Wave 1 - Web 2.0 The Global Impact | UM | Social Media Tracker

-

Upload

um-wave -

Category

Social Media

-

view

255 -

download

1

Transcript of Wave 1 - Web 2.0 The Global Impact | UM | Social Media Tracker

Web 2.0: The Global ImpactStudy by Universal McCann Dec 2006

A welcome note

Universal McCann's global research into the impact ofWeb 2.0 on frequent Internet users is the largestexploration of its kind. Interviews from more than 16,000online users worldwide has for the first time allowed a trueworld-wide perspective into to key trends associated withthe changing Internet. This research focuses on levels ofpenetration, the differences by market and the potentialuniverse sizes of Web 2.0 technologies, platforms andapplications; exploring 3 key areas:

Creation: Blogging, social networks, photo sharing, Wiki's,social news sites and writing comments, reviews andfeedback have all fundamentally changed the web,providing consumers with the tools to drive thecontent agenda.

Connection: Social networking, personal blogging, instantmessenger and VOIP are all playing a role to revolutioniseand globalise the way we interact, stay in touch and meetnew people.

Entertainment: Thanks to the unstoppable rise ofbroadband - video, audio, live TV and radio are all centralto the way we use the web today.

The results are staggering. From a global perspective Web2.0 applications and technology are being adopted inimmense numbers with hundreds of millions creating andsharing their own content, socialising and communicatingregardless of local culture, demographic, economicdevelopment or local Internet penetration.There are 40m+ active bloggers, 100m+ blog readersin the markets surveyed.

Asia is at the forefront of many aspects of Web 2.0adoption; in particular user generated content wherepersonal blogging is an obsession for millions across theregion. China leads the world, where despite decades ofmedia oppression, millions of Chinese consumers areusing blogging platforms to express themselves in waysunthinkable in years gone by.

This research confirms what marketers, advertisers andmedia owners should already know. The changing internetis radically altering user's media habits the world over;irreversibly altering the media and communicationsenvironment by driving globalisation of mediaconsumption, mega fragmentation of media channels andcreating a truly international social network. These arereal challenges that brands and media companiesregardless of country must face up to now -not in ten years time.

This research is an ongoing commitment, tracking theadoption of Web 2.0 platforms and technologies from aglobal perspective, understanding the evolving impact ofthe changing internet. To contact me regarding this andfuture research please email:

3Global Web 2.0 Research

Introduction

Over the last 18 months the term “Web 2.0” has firmlyentered the mainstream consciousness of the online world;however the definition and even its existence as a concepthave been hotly disputed. We like to define it in the simplest of terms: “an evolution of the internet to becomea network of interconnected web pages and applicationsthat encourage consumer participation, creativity and interaction”.

The really important point behind Web 2.0, particularly foradvertisers, marketers and media owners is not the nameor the definition, but the impact. It is clear that theserecent online developments have the potential to transformthe media landscape quicker than at any other time inhistory. The technologies commonly associated with Web2.0 such as social networking, RSS, tagging, blogging,aggregators, and Wiki's, coupled with the explosion of broadband enabled services like Instant Messenger, IPTV,Podcasting and VOIP (see glossary for more information)mean it has never been easier to create and share content, meet people and enjoy a personalised multimediaexperience. The tools and channels to create and sharevideo, images and the written word have never before been as accessible or democratic - never before has therebeen a completely open media and communication platform available for everyone to contribute to. Controlledmedia distribution channels, the need for funding, lack ofaccess to production technology and the need for industrycontacts have all been eroded as barriers to becoming a‘media owner’. The only barrier today is a willingness tocreate. The potential is clear - if consumers want to theycan be the lead creators of media content.

Of course the hype has been huge; Newspapers the worldover proclaim the ‘Citizen Journalist’, investors push hugesums of money into online start ups, while establishedmedia companies desperately try to grab a piece of the action.It’s hard not get caught up in the hype; Technorati claim52 million blogs in existence, with 75,000 added eachday, Youtube stream in excess of 3 billion videos amonth and MySpace recently breached the 100 millionmembers mark. The media, advertising and communicationsenvironment shows all the signs of changing as quickly as hype.

To understand the real impact, Universal McCann implemented a global study into the adoption of Web 2.0 tools, sites and services to assess the extent towhich consumers are getting involved, establish howthey are adopting and identify the country by countrydifferences. The results form the basis for the explorationof Web 2.0 that follows, considering the impact for mediaowners, advertisers and marketers the world over.

4Key findings

•Web 2.0 technologies have made a global impact. o Internet users in every country are adopting

Web 2.0 applications, platforms and mediain vast numbers.

o In some markets the numbers of users may besmall, but on a global level all these technologiesare huge. •Adoption does not follow traditional economic lines -

online users in less developed markets are as involvedas developed ones, in many cases more involved.o Asia leads the way - the top 5 markets in terms of

adopting Web 2.0 services are China, South Korea,Malaysia, Hong Kong and the Philippines.

o Spain, Italy and France are driving the Westernworld's usage, up there with Asia in adoption terms.

o This is far from being just a US phenomenon asoften assumed. The sheer size of the US marketoften masks lower than average adoption rates.

o China is vying with the US as the largest volumemarket for the adoption of Web 2.0 technologies,platforms and applications. •There are clear global trends in the adoption of

different technologies. If you were to order technologiesin terms of popularity it would be as follows: o 1 - Instant Messenger 2 - Reviewing products and

services / leaving feedback 3 - Photo Sharing 4 - Streaming live media 5 - Reading Blogs 6 - Watching video clips on demand 7 -Social Networking 8 - Creating a Blog 9 - VOIP 10 -RSS 11 - Podcasting

o Generally speaking Asia is the most actively involvedin content creation and sharing thanks to theirpassion for personal blogging while Europe and theUS lead with entertainment and social networking.

o The differences between the regions is magnifiedwhen looking at blogging: In Asia personal bloggingis key, interacting with your social group, while inUS and Europe its more about individuals makingtheir opinion heard - often on a broad rang of topics. •The large scale global adoption of Web 2.0 means

the impact of these technologies is massive, not just for media, advertising and telecoms butfor wider society and culture. Their role in theinter-connectedness of the world is huge and ishelping to fuel a global culture of sharing. Technologiessuch as photo sharing, video platforms, instant messenger, VOIP and social networking are truly international and being used everywhere world-wide. •Media distribution platforms and consumption of multimedia content is moving to become more globalin outlook, or developing along language lines asopposed to market lines - marketing, advertising andbranding will have to follow to stay relevant.

5Methodology

Figure 1: 16-44 Online Universe - Frequency users V Non FrequentSource: TGI Europa / TGI Russia / Simmons / Media in Mind / SynovateAsiaPacific Media Handbook / Nielsen Media Index

.

USA

60% of the world’s Internet Population

France,Germany,

Italy, Spain,UK, Russia

ChinaHong KongPhilippines

Thailand

MalaysiaSingapore

Australia

South Korea

The research was conducted amongst a representativesample of frequent internet users (Use the internet everyday / every other day), who in general now make up the majority of the online universe particularly in developed markets (see Figure1). These users are bestplaced to demonstrate consumer uptake of Web 2.0 services. They are the vast majority of adopters of new products and services online and will be themajority of Web 2.0 adopters.

