Reef Keeping. Top ten most costly mistakes Top ten most costly mistakes.

Top Ten Legal MistakesMade By Entrepreneurs

J. Matthew LyonsAndrews Kurth LLP

April 8, 2015

Copyright 2015 Andrews Kurth LLP and J. Matthew Lyons. All rights reserved.

Andrews Kurth LLP

“Understand the ways in which the law is a constraint, but also the ways in which it is a tool to help you create and capture value.”

--Constance Bagley, Harvard Business School

1

2

1. Failure to Incorporate Soon Enough

• Establishes vehicle with limited liability• Specifies relationship among founders,

including share ownership• Creates “vehicle” to hold IP, business

plan / ideas• Provides impetus to organize• CONVERSE: Incorporating too soon

Selecting the Right Entity and Jurisdiction

• Limitation of liability for owners: Limited liability vs. unlimited liability

• Tax treatment of entity and owners

• Pass-through of profits and losses to owners

• Impact on exit strategies and liquidity options

• Formality and centralization of management structure and decision-making

• Choice of formation jurisdiction: Delaware vs. state of residence

• Choice will depend on expected investment source and exit strategy

3

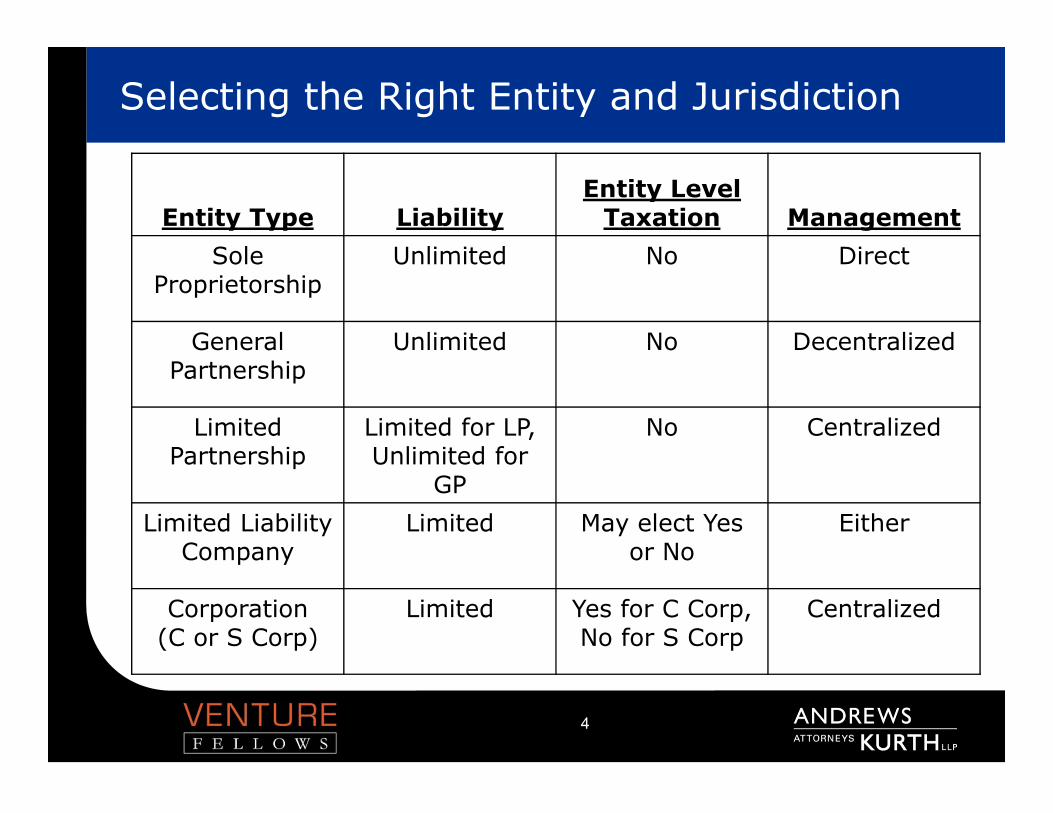

Selecting the Right Entity and Jurisdiction

Entity Type LiabilityEntity Level

Taxation ManagementSole

ProprietorshipUnlimited No Direct

General Partnership

Unlimited No Decentralized

Limited Partnership

Limited for LP, Unlimited for

GP

No Centralized

Limited Liability Company

Limited May elect Yes or No

Either

Corporation(C or S Corp)

