TILITIES ÜSSELDORF Utilities Unbundled - Ernst & … Unbundled ISSUE ONE - NOVEMBER 2006 - ANALYSIS...

24

Utilities Unbundled ISSUE ONE - NOVEMBER 2006 - ANALYSIS AND COMMENT ON CURRENT ISSUES IN UTILITIES Managing for growth in an uncertain world !@# Contents Introduction Going for growth Financing global power generation Where are the investors heading? Consolidation good? Recent transactions have revived a flagging M&A market, but will the trend continue? Open sesame? Competing investors in infrastructure are vying to unlock huge potential returns Regional report India surges ahead How the world’s fifth-largest consumer of commercial energy is clearing a path for growth Fuelling growth Green goes Gucci Alternative energy is joining the mainstream Coal cleans up How new technologies will put coal centre stage Back from the cold Nuclear power - set for a comeback? Water and Waste Liquid assets Infrastructure investment and service efficiency are key challenges for water utilities Recycling and renewal Environmental concerns are shaping the waste management industry Regulation and reporting update Deregulation: Adapt and survive Unbundling: What’s best for business? MiFID: New rules, new game? IFRS: Wearing your strategy on your sleeve G LOBAL U TILITIES C ENTER D ÜSSELDORF - G ERMANY

Transcript of TILITIES ÜSSELDORF Utilities Unbundled - Ernst & … Unbundled ISSUE ONE - NOVEMBER 2006 - ANALYSIS...

Utilities UnbundledISSUE ONE - NOVEMBER 2006 - ANALYSIS AND COMMENT ON CURRENT ISSUES IN UTILITIES

Managing for growthin an uncertainworld

!@#

ContentsIntroduction

Going for growthFinancing global power generationWhere are the investors heading?Consolidation good?Recent transactions have revived a flagging M&Amarket, but will the trend continue?Open sesame?Competing investors in infrastructure are vyingto unlock huge potential returns

Regional reportIndia surges aheadHow the world’s fifth-largest consumer of commercial energy is clearing a path for growth

Fuelling growthGreen goes GucciAlternative energy is joining the mainstreamCoal cleans upHow new technologies will put coal centre stage Back from the coldNuclear power - set for a comeback?

Water and WasteLiquid assetsInfrastructure investment and service efficiencyare key challenges for water utilities Recycling and renewalEnvironmental concerns are shaping the waste management industry

Regulation and reporting updateDeregulation: Adapt and surviveUnbundling: What’s best for business?MiFID: New rules, new game?IFRS: Wearing your strategy on your sleeve

GL O BA L UT I L I T I E S CE N T E R

DÜ S S E L D O R F - GE R M A N Y

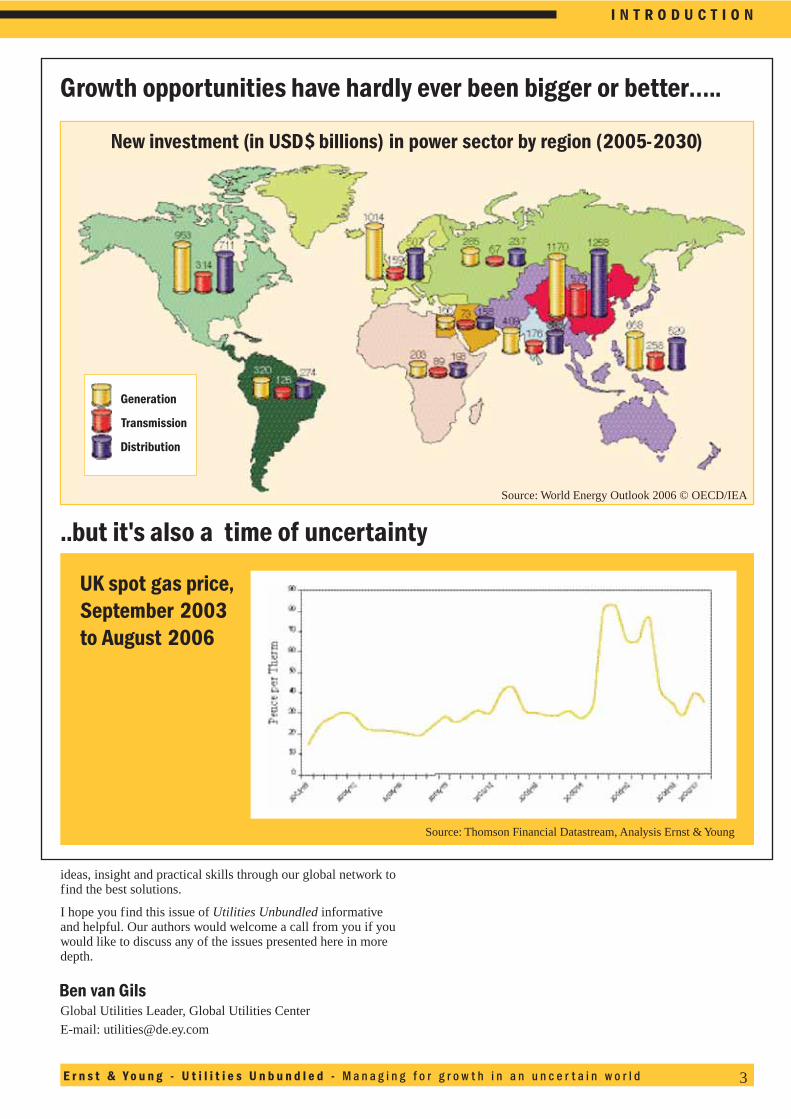

Welcome to the first issue of UtilitiesUnbundled, a round-up of analysis andcomment on current issues in utilities.Statistics just released by the International Energy Agencyprove that, for the utilities industry today, growth opportunitieshave hardly ever been bigger or better. World demand forenergy is soaring at an unprecedented rate. And increasingenergy demands call for huge investments in infrastructure andinnovation to meet the world’s needs. That’s good news.

But – and there’s always a ‘but’ – it is also a time ofunprecedented uncertainty. We have seen wide fluctuations inprices for primary resources like gas. A recent hike in uraniumprices threatened to hit the cost of power in Germany, and onecan’t imagine it will stop there. Deregulation of the market isprobably going to be enforced around Europe, but at themoment nobody can say when - or quite how - it will bite.Meanwhile, the new IFRS regulations are putting pressure oncompanies to make their strategy visible. There is uncertainty,too, around environmental regulations: who knows, forexample, what is going to happen to carbon trading after 2012?

In putting together this issue of Utilities Unbundled, we haveexplored both the growth opportunities and the uncertaintiesthat surround us. We discuss investment opportunities andcurrent consolidation trends. Our article on the burgeoningIndian energy sector explores the country’s decentralizedgeneration plans and its use of wind and renewables. Weinvestigate the rise of alternative energy, clean coal and newnuclear capacity, particularly as they reflect on security ofsupply. We look at the challenges facing the water and wastemanagement industries, and present an in-depth look at newdevelopments in regulation which will fundamentally changethe way energy utilities are structured and governed.

The common theme that emerges is the importance oforganizational agility. Businesses with a flexible approach havean enormous advantage in times like these. To generate growthin an environment as uncertain as the one we face, managersneed to be able to anticipate trends, adapt their business modelsand, above all, act fast to seize new opportunities. Our globalutilities practice works with clients all round the world to makesure they have the agility to face these challenges - sharing

2 E r n s t & Y o u n g - U t i l i t i e s U n b u n d l e d - M a n a g i n g f o r g r o w t h i n a n u n c e r t a i n w o r l d

Managing forgrowth in anuncertainworld

I N T R O D U C T I O N

Ben van Gils

Global Utilities Leader

Ernst & Young Global Utilities Center

Graf-Adolf-Platz 15

40213 Düsseldorf

Direct tel: +49 (211) 9352 21557

ideas, insight and practical skills through our global network tofind the best solutions.

I hope you find this issue of Utilities Unbundled informativeand helpful. Our authors would welcome a call from you if youwould like to discuss any of the issues presented here in moredepth.

Ben van GilsGlobal Utilities Leader, Global Utilities Center

E-mail: [email protected]

E r n s t & Y o u n g - U t i l i t i e s U n b u n d l e d - M a n a g i n g f o r g r o w t h i n a n u n c e r t a i n w o r l d 3

I N T R O D U C T I O N

Growth opportunities have hardly ever been bigger or better…..

..but it's also a time of uncertainty

UK spot gas price,September 2003 to August 2006

New investment (in USD$ billions) in power sector by region (2005-2030)

Source: Thomson Financial Datastream, Analysis Ernst & Young

Source: World Energy Outlook 2006 © OECD/IEA

Generation

Transmission

Distribution

As global demand forpower increases,investment opportunitiesare on the rise. Jon Hughes reports onwhere the money isheaded in this dynamicsector

Huge demand for investmentDemand for electricity is accelerating and islikely to grow fastest in developing nations,particularly China and India with their rapidly-growing populations and economies. Thisopens up enormous opportunities for investment in overseas electricity assets:money is needed both for generation itself,and for the underlying infrastructure of wiresand networks.

