Growth Crossings: Africa's Role Investment in African Infographics

Understanding the role of the Ladder of InvestmentBusiness-to-Business Communications

Barney Lane30 March 2006

Ovum Paper.qxp 6/6/06 11:36 Page 1

2 BUSINESS TO BUSINESS COMMUNICATIONS | UNDERSTANDING THE ROLE OF THE LADDER OF INVESTMENT

Understanding the role of the Ladder of InvestmentBusiness-to-Business Communications

1 EXECUTIVE SUMMARY

BT commissioned Ovum Consulting to fill a gap inthe current literature which focuses the Ladder ofInvestment (LOI) concept predominantly on therequirements of the consumer sector. This reporttherefore focuses specifically on the application ofthe LOI to business services. The views expressed inthis Report are those of the authors.

There are two main conclusions. To enable aneffective European market in the provision ofcommunications to the business community it isnecessary for regulators to:

consider allowing multiple access services, or LOIrungs, for operators serving multi-site businesscustomers even where such services have beenwithdrawn from operators serving residentialcustomers; and

modify the LOI so that, rather then being based on atime-bound pre-commitment for regulatorywithdrawal based on a prediction of competitiveentry, the criterion for the removal of rungs forbusiness services should be the actual state ofcompetition.

Some regulatory experts recommend a phasedwithdrawal from access regulation to encouragealternative operators to develop their own facilitiesin competition with the incumbent. Some argue forwithdrawing services at predetermined intervals.Professor Martin Cave, for example, has argued thataccess services that are economically replicableshould be withdrawn after two to three years.

These arguments partly reflect a view that, to bebeneficial and sustainable in the long-run,competition should be only minimally dependent onthird-party access. Regulation is not only expensiveto administer but can also distort markets and limitincentives to invest in next-generation networks andservices. Competition is therefore to be encouragedto the maximum extent feasible.

Although the principles of regulation are largely thesame regardless of whether they are applied to thebusiness or residential sectors, the practicalapplication differs significantly. This results from thefact that business services are typically supplied by asingle supplier to multiple sites and the muchgreater complexity of services offered to businesscustomers.

The communications needs of business customersare complex and demanding. Business customerstypically operate in a range of locations that includea corporate HQ, regional offices, international officesand home working facilities. Business customersstrongly favour the appointment of a single partnerto serve their communications requirements on anational and, increasingly, on a global basis.Although multiple sourcing is often used for morebasic services, for complex services it is bothexpensive and inefficient.

Access is crucial to competition for multi-sitebusiness customers – absent regulatory measuresto ensure the availability of access in all regions inwhich the development of own-infrastructure is noteconomically viable, customers will default to theincumbent. Margins for large business contracts aregenerally low and without regulated access wherenecessary, entrants face substantial difficulties inproviding effective competition in situations wherefailure to provide access to just one regional site oreven to a small number of home working siteswould result in the loss of the entire contract.

Pre-commitments to the withdrawal of regulatedaccess under the LOI thus have a high cost of error ifthe initial calibration is too optimistic about thestrides that new entrants can make in self-provingaccess. This is an important difference between B2Band B2C services that has far-reaching implicationsfor regulation. For B2C services, the damage causedby the premature withdrawal of an access productwould be largely confined to the geographic areas inwhich the access product has been withdrawn.

But demand for multi-site B2B services createslinkages between regions - entry needs to happeneverywhere if it is to happen at all. The danger ofpremature withdrawal would not just be to force exitfrom the isolated regions where infrastructure isless developed, but potentially from the marketaltogether. As a result, following through with such acommitment before the market is ready couldpermanently harm competition in B2B multi-sitecommunications services.

These considerations have profound implications forregulatory policy in the EU. Communicationsservices are key enablers of the ICT services andapplications in which European business must investif they are to compete effectively with their globalrivals.

Ovum Paper.qxp 6/6/06 11:36 Page 2

Understanding the role of the Ladder of InvestmentBusiness-to-Business Communications

BUSINESS TO BUSINESS COMMUNICATIONS | UNDERSTANDING THE ROLE OF THE LADDER OF INVESTMENT 3

1 Executive Summary 2

2 Introduction 4

3 The Ladder of Investment Framework 5

4 Achieving Competition in Business-to-Business Services 6

4.1 The Characteristics of B2B Services 6

4.2 Multi-Site Services 7

4.3 LOI rungs required for competitive B2B services 8

5 Applying the Ladder of Investment to B2B services 8

5.1 Professor Cave : “Making the Ladder of Investment Operational” 8

5.2 Assessment in relation to B2B services 9

5.2.1 Platform Migration 10

5.2.2 Applying the LOI to Multi-Site B2B Services: Conclusions 10

5.3 Designing a LOI for B2B services 10

6 The Contribution of B2B Communications Services to Economic Performance 11

6.1 Linkages between ICT Deployment and Economic Performance 11

6.1.1 How does ICT Investment Impact Economic Performance? 11

6.1.2 Quantifying the Impact 12

6.2 Policy Implications 12

6.2.1 Effect of Regulatory Policy on service take-up, competition and investment 13

6.3 Regulatory Policy, ICT and Investment: Summary 15

7 Conclusion 16

8 About the Author 16

Ovum Paper.qxp 6/6/06 11:36 Page 3

4 BUSINESS TO BUSINESS COMMUNICATIONS | UNDERSTANDING THE ROLE OF THE LADDER OF INVESTMENT

Understanding the role of the Ladder of InvestmentBusiness-to-Business Communications4

1 ERG Common Position onthe approach toAppropriate remedies inthe new regulatoryframework, 2003

2 INTRODUCTION

The “Ladder of Investment” (LOI) is not a new ideabut it has received unprecedented attentionfollowing a paper by the European RegulatorsGroup (ERG) in 2003.1 Most studies have focused onits applicability to business-to-consumer (B2C)services with relatively little research on itsrelevance to business-to-business (B2B). The aimof this study is to fill this gap.

We find that the needs of business customers differfrom those of residential customers in severalimportant respects, particularly the following:

• The multi-site nature of business premises andservices compared with the single site nature ofresidential premises

• The far greater degree of variety or productdifferentiation between the offerings ofbusiness compared with residential serviceproviders.

Some commentators use the LOI framework torecommend a pre-determined timetable of exitfrom regulation as competition develops. We findthat this is unlikely to work for B2B services. Whenthe actual outcome of investment differs even to asmall degree from assumptions made at the timeof the commitment, the costs of withdrawing anaccess product when it is still needed arepotentially much larger for B2B than B2C services.In such circumstances, when the main source ofthe uncertainty and risk is the outcome ofinvestment programmes, a pre-commitment to aphased withdrawal of regulated access mayactually deter investment - precisely the oppositeof the intended result.

In some cases, regulators may choose to commit toa phased withdrawal of regulation based on a beliefthat this maximises the long-run welfare ofconsumers. Although a full evaluation of thisapproach is beyond the scope of this paper, ourthesis is that it is unlikely to lead to an optimaloutcome in B2B markets. Therefore, a different

approach is needed. One candidate would be for aregulator, when it removes a LOI rung, to maintainit for B2B services. We do not consider in detailhow such a policy might be implemented inpractice, although we offer some suggestions forconsideration.

In balancing the needs of businesses andconsumers, regulators may wish to consideradopting a separate approach for each. Anexample of such an approach would be to maintainregulated access products necessary to providemulti-site B2B services even where they have beenwithdrawn for use with B2C services.

