoline and diesel fuels

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

Dual Fuel Vehicles - 101

CNG Conversion Rates

Source – FTA

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

Conversion Factors for LNG

• We told you LNG always sold as a liquid (we were right but there is still a problem)

• In the United States two different methodologies exist to convert LNG to volume measures: – Straight weight - 1 gallon weighs 3.5 pounds – Energy equivalent weight - 1 DGE weighs 6.06

pounds

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

• In Canada:– The Federal government determines the units of

measure and is strongly opposed to energy equivalents:• The source of the raw product, the refining/manufacturing

process, age of the finished product and season of use can all significantly affect the energy content of diesel and LNG

• In addition, temperature and pressure greatly affect LNG energy content

• The result, it is almost impossible to establish a fixed ratio to accurately compare these fuels

Conversion Factors for LNG

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

• In the United States:– Retail stations want DGE so the public can

compare LNG with diesel – National Conference on Weights and Measures is

likely to adopt DGE– Understand 18 states have DGE legislation (with two

more likely before year-end)

Conversion Factors for LNG

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

Short TrackBallot #05-2014

• As with last years CNG Ballot:– We need a consistent process for LNG reporting and

disbursement of taxes between jurisdictions– There is no impact to sovereignty (a jurisdiction tax

rates and units of measure are their responsibility (in the US)

– Other standards exist to ensure consistent reporting and distribution of taxes between IFTA members (e.g., distances, volumes, and currency)

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

Short TrackBallot #05-2014

• Are recommending, for IFTA reporting and transmittal purposes, that LNG be reported in energy equivalent measures:

• diesel gallon equivalent weighs 6.06 pounds; and • diesel liter equivalent weighs 0.7263 kilograms

• As an example:– If this ballot does not pass; and– I post an LNG tax rate of $0.29 per “gallon” is it…..

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

Short TrackBallot #05-2014

?

?

$0.29 / straight gallon (3.5 pounds)

$0.29 / Diesel Gallon Equivalent (6.06 pounds)

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

Short TrackBallot #05-2014

• At a high level:– Jurisdictions will send LNG tax rates to IFTA which

convert:• $C/litre to $US/gallon (for US jurisdictions - but is it a straight gallon or DGE?)

• $US/gallon to $C/litre (for Cdn jurisdictions - but is it based on a straight gallon or DGE?)

• IFTA and jurisdictions post LNG tax rates for carriers (straight gallon or DGE?)

– Carriers submit tax returns, base jurisdiction process and then send to Clearinghouse (straight gallon or DGE?)

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

Short TrackBallot #05-2014

– Base jurisdictions get Clearinghouse data from other jurisdictions and try to compare with Funds Netting (but will find that difficult because they don’t know if a straight gallon or DGE are being used?)

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

Short TrackBallot #05-2014

• Proposing:P1320 - FUELS NOT MEASURED IN LITERS OR GALLONSFor IFTA reporting and transmittal purposes, the use of liquefied natural gas shall be reported in energy equivalent measures (i.e., a diesel gallon equivalent in U.S. jurisdictions weighs 6.06 pounds, and a diesel liter equivalent in Canadian jurisdictions weighs 0.7263 kilograms).

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

Short TrackBallot #05-2014

• Proposing:– An effective date of July 2015 but comfortable

moving out to July 2016, if additional time is needed to make system changes

• Key issue is that we:– Think about the impact of dual fuels; and– Get a consistent unit of measure for LNG reporting

and disbursement of taxes between jurisdictions

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

Questions / Discussion

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

• Last year we proposed a methodology for accurately reporting dual fuel activity using the existing IFTA return concept

• This year I’d like to provide some further thoughts on how carriers, jurisdictions and IFTA could more easily communicate dual fuel activity

Dual Fuel Reporting for IFTA

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

• As background:• Dual fuel vehicles must be treated and reported

separately (e.g., pure diesel fuel fleet, the Diesel /LNG fleet, and the pure LNG fleet)

• In addition, each dual fuel fleet must be treated as if two vehicles, separately reporting the:• Distances travelled (after pro-rating to void double

counting distance travelled); and • Fuels purchased (e.g., pure diesel fleet vs. the diesel used in

the dual diesel/LNG fleet)

