TM12009 Processing Tomato Strategic Investment Plan · PDF fileAPTRC Inc . TM12009 Processing...

47

APTRC Inc TM12009 Processing Tomato Strategic Investment Plan (23/08/2013) Final Report Author: Robert Rendell et al, RMCG 23 August 2013 Bendigo Office: 135 Mollison Street, Bendigo PO Box 2410 Mail Centre, Bendigo, Victoria 3554 T (03) 5441 4821 F (03) 5441 2788 E [email protected] W www.rmcg.com.au

Transcript of TM12009 Processing Tomato Strategic Investment Plan · PDF fileAPTRC Inc . TM12009 Processing...

APTRC Inc

TM12009 Processing Tomato Strategic Investment Plan (23/08/2013)

Final Report

Author: Robert Rendell et al, RMCG

23 August 2013

Bendigo Office: 135 Mollison Street, Bendigo PO Box 2410 Mail Centre, Bendigo, Victoria 3554 T (03) 5441 4821 F (03) 5441 2788 E [email protected] W www.rmcg.com.au

Document Review & Authorisation Job Number: 1-A-22 Document Version

Final/ Draft Date Author Reviewed

By Checked by BUG

Release Approved By Issued to Copies Comments

1.0 Draft 25/06/13 R. Rendell P. Gray

APTRC APTRC and HAL 1(e)

2.0 Final 23/08/13 R. Rendell P. Gray

R. Rendell P. Mawson R. Rendell APTRC and HAL 1(e)

Note: (e) after number of copies indicates electronic distribution

TM12009: Processing Tomato Strategic Investment Plan

Project Leader: Robert Rendell, RMCG. [email protected]

The purpose of this report is to identify the Research & Development program which the Australian Processing Tomato Research Council Inc will undertake to meet industry objectives during the next five years.

Funded by the Australian Processing Tomato Research Council Inc and Horticulture Australia Limited.

Any recommendations contained in this publication do not necessarily represent current HAL policy. No person should act on the basis of the contents of this publication, whether as to matters of fact or opinion or content, without first obtaining specific independent professional advice in respect of the matters set out in this publication.

Contact Details: Name: Peter Gray Title: Senior Consultant Address: PO Box 2410, Mail Centre, Bendigo 3554 P: (03) 5441 4821 F: (03) 5441 2788 M: 0428 261 252

International Standards Certification

QAC/R61//0611

Disclaimer: This report has been prepared in accordance with the scope of services described in the contract or agreement between RMCG and the Client. Any findings, conclusions or recommendations only apply to the aforementioned circumstances and no greater reliance should be assumed or drawn by the Client. Furthermore, the report has been prepared solely for use by the Client and RMCG accepts no responsibility for its use by other parties.

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Classified - Restricted

Table of Contents

Executive Summary 1

1 Background 2

2 Situation Analysis 3

2.1 Introduction .............................................................................................................................. 3

2.2 Customers and markets .......................................................................................................... 3

2.2.1 Markets and consumption ............................................................................................. 3

2.2.2 Competition ................................................................................................................... 4

2.3 Industry performance .............................................................................................................. 4

2.3.1 Location and extent of production ................................................................................. 4

2.3.2 Technology in the industry ............................................................................................ 6

2.3.3 Industry economics ....................................................................................................... 7

2.4 Risk and opportunity ............................................................................................................... 9

2.4.1 Managing harvest risk ................................................................................................... 9

2.4.2 The processing tomato production system ................................................................. 10

2.4.3 Logistics and profit ...................................................................................................... 10

2.5 People – growers .................................................................................................................. 11

2.6 People – primary processors ................................................................................................ 12

2.7 Industry Organisation ............................................................................................................ 14

2.7.1 Peak industry body, and IDM ...................................................................................... 14

2.7.2 The IDM role ............................................................................................................... 15

2.7.3 Funding ....................................................................................................................... 16

2.7.4 Technical information and communication ................................................................. 16

2.8 Biosecurity and risk management ......................................................................................... 17

2.9 Industry vision ....................................................................................................................... 17

2.10 Summary of Industry Issues .................................................................................................. 17

3 The current investment plan 19

3.1 Strategic objectives ............................................................................................................... 19

3.2 Plan implementation .............................................................................................................. 19

4 Industry objectives for the next five years 22

4.1 Limiting factors ...................................................................................................................... 22

4.2 Industry objectives ................................................................................................................ 22

4.3 Implications for industry development ................................................................................... 22

4.4 Strategies and actions ........................................................................................................... 23

5 Strategic Investment Plan 25

6 Business case analysis 39

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Classified - Restricted

6.1 Introduction ............................................................................................................................ 39

6.2 Business Analysis ................................................................................................................. 39

7 Example of audit scope for crop production 40

Appendix 1: IDNA – Industry characteristics 41

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 1

Executive Summary Since its record year of 380,000 tonnes in 2000/01, production of Australian processing tomatoes has declined to its present level of 193,000 tonnes in 2013.

The industry is now comprised of three processors, one corporate farm and eleven independent farms. Three processors operate in different market segments. Kagome processes tomatoes for bulk products such as paste and puree for domestic and international markets, SPCA produces canned tomatoes predominantly for the domestic retail market and Billabong produces canned tomatoes for the domestic and retail food service sector. Imports have penetrated the Australian processed tomato market over past few years.

This Strategic Investment Plan identifies strategies and actions that will enable the local industry to be competitive, and provide opportunities for it to regain share of the market. Industry development will be driven by the following activities:

Improve productivity to reduce unit costs

Mitigate harvest risk to improve the contract fulfillment rate

Increase average yield to reduce unit costs. Develop quality attributes to improve conversion rates.

Reduce input costs through informed agronomic practices and technology.

Maintain innovation and skills capacities

Redefine the IDM role to ensure that the development program is delivered

Engage the personnel required to effectively conduct trials

Conduct study tours to expose growers and processors to new ideas

Continue network development through the World Tomato Processing Council.

Influence national consumption of Australian processed tomato products

A pilot plant will enable the industry to conduct low-volume fruit trials and develop new products

Undertake market research to inform new product development

Develop a social media platform to influence consumer perception of Australian tomato processing industry and Australian processed tomato products.

Refine APTRCs structure and funding

Ensure that Committee members have the appropriate skills

Appoint an independent Chair to drive accountability

Allocate a Committee member to mentor each strategic action

Increase the industry levy rate.

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 2

1 Background

The Australian processing tomato Industry comprises 12 growers producing 193,000 tonnes in Northern Victoria and Southern New South Wales, with a farm gate value of about $19 million.

The tomatoes are processed in three plants, which employ about 240 seasonal staff.

The main processed product is aseptic paste which is value-added by secondary processors into paste-based foods. The remaining tomatoes are sold into the retail market as wholepeel, diced or juiced products. Apparent Australian consumption is about 520,000 equivalent raw tonnes of tomato-based products, of which the local industry supplies 30%.

The industry has seen enormous consolidation; from 38 growers producing 380,000 tonnes supplying seven factories in 2001, to its current state.

Apparent national consumption has increased by 50% since 1997, slightly greater than population increase, but the Australian-produced share has declined.

In the past, the industry generally has undertaken some significant strategic activities, such as; full-industry benchmarking, strategic reviews, and hosting the World Congress symposium in Melbourne.

The industry has been active in world industry strategies, and has twice provided Chairs for the World Processing Tomato Council.

Industry research has been historically coordinated by APTRC and activated through a series of three-five year strategic plans.

APTRC is a committee of grower and processor representatives, and has an annual budget of about $145,000 funded by levies and HAL; in 2001 the annual budget was $314,000.

APTRC has been a leader in encouraging significant productivity gains in an industry that has been open to intense international competition for many years.

APTRC has undertaken the development of a strategic plan by engaging an independent facilitator who conducted detailed discussions with processor management and growers. This document represents the findings of that process.

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 3

2 Situation Analysis

2.1 Introduction

The industry has collected high-quality seasonal data for many years, and the ‘Annual Industry Survey’ is included in the annual magazine which is distributed to all stakeholders. Most of the data for this analysis was sourced from those surveys.

2.2 Customers and markets

2.2.1 Markets and consumption

Raw tomatoes are grown under contract for businesses which process them into a range of food products. The substantial bulk of the crop is primary processed into aseptic paste. This is further value-added by secondary processors which on-sell their branded (and supermarket home-brand) products to retailers. The remaining primary-processed output is sold as wholepeel, diced/crushed or juiced products.

The global processed tomato industry has well-established, collegiate networks and innovation moves quickly once ideas are proven commercially. Australian processors are typically multi-national and have continuously introduced new products and marketing attributes to stimulate demand. Tomato products are well-recognised by consumers, given the household brands associated with Mars, Simplot, SPC Ardmona and Unilever.

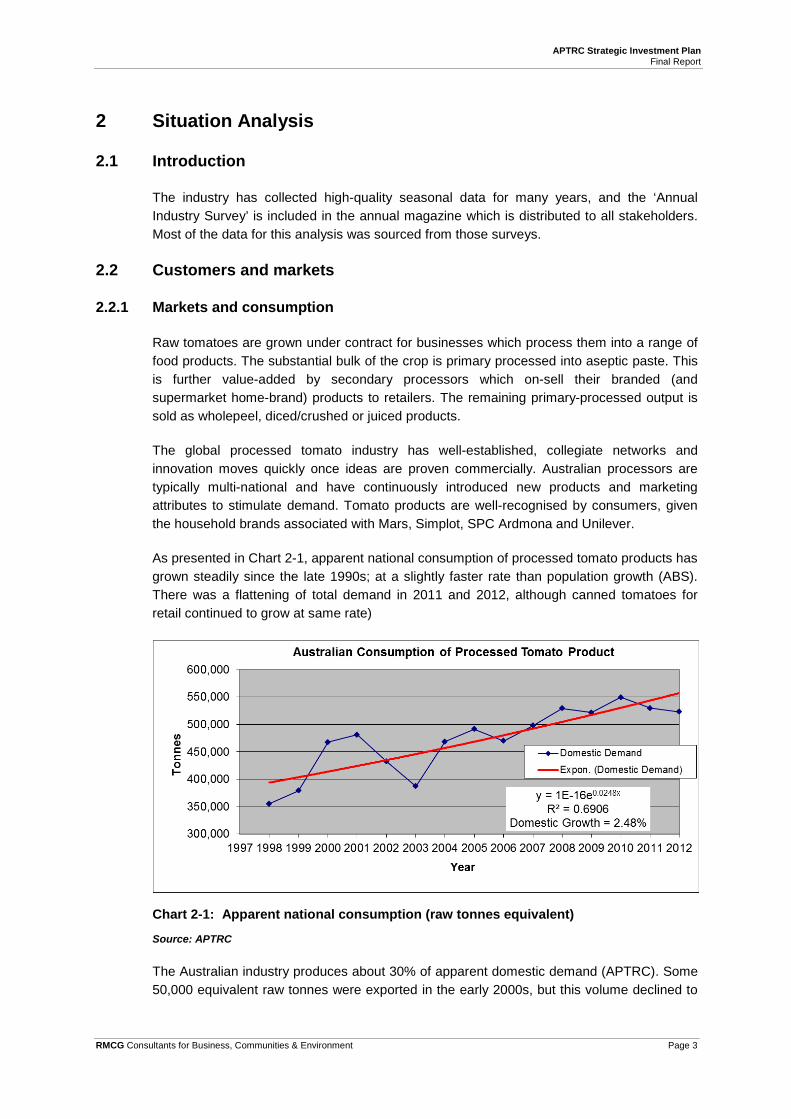

As presented in Chart 2-1, apparent national consumption of processed tomato products has grown steadily since the late 1990s; at a slightly faster rate than population growth (ABS). There was a flattening of total demand in 2011 and 2012, although canned tomatoes for retail continued to grow at same rate)

Chart 2-1: Apparent national consumption (raw tonnes equivalent)

Source: APTRC

The Australian industry produces about 30% of apparent domestic demand (APTRC). Some 50,000 equivalent raw tonnes were exported in the early 2000s, but this volume declined to

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 4

about 15,000 tonnes by 2010. Export trade increased a little by 2012, to just under 20,000 tonnes, due to significantly higher sales of paste/puree. New Zealand is the largest buyer of solids products and Singapore is the largest buyer of juice. There may be a future opportunity for Kagome to supply high-quality products to Japan.

Australian industry stakeholders have assisted commercial marketing by identifying and promoting health factors associated with processed tomato consumption, particularly with respect to lycopene, and processors have subsequently developed niche products to capitalise on the nutritional attributes of tomatoes. This market development mirrors international research and promotion.

2.2.2 Competition

Retail canned tomatoes segment have seen an increase in import penetration in recent years. This increase in the share was driven due to cheap prices of imported products. SPCA has done extensive research with consumers which indicates that there is a strong preference for Australian canned tomatoes if price was not the barrier.