A drawback of such an approach is greaterregulatory complexity, which has costs. It isreasonable to ask whether the benefits of such anapproach exceed the costs. A comprehensive cost-benefit analysis of this option is beyond the scopeof this report. However, to provide some insight onthe benefits side, we review some empiricalevidence relating to how such an approach mightcontribute to productivity growth throughstimulating ICT investment by businesses.

The remainder of this paper is structured asfollows.

Section 3 sets out the LOI framework in broadoverview.

Section 4 outlines some of the specialcharacteristics of B2B services that need to betaken into account when understanding how theLOI framework applies to these services. It alsoconsiders the applicability of Professor Cave’s LOIrecommendations to B2B services.

Section 5 reviews some of the empirical evidenceon the relationship between ICT investment andproductivity and the implications of such arelationship, if any, for the regulation of B2Bservices.

Section 6 presents our conclusions.

Ovum Paper.qxp 6/6/06 11:36 Page 4

Understanding the role of the Ladder of InvestmentBusiness-to-Business Communications5

BUSINESS TO BUSINESS COMMUNICATIONS | UNDERSTANDING THE ROLE OF THE LADDER OF INVESTMENT 5

2 The viability of buildingalternative localinfrastructure for businesscustomers variessignificantly with thebandwidth of the servicesoffered.

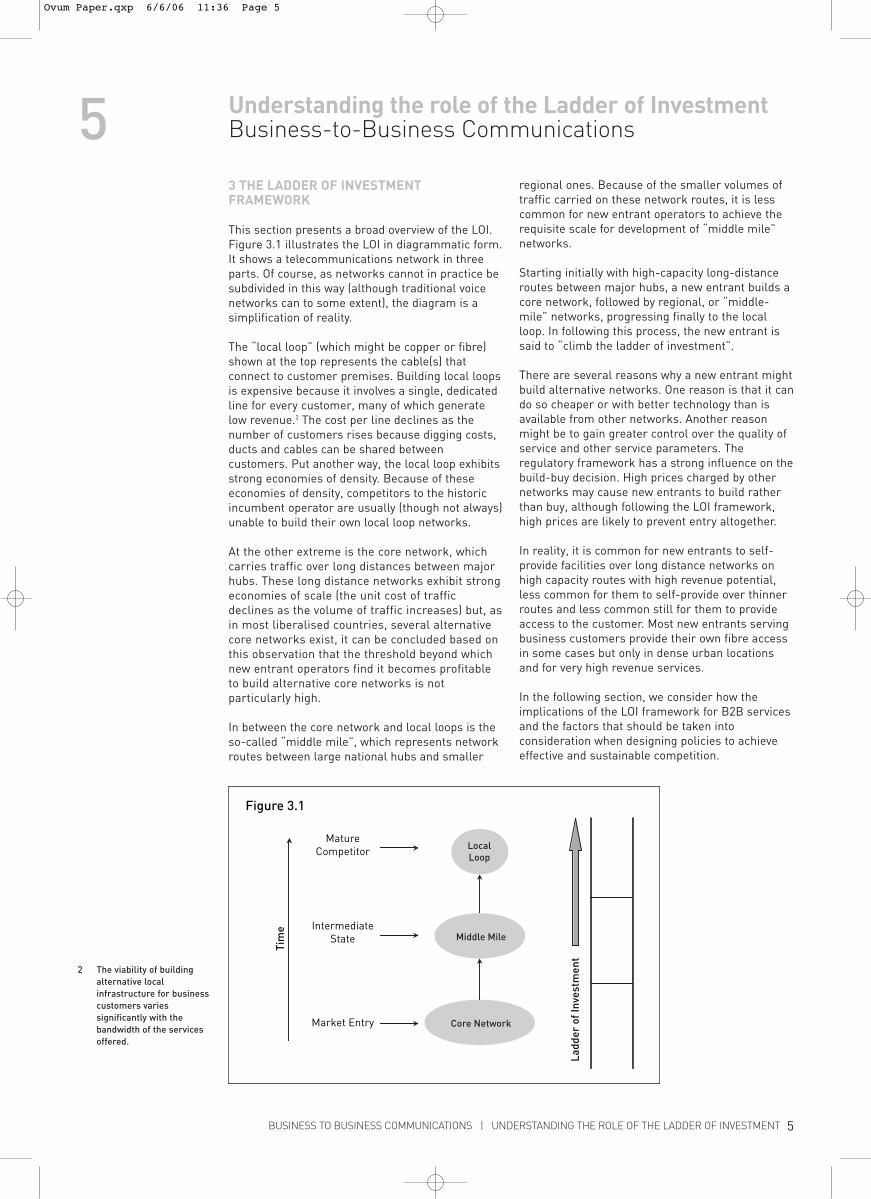

3 THE LADDER OF INVESTMENTFRAMEWORK

This section presents a broad overview of the LOI.Figure 3.1 illustrates the LOI in diagrammatic form.It shows a telecommunications network in threeparts. Of course, as networks cannot in practice besubdivided in this way (although traditional voicenetworks can to some extent), the diagram is asimplification of reality.

The “local loop” (which might be copper or fibre)shown at the top represents the cable(s) thatconnect to customer premises. Building local loopsis expensive because it involves a single, dedicatedline for every customer, many of which generatelow revenue.2 The cost per line declines as thenumber of customers rises because digging costs,ducts and cables can be shared betweencustomers. Put another way, the local loop exhibitsstrong economies of density. Because of theseeconomies of density, competitors to the historicincumbent operator are usually (though not always)unable to build their own local loop networks.

At the other extreme is the core network, whichcarries traffic over long distances between majorhubs. These long distance networks exhibit strongeconomies of scale (the unit cost of trafficdeclines as the volume of traffic increases) but, asin most liberalised countries, several alternativecore networks exist, it can be concluded based onthis observation that the threshold beyond whichnew entrant operators find it becomes profitableto build alternative core networks is notparticularly high.

In between the core network and local loops is theso-called “middle mile”, which represents networkroutes between large national hubs and smaller

regional ones. Because of the smaller volumes oftraffic carried on these network routes, it is lesscommon for new entrant operators to achieve therequisite scale for development of “middle mile”networks.

Starting initially with high-capacity long-distanceroutes between major hubs, a new entrant builds acore network, followed by regional, or “middle-mile” networks, progressing finally to the localloop. In following this process, the new entrant issaid to “climb the ladder of investment”.

There are several reasons why a new entrant mightbuild alternative networks. One reason is that it cando so cheaper or with better technology than isavailable from other networks. Another reasonmight be to gain greater control over the quality ofservice and other service parameters. Theregulatory framework has a strong influence on thebuild-buy decision. High prices charged by othernetworks may cause new entrants to build ratherthan buy, although following the LOI framework,high prices are likely to prevent entry altogether.

In reality, it is common for new entrants to self-provide facilities over long distance networks onhigh capacity routes with high revenue potential,less common for them to self-provide over thinnerroutes and less common still for them to provideaccess to the customer. Most new entrants servingbusiness customers provide their own fibre accessin some cases but only in dense urban locationsand for very high revenue services.

In the following section, we consider how theimplications of the LOI framework for B2B servicesand the factors that should be taken intoconsideration when designing policies to achieveeffective and sustainable competition.

