The mobile data challenge - Economist Intelligence...

17

The mobile data challenge A report from the Economist Intelligence Unit Sponsored by InnoPath

-

Upload

hoangkhanh -

Category

Documents

-

view

217 -

download

0

Transcript of The mobile data challenge - Economist Intelligence...

The mobile data challenge A report from the Economist Intelligence UnitSponsored by InnoPath

© Economist Intelligence Unit Limited 20101

The mobile data challenge

Preface 2

Introduction 3

A focus on content and applications 5

Effi ciency is paramount 7

Keeping the customer satisfi ed 9

Conclusion 10

Appendix: Survey results 11

Contents

© Economist Intelligence Unit Limited 2010

The mobile data challenge

2

Preface

The mobile data challenge is an Economist Intelligence Unit research paper, sponsored by InnoPath. The Economist Intelligence Unit’s editorial team executed the survey and wrote the report. The fi ndings and views expressed in the report do not necessarily refl ect the views of the sponsor.

Iain Morris was the author of the report and Katherine Dorr Abreu was the editor. Mike Kenny was responsible for layout and design. Our thanks go to all survey respondents for their time and insight.

February 2010

© Economist Intelligence Unit Limited 20103

The mobile data challenge

Introduction

Sceptics have long doubted whether mobile data services can deliver big, new profi ts for service providers. There is no question that revenue from global mobile telecommunications is expanding,

thanks to the adoption of mobile data services worldwide. Yet many providers are still unsure whether data services will help them to increase profi ts signifi cantly. In the absence of fresh thinking, service providers are focusing on cutting costs. But this is unlikely to be suffi cient to maintain profi ts, let alone increase profi t margins.

In a survey of mobile-phone operators conducted by the Economist Intelligence Unit and sponsored by InnoPath, only a minority (44%) of respondents say that growth in revenue from mobile data services will make up for a decline in their company’s revenue from voice services over the next fi ve years. Twenty-four percent expect data services merely to offset a decline in their mainstream voice business, while another 25% say overall revenue will decline despite the rapid growth of data services.

Increasing revenue from these services is hard enough. Actually boosting profi ts from data services will entail major changes by mobile-phone operators in areas such as content and application development, pricing strategy and network development. It is also likely to require further improvements in effi ciency, identifi cation of new revenue sources and an even sharper focus on the customer.

Data Voice Data as % of total

Data* spurs mobile revenue growth worldwide

0

100

200

300

400

500

600

700

800

2005 2006 2007 2008 2009e 2010e 2011e 2012e 2013e 2014e

Global mobile telecoms services revenues(US$bn)

Data as % of total

* Data revenue includes messaging. e Estimate. Data source: Pyramid Research.

0

5

10

15

20

25

30

35

40

© Economist Intelligence Unit Limited 2010

The mobile data challenge

4

Who took the survey?

A total of 197 executives in the mobile communications industry took part in the survey. They are based worldwide: 30% in the Asia-Pacifi c region, 28% in North America, 26% in Western Europe, and the remaining 16% in Latin America, the Middle East and Africa, and Eastern Europe.

They represent a wide range of company size: 30% are in companies with annual revenue of US$500m or less, 14% with revenue of US$500m to US$1bn, 18% from US$1bn to US$5bn, and 38% with revenue of US$5bn or more. Their companies offer a wide variety of product lines, both consumer and business, wireless and wireline.

The panel is very senior: 43% hold C-suite or equivalent positions, another 24% are senior vice-presidents, directors or heads of business units, and the remaining 33% are other managers. Respondents carry out a range of functional roles, including marketing and sales (41%), strategy and development (37%), and general management (27%).

All companies offer wireless services, but provide other services as wellWhich of the following product lines does your organisation offer?(% respondents)

Source: Economist Intelligence Unit survey, December 2009.

Wireless data

Wireless voice

Business internet (T1, T2, etc)

Voice over IP (VoIP)

Landline telephony

Residential internet (eg, dial-up, ISDN, cable modem)

In-home entertainment (TV, movies, etc)

88

85

63

57

52

48

30

© Economist Intelligence Unit Limited 20105

The mobile data challenge

Perhaps the biggest transformation facing mobile operators relates to the development of content and software applications for phone users. Some 47% of survey respondents say this is an area on which

they will focus their efforts in the next fi ve years.

