World Bank Documentdocuments.worldbank.org/curated/en/756371468318534862/pdf/multi-page.pdfSEKA...

43

FILE Copy DOCUMENT OF INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATIONAL DEVELOPMENT ASSOCIATION Not For Public Use Report No- 240a-TU APPRAISAL OF -A1ANTALYA FOREST UTILIZATION PROJECT 'TURKEY (in two volumes) - VOLUME I ' THE MAIN REPORT -/December 17, 1973 Industrial Projects Department This report was prepared for official use only by the Bank Group. It may not be published, quoted | or cited without Bank Group authorization. The Bank Group does not accept responsibility for the accuracyor completeness of the report. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of World Bank Documentdocuments.worldbank.org/curated/en/756371468318534862/pdf/multi-page.pdfSEKA...

FILE Copy

DOCUMENT OF INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENTINTERNATIONAL DEVELOPMENT ASSOCIATION

Not For Public Use

Report No- 240a-TU

APPRAISAL OF

-A1ANTALYA FOREST UTILIZATION PROJECT

'TURKEY

(in two volumes)

- VOLUME I

' THE MAIN REPORT

-/December 17, 1973

Industrial Projects Department

This report was prepared for official use only by the Bank Group. It may not be published, quoted |or cited without Bank Group authorization. The Bank Group does not accept responsibility for theaccuracy or completeness of the report.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS WEIGHTS AND MEASURES

TL 1.0 = US$ 0.714 All weights and measures are in metric unitsTL 14.0 = US$ 1.00 1 Metric Ton (t) = 1,000 Kilograms (kg)1 EIB Unit of Account = US$ 1.20 1 Metric Ton (t) = 2,206 Pounds

1 Kilometer (km) = 0.62 Miles1 Hectare (ha) = 2.47 AcresVolumes of logs and sawnwood refer toSolid Wood Measure

PRINCIPAL ABREVIATIONS AND ACRONYMS USED

EIB European Investment BankGDF General Directorate of ForestryMF Ministry of ForestrySEKA Seluloz ve Kagit Sanayii - The State Pulp and Paper IndustrySIB State Investment BankSPO State Planning Organization

Fiscal Year

January 1 - December 31

TURKEY

APPRAISAL OF ANTALYA FOREST UTILI7ATION PROJFCT

TABLTE OF CONTENTS

VOLT E I

THE MAIN REPORT

SUNMARY AND CONCLUSIONS ... ........ q...... i - iii

I. INTRODUCTION .... ............... . . ......

II. FORESTRY IN TURKEY AND THE STATE PILP AND PAPER COMPANY 2

A. Background . ... . ....... ........... ,, 2B. The Ministry of Forestry . ...... 3C. The State Pulp and Paper Company. 4

1. Plant Facilities and Operations . 42. Management and Labor ..... .......... 53. Financial Analysis - Past and Future 6

III. THE PROJECT ....... ........... ..... 7

A. The Forestry Part ....... ....... ........... .. 7B. The Industrial Part , .... . ..... .......... .... . 8

C. The Feasibility Studies Part ..................... 10D. Ecology .............. 1n

IV. THE MARKET .......................... , ... ........... 1?

A. Sawnwood . ........ . ... . . . . 1 2B. All Paners ............. 12C. Linerboard ............. a .,........... . 14D). Sackkraft ................ ...... .. ... , 14

V. CAPITAL COSTS AND FINANCIAL PLAN ...... ................ 15

A. Forestrr Part ...........................,.,, 151. Investment Costs .................... , , 152. Financial Plan ............... . . .,.. .... 16

B, Industrial Part ............... 171. Investment Costs ............................ 172. Financial Plan ......... ..................... 1q

C. Stmymary of Project Costs and Financing Sources ,.. 20D. Allocation of Bank Loan and Dishursements ,, ... . 21E. Procurement . .... ............... 22

TABLE OF CONTENTS CONTINUED

Page No.

VI. PROJECT IMPLEMENTATION . ................ 24

A. Forestry Part ..................... .. .,...., 24B. Industrial Part ................. ,,,,... 245C. Studies Part .. ........ ..... .- ... ..... ,. 25D. Role of State Investment Bank . ........... 25

VII. FINANCIAL ANALYSIS ......... ............ ..... 26

A. Forestry Part ............. ... 26B. Industrial Part ................ .. *.*. ....... .. 27

1. Revenues and Operating Costs ........... : 272. Financial Projections ..................... 283. Financial Return and Risks ... 30

VIII. ECONOMIC ANALYSIS ............. # ..... 31

IX. RECOMT1ENDATIONS . . ....... **...... , , , 32

Map 1: Forest Map of Turkey (IBRD 10502)

VOLUME II

ANNEX 1 Glossary of TermsANNEX 2 Place of Antalya Project in the Development of

Turkev's ForestsANNEX 3 Institutional BackgroundANNEX 4 The Forestrv Project,ANNEX 5 The Industrial ProjectAINEX 6 Future Feasibility StudiesANNEX 7 TransportationANNEX 8 Plant Site and Environmental ImpactANNEX 9 Markets and MarketingANN'EX 10 Capital Costs and Financial Plan - Forestry PartANNEX 11 Capital. Costs and Financial Plan - Industrial PartANNEX 12 State Investment Bank, TuirkeyANNEX 13 Financial Analysis - Forestrv PartANNEX 14 Financial Analysis - Industrial PartANNEX 15 Economic Analysis

-ANNEX 16 Socio-Economic Structure of Antalva Region

Map 1: Forest Map of Turkey (IBRD 10502)Map 2: Site Layout, (IBRD 10789)

APPRAISAL OF ANTALYA FOREST ITILIZATION PROJECT

SUMMARY AND CONCLUSIONS

i. This report appraises a proposed project for the utilization of thenatural pine forests of the Antalya region of Turkey. Tne integrated projectis composed of: a forestry program, a large pulp and paper plant and sawmilland a study part. The aggregate cost of the project (including its threeparts) is US$170.1 million, including about US$68.0 million in foreign exchange,of which the Bank has been asked to provide US$40.0 million. The balance ofthe foreign exchange is to be provided by a European Investment Bank (EIB)Loan of about US$24.4 million plus USl.l million from EIB country funds allo-cated for studies and by US$2.5 million out of Government equity contributions.The local currency financing is to be provided as equity funds by the Govern-ment and by a loan by Turkey's State Investment Bank (SIB), which also willbe the channel for the Bank's and EIB's financing for the industrial part ofthe project.

ii. The forestry part of the project involves increasing log productionin the Antalya forestry region, which has 472,000 ha of good forest land, fromits prese5t level of about 300,000 m /year (solid measure) to a level of about800,000 m /year, almost entirely of pine. The industrial part of the projectinvolves: (a) a s wmill to process about 340,000 m /year of logs to produceannually 182,000 m /year of sawnwood with the sawmill residues and other logsgoing to the pulp mill; (b) a pulp mill with an annual capacity of about 147,000bone-dry tons of unbleached kraft pulp; (c) a papermill with an annual capacityof either 155,000 tons of kraft linerboard or a lesser quantity of a mix oflinerboard and sackkraft. The studies part of the project involves feasibilitystudies of future integrated forest utilization projects. One has been de-fined in the Adana/Mersin/Maras region east of Antalya and others are current-ly being defined.

iii. The Bank and the EIB loans would be extended to the Government atthe usual lending rate of each institution. The Bank and EIR loans for theindustrial part of the project totalling US$56.1 million would be onlent onthe same terms, with a life of 16 years, including a five years grace period,at 9% p.a. interest. These funds would be passed through SIB and throughSeluloz ve Kagit Sanayii (SEKA), the State Economic Enterprise for pulp andpaper, to the industrial project entity (The Antalya Establishment) which isa separate legal and financial entity. The joint financing totalling US$7.9million for the forestry part would not be onlent by the Government but thispart would be implemented by the Ministry of Forestry (Mr) and the funds willbe passed on to this organization for the purposes of the project. Arrange-ments for passing on the funds for the studies and their implementation arebeing finalized.

iv. The project is the result of many years of planning and promotionaleffort by the Government and international agencies. The principal aim is toexploit more efficiently a major forest area of Turkey, a country whose forests

- ii -

are the fourth most extensive in Europe. The project contributes to improvingforest management and practices and to meeting the strong local demand forpaner and wood products while at the same time not interfering with theecological balance. The preparation of the project required extensiveexpenditures of time and money to find the best way to achieve these objectives.It is of major significance for the future economic development of Turkeythat the two primary entities involved, MY and SEKA, which have faced severegrowing problems, will be beneficiaries of the expertise and direction growingour of the project.

v. The forestry part of the project will be executed by the MF andits General Directorate of Forestry (GDF) through the existing Antalyaregional administration. The industrial part will be executed by SEKA throughits Antalya Establishment, created especially for the project. In order toachieve integration of the project, the forestry and industrial parts willbe coordinated by arrangements formalized in a wood supply contract. The coor-dination and implementation of the studies continues under discussion, butthe studies will be carried out by qualified consultants. The forestry partwill utilize well-proven methods of forest management which are new to Turkeyto increase forest yields and improve harvesting methods now generally in usein Turkey that are considered appropriate under present social conditions.The industrial part will utilize well-proven processes and methods. Theproject will require extensive use of consultants, the scope of whose activi-ties has been quite clearly defined. It is expected that the major portionof the industrial part will require four years to execute, with commercialproduction of the pulp and paper mill commencing in January, 1978; the sawmillwould commence operations two years earlier. The major forestry investmentswill also be made during this period.

vi. Based upon detailed marketing studies, no problems in sellingAntalya's products are foreseen. The sawn goods will be used primarily inconstruction, and the linerboard and sackkraft in packaging. Antalya'sproduct flexibility, coupled with the flexibility in product mix at the otherSEKA plants, will allow latitude to cope with unexpected shifts in marketdemand. Imports of linerboard or sackkraft are expected to prove virtuallyunavailable or at least very expensive. Even after Antalya begins operationa shortage of construction sawnwood is anticipated, and the supply of liner-board and sackkraft is geared only to median forecast demand until 1981, afterwhich there may again be a shortage.

vii. Given the tourist potential of the Antalya coast, the choice of plantsite was made only after a careful review of a number of alternative possibili-ties by an inter-ministerial committee chaired by the State Planning Organiza-tion (SPO). The site chosen minimizes possible adverse effect on regionaltouristic and agricultural development with only a modest increase in costover the lowest-cost site considered. The pulp and paper mill will be equippedwith all the proven facilities to reduce odors and particulates to a minimumlevel, and with liquid effluent treatment facilities appropriate to a sea-coast location.