LocalLoop

Tim

e

Ladd

er o

f Inv

estm

ent

Middle Mile

Core Network

IntermediateState

Market Entry

MatureCompetitor

Figure 3.1

Ovum Paper.qxp 6/6/06 11:36 Page 5

6 BUSINESS TO BUSINESS COMMUNICATIONS | UNDERSTANDING THE ROLE OF THE LADDER OF INVESTMENT

Understanding the role of the Ladder of InvestmentBusiness-to-Business Communications64 ACHIEVING COMPETITION IN BUSINESS-TO-BUSINESS SERVICES

This section outlines the key features of Business-to-Business (B2B) services, in so far as is relevantto applying the LOI. For the present purpose, twodifferences between B2B and B2C are particularlyimportant. These are:

The characteristics of B2B services (covered insection 4.1). Key points here are that B2B servicesare:

Largely platform independent. Services are largelyindependent of the network infrastructure overwhich they run. This is a key distinction betweenB2B and B2C services: in the latter, the service isusually integral to the network (this will change as“Next Generation Networks” based on a unifiedcore become more widespread);

Complex and diverse. The range of B2B services ismuch wider, more complex and has greater scopefor product differentiation than B2C services.

The multi-site nature of B2B services (covered insection 4.2). B2B services are usually provided tomultiple sites, often spanning internationalboundaries.

Section 4.3 considers, in the light of the previoussections, which ladder rungs are necessary for acompetitive market for B2B services to operators. Insection 4.4 we outline some particular issues for policyarising from the international scope of B2B services.

4.1 THE CHARACTERISTICS OF B2B SERVICES

Figure 4.1 illustrates the characteristics of B2Bservices. The key point to observe in figure 4.1 isthe scope for product differentiation in B2Bservices, which is substantially greater in B2Bservices compared with B2C services.

In B2B services, the access pipe, represented bythe inner circle in figure 4.1 is usually providedeither by a third party leased line, including newtechnologies such as Ethernet. Access may bedistinguished by bandwidth and quality of servicefeatures but little else. Access is a “low level”service (in terms of the OSI network layer model)and therefore highly platform independent,meaning that, as illustrated in figure 4.1, just aboutany electronic communications service can runover it.

The key differentiators between the offerings ofdifferent B2B service providers are theapplications, some of which are represented in theouter circle of figure 4.1. Any combination of theapplications shown, or all of them at the sametime, can be offered over the same access pipe. Inthe current context, the B2B applications underconsideration have at least three importantproperties:

• developing applications is R&D intensive,involving substantial sunk costs and risk.Sometimes the applications are developed in-house by the service provider. Sometimes productdevelopment can be outsourced to specialists

AccessOwn fibre or third party

(usually leased linefrom SMPO),

differentiated by bandwidthand QoS features

Applications

Remote Access

Data Warehousing

Storage and Backup

Voice VPNMs to multi-sites

IP VPNs

Non-geographicnumbers

Least-cost routing

Data VPNs to multi-sites

Security, eg Firewall,

content filtering

Internet Access

InternalLAN/WLAN

Management

VoIP

Video Conferencing

Web-Hosting

Figure 4.1: Nature of B2B services

Ovum Paper.qxp 6/6/06 11:36 Page 6

Understanding the role of the Ladder of InvestmentBusiness-to-Business Communications7

BUSINESS TO BUSINESS COMMUNICATIONS | UNDERSTANDING THE ROLE OF THE LADDER OF INVESTMENT 7

• the quality, range and diversity of theapplications offered differ substantially fromone operator to another

• providing these applications often involves ahigh degree of bespoke tailoring to eachindividual customer’s needs. There are very fewone-size-fits-all products in this market andcustomisation involves a high fixed cost.

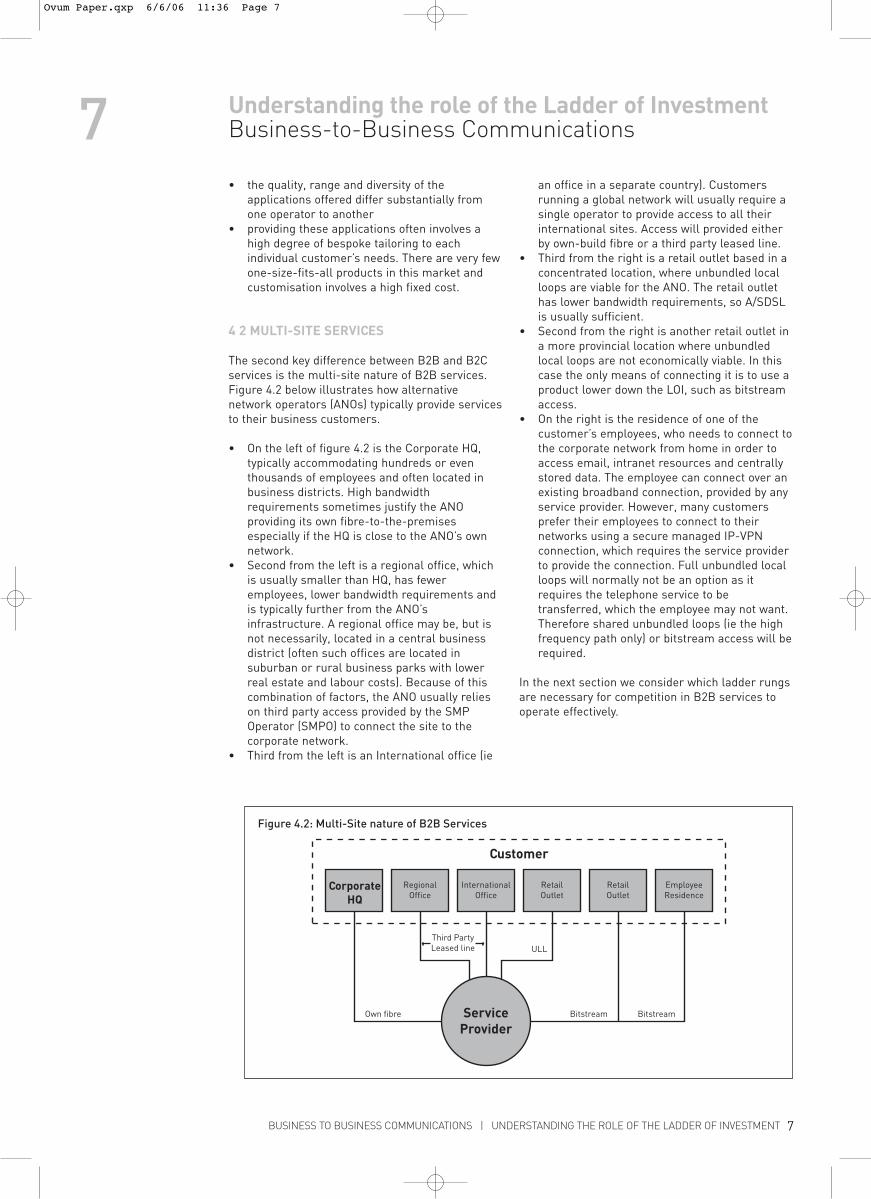

4 2 MULTI-SITE SERVICES

The second key difference between B2B and B2Cservices is the multi-site nature of B2B services.Figure 4.2 below illustrates how alternativenetwork operators (ANOs) typically provide servicesto their business customers.

• On the left of figure 4.2 is the Corporate HQ,typically accommodating hundreds or eventhousands of employees and often located inbusiness districts. High bandwidthrequirements sometimes justify the ANOproviding its own fibre-to-the-premisesespecially if the HQ is close to the ANO’s ownnetwork.

• Second from the left is a regional office, whichis usually smaller than HQ, has feweremployees, lower bandwidth requirements andis typically further from the ANO’sinfrastructure. A regional office may be, but isnot necessarily, located in a central businessdistrict (often such offices are located insuburban or rural business parks with lowerreal estate and labour costs). Because of thiscombination of factors, the ANO usually relieson third party access provided by the SMPOperator (SMPO) to connect the site to thecorporate network.