Dual Fuel Reporting for IFTA

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

• This reporting has the potential to create significant problems/complexities for:• Carriers reporting to base jurisdictions• Base jurisdictions:

• Processing carrier tax returns;• Transmitting data via the Clearinghouse (and non-

Clearinghouse jurisdictions), and• Desk/field audit activities

• Think simplest solution is to create several new fuel types to keep dual fleet activity separate

Duel Fuel Reporting for IFTA

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

• Recommending four new fuel types so everyone can better understand/see dual fuel activity

• End result is 3 for Diesel, 2 for LNG, and 2 for CNG as outlined below:

• D - for pure diesel vehicles (existing)

• LNG - for pure LNG vehicles (existing)

• CNG - for pure CNG vehicles (existing)

• DDL and DLNG - for diesel/LNG vehicles (two new)

• DDC and DCNG - for diesel/CNG vehicles (two new)

Duel Fuel Reporting for IFTA

Final Tax Return and Transmittal Data

A B C D E F G H

Fuel Type Jurisdiction Total Distance Taxable Distance

Taxable Fuel Volume

Tax Paid Volume

Net Taxable Volume

Tax Rate Tax Due

Pure Diesel Fleet

D J1 1,600,000 1,600,000 440,000 500,000 - 60,000 0.2000 -12,000.00

D J2 400,000 400,000 110,000 50,000 60,000 0.1500 9,000.00

DDL-DLNG Fleet

DDL J1 48,000 48,000 9,600 12,000 - 2,400 0.2000 -480.00

DDL J2 12,000 12,000 2,400 - 2,400 0.1500 360.00

DLNG J1 32,000 32,000 6,400 6,400 0.0500 320.00

DLNG J2 8,000 8,000 1,600 8,000 - 6,400 0.2000 -1,280.00

DDC-DCNG Fleet

DDC J1 10,667 10,667 3,200 2,000 1,200 0.2000 240.00

DDC J2 2,667 2,667 800 800 0.1500 120.00

DCNG J1 5,333 5,333 1,600 1,600 0.2500 400.00

DCNG J2 1,333 1,333 400 2,000 - 1,600 0.1000 -160.00

Duel Fuel Reporting for IFTA

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

• Clearinghouse Advisory Committee: • Is aware of the additional fuel types concept;• Clearinghouse can accept the additional fuel

types; but• Based on recent CAC survey 14 jurisdictions have

system limitations (i.e., no more than two characters for fuel types)

– I’m not sure two characters are sufficient but I’d like to leave that for CAC

Duel Fuel Reporting for IFTA

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

General Thoughts

• From a tax reporting/transmittal process dual fuel technology is:– A significant change in how we operate and will require

system changes; and – Also places a significant burden on carriers and auditors• Assuming everyone is in agreement it will take time

for jurisdictions to make system changes to accept/correctly process the incoming dual fuel returns

– Future Program Compliance Reviews should “note” but not “cite”

25

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

General Thoughts

• Lastly:• Natural gas use is growing; and• Jurisdictions that currently exempt or tax

natural gas at lower rates will likely see a reduction in overall fuel tax revenues as consumers convert to natural gas (e.g., private and commercial vehicles including marine applications etc.)

26

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

Questions / Discussion

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

Thanks!

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

FYI - Following slides are from last year’s presentation for reference purposes only/in case questions come up.

Recommended Reporting Process• At a high level:

– Dual fuel vehicles must be treated and reported separately (e.g., gasoline fleet, diesel fuel fleet, LNG fleet, dual fuel fleet)

– Duel fuel vehicles must be treated and reported as two vehicles: • Separately reporting the distances travelled and fuel purchased• Pro-rating the distances to avoid double counting

