Topic 2

55

STRATEGIC MANAGEMENT ACCOUNTING 1

-

Upload

kim-rae-ki -

Category

Education

-

view

77 -

download

2

Transcript of Topic 2

STRATEGIC MANAGEMENT ACCOUNTING

1

Identify the strategic issues in MA Describe the issues conceptually Explain approaches used in handling the

strategic issues Discuss the role of management accountant

in confronting the issues Discuss strategic environmental MA

Learning objectives

BKAM 3033 – Topic 22

Introduction

Strategyan integrated set of actions aimed at securing a sustainable competitive advantage.

Strategic planning

- a process of designing a mission statement, setting long-term goals and objectives, and establishing strategies.- a long term plan.

BKAM 3033 – Topic 23

Introduction

Strategic management

long term planning, implementation and controlling which provides a framework for all the actions managers take and

how they are assessed.

Strategic management accounting

the role of mgt accounting in the strategic analysis, planning and control

of org.

BKAM 3033 – Topic 24

Why Traditional Management Accounting is not sufficient to provide information for strategic decisions?

BKAM 3033 – Topic 25

Comparison between SMA and Conventional MA

ConventionalHistorical

Manufacturing focus

Existing activities

Reactive

Overlook linkages

Data orientation

SMAProspective

Competitive focus

Possibilities

Proactive

Embraces linkages

Information orientation

BKAM 3033 – Topic 26

Ability to acquire, allocate and utilize resources in line with the needs of environment is very crucial, so the focus of management accountant, therefore, should be outwards and forward.

The Needs of SMA

BKAM 3033 – Topic 27

What is SMA• The provision of information to support strategic decisions in organizations

(Innes,1998).

• Review of literature by Lord (1996) identified the following strands:

1. Extension from internal focus of management accounting (MA) to include external information about competitors.2.The relationship between the strategic position chosen by the

firm and the expected emphasis on MA.3. Gaining competitive advantage through exploiting linkages in the value

chain.

• Target costing is also identified as falling within the domain of SMA.

• Strategic role of MA emphasized in formulating and supporting the overall strategy of an organization by developing an integrated framework of performance measurement.

8

BKAM 3033 – Topic 2

Life Cycle Costing (LCC), Kaizen Costing Target Costing (TC) Benchmarking.

Strategic Issues & Techniques in Management Accounting

9

BKAM 3033 – Topic 2

LCC – strategic analysis tool/discussed in form of life cycle cost management and life cycle cost analysis.

Kaizen Costing – effort to reduce costs of existing products and processes continually.

TC – the difference between the sales price needed to capture a predetermined market share and the desired per-unit profit.

Strategic Issues in Mgt Accounting

10

BKAM 3033 – Topic 2

Benchmarking – a close phenomenon to competitor accounting. Competitor accounting is a special accounting-based form of strategic level benchmarking, which does not include cooperation with the object of this comparison activity.

Strategic Issues in Mgt Accounting

11

BKAM 3033 – Topic 2

Life Cycle – defined as the period of a product in the market. Life cycle analysis should consider the period between birth and decease which studies the phases of life, the repeated patterns that occur during life, and the causes an effects of incidences, aiming at something that can be recognized and learned from the earlier life cycles of the items under study.

.

Strategies and Techniques in Management Accounting- LCC

12

BKAM 3033 – Topic 2

Life cycle costing defined as the total cost of ownership of a system during its operational life where it embraces all costs associated with the feasibility studies, research, development, production, maintenance, replacement and disposal as well as support, training and operating costs generated by acquisition of the equipment (accumulates the actual costs attributable to each product form start to finish

Whole life cost, the total cost of ownership over the life of an asset, also commonly referred to as "cradle to grave" or "womb to tomb"

Strategies and Techniques in Management Accounting- LCC

13

BKAM 3033 – Topic 2

Strategies and Techniques in Management Accounting- LCC

• Traditional management accounting procedures have focused primarily on the manufacturing stage of a product ’s life cycle.

• LCC focuses on costs over the product ’s entire life cycle to determine whether profits earned during the manufacturing phase will cover the costs incurred during the pre-and post-manufacturing stages.

