WEEKLY REPORT Soybean - Portal - MarketIntelligence · WEEKLY REPORT FCStone do Brasil ......

6

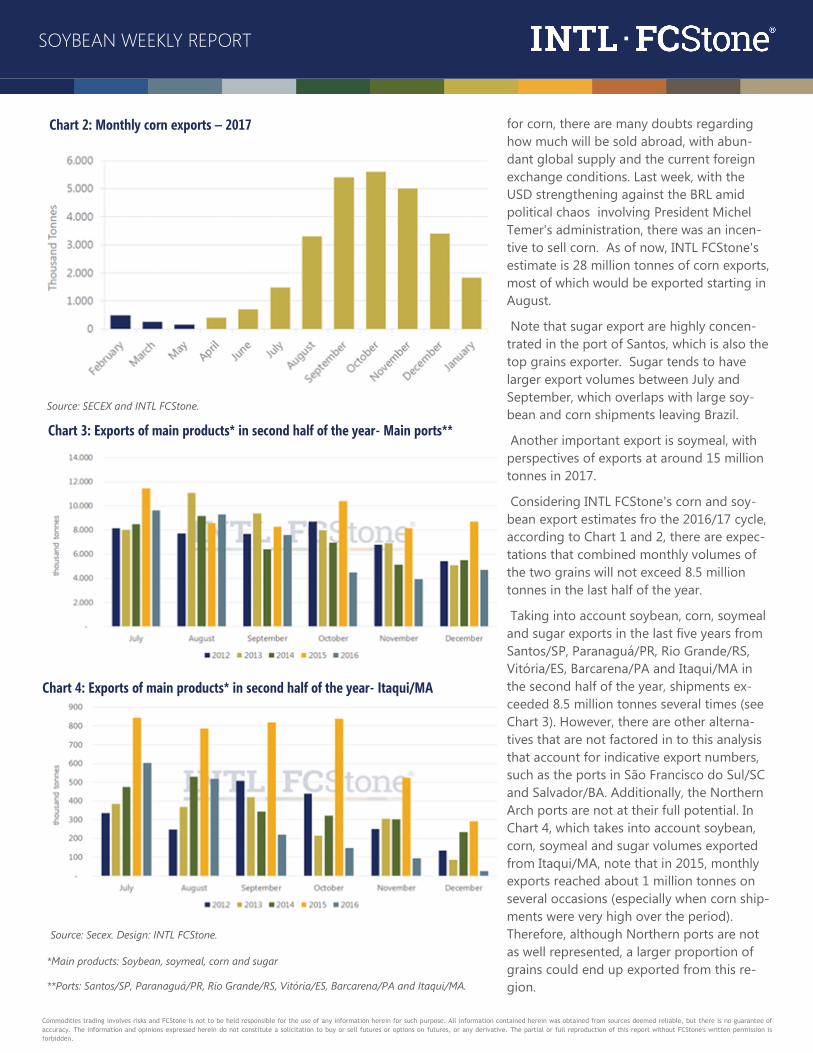

Soybean WEEKLY REPORT FCStone do Brasil Consultoria em Futuros e Commodities Commodities trading involves risks and FCStone is not to be held responsible for the use of any information herein for such purpose. All information contained herein was obtained from sources deemed reliable, but there is no guarantee of accuracy. The information and opinions expressed herein do not constitute a solicitation to buy or sell futures or options on futures, or any derivative. The partial or full reproduction of this report without FCStone's written permission is forbidden. by Rafael Morais [email protected] Even with soybean and corn exported in the same period, ports should not have problems Looking Brazilian soybean and corn exports exhibited reverse seasonality While most soy- beans are shipped in the first half of the year, corn is mostly exported in the second half, after the safrinha harvest. In 2017, there are expectations of record soybean, around 60 million tonnes, according to INTL FCStone estimates. From the beginning of January to May 18, 30.7 million tonnes of soybean were shipped, according to official data from SECEX ( Foreign Trade Secretariat). Considering available line-up data, there are more than 5 million tonnes scheduled to de- part, and with the USD up against the BRL since last week, trades are getting a boost, which tends to increase shipments. Within this context, soybean exports should total around 43 million tonnes by the end of June, with 17 million tonnes departing in the second half of 2017, especially since exports could increase even more. Therefore, soybean exports could compete with other commodities for export at ports. As May 29, 2017 Edition No. 392 Even with soybean and corn exported in the same period, ports should not have problems Harvest exceeds 79% of planted area in Argentina Soybean declines with US planting and lower oil prices Chart 1: Monthly soybean exports – 2017 Source: SECEX and INTL FCStone.

