The Malta UCITS Investment Funds - Building a better...

68

The Malta UCITS Investment Funds A technical guide June 2016

Transcript of The Malta UCITS Investment Funds - Building a better...

The Malta UCITSInvestment FundsA technical guideJune 2016

It is my great pleasure to welcome you to our 2016 edition of “The Malta UCITS Investment Funds — A technical guide.”

The UCITS brand is a renowned pan-European investment product which is principally designed for the retail market given itsprescriptive requirements introduced through the UCITS directive. The brand also enables easier access in different EU countries on the basis of single authorization from one EU Member State. While having its inherent benefits, the UCITS brand is still evolving to meet the changing investment landscape. In the past, the UCITS has broadened the spectrum of eligible assets and introduced the “marketing passporting” regime amongst others. Now the EU is seeking to improve governance requirements through theimplementation of “UCITS V” directive.

Under the UCITS directive, UCITS funds are freely marketable across the EU. Furthermore, investors recognize and demand “UCITS brand” products, mainly because they are EU regulated. In Malta, these investment funds offer flexibility and tax efficient solutions, as will be explained in this guide.

The local industry continues to enjoy the commitments of the local Government as well as the Malta Financial Services Authority which strive to preserve a leading regulatory and legislative regime that is attractive to foreign business whilst maintaining investor protection. The implementation of the regulatory agenda continues unabated, with much focus and discussion on depositary reform, remuneration policies and practices, the future of money market funds, extension of the UCITS directive Passport to non-EU domiciled products and managers, and the likely impact of MiFID II all being in the headlines.

The purpose of this practical guide is to provide, in a clear and concise format, an overview of the UCITS directive. I hope you findthis guide useful.

Our Asset Management Advisory team looks forward to your feedback and in supporting you over the coming years so that we may collectively realize the many opportunities offered by thisindustry.

Ronald AttardCountry Managing PartnerErnst & Young Limited +356 2134 2134 [email protected]

Fore

wor

d

| The Malta UCITS Investment Funds

s0102030405060708091011121314

Forward

In this report

Professional Investor Funds

Requirements of a PIF

Setting up and running a PIF

Investment Restrictions

Key service providers

Authorisation

Salient features of PIFs

Distribution of PIF products

PIF structures

Fund information and reporting obligations

Admissibility for Listing

Taxation

How can we help you?

Glossary

Malta’s key success factors

01 UCITS funds

02 Requirements of a UCITS

03Investment restrictions04Key service providers05Internally managed UCITS06Authorization07

Marketing08Risk management09Key investor information document10Mergers of UCITS and redomiciliation11Specific types of UCITS structures12Fund information and reporting obligations13Admissibility for listing14

Setting up and running a UCITS

2

4

6

8

10

12

16

22

24

28

32

36

40

44

46

UCITS V15 48

Taxation16 52

How can we help?17 54

Glossary18 56

Annexes19 57

2 | The Malta UCITS Investment Funds

• The Maltese workforce provides Malta with a competitive edge through a high-quality labor force at competitive rates. A key attraction of the Maltese labor force is its language skills and its advanced level of education.

• Financial services are an attractive career proposition for well-trained, highly motivated graduates and support personnel. Training in this sector is provided through institutions such as the University of Malta, Institute of Financial Services, the Malta Institute of Accountants, the Malta Institute of Management and renowned European Institutions.

Highly skilledlabor force

• Given Malta’s membership in the EU, legislation is reflective of EU legislation and directives. Therefore, further to having a legislative structure that facilitates the conduct of business in or from Malta, it provides foreign investors in Malta with the assurance of the quality and consistency synonymous with the EU.

• As an EU member state, businesses in Malta can passport their services to all other member states while the growing markets of North Africa and the Middle Eastern countries bordering the southern coast of the Mediterranean basin are easily accessible.

• The Government is continually striving to simplify bureaucracy and shorten decision- making times.

Businessfriendlylegislativeframework

Soundregulatoryframeworkand accessibleregulator

• Malta’s legislation is in line with EU law and built on best practices from other finance centres. All financial services fall under one regulator, the Malta Financial Services Authority (MFSA). Companies benefit from streamlined procedures, reduced bureaucracy and lower regulatory fees.

• The MFSA is signatory to almost 30 Memoranda of Understanding with foreign regulators in order to provide a smooth trading environment for the financial services sector. One of Malta’s most appreciated advantages is the accessibility of the regulator, which establishes constructive working relationships with companies investing in Malta.

• Malta consistently scores high on the stability stakes, and its regulatory framework is also deemed to be particularly strong.

Malta’s key successfactors

The Malta UCITS Investment Funds | 3

Small, activestock exchange

• Full member of International Organization of Securities Commissions (IOSCO) and the World Federation of Exchanges (WFE); following Malta’s accession to the EU, the Malta Stock Exchange, together with the exchanges of the other accession countries, was granted the status of full member of the Federation of European Securities Exchanges (FESE). Major sectors of the Maltese economy are represented on the lists of the Malta Stock Exchange.

• Since being set up in 1992, almost €3b worth of capital has been raised on the market for the private sector through the issue of corporate bonds and equity while a further €15b worth of Government of Malta stocks and Treasury Bills have been issued and fully taken up. Investor base of over 75,000 individual investors, which is a significant number given Malta’s economic size and population. The focus of the Malta Stock Exchange is mostly domestic.

Cost competitiveenvironment

• Competitive labor costs, rental rates and general expenses compared to mainland Europe. Companies in Malta can benefit from an extensive network of double taxation treaties as well as from a number of business promotional incentives.

• Malta has excellent communication links with regular flights to main international airports as well as fully digitalized national telephone network. Malta boasts a truly modern infrastructure with one of the highest broadband access rates in the EU.

• International connectivity is ensured by two satellite stations and four submarine fiber-optic links to mainland Europe. A wide range of quality office and industrial space with commercial office space in purposely built developments or stand-alone blocks readily available at affordable prices.

Infrastructure

4 | The Malta UCITS Investment Funds

1 Directive 2009/65/EC of the European Parliament and of the Council of 13 July 2009 on the coordination of laws, regulations and administrative provisions relating to undertakings for collective investment in transferable securities (UCITS)

1.2 An investment fund adapted to any type of investment fund product

UCITS are subject to prescriptive restrictions on the type of eligible assets they may invest in, however this does not preclude UCITS from adopting different investment fund structures:

• Traditional funds: • Equity • Fixed income • Mixed• Money market funds (see Section 12.2)• Exchange traded fund (ETFs) (see Section 12.3)• Index-tracking funds (see Section 12.4)• Multiple-asset class UCITS: UCITS with multiple of sub-funds/ compartments investing in different asset classes (see Section 3.2)

1.1 The UCITS directive in brief

The Undertaking in Collective Investment Scheme (UCITS) brand is a pan-European regulated branded investment fund which is designed for the retail investor market.

• A regulated EU structure under the UCITS directive1

• Suitable for retail investors• Prescriptive diversification and leverage rules (see Section 4)• Single fund or multi-fund structure, combining different investment strategies or asset classes in different sub-funds (see Section 3.2)• Possibility of internally managed (self-managed) UCITS (see Section 6)• Availability of marketing passporting of UCITS to all EU member states (see Section 8)

EY supports asset managers and investment fund houses through the choice of investmentfund vehicle, the analysis of target markets,the definition of an efficient operating model and distribution strategy, and the selection of service providers.

01 UCITS funds

The Malta UCITS Investment Funds | 5

6 | The Malta UCITS Investment Funds

2.2 Implications under the UCITS directive

The UCITS directive, which regulations are transposedin the Act and constituent rules and regulations, provides a harmonized regulatory framework amongthe EU Member States for the regulation and supervision of investment funds (excluding Alternative Investment Funds). It specifies the core features of such type of investment funds as being risk diversified, prescriptive target assets, continuous subscription and redemptions, regular valuations and oversight by a depositary.

In terms of the UCITS directive the following undertakings shall not be considered as UCITS:

• Investment funds of a closed-ended type• Investment funds which raise capital without promoting the sale of their units to the public within the Community or any part of it• Units of investment funds which, under its fund rules or the instruments of incorporation, may be sold only to the public in third countries • Investment funds prescribed by the regulations of the Member State in which such investment fund is established, for which the rules laid down in the UCITS directive are inappropriate in view of their investment and borrowing policies

2.1 Investment services act

The Maltese Investment Services Act (the Act) provides the statutory basis for regulating investmentfunds constituted in or from Malta.2 UCITS are a special class of investment funds which fall within the provisions of the Act.

The primary objective of a UCITS must be the collective investment of capital acquired by means of an offer of units for subscription, sale or exchange and which has the following characteristics:

• The investment fund or arrangement operates according to the principle of risk spreading and either• The contributions of the participants and the profits or income out of which payments are to be made to them are pooled Or• At the request of the holders, units are or are to be re-purchased or redeemed out of the assets of the investment fund or arrangement, continuously or in blocks at short intervals Or• Units are, or have been, or will be issued continuously or in blocks at short intervals

Every licenced UCITS is subject to standard licence conditions which are set out in full in the investments services rules for retail collectiveinvestment schemes.

2 Investment Services Act, 1994

02 Requirements of a UCITS

The Malta UCITS Investment Funds | 7

2.3 The investment services rules for UCITS

Every license for a UCITS is subject to standard licenseconditions which are set out in full in the Investment Services rules for Retail Collective Investment Schemes issued by the Malta Financial Services Authority (MFSA). The Investment Services rules(the rules) describe the basic principles to whichlicense holders must adhere in the provision of investment services or in the operation of an investment fund. In certain circumstances, the standard requirements can be tailored to meet specific circumstances. The rules also include the necessary forms to be completed by applicants for an investmentfund license.

8 | The Malta UCITS Investment Funds

the UCITS. They are not deemed to be a separate legal entity since they are established through a contractual obligation and can be licensed as a multi-fund or multi-class UCITS. A contractual fund may set up one or more special purpose vehicle, which would be a company and through which the UCITS may gain access to double taxation treaties.

3.1.3 Unit trusts

UCITS can also be constituted by a trust deed between a management company and a trustee. They are governed by the Trusts and Trustees Act7 which Actenables both residents and non-residents to set up various trust structures such as constructive trusts,discretionary trusts, fixed interests trust and purposetrust. Trustees operating in Malta must be approvedby the MFSA whilst trusts established in foreignjurisdictions may be recognized in Malta and it istherefore possible to set up an investment fund as a foreign law trust.

3.1.4 Limited partnerships

Limited Partnerships benefit from a similar legislativeframework to the one offered to SICAVs and may beconstituted as multi-class partnerships or as multi-fundpartnerships and the capital of the partnership can bedivided into shares.

3.1 UCITS structures

A UCITS can be structured as an investment company (SICAV), a contractual fund, unit trust or as a limited partnership.

3.1.1 Investment company

UCITS may be set up as limited liability companies andmay be established as open-ended investmentcompanies (SICAVs).

A SICAV3 may be formed as a public or private company with variable share capital and is governedby the Companies Act4 . A private company is restricted to the extent to which it can transfer sharesand is prohibited from issuing any invitation to the public to subscribe to any of the shares or debenturesof the company whilst a public company may offer itsshares or debentures to the public. SICAVs allow forthe introduction of additional investors without havingto wait for the liquidation of an existing investor. In anopen-ended UCITS, the value of a share reflects the Net Asset Value of the investment fund. SICAVs canbe formed as Incorporated Cell Companies, in terms of the Companies Act5 having each incorporated cellwithin an incorporated cell company as a limited liability company endowed with its own legalpersonality.

SICAVs can operate as a multi-fund structure, whereby the share capital may be divided into different classes of shares, with each class of shares representing a distinct sub-fund of the UCITS.

3.1.2 Contractual funds

Contractual funds are governed by the Investment Services Act6 established by means of a deed of constitution entered into for such purpose by the UCITS Management Company and the depositary of

3 Investment Companies with Variable Share Capital4 Companies Act (Chapter 386 of the Laws of Malta)5 Companies Act (SICAV Incorporated Cell Companies) Regulations, 2010

6 Investment Services Act (Contractual Funds) Regulaions, 20117 Trust and Trustees Act (Chapter 331 of the Laws of Malta)

EY supports asset managers and investmentfund houses through the creation of an investment fund structure that meets the regulatory requirements and tax specifications.

