The performativity of potential output - Arbeiterkammer · production function, where ↵ and (1...

61

Philipp Heimberger Vienna Institute for International Economic Studies (wiiw) and Institute for Comprehensive Analysis of the Economy (ICAE), Johannes Kepler University Linz Young Economists Conference October 5th 2016 The performativity of potential output: Pro-cyclicality and path-dependency in coordinating European fiscal policies

Transcript of The performativity of potential output - Arbeiterkammer · production function, where ↵ and (1...

Philipp Heimberger Vienna Institute for International Economic Studies (wiiw)

and

Institute for Comprehensive Analysis of the Economy (ICAE), Johannes Kepler University Linz

Young Economists Conference October 5th 2016

The performativity of potential output: Pro-cyclicality and path-dependency

in coordinating European fiscal policies

Philipp Heimberger

Starting point

• Recent economic developments in Europe and the role of fiscal policy

• Specific focus: Potential output model of the European Commission used for

calculating structural budget balances

• Research interest: Impact of the model on medium-term economic development (focus

on euro area economies during 1999-2014)

2

European economic policy: PO model („an essential ingredient in the fiscal surveillance process“)

Performativity of economic models („an engine, not a camera!“)

Philipp Heimberger

The inner workings of the potential output model A short introduction

3

Philipp Heimberger

The inner workings of the potential output model A short introduction

3

and the NAWRU is that the latter is subject to small cyclical spillovers (which, e.g.,are the consequence of wage rigidities or cyclical wage mark-ups; see: Havik et al.(2014), p. 28-30 or EuropeanCommission (2013), p. 85-86). So while the modelincludes two main ’structural’ variables for explaining changes in potential outputover time, it only provides one practical lever to increase potential output when itcomes to questions of economic policy design: here, the clear policy imperative is todecrease labor market regulation and lower social welfare standards, since technol-ogy is conceptualized as completely autonomous and exogenous; as a residual whichonly explains the part of the evolution of the output gap over time which cannot beexplained by deviations of actual unemployment from the NAWRU. 1

3 The European Commission’s production functionapproach to estimating potential output

Non-observable potential output is calculated by means of a production functionapproach: Under the assumptions of constant returns to scale and perfect compe-tition, the relevant components of the labor input, capital stock and total factorproductivity are plugged into a neoclassical Cobb-Douglas production function:

Y POTt

= L↵

t

⇤K1�↵

t

⇤ TFPt

(3)

where Y POTt

is potential output, Lt

is the contribution of the production factorlabour to potential output, K

t

is the contribution of capital to potential output, andTFP

t

is total factor productiviy (all at time t). We are looking at a Cobb-Douglasproduction function, where ↵ and (1 � ↵) are the constant output elasticities oflabour and capital, respectively (Havik et al. (2014), p. 10).

In what follows, we focus on the estimation of the labour component Lt

, becausethis is of central importance for the concept of potential output, as defined by theEuropean Commission.

The contribution of labour to potential output is defined as follows:

Lt

= (POPWt

⇤ PARTSt

⇤ (1�NAWRUt

)) ⇤HOURSTt

(4)

where

POPWt

is population of working age, PARTSt

is the smoothed participation rate,NAWRU

t

is the non-accelerating wage inflation rate of unemployment andHOURSTt

is the trend of average hours worked (all at time t) (Havik et al. (2014), p. 14).PARTS

t

and HOURSTt

are detrended variables; they are calculated by makinguse of the Hodrick-Prescott-Filter (HP filter).2 NAWRU

t

is calculated by meansof a statistical technique called Kalman filter (see below for an introduction to theKalman filter approach).

1Which could well be wrong as technological advances and labor standards might well be correlatedpositively (see: QUELLEN).

2The HP filter is a univariate approach to removing the cyclical component of a time series from the”trend component” (Hodrick and Prescott (1997)). Regarding the basic limitations of the HP filter- with particular emphasis on the so called ”end-point bias -, see, e.g., Kaiser and Maravall (2001).

6

potential output

Philipp Heimberger

The inner workings of the potential output model A short introduction

3

and the NAWRU is that the latter is subject to small cyclical spillovers (which, e.g.,are the consequence of wage rigidities or cyclical wage mark-ups; see: Havik et al.(2014), p. 28-30 or EuropeanCommission (2013), p. 85-86). So while the modelincludes two main ’structural’ variables for explaining changes in potential outputover time, it only provides one practical lever to increase potential output when itcomes to questions of economic policy design: here, the clear policy imperative is todecrease labor market regulation and lower social welfare standards, since technol-ogy is conceptualized as completely autonomous and exogenous; as a residual whichonly explains the part of the evolution of the output gap over time which cannot beexplained by deviations of actual unemployment from the NAWRU. 1

3 The European Commission’s production functionapproach to estimating potential output

Non-observable potential output is calculated by means of a production functionapproach: Under the assumptions of constant returns to scale and perfect compe-tition, the relevant components of the labor input, capital stock and total factorproductivity are plugged into a neoclassical Cobb-Douglas production function:

Y POTt

= L↵

t

⇤K1�↵

t

⇤ TFPt

(3)

where Y POTt

is potential output, Lt

is the contribution of the production factorlabour to potential output, K

t

is the contribution of capital to potential output, andTFP

t

is total factor productiviy (all at time t). We are looking at a Cobb-Douglasproduction function, where ↵ and (1 � ↵) are the constant output elasticities oflabour and capital, respectively (Havik et al. (2014), p. 10).

In what follows, we focus on the estimation of the labour component Lt

, becausethis is of central importance for the concept of potential output, as defined by theEuropean Commission.

The contribution of labour to potential output is defined as follows:

Lt

= (POPWt

⇤ PARTSt

⇤ (1�NAWRUt

)) ⇤HOURSTt

(4)

where

POPWt

is population of working age, PARTSt

is the smoothed participation rate,NAWRU

t

is the non-accelerating wage inflation rate of unemployment andHOURSTt

is the trend of average hours worked (all at time t) (Havik et al. (2014), p. 14).PARTS

t

and HOURSTt

are detrended variables; they are calculated by makinguse of the Hodrick-Prescott-Filter (HP filter).2 NAWRU

t

is calculated by meansof a statistical technique called Kalman filter (see below for an introduction to theKalman filter approach).

1Which could well be wrong as technological advances and labor standards might well be correlatedpositively (see: QUELLEN).

2The HP filter is a univariate approach to removing the cyclical component of a time series from the”trend component” (Hodrick and Prescott (1997)). Regarding the basic limitations of the HP filter- with particular emphasis on the so called ”end-point bias -, see, e.g., Kaiser and Maravall (2001).

6

potential output

NAIRU == Kalman-Filtered Unemployment Rate

Philipp Heimberger

The inner workings of the potential output model A short introduction

3

and the NAWRU is that the latter is subject to small cyclical spillovers (which, e.g.,are the consequence of wage rigidities or cyclical wage mark-ups; see: Havik et al.(2014), p. 28-30 or EuropeanCommission (2013), p. 85-86). So while the modelincludes two main ’structural’ variables for explaining changes in potential outputover time, it only provides one practical lever to increase potential output when itcomes to questions of economic policy design: here, the clear policy imperative is todecrease labor market regulation and lower social welfare standards, since technol-ogy is conceptualized as completely autonomous and exogenous; as a residual whichonly explains the part of the evolution of the output gap over time which cannot beexplained by deviations of actual unemployment from the NAWRU. 1

3 The European Commission’s production functionapproach to estimating potential output

Non-observable potential output is calculated by means of a production functionapproach: Under the assumptions of constant returns to scale and perfect compe-tition, the relevant components of the labor input, capital stock and total factorproductivity are plugged into a neoclassical Cobb-Douglas production function:

Y POTt

= L↵

t

⇤K1�↵

t

⇤ TFPt

(3)

where Y POTt

is potential output, Lt

is the contribution of the production factorlabour to potential output, K

t

is the contribution of capital to potential output, andTFP

t

is total factor productiviy (all at time t). We are looking at a Cobb-Douglasproduction function, where ↵ and (1 � ↵) are the constant output elasticities oflabour and capital, respectively (Havik et al. (2014), p. 10).