Independent market research by Colmar Brunton also suggests that consumers do not identify strongly with Italian tomato products. In 1999, 23,000 equivalent raw tonnes of wholepeel product was imported. By 2011 that volume was 69,000 equivalent raw tonnes, which was substantially maintained in 2012 (APTRC, ABS).

About 83% of the retail canned tomatoes were imported in 2012, which is up from 62% in 2009. This is a significant loss of higher-margin product from the Australian industry. Australian production steadily increased between the early 1990s and the early 2000s. However, seven weather-affected seasons between 2001 and 2012 caused a decline in the availability of raw tomatoes for processing; canning tomatoes were not affected. With apparent national consumption increasing, secondary processors had to import increasing volumes of paste in order to supply their customers. In addition, the major supermarkets chains have sourced higher volumes of low-cost imported wholepeel and diced products.

In 2010, imports equated to 54% of apparent domestic consumption; in the very wet 2011 season imports equated to 86% of apparent domestic consumption (APTRC) for the total processing tomatoes market.

Australian producers face a significant challenge from imported product. In particular, the industry has lost share of higher-margin products. The opportunity is to replace imports for the long-term, and to regain share of high-margin categories.

2.3 Industry performance

2.3.1 Location and extent of production

The processing tomato industry is comprised of one major paste processor, Kagome Australia, one major grower, Kagome Farms, a small number of independent, contracted growers and two other primary processors, SPC Ardmona and Billabong Foods (also a grower). Tomatoes are grown in the following districts:

Victoria – Boort, Colbinabbin, Corop and Rochester/Echuca

New South Wales – Barooga and Jerilderie.

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 5

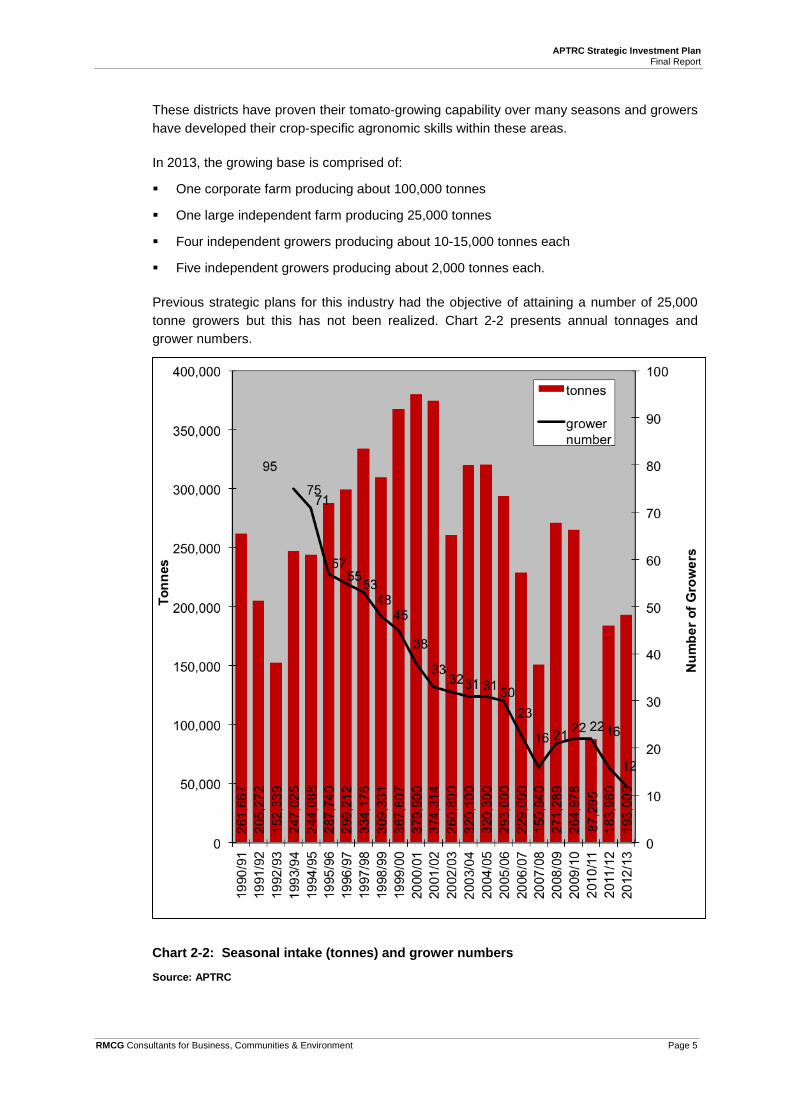

These districts have proven their tomato-growing capability over many seasons and growers have developed their crop-specific agronomic skills within these areas.

In 2013, the growing base is comprised of:

One corporate farm producing about 100,000 tonnes

One large independent farm producing 25,000 tonnes

Four independent growers producing about 10-15,000 tonnes each

Five independent growers producing about 2,000 tonnes each.

Previous strategic plans for this industry had the objective of attaining a number of 25,000 tonne growers but this has not been realized. Chart 2-2 presents annual tonnages and grower numbers.

Chart 2-2: Seasonal intake (tonnes) and grower numbers

Source: APTRC

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 6

From the poor 1992/93 season production increased strongly until about 2002, but has since declined to about 190,000 tonnes, for the following reasons:

Adverse seasonal conditions, including years of low rainfall and the impact of severe wet weather, especially in 2011

Heinz closed its Girgarre factory, taking its 80,000 tonne requirement offshore

Secondary processors and retailers sourced more imported product

The Australian dollar appreciated strongly against the US dollar.

Grower numbers have declined for the following reasons:

As crop yields improved and processing intake reduced, the land required decreased; from 5,100 hectares in 1999/2000 to 1,999 hectares in 2012/2013 (APTRC).

Growers became more comfortable about leaving the industry. Previously held to the industry because of the higher residual seasonal debt this crop can entail, growers acted on their perception of seasonal risk. Some left agriculture altogether but many turned to other farming enterprises.

The corporate farm initially reduced the reliance on independent growers. Over the years it has maintained an important role for its processor, insuring it against variable production from independent farms. However, in doing so it may also have reduced some encouragement for independent growers to get bigger.

Structural consolidation of the industry has been significant, particularly for the grower sector, and the development of positive grower-processor business relationships will be critical to the future. The great opportunity is that consumers are demanding more product than the industry can produce and there is clear potential to expand if competitive challenges can be met.

2.3.2 Technology in the industry

Continuous improvement

The industry has undertaken a series of important technology improvements that have increased productivity to maintain grower margin despite a static price. These improvements include;

The introduction of mechanical harvesting to reduce labour cost

The use of sub-surface drip systems to increase yield through targeted irrigation

Using the drip systems to target-fertigate crops

The introduction of transplants to provide improved crop establishment

The largest processing plant being designed to include the best equipment and processes at the time

The introduction of bulk bins to transport the crop efficiently

The introduction of contract harvesting to reduce grower capital cost.

In a globally-competitive business, the Australian industry has demonstrated that it can improve its productivity through innovation. The challenge is to identify the next

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 7

technological changes that will continue that improvement; an opportunity to be a sustainable industry.

Precision agriculture

Some new technologies may be found through precision agriculture techniques. Although there may be initial limitations (for example, fertigation control), the new technologies that could emerge from a wide canvassing of precision agriculture are worth doing some research on the subject. Initial projects might be based on EM38 and yield mapping.

GRDC has worked on precision agriculture for many years with broadacre farmers. As tomato growers are themselves broadacre farmers there must be capacity to better-understand processes and techniques which have already been identified elsewhere.

Much industry innovation has been implemented after seeing what has been taking place elsewhere; in California, Israel and Europe, for example. The application of learnings from past study trips and contact within networks indicates that these should be maintained.

Automated machinery

Although nursery and planting costs associated with transplants are significant, 81% of area used transplants in 2011/12 (APTRC). However, Kagome Farms began trials to investigate direct seeding again to reduce labour cost. Direct seeding and transplants each require different varieties and agronomics at crop establishment, and there is value in including this investigation as a project to ensure that trials are well-planned and measured.

Some sectors of the vegetable industry have successfully introduced automated machines, and some trials have taken place for tomatoes. A project could investigate whether the latest automated machines being used for vegetables could be adapted for tomato transplants.

2.3.3 Industry economics

The price which a processor can pay for raw tomatoes is predominantly dictated by the prices of imported paste and finished products.

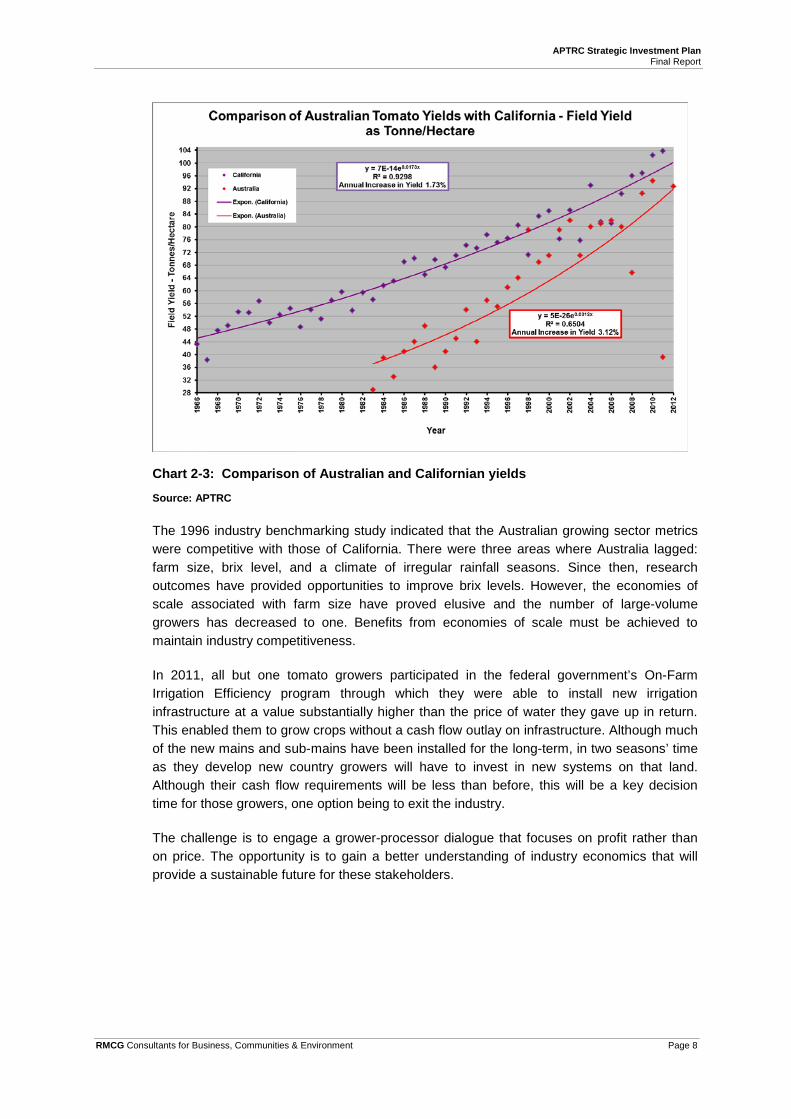

The raw tomato price has not moved appreciably (effectively reducing in value through inflation) for about twenty years; varying around $100 per tonne and valuing current tomato production at about $19 million. Thus the raw tomato value price is now only worth $40 per tonne compared to the 1985 price of $100 per tonne (CPI, RBA).

Given the static raw tomato price, growers have remained in business by steadily increasing productivity. In 1990 average yield was about 40 tonnes per hectare; the 2013 average yield was 96.6 tonnes per hectare and individual field yields can now be in excess of 120 tonnes per hectare. The increase in yields has offset the effective price decline. Increased yields have been driven by changing agronomic technology and practices, and tomato varieties that perform well under Australian conditions.

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 8

Chart 2-3: Comparison of Australian and Californian yields

Source: APTRC

The 1996 industry benchmarking study indicated that the Australian growing sector metrics were competitive with those of California. There were three areas where Australia lagged: farm size, brix level, and a climate of irregular rainfall seasons. Since then, research outcomes have provided opportunities to improve brix levels. However, the economies of scale associated with farm size have proved elusive and the number of large-volume growers has decreased to one. Benefits from economies of scale must be achieved to maintain industry competitiveness.

In 2011, all but one tomato growers participated in the federal government’s On-Farm Irrigation Efficiency program through which they were able to install new irrigation infrastructure at a value substantially higher than the price of water they gave up in return. This enabled them to grow crops without a cash flow outlay on infrastructure. Although much of the new mains and sub-mains have been installed for the long-term, in two seasons’ time as they develop new country growers will have to invest in new systems on that land. Although their cash flow requirements will be less than before, this will be a key decision time for those growers, one option being to exit the industry.

The challenge is to engage a grower-processor dialogue that focuses on profit rather than on price. The opportunity is to gain a better understanding of industry economics that will provide a sustainable future for these stakeholders.

