WTO Agriculture Negotiations – Challenges and ... · WTO Agriculture negotiations – Challenges...

106

` Lahore, 7 – 8 July 2006 Seminar proceedings WTO Agriculture negotiations – Challenges and opportunities for Pakistan

Transcript of WTO Agriculture Negotiations – Challenges and ... · WTO Agriculture negotiations – Challenges...

`

Lahore, 7 – 8 July 2006

Seminar proceedings

WTO Agriculture negotiations – Challenges and opportunities for Pakistan

This publication has been produced with the assistance of the European Union (EU) as part of an EU-funded Trade Related Technical Assistance (TRTA) programme with the Government of Pakistan. The International Trade Centre (ITC) is implementing the programme. The content of this publication is the sole responsibility of the implementing agency. Facts and figures set forth in this publication are the responsibility of the implementing agency and should not be considered as reflecting the views or carrying the endorsement of the EC, ITC, UNCTAD, or WTO. The factual details and in-country resources in the publication have been researched and compiled by the implementing agency. ITC has not formally edited this report.

Written by: ITC/DTSS/BAS

© International Trade Centre (UNCTAD/WTO) Palais des Nations, 1211 Geneva 10, Switzerland Email: [email protected] http://www.intracen.org Publication No. BAS/TS/PAK/E/06/02 Distribution: UNRESTRICTED October 2006

ITC: Your Partner in Trade Development The International Trade Centre is the joint technical cooperation agency of the United Nations Conference on Trade and Development (UNCTAD) and the World Trade Organization (WTO) for business aspects of trade development. ITC’s mission is to contribute to sustainable development through technical assistance in export promotion and international business development. ITC’s strategic objectives are:

Enterprises – Strengthen the international competitiveness of enterprises.

Trade support institutions – Develop the capacity of trade service providers to support businesses.

Policymakers – Support policymakers in integrating the business sector into the global economy.

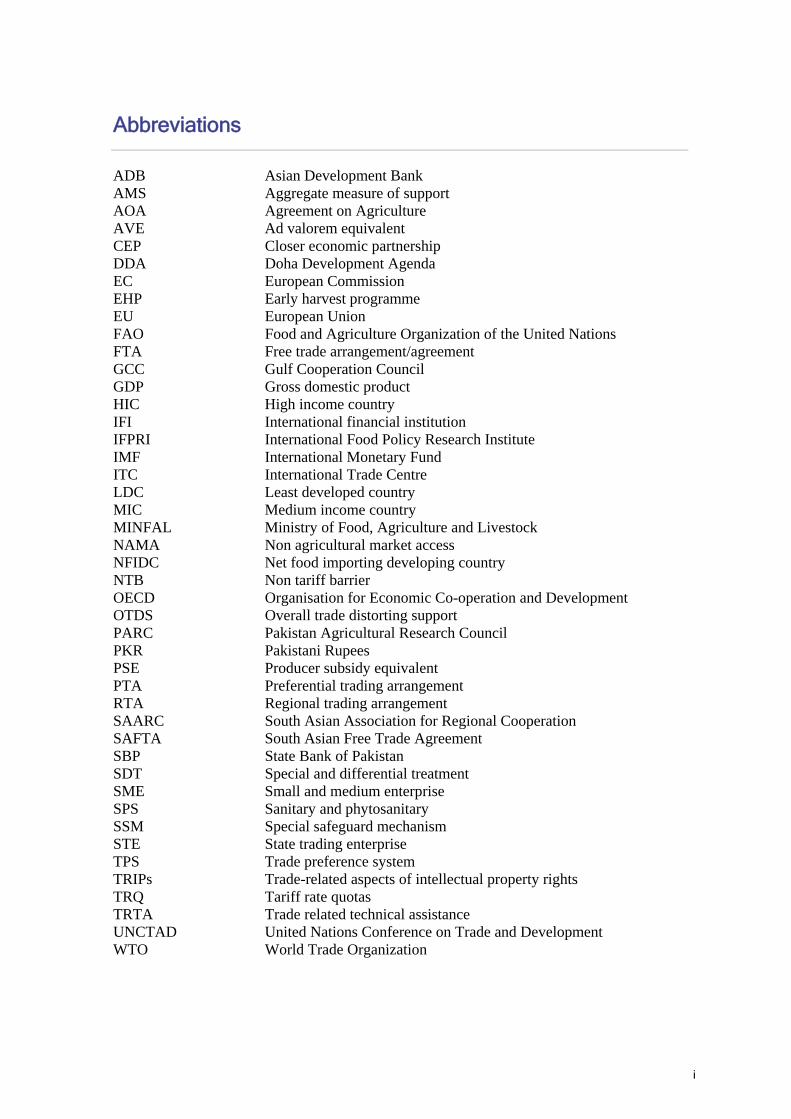

Abbreviations

ADB Asian Development Bank AMS Aggregate measure of support AOA Agreement on Agriculture AVE Ad valorem equivalent CEP Closer economic partnership DDA Doha Development Agenda EC European Commission EHP Early harvest programme EU European Union FAO Food and Agriculture Organization of the United Nations FTA Free trade arrangement/agreement GCC Gulf Cooperation Council GDP Gross domestic product HIC High income country IFI International financial institution IFPRI International Food Policy Research Institute IMF International Monetary Fund ITC International Trade Centre LDC Least developed country MIC Medium income country MINFAL Ministry of Food, Agriculture and Livestock NAMA Non agricultural market access NFIDC Net food importing developing country NTB Non tariff barrier OECD Organisation for Economic Co-operation and Development OTDS Overall trade distorting support PARC Pakistan Agricultural Research Council PKR Pakistani Rupees PSE Producer subsidy equivalent PTA Preferential trading arrangement RTA Regional trading arrangement SAARC South Asian Association for Regional Cooperation SAFTA South Asian Free Trade Agreement SBP State Bank of Pakistan SDT Special and differential treatment SME Small and medium enterprise SPS Sanitary and phytosanitary SSM Special safeguard mechanism STE State trading enterprise TPS Trade preference system TRIPs Trade-related aspects of intellectual property rights TRQ Tariff rate quotas TRTA Trade related technical assistance UNCTAD United Nations Conference on Trade and Development WTO World Trade Organization

i

ii

Contents

Abbreviations i Introduction 1

EC TRTA programme for Pakistan 1 The seminar 1 The negotiations 2 The role of business 3

Seminar report 5 Invitation 7 Programme 9 Presentations 13

Welcome and introductions 13 Mr. Fayyaz Bashir, Secretary of Agriculture, Government of the Punjab 13 Mr. Michael Dale, Counsellor and Head of Operations, European Commission Delegation to Pakistan, Islamabad 14 Mr. Bruce Shepherd, International Trade Centre, Geneva 15

Opening remarks 19 Mr. Sikandar Hayat Khan Bosan, Federal Minister for Food, Agriculture & Livestock 19

Economics and dynamics of agricultural trade liberalisation 21 Dr. David Blandford, Pennsylvania State University 21

Quantitative analysis of the negotiations 29 Dr. David Orden, International Food Policy Research Institute (IFPRI) and Virginia Polytechnic Institute and State University 29

Analysis of the negotiations: Market access proposals 40 Dr. H. Bruce Huff, Huff & Associates, Ottawa 40

Implications for Pakistan 46 Mr. Shezada Taimur Khusrow, Deputy Secretary (Planning), Federal Ministry of Food, Agriculture & Livestock 46 Dr. Sohail Malik, Higher Education Commission of Pakistan Professor of Economics at the University of Sargodha 51

Commodity presentations 62 Cotton – Mr. Ibad Bader, Vice President, Pakistan Central Cotton Committee, Karachi 62