03 Setting up and running a UCITS

The Malta UCITS Investment Funds | 9

Partnerships must have a registered office in Maltawhere they keep the personal information of all limited partners.

In addition, a limited partnership requires generalpartners who are fully liable and both partners canbe limited liability companies formed in any jurisdiction. Limited partnerships are governed bythe Companies Act.8

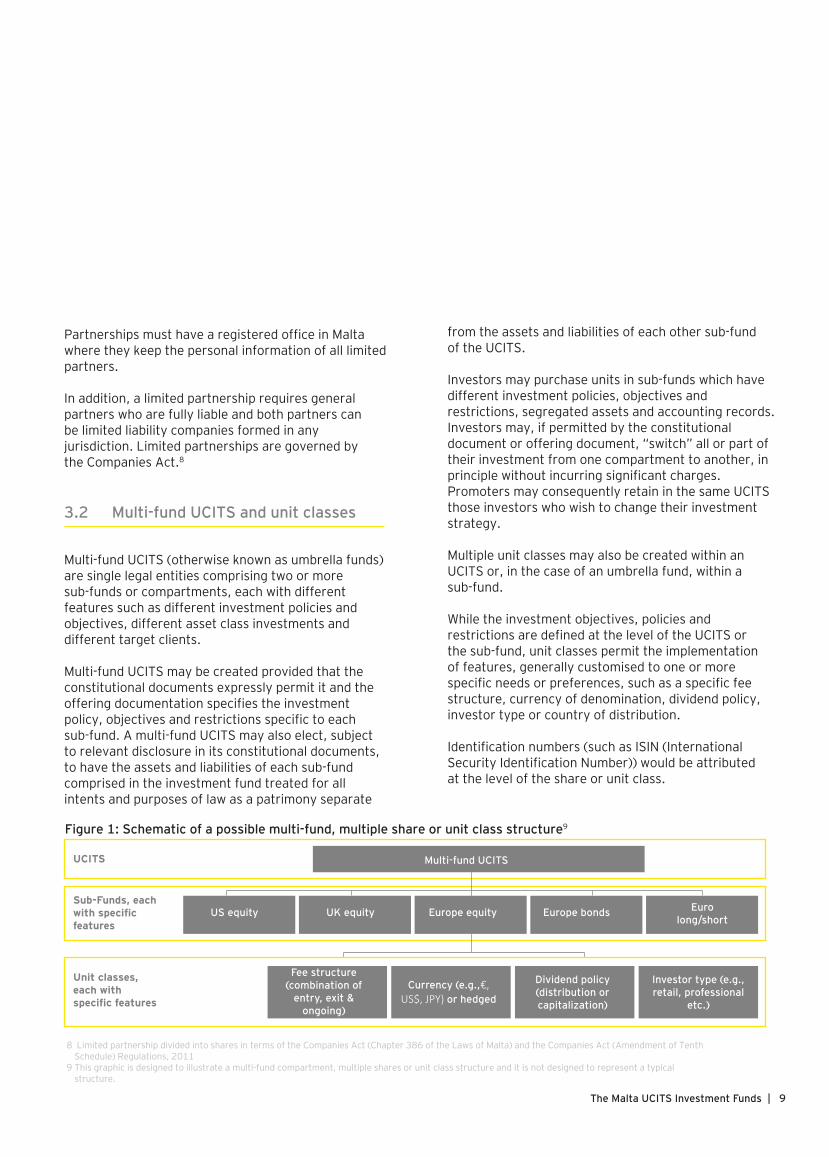

3.2 Multi-fund UCITS and unit classes

Multi-fund UCITS (otherwise known as umbrella funds)are single legal entities comprising two or more sub-funds or compartments, each with differentfeatures such as different investment policies andobjectives, different asset class investments and different target clients.

Multi-fund UCITS may be created provided that the constitutional documents expressly permit it and theoffering documentation specifies the investment policy, objectives and restrictions specific to each sub-fund. A multi-fund UCITS may also elect, subject to relevant disclosure in its constitutional documents, to have the assets and liabilities of each sub-fund comprised in the investment fund treated for all intents and purposes of law as a patrimony separate

from the assets and liabilities of each other sub-fund of the UCITS.

Investors may purchase units in sub-funds which havedifferent investment policies, objectives and restrictions, segregated assets and accounting records. Investors may, if permitted by the constitutional document or offering document, “switch” all or part oftheir investment from one compartment to another, inprinciple without incurring significant charges. Promoters may consequently retain in the same UCITSthose investors who wish to change their investment strategy.

Multiple unit classes may also be created within an UCITS or, in the case of an umbrella fund, within a sub-fund.

While the investment objectives, policies and restrictions are defined at the level of the UCITS or the sub-fund, unit classes permit the implementation of features, generally customised to one or more specific needs or preferences, such as a specific fee structure, currency of denomination, dividend policy, investor type or country of distribution.

Identification numbers (such as ISIN (International Security Identification Number)) would be attributedat the level of the share or unit class.

Figure 1: Schematic of a possible multi-fund, multiple share or unit class structure9

US equity UK equity Europe bonds Eurolong/short

Fee structure(combination of

entry, exit &ongoing)

Currency (e.g.,€,US$, JPY) or hedged

Dividend policy(distribution orcapitalization)

Investor type (e.g.,retail, professional

etc.)

Sub-Funds, each with specificfeatures

Unit classes, each withspecific features

8 Limited partnership divided into shares in terms of the Companies Act (Chapter 386 of the Laws of Malta) and the Companies Act (Amendment of Tenth Schedule) Regulations, 20119 This graphic is designed to illustrate a multi-fund compartment, multiple shares or unit class structure and it is not designed to represent a typical structure.

UCITS Multi-fund UCITS

Europe equity

4.1 Investment restrictions

The UCITS directive contains prescriptive provisions on assets which are eligible for investment by UCITS and detailed investment and borrowing rules.

The rules on investment and borrowing applicable toUCITS are principally derived from the UCITS IV directive. The European Securities and Markets Authority (ESMA) had also issued two sets of additional guidelines to clarify certain aspects related to the eligibility of assets:

• Guidelines concerning eligible assets for investment by UCITS of March 2007 (amended September 2008)• Guidelines concerning eligible assets for investment by UCITS: The classification of hedge fund indices as financial indices issued in July 2008

4.2 UCITS permissible investment instruments

In this section we introduce the concept of “core” and“non-core” eligible assets applicable to UCITS. It then outlines the investment and borrowing rules which can be classified as follows:

• “Core” and “non-core” eligible assets • Diversification requirements• Borrowing restrictions

4.2.1 Core and non-core eligible assets

A UCITS must invest in “eligible assets” and for this purpose may be classified as “core” and “non-core”.“Core” and “non-core” eligible assets are not terms used in the UCITS directive.

10 | The Malta UCITS Investment Funds

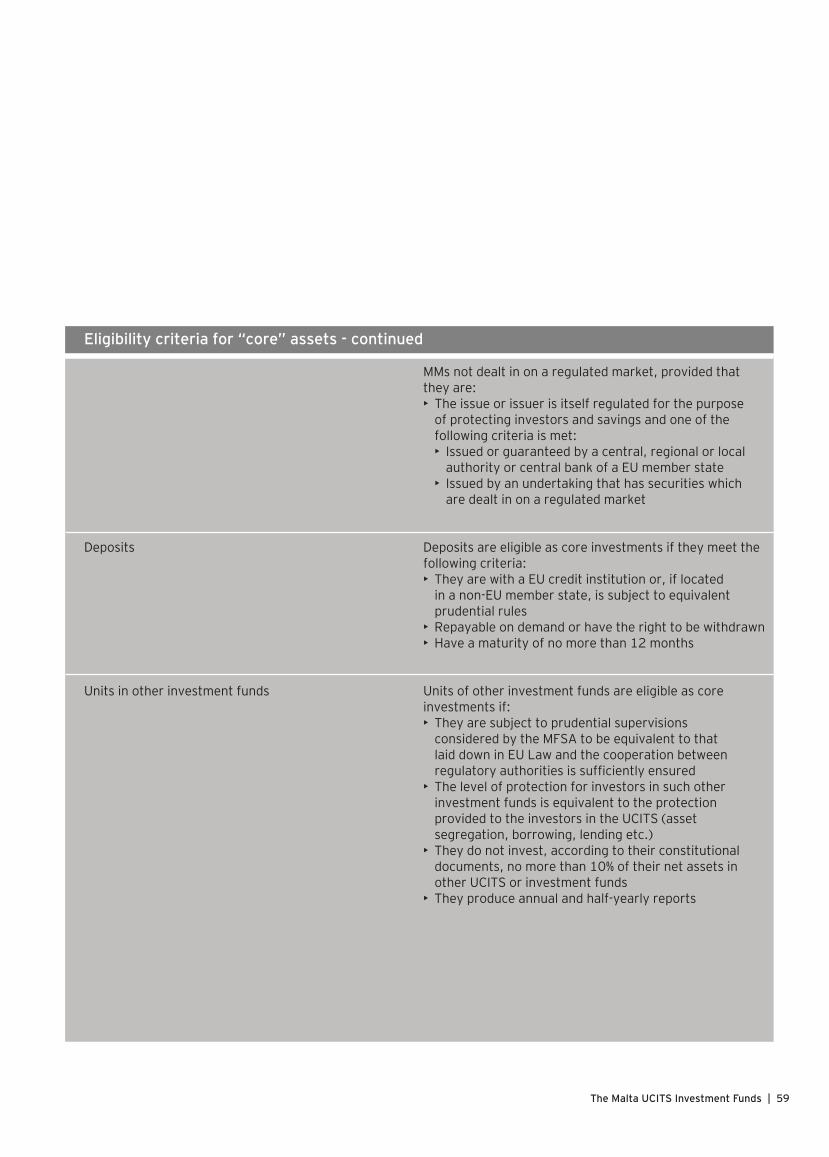

Core eligible assets include the following:

• Transferable securities listed or dealt in on a regulated market, including: • Structured financial instruments (SFI) • Transferable securities or money market instruments embedding derivatives • Recently issued securities or money market instruments• Money market instruments (MMIs)• Deposits• Units in other investment funds• Financial derivative instruments (FDI) including FDIs on financial indices• Ancillary assets, including: • Movable or immovable property required for the operations of the UCITS • Ancillary liquid assets

EY supports asset managers and investment houses through the structure and choice ofthe optimum investment fund structure coherent with the relevant investment objectives, policies and restrictions requirements.

04 Investment restrictions

The Malta UCITS Investment Funds | 11

Annex 1 provides a high level overview of the eligibility criteria of core assets for investment byUCITS. Non-core assets refer to those assets eligible for the “trash ratio” exemption. The applicabilitythereof is reliant on ESMA’s opinion on the interpretation of the “trash ratio” issued in November 2012.

