Wachovia Securities 2006 Media and Communications Conference

21

Wachovia Securities 2006 Media and Communications Conference May 24, 2006

-

Upload

conan-ramirez -

Category

Documents

-

view

29 -

download

0

description

Wachovia Securities 2006 Media and Communications Conference. May 24, 2006. - PowerPoint PPT Presentation

Transcript of Wachovia Securities 2006 Media and Communications Conference

Wachovia Securities2006 Media and Communications

Conference

May 24, 2006

2

Caution Concerning Forward Looking Statements and Non-GAAP Financial Measures

This presentation contains certain forward-looking statements relating to future events and This presentation contains certain forward-looking statements relating to future events and Mediacom’s future financial performance. These forward-looking statements are subject to risks Mediacom’s future financial performance. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from historical results or those and uncertainties that could cause actual results to differ materially from historical results or those anticipated. Factors that could cause actual results to differ from those contained in the forward-anticipated. Factors that could cause actual results to differ from those contained in the forward-looking statements include: competition in the video, high-speed Internet access and telephone looking statements include: competition in the video, high-speed Internet access and telephone businesses; Mediacom’s ability to achieve anticipated customer and revenue growth and to businesses; Mediacom’s ability to achieve anticipated customer and revenue growth and to successfully introduce new products and services; increasing programming costs; changes in laws successfully introduce new products and services; increasing programming costs; changes in laws and regulations; Mediacom’s ability to generate sufficient cash flow to meet its debt service and regulations; Mediacom’s ability to generate sufficient cash flow to meet its debt service obligations and to access capital to maintain its financial flexibility; and the other risks and obligations and to access capital to maintain its financial flexibility; and the other risks and uncertainties described in the reports and documents Mediacom files from time to time with the uncertainties described in the reports and documents Mediacom files from time to time with the Securities and Exchange Commission. Mediacom assumes no obligation to update or alter these Securities and Exchange Commission. Mediacom assumes no obligation to update or alter these forward-looking statements, whether as a result of new information, future events or otherwise, forward-looking statements, whether as a result of new information, future events or otherwise, except as otherwise required by law.except as otherwise required by law.

This presentation may include financial measures which are not determined in accordance with This presentation may include financial measures which are not determined in accordance with generally accepted accounting principles (GAAP) in the United States. Any applicable generally accepted accounting principles (GAAP) in the United States. Any applicable reconciliation of historical non-GAAP financial measures included in this presentation to the most reconciliation of historical non-GAAP financial measures included in this presentation to the most directly comparable GAAP financial measures is available at the Press Releases link in the Investor directly comparable GAAP financial measures is available at the Press Releases link in the Investor Relations section of the Company’s website at www.mediacomcc.com. Relations section of the Company’s website at www.mediacomcc.com.

3

Mark StephanMark Stephan

Executive VP and Chief Financial OfficerExecutive VP and Chief Financial Officer

4

Mediacom Today

Improving basic subscriber trendImproving basic subscriber trend

Expanding RGU penetrationExpanding RGU penetration

Delivering solid operating performanceDelivering solid operating performance

Maintaining financial flexibilityMaintaining financial flexibility

5

2006 Objectives

Scaling of phoneScaling of phone Add 1 million marketable homes by Add 1 million marketable homes by

YE 2006 (reaching 87% of total) YE 2006 (reaching 87% of total)

Realize triple-play pull through across Realize triple-play pull through across all products all products

Retention of 2005 discounted customersRetention of 2005 discounted customers Exceeding expectations YTDExceeding expectations YTD

Cost controlsCost controls Capture operating efficienciesCapture operating efficiencies

6

Potential Upside in Pull Through Effect

18%

23%

0%

10%

20%

30%

40%

50%

Mediacom MSO Average (1)

Data Penetration% of HP

35%

49%

0%

10%

20%

30%

40%

50%

Mediacom MSO Average (1)

Digital Penetration% of basic

(1) Weighted average of Comcast, Time Warner, Charter, Adelphia, Cablevision and Insight. Source: Public information.