In what follows, we focus on the estimation of the labour component Lt

, becausethis is of central importance for the concept of potential output, as defined by theEuropean Commission.

The contribution of labour to potential output is defined as follows:

Lt

= (POPWt

⇤ PARTSt

⇤ (1�NAWRUt

)) ⇤HOURSTt

(4)

where

POPWt

is population of working age, PARTSt

is the smoothed participation rate,NAWRU

t

is the non-accelerating wage inflation rate of unemployment andHOURSTt

is the trend of average hours worked (all at time t) (Havik et al. (2014), p. 14).PARTS

t

and HOURSTt

are detrended variables; they are calculated by makinguse of the Hodrick-Prescott-Filter (HP filter).2 NAWRU

t

is calculated by meansof a statistical technique called Kalman filter (see below for an introduction to theKalman filter approach).

1Which could well be wrong as technological advances and labor standards might well be correlatedpositively (see: QUELLEN).

2The HP filter is a univariate approach to removing the cyclical component of a time series from the”trend component” (Hodrick and Prescott (1997)). Regarding the basic limitations of the HP filter- with particular emphasis on the so called ”end-point bias -, see, e.g., Kaiser and Maravall (2001).

6

potential output

AMECONAIRU == Kalman-Filtered Unemployment Rate

Philipp Heimberger

The inner workings of the potential output model A short introduction

3

and the NAWRU is that the latter is subject to small cyclical spillovers (which, e.g.,are the consequence of wage rigidities or cyclical wage mark-ups; see: Havik et al.(2014), p. 28-30 or EuropeanCommission (2013), p. 85-86). So while the modelincludes two main ’structural’ variables for explaining changes in potential outputover time, it only provides one practical lever to increase potential output when itcomes to questions of economic policy design: here, the clear policy imperative is todecrease labor market regulation and lower social welfare standards, since technol-ogy is conceptualized as completely autonomous and exogenous; as a residual whichonly explains the part of the evolution of the output gap over time which cannot beexplained by deviations of actual unemployment from the NAWRU. 1

3 The European Commission’s production functionapproach to estimating potential output

Non-observable potential output is calculated by means of a production functionapproach: Under the assumptions of constant returns to scale and perfect compe-tition, the relevant components of the labor input, capital stock and total factorproductivity are plugged into a neoclassical Cobb-Douglas production function:

Y POTt

= L↵

t

⇤K1�↵

t

⇤ TFPt

(3)

where Y POTt

is potential output, Lt

is the contribution of the production factorlabour to potential output, K

t

is the contribution of capital to potential output, andTFP

t

is total factor productiviy (all at time t). We are looking at a Cobb-Douglasproduction function, where ↵ and (1 � ↵) are the constant output elasticities oflabour and capital, respectively (Havik et al. (2014), p. 10).

In what follows, we focus on the estimation of the labour component Lt

, becausethis is of central importance for the concept of potential output, as defined by theEuropean Commission.

The contribution of labour to potential output is defined as follows:

Lt

= (POPWt

⇤ PARTSt

⇤ (1�NAWRUt

)) ⇤HOURSTt

(4)

where

POPWt

is population of working age, PARTSt

is the smoothed participation rate,NAWRU

t

is the non-accelerating wage inflation rate of unemployment andHOURSTt

is the trend of average hours worked (all at time t) (Havik et al. (2014), p. 14).PARTS

t

and HOURSTt

are detrended variables; they are calculated by makinguse of the Hodrick-Prescott-Filter (HP filter).2 NAWRU

t

is calculated by meansof a statistical technique called Kalman filter (see below for an introduction to theKalman filter approach).

1Which could well be wrong as technological advances and labor standards might well be correlatedpositively (see: QUELLEN).

2The HP filter is a univariate approach to removing the cyclical component of a time series from the”trend component” (Hodrick and Prescott (1997)). Regarding the basic limitations of the HP filter- with particular emphasis on the so called ”end-point bias -, see, e.g., Kaiser and Maravall (2001).

6

potential output

Kalman-Filtered Solow-Residual

AMECONAIRU == Kalman-Filtered Unemployment Rate

Philipp Heimberger

The inner workings of the potential output model A short introduction

3

and the NAWRU is that the latter is subject to small cyclical spillovers (which, e.g.,are the consequence of wage rigidities or cyclical wage mark-ups; see: Havik et al.(2014), p. 28-30 or EuropeanCommission (2013), p. 85-86). So while the modelincludes two main ’structural’ variables for explaining changes in potential outputover time, it only provides one practical lever to increase potential output when itcomes to questions of economic policy design: here, the clear policy imperative is todecrease labor market regulation and lower social welfare standards, since technol-ogy is conceptualized as completely autonomous and exogenous; as a residual whichonly explains the part of the evolution of the output gap over time which cannot beexplained by deviations of actual unemployment from the NAWRU. 1

3 The European Commission’s production functionapproach to estimating potential output

Non-observable potential output is calculated by means of a production functionapproach: Under the assumptions of constant returns to scale and perfect compe-tition, the relevant components of the labor input, capital stock and total factorproductivity are plugged into a neoclassical Cobb-Douglas production function:

Y POTt

= L↵

t

⇤K1�↵

t

⇤ TFPt

(3)

where Y POTt

is potential output, Lt

is the contribution of the production factorlabour to potential output, K

t

is the contribution of capital to potential output, andTFP

t

is total factor productiviy (all at time t). We are looking at a Cobb-Douglasproduction function, where ↵ and (1 � ↵) are the constant output elasticities oflabour and capital, respectively (Havik et al. (2014), p. 10).

In what follows, we focus on the estimation of the labour component Lt

, becausethis is of central importance for the concept of potential output, as defined by theEuropean Commission.

The contribution of labour to potential output is defined as follows:

Lt

= (POPWt

⇤ PARTSt

⇤ (1�NAWRUt

)) ⇤HOURSTt

(4)

where

POPWt

is population of working age, PARTSt

is the smoothed participation rate,NAWRU

t

is the non-accelerating wage inflation rate of unemployment andHOURSTt

is the trend of average hours worked (all at time t) (Havik et al. (2014), p. 14).PARTS

t

and HOURSTt

are detrended variables; they are calculated by makinguse of the Hodrick-Prescott-Filter (HP filter).2 NAWRU

t

is calculated by meansof a statistical technique called Kalman filter (see below for an introduction to theKalman filter approach).

1Which could well be wrong as technological advances and labor standards might well be correlatedpositively (see: QUELLEN).

2The HP filter is a univariate approach to removing the cyclical component of a time series from the”trend component” (Hodrick and Prescott (1997)). Regarding the basic limitations of the HP filter- with particular emphasis on the so called ”end-point bias -, see, e.g., Kaiser and Maravall (2001).

6

potential output

2 How does the European Commission define andmodel the key concepts: structural budget balance,potential output, output gap and NAWRU

This section introduces the key concepts for estimating structural budget balances.It provides definitions for the most important terms and components of the EuropeanCommission’s model and illuminates their theoretical background.

2.1 The structural budget balance

The basic rationale behind the structural budget balance (SB) is to provide anestimate for EU member states’ fiscal performance, which takes additional economicand political considerations into account to look beyond short term ’headline’ fiscalbalances as reported by individual countries. Specifically, the structural budgetbalance considers cyclical movements in economic activity as well as extraordinaryevents a↵ording extraordinary political e↵orts.