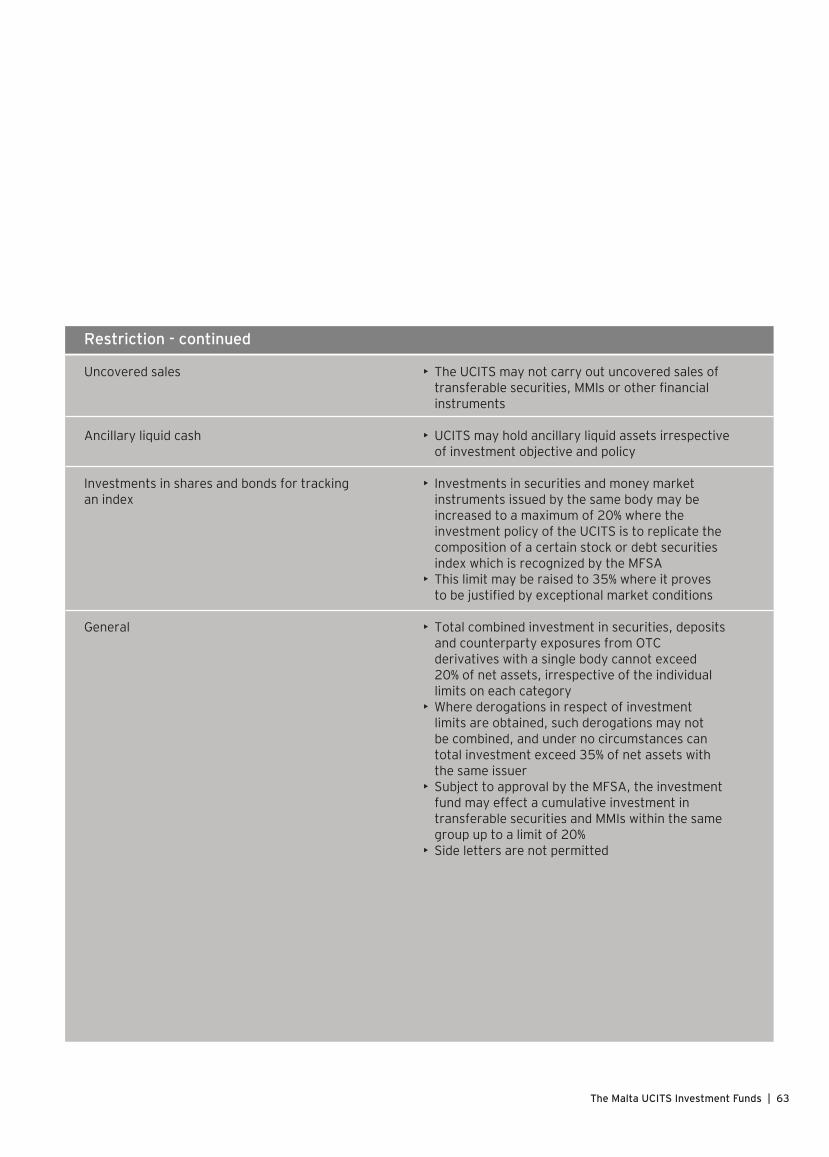

No more than 10% of the net asset may be invested intransferable securities and MMIs other than those referred to in 4.2.1.A and 4.2.1.B (non-core assets). UCITS are not allowed to acquire precious metals or certificates representing them.

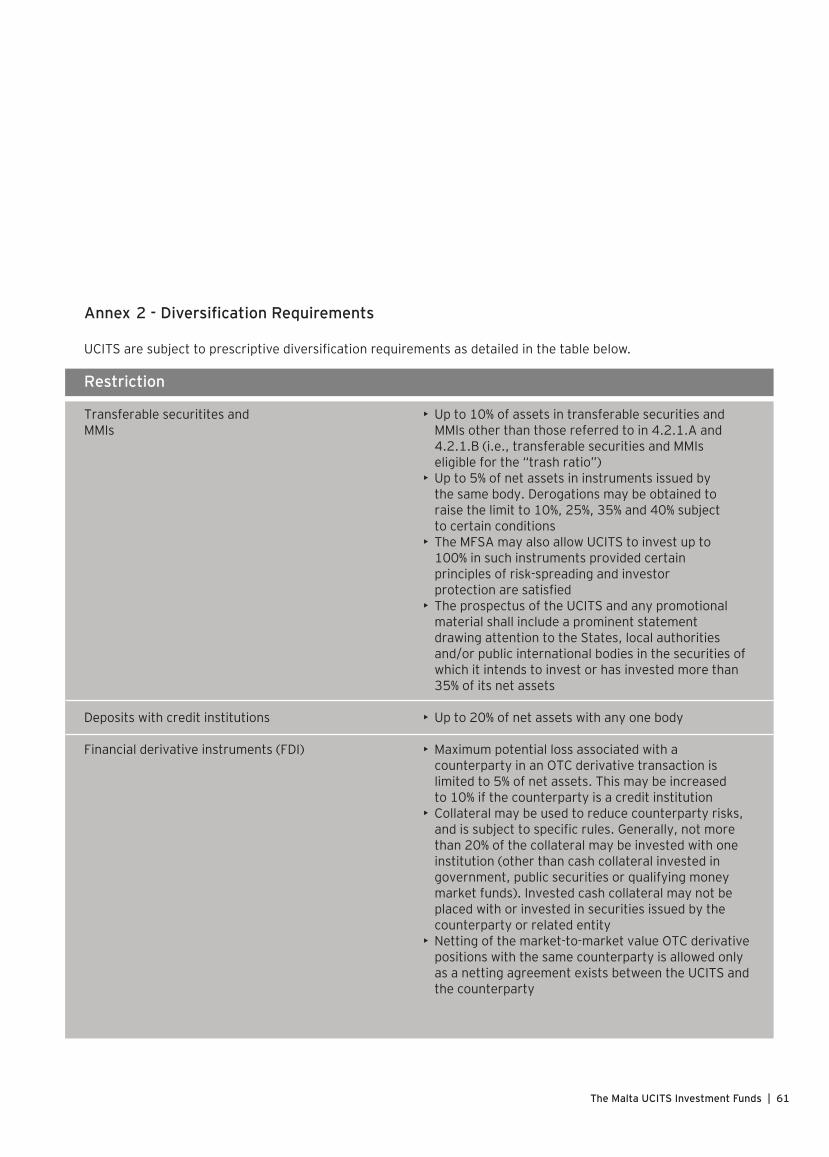

4.2.2 Diversification requirements

This Section provides a high level overview of the diversification requirements for UCITS.

In addition to satisfying the eligibility criteria (see Section 4.2.1) any investment by UCITS mustmeet the following diversification requirements: • No more than 5% of net assets may be invested in transferable securities and MMIs issued by the same body. Derogations for higher limits may be obtained in certain cases (e.g., the issuer meets certain criteria)• No more than 10% of net asset may be invested in transferable securities and MMIs qualifying for the “trash ratio” exemption• Up to 20% of net assets may be invested in deposits with the same credit institution• Potential loss with a counterparty in an OTC derivative transaction may not exceed 5% of net assets and 10% of net assets in case of a credit institution • The total value of transferable securities and MMIs held in issuing bodies in each of which is invested more than 5% of net assets must not exceed 40% of net assets

• No more that 20% of net assets may be invested in any combination of the following with a single body: • Transferable securities and MMIs • Deposits • Counterparty to OTC derivative transactions • May invest up to 20% if net assets in any other single UCITS or investment fund• Investment in units of investment funds not qualifying as UCITS is limited in aggregate to 30% of net assets• A UCITS may acquire no more than: • 10% of non-voting units or shares • 10% of debt securities of the same issuer • 25% of the shares or units of the same investment fund

Detailed diversification requirements are outlined inAnnex 2.

4.2.3 Borrowing restrictions

Neither an investment company, a UCITS ManagementCompany nor depositary acting on behalf of a commonfund may borrow. However, there are certain exemptions including:

• Up to 10% of net asset borrowed on a temporary basis • To enable the acquisition of immovable property for the pursuit of the UCITS business capped at 10% of its assets

A UCITS may however acquire foreign currency lending by means of a “back-to-back” loan.

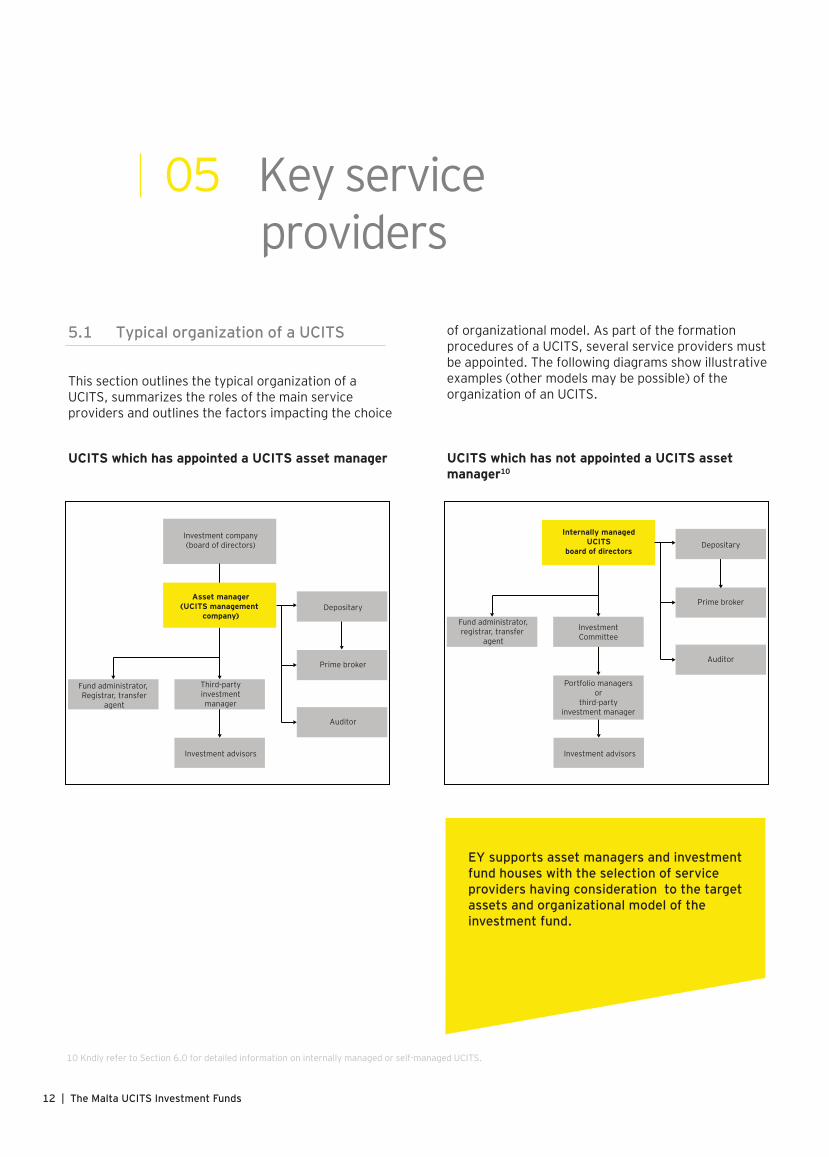

5.1 Typical organization of a UCITS

This section outlines the typical organization of a UCITS, summarizes the roles of the main service providers and outlines the factors impacting the choice

UCITS which has appointed a UCITS asset manager

12 | The Malta UCITS Investment Funds

of organizational model. As part of the formationprocedures of a UCITS, several service providers must be appointed. The following diagrams show illustrative examples (other models may be possible) of the organization of an UCITS.

UCITS which has not appointed a UCITS asset manager10

EY supports asset managers and investment fund houses with the selection of service providers having consideration to the target assets and organizational model of the investment fund.

10 Kndly refer to Section 6.0 for detailed information on internally managed or self-managed UCITS.

Internally managedUCITS

board of directorsDepositary

Prime broker

Auditor

Fund administrator,registrar, transfer

agent

InvestmentCommittee

Portfolio managersor

third-partyinvestment manager

Depositary

Prime broker

Auditor

Fund administrator, Registrar, transfer

agent

Third-partyinvestmentmanager

Investment advisors

Asset manager(UCITS management

company)

Investment company(board of directors)

Investment advisors

05 Key service providers

The principle duties of the service providers are as follows:

5.2 Asset manager

A UCITS may appoint a Maltese or European UCITS Management Company, in terms of the UCITS directive, as its asset manager to be responsible formanagement, investment and administration of its assets. It is a delegate of the UCITS and it must be duly authorised to provide such services.11

Management services of a UCITS Management Company include, in general, investment management, risk management and administration. It may howeverdelegate some of these functions. Also the administration function is ordinarily delegated to an Administrator (see Section 5.5).

In this regard, the UCITS Management Company may delegate, in part or in full, the investment management function to a third-party investment company provided it is authorised to undertake such activities (e.g., EUMiFID Investment Manager)

The UCITS Management Company need not bedomiciled and regulated where the UCITS is domiciled. Not all UCITS are required to appoint an external asset manager (see Section 6).

5.3 Investment advisor

The investment advisor advices the asset manager of the UCITS in respect of transactions relating tofinancial instruments. The investment advisor will not have any discretion with respect to the investment and re-investment of the assets of the UCITS.

UCITS are generally not required to appoint an investment advisor. Furthermore, the proposed investment advisor need not be established and regulated in the same jurisdiction as the UCITS, but shall have sufficient financial resources and liquidity at its disposal to enable it to conduct its business.

When the investment advisor is appointed directly by the asset manager rather than by the UCITS, such investment adviser is not subject to the MFSA’s approval and no eligibility criteria apply.