Limited Yes for C Corp, No for S Corp

Centralized

4

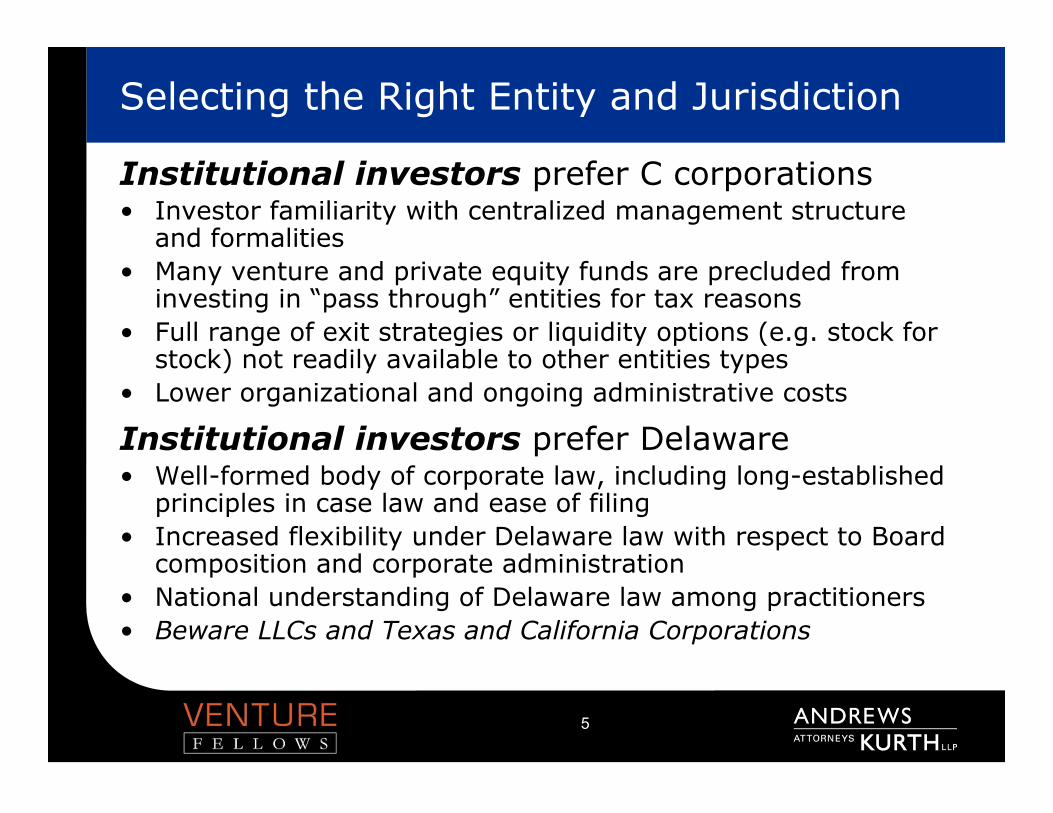

Selecting the Right Entity and Jurisdiction

Institutional investors prefer C corporations• Investor familiarity with centralized management structure

and formalities• Many venture and private equity funds are precluded from

investing in “pass through” entities for tax reasons• Full range of exit strategies or liquidity options (e.g. stock for

stock) not readily available to other entities types• Lower organizational and ongoing administrative costs

Institutional investors prefer Delaware• Well-formed body of corporate law, including long-established

principles in case law and ease of filing• Increased flexibility under Delaware law with respect to Board

composition and corporate administration• National understanding of Delaware law among practitioners• Beware LLCs and Texas and California Corporations