The calculation of the structural budget balance is based on a two step-correctionprocedure, which takes the reported fiscal balance FB - defined as governmentrevenues (R) minus government expenditures (G) relative to nominal GDP (Y )(FB = R

t

�G

t

Y

nom

t

) - as its starting point. The aim of thefirst correction step is to ac-

count for the impact of cyclical fluctuations on fiscal performance by calculating avirtual fiscal balance that would prevail if the economy was operating at potentialoutput(e.g. Angerer (2015)). It is in this context that economic theory and, specifi-cally, the GAP-model of the European Commission comes in to play a decisive role,since the European Commission makes use of the GAP-model’s estimates to adjustreported ’headline’ fiscal balances. In detail, the Commission combines estimateson the di↵erence between ’observed’ and ’potential’ output - labelled the ’outputgap’ (OG

t

) - as produced by the Commission’s GAP-model with an estimate forthe budgetary semi-elasticity (✏

t

) measuring the reaction of the budget balance tothe output gap (provided by the OECD, see: INCLUDE SOURCE PRICE ET AL.2014; Mourre et al. (2014), p. 21). This parameter is used for mapping the estimated’output gap’ onto the dimension of fiscal policy via ✏

t

OGt

to calculate the so-called’cyclicaly adjusted budget balance’ (CAB). Finally, politically negotiated country-specific budgetary one-time and temporary e↵ects (OE

t

) enter the calculation toeventually arrive at the structural budget balance SB :

SBt

= FBt

� ✏t

OGt

�OEt

(1)

2.2 The output gap as a residual of potential output

The output gap is defined as the gap between actual (Y ) and potential output (YP)in percent of potential output, both given at constant prices:

OGt

=Yt

� Y Pt

Y Pt

(2)

The European Commission uses the output gap as an indicator for the positionof an economy in the business cycle: A positive output gap is said to indicate anover-heating economy, a negative output gap signals underutilization of economic

4

structural balance

Kalman-Filtered Solow-Residual

AMECONAIRU == Kalman-Filtered Unemployment Rate

Philipp Heimberger

The inner workings of the potential output model A short introduction

3

and the NAWRU is that the latter is subject to small cyclical spillovers (which, e.g.,are the consequence of wage rigidities or cyclical wage mark-ups; see: Havik et al.(2014), p. 28-30 or EuropeanCommission (2013), p. 85-86). So while the modelincludes two main ’structural’ variables for explaining changes in potential outputover time, it only provides one practical lever to increase potential output when itcomes to questions of economic policy design: here, the clear policy imperative is todecrease labor market regulation and lower social welfare standards, since technol-ogy is conceptualized as completely autonomous and exogenous; as a residual whichonly explains the part of the evolution of the output gap over time which cannot beexplained by deviations of actual unemployment from the NAWRU. 1

3 The European Commission’s production functionapproach to estimating potential output

Non-observable potential output is calculated by means of a production functionapproach: Under the assumptions of constant returns to scale and perfect compe-tition, the relevant components of the labor input, capital stock and total factorproductivity are plugged into a neoclassical Cobb-Douglas production function:

Y POTt

= L↵

t

⇤K1�↵

t

⇤ TFPt

(3)

where Y POTt

is potential output, Lt

is the contribution of the production factorlabour to potential output, K

t

is the contribution of capital to potential output, andTFP

t

is total factor productiviy (all at time t). We are looking at a Cobb-Douglasproduction function, where ↵ and (1 � ↵) are the constant output elasticities oflabour and capital, respectively (Havik et al. (2014), p. 10).

In what follows, we focus on the estimation of the labour component Lt

, becausethis is of central importance for the concept of potential output, as defined by theEuropean Commission.

The contribution of labour to potential output is defined as follows:

Lt

= (POPWt

⇤ PARTSt

⇤ (1�NAWRUt

)) ⇤HOURSTt

(4)

where

POPWt

is population of working age, PARTSt

is the smoothed participation rate,NAWRU

t

is the non-accelerating wage inflation rate of unemployment andHOURSTt

is the trend of average hours worked (all at time t) (Havik et al. (2014), p. 14).PARTS

t

and HOURSTt

are detrended variables; they are calculated by makinguse of the Hodrick-Prescott-Filter (HP filter).2 NAWRU

t

is calculated by meansof a statistical technique called Kalman filter (see below for an introduction to theKalman filter approach).

1Which could well be wrong as technological advances and labor standards might well be correlatedpositively (see: QUELLEN).

2The HP filter is a univariate approach to removing the cyclical component of a time series from the”trend component” (Hodrick and Prescott (1997)). Regarding the basic limitations of the HP filter- with particular emphasis on the so called ”end-point bias -, see, e.g., Kaiser and Maravall (2001).

6

potential output

2 How does the European Commission define andmodel the key concepts: structural budget balance,potential output, output gap and NAWRU

This section introduces the key concepts for estimating structural budget balances.It provides definitions for the most important terms and components of the EuropeanCommission’s model and illuminates their theoretical background.

2.1 The structural budget balance

The basic rationale behind the structural budget balance (SB) is to provide anestimate for EU member states’ fiscal performance, which takes additional economicand political considerations into account to look beyond short term ’headline’ fiscalbalances as reported by individual countries. Specifically, the structural budgetbalance considers cyclical movements in economic activity as well as extraordinaryevents a↵ording extraordinary political e↵orts.

The calculation of the structural budget balance is based on a two step-correctionprocedure, which takes the reported fiscal balance FB - defined as governmentrevenues (R) minus government expenditures (G) relative to nominal GDP (Y )(FB = R

t

�G

t

Y

nom

t

) - as its starting point. The aim of thefirst correction step is to ac-

count for the impact of cyclical fluctuations on fiscal performance by calculating avirtual fiscal balance that would prevail if the economy was operating at potentialoutput(e.g. Angerer (2015)). It is in this context that economic theory and, specifi-cally, the GAP-model of the European Commission comes in to play a decisive role,since the European Commission makes use of the GAP-model’s estimates to adjustreported ’headline’ fiscal balances. In detail, the Commission combines estimateson the di↵erence between ’observed’ and ’potential’ output - labelled the ’outputgap’ (OG

t

) - as produced by the Commission’s GAP-model with an estimate forthe budgetary semi-elasticity (✏

t

) measuring the reaction of the budget balance tothe output gap (provided by the OECD, see: INCLUDE SOURCE PRICE ET AL.2014; Mourre et al. (2014), p. 21). This parameter is used for mapping the estimated’output gap’ onto the dimension of fiscal policy via ✏

t

OGt

to calculate the so-called’cyclicaly adjusted budget balance’ (CAB). Finally, politically negotiated country-specific budgetary one-time and temporary e↵ects (OE

t

) enter the calculation toeventually arrive at the structural budget balance SB :

SBt

= FBt

� ✏t

OGt

�OEt

(1)

2.2 The output gap as a residual of potential output

The output gap is defined as the gap between actual (Y ) and potential output (YP)in percent of potential output, both given at constant prices:

OGt

=Yt

� Y Pt

Y Pt

(2)

The European Commission uses the output gap as an indicator for the positionof an economy in the business cycle: A positive output gap is said to indicate anover-heating economy, a negative output gap signals underutilization of economic

4

structural balance

Kalman-Filtered Solow-Residual

AMECONAIRU == Kalman-Filtered Unemployment Rate

850

900

950

1000

1050

1100

1150

2001 2003 2005 2007 2009 2011 2013 2015

inbillion€(at2

010prices)