- iii -

viii. Upon project completion, the Antalya Establishment is expected tohave a satisfactorv financial structure, the debt/equity ratio will be 60:40and the debt service coverage will be about 1.6 after the first two years ofoperation. The financial return for the industrial part of the project is15.0% before and 13.5% after taxes on income. International paper and lumberprices have significantly increased during the last year. It is expected thatupward pressure on prices will continue, reflecting in part rising investmentcosts and also operating costs in major supplying countries. Neverthelessconservative import prices of US$236 per ton of sackkraft and US$191 per tonof linerboard cif Turkey have been assumed to determine the economic rate ofreturn of the project. On this basis, the economic rate of return of theproject is about 14%, which is satisfactory. The return is sensitive tochanges in revenues and to a lesser degree to changes in investment and opera-ting costs. A 10% decrease in revenue would drop the economic return to 11%.

ix. Apart from the benefits of the project included in the economicreturn calculation, major indirect benefits can be attributed. The projectwhich is the first integrated forest utilization project in Turkey, will sub-stantially improve the utilization of the country's resources. The projectitself should become a pilot for this kind of development and the studiesshould contribute to its further advancement. The project will also createadditional steadv employment for more than 4,000 people living in the forestvillages, who are regardea as the poorest section of the Turkish population.Furthermore, it includes training of labor and will provide a steady and re-liable source of unfinished sawnwood for small sawmills. The net annualforeign exchange saving of the project is estimated at some US$25 million.

x. Based on agreements reached during negotiations, the project isconsidered suitable for a Bank loan of US$40.0 million.

I. INTRODUCTION

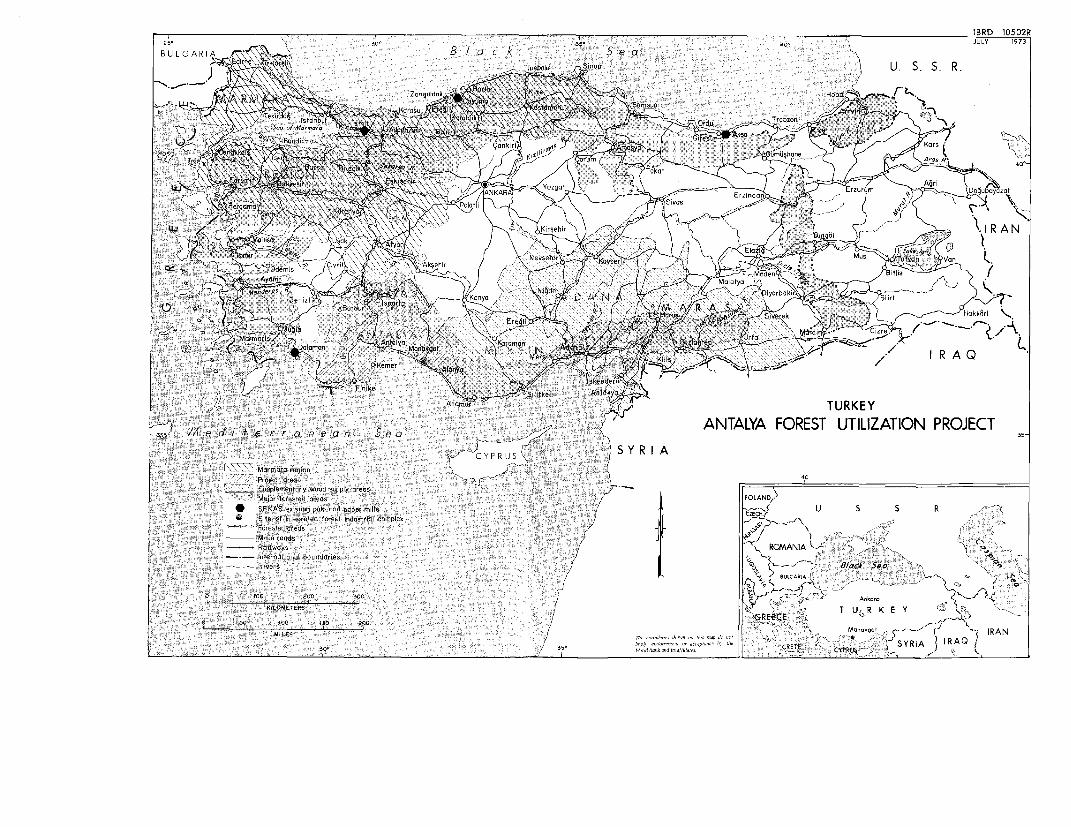

1.01 The Government of Turkey has requested a Bank loan of US$40.0million equivalent for a major forestry utilization project in the Antalyaregion of southern Turkey (Map IBRD 10502), the aggregate cost of which isestimated at about US$1.70.l million iincluding about US$68.0 million in foreignexchange. The project includes three separate but integrated parts: (a) aforestry program; kb) a large pulp and paper mill as well as a sawmill; and(c) studies for future forest utilization projects in Turkey. The projectis the culmination of many years of planning and promotional efforts by theGovernment and international agencies, including the United Nations Develop-ment Program (UNDP); the Food and Agriculture Organization (FAO); the EuropeanInvestment Bank (EIB) and the World Food Program (WFP). The Government ofTurkey, the Turkish State Investment Bank (SIB) and EIE will also providefinancing for the project.

1.02 The Bank's involvement in the project commenced in 1969 when theFAO/IBRD Cooperative Program started major project preparation. Subsequently,in -'~arch 1972, as Executing Agency for a UNDP financed study, the Bank engagedSandwell & Co., a well known Canadian firm of forest industry consultantsbto carry out a feasibility study. This study determined how best to utilizethe Antalya forest resources and defined the specific forestry and industrialelements to be financed. In preparing the project, improved cooperationbetween the two entities which are to carry out the project -- tne Ministryof Forestry (IT) and Seluloz ve Kagit Sanayii (SEKA), the State-owned pulpand paper company -- was achieved and a Turkish project preparation team wasestablished jointly with personnel recruited from MF and SEKA. This impor-tant joint effort was the first time the integrated development of a forestregion has been tackled.

1.03 The Bank appraisal is based largely upon Sandwell's detailedfeasibility study 1/, wrhich was completed in February 1973, and carried outin close cooperation with the Bank and the Turkish project preparationteam. Five review sessions with the Bank and Government during the studyhelped ensure agreement on its findings. The project was appraised by Bankmissions which visited Turkey in April and June 1973. The appraisal teamconsisted of Messrs. Peter Glenshaw (chief), Ilanfred Ferber and Max Oberdorferof the Industrial Projects Department, Mr. Raymond Rowe of the AgricultureDepartment CPS, Mr. Richard Palmer of the EMIENA Regional Office ProgramDepartment, Mr. Edgar Su of the EMENA Regional Office Projects Departmentand Mr. Colin Southall of the Legal Department. Both missions were joinedin the field by staff of the EIB and worked closely with members of allconcerned Turkish organizations, especially NP, SEKA and SIB.

1.04 A glossary of terms used in this re2ort is given in Annex 1.

1/ A six report study in seven volumes of some 1,200 pages.

-2-

II. FORESTRY IN TURKEY AND ThE STATE PULP AND PAPER COMPANY

A. Background

2c01 It is not widely recognized that Turkey possesses extensive forestresources and that it is fourth in Europe in terms of forested area. Thislack of recognition is probably due to the very poor yield from Turkey'sforests (0.3 m3/ha/year compared with 1.7 m3/ha/year or better in Finlandand Sweden) and the fact that forestry makes only a minor contribution tothe country's economy - under 4% of GDP in 1972, compared with about 14%and 12% of GDP for Finland and Sweden respectively in 1970.

2.02 The poor yield from Turkey's forests - even more apparent whenrecognizing that Turkey's mild climate makes trees grow faster than in theNordic countries - is due to obsolete systems of forest management whereconservation rather than production has been the guiding principle. Thedisadvantage of such a principle is that after a period of rapid growth,the growth rate declines and eventually mortality causes forest stands todiminish. Modern forest management allows for harvesting at the end of theperiod of rapid growth with immediate replanting using improved young treesto ensure full use of the combined resources of land and climate.

2.03 The need to change this practice in Turkey has long been recognizedby the Government, which owns all of the natural forests; but to put thesedesired changes into practice has been found difficult. The people livingin or near the forests - 13 million or over one third of the country'spopulation - have legal rights to grazing and procuring forest products atlow prices from the forest administration, making it difficult to introduceany changes that might seem to encroach on these rights.

2.04 The result is that Turkey's forest exploitation lags behind thatof its European neighbors and its forest-based industries are scattered anddisorganized. Partly due to a haphazard growth and uncertainties in woodsupply, its pulp and paper sector has mills which are small and rather highcost producers by world standards. At the same time, the economy is creatinga strong demand for paper and wood products. The need for change thereforehas become increasingly urgent and the proposed project should - at leastin the Antalya region - help to overcome these deficiencies and act as animpetus for other regions to follow. A detailed description of the placeof the Antalya project in the development of Turkey's forests is given inAnnex 2.

-3-

B. The Ministry of Forestry

2.05 Government control of forest operations extends back to the mid-19th century, but waned in the early 1900's. In 1937, the Republic'sForestry Department took control of all fellinig and marketing of logs andby 1956 all privately owned forests over 3 ha in area had been nationalized.Compensation was given mostly in the form of the rights mentioned above.The Ministry of Forestry (MF) was established in 1969. Its operationaldepartment, the General Directorate of Forestry (GDF), manages all forestoperations including that in the Antalya area where one of GDF's 24 Regionsare located.

2.06 MF is charged with preserving the national forests and increasingtheir yield, planting trees, building forest roads, seeing to the needs offorest villagers and operating some wood using industries (mostly sawmills).MF administration is highly centralized, although the vast majority of its1,500 forest officers who in about equal parts are graduates of the ForestryFaculty of Istanbul University and the Turkish Forest Training Schools arein the field. A large portion of the staff have professional competence,although somewhat outdated training has left them with the overly conservativeattitude to forest management referred to previously.

2.07 MF has a high degree of financial independence, selling logs andother wood products - and using the income to cover operating, administrativeand investment expenses. In 1972, its total revenues amounted to aboutTL 2,100 million, covering about TL 850 million direct production costs, TL 750million salaries and overheads, TL 400 million investments and about TL 100million corporation taxes and payments to the National Export Fund. 1/ TheME has been contributing mainly through corporation taxes and Export Fundpayments to the national budget in recent years; given the strong wood pricesthese contributions are likely to increase in future years and may exceed TL 200million in 1973. Details on the budget mechanism, breakdowns of the individualcosts and revenue components and profit and loss statements and balance sheetsfor MF comparable to corporations are presented in Annex 3. The last availa-ble ones for 1970 indicate a net profit before taxes of TL 137 million; thebalance sheet slhows ecuity funds from retained earnings of almost TL 600million.

2.08 Roundwood production in 1972 amounted to 5.6 million m3 which willbe increased to 6.4 million m3 in 1973. Additionally, about 19 millionsteres 2/ of fuelwood will be produced in 1973. Of the investment expendi-tures in recent years nearly two-thirds have gone into reforestation, affores-tation, forest roads and machinery and equipment for forest operations, whilethe rest went into forest management, wood processing industries and othermiscellaneous activities. Although MF has in the past devoted a good dealof its efforts and expenditures directly to improving the social conditionsof forest villagers primarily through developing forest infrastructure wellin advance of need, this is rare today, axcept for very remote areas. There-

l/ A Government controlled fund to promote and subsidize selected exports.2/ A stere is a cubic meter of stacked wood.

-4-

fore, Turkey's wood prices are no longer loaded with "social costs" whichshould more properly be the burden of the State rather than the ForestryBudget. On the other hand because of the lagging forest yields, log supplieshave been falling behind demand and thus have pushed up prices.