5

6

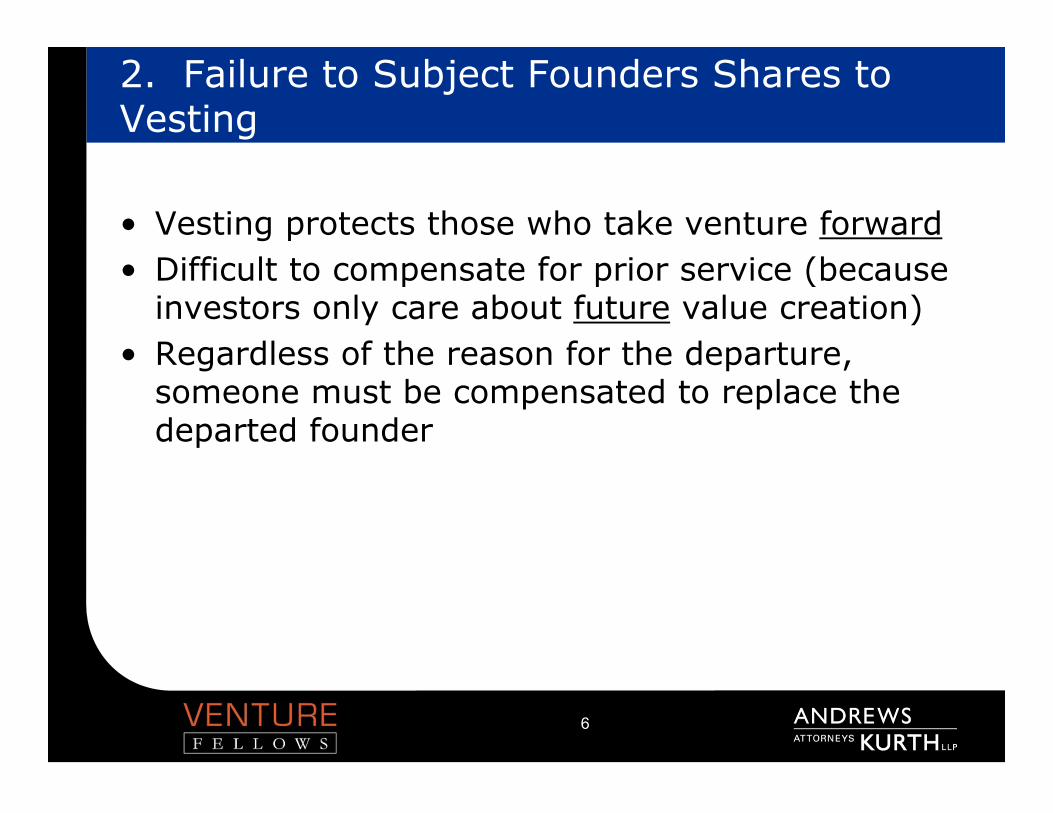

2. Failure to Subject Founders Shares to Vesting

• Vesting protects those who take venture forward• Difficult to compensate for prior service (because

investors only care about future value creation)• Regardless of the reason for the departure,