The study took place between March and September 2006 in mix of 15 highly developed and emerging internet markets; France, Germany, Italy, Spain, Russia, UK, US,China, South Korea, Thailand, Malaysia, Hong Kong,Singapore, Philippines and Australia. Combined they make up 60% of the global Internet universe: In every market the sample is representative to the 16-44frequent internet user population with the research con-ducted online. Respondents were provided by Ciao

European Media Panel, Insight Express in the US and localmedia partners in Asia. Unsurprisingly (Figure 1) relativenumbers by market differ hugely both in size and overallpenetration of online - however it is clear that frequentusage is becoming the norm. It also worth reflecting onthese numbers for the results that follow and the relativesizes of the universes that the results indicate.All universe size estimates are based upon applying thepercentages in the survey to the latest universe sizes thatexist from industry surveys such as TGI and Simmons.As the research audience makes up 60% of frequentonline world for 16-44's and as there are consistencies intechnology adoption, it allows for robust estimations on theglobal reach of these technologies. It should also beconsidered that some Internet markets are less maturethan others and so tend to have a younger, male skew,whereas markets such as the US, UK, France and SouthKorea are more established tend to have normalisedprofiles. This can be a factor in overall penetration of services.

7Creating and sharing content

Blogging

One of the most exciting outcomes of Web 2.0 is thepossibility for web users to create and share their owncontent. It has never been easier to create the writtenword, photos, video and music; sharing with friends,family and the wider world. In the past it was possible,but it took technical knowledge and determination, preventingthese activities from entering the mainstream. Today, thanksto blogging platforms like Typepad, Blogcn.com and SkyBlog; social network sites like Myspace, Bebo and Cyworld;video sharing sites such as Youtube.com, Guba and Revverand photo sharing sites like Flickr, Webpics and Picassa -creating and sharing content has never been simpler.Web 2.0 has made media ownership possible for allpropelling it to the mainstream.

Blogging

Blogging has been at the epicentre of the Web 2.0movement typifying the rise of the shift towards consumercontent. Over the past couple of years there has been anexplosion of blogs covering every topic imaginable.Companies and media organisations have begun tointegrate blogging into their online activities; however itis consumer usage that is really exciting, and promisesthe biggest potential to shake up the media landscape.The ever expanding blogosphere has whipped up a feverof hype about the emergence of the ‘Citizen Journalist’and the flipping of the media world from top down tobottom up, with consumers leading the news agenda.So is this hype justified?

Blogs - “A regularly updated website in which items are posted in reverse chronological order, known as Blogs or Weblogs the act of postingstories is known as Blogging. Blogs usually focus on one subject - a typical Blog will contain stories in a diary format, pictures, links to other Blogs and web pages and willorganise content by category and month ofposting. The collective universe of blogs is often referred to as the blogosphere”

8Creating and sharing content

Blogging

The results from the study show that Blogging ismaking a big impact. The global average (figure 2) forreading and visiting blogs is an impressive 48%. It hasentered the mainstream as an established online mediumfor browsing and reading. There are however largemarket differences, with Italy, Spain, France, Russia,South Korea and China leading the way. Interestinglythe US, the perceived home of the blog lags inrelative terms. Northern European markets and SouthEast Asian markets also lag; in particular Germany andAustralia are failing to embrace the blog as a mediasource. Looking at this in the context of universe sizes(figure 3) it is clear that despite the lower than averagelevel of overall adoption, the US with its vast universeof 27m readers, has led the blogosphere in audienceterms. The impact on China's is clear - its 26m readers, nearly matching the US.

Figure 2: “Visiting / Reading any Blog” - Base = All Respondents

Figure 3: “Visiting / Reading any Blog universe sizes”.Base = All Respondents. Figures in Million

US,27.64

Australia, 0.34

China, 26.01

South Korea, 6.18

Singapore, 0.17

Hong Kong, 0.18

Thailand, 0.35Malaysia, 0.43

Philippines, 0.46France, 5.9Germany, 1.55

Italy, 7.48

Spain, 3.63

UK, 4.16

Russia, 3.48

9Creating and sharing content

Blogging

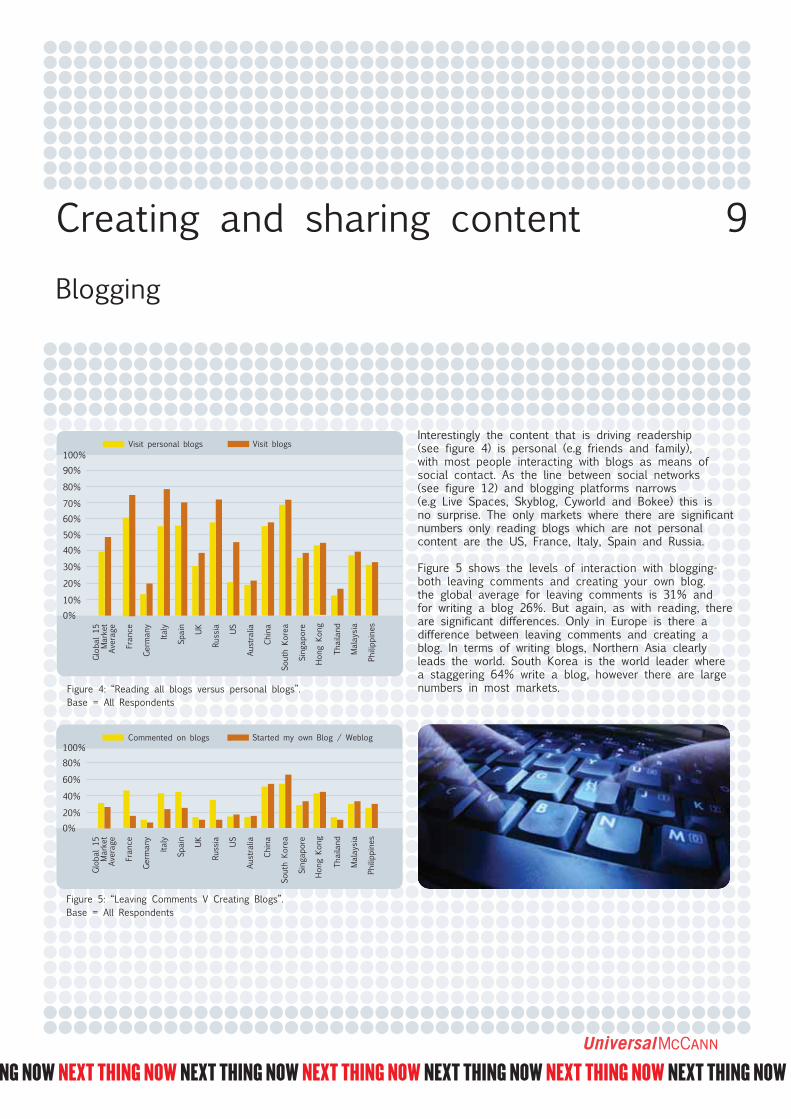

Interestingly the content that is driving readership(see figure 4) is personal (e.g friends and family),with most people interacting with blogs as means ofsocial contact. As the line between social networks(see figure 12) and blogging platforms narrows(e.g Live Spaces, Skyblog, Cyworld and Bokee) this isno surprise. The only markets where there are significantnumbers only reading blogs which are not personalcontent are the US, France, Italy, Spain and Russia.