Transcript of WEEKLY REPORT Soybean - Portal - MarketIntelligence · WEEKLY REPORT FCStone do Brasil ......

Soybean WEEKLY REPORT

FCStone do Brasil

Consultoria em Futuros e Commodities

Commodities trading involves risks and FCStone is not to be held responsible for the use of any information herein for such purpose. All information contained herein was obtained from sources deemed reliable, but there is no guarantee of

accuracy. The information and opinions expressed herein do not constitute a solicitation to buy or sell futures or options on futures, or any derivative. The partial or full reproduction of this report without FCStone's written permission is

forbidden.

by Rafael Morais

Even with soybean and corn exported in the same period, ports should

not have problems

Looking Brazilian soybean and corn exports exhibited reverse seasonality While most soy-

beans are shipped in the first half of the year, corn is mostly exported in the second half,

after the safrinha harvest.

In 2017, there are expectations of record soybean, around 60 million tonnes, according to

INTL FCStone estimates. From the beginning of January to May 18, 30.7 million tonnes of

soybean were shipped, according to official data from SECEX ( Foreign Trade Secretariat).

Considering available line-up data, there are more than 5 million tonnes scheduled to de-

part, and with the USD up against the BRL since last week, trades are getting a boost, which

tends to increase shipments. Within this context, soybean exports should total around 43

million tonnes by the end of June, with 17 million tonnes departing in the second half of

2017, especially since exports could increase even more.

Therefore, soybean exports could compete with other commodities for export at ports. As

May 29, 2017

Edition No. 392

Even with soybean and

corn exported in the

same period, ports

should not have

problems

Harvest exceeds 79% of

planted area in

Argentina

Soybean declines with

US planting and lower

oil prices

Chart 1: Monthly soybean exports – 2017

Source: SECEX and INTL FCStone.

Commodities trading involves risks and FCStone is not to be held responsible for the use of any information herein for such purpose. All information contained herein was obtained from sources deemed reliable, but there is no guarantee of

accuracy. The information and opinions expressed herein do not constitute a solicitation to buy or sell futures or options on futures, or any derivative. The partial or full reproduction of this report without FCStone's written permission is

forbidden.

SOYBEAN WEEKLY REPORT

for corn, there are many doubts regarding

how much will be sold abroad, with abun-

dant global supply and the current foreign

exchange conditions. Last week, with the

USD strengthening against the BRL amid

political chaos involving President Michel

Temer's administration, there was an incen-

tive to sell corn. As of now, INTL FCStone's

estimate is 28 million tonnes of corn exports,

most of which would be exported starting in

August.

Note that sugar export are highly concen-

trated in the port of Santos, which is also the

top grains exporter. Sugar tends to have

larger export volumes between July and

September, which overlaps with large soy-

bean and corn shipments leaving Brazil.

Another important export is soymeal, with

perspectives of exports at around 15 million

tonnes in 2017.

Considering INTL FCStone's corn and soy-

bean export estimates fro the 2016/17 cycle,

according to Chart 1 and 2, there are expec-

tations that combined monthly volumes of

the two grains will not exceed 8.5 million

tonnes in the last half of the year.

Taking into account soybean, corn, soymeal

and sugar exports in the last five years from

Santos/SP, Paranaguá/PR, Rio Grande/RS,

Vitória/ES, Barcarena/PA and Itaqui/MA in

the second half of the year, shipments ex-

ceeded 8.5 million tonnes several times (see

Chart 3). However, there are other alterna-

tives that are not factored in to this analysis

that account for indicative export numbers,

such as the ports in São Francisco do Sul/SC

and Salvador/BA. Additionally, the Northern

Arch ports are not at their full potential. In

Chart 4, which takes into account soybean,

corn, soymeal and sugar volumes exported

from Itaqui/MA, note that in 2015, monthly

exports reached about 1 million tonnes on

several occasions (especially when corn ship-

ments were very high over the period).

