Wachovia Securities Databook. Corporate & Investment Banking Product Expertise.

Upload

claire-knightCategory

view

215download

0

1

Wachovia Securities Convertible Securities

Conference March 5th, 2003

2

Certain matters discussed in this presentation are "forward-looking statements" intended to qualify for the safe harbors from liability established by the Private Securities Litigation Reform Act of 1995. These forward-looking statements can generally be identified as such because of the context of the statement and may include words such as "believes," "anticipates," "expects," "estimates," or words of similar import. Similarly, statements that describe Hanover's future plans, objectives or goals are also forward-looking statements. Such forward-looking statements are subject to certain risks and uncertainties, which could cause actual results to differ materially from those anticipated as of the date of this presentation. These risks and uncertainties include: the loss of market share through competition; reduced profit margins resulting from increased pricing pressure in our business, the introduction of competing technologies by other companies; a prolonged, substantial reduction in oil and gas prices which could cause a decline in the demand for Hanover's compression and oil and gas production equipment; new governmental safety, health and environmental regulations which could require Hanover to make significant capital expenditures; inability to successfully integrate acquired businesses; currency fluctuations; changes in economic or political conditions in the countries in which Hanover operates; adverse results of regulatory inquiries or shareholder litigation; inability to comply with loan and lease covenants; inability to access capital markets; and legislative changes in the various countries in which Hanover does business. The forward-looking statements included in this presentation are only made as of the date of this presentation, and Hanover undertakes no obligation to publicly update such forward-looking statements to reflect subsequent events or circumstances. A discussion of these factors is included in the Company's periodic reports filed with the Securities and Exchange Commission.

Forward Looking Statements

3

Corporate Overview

Market Capitalization (2/25/03): $ 632 MM

Enterprise Value (2/25/03)(1) $2,413 MM

S&P/Moody’s ratings: BB-/Ba3

2002 Revenues: $1,029 MM

(1) Includes Synthetic Lease Financings

2002 Revenue MixBusiness Segment

2002 Revenue MixBy Geographic Region

Domestic 70%

International 30%

Comp. Fab 11%

Other 2%

Domestic Compression Rental 32%

Parts & Service 22%

Prod. Equip. Fab 15%

International Compression Rental 18%

4

Hanover History

• Dramatic Growth Since 1997 Fueled by Acquisitions and Management Focus on Top Line Growth

• Positives of Growth Market Leader in Outsourced Compression Critical Mass for Global Solutions Expanded Business Lines

• Negatives of Growth Growth Exceeded Infrastructure Control Environment Strained Increased Leverage Lack of Consolidation of Acquired Company

Operations

• 2002 Review Restatements, SEC Inquiry, and Shareholder

Lawsuits Management and Organizational Changes New Phase in Hanover History

$199$286

$1,029

$318

$1,041

$563

1997 1998 1999 2000 2001 2002

39% CAGR

Total Revenue ($ MM)

Total Debt/Total Capitalization

36%

53%55%

57%60%

62%

1997 1998 1999 2000 2001 2002*

*As of 9/30/02

5

Hanover – The Future

• Integrate Hanover’s Systems and Operations Enabling the Company to Move Quickly to React to Our Customer's Needs – Both Domestically and Internationally

• Become the Solutions Provider for Our Customers Surface Production and Processing Needs

• Change Operations and Management Focus to Increased Capital Discipline and Improving Returns on Capital Employed

• Structure Organization Around Geographical Business Units

• Focus on Key Product Lines:– Services (Includes all Rental Income)– 3rd Party Parts and Services– Packaging (Compression, Processing, Power, etc.)– Alternative Fuels