Funding is abundant, from traditionaland non-traditional sourcesThe financing of power projects around theworld has changed greatly in recent years.The balance has shifted towards privatesources of investment, with the role of publicly-financed institutions in financingelectrical projects diminishing. Investors arekeen to capitalize on the potentially highreturns on offer, and the chance to realizegreater growth than is available by staying athome. New entrants in overseas electricpower investment include private equityhouses, major construction and power equipment manufacturing companies and arange of utility companies.

Key investment areas Power generation growth is expected to beparticularly strong in the growing economiesof China and India, where the substantiallevel of new build has attracted hordes ofpotential investors. In terms of additionaland replacement capacity we expect to seeChina adding approximately 100GW thisyear, whilst India will add around 40GW.However, a good number of the independentpower producers who went into India recently on investment deals have beenpulling out, because the opportunities tomake money have been compromised by

price cap interference by state governments.Better models are developing to attract capital where new projects are needed, buttime will tell whether this region can becomemore commercial.

The US and Europe are other areas planningsignificant growth, and both will add around20GW this year.

Increasing pressure in AfricaThe big unknown is Africa, which currentlyhas the lowest rate of public access to electrification in the world: just 20% of thetotal African population is connected to electricity. A substantial investment is neededin networks and in generation capacity toimprove these rates. Many European andinternational electricity companies arealready active in Africa - including AES,Globelec, EDF and Tractebel – and they willundoubtedly become more active as localregulatory environments evolve to suit them.

Constraints on spending: political certainty and greenhouse gasesOne of the big issues for global investors inpower is certainty, both from a political andmarket standpoint. The payback period ongeneration investments is commonly 10-20years, during which time all kinds of instabilities can have an influence on projects before even one kilowatt of electricityhas been generated. In pursuit of the bestreturns, investors will continue to look togovernments around the world for stablepolitical policy, consistent regulatory andplanning regimes, and a forward-thinkingapproach to grants for new technologies.

The other key concern is action on greenhousegas emissions. Whether or not they are government owned, power generation businesses are commercial concerns andhave to take commercial decisions. It will beinteresting to see if the emissions tradingschemes and the ‘cost of carbon’ attached togeneration begin to influence changes ininvestment decisions in the future, towardsmore carbon efficient generation technology.

Need to strike a balance of technologiesFor the world’s governments, who are understandably sensitive about keeping thelights on, it is paramount to create an environment where investment can continue

to give consumers security of supply - andprovide shareholders with secure returns. InEurope and the US there is continuing consciousness of the need for generationcapacity that is independent of, say, Russia’sgas or the Middle East’s LNG, which is creating substantial investment opportunitiesin clean coal and nuclear. Almost all the newgeneration capacity being built in India andChina over the next 5-10 years will be coal.And although some countries have formallysaid ‘no’ to nuclear, in truth its popularitytends to change with governments. The concerns over CO2 emissions mean thatnuclear will always have a place in the powergeneration mix. The world’s handful of uranium producers are themselves attractinga great deal of investment.

We can also expect to see something of asurge in renewables, particularly hydro andwind. Government policy over renewablestargets sets a massive challenge for supplierslike Siemens, GE and Westinghouse to manufacture and supply - which makes for adynamic sector.

To achieve the best investment solution, theworld’s power generation investors face acomplex set of decisions on how to shareand manage the risks associated with thesetechnologies and markets.

4 E r n s t & Y o u n g - U t i l i t i e s U n b u n d l e d - M a n a g i n g f o r g r o w t h i n a n u n c e r t a i n w o r l d

Financingglobalpower

G O I N G F O R G R O W T H

Jon HughesHead of Utilities – UK & NEMIA UK Head of Corporate FinanceTransaction Advisory ServicesDirect tel: +44 121 535 2750 E-mail: [email protected]

Jon’s experience includes working with thegovernment, the regulator and some of Ernst &Young’s major energy/energy-related clients. Priorto joining Ernst & Young 7 years ago, he wasseconded as general manager of a power stationfor 14 months.

Latest IEA World Energy Outlook New figures just published by the International Energy Agency1 reveal that: ■ World electricity demand is projected to double by 2030, at an average of 2.6% per year

■ Total power sector investment over 2005-2030 (including generation, transmission and distribution) exceeds USD$11 trillion, of which USD$5.2 trillion relates to generation

■ The largest investment requirements – some USD$3 trillion – arise in China

■ Investment needs are also very large in OECD North America and Europe, totalling almost USD$3.7 trillion

1 World Energy Outlook 2006 © OECD/IEA

E r n s t & Y o u n g - U t i l i t i e s U n b u n d l e d - M a n a g i n g f o r g r o w t h i n a n u n c e r t a i n w o r l d 5

G O I N G F O R G R O W T H

Consolidation good? Debate.Recent transactions have revived a flagging M&A market. Will the consolidationtrend continue? - Interview with Joseph Fontana and Ed Kleinguetl

Q: What do you think is driving M&A in Utilitiestoday?

A: It’s growth, as always. For most of thedeveloped world this is a very mature sector,with organic growth generally in the 2-3%range. Growth through acquisition presentsan attractive way to spike returns for years tocome, and benefit from economies of scale

and diversification into new markets. Ofcourse the marketplace is not just seeingutilities buying other utilities. Non-traditionalplayers like investment banks and privateequity funds are active in this space, takingadvantage of deregulation around the world.A good recent example is Macquarie’sacquisition of Thames Water1 in the UK andDuquesne Energy in the US. These non- traditional buyers add welcome liquidity tothe market place. This is good news for thesmall utilities out there who are strugglingfor capital investment or the large utility thatis interested in selling non-core assets: andmore buyers means that more sellers get theprice they want.

Q: And what do you see as the main inhibitor?

A: The key one is still probably regulation.Deals must not only make economic sense,but they also need to satisfy the local regulators. Regulators basically tend to thinkand act locally, and because their paramountconcern is consumer protection, they willnot approve a merger unless consumersreceive an adequate share of the merger benefits. This can set the regulators’ objective of consumer protection (generallythrough lower rates) against the utility companies’ objectives of maximizing stockholder return. A number of US transactions over the last several years havebeen scuttled because the regulator could notbe convinced that the transaction was in theconsumers’ best interest. The failed Exelon/

PSEG transaction, which would have createdthe largest utility in the US, and the FPL/Constellation transaction are just the latestexamples.

Of course, the regulatory market in the US isvery different from regulation in Australia,or the UK, or across Asia. In India andChina, for example, where they have atremendous need for new generation, companies have been tempted to invest.There have been attempts to deregulate themarket, but the State governments haveinterfered by capping prices, making ituneconomic to operate there – leavinginvestors less prepared to take the risk. The sheer complexity of the regulatory environment is probably going to continue asthe main barrier to consolidation, and this istrue whether the target is the neighboringutility or the utility in a neighboring country.

Going forward, the successful industry consolidators will think strategically aboutregulation and consider regulatory approvalin the same light as they think about convincing the capital markets of their transactions benefits. A good example ofthis is the Duke/Cinergy merger earlier thisyear: Duke managed to convince regulatorsin three different states of the benefits of thecombined operation, but they had to makeconcessions – like maintaining HQs in twostates and guaranteeing the benefits of synergy savings to its customers over a tenyear period. Continued overleaf

1 Macquarie bought Thames for USD$15 billion on 16 October 2006

Target Acquiror Acquiror countryKeySpan Corp National Grid Transco PLC UKDuquesne Light Holdings Investor Group AustraliaNorthWestern Corp Babcock & Brown Infrastructure AustraliaColeto Creek Power Plant International Power PLC UKNew England Gas-Rhode Island National Grid USA UKEnron Corp.'s Prisma Energy, Inc. subsidiary Ashmore Energy International Ltd. UKCinergy Marketing & Trading and Cinergy Canada Fortis NetherlandsPrimary Energy Holdings LLC EPCOR Power LP CanadaRumford-Hydroelectric Facility Brookfield Power Inc CanadaFrederickson Power LP EPCOR Power LP CanadaStakes in COB Energy Facility LLC and Elwood J-POWER USA Development Co. Ltd. Japan (US sub)Energy LLCGreenlight Energy, Inc. BP PLC UKCalpine Corporation's Dighton Power Plant BG North America, a wholly owned UK

subsidiary of BG Group plc Trans-Elect NTD Path 15 LLC Atlantic Power Holdings, LLC CanadaStakes in two wind farms Babcock & Brown Wind Partners AustraliaMREC Partners LLC and Iberdrola SA SpainMidwest Renewable Energy Projects LLC

Community Energy, Inc. Iberdrola SA Spain

Redefining the landscape: selected US utilities deals announced 2006

Joseph FontanaGlobal Utilities & Power Industry LeaderTransaction Advisory Services, USDirect tel: +1 212 7733382E-mail: [email protected]

Joseph has over 20 years’ corporate finance andtransaction experience, and 15 years’ experiencewith power generation and utilities He has lednumerous transactions for strategic buyers andprivate equity investors in this industry, includingelectric and gas utilities, independent powerproducers, electric and gas marketing company’s,gas pipelines, LNG plant construction projects, gasstorage and T&D outsourcing.