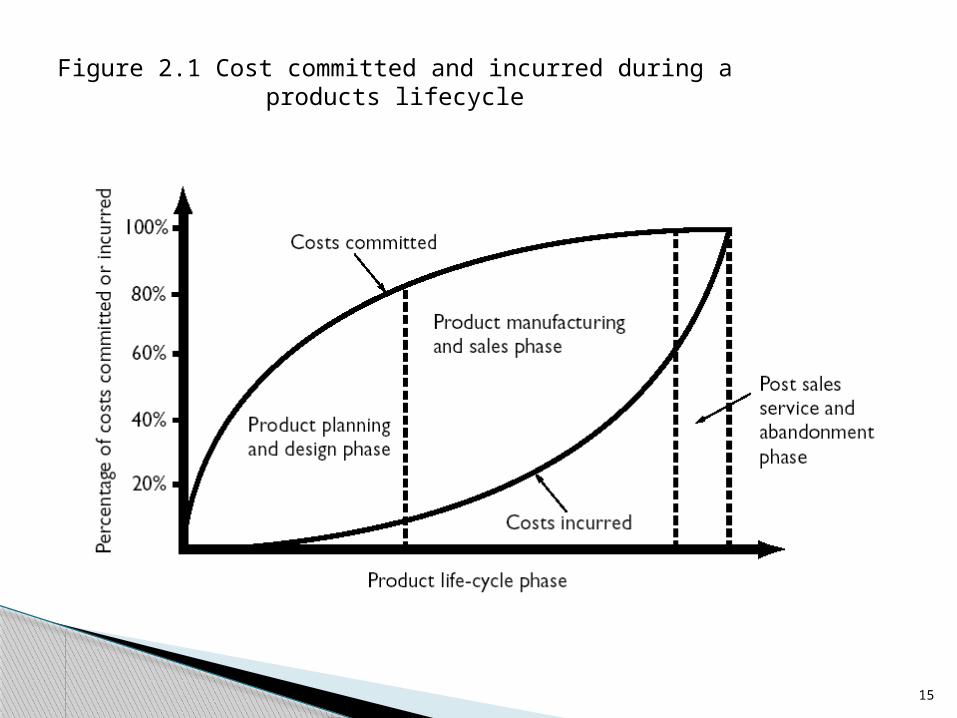

• A large proportion of a product ’s costs can be committed or ‘locked in ’during the planning and design stage (see Figure 2.1).

• Cost management can be most effectively exercised during the planning and design stage.

14

BKAM 3033 – Topic 2

Figure 2.1 Cost committed and incurred during a products lifecycle

15

Kaizen Costing – defined as the maintenance of present cost levels for products currently being manufactured via systematic efforts to achieve the desired cost level.

Kaizen means improvement which contain two elements- improvement and continuity. One important advantage is its low cost setup. There is basically not much investment in terms of equipment. It is more of using the already existing resources and information to reduce cost.

Strategies and Techniques in Management Accounting - Kaizen

16

BKAM 3033 – Topic 2

Strategies and Techniques in Management Accounting - Kaizen Costing

• Kaizen costing is applied during manufacturing stage whereas target costing is during planning stage.

• Kaizen costing focuses on production processes whereas target costing focuses on the product.

• Kaizen costing aims to reduce costs of processes by a pre-specified amount relying on employee empowerment.

17

BKAM 3033 – Topic 2

Target Costing – is a relatively new concept first adopted by some Japanese companies in the early 1970’s. it is a procedural approach to determining a maximum allowable cost for an identifiable, proposed product assuming a given target profit margin.

- Has two objectives:i) To lower the costs of new products so that the

required profit level can be ensured while the new products meet the levels of quality, delivery timing, and price required by the market.

ii) To motivate all company employees to achieve the target profit during new product development by making target costing a company wide profit management activity.