ThecaseofSpain:RealGDPandpoten>aloutput

Poten/aloutput

RealGDP

Philipp Heimberger

The inner workings of the potential output model A short introduction

3

and the NAWRU is that the latter is subject to small cyclical spillovers (which, e.g.,are the consequence of wage rigidities or cyclical wage mark-ups; see: Havik et al.(2014), p. 28-30 or EuropeanCommission (2013), p. 85-86). So while the modelincludes two main ’structural’ variables for explaining changes in potential outputover time, it only provides one practical lever to increase potential output when itcomes to questions of economic policy design: here, the clear policy imperative is todecrease labor market regulation and lower social welfare standards, since technol-ogy is conceptualized as completely autonomous and exogenous; as a residual whichonly explains the part of the evolution of the output gap over time which cannot beexplained by deviations of actual unemployment from the NAWRU. 1

3 The European Commission’s production functionapproach to estimating potential output

Non-observable potential output is calculated by means of a production functionapproach: Under the assumptions of constant returns to scale and perfect compe-tition, the relevant components of the labor input, capital stock and total factorproductivity are plugged into a neoclassical Cobb-Douglas production function:

Y POTt

= L↵

t

⇤K1�↵

t

⇤ TFPt

(3)

where Y POTt

is potential output, Lt

is the contribution of the production factorlabour to potential output, K

t

is the contribution of capital to potential output, andTFP

t

is total factor productiviy (all at time t). We are looking at a Cobb-Douglasproduction function, where ↵ and (1 � ↵) are the constant output elasticities oflabour and capital, respectively (Havik et al. (2014), p. 10).

In what follows, we focus on the estimation of the labour component Lt

, becausethis is of central importance for the concept of potential output, as defined by theEuropean Commission.

The contribution of labour to potential output is defined as follows:

Lt

= (POPWt

⇤ PARTSt

⇤ (1�NAWRUt

)) ⇤HOURSTt

(4)

where

POPWt

is population of working age, PARTSt

is the smoothed participation rate,NAWRU

t

is the non-accelerating wage inflation rate of unemployment andHOURSTt

is the trend of average hours worked (all at time t) (Havik et al. (2014), p. 14).PARTS

t

and HOURSTt

are detrended variables; they are calculated by makinguse of the Hodrick-Prescott-Filter (HP filter).2 NAWRU

t

is calculated by meansof a statistical technique called Kalman filter (see below for an introduction to theKalman filter approach).

1Which could well be wrong as technological advances and labor standards might well be correlatedpositively (see: QUELLEN).

2The HP filter is a univariate approach to removing the cyclical component of a time series from the”trend component” (Hodrick and Prescott (1997)). Regarding the basic limitations of the HP filter- with particular emphasis on the so called ”end-point bias -, see, e.g., Kaiser and Maravall (2001).

6

potential output

2 How does the European Commission define andmodel the key concepts: structural budget balance,potential output, output gap and NAWRU

This section introduces the key concepts for estimating structural budget balances.It provides definitions for the most important terms and components of the EuropeanCommission’s model and illuminates their theoretical background.

2.1 The structural budget balance

The basic rationale behind the structural budget balance (SB) is to provide anestimate for EU member states’ fiscal performance, which takes additional economicand political considerations into account to look beyond short term ’headline’ fiscalbalances as reported by individual countries. Specifically, the structural budgetbalance considers cyclical movements in economic activity as well as extraordinaryevents a↵ording extraordinary political e↵orts.

The calculation of the structural budget balance is based on a two step-correctionprocedure, which takes the reported fiscal balance FB - defined as governmentrevenues (R) minus government expenditures (G) relative to nominal GDP (Y )(FB = R

t

�G

t

Y

nom

t

) - as its starting point. The aim of thefirst correction step is to ac-

count for the impact of cyclical fluctuations on fiscal performance by calculating avirtual fiscal balance that would prevail if the economy was operating at potentialoutput(e.g. Angerer (2015)). It is in this context that economic theory and, specifi-cally, the GAP-model of the European Commission comes in to play a decisive role,since the European Commission makes use of the GAP-model’s estimates to adjustreported ’headline’ fiscal balances. In detail, the Commission combines estimateson the di↵erence between ’observed’ and ’potential’ output - labelled the ’outputgap’ (OG

t

) - as produced by the Commission’s GAP-model with an estimate forthe budgetary semi-elasticity (✏

t

) measuring the reaction of the budget balance tothe output gap (provided by the OECD, see: INCLUDE SOURCE PRICE ET AL.2014; Mourre et al. (2014), p. 21). This parameter is used for mapping the estimated’output gap’ onto the dimension of fiscal policy via ✏

t

OGt

to calculate the so-called’cyclicaly adjusted budget balance’ (CAB). Finally, politically negotiated country-specific budgetary one-time and temporary e↵ects (OE

t

) enter the calculation toeventually arrive at the structural budget balance SB :

SBt

= FBt

� ✏t

OGt

�OEt

(1)

2.2 The output gap as a residual of potential output

The output gap is defined as the gap between actual (Y ) and potential output (YP)in percent of potential output, both given at constant prices:

OGt

=Yt

� Y Pt

Y Pt

(2)

The European Commission uses the output gap as an indicator for the positionof an economy in the business cycle: A positive output gap is said to indicate anover-heating economy, a negative output gap signals underutilization of economic

4

structural balance

Stability and Growth Pact and Fiscal Compact

Kalman-Filtered Solow-Residual

AMECONAIRU == Kalman-Filtered Unemployment Rate

850

900

950

1000

1050

1100

1150

2001 2003 2005 2007 2009 2011 2013 2015

inbillion€(at2

010prices)

ThecaseofSpain:RealGDPandpoten>aloutput

Poten/aloutput

RealGDP

Philipp Heimberger

The inner workings of the potential output model A short introduction

3

and the NAWRU is that the latter is subject to small cyclical spillovers (which, e.g.,are the consequence of wage rigidities or cyclical wage mark-ups; see: Havik et al.(2014), p. 28-30 or EuropeanCommission (2013), p. 85-86). So while the modelincludes two main ’structural’ variables for explaining changes in potential outputover time, it only provides one practical lever to increase potential output when itcomes to questions of economic policy design: here, the clear policy imperative is todecrease labor market regulation and lower social welfare standards, since technol-ogy is conceptualized as completely autonomous and exogenous; as a residual whichonly explains the part of the evolution of the output gap over time which cannot beexplained by deviations of actual unemployment from the NAWRU. 1

3 The European Commission’s production functionapproach to estimating potential output

Non-observable potential output is calculated by means of a production functionapproach: Under the assumptions of constant returns to scale and perfect compe-tition, the relevant components of the labor input, capital stock and total factorproductivity are plugged into a neoclassical Cobb-Douglas production function:

Y POTt

= L↵

t

⇤K1�↵

t

⇤ TFPt

(3)

where Y POTt

is potential output, Lt

is the contribution of the production factorlabour to potential output, K

t

is the contribution of capital to potential output, andTFP

t

is total factor productiviy (all at time t). We are looking at a Cobb-Douglasproduction function, where ↵ and (1 � ↵) are the constant output elasticities oflabour and capital, respectively (Havik et al. (2014), p. 10).

In what follows, we focus on the estimation of the labour component Lt

, becausethis is of central importance for the concept of potential output, as defined by theEuropean Commission.

The contribution of labour to potential output is defined as follows:

Lt

= (POPWt

⇤ PARTSt

⇤ (1�NAWRUt

)) ⇤HOURSTt

(4)

where

POPWt

is population of working age, PARTSt

is the smoothed participation rate,NAWRU

t

is the non-accelerating wage inflation rate of unemployment andHOURSTt

is the trend of average hours worked (all at time t) (Havik et al. (2014), p. 14).PARTS

t

and HOURSTt

are detrended variables; they are calculated by makinguse of the Hodrick-Prescott-Filter (HP filter).2 NAWRU

t

is calculated by meansof a statistical technique called Kalman filter (see below for an introduction to theKalman filter approach).