Therefore, although Northern ports are not

as well represented, a larger proportion of

grains could end up exported from this re-

gion.

Chart 2: Monthly corn exports – 2017

Source: SECEX and INTL FCStone.

Chart 3: Exports of main products* in second half of the year- Main ports**

Chart 4: Exports of main products* in second half of the year- Itaqui/MA

Source: Secex. Design: INTL FCStone.

*Main products: Soybean, soymeal, corn and sugar

**Ports: Santos/SP, Paranaguá/PR, Rio Grande/RS, Vitória/ES, Barcarena/PA and Itaqui/MA.

Commodities trading involves risks and FCStone is not to be held responsible for the use of any information herein for such purpose. All information contained herein was obtained from sources deemed reliable, but there is no guarantee of

accuracy. The information and opinions expressed herein do not constitute a solicitation to buy or sell futures or options on futures, or any derivative. The partial or full reproduction of this report without FCStone's written permission is

forbidden.

SOYBEAN WEEKLY REPORT

Therefore, the more soybean exports ex-

tend into the second half of the year, poten-

tially exceeding 60 million tonnes in total,

the risk of overcrowding at ports is very low.

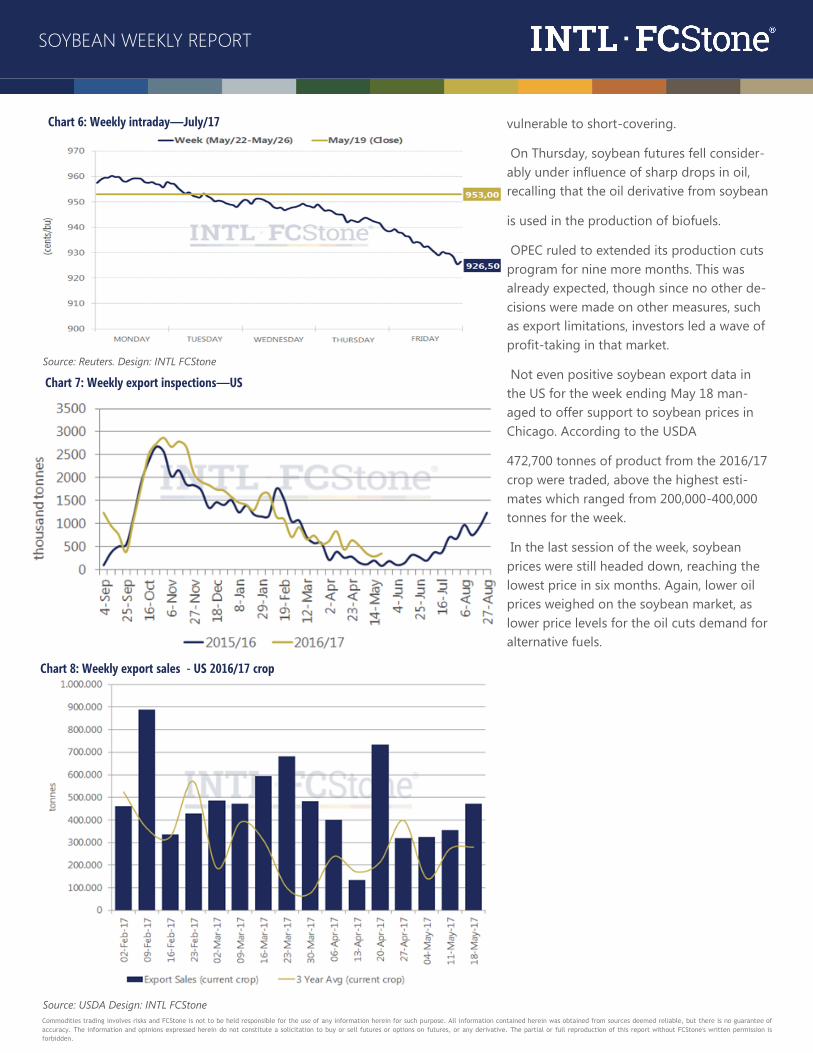

Harvest exceeds 79% of planted area in

Argentina

On Wednesday (24) the Argentinian Cereals

Exchange updated its crop follow-up report.