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 9

2.4 Risk and opportunity

2.4.1 Managing harvest risk

The Australian crop is typically harvested from February to April each season. A big issue for growers and processors is that of adverse weather conditions during harvest. Wet weather makes harvest slower, forces processing plants to take in sub-optimal fruit and, in the worst cases, causes crops to be abandoned.

There are three major effects associated with harvest risk:

Growers get paid less than they had hoped for. They need to be paid for every tonne they grow in order to generate enough income in most seasons to mitigate the risks associated with wet seasons. Where they perceive the risk to be too great, they either leave the industry at a time of their choosing, or they are forced to leave.

If raw tomatoes are not delivered per plan, processors cannot optimise their costs through full plant capacity

Relationships between processors and growers suffer, and confidence about the next season is diminished.

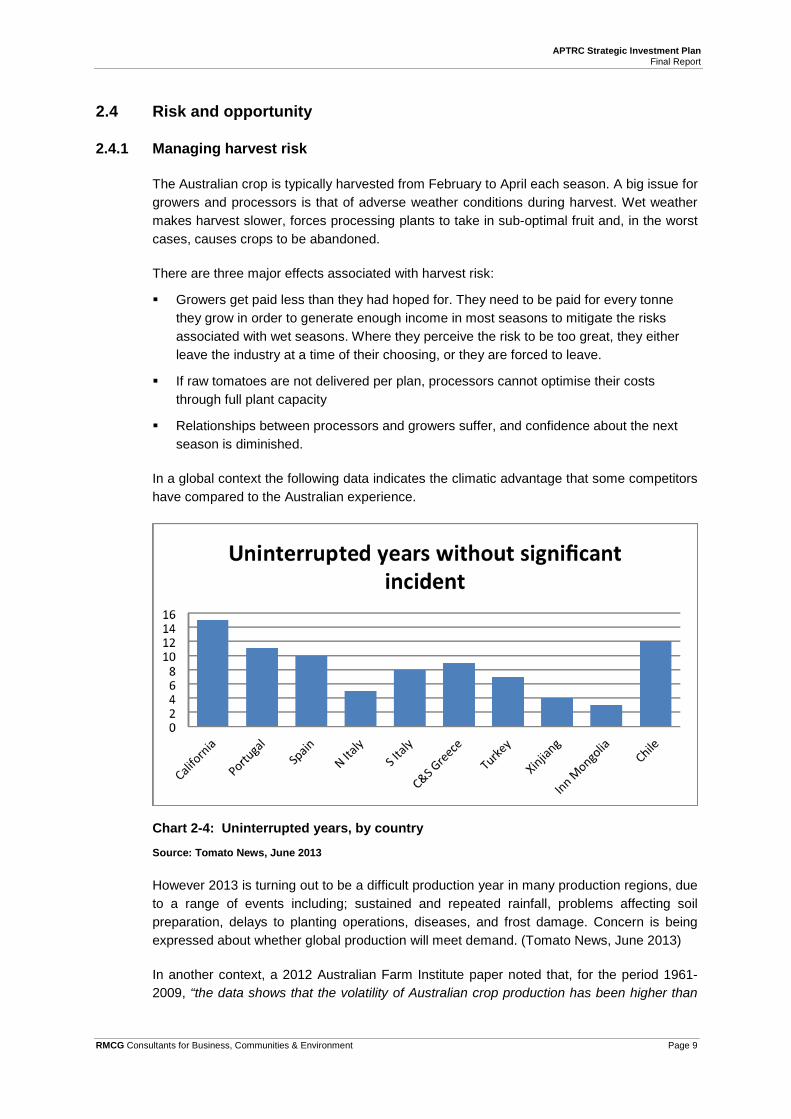

In a global context the following data indicates the climatic advantage that some competitors have compared to the Australian experience.

Chart 2-4: Uninterrupted years, by country

Source: Tomato News, June 2013

However 2013 is turning out to be a difficult production year in many production regions, due to a range of events including; sustained and repeated rainfall, problems affecting soil preparation, delays to planting operations, diseases, and frost damage. Concern is being expressed about whether global production will meet demand. (Tomato News, June 2013)

In another context, a 2012 Australian Farm Institute paper noted that, for the period 1961-2009, “the data shows that the volatility of Australian crop production has been higher than

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 10

for any other nation (either by value or by volume) over the period, and was more than 100% higher than the average for all other nations”.

If there is one issue that must be addressed to enable the Australian industry to grow, it is mitigating poor harvest conditions.

2.4.2 The processing tomato production system

This compact industry offers an opportunity to plan for a profitable future. It is possible to view the industry as one production system, comprised of the following elements:

An internationally recognised paste processor who has made an Australian investment for the long term, and whose ethos is one of working constructively with growers

Two canned tomato processors

One very large corporate farm growing about half the tomato crop

A group of skilled independent growers, some of whom will grow large crops, some medium crops and some smaller crops

A single logistics office to run seasonal tomato scheduling. This task is currently managed by Kagome’s General Manager of Field Operations, and

A competitive unit cost structure.

A key element in achieving this objective is to minimise harvest risk.

2.4.3 Logistics and profit

The tomato season is a major logistical exercise and includes the following steps:

Discussions are held with growers to determine who will be growing tomatoes for the coming season

The establishment of district ‘pods’ of growers whose crops can be harvested efficiently to meet optimum daily factory needs

An agreed schedule with each grower as to when individual blocks of tomatoes will be planted so fruit can be harvested during specific harvest weeks to fill the factory’s intake requirement

Growers prepare their ground, develop their infrastructure and sow their crop at a time that allows them to meet the agreed schedule

The necessary harvesting and transport equipment is contracted for each harvest week to transfer fruit to the factory.

Despite the close attention given to the logistical tasks, the industry has suffered from events that create unease amongst growers and processing staff. These include:

Unusual rain events, and low yields

The inability of some growers to plant according to schedule

Very slow harvesting, and difficulties in deciding which grower’s crop to harvest

Optimising harvest outcomes during normal harvest rainfall events.

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 11

During the past ten years (excluding incomplete data for 2006, and the very poor 2011 year), an average of 89% of Cedenco/Kagome contracts were filled – this includes a 120% fulfilment in 2009. This shortfall equates to 166,453 tonnes of tomatoes contracted by Cedenco/Kagome form paste processing but not delivered. Canned tomato production has been unaffected.

Assuming a price of $100 per tonne, Cedenco/Kagome growers lost gross income of $16.6 million. Assuming a conversion rate of 6 tonnes of raw tomatoes to 1 tonne of paste, and a price of $1,000 per tonne of paste, the processor lost $27.7 million of gross income, or $11.1 million of farmgate margin.

Many key costs are already fixed in the existing production level. Also, this evaluation does not take into account the potential for growers to contract for a 100 tonnes per hectare crop, but grow a 120 tonnes per hectare crop – the additional fruit might not be taken, depending on the season; yet another leakage from the system.

Much industry effort has been put into the annual price negotiations and there is a general fixation around price as being the key economic indicator of success. It is apparent that substantial value leaks from the industry have nothing to do with price, but everything to do with getting the job done better.

It is critical for the industry’s future that growers produce larger-volume crops. To become bigger, growers must have confidence that income from the relatively good years will allow them to bear a bad year. The following processor-grower relationship elements will contribute to encouraging confidence:

Scheduling which optimises factory use and grower returns

Tomatoes being sown on time

Tomatoes being harvested at the optimum time

Every tomato grown being harvested and delivered

Growers being fully paid for every tomato grown.

The challenge is that growers do not perceive the price received for their tomatoes covers the seasonal risk they face, especially in recent years. The opportunity is to create an environment whereby their good years provide sufficient return to mitigate poor years.

2.5 People – growers

Chart 2.2 indicated the dramatic consolidation in grower numbers. As noted previously, Kagome Farms is now the largest grower. Allowing for this, the number of independent growers declined from 71 in 1996 to 11 in 2013.

Growing tomatoes demands very good agronomic skills. It can also be a very rewarding crop. Published studies indicate that gross margin is about $3,500 per hectare; by comparison wheat generates about $250 per hectare and corn about $1,800 per hectare. Over the years, good tomato growers have generally increased their farm sizes and have become some of the best exponents of irrigated agriculture in this country.

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 12

Tomato crops are also associated with high funding requirements. In addition to regular infrastructure investment, a 10,000 tonne crop may have $700,000 invested in it prior to harvest; hence the risk associated with wet seasons. In past seasons higher farm debt has made growers reliant on sowing next year’s crop. However, this nexus has been loosened in recent years, encouraged by the introduction of contract harvesting. Growers are now more willing to grow alternative crops, although they can also re-enter the industry if they perceive conditions to be favourable.

As previously noted, growers have benefitted from the On-farm Irrigation Efficiency program. This has helped with costs but also reduced the dependence on growing tomatoes to pay for the system and some have left the industry because of this.

That recent economic advantage gained by growers has left the industry in danger of losing expertise by not having enough different growers. It is also clear that the number of large-crop growers has declined and, if 25,000 tonnes is likely to be an optimum crop size, efforts are required to develop growers who are willing to grow that volume.

Processing tomato farms have demonstrated that succession to younger family members is alive and well. These are relatively large farming operations, and the industry offers an active international dimension that is attractive to many participants.

The demands, risk and potential reward associated with processing tomatoes has encouraged a collegiate, skilled and vocal group of stakeholders who have the capacity to take the industry forward if they can be encouraged to meet its challenges.

The industry challenge is to increase the number of large-crop growers, to at least four. In doing so, the opportunity is that the combination of these growers plus Kagome Farms will enable the industry to grow at least 75% of its future crop needs at its lowest economic cost.

2.6 People – primary processors

Kagome Australia at Echuca is the industry’s largest primary processor, purchasing its factory from New Zealand/US operators who had tried to incorporate best practice technology and processes. It is an internationally important food manufacturer known for taking a long-term view of its investments. Its business strategies are fundamental to the future of the industry.

The future for Kagome is one where:

It is a patient company that will carefully invest capital to build its business

Production will grow to 400,000 raw tonnes equivalent. To do that it will invest in additional factory capacity.

At least 50% of the tomato crop will be grown by independent growers; the parent company has a strong grower-supportive ethos

Sustainable expansion necessitates driving down growing and processing unit costs to ensure a competitive product. This will be achieved through a combination of scale and technology.

SPC Ardmona at Shepparton is the last of the original primary processors. It takes in raw tomatoes through Kagome, to produce wholepeel, diced and juice products, and

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 13

incorporates paste from Kagome in its added-value products. Its products have faced stiff competition from imported European product that sells at significantly lower price points. In 2002/3 its intake was 87,000 tonnes; in 2013 its intake was 18,000 tonnes. The company has developed differentiated products, and its successful ‘Rich and Thick’ range emerged from collaborative research with Horticulture Australia Limited. Initiatives which reduce unit costs will also benefit SPC Ardmona.

Billabong Foods at Jerilderie is a small family-owned primary processor of wholepeel and diced products. It originally emerged from a tomato-growing business, and formed a connection with SPC Ardmona. This business is largely self-contained.

Two risk management practices were recently presented by Simplot at the industry’s annual forum:

Using an ‘as needed’ offshore product as a safety valve to assist factory utilization. In effect, Kagome would work to full capacity through the intake of the Australian crop, but any seasonal shortfall could be covered by Kagome paste from the US, say; and

Over time Simplot Tasmania and its vegetable growers have established a fund which provides an insurance pool to mitigate seasonal losses.

Although growers and their processors have traditionally held end-of-season reviews, there is a need to become more focused about this process. It should be guided by; the need to grow the industry, be based on objective data, and make each grower and processor accountable for their roles and responsibilities during the season.

As previously noted, there is a fundamental problem that the primary product produced is paste, a commodity, whereas processed tomatoes can be wholepeeled, diced and juice – all higher value and yet this share has declined dramatically.

The processing sector would benefit from the establishment of a pilot plant, where small batches of 10 tonnes, say, could be evaluated for finished product attributes. Although a construction value of up to $1 million may be realistic, there is potential for the plant to be used by; Kagome, SPC Ardmona, Simplot, Unilever, and Mars amongst others. The pilot plant could also be a tool to research options for other processed crops.

Such a plant could be used by the supply chain to develop new products or processes that would increase the proportion of domestic market volume, as well as encourage more exports.

The industry is experiencing significant structural change. Consolidation of factory capacity combined with a more mobile grower base means that robust relationships need to be carefully nurtured in coming seasons. Achieving this will again create a strong industry.

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 14

2.7 Industry Organisation

2.7.1 Peak industry body, and IDM

Australian Processing Tomato Research & Development Committee Inc (APTRC) is the industry’s peak body. Its members are comprised of grower and processor representatives, and it employs an Industry Development Manager as a specific R&D project. APTRC’s formal purposes are:

To allocate funds for, and to oversee various research and industry development projects pertaining to, the tomato processing industry and to administer funds for those purposes

To promote and encourage interest in all aspects of the commercial tomato processing industry

To maintain and improve the sustainability and profitability of the Australian processing tomato industry through the provision of cost-effective administration of project management services which will directly or indirectly benefit the industry, and

To conduct its operations in a non-political manner.