iii

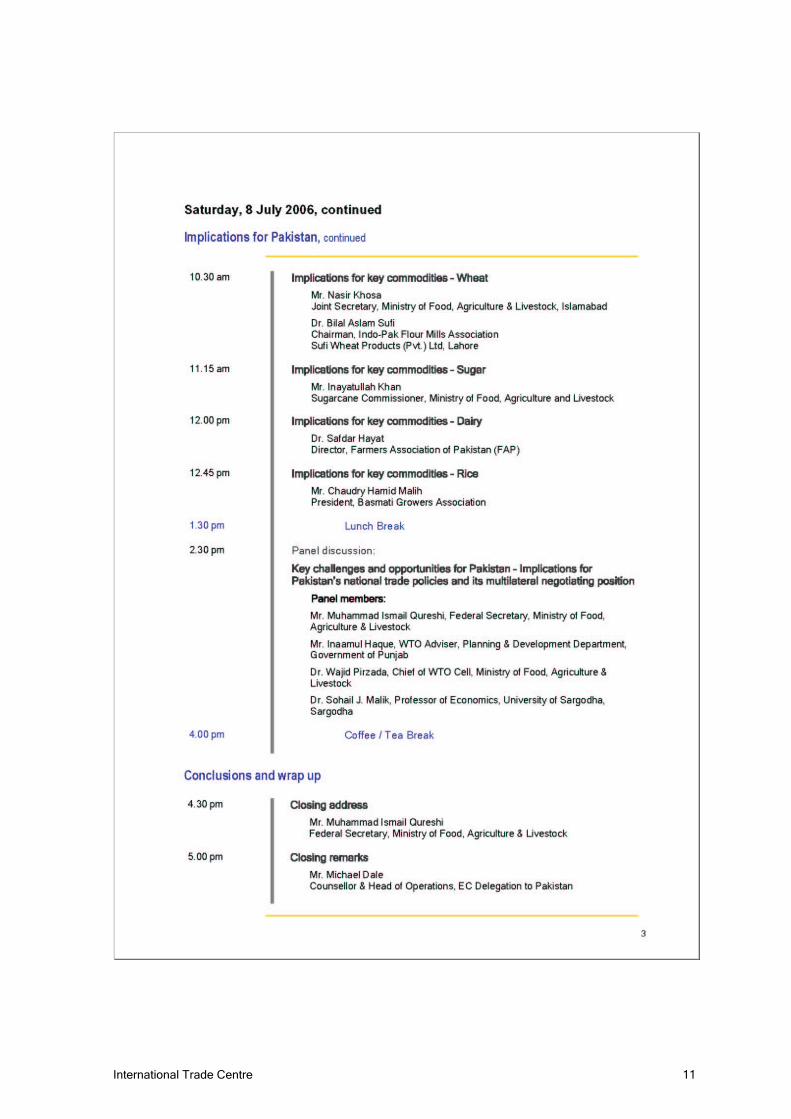

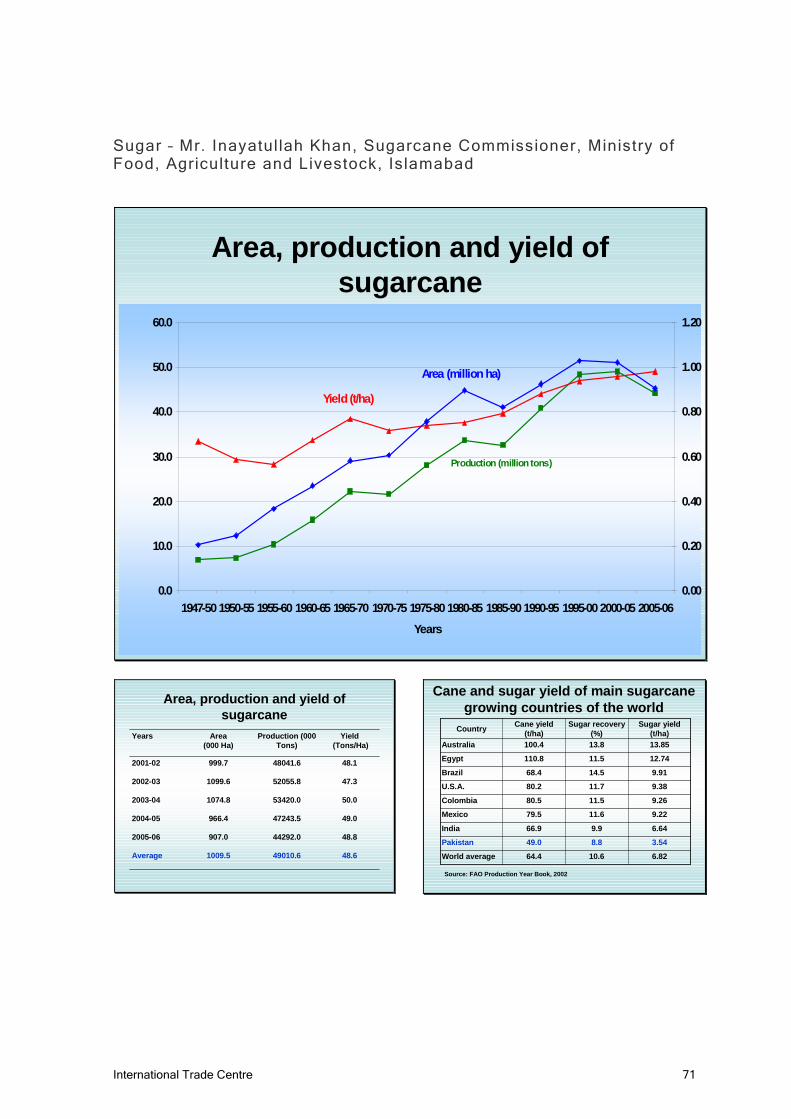

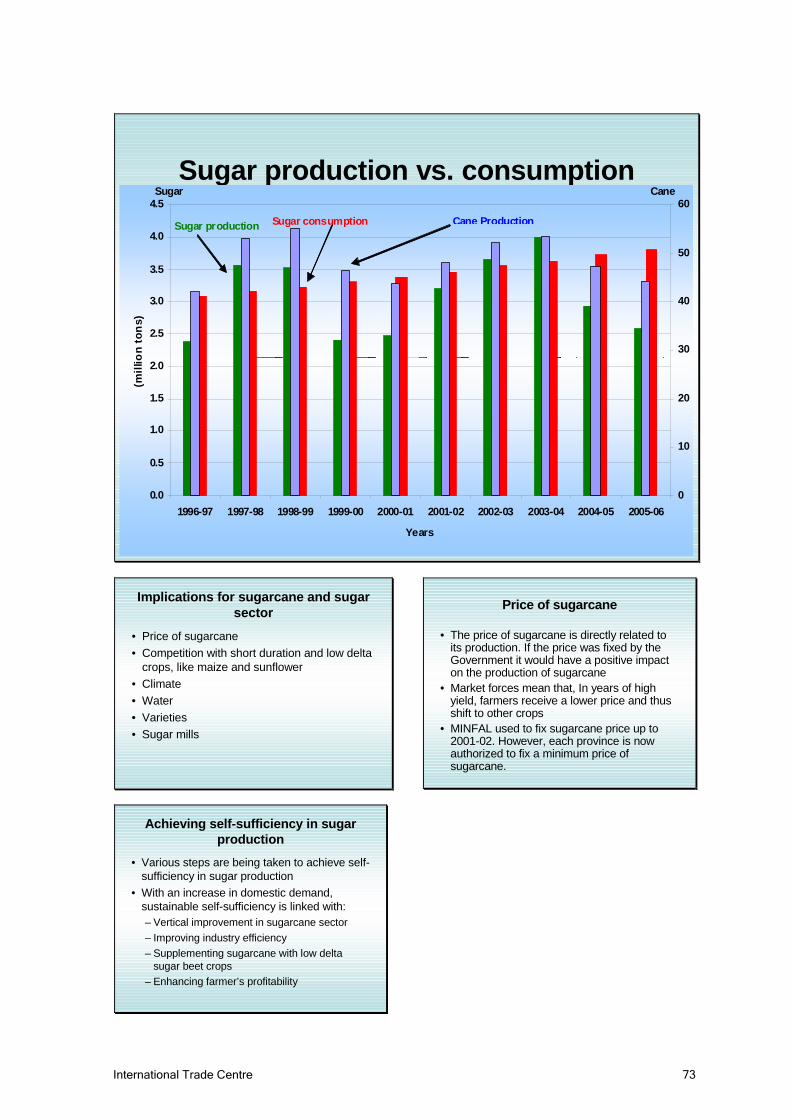

Wheat – Mr. Nasir Khosa, Joint Secretary, Federal Ministry of Food, Agriculture & Livestock 64 Wheat – Mr. Bilal Aslam Sufi, Chairman, Indo-Pak Flour Mills Association, and Head, Sufi Wheat Products (Pvt.) Ltd, Lahore 67 Sugar – Mr. Inayatullah Khan, Sugarcane Commissioner, Ministry of Food, Agriculture and Livestock, Islamabad 71 Dairy – Mr. Safdar Hayat, Director, Farmers Association of Pakistan, Lahore 74 Rice – Mr. Chaudry Hamid Malih, President, Basmati Growers Association, Lahore 77 Questions and comments on the commodity presentations 79

Panel discussion 82 Dr. Sohail J. Malik, University of Sargodha 82 Mr. Inaamul Haque, WTO Adviser, Planning & Development Department, Government of Punjab 83 Questions and comments 85

Concluding remarks 88 Mr. Muhammad Ismail Qureshi, Federal Secretary of Food, Agriculture & Livestock 88 Mr. Michael Dale, EC Delegation to Pakistan 90

Part icipants 93

iv

Introduction

EC TRTA programme for Pakistan

This report presents the proceedings from the seminar entitled “WTO Agriculture negotiations: Challenges and opportunities for Pakistan”, held in Lahore, Pakistan, on 6 and 7 July 2006.

The seminar was held as part of the European Commission (EC) Trade-related Technical Assistance (TRTA) Programme for Pakistan, which the International Trade Centre (ITC) is implementing. The programme aims to enhance awareness among government officials, the business sector and civil society about the implications of the World Trade Organization (WTO) Agreements on the national economy, and to assist Pakistan in building the necessary capacity to address issues resulting from its participation in the WTO.

The seminar was one of a series of seminars focusing on various aspects of the WTO negotiating framework – the others include Services (Karachi, May 2005), NAMA (Karachi, November 2006), and Trade Facilitation (end 2006).

The seminars involve both public and private sector stakeholders, and are designed to increase awareness of the negotiations and their progress, to look ahead to the challenges and opportunities that the negotiations may provide for both government policy and business practice. This enhanced knowledge will equip business leaders to play a more meaningful advocacy role with the government, with a view to contributing to the completion of the WTO negotiations. The seminars are intended to foster communication between business and government, leading to the formation of negotiating positions in line with national needs and inclusive of the real and concrete economic and commercial interests of the country.

Although the WTO negotiations were suspended in late July, WTO Members are hopeful that the break will be temporary and short. Therefore, it is still very important for all interested actors to take a close interest in the issues under negotiation. Indeed, calls for a swift resumption of the negotiations have since come from many quarters — ASEAN, the G20, the Cairns Group, the World Bank-IMF Finance Committee and many Presidents and Ministers around the world. Developing countries have been loudest in calling for a resumption of the negotiations, recognising that the costs of failure, and the missed opportunity to rebalance the multilateral trading system, would hurt them more than others.

The seminar

The WTO Agriculture negotiations are important for business actors involved in trade in agricultural goods because they will influence the global and national conditions of doing business. The negotiations encompass strengthened rules, and specific commitments on government support and protection for agriculture, in order to correct and prevent restrictions and distortions in world agricultural markets. This will improve predictability and security for importing and exporting countries alike.

International Trade Centre 1

This seminar was designed to deepen the understanding of the commercial and economic implications of these negotiations, and of the emerging international trading system. Discussion was designed to bring out the new market access opportunities and threats for business through discussion with international and national experts, business leaders, academicians and trade policy analysts and negotiators.

The seminar programme covered:

• The state of play of the negotiations

• The likely results of the negotiations for important products and markets — specifically, cotton, wheat, sugar, dairy and rice

• The new market access opportunities that might emerge from the negotiations

• The challenges business might need to face in an open trading environment

• Factors the Government might need to consider in terms of its national and international trade policies, regulations and obligations

• How the government and business can best work together to make the most of the new environment.

The negotiations

The WTO Agriculture negotiations have their origins in the Agreement on Agriculture (AOA), negotiated during the Uruguay Round. In early 2002 these negotiations became part of both the Doha Development Agenda (DDA) and the overall package comprising all negotiating issues, called the “single undertaking”. A new phase of the DDA started in September 2004, and these negotiations entered a crucial phase from 2005.

The mandate for the Agriculture negotiations is set out in paragraphs 13 and 14 of the Doha Ministerial Declaration. The long-term objective of the reform process – a fair and market-oriented trading system for agricultural products – is to be achieved through a reform programme consisting of both strengthened rules and specific commitments on support and protection. The comprehensive negotiations cover the three basic pillars contained in the AOA:

• Improvements in market access,

• Reduction, with a view to phasing out, of all forms of export subsidies, and

• Reduction of trade-distorting domestic subsidies.

Special and differential treatment (SDT) for developing countries is an integral part of the negotiations. The outcome should be effective in practice and enable developing countries to meet their needs, in particular in food security and rural development.

The negotiations also take note of the non-trade concerns (such as environmental protection, food security, rural development, etc) provided for in the Agriculture Agreement.

2 International Trade Centre

The Agriculture talks constitute an integral part – possibly the most important part – of the DDA negotiations. The negotiations, including Agriculture, form a single undertaking, i.e. the outcome of the talks will constitute a set of rights and obligations that Members must accept in their entirety. Accordingly, the balance of rights and obligations needs to be ensured across the entire package.

Because of this inter-linkage, progress in the Agriculture negotiations is seen as critical to unlocking progress in other negotiation areas. While some progress has been made, much remains to be done to conclude the negotiations. This was recognised in the Hong Kong Ministerial Declaration, which agreed to intensify work on all outstanding issues to fulfil the Doha objectives, and set a deadline for the establishment of modalities no later than 30 April 2006 and to submit comprehensive draft Schedules based on these modalities no later than 31 July 2006.

In the event, it was not possible to meet the 30 April deadline. A Ministerial meeting held at the end of June was unable to narrow the gaps on formulas for reducing tariffs and subsidies, various flexibilities, and other disciplines that would be in the “modalities” for agriculture and industrial goods (NAMA).

Members agreed that WTO Director General, Pascal Lamy, should consult intensively and widely in order to establish these “modalities”. Unfortunately, the Director General was unable to identify any significant changes in negotiators’ positions and the gaps remained too wide.

Faced with this situation, the entire negotiations were suspended in late July to enable serious reflection by participants. WTO Members expressed the hope that this “time-out” would be temporary and short since there was a need to put the negotiations back on track as soon as possible. They also said that the achievements of the negotiation so far should be preserved and built upon rather than unravelled. They agreed not to modify the mandate or split it allowing for selective progress.

The role of business

Business actors have a vital role to play in the Agriculture negotiations. A successful DDA will bring important changes affecting not just trade but also core agricultural policies, the conditions of protection and the support of agricultural production. All these changes directly affect the interests of business within, and even outside, the farm sector.

The stakes for business are high — developments in the WTO negotiations will have a huge impact on the way business is done in Pakistan. For example, improvements in market access, the reductions in subsidies and tariffs and the elimination of non-tariff barriers (NTBs), will all affect the trading environment. Therefore, business actors have a vital role to play in the Agriculture negotiations.

It is also important for business to follow closely the negotiating process. If business wants to be in a position to influence the outcome, they need to be aware of the details. Business needs to do its homework, on an industry basis, and to inform governments under what sort of rules it can do business.

International Trade Centre 3

Both sides gain to benefit from a constructive two-way dialogue on these issues. Business leaders need to be aware of international trading rules and their implications so that their businesses can adapt and grow in an ever more competitive environment. Governments, also, need to be up-to-date with the views of their business sectors when they are devising negotiating strategies and formulating trade policies. Trade policy and negotiations are about commerce, and business groups can provide information or insights on commercial issues that government officials do not have.

4 International Trade Centre

Seminar report

The seminar was designed to increase awareness of the WTO Agriculture negotiations and their progress, and to look ahead to the challenges and opportunities that the negotiations may provide for both government policy and business practice in Pakistan. The seminar was well attended, with approximately 80 participants, including international and national experts, business leaders, academicians and trade policy analysts and negotiators. The participants included around 15 women.

Following introductions by key stakeholders, day one was focused on analysing the negotiations from multinational, regional and national perspectives. The following day, presenters looked at the implications of the negotiations on key agricultural commodities of cotton, wheat, sugar, dairy and rice. A panel discussion followed, drawing out the challenges and opportunities for Pakistan, including the implications for Pakistan’s national trade policies and its multilateral negotiating position. The Federal Secretary of Food, Agriculture & Livestock and the representative of the EC Delegation to Pakistan made closing remarks.