2.09 Within the Ministry of Forestry there are three main budgets. First,there is the budget of the Ministry of Forestry itself, which is relativelyunimportant because it covers just the personnel costs of the Ministry. In1973 this budget amounts to TL 20 million and is covered through the nationalbudget. Second, there is the "Annex Budget" providing for forest activitieswhich are of a national nature, for example generally applicable researchprojects. The GDF is in charge of the Annex Budget activities and it isfinanced through surpluses of the forest operations of the various districts.Third, there is the "Revolving Fund", which is by far the largest budget andcovers all current and investment costs for forest activities related to pro-duction and sales. The GDF is also in charge of the overall coordination ofthe Revolving Fund whereas detailed execution of the Revolving Fund activitiestakes place in the individual Forestry Districts. A detailed breakdown of thedifferent budgets is given in Annex 3.

C. The State Pulp and Paper Company

1. Plant Facilities and Operations

2.10 Seluloz ve Kagit Sanayii (SEKA) was founded in 1934 as a StateEconomic Enterprise under Law 440 1/ and is by far the largest pulp and paperproducer in Turkey. In 1972, SEKA was responsible for 100% of Turkey's outputof pulp and 85% of paper production; the remainder was produced by numeroussmall private plants, most of which are based upon waste paper.

2.11 SEKA is a holding company with each of its plants effectivelyoperating as separate legal and financial entities. The industrial part ofthe project, for which SEKA is sponsor, will also be established under Law440 as the Seka Antalya Muessessesi (The Establishment) and it will be theultimate borrower. Given SEKA's responsibility for project implementation,its operational influence on its subsidiaries, and its position in the Turkishpulp and paper industry, its activities and financial situation are presentedin Annex 3 and summarized below.

2.12 SEKA's first plant and its head office are at Izmit. The IzmitPlant contains much obsolete equipment and a modernization project is beingimplemented. The Izmit Plant was added to piecemeal until the mid-1960'swhen SEKA embarked on a major expansion program, building three modern -though small - plants at Aksu, Caycuma and Dalaman. Although all of thesehad experienced substantial delays in implementation, higher than estimatedcapital costs and initial operating difficulties, the first two mills are

1/ Law concerning State Economic Enterprises and their Establishments, andgoverning their Participations.

- 5-

now operating at reasonable levels of capacity utilization. Major start-updifficulties at Dalaman were experienced in 1972, the first year of operation.These difficulties have by now been largely overcome and full capacity utiliza-tion should be reached in 1974. All these new plants were built with foreigntechnical and financial assistance and partly on a turnkey basis.

2.13 Wood is SEKARs main raw material, but straw, reeds and waste paperare also used. The plants are generally well run and kept in good mechanicalcondition, although the labor force is substantially in excess of what isusual in other countries. Principal features of SEKA's plants are shown indetail in Annex 3 and are summarized below:

Principal Features of SEKA Plants

1972Capacity

Original Utili- Appr.Capacity On-Stream zation Labor

Location Principal Products (tons/year) Year (%) Force

Izmit Paper and Board 120,000 1936 100 5,850Caycuma Sackkraft 60,000 1970 100 990Aksu Newsprint 82,500 1971 85 1,020Dalaman Paper and Board 75,000 1972 30 1,710

337,500 77 9,570

2. Management and Labor

2.14 SEKA's Board consists of six members: one each from the Ministryof Finance and the Ministry of Industry and Technology, one Labor representa-tive and three members of the Company's top management. The Board functionsas a policymaking and controlling body as well as a liaison and coordinatinggroup between the Company and the Government. The influence of the Govern-ment on financial and investment planning is strong, although there is littleinterference in day-to-day operational matters. Since 1967, the ManagingDirector of SEKA and Chairman of the Board has been Mr. Aziz Gumus, who hashad substantial managerial experience.

2.15 SEKA's management and staff are generally capable but have beenunder considerable pressure over tne last 5-10 years, because of the majorexpansion program and substantial staff turnover because of salary levelsslipping below those paid by private industry. SEKA's staff is paid inaccordance with the Personnel Law for civil servants. Tnis is felt as aconsiderable restraint particularly in middle and upper management whereprivate industry's salaries are multiples of salaries based on the PersonnelLaw. Good staff is thus difficult to attract and to liold and SEKA and the

-6-

Establishment will, if necessary, improve the compensation for certain keypositions by making special contracts as is done in other State EconomicEniterprises. Relations between management and workers have been relativelygood and no major strikes have taken place in recent years.

3. Financial Analysis - Past and Future

2.i6 Historical and projected production, income statements, balancesheets and cash flow statements of SEKA through 1978 are shown in detailin Annex 3.

2.17 SEKA's present financial situation is dominated by its expansionprogram. In each of the years 1970-72, SEKA brought on stream one of itsthree new plants. The first two plants are now breaking even, but theDalaman Plant incurred losses of TL 179 million in 1972 and a similar lossis expected for 1973. The unfavorable development at Dalaman has more thanoffset the profits of TL 143 million at Izmit.

2.18 On the other hand the cash generation of SEKA has increasedsubstantially in the past years and the debt/equity ratio was strengthenedafter a substantial infusion of new equity by the Government in 1971. How-ever, repayments of loans incurred for the recent expansion program causeddebt service coverage to decrease to a point in 1972 and 1973 where cashgeneration is just barely sufficient to meet current debt obligations.Therefore, under normal circumstances, the Company's financial positionwould be unsatisfactory. Nevertheless, SEKA has the possibility of furtherequity calls on the Treasury and its financial position should improve asit reaches full capacity utilization at Dalaman. M4oreover, the Establishmentis not directly affected financially by SEKA.

2.19 To meet anticipated demand SEKA has four major projects underconsideration: Izmit modernization, Afyon and Balikesir (Annex 3) andAntalya, the subject of this report. Total investment costs of theseprojects are estimated at about TL 4 billion; their additional capacitytotalling about 300,000 tons/year is almost equal to SEKA's existing capacity.Given SEKA's present financial situation and this major expansion program,it is important that SEKA pay particular attention to its financial positionif it is to become independent of further budgetary support by the Treasury.As a start, SEKA has undertaken to review and improve its own financial con-trol and reporting system.

-7-

III. ThIE PR0JECT

3.01 The project, which is expected to be completed by the end of 1977,consists of three parts - forestry, industrial and feasibility studies. Theyare described in detail in Annexes 4, 5 and 6 and are briefly stsmnarized below.

A. The Forestry Part

3.02 The forestry part involves increasing 3 log production in She Antalyaregion from its present level of some 300,000 m /year to 800,000 m /year.Tree felling, transport and replanting activities will have to be inereasedand as a result new equipment (mostly transport vehicies and road buildingmachines 1/) will be needed. About 475 km of roads (plus one bridge) andsome 209 buildings will be constructed and the work force (but not theadministrative staff) increased from 7,000 to 11,000 men*

3.03 Antalya has some 472,000 ha of good productive forest land out ofa total area designated as forest of 1,320,000 ha - the remainder being mostlymaquis scrub. The predominant species is Pinus Brutia (kizilcam in Turkish,or red pine), w'Lich is acceptable for the production of sawnwood and paper.The forest blocks are scattered over a wide area and are generally understockedwith trees, i5ostly over-mature. The productive forest is estimated to contain30 million m of wood, about 75% of which is classified as sawlogs, 14% aspulpwood, 1% as plywood logs and 10% as industrial shortwood.

3.04 Management on the basis of sustained yield involves the regulationof timber harvesting to ensure in perpetuity, an equal, or increasing (butnever diminishing) supply of wood. The annual allowable cut by 1979 whenthe pulp and paper3mill should start up has been conservatively calculatedat about 800,000 m . While maintaining the sustained yield principle, MFhas agreed that overmature trees will be liquidated as quickly as possibleand inmmediately restocked with young, healthy seedlings. Reforestation ofsome 9,500 ha/year will thus be needed, which when added to the afforestationeffort of 1,500 ha/year makes a planting program of 11,000 ha/year - aformidable program by any standards.

3.05 Present log production methods and forest organization will be main-tained and will be extended generally to the whole Antalya region (Map IBRD10502). Hand felling with animal skidding of the felled logs to the roadsideis used. The logs are manually loaded onto ordinary 3 to 5 ton trucks forhauling to the mill or to log depots for sale to the public. The emphasis onmanual labor might create labor shortages in the future and productivity in-:creases by such simple devices as inproved-harnesses, better draught'animals,and training of workers will then be necessary.

1/ See Annex 4.

-8-

3Of the annual allowable cut of 800,000 m3 from 1979 onwards, some

o, &,000 m3/year will be available to the Establishment. Of the remaining90,00oi m3 , about 80,000 m3 is expected to be demanded by the forest villagerstndar their legal priority rights. The remaining 110,000 m3 would be avail-abLe to meet the Antalya region's demand for other purposes such as other saw-mills and furniture makers. In addition to the 610,000 m3/year, the mill willhave available to it 15,000 m3/year from the Isparta region to the north ofAntalya and up to 200,000 m3/year from the Adana/Mersin region should the needari.se.

B. The industrial Part

3.07 The plant is proposed to be located on the Mediterranean coast(para. 3.18) near the town of Manavgat and a river of the same name that willsupply the water year round that is essential in the production of pulp andpaper. As mentioned Previously, the plant will consist of a sawmill and apulp and paper plant with all necessary ancillary installations as well asextensive and entirely acceptable effluent treatment facilities (describedin para. 3.17 and Annex 8), some housing and administrative offices. Adetailed description and a flow sheet are given in Annex 5.

33.08 The sawmill will process about 340,000 m /yearl/ of logs 20 cm ormore in top diameter and 2.5 and 5.0 m in length to produce annually 182,000m3 of sawnwood in three shifts. The logs will be sorted into species in thewoods and delivered by truck to the mill. They will be debarked partly inthe woods and partly at the plant depending on the availability of labor,although the plant will be capable of debarking the entire log input. Theprimary breakdown will be a conventional bandsaw and no-man carriage, followedby a quad bandsaw, a horizontal resaw, two other resaws and two adjustableedgers. Because this will be by far the largest sawmill in Turkey the degreeof mechanization will be relatively high by Turkish standards, although manualhandling and sorting will be far greater than in North America or Europe.After sawing, the wood will be airdried 2/ for some three months in the yardand then trimmed and graded before shipment. Sawdust, slabs and edgings willbe collected for dispatch to the pulp mill.

3.09 The pulp mill will have an annual capacity of some 147,000 tons(bone dry) of unbleached kraft pulp and be operated continuously, as is usualin this industry. The pulp logs (472,000 m3/year) and sawmill residues(142,000 m3/year) will be chipped and blended to assure a constant speciesmix. Batch digesters have been suggested for simplicity of operation, es-pecially as cooking conditions will differ for the two types of pulp (high

1/ Wood volume figures used for the industrial part are on a true volumebasis whereas MF figures for sawlogs represent scaled volume whichamounts to about 10% less than true volume.

2/ Kiln drying does not appear to offer enough advantages to include a kilnin the initial investment. However, this matter will again be reviewedafter some actual operating experience has been obtained.

-9-

and normal yield) needed for linerboard manufacture. Sackkraft requires onlynormal yield pulp. Pulp washing and screening will be in two lines also forthis reason and the refining will be done in five double disk refiners, beforethe pulp is fed to the paper machine.