6

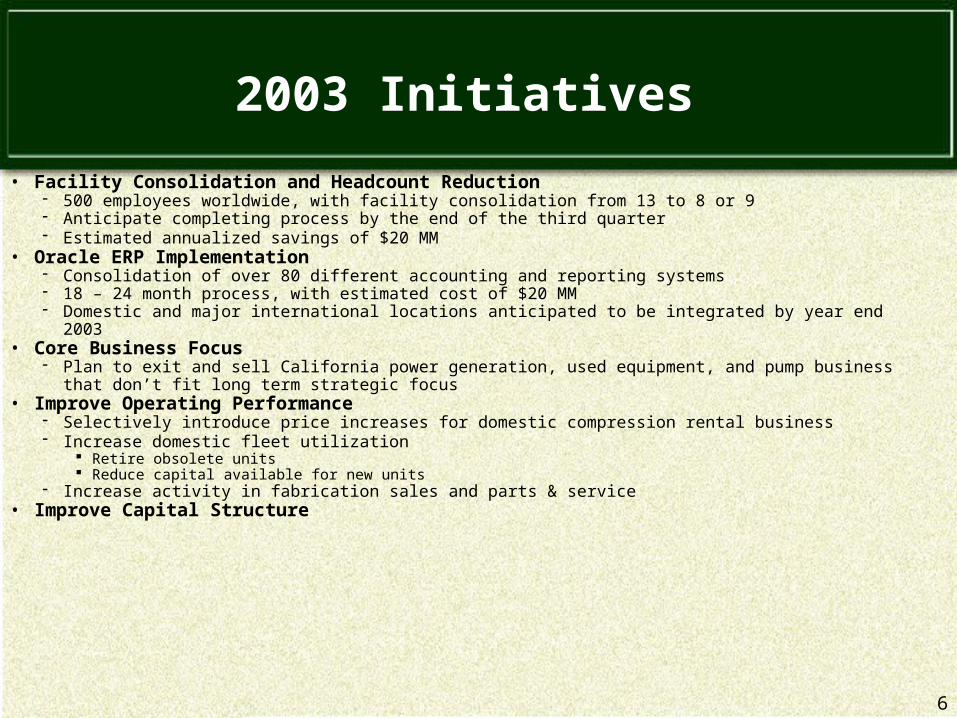

2003 Initiatives

• Facility Consolidation and Headcount Reduction 500 employees worldwide, with facility consolidation from 13 to 8 or 9 Anticipate completing process by the end of the third quarter Estimated annualized savings of $20 MM

• Oracle ERP Implementation Consolidation of over 80 different accounting and reporting systems 18 – 24 month process, with estimated cost of $20 MM Domestic and major international locations anticipated to be integrated by year end 2003

• Core Business Focus Plan to exit and sell California power generation, used equipment, and pump business that don’t fit long

term strategic focus• Improve Operating Performance

Selectively introduce price increases for domestic compression rental business Increase domestic fleet utilization

Retire obsolete units Reduce capital available for new units

Increase activity in fabrication sales and parts & service• Improve Capital Structure

7

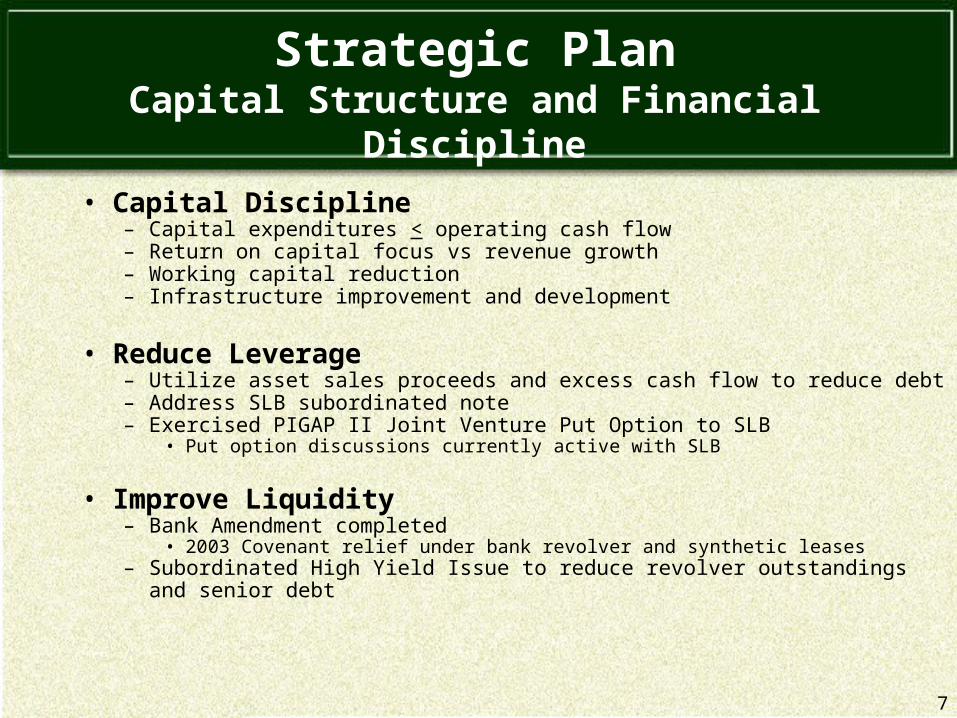

Strategic PlanCapital Structure and Financial Discipline

• Capital Discipline– Capital expenditures < operating cash flow– Return on capital focus vs revenue growth– Working capital reduction– Infrastructure improvement and development