Figure 5 shows the levels of interaction with blogging-both leaving comments and creating your own blog. the global average for leaving comments is 31% and for writing a blog 26%. But again, as with reading, thereare significant differences. Only in Europe is there a difference between leaving comments and creating ablog. In terms of writing blogs, Northern Asia clearlyleads the world. South Korea is the world leader wherea staggering 64% write a blog, however there are largenumbers in most markets.Figure 4: “Reading all blogs versus personal blogs”.

Base = All Respondents

Figure 5: “Leaving Comments V Creating Blogs”.Base = All Respondents

10Creating and sharing content

Blogging

From a regional perspective Asia has by far the highestlevels of active involvement, a fact that is particularlyclear when looking at the impressive levels of blogreaders who have their own blog as shown in figure 6.This suggests that web users from Northern Europe,the US and Australia are far more passive in theiruptake of blogging as a media platform, using it moreas a one way traditional media channel as opposedto a dialogue.

Figure 6: “Conversion of blog reader to blog creator -% of blog visitors who have their own blog”.Base = All Respondents

Figure 7: “percentage of blog readers who are blog creators.Base = All Respondents. Figures in Millions

US, 10.7

Australia, 0.26

China, 24.83

South Korea, 5.46

Singapore, 0.14

Hong Kong, 0.17

Thailand, 0.25Malaysia, 0.38

Philippines, 0.43France, 1.38

Germany, 0.47Italy, 2.14Spain, 1.29

UK, 1.07Russia, 0.5

China makes up just over half of our blogging internetuniverse, with a staggering 25 million bloggers, farexceeding the US, where 10.7m 16-44's have theirown sites. This makes China the world's biggest activeblogging market by some distance, a dramatic findingwith interesting ramifications for China's restrictedmedia market.

In total there are massive 50 million people bloggingacross our research universe. The markets covered in theresearch make up 60% of the world's Internet population,which would suggest that there are at least 80 million16-44 active bloggers worldwide.

11Creating and sharing content

Blogging

These numbers are set to grow thanks to consumerinterest translating into major future potential.Figure 8 below, shows the numbers of users who planto create their own blog in the future and the resultsare surprisingly consistent across markets, demonstratinga uniform level of interest and future growth.All markets fall broadly around the 20% mark with only Italy, Spain and the South East Asian marketsof Thailand, Malaysia and Philippines showing anysignificant upward deviation on the global average.When translated into numbers (figure 9) it is clear theblogging universe has potential to almost double with33m planning to start their own blog. Interestinglypotential adoption rates in Northern Chineseinfluenced Asia are lower than the average, suggestingsome element of saturation. However is also worthconsidering the growth potential from the enlarginginternet universe and the large number of under16 bloggers moving into the 16+ category.Which ever way you look it; blogs are not goingaway and set to become the mainstream.

Figure 8: “I plan to start my own blog in future”.Base = All Respondents

Figure 9: “I plan to start my own blog in future” universe figures.Base = All Respondents. Figures in Millions

US, 9.3

Australia, 0.3

China, 10.3

South Korea, 1.4

Singapore, 0.1

Hong Kong, 0.1

Thailand, 0.6Malaysia, 0.3

Philippines, 0.4France, 1.8Germany, 1.1

Italy, 2.9

Spain, 1.8

UK, 1.5

Russia, 0.9

12Creating and sharing content

Implications

From a global perspective the numbers of blog owners and readers shown in this report are huge for a media platformthat is little more than a couple of years old. Sure some ofthe markets are small, but combined it is a large platform. Blogging is living up to some of its hype and it looks setto grow into a mainstream media platform.

The differences between Asia and the rest of the world are interesting with the conversion of readers to active users in Asiaparticularly impressive. Compare this to Europe and the US wherethe blog readership universe is substantial, but conversions tocreating content are relatively low - it is clear that Asia is drivingblogging in terms of creating content. There are a number of factors that could explain this difference •Asian use of blogging is orientated around personal content -

its use is closer to social networking. The barriers to entryhere are lower and growth is viral thanks to this social aspect. •The huge uptake in China can be linked to the lack of uncensored media and a thirst for independent informationand fresh opinions. The blog run by Chinese actress Xu Jinglei is now the world's most popular blog. (Technorati August 2006)•Due to the heavy governmental controls in China, personal blogging is a safe subject matter. Chinese blogs tend to avoid political topics and so have little impact on political discourse, unlike in Western Europe and the US. This strengthens the associations of blogging as a social medium and fuels adoption. (International Herald Tribune “Battle of the blogs in China” August 2005)•Asian markets like China, South Korea tend to be more closed to the outside world for cultural, social and political reasons that help build the internal focus that drives person blogging.

•The emphasis on personal content is reflected by the success of platforms such as Cyworld, Bokee and BlogCN shows that blogging has become an essential social tool. •Blogs in Asia tend to be populated by very short posts and photos making them easier to maintain and more accessible. •The concepts of Confucianism (which manifests itself as a strong respect for others and authority) that govern social conduct in Chinese influenced culture affect blogging in two ways. Firstly bloggers have strong ideas of responsibilityfor what they write, which makes blogging more community focused, and secondly there is an unwritten code of conduct - that it is basic manners to comment on friend's blogs - developing the community aspect. (APAC UM)•In China blogging is the first time many have had the chance for self expression. •Blogging in Western Europe and US is more associated with individualism and sharing your opinion. This is likely to have channeled social interaction into established social networking sites. (see figure 13) •This explains the rise of personality blogs in the US and Europe, something less evident in Asia •Blogging in China is popular due to a generation of only children.

13Creating and sharing content

Implications

•Reading blogs as a media platform is higher in Europe and there are huge numbers in the US due to the rise of the professional blog. Blogs are integrated into existingmedia organisations’ output, used by corporations as aconsumer communication tool and run as full time blog sites such as Engadget and Cool Hunting. In the US and Europe there is a wider universe of non personal blog content to tap into - this is a bigger threat to media owners than the personal blogging of Asia. It also means the perceived barriers to entry are higher.•The huge usage of blogs as a media platform in Spain, France, Italy and Russia is influenced by language. The huge amount of English language content on the web means US and UK readers are already overwhelmed with choice and there is less of a personal urge to create. •Some of these markets have a younger profile than others - Spain, Italy and China have a younger and more male profile than the more established markets of the US, UK and South Korea. This will be a factor in higher levels of usage.•South Korea has an exceptionally well developed broadband market. Hong Kong and Singapore are also very developed internet markets that have led to strong adoption of online as a core social medium.

Despite this variance by market there is clearly global takeup and growth potential. This suggests that there may be

truth in some of the hype around the consumer as the leadcontent creators. Two facts are clear; online users read blogsand increasing numbers are writing them. Although most ofthis will cover personal subjects there is clearly a threat. If

just 5% of our 50m bloggers blog about non personal topics,that is 2.5m new media sources - obviously not all of thesewill be able to maintain an audience or have compellingcontent, but when amplified through blog search enginesand aggregators like Technorati and Google Blog search,it is clearly a potential threat.