Strategies and Techniques in Management Accounting - Target

18

BKAM 3033 – Topic 2

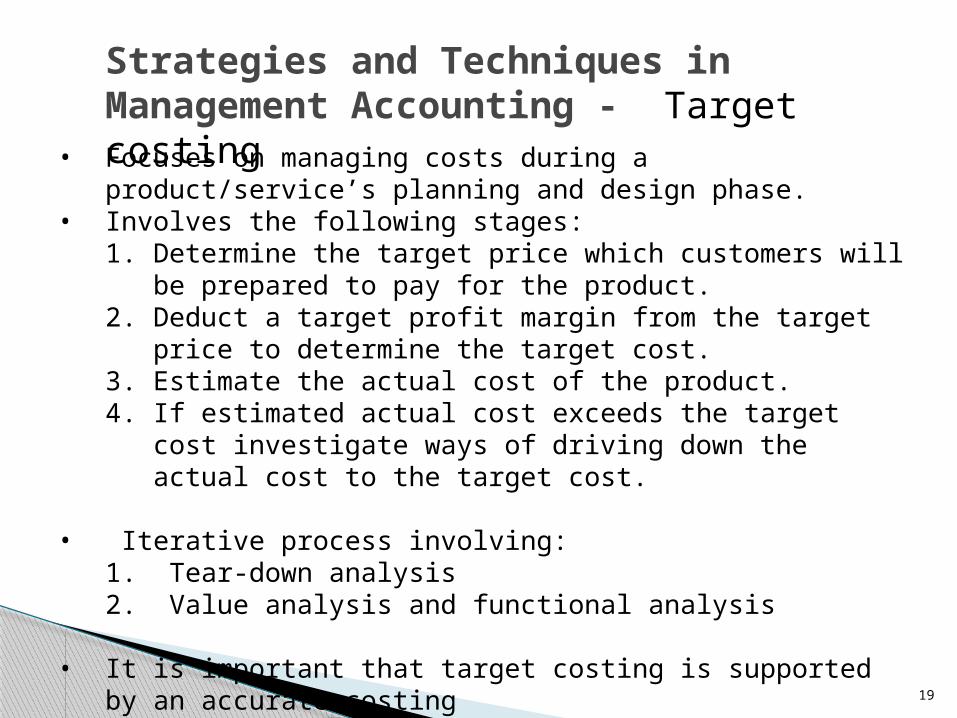

Strategies and Techniques in Management Accounting - Target costing

• Focuses on managing costs during a product/service’s planning and design phase.

• Involves the following stages:1. Determine the target price which customers will be prepared to

pay for the product.2. Deduct a target profit margin from the target price to determine

the target cost.3. Estimate the actual cost of the product.4. If estimated actual cost exceeds the target cost investigate ways

of driving down the actual cost to the target cost. • Iterative process involving:

1. Tear-down analysis2. Value analysis and functional analysis

• It is important that target costing is supported by an accurate costing

19

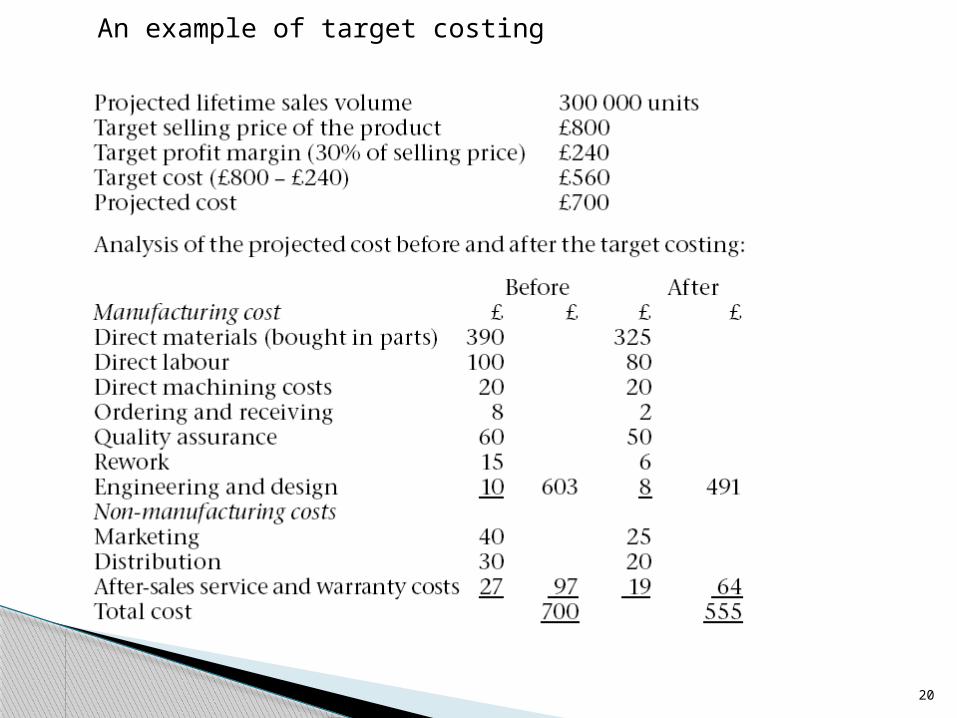

An example of target costing

20

Benchmarking – defined as a process of studying and adapting the best practices of other organizations to improve the firms own performance and establish a point of reference by which other internal performance can be measured.

Also referred as “best practice benchmarking” or “process benchmarking”.