• Reduce Leverage– Utilize asset sales proceeds and excess cash flow to reduce debt– Address SLB subordinated note – Exercised PIGAP II Joint Venture Put Option to SLB

• Put option discussions currently active with SLB

• Improve Liquidity– Bank Amendment completed

• 2003 Covenant relief under bank revolver and synthetic leases– Subordinated High Yield Issue to reduce revolver outstandings and senior debt

8

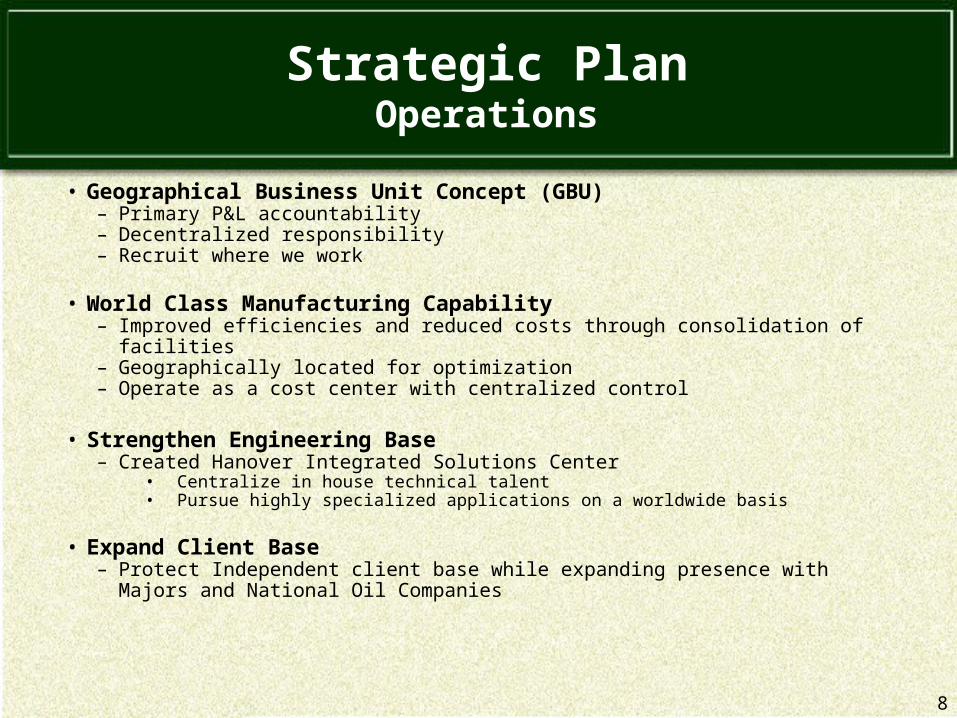

Strategic PlanOperations

• Geographical Business Unit Concept (GBU)– Primary P&L accountability– Decentralized responsibility– Recruit where we work

• World Class Manufacturing Capability– Improved efficiencies and reduced costs through consolidation of facilities– Geographically located for optimization– Operate as a cost center with centralized control

• Strengthen Engineering Base– Created Hanover Integrated Solutions Center

• Centralize in house technical talent • Pursue highly specialized applications on a worldwide basis

• Expand Client Base– Protect Independent client base while expanding presence with Majors and

National Oil Companies

9

Growth Opportunities

• Demand for Natural Gas

• Domestic Outsourcing

• Large Scale International Projects

• Total Solutions Focus

10

1994 1995 1996 1997 1998 1999 2000 2001 2002

Domestic International

Rental Fleet Growth

4,000

3,500

3,0002,500

2,000

1,500

1,000

500Ho

rse

po

wer

– (

00

0’s

)

11

Worldwide Operations

12

Total Solutions Capabilities

13

Global Market Share

• E&P Estimated Annual Capital Expenditures:– $115 billion per year– Exxon $9.9B, Shell $8B, ChvTex $7.5B, BP $7.5B, Woodside $2.4B– Does not include NOCs: (Pemex, PDVSA, Sonotrac, Sonogal, ADNOC,

etc)