1Which could well be wrong as technological advances and labor standards might well be correlatedpositively (see: QUELLEN).

2The HP filter is a univariate approach to removing the cyclical component of a time series from the”trend component” (Hodrick and Prescott (1997)). Regarding the basic limitations of the HP filter- with particular emphasis on the so called ”end-point bias -, see, e.g., Kaiser and Maravall (2001).

6

potential output

2 How does the European Commission define andmodel the key concepts: structural budget balance,potential output, output gap and NAWRU

This section introduces the key concepts for estimating structural budget balances.It provides definitions for the most important terms and components of the EuropeanCommission’s model and illuminates their theoretical background.

2.1 The structural budget balance

The basic rationale behind the structural budget balance (SB) is to provide anestimate for EU member states’ fiscal performance, which takes additional economicand political considerations into account to look beyond short term ’headline’ fiscalbalances as reported by individual countries. Specifically, the structural budgetbalance considers cyclical movements in economic activity as well as extraordinaryevents a↵ording extraordinary political e↵orts.

The calculation of the structural budget balance is based on a two step-correctionprocedure, which takes the reported fiscal balance FB - defined as governmentrevenues (R) minus government expenditures (G) relative to nominal GDP (Y )(FB = R

t

�G

t

Y

nom

t

) - as its starting point. The aim of thefirst correction step is to ac-

count for the impact of cyclical fluctuations on fiscal performance by calculating avirtual fiscal balance that would prevail if the economy was operating at potentialoutput(e.g. Angerer (2015)). It is in this context that economic theory and, specifi-cally, the GAP-model of the European Commission comes in to play a decisive role,since the European Commission makes use of the GAP-model’s estimates to adjustreported ’headline’ fiscal balances. In detail, the Commission combines estimateson the di↵erence between ’observed’ and ’potential’ output - labelled the ’outputgap’ (OG

t

) - as produced by the Commission’s GAP-model with an estimate forthe budgetary semi-elasticity (✏

t

) measuring the reaction of the budget balance tothe output gap (provided by the OECD, see: INCLUDE SOURCE PRICE ET AL.2014; Mourre et al. (2014), p. 21). This parameter is used for mapping the estimated’output gap’ onto the dimension of fiscal policy via ✏

t

OGt

to calculate the so-called’cyclicaly adjusted budget balance’ (CAB). Finally, politically negotiated country-specific budgetary one-time and temporary e↵ects (OE

t

) enter the calculation toeventually arrive at the structural budget balance SB :

SBt

= FBt

� ✏t

OGt

�OEt

(1)

2.2 The output gap as a residual of potential output

The output gap is defined as the gap between actual (Y ) and potential output (YP)in percent of potential output, both given at constant prices:

OGt

=Yt

� Y Pt

Y Pt

(2)

The European Commission uses the output gap as an indicator for the positionof an economy in the business cycle: A positive output gap is said to indicate anover-heating economy, a negative output gap signals underutilization of economic

4

structural balance

Stability and Growth Pact and Fiscal Compact

if YPOT > Y (negative output gap) → more fiscal leeway if YPOT < Y (positive output gap)→ less fiscal leeway

Kalman-Filtered Solow-Residual

AMECONAIRU == Kalman-Filtered Unemployment Rate

850

900

950

1000

1050

1100

1150

2001 2003 2005 2007 2009 2011 2013 2015

inbillion€(at2

010prices)

ThecaseofSpain:RealGDPandpoten>aloutput

Poten/aloutput

RealGDP

Philipp Heimberger

The inner workings of the potential output model A short introduction

3

and the NAWRU is that the latter is subject to small cyclical spillovers (which, e.g.,are the consequence of wage rigidities or cyclical wage mark-ups; see: Havik et al.(2014), p. 28-30 or EuropeanCommission (2013), p. 85-86). So while the modelincludes two main ’structural’ variables for explaining changes in potential outputover time, it only provides one practical lever to increase potential output when itcomes to questions of economic policy design: here, the clear policy imperative is todecrease labor market regulation and lower social welfare standards, since technol-ogy is conceptualized as completely autonomous and exogenous; as a residual whichonly explains the part of the evolution of the output gap over time which cannot beexplained by deviations of actual unemployment from the NAWRU. 1

3 The European Commission’s production functionapproach to estimating potential output

Non-observable potential output is calculated by means of a production functionapproach: Under the assumptions of constant returns to scale and perfect compe-tition, the relevant components of the labor input, capital stock and total factorproductivity are plugged into a neoclassical Cobb-Douglas production function:

Y POTt

= L↵

t

⇤K1�↵

t

⇤ TFPt

(3)

where Y POTt

is potential output, Lt

is the contribution of the production factorlabour to potential output, K

t

is the contribution of capital to potential output, andTFP

t

is total factor productiviy (all at time t). We are looking at a Cobb-Douglasproduction function, where ↵ and (1 � ↵) are the constant output elasticities oflabour and capital, respectively (Havik et al. (2014), p. 10).

In what follows, we focus on the estimation of the labour component Lt

, becausethis is of central importance for the concept of potential output, as defined by theEuropean Commission.

The contribution of labour to potential output is defined as follows:

Lt

= (POPWt

⇤ PARTSt

⇤ (1�NAWRUt

)) ⇤HOURSTt

(4)

where

POPWt

is population of working age, PARTSt

is the smoothed participation rate,NAWRU

t

is the non-accelerating wage inflation rate of unemployment andHOURSTt

is the trend of average hours worked (all at time t) (Havik et al. (2014), p. 14).PARTS

t

and HOURSTt

are detrended variables; they are calculated by makinguse of the Hodrick-Prescott-Filter (HP filter).2 NAWRU

t

is calculated by meansof a statistical technique called Kalman filter (see below for an introduction to theKalman filter approach).

1Which could well be wrong as technological advances and labor standards might well be correlatedpositively (see: QUELLEN).

2The HP filter is a univariate approach to removing the cyclical component of a time series from the”trend component” (Hodrick and Prescott (1997)). Regarding the basic limitations of the HP filter- with particular emphasis on the so called ”end-point bias -, see, e.g., Kaiser and Maravall (2001).

6

potential output

2 How does the European Commission define andmodel the key concepts: structural budget balance,potential output, output gap and NAWRU

This section introduces the key concepts for estimating structural budget balances.It provides definitions for the most important terms and components of the EuropeanCommission’s model and illuminates their theoretical background.

2.1 The structural budget balance

The basic rationale behind the structural budget balance (SB) is to provide anestimate for EU member states’ fiscal performance, which takes additional economicand political considerations into account to look beyond short term ’headline’ fiscalbalances as reported by individual countries. Specifically, the structural budgetbalance considers cyclical movements in economic activity as well as extraordinaryevents a↵ording extraordinary political e↵orts.