Q1 2006Q1 2006

7

Orders per Month

Usage Rates

Over 1,200 hoursOver 1,200 hoursof contentof content

Competitive Advantage

No equipment toNo equipment to purchase purchase

No contractNo contract

Low entry priceLow entry price

Our advantage today: Our advantage today: local broadcast local broadcast channels channels

Up to 16 HD channelsUp to 16 HD channels

44%

40%

April 2005 April 2006

3.8 million3.8 million

1.9 million1.9 million

ONDEMAND

8

Enhanced High-Speed Data Product

Mediacom OnlineMax: 10 MbpsMediacom OnlineMax: 10 Mbps Free wireless routerFree wireless router Free premium contentFree premium content

9

RGU Rebound

123,000

52,000

15,000

196,000

52,000

FY 2002 FY 2003 FY 2004 FY 2005 Q1 2006

RGU AddsRGU Adds

Penetration of Penetration of Homes PassedHomes Passed 79.3%79.3% 80.1%80.1% 79.7%79.7% 86.1%86.1% 87.9% 87.9%

10

Mediacom Phone Rollout

1.6 million 1.6 million homes homes

marketed Q1 marketed Q1 20062006

0.9 million 0.9 million additional additional homes by homes by YE 2006YE 2006

Total homes passed = 2.8 millionTotal homes passed = 2.8 millionMediacom Phone CustomersMediacom Phone Customers

0

46,000

Q2 2005 Q1 2006

11

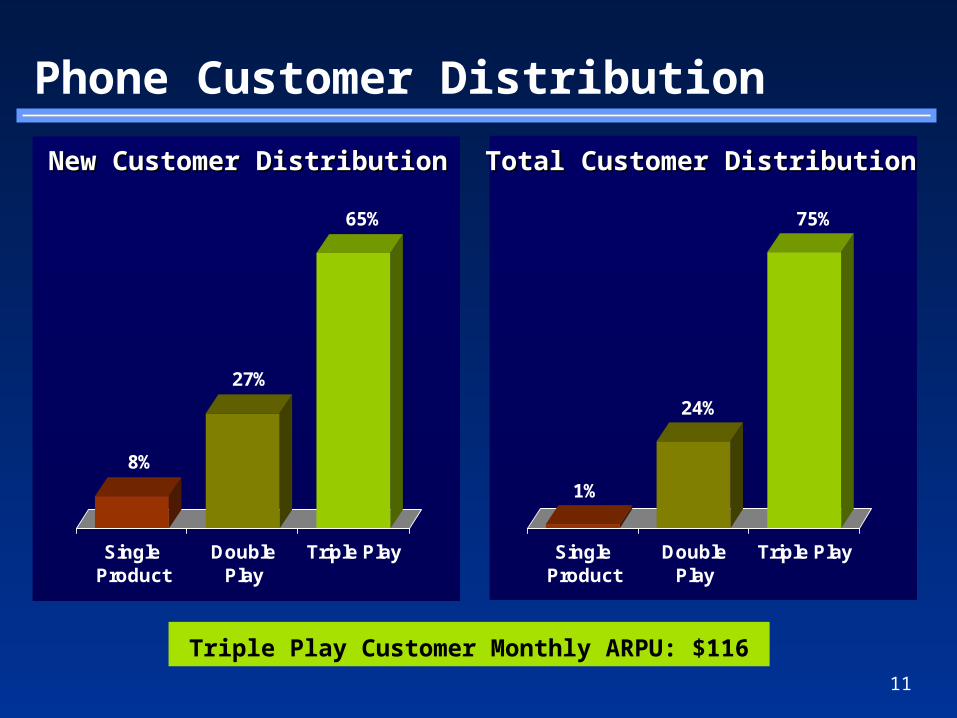

Phone Customer Distribution

8%

27%

65%

SingleProduct

DoublePlay

Triple Play

Triple Play Customer Monthly ARPU: $116

1%

24%

75%

SingleProduct

DoublePlay

Triple Play

New Customer DistributionNew Customer Distribution Total Customer DistributionTotal Customer Distribution

12

Phone’s Ripple Effect

1.3 million1.3 millionhomeshomes

1.5 million homes1.5 million homes(customer relationships)(customer relationships)

MEDIACOM’sMEDIACOM’sOPPORTUNITY:OPPORTUNITY:

Total Homes Passed = 2.8 millionTotal Homes Passed = 2.8 million

New video, voice and New video, voice and data customersdata customers

Incremental RGU Incremental RGU penetrationpenetration

13

MSO-RBOC Footprint Overlap

91%

9%

44%

35%

4%

17%

36%

48%

6%

10%

38%

39%

11%

12%

36%

45%

2%

17%

19%

68%

0%

13%

17%

56%

18%

9%

13%

26%

31%

30%

Cablevision Adelphia Charter Comcast Time Warner Insight Cox Mediacom

Other

Qwest

AT&T*

Verizon

100% = Total Homes Passed

Source:Source: Wall Street ResearchWall Street Research* Pro forma for AT&T-BellSouth merger* Pro forma for AT&T-BellSouth merger

14

Business Services – the Next Growth Market

Business voice penetration expected to Business voice penetration expected to converge with residential VoIP converge with residential VoIP

Estimated 250,000 businesses in Mediacom’sEstimated 250,000 businesses in Mediacom’s markets markets

Business interest in VoIP has gone from Business interest in VoIP has gone from weak to strong weak to strong

We become a full service provider to We become a full service provider to commercial marketplace commercial marketplace

15

Matt DerdeynMatt Derdeyn

Group VP, Corporate Finance and TreasurerGroup VP, Corporate Finance and Treasurer

16

MCCC – Summary Q1 06 Results

Q1 2006Q1 2006 Q4 2005Q4 2005 Q1 2005Q1 2005

Revenues ($ in millions)Revenues ($ in millions) $289.3$289.3 $280.3$280.3 $266.2$266.2

YOY GrowthYOY Growth 8.7%8.7%

Adjusted OIBDA ($ in millions)Adjusted OIBDA ($ in millions) (1) (1) $107.6$107.6 $101.1$101.1 $99.1$99.1

YOY GrowthYOY Growth 8.5%8.5%

MarginMargin 37.2%37.2% 36.1%36.1% 37.2%37.2%

Customer DataCustomer Data Q1 2006Q1 2006 Q4 2005Q4 2005 Q1 2005Q1 2005

Basic subscribersBasic subscribers 1,422,0001,422,000 1,423,0001,423,000 1,461,0001,461,000

Digital customersDigital customers 497,000497,000 494,000494,000 430,000430,000

Data customersData customers 504,000504,000 478,000478,000 407,000407,000

Phone customersPhone customers 46,00046,000 22,00022,000 --

Total Revenue Generating Units (RGU)Total Revenue Generating Units (RGU) 2,469,0002,469,000 2,417,0002,417,000 2,298,0002,298,000

Average monthly revenue Average monthly revenue

per basic subscriberper basic subscriber

$67.80$67.80 $65.52$65.52 $60.81$60.81

Year-over-year growthYear-over-year growth 11.5%11.5% 8.2%8.2% 6.5%6.5%

Average monthly revenue per RGUAverage monthly revenue per RGU $39.48$39.48 $39.11$39.11 $39.28$39.28

Average monthly data revenue per data Average monthly data revenue per data customerscustomers

$37.40$37.40 $37.33$37.33 $38.78$38.78

(1) Excludes non-cash stock compensation charges.

17

Capex Shift to Success-Based Product Growth

$0

$100

$200

$300

$400

$500

2002 2003 2004 2005 2006G

CPE/Scalable Upgrade Line Extension Support

Hurricane CapexHurricane Capex $8.1$8.1 $6.6$6.6 $2.2$2.2

$408

33%33% 52%52% 55%55% 66%66%

$241

$181$228

($ in millions)($ in millions)

$200

67%67%

Q1 2006: Q1 2006: $47.6$47.6

Massive shift to success-based investmentMassive shift to success-based investment

18

Flexible Capital Structure

Mediacom Broadband LLCSubsidiaries

Senior Debt(1) $861Unused Credit Commitments $581Senior Debt/SCF 3.4x

Mediacom Broadband LLC

Senior Notes $600Total Debt/OCF 6.1x

Mediacom LLCSubsidiaries

Senior Debt(1) $862Unused Credit Commitments $388Senior Debt/SCF(2) 4.0x

Mediacom LLC

Senior Notes $625Total Debt/OCF(2) 7.1x

Mediacom Communications Corporation

Convertible Notes $173Total Debt $3,100

Note: Note: Based on Q1 2006 data. OCF and SCF are Q1 annualized and exclude non-cash compensation charges. Pro forma for refinancings of Mediacom LLC Group Term Loan B Based on Q1 2006 data. OCF and SCF are Q1 annualized and exclude non-cash compensation charges. Pro forma for refinancings of Mediacom LLC Group Term Loan B and Mediacom Broadband Group Term Loan C on May 5, 2006.and Mediacom Broadband Group Term Loan C on May 5, 2006.