14Creating and sharing content

Sharing photos

Figure 10 below demonstrates the impact of thesechanges - photo sharing is clearly a mainstream form of content creation and sharing in all markets. The global average is 68% but the variation is smallcompared to blogging - even in France, the market oflowest adoption 48% have shared. These numbers areconsequently vast (see figure 11). The total universe forphoto sharing is 122 million in our research universe -with a massive 43 million in the US and 41 million in China alone.

Figure 10: “Sharing Photos Online”.Base = All Respondents

Figure 11: “Sharing Photos - Universe”.Base = All Respondents. Figures in Millions.

The way we take and share photos has transformedthanks to the combination of broadband, the availabilityof digital cameras and camera enabled mobile phones.When photos are in a digital format there is clearly ademand to share them. Thanks to the rise of simpleonline photo management and sharing tools such asFlickr.com, Ringo.com and Photobucket.com it has neverbeen easier. These new services have changed photosharing by making your photos publicly searchablethrough the introduction of tagging (labelling a photo with a searchable keyword) and social networking aspects. Also as users have become more sophisticated,photos have also become an integral part of social networking profiles and personal blog pages.

US, 43.23

Australia, 1.05

China, 40.67

South Korea, 6.6

Singapore, 0.35

Hong Kong, 0.35

Thailand, 1.09Malaysia, 0.91

Philippines, 1.13France, 3.73

Germany, 3.95

Italy, 5.74Spain, 3.72

UK, 6.03

Russia, 2.74

Tags / Tagging“A series of keywords assigned by users to cat-egorise web pages, products and services orcontent by subject or category. Pages can alsobe scored or ranked allowing search for contentbased on Social Recommendation rather thantraditional algorithm based search engines.”

15Creating and sharing content

Implications

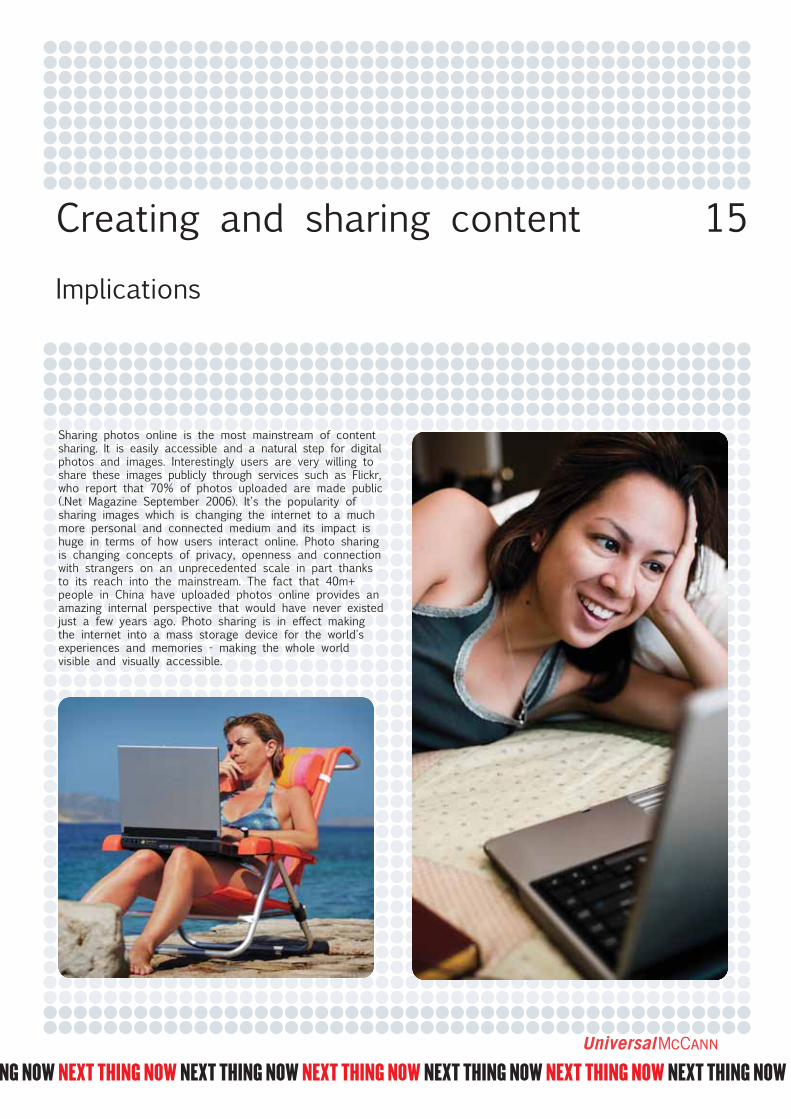

Sharing photos online is the most mainstream of contentsharing. It is easily accessible and a natural step for digitalphotos and images. Interestingly users are very willing toshare these images publicly through services such as Flickr,who report that 70% of photos uploaded are made public(.Net Magazine September 2006). It's the popularity of sharing images which is changing the internet to a muchmore personal and connected medium and its impact ishuge in terms of how users interact online. Photo sharingis changing concepts of privacy, openness and connectionwith strangers on an unprecedented scale in part thanksto its reach into the mainstream. The fact that 40m+ people in China have uploaded photos online provides anamazing internal perspective that would have never existedjust a few years ago. Photo sharing is in effect makingthe internet into a mass storage device for the world'sexperiences and memories - making the whole worldvisible and visually accessible.

16Reviewing products and services

Implications

Although there has long been the facility to reviewproducts and services, in a Web 2.0 enabled space thishas become more central to shopping online andresearching purchases. Reviews have become easier tocreate and due to integration with tagging and profiles,now carry more weight than they did. Reviews matchedwith social profiles allow you to search for productsand services that will interest you from people youtrust. Regular reviewers are often rewarded for theirwork with a higher status and often users becomehabitual reviewers.