But it will be tough to make money from content and applications. Inconsistencies in the survey fi ndings suggest that operators’ strategies in this area are in their infancy.

Most mobile-phone operators are investing heavily in next-generation networks rather than developing and selling mobile-phone applications. Fully 60% of respondents say their companies are building next-generation networks—third- or fourth-generation (3G or 4G) systems—mostly to meet customer demand for new services. Mobile TV and gaming require 4G networks for optimal operation, yet these services rank low in the survey as potential revenue drivers over the next fi ve years. Simple web browsing, e-mail and messaging, and social media (such as Twitter) are the services most likely to spur revenue growth in this period, according to the survey. But these services are already in widespread use, and typically available for free (apart from the connection fee). Furthermore, they can be delivered to customers quite satisfactorily using 3G networks, which have already been deployed by most operators in developed countries.

How, then, will next-generation networks benefi t operators? Respondents seem to think that the

A focus on content and applications

Meeting the threat of commoditisation with revenue-generating content and appsOver the next five years, in which areas do you think your company will focus its efforts? Select up to three. My organisation will focus on:(% respondents)

Source: Economist Intelligence Unit survey, December 2009.

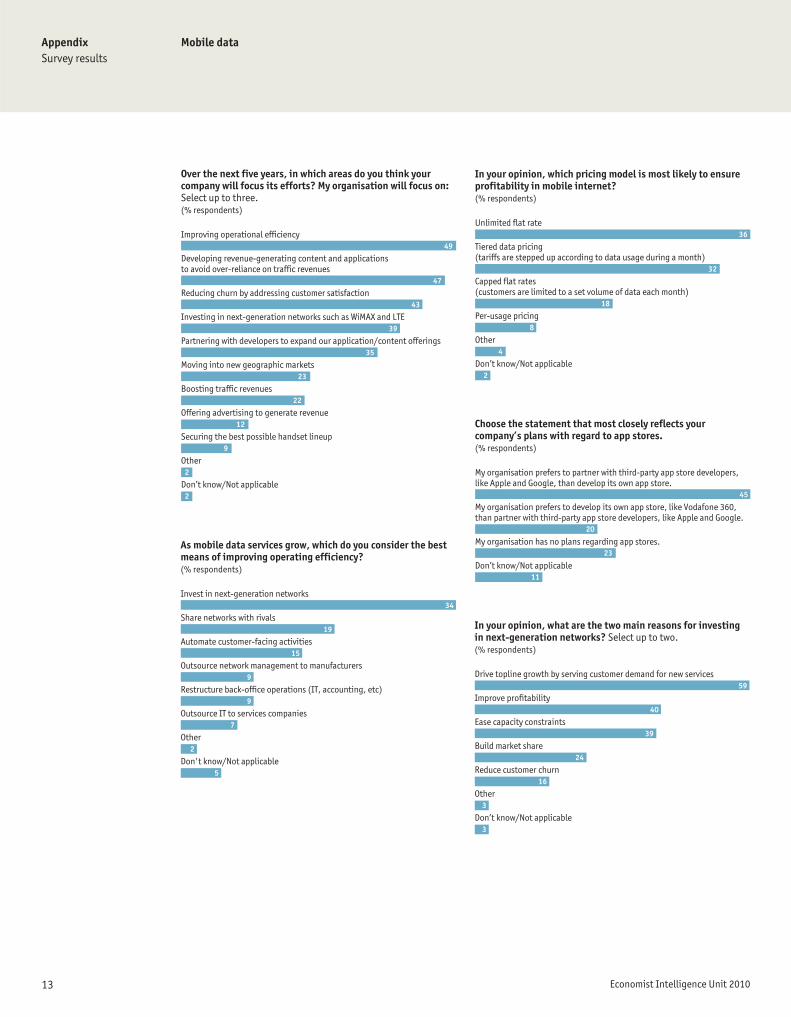

Improving operational efficiency

Developing revenue-generating content and applications to avoid over-reliance on traffic revenue

Reducing churn by addressing customer satisfaction

Investing in next-generation networks such as WiMAX and LTE

Partnering with developers to expand our application/content offerings

49

47

43

39

35

© Economist Intelligence Unit Limited 2010

The mobile data challenge

6

development of enhanced browsing, messaging and social media services will enable them to sell advertisements and thus generate profi ts. More than 60% of respondents say that advertising will become an important source of revenue in the next fi ve years.