The international experts set the scene in the substantive part of the seminar by presenting comprehensive overviews of the status of the negotiations, possible scenarios for Pakistan when these eventually concluded, and the need for Pakistan to continue to look at the details of the process. Commodity producers picked up these themes in presentations covering Pakistan’s cotton, wheat, sugar, dairy and rice sectors.

Discussion followed on issues related to production, dealing with subsidies and getting more government understanding of what producers need to become more efficient. Participants were concerned to ensure that Pakistan did not “miss out” on any potential benefits from an Agreement on Agriculture. In expressing this concern, participants recognized the need to improve both their understanding of the issues and their capacity to better dialogue with government negotiators to ensure the negotiators had a better understanding of business and producer concerns.

Participants were interested to ensure the competitiveness of both traditional and emerging export sectors. Sanitary and phytosanitary (SPS) issues came in for comment, as did the need for producers to be better informed about the requirements of importing authorities, and the desires of consumers. Pakistan’s capacity to market its exports also came in for much discussion.

In addition to these seminar proceedings, a national study of Pakistan’s agriculture sector has been published separately. The study, prepared by Dr. Sohail Malik as input to the seminar discussions, specifically focuses on the challenges and opportunities presented by the WTO Agriculture negotiations. Copies of both publications are available to download from http://www.accesspakistan.org.

International Trade Centre 5

6 International Trade Centre

Invitation

International Trade Centre 7

8 International Trade Centre

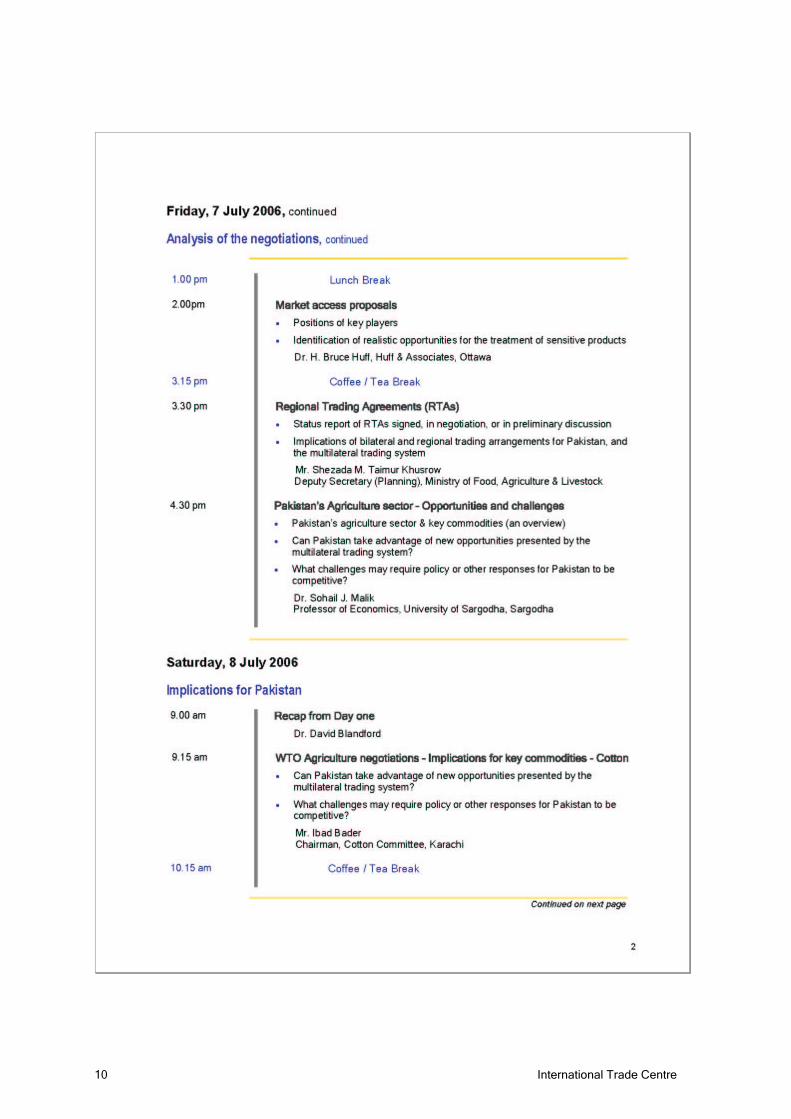

Programme

International Trade Centre 9

10 International Trade Centre

International Trade Centre 11

12 International Trade Centre

Presentations

Welcome and introductions

Mr. Fayyaz Bashir, Secretary of Agriculture, Government of the Punjab

[Edited transcript]

Honourable Minister of Food, Agriculture & Livestock; distinguished foreign delegates; national and international WTO experts; business leaders; ladies and gentlemen.

On behalf of the Punjab Government and the Agriculture Department, it is my privilege to welcome you to participate in this seminar on the WTO Agriculture Negotiations – Challenges and Opportunities for Pakistan.

We are grateful to the Ministry of Food, Agriculture & Livestock (MINFAL) and the International Trade Centre (ITC) for arranging this seminar under the European Commission Trade Related Technical Assistance (TRTA) Programme. The seminar will provide an excellent opportunity for business people, government officials and other provincial colleagues to listen to, and discuss, various aspects of the WTO Agriculture negotiations with the national and international WTO experts, so as to deepen our understanding of the commercial and economic implications of the negotiations and the multilateral global trading system.

Agriculture is the largest and most important sector of Pakistan’s economy, comprising almost 50% of exports and, directly or indirectly, contributing more than 50% of international trade. Therefore, the implications of the WTO agriculture negotiations are extremely critical for our economy. More favourable conditions, such as greater market access and better prices of agricultural products due to reductions in subsidies from developed countries, can greatly support Pakistan’s farmers and reduce poverty in rural areas.

The Government and private sector are fully aware of the importance of the WTO Agreements regulating the multilateral trading system. Pakistan fully supports the WTO. We are also closely following the WTO negotiations on agriculture, which are at a crucial stage at this moment. We hope the negotiations are successfully concluded, leading to a fair, market-oriented trading system for agricultural products.

International Trade Centre 13

Mr. Michael Dale, Counsellor and Head of Operat ions, European Commission Delegation to Pakistan, Islamabad

[Edited transcript]

Honourable Minister of Agriculture; Secretary of Agriculture, Government of Punjab; friends from ITC; honourable ladies and gentlemen.

I am very pleased to be here on this important occasion. I want to welcome you on behalf of the European Commission to this very important seminar, which comes at a critical time – not only for Pakistan but also for a very large number of developing countries involved in agriculture.

I would like to extend my thanks to ITC and the government partners who have organized this high-level seminar on the challenges and opportunities for Pakistan arising out of the WTO agriculture negotiations.

I am very glad that, under the TRTA, we have brought you a discussion on a key issue of paramount importance globally – especially to Pakistan, which is very involved in agriculture exports. The WTO negotiations are at a critical stage at this time. There is now a strong realization that real concessions on many sides are needed to enable a proper level playing field in the negotiations. As far as the EU is concerned – and I know this from our Directorate General for Trade – there needs to be real dialogue in order to establish real cuts. Thus, I think this seminar is very timely.

I believe that all of you in the export business, or who would like to be, should be involved in the negotiations: whatever comes out of the negotiations will affect, directly or indirectly, the way you do business. The EC is very concerned about its developing country trading partners. It has been supporting developing countries in trade negotiations, providing them trade related assistance financed by the successful TRTA programme. The TRTA was conceived to help countries like Pakistan deal with the technicalities of the multilateral trading system. I hope, with new programmes in the future, we can continue to provide support to businesses in Pakistan, and also to do better business with our trading partners.

I hope that one thing this seminar will do is “demystify” these negotiations. Not everyone can understand the WTO negotiations. However, the outcome of the negotiations will affect us all. Thus, it is vital that people are aware of what is going on so they can provide more input to these negotiations.

I am very happy that the EC can support this seminar. I hope you will be able to stay until the end. The programme will bring a lot of inputs from specialists. I know we are dealing with complex and technical matters, so I hope that our experts will make their presentations in a way that we can follow them. In this type of seminar, it is important for everybody to understand what is going on and how he or she can contribute.

I look forward to a very positive dialogue, especially with regard to the question and answer sessions.

14 International Trade Centre

Mr. Bruce Shepherd, International Trade Centre, Geneva Bruce Shepherd is a New Zealand national currently working as Senior Business Advisory Services Officer in the Division of Trade Support Services at the International Trade Centre (ITC) in Geneva. During his time at ITC, Mr. Shepherd has been involved in developing tools for use by small and medium enterprises (SMEs) to improve their export competitiveness, working with ITC partners to improve the provision to export development services to SMEs, and delivering trade related technical assistance to ITC partner countries.

Before joining ITC, Mr. Shepherd had assignments in both the trade promotion and trade policy arenas, with postings in the Middle East as New Zealand Trade Commissioner to the six countries of the Gulf Cooperation Council, and in the Pacific as New Zealand Deputy High Commissioner in Tonga.

Mr. Shepherd has specific interests in export development, trade promotion, market development and international trade issues. In addition to his work offshore, Mr. Shepherd has worked closely on indigenous economic development issues in New Zealand and retains strong linkages to developments in this area.

The Honourable Mr. Sikandar Hayat Khan Bosan, Minister of Food, Agriculture & Livestock; Mr. Muhammad Ismail Qureshi, Federal Secretary of Food, Agriculture & Livestock; Mr. Michael Dale, Counsellor and Head of Operations, EC Delegation to Pakistan; Mr. Fayyaz Bashir, Secretary of Agriculture, Government of Punjab; Distinguished guests; Ladies and gentlemen.

I am very pleased to be here today to welcome you – on behalf of the International Trade Centre – to this seminar on the WTO agriculture negotiations.

The seminar is entitled “WTO Agriculture Negotiations – Challenges and Opportunities for Pakistan”.

Despite the lack of agreement in Geneva a week ago – or perhaps because of it – the next two days provide us with a very well-timed opportunity to deepen our understanding of the commercial and economic implications for Pakistan of these negotiations, and of the evolving multilateral trading system.

The seminar has brought together international and national experts, business leaders, academics, trade policy analysts and trade negotiators, to consider and discuss:

• What new market access opportunities might emerge from the negotiations?

• The challenges business might need to face in an open trading environment?

• What might the Government of Pakistan need to consider in terms of its national and international trade policies, regulations and obligations?

• How the government and business can best work together to make the most of the new environment?

This seminar is one of a number on various aspects of the WTO negotiations, taking place as part of a Trade Related Technical Assistance (TRTA) programme for Pakistan, funded by the European Union.

International Trade Centre 15

The EC TRTA programme started in September 2004 with the objective of assisting Pakistan to foster its integration into the world economy and to contribute to Pakistan’s development through the achievement of trade-related conditions for sustained and stable economic growth.

Through this programme, the International Trade Centre (ITC) is working with Pakistan to enhance awareness and assist in building its capacity to benefit fully from participation in the WTO Agreements.

ITC is the technical cooperation agency of the United Nations Conference on Trade and Development (UNCTAD) and the World Trade Organization (WTO) for operational and enterprise-oriented aspects of international trade development.

ITC is also the UN’s focal point for technical cooperation in trade promotion – we work with developing countries and economies in transition to set up effective trade promotion programmes to expand their exports and improve their import operations.

In other words, our focus is on business.

Business needs to be aware of WTO rules and their implications, so that their businesses can grow and thrive in an ever more competitive environment.

Governments need to be up-to-date with the views of their business sector when devising negotiating strategies and formulating national positions in WTO trade discussions.

An important part of ITC’s work involves:

• Ensuring that businesses have good access to useful and up-to-date information about the multilateral trading system, and

• Promoting an informed and useful dialogue on trade between governments and their business communities.

Establishing and supporting effective consultations between the government and the private sector on trade issues is also a goal shared by the EC.

The Hong Kong Ministerial Declaration talked about ITC’s role in providing a platform for business to interact with trade negotiators, and practical advice for [SMEs] to benefit from the multilateral trading system …”

This seminar is a perfect example of such a platform for interaction to take place.

Business should play a vital role in the Agriculture negotiations. Successful negotiations will bring important changes, affecting not just trade but also core agricultural policies, the conditions of protection and the support of agricultural production. All these changes directly affect the interests of farmers and other business within, and even outside, the farm sector.

If business wants to be in a position to influence the outcome of the negotiations, they have to be aware of the details. This enhanced knowledge will equip farmers and business leaders to play a more meaningful advocacy role with the government, with a view to contributing to the completion of the negotiations.