Source: Factiva

In 2006 a total of 96 deals were announced in the US alone, resurrecting a previously flat M&A market in utilities. The sample above demonstrates the international nature ofmany of these deals. In creating super-regional companies with broader portfolios, these transactions indicate the nature of future strategic moves.

Q: What is your prediction for the shape of theindustry in ten years’ time?

A: Generally speaking, the utility game is alocal game - local businesses, driven by localneeds, regulated by a local regulator. For distribution, this will always be true. Forgeneration, and possibly also transmission,businesses will go wherever they see ademand. I think what we are most likely tosee is regional consolidation in these areas,across North America and within theEuropean market. The US and Europeans

will be involved in Asia, probably on thebasis of contracts with government.

Putting the emerging markets aside, I thinkwe only really need a small number of utilitycompanies. In the US, I would ultimatelyexpect to see 20-30 utilities - as opposed tothe 90 or so we currently have. In Europe itwill make sense to have fewer utilities too –and the E.ON/Endesa deal indicates the waythings might progress. In Europe, whereunbundling is being forced by the regulator,businesses are being forced to split up.

As E.ON is squeezed by the German regulator to unbundle, it will have to look toacquisitions abroad (for example Endesa) ifit is to achieve substantial growth. Then, justlike the Gaz de France/Suez deal, they willhave to divest certain assets if they combine,and buyers like Centrica will come in andsnap up those assets. This echo effect is veryhealthy for the sector.

6 E r n s t & Y o u n g - U t i l i t i e s U n b u n d l e d - M a n a g i n g f o r g r o w t h i n a n u n c e r t a i n w o r l d

G O I N G F O R G R O W T H

Edward KleinguetlTransaction Integration, USDirect tel: +1 713 750 8242E-mail: [email protected]

Ed has over 20 years’ experience in accounting,finance, M&A, integration, sales and marketing andexecutive development. He has advised ontransactions - including carve-outs andintegrations - in construction, engineering,industrial services, environmental, pulp and paper,telecommunications, retail and commercialbanking, and other services industries.

As global trends see ownership andprovision of infrastructure servicesmove from government to the privatesector, competing investors areseeking to unlock huge potentialreturns from utilities - Ben van Gilsreports

The sheer scale of infrastructure investment needed for utilities presents enormous opportunities for investors around the world. Theyhave recognized the potential of infrastructure as an emerging assetclass that not only offers regulated, long-term investment returns, butalso gives them the opportunity to diversify their portfolio, leading tobetter risk management.

Who is investing?

Many of the major global utilities are themselves key players in thismarket - especially the European companies. In many cases, investment in other utilities provides the only route to growth in

restricted local markets. Utility company shareholders, for their part,are supportive of consolidation and see it as wholly positive.

Infrastructure funds run by large banks are scooping up big chunksof the infrastructure value chain. For them, infrastructure funds arehighly attractive because they generate stable, long-term revenues toboost their pension funds. Because they can do this at a low capitalcost, the banks are able to be quite aggressive in the market - in away that perhaps the utilities companies themselves cannot. Thepotential size of their funds is huge – for example, Macquarie currently manages approximately USD$26 billion in infrastructureequity, invested in around 100 assets across 25 countries1.

Thirdly, there are the Private Equity houses, representing a portfolioof different risk takers. Their participation in the market is just askeen, but they may not have a completely free rein if many nationalgovernments follow the example of the Dutch government, which isconsidering the introduction of legislation which would prevent PEhouses from investing freely.

What are they investing in?

Infrastructure funds are focusing largely on existing assets withingeneration companies - but money is also available for other sectorsincluding water, rail, telecommunications, airports and other regulat-ed assets. At the moment, it is questionable whether pure funds will

Typical synergies that drive a utilitiestransaction■ Leveraging the competency of one utility across the other (eg, trading, power generation,

distribution)

■ Leveraging operational best practices (eg fossil fuel, nuclear, maintenance, environmental, health and safety)

■ Enhancing reliability, availability, and performance

■ Enhancing procurement leverage (eg fuel, maintenance, outage services)

■ Reducing general and administrative costs by leveraging leading practices (information technology / systems, call centers, customer service, insurance / risk management, human resources, accounting and finance) to greater advantage and over greater scale

■ Establishing an enterprise-level shared services organization

■ Enhanced competitiveness for deregulated businesses or businesses soon to be regulated

Open sesame?Coal has a number of ad

1 Source: Macquarie website

G O I N G F O R G R O W T H

be willing to invest in new, rather than existing, infrastructure -unless forced to do so by a regulator.

Although investment has been underway for some years, to dateinvestors have not had much opportunity to buy, because legislationhas prevented private infrastructure ownership in many countries.This is all due to change within the coming months (see sidebar fornews of change in The Netherlands). Another factor is a utility’s willingness to restructure in order to allow a transaction of this kindto go through: infrastructure assets provide utility companies withvital financial security that supports their commercial activities, andthey may not willingly let them go.

However, we are further down the line in terms of transfer of ownership than many people realize. It has been estimated that, ineffect, some 90% of the transportation and distribution infrastructureof power utilities in continental Europe has been transferred toAmerican investment groups and pension funds over the last 20years, in the form of cross-border leases. In this scheme, utility companies have transferred ownership of the infrastructure to theAmerican interest and immediately leased the property back for 25-30 years. Tens of billions of dollars are involved in these structures. This complicates life for today’s prospective investors,because they are confronted with infrastructure that is not free in themarket – what is available to buy is not a network, but a lease contract on a network.

Regulatory influences

Depending on the course they choose, regulators may act either as aspur or a brake on investment. Deregulation and enforced unbundlingof the market provide the opportunity for funds to flow in; but regulator action may also inhibit investment if the ceiling is set toolow on how much profit can be reserved for shareholders, therebywrecking a deal’s commercial benefits.

Regulators therefore need to show some sensitivity in setting up theright economic incentives: they may have to lift cost reduction pressure on the various operators, to take into account the longer-term interests of the industry and customers. At the same time, it isparamount that utility assets continue to function well, for the sake ofall consumers and users of the services they provide. So when infrastructure does fall into private hands, it’s the regulator’s duty toensure that shareholders (of both buyer and seller) do not gain unduly at the expense of the consumer. Politicians, for their part,need to invest their political capital to make constructive legislationmove forward.

Who really benefits?

In theory, investment deals should translate into price benefits forconsumers: regulators can demand that they get a ‘slice of the cake’in terms of lower-cost energy and other services. Investors shouldalso (in theory, again) be happy to spend money improving the facili-ties of the utilities they buy, because they will be interested in theirnewly-acquired asset functioning well in the long term. The deals arealso likely to prove healthy for the wider economy. Shareholders inutilities are often public bodies, including local governments, whocan use the extra dividends resulting from new investment money tofund public building programs and other projects of benefit to localcommunities.

The prognosis

The utility industry will be going through a turmoil of change overthe next 5-10 years whilst this phenomenon works through: no-onecan say for sure what the resulting ownership structures will look like.

As further deregulation and unbundling of the energy industry bringsmore infrastructure assets to market, it seems likely that it will be the‘utility-to-utility’ deals that prove the most successful, and that thesedeals will largely be regional in nature. The E.ON/ Endesa and Gazde France/Suez deals both give an indication of where we are heading in the long term. In both cases, we see national governmentstrying to maintain an influence, whilst the EU tries to make sure thatthe open market philosophy prevails. Each deal that is done will takeus a step closer to that vision.

E r n s t & Y o u n g - U t i l i t i e s U n b u n d l e d - M a n a g i n g f o r g r o w t h i n a n u n c e r t a i n w o r l d 7

Ben van GilsGlobal Utilities Leader Global Utilities Center, GermanyDirect tel: +49 211 9352 21557E-mail: [email protected]

Ben works with utility and energy companies all over the world. He advises theEuropean and Dutch parliaments on energy matters; writes on energy for theFinancial Times and the Wall Street Journal; and has appeared regularly on CNN,the BBC and Dutch TV.

New Netherlandslegislation could setunbundling precedentEU Directives require all Member States to design legislation

for unbundling energy utilities – effectively splitting

transportation from commercial activities. The issue is

under consideration in The Netherlands parliament as we

write, and it looks like the Dutch will be taking the concept

of unbundling much further than the original Directive

envisaged. The Dutch government’s lower chamber has

already passed a bill stipulating that the industry should be

unbundled to the strictest extent possible: absolutely no

organization will be allowed to combine infrastructure

ownership with any commercial activities. If the Dutch upper

chamber passes this legislation, other governments could

see this as a precedent. Many commentators feel this

approach is over-zealous, over complicated, and will not

provide the healthiest operational environment.