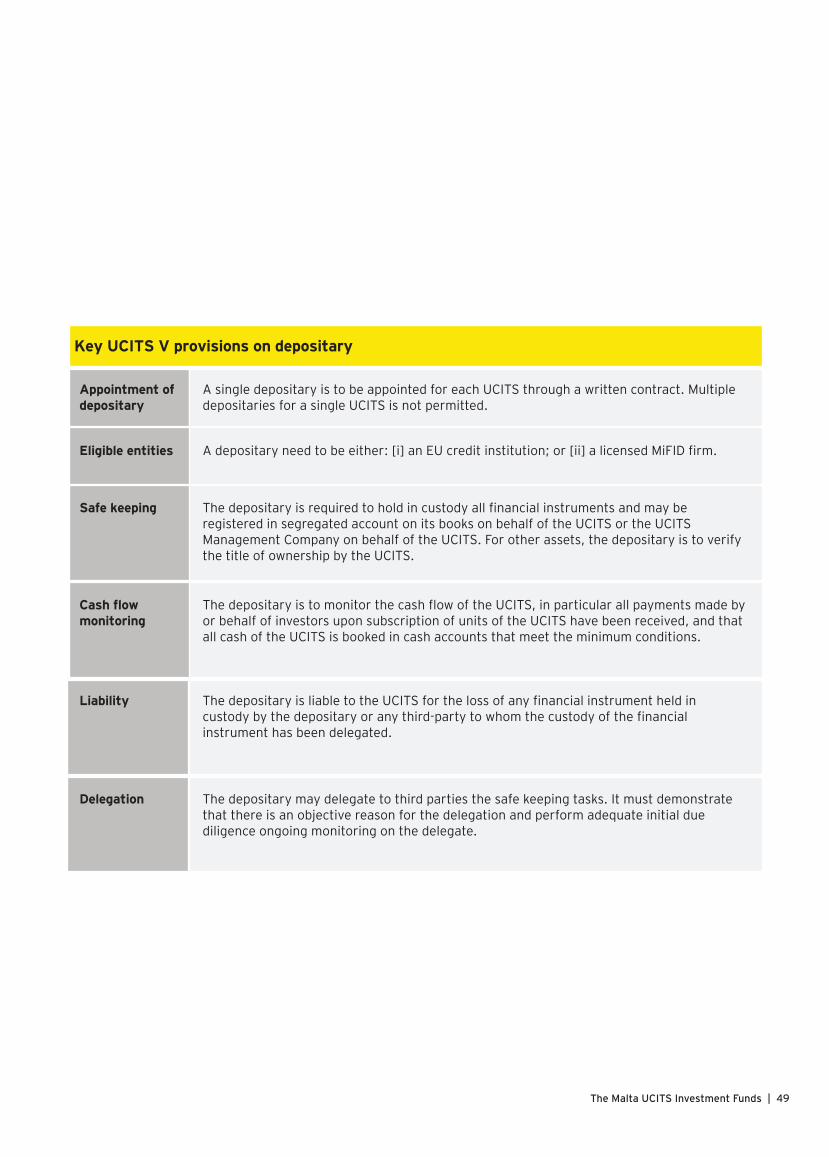

5.4 Depositary

The assets of UCITS must be entrusted to a depositary for safe keeping. The depositary is also responsible to ensure that the asset manager is abiding by theinvestment and borrowing powers laid out in theprospectus. The depositary shall be either:

• A licensed EU credit institution• The services of safe keeping of assets on behalf of clients or• An entity authorised to act as depositaries pursuant to the UCITS IV directive any other entity permitted under the UCITS IV directive.

A depositary shall either have its registered office or be established in the UCITS home Member State, it shall be independent from the asset manager and it shall be subject to prudential regulation and ongoing supervision.

While safe keeping the assets in which the investmentfund invests is the core function of the depositary, this party is also responsible to:

• Ensure that the sale, issue, repurchase, redemption and cancellation of units effected on behalf of UCITS are carried out in accordance with the applicable national law and the rules of incorporation

11 The Regulator of the jurisdiction in question having enacted a (bilateral) Memorandum of Understanding with the MFSA in the area of Securities supervision

The Malta UCITS Investment Funds | 13

• Ensure that the value of units is calculated in accordance with the applicable national law and the rules of incorporation• Carry out the instructions of the UCITS management company, unless they conflict with the applicable national law or the rules of incorporation• Ensure that the UCITS’ income is applied in accordance with the applicable national law and the rules of incorporation• Ensure that the calculation and distribution of any performance fees paid to the UCITS management company, if any, is carried out in line with the rules of incorporation of the UCITS

The safe keeping task is the only task that a depositarymay delegate.

5.5 Administrator

Administrative services in relation to a UCITS may be carried out by an administrator. The administrator’s role ordinarily covers, amongst other things:

• Liaison with shareholders• Calculation of the net asset value• Reconciliations• Pricing the investment portfolio• Payment of bills• Preparation of financial statements• Fund accounting• Performance reporting• Compliance reporting• Preparation of contract notes

The administrator ordinarily also provides registrar and transfer agency services.

The role of the administrator may be carried out eitherby the asset manager or alternatively may be delegatedto a separate entity which provides fund administrativeservices to investment funds.

5.6 Prime broker and counterparties

The UCITS, or its asset manager, may appoint one or more prime brokers or counterparties. Before entering into relevant agreement with a prime broker or counterparty, the UCITS or the asset manager on behalf of the UCITS shall exercise due skill, care and diligence on an on-going basis.

The depositary may be appointed as prime broker provided that it must separate the custody activities from its brokerage activities.

5.7 Auditor

The UCITS shall appoint an auditor approved by the MFSA and the UCITS shall obtain a signed letter ofengagement from its auditor defining clearly the extent of the auditor’s responsibilities and the terms of appointment.

14 | The Malta UCITS Investment Funds

The Malta UCITS Investment Funds | 15

16 | The Malta UCITS Investment Funds

As such a UCITS may consider either of the following options:

• To integrate a fully fledged investment management function Or• To delegate either the investment management or risk management function to a third-party while retaining the other function

6.1 Introduction

A UCITS may opt not to appoint a UCITS managementcompany and thus the UCITS will be carrying out internally the investment management function. In this regard, the UCITS shall at least perform the portfolio management and risk management functions.

For the purpose of this section the term “UCITS” shallbe understood to refer to “internally managed UCITS.”The term “investment management” shall refer to the “portfolio management and risk managementfunctions.”

6.2 Operational arrangements

A UCITS is to organise and control its affairs in a responsible manner and is to have adequate operational, administrative and financial procedures and controls to ensure compliance with all regulatoryrequirements.

The UCITS would also need to have adequate and appropriate human and technical resources that are necessary for the proper management and to effectively perform its activities.

6.2.1 Investment management

The board of directors of the UCITS would be responsible for the investment management function. In undertaking its activities, a UCITS is to functionally separate the functions of portfolio management and risk management. In that persons ordinarily engaged in either of the said functions are not to be supervised by those responsible for the other operating units nor are they to be engaged in other operating activities.Compensation to such persons should also be relatedsolely to the performance of the function involved in.

EY supports asset managers and investmentfund houses with the organizational modeling,internal structuring and policies as well as anydelegation arrangements for internally managed investment funds.

06 Internally managed UCITS

The Malta UCITS Investment Funds | 17

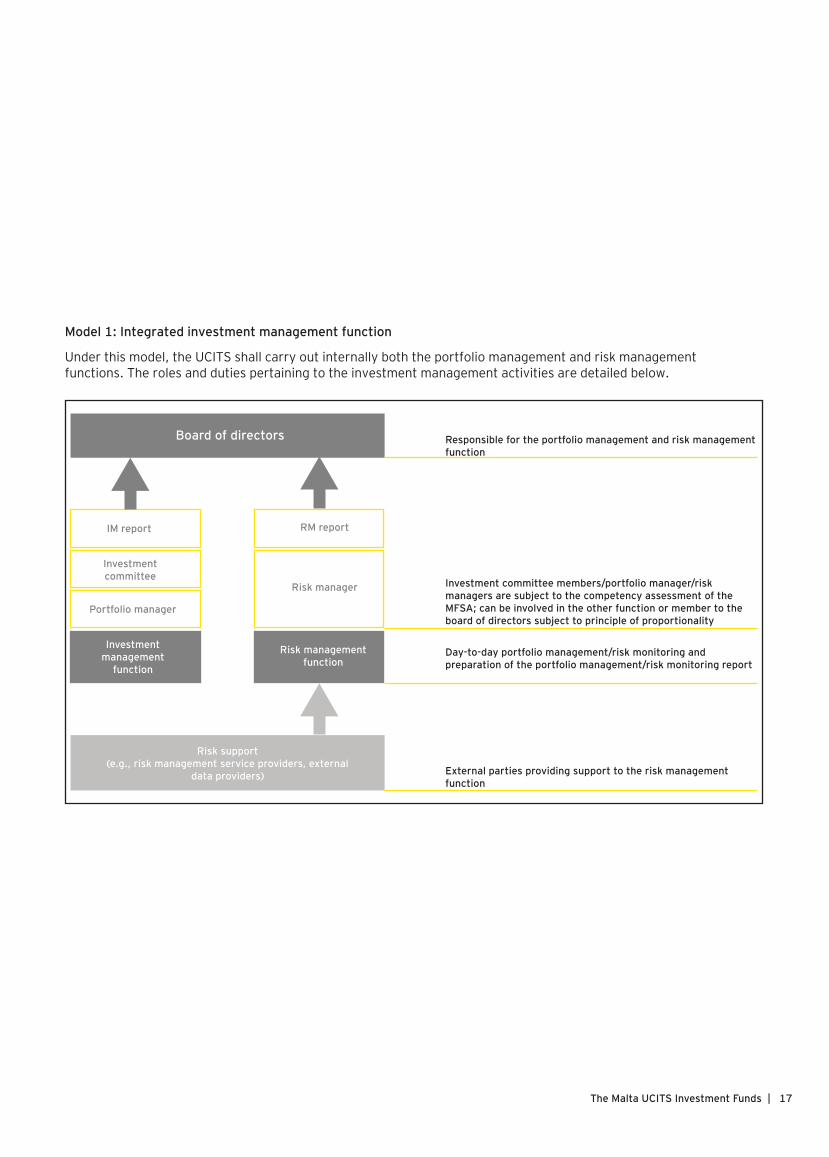

Model 1: Integrated investment management function

Under this model, the UCITS shall carry out internally both the portfolio management and risk management functions. The roles and duties pertaining to the investment management activities are detailed below.

IM report

Investmentmanagement

function

Board of directors

Investmentcommittee

Portfolio manager

Risk managementfunction

RM report

Risk manager

Risk support(e.g., risk management service providers, external

data providers)

Investment committee members/portfolio manager/risk managers are subject to the competency assessment of the MFSA; can be involved in the other function or member to the board of directors subject to principle of proportionality

Day-to-day portfolio management/risk monitoring andpreparation of the portfolio management/risk monitoring report

External parties providing support to the risk management function

Responsible for the portfolio management and risk management function

18 | The Malta UCITS Investment Funds

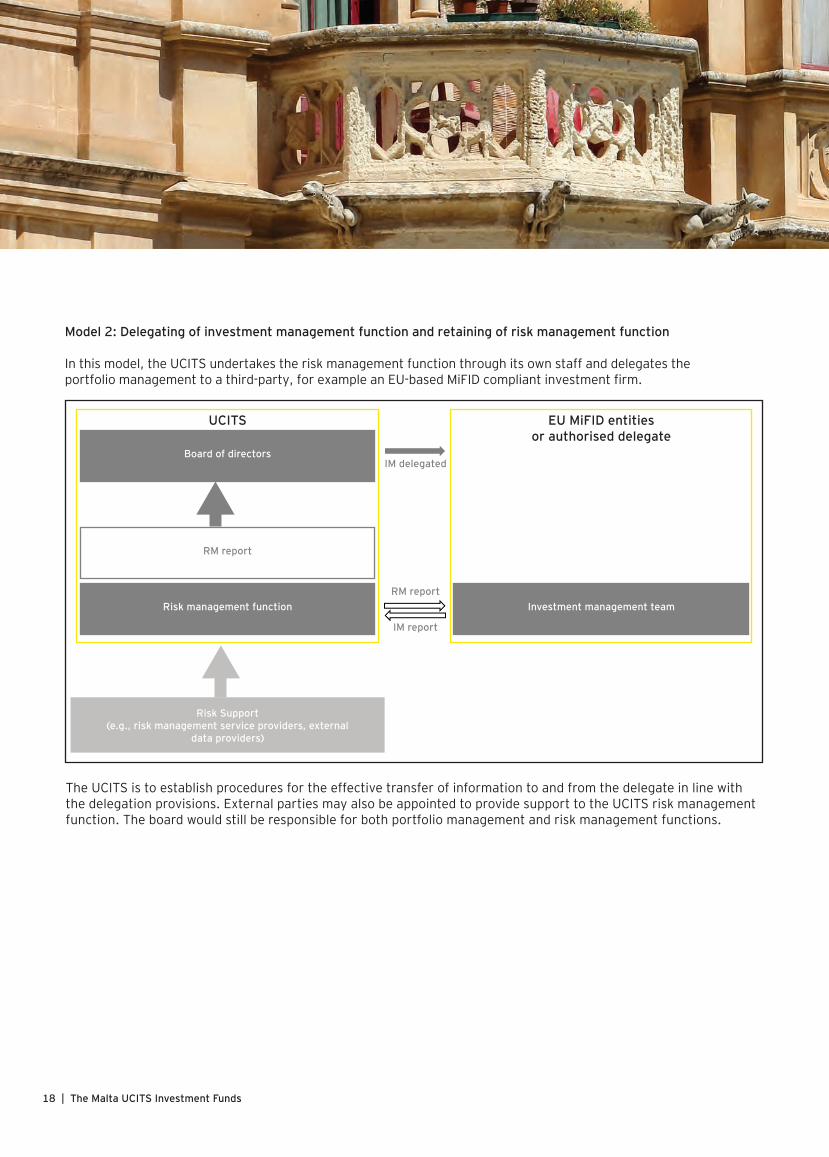

Model 2: Delegating of investment management function and retaining of risk management function

In this model, the UCITS undertakes the risk management function through its own staff and delegates the portfolio management to a third-party, for example an EU-based MiFID compliant investment firm.