Types of benchmarking:◦ Internal benchmarking◦ Functional benchmarking◦ Competitive benchmarking◦ Strategic benchmarking◦ Product benchmarking◦ Process benchmarking

Strategies and Techniques in Management Accounting - Benchmarking

21

BKAM 3033 – Topic 2

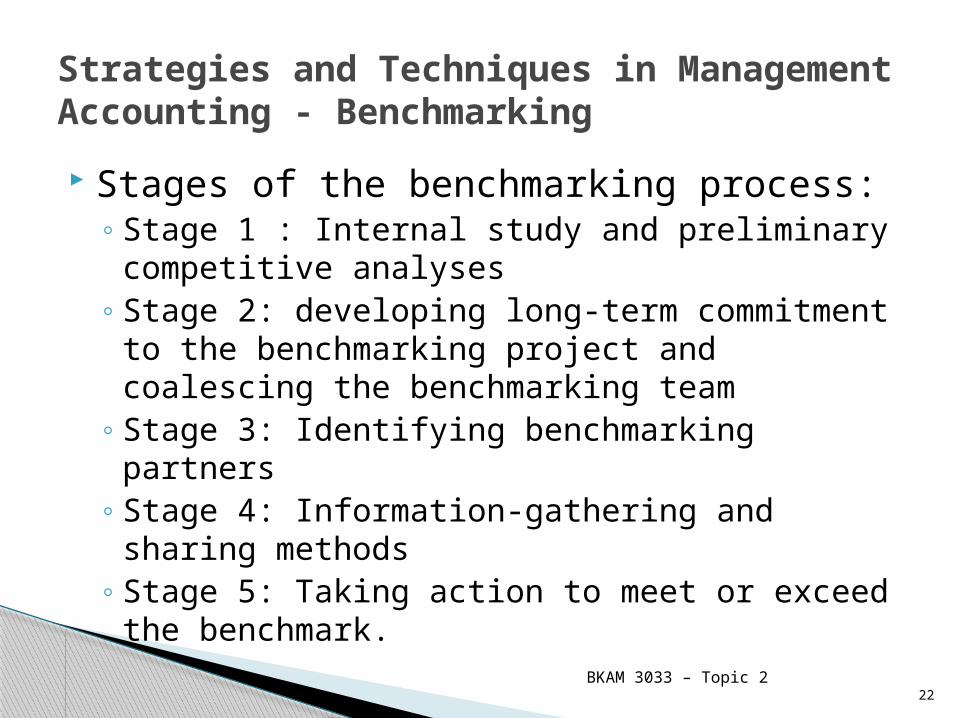

Stages of the benchmarking process:◦ Stage 1 : Internal study and preliminary

competitive analyses◦ Stage 2: developing long-term commitment to

the benchmarking project and coalescing the benchmarking team

◦ Stage 3: Identifying benchmarking partners◦ Stage 4: Information-gathering and sharing

methods◦ Stage 5: Taking action to meet or exceed the

benchmark.