Largely state owned

With a population of 1 billion people, Indiahas three times the population of the US injust one-third of the area.

The utility sector in India is still largely state owned; NTPC Ltd. is the country’slargest power generator. While policies are set at a national level, each of India’s states can set its own pace within these central guidelines.

Huge coal reserves

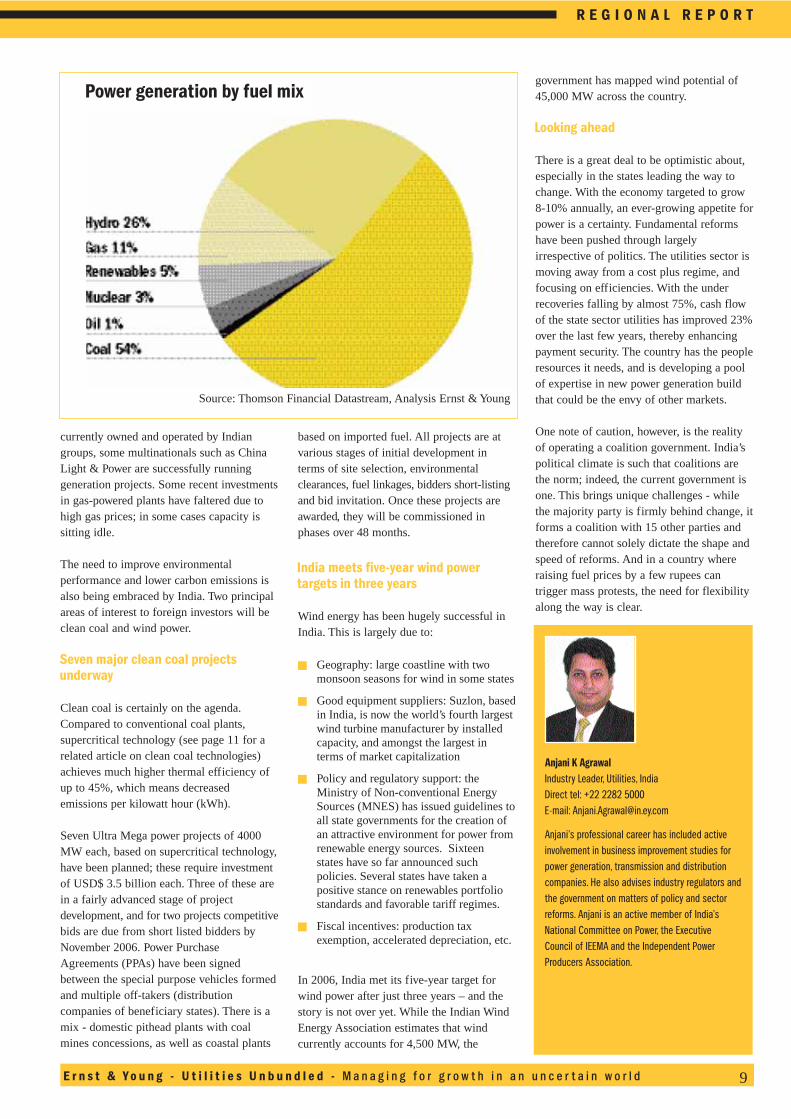

With the third largest coal reserves in theworld (after China and the US), India relieson coal for over half of its generation mix:(see chart opposite).

The path to reform

India has set a goal of ‘Power for all’ by2012. To do this, it must improve the quality

and reliability of supply, access many remoterural areas, and address some sensitive political issues such as pricing and collectingrevenues.

At present, many utilities run at a lossbecause the average revenue realized (ARR)still falls short of average cost of supply, inspite of an 85% rise in ARR over the lasteight years. Many governments have beenelected on the promise of cheap (even free)power to agriculture. The cross subsidiesbetween industrial users (who pay cost plus)and domestic and agricultural users (who pay cost minus) continue, albeit at diminishing levels. These subsidies varybetween states, with a ratio of 1:10 betweenthe lowest and the highest paying consumers,not uncommon. Despite this practice beinga political lynchpin for the last 50 years,consensus has emerged that such tariffdesign is no longer sustainable. The government and regulators are committed toremoving subsidies fully within five years,and also requiring states to budget for andfund subsidies upfront.

Reforms are now being implemented inearnest. India has moved from a single-buyermarket to a multi-buyer, multi-seller system.States are unbundling their utilities into threeseparate entities: generation, transmission,and distribution (this includes supply to consumers). At present, apart from industrialconsumers, most customers have no choiceover their power supplier. Moving forwardthe principle is give everybody choice, but ina phased manner.

Opportunities for foreign investment

In the next five years, it is estimated thatinvestments of USD$200 billion will beneeded in the sector, and foreign investorswill find opportunities in generation moreattractive than in transmission and distribution. Given the intimate relationshipsbetween politics and the energy sector, jointventures look to be the most effective routeinto India. While most of the business is

8 E r n s t & Y o u n g - U t i l i t i e s U n b u n d l e d - M a n a g i n g f o r g r o w t h i n a n u n c e r t a i n w o r l d

India surges ahead despite challengesAs the world’s fifth largest consumer of commercial energy, India currently suffers from energy and peak shortages. Anjani Agrawal reports on how the government is removing obstacles to growth in the utilities sector, as severalstates lead the path to reform.

R E G I O N A L R E P O R T

India’s states can each set their ownpace of regulation

currently owned and operated by Indiangroups, some multinationals such as ChinaLight & Power are successfully running generation projects. Some recent investmentsin gas-powered plants have faltered due tohigh gas prices; in some cases capacity is sitting idle.

The need to improve environmental performance and lower carbon emissions isalso being embraced by India. Two principalareas of interest to foreign investors will beclean coal and wind power.

Seven major clean coal projects underway

Clean coal is certainly on the agenda.Compared to conventional coal plants, supercritical technology (see page 11 for arelated article on clean coal technologies)achieves much higher thermal efficiency ofup to 45%, which means decreased emissions per kilowatt hour (kWh).

Seven Ultra Mega power projects of 4000MW each, based on supercritical technology,have been planned; these require investmentof USD$ 3.5 billion each. Three of these arein a fairly advanced stage of project development, and for two projects competitivebids are due from short listed bidders byNovember 2006. Power PurchaseAgreements (PPAs) have been signedbetween the special purpose vehicles formedand multiple off-takers (distribution companies of beneficiary states). There is amix - domestic pithead plants with coalmines concessions, as well as coastal plants

based on imported fuel. All projects are atvarious stages of initial development interms of site selection, environmental clearances, fuel linkages, bidders short-listingand bid invitation. Once these projects areawarded, they will be commissioned in phases over 48 months.

India meets five-year wind power targets in three years

Wind energy has been hugely successful inIndia. This is largely due to:

■ Geography: large coastline with two monsoon seasons for wind in some states

■ Good equipment suppliers: Suzlon, basedin India, is now the world’s fourth largest wind turbine manufacturer by installed capacity, and amongst the largest in terms of market capitalization

■ Policy and regulatory support: the Ministry of Non-conventional Energy Sources (MNES) has issued guidelines toall state governments for the creation of an attractive environment for power from renewable energy sources. Sixteen states have so far announced such policies. Several states have taken a positive stance on renewables portfolio standards and favorable tariff regimes.

■ Fiscal incentives: production tax exemption, accelerated depreciation, etc.

In 2006, India met its five-year target forwind power after just three years – and thestory is not over yet. While the Indian WindEnergy Association estimates that wind currently accounts for 4,500 MW, the

government has mapped wind potential of45,000 MW across the country.

Looking ahead

There is a great deal to be optimistic about,especially in the states leading the way tochange. With the economy targeted to grow8-10% annually, an ever-growing appetite forpower is a certainty. Fundamental reformshave been pushed through largely irrespective of politics. The utilities sector ismoving away from a cost plus regime, andfocusing on efficiencies. With the underrecoveries falling by almost 75%, cash flowof the state sector utilities has improved 23%over the last few years, thereby enhancingpayment security. The country has the peopleresources it needs, and is developing a poolof expertise in new power generation buildthat could be the envy of other markets.

One note of caution, however, is the realityof operating a coalition government. India’spolitical climate is such that coalitions arethe norm; indeed, the current government isone. This brings unique challenges - whilethe majority party is firmly behind change, itforms a coalition with 15 other parties andtherefore cannot solely dictate the shape andspeed of reforms. And in a country whereraising fuel prices by a few rupees can trigger mass protests, the need for flexibilityalong the way is clear.