16 International Trade Centre

I won’t talk in detail about the Agriculture negotiations themselves – I’ll leave that to the experts we’ve brought together for the seminar.

However, it is worth mentioning that the Agriculture negotiations are an integral part – some say the most important part – of the Doha Development Agenda negotiations.

This is because the negotiations, including Agriculture, form a single undertaking – that is, the outcome of the talks will constitute a set of rights and obligations that Members must accept in their entirety.

Because of this link, making progress in the Agriculture negotiations is seen as critical to making progress in other negotiation areas. And, as we have seen, achieving this progress has not been easy.

This difficulty in finding agreement was again obvious a week ago in Geneva when, after several days of intensive meetings, Ministers and officials were unable to narrow the gaps on formulas for reducing tariffs and subsidies, various flexibilities, and other disciplines that would be in the “modalities” for agriculture and industrial goods (NAMA).

Members agreed that WTO Director General, Pascal Lamy, should consult intensively and widely in order to establish these “modalities”. The consultations are based on the draft texts in agriculture and non-agricultural market access.

No deadline was set – the Director-General will report back to the members as soon as possible. WTO Members remain committed to completing the negotiations by the end of the year.

I am sure that Pakistan’s trade policy officials and negotiators will continue to be actively involved in this work over the coming months. In doing so, there is no doubt that they will benefit from the presentations and discussion on the challenges and opportunities for Pakistan that will take place in this seminar over the next two days.

I look forward to a productive and informative two days.

International Trade Centre 17

18 International Trade Centre

Opening remarks

Mr. Sikandar Hayat Khan Bosan, Federal Minister for Food, Agriculture & Livestock

[Edited transcript]

Mr. Bashir; Mr. Dale; distinguished ladies and gentlemen.

It is a great privilege for me to address such a diverse group of people, including national and international experts, business leaders, trade policy analysts and negotiators, looking at the WTO agriculture negotiations and their challenges and opportunities for Pakistan. I understand that bringing together such a wide range of knowledgeable people requires tremendous coordination and allocation of resources. I am grateful to ITC and the TRTA for initiating this activity and hope that all stakeholders will benefit from this two-day session with the national and international experts.

It is widely recognized that the agriculture negotiations are pivotal to the overall Doha Development Agenda. Without a successful conclusion of the agriculture negotiations, there will be no agreement. Pakistan has been a strong supporter of the multilateral negotiations. Reductions in agricultural support and protection are expected to benefit Pakistan’s producers through higher and more stable global commodity prices. Pakistan’s agricultural exports will benefit from improved market access. Realizing that the real benefits will come from “market access”, we are pursuing our interests without compromising the other pillars of the negotiations.

For Pakistan, higher global prices expected as an outcome from the WTO negotiations are viewed as very important to the reduction in rural poverty. As an example, an Asian Development Bank (ADB) study estimates that just a 20% increase in cotton prices would move 2 million people out of poverty in Pakistan. Pakistan is well aware that the growth markets in the 21st century are in developing countries. Population and income growth in developing countries will greatly exceed those in OECD countries. Similar quality and food safety standards in developing countries make it easier for Pakistan to supply these markets. Pakistan is conscious that, as part of the WTO negotiations, market access must also be improved in developing countries to accelerate the growing South-South trade.

We have already made the difficult internal adjustments on market access. Pakistan has lowered its applied tariffs on most agriculture and food products to the range of 0%–25%. As a result, Pakistan stands ready to take advantage of the reductions in support and protection in other countries coming out of the Doha Round. Pakistan has worked in the WTO to ensure that any agreement will not restrict Pakistan’s ability to introduce new policies and programmes for the agriculture sector. A new agreement will not limit the introduction of any ‘Green’ or non-trade distorting programmes for the agriculture and food sector in Pakistan. Even for the more trade distorting, or Amber-type programmes, Pakistan would have the ability to spend up to 20% of the value of its agricultural production.

International Trade Centre 19

Pakistan is a small player in the international agriculture market. We have been able to leverage our limited influence within the WTO through membership of a number of negotiating groups, including the G-33, the G-20 and the Cairns Group.

The Doha negotiations have made considerable progress. They have achieved a consensus among countries in a number of areas that only a short time ago would have been considered impossible. In Hong Kong, countries agreed to eliminate all export subsidies by 2013. Also in Hong Kong, there was agreement by developed countries to allow duty-free and quota free access on most products to the poorest countries. There is relatively close agreement on the process and level of tariff cuts. Failure of the round will mean that gains made so far for developing countries will disappear or will lead to more FTAs and PTAs at the cost of multilateralism.

Unfortunately, there are many differences that remain. At the WTO meeting in Geneva last weekend, Ministers were not able to resolve these differences. There is agreement to continue the negotiations process. The differences among countries are considered “bridgeable”. All countries recognize the importance of an agreement and do not want the Doha Round to fail. The Director-General of the WTO has been asked to undertake a consultative process with the members with the expectation that there may be an agreement reached before the end of this month. All members remain committed to completing the negotiations by the end of 2006.

20 International Trade Centre

Economics and dynamics of agricultural trade l iberalisat ion

Dr. David Blandford, Pennsylvania State University David Blandford is a Professor, and former department head, in the Department of Agricultural Economics & Rural Sociology at the Pennsylvania State University.

Born and educated in the United Kingdom, Dr. Blandford was formerly a division director at the Organization for Economic Cooperation & Development (OECD) in Paris and a professor at Cornell University. He has twice served as chair of the International Agricultural Trade Research Consortium – an organization composed of researchers from government, academia and industry.

Dr. Blandford teaches courses in agribusiness at Penn State and conducts research into food, agricultural and environmental policy, and international trade.

Economics and dynamics of agricultural trade liberalization

David BlandfordProfessor of Agricultural EconomicsThe Pennsylvania State University

WTO Agricultural Negotiations – Challenges and Opportunities for Pakistan

Lahore, 7-8 July 2006

The coverage of this presentation

• Current status of the Doha Round negotiations• The next steps• Likely outcomes

The draft modalities on agriculture

• Circulated by the Chair of the Committee on Agriculture on June 22 with a corrigendum on June 29

• Numerous items in square brackets (yet to be agreed) and with contradictory provisions

• This presentation will try to summarize the main elements

The main agricultural issues

• Market access – tariffs and tariff-rate quotas• Export competition – export subsidies, export

credits, state-trading exporters, food aid• Domestic support – amber, blue and green box

measures• Special and differential treatment for developing

countries – smaller reductions in tariffs and domestic support, longer implementation period, other special provisions (e.g., exemptions for least-developed countries)

Market Access

Tariff reductions

• Tariff bands – bound tariffs to be grouped under four bands

• Linear reductions – higher percentage cuts for higher bands

International Trade Centre 21

Tariff reductions – proposals for developed countries

42-90Over 60-90

35-85From 40-60 to 60-90

30-75From 20-30 to 40-60

20-65Up to 20-30

Reduction percentageSize of current tariff (ad valorem percentage)

Tariff reductions – proposals for developing countries

30-90Over 60-150

30-90From 40-100 to 60-150

20-75From 20-50 to 40-100

15-65Up to 20-50

Reduction percentageSize of current tariff (ad valorem percentage)

Tariff reductions

• Tariff bands – bound tariffs to be grouped under four bands

• Linear reductions – higher percentage cuts for higher bands

• Tariff cap – 75-100 percent for developed countries; 150 percent for developing countries

• S&D – possible lower cuts for developing countries with uniformly low tariffs

Tariff reductions and the US

US Tariff Profile Under EU and US Proposals (excludes two initial tariffs of >400%)

0

50

100

150

200

250

300

350

Perc

enta

ge ta

riff

InitialUS EU

22 International Trade Centre

Tariff reductions and the EU

EU Tariff Profile Under EU and US Proposals (excludes 1 initial tariff of >400%)

0

50

100

150

200

250

Perc

enta

ge ta

riff

InitialUSEU

Tariff reductions and the EU

Implications for Selected Product Categories

0

10

20

30

40

50

60

70

Meat (0

2)

Dairy (

03)

Cereals

(10)

Oilsee

ds (1

2)

Sugar

(17)

Cereal

Preps (

19)

Ave

rage

per

cent

age

tarif

f

Initial DutyUruguay roundEU proposal

International Trade Centre 23

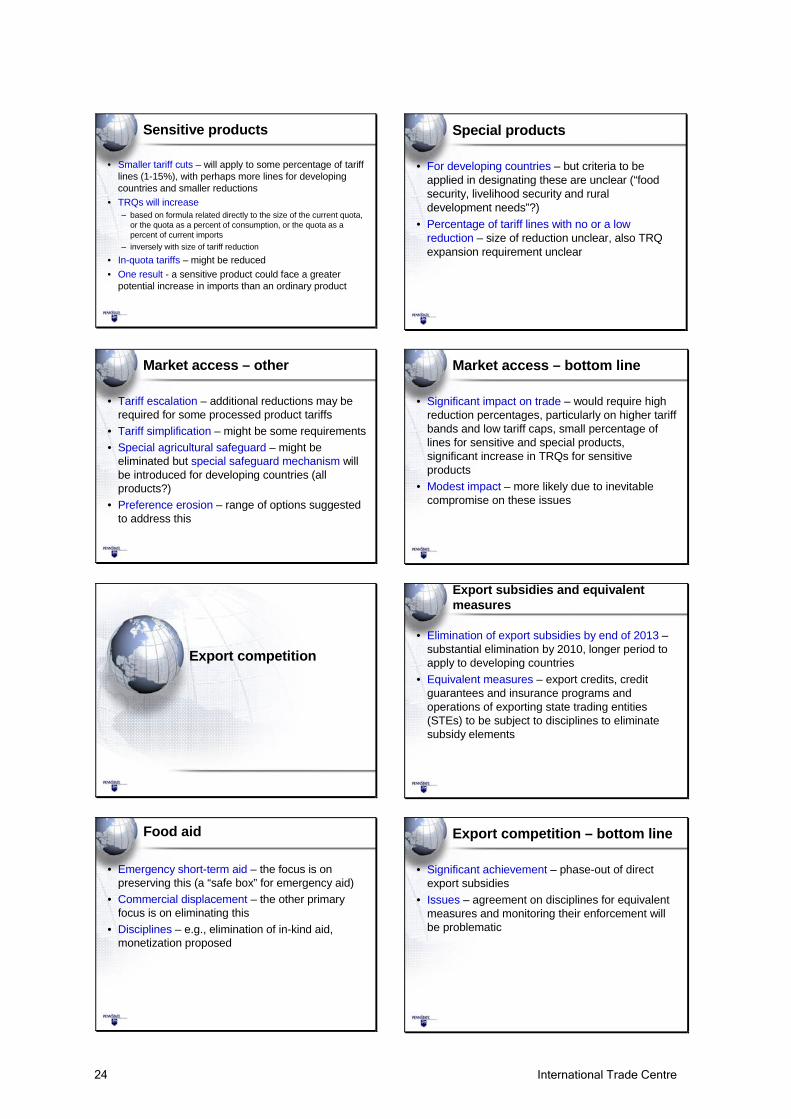

Sensitive products

• Smaller tariff cuts – will apply to some percentage of tariff lines (1-15%), with perhaps more lines for developing countries and smaller reductions

• TRQs will increase– based on formula related directly to the size of the current quota,

or the quota as a percent of consumption, or the quota as a percent of current imports

– inversely with size of tariff reduction

• In-quota tariffs – might be reduced • One result - a sensitive product could face a greater

potential increase in imports than an ordinary product

Special products

• For developing countries – but criteria to be applied in designating these are unclear (“food security, livelihood security and rural development needs”?)

• Percentage of tariff lines with no or a low reduction – size of reduction unclear, also TRQ expansion requirement unclear

Market access – other

• Tariff escalation – additional reductions may be required for some processed product tariffs

• Tariff simplification – might be some requirements • Special agricultural safeguard – might be

eliminated but special safeguard mechanism will be introduced for developing countries (all products?)