(1) Excludes letters of credit.(1) Excludes letters of credit.(2) OCF and SCF for Mediacom LLC includes cash investment income.(2) OCF and SCF for Mediacom LLC includes cash investment income.

($ in millions)($ in millions)

18

19

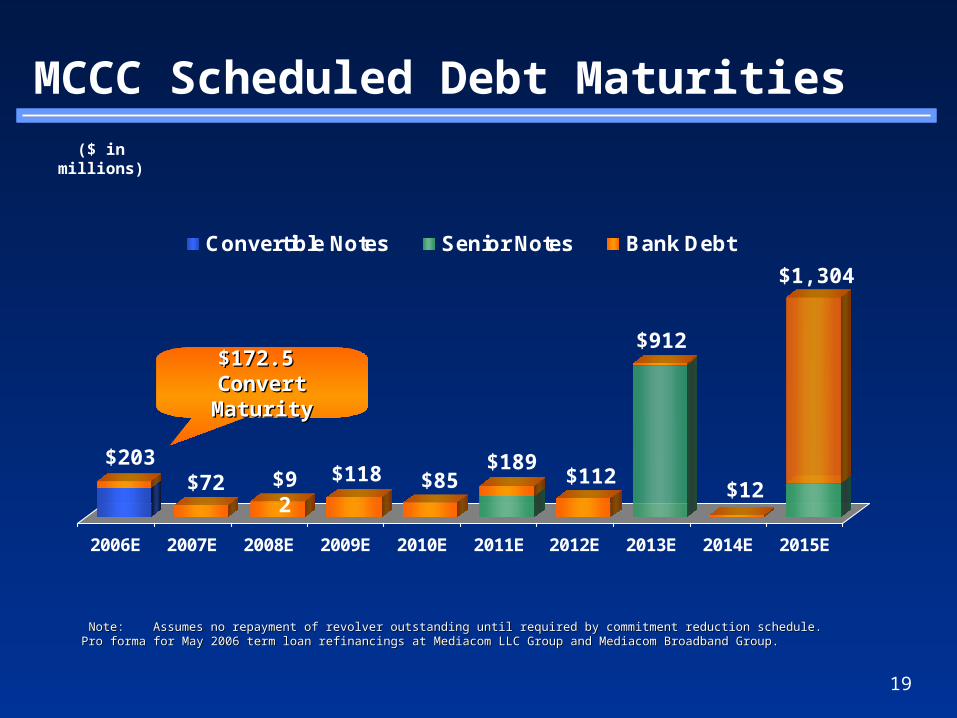

2006E 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E

Convertible Notes Senior Notes Bank Debt

Note:Note: Assumes no repayment of revolver outstanding until required by commitment reduction schedule.Assumes no repayment of revolver outstanding until required by commitment reduction schedule.

Pro forma for May 2006 term loan refinancings at Mediacom LLC Group and Mediacom Broadband Group.Pro forma for May 2006 term loan refinancings at Mediacom LLC Group and Mediacom Broadband Group.

$203$72 $118

$189$85 $112

$912

MCCC Scheduled Debt Maturities

$1,304

$12

($ in millions)

$92

$172.5 $172.5 Convert MaturityConvert Maturity

20

$437

$1,100

$844$770

$909 $871$969 $1,014

$1,014$969

$871$909

$562$600

$800

$358

FYE 2000 FYE 2001 FYE 2002 FYE 2003 FYE 2004 FYE 2005 Q1 2006PF*

Q1 2006PF**

Unused Credit Commitments Borrowing Availability

Credit Availability

Solid track record of preserving liquidity and Solid track record of preserving liquidity and maintaining ample borrowing availabilitymaintaining ample borrowing availability

** Pro forma for May 2006 term loan refinancings at Mediacom LLC Group and Mediacom Broadband Group.Pro forma for May 2006 term loan refinancings at Mediacom LLC Group and Mediacom Broadband Group.**** Pro forma for drawdown of $250.0 million Mediacom Broadband Group Term Loan D-2 and repayment of MCC 5.25% convertible notes due July 1, 2006.Pro forma for drawdown of $250.0 million Mediacom Broadband Group Term Loan D-2 and repayment of MCC 5.25% convertible notes due July 1, 2006.

20

($ in millions)

21