• Third from the left is an International office (ie

an office in a separate country). Customersrunning a global network will usually require asingle operator to provide access to all theirinternational sites. Access will provided eitherby own-build fibre or a third party leased line.

• Third from the right is a retail outlet based in aconcentrated location, where unbundled localloops are viable for the ANO. The retail outlethas lower bandwidth requirements, so A/SDSLis usually sufficient.

• Second from the right is another retail outlet ina more provincial location where unbundledlocal loops are not economically viable. In thiscase the only means of connecting it is to use aproduct lower down the LOI, such as bitstreamaccess.

• On the right is the residence of one of thecustomer’s employees, who needs to connect tothe corporate network from home in order toaccess email, intranet resources and centrallystored data. The employee can connect over anexisting broadband connection, provided by anyservice provider. However, many customersprefer their employees to connect to theirnetworks using a secure managed IP-VPNconnection, which requires the service providerto provide the connection. Full unbundled localloops will normally not be an option as itrequires the telephone service to betransferred, which the employee may not want.Therefore shared unbundled loops (ie the highfrequency path only) or bitstream access will berequired.

In the next section we consider which ladder rungsare necessary for competition in B2B services tooperate effectively.

Customer

Own fibre Bitstream Bitstream

Third PartyLeased line ULL

CorporateHQ

RegionalOffice

InternationalOffice

RetailOutlet

RetailOutlet

EmployeeResidence

ServiceProvider

Figure 4.2: Multi-Site nature of B2B Services

Ovum Paper.qxp 6/6/06 11:36 Page 7

8 BUSINESS TO BUSINESS COMMUNICATIONS | UNDERSTANDING THE ROLE OF THE LADDER OF INVESTMENT

Understanding the role of the Ladder of InvestmentBusiness-to-Business Communications8

3 As Ethernet is increasinglybecoming the accesstechnology of choice forbusiness customers, thismay also be required as analternative to leased lines.

4 Leased lines need to beavailable at a variety ofdifferent bandwidths.Furthermore, they mustinclude terms andconditions to facilitateeasy migration to differentbandwidths as demandschange.

5 Bitstream access needsoffer a variety of quality ofservice features such asCBR, UBR, r-t, n-rt) toallow greaterdifferentiation andinnovation.

6 “Making the ladder ofinvestment operational”,Professor Cave (2004)

4.3 LOI RUNGS REQUIRED FOR COMPETITIVEB2B SERVICES

From the above, it should be clear that for ANOs toprovide service to a typical multi-site customer, thefollowing “ladder rungs” should be available:

• third party leased lines, short and long,including substitute technologies to traditionalleased lines such as ethernet.3 Short leasedlines to serve offices in concentrated locationsclose to the ANO’s network infrastructure,longer lines to serve sites in less concentratedlocations

• third party leased lines to serve internationalsites (supra-national organisations such as theEuropean Commission and the WTO have animportant role to play to ensure that leasedlines are available under liberal conditions toallow service providers to provide serviceinternationally)4

• Unbundled Local Loops (ULL) where this is aneconomically viable access methodology

• bitstream access to serve small sites (eg retailoutlets) in provincial locations5

• bitstream access to connect employees to thecorporate network via a secure IP-VPN (sharedaccess where ULL is a viable option)

If any of the LOI rungs are not available to the ANOcommunity, this may result in the customer havingno choice but to take service from the SMPOperator (SMPO).

5 APPLYING THE LADDER OF INVESTMENTTO B2B SERVICES

Most literature on the LOI has focused on itsapplication to B2C services. In this section weconsider some of the issues that arise whenapplying the LOI framework to B2B services. Atypical and well-known approach is that advocatedby Professor Cave6, which interprets the LOI as amodel whereby regulators actively manage aphased transition between infrastructure andservice competition. Following this approach, asANOs ascend the ladder, rungs should be removed.We consider whether this approach should befollowed in relation to B2B services. Section 5.1outlines Professor Cave’s approach and section 5.2considers its applicability to B2B services.

We find that the existence of network externalitieswithin private corporate networks stronglysuggests that a policy of timed withdrawal ofregulated access may not be the optimal approachto ensuring long-run sustainable competition inB2B services. Furthermore, we note that the costsinvolved in migrating services from oneinterconnect platform to another are likely to be

very high for B2B services and may deter usersfrom taking service from ANOs.

Section 5.3 provides some preliminary ideas to betaken into consideration when designing a LOI toserve the needs of business customers.

5.1 PROFESSOR CAVE: “MAKING THELADDER OF INVESTMENT OPERATIONAL”

Professor Cave advocates a regulatory programmeinvolving a pre-commitment to timed withdrawalfrom regulation. This is considered important to:

• Provide ANOs with incentives to developcompeting facilities

• Reduce the costs of regulation (both in terms ofthe resources expended by the regulator andcompliance departments within the regulatedentity, and in terms of the effect of regulation inconstraining otherwise welfare enhancingactivity).

The paper envisages a market that evolves, throughsteadily diminishing access-based regulation,towards one that progressively depends less onregulation until the only access requirementsremaining relate to “non-replicable assets” –assets that cannot be economically installed bynew entrants.

Professor Cave argues that to construct ladderrungs, the regulator should study the underlyingcost structures of the activities of interest. In thecontext of DSL based broadband access, he arguesthat such a study gives rise to the following ladderrungs:

1 Access to the customer via a copper loop orshared loop

2 DSLAMs located at the local exchange3 ATM backhaul4 Access to an IP network5 Access to the world wide web via transit or

peering services6 Retailing functions (marketing, billing, helplines

etc.)

Professor Cave then advocates a timed withdrawalfrom regulation (either by increasing prices orwithdrawing regulation) from ladder rungs toencourage ANOs to develop their own facilities. Herecommends a 6-12 month withdrawal period foreasily replicable assets and a 2-3 year withdrawalperiod for less easily replicable assets.Furthermore, he emphasises the importance ofpre-announcing and committing to such a policy.

Ovum Paper.qxp 6/6/06 11:36 Page 8

Understanding the role of the Ladder of InvestmentBusiness-to-Business Communications9

BUSINESS TO BUSINESS COMMUNICATIONS | UNDERSTANDING THE ROLE OF THE LADDER OF INVESTMENT 9

7 Or failure to provide aninterconnection point on abackbone network,discriminatory accessprices or a degradedquality of service.

5.2 ASSESSMENT IN RELATION TO B2BSERVICES

Much of telecoms regulation is designed to addressproblems created by dominance in access.However, when considering how to extendcompetition to multi-site customers an additionalproblem must be addressed.

This is the phenomenon of network externalities.The existence of network externalities is wellrecognised in telecoms. As users join a network,the benefits do not just accrue to themselves, butalso to other users of the network. The significanceof network externalities can be seen in relation tovoice telephony, fax, email, the Internet and indeedalmost all network based communicationsservices. In mobile telephony, some regulatorshave allowed an additional mark-up to interconnectfees to reflect the value to other telephony users ofincreasing the number of mobile users.

The same phenomenon also exists in privatecommunications networks provided to businesscustomers. For example:

• the value of the internal telephone and emailand conferencing networks rises with thenumber of corporate employees on the samenetwork;

• the value of server-client based services suchas intranet based applications and data storageand access rises with the number of employeesable to access such services. The value of suchservices increases still further if employees areable to access them from a wide range oflocations such as from home or via wirelessdevices.