• Preference erosion – range of options suggested to address this

Market access – bottom line

• Significant impact on trade – would require high reduction percentages, particularly on higher tariff bands and low tariff caps, small percentage of lines for sensitive and special products, significant increase in TRQs for sensitive products

• Modest impact – more likely due to inevitable compromise on these issues

Export competition

Export subsidies and equivalent measures

• Elimination of export subsidies by end of 2013 –substantial elimination by 2010, longer period to apply to developing countries

• Equivalent measures – export credits, credit guarantees and insurance programs and operations of exporting state trading entities (STEs) to be subject to disciplines to eliminate subsidy elements

Food aid

• Emergency short-term aid – the focus is on preserving this (a “safe box” for emergency aid)

• Commercial displacement – the other primary focus is on eliminating this

• Disciplines – e.g., elimination of in-kind aid, monetization proposed

Export competition – bottom line

• Significant achievement – phase-out of direct export subsidies

• Issues – agreement on disciplines for equivalent measures and monitoring their enforcement will be problematic

24 International Trade Centre

Domestic support

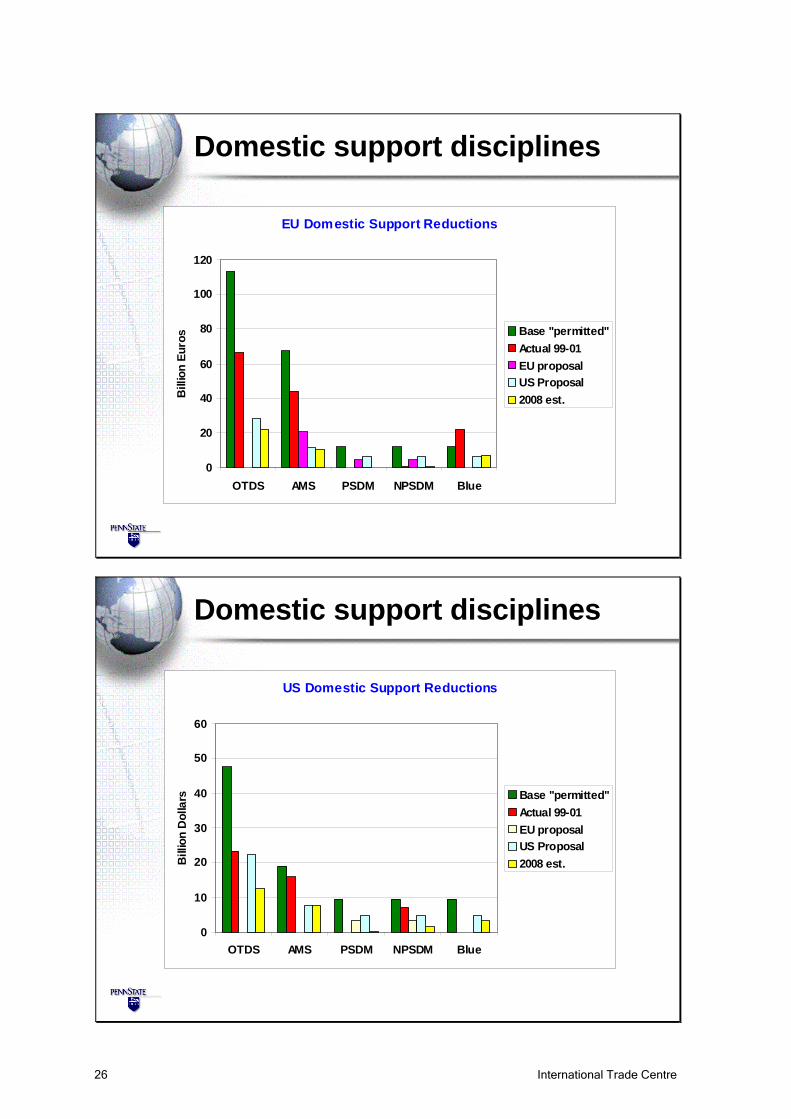

Domestic support disciplines

• Amber Box – primary focus on the most trade-distorting forms of support

• Uruguay round approach – limited the total Aggregate Measure of Support (AMS), i.e., Amber Box excluding de minimis (product and non-product specific support falling below agreed thresholds)

• Doha approach – limits on Overall Trade Distorting Support (OTDS) and its components

• OTDS – the sum of Total AMS, de minimis, and Blue Box support

• Blue Box – direct payments that are made under production limiting programs or that are based on, but do not require, production

The new disciplines

• Reduction in the OTDS – use of bands with larger reductions for higher bands

OTDS reductions – proposals for developed countries

31-70Less than $US 10 billion

53-75Between $US 10 and 60 billion

70-80Greater than $US 60 billion

Reduction percentageSize of current OTDS

The new disciplines

• Reduction in the OTDS – use of bands with larger reductions for those in higher bands

• Reduction in Total AMS – similar approach

AMS reductions – proposals for developed countries

37-60Less than $US 15 billion

60-70Between $US 15 and 25 billion

70-83Greater than $US 25 billion

Reduction percentageSize of current AMS

The new disciplines

• Reduction in the OTDS – use of bands with larger reductions for those in higher bands

• Reduction in Total AMS – similar approach• Product-specific AMS caps – to prevent support

reallocation• Reduced de minimis allowances – maybe cut from 5% to

2.5% of production values• Cap on Blue Box payments – 5% of total production value

maybe with a required reduction to 2.5% for developed countries and possibly product-specific caps

• Developing countries – lower reduction percentages and less stringent caps

International Trade Centre 25

Domestic support disciplines

EU Domestic Support Reductions

0

20

40

60

80

100

120

OTDS AMS PSDM NPSDM Blue

Bill

ion

Euro

s Base "permitted"Actual 99-01EU proposalUS Proposal2008 est.

Domestic support disciplines

US Domestic Support Reductions

0

10

20

30

40

50

60

OTDS AMS PSDM NPSDM Blue

Bill

ion

Dol

lars Base "permitted"

Actual 99-01EU proposalUS Proposal2008 est.

26 International Trade Centre

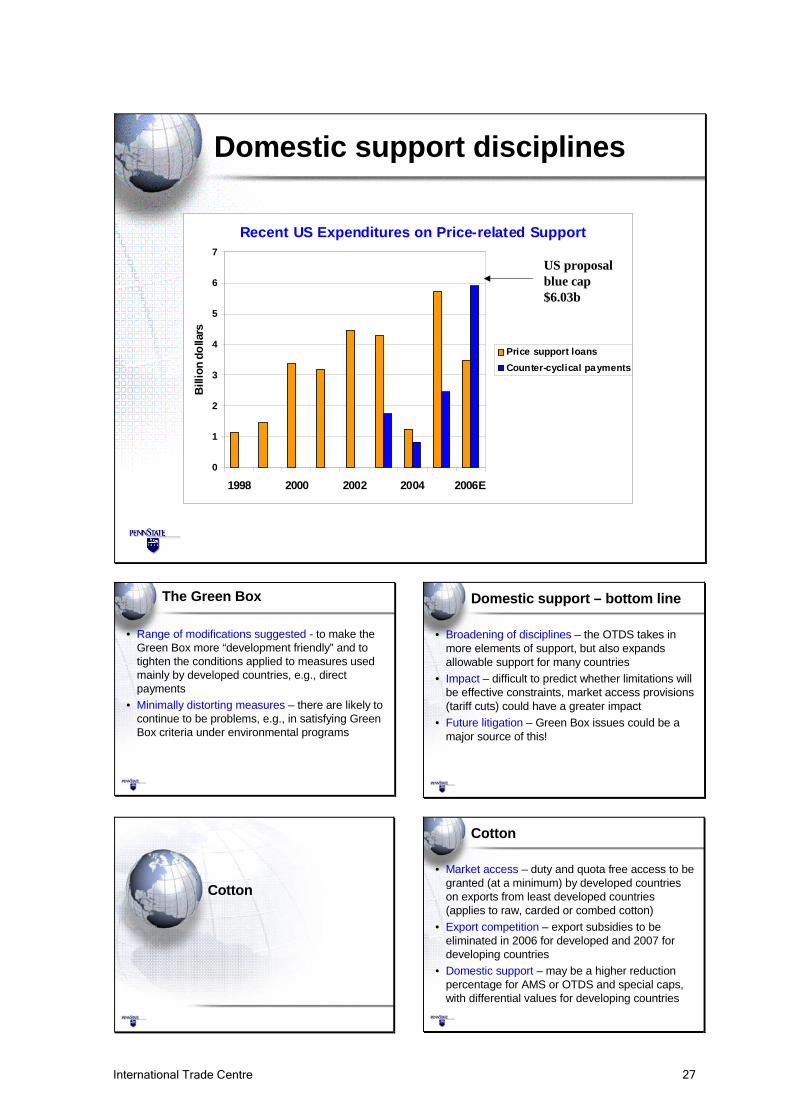

Domestic support disciplines

Recent US Expenditures on Price-related Support

0

1

2

3

4

5

6

7

1998 2000 2002 2004 2006E

Bill

ion

dolla

rs

Price support loansCounter-cyclical payments

US proposal blue cap $6.03b

The Green Box

• Range of modifications suggested - to make the Green Box more “development friendly” and to tighten the conditions applied to measures used mainly by developed countries, e.g., direct payments

• Minimally distorting measures – there are likely to continue to be problems, e.g., in satisfying Green Box criteria under environmental programs

Domestic support – bottom line

• Broadening of disciplines – the OTDS takes in more elements of support, but also expands allowable support for many countries

• Impact – difficult to predict whether limitations will be effective constraints, market access provisions (tariff cuts) could have a greater impact

• Future litigation – Green Box issues could be a major source of this!

Cotton

Cotton

• Market access – duty and quota free access to be granted (at a minimum) by developed countries on exports from least developed countries (applies to raw, carded or combed cotton)

• Export competition – export subsidies to be eliminated in 2006 for developed and 2007 for developing countries

• Domestic support – may be a higher reduction percentage for AMS or OTDS and special caps, with differential values for developing countries

International Trade Centre 27

Current state of play and prospects for the future

The current position and next steps

• WTO Director General Pascal Lamy announces on July 1 that after three days of Ministerial meetings “we are now in a crisis situation” due to lack of progress in finalizing the modalities

• Members are “committed to completing the negotiations by the end of the year”

• Lamy to act as a catalyst with G-6 (Australia, Brazil, EU, India, Japan, US) likely to play a key role as representatives of various positions

• The likely outcome?

28 International Trade Centre

Quantitative analysis of the negotiations

Dr. David Orden, International Food Policy Research Institute (IFPRI) and Virginia Polytechnic Institute and State University David Orden is Senior Research Fellow in the Markets, Trade & Institutions Division at the International Food Policy Research Institute (IFPRI), and Professor of Agricultural and Applied Economics at Virginia Polytechnic Institute and State University. He is engaged in active research and public policy education programs on the economics and political economy of domestic support policies, international trade negotiations, and technical barriers to trade.

Dr. Orden has been a Visiting Fellow at the University of New South Wales in Australia, Chairman of the International Agricultural Trade Research Consortium, and Visiting Professor at Stanford University. Dr. Orden has a Ph.D. in economics from the University of Minnesota.

INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Two Opportunities to Deliver on the Doha Development PledgeIFPRI Research Brief 6, July 2006

Presented at the workshop on WTO Agriculture Negotiations: Challenges and Opportunities for PakistanLahore, July 7-8, 2006

Study completed at IFPRI by Antoine Bouët, Simon Mevel and David Orden

Page 2INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Trade policy and developing countries

Complexity and high level of distortions affecting international agricultural tradeLower tariffs in manufacturing (but relatively high in textiles and apparel) Heterogeneity among developing countries• applied protection• access to the world market• net food importing/exporting countries

International Trade Centre 29

Page 3INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Current tariffs imposed and faced by exports

-4.0%

0.0%

4.0%

8.0%

12.0%

16.0%

-10.0% 0.0% 10.0% 20.0% 30.0%

Applied duty on imports relative to world average

App

lied

duty

on

expo

rts re

lativ

e to

wor

ld a

vera

ge

Malawi

Zimbabwe

India

Uruguay

Brazil

Argentina

Tunisia

Morocco

Tanzania

Bangladesh

China

ThailandColombia

EUUSA

Singapore

Canada

Madagascar Philippines

Chile

Mexico

Venezuela

Mozambique

ZambiaPeru

Malaysia

Australia/NZ

Page 4INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Modeling trade liberalization impacts

MIRAGE model (CEPII – Paris)• multi-sector, multi-region computable general

equilibrium• dynamic set-up with exogenous technology• MacMap-HS6 and GTAP6 data bases

Our application • country disaggregation focused on developing

countries • commodity application focused on agriculture• results reported for 2019 assuming

implementation begins in 2006

Page 5INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Pre-Hong Kong analysis

Compared results from “Ambitious” and “Unambitious” outcomes based on pre-Hong Kong proposals from the US and the EUMeasure what is at stake in the negotiation

Page 6INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Pre-Hong Kong results