Most of APTRC’s work has related to on-farm production crop management research and development, and it has been very successful at this. Some factory development has also occurred, and in recent years APTRC has participated in market research to better-understand consumer awareness of, and attitudes towards, processed tomato products.

The industry has clearly evolved and is now very much vertically-integrated with Kagome emerging as the primary stakeholder. This places a great deal of trust in the abilities of Kagome’s management team who now figure largely in developing a future for the industry. There is potential for APTRC to become insular, and for discussion to become one-sided.

The structure of APTRC’s committee should reflect the evolving industry. A small group of knowledgeable and committed industry representatives is preferable to a larger number, and APTRC could benefit from the introduction of an independent Chair; as employed by many horticulture IACs. Acting like an independent director, a Chair should be knowledgeable, strong, and able to successfully integrate sometimes competing opinions to achieve industry objectives.

Benefit would also be gained by each research project having a committee member allocated to it, in mentoring, support and informative roles.

APTRC must apply rigor to ensure that industry objectives are met. In particular, improved planning and implementation is needed around projects such as cultivar evaluation. More trials are required each season; these need to be planned with clear objectives, and be implemented well to obtain high-quality outcomes. A more focused approach will also apply to fertilizer/chemical efficacy trials and precision agriculture projects, for example.

Over many years, APTRC has conducted a substantial volume of research. Added to this is the volume undertaken by other broadacre and vegetable industries. A current context behind APTRC research has not been developed, and applicable research from other

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 15

industries has only been partially explored. Departments and CMAs also have a knowledge base that should be considered (about soils, for example). From the commencement of the new plan period APTRC should identify and bring together the research findings that have a direct bearing on the industry’s future needs. Growers should then be re-acquainted with this body of knowledge, and methods adopted through which they can easily and consistently implement the best of this. As new knowledge develops inside and outside the industry the ‘knowledge pack’ can be continuously updated.

Despite encouragement from APTRC, processors have not often come forward to undertake production research under the APTRC banner. At the very least, the industry has lost access to external funding through this lack of interest. With Kagome being substantially the largest primary processor, there is an opportunity to include its production research needs within the umbrella of industry development under APTRC.

Colmar Brunton stated that consumers identify with “Australian-grown” products and could be educated about the production and use of tomato products. APTRC is not in a position to advertise for the industry; that is already done by the brand-name manufacturers. However, given the compact nature of the industry, APTRC is in a position to use social media to project a presence into the national community. An appropriate medium could provide information such as; profiles of growers and processors; descriptions of the unfolding season; how the industry addresses food safety issues; health attributes of tomatoes; using processed tomato products in emerging cuisines; or providing stories about development work. There may be potential for other primary and secondary processors to participate in this generic communication, bringing additional skills and funds to its development.

The challenge for APTRC is that it must evolve to meet increasingly-demanding industry needs. One opportunity is for APTRC to play a key role in delivering industry objectives through high-quality work that will be at the cutting edge of horticultural industry development. There is also an opportunity to recognize and include processor research projects.

2.7.2 The IDM role

Planning discussions with Kagome and independent growers reiterated that the industry perceives the IDM position as being very important to its development.

The industry has been fortunate in its choice of IDMs, with Lauren Thompson and Liz Mann widely recognized for the professionalism and energy they have applied to the role. However, in light of the challenges ahead, it is timely that the IDM role is reviewed and clearly defined for maximum effectiveness. The position is critical to the industry’s development needs being met successfully and the person in that position needs to be used in the best way possible.

The IDM is currently employed on a three-day week basis, and had some assistance during the 2013 season. Even on this basis there were an insufficient number of field trials and a lack of clarity around planning and implementation. Where personnel are being directly employed by APTRC, compared to being part of an external project in the past, then a greater investment in this resource is warranted.

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 16

2.7.3 Funding

APTRC has taken a prudent approach to funding in that its year-end balances are typically about $200,000. Having been through some very poor seasons that almost drained the association of its funds, maintaining a buffer is a reasonable strategy. As to its quantum, it seems reasonable to have a year-end balance equivalent to one year’s forecast expenditure plus 20%, say, of forecast expenditure (average contract fulfillment is 89%). This value will still not cover the levy effect of a season such as 2011 when contract fulfillment was 32%. That was an abnormal year, and it may be too conservative to maintain a balance of 170% of forecast expenditure to allow for rare events.

There is an issue, however, about the current levy rate. In past years it has been $0.50 per tonne for growers, matched $0.50 per tonne by processors. To assist growers through some poor seasons, the rate was reduced to $0.20 per tonne, matched – this means that 2013’s 193,000 tonne crop will produce levy income of a modest $77,000.

A previously unrecognized part of industry funding is that which is spent by processors to implement productivity gains and research new products. There is potential to leverage this development effort through an APTRC/HAL perspective, and APTRC should encourage processors to bring about innovation through collaborative projects.

Tackling current industry issues will require a concerted application of time and money. A development program that must achieve a doubling of the industry is unlikely to be achieved at the current levy rate. APTRC should consider reverting the matched levy rate to $0.50 per tonne, in light of this good 2013 season.

The funding challenge is that innovation must happen quickly and efficiently, and the current funding level is unlikely to meet those criteria. The opportunity is that the industry has proven it can adapt quickly, and the objective of doubling production in three years can be met.

2.7.4 Technical information and communication

Due to its compact size, it has not been difficult for information to flow between industry representatives. Modes of communication are instigated by the IDM and include the following, as described in the industry magazine:

Facilitate the development of the skills and networks amongst growers, processors and support service providers, through:

i. Grower group meetings and visits ii. Coordination of training iii. Field days, on farm demonstrations iv. Technical tours for growers v. Visiting scientists and growers from overseas

Communication activities, including:

vi. A quarterly newsletter, “Tomato Topics” vii. The annual publication, the “Australian Processing Tomato Grower” viii. The annual processing tomato forum.

Communication between stakeholders is done on a personal basis followed up by phone call or text. For example, invitations for a field day can be initiated by email and followed up by phone call.

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 17

The industry has developed an extensive international information network over many years. Industry representatives have twice been Chair of the World Processing Tomato Council, and this body’s meetings are regularly attended to gain a full understanding of global developments that are relevant to the Australian industry.

2.8 Biosecurity and risk management

APTRC is a member of Plant Health Australia, and the IDM initiates, monitors and communicates information about potential plant risks. For example, Tomato Spotted Wilt Virus transmitted by Western Flower Thrips was flagged early for the industry, and crop monitors were given training prior to severe WFT incursions in 2012. The significant WFT incursions experienced by the industry indicate that the IDM’s role relating to biosecurity should continue.

The industry does not yet have its evidence framework in place should an emergency arise, but industry data is substantially better than for many other horticultural industries and APTRC should be able to quickly present a robust case should a serious event occur that would trigger the Deed.

The challenge for the industry is to anticipate pests and diseases that could cause severe damage to tomato crops. Its opportunity is to develop a robust recognition and treatment process that can be quickly rolled out to mitigate significant crop damage.

2.9 Industry vision

Developing an industry vision will be determined by the following:

Currently Kagome – the main player – has a vision of substantially increasing its tomato processing capacity, with 50% independent growers, but at a competitive tomato price

Growers don’t have that vision or confidence

Kagome and its growers need to develop a shared vision through an industry plan

The plan must spell out required yields, scheduling performance, brix, factory yield, and all the other elements which must be achieved for success.

This is a critical project for development funding.

2.10 Summary of Industry Issues

The processing tomato industry is characterised by the following elements:

Australian consumption is increasing but the majority of this increased consumption in recent years has been fulfilled by imports

The domestic industry’s share of higher-margin products has fallen substantially

Farm crop size needs to increase to capture economies of scale

Lack of a shared vision

There is an opportunity to concentrate on profit rather than price by addressing the significant economic leakage from the system through a detailed audit of the supply system

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 18

Unit costs can be reduced by implementing a range of strategies, such as:

− Increasing yields and improving product-related quality attributes

− Conducting ongoing variety evaluation

− Providing clear data about the economic outcomes from direct seeding versus transplants

− Investigating the potential benefits from precision agriculture

− Planning for a longer tomato season to optimise factory capacity

− Maintaining competitive factory processes

− Growing larger-volume farm crops to capture economies of scale. A number of 20,000+ tonne crops are needed.

− Implementing strategies to maintain competitive farm unit cost

− Employing harvesting logistics that capture every tomato grown, at the optimum time

Minimising harvest risk

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 19

3 The current investment plan

3.1 Strategic objectives

The current plan identifies the industry strategic objectives as:

We will meet consumer needs and increase demand

Through new product development based on market research

Generic promotion of the distinctive health benefits of Australian-grown tomatoes, and

Testing imported products for their compliance with Australian food safety standards.

We will improve production efficiency

Through more productive manufacturing technologies and processes

By adopting agronomic practices that optimise fruit yield and quality while containing cost

By growing varieties that can deliver higher yields and improved quality at reduced cost, and

Benchmarking industry performance and sharing knowledge.

We will improve market intelligence

By commissioning an annual report on global economic and industry trends and drivers.

We will pursue the efficient use of industry resources

By managing climate variability effectively

By building skills and leadership, and

Encouraging collaborative research with other industries.

The following section considers APTRC’s implementation of this plan.

3.2 Plan implementation

Previous industry plans have identified issues, objectives and strategies, but project choice and implementation has been left to APTRC’s discretion. The following table considers actual development work against the plan.

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 20

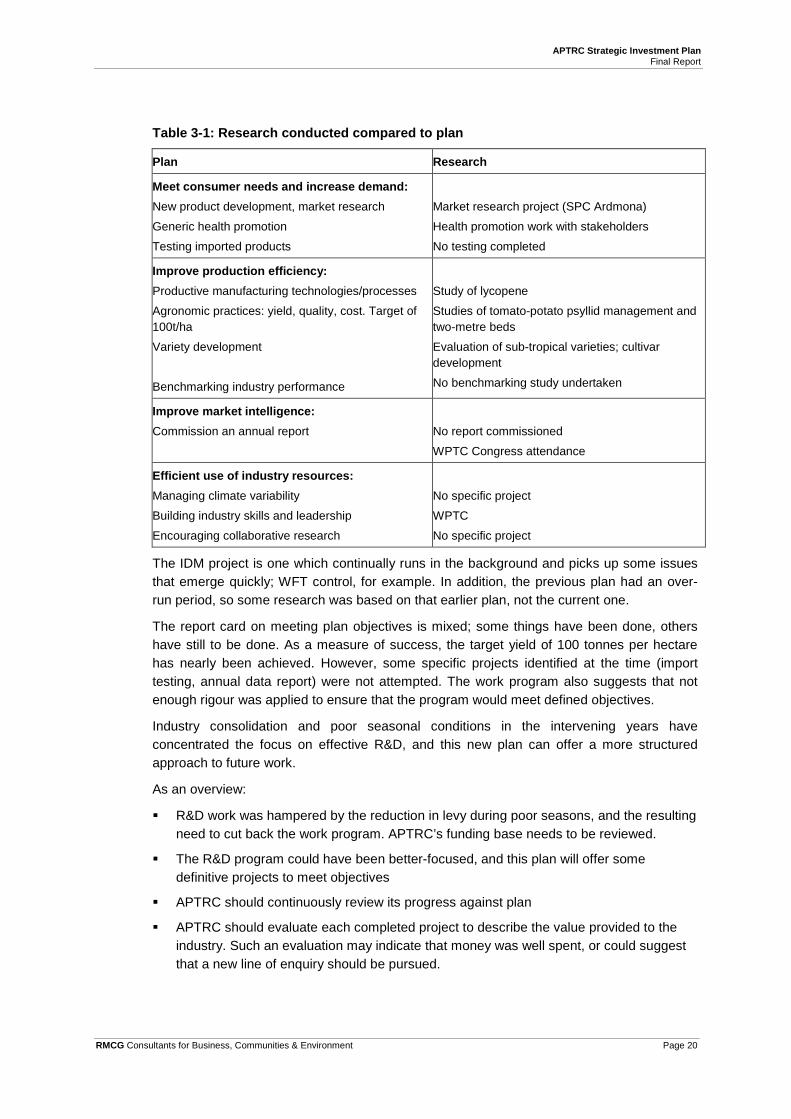

Table 3-1: Research conducted compared to plan

Plan Research

Meet consumer needs and increase demand: New product development, market research

Generic health promotion

Testing imported products

Market research project (SPC Ardmona)

Health promotion work with stakeholders

No testing completed

Improve production efficiency: Productive manufacturing technologies/processes

Agronomic practices: yield, quality, cost. Target of 100t/ha

Variety development

Benchmarking industry performance

Study of lycopene

Studies of tomato-potato psyllid management and two-metre beds

Evaluation of sub-tropical varieties; cultivar development

No benchmarking study undertaken

Improve market intelligence: Commission an annual report

No report commissioned

WPTC Congress attendance

Efficient use of industry resources: Managing climate variability

Building industry skills and leadership

Encouraging collaborative research

No specific project

WPTC

No specific project

The IDM project is one which continually runs in the background and picks up some issues that emerge quickly; WFT control, for example. In addition, the previous plan had an over-run period, so some research was based on that earlier plan, not the current one.