The important point about network externalities inthis context is that the full value of B2Bcommunications services will not be realised ifsome business locations cannot be connected tothe corporate network. This translates into a strongadvantage for an operator able to provideconnectivity in all locations.

It also has important implications for policybecause where an operator holds a dominantposition in access in one location or set oflocations, such dominance can in theory beleveraged across to locations in which it does nothold dominance. The greater the number oflocations in which an SMPO holds a dominantposition in access, the greater is its ability toleverage those dominant positions into othergeographic locations, even those in which it doesnot enjoy a dominant position in access.

Multi-site services may thus exhibit strong“tipping” (or unstable equilibrium) effects.

Professor Cave ’s suggestion of a gradualwithdrawal from regulation with the aim ofencouraging alternative infrastructure investmentwould be ineffective for ANOs focusing on multi-site business customers because without economicaccess to provincial sites they would never developa foothold, even in the urban locations. Thus, themarket for services to multi-site businesscustomers has an inherent tendency to tip towardsno entry. Of course, in situations in which thecustomer‘s sites are all located in districts withwell developed competitive access for all servicesrequired, this might not be such a problem, but thiswould be the exception rather than the rule.

In voice telephony, market power conferred bynetwork externalities is addressed through rulesrequiring all operators to offer a service toterminate calls originating on other networks.However, such rules fail to deal with situationswhere a customer requires the same operator toprovide services to all its locations. Under suchcircumstances, arguably the only tool available toregulators for addressing dominance arising fromnetwork externalities is to address local dominancein all locations. Otherwise, failure by an SMPO toprovide access7 to even a very few sites will besufficient to prevent an ANO from providing serviceto any.

This point is very important when considering howto extend competition in B2B services providedacross international boundaries, for example topan-European customers. Many large corporatecustomers require services to be supplied in anumber of EU countries. This strongly suggests aneed for regulatory harmonisation across EUcountries to ensure that, as far as possible, accessconditions are relatively homogeneous acrossMember States. This can either be achievedthrough competition, in areas where competition issufficient to ensure that access is available toANOs, or through regulated access wherecompetition is not sufficient.

The Commission therefore needs to be pro-activein seeking harmonisation. An SMPO belonging to acountry without a pro-competitive regulatoryregime has an inherent advantage over one in acountry with one. Pan European customers will“tip” towards taking service from the SMPO in thecountry without favourable access conditions andaway from operators in the country with them. Thisleads to perverse incentives on governments andregulators to support their national operators ininternational markets by preventing access byANOs, many of which will be from differentcountries and attempting to address the same pan-European markets.

Ovum Paper.qxp 6/6/06 11:36 Page 9

10 BUSINESS TO BUSINESS COMMUNICATIONS | UNDERSTANDING THE ROLE OF THE LADDER OF INVESTMENT

Understanding the role of the Ladder of InvestmentBusiness-to-Business Communications10

8 As an example, one ANO inEurope (the details mustremain confidential)recently migrated itsentire business customerbase in a medium sizedEuropean country fromSMPO-provided retailleased lines to the lowerpriced wholesaleequivalent. Although thecost savings wereworthwhile in the long-run, the migration processrequired over six staff-years of time. The sameANO was faced with asimilar problem in France,although in this case itconcluded that there wasno business case toconclude the migration.

5.2.1 PLATFORM MIGRATION

There is a further problem with applying ProfessorCave’s proposals that becomes apparent whenconsidering the requirements of businesscustomers in general, particularly multi-sitecustomers. The ANO would be forced by regulatorywithdrawal to migrate its interconnectarrangements to another platform. Migration canbe very costly eroding further the low margins onB2B services.8 Migration also introduces asignificant risk of service disruption, typicallyinvolving outages of hours. Business customerstend to require 24/7 service availability and insiston penalty-backed SLAs (with provision fordamages) to protect them from service disruption.Residential customers generally do not. An ANOthat expects the interconnect platform to bechanged might not be able to offer businesscustomers the SLAs they require.

5.2.2 APPLYING THE LOI TO MULTI-SITE B2BSERVICES: CONCLUSIONS

What, therefore, are we to make of Professor Cave’s proposals of a pre-committed programme ofregulatory withdrawal in the light of therequirements of multi-site customers?

We offer two main conclusions, as follows:

1 To avoid damaging competition for multi-sitebusiness customers, any withdrawalprogramme must allow multiple ladder rungsto exist simultaneously. This will allow serviceto be provided in locations with varying geo-demographic characteristics and to allowservice to be provided to different types of sites(eg HQ and retail outlet) within the same geo-demographic area.

2 Any withdrawal of regulated access tobusiness customers must be based on theactual development of competition and not juston a projection about how competition mightdevelop. This is due to the tipping nature of themarket. If a decision to withdraw fromregulation is made on the basis of prospectiveentry, the withdrawal may by itself destroy thevery prospect of market entry occurring asprospective competitors on whom the hoped-fornew competition depends would be eliminatedby the withdrawal. Therefore, it is reasonable toconclude that the “error costs” of withdrawingof access required to serve multi-sitecustomers are far greater than those requiredto serve single-site customers. Another reasonwhy a pre-commitment to withdraw a productafter three years (as suggested by Professor

Cave) is unlikely to be effective is that this isoften the length of time from when an accessproduct is first mandated to when it becomescommercially useable.

5.3 DESIGNING A LOI FOR B2B SERVICES

How might a regulator reconcile a policy ofwithdrawing LOI rungs for B2C services butmaintaining them for B2B services? One approachwould be to adopt a different withdrawalprogramme for service providers offering servicesto single sites and multiple sites. If such a policycould be practically implemented, it would allowregulators to follow their desired regulatoryprogramme for the residential sector whilstavoiding the loss of competition in the businesssector.

Practical implementation of such a policy wouldobviously present a challenge. To enforce it, theoperator might be required to provide evidence ifrequired (for example if there was a reasonablesuspicion that the rule was being breached) that itwas using the product in question only for multi-site customers.

If there is no cost effective way of making ladderrungs available for ANOs serving multi-sitecustomers whilst restricting their availability tosingle-site customers, the question arises, whichpolicy should prevail? Should the benefits ofphasing out services outweigh the benefits ofretaining them, or vice versa?

It is impossible without a detailed analysis toanswer this question definitively. However, it is areasonable hypothesis that the benefits of retainingservices would outweigh the benefits ofwithdrawing them. The projected benefits ofwithdrawing services in terms of greater incentivesto invest and innovate are at best, based oneconomic models that are unproven empirically,whilst the loss of competition of withdrawingaccess is arguably more obvious. Considering thehypothesis that competition between serviceproviders may act to boost productivity-enhancingICT investment, and that such competition dependson regulated access, it is reasonable to supposethat the economy-wide costs of withdrawing accesswould be high.

The benefits of ICT investment on economicperformance – and the role of a competitive marketin B2B communications services in promoting it –are considered in the next section.

Ovum Paper.qxp 6/6/06 11:36 Page 10

Understanding the role of the Ladder of InvestmentBusiness-to-Business Communications11

BUSINESS TO BUSINESS COMMUNICATIONS | UNDERSTANDING THE ROLE OF THE LADDER OF INVESTMENT 11

0 Reaping the benefits ofICT: Europe’s productivitychallenge, A report fromthe Economist IntelligenceUnit, sponsored byMicrosoft, 2004

11 ICT and Economic Growth,Evidence from OECDcountries, industries andfirms, 2003

12 Restoring EuropeanEconomic and SocialProgress: unleashing thepotential of ICT: A reportfor the Brussels RoundTable by Indepen, January2006

6 THE CONTRIBUTION OF B2BCOMMUNICATIONS SERVICES TO ECONOMICPERFORMANCE

In this section we consider how B2BCommunications services can contribute to theperformance of an economy more broadly. Despitethe famous “Solow Paradox”9, that “you can see thecomputer age everywhere but in the productivitystatistics”, more recent experience has ledcommentators to believe the use of ICT is apowerful contributor to economic performance.