3.10 The paper miLl will have an annual capacity to produce 155,000 tonsof kraft linerboard 1/ on one paper machine. However, in order to meet expectedmarket growth optilmally and taking into account other paper making capacityin Turkey, the paper mill will also be able to produce sackkraft though of asmaller combined tonnage. The capacity of the mill producing sackkraft onlywould be 90,000 tons per year. The paper machine, a conventional "fourdri-nier", will have a finished paper width of 6.4 m and maximum machine speed of600 meters per minute.

3.11 Electric power will be mostly (93%) generated on site and the re-mainder purchased. Steam will be produced in the chemical recovery furnace(46%) and in a fuel-oil fired boiler. As mentioned previously, water will beobtained from the nearby Manavgat River. A small townsite at the mill willcontain 177 housing units for key personnel, a guest house, a shop, a schooland a mosque. Some 857 people will be employed in the mill of which 534 areclassified as unskilled and no difficulty is expected in hiring them locally.Of the remaining workers, some 145 should have some direct experience in thepulp and paper and sawmill industry and will be difficult to hire from out-side. SEKA will transfer personnel from its existing mills after they havebeen trained to upgrade their skills. Adequate training is an essential elementof the project and is being provided for (para 6.05 and Annex 5).

3. 12 Transport of inbound traffic (primarily logs, fuel oil and chemicals)will be arranged by SEKA and outbound shipments (sawnwood and paper) by thecustomers (Annex 7). With the considerable quantities involved and the rel-atively small size of trucks now in use in the area, traffic congestion couldoccur at certain times and, improvement of the coastal highway leading tothe plant in places and alternative means of transport should therefore bestudied. Preliminary investigations by Sandwell show considerable savingsin transport costs if truck sizes could be increased from 6 to 20 tons, andespecially if tug/barge sea shipments of products (and eventually wood fromMersin) could be used. While any road congestion should not affect theplant's operations it will inconvenience and create problems for local roadusers and tourists. This problem has been discussed with the Government,which will study the impact of the mill on highway capacity in the adjacentarea by the end of 1974 and will implement the necessary steps to ensureadequate transport infrastructure.

1/ Linerboard is the paper used as the outside and inside layers of corru-gated containers. The layers are separated by a corrugated paper calledcorrugating medium or "fluting".

- 10 -

C. Tne Studies Part

3.-.3 IBRD financing of US$0.4 million is proposed to help finance studiesfor the future development of the forest sector. Such studies and potentialresulting investments have always formed part of the discussion leading tothe Antalya Project which is just one step on the long road of Turkey's forestdevelopment. The studies are currently being defined more precisely and theirforeign exchange cost appears to be between US$2.5 and US$3.5 million. TheBank iinancing would be used for one or more specific studies in this program.Additional financing is being considered by UNDM in the amount of US$1 millionfrom the Turkey Country Program and the Administrator's Program Reserve, andfrom EIB in the amount of US$1.1 million from an existing line of credit of2.0 million Unit of Account (US$2.4 million equivalent) already available toTurkey for pre-investment studies.

3.14 The Groad scope of the studies has been clarified by a "Pilot Study"of the northwest region of Turkey in the vicinity of the Marmara Sea. Thisstudy was financed by the UNDP and executed by the FAO using Sandwell & Com-pany as the subcontractor. The study 1/ shows that the Marmara region has32% of the forested area of Turkey but that the present forest management sys-tem would not allow enough additional wood to be produced for further indus-trial development in Turkey. If an accelerated cutting and planting in theMarmara Region program was instituted it would be possible to raise the annualallowable cut from 3 to over 5 million cubic meters per year for coniferouswood. With this increased wood supply it would be possible to expand paperand sawnwood production to meet Turkey's expected future demands through theearly 1980s. The cost of the forestry and industrial developments would besome US$700 million over a 5- to 8-year period and initial indications arethat the investments would yield a satisfactory return.

3.15 Much remains to be done in defining the specific scope of the stud-ies, in establishing the implementation machinery, and particularly in coor-dinating the efforts of both the Turkish and International institutions, butthese should be finalized by the middle of 1974. It is therefore recommendedthat IBRD funds of US$0.4 million be made available to the Government to beutilized at the discretion of the Bank management in accordance with normalBank practice for preinvestment studies.

D. Ecology

3.16 The Antalya coast is widely reputed for its natural beauty, its his-torical sites and its delightful climate and has therefore a high potentialfor the development of tourism. Pulp and paper plants, on the other hand,have also been reputed for their adverse impact on the environment. Therewould therefore appear to be a conflict in building such a mill in such anarea. However, modern technology has reduced the degrading effect of pulpand paper plants to a level which need not interfere with tourism development,so that the two types of development could proceed side-by-side (Annex 8).

1/ Described more fully in Annex 6.

- 11 -

3.17 While marginal risks due to plant upsets may still remain, the en-vironmental protection measures proposed for the plant will ensure that itsimpact on scenic view, air and water quality and traffic congestion will bereduced to acceptable levels. Careful architectural planning and landscapingwill ensure that the view is not marred by an ugly industrial plant. Thegaseous and liquid effluents will be minimized through maximum in-plant re-cycling, and the emissions will be treated and disposed of to render themharmless. Gaseous emissions will all be disposed of to the atmosphere viaa single tall stack. Liquid effluents will be settled and clarified beforebeing discharged to the sea via a pipeline, long enough (probably 1 to 2 kminto the sea) to ensure sufficient dilution. Plant operating procedures willspecify proper operations of these systems and the personnel will be adequatelytrained in their operation and maintenance. The traffic problem will be stud-ied as discussed in para 3.12 and suitable measures such as highway improvements,and/or sea shipments introduced.

3.18 The constraints of topography put primary emphasis on locating plantsites along a 90 km belt of coastal land, some 5-10 km deep. The Governmentestablished an interministerial committee to conduct a detailed comparison often specific sites in a zone 25 km either side of the Manavgat River. Thecommittee recommended, and the Government concurred in, a site 3 km inland andsome 25 km froi. the historical and touristic area of Side as being the onebest able to satisfy a list of economic, ecological, and tourism criteriadrawn up to compare the sites. It is estimated that the site chosen willentail initial capital costs of some TL 45 million more than the lowest costalternative which would have been some 11 km from Side. Although the site isowned by private parties there should be no difficulties with land acquisition.

3.19 The Government will ensure that the mill follows strict standardsfor air and effluent emission controls and architectural design standards.The Bank's approval will be sought on the character and implementation ofthese ecological controls. The Government will ensure that haphazard devel-opment of the area surrounding the plant site is avoided. No other indus-trial plants will be allowed to be built in the vicinity of the mill.

3.20 Forestry operations will be conducted according to sound silvi-cultural and cutting practices. Management of the forest resources will bebased on the principle of sustained yield to ensure that through regulationof annual allowable cut, timber supplies will not be diminished. Fellingoperations will be carried out with due regard for erosion controls. Bothreforestation and afforestation with indigenous species will further ensurethe maintenance of the natural forest cover. Policing by the Government ofcutting regulations and effective fire and erosion control is expected toensure the environmental integrity of the forests and its wildlife.

- 12 -

IV. TIFE MARKET

4.01 The market for Antalya's forest products - sawnwood, linerboard andsackkraft - which will all be sold domestically, is described in detail inAnnex 9 and summarized in the following paragraphs.

A. Sawnwood

4.02 The availability of good and ample supplies of sawlogs in the Antalyaforests fits well with the rising national demand for sawnwood. About 80% ofsawn goods are used for construction purposes, and the boom in house, apartment,office and industrial building construction will require large amounts. Mostof the Antalya sawn goods from the Pinus Brutia trees will be constructiongrade only, used for scaffolding, concrete framework, roof rafters, and rooftile support battens.

4.03 Current (1972) consumption of sawnwood for these uses in the proj-ect's natural marketing area (i.e. Istanbul, Ankara, Izmir, Mersin-Adana,Konya and Antalya whicl together account for about 45% of total Turkish con-sumption) is 735,000 m and is expected to grow in future at some 6.5% peryear. Such a projected growth rate may be on the conservative side on thebasis of both the expected growth in construction activities in Turkey andpast consumption growth in sawnwood in the country which during the period1962-72 may have reached 10% per year (available statistics are unreliable).

4.04 By 1979, when3the Antalya sawmill is expected to have reached fullproduction of 182,000 m , the incremental sjwnwood consumption in the mill'smarketing a ea would have reached 405,000 m (for a total consumption of1,140,000 m ). Consequently, the Antalya mill would supply only 45% of the iincremental consumption. Since there are no known major expansions of sawnwoodcapacity in the marketing area, and accepting that consumption of sawnwoodmay fluctuate with developments in the construction industry, there is nodifficulty foreseen in disposing of the mill's total outpuit. The AntalyaEstablishment, with SEKA's help, will prepare a detailed marketing and dis-tribution plan by the end of 1974 well before production starts and prepara-tion of such a plan is part of a Project Agreement between the Bank and TheEstablishment and SEKA.

B. All Papers

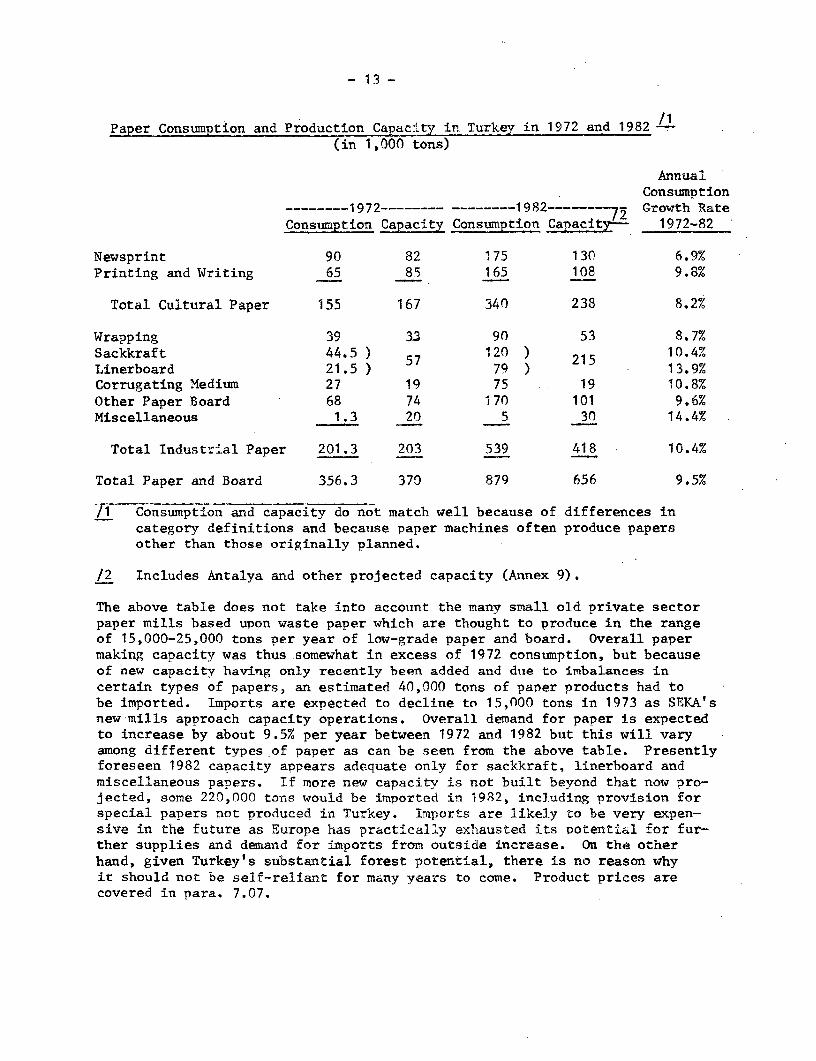

4.05 Paper consumption rose in Turkey between 1960 and 1972 at an aver-age annual rate of about 13%. This is a considerable increase consideringimport constraints and the relatively high Turkish paper prices. The follow-ing table shows consumption and production capacity for major groups of paperin Turkey in 1972 (actual) and 1982 (projected),

- 13 -

Paper Consumption and Production Capacity in Turke in 1972 and 1982 (in 1,000 tons)

AnnualConsumption

---- 1972…------- --------1982-------- -2 Growth RateConsumption Capacity Consumption Capacit 1972-82

Newsprint 90 82 175 130 6.9%Printing and Writing 65 85 165 108 9.8%

Total Cultural Paper 155 167 340 238 8.2t

Wrapping 39 33 90 53 8.7%Sackkraft 44.5 ) 120 ) 15 10.4%Linerboard 21.5 ) 79 2 13.9%Corrugating Medium 27 19 75 19 10.8%Other Paper Board 68 74 170 101 9.6%Miscellaneous 1.3 20 5 30 14.4%

Total Industrial Paper 201.3 203 539 418 10.4%

Total Paper and Board 356.3 370 879 656 9.5%

/1 Consumption and capacity do not match well because of differences incategory definitions and because paper machines often produce papersother than those originally planned.