As observed in Chart 5, soybean harvesting

reached 79.6% of planted area, which equals

a 4.9 p.p. increase from the previous week.

As observed for the past four weeks, field

work is still ahead of the 2015/16 cycle with

average yields of 3.27 tonnes per hectare at

this time.

However, even with these positive results on

plantations, there are concerns over the pos-

sibility of losses due to excess moisture in

some areas in Argentina's primary agricul-

tural regions, such as Buenos Aires and La

Pampa provinces.

Despite this apprehension, the Cereals Ex-

change maintained its production estimate

for the 2016/17 crop at 57 million tonnes. If

this number is confirmed in coming weeks,

there would be an expansion of 2.7 p.p.

compared to last year for Argentinian soy

production.

Soybean week in Chicago

Soybean declines with US planting and lower

oil prices

In the second-to-last week of May, corn

prices in Chicago were down again amid

good planting progress in the US despite

weather concerns and falling oil prices over

the week. The July contract closed Friday

(26) priced at US$ 9.265 per bushel.

In the first session of the week, soybean

contracts were up amid US weather con-

cerns with possible delays in planting for

the next crop.

In addition, weekly export inspections were

published. Up through May 18, shipments

reached 348,500 tonnes (see Chart 7), within

estimates, which varied between 250,000

and 400,000 tonnes.

At the end of the afternoon, the USDA re-

leased its weekly crop follow-up report for

the US. Soybean crop planting was 53%

complete as of Sunday (21), slightly above

the five-year average and in line with the

same period last year.

With good planting progress, prices were

down at the end of Tuesday. Investors' profit

-taking also contributed to this movement.

In a session with more limited change, soy

closed Wednesday nearly stable. Worries

over weather and excess moisture in US

fields still linger, though the soybean market

had increased short positions, which left it

Chart 5: Crop follow-up - Argentina

Source: USDA. Design: INTL FCStone

Source: Reuters Design: INTL FCStone

Commodities trading involves risks and FCStone is not to be held responsible for the use of any information herein for such purpose. All information contained herein was obtained from sources deemed reliable, but there is no guarantee of

accuracy. The information and opinions expressed herein do not constitute a solicitation to buy or sell futures or options on futures, or any derivative. The partial or full reproduction of this report without FCStone's written permission is

forbidden.

SOYBEAN WEEKLY REPORT

vulnerable to short-covering.

On Thursday, soybean futures fell consider-

ably under influence of sharp drops in oil,

recalling that the oil derivative from soybean

is used in the production of biofuels.

OPEC ruled to extended its production cuts

program for nine more months. This was

already expected, though since no other de-

cisions were made on other measures, such

as export limitations, investors led a wave of

profit-taking in that market.

Not even positive soybean export data in

the US for the week ending May 18 man-

aged to offer support to soybean prices in

Chicago. According to the USDA

472,700 tonnes of product from the 2016/17

crop were traded, above the highest esti-

mates which ranged from 200,000-400,000

tonnes for the week.

In the last session of the week, soybean

prices were still headed down, reaching the

lowest price in six months. Again, lower oil

prices weighed on the soybean market, as

lower price levels for the oil cuts demand for

alternative fuels.

Chart 6: Weekly intraday—July/17

Source: Reuters. Design: INTL FCStone

Chart 7: Weekly export inspections—US

Chart 8: Weekly export sales - US 2016/17 crop

Source: USDA Design: INTL FCStone

Commodities trading involves risks and FCStone is not to be held responsible for the use of any information herein for such purpose. All information contained herein was obtained from sources deemed reliable, but there is no guarantee of

accuracy. The information and opinions expressed herein do not constitute a solicitation to buy or sell futures or options on futures, or any derivative. The partial or full reproduction of this report without FCStone's written permission is

forbidden.