B2B communications services comprise animportant input to the use of ICT, providing theplatform on which businesses can deploy andenhance the use of ICT. Corporate networking,through its ability to link and propagate technologythroughout an organisation, has the potentialsignificantly to enhance the effectiveness withwhich information technology can be deployed.

6.1 LINKAGES BETWEEN ICT DEPLOYMENTAND ECONOMIC PERFORMANCE

There is a considerable body of research indicatingthat investment in ICT-related activity generatesbenefits for the economy at large. Much of it isdevoted to understanding why productivity growthin Europe has lagged that in the United States inrecent years.

In designing regulatory policy in electroniccommunications, it is important for policy makersto understand:

• the nature of the link between ICT investmentand economic growth. How in practical termsdoes ICT investment affect economicperformance?

• the extent of the link between ICT investmentand economic growth. How much would a givenincrease in ICT investment increase economicgrowth?

• the types of policies that are likely to lead to animprovement in ICT investment. This isconsidered in the section below on “PolicyAnalysis”.

These are considered in the sections below.

6.1.1 HOW DOES ICT INVESTMENT IMPACTECONOMIC PERFORMANCE?

Most studies on the impact of ICT have focused onits ability to create efficiencies inter alia by:

• Allowing greater automation of production ingoods and services (an example would be the

retail banking industry where the introductionof ATM machines reduce the labour intensity ofbanking. Another would be the use of softwarein knowledge intensive industries.)

• Allowing greater automation of sales andmarketing. The increased use of the Internetallows traders of goods and services to reducethe dependency on retail outlets and costlyadvertising for attracting customers and sales

• Allowing business-critical data such asfinancial information and stock information tobe stored more efficiently and accessed moreeasily

• Creating opportunities for communicating withsuppliers and customers more efficiently thanface-to-face or telephone communications.

A study by the Economist Intelligence Unit (EIU) forMicrosoft10 found three ways in which ICTinvestment can boost the economy, as follows:

• First, ICT investment leads to “capitaldeepening”, meaning that it improves labourproductivity (as opposed to “capital widening”which refers to the addition of capital andlabour in constant proportions).

• Second, the ICT producing sector comprises asignificant and growth proportion of economicoutput.

• Third, (which the EIU considered the largestcontribution), ICT investment creates spillovereffects that create a sustainable boost toproductivity growth in the rest of the economy.

The OECD11 argued that the strongest evidence forthe impact of ICT use comes from studying firmlevel performance. In this study, the OECD reportedevidence that computer networks are particularlyimportant as they allow a firm to outsource certainactivities, to work closer with customers andsuppliers, and to better integrate activitiesthroughout the value chain.

A report by Indepen12 reported evidence from theUS that approximately 75% of the growth in GDPattributable to ICT investment results from indirectrather than direct effects. In this context a “direct”effect refers to economic growth resulting fromvalue added attributable to investment in the ICTproducing sector, whilst an “indirect” effect refersto the impact of ICT investment on productivity inother sectors of the economy. The same studyreferred to the example of the pioneering work byWal-Mart, which introduced innovations such asbar code scanning. This created significantefficiency improvements in a wide range offunctions such as stock control and supply chainmanagement leading to a jump in productivitygrowth and an increase in Wal-Mart’s marketshare. These innovations have had strong spill overeffects as similar companies throughout the worldhave followed Wal-Mart’s lead.

Ovum Paper.qxp 6/6/06 11:36 Page 11

12 BUSINESS TO BUSINESS COMMUNICATIONS | UNDERSTANDING THE ROLE OF THE LADDER OF INVESTMENT

Understanding the role of the Ladder of InvestmentBusiness-to-Business Communications12

13 www.ovum.com

A report by HM Treasury13 in the UK has identified afurther source of productivity improvementresulting from ICT investment. According to thisreport, the ICT revolution has intensified trade inservices by eliminating many of the technicalconstraints that had hitherto required the place ofconsumption to be at or close to the point ofproduction. The effective use of communicationallows companies to eliminate duplication andother inefficiencies, centralising the production anddelivery of services to the points where skills andexpertise can most effectively be deployed.

6.1.2 QUANTIFYING THE IMPACT

The EIU argued that almost 80% of the difference inGDP per head growth rates in the US and the eurozone big three (Germany, France, Italy) in 1995-2002 can be attributed to ICT use. During thisperiod, GDP per head growth rates were 0.52percentage points higher in the US, of which theEIU considered 0.4 percentage points were theresult of superior ICT use. The EIU argued that it isnot merely the amount of ICT deployed thataccounts for the difference but the combination of arange of factors including the business andnetwork infrastructure environment that allowsinvestors to deploy ICT more effectively. Thisconclusion supports the hypothesis above thateffective ICT deployment is related to effectivecommunications services.

The OECD presented similar conclusions, arguingthat investment in ICT capital has supported stronglabour productivity growth in Australia, Canada andthe United States. In a number of countries, notablyFinland, Ireland and Korea, they argue that ICTproduction has not only improved labourproductivity but also economy-wide total-factorproductivity (TFP).

Following a growth accounting approach, the OECDfound that ICT investment accounted for between0.3 and 0.8 percentage points of economic growthin OECD countries between 1995 and 2001 andfound a positive correlation between total factorproductivity growth and ICT investment at theaggregate level.

Indepen found that lack of ICT use accounts forEurope’s decline in productivity growth relative tothe US. The authors quote the results of researchthat shows that the absolute contribution of ICT toproductivity growth in the EU-15 countries (whilstproductivity growth declined) remained almoststatic between 1983 and 2000 whilst in the USproductivity growth accelerated rapidly in the late1990s, virtually all of the acceleration wasaccounted for by the use of ICT in the technologybased private sector.

6.2 POLICY IMPLICATIONS

The evidence that ICT investment contributes toeconomic performance is strong. Moreover, B2Bcommunications is a fundamental input to ICTcapital through its ability to provide the networkinginfrastructure linking technology and applications –and providing the technology and applicationsthemselves. What types of regulatory policies arelikely to increase ICT investment?

One factor that is likely to lead to greater and moreeffective use of ICT is effective competition betweencommunications service providers. Competitionallows customers to choose suppliers on price,features and service quality and forces competitorsto innovate, differentiate, invest and improve theirefficiency in order to stay ahead of the pack.Therefore, successful regulatory policies are likelyto be those that create opportunities for effectivecompetition.

This paper has two policy recommendations forimproving competition among B2B communicationsproviders. It recommends that regulators:

consider allowing multiple access services, or LOIrungs, for operators serving multi-site businesscustomers even where such services have beenwithdrawn from operators serving residentialcustomers; and

modify the LOI so that, rather then being based ona time-bound pre-commitment for regulatorywithdrawal based on a prediction of competitiveentry, the criterion for the removal of rungs forbusiness services should be the actual state ofcompetition.