The calculation of the structural budget balance is based on a two step-correctionprocedure, which takes the reported fiscal balance FB - defined as governmentrevenues (R) minus government expenditures (G) relative to nominal GDP (Y )(FB = R

t

�G

t

Y

nom

t

) - as its starting point. The aim of thefirst correction step is to ac-

count for the impact of cyclical fluctuations on fiscal performance by calculating avirtual fiscal balance that would prevail if the economy was operating at potentialoutput(e.g. Angerer (2015)). It is in this context that economic theory and, specifi-cally, the GAP-model of the European Commission comes in to play a decisive role,since the European Commission makes use of the GAP-model’s estimates to adjustreported ’headline’ fiscal balances. In detail, the Commission combines estimateson the di↵erence between ’observed’ and ’potential’ output - labelled the ’outputgap’ (OG

t

) - as produced by the Commission’s GAP-model with an estimate forthe budgetary semi-elasticity (✏

t

) measuring the reaction of the budget balance tothe output gap (provided by the OECD, see: INCLUDE SOURCE PRICE ET AL.2014; Mourre et al. (2014), p. 21). This parameter is used for mapping the estimated’output gap’ onto the dimension of fiscal policy via ✏

t

OGt

to calculate the so-called’cyclicaly adjusted budget balance’ (CAB). Finally, politically negotiated country-specific budgetary one-time and temporary e↵ects (OE

t

) enter the calculation toeventually arrive at the structural budget balance SB :

SBt

= FBt

� ✏t

OGt

�OEt

(1)

2.2 The output gap as a residual of potential output

The output gap is defined as the gap between actual (Y ) and potential output (YP)in percent of potential output, both given at constant prices:

OGt

=Yt

� Y Pt

Y Pt

(2)

The European Commission uses the output gap as an indicator for the positionof an economy in the business cycle: A positive output gap is said to indicate anover-heating economy, a negative output gap signals underutilization of economic

4

structural balance

Stability and Growth Pact and Fiscal Compact

if YPOT > Y (negative output gap) → more fiscal leeway if YPOT < Y (positive output gap)→ less fiscal leeway

Kalman-Filtered Solow-Residual

AMECONAIRU == Kalman-Filtered Unemployment Rate

850

900

950

1000

1050

1100

1150

2001 2003 2005 2007 2009 2011 2013 2015

inbillion€(at2

010prices)

ThecaseofSpain:RealGDPandpoten>aloutput

Poten/aloutput

RealGDP

Data: AMECO (Spring 2016)

Philipp Heimberger

Downward revisions of potential output during the crisis

4

Philipp Heimberger

Downward revisions of potential output during the crisis

4

750

800

850

900

950

1000

1050

1100

2000 2002 2004 2006 2008 2010 2012 2014 2016

inbillion€(at2

005prices)

Poten5aloutputrevisions,Spain

Spring2005

Autumn2007

Spring2010

Autumn2013

Philipp Heimberger

Downward revisions of potential output during the crisis

4

750

800

850

900

950

1000

1050

1100

2000 2002 2004 2006 2008 2010 2012 2014 2016

inbillion€(at2

005prices)

Poten5aloutputrevisions,Spain

Spring2005

Autumn2007

Spring2010

Autumn2013

Philipp Heimberger

The performativity of potential output: Theoretical Background

5

Philipp Heimberger

The performativity of potential output: Theoretical Background

5

Out

put

Debt

Expansion Compression

Panic

Consolidation

Philipp Heimberger

The performativity of potential output: Theoretical Background

5

Post-Keynesian macroeconomics (“Minsky-Veblen Cycles“)

Out

put

Debt

Expansion Compression

Panic

Consolidation

Philipp Heimberger

The performativity of potential output: Theoretical Background

5

Post-Keynesian macroeconomics (“Minsky-Veblen Cycles“)

Out

put

Debt

Expansion Compression

Panic

Consolidation

heterodox trade theory: path-dependency (“the rich get richer and the poor get poorer“)

Philipp Heimberger

The performativity of potential output: Theoretical Background

5

Post-Keynesian macroeconomics (“Minsky-Veblen Cycles“)

Out

put

Debt

Expansion Compression

Panic

Consolidation

heterodox trade theory: path-dependency (“the rich get richer and the poor get poorer“)

Philipp Heimberger

The performativity of potential output: Theoretical Background

5

Post-Keynesian macroeconomics (“Minsky-Veblen Cycles“)

Out

put

Debt

Expansion Compression

Panic

Consolidation

heterodox trade theory: path-dependency (“the rich get richer and the poor get poorer“)

complexity economics (“vector-like representations of complex system dynamics“)

Philipp Heimberger

Recent economic developments in Europe A rough theoretical view on European economies

6

Macro(global tendencies)

Meso(continental level)

Micro(nation states)

Philipp Heimberger

Recent economic developments in Europe A rough theoretical view on European economies

6

Macro(global tendencies)

Meso(continental level)

Micro(nation states)

Increase in inequality

Financial deregulation

Philipp Heimberger

Recent economic developments in Europe A rough theoretical view on European economies

6

Macro(global tendencies)

Meso(continental level)

Micro(nation states)

Increase in inequality

Financial deregulation

Decrease in demand

Key

nes

Philipp Heimberger

Recent economic developments in Europe A rough theoretical view on European economies

6

Macro(global tendencies)

Meso(continental level)

Micro(nation states)

Increase in inequality

Financial deregulation

Decrease in demand

Key

nes

Bubbles inhousing / financial

markets

Veblen

Minsky

Philipp Heimberger

Recent economic developments in Europe A rough theoretical view on European economies

6

Macro(global tendencies)

Meso(continental level)

Micro(nation states)

Increase in inequality

Financial deregulation

and / or

Debt-led private sectorexpansion

Expansionary fiscalpolicy

Expandingvia the export side

Decrease in demand

Key

nes

Bubbles inhousing / financial

markets

Veblen

Minsky

Philipp Heimberger

Recent economic developments in Europe A rough theoretical view on European economies

6

Macro(global tendencies)

Meso(continental level)

Micro(nation states)

Increase in inequality

Financial deregulation

and / or

Debt-led private sectorexpansion

Expansionary fiscalpolicy

Expandingvia the export side

Decrease in demand

Key

nes

+Bubbles in

housing / financialmarkets

Veblen

Minsky

Philipp Heimberger

Recent economic developments in Europe A rough theoretical view on European economies

6

Macro(global tendencies)

Meso(continental level)

Micro(nation states)

Increase in inequality

Financial deregulation

and / or

Debt-led private sectorexpansion

Expansionary fiscalpolicy

Expandingvia the export side

Decrease in demand

Key

nes

+Bubbles in

housing / financialmarkets

Veblen

Minsky

Philipp Heimberger

Recent economic developments in Europe A rough theoretical view on European economies

6

Macro(global tendencies)

Meso(continental level)

Micro(nation states)

Increase in inequality

Financial deregulation

and / or

Debt-led private sectorexpansion

Expansionary fiscalpolicy

Expandingvia the export side

Decrease in demand

Key

nes

+Bubbles in

housing / financialmarkets

Veblen

Minsky

Current accountimbalances

Deficit countries Surplus countries

Structural polarization

Philipp Heimberger

Recent economic developments in Europe A rough theoretical view on European economies

6

Macro(global tendencies)

Meso(continental level)

Micro(nation states)

Increase in inequality

Financial deregulation

and / or

Debt-led private sectorexpansion

Expansionary fiscalpolicy

Expandingvia the export side

Decrease in demand

Key

nes

+Bubbles in

housing / financialmarkets

Veblen

Minsky

Current accountimbalances

Deficit countries Surplus countries

Structural polarization

Financial crisis

Philipp Heimberger

Recent economic developments in Europe A rough theoretical view on European economies

6

Macro(global tendencies)

Meso(continental level)

Micro(nation states)

Increase in inequality

Financial deregulation

and / or

Debt-led private sectorexpansion

Expansionary fiscalpolicy

Expandingvia the export side

Decrease in demand

Key

nes

+Bubbles in

housing / financialmarkets

Veblen

Minsky

Current accountimbalances

Deficit countries Surplus countries

Structural polarization

Financial crisis

kills viability of one strategy: change in trajectory

Philipp Heimberger

Recent economic developments in Europe A rough theoretical view on European economies