someone must be compensated to replace the departed founder

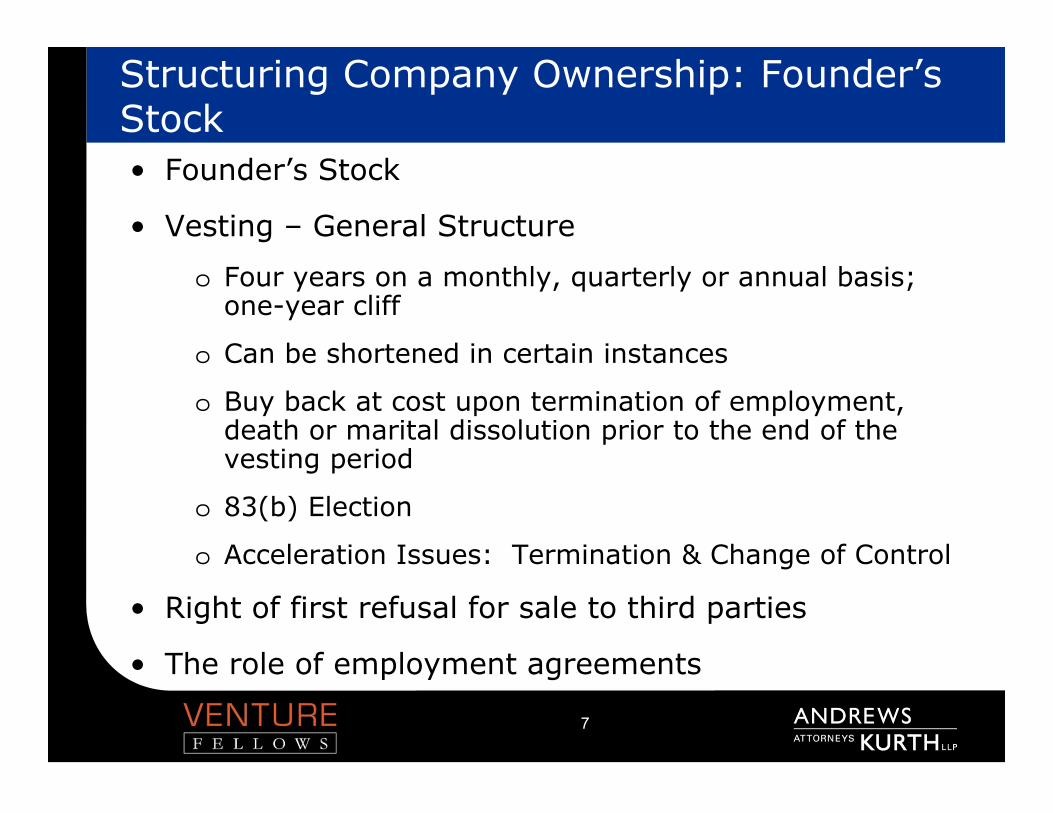

Structuring Company Ownership: Founder’s Stock• Founder’s Stock

• Vesting – General Structure

o Four years on a monthly, quarterly or annual basis; one-year cliff

o Can be shortened in certain instances

o Buy back at cost upon termination of employment, death or marital dissolution prior to the end of the vesting period