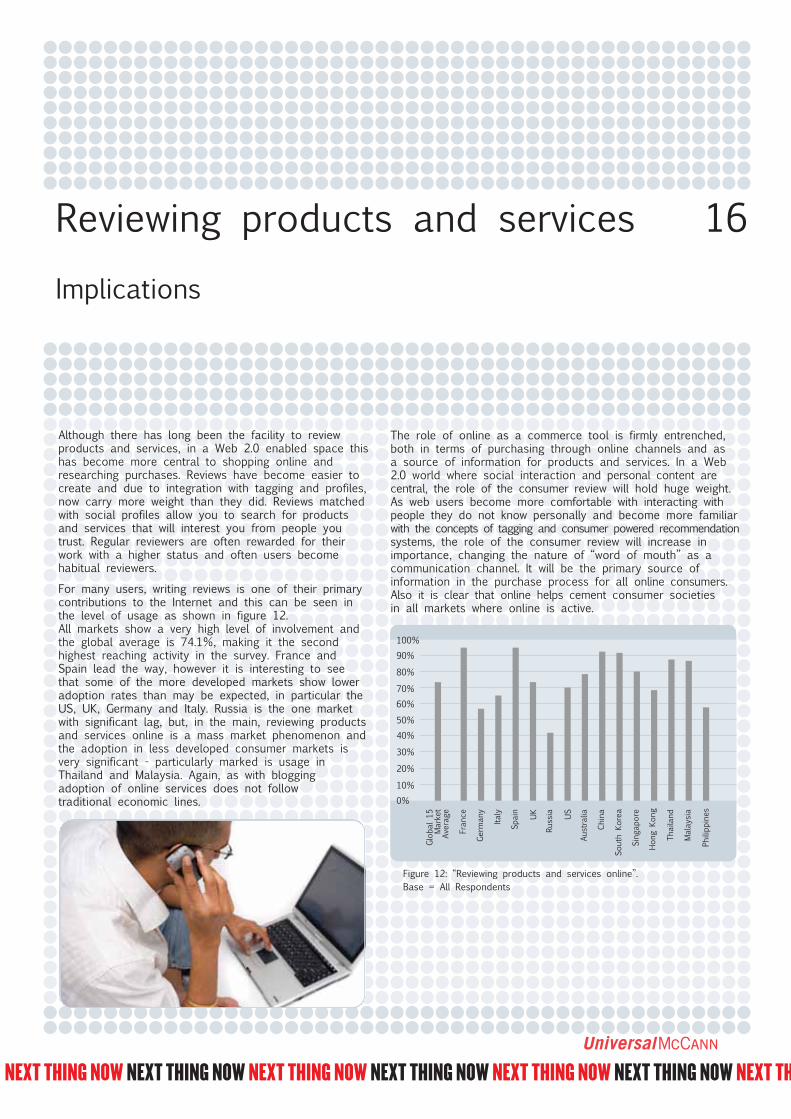

For many users, writing reviews is one of their primarycontributions to the Internet and this can be seen in the level of usage as shown in figure 12.All markets show a very high level of involvement andthe global average is 74.1%, making it the secondhighest reaching activity in the survey. France andSpain lead the way, however it is interesting to see that some of the more developed markets show loweradoption rates than may be expected, in particular theUS, UK, Germany and Italy. Russia is the one marketwith significant lag, but, in the main, reviewing productsand services online is a mass market phenomenon andthe adoption in less developed consumer markets isvery significant - particularly marked is usage inThailand and Malaysia. Again, as with bloggingadoption of online services does not followtraditional economic lines.

The role of online as a commerce tool is firmly entrenched,both in terms of purchasing through online channels and as a source of information for products and services. In a Web2.0 world where social interaction and personal content arecentral, the role of the consumer review will hold huge weight.As web users become more comfortable with interacting withpeople they do not know personally and become more familiarwith the concepts of tagging and consumer powered recommendationsystems, the role of the consumer review will increase inimportance, changing the nature of “word of mouth” as acommunication channel. It will be the primary source ofinformation in the purchase process for all online consumers.Also it is clear that online helps cement consumer societies in all markets where online is active.

Figure 12: “Reviewing products and services online”.Base = All Respondents

18Social interaction online

Communication online has never been simpler. Not onlyhave a wealth of new social networking sites emergedsuch as Myspace, Tagworld and Bebo that encourageinteraction through personal profiles and message boards;but technologies such as Instant Messaging and VOIP havebecome essential online tools that have opened up wholenew channels of real time peer to peer communications.These two platforms could potentially revolutionisetelecoms and could transform the Internet into thekey communication medium, spelling trouble for thefixed line telecoms world.

Social Networking The first clear observation on the uptake of dedicatedSocial Networking platforms (figure 13) is that usage ishigher than blogging, with a global average of 28.6%.Again as with blogging there are some differences by market, with South Korea leading the way on 51.5%, however Asia does not dominate as it does with blogging.The other interesting point is that Russia, with its youngeronline profile has the highest usage in Europe, far exceedingthat of Western Europe. The US, often seen as the homeof social networking thanks to Myspace, Friendster andFacebook amongst others, actually lags other markets inpercentage reach but in terms of numbers (see figure 14)remains the largest market - its 17.8m users representingnearly half the global research universe.

Social Networking “Virtual communities of users who have theirown online profile of personal information andcontent. The social network technology allowsthem to associate, communicate and sharecontent with other users based on their personalprofiles - thus building a network of individuals.”

VOIP (Voice Over Internet Protocol) ”Voice telephone calls conducted over theinternet. The most well known service is Skype”

Instant Messenger “Software that allows real time email typeconversations with messenger buddies. Popularprogrammes include MSN Messenger, YahooMessenger and Google Talk”

Figure 13: “Usage of Social Networking Sites / Platforms”Base = All Respondents

19Social interaction online

Implications

Social networking is outperforming blogging in WesternEurope and the US. Why? Well mainly because it is verysimple to use and interact with, but also because it hasbecome an essential part of maintaining social status fora certain generation. It is now a core tool, along with themobile phone to both to stay in contact with friends butalso as a way of meeting new people. Blogging in its traditional sense is more demanding, even when writingabout personal topics. However, increasingly it will becomedifficult to pick the two apart as the big social networksincreasingly make blogging a core component.

It is also worth considering that mass usage of SocialNetworking is a fairly new concept and many users ofthese sites are populated by under 16's (hence outside our research). Dramatic growth should be anticipated asthey move into the 16+ bracket. That said there arealready huge numbers using Social Networks between the ages of 16-44, with our research estimated at least49m - suggesting a worldwide figure of almost 90m.These are massive numbers and its impact is big in terms of socialising the web - in particular changing concepts of privacy, by making every one and everythingpublic and searchable. It is also making users comfortablewith the idea of meeting people online and using onlineas a social tool.

Also we should not forget the role that Social Networksites play in content creation and sharing. Users arebecoming more sophisticated in the creation of their personal pages with the integration of graphics, photos,blogging, music and video. For many people online this is where they create most content. The social networkshave embraced this, integrating music and video streaming, blogging platforms and full html support. As personal blogging and social networking continue to merge this is a trend set to continue.

Figure 14: “Social Networking Universe Sizes”Base = All Respondents

US, 17.87

Australia, 0.31

China, 15.64

South Korea, 4.39

Singapore, 0.14

Hong Kong, 0.11

Thailand, 0.4Malaysia, 0.51

Philippines, 0.64France, 1.1

Germany, 1.77

Italy, 1.01Spain, 1.32

UK, 1.85Russia, 1.81

20Social interaction online

Instant Messenger (IM)

The number of IM users is vast, one that could only berivalled by email. Figure 15 below shows how massmarket Messenger has become, with a global averagepenetration of 78.4%. There are small marketdifferences, with Asia marginally ahead of Europe,US and Australia. China leads the way with nearuniversal usage at 97% and (see figure 15 and 16)43m users, tied with the US also on 43m.The only exception is Germany, where strangely it hasfailed to take off. The interesting difference with otherplatforms is that usage is consistently high across thewhole of Asia, regardless of market development.