/2 Includes Antalya and other projected capacity (Annex 9).

The above table does not take into account the many small old private sectorpaper mills based upon waste paper xwhich are thought to produce in the rangeof 15,000-25,000 tons per year of low-grade paper and board. Overall papermaking capacity was thus somewhat in excess of 1972 consumption, but becauseof new capacity having only recently been added and duie to imbalances incertain types of papers, an estimated 40,000 tons of paner products had tobe imported. Imports are expected to decline to 15,000 tons in 1973 as SEKA'snew mills approach capacity operations. Overall demand for paper is expectedto increase by about 9.5% per year between 1972 and 1982 but this will varyamong different types of paper as can be seen from the above table. Presentlyforeseen 1982 capacity appears adequate only for sackkraft, linerboard andmiscellaneous papers. If more new capacity is not built beyond that now pro-jected, some 220,000 tons would be imported in 1982, including provision forspecial papers not produced in Turkey. imports are likely to be very expen-sive in the future as Europe has practically exhausted its potential for fur-ther supplies and demand for imports from outside increase. On the otherhand, given Turkey's substantial forest potential, there is no reason whyit should not be self-reliant for many years to come. Product prices arecovered in para. 7.07.

- 14 -

C. Linerboard

4.06 Linerboard consumption is directly related to packaging. In 1972,linerboard consumption in Turkey is estimated to have reached about 21,500tons, up from 6,000 tons in 1962 and equivalent to an average annual growthrate of 13%. But in addition, there was probably a substantial unsatisfieddemand. Corrugated box makers, which are all located near population centers,and packaging users in Turkey have been complaining of chronic deficienciesin supply and it also appears that the cotmtry's exports of fruit and veg-etables have been inhibited by the shortage of modern packaging. Neighboringcountries such as Greece and Israel which are known exporters of these commo-dities have a per capita linerboard consumption of 4 and 25 times respectivelyas large as Turkey, which has much greater timber resources than either ofthem. Finally, corrugated container plants in 1972 operated at only abouttwo-thirds of their capacity for lack of linerboard. Thus, true linerboarddemand in 1972 may have been between 5,500 and 7,000 tons above the actualconsumption of 21,500 tons.

4.07 In future, demand for linerboard is expected to grow by between 12%and 15% annually, and is thus forecast to reach between 52,700 and 63,000 tonsin 19-79, the first year in which the paper mill is assumed to be operating atfull capacity. It is probable that a corrugating medium pulp and paper millwill be added at Caycuma. Meanwhile, Caycuma could increase corrugating med-ium production by up to 30,000 tons per year to meet the needs for this othercomponent of corrugated containers. Growth in corrugated container demandwill be stimulated mainly by export packaging and also by domestic trade inhigh value items such as industrially produced consumer goods while woodenboxes will most likely continue to be used for agricultural trade in Turkey.

D. Sackkraft

4.08 The major consumer of multiwall-sackkraft paper in Turkey is thecement industry which absorbs 80% of all domestic production while the re-maining 20% is taken up by three other industries: fertilizer, feed grainand gypsum. All these are rather strong growth industries in Turkey and itis expected that demand will increase by between 9 and 12% per year from theestimated 1972 consumption of 44,500 tons to between 84,000 and 97,000 tonsin 1979. The mean demand of 90,000 tons is expected to be met by the Caycuma(60,000 tons) and the Antalya (30,000 tons) mills. The Antalya mill has theflexibility of producing both linerboard and sackkraft and the followingtable summarizes the expected supply/demand ranges for these two papers.

- 15 -

Demand/Supply Ranges for Linerboard and Multiwall Kraft Sackkraft

(in 1,000 tons)

…----Linerboard…---------- --------------Multiwall Sackkraft-----------Demand Production Demand Production

Excess ExcessLow ih Antalya (Shortfall) Low Sigh Caycuma Antalya Total (Shortfall)

1978 48 56 38 (10) - (18) 77 88 60 23 83 6 - (5)1979 53 63 58 5 - (5) 84 97 60 30 90 6 - (7)1980 58 71 64 6 - (7) 92 108 60 40 100 8 - (8)1981 64 79 71 7 - (8) 101 118 60 49 109 8 - (9)1982 70 88 71 1 - (17) 112 128 60 49 109 (3)-(19)1983 75 97 84 9 - (13) 121 141 60 41 101 (20)-(40)

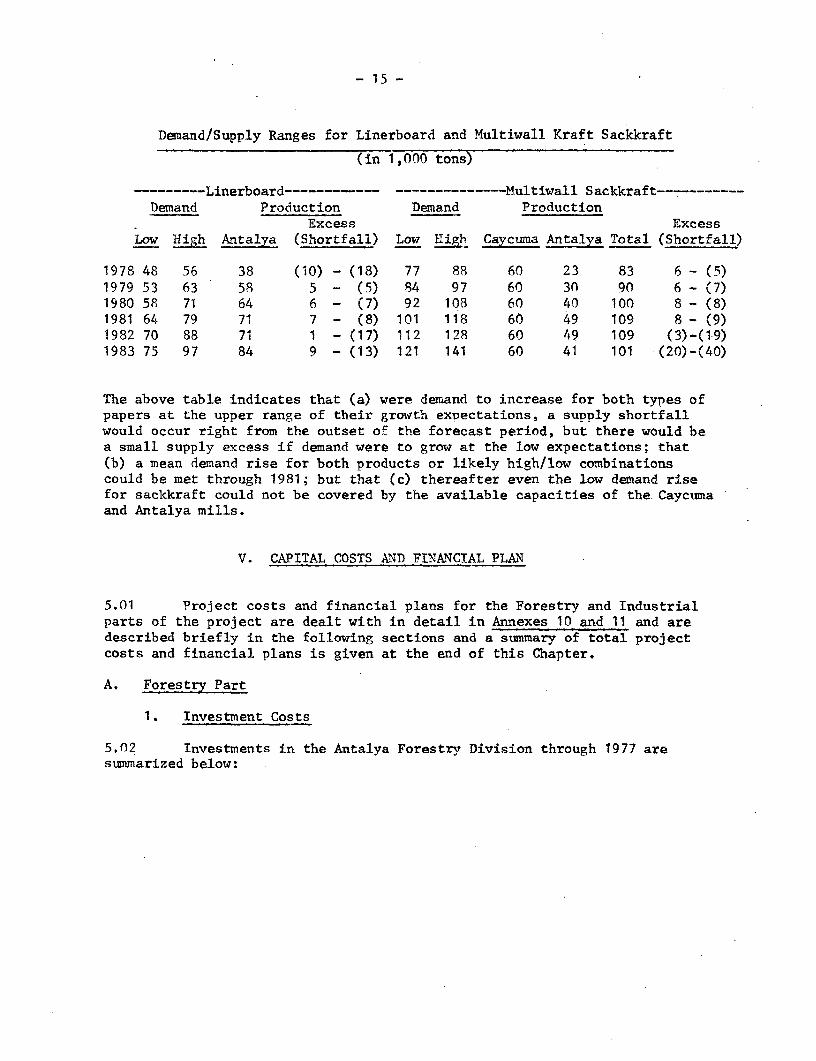

The above table indicates that (a) were demand to increase for both types ofpapers at the upper range of their growth expectations, a supply shortfallwould occur right from the outset of the forecast period, but there would bea small supply excess if demand were to grow at the low expectations; that(b) a mean demand rise for both products or likely high/low combinationscould be met through 1981; but that (c) thereafter even the low demand risefor sackkraft could not be covered by the available capacities of the.Caycumaand Antalya mills.

V. CAPITAL COSTS AND FINANCIAL PLALN

5.01 Project costs and financial plans for the Forestry and Industrialparts of the project are dealt with in detail in Annexes 10 and 11 and aredescribed briefly in the following sections and a summary of total projectcosts and financial plans is given at the end of this Chapter.

A. Forestry Part

1. Investment Costs

5.n2 Investments in the Antalya Forestry Division through 1977 aresummarized below:

- 16 -

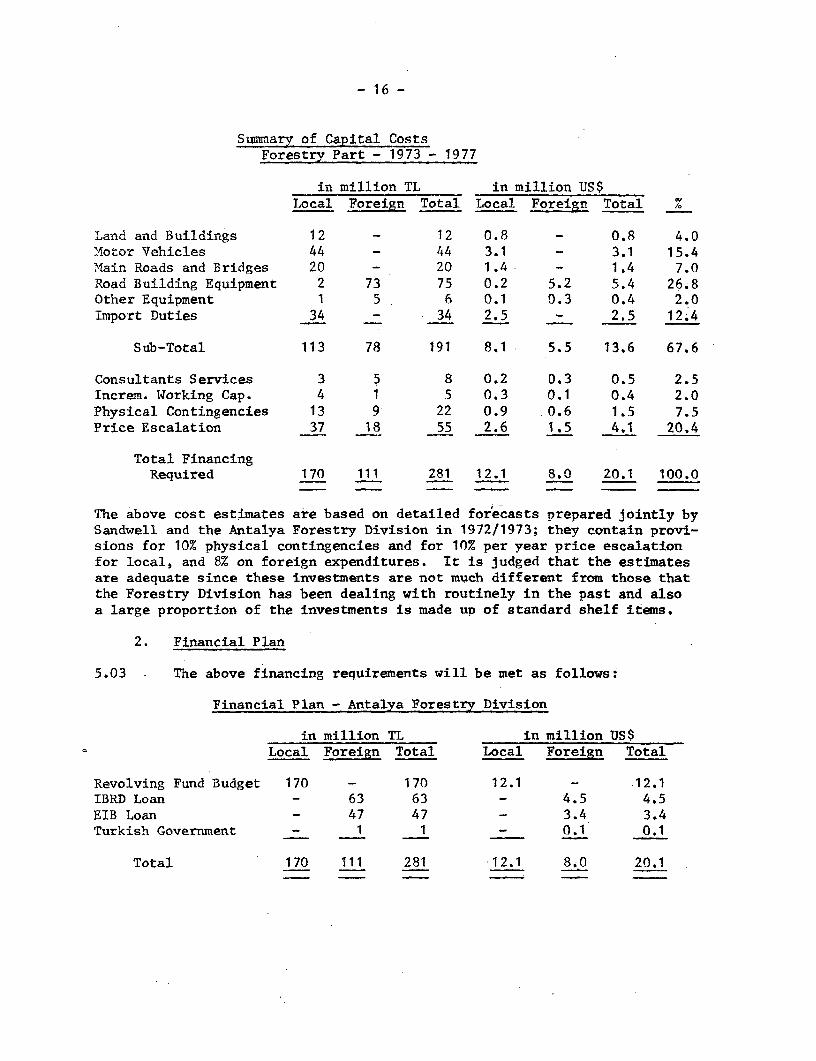

Summary of Capital CostsForestry Part - 1973 - 1977

in million TL in million US$Local Foreign Total Local Foreign Total %

Land and Buildings 12 - 12 0.8 - 0.8 4.0Motor Vehicles 44 - 44 3.1 - 3.1 15.4Main Roads and Bridges 20 - 20 1.4 - 1.4 7.0Road Building Equipment 2 73 75 0.2 5.2 5.4 26.8Other Equipment 1 5 6 0.1 0.3 0.4 2.0Import Duties 34 - 34 2.5 - 2.5 12.4