o 83(b) Election

o Acceleration Issues: Termination & Change of Control

• Right of first refusal for sale to third parties

• The role of employment agreements

7

8

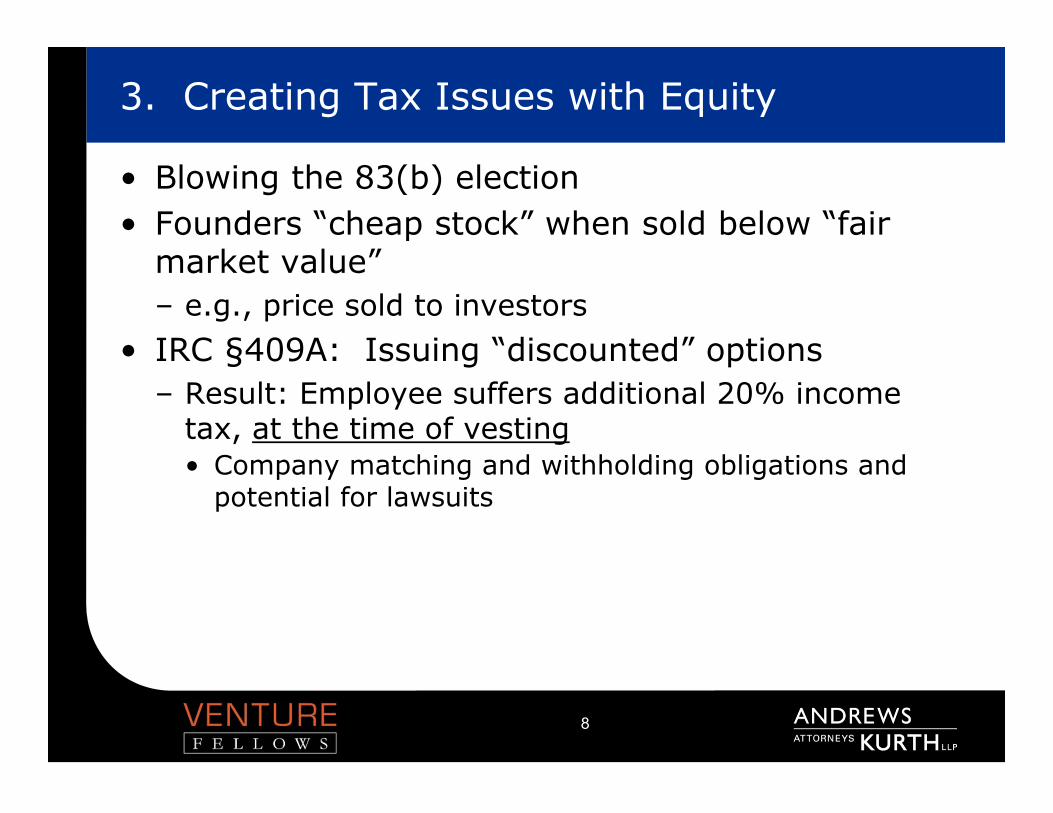

3. Creating Tax Issues with Equity

• Blowing the 83(b) election• Founders “cheap stock” when sold below “fair

market value”– e.g., price sold to investors

• IRC §409A: Issuing “discounted” options– Result: Employee suffers additional 20% income

tax, at the time of vesting• Company matching and withholding obligations and

potential for lawsuits

9

4. Failure to Maintain Proper Documentation; Capitalization Errors

• Inadequate Capitalization Hygiene– Too many “promises”; too little documentation

• Promising a %, especially when non-dilutable• Convertible note should not convert into a % interest,

but rather a number of shares based on share price formula

– Failure to approve at Board / shareholder level– “Handshake” deals

• Inadequate Recordkeeping– Failing to maintain adequate organizational records– Failing to track agreements (e.g. NDAs)

• CONVERSE: Too many agreements

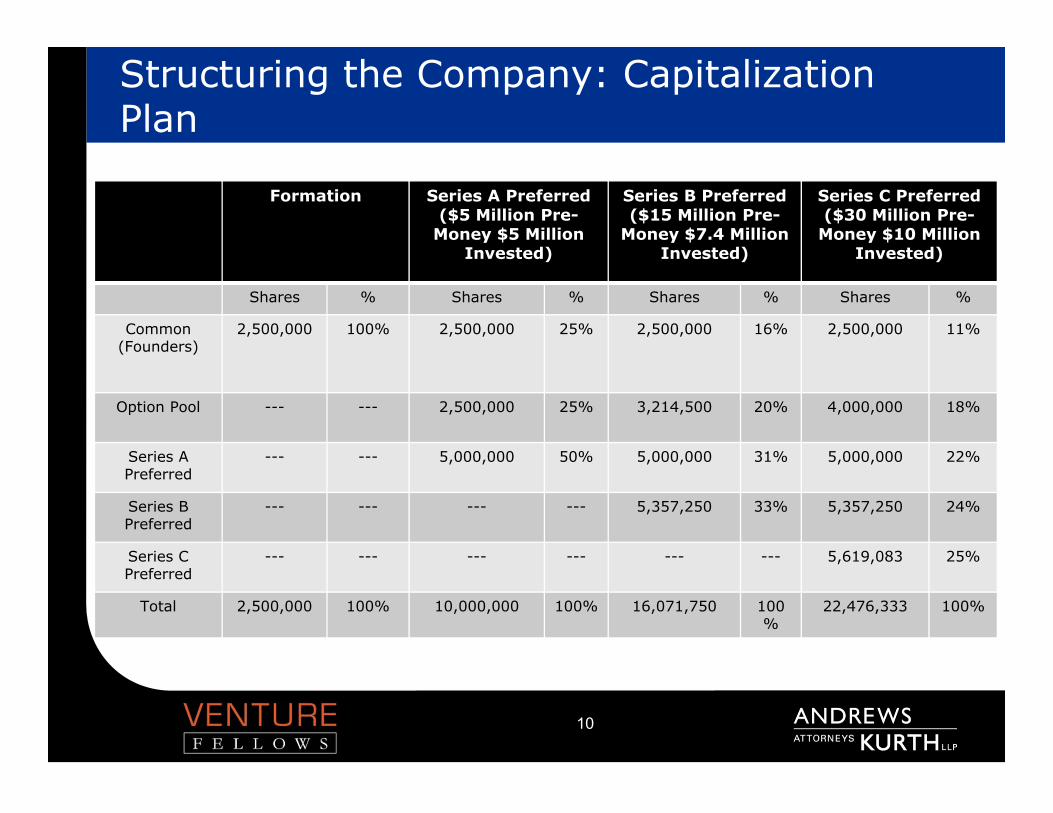

Structuring the Company: Capitalization Plan

10

Formation Series A Preferred ($5 Million Pre-

Money $5 Million Invested)