Figure 15: “Instant Messenger”Base = All Respondents

Figure 16: “Instant Messenger Universe Sizes”Base = All Respondents

US, 43.1

Australia, 1.14

China, 43.35

South Korea, 6.89

Singapore, 0.38

Hong Kong, 0.35

Thailand, 1.65Malaysia, 0.98

Philippines, 1.24France, 6.58

Germany, 3.78

Italy, 6.53

Spain, 4.35

UK, 7.74

Russia, 3.87

21VOIP (Voice Over Internet Protocol)

As a technology VOIP could be one of most revolutionaryonline developments in the past few years. The ability tomake phone calls for free anywhere in the world couldcompletely revolutionise not just the online experience butthe telecoms model. VOIP is becoming more consumercentric with services such as Skype and retailers like Tescomaking it easier to set up and operate while existing onlineplatforms like Ebay are beginning to integrate it as a formof buyer / seller communication. Understandably telecomcompanies the world over look at VOIP with a sense offoreboding and figure 17 will show why. For such a newand relatively complex technology the growth in VOIP users isimpressive. The global average is 23.4% with less developedmarkets leading the way; embracing a service that bypassesunreliable, expensive and bureaucratic fixed line services.Malaysia has the highest level of usage with 39%, whileinterestingly the US and the UK which are two of the mostdeveloped telecoms markets, rank last with just 12%.This suggests that VOIP may grow more slowly in moredeveloped markets. Once again, adoption of onlineservices is not linked to economic development.

Figure 18: “VOIP universe”Base = All Respondents

US, 6.73

Australia, 0.27

China, 16.04

South Korea, 1.54

Singapore, 0.12

Hong Kong, 0.08

Thailand, 0.47Malaysia, 0.44

Philippines, 0.48France, 2.06

Germany, 1.87

Italy, 2.92

Spain, 0.95

UK, 1.36

Russia, 0.66

Figure 17: “Usage of VOIP”Base = All Respondents

22VOIP (Voice Over Internet Protocol) + (IM)

Implications

It is clear that IM is changing the nature of global communication.Its stealth growth has made IM a main stream form ofcommunication. Its impact is much underrated, enabling real-timeglobal communication for no cost above the price of the internetconnection. Anyone with friends and relatives abroad will tell youhow important it is. Thanks to these factors it is universallyembraced in all markets (except strangely Germany) and playsa big role in globalising and connecting the web. It is a much untapped platform and more could be done to integrateit into social network platforms, ecommerce or as a real timemethod of customer service and site assistance. It is howeverclearly acting as a catalyst for VOIP, with growing availability ofvideo and voice via webcams through Instant Messenger platforms.Most VOIP services are not much more than enhanced Messengerservices and it's this similarity that could propel it into the mainstream and potentially revolutionise telecoms.It could have bigger ramifications for an existing business modelthan consumer content creation could have on the establishedmedia world. It is also interesting to see that growth of VOIPis driven by less developed markets suggesting that this technologycould help level the playing field and play a role in creatingan increasingly globalised and connected world.

24Personalised multimedia experience

Watching video clips online

Fuelled by Web 2.0 technology and the massive growthin broadband the Internet has taken real steps towardsbecoming an entertainment medium. The much quotedrise of youtube.com and its 3 billion streams a monthsum up the rise of multimedia content online. There are signifiers of the multimedia nature of theInternet everywhere you look, for example: all Champions League football is now broadcast online; Warner Musicsigning a deal to make all their music videos availablethrough youtube.com; MTV launching MTV flux an online video portal. It's a clear shift - not only for video, but podcasts, online radio, music, aggregators and personalised homepages. It is also easier for consumers to get involved: creating video and audiothanks to the wealth of low cost and increasingly high quality digital cameras and mobile phones whichoffer live recording.

Figure 19 shows the extent to which watching online video is now beginning to enter the mass market - witha global average penetration of 32%. There are howeversome interesting distinctions by market. China leads theway with a massive 56.2%, fuelled by the opportunity toconsume independent and relatively un-censored media.

The next two markets are Malaysia and Philippines, againdemonstrating the global appeal of new Internet services. The other interesting point within Asia is the relativelylow take up in South Korea - a market normally at theforefront. Within Europe, Italy, Spain and the UK are moreentertainment oriented, while France and Germany lag.The US hits the global average which for such a maturemarket shows the real impact of online video.

Figure 19: “Watching Video clips online”Base = All Respondents

25Personalised multimedia experience

Podcasts

Podcasts“A method of delivering audio files over the net.Podcasts are typically half and hour to an hourin length and usually recorded in the style of aradio show. Podcasts available to today coverevery imaginable topic from unsigned bands totechnology. You can subscribe to Podcasts viaRSS, through services like iTunes or downloadeddirectly from the publishers website. Once youhave subscribed you automatically receive thenext installment when it is published” individuals.”

PodcastsCompare watching video clips to Podcasts (figure 20), andit's clear that on demand video is beating audio handsdown. The global average is just 17.4%, well beneath videoclips. Interestingly France and South Korea have the highestreach, but the pattern across all markets is similarly low.Why? There are a number of clear reasons that couldexplain this: copyright limits the musical content thatPodcasts can include so the vast majority are voice andspecial / niche interest; video clips are shorter, more interactive and easier to share virally; it is easier to createvideo clips that are entertaining - Podcasts require moreequipment and radio production skills to make engagingcontent; the distribution platforms for video clips are more consumer friendly and easier to make part of yourday to day surfing. Distribution platforms for Podcastsare improving, in particular the integration with the Itunesmusic store, however until copyright issues are resolvedthen the Podcasts in the future are still likely to lag video.

Figure 20: “Listening to Podcasts”Base = All Respondents

26Personalised multimedia experience

Streaming

Comparing these figures to Figure 21 for Streaming LiveVideo / Audio and some interesting differences emerge.Firstly the levels of streaming live are much higher inall markets, secondly live streaming is driven by WesternEurope and the US - whereas watching video clips isdriven by Asia. This suggests a different relationship tomedia, with established Western Europe and US marketsorientated around delivery in a more conventional liveform. One reason is that the majority of live streamingis likely to be audio, hence far more likely to beInternet radio streams. Radio has a stronger heritage inWestern Europe and the US and higher levels of onlinelistening have been inherited from traditional broadcasters.Also developed media markets have better resourcedorganisations such as the BBC, Canal+, CBS who havethe resource to deliver live content and have promotedit. The one Asian market that matches Europe and theUS is China, whose figures again indicate the appeal of external new sources of media.

Figure 21: “Streaming Live Music / Video”Base = All Respondents

27Personalised multimedia experience

Streaming

Comparing the universe sizes for streaming to thosefor watching video clips on demand (figure 22 /23)makes these differences even more obvious.Asia has a much larger share of watching video clipsversus streaming and China is marginally the largestmarket. The other interesting comparison is withinWestern Europe, where France, Germany and theUK lead in terms of volume for streaming but onlythe UK has a large take up of watching clips. The enthusiasm with which Europe and the US embrace streaming is an interesting difference and one that islikely to be a result of the legacy of well resourcedand established media organisations that are more likely to stream live and more likely to promote it.