• Compression Sales:– 10% of global market

• Compression Rental Revenue:– 15% of potential US market

• Standard Production Equipment– 12% of US market

• Custom Production Equipment– 4% of global market

14

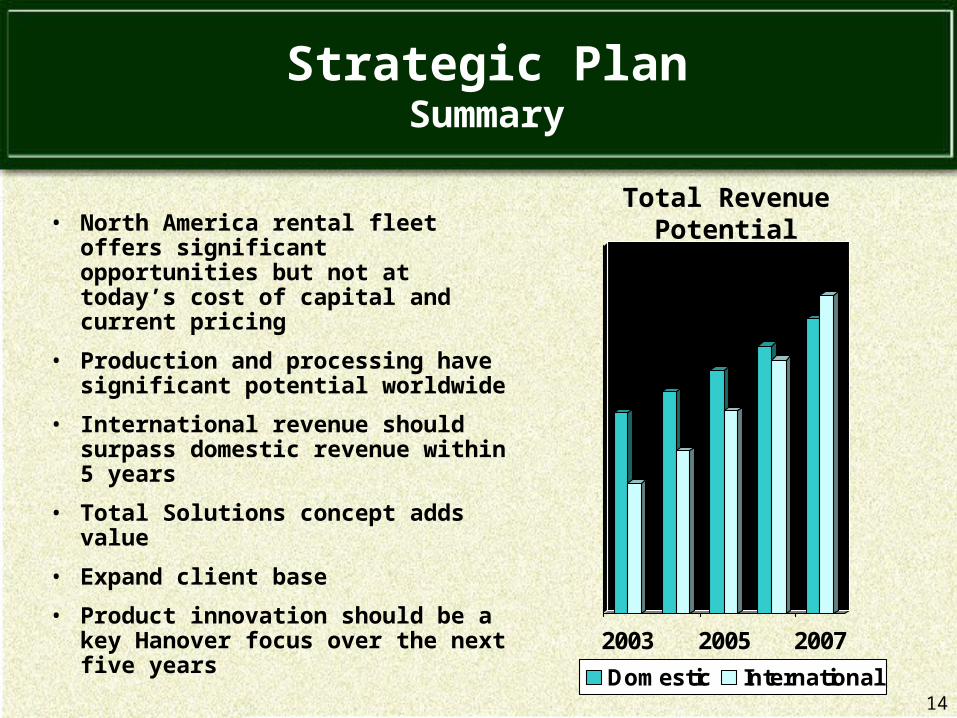

Strategic PlanSummary

• North America rental fleet offers significant opportunities but not at today’s cost of capital and current pricing

• Production and processing have significant potential worldwide

• International revenue should surpass domestic revenue within 5 years

• Total Solutions concept adds value

• Expand client base

• Product innovation should be a key Hanover focus over the next five years

2003 2005 2007

Domestic International

Total Revenue Potential

15

Financial Overview

16

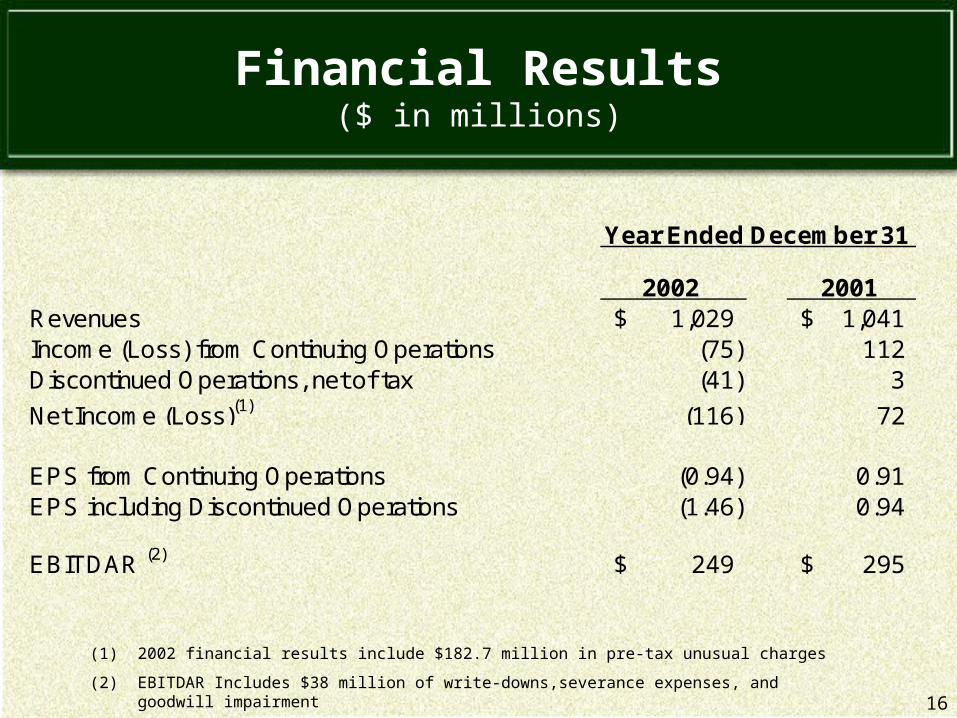

2002 2001Revenues 1,029$ 1,041$ Income (Loss) from Continuing Operations (75) 112Discontinued Operations, net of tax (41) 3