Strategies and Techniques in Management Accounting - Benchmarking

22

BKAM 3033 – Topic 2

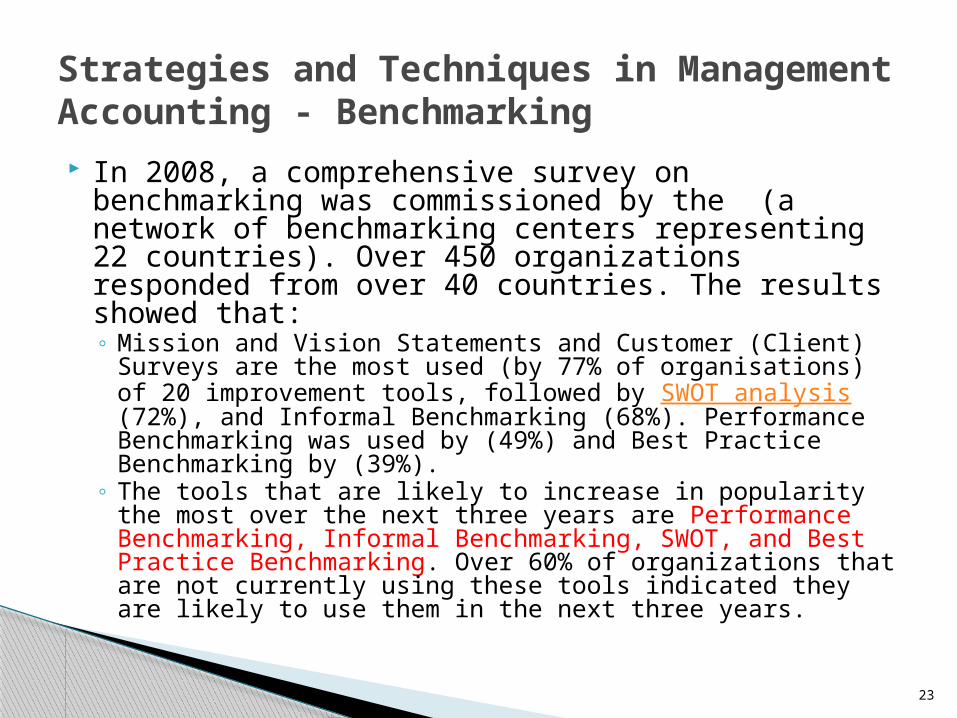

In 2008, a comprehensive survey on benchmarking was commissioned by the (a network of benchmarking centers representing 22 countries). Over 450 organizations responded from over 40 countries. The results showed that:◦ Mission and Vision Statements and Customer (Client)

Surveys are the most used (by 77% of organisations) of 20 improvement tools, followed by SWOT analysis(72%), and Informal Benchmarking (68%). Performance Benchmarking was used by (49%) and Best Practice Benchmarking by (39%).

◦ The tools that are likely to increase in popularity the most over the next three years are Performance Benchmarking, Informal Benchmarking, SWOT, and Best Practice Benchmarking. Over 60% of organizations that are not currently using these tools indicated they are likely to use them in the next three years.

Strategies and Techniques in Management Accounting - Benchmarking

23

Porter’s Approach Michael Porter in 1980’s. Premised on two basic questions: How attractive, from the viewpoint of long-

term profitability, are different industries? What is the enterprise’s relative position in

its industry?

Approaches in Handling Strategic Issues

24

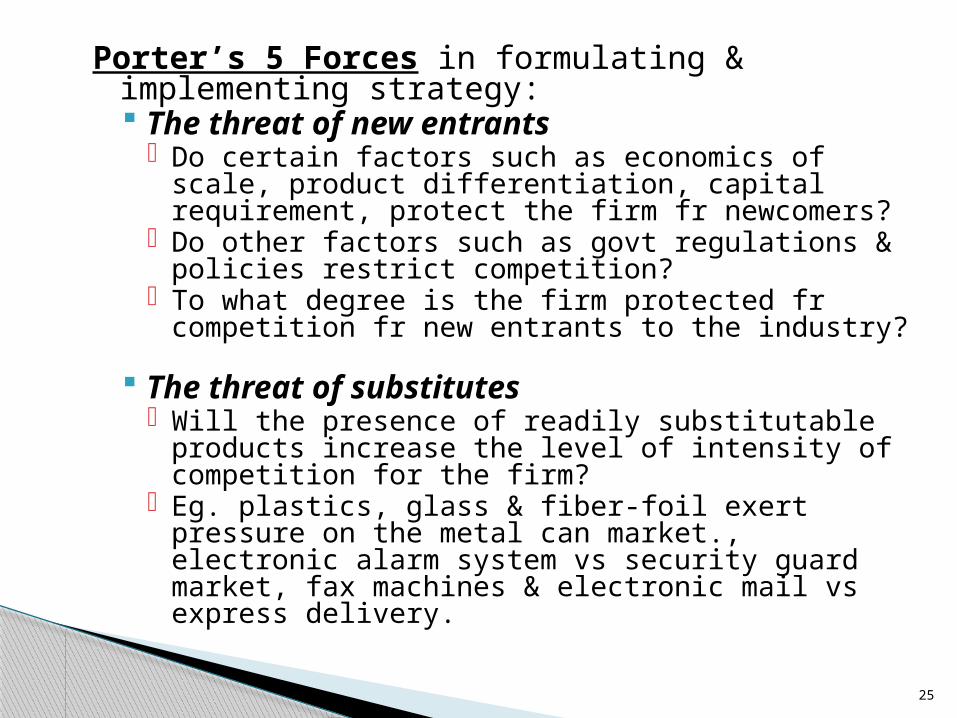

Porter’s 5 Forces in formulating & implementing strategy: The threat of new entrants

- Do certain factors such as economics of scale, product differentiation, capital requirement, protect the firm fr newcomers?

- Do other factors such as govt regulations & policies restrict competition?

- To what degree is the firm protected fr competition fr new entrants to the industry?

The threat of substitutes- Will the presence of readily substitutable products

increase the level of intensity of competition for the firm?