Sub-Total 113 78 191 8.1 5.5 13.6 67.6

Consultants Services 3 5 8 0.2 0.3 0.5 2.5Increm. Working Cap. 4 1 5 0.3 0.1 0.4 2.0Physical Contingencies 13 9 22 0.9 .0.6 1.5 7.5Price Escalation 37 18 55 2.6 1.5 4.1 20.4

Total FinancingRequired 170 111 281 12.1 8.0 20.1 100.0

The above cost estimates are based on detailed forecasts prepared j.ointly bySandwell and the Antalya Forestry Division in 1972/1973; they contain provi-sions for 10% physical contingencies and for 10% per year price escalationfor local, and 8% on foreign expenditures. It is judged that the estimatesare adequate since these investments are not much different from those thatthe Forestry Division has been dealing with routinely in the past and alsoa large proportion of the investments is made up of standard shelf items.

2. Financial Plan

5.03 . The above financing requirements will be met as follows:

Financial Plan - Antalya Forestry Division

in million TL in million US$Local Foreign Total Local Foreign Total

Revolving Fund Budget 170 - 170 12.1 - .12.1IBRD Loan - 63 63 - 4.5 4.5EIB Loan - 47 47 _ 3.4 3.4Turkish Government - 1 1 - 0.1 0.1

Total 170 111 281 12.1 8.0 20.1

- 17 -

5.04 The financial needs of any of the Forestry Divisions are providedby the Revolving Fund which is prepared annually by the GDF in coordinationwith the Forestry Divisions as discussed in para. 2.09. The Ministry ofForestry is, for its operations, financially independent from the Treasuryexcept for foreign funds.

5.05 The Bank and EIB will lend to the Government US$7.9 million equiv-alent (para. 5.15) to cover the foreign exchange requirements of this partof the project, except for the small amount of the incremental workingcapital (US$O.1 million) which will have to be met by th.e Government. TheBank's contribution of US$4.5 million will be for 16 years including 5 yearsof grace and carry an interest rate of 7-1/4% and the EIB portion of US$3.4million will be on the sane terms, except for an interest rate of 4 1/2%.The Government will allocate the proceeds of the two loans to GDF for invest-ments in the Antalya Forestry Division. Assurances have been given that(a) the foreign loan proceeds will be made available as required by the pro-ject; (b) the necessary budget provisions will be made to meet the project'slocal costs and the foreign exchange portion of the working capital as wellas any additional budgetary provisions to meet any possible project costoverrun; and that (c) at the same time adequate budget allocations will bemade for GDF's current operations.

B. Industrial Part

1. Investment Costs

5.06 The estimated capital costs and total financing required for thesawmill and the pulp and paper plant are summarized below:

- 18 -

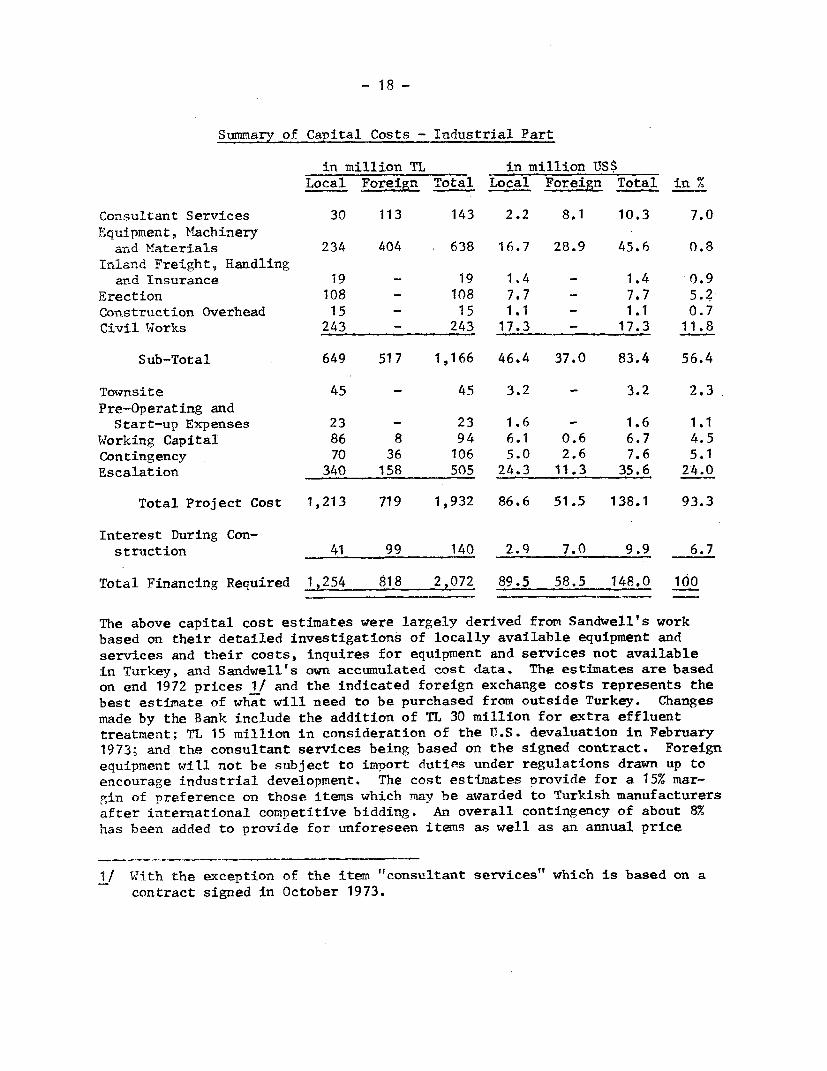

Summary of Capital Costs - Industrial Part

in million TL in million US$Local Foreign Total Local Foreign Total in %

Consultant Services 30 113 143 2.2 8.1 10.3 7.0Equipment, Machinery

and Materials 234 404 638 16.7 28.9 45.6 0.8Inland Freight, Handlingand Insurance 19 - 19 1.4 - 1.4 0.9

Erection 108 - 108 7.7 - 7.7 5.2Construction Overhead 15 - 15 1.1 - 1.1 0.7Civil Works 243 - 243 17.3 - 17.3 11.8

Sub-Total 649 517 1,166 46.4 37.0 83.4 56.4

Townsite 45 - 45 3.2 - 3.2 2.3Pre-Operating andStart-up Expenses 23 - 23 1.6 - 1.6 1.1

Working Capital 86 8 94 6.1 0.6 6.7 4.5Contingency 70 36 106 5.0 2.6 7.6 5.1Escalation 340 158 505 24.3 11.3 35.6 24.0

Total Project Cost 1,213 719 1,932 86.6 51.5 138.1 93.3

Interest During Con-struction 41 99 140 2.9 7.0 9.9 6.7

Total Financing Required 1,254 818 2,072 89.5 58.5 148.0 100

The above capital cost estimates were largely derived from Sandwell's workbased on their detailed investigations of locally available equipment andservices and their costs, inquires for equipment and services not availablein Turkey, and Sandwell's own accumulated cost data. The estimates are basedon end 1972 prices 1/ and the indicated foreign exchange costs represents thebest estimate of what will need to be purchased from outside Turkey. Changesmade by the Bank include the addition of TL 30 million for extra effluenttreatment; TL 15 million in consideration of the IJ.S. devaluation in February1973; and the consultant services being based on the signed contract. Foreignequipment will not be subject to import duties under regulations drawn up toencourage industrial development. The cost estimates provide for a 15% mar-gin of preference on those items which may be awarded to Turkish manufacturersafter international competitive bidding. An overall contingency of about 8%has been added to provide for unforeseen items as well as an annual price

1/ With the exception of the item "consultant services" which is based on acontract signed in October 1973.

- 19 -

escalation of 10% for local and 8% for foreign expenditures. The estimatesare based on a construction period of four years; this is conservative byinternational standards, but probably necessary for Turkey.

5.07 The working capital estimated at TL 94 million may appear ratherlow, but this is principally due to the relatively small requirements for re-ceivables, since according to prevailing practice in Turkey, 75% of the papersales value is paid by the customer prior to shipment.