Risk Support(e.g., risk management service providers, external

data providers)

Risk management function

RM report

Board of directors

Investment management team

IM delegated

IM report

UCITS EU MiFID entitiesor authorised delegate

The UCITS is to establish procedures for the effective transfer of information to and from the delegate in line withthe delegation provisions. External parties may also be appointed to provide support to the UCITS risk managementfunction. The board would still be responsible for both portfolio management and risk management functions.

RM report

The Malta UCITS Investment Funds | 19

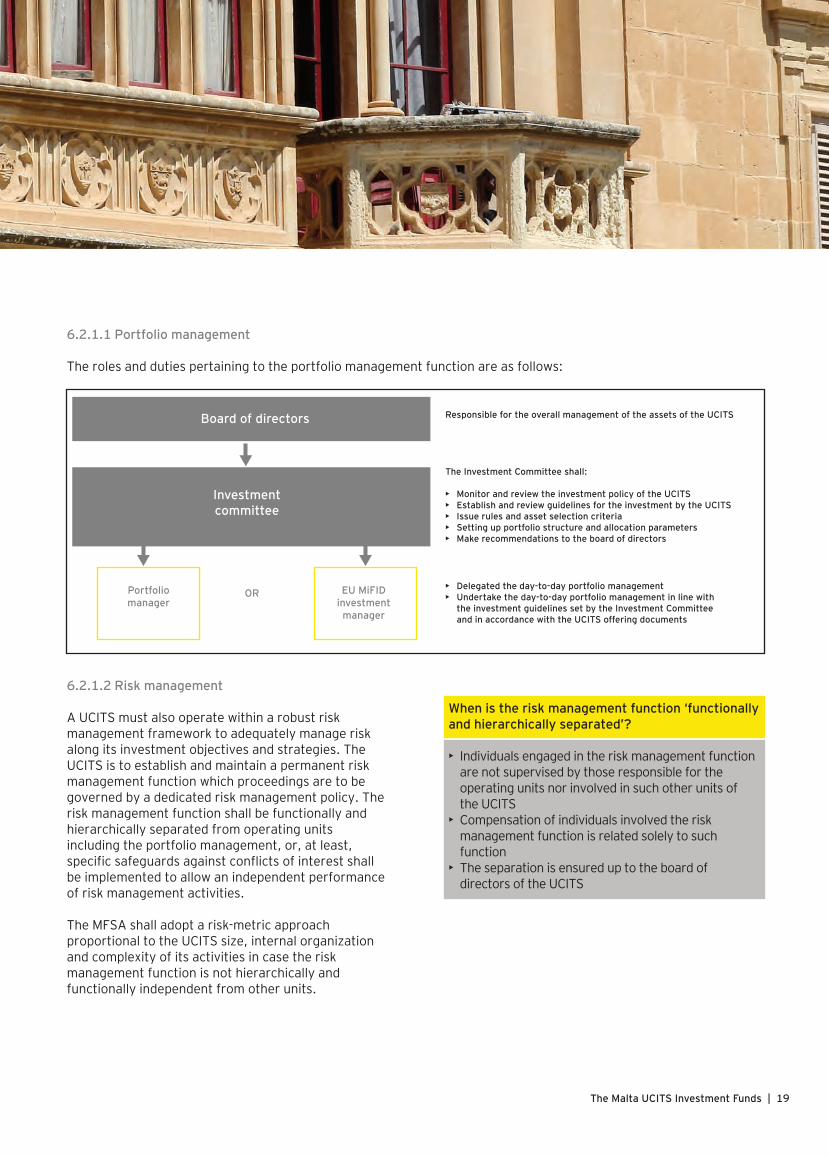

6.2.1.1 Portfolio management

The roles and duties pertaining to the portfolio management function are as follows:

6.2.1.2 Risk management

A UCITS must also operate within a robust riskmanagement framework to adequately manage riskalong its investment objectives and strategies. The UCITS is to establish and maintain a permanent riskmanagement function which proceedings are to be governed by a dedicated risk management policy. Therisk management function shall be functionally and hierarchically separated from operating units including the portfolio management, or, at least, specific safeguards against conflicts of interest shallbe implemented to allow an independent performance of risk management activities.

The MFSA shall adopt a risk-metric approach proportional to the UCITS size, internal organization and complexity of its activities in case the risk management function is not hierarchically and functionally independent from other units.

When is the risk management function ‘functionallyand hierarchically separated’?

• Individuals engaged in the risk management function are not supervised by those responsible for the operating units nor involved in such other units of the UCITS • Compensation of individuals involved the risk management function is related solely to such function • The separation is ensured up to the board of directors of the UCITS

Board of directors

EU MiFIDinvestment

manager

OR

Investmentcommittee

The Investment Committee shall:

• Monitor and review the investment policy of the UCITS• Establish and review guidelines for the investment by the UCITS• Issue rules and asset selection criteria• Setting up portfolio structure and allocation parameters• Make recommendations to the board of directors

Responsible for the overall management of the assets of the UCITS

• Delegated the day-to-day portfolio management• Undertake the day-to-day portfolio management in line with the investment guidelines set by the Investment Committee and in accordance with the UCITS offering documents

Portfoliomanager

20 | The Malta UCITS Investment Funds

The UCITS may also elect to contractually delegate the risk management function to third parties (not being the depositary or a delegate of the depositary) for the purpose of a more efficient conduct ofbusiness provided that the UCITS is able to demonstrate that the third-party has the professional ability and capacity to perform such duties, is dulyauthorised or registered to perform such duties andits appointment is acceptable to the MFSA.

In doing so the UCITS must establish methods for ongoing assessment of the standard of performance of the third-party.

6.3 Delegation

The portfolio manager(s) may either be individual(s) or a licensed manager which is authorised or registered to perform such function and accordinglyit may not necessarily be authorised as an UCITSmanagement company (e.g., EU MiFID investmentmanagers) and acceptable to the MFSA. A UCITS may confer the portfolio management function to managers licensed in third countries provided that a cooperation agreement is in place between the MFSAand the supervisory authorities of the manager’sthird country. Portfolio management activities may not be delegated to the depositary.

6.4 Capital requirements

The UCITS is to have sufficient financial resources atits disposal to enable it to conduct its business effectively, to meet its liabilities and to be prepared tocope with the risks to which it is exposed. It is tomaintain an “initial capital” of €300,000 and thatthe net asset value of the UCITS is expected to exceed this amount on an ongoing basis.

The Malta UCITS Investment Funds | 21

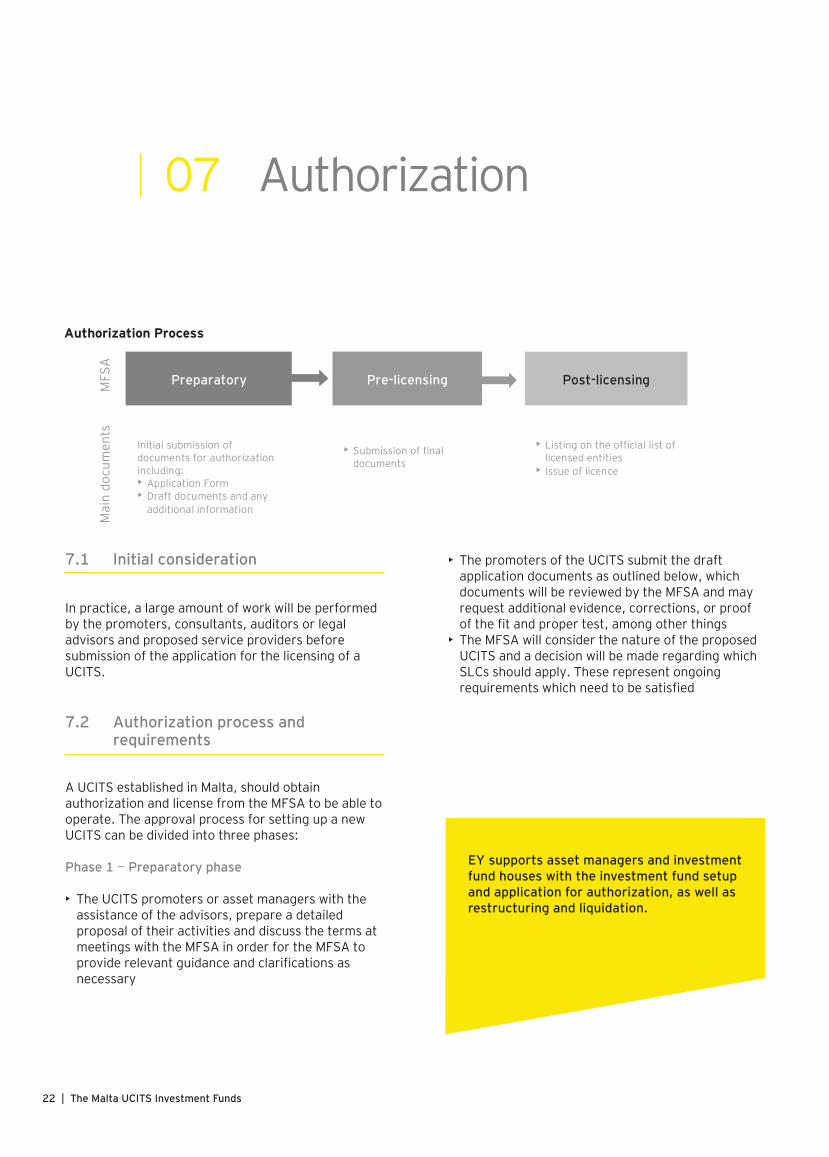

Preparatory Pre-licensing Post-licensing

Initial submission of documents for authorization including: • Application Form • Draft documents and any

additional information

• Submission of final documents

• Listing on the official list of licensed entities

• Issue of licence

MFS

AM

ain

docu

men

ts

7.1 Initial consideration

In practice, a large amount of work will be performedby the promoters, consultants, auditors or legal advisors and proposed service providers before submission of the application for the licensing of a UCITS.

7.2 Authorization process and requirements

A UCITS established in Malta, should obtain authorization and license from the MFSA to be able to operate. The approval process for setting up a new UCITS can be divided into three phases:

Phase 1 — Preparatory phase

• The UCITS promoters or asset managers with the assistance of the advisors, prepare a detailed proposal of their activities and discuss the terms at meetings with the MFSA in order for the MFSA to provide relevant guidance and clarifications as necessary

Authorization Process

22 | The Malta UCITS Investment Funds

• The promoters of the UCITS submit the draft application documents as outlined below, which documents will be reviewed by the MFSA and may request additional evidence, corrections, or proof of the fit and proper test, among other things • The MFSA will consider the nature of the proposed UCITS and a decision will be made regarding which SLCs should apply. These represent ongoing requirements which need to be satisfied

EY supports asset managers and investment fund houses with the investment fund setupand application for authorization, as well as restructuring and liquidation.