Net Income (Loss)(1) (116) 72

EPS from Continuing Operations (0.94) 0.91EPS including Discontinued Operations (1.46) 0.94

EBITDAR (2) 249$ 295$

Year Ended December 31

Financial Results($ in millions)

(1) 2002 financial results include $182.7 million in pre-tax unusual charges

(2) EBITDAR Includes $38 million of write-downs,severance expenses, and goodwill impairment

17

0

50

100

150

200

250

300

350

2001 2002

0

50

100

150

200

250

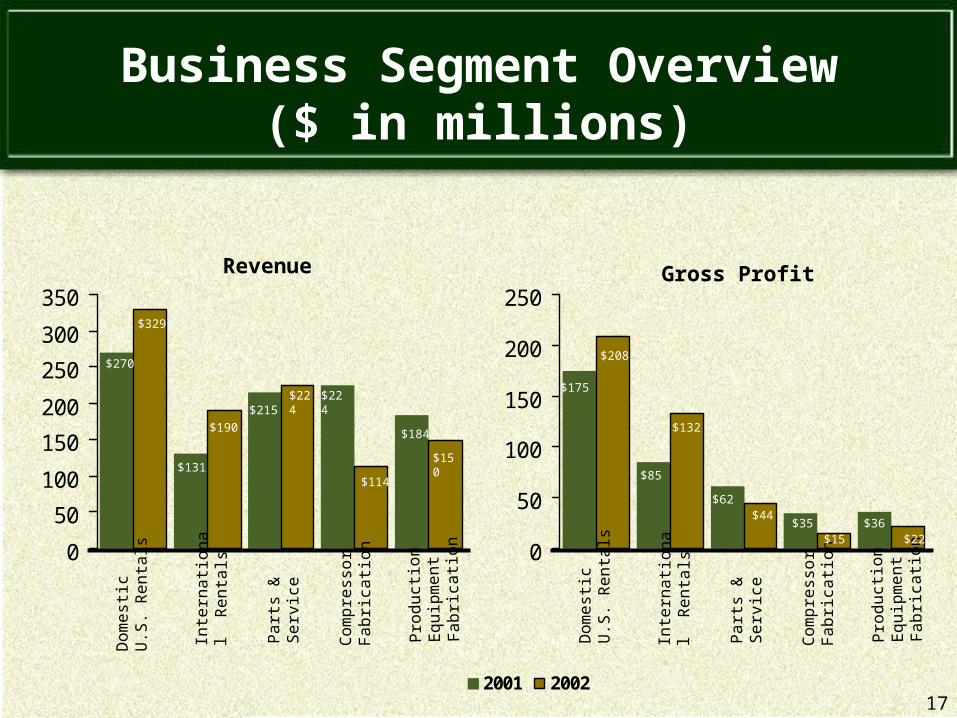

Business Segment Overview($ in millions)

Co

mp

ress

or

Fa

bric

atio

n

Do

me

stic

U.S

. R

en

tals

Pa

rts

&

Se

rvic

e

Inte

rna

tion

al

Re

nta

ls

Pro

du

ctio

n

Eq

uip

me

nt

Fa

bric

atio

n$131

$190

$270

$329

$215$224 $224

$114

$184

$150

Co

mp

ress

or

Fa

bric

atio

n

Do

me

stic

U.S

. R

en

tals

Pa

rts

&

Se

rvic

e

Inte

rna

tion

al

Re

nta

ls

Pro

du

ctio

n

Eq

uip

me

nt

Fa

bric

atio

n

$175

$208

$85

$132

$62$44

$35$15

$36$22

Revenue Gross Profit

18

Compression Rental Fleet Composition by Geographic Region

860 HP

International

2,654 HPDomestic

Total Horsepower (000’s)3,514 HP

International Horsepower (000’s)860 HP

Venezuela

41%

Other 15%

Mexico

11%

Canada11%

Argentina22%

As of December 31, 2002

19

Impact of Changes in Utilization

EBITDA

87 93

$2.5 MM per 1% Increase

% Fleet Utilization

$15 MM

$0

Represents Annualized Impact

20

Impact of Changes in Pricing

$/HP per month

EBITDA

$35 MM

$15.00$13.50

$3.5 MM per $0.15/HP Increase

$0

Represents Annualized Impact

21

Key Investment Considerations

• Total Solutions Provider

• Refocused Operating Model

• Strong Diversified Cash Flow Stream

• Significant Growth Opportunities

• Strengthened Management Team and Board Of Directors

• Focus On Reducing Leverage