What impact are such policies likely to have on ICTinvestment? It is sometimes claimed that access-based regulatory policies can disincentiviseinvestment in new access infrastructure. Such aview is the basis for many LOI type policiesinvolving gradual withdrawal of regulation,including that advanced by Professor Cave. The EIUargues that boosting competition in the telecomssector is particularly important, stating:

“governments must maintain the assault onbarriers to competition, particularly intelecommunications markets. This is particularlycritical for the growth of broadband access.Moreover, the benefits of enhanced telecomscompetition must be extended to businesses andconsumers in the EU accession countries”

The OECD’s assessment (page 89) is similar to theEIU’s. They argue that increased competition intelecommunications, resulting from regulatoryreform has delivered benefits in terms of price,

Ovum Paper.qxp 6/6/06 11:36 Page 12

Understanding the role of the Ladder of InvestmentBusiness-to-Business Communications13

BUSINESS TO BUSINESS COMMUNICATIONS | UNDERSTANDING THE ROLE OF THE LADDER OF INVESTMENT 13

technological diffusion, new service development,improved efficiency and quality of service. However,the OECD argues that efforts to improvecompetitive conditions are not yet sufficient andcalls upon countries to increase competition andcontinue with regulatory reform in thetelecommunications industry to enhance theuptake of ICT.

Some commentators refer to the FCC’s TriennialReview order of 2003 when attempting to explainthe superior productivity performance in the US.The order removed regulated access to unbundlednetwork elements and newly deployed fibre-to-the-home. The decision was extended to fibre-to-the-curb in 2004.

However, it should be noted that the acceleration inproductivity growth in the US occurred mainly inthe 1990s, long before the 2003 Triennial Revieworder. Second, it is not true that the FCC hasentirely withdrawn from regulated access as issometimes claimed. Crucially, the LECs still have alimited obligation to provide “special access” (theUS term for a leased line part circuit) to ANOs. Thisis important in the current context because leasedline part circuits represent the access service mostcommonly used by ANOs to deliver B2B services.

The section immediately below considers whetherregulatory policies such as those advocated herehave had a positive effect on use of and investmentin ICT and related services.

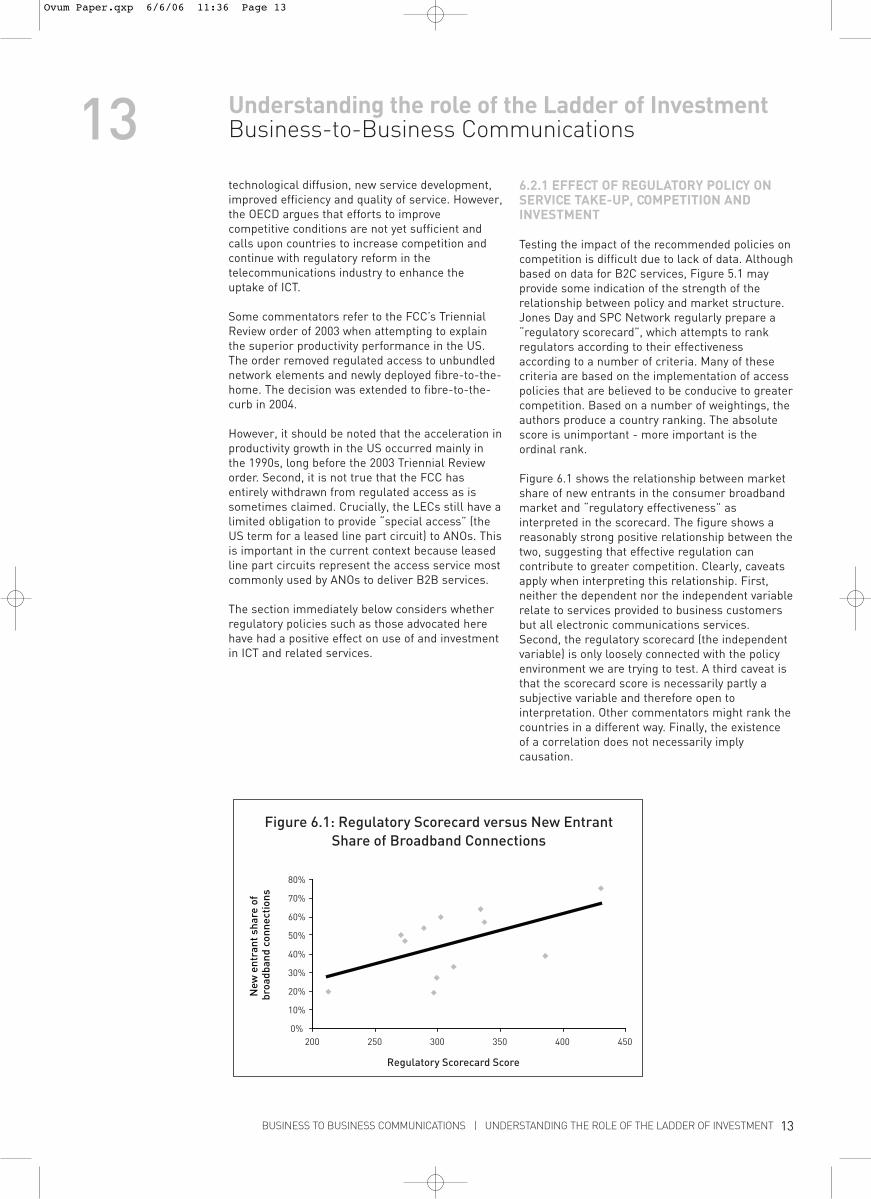

6.2.1 EFFECT OF REGULATORY POLICY ONSERVICE TAKE-UP, COMPETITION ANDINVESTMENT

Testing the impact of the recommended policies oncompetition is difficult due to lack of data. Althoughbased on data for B2C services, Figure 5.1 mayprovide some indication of the strength of therelationship between policy and market structure.Jones Day and SPC Network regularly prepare a“regulatory scorecard”, which attempts to rankregulators according to their effectivenessaccording to a number of criteria. Many of thesecriteria are based on the implementation of accesspolicies that are believed to be conducive to greatercompetition. Based on a number of weightings, theauthors produce a country ranking. The absolutescore is unimportant - more important is theordinal rank.

Figure 6.1 shows the relationship between marketshare of new entrants in the consumer broadbandmarket and “regulatory effectiveness” asinterpreted in the scorecard. The figure shows areasonably strong positive relationship between thetwo, suggesting that effective regulation cancontribute to greater competition. Clearly, caveatsapply when interpreting this relationship. First,neither the dependent nor the independent variablerelate to services provided to business customersbut all electronic communications services.Second, the regulatory scorecard (the independentvariable) is only loosely connected with the policyenvironment we are trying to test. A third caveat isthat the scorecard score is necessarily partly asubjective variable and therefore open tointerpretation. Other commentators might rank thecountries in a different way. Finally, the existenceof a correlation does not necessarily implycausation.

New

ent

rant

sha

re o

f br

oadb

and

conn

ecti

ons

80%

70%

60%

50%

40%

30%

20%

10%

0%

Figure 6.1: Regulatory Scorecard versus New EntrantShare of Broadband Connections

Regulatory Scorecard Score

200 250 300 350 400 450

Ovum Paper.qxp 6/6/06 11:36 Page 13

14 BUSINESS TO BUSINESS COMMUNICATIONS | UNDERSTANDING THE ROLE OF THE LADDER OF INVESTMENT

Source: “Report on the relative effectiveness of the regulatory frameworks for electronic communications in Austria,Belgium, Czech Republic, Denmark, France, Germany, Greece, Hungary, Ireland, Italy, The Netherlands, Poland,Portugal, Spain, Sweden and the United Kingdom”, Broadband Competition Report, ERG 2005

Understanding the role of the Ladder of InvestmentBusiness-to-Business Communications14

Using a similar methodology, we can also test therelationship between regulatory policy andinvestment in electronic communications, the latterprovided by the OECD. Figure 6.2 plots theregulatory scorecard score against electroniccommunications investment as a percentage ofGDP, as reported by the OECD.