6

Macro(global tendencies)

Meso(continental level)

Micro(nation states)

Increase in inequality

Financial deregulation

and / or

Debt-led private sectorexpansion

Expansionary fiscalpolicy

Expandingvia the export side

Decrease in demand

Key

nes

+Bubbles in

housing / financialmarkets

Veblen

Minsky

Current accountimbalances

Deficit countries Surplus countries

Structural polarization

Financial crisis

kills viability of one strategy: change in trajectory

reinforces polarization

Philipp Heimberger

The impact of the PO-Model before the crisis

7

Increase in inequalityMacro

(global tendencies)

Meso(continental level)

Micro(nation states)

Decrease in demand

Financial deregulation

and / or

Debt-led private sectorexpansion

Expansionary fiscalpolicy

Expandingvia the export side

Bubbles inhousing / financial

markets Current accountimbalances

Deficit countries Surplus countries

Key

nes Veblen

Minsky

Structural polarization

PO Model &NAIRU-Estimates

Philipp Heimberger

The impact of the PO-Model before the crisis

7

Increase in inequalityMacro

(global tendencies)

Meso(continental level)

Micro(nation states)

Decrease in demand

Financial deregulation

and / or

Debt-led private sectorexpansion

Expansionary fiscalpolicy

Expandingvia the export side

Bubbles inhousing / financial

markets Current accountimbalances

Deficit countries Surplus countries

Key

nes Veblen

Minsky

Structural polarization

PO Model &NAIRU-Estimates

Philipp Heimberger

The impact of the PO-Model before the crisis

7

Increase in inequalityMacro

(global tendencies)

Meso(continental level)

Micro(nation states)

Decrease in demand

Financial deregulation

and / or

Debt-led private sectorexpansion

Expansionary fiscalpolicy

Expandingvia the export side

Bubbles inhousing / financial

markets Current accountimbalances

Deficit countries Surplus countries

Key

nes Veblen

Minsky

Structural polarization

PO Model &NAIRU-Estimates

Philipp Heimberger

The impact of the PO-Model before the crisis

7

Increase in inequalityMacro

(global tendencies)

Meso(continental level)

Micro(nation states)

Decrease in demand

Financial deregulation

and / or

Debt-led private sectorexpansion

Expansionary fiscalpolicy

Expandingvia the export side

Bubbles inhousing / financial

markets Current accountimbalances

Deficit countries Surplus countries

Key

nes Veblen

Minsky

Structural polarization

PO Model &NAIRU-Estimates

+

Philipp Heimberger

The impact of the PO-Model after the crisis

8

Increase in inequalityMacro

(global tendencies)

Meso(continental level)

Micro(nation states)

Decrease in demand

Financial deregulation

and / or

Debt-led private sectorexpansion

Expansionary fiscalpolicy

Expandingvia the export side

Bubbles inhousing / financial

markets Current accountimbalances

Deficit countries Surplus countries

Key

nes Veblen

Minsky

Structural polarization

Financial crisis

PO Model &NAIRU-Estimates

Philipp Heimberger

The impact of the PO-Model after the crisis

8

Increase in inequalityMacro

(global tendencies)

Meso(continental level)

Micro(nation states)

Decrease in demand

Financial deregulation

and / or

Debt-led private sectorexpansion

Expansionary fiscalpolicy

Expandingvia the export side

Bubbles inhousing / financial

markets Current accountimbalances

Deficit countries Surplus countries

Key

nes Veblen

Minsky

Structural polarization

Financial crisis

PO Model &NAIRU-Estimates

some are ‘winners’ some are ‘losers’

Philipp Heimberger

The impact of the PO-Model after the crisis

8

Increase in inequalityMacro

(global tendencies)

Meso(continental level)

Micro(nation states)

Decrease in demand

Financial deregulation

and / or

Debt-led private sectorexpansion

Expansionary fiscalpolicy

Expandingvia the export side

Bubbles inhousing / financial

markets Current accountimbalances

Deficit countries Surplus countries

Key

nes Veblen

Minsky

Structural polarization

Financial crisis

PO Model &NAIRU-Estimates

some are ‘winners’ some are ‘losers’

Philipp Heimberger

The impact of the PO-Model after the crisis

8

Increase in inequalityMacro

(global tendencies)

Meso(continental level)

Micro(nation states)

Decrease in demand

Financial deregulation

and / or

Debt-led private sectorexpansion

Expansionary fiscalpolicy

Expandingvia the export side

Bubbles inhousing / financial

markets Current accountimbalances

Deficit countries Surplus countries

Key

nes Veblen

Minsky

Structural polarization

Financial crisis

PO Model &NAIRU-Estimates

some are ‘winners’ some are ‘losers’

Philipp Heimberger

The impact of the PO-Model after the crisis

8

Increase in inequalityMacro

(global tendencies)

Meso(continental level)

Micro(nation states)

Decrease in demand

Financial deregulation

and / or

Debt-led private sectorexpansion

Expansionary fiscalpolicy

Expandingvia the export side

Bubbles inhousing / financial

markets Current accountimbalances

Deficit countries Surplus countries

Key

nes Veblen

Minsky

Structural polarization

Financial crisis

PO Model &NAIRU-Estimates

some are ‘winners’ some are ‘losers’

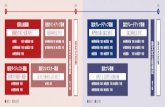

+

Philipp Heimberger

Performativity I: The pro-cyclicality of the PO-model The example of Spain

9

Philipp Heimberger

Debt and NAIRU: Typical trajectories and the role of the crisis

10

Data:OECD(privatesectordebtin%ofGDP),AMECO(November2015);authors’calculations.Totaldebt(y-axis)isthesumofprivatesectorandpublicsectordebtin%ofGDP.

Philipp Heimberger

Performativity II: Path dependency and the PO model

11

Philipp Heimberger

Performativity II: Path dependency and the PO model

11

successively less fiscal leeway

Philipp Heimberger

Performativity II: Path dependency and the PO model

11

successively less fiscal leeway

successively greater fiscal leeway

Philipp Heimberger

Performativity II: Path dependency and the PO model

11

successively less fiscal leeway

more fiscal leeway in boom,

less fiscal leeway in crisis

successively greater fiscal leeway

Philipp Heimberger

Performativity II: Path dependency and the PO model

12

Philipp Heimberger

Performativity II: Path dependency and the PO model

12

highly financialized countries

Philipp Heimberger

Performativity II: Path dependency and the PO model

12

highly financialized countries

path of hope

Philipp Heimberger

Performativity II: Path dependency and the PO model

12

highly financialized countries

path of hope

valley of d

espair

Philipp Heimberger

Summary

• Potential output model mimics and reinforces divisions in ‘winners’ and

‘losers’ within the euro area.

• The model promotes an inversion of the traditional ‘anti-cyclical’ use of

fiscal policy to one that amplifies booms and busts.

• The transmission of the model’s outcomes into economic policy-making

reinforces path-dependent developments across European economies.

• Restrictions in fiscal policy leeway have been most severe in those

countries that would need it the most

• “Experts’ cage” for confining democratic policy-making, which

underscores the relevance of macroeconomic models for politics in

general.

13

Philipp Heimberger

Outlook: A possible future research venue

• An idea: Drop the PO model as a reference point and increase the weight

assigned to heterodox trade theory

• Less focus on the assessing the ‘structural budget balance’ by means of estimating the

output gap, but rather on structural development paths.

• Analyze and discuss the sectoral composition and export structure of different

economies.