Series B Preferred ($15 Million Pre-

Money $7.4 Million Invested)

Series C Preferred ($30 Million Pre-

Money $10 Million Invested)

Shares % Shares % Shares % Shares %

Common(Founders)

2,500,000 100% 2,500,000 25% 2,500,000 16% 2,500,000 11%

Option Pool --- --- 2,500,000 25% 3,214,500 20% 4,000,000 18%

Series A Preferred

--- --- 5,000,000 50% 5,000,000 31% 5,000,000 22%

Series B Preferred

--- --- --- --- 5,357,250 33% 5,357,250 24%

Series C Preferred

--- --- --- --- --- --- 5,619,083 25%

Total 2,500,000 100% 10,000,000 100% 16,071,750 100%

22,476,333 100%

11

5. Failure to Adequately Protect IP

Patents– ‘First to file’ rule harmonizes U.S. patent system with rest of

the world; now more complex interplay between the dates of filing and of any pre-filing disclosures of the invention.

– Old U.S. rule: Filing required one year from “public disclosure” or sale

– International (PCT) filings

Trademarks– Failure to protect valuable brand– Overinvesting in unprotected/unprotectable brand

• URLs, Facebook, Twitter, etc. accounts• “Bootstrapping” with consulting services without adequate

ownership of services/product delivered• Copyrights: Must register CR before pursuing legal remedies

against infringer. In the case of web software (e.g. iphone app), often costs less than $1,000.

12

6. Hiring Employees Without Regard to Prior Employee Obligations

• Non-competes, non-solicitation• Trade secrets, inevitable disclosure• Using inadequate or outdated forms• Software code, open source• Prior employer documents in possession• No short cuts!

IP Issues and Hiring Employees

• Consider obligations to prior employero Non-disclosure, non-compete, non-solicitationo Even without an agreement, common law trade secret

obligations existo Did you or another develop idea while employed?o Any employer files, documents, computers, smartphone,

storage media, etc. spell trouble

• Beware of the Inevitable Disclosure doctrineo Under the “Inevitable Disclosure” Doctrine, a former employee

of one company may be prohibited from working for a competitor of the previous employer based on the theory that the employee could not perform duties of the new position with the competitor without relying on trade secrets obtained from the previous employer

o Application of the Doctrine does not require the former employee to have executed a non-compete agreement

o Not all states apply the Doctrine13

14

7. Inadequate Agreements with Employees and Contractors

• Employees– Documented offer letters– IP assignments, non-competes, non-solicits

• Contractors– Misclassification when acting as employee– IP assignments; restrictions on competition

Employee and Contractor Agreements

• Obtain a signed proprietary information and invention assignment agreement before (or immediately upon) commencing employment

o Don’t ignore any carve-outs – have someone technical review them

o Get it as of “Day 1” – prior to disclosure of company confidential information

o Consider appropriate, enforceable non-compete/non-solicitation (note state by state enforceability)

o Beware of contractors who become employees – good time to clean-up IP ownership

• Obtain agreements (assignment and NDA) from each consultant and advisor

• Trademarks, URLs and pre-formation IP assignments15

16

8. Failure to Seek or Receive Adequate NDAsCan lose patent/trade secret protection without NDA or other reasonable steps to protect• Watch out for termination dates, residuals,

concurrent development clauses• Failure to police• Using inadequate or outdated forms

Business plans and offering memorandums• At least include confidentiality statement• VCs will not sign – choose carefully before

sending

17

9. Angel/Friends & Family Financings

• Sales to non-accredited investors• Often overpriced

– Creates barriers to future rounds– Dilution and disappointment– “Dumb money”– Option pricing issues when common stock sold

• Inadequate resources to continue to invest and “protect” prior investment

• Administrative hassles– Expensive to administer and may deter VCs– Complex Structures for small dollars