Wor

ld p

rote

ctio

n

Rea

l inc

ome

gain

Wor

ld tr

ade

Full trade lib'n -5.4% $ 157 bln 12.1%Ambitious scenario -2.2% $ 103.7 bln 4.1%

(41%) (66%) (34%)Unambitious scenario -1.4% $ 41.5 bln 2.0%

(26%) (26%) (16%)

Page 7INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Pre-Hong Kong assessment

A Doha agreement within proposals on the table is potentially beneficial for developing countriesCritical issues include• tariff and subsidy binding reduction rates have to

be high• developing countries have to liberalize • likely outcomes more beneficial for middle income

countries than LDCs• for LDCs to benefit from a trade agreement specific

actions are needed to address problems arising from less preferential access, net food importing countries, and broad development needs

30 International Trade Centre

Page 8INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

June 2006 analysis

Design a central scenario based on US, EU and G20 offersMeasure the gains for developed and developing countriesIdentify specific development-oriented additional opportunities• 100% free OECD access for LDCs • 1% Special and Sensitive Products

Page 9INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Central scenario - Assumptions

Agricultural market access• Tariff reductions

G20 thresholds; EU reduction coefficientsDeveloping country coefficients 1/3 less

• Ad valorem equivalents2005 WTO formula

• Tariff caps150% for developed and 300% for developing

• Sensitive/Special Products5% of agricultural tariff lines exemptedTariff reduction 50% less, no caps TRQ expansion using European formula

Page 10INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Central scenario - Assumptions

Manufacturing market access• Swiss formula with 10% coefficient for developed, 25% for

developing

No agricultural or manufacturing liberalization for LDCsNo services liberalization

Export Subsidies• Eliminated in 2013

Domestic Support• Applied levels not reduced

Page 11INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Central scenario - Assumptions

97% duty-free access to OECD for LDCs in 2008

Market access implementation• 5 years for developed countries • 10 years for developing countries

Page 12INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Central scenario - Assumptions

Sensitive Products Selected according to political economy model

United States: Dairy, Rice, Fresh Fruits and Vegetables, Sugar, Processed Foods, Other

Japan: Meat, Dairy, Grains, Rice, Beans, Sugar, Processed Foods, Other

European Union: Meat, Dairy, Bananas, Rice, Sugar, Processed Foods, Other

Page 13INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Central scenario - Assumptions

Products exempted from LDC free accessSelected according to political economy model

95 products chosen by each non-EU country

United States: 84 Textiles and Apparel Products, Sugar

Japan: Rice, Fishery Products, Processed Food, Footwear and Apparel

European Union: No exemptions because of EBA

Page 14INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Central scenario – Tariff Cuts

Applied Tariffs 2005-2015

26.3%3.6%4.9%Industry

Percent Decrease

2015 Tariff Rate

2005 Tariff Rate

17.8%56.3%68.5%Rice

18.7%42.6%52.4%Sugar

18.7%14.8%18.2%Agriculture

Page 15INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Applied Tariffs by 2015

Low Income Countries group includes LDCs plus other developing countries in regions with a large share of LDCs

Central scenario – Tariff Cuts (Rates)

32.5%10.3%Low Income Countries

25.3%19.1%Middle Income Countries

23.5%31.0%High Income Countries

Decrease in tariffs faced on exports

Decrease in tariffs placed on imports

International Trade Centre 31

Page 16INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Real world income increases by $54.5 billion (+0.13%)

• This is 25% of the gains from full trade liberalization

• Effect on real world income is close to the unambitious scenario in the pre-Hong Kong analysis

Central scenario – Real Income

Page 17INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

1.9%39.6%58.5%Share of World Real Income Gain

$1.03$21.66$31.98Real Income Gain ($Billion)

Low Income

Countries

Middle Income

Countries

High Income

Countries1.2%18.7%80.0%Share of Initial

Real World Income

Central scenario – Real income

Page 18INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Central scenario – Trade

Exports increase (volume - %) ; HICs

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Australia/New Zealand Developed Asia European Union United States

32 International Trade Centre

Page 19INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Central scenario – Trade

Exports increase (volume - %) ; MICs

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Argentina Brazil China India

Page 20INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Central scenario – Trade

Exports increase (volume - %) ; MICs

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Malaysia Mexico Morocco Pakistan

International Trade Centre 33

Page 21INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

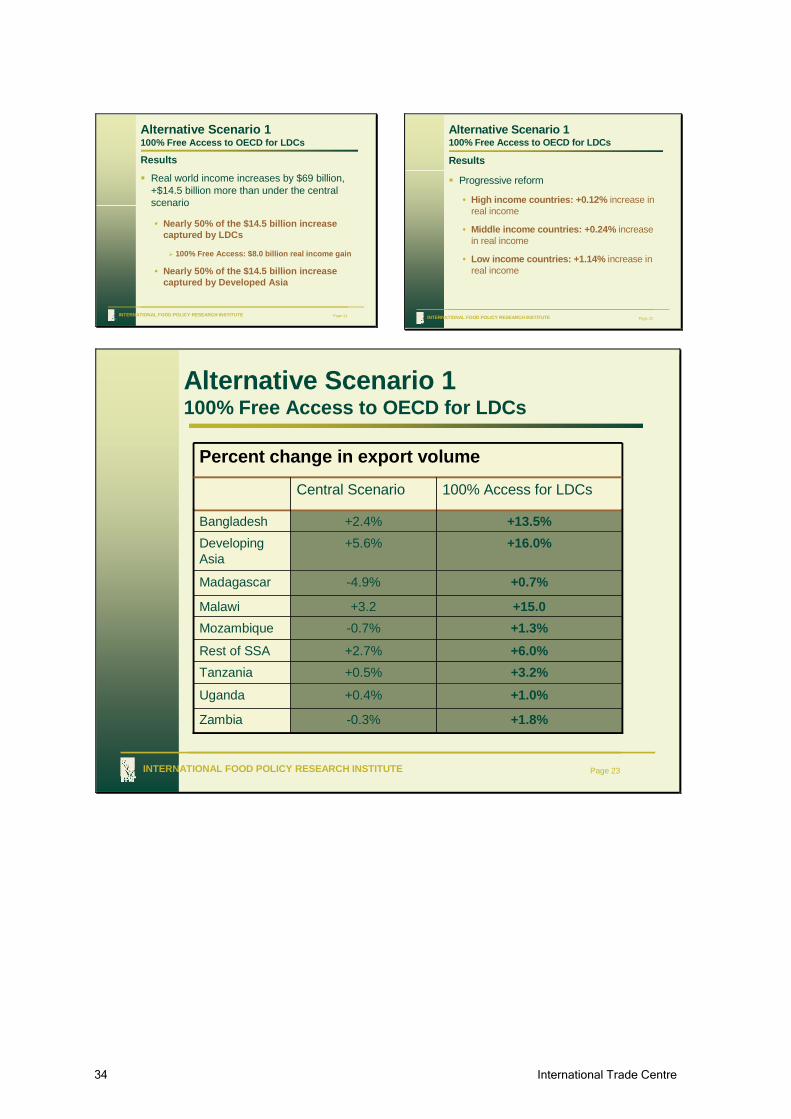

Alternative Scenario 1100% Free Access to OECD for LDCs

Results

Real world income increases by $69 billion, +$14.5 billion more than under the central scenario

• Nearly 50% of the $14.5 billion increase captured by LDCs

100% Free Access: $8.0 billion real income gain

• Nearly 50% of the $14.5 billion increase captured by Developed Asia

Page 22INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Results

Progressive reform

• High income countries: +0.12% increase in real income

• Middle income countries: +0.24% increase in real income

• Low income countries: +1.14% increase in real income

Alternative Scenario 1100% Free Access to OECD for LDCs

Page 23INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

+1.8%-0.3%Zambia

+1.0%+0.4%Uganda

+3.2%+0.5%Tanzania+6.0%+2.7%Rest of SSA

+1.3%-0.7%Mozambique+15.0+3.2Malawi

Percent change in export volume

+0.7%-4.9%Madagascar

+16.0%+5.6%Developing Asia

+13.5%+2.4%Bangladesh

100% Access for LDCsCentral Scenario

Alternative Scenario 1100% Free Access to OECD for LDCs

34 International Trade Centre

Page 24INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Alternative Scenario 1100% Free Access to OECD for LDCs

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Bangladesh Developing Asia Madagascar Malawi

Scenario Central

Page 25INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Alternative Scenario 1100% Free Access to OECD for LDCs

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Bangladesh Developing Asia Madagascar Malawi

Scenario Central SC + Full free access

International Trade Centre 35

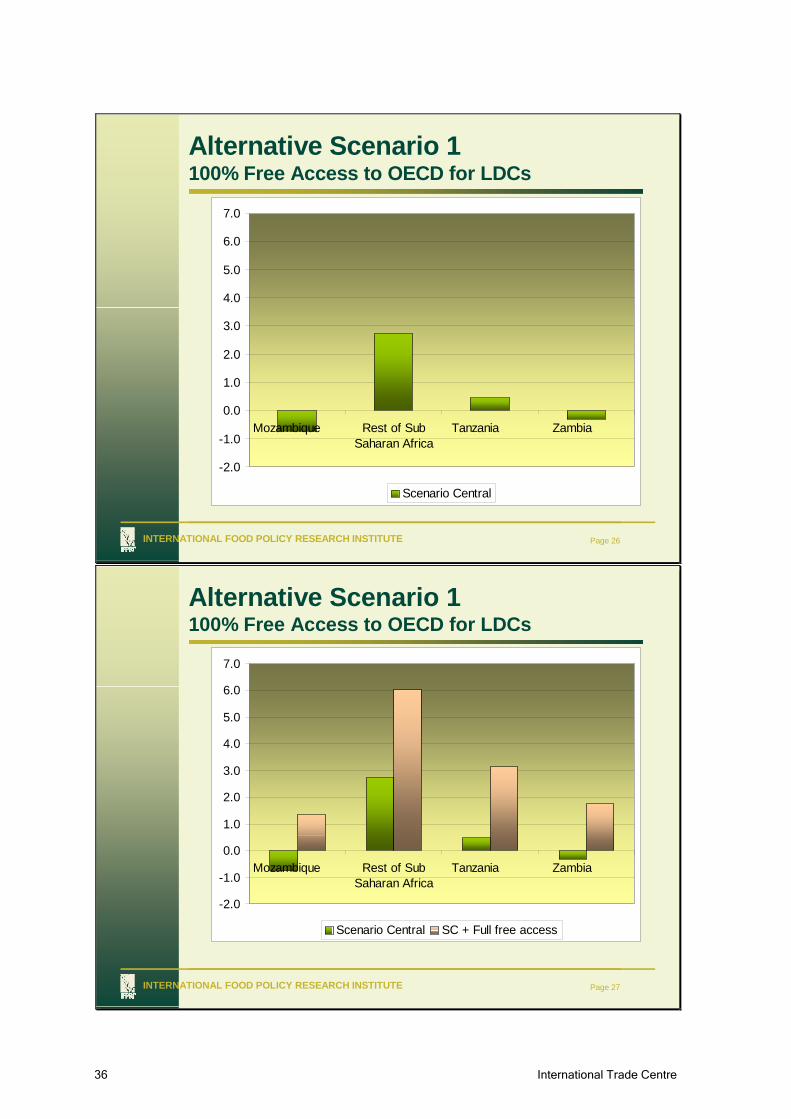

Page 26INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Alternative Scenario 1100% Free Access to OECD for LDCs

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Mozambique Rest of SubSaharan Africa

Tanzania Zambia

Scenario Central

Page 27INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Alternative Scenario 1100% Free Access to OECD for LDCs

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Mozambique Rest of SubSaharan Africa