E r n s t & Y o u n g - U t i l i t i e s U n b u n d l e d - M a n a g i n g f o r g r o w t h i n a n u n c e r t a i n w o r l d 9

R E G I O N A L R E P O R T

Anjani K AgrawalIndustry Leader, Utilities, IndiaDirect tel: +22 2282 5000E-mail: [email protected]

Anjani’s professional career has included activeinvolvement in business improvement studies forpower generation, transmission and distributioncompanies. He also advises industry regulators andthe government on matters of policy and sectorreforms. Anjani is an active member of India’sNational Committee on Power, the ExecutiveCouncil of IEEMA and the Independent PowerProducers Association.

Source: Thomson Financial Datastream, Analysis Ernst & Young

Power generation by fuel mix

Climate change and the environment hasbecome a major political and business issue.In October, UK Prime Minister Tony Blairsent a letter to the leaders of the EuropeanUnion, warning that Europe had only 10-15years to avoid “catastrophic tipping points”for climate change. As a political consensusemerges on the need for action, alternativeenergy projects are attracting investors,graduates are quizzing potential employersabout environmental policies, and businessesare being hit by rising energy prices.

This increased political will to tackle climatechange, combined with concerns aboutsecurity of supply, have pushed alternativeenergy out of its niche market intomainstream fashion – if you like, fromsandals to Gucci shoes.

Actions speak louder than words

Recent activity has moved away fromstatements of corporate responsibility andinto hard corporate spend. Fortune 500companies such as Siemens, Goldman Sachs,Dupont, GE, BP, Shell and Total have showna desire to develop real business presence inthis market. New financing is being soughtfor expansion, consolidation is taking placeto meet surging demand, and newtechnologies are emerging. In addition,political interest has spurred nationalregulation in many countries to supportcarbon-friendly power generation (e.g.mandatory quotas for renewable generation,fixed prices, and tax credits) and a greateruse of energy efficiency measures by allenergy users.

All this is dispelling the myth that there is nomoney to be made in alternative energy.Below we explore five themes that should befactored into any utility’s strategic plans.

Defining alternative energyAlternative energy is a wide-ranging termthat includes a number of technologies torival and/or displace fossil fuels. The keycriteria are that they be low in carbonemissions and sustainable.

It may be helpful to think of energy as fallinginto three broad categories:

Dirty (high carbon emissions) CoalPetroleum

Cleaner technologies (reduced carbonemissions)Biofuels (transport fuels and oils fromrenewable sources, e.g. vegetable oils,ethanol and oilseeds)Biomass (biodegradable crops or waste thatcan be burnt to produce fuel, e.g. hemp, corn,organic municipal waste)Biogas (landfill gas)Clean coalCogeneration (combined heat and powerplants)Energy efficiency measures (e.g. insulation)Natural gasNuclear (zero emissions but remainingchallenges with waste storage)

Clean technologies (zero carbon emissions)GeothermalHydro (though some sustainability issues areassociated with large scale hydro)Solar (thermal, photovoltaic)Wave powerWind (onshore and offshore)

With scale comes cost efficienciesChina, India and Russia are making massiveinvestments in power generation to meetbooming demand. The actions they take inthe next few years will greatly influence theavailability and price of alternative energytechnologies.

One of the past stumbling blocks forrenewables has been the lack of large-scaleinvestment – casting them as pricey andrelatively untested niche products. This haschanged with China’s mass production ofsolar panels – which has lowered prices,increased availability and created a pool ofexpertise that the country is sharing with thedeveloping world. India’s success with windpower (see next point below) also proves thatcapacity from renewables can be addedquickly and at reasonable cost.

Rapid growth brings risk and rewardAlternative energy is a fast moving market.For example, India’s investment in windpower has proved so successful that it met itsfive-year target for wind generation in justthree. India’s wind firm Suzlon, listed in2005, is now the fifth largest wind turbinemanufacturer (by installed capacity) in theworld and has the highest marketcapitalization in its industry. (See relatedarticle on India on page 8).

China’s sheer size and rate of economic

growth has brought billions of dollars ofinvestment in renewables into the country,both in manufacturing and development.Some analysts expect China’s wind capacityto reach 50GW by 2030 – double thatglobally today.

With so many bright minds focused onclimate change, new technologies andapproaches are emerging. This speed bringsboth risks and rewards – and requires well-considered strategies – but few utilities willwant to sit this game out.

Diversity is keyThere is no one alternative energy product orpower source that utilities should pursue.Strategies will depend on your country’snatural resources (eg wind in the UK, hydroin the Nordics, solar in Spain, gas in Russia),existing infrastructure, industrial needs, andthe regulatory environment. For insight into20 renewable energy markets and theirsuitability for individual technologies, seeErnst & Young’s Renewable Energy CountryAttractiveness Indices (www.ey.com/renewables).

Utilities are likely to follow a number ofinvestment strategies, from venture capital tojoint ventures to mergers and acquisitions.Spain’s Iberdrola, for example, has been veryacquisitive, purchasing French projectdeveloper Perfect Wind, Community Energyin the US, and a stake in Spain’s Gamesa –all in Q2 2006.

Improving energy security

Disruptions and vulnerabilities in energysupply have become a political hot potato,and something that governments are keen toaddress. Alternative energy provides powerthat is less vulnerable to terrorism, andreduces dependency on foreign sources.

1 0 E r n s t & Y o u n g - U t i l i t i e s U n b u n d l e d - M a n a g i n g f o r g r o w t h i n a n u n c e r t a i n w o r l d

GreengoesGucciAlternative energygoes mainstream -report by Jon Hughesand Jonathan Johns

F U E L L I N G G R O W T H

Technology Current installed capacity

(GW as of 2005)

Small hydropower 66Wind power 59Biomass power 44Geothermal power9.3Solar photovoltaic-grid3.1Solar thermal electric0.4Ocean (tidal) power0.3Total renewable power182capacity (excluding large hydro)

For comparisonLarge hydropower750Total electric power 4,100capacity

Current globalrenewables capacity

Source: REN21

Customers could become producers The emergence of microgeneration, eghouses and buildings with solar panels ormini wind turbines, could change the entiredynamic of the industry. Though still in itsinfancy, microgeneration transformscustomers from users to self-suppliers andexporters as they sell excess capacity to thegrid. The UK, for example, is incorporatingmicrogeneration as part of the country’soverall energy strategy.

Upgrading existing infrastructure to copewith this complexity could be a challenge inmature markets; developing countries havean advantage when building newinfrastructure. While it is too early to sayhow microgeneration and its regulation willdevelop, it is something that should beconsidered in scenario planning, particularlyif the development of such technologiesbecomes the norm amongst the general public.

ConclusionRecent developments have shown thatalternative energy is no longer alternative: itis inevitable. Fossil fuels will reach a point ofdecline. This will affect any businessconsuming energy –not just utilities. Hencewe have leaders such as Virgin, which haspledged to invest USD$3 billion over thenext 10 years in biofuels and renewables. AsSir Richard Branson said, “We have to weanourselves off our dependence on coal andfossil fuels. Our generation has the

knowledge, it has the financial resources andas importantly it has the willpower to do so.”

Utilities must prepare themselves to addressthe challenges of this high growth market.Though strategies will differ based on localresources, needs and political will, twoimportant elements must be diversity andsustainability. The activist mantra, “Thinkglobally, act locally” has never seemed more apt.

E r n s t & Y o u n g - U t i l i t i e s U n b u n d l e d - M a n a g i n g f o r g r o w t h i n a n u n c e r t a i n w o r l d 1 1

F U E L L I N G G R O W T H

Coal cleans up its actCoal has a number of advantages: huge proven reserves, security of supply, stable prices, and flexibility. But ithas one big disadvantage – environmental impact. Will clean coal technologies be enough to save the day?Report by Michael Cupit

Jonathan JohnsTransaction Advisory Service, Renewable EnergyGroup, UKDirect tel: +44 1392 284382E-mail: [email protected]

Jonathan is the originator of Ernst & Young’sRenewable Energy Country Attractiveness Indices.He has wide experience of venture capital andproject finance using different renewable energytechnologies in a number of countries, includingadvising on financing the UK’s first-evercommercial wind farm in 1990. He is author ofnumerous papers on renewable energy, projectfinance and PFI, and is regularly invited to speak atinternational conferences.

Jon HughesHead of Utilities – UK & NEMIA UK Head of Corporate FinanceTransaction Advisory ServicesDirect tel: +44 121 535 2750 E-mail: [email protected]

Jon’s experience includes working with thegovernment, the regulator and some of Ernst &Young’s major energy/energy-related clients. Priorto joining Ernst & Young 7 years ago, he wasseconded as general manager of a power stationfor 14 months.

Despite its awakening to the dangers of climate change, the world isstill reliant on fossil fuels. In countries such as China, India and theUS – all with huge reserves – coal is set to retain its core position inthe generation mix in the near to mid term.