Fleet Type Fuel TypeIFTA Return

or Return Line

Actual Distance Travelled

Distances Reported

Pure Diesel Diesel “D” Return #1 100 100

Dual FuelDiesel “dD” Return #2 100 (pro-rated) 25

LNG “dL” Return #3 (pro-rated) 75

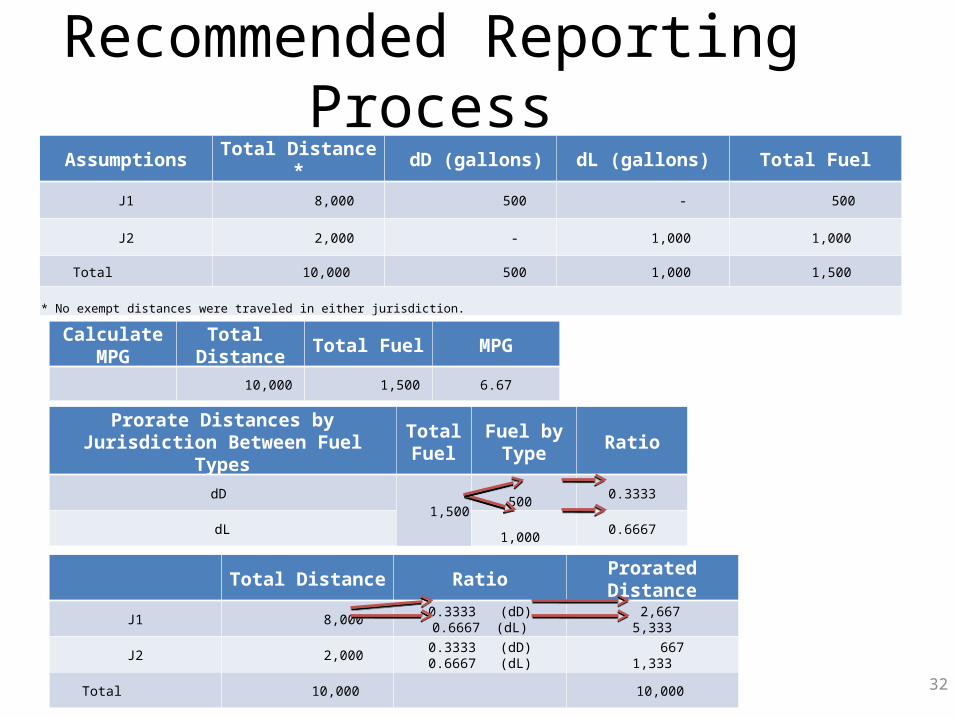

Recommended Reporting Process

• Dual vehicle distances are pro-rated based on their fuel purchases:

dD Distance = Total Distance Travelled * Diesel purchase Total (Diesel + LNG)

purchases

dL Distance = Total Distance Travelled * LNG purchases Total (Diesel + LNG) purchases

Recommended Reporting ProcessAssumptions Total Distance * dD (gallons) dL (gallons) Total Fuel

J1 8,000 500 - 500

J2 2,000 - 1,000 1,000

Total 10,000 500 1,000 1,500

* No exempt distances were traveled in either jurisdiction.

32

Calculate MPG Total Distance Total Fuel MPG

10,000 1,500 6.67

Prorate Distances by Jurisdiction Between Fuel Types

Total Fuel Fuel by Type Ratio

dD 1,500

500 0.3333

dL 1,000 0.6667

Total Distance Ratio Prorated Distance

J1 8,000 0.3333 (dD)0.6667 (dL)

2,667 5,333

J2 2,000 0.3333 (dD)0.6667 (dL)