- Eg. plastics, glass & fiber-foil exert pressure on the metal can market., electronic alarm system vs security guard market, fax machines & electronic mail vs express delivery.

25

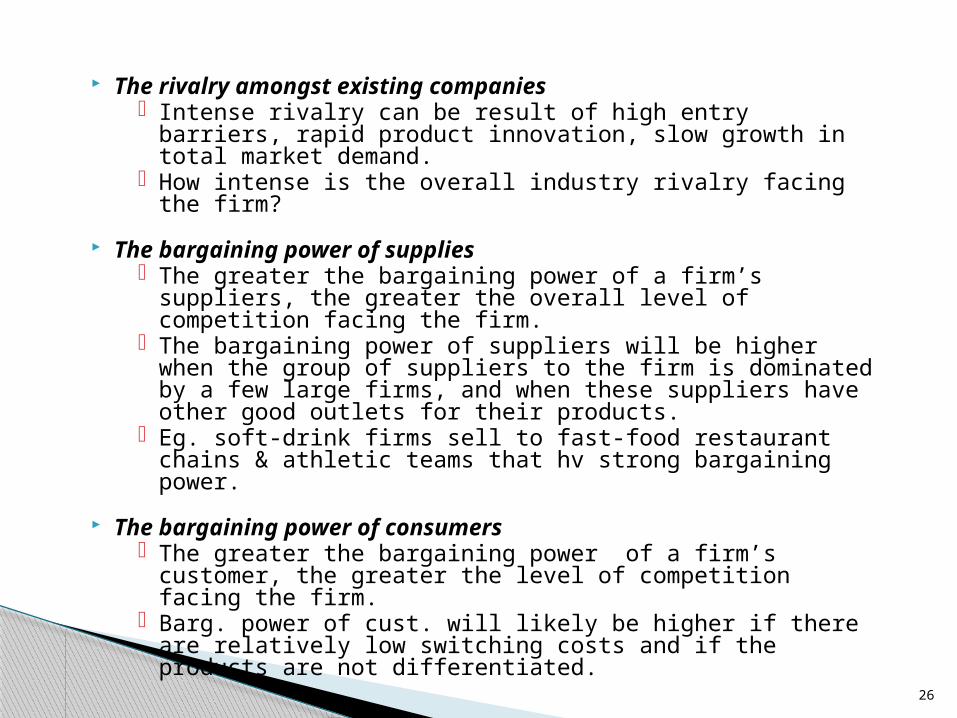

The rivalry amongst existing companies- Intense rivalry can be result of high entry barriers, rapid

product innovation, slow growth in total market demand.

- How intense is the overall industry rivalry facing the firm?

The bargaining power of supplies- The greater the bargaining power of a firm’s suppliers,

the greater the overall level of competition facing the firm.

- The bargaining power of suppliers will be higher when the group of suppliers to the firm is dominated by a few large firms, and when these suppliers have other good outlets for their products.

- Eg. soft-drink firms sell to fast-food restaurant chains & athletic teams that hv strong bargaining power.

The bargaining power of consumers- The greater the bargaining power of a firm’s customer,

the greater the level of competition facing the firm.- Barg. power of cust. will likely be higher if there are

relatively low switching costs and if the products are not differentiated.

26

Porter’s Competitive Advantage

Competitive Strength/ Strategic Advantage

Uniqueness Perceived by the

customer

Low Cost Position

No.of Strategic options/ Targets

Industry Wide DIFFERENTIATION COST LEADERSHIP

Specific Segment Only

FOCUS STRATEGY

27

Cost leadership strategy: aims to be the lowest-cost

producer◦ *product design *scale economics

*experience curve To provide the same or better value to

customers at a lower cost than offered by competitors.

Example: A company might redesign a product so that fewer parts are needed, lowering production costs and the costs of maintaining the product after purchase.