The report card on meeting plan objectives is mixed; some things have been done, others have still to be done. As a measure of success, the target yield of 100 tonnes per hectare has nearly been achieved. However, some specific projects identified at the time (import testing, annual data report) were not attempted. The work program also suggests that not enough rigour was applied to ensure that the program would meet defined objectives.

Industry consolidation and poor seasonal conditions in the intervening years have concentrated the focus on effective R&D, and this new plan can offer a more structured approach to future work.

As an overview:

R&D work was hampered by the reduction in levy during poor seasons, and the resulting need to cut back the work program. APTRC’s funding base needs to be reviewed.

The R&D program could have been better-focused, and this plan will offer some definitive projects to meet objectives

APTRC should continuously review its progress against plan

APTRC should evaluate each completed project to describe the value provided to the industry. Such an evaluation may indicate that money was well spent, or could suggest that a new line of enquiry should be pursued.

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 21

APTRC should review research conducted by other industries. Processing tomatoes has an opportunity to draw on work being done elsewhere. That work might either be complete, or might need a little further tomato-related work to have it industry-ready.

Although an open approach was used to implement past plans, it is preferable to provide a project structure for initial consideration by APTRC (to be discussed during the review of this report). There is an interesting and challenging program ahead upon which the industry’s future will clearly depend.

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 22

4 Industry objectives for the next five years

4.1 Limiting factors

The current limiting factors include the following elements:

Pressure to attain a competitive cost/price structure for Australian products will impact on prices for raw tomatoes and finished product

Factory capacity is fixed, but is about to increase

Grower confidence has been dented by factory consolidation and challenging seasons; who will grow 20,000+tonnes?

Removing or mitigating risk.

4.2 Industry objectives

The industry is recovering from stakeholder consolidation and wet seasons. To be sustainable it must grow. Doubling in size, for example, will take it back to where it was in 2001.

We suggest that key objectives are as follows:

Primary processing output will double, potentially to the 2001 level of 380,000

Primary processing products will be import-competitive

One corporate farm will produce 200,000 tonnes of tomatoes

Independent farms will produce 200,000 tonnes of tomatoes. Of these, four will produce about 25,000 tonnes each.

Processors and growers will generate a viable return on capital.

In summary:

“The industry will double in size by producing competitive, profitable, products”

4.3 Implications for industry development

Some industry issues will be solved by the stakeholders, others will benefit from investment in research. Those which will be solved by stakeholders include;

Additional capital investment in farm and paste production infrastructure; (canned tomato production capacity is sufficient)

Developing grower/processor relationships that could open up new ways of doing business

Changing the R&D structure to focus on the industry vision, and ensuring that successful outcomes are delivered through high-quality research

Improving the understanding of seed/transplant economics

Investigating the potential for precision agriculture

Encouraging growers who would be willing to grow 20,000 or more tonnes

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 23

Planning for early-season tomatoes and allowing growers a bigger say in the varieties that would be grown

Paying more attention to the ground in which tomatoes will be planted, and ensuring tomatoes are planted when they should be

More accountability and transparency around roles and responsibilities

Contracting to optimum plant capacity

Harvesting at the optimum time

Considering post-harvest price step-ups as international trading conditions allow them.

Research will play a role in:

Reducing farm unit costs. One element is increasing average yield.

Improved crop outturn, with the objective of harvesting every tomato from higher yields at the optimum time. Contract fulfillment must be 100% or better.

Developing practices that mitigate seasonal risk and encourage larger crops. Average grower crop size must increase significantly.

Reducing processing unit costs

Investigating new products and processes in a pilot plant.

The primary objective of any R&D project will be to increase productivity. The defined target is to attain an industry cost structure that is competitive with the imported aseptic paste, diced and whole peeled products price. To this end, every project must be well-planned and measurable data captured.

4.4 Strategies and actions

The industry R&D program will be based on the following pillars:

Pillar 1 – Improve productivity to reduce unit costs

Growers and processes do not currently share a common vision for the industry. This needs to be discussed and addressed so that businesses can invest in the future.

Mitigate harvest risk to improve the contract fulfillment rate

Increase average yield to reduce unit costs. Develop quality attributes to improve conversion rates.

Reduce input costs through informed agronomic practices and technology.

Pillar 2 – Maintain innovation and skills capacities

Maintain and redefine the IDM role to ensure that the R&D program is delivered

Engage the personnel required to effectively conduct trials

Conduct study tours to expose growers and processors to new ideas

Continue network development through WTPC.

Pillar 3 – Influence national consumption of Australian processed tomato products

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 24

A pilot plant will enable the industry to conduct low-volume fruit trials and develop new products

Undertake market research to inform new product development

Develop a social media platform to influence consumer perception of the Australian industry and its products.

Pillar 4 – Refine APTRCs structure and funding

Ensure that Committee members have the appropriate skills

Appoint an independent Chair to drive accountability

Allocate a Committee member to mentor each strategic action

Increase the industry levy from its current rate of $0.20 per tonne matched to the previous rate of $0.50 per tonne.

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 25

5 Strategic Investment Plan

PILLAR 1 – SYSTEM PRODUCTIVITY --------------------------------------------------------------------------------------------------------------------------------------------------------------------------- Overarching SIP Objective “The industry will double in size by producing competitive, profitable, products” System Productivity Objective Develop a competitive production platform by reducing unit cost Strategies Strategy 1.1 Processors and growers agree an Industry Plan Strategy 1.2 Mitigate harvest risk Strategy 1.3 Increase average yield and improve quality attributes Strategy 1.4 Reduce input costs ---------------------------------------------------------------------------------------------------------------------------------------------------------------------------

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 26

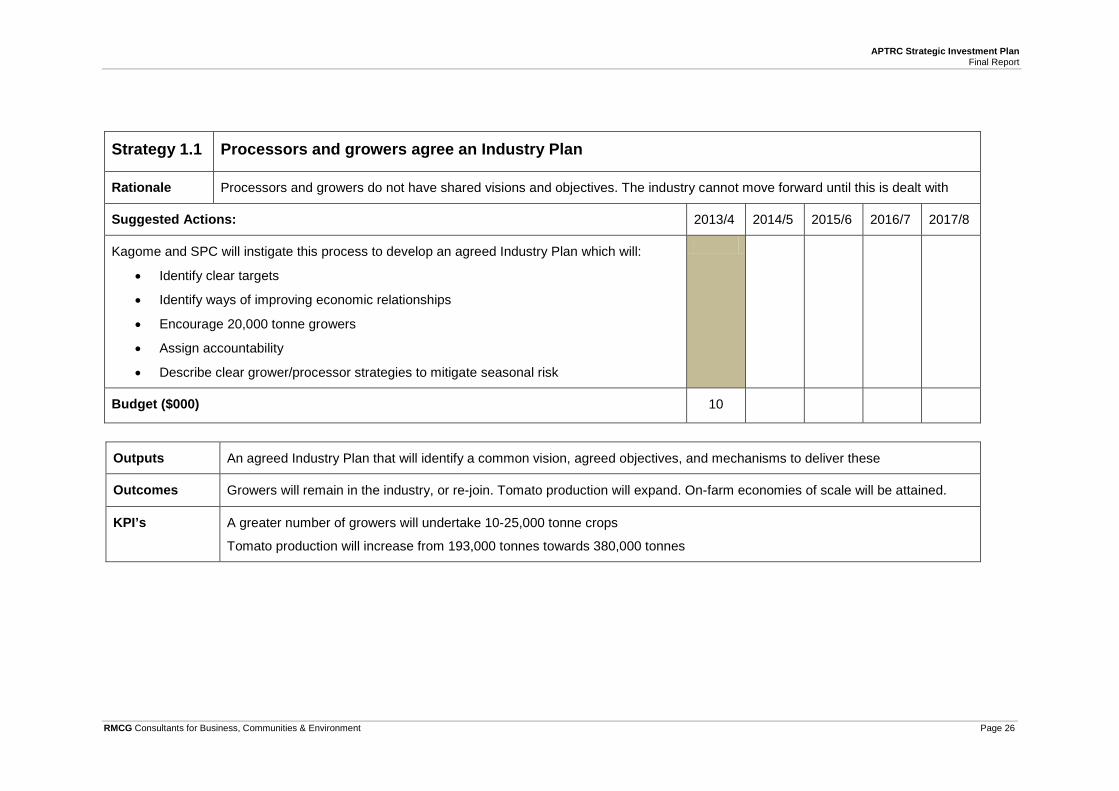

Strategy 1.1 Processors and growers agree an Industry Plan

Rationale Processors and growers do not have shared visions and objectives. The industry cannot move forward until this is dealt with

Suggested Actions: 2013/4 2014/5 2015/6 2016/7 2017/8

Kagome and SPC will instigate this process to develop an agreed Industry Plan which will:

• Identify clear targets

• Identify ways of improving economic relationships

• Encourage 20,000 tonne growers

• Assign accountability

• Describe clear grower/processor strategies to mitigate seasonal risk

Budget ($000) 10

Outputs An agreed Industry Plan that will identify a common vision, agreed objectives, and mechanisms to deliver these

Outcomes Growers will remain in the industry, or re-join. Tomato production will expand. On-farm economies of scale will be attained.

KPI’s A greater number of growers will undertake 10-25,000 tonne crops

Tomato production will increase from 193,000 tonnes towards 380,000 tonnes

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 27

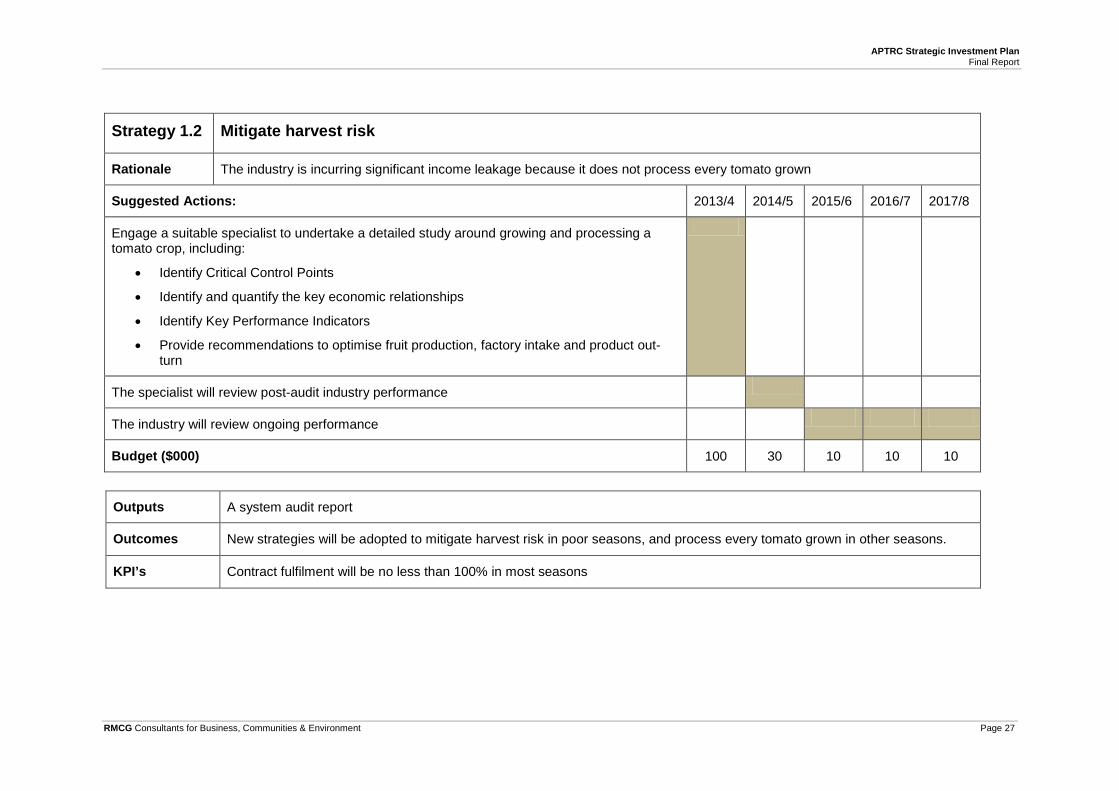

Strategy 1.2 Mitigate harvest risk

Rationale The industry is incurring significant income leakage because it does not process every tomato grown

Suggested Actions: 2013/4 2014/5 2015/6 2016/7 2017/8

Engage a suitable specialist to undertake a detailed study around growing and processing a tomato crop, including:

• Identify Critical Control Points

• Identify and quantify the key economic relationships

• Identify Key Performance Indicators

• Provide recommendations to optimise fruit production, factory intake and product out-turn

The specialist will review post-audit industry performance

The industry will review ongoing performance

Budget ($000) 100 30 10 10 10

Outputs A system audit report

Outcomes New strategies will be adopted to mitigate harvest risk in poor seasons, and process every tomato grown in other seasons.