The figure shows a positive, although weaker,relationship between “regulatory effectiveness” asmeasured by the scorecard and investment inelectronic communications. As before, there are a

number of caveats in interpreting such acomparison. One is that the data on investment fromthe OECD (2003) and the scorecard score (2005) arenot contemporaneous, although the ordinal rankingof countries is similar to that in previous years.Again, another is that neither the dependent nor theindependent variable relate to services provided tobusiness customers but all electroniccommunications services. Also, investment inelectronic communications in only a subset ofinvestment in ICT in general. Finally, as before acorrelation does not necessarily imply causation.

Austria 334 64%Belgium 271 50%Denmark 386 39%France 337 57%Germany 213 20%Ireland 313 33%Italy 299 27%Netherlands 289 54%Portugal 297 19%Spain 274 47%Sweden 302 60%UK 430 75%

RegulatoryScoreboard

New entrant share ofbroadband connections

New

ent

rant

sha

re o

f br

oadb

and

conn

ecti

ons

80%

70%

60%

50%

40%

30%

20%

10%

0%

Figure 6.1: Regulatory Scorecard versus New EntrantShare of Broadband Connections

Regulatory Scorecard Score

200 250 300 350 400 450

Ovum Paper.qxp 6/6/06 11:36 Page 14

Understanding the role of the Ladder of InvestmentBusiness-to-Business Communications15

BUSINESS TO BUSINESS COMMUNICATIONS | UNDERSTANDING THE ROLE OF THE LADDER OF INVESTMENT 15

6.3 REGULATORY POLICY, ICT ANDINVESTMENT: SUMMARY

There is strong evidence that ICT investment has apositive impact on economic performance. Severalstudies have pointed to the superior productivityperformance in the US compared with Europe inthe 1990s and have ascribed it, at least in part, togreater investment and superior use of ICT.Communications services provide the means forlinking and networking ICT applications andservices and are thus fundamental to allowing ICTto be deployed effectively.

More recently, the US has changed its policytowards the communications sector by removingregulated access in a number of areas. The longer-term effects of these policies remain to be seen.

Most commentators agree that effective competitionin electronic communications has the potential toboost ICT investment through allowing customers agreater choice of services and creating incentives forservice providers to invest, innovate and differentiateto stay ahead of competitors.

The thesis of this paper is that to allow effectiveand sustainable competition in B2B services,regulators should allow multiple LOI rungs andbase any decision to withdraw regulated accessfrom services on an ex-post assessment of thestate of competition and not any prediction of thedevelopment of competition.Testing empirically whether such policies wouldhave their intended effect is difficult due to lack ofdata. However, there is some evidence that access-based regulatory policies can lead to greatercompetition and investment. It is also reasonable toexpect that the effect of such policies would be feltmore strongly in the business sector than theresidential sector. This is for two reasons. First,businesses are more intensive users of ICT.Second, any potentially investment suppressingeffects of access-based regulatory policies are lesslikely to be seen in the business sector because ofthe greater separation between networkinfrastructure and services and because fibreaccess is already widespread in many situations.

Source: “Report on the relative effectiveness of the regulatory frameworks for electronic communications in Austria,Belgium, Czech Republic, Denmark, France, Germany, Greece, Hungary, Ireland, Italy, The Netherlands, Poland,Portugal, Spain, Sweden and the United Kingdom”, 2005, OECD 2003

Austria 334 0.61%Belgium 271 0.27%Denmark 386 0.40%France 337 0.25%Germany 213 0.23%Ireland 313 0.38%Italy 299 0.54%Netherlands 289 0.36%Portugal 297 0.61%Spain 274 0.54%Sweden 302 0.48%UK 430 0.61%

RegulatoryScoreboard

Investment in ElectronicCommunications as a % of GDP

Ovum Paper.qxp 6/6/06 11:36 Page 15

16 BUSINESS TO BUSINESS COMMUNICATIONS | UNDERSTANDING THE ROLE OF THE LADDER OF INVESTMENT

Understanding the role of the Ladder of InvestmentBusiness-to-Business Communications167 CONCLUSION

There is evidence that Europe is falling behind itsmajor global competitors in most areas ofeconomic performance, particularly productivitygrowth. Key to Europe’s ability to bridge the gapwill be its ability to deploy technology as cheaplyand effectively as elsewhere in the world. Thecompetitiveness of the B2B communicationssector is a fundamental factor in whether or notit achieves this. Of course, it is not the onlyfactor: in the eyes of most commentators, labourmarket rigidities and restrictive labour laws areother main contributor to Europe’s relatively poorperformance in recent years.

Policies of regulatory withdrawal designed toachieve sustainable competition in residentialservices are unlikely to be effective in B2Bcommunications for two reasons as follows:

Premature removal of LOI rungs would harmcompetition in B2B services to a greater extentthan in B2C services because, as a consequenceof the multi-site nature of B2B services it willcause business customers to default to theSMPO;

The reason for removing LOI rungs is arguablyless applicable to B2B services in the first placebecause the key areas in which innovation anddifferentiation occur are not in the infrastructurebut in the services.

The propensity of business customers to defaultto the incumbent in the absence of appropriateaccess may also be described as a “tippingeffect” in reference to the tendency for themarket to “tip” towards monopoly and away fromcompetition. The tipping effect can workinternationally as well as nationally, implying arole for the European Commission in ensuringthat conditions are amenable to competitive entryin all EU markets. The Commission should beaware of the potentially perverse incentivesfacing governments and regulators who, bydenying competitive access in their country, canprovide local operators with significantadvantages in pan-European markets, to thedetriment of competition in the EU as a whole.

The inherent tipping effect in the B2Bcommunications market has an importantimplication for policy. If a regulator announces aplan of regulatory withdrawal based on a forecastof the development of competition over aspecified period of time and competition fails totake off as forecast, the cost to competition inB2B markets will be will be very high ascustomers will naturally tip towards the SMPO. Itfollows that regulators should guard againstpolicies based on a predetermined plan ofregulatory withdrawal of access products forbusiness services because of the high costs oferroneous forecasts.

The need to serve sites with widely varyingbandwidth requirements in geographic areas thatdiffer markedly in terms of competition alsoimplies that regulators should allow multipleaccess points along the LOI for B2B services.

A potential problem may exist if regulators decidethe optimal policies for B2B services andresidential services are different. This may ariseif the regulator prefers a programme of accesswithdrawal to serve the competitive needs ofresidential customers but sees the risk tocompetition in B2B services of such a policy. Onepossible resolution would be to maintainregulated access for LOI rungs for use in servingmulti-site customers after withdrawing them forsingle site customers.

8 ABOUT THE AUTHOR

Barney Lane is a Principal Consultant in Ovum'sTelecoms Consulting Practice in London. He is aleading expert advisor in telecom regulation andstrategy. Barney has over 10 years experience in thetelecoms industry and has covered a variety ofsectors including fixed, mobile and internet servicesin Europe, North America, the Middle East andAfrica.

Before joining Ovum, Barney spent 6 years at MCI,the global telecoms and IP carrier, focussing on theUK and European markets. Barney graduated fromOxford University with Bachelors and Mastersdegrees in Economics, which he followed up with anM.B.A. from Cranfield University.

Ovum Paper.qxp 6/6/06 11:36 Page 16