US, 19.17

Australia, 0.4

China, 25.2

South Korea, 2.53

Singapore, 0.15

Hong Kong, 0.15

Thailand, 0.58Malaysia, 0.44

Philippines, 0.56France, 1.83

Germany, 1.57Italy, 3.29

Spain, 1.46

UK, 3.52

Russia, 1.03

US, 32.84

Australia, 0.44

China, 25.39

South Korea, 2.96

Singapore, 0.15

Hong Kong, 0.12

Thailand, 0.59Malaysia, 0.5

Philippines, 0.61France, 5.33Germany, 4.23

Italy, 4.09

Spain, 3.42

UK, 5.52

Russia, 1.63

Figure 22: “Universe of users viewing video clips online”Base = All Respondents

Figure 23: “Universe of users streaming live music / videoonline”Base = All Respondents

28Personalised multimedia experience

Implications

Multi-media online is now the norm for our online universein all markets. This is particularly case for streaming media via online in the traditional live sense. Watchingclips on demand has a much smaller reach but its growthis significant. The idea of trawling pre made and user generated video is a fairly new concept. Podcasting is alsorelatively new and, although its take up is markedly lower,thanks to the global nature of online there is still an audience of millions. Streaming live media is more popularparticularly in developed media markets mainly due toexisting media organisations moving their radio and,increasingly, TV delivery online. This has been promotedheavily and has been made available through existingmedia organisations' online properties. In the main it is an easier point of entry for consumers wishing to utilisetheir PC as an entertainment medium. It is also a morefamiliar concept, with media delivered in real time.On-demand media is newer, requiring more consumerinput and sifting of content.

Despite this, on demand is clearly set to grow andbecome the preferred method of receiving content online.Video will lead the way especially as established mediacontent producers start distribution of new productions inan on-demand format and see the value of monetisingtheir archives. Podcasting is likely to continue to lag andwill only compete if copyright issues are resolved - currently the record industry is holding this back.

In summary the internet clearly is evolving into a globalentertainment platform, which, for content producers bothconsumer and professional, is a massive opportunity. It is also a big boost for the advocates of convergenceand the idea of internet delivered content being madeavailable through your main TV set in the living room. It is surely only a matter of time before this is the normand many companies will benefit substantially: online distribution channels like Yahoo Go; technology companiessuch as Sony who will connect the PC and the TV andcontent producers themselves. The barriers to creatingglobally recognised and appreciated content are falling and a golden age of video could emerge. The industries who should be really concerned are the networks, cable companies and satellite broadcasters who have historically controlled distribution within markets very tightly.

29Personalised multimedia experience

RSS (Really Simple Syndication)

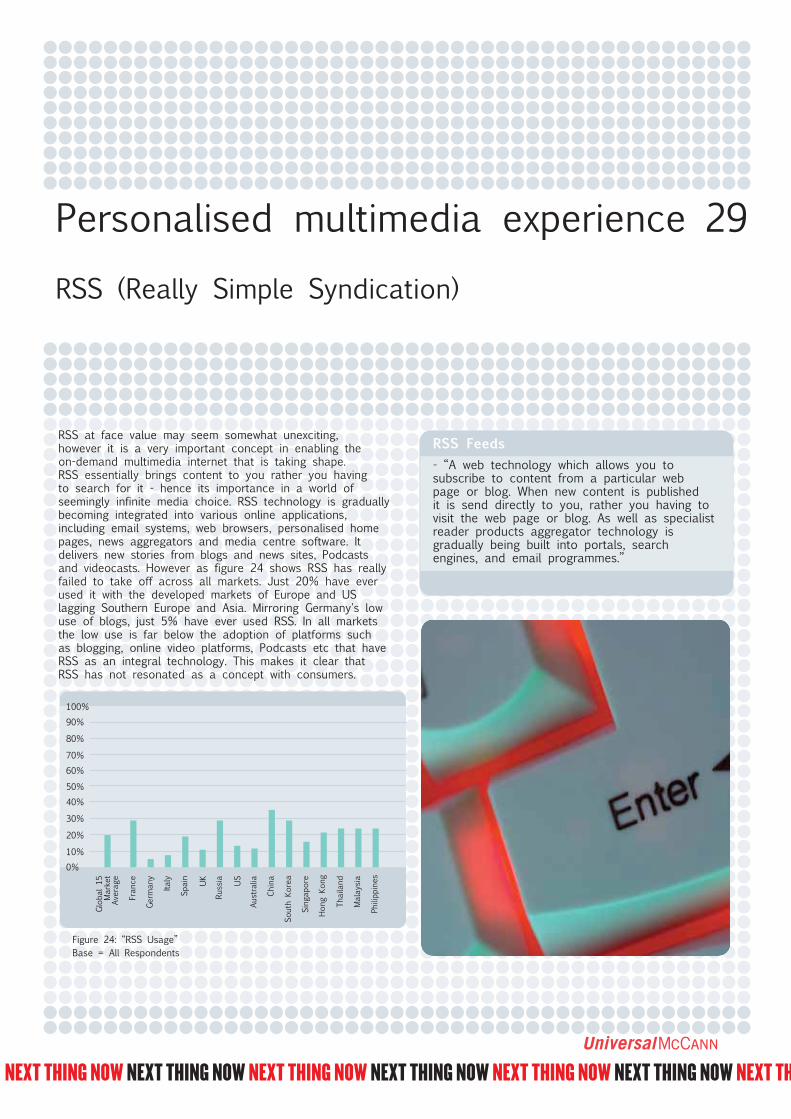

RSS at face value may seem somewhat unexciting,however it is a very important concept in enabling theon-demand multimedia internet that is taking shape.RSS essentially brings content to you rather you havingto search for it - hence its importance in a world ofseemingly infinite media choice. RSS technology is graduallybecoming integrated into various online applications,including email systems, web browsers, personalised homepages, news aggregators and media centre software. Itdelivers new stories from blogs and news sites, Podcastsand videocasts. However as figure 24 shows RSS has reallyfailed to take off across all markets. Just 20% have everused it with the developed markets of Europe and USlagging Southern Europe and Asia. Mirroring Germany's lowuse of blogs, just 5% have ever used RSS. In all marketsthe low use is far below the adoption of platforms suchas blogging, online video platforms, Podcasts etc that haveRSS as an integral technology. This makes it clear thatRSS has not resonated as a concept with consumers.

RSS Feeds - “A web technology which allows you to subscribe to content from a particular web page or blog. When new content is published it is send directly to you, rather you having tovisit the web page or blog. As well as specialistreader products aggregator technology is gradually being built into portals, search engines, and email programmes.”

Figure 24: “RSS Usage”Base = All Respondents

30Personalised multimedia experience

Implications

RSS clearly has a bit of image problem and itsadoption lags the technology it helps consumers find,use and subscribe to. The concept of subscribing tocontent is not yet consumer friendly enough and hasnot been promoted or packaged correctly. It needs simplifying and needs clearer integration into the toolseveryone uses online, such as web mail and instant messenger. Once RSS has been integrated properly across all platforms, particularly home media centers, it will inevitably become a core mass market technology, even if it is not known as RSS. As more and moreweb users immerse themselves in user generated contentand the world of near infinite media choice, RSS willbecome required to navigated the wealth of content choice.

31Overall summary - what is the impact?