Operators must also decide how to deal with the challenge of fi rms such as Google and Apple in the development of content and applications. Forty percent of survey respondents say competition from such “non-traditional rivals” is a signifi cant problem facing operators. In the past, operators tried countering this threat by preventing customers from visiting certain third-party sites—creating a “walled garden”. But with few compelling services of their own, operators alienated their customers.

Some 72% of respondents agree that operators adopting an open-network policy will be more successful than those that do not. Only 32% say that legislation supporting the principle of “net neutrality” (which could outlaw the walled garden) would hamper their ability to invest in advanced networks. The risk is that an open-network policy leaves operators with an even weaker presence in the content and applications market than they currently claim.

For all their eagerness to offer more content and applications, few respondents show an interest in setting up online applications stores (so-called app stores). Despite the recent high-profi le opening of stores by two operators, Vodafone and France Telecom, some two-thirds of respondents with a strategy in this area prefer to partner with app store developers such as Apple rather than go it alone. Twenty-three percent of all respondents say they have no app store strategy. The apparent lack of enthusiasm could leave operators sidelined in the content and applications market and missing out on a revenue opportunity.

69

31

My organisation prefers to partner with third-party app store developers

My organisation prefers to develop its own app store

Source: Economist Intelligence Unit survey, December 2009.

Operators with an app store plan prefer to partnerChoose the statement that most closely reflects your company’s plans with regard to app stores.(% of respondents who said their companies have plans regarding app stores)

© Economist Intelligence Unit Limited 20107

The mobile data challenge

Operators responding to the survey are more confi dent when it comes to improvements in effi ciency. Faced with diffi culties in generating increased revenue and with the need for some costly

investments, 49% of respondents say they plan to focus on boosting operational effi ciency over the next fi ve years. Building next-generation networks is the best way for operators to do so, according to 34% of respondents.

Next-generation networks might help operators to expand their margins by providing new capacity for

high-bandwidth services. Operators are offering fl at-rate tariffs, which allow customers unlimited usage of data services. This has prompted a surge in mobile data traffi c, exerting a heavy burden on existing 3G networks. More effi cient 4G infrastructure can ease the strain.

Some 37% of survey respondents believe that fl at-rate pricing is the most likely way to ensure profi tability, probably because consumers have tended to be wary about signing contracts based on per-usage pricing. US-based AT&T has experienced heavy demand on its network from Apple’s iPhone, but the carrier has so far resisted the introduction of per-usage pricing because it fears that such a move would deter customers.

Effi ciency is paramount

Next-generation networks considered the key to operational efficiencyAs mobile data services grow, which do you consider the best means of improving operating efficiency?(% respondents)

Source: Economist Intelligence Unit survey, December 2009.

Invest in next-generation networks

Share networks with rivals

Automate customer-facing activities

Outsource network management to manufacturers

Restructure back-office operations (IT, accounting, etc)

Outsource IT to services companies

34

19

15

9

9

7

© Economist Intelligence Unit Limited 2010

The mobile data challenge

8

In recent interviews, however, senior AT&T executives have expressed doubts that fl at-rate tariffs are sustainable. In our survey, some 59% of respondents think per-usage pricing is more likely to ensure the profi tability of mobile data services. Firms can charge per megabyte consumed, impose a megabyte ceiling on usage or introduce tiered pricing, whereby customers are given a specifi c allocation of megabytes per month for a fl at fee (paying more for a bigger allocation).