07 Authorization

• A draft of the investment management agreement, depositary agreement and administration agreement

In the case of internally managed UCITS, the followingadditional documents must also be submitted:

• Personal questionnaire forms, competency forms and CVs of the individuals responsible for the portfolio management function and risk management function of the UCITS • A near final investment committee terms of reference• Confirmations from the investment committee members and portfolio managers• Portfolio delegation agreement and/or risk management delegation agreement (if applicable)• A near final risk management policy

Further details of the operational structure of an internally managed UCITS are outlined in Section 6.

The MFSA recommends applicants to file an application only once all constituents of the project are in final draft form.

The Malta UCITS Investment Funds | 23

Phase 2 — Pre-licensing phase

• When all review points noted in the draft application are resolved, the MFSA will issue an “in principle” approval for a license. Following this, promoters of the UCITS must:

• Finalize any outstanding matters • Submit signed final application documents

• A license will be issued once all pre-licensing issues are resolved

Phase 3 — Post-licensing / pre-commencement of business phase

• The MFSA will determine whether the applicant needs to satisfy any post-licensing matters before formal commencement of business can take off

The initial application documents to be submitted should at least include:

• Application form• Application fee• A near final draft prospectus including relevant offering supplements of the UCITS• A near final draft of the memorandum and articles of association/partnership deed/ trust deed/fund rules (as applicable)• Resolution from the board of directors/ general partners/management company• Information including personal questionnaire forms on the directors/general partners• Information including personal questionnaire forms on the qualifying founder shareholders (holding 10% or more of the voting rights)• Personal questionnaire forms and competency forms of the individuals holding the post of compliance officer and money laundering reporting officer

8.1 Introduction

One of the main benefits of UCITS is that it can be marketed to all types of EU/EEA investors — retail,professional and institutional investors — and are relatively easier to distribute compared to other typesof investment funds licensed in Malta.

The UCITS directive provides a harmonized“European” passporting regime for UCITS whereby aUCITS authorised in any EU member state (the homemember state) may be marketed to investors in other member states (the host member state) following notification to the host member statecompetent authority.

Marketing of UCITS outside the EEA is subject to eachcountry’s national regime.

8.2 Marketing of maltese UCITS in other EU or EEA member states

Before a Maltese UCITS may benefit from the passporting provisions to market its units to investors in other EU Member States, it must submit a notification to the competent authority of its home Member State, in Malta the MFSA. This procedure applies in cases of:

• A UCITS intending to market all or part of its units in the host member state for the first time• An umbrella UCITS intending to market all or part of its units of one or several of its sub-funds in that host member state for the first time• An umbrella UCITS intending to market all or part of the units of one or several additional sub-funds (i.e., where the marketing of unit of other sub-funds has already been notified to the host member state) for the first time

Any subsequent update to the information submitted via the notification procedure is to be provided directly to the host member state via a written notice.

8.2.1 The notification procedure

The following sequential process will need be carried out for a Malta UCITS to market units in other EU member states.

The Malta UCITS is required to submit to the MFSA a notification file that contains:

• A notification letter • The latest version of the required documents (see Section 8.2.2)

The Malta UCITS is to complete and submit a separatenotification file for each EU member state it intends to market its units.

24 | The Malta UCITS Investment Funds

EY supports asset managers and investmentfund houses in the regulatory assessment and notification for the distribution of the investment fund.

08 Marketing

• Other information required by the competent authority of the host member state that are not governed by the UCITS IV directive, and are relevant to the arrangements made for the marketing of the units of the UCITS

The notification letter must follow the template provided for in Schedule C to the MFSA rules applicable to UCITS schemes.

• The latest version of the: • Constitutional documents of the UCITS (e.g., memorandum and articles of association) • Prospectus: The latest stamped version by the MFSA of the prospectus and relevant offering supplements (as appropriate) • Reports: Latest audited annual statements and half-yearly report • Key investor information documents (KIID) • Confirmation: If required by host member state, confirmation of payment due to the competent authority of the host member state

The reports and KIIDs are to be translated in the official language or one of the official languages of the host member state or any other language approved by the competent authority of the host member states.

The MFSA shall verify the information provided in thenotification file and if satisfied, shall complete an attestation that the Malta UCITS fulfils the conditions of the UCITS IV directive. It then transmits, within a maximum of 10 working days, the complete notificationfile to the competent authorities of the host memberstate together with the attestation. The host memberstate regulator confirms receipt and completeness ofthe notification file.

The transmission to the competent authorities of the host member state is notified without delay by the MFSA to the Malta UCITS. The Malta UCITS then may access the market of the relevant host member state as at the date of this notification.

Any changes to the information submitted via the notification procedure must give written notice to thecompetent authority of the host member state inwhich it is currently marketing its units prior to implementing the change.

It is not necessary to submit this notice to the MFSA. The MFSA however remains responsible for theapproval of any amendments to the constitutionaldocuments or prospectus of the UCITS. Such approval must be sought prior to sending the written notice.

8.2.2 The content of the notification

The notification must contain:

• A notification letter which includes: • Information on the UCITS, the sub-funds, and, where relevant the units to be marketed, the UCITS management company or internally managed UCITS • The arrangements for marketing the UCITS in the host EU member state • Details of the facilities available in the host member state for making payments to investors, repurchasing and redeeming units, and making available the information that UCITS are required to provide

The Malta UCITS Investment Funds | 25

8.2.3 Information to be provided to investors

Where a Malta UCITS markets its units in a host member state, it must provide investors in the host member state, free of charge, with the relevant KIID, prospectus, annual report (for each financial year) and a half-yearly report.

Such information and documents must be provided toinvestors in compliance with the following provisions:

• The information or documents must be provided to investors in the host member states in the way prescribed by the laws and regulations of the host member state• The KIID must be translated in any of the official languages of the host member state or into a language approved by the competent authority of the host member state• Information or documents apart from the KIID may be translated, at the discretion of the Malta UCITS, into any one of the official languages of the host member state or a language approved by the host member state regulator or into a language customary in the sphere or international finance • The Malta UCITS is responsible to provide accurate translations of information and documents and must faithfully reflect the content of the original information

26 | The Malta UCITS Investment Funds

The Malta UCITS Investment Funds | 27

For UCITS the risk management requirements focus in detail on risk management, in particular on market risk measurement.

The following section provides a brief overview of the risk management requirements

9.1 Risk management policy

UCITS management companies or UCITS if internally managed, are required to establish, implement and maintain an adequate and documented risk management policy which identifies the risks the UCITS is or might be exposed, taking into account the nature, scale and complexity of the business of the UCITS.

The risk management policy shall comprise suchprocedures as are necessary to enable an investment fund to assess the exposure of that investment fund to market, liquidity and counterparty risks, and the exposure of the investment fund to all other risks, including operational risks, which may be material forthe investment fund.

The risk management policy must cover:

• The techniques, tools and arrangements that enable them to comply with its obligations regarding the measurement and management of risk • The allocation of risk management responsibilities within the UCITS management company or UCITS if internally managed

The risk management policy must state the terms, contents and frequency of reporting of the risk management function to the board of directors and to senior management and, where appropriate, to the supervisory function.

28 | The Malta UCITS Investment Funds

EY supports asset managers and investment fund houses in defining or reviewing the risk management process and the formation of internal policies and procedures.

9.2 Risk profile

The board of directors of the UCITS management company must define and approve the risk profile of the UCITS with consultation from the risk management function. The risk profile is determined from theprocess of risk identification, which must take into account all risks that may be material to the UCITS.

The risk profile of a UCITS may be defined as the measure of risk aversion relative to the investment strategy (i.e., risk-reward trade-off)

09 Risk management

Each FDI position is converted into the market value of an equivalent position in the underlying asset of thederivative.

When calculating the global exposure, the UCITS management company must:

• Calculate the gross commitment of each individual position (including any embedded derivatives)• Identify any netting and hedging arrangements. For each netting or hedging arrangement, to calculate the net commitment the absolute value of which is the offset of the netting or hedging arrangements to the gross commitment • Global exposure is then the sum of: • The absolute value of the commitment of each individual position not involved in netting or hedging arrangements • The absolute value of the net commitment of each individual position involved in netting or hedging arrangements • The absolute value of the commitment linked to any efficient portfolio management techniques

(b) Value-at-risk (VaR)

VaR Approach measures the maximum potential lossdue to market risk rather than leverage. It measures the maximum potential loss at a given confidencelevel over a specific time period under normal market conditions.

A UCITS must consider all of its positions when calculating the global exposure using the VaR approach.

The Malta UCITS Investment Funds | 29

9.3 Risk measurement and management

UCITS management companies or UCITS (whereinternally managed) must determine according to therisk profile of the UCITS the methodology to be used for the calculation of the global exposure (commitment approach or value-at-risk (VaR)approach/other advanced risk measurement)

ESMA’s guidelines on risk measurement and the calculation of global exposure and counterparty risk for UCITS it indicated that the commitment approach should not be applied to UCITS that either: • Engage in complex investment strategies which represent more than a negligible part of the UCITS’ investment policy • Has more than a negligible exposure to exotic derivatives • The commitment approach does not adequately capture the market risk of the UCITS

Calculation of the global exposure is to be carried out at least on a daily basis.

(a) Commitment approach

The commitment approach measures global exposure in terms of the total incremental exposure andleverage (total commitment) generated by theUCITS through the use of FDIs. The total commitment must not exceed the total net assets of the UCITS.

The total commitment is the sum of the absolute valueof the commitment of each individual position, aftertaking into account netting and hedging.

30 | The Malta UCITS Investment Funds

The choice of the appropriate VaR model (e.g., parametric, historical simulation, Monte Carlo etc.) remains the responsibility of the UCITS or the UCITS management company. It must however be supplemented by stress tests and back testing.

Any model used must undergo a validation by a party independent of the building process for ensuring that the model is conceptually sound and captures adequately all material risks. Validation must also be carried out in case of any significant change to the model.

Two concepts of VaR with different limits may be adopted:

• If a reference portfolio (or benchmark) can be determined, a relative VaR may be used where the portfolio VaR cannot be more than twice the reference portfolio VaR. The choice of the reference portfolio needs to be fully documented • Where there is no reference portfolio, an absolute VaR figure must be calculated. Absolute VaR limit cannot exceed 20% of the net assets

ESMA guidelines on risk management detail the requirements related to the selection of the reference portfolio under the relative VaR approach. The reference portfolio should comply with the following requirements: • It should be unleveraged and not contain any FDIs (or embedded derivatives) with the exception of UCITS engaging in long/ short investment strategies and UCITS that intends to have a currency hedged portfolio • The risk profile of the reference portfolio should be consistent with the UCITS investment objectives • The risk/ return profile of the UCITS should not change frequently • The process relating to the determination and the ongoing maintenance of the reference portfolio should be documented

The VaR model parameters to be used are the following:

• Confidence Interval: 99 %• Holding Period: 20 business days• Observation period of risk factors: At least 250 business days, unless a shorter observation period is justified by a significant increase in price volatility (for instance extreme market conditions)• Data update: Quarterly or more frequent when market prices are subject to material changes• Calculation frequency: At least daily

A different confidence interval or holding period maybe used and subject to the approval of the MFSA. Additional details on rescaling of the VaR limits are provided in ESMA’s guidelines.

The Malta UCITS Investment Funds | 31

(c) Additional measures to be implemented in case of the use of VaR approach

Back testing

The purpose of back testing is to monitor the accuracyand performance of the VaR model and must be carried out at least on a monthly basis. It must bebased on a comparison between the portfolio’s end-of-day value-at-risk and its value at the end of the subsequent day (i.e., clean back testing).

The UCITS management company or UCITS must determine and monitor the “overshootings” on the basis of the back-testing. An “overshooting” is a one-day change in the portfolio’s value that exceeds the related one-day VaR measure calculated by the model.

Stress testing

Stress tests aim at capturing extreme events with theoretical or historical scenarios. ESMA provides additional guidelines on stress testing qualitative and quantitative requirements. It should ideally cover all risks which affect the value of the UCITS particularly those risks not fully captured by the VaR model and those risks that are likely to by significant in stress situations (e.g., illiquidity in the market) and adequately captures significant leverage that exposes the UCITS to significant downside risk.