SOYBEAN WEEKLY REPORT

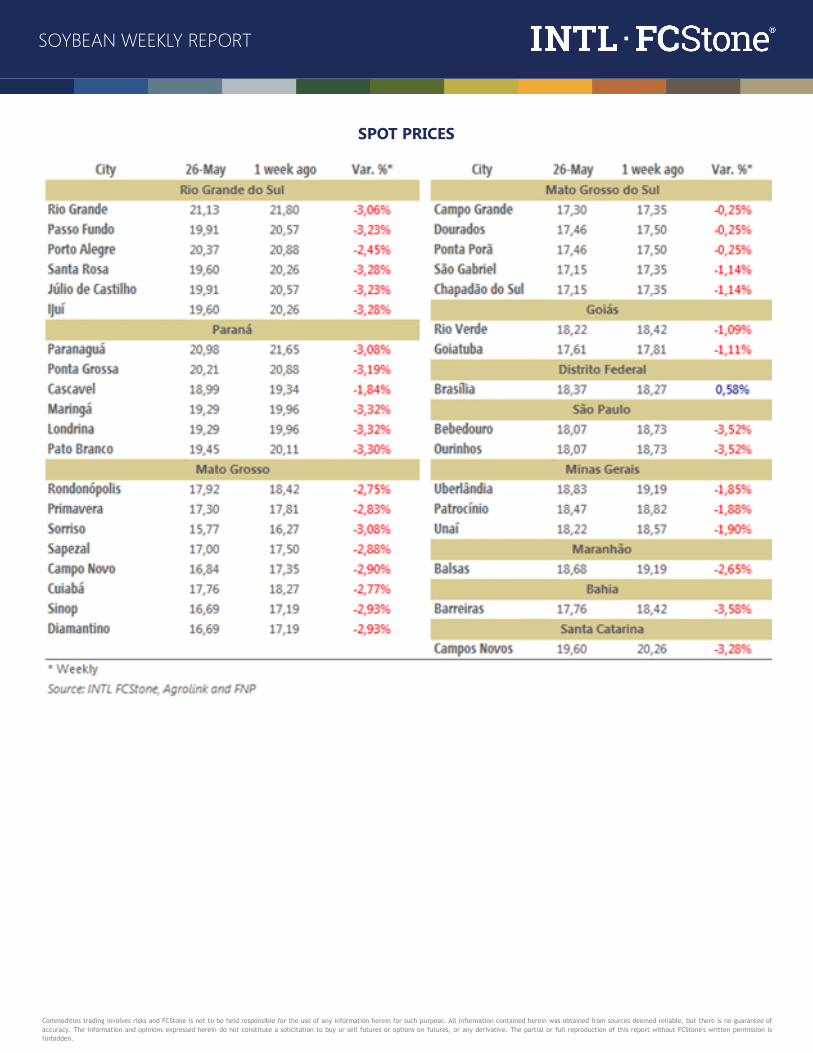

SPOT PRICES

Commodities trading involves risks and FCStone is not to be held responsible for the use of any information herein for such purpose. All information contained herein was obtained from sources deemed reliable, but there is no guarantee of

accuracy. The information and opinions expressed herein do not constitute a solicitation to buy or sell futures or options on futures, or any derivative. The partial or full reproduction of this report without FCStone's written permission is

forbidden.