For all the interest in building next-generation networks, the high cost of new infrastructure is a serious concern. Investments in 3G were largely responsible for the 28.5% increase in annual spending by China’s operators in 2009, for example. Iliad, France’s newly licensed 3G operator, reckons that it will have to spend €1bn on network construction over the next 18 months—roughly equivalent to its revenue in the fi rst half of 2009.

Forty-fi ve percent of respondents say cost is one of the most pressing problems that operators face over the next fi ve years. This will put further pressure on operators to fi nd ways to cut costs. Ending the subsidies on expensive handsets, for example, would help to restore margins, but this seems unlikely. Fifty-nine percent of respondents say that the policy has helped them to attract and retain customers who generate higher service revenue.

Usage based (59)

Tiered data pricing (33)

Capped flat rates (18)

Per-usage pricing (8)

Unlimited flat rate (37)

Other (4)

Source: Economist Intelligence Unit survey, December 2009.

Usage-based pricing can help ensure profitabilityIn your opinion, which pricing model is most likely to ensure profitability in mobile internet?(% respondents)

© Economist Intelligence Unit Limited 20109

The mobile data challenge

One way of lowering costs would be to focus on retaining customers. Some 66% of respondents say they already do this, while 43% say reducing “churn”—the customer turnover rate—is one of their

focus areas for the next fi ve years. Automating customer-related activities can also help to reduce costs, according to 15% of respondents.

Despite the emphasis on customer retention, however, respondents say that reducing the rate of

turnover comes low on the list of priorities. This probably refl ects their self-confi dence: 71% say they outperform their peers with regard to customer perception of products and services, and 60% say they do better than their competitors in terms of customer service. Only 20% say they underperform their peers with regard to churn.

Keeping the customer satisfi ed

Companies are focusing on customer retention to safeguard profitabilityDo you agree or disagree with the following statement? My company is focusing on customer retention as a primary means of safeguarding the bottom line.(% respondents)

Source: Economist Intelligence Unit survey, December 2009.

Agree

Disagree

66

12

0 20 40 60 80 100

Outperform About the same Underperform

Customer perception of products and services

Prices

Innovative products and services

Service reliability

Network reach

Quality of network

Customer service

Churn (customer turnover rate)

Operators are confident of their competitive positioningCompared with your competitors, how well does your organisation perform with respect to the following criteria? (% respondents)

Source: Economist Intelligence Unit survey, December 2009.

65 23 12

49 38 13

61 29 10

71 22 7

62 24 13

71 22 7

60 28 12

51 29 20

© Economist Intelligence Unit Limited 2010

The mobile data challenge

10

Despite the doubts about the profi t potential of data services, operators are transforming themselves into data-service providers to compensate for a continual decline in their voice revenue. They are

investing in next-generation networks both to meet customer demand for new applications and content and to improve their effi ciency in delivering these services. Yet the survey suggests that operators can further improve their performance.

l If operators want to be more than just “dumb pipes”, they need to come up with a clear strategy for the development of new revenue-generating content and mobile applications. Given the growing importance of app stores, it is surprising that 23% of respondents have no strategy in this area. Moreover, the data services in which respondents expressed most interest are already in widespread use, and typically generate nothing in revenue apart from connection fees.

l Improving operational effi ciency, cited by 49% of survey respondents as a central focus over the next fi ve years, cannot come about solely as a result of investments in next-generation networks. Given the cost and time needed to build them, operators will have to develop other ways to enhance effi ciency, such as sharing of networks or automation of processes.

l Keeping customers is less costly than attracting new ones, and so reducing the churn rate by improving customer satisfaction must be a part of any effi ciency-enhancing strategy.

Conclusion

11 Economist Intelligence Unit 2010

AppendixSurvey results

Mobile data

Appendix: Survey resultsPercentages may not add to 100% due to rounding or the ability of respondents to choose multiple responses.