14

Philipp Heimberger

Backup I: Cyclical factors and NAIRU estimates

15

y = −0.79x + 14.82T−value (HAC−robust) = −16.04 (***)

R_sq = 0.96

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

20102011

2012

2013

2014

13

15

17

19

−4 −2 0 2HBOOM 1999−2014

NAI

RU 1

999−

2014

HBOOM and NAIRU in Spain

y = −0.93x + 8.38T−value (HAC−robust) = −7.36 (***)

R_sq = 0.55

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

20092010

2011

2012

2013

2014

5

10

−2.5 0.0 2.5HBOOM 1999−2014

NAI

RU 1

999−

2014

HBOOM and NAIRU in Ireland

y = −1.48x + 9.07T−value (HAC−robust) = −4.29 (***)

R_sq = 0.62

1999

2000

2001

2002

2003

20042005

2006

2007

2008

2009

20102011

2012

2013

2014

8

9

10

−0.5 0.0 0.5HBOOM 1999−2014

NAI

RU 1

999−

2014

HBOOM and NAIRU in Italy

y = −0.65x + 9.13T−value (HAC−robust) = −4.72 (***)

R_sq = 0.78

1999

2000

20012002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

4.0

4.5

5.0

6.4 6.8 7.2 7.6ACCU 1999−2014

NAI

RU 1

999−

2014

ACCU and NAIRU in Austria

y = −0.66x + 9.52T−value (HAC−robust) = −2.60 (**)

R_sq = 0.52

1999

2000

200120022003

2004

20052006

2007

20082009

2010

2011

2012

2013

2014

3.5

4.0

4.5

5.0

5.5

6.0

6.5 7.0 7.5 8.0 8.5ACCU 1999−2014

NAI

RU 1

999−

2014

ACCU and NAIRU in Netherlands

y = −0.59x + 13.80T−value (HAC−robust) = −3.72 (***)

R_sq = 0.70

1999

2000

20012002

2003

2004

2005

2006

2007

2008

2009

20102011

2012

2013

2014

9.00

9.25

9.50

9.75

7.2 7.6 8.0ACCU 1999−2014

NAI

RU 1

999−

2014

ACCU and NAIRU in France

Philipp Heimberger

Backup II: Kalman filter recursions for the EC’s NAIRU model

16

where �Nt

is equal to Nt

� Nt�1; �⌘

t

is equal to ⌘t

� ⌘t�1; and where all shocks

are normally distributed white noises. From the first and second equation on thedynamics of the unobserved components, we can see that the trend component ofthe unemployment rate is modeled as a second-order random walk.11 And the lastequation means that the unemployment gap (G

t

) is assumed to be a second-orderauto-regressive process (AR(2)).

8 The NAWRU model in state space form

Before the Kalman filter approach can be used to obtain estimates of the NAWRU,the European Commission’s NAWRU model from the subsection above has to bewritten in state space form.

The observation equation is:

ut

�rulct

�=

1 0 1 00 0 �1 �2

�2

664

Nt

⌘t

Gt

Gt�1

3

775+

0

V rulc

t

�(11)

where the observation vector consists of the actual unemployment rate (ut

) andthe growth rate of real unit labour costs (�rulc

t

); the state vector’s elements arethe NAWRU, modelled as the trend component of the unemployment rate (N

t

), theGaussian noise process which characterizes the evolution of the unemployment trendcomponent (⌘

t

; correct description ???), the unemployment gap (Gt

) and the laggedunemployment gap (G

t�1). The matrix Zt

in the observation equation includes theregression coe�cient of the unemployment gap (-�1) and of the lagged unemploy-ment gap (�2) from the Phillips curve relation.12 V rulc

t

indicates that there is ameasurement error in the data on the growth rate in real unit labour costs.13

11In general, a second-order random walk can be written as:

yt = yt1 + vt

= yt1 + vt1 + ✏t

= 2yt1yt2 + ✏t

The GAP programme would also allow the trend component of the unemployment rate to bemodeled as a first-order random walk or as a damped trend.

12How does the European Commission estimate the values for -�1 and �2? On this, see section 12.13In practice, Zt might change with each measurement or time step, but in the European Commission’s

approach it is assumed to be constant. Note also that ”the Phillips curve can alternatively beformulated with more lags and other exogenous variables (in particular, labour productivity growth�yl). Also, uncertainty as to whether wage setters are targeting consumer price inflation or the GDPdeflator can be addressed by adding a terms of trade (tot) indicator)”. (Havik et al. (2014), p. 16)

Including one exogenous regressor would change the observation equation to:

13

And the state equation is given by:2

664

Nt+1

⌘t+1

Gt+1

Gt

3

775 =

2

664

1 1 0 00 1 0 00 0 �1 �2

0 0 1 0

3

775

2

664

Nt

⌘t

Gt

Gt�1

3

775+

2

664

V N

t

V ⌘

t

V G

t

0

3

775 (12)

where the state vector has the same elements as in the observation equation; thetransition matrix T

t

includes the autoregressive coe�cients �1 and �2, which we getfrom modeling the unemployment gap as an AR(2) process (see section 7); and V N

t

,V ⌘

t

, V G

t

are the process error variances related to the NAWRU (Nt

), the Gaussiannoise process which characterizes the evolution of the NAWRU (⌘

t

; correct descrip-tion???) and the unemployment gap (G

t

), respectively. These variances are thediagonal elements of the process noise covariance matrix Q

t

.14

9 Kalman filter equations

The true state ↵t

of the system modeled by the European Commission in order toestimate the unobserved components (and thereby find values for the NAWRU) isunknown. The Kalman filter15 provides an algorithm to finding state estimates ↵

t

,which is based on the following equations, called the Kalman filter recursions, whichhave to be run forwards (starting from t = 1) in a loop for each time step

t

16

vt

= yt

� Zt

↵t

Ft

= Zt

Pt

ZT

t

+Ht

Kt

= Tt

Pt

ZT

t

F�1t

Lt

= Tt

�Kt

Zt

↵t|t = ↵

t

+ Pt

ZT

t

F�1t

vt

Pt|t = P

t

� Pt

ZT

t

F�1t

Zt

Pt

↵t+1 = T

t

↵t

+Kt

vt

Pt+1 = T

t

Pt

(Tt

�Kt

Zt

)T +Rt

Qt

RT

t

(13)

ut

�rulct

�=

1 0 1 00 0 �1 �2

�2

664

Nt

⌘tGt

Gt�1

3

775+

0 0c �1

� 1Z1t

�+

0

V rulct

�

where Z1t is the exogenous variable, c is a constant (the intercept???) and �1 is the regressioncoe�cient of the exogenous variable.

14See section 12 on how to estimate the elements of Qt and the values for �1 and �2. In practice, theprocess noise covariance matrix Qt and measurement noise covariance matrix Ht might change witheach observation or time step; however, in the European Commission’s approach they are assumedto be constant.

15The filter is named after Rudolph Kalman, who made a major contribution to developing the under-lying theory in a seminal paper (Kalman (1960)).

16see (Durbin and Koopman (2012), p. 85)

14

first: run recursions to obtain parameter values (numerical MaxLikelihood) second: run filter with parameters to calculate N(AIRU) third: smooth obtained values by rerunning the filter

Philipp Heimberger

Backup III

17

Philipp Heimberger

Backup IV: Downward revisions in PO and structural budget balances

18

Philipp Heimberger

Backup V: Spain and the PO model in pre-crisis years

19

Philipp Heimberger

Backup VI: Correlation of actual and potential output losses

20

Philipp Heimberger

Backup VII: The case of Spain

21

Philipp Heimberger

Backup VIII: The pro-cyclicality of the EC’s NAIRU estimates

22

7

9

11

13

15

17

19

21

23

25

27

1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

in%

NAIRUes,matesandunemploymentrateinSpain

Autumn2007

Spring2015

Actualunemploymentrate