KPI’s Contract fulfilment will be no less than 100% in most seasons

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 28

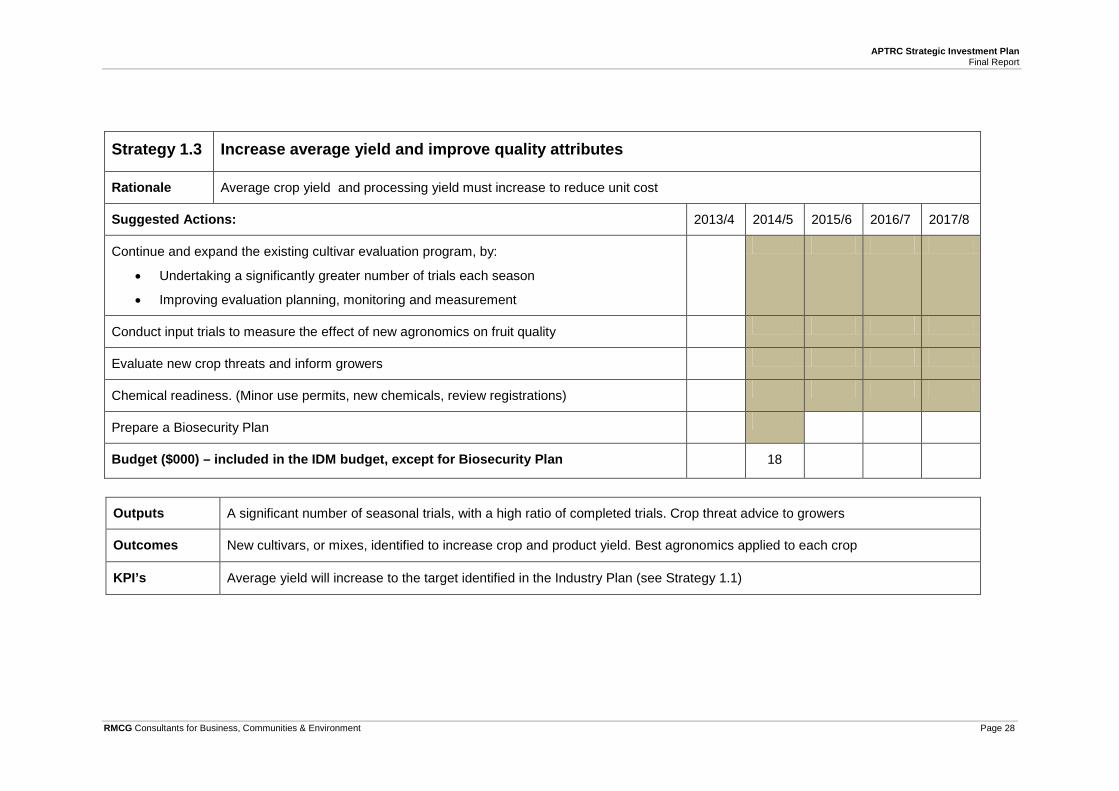

Strategy 1.3 Increase average yield and improve quality attributes

Rationale Average crop yield and processing yield must increase to reduce unit cost

Suggested Actions: 2013/4 2014/5 2015/6 2016/7 2017/8

Continue and expand the existing cultivar evaluation program, by:

• Undertaking a significantly greater number of trials each season

• Improving evaluation planning, monitoring and measurement

Conduct input trials to measure the effect of new agronomics on fruit quality

Evaluate new crop threats and inform growers

Chemical readiness. (Minor use permits, new chemicals, review registrations)

Prepare a Biosecurity Plan

Budget ($000) – included in the IDM budget, except for Biosecurity Plan 18

Outputs A significant number of seasonal trials, with a high ratio of completed trials. Crop threat advice to growers

Outcomes New cultivars, or mixes, identified to increase crop and product yield. Best agronomics applied to each crop

KPI’s Average yield will increase to the target identified in the Industry Plan (see Strategy 1.1)

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 29

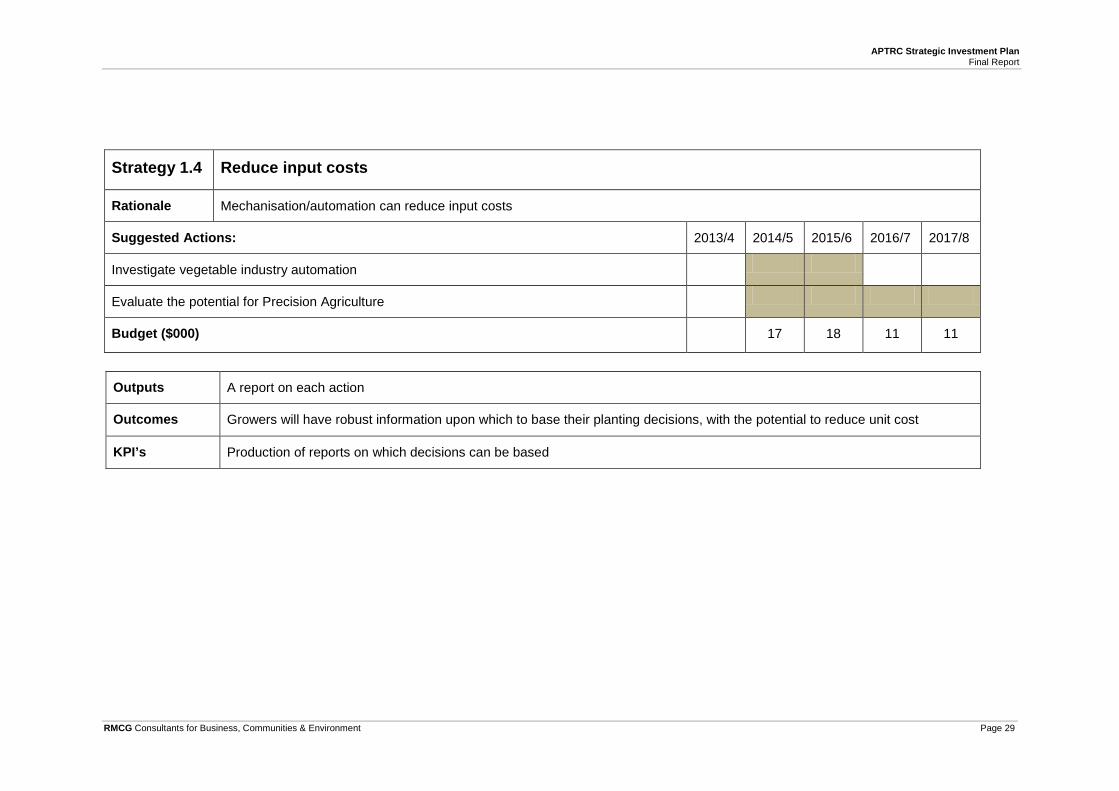

Strategy 1.4 Reduce input costs

Rationale Mechanisation/automation can reduce input costs

Suggested Actions: 2013/4 2014/5 2015/6 2016/7 2017/8

Investigate vegetable industry automation

Evaluate the potential for Precision Agriculture

Budget ($000) 17 18 11 11

Outputs A report on each action

Outcomes Growers will have robust information upon which to base their planting decisions, with the potential to reduce unit cost

KPI’s Production of reports on which decisions can be based

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 30

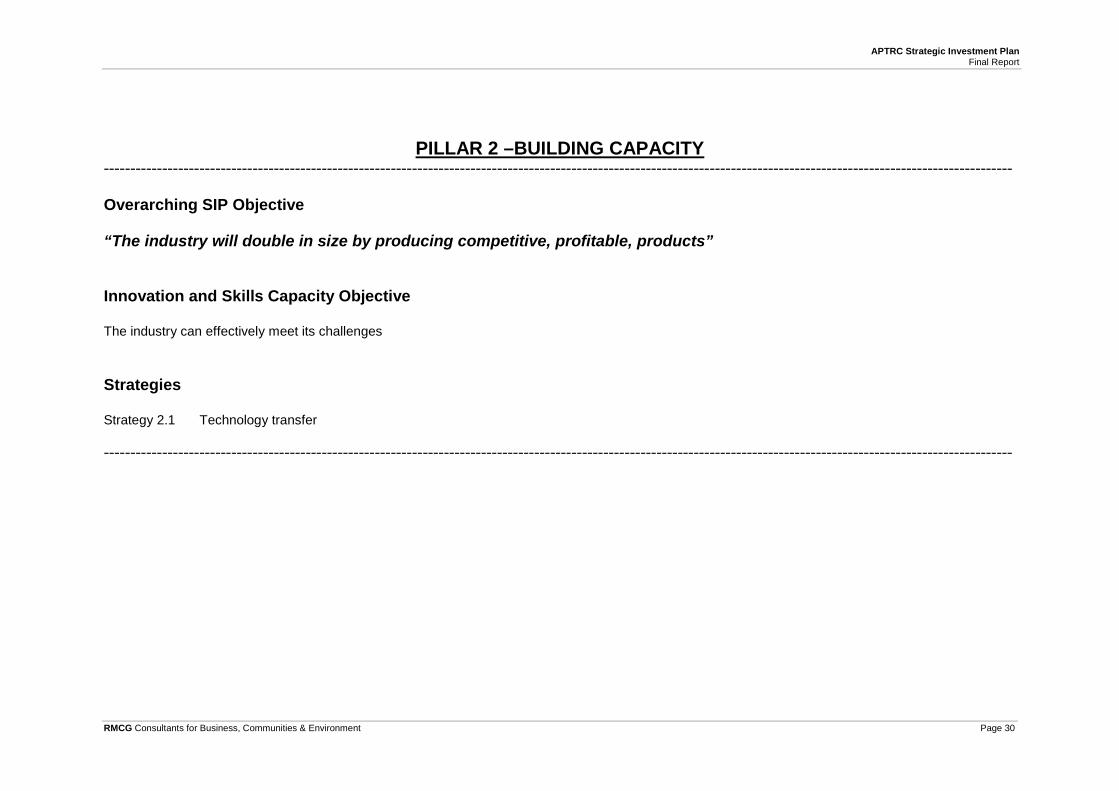

PILLAR 2 –BUILDING CAPACITY --------------------------------------------------------------------------------------------------------------------------------------------------------------------------- Overarching SIP Objective “The industry will double in size by producing competitive, profitable, products” Innovation and Skills Capacity Objective The industry can effectively meet its challenges Strategies Strategy 2.1 Technology transfer ---------------------------------------------------------------------------------------------------------------------------------------------------------------------------

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 31

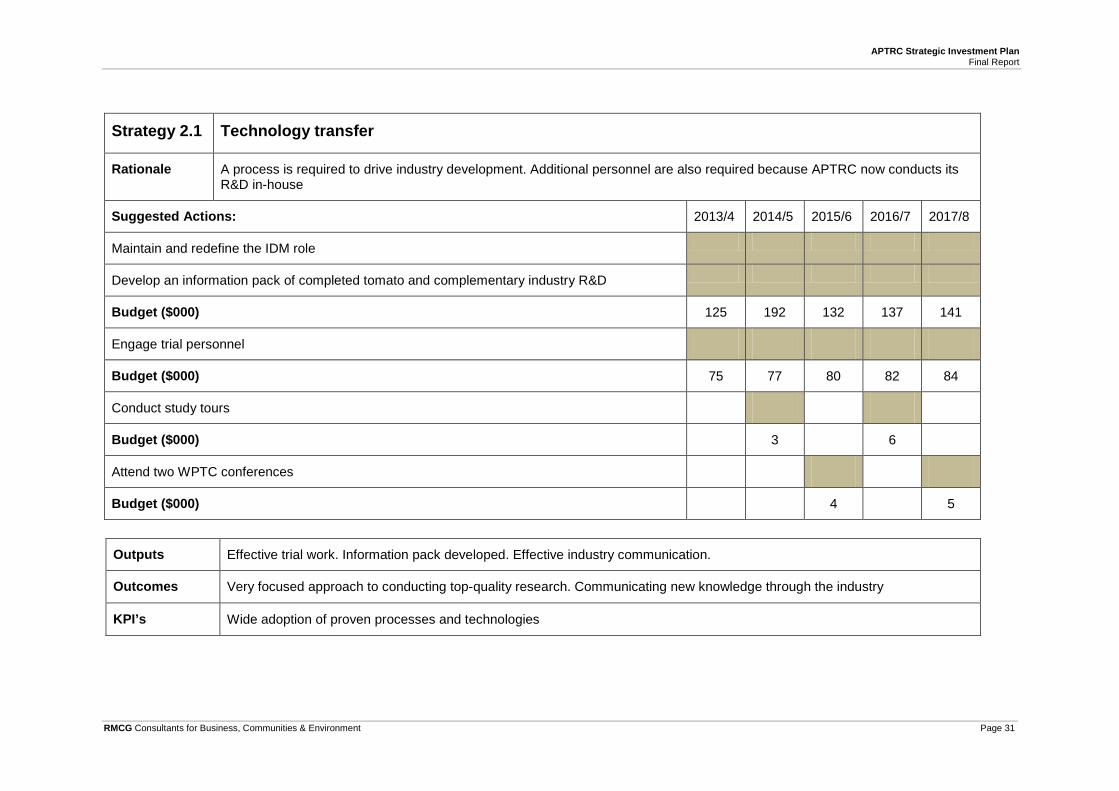

Strategy 2.1 Technology transfer

Rationale A process is required to drive industry development. Additional personnel are also required because APTRC now conducts its R&D in-house

Suggested Actions: 2013/4 2014/5 2015/6 2016/7 2017/8

Maintain and redefine the IDM role

Develop an information pack of completed tomato and complementary industry R&D

Budget ($000) 125 192 132 137 141

Engage trial personnel

Budget ($000) 75 77 80 82 84

Conduct study tours

Budget ($000) 3 6

Attend two WPTC conferences

Budget ($000) 4 5

Outputs Effective trial work. Information pack developed. Effective industry communication.