Global proven reservesCoal 200 years

Gas 60 years

Oil 40 years

Source: World Energy Council, Annual Survey of Energy Resources (2004)

Back to the futureCoal is attractive to utilities for a number of reasons. Over the lastthree to four decades, the price of coal has remained roughly constantat USD$30-40/ton; compare this to the volatility of gas prices andyou can see the appeal. Utilities can store huge volumes of coal at thepoint of generation, as much as three to four months, which reducesvulnerability of supply interruption. Finally, coal is also a flexibleenergy source. Historically, coal-fired power plants have beendesigned with huge amounts of generation flexibility, providingsystem operators with high levels of response in managing electricitysupply. Continued overleaf

1 2 E r n s t & Y o u n g - U t i l i t i e s U n b u n d l e d - M a n a g i n g f o r g r o w t h i n a n u n c e r t a i n w o r l d

F U E L L I N G G R O W T H

But these positives are offset by an increasingly important negative:environmental performance. Coal combustion releases a number ofemissions harmful to human health and the environment, includingsulphur dioxide, nitrogen oxides, particles, and greenhouse gases. Buta number of technologies are emerging to reduce this problem (seeinset box).

In brief: clean coal technologiesAt present most coal is burned in sub-critical pulverized fuelplants, achieving efficiencies of around 35% (although higher canbe achieved). There are a number of newer technologies that arebeing deployed or further developed. The most promising cleancoal technologies include:

1) Supercritical technologies: aimed at improving efficiency by utilizing higher pressures and temperatures in the generation, increasing efficiencies for electricity generation (typically in the range of 42-45%). Greater efficiency reduces the amount ofcoal used and hence, reduces emissions.

2) Fluidized beds: this technology family mixes coal with another media (such as sand) as it is fluidized, greatly reducing sulphur dioxide and nitrogen oxide emissions. Greenhouse gas emissions are reduced with higher efficiencies, in the range of 40-45%.

3) Gasification: Integrated Gasification Combined Cycle (IGCC) is a chemical process that turns coal into a synthetic gas, which generates lower emissions. Greenhouse gases are reduced, againas a consequence of higher efficiencies (45%). Significant R&D funding is being spent on this technology, to speed deployment on a commercial scale.

Improving coal’s carbon performanceIn terms of carbon emissions, the difference between an averageand a best in class coal plant is significant. But even the best inclass coal plant produces higher carbon emissions than gasequivalents, as shown below:

Beyond clean coal technologies that address combustion (see insetbox), there are also emerging technologies in the area of carboncapture and storage. These are relevant to all fossil fuel plants, butparticularly important for coal plants if we are to take the threat ofclimate change seriously. Two of the most promising technologiesare:

1) Pre-combustion decarbonization: High pressure, hightemperature steam is used to reform natural or synthetic gas, whichsplits out the carbon dioxide. This can then be pumped offshore orinto aquifers (see ‘Carbon storage’). This is available now, and hasbeen proven to work in trials.

2) Amine scrubbing: This is a chemical process that absorbscarbon dioxide into the Amine solution through a separatingmembrane. This offers great potential but is still being researchedand commercialized – a key challenge being scale.

Carbon storageOnce carbon dioxide has been captured, it can be safely pumpedunderground into depleted gas fields, oil fields and aquifers. Ofthese, oil fields may be the preferred route in the short term ascarbon storage helps to increase oil recovery. However, a persistentchallenge will be the infrastructure to pipe carbon dioxide to theselocations. This makes aquifers a better (if unproven) alternative asthey are more widely available, and on first examination may offersignificantly greater capacity.

The main barrier right now is cost, with estimates suggesting costsper ton of carbon dioxide in the USD$75-150 range. It is hopedthat these challenges can be addressed by ongoing research anddevelopment (R&D) investment in the US and through theEuropean Union’s research programs FP6 and FP7.

Longer time frame neededWhile clean coal technologies are ready to be tested, no long-termcarbon framework exists. Building a new coal station takes at leastten years, from inception to operation. Kyoto expires in 2012, andthere aren’t enough financial incentives to invest in the mostbeneficial technologies, such as IGCC. Policy makers need tothink longer term.

In the meantime, many countries - including China and India – areinvesting in available higher efficiency technologies. For example,India is investing in supercritical technology for seven major newcoal plants of 4,000 MW each (see related article on page 8). Insome European countries, new coal plants are being designed toenable sufficient space for carbon capture to be added at a laterdate with minimal disruption.

Over the next five to ten years, we should see coal retain itsimportance as a fuel source, thanks to its proven reserves, pricestability and security of supply. We will have cleaner coal, but weare unlikely to see a commercial deployment of zero emissions inthis timeframe.

Michael CupitTransaction Advisory ServicesEnergy, Chemicals and Utilities Direct tel: +44 20 7951 0127E-mail: [email protected]

Michael advises clients on transactions in both the renewables and theconventional power sectors. Before joining Ernst & Young in 2004, he ledthe energy practice at ERM Energy. A regulatory economist by background,he has 10 years’ experience on projects in Europe, the Middle East andCentral and South East Asia.

Aver

age

coal

pla

nt

Aver

age

supe

rcrit

ical

pla

nt

Aver

age

IGCC

pl

ant (

tria

l pla

nt)

Aver

age

gas

plan

t

Best

in c

lass

ga

s pla

nt

g CO2 / kWh (carbon emissions per kilowatt hour)

300360

700750

850

E r n s t & Y o u n g - U t i l i t i e s U n b u n d l e d - M a n a g i n g f o r g r o w t h i n a n u n c e r t a i n w o r l d 1 3

F U E L L I N G G R O W T H

Just a few notes. But a few notes chosen skilfully from an almostlimitless number of combinations.

Now, whilst Ernst & Young would never claim the genius ofBeethoven, we do pride ourselves on a similar ability to cutthrough the clutter of a complicated area to help you play toyour strengths.

Composing simple solutions to address the complex issues facedby Utilities is Ernst & Young’s forte. Our deep knowledge of theindustry allows us to develop leading-edge, cost-effective riskmanagement and compliance solutions tailored to your needs.

It’s a pragmatic approach that helps your business become moreattuned to significant areas of uncertainty. So you know when totake action, and when to take advantage with a perfectly-orchestrated response.

Ernst & Young Global Utilities Center, DüsseldorfTelephone: +49 (211) 9352 18427, email: [email protected]

!@#© 2006 EYGM LIMITED. ALL RIGHTS RESERVED.

After ten years in thedoldrums, nuclear poweris set for a comeback.Tony Ward reports onwhat’s driving new-buildnuclear There are currently some 440 nuclearreactors in the world, supplying about 15-16% of the world’s electricity. This fleet ofstations was built predominantly in the last30 years, but aside from activity in certainAsian markets, little has happened elsewhereover the last ten. However, nuclear constructionhas recently been stirring to life. Factorsrevitalizing the sector include a heavyincrease in demand for power to secureeconomic growth; stringent environmentalconstraints; and the tandem issues of security

and diversity of fuel supply. Today, there aresome 28 new nuclear power stations underconstruction in 12 countries around the world.1

The major drivers fornuclear’s resurgenceFuel security and economic growthIt’s increasingly important to many countriesto gain a greater degree of control and self-sufficiency over their power production:many are therefore moving away fromdependence on imported gas and oil, andtowards coal and nuclear. Countries withambitious goals for economic growth, forexample in Asia, need access to more power.The majority of new-build nuclear powerstations are located in the Far East, primarilyIndia (7), China (5) and Russia (3).

Controlling emissions Nuclear power potentially plays a significantrole in reducing emissions: taking intoconsideration the lifecycle of building,operating and decommissioning powerstations, as well as their fuel cycle, they emit relatively little greenhouse gas. James Lovelock, the respected campaignerfor environmental and green issues,

compellingly said earlier this year: ‘To reconcile global human need andenvironmental preservation, our world needs nuclear energy’. Whilstenvironmentalists would like othertechnologies to be available to generatepower with minimal environmental impact,the fact is that those technologies are not yet readily available on the scale we need.

Changing attitudesThe extent to which nuclear is welcomevaries widely around the world. Germany has continually said ‘no’, whilst just a shortdistance away in Scandinavia, communitieshave been competing to host an undergroundnuclear waste repository. They perceivenuclear to be safe, and welcome it as a fuelsource since it will make them moreindependent of Russia. Even in the US,where no new reactors have been built for 15 years (primarily in response to the 1979accident at Three Mile Island) attitudes arechanging. The US government is puttingtaxpayers’ money into a programencouraging new nuclear build, which byOctober 2006 had already brought forwardmore than 20 new nuclear reactor projects for licensing approval.

1 4 E r n s t & Y o u n g - U t i l i t i e s U n b u n d l e d - M a n a g i n g f o r g r o w t h i n a n u n c e r t a i n w o r l d

Back fromthe cold

F U E L L I N G G R O W T H

1Source WNA website: www.world-nuclear.org/info/reactors.htm and www.world_nuclear.org/info/inf17.htm

Challenges to newnuclearHistory and perceptions of safetyFor countries like the US, the UK andRussia, nuclear is inextricably linked withmilitary programs, fears about accidents, and protest over environmental damage andthe legacy of irradiated waste. But in reality,the safety record of the industry standscomparison with other fuel technologies.Modern reactors are built to maximize safetyand efficiency. And there is a very robustregulatory environment - nationally andinternationally - to ensure thoroughassessment and adequate controls are inplace. In the light of these factors, onemessage that the industry will be concernedto get across is that choosing nuclear doesnot mean compromising safety for the sakeof better generation capacity.