18

10. Institutional Fundraising Errors

• Seeking institutional capital too early• Soliciting the wrong type of investor for the

venture• Choosing the “wrong” VC• Selecting a “strategic” in the first round• Must do your diligence on the investors• Take too much money or too little money with

regard to next value inflection point

19

Bonus: Choosing Wrong Attorney for Venture (or not using one)• Expertise, experience, personality must be a

match• Relationships; understands terms, market,

process• Make the complex simple

– Avoid doing too much, too early– Focus on right things, avoid subtle traps

• Pay me (a lot less) now, or (a lot more) later...IF it can be fixed

• Not being involved in the legal process• Not using AK Fixed Fee Startup Package

20

AK Startup Package (www.akstartup.com)

Incorporation, Organization and Qualification• Reservation of corporate name• Preparation and filing of Delaware

Certificate of Incorporation • Preparation of Bylaws and Certificate of

Secretary • Preparation of Action by Incorporator• Preparation of Organizational Board

Consent regarding various organization and corporate governance matters

• Preparation and filing of Form SS-4 Application for Employer Identification Number

• Preparation and filing of qualification to do business as foreign corporation

• Preparation and organization of corporate records and minute book

• Preparation of Stockholder Consent• Preparation of form Indemnification

Agreements for directors & officers

Capitalization Matters• Entry of capitalization data and corporate

records into capitalization tracking software and corporate records database

• Preparation of Founder’s Restricted Stock Purchase Agreement for up to four Founders

• Preparation of Stock Certificates for up to four Founders

• Preparation of Memorandum re 83(b) Elections for Founders

• Preparation and filing of state securities filings for stock issuances to Founders

• Preparation of Stock Option/Stock Issuance Plan

• Preparation of forms of Early and Standard Exercise Stock Option Agreement

• Preparation of form of Stock Issuance Agreement

• Preparation/filing of Form U-2 Uniform Consent to Service of Process

21

AK Startup Package

Employment and Consulting Matters• Preparation of form of At-Will Employment

Offer Letter• Preparation of form of Proprietary

Information and Inventions Agreement• Preparation of Form of Independent

Contractor Services Agreement

Intellectual Property Matters• Preparation of form of Unilateral

Nondisclosure Agreement• Preparation of form of Mutual

Nondisclosure Agreement• Preparation of Assignment of Intellectual

Property from Founders to the company• Preparation of Memorandum re Trademark

Matters for a new company

Consultations• One hour of advice on employment

matters• One hour of advice on employee

benefits matters• One hour of advice on protecting

intellectual property • One hour of advice on venture capital

term sheets

22

A Focus on Emerging Growth

Andrews Kurth is a leading law firm for entrepreneurs, public and private emerging growth companies, and venture capital and private equity firms. Our Technology and Emerging Companies Practice Group comprises a dedicated team of attorneys providing focused representation to public and private emerging growth companies and entrepreneurs as well as the venture capital and private equity firms that finance them. We take pride in having a practical, business-like approach to advising our clients, and we share their entrepreneurial spirit and drive.

Our client service teams combine relevant experience with an understanding of a client’s business and markets to provide efficient legal services and solutions with an outstanding degree of responsiveness.

We thrive in the fast-paced entrepreneurial world by combining flexibility and speed with the experience that comes from taking billions of dollars in new ventures from inception to IPO and beyond.

Matt Lyons is the Managing Partner of the Austin office of Andrews Kurth LLP. He represents public and private companies, venture and private equity funds, emerging growth companies and entrepreneurs in public and private offerings, mergers, acquisitions and divestitures, and issues related to business formation, operation, executive compensation and corporate governance.

Matt received his J.D. in 1993, with honors, from The University of Texas School of Law and his B.A., with high honors, from The University of Texas in 1990.

Matt has been profiled as one of The Best Lawyers in America in Securities/Capital Markets Law (2013-2015) and as a leading technology lawyer in the United States in The US Legal 500 (2010-2014) and Chambers USA: America’s Leading Business Lawyers (2006-2104).

ANDREWS KURTH LLPTechnology & Emerging Companies Practice Growth

MATT LYONS

phone: (512) 320-9284fax: (512) 320-9292email: [email protected]

The materials included herein provide a general description of certain legal and business matters and should not be construed as providing specific legal

advice or establishing an attorney-client relationship.

23

Q&A

Thank You!Open Discussion / Q&A