Outcomes Very focused approach to conducting top-quality research. Communicating new knowledge through the industry

KPI’s Wide adoption of proven processes and technologies

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 32

PILLAR 3 – INFLUENCE NATIONAL CONSUMPTION --------------------------------------------------------------------------------------------------------------------------------------------------------------------------- Overarching SIP Objective “The industry will double in size by producing competitive, profitable, products” Influence National Consumption Objective Enable the industry to conduct low-volume product trials, and influence consumer perception of the industry and its products Strategies Strategy 3.1 Construct a pilot plant Strategy 3.2 Conduct market research to inform new product development Strategy 3.3 Develop a social media platform ---------------------------------------------------------------------------------------------------------------------------------------------------------------------------

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 33

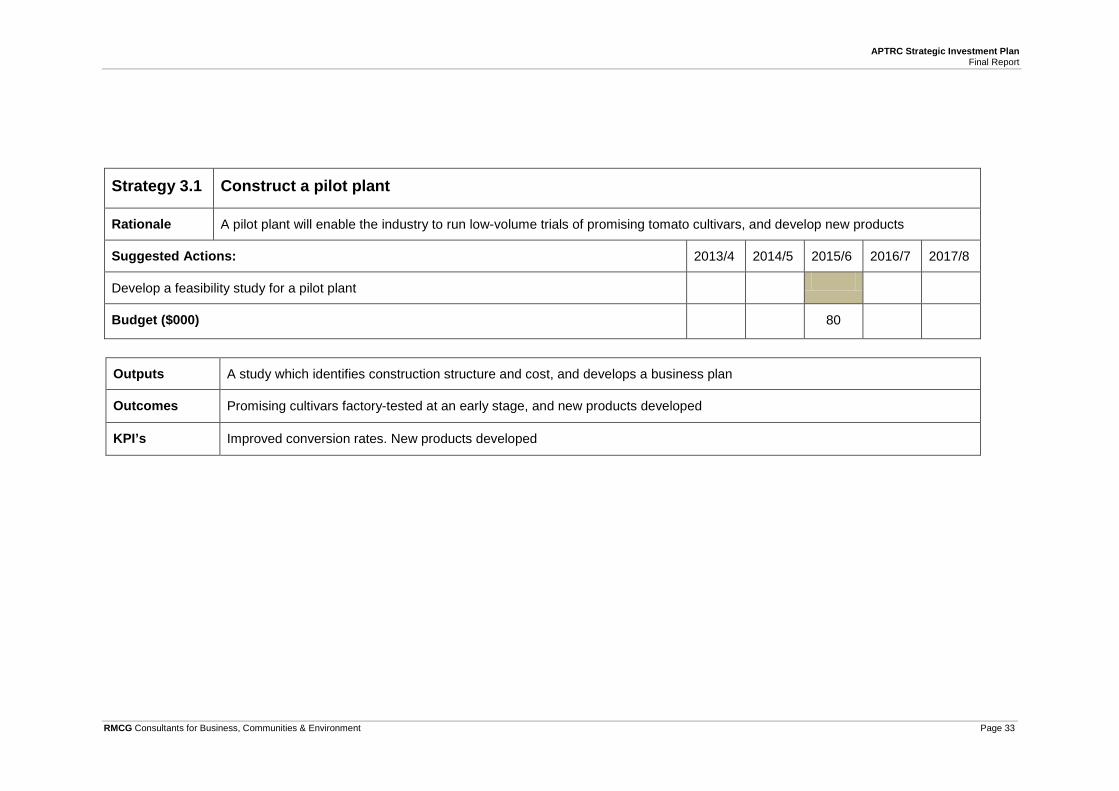

Strategy 3.1 Construct a pilot plant

Rationale A pilot plant will enable the industry to run low-volume trials of promising tomato cultivars, and develop new products

Suggested Actions: 2013/4 2014/5 2015/6 2016/7 2017/8

Develop a feasibility study for a pilot plant

Budget ($000) 80

Outputs A study which identifies construction structure and cost, and develops a business plan

Outcomes Promising cultivars factory-tested at an early stage, and new products developed

KPI’s Improved conversion rates. New products developed

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 34

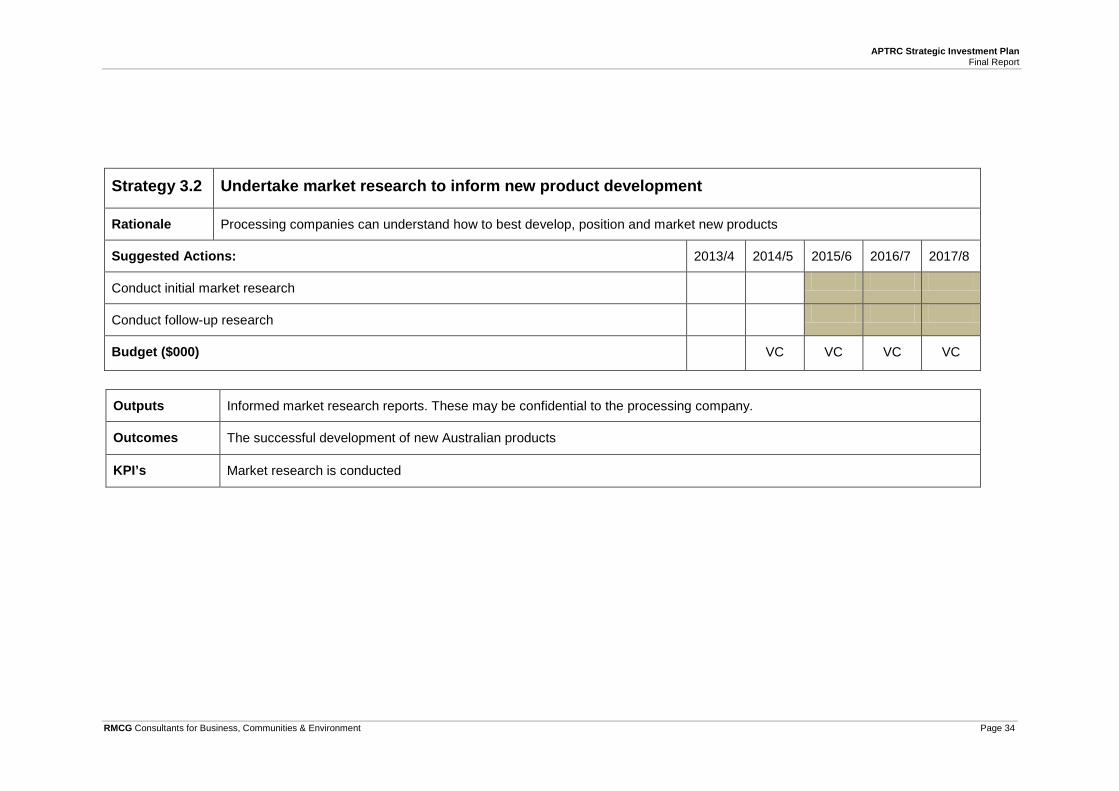

Strategy 3.2 Undertake market research to inform new product development

Rationale Processing companies can understand how to best develop, position and market new products

Suggested Actions: 2013/4 2014/5 2015/6 2016/7 2017/8

Conduct initial market research

Conduct follow-up research

Budget ($000) VC VC VC VC

Outputs Informed market research reports. These may be confidential to the processing company.

Outcomes The successful development of new Australian products

KPI’s Market research is conducted

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 35

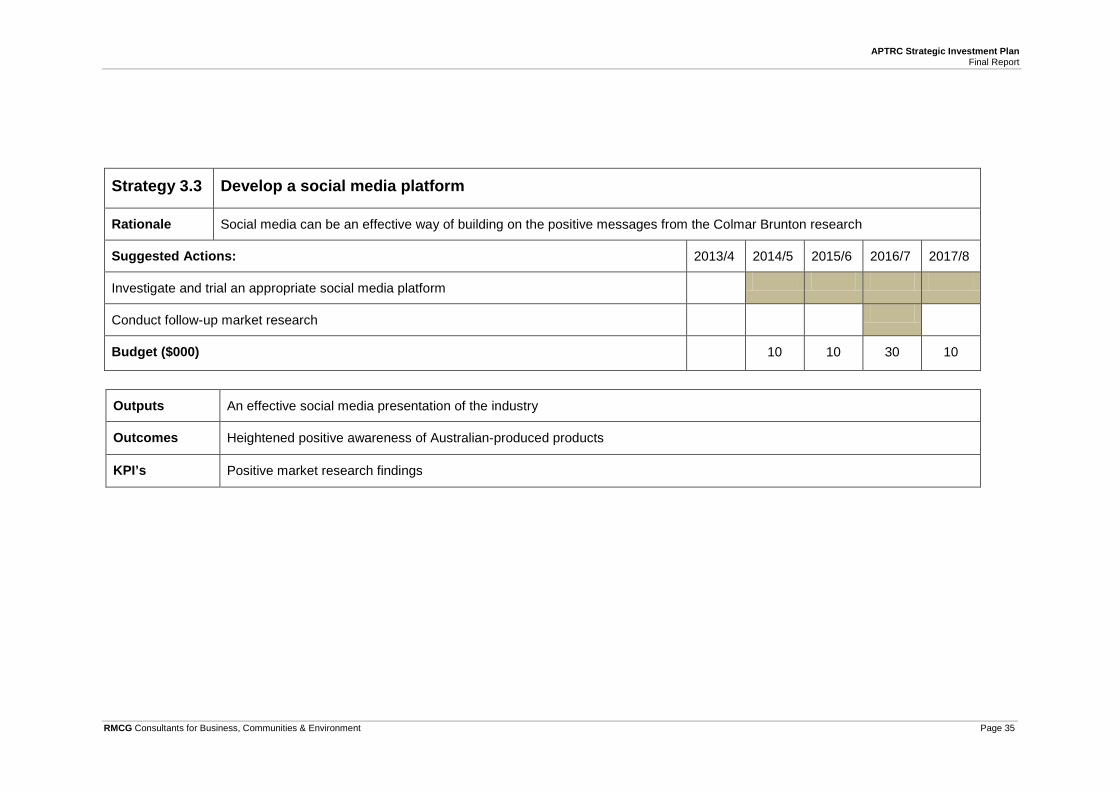

Strategy 3.3 Develop a social media platform

Rationale Social media can be an effective way of building on the positive messages from the Colmar Brunton research