Stress testing must be performed at least on a monthly basis or more frequent as determined by:

• The rate of portfolio turnover (i.e., the higher the portfolio turnover, the more frequent such testing should be carried out)• Any changes in a relevant manner to the composition/ value of the portfolio of the UCITS or market conditions that result in the test results to differ significantly

10.1 Introduction

KIIDs must be drawn for every UCITS as a stand-alonedocument which must include appropriate information about the essential characteristics of theUCITS. It must be provided to investors so that they are reasonably able to understand the nature andrisks of the investment product that is being offered to them, and to take informed decisions.

The KIID is supplementary to the UCITS’ offering memorandum and any offering supplement.

10.2 Principles for the production of KIIDs

The production of any KIID is governed by the Commission Regulation12 which specifies the principles to be adopted in preparing the KIID including the main elements of the information that is to be disclosed.

A summary of the said requirements are covered inthe table (Guidance on the production of KIIDs):

32 | The Malta UCITS Investment Funds

EY supports asset managers and investmentfund houses in the formation of the contentand layout production of Key Investor Information documents for investment funds.

12 Commission regulation (EU) 583/2010 of 1 July 2010

10 Key Investor information document

The Malta UCITS Investment Funds | 33

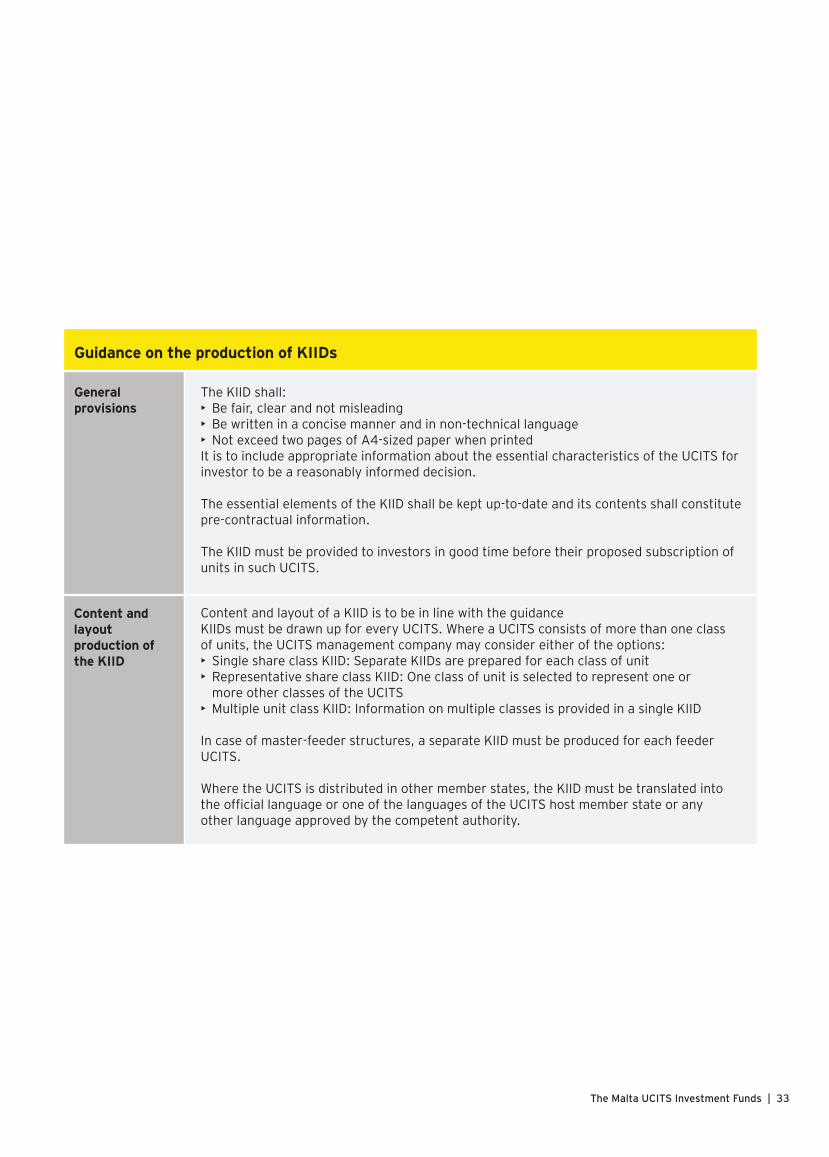

Content and layout production of the KIID

Generalprovisions

The KIID shall:• Be fair, clear and not misleading • Be written in a concise manner and in non-technical language • Not exceed two pages of A4-sized paper when printed It is to include appropriate information about the essential characteristics of the UCITS forinvestor to be a reasonably informed decision.

The essential elements of the KIID shall be kept up-to-date and its contents shall constitutepre-contractual information.

The KIID must be provided to investors in good time before their proposed subscription ofunits in such UCITS.

Content and layout of a KIID is to be in line with the guidanceKIIDs must be drawn up for every UCITS. Where a UCITS consists of more than one classof units, the UCITS management company may consider either of the options: • Single share class KIID: Separate KIIDs are prepared for each class of unit• Representative share class KIID: One class of unit is selected to represent one or more other classes of the UCITS• Multiple unit class KIID: Information on multiple classes is provided in a single KIID

In case of master-feeder structures, a separate KIID must be produced for each feederUCITS.

Where the UCITS is distributed in other member states, the KIID must be translated into the official language or one of the languages of the UCITS host member state or anyother language approved by the competent authority.

Guidance on the production of KIIDs

34 | The Malta UCITS Investment Funds

Distribution andpublication

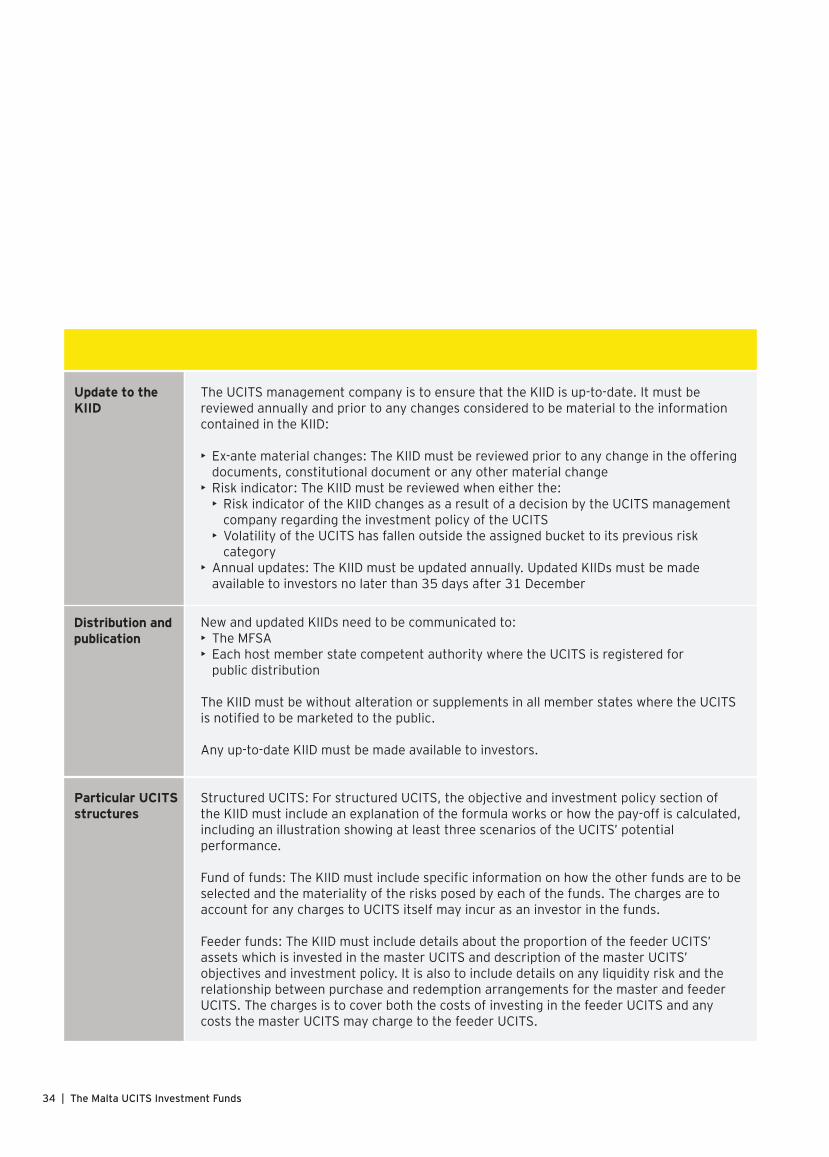

Update to theKIID

The UCITS management company is to ensure that the KIID is up-to-date. It must be reviewed annually and prior to any changes considered to be material to the information contained in the KIID:

• Ex-ante material changes: The KIID must be reviewed prior to any change in the offering documents, constitutional document or any other material change• Risk indicator: The KIID must be reviewed when either the: • Risk indicator of the KIID changes as a result of a decision by the UCITS management company regarding the investment policy of the UCITS • Volatility of the UCITS has fallen outside the assigned bucket to its previous risk category• Annual updates: The KIID must be updated annually. Updated KIIDs must be made available to investors no later than 35 days after 31 December

New and updated KIIDs need to be communicated to: • The MFSA• Each host member state competent authority where the UCITS is registered for public distribution

The KIID must be without alteration or supplements in all member states where the UCITSis notified to be marketed to the public.

Any up-to-date KIID must be made available to investors.

Particular UCITSstructures

Structured UCITS: For structured UCITS, the objective and investment policy section of the KIID must include an explanation of the formula works or how the pay-off is calculated,including an illustration showing at least three scenarios of the UCITS’ potentialperformance.

Fund of funds: The KIID must include specific information on how the other funds are to beselected and the materiality of the risks posed by each of the funds. The charges are to account for any charges to UCITS itself may incur as an investor in the funds. Feeder funds: The KIID must include details about the proportion of the feeder UCITS’ assets which is invested in the master UCITS and description of the master UCITS’ objectives and investment policy. It is also to include details on any liquidity risk and therelationship between purchase and redemption arrangements for the master and feeder UCITS. The charges is to cover both the costs of investing in the feeder UCITS and anycosts the master UCITS may charge to the feeder UCITS.

The Malta UCITS Investment Funds | 35

The Maltese legislative framework allows for cross-border and domestic merger of UCITS and lays down detailed requirements to be met.