Delivering projects on time and tobudgetAn issue that the nuclear industry mustaddress is building confidence that it isable to deliver timely and cost-effectiveconstruction. To date in the West, we haveseen a pattern of planning delays andconstruction cost overruns. For example inthe US, only 2 of the 104 reactors inoperation are believed to have come in aheadof time and on budget. The reactor currentlyunder construction in Finland for TVO - thefirst of a potential new wave around Europe -is now 12 months into construction and hasaccumulated 12 months of delays, togetherwith a significant escalation in costs. InFrance, EDF increased their estimate of thecost of the new Flamanville 3 power stationby 10% before they even signed theconstruction contract.

In a sense, the delays to which nuclear buildhas been subject are no different to any majorconstruction project: failures in projectmanagement; quality and supply issues withcritical components; and regulatory andplanning regimes which require majorchanges and force costs up. Some of theAsian constructors currently building inJapan, Korea and China are nowdemonstrating they can deliver both onbudget and on time. One potential reason isthat they are tending to build fleets of similarreactors, so they have the benefit of learningfrom one project to another. It will be criticalfor other countries and operators to learnfrom this experience if the pitfalls of the pastare to be avoided.

Dealing with wasteMost groups who lobby against nuclear nolonger argue that it is unsafe, but they doexpress worries about nuclear waste and the fact that its storage or disposal createsinter-generational issues.

Unless reprocessing returns to favour, themost likely disposal method is some form of underground repository. Whilst plansexist, and nations have reached decisions topursue such a disposal route, no-one has yetbuilt and operated a repository. It is likelythat the technology for deep disposal willdevelop and become more widely appliedover the coming decades. A key factor that isinfluencing the seemingly slow progress tofinal disposal is the concern to ensure thatthe waste remains retrievable. It is importantnot to cut off a future generation’s option todig it up, and either dispose of it in a betterway, or perhaps to reprocess it and recoverthe uranium.

Future uranium suppliesRecent studies have consistently assessed theproven reserves to be in excess of 40 years’worth of high-grade uranium, assuming wecontinue to use it at today’s rate. We canassume that if demand increases, then so willthe price, stimulating the discovery of furtherreserves (as has happened with oil and gas).Lower-grade uranium is also available. It isquite conceivable that, over the nextgeneration, reprocessing of spent fuel mayagain be judged viable, and provide anotheruranium source. It therefore seemsreasonable to assume that plenty of reservesat an economic price will be available forsubstantially more than 40 years.

Alternatively, the use of thorium as a fuel isconceivable, and is being pursued by India.This has potential attractions - not least that thorium is considerably more abundantthan uranium.

Looking forwardAsia’s commitment to nuclear is clear – as well as the reactors currently underconstruction there, many more are planned or proposed, principally in China and India.

We can therefore expect to see further steadyincreases in the rate of construction. Theemerging consensus in many Westerneconomies regarding the significance ofglobal warming, and the combined impact ofconcerns over security of national energysupplies -together with the desire foreconomic growth not to be constrained -makes it highly likely that we will seesubstantial new nuclear build all around theworld in the years to come.

E r n s t & Y o u n g - U t i l i t i e s U n b u n d l e d - M a n a g i n g f o r g r o w t h i n a n u n c e r t a i n w o r l d 1 5

F U E L L I N G G R O W T H

Tony WardTransaction Support, UKDirect tel: +44 121 535 2921E-mail: [email protected]

Tony has worked in the power generation and wider utilities sector since 1994. He spent twoyears on secondment to the UK’s main nucleargenerator, and has also been responsible forproviding market-wide assurance on the UK’selectricity wholesale and retail markets. He hasrecently been advising the UK Government on itsReview of Energy Policy, primarily with regard tonuclear generation.

!@#

Diary Date: 2007

Ernst & Young Official Sponsor

Infrastructureinvestment and serviceefficiency are keychallenges for waterutilities today – interview with ChristineStaub and Laurent Vitse Q: What would you say are the mostimportant issues facing the waterindustry today?

A: Top priority is probably maintainingenvironmental, health and performancestandards: performance is key to keeping thewater price reasonable, which is vital whetherwe’re talking about the western world orelsewhere. For developing countries, dealingwith the twin problems of scarcity of thebasic resource and the issue of access isanother huge challenge for governments andthe industry. In countries where watershortages happen, often the problem is not a lack of water resource as such, but accessto that water. So you get situations like Sub-Saharan Africa or Latin America on theone hand, where water is in abundant supply,but between one-quarter and one-half of thepopulation has no access to drinking water;and on the other hand, in some arid countries,100% of the population is served 1.

Developing countries without appropriateinfrastructure find it almost impossible toprovide water services or protect against therisk of water-related disasters and disease.Currently, 1.1 billion people have no access

to any type of improved source of drinkingwater 2. One of the UN’s MilleniumDevelopment Goals is to cut by half theproportion of people without sustainableaccess to safe drinking water and basicsanitation by 2015. The estimated costs toachieve this vary from USD$9-30 billion perannum 3. If the industry is going to help toachieve the goal, there will have to be muchgreater access to financial resources, as wellas a strong political will.

Another big issue the industry has is thebasic efficiency of the service – the problemof ‘non-revenue’ water – which is aparticular problem in emerging countries. In the developed world, more than 75% ofthe water produced is actually charged to theend users. In emerging countries like Africa,the Phillippines and Indonesia, this ratio israrely higher than 50%. There is a huge lossof water through leakage, incorrect metering,frauds and other misuse. It comes back to aquestion of investment in infrastructure – thatis, upgrading existing infrastructure to get itto a sound, acceptable standard, and layingdown new infrastructure where there is none.

This is a big issue all over the world, whetheryou’re talking about reaching a minimumplatform of water security in the emergingcountries, or strengthening growth in thedeveloped world. But can we find the moneyto finance the investment that is needed? The key question is how costs will be passedon to the customer. Regulation has clarifiedthe rules to some extent, and investmentoften equates to revenue growth. But finally,it is the public entity’s job to strike thatfragile balance between capital expenditurerequirements on one hand and affordabilityon the other.

Q: Given these huge financingrequirements, do you see infrastructurefunds playing a more prominent role in the industry in future?

A: I think infrastructure funds are certainlyinterested – after all, water is a secure

investment. It provides good returns and thefunds can be sure people will still want todrink it in 50 years’ time. However, I thinkoutright acquisitions, like the recentMacquarie acquisition of Thames Water inthe UK, will be something of an exception to the rule, due to the limited number ofpotential targets.

In general, the infrastructure funds are morelikely to want to work in partnerships, and we might see some sophisticated andinnovative new co-financing structurescoming through, in terms of Public PrivatePartnerships (PPP) and other multi-stakeholderpartnerships. For example, if you want to wina water contract in the major city of anemerging country, and the municipality needshalf a billion dollars of investment, it isunlikely that a fund would go in alone. It’salso a heavy capital burden for an operator totake on alone. But a three-way partnershipbetween the municipality, the private operatorand the infrastructure fund could work well.

Q: What opportunities does the Asian economy offer?

There is growing environmental awareness in China - big concerns about the level ofpollution and the fact that water is notdrinkable everywhere. The localmunicipalities are not water experts, and as well as these difficult environmentalchallenges, they need to build in efficiency.So they are looking to private companies for expertise. Each municipality in China isfree to organize its own tender process for itswater contract, which would normally be a30 to 50-year arrangement.

As well as opportunities in China, we’re alsoseeing local infrastructure investment fundsbeing structured by national companies inplaces like India and the Middle East. We are talking about big money – as much ashalf a billion dollars for some of these funds.All of this means there is huge potential forprivate operators to export their expertise andgrow through winning these contracts.

Liquidassets

1 6 E r n s t & Y o u n g - U t i l i t i e s U n b u n d l e d - M a n a g i n g f o r g r o w t h i n a n u n c e r t a i n w o r l d

W A T E R A N D W A S T E

What does the water industry do? Water is a natural resource that belongs to everyone and no-one.The world’s water companies do not own water - and they don’t sell it to us, either. What they market are the costs of:

■ producing drinkable water

■ distributing water to end users

■ collecting waste water

■ treating waste water

1Source: World Water Forum 2Source: World Health Organisation website 3Source: World Water Forum

Recycling and renewalEnvironmental concerns are shaping the waste management industryReport by Jean Bouquot, Steve Brown and Rob Winchester

The potential for the world’s waste to pollute our ground and water has always been a major concern for environmentalists and governments. Gas emissions from waste also have the potential to contribute to global warming if not properly managed. Not surprisingly, therefore, it is environmental issues and regulationwhich are driving the waste management industry today. In the EU,there is a wide range of legislation and programs which aim to dispose of waste in a more environmentally-friendly manner, or reduce the volume of waste at source. The US also has similarrecycling programs which vary by state, as well as Federal guidelines regarding landfill construction and management.