28

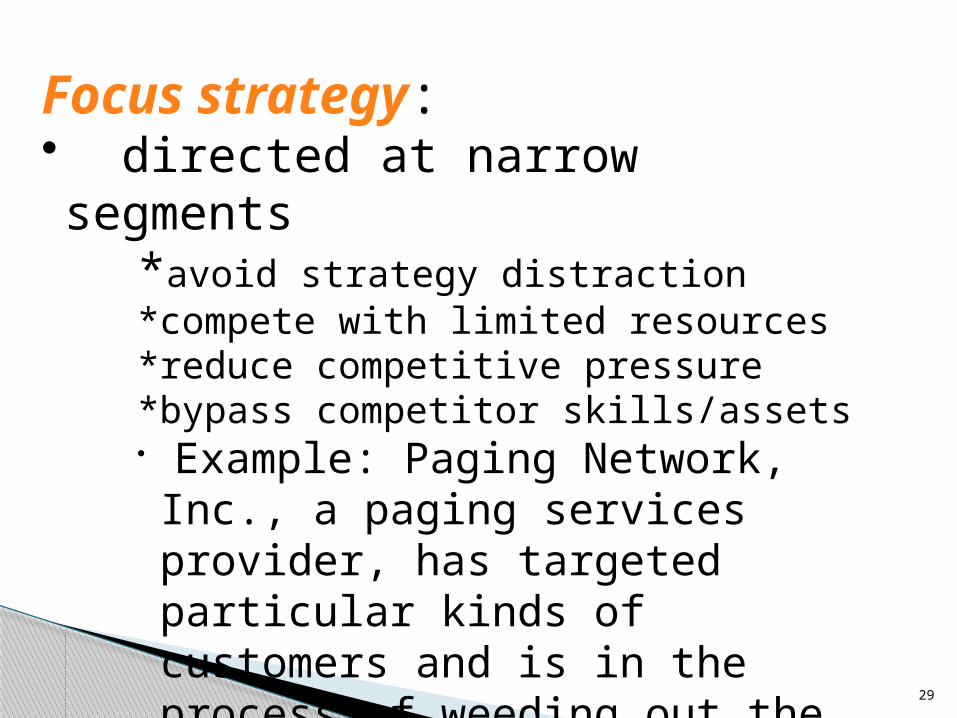

Focus strategy:

• directed at narrow segments *avoid strategy distraction *compete with limited resources *reduce competitive pressure *bypass competitor skills/assets• Example: Paging Network, Inc., a paging services provider, has targeted particular kinds of customers and is in the process of weeding out the nontargeted customers.

• Competitive advantage is based on either cost leadership or product differentiation.

29

offer some unique dimension*generate customer value *be difficult to copy

Strives to increase customer value by increasing what the customer receives (customer realization).

Example: A retailer of computers might offer on-site repair service, a feature not offered by other rivals in the local market.

Differentiation strategy:

30

Is a strategic analysis tool used to identify where value to customers can

be increased or costs reduced & to better understand the firm’s linkage

with suppliers, customers & other firms in the industry.

Value Chain Analysis

31

The value chain

32

Value chain analysis

Steps required in under-taking value-chain analysis:

Identify the appropriate value-chain and assign costs and assets to it

Diagnose the cost driver of each activity and how they interact

Identify competitor value-chains, and determine the relative cost of competitors and the sources of cost differences

Develop a strategy to achieve a lower relative cost position through controlling cost drivers or reconfiguring the value-chain

Ensure that cost reduction efforts do not erode differentiation

Test the cost reduction strategy for sustainability

33

Example Cost Driver in Value Chain

34

Organizational activities: ◦ Structural activities: activities that determine

the underlying economic structure of the organization.

◦ Executional activities: activities that define the processes and capabilities of an organization and thus are directly related to the ability of an organization to execute successfully.

Value Chain Analysis

35

VC analysis is identifying a and exploiting internal and external linkages with the objective of strengthening a firm’s strategic position.

The exploitation of linkages relies on analyzing how costs and other nonfinancial factors vary as different bundles of activities are considered.

Value Chain Analysis

36

Value-chain framework linkages◦ Internal linkages: relationships among activities

that are performed within a firm’s portion of the value chain

◦ External linkages: the firm’s value-chain activities that are performed with its suppliers and customers- Supplier linkages- Customer linkages

Value Chain Analysis

37

Exploiting Internal linkages ◦ Relationship between activities are

assessed and used to reduce costs and increase value.

Example: Product design & development activities are occur before production and are linked to production activities.◦The way the product is designed affects the

costs of production.◦How production costs are affected requires

a knowledge of cost drivers.◦Thus, knowing the cost drivers of activities

is crucial for understanding and exploiting linkages.

Value Chain Analysis

38

Exploiting external linkages – supplier & customer◦Means managing these linkages so both the

company and the external parties receive an increase in benefits.

Exploiting supplier linkages◦Example: in Total quality control,

relationship between company and supplier is very important to ensure raw materials are delivered on time and high quality.