Tanzania Zambia

Scenario Central SC + Full free access

36 International Trade Centre

Page 28INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

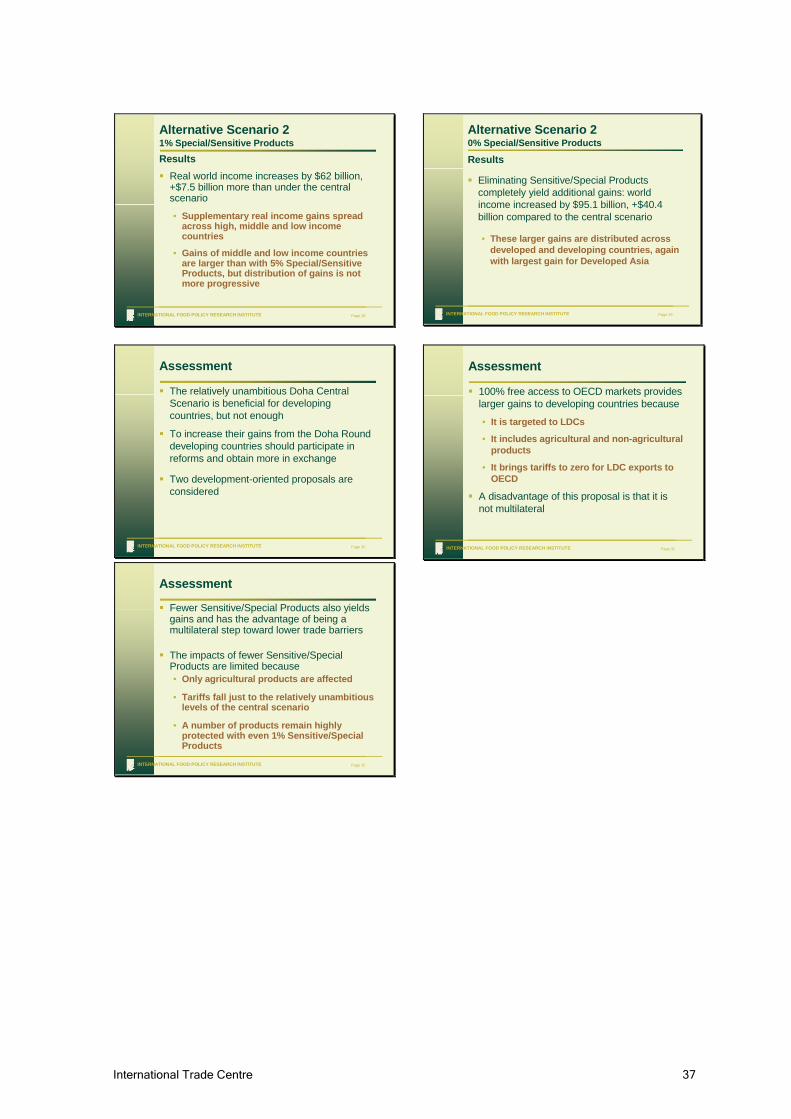

Alternative Scenario 21% Special/Sensitive ProductsResults

Real world income increases by $62 billion, +$7.5 billion more than under the central scenario

• Supplementary real income gains spread across high, middle and low income countries

• Gains of middle and low income countries are larger than with 5% Special/Sensitive Products, but distribution of gains is not more progressive

Page 29INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Alternative Scenario 20% Special/Sensitive Products

Results

Eliminating Sensitive/Special Products completely yield additional gains: world income increased by $95.1 billion, +$40.4 billion compared to the central scenario

• These larger gains are distributed across developed and developing countries, again with largest gain for Developed Asia

Page 30INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Assessment

The relatively unambitious Doha Central Scenario is beneficial for developing countries, but not enough

To increase their gains from the Doha Round developing countries should participate in reforms and obtain more in exchange

Two development-oriented proposals are considered

Page 31INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Assessment

100% free access to OECD markets provides larger gains to developing countries because

• It is targeted to LDCs

• It includes agricultural and non-agricultural products

• It brings tariffs to zero for LDC exports to OECD

A disadvantage of this proposal is that it is not multilateral

Page 32INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Assessment

Fewer Sensitive/Special Products also yields gains and has the advantage of being a multilateral step toward lower trade barriers

The impacts of fewer Sensitive/Special Products are limited because• Only agricultural products are affected

• Tariffs fall just to the relatively unambitiouslevels of the central scenario

• A number of products remain highly protected with even 1% Sensitive/Special Products

International Trade Centre 37

Page 33INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Domestic Support – U.S. Case(billion dollars)

239.612.06.0

241.212.16.0

Value of U.S. Agricultural ProductionFive (5) Percent of ValueTwo and one-half (2.5) Percent of Value

2.51.50.4 4.4

1.01.50.42.9

Amber Box AMS (Non-Product Specific)Countercyclical PaymentsCrop Insurance SubsidiesOther subsidiesSubtotal

7.65.1

12.7

1.25.16.3

Amber Box AMS (Product Specific)Commodity Support Payments Price Support Programs (dairy, sugar)

Subtotal

5.35.3Green Box

Income Support Direct Payments

20052004

YearCategory

Page 35INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

Simulated effects of increased prices on poverty among cotton farmers in Pakistan

0.200.200.170.180.210.2140%

0.230.240.210.220.240.2430%

0.280.280.320.27

0.400.500.36

0.320.2720%

0.330.330.390.390.310.3110%

With Cotton Price Increase of:

Base

Percent of Households (As Proportion)Incidence of poverty

5,9275,8398,4308,3054,9304,857Income Gain from a 10% Cotton Price Increase

75,84875,01375,942Base HH Expenditures (PRs)

Supply Response

Fixed Supply

Supply Response

Fixed Supply

Supply Response

Fixed Supply

PakistanSindhPunjab

38 International Trade Centre

References:

Antoine Bouet, Simon Mervel, David Orden. Two Opportunities to Deliver on the Doha Development Pledge. IFPRI Research Brief No. 6, July 2006.

David Orden, Abdul Salam, Reno Dewina, Hina Nazli and Nicholas Minot. Impact of Global Cotton Markets on Rural Poverty in Pakistan. ADB Pakistan Poverty Assessment Update, Background Paper 8, February 2006.

International Trade Centre 39

Analysis of the negotiations: Market access proposals

Dr. H. Bruce Huff, Huff & Associates, Ottawa Since 1998, Bruce Huff has operated an economic consulting company, based in Ottawa, Canada. Formerly, he was a senior manager and policy advisor with Agriculture & Agri-Food Canada. He has also served as head of Trade Policy in the Agriculture Division of the OECD in Paris. He has been a faculty member in the Agricultural Economics Department at the University of Guelph, and a visiting scholar at the International Institute for Applied Systems Analysis in Vienna, Austria.

Dr. Huff has served as an advisor on trade negotiations for the governments of Mexico, Brunei, Syria, Pakistan and Canada. He has conducted agricultural policy studies for several international organizations, including the OECD, The World Bank, the Commonwealth Secretariat, UN Food and Agriculture Organization (FAO), and the International Trade Centre. For the past year, Dr. Huff has served as a Trade Policy Advisor to the Ministry of Food, Agriculture and Livestock in Pakistan.

Dr. Huff holds a Ph.D. degree in agriculture economics from Michigan State University. He was named a Fellow of the Canadian Agriculture Economics Society in 2002.

Market Access Proposals

H. Bruce HuffHuff and AssociatesOttawa

Status of Negotiations: Basic Information

Framework Document July 2004 most comprehensive statement of agreementHong Kong Ministerial: additional agreementsChair’s modalities June 22Assessment– Own analysis– Published/unpublished reports

Importance of Market Access

Studies show that it is most important pillarAffects most of the 149 WTO countriesAffects both supply and demand forcesTariffs high in agriculture (many mega tariffs)Tariff Rate Quotas affect production and trade

Most Complex Pillar

Tariff Rate Quotas involve 3 componentsMany exemptions permitted for

– Sensitive and Special Products– Least developed countries– Special Safeguard

Higher rates of reductions sought for – Tariff escalation– Tropical Products– PreferencesLink between expansion of TRQ volume and Sensitive

Products

40 International Trade Centre

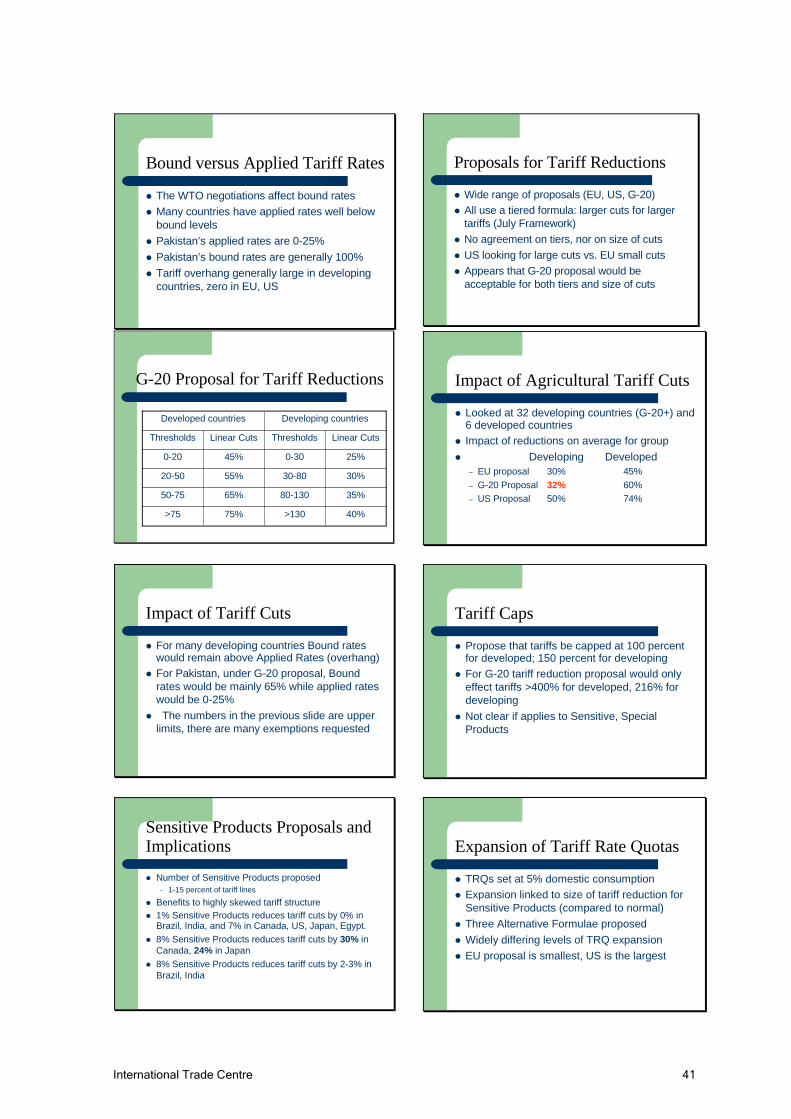

Bound versus Applied Tariff Rates

The WTO negotiations affect bound ratesMany countries have applied rates well below bound levelsPakistan’s applied rates are 0-25%Pakistan’s bound rates are generally 100% Tariff overhang generally large in developing countries, zero in EU, US

Proposals for Tariff Reductions

Wide range of proposals (EU, US, G-20)All use a tiered formula: larger cuts for larger tariffs (July Framework)No agreement on tiers, nor on size of cutsUS looking for large cuts vs. EU small cutsAppears that G-20 proposal would be acceptable for both tiers and size of cuts

G-20 Proposal for Tariff Reductions

40%>13075%>75

35%80-13065%50-75

30%30-8055%20-50

25%0-3045%0-20

Linear CutsThresholdsLinear CutsThresholds

Developing countriesDeveloped countries

Impact of Agricultural Tariff Cuts

Looked at 32 developing countries (G-20+) and 6 developed countries Impact of reductions on average for group

Developing Developed – EU proposal 30% 45%– G-20 Proposal 60%– US Proposal 50% 74%

32%

Impact of Tariff Cuts

For many developing countries Bound rates would remain above Applied Rates (overhang)For Pakistan, under G-20 proposal, Bound rates would be mainly 65% while applied rates would be 0-25%The numbers in the previous slide are upper

limits, there are many exemptions requested

Tariff Caps

Propose that tariffs be capped at 100 percent for developed; 150 percent for developingFor G-20 tariff reduction proposal would only effect tariffs >400% for developed, 216% for developingNot clear if applies to Sensitive, Special Products

Sensitive Products Proposals and Implications

Number of Sensitive Products proposed– 1-15 percent of tariff lines

Benefits to highly skewed tariff structure 1% Sensitive Products reduces tariff cuts by 0% in Brazil, India, and 7% in Canada, US, Japan, Egypt.8% Sensitive Products reduces tariff cuts by 30% in Canada, 24% in Japan8% Sensitive Products reduces tariff cuts by 2-3% in Brazil, India