It's clear that Web 2.0 technologies are being adoptedon a global scale regardless of internet penetration,region of the world and economic development.It is a global phenomenon and web users are showingsigns of living up to the hype. The summary of adoptionas shown in figure 23 demonstrates how wide-scale overalladoption levels are, while figure 24 demonstrates the sizeof these potential audiences. Consumers are creating andsharing content, connecting socially and increasingly usingthe internet as a multi-media experience.

The numbers are huge (see figure 24) and it is happeningnow, not in the future. Interestingly adoption is not alongthe traditional economic lines. Figure 25 reveals the extentto which online is going to be driven by Asia, with the topfive markets all being from Asia, with only Thailand falling into the bottom half. Spain and France lead the rest of the world, including the US.

Figure 23: “Global reach”Base = All Respondents: Average usage across all markets

Figure 24: “Global Research Universes” (Figures in millions)Base = All Respondents

Figure 25: Global Web 2.0 adoption index (average take up bymarket across all technologies and activities in the questionaire)- All Respondents

32Overall summary

Implications for media owners

Online is progressively becoming the core medium for interaction,creativity and entertainment across the world. Although it goeswithout saying that internet users are not yet entirely bypassingregular media sources in favour of creating, sharing and consuminguser generated content there are clearly massive implications forall media owners, in terms of near and far future trends.

If offline media owners have not already put online at the heartof their product, they must do so regardless of the market theyoperate in. Media brands need stretch across a variety of digitalplatforms if they are going to survive this world of unlimited fragmentation and the demise of tightly controlled market orientated distribution platforms. Web 2.0 technologies areincreasingly shifting media distribution platforms to a global scale - presenting media owners both with opportunities to reach new audiences, but also the some key challenges: remaining relevant to their audience; increased competition; growing issues with copyright and rights ownership. Also, mediaowners will have to produce more as the delivery of basic newswill increasingly become commoditised due to the wealth ofsources and the always switched on nature of online. Editoriallythere will be more demand for expertise and niche content aspeople increasingly mix and match expert content with a distinctvoice and point of view via their personalised page or content aggregator.

As well as an increasingly competitive professional environment,there is going to be huge competition from consumer content,which as demonstrated has a big future in all markets. Asia isleading the way with content creation and interaction, but theother regions will follow along the path from passivity tointeractivity. Although vast majority of this content is of personalinterest and clearly not everyone will start creating content, thescale is alarming for established media companies. Supposing that10% of users create content and 10% of these produce something of wider interest, millions of new media sources willemerge to challenge established media owners. The threat ismagnified by the new online platforms that are emerging: videosites, photo sharing, aggregators and personalised homepages allsift and sort the best of user generated content bringing togetheruser created media into a viable channel.

In order to survive this onslaught of user generated content, existing media brands must try to involve consumer interaction andcontent creation within their digital platforms, while at the sametime opening up communication with users to become more conversant. They must be comfortable at releasing their content in channels not controlled by them, while delivery should evolveinto short regular feeds in order to remain relevant in an age of RSS feeds, aggregators and personalised home pages.

Anyone that produces video and audio content is provided amassive opportunity if they embrace Web 2.0 properly: broadcasters,production companies, record labels, movie production companiesand TV stations could potentially distribute their new and archivedcontent across the world - directly controlling distribution andaccess rather than relying on the satellite, cable and TV networksor the DVD and CD store. This should be seen as a massiveopportunity rather than a threat. Also the potential to makerevenue from old content currently sitting in dusty boxes is vast -it can be monetised through sponsorship, adverts, subscription orpay per view. Why TV networks, movie studios and record companies cannot see this currently is baffling. Rather thanthreatening to sue the users and channels who use their contentillegally they should be embracing the potential to reach hundredsof millions of consumers in new markets with recycled content.

Media in this on-demand format will change revenue structuresmeaning that retaining revenue through traditional interruptiveadvertising formats, such as the 30 second commercial willbecome more difficult. Live broadcasting and event TV willbecome more important to deliver any kind of significant massaudience. However the rights to screen live events will becomemore difficult to source as rights owners may in the futureincreasingly wish to distribute coverage themselves rather thansell their rights to the TV networks and Satellite broadcasters.

The real threat is to the existing controllers of the distributionchannels. The appetite online users across the world show forconsuming audio and video media online is a real long termthreat to the cable, satellite and TV networks. When online linksto the main screen in the household as will happen inevitably in the near future, services such as Youtube and Itunes, or thefuture as yet to emerge equivalent could be the distributionchannels of the future.

33Overall summary

Implications for advertisers

Advertisers and marketers who embrace the changes that Web2.0 is delivering have massive opportunities to connect withconsumers as never seen before. The number of new channels ofcommunication are huge and the possibilities are endless. It alsoopens up new revenue streams, and links communications andsales in ways that were never previously possible.Future communications can work as revenue earner for Web 2.0embracing brands. There is also a major opportunity to buildglobal brands and access new markets in ways and at a costnever previously possible. As culture becomes more intermixedand accessible it is likely that existing established internationalbrands many of which are European and American will be wellplaced to benefit.

Marketers and agencies that continue view this as a threat andrefuse to adapt from the old interruptive model will see theircommunications lose effectiveness over time and their brandsand sales suffer. The clear global trends of adoption show thisis taking off now so it is not something to plan for in ten totwenty years. This is a current reality and as more and morepeople move online and embrace Web 2.0 services it willgrow and grow.

There are a number of things that marketers, advertisers andcommunications agencies need to do to survive in a world ofconsumer generate media and infinite channel fragmentation.

•Ensure online is central to all brand communications - linking all elements together •Shift from thinking about interruptive advertising to creating content and services available across multiple digital platformsthat offer genuine consumer benefit.

E.g Pampers.com which offers a full online resource for parents with young children.•Brands have the same opportunities as consumers - it's never been easier to create and share content and they should embrace it.

E.g BMW video casts on iTunes

•Embrace sponsorship and new online formats, such as Podcasts and Videocasts. Consumers like online because access is generally free and will happily trade commercial intrusion for access.

E.g Visa and Dell sponsoring “This week in technology” and “Inside the Net” Podcasts • In an on-demand content world there are huge opportunities for brands to create experience for customers by providing free content and media.

E.g Free iTunes downloads with Coca-Cola.•Encourage consumers to interact with your brand

E.g Lynx Boost - Shower boy blog and myspace sitetracking their on street event activity •Be comfortable distributing your brand in channels you cannot control. In a world orientated around consumers creating content anything could happen. Good brands will benefit, bad brands with false promises will be found out

E.g Mentos and Diet Coke fountains competition on youtube•Do not try to control the channels of creativity - consumers have too many options. They will go somewhere else

E.g. Land Rover’s ‘go beyond’ video platform.• In the new world of online, everything is inter-connected. This also applies to branded websites - siloed sites will struggle to engage in the future online space. •Web 2.0 is globalising media consumption - online media platforms work across markets, really only limited by language.The conventions of working within a market will loserelevance and increasingly, a global perspective will be needed.Brands will have to have global identities and positioninguniversal, executed through global strategies by agencies whocan deliver on a worldwide basis. Conflicting local positioningin a Web 2.0 world is likely to create confusion in the eyesof consumers.

For more information contact