Wireless data

Wireless voice

Business internet (T1, T2, etc)

Voice over IP (VoIP)

Landline telephony

Residential internet (eg, dial-up, ISDN, cable modem)

In-home entertainment (TV, movies, etc)

Other

Which of the following product lines does your organisation offer? Select all that apply.(% respondents)

88

85

63

57

52

48

30

14

Mobile data revenue will drive new topline growth

Mobile data revenue will compensate for stagnating voice markets and keep revenues stable

While growth of mobile data revenue will be impressive, it will not be sufficient to prevent a decline in revenue as voice markets stagnate

Don’t know/Not applicable

In your opinion, what will be the impact of mobile data on your organisation’s revenues in the next five years?(% respondents)

44

24

25

8

0 20 40 60 80 100

1 Significantly outperform 2 3 4 5 Significantly underperform Don’t know

Margins

Customer perception of products and services

Prices

Innovative products and services

Service reliability

Network reach

Quality of network

Customer service

Churn (eg, customer turnover rate)

Compared with your competitors, how well does your organisation perform with respect to the following criteria? For each criteria, rate on a scale of 1 to 5, where 1=Significantly outperform and 5=Significantly underperform.(% respondents)

18 39 25 11 3 5

17 47 22 10 2 2

15 33 38 11 3 1

25 35 28 7 3 2

26 44 22 6 1 2

30 29 23 11 2 4

30 37 21 5 2 5

24 36 27 9 4 1

14 35 28 14 5 5

12 Economist Intelligence Unit 2010

AppendixSurvey results

Mobile data

0 20 40 60 80 100

1 Strongly agree 2 3 4 5 Strongly disagree Don’t know

Advertising will be an important source of revenue for mobile service providers in the next five years

App stores, such as Vodafone 360 or Apple's iPhone app store, will be an important source of revenue for mobile service providers in the next five years

Smartphones that use an open-source operating system, such as Google Android or LiMo, will become more popular than devices using proprietary software, such as the Apple iPhone or RIM Blackberry

The practice of subsidising expensive devices erodes profitability in the short term but will ultimately pay off by helping retain customers who generate higher service revenues

My company is focusing on customer retention as a primary means of safeguarding the bottom line

Third-party VoIP providers will be less of a competitive threat to operators once next-generation networks are deployed

Operators that adopt an open network approach that allows users to access all Web content and services are most likely to be successful in the future

Legislation supporting the principle of “net neutrality” will hamper my organisation's ability to invest in its network

Do you agree or disagree with the following statements? For each statement, rate on a scale of 1 to 5, where 1=Strongly agree and 5=Strongly disagree.(% respondents)

30 30 22 12 4 2

26 30 23 13 3 5

22 33 24 13 6 3

18 40 22 11 7 2

32 35 19 9 4 3

17 29 24 16 6 7

30 42 16 8 2 2

15 17 36 14 8 10

The cost of deploying state-of-the art networks

Competition from non-traditional service providers such as Skype and Google

The commoditisation of telecoms services

Competition from traditional service providers

Slowing demand growth as a result of market saturation

The need to provide seamless service across several technology platforms

The impact of government policy and regulation

Uncertainty about which technologies will prevail (such as WiMAX, LTE [Long term Evolution] or others)

Customer churn

A shortage of qualified workers

Other

Don’t know/Not applicable

In the next five years, what do you think will be the most pressing problems faced by mobile operators in the country in which you reside? Select up to three.(% respondents)

45

40

37

28

28

26

26

22

19

12

2

1

Web browsing

Email and messaging

Social media

Business applications

Location-based and mapping services

Mobile TV

Legacy or traditional voice services

Music

VoIP

Gaming

Other

Don’t know/Not applicable

Which services will be the most important drivers of revenues in mobile telecoms services in the next five years? Select up to three.(% respondents)

49

47

42

34

28

26

18

15

13

12

4

1

13 Economist Intelligence Unit 2010

AppendixSurvey results

Mobile data

Improving operational efficiency

Developing revenue-generating content and applications to avoid over-reliance on traffic revenues

Reducing churn by addressing customer satisfaction

Investing in next-generation networks such as WiMAX and LTE

Partnering with developers to expand our application/content offerings

Moving into new geographic markets

Boosting traffic revenues

Offering advertising to generate revenue

Securing the best possible handset lineup

Other

Don’t know/Not applicable

Over the next five years, in which areas do you think your company will focus its efforts? My organisation will focus on:Select up to three. (% respondents)