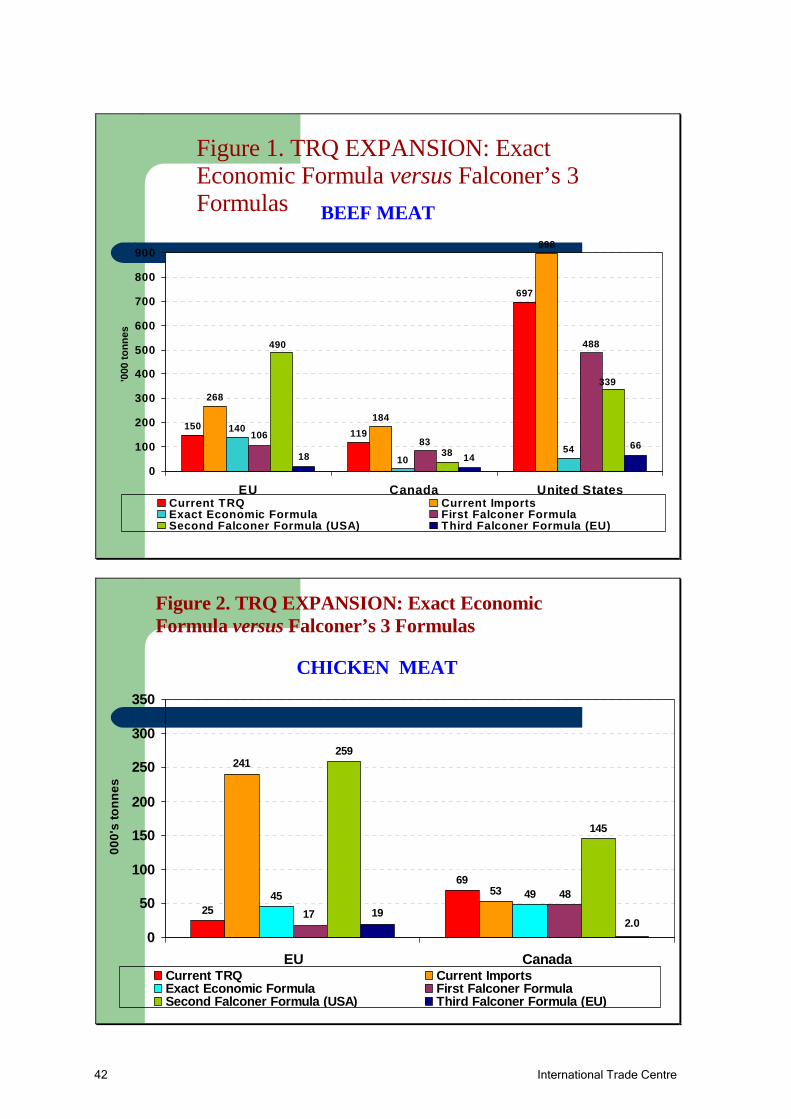

Expansion of Tariff Rate Quotas

TRQs set at 5% domestic consumptionExpansion linked to size of tariff reduction for Sensitive Products (compared to normal)Three Alternative Formulae proposedWidely differing levels of TRQ expansionEU proposal is smallest, US is the largest

International Trade Centre 41

Figure 1. TRQ EXPANSION: Exact Economic Formula versus Falconer’s 3 Formulas BEEF MEAT

150119

697

268

184

898

140

1054

83

488

106

339

38

490

661418

0

100

200

300

400

500

600

700

800

900

EU Canada United States

'000

tonn

es

Current TRQ Current ImportsExact Economic Formula First Falconer FormulaSecond Falconer Formula (USA) Third Falconer Formula (EU)

25

69

241

5345 49

259

145

48

172.0

19

0

50

100

150

200

250

300

350

EU Canada

000'

s to

nnes

Current TRQ Current ImportsExact Economic Formula First Falconer FormulaSecond Falconer Formula (USA) Third Falconer Formula (EU)

Figure 2. TRQ EXPANSION: Exact Economic Formula versus Falconer’s 3 Formulas

CHICKEN MEAT

42 International Trade Centre

1117

2009

1111

685

539

1183

743

1600

782

1120

76136

0

300

600

900

1200

1500

1800

2100

EU United States

'000

tonn

es

Current TRQ Current ImportsExact Economic Formula First Falconer FormulaSecond Falconer Formula (USA) Third Falconer Formula (EU)

Figure 4. TRQ EXPANSION: Exact Economic Formula versus Falconer’s 3 Formulas

SUGAR

84

682755

648

12

532 477

59

1753

7219

63

0

200

400

600

800

1000

1200

1400

1600

1800

2000

EU JapanCurrent TRQ Current ImportsExact Economic Formula First Falconer FormulaSecond Falconer Formula (USA) Third Falconer Formula (EU)

Figure 5. TRQ EXPANSION: Exact Economic Formula versus Falconer’s 3 Formulas

RICE

International Trade Centre 43

2982

13736

11312087

4800

1025

0

2000

4000

6000

8000

10000

12000

14000

EU

'000

tonn

es

Current TRQ Current ImportsExact Economic Formula First Falconer FormulaSecond Falconer Formula (USA) Third Falconer Formula (EU)

Figure 6. TRQ EXPANSION: Exact Economic Formula versus Falconer’s 3 Formulas

Wheat

Special Products

Developing countries permitted to identify up to 20% of tariff linesSelection based on food security, livelihood security, and rural development (very general)Tariff reductions required

– First 50% is zero– Next 25% is 5%,– Next 25% is 10%

Would result in limited new market access in any developing country.

Special Safeguard Mechanism (SSM)

Protect against import surges and low international pricesEncourage countries to make larger tariff reductions Aimed at products where tariffs are cut Trigger mechanism uses three year moving average of both prices and import volumes.Volumes exceeding 30%; prices falling by 30% of average could trigger SSMAdditional duties would remain for 12 months Duties could revert to previous bound level or increase 60%

Tariff Escalation

Processed products tariffs higher than unprocessed Results in high protection for food processingElimination provides more jobs in rural areasFood processing brings more investment and new technologyOptions for elimination

– Food chain– Higher tariff cuts for processed foods

Tropical Products

Seek greater liberalization of tropical products86 tariff lines (HS-4) identified (e.g., citrus, fruits, vegetables)Many of Pakistan’s non-tradition exportsProvides additional growth opportunities

44 International Trade Centre

Preference Erosion

Many developing countries have tariff preferences (mainly sugar, bananas)Lower general tariff reduces value of preferencePreference holders seek greater tariff cut or compensation Pakistan does not have any preferences

Cotton

Tariffs on cotton are generally smallDeveloped (and developing) would provide duty-free and quota free access to all Least Developed Countries (Hong Kong)Pakistan would benefit if extended to all developing countries

Negotiating Priorities for Pakistan

Seek large tariff cuts (applied tariffs will remain below bound rates)Limit exemptions: Sensitive (mega tariffs)Limit exemptions in other developing countries as future growth in these marketsTariff caps on Sensitive/SpecialLarge expansion in TRQs (end date)Improve administration of TRQs

Overall Assessment

G-20 proposal on tariff reductions provides significant reductions to bound tariffsOverhang would remain in many countriesExemptions widespread

– Sensitive Products likely 8% tariff lines– Special Products exempt from much reduction– SSM protects against big adjustments

Overall impact would be modest, improvements mainly limited to small number of developed countries No incentive for South-South trade

International Trade Centre 45

Implicat ions for Pakistan

Mr. Shezada Taimur Khusrow, Deputy Secretary (Planning), Federal Ministry of Food, Agriculture & Livestock

Regional Trading Regional Trading AgreementsAgreements

&&Implications for PakistanImplications for Pakistan

Shahzada Taimur KhusrowShahzada Taimur KhusrowDeputy SecretaryDeputy Secretary

MINFALMINFAL

2

Surge in RTAsSurge in RTAsNearly 293 in operation and notified with the WTONearly 293 in operation and notified with the WTOGATT Article 24 allows regional trading or Customs Union GATT Article 24 allows regional trading or Customs Union with the condition that it should not make trade more with the condition that it should not make trade more restrictive to non membersrestrictive to non membersRegional trading arrangements support multilateral trading Regional trading arrangements support multilateral trading as both promote freer trading and removal of trade as both promote freer trading and removal of trade barriersbarriersGATS Article 5 allows developing countries to enter into GATS Article 5 allows developing countries to enter into regional or global arrangement for reduction or elimination regional or global arrangement for reduction or elimination of tariffs and non tariff barriersof tariffs and non tariff barriersWTO Regional Trade Agreements Committee examines WTO Regional Trade Agreements Committee examines regional groups to assess whether they are consistent regional groups to assess whether they are consistent with WTO ruleswith WTO rules

3

PTAs and AgriculturePTAs and AgricultureNegotiations mostly on market access, i.e tariff reduction, Negotiations mostly on market access, i.e tariff reduction, not on domestic support or export subsidies as in not on domestic support or export subsidies as in multilateral negotiationsmultilateral negotiations

Market access negotiationsMarket access negotiationsExclude some sectors Exclude some sectors Extended time for adjustmentExtended time for adjustment

Agriculture issue: affects choice of better trading partnerAgriculture issue: affects choice of better trading partner

Market access negotiations start with applied tariffs in Market access negotiations start with applied tariffs in PTAsPTAsMost FTAs or PTAs do not go substantially beyond WTO Most FTAs or PTAs do not go substantially beyond WTO provisions in safeguard and nonprovisions in safeguard and non--tariff measurestariff measures

4

PTAs and Multilateral TradePTAs and Multilateral Trade

PositivePositive::Removal of sensitive sectors: allows some negotiations Removal of sensitive sectors: allows some negotiations to move forward, avoids stalling of agreement, puts to move forward, avoids stalling of agreement, puts focus on sectors where there is mutual benefitfocus on sectors where there is mutual benefitExtended adjustment: prepares political economy about Extended adjustment: prepares political economy about workability of a liberalized environment; eventual workability of a liberalized environment; eventual incorporation laterincorporation later

NegativeNegative::Distraction from multilateral effort; thin negotiating Distraction from multilateral effort; thin negotiating resourcesresourcesDifferent sensitive agricultural sectors means difficulty in Different sensitive agricultural sectors means difficulty in future harmonization of PTAsfuture harmonization of PTAs

5

Effect of FTAs on TradeEffect of FTAs on Trade

Past studies show that FTA is a building block, not a Past studies show that FTA is a building block, not a stumbling blockstumbling block

Both intraBoth intra-- and inter trade grew over a period of timeand inter trade grew over a period of time

Increase in most FTAs shows that intraIncrease in most FTAs shows that intra--trade came trade came mostly from industry, not from agriculturemostly from industry, not from agriculture

Agriculture is widely protected because of politicalAgriculture is widely protected because of political--economy sensitivityeconomy sensitivity

7

FTA ExperiencesFTA Experiences

FTA and PTAs helped accelerate the bringing down FTA and PTAs helped accelerate the bringing down of tariff barriers. In most cases tariffs are within 0of tariff barriers. In most cases tariffs are within 0--5%5%

RTR showed agriculture tariff barriers remain RTR showed agriculture tariff barriers remain relatively high visrelatively high vis--àà--vis developed countriesvis developed countries

46 International Trade Centre

8

FTA ExperiencesFTA Experiences

Countries with low tariff barrier in agriculture have Countries with low tariff barrier in agriculture have many nonmany non--tariff measures on agriculture productstariff measures on agriculture products

FTAs allow liberalization of agriculture, with extended FTAs allow liberalization of agriculture, with extended timetable and several exclusions, and a high number timetable and several exclusions, and a high number of sensitive productsof sensitive products

FTAs proved to be a building block for total trade, FTAs proved to be a building block for total trade, even for agricultural tradeeven for agricultural trade

10

MINFAL InitiativesMINFAL Initiatives

Since 2005 MINFAL has been actively participating in Since 2005 MINFAL has been actively participating in FTA negotiationsFTA negotiations

To take offensive and defensive positions on To take offensive and defensive positions on Pakistan’s 1138 agriculture item of HS Chapter 1Pakistan’s 1138 agriculture item of HS Chapter 1--2424

Positions are adopted on the basis of:Positions are adopted on the basis of:Agriculture productivityAgriculture productivityDomestic demand and supplyDomestic demand and supplyFuture growth potentialFuture growth potentialExport potentialExport potentialComparative and competitive advantageComparative and competitive advantage

11

Pakistan Position OffensivePakistan Position OffensivePositions adopted on basis of reciprocity and Positions adopted on basis of reciprocity and Pakistan wants market access for its agricultural Pakistan wants market access for its agricultural products at the same timeproducts at the same timePakistan fully compliant with its commitments under Pakistan fully compliant with its commitments under AoA AoA