What this new legislation is doing is converting environmentalconcerns into financial risk to achieve change - either banning andpenalizing bad behaviors, or making them uneconomic. This meansboth businesses and governments are facing major investmentdecisions on how best to mitigate this new order of financial risk. It is also creating major opportunities for the waste managementindustry, and giving them an opportunity to take a leadership role,ahead of governmental mandates.

European Union’s tough exampleThe European Union is probably the most advanced example of howclimate concerns are driving change in the industry. The 1999 EULandfill Directive introduced progressively increasing targets toreduce reliance on landfill across Europe. Countries with a traditionalreliance on landfilling waste - including the UK, Ireland, Spain,

Portugal and Italy - all have major investment programs to fund,which will be delivered by the private sector. The UK, for example,has a £10 billion investment requirement over the next 10 years.

The member states which have recently joined the EU are currentlylagging behind in terms of sophisticated waste managementapproaches. Their first priority will be to put investment into updatingtheir landfill practices, and then consider landfill diversion as asecond stage.

Potential major new markets in AsiaThe regions facing the greatest waste management challenge aredeveloping economies which, as well as producing a significantamount of the world's goods, are now facing the associated waste andpollution problems. Up until now, there hasn’t been a great deal ofattention focused on environmental protection in this region. But with the Kyoto environmental targets already in force, furtherlegislative pressure is sure to follow in due course. At the momentthere is a lack of homegrown expertise and this region lags the Westby a long distance. Western waste management companies – likeVeolia and Suez – are therefore leading the way, having moved intowater treatment and solid waste disposal in China (having had a long-term presence in Hong Kong). However, their operations are stillcurrently relatively small compared to the potential size of the Asianmarket. The key issue governing growth here is whether localauthorities will pay the right price to do the right thingenvironmentally. Continued overleaf

E r n s t & Y o u n g - U t i l i t i e s U n b u n d l e d - M a n a g i n g f o r g r o w t h i n a n u n c e r t a i n w o r l d 1 7

W A T E R A N D W A S T E

Christine StaubAssurance and Advisory Business ServicesUtilities, FranceDirect tel: +33 1 55 61 08 84E-mail: [email protected]

Christine has worked for Ernst & Young for 15years, and within the Utilities sector for over 10years. She is currently focusing on the Waterindustry. Since joining Ernst & Young, Christine hasworked on a number of buy-side due diligences in the utilities and infrasructure sectors.

Annual investment in water across Europe(in euros per inhabitant)

Annual investment in water across Europe (in euros per inhabitant)Data 2001, except for Spain (2000), the Czech Republic and The Netherlands (2002), France (2003).

Source: SPDE (Syndicat professionel des entreprises de service d’eau et d’assainissement)

1 8 E r n s t & Y o u n g - U t i l i t i e s U n b u n d l e d - M a n a g i n g f o r g r o w t h i n a n u n c e r t a i n w o r l d

W A T E R A N D W A S T E

Rob WinchesterTransaction Advisory Services, UKDirect tel: +44 20 7951 3227E-mail: [email protected]

Rob is head of Ernst & Young’s UK wastemanagement team, which advises exclusively on waste projects including - but not limited to -Public Private Partnership transactions.

Steve BrownAssurance and Advisory Business ServicesUtilities, USDirect tel: +1 713 750 8374E-mail: [email protected]

Steve has over 23 years of public accountingexperience and has been part of the Ernst & Youngteam since 2002. His current focus within theUtilities sector is in solid waste and wastewater,where he serves Waste Management and VeoliaWater North America.

Jean BouquotHead of Utilities, Continental Western Europe AABS representative, Global Utilities Core TeamDirect tel : + 33 1 55 61 02 14E-mail : [email protected]

Jean works with utilities and environment-relatedcompanies and also has experience with variousmanufacturing and distribution industries. Inaddition to auditing major listed companies andadvising on transactions, he has worked extensivelywith clients on registration statements in the US.

Legislation causing consolidation inthe private sector With increased legislation driving up R&Dand other costs and pushing up requiredlevels of investment, many markets arebecoming punishingly competitive. Theindustry’s reaction has been to consolidate,pushing out the smaller players.

In 2000, thirteen companies made up half theUK market: now there are only seven. InEurope, the large operators from the solidnon-hazardous side of the business have beenacquiring niche operators in the hazardous

waste market. Interestingly, in the US, where the market is dominated by just threemajors, the industry went through thisconsolidation cycle some time ago, andseems to be reversing to some degree asoperating strategies evolve.

Recycling and power generation For their part, waste management companiesare concentrating a good deal of effort onincreasing their recycling capacity. This isnot just good citizenship: it makes pragmatic

business sense. Good environmentalcredentials are crucial in, for example,securing planning permission to develop newlandfill capacity. In addition, recycling ispotentially highly profitable. Waste managersare therefore industrializing the process, andforming joint ventures to recycle productslike used oil. They are also becoming part ofthe power grid: US and European companiesare generating power from landfill gas andincinerators, which is sold back into theelectricity grid. In the future, waste couldbecome a valuable alternative power source.

The facts about global wasteIn developed countries, each personproduces 5-10 times his or her body weight in municipal waste per year. But there are huge variations: the average Japaneseproduces 45% less than the averageAmerican. Industrial, mining andconstruction wastes are many times greaterthan municipal. The shares going torecycling, incineration or landfill also varywidely, as is clear from the chart.

In most countries, waste generationcontinues to grow – even in developedeconomies where comprehensive wastereduction strategies have been initiated.However, in general statistics are poorlyreported, often incomplete and lackingharmony of definition from country tocountry. Now that the industry is starting to treat different parts of the waste streamin different ways, the data is graduallyimproving – as it must, if businesses are to be able to plan correctly for thenecessary investment required in future.

Municipal waste treatment

Source: United Nations Statistics Division, 2006

recycled

incinerated

landfill

amou

nt o

f w

aste

trea

ted

(kg/

capi

ta)

A review of the utility regulator activityaround the world reveals the extent to whichtheir roles can differ. We’re also seeing acontinuing (and highly lively) debate onwhether privatization arguments are oversold,and the need and scope for regulatory controlunderrated.

European UnionGovernments and regulators in the EU arefairly convinced of the benefits of thecompetition model. A number of marketshave already liberalized quite extensively.Some 22 years after the first Directives startedto open up the energy markets, we’ll reachthe point next year when the final barrier(residential-level competition) comes down.

But the regulatory debate is still energetic: onone side we have enthusiastic supporters ofcompetition who believe regulators must doeverything they can to aid – or even force –competition to deliver. Fans of liberalizationinsist ‘the market will provide’, and that eventhe significant price volatility we have seenin the UK market is not a sign thatcompetition is not working (and thereforethat regulators need to step in and correct it),but that it is working. Their view is thatvolatility and rising prices send the rightsignals for markets to invest, and thereforeregulators need to step back and let theseforces work. On the other side of the debateare countries like France where there is aconcern that the State needs to retainsignificant stakes in the infrastructurecompanies, to make sure that essentialinvestment decisions which relate topreserving security of supply are approved.

Eastern Europe (non-EU)Here the dynamics are mixed. There is adesire to privatize, and some countries arebeginning to align themselves with theregulatory and market models of WesternEurope. We are seeing fairly significantrestructuring on the fringes of the EU.

Infrastructure renewal is a big issue:individual countries are no longer able toinvest in their ageing assets to the extentneeded and this, for example, has promptedthe proposals to privatize and list parts ofRussia’s Unified Electrical System toencourage additional capital to flow in.However, this doesn’t mean Russianregulators are in any big rush to change: the Russian government has actively resistedcalls from the EU to restructure and allow,for example, third party access to networks.

North America This region is in a sensitive, unstable state asfar as liberalization is concerned. A numberof States have progressed to residential levelcompetition and paused; others have allowedthe whole process to stall at the industrial andcommercial level. This is creating tensionsover pricing, and there is little clarity aboutwhat we can expect. There may be slowprogress; on the other hand the residential-level competition pilots currently underwaymay end up in failure - in the same way, for example, as we saw Ontario ultimatelyretreat from the competitive model followingmishandling of tariff setting. The FederalEnergy Regulatory Commission (FERC), the independent regulatory agency for the USenergy sector, focuses largely on inter-stateissues, so their remit is more structural thancompetition-related. Independent marketingorganizations are beginning to lobby both atstate and national level to breathe some lifeback into the process of liberalization. The USneeds to do something to get back on track.The issue at stake is international competitiveness:if their industry cannot hold its own againstother nations, who ultimately pays?