5.08 In view of Sandwell's detailed project preparation, the above cap-ital costs estimates appear realistic.

2. Financial Plan

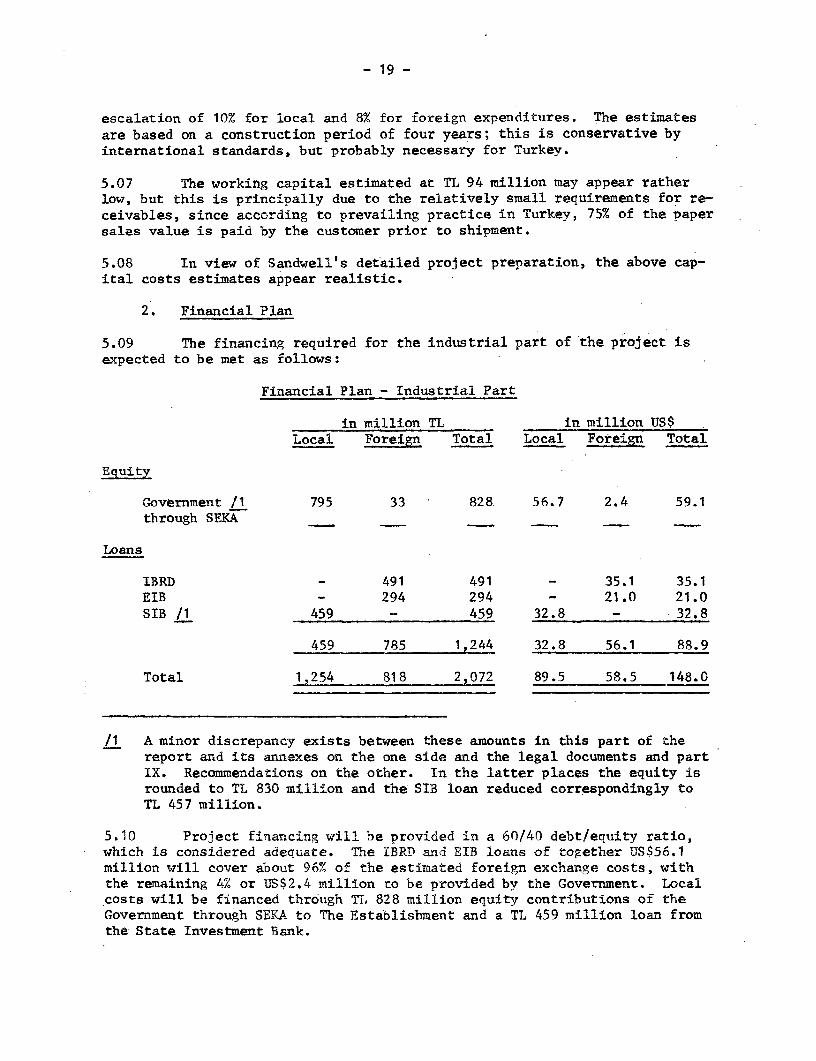

5.09 The financing required for the industrial part of the project isexpected to be met as follows:

Financial Plan - Industrial Part

in million TL in million US$Local Foreign Total Local Fotei Total

Equity

Government /1 795 33 828. 56.7 2.4 59.1through SEKA_

Loans

IBRD - 491 491 - 35.1 35.1EIB - 294 294 - 21.0 21.0SIB /1 459 - 459 32.8 - 32.8

459 785 1,244 32.8 56.1 88.9

Total 1,254 818 2,072 89.5 58.5 148.0

/1 A minor discrepancy exists between these amounts in this part of thereport and its annexes on the one side and the legal documents and partIX. Recommendations on the other. In the latter places the equity isrounded to TL 830 million and the SIB loan reduced correspondingly toTL 457 million.

5.10 Project financing will be provided in a 60/40 debt/equity ratio,which is considered adequate. The IBRD and EIB loans of together USS56.1million will cover about 96% of the estimated foreign exchange costs, withthe remaining 4% or US$2.4 million to be provided by the Government. Localcosts will be financed through T. 828 million equity contributions of theGovernment through SEKA to The Establishment and a TL 459 million loan fromthe State Investment Bank.

- 20 -

5.a 1" Proposed Bank lending of US$35.1 million equivalent will be made tothe Turkish Government at an interest rate of 7-1/4% and for 16 years includ-ing 5 vears of grace. The Government will channel the loan proceeds throughSIB for onlending to The Establishment at an interest rate of 9% per annum,which rate is generally consistent with the current IFC interest rate forprojects in Turkey and considered roughly in line with foreign exchangefinancing from commercial sources although differences in terms make com-parison difficult. The interest margin of 1-3/4% (between 7-1/4% and 9%)will be allocated to SIB and the Treasury (in lieu of a guarantee fee),in the proportion of 1% to SIB and 3/4% to the Treasury. A subsidiary loanAgreement for these arrangements will be drawn up on terms satisfactory tothe Bank.

5.12 The EIB loan of US$21.0 million equivalent would also be made tothe Government but at an interest rate of 4 1/2% for 30 years including 8 yearsof grace. It would be passed to the project on the same terms as the Bankloan, and also through the same channels. The interest margin of 4 1/2%(9% - 4 1/2%) will also be allocated to SIB and the Treasury, but in the pro-portion of 1% to SIB and 3 1/2% to the Treasury.

5.13 The SIB loan in the amount of to TL 459 million (US$32.8 million)for local expenditures would be granted at their usual interest rate of 10-1/2%for 15 years including 5 years of grace.

5.14 The equity of TL 828 million (USS59.1 million) - TL 795 million forlocal costs and TL 33 million for foreign costs - will be Provided by theGovernment through SEKA. The Government will provide the equity in time asrequired by the project and at least at a rate of 40X of project expenditures.Also as a guard against any unexpected cost overrun (both in foreign exchangeand local currency) and to keep The Establishment on a sound financial foot-ing until the project is operating normally, the Government will provide anyadditional funds as necessary to complete the project 1/ and on terms satis-factory to the Bank and to provide at the completion date a current ratio ofat least 1.3:1 in The Establishment. Finally, at least 40% of any additionaloverrun financing will be provided in the form of equity or subordinated debtand the terms of the additional loan funds will be substantially the same asthe original loans.

C. Summary of Project Costs and Financing Sources

5.15 The following gives a summary of the costs and sources of financingfor each of the three Project Parts. The scope of the studies included inthe project has been discussed in paras. 3.13-3.15 and the financing of thestudies has been included in the presentation below.

1/ The Project "Completion Date" is defined as the date on which the millhas run at 90% of its rated capacity for 180 consecutive days. Thisnormally occurs some 2-3 years after mill start up.

-21-

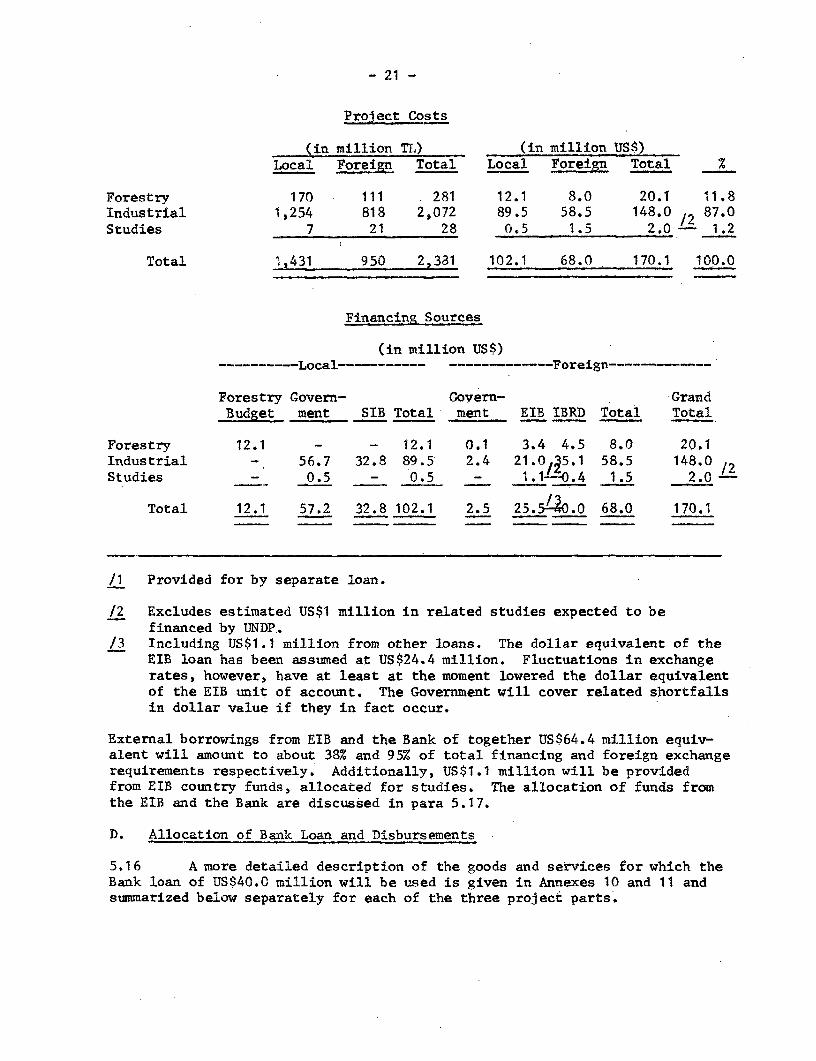

Project Costs

(in million TL) (in million US$)Local Foreign Total Local Foreign Total %

Forestry 170 111 281 12.1 8.0 20.1 11.8Industrial 1,254 818 2,072 89.5 58.5 148*0 /2 87.0Studies 7 21 28 0.5 1.5 2.0 - 1.2

Total 1,431 950 2,381 102.1 68.0 170.1 100.0

Financing Sources

(in million US$)-- -Local - - --- - ------ Foreign…---------

Forestry Govern- Govern- -GrandBudget ment SIB Total ment BIB IBRD Total Total

Forestry 12.1 - - 12.1 0.1 3.4 4.5 8.0 20.1Industrial - 56.7 32.8 89.5 2.4 21.0,@5.1 58.5 148.0 /2Studies - 0.5 - 0.5 - 1.1-0.4 1.5 2.0

Total 12.1 57.2 32.8 102.1 2.5 25 .5LO .0 68.0 170.1

/1 Provided for by separate loan.

/2 Excludes estimated US$1 million in related studies expected to befinanced by UNDR.

/3 Including US$1.1 million from other loans. The dollar equivalent of theEIB loan has been assumed at US$24.4 million. Fluctuations in exchangerates, however, have at least at the moment lowered the dollar equivalentof the EIB unit of account. The Government will cover related shortfallsin dollar value if they in fact occur.

External borrowings from EIB and the Bank of together US$64.4 million equiv-alent will amount to about 38% and 95% of total financing and foreign exchangerequirements respectively. Additionally, US$1.1 million will be providedfrom EIB country funds, allocated for studies. 'The allocation of funds fromthe EIB and the Bank are discussed in para 5.17.

D. Allocation of Bank Loan and Disbursements

5.16 A more detailed description of the goods and services for which theBank loan of US$40.0 million will be used is given in Annexes 10 and 11 andsummarized below separately for each of the three project parts.

- 22 -

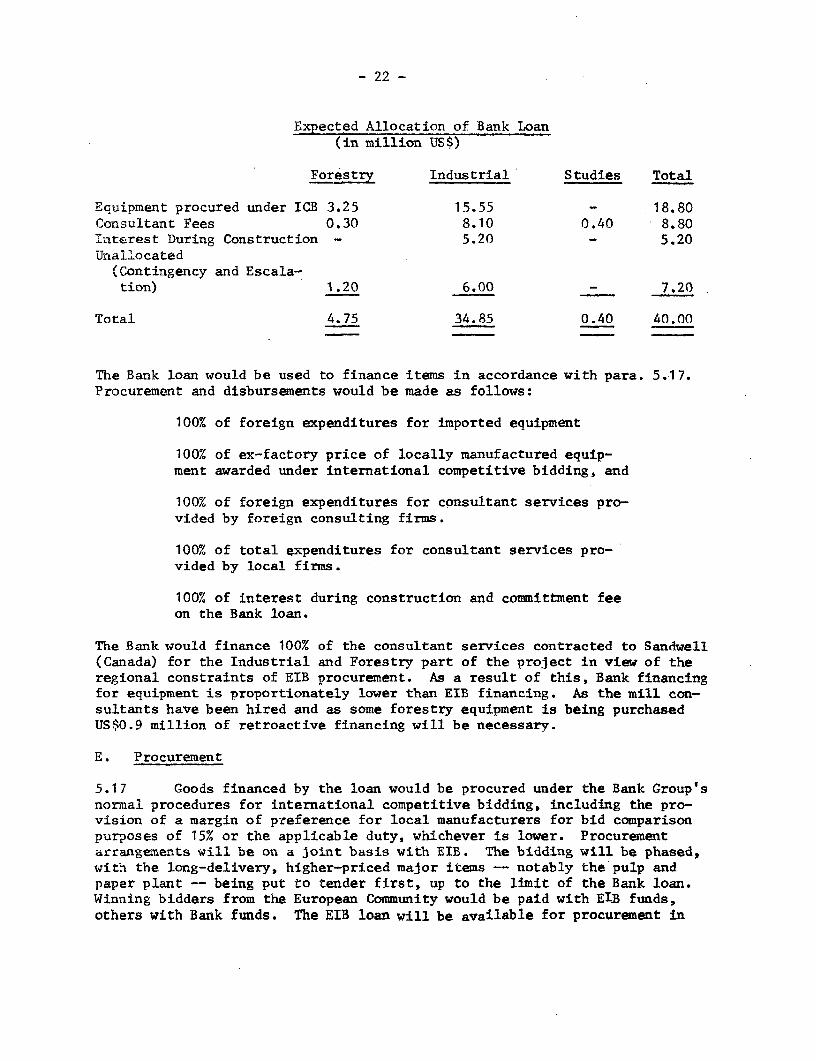

Expected Allocation of Bank Loan(in million US$)

Forestry Industrial Studies Total

Eauipment procured under ICB 3.25 15.55 - 18.80Consultant Fees 0.30 8.10 0.40 8.80Interest During Construction - 5.20 - 5.20Unallocated(Contingency and Escala-tion) 1.20 6.00 - 7.20

Total 4.75 34.85 0.40 40.00

The Bank loan would be used to finance items in accordance with para. 5.17.Procurement and disbursements would be made as follows:

100% of foreign expenditures for imported equipment

100% of ex-factory price of locally manufactured equip-ment awarded under international competitive bidding, and

100% of foreign expenditures for consultant services pro-vided by foreign consulting firms.