667 1,333

Total 10,000 10,000

Recommended Reporting Process

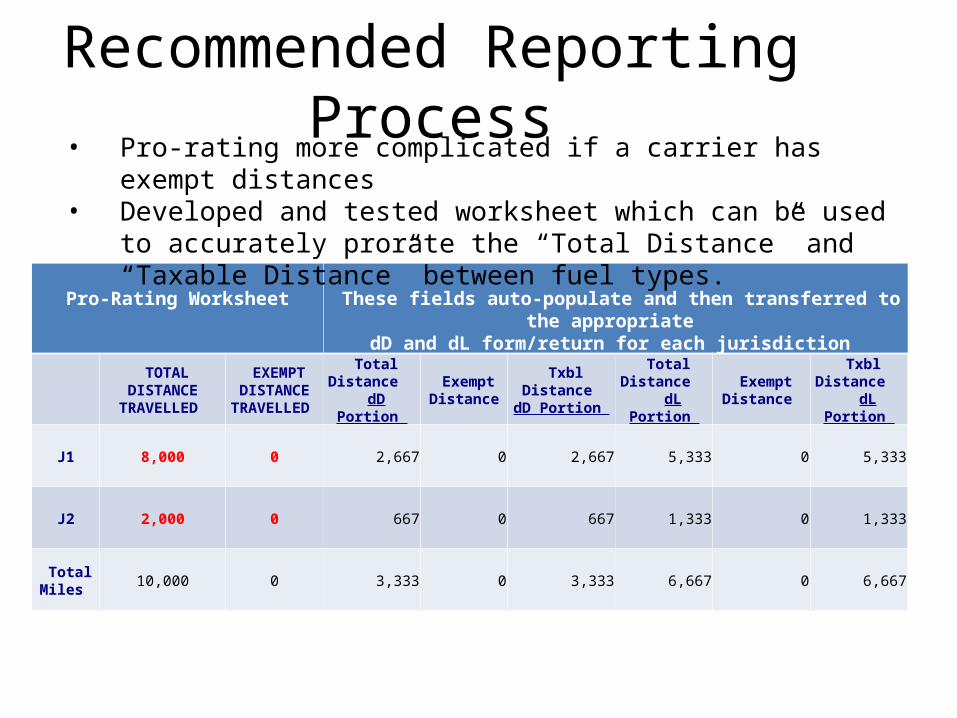

Pro-Rating Worksheet

These fields auto-populate and then transferred to the appropriate

dD and dL form/return for each jurisdiction

TOTAL DISTANCE

TRAVELLED

EXEMPT DISTANCE

TRAVELLED

Total Distance dD Portion

Exempt Distance

Txbl Distance dD Portion

Total Distance dL Portion

Exempt Distance

Txbl Distance dL Portion

J1 8,000 0 2,667 0 2,667 5,333 0 5,333

J2 2,000 0 667 0 667 1,333 0 1,333

Total Miles

10,000 0 3,333 0 3,333 6,667 0 6,667

• Pro-rating more complicated if a carrier has exempt distances• Developed and tested worksheet which can be used to accurately

prorate the “Total Distance” and “Taxable Distance” between fuel types.

Recommended Reporting Process Dual Fuel Vehicles – Diesel Average MPG 6.67

Fuel Type Jurisdiction Total Distance

Txbl Distance

Txbl Volume

Tax Paid Volume

Net Txbl Volume Tax Rate Tax Due

dD J1 2,667 2,667 400 500 -100 0.2000 -$ 20.00

dD J2 667 667 100 0 100 0.1000 $ 10.00

Sub-total 3,333 3,333 500 500 0 -$ 10.00

Dual Fuel Vehicles – LPG

Average MPG 6.67

Fuel Type Jurisdiction Total Distance

Txbl Distance

Txbl Volume

Tax Paid Volume

Net Txbl Volume Tax Rate Tax Due

dL J1 5,333 5,333 800 0 800 0.0500 $ 40.00

dL J2 1,333 1,333 200 1,000 -800 0.1000 - $ 80.00

Sub-total 6,667 6,667 1,000 1,000 0 -$ 40.00

TOTAL DUAL-FUEL VEHICLES 10,000 10,000 1,500 1,500 -$ 50.00

August 13-14 Pittsburgh, Pennsylvania2014 Annual Business Meeting

General Thoughts

• Worst Case - US carrier with a dual fuel vehicle in Canada• Buys:

• Diesel in Canadian currency and litres; and• LNG in Canadian currency and kilograms

• Separately track all fuel purchases (e.g., D, DDL, DLNG, DDC, and DCNG):• Convert to US currency and converts:

• Diesel liters to gallons• LNG kilograms to a straight gallon or DGE…?

• Combines with all US activity• Then pro-rates distances travelled by dual fuel vehicle to avoid double

counting• Then completes tax separate tax returns/schedules for each fuel type:

• DDL - diesel portion of the dual fuel vehicle; and• DLNG - LNG portion of the dual fuel vehicle

35

Top Related