◦Activity-based supplier costing

Value Chain Analysis

39

Exploiting customer linkages Customers can also have a significant

influence on a firm’s strategic position. Managing customer service costs

◦ Identify which profitable and unprofitable customers

◦ Customer profitability analysis◦ Activity-based customer costing

Value Chain Analysis

40

Gaining competitive advantage through exploiting linkages in the value chain:

• Focuses on each link in the chain from the customer’s perspective.

• Claimed that traditional management accounting starts too late and finishes too soon in terms of the value chain.

• Porter advocates identifying the value chain and operation of cost drivers of competitors in order to understand relative competitiveness.

41

Definition of SMA by Simmonds:The provision and analysis of management accounting data about a business and its competitors for use in developing and monitoring the business strategy

Emphasizes on:Real cost and priceVolumeMarket shareCash flowThe proportion demanded of an enterprise’s total resources

The focus shifts from the analysis of cost per se to the value of information

* Data orientation vs Information orientation The significant of competitive position as being the

basic determinant of future profits & of the enterprise value.

Simmond’s approach

42

Bromwich define SMA as;- The provision and analysis of financial information on the firm’s product markets and competitor’s cost and cost structures and the monitoring of the enterprise’s strategies and those of its competitors in these markets over a number of periods.

Focus on identifying the distinctive characteristics of market offering in order that these might be costed.

To secure competitive advantage, cost positioning relative to rivals, should be conducted

Purpose of analysis: the attribution of costs which are normally treated as product costs to the benefits they provide to the customer

Recommended approach: List separately the benefits to consumers contained in the market offering, then to relate costs to these.

Bromwich’s approach

43

◦ Dr William G.Ouchi, management theorist introduced Theory Z in 1981. The CLAN based approach.

◦ Traditionally, strategy has been viewed as the response of an organization to environment.

◦ A growing understanding that strategy of an enterprise, its structure, people who hold power, its control system, the way its operates reflect culture of org.

◦ Ouchi suggested that Japanese commitment to democratic leadership that resulted in increased quality, increased productivity and decreased costs while making workers at all levels full partners in business.

Ouchi’s approach

44

Environmental cost management

• Becoming of increasing importance because:

1. Environmental costs can represent a large proportion of operating costs in some companies.

2. Demands from society for companies to become environmentally friendly

STRATEGIC ENVIRONMENTAL MANAGEMENT ACCOUNTING

45

ENVIRONMENTAL COST◦ Incurred because of poor environmental quality◦ Environmental quality cost◦ Link to creation, detection, remediation and

prevention of environmental degradation◦ Type of environmental cost

- Environmental prevention cost- Environmental detection cost- Internal failure environmental cost- External failure environmental cost

STRATEGIC ENVIRONMENTAL MANAGEMENT ACCOUNTING

46

Environmental prevention cost◦ Objective: to minimize, if not eliminated, the

amount of waste material generated.◦ Include: all costs associated with training

employees, evaluating and selecting suppliers, evaluating and selecting equipment to control pollution, designing process to reduce environmental problems etc

Cont..

47

Environmental detection costs◦ Cost of activities executed to determine if

products, processes and other activities are in compliance with environmental standards.

◦ Environmental standards:- Regulatory laws of governments- ISO 14001- Environmental policies developed by management

◦ Examples: auditing environmental activities, inspecting product and processes, carry out contamination test etc

Cont..

48

Internal failure environmental costs◦ Cost of activities performed because of

contaminants and waste have been produced but not discharged into the environment.

◦ Examples: operating equipment to minimize or eliminate pollution, treating and disposing of toxic materials, maintaining pollution equipment etc

Cont..

49

External failure environmental costs◦ Costs of activities performed after discharging

contaminants and waste into the environment ◦ Two types: realized and unrealized◦ Realized: incurred and paid for the firm◦ Unrealized: caused by the firm but incurred and

paid by parties outside

Cont..

50

Definition by the Brundland Report◦ To meet the needs of the present without

compromising the ability of future generations to meet their own needs

Combines three dimensions: social, economic and environment

Sustainable development and competitive advantage

51

Sustainable developmen

t

Economy

Social

Environmental

Main goal of sustainable development

Eco JusticeSocio-efficiency

Eco-efficiency52

Sustainability – the goal of the process of sustainable development

Sustainable development – balancing concept between economic growth and environmental protection

Cont..

53

Application of the control system to environmental management

Is about learning how people in the firm manage to control environmental issues as a whole

Ensures that environmental issues are dealt with through a continuous process

Similar to management control system◦ Planning, action, measurement, comparison

between plans and actual outcomes, feedback and revision of expectation for future periods

ECO-CONTROL

54

End of Chapter 2

55