49

47

43

39

35

23

22

12

9

2

2

Invest in next-generation networks

Share networks with rivals

Automate customer-facing activities

Outsource network management to manufacturers

Restructure back-office operations (IT, accounting, etc)

Outsource IT to services companies

Other

Don't know/Not applicable

As mobile data services grow, which do you consider the best means of improving operating efficiency?(% respondents)

34

19

15

9

9

7

2

5

Unlimited flat rate

Tiered data pricing (tariffs are stepped up according to data usage during a month)

Capped flat rates (customers are limited to a set volume of data each month)

Per-usage pricing

Other

Don’t know/Not applicable

In your opinion, which pricing model is most likely to ensure profitability in mobile internet?(% respondents)

36

32

18

8

4

2

My organisation prefers to partner with third-party app store developers, like Apple and Google, than develop its own app store.

My organisation prefers to develop its own app store, like Vodafone 360, than partner with third-party app store developers, like Apple and Google.

My organisation has no plans regarding app stores.

Don’t know/Not applicable

Choose the statement that most closely reflects your company’s plans with regard to app stores.(% respondents)

45

20

23

11

Drive topline growth by serving customer demand for new services

Improve profitability

Ease capacity constraints

Build market share

Reduce customer churn

Other

Don’t know/Not applicable

In your opinion, what are the two main reasons for investing in next-generation networks? Select up to two.(% respondents)

59

40

39

24

16

3

3

14 Economist Intelligence Unit 2010

AppendixSurvey results

Mobile data

United States of America

India

United Kingdom

Malaysia

Brazil, Finland, Singapore, Spain, Australia, Nigeria, Pakistan, Sweden

Canada, Germany, Bangladesh, Denmark, Ireland

Czech Republic, Italy, Luxembourg, Mauritius, Mexico, Portugal,South Africa, Switzerland, Argentina, Austria, Bolivia, Cyprus, Egypt,Estonia, Ghana, Greece, Hong Kong, Indonesia, Malta, Netherlands,New Zealand, Oman, Philippines, Qatar, Romania, Slovakia, Sri Lanka,Thailand, Ukraine, United Arab Emirates, Uzbekistan, Venezuela

In which country are you personally located?(% respondents)

26

13

6

4

3

2

1

Asia-Pacific

North America

Western Europe

Latin America

Middle East and Africa

Eastern Europe

In which region are you personally based?(% respondents)

30

28

26

7

6

3

30

14

18

13

24

$500m or less

$500m to $1bn

$1bn to $5bn

$5bn to $10bn

$10bn or more

What are your organisation’s global annual revenues in US dollars? (% respondents)

Board member

CEO/President/Managing director

CFO/Treasurer/Comptroller

CIO/Technology director

Other C-level executive

SVP/VP/Director

Head of business unit

Head of department

Manager

Other

Which of the following best describes your job title?(% respondents)

5

17

2

7

13

16

8

10

18

5

Marketing and sales

Strategy and business development

General management

Operations and production

Customer service

IT

Finance

R&D

Information and research

Human resources

Supply-chain management

Procurement

Legal

Risk

Other

What are your main functional roles? Please choose no more than three functions.(% respondents)

41

37

27

17

14

13

12

12

7

4

2

2

1

1

6

Whilst every effort has been taken to verify the accuracy of this information, neither The Economist Intelligence Unit Ltd. nor the sponsors of this report can accept any responsibility or liability for reliance by any person on this white paper or any of the information, opinions or conclusions set out in the white paper. Co

ver i

mag

e: S

hutt

erst

ock

LONDON26 Red Lion SquareLondon WC1R 4HQUnited KingdomTel: (44.20) 7576 8000Fax: (44.20) 7576 8476E-mail: [email protected]

NEW YORK111 West 57th StreetNew York NY 10019United StatesTel: (1.212) 554 0600Fax: (1.212) 586 1181/2E-mail: [email protected]

HONG KONG6001, Central Plaza18 Harbour RoadWanchai Hong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]