100% of total expenditures for consultant services pro-vided by local firms.

100% of interest during construction and committment feeon the Bank loan.

The Bank would finance 100% of the consultant services contracted to Sandwell(Canada) for the Industrial and Forestry part of the project in view of theregional constraints of EIB procurement. As a result of this, Bank financingfor equipment is proportionately lower than EIB financing. As the mill con-sultants have been hired and as some forestry equipment is being purchasedUS$0.9 million of retroactive financing will be necessary.

E. Procurement

5.17 Goods financed by the loan would be procured under the Bank Group'snormal procedures for international competitive bidding, including the pro-vision of a margin of preference for local manufacturers for bid comparisonpurposes of 15% or the applicable duty, whichever is lower. Procurementarrangements will be on a joint basis with EIB. The bidding will be phased,with the long-delivery, higher-priced major items -- notably the pulp andpaper plant - being put to tender first, up to the limit of the Bank loan.Winning bidders from the European Community would be paid with EIB funds,others with Bank funds. The EIB loan will be available for procurement in

- 23 -

the Six founder members rather than the Nine since ratification of the entryon the new members has not been completed. As bidding proceeds - should itbecome evident that EIB's loan could not be fully utilized during the firstphase, then in the second phase certain goods would be restricted to biddingwithin the Six only, to make sure that all EIB funds will be utilized. Costpenalties, if any, on account of such restrictive bidding should be minor,since there would still be adequate competition among Community suppliers.A Loan Administration Agreement under which procedures for bidding, disburse-ments and supervision will be establ:Lshed has been agreed upon between theBank and EIB.

- 24 -

VI. PROJECT IMPLEMENTATION

A. Forestry Part

6.01 The Antalya Forestry Division, will have prime responsibility forthe day-to-day implementation of this part of the project; it will be assistedby the GDF head office staff in Ankara in overall policy planning and thesupply of particular technical expertise. Although not on the same scale,the Antalya Forestry Division has been confronted with similar tasks in thepast and is therefore judged to be capable of executing the primarily physicalpart of the forestry project, i.e. increasing the wood supply for the Antalyamill within a relatively short period of time.

6.02 However, outside assistance is needed for meeting the other objec-tive of the project, namely to help reform an existing forestry operation intoone with a more aggressive approach towards forest management. To this end,4-6 experienced Turkish foresters assisted by two foreign forestry consul-tants will form the nucleus of a Project Implementation Team, which is intendedto be in existence for the next 6-7 years although the expatriates would com-plete most of their work within 2 years. The Team's basic task will be toprepare detailed forest management plans for the Antalya region. Initially,it will work out a 5-year development and operations plan, laying down the over-all objectives to be achieved, to be followed up subsequently with more de-tailed annual operating plans and instructions. In addition, the Team willprepare a 20-year plan, setting out the principal objectives of how the region'sforests should be developed and managed to maximize their yield in the longerterm. The Government will cause the MF/GDF to enter into agreements satisfac-tory to the Bank to hire the consultants and establish the Project Implemen-tation Team and prepare and implement a forest development plan.

B. Industrial Part

6.03 The execution of the pulp, paper and sawmills will be the respon-sibility of The Establishment assisted to a large degree by SEKA. Theproject manager has already been appointed - he was the general managerof the Caycuma mill and has considerable experience in project constructionas well as operations. As the project and general manager, he will be re-sponsible to an administrative committee, which will consist of the Chairmanand three members who all belong to SEKA's top management and form the linkbetween The Establishment and SEKA as parent company. Apart from major pol-icy decisions, The Establishment will have the authority to execute and op-erate this part of the project. Execution will follow a critical path sched-ule to be established.

6.04 Sandwell & Co. has been engaged to help in the implementation ofthe project. The contract has been reviewed by Bank and EIB staff and foundto be satisfactory. Sandwell's first task will be to finalize the design ofthe project and prepare a detailed construction budget and time schedule forthe project execution. Subsequently, Sandwell will have prime responsibility

- 25 -

for detailed design, procurement of equipment through all stages, the obtain-ing of subcontract services for civil, structural, erection, mechanicaland electrical work on site, and the preparation and issuance of controldocumentation to monitor progress of the project. All Sandwell's work willbe done in close cooperation with The Establishments staff and a field officewill be established at The Establishment's plant site, as well as a liaisonoffice at SEKA's headquarters at Izmit.

6.05 Soon after construction commences and within the same consultantcontract, a program of operational assistance would be started, which willlast from about 2 years before until about 6 months after commencement ofplant operations. Some 20 key expatriate personnel will be provided to estab-lish the operational organization, develop detailed work programs for thestart-up operation of the mills, run training programs and prepare operatingnanuals. They will have line responsibility for plant operation initially,training local counterparts to take their places as soon as possible.

6.06 To strengthen the Antalya operation, The Establishment will by June30, 1974 undertake and implement appropriate recommendations of studies todetermine the optimum method of wood transport to the plant; to determine thebest marketing methods for the distribution of its products, particularlysawnwood, which is new to SEKA Establishments; and of Turkey's capacity toproduce corrugating medium and corrugated containers.

C. Studies Part

6.07 The studies to be financed by the UNDP, the EIB and the Bank willbe defined and implementation machinery established by the three institutionsand the Government during the first half of 1974 (paras 3.13 and 3.15 andAnnex 6).

D. Role of State Investment Bank (SIB)

6.08 The State Investment Bank (SIB) would be a co-lender for the indus-trial part of the project and would disburse all loan funds to The Establish-ment. The proposed Bank and EIB funds would be lent to the Government whowould onlend them to SIB who in turn would onlend them to The Establishment.A subsidiary loan agreement between the Government, SIB, SEKA and The Estab-lishment will be entered into in form and substance satisfactory to the Bank.The arrangements with SIB serve two purposes: they will provide a singlechannel for all loan funds to The Establishment, and they will help establishan initial working relationship between SIB and the Bank in preparation forpossible future lending to SIB. A detailed description of SIB and its rolein the project is given in Annex 12.

6.09 SIB has been playing an increasingly important role in providinglong-term finance needed by the State Economic Enterprises (SEEs). Its con-tribution has exceeded 20% of the total investments in the SEEs recently.In 1973, SIB is expected to provide TL 4.2 billion against a total require-ment of TL 13.7 billion by the SEEs. The resources of SIB are provided mainlyfrom tax free bond issues, but also from equity contributions and advancesfrom the Government as well as loan repayments.

- 26 -

6. O SIB's organization, policies and procedures are generally soundgiven the constraints faced by the public sector entities in Turkey. SIBstaff are competent and its management shows initiative, drive and readinessto take on new activities. SIB will provide in its bookkeeping and financialreporting system for separate treatment of the proceeds of the Bank and EIBloans, and strengthen nroject appraisal and supervision to meet the requirementsof its rapidly increasing lending volume.

VII. FINANCIAL ANALYSIS

A. Forestry Part

7.01 The Antalya Forestry Division derives revenues from the sale of itswood products - firewood, sawlogs, pulplogs, mine props, etc. - and othermaterial such as pine resin. It uses the revenue to cover its operatingcosts - mostly labor and transportation - to meet various contributions tothe MF as support for its nationwide programs, to pay income taxes, and toput aside a depreciation reserve for equipment replacements. The AntalyaForestry Division's production plan, operating costs and investment costsare coordinated with the GDF and become part of the Annual Revolving Fund(para. 2.09) which is consolidated on a national basis.

7.02 The projected revenues and costs of the Antalya Forestry Divisionare shown in detail in Annex 13 and are summarized below.

Projected Revenues and Costs for Antalya Forestry Division(in million TL)

1973 1974 1975 1976 1977 1978 1979 1980 1981 1982

Production ofwood in 00'm3 342 350 393 491 630 750 815 811 805 805

Revenues /1 131 123 149 184 231 267 277 270 267 267

Operating Costs 130 162 179 191 213 209 203 197 195 193

Income Tax - - - - - - 28 29 28 29

Net lucomeAfter Taxes 1 (39) (30) (7) 18 58 46 44 44 45

Cash Flow 1 (13) 1 27 56 85 89 85 81 81

/1 Revenues from 1978 onwards do not increase in direct proportion to theproduction volume because an increasing proportion of pulpwood is produced.

- 27 -

The projections have been prepared at constant prices prevailing in Turkeyin 1972. However, given the worldwide trend of increasing wood prices, therevenue/cost margin is expected to widen since operating costs are not ex-pected to increase to the same extent as wood prices. Even on the conserva-tive assumption of constant prices, income and cash flow statements for theforestry activities of the project show that the Antalya Forestry Divisionwill have operating losses only from 1974 to 1976 while it builds up itsproduction activities. However, from 1976 net income and cash generationis expected to greatly improve leading to substantial cash surpluses tocover all replacement investments.

7.03 The biggest source of revenues (about 63%) for the Antalya ForestryDivision will be the sales to The Establishment; they will be based on along-term wood supply contract, discussed in para. 7.06. The costs aredominated by direct operational costg, particularly the forest maintenance(reforestation, afforestation, erosion contr5l, fire protection) productionand transportation. In 1982, some 800,000 m of wood are expected to be 3 pro-duced. jnit production costs - before income taxes - are about 250 TL/m(US$18/m ) which compares favorably with cost in other parts of the world.

7.04 Given the strong expected cash position, the Antalya ForestryDivision should not need to call on outside funds for operations andinvestments after 1977 but should become a net contributor to its Ankaraheadquarters even if notional debt service payments are allocated to theAntalya Forestry Division. The financial return of the forestry part ofthe project on an increcremental basis is 24%.

B. Industrial Part

1. Revenues and Operating Costs

7.05 A detailed description of the assumptions for revenues and operat-ing costs is given in Annex 14 and the major findings are discussed below.