SOYBEAN WEEKLY REPORT

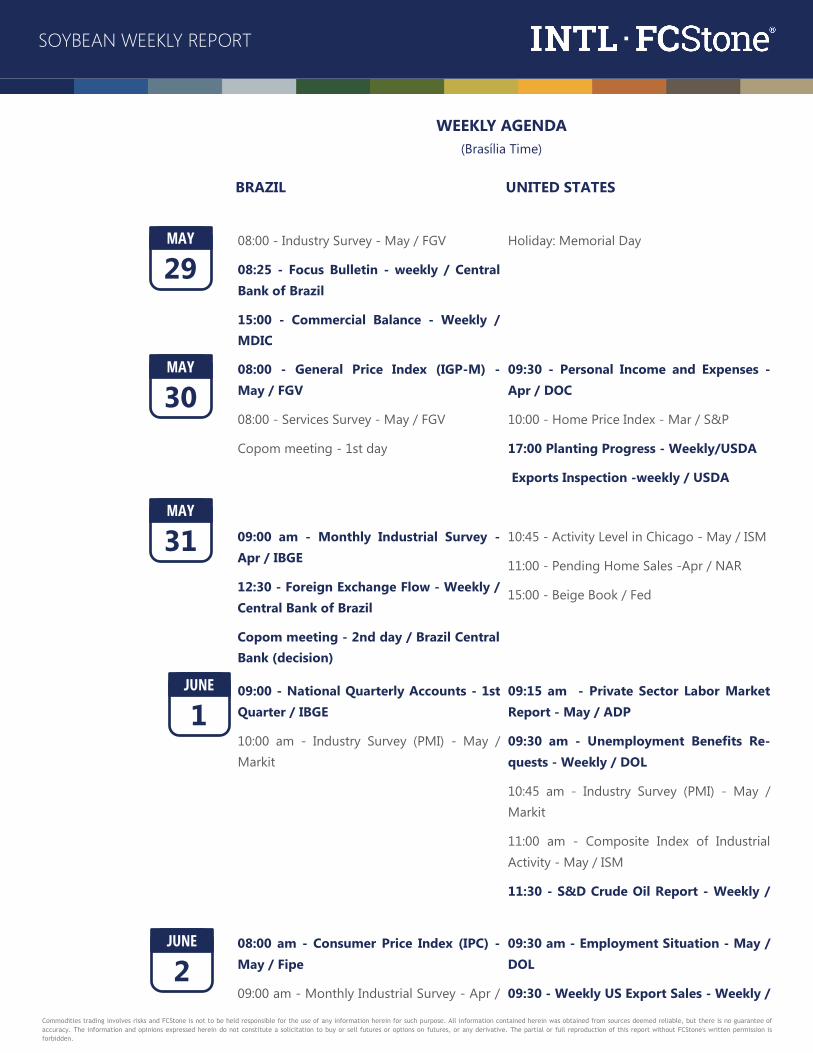

MAY

29

MAY

30

MAY

31

JUNE

1

JUNE

2 09:30 am - Employment Situation - May /

DOL

09:30 - Weekly US Export Sales - Weekly /

08:00 am - Consumer Price Index (IPC) -

May / Fipe

09:00 am - Monthly Industrial Survey - Apr /

08:00 - Industry Survey - May / FGV

08:25 - Focus Bulletin - weekly / Central

Bank of Brazil

15:00 - Commercial Balance - Weekly /

MDIC

Holiday: Memorial Day

08:00 - General Price Index (IGP-M) -

May / FGV

08:00 - Services Survey - May / FGV

Copom meeting - 1st day

09:30 - Personal Income and Expenses -

Apr / DOC

10:00 - Home Price Index - Mar / S&P

17:00 Planting Progress - Weekly/USDA

Exports Inspection -weekly / USDA

09:00 am - Monthly Industrial Survey -

Apr / IBGE

12:30 - Foreign Exchange Flow - Weekly /

Central Bank of Brazil

Copom meeting - 2nd day / Brazil Central

Bank (decision)

10:45 - Activity Level in Chicago - May / ISM

11:00 - Pending Home Sales -Apr / NAR

15:00 - Beige Book / Fed

09:00 - National Quarterly Accounts - 1st

Quarter / IBGE

10:00 am - Industry Survey (PMI) - May /

Markit

09:15 am - Private Sector Labor Market

Report - May / ADP

09:30 am - Unemployment Benefits Re-

quests - Weekly / DOL

10:45 am - Industry Survey (PMI) - May /

Markit

11:00 am - Composite Index of Industrial

Activity - May / ISM

11:30 - S&D Crude Oil Report - Weekly /

WEEKLY AGENDA

(Brasília Time)

UNITED STATES BRAZIL