Suggested Actions: 2013/4 2014/5 2015/6 2016/7 2017/8

Investigate and trial an appropriate social media platform

Conduct follow-up market research

Budget ($000) 10 10 30 10

Outputs An effective social media presentation of the industry

Outcomes Heightened positive awareness of Australian-produced products

KPI’s Positive market research findings

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 36

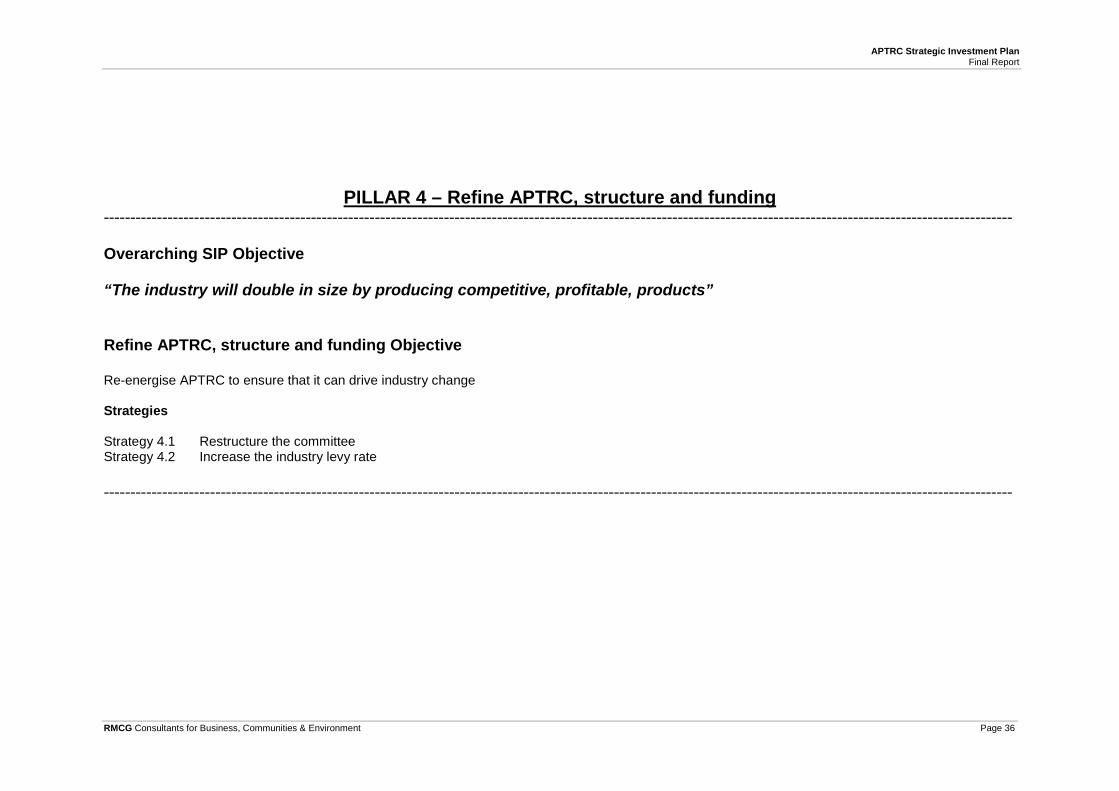

PILLAR 4 – Refine APTRC, structure and funding --------------------------------------------------------------------------------------------------------------------------------------------------------------------------- Overarching SIP Objective “The industry will double in size by producing competitive, profitable, products” Refine APTRC, structure and funding Objective Re-energise APTRC to ensure that it can drive industry change Strategies Strategy 4.1 Restructure the committee Strategy 4.2 Increase the industry levy rate ---------------------------------------------------------------------------------------------------------------------------------------------------------------------------

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 37

Strategy 4.1 Restructure the committee

Rationale The APTRC committee will be critical to ensuring that the industry meets its stated objectives

Suggested Actions: 2013/4 2014/5 2015/6 2016/7 2017/8

Restructure the APTRC committee:

• Have a team of knowledgeable and committed representatives

• Co-opt specialist skills: eg, marketing

• Appoint an independent Chair

• Allocate a committee member as a mentor to each major project

• Review APTRC’s effectiveness annually, in the industry magazine (Chair’s report)

Budget ($000) - Chair 4 4 4 5 5

Outputs The committee drives an effective program

Outcomes The industry is given the best chance to meet its objectives

KPI’s The Strategic Investment Plan is delivered

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 38

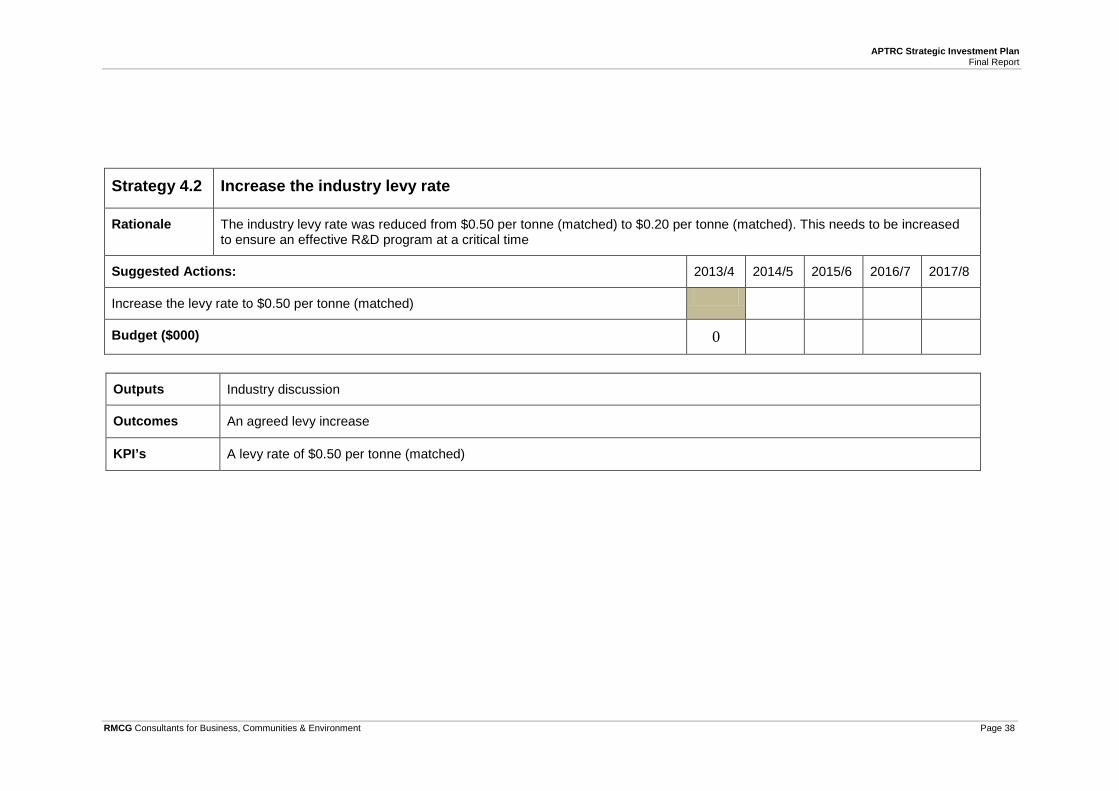

Strategy 4.2 Increase the industry levy rate

Rationale The industry levy rate was reduced from $0.50 per tonne (matched) to $0.20 per tonne (matched). This needs to be increased to ensure an effective R&D program at a critical time

Suggested Actions: 2013/4 2014/5 2015/6 2016/7 2017/8

Increase the levy rate to $0.50 per tonne (matched)

Budget ($000) 0

Outputs Industry discussion

Outcomes An agreed levy increase

KPI’s A levy rate of $0.50 per tonne (matched)

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 39

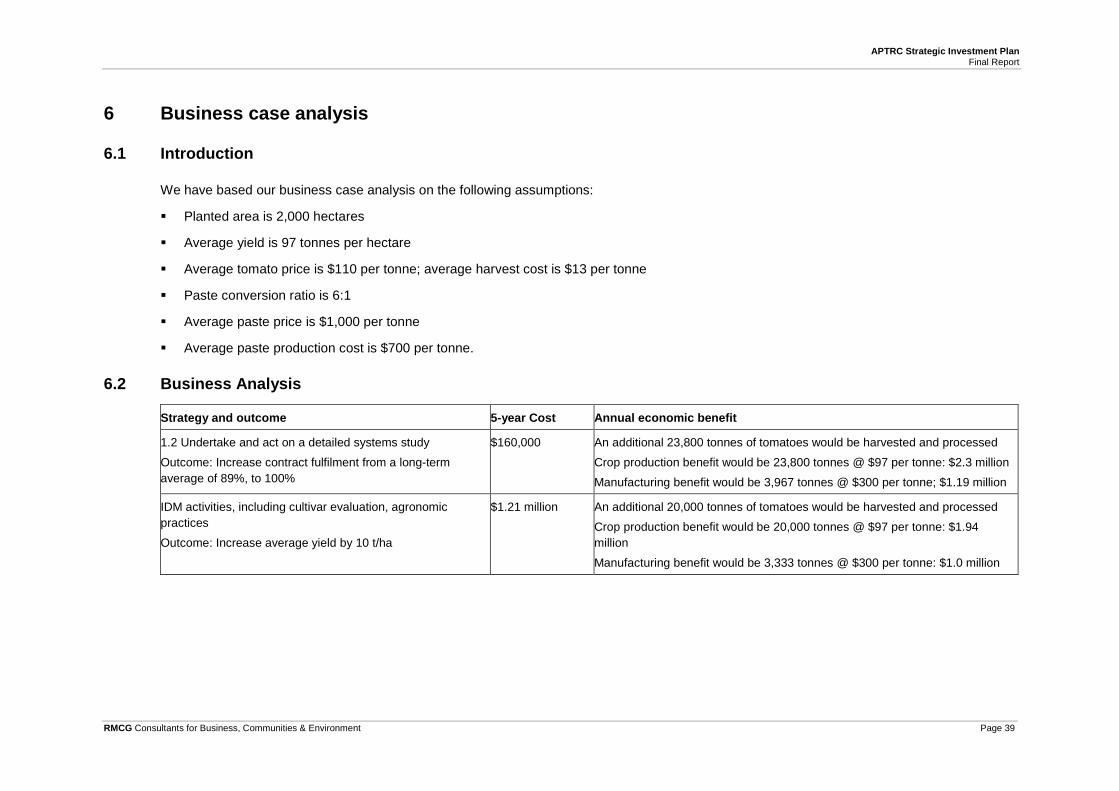

6 Business case analysis

6.1 Introduction

We have based our business case analysis on the following assumptions:

Planted area is 2,000 hectares

Average yield is 97 tonnes per hectare

Average tomato price is $110 per tonne; average harvest cost is $13 per tonne

Paste conversion ratio is 6:1

Average paste price is $1,000 per tonne

Average paste production cost is $700 per tonne.

6.2 Business Analysis

Strategy and outcome 5-year Cost Annual economic benefit

1.2 Undertake and act on a detailed systems study

Outcome: Increase contract fulfilment from a long-term average of 89%, to 100%

$160,000 An additional 23,800 tonnes of tomatoes would be harvested and processed

Crop production benefit would be 23,800 tonnes @ $97 per tonne: $2.3 million

Manufacturing benefit would be 3,967 tonnes @ $300 per tonne; $1.19 million

IDM activities, including cultivar evaluation, agronomic practices

Outcome: Increase average yield by 10 t/ha

$1.21 million An additional 20,000 tonnes of tomatoes would be harvested and processed

Crop production benefit would be 20,000 tonnes @ $97 per tonne: $1.94 million

Manufacturing benefit would be 3,333 tonnes @ $300 per tonne: $1.0 million

APTRC Strategic Investment Plan Final Report

RMCG Consultants for Business, Communities & Environment Page 40

7 Example of audit scope for crop production

variety selection soil preparation seed/ transplants planting & crop establishment weed control

pest & disease control

biosecurity irrigation management

nutrition management

soil management

between tomato crops

logistics and climate (early / late regions,

climatic risks)

soil type and condition, paddock uniformity, paddock

size, rotation

management capability

vigour, yield, disease resistance, ripening

time, fruit characteristics (solids post maturity keeping)

timing, equipment, pre-plant fertiliser, seedbed quality /

configuration

source, quality, health

planting density

timing, efficacy, resistance

management, products available,

biosecurity

timing, efficacy, resistance

management, products available,

biosecurity

pest risk analysis,

awarenes, preparedness

scheduling, monitoring, water

quality

timing, amounts, application technology, monitoring, fertilise type

rotation crops, green crops, sheep, tillage approach etc.

1 ResponsibilityWho is responsible? ID shared responsibilities and how they are split.

Kagome Growers, Kagome Kagome, growers Kagome Growers, Kagome Growers, Kagome Growers, Kagome Growers GrowersGrowers, Kagome Growers Growers Growers

2 Specification Requirements (what, how, when) based on current knowledge

Non saline soil, free draining, organic carbon >1.2%

Suitable equipment, irrigation set up,

knowledge & skills

What can go wrong?

Crop maturity pattern does not match processing capacity, a number of crops ready in the same harvest group at the same time

Site does not meet above specifications

People need to be aware of legal

responsibilities in regards to employing

people etc

variety does not match what processor

requires, variety may be poor yielding, or not hold in the paddock

seson too dry or too wet for ideal soil

preparation

Poor establishment, pest and disease

issues

too dry at establishment, poor

quaity transplants

timing of herbicide applications not

suitable, herbicides are not

effective on the spectrum of

weeds present

incorrect sprays, resistance, poor spray coverage, lack of chemcial control options

new pest or disease arrives

and crop damage occrs prior to

growers being aware of problem.

No method of control available for new pest or

disease.

will need to be used if Metham

Sodium is deregistered

Likelihood moderate moderate low low low low moderate high low high

Consequences (e.g. extent of crop or economic loss)

moderate to high high high low moderate moderate moderate high significant significant

5 Preventive action Currently available production spread across areas

Farm employee induction package

developed a number of years ago

currrent industry variety trials enable growers to

compare yield of different varieties

metham, titus, sencor

None

12 Capacity building / training

Who needs training in what to perform the activity or improve processes/outcomes? Capacity building goals?