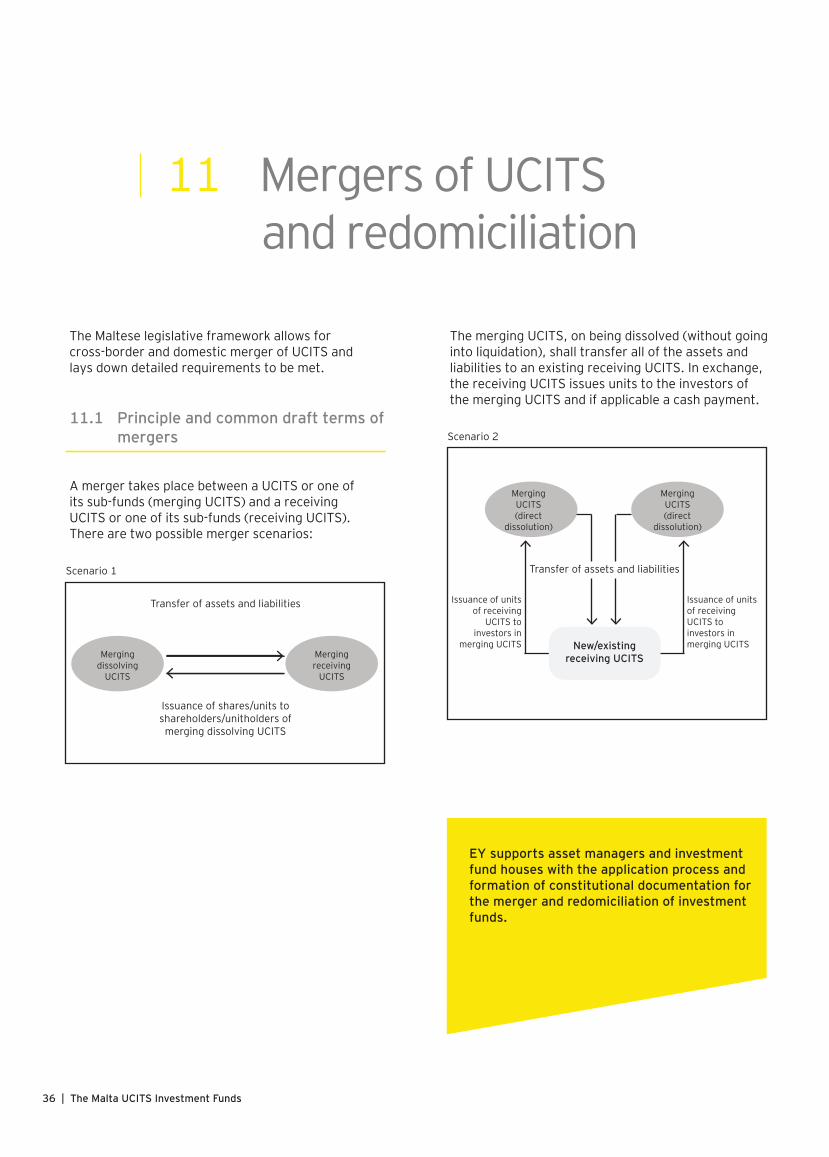

11.1 Principle and common draft terms of mergers

A merger takes place between a UCITS or one ofits sub-funds (merging UCITS) and a receiving UCITS or one of its sub-funds (receiving UCITS). There are two possible merger scenarios:

The merging UCITS, on being dissolved (without goinginto liquidation), shall transfer all of the assets and liabilities to an existing receiving UCITS. In exchange,the receiving UCITS issues units to the investors ofthe merging UCITS and if applicable a cash payment.

36 | The Malta UCITS Investment Funds

EY supports asset managers and investment fund houses with the application process andformation of constitutional documentation forthe merger and redomiciliation of investmentfunds.

Mergingdissolving

UCITS

Mergingreceiving

UCITS

Transfer of assets and liabilities

Issuance of shares/units toshareholders/unitholders ofmerging dissolving UCITS

Scenario 1

Scenario 2

MergingUCITS(direct

dissolution)

Transfer of assets and liabilities

New/existingreceiving UCITS

MergingUCITS(direct

dissolution)

Issuance of unitsof receiving

UCITS toinvestors in

merging UCITS

Issuance of unitsof receivingUCITS toinvestors inmerging UCITS

11 Mergers of UCITS and redomiciliation

The merging UCITS, on being dissolved, shall transferall of their assets and liabilities to a receiving UCITS that they form. In exchange, the receiving UCITS issues units to the investors of each of the merging UCITS; and if applicable a cash payment.

As a result of a merger, regardless of the technique:

• All the assets and liabilities of the merging UCITS are transferred to the receiving UCITS or depositary of the receiving UCITS• The investors of the merging UCITS shall become investors of the receiving UCITS• The merging UCITS shall cease to exist on the entry into effect of the merger

The merger of a master UCITS will result in the feederUCITS to be liquidated unless the MFSA grants approval to the Malta-based feeder UCITS for one of the following:

• Continue to be a feeder UCITS of the master UCITS or another UCITS resulting from the merger or division of the master UCITS• Invest at least 85% of its assets in units of another master UCITS not resulting from the merger or the division• Amend its instruments of incorporation in order to convert into a UCITS which is not a feeder UCITS

11.2 Common draft terms or merger

In seeking the approval for a merger, the mergingUCITS and the receiving UCITS must draw up common draft terms of merger inter alia:

• The type of merger and the name of the UCITS involved• The rationale of the proposed merger • The expected impact of the proposed merger on the investors of both the merging UCITS and the receiving UCITS

• the criteria adopted for valuation of the assets and, where applicable, the liabilities on the planned effective date of the merger • the respective fund rules applicable to the transfer of assets and the exchange of shares or units • the instruments of incorporation of the receiving UCITS or in case of a merger described in Scenario 2 (if there is the creation of a new receiving UCITS), the constitutional document of the newly constituted receiving UCITS

11.3 Authorization

11.3.1 The merging UCITS established in Malta

Where the merging UCITS is a Maltese UCITS, it shall apply to the MFSA for authorization to undergo such merger.

The merging UCITS must provide to the MFSA an authorization file including the following:

• The common draft terms of the proposed merger duly approved by the merging UCITS and the receiving UCITS• An up-to-date version of the prospectus and KIID of the receiving UCITS (if established in another member state)• A statement by each of the depositaries of the merging and the receiving UCITS confirming that they have verified that the identification of the type of merger and UCITS involved; theplanned effective date of the merger; and the rules applicable, respectively, to the transfer of assets and the exchange of units, are in accordance with the requirements of the UCITS directive and the instruments of incorporation of their respective UCITS

The Malta UCITS Investment Funds | 37

38 | The Malta UCITS Investment Funds

• The information on the proposed merger that the merging UCITS and the receiving UCITS intend to provide to their respective investors

When the receiving UCITS is not established in Malta and once the authorization file is complete, the MFSAmust immediately transmit copies of the authorizationfile to the regulatory authority of the receiving UCITS home member state.

The MFSA shall inform the merging UCITS within 20 working days of submission of the complete authorization file whether or not the merger has beenauthorized. It shall also inform regulatory authority ofthe receiving UCITS home member state of its decision to approve or otherwise the merger.

11.3.2 The merging UCITS established in another member state and the receiving UCITS established in Malta

The MFSA must receive copies of the authorization file (except the prospectus and KIID of the receivingUCITS) from the regulatory authority of the merging UCITS home member state.

The MFSA and the regulatory authority of the mergingUCITS home member state will consider the potential impact of the proposed merger on the investor of bothmerging UCITS and receiving UCITS respectively in order to assess whether appropriate information isbeing provided to investors.

If necessary, the MFSA may require in writing and nolater than 15 working days of receipt of the authorization file that the receiving UCITS modifies the information to be provided to its investors.

The MFSA will inform the regulatory authority of the merging UCITS home member state within 20 working days of being notified thereof as to whether it is satisfied with such modified information to be provided to investors in the receiving UCITS.

11.4 Redomicilation of foreign entities to Malta

The Malta has legislative provisions allowing for inward and outward continuation of companies and thus body corporates may redomicile to Malta their business if:

• The corporate body is formed and registered in an approved jurisdiction• The corporate body is similar in nature to a company under the laws of Malta the laws of the country of incorporation and the rules of incorporation of the corporate body allow redomiciliation • The corporate body is not in the process of dissolution or winding up

For a foreign investment fund to redomicile to Malta,the following process would normally be followed:

• A corporate decision is made by the shareholders and/or governing body of the foreign investment fund to redomicile to Malta• If applicable, a notification is sent to the foreign regulator of the foreign investment fund• The fund documentation (e.g., prospectus) of the foreign investment funds is amended to comply with the law of Malta• Prior approval of the MFSA is obtained before the transfer (see Section 7)• Local service providers are appointed

See table on the next page for list of documents to be submitted to the MFSA as part of the redomiciliation.

• Recent copies of the audited financial statements of the foreign company• Copy of the (pre-redomiciliation) existing rules of incorporation (with details of the current directors) and offering documents of the foreign company• Signed resolution from the existing board of the foreign company confirming their intention to re-domicile to Malta, to apply for an investment fund Licence in favour of the company and that there are no regulatory issues relating to the said redomiciliation and no pending litigation or disputes and that the directors are not aware of any potential litigation or disputes• If there is a change in the composition of the board, a signed board of directors’ resolution from the new board (upon redomiciliation) confirming inter alia that: The directors endorse the application for an investment fund licence in favour of the company and that they have reviewed the final revised version of the prospectus/ offering document and assume responsibility thereof

Public companies

Same as above in addition to: • The most recent prospectus/ offering documentation, if instruments have been offered to the public• Evidence of consent given by the foreign stock exchange that business may be continued in Malta if company is listed• Evidence of the current members of the company

The Malta UCITS Investment Funds | 39

Privatecompanies

Documents for redomiciliation to Malta

12.1 Recognized incorporated cell companies (RICC)

The MFSA has introduced the “cellular concept” as a new vehicle for setting up Investment funds in Maltawhich caters in particular to fund platforms. Investment funds would be established as incorporated cells within the platform of a recognized cell company (RICC).

Similar to a multi-fund, the RICC platform provides forthe separation of the assets and liabilities between the RICC and each incorporated cell. The difference isthat in a RICC structure, liability is limited throughthe separate legal identity of each incorporated cell(as each cell has its separate legal personality), whereas in multi-fund investment fund, limitation ofliability is achieved through the option of segregation of assets and liabilities of each sub-fund stipulated byvirtue of the memorandum of association of the UCITS. The benefit of the RICC structure is that it allows for several types of licensed investment fundsto coexist under one platform while retaining separate features and separate legal patrimonieswhile each incorporated cell may benefit from certain cost savings through the centralization and standardization of contractual agreements.

40 | The Malta UCITS Investment Funds

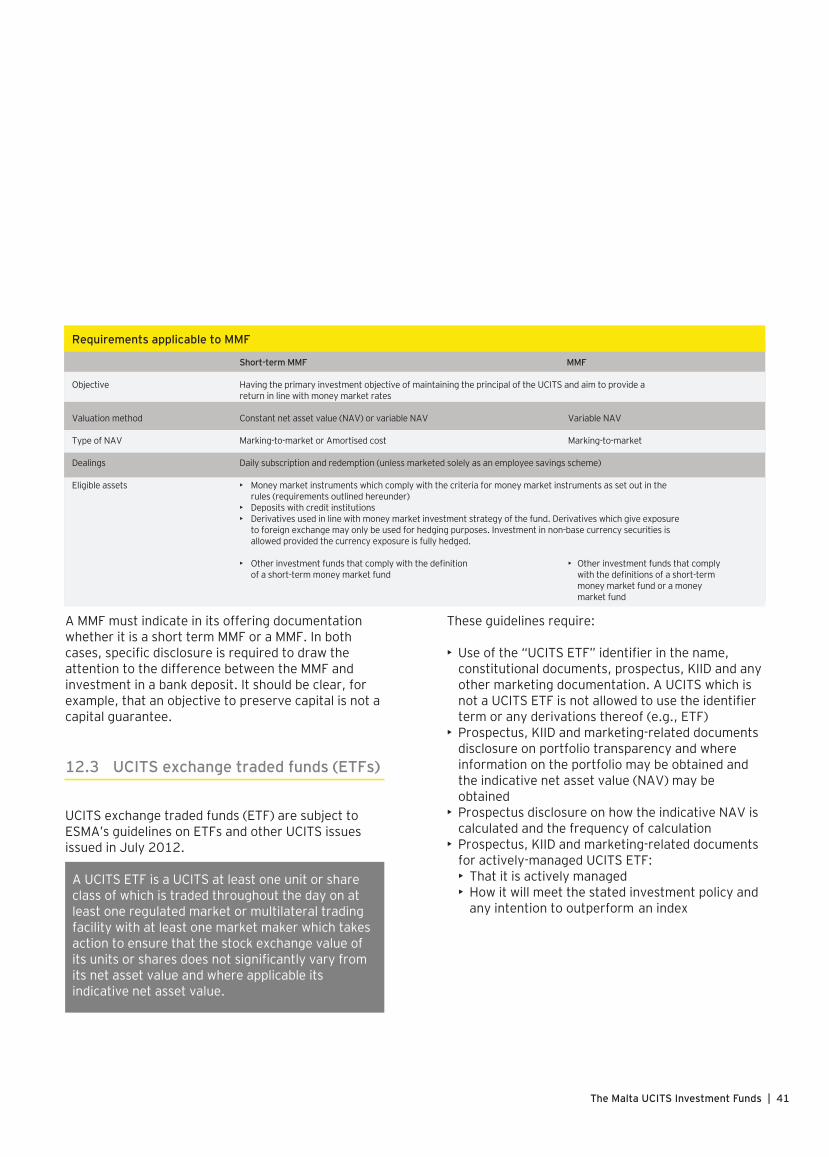

12.2 Money market funds

Money market funds (MMF) are subject to ESMA’s (previously CESR) guidelines on a common definition of European money market funds issued in May 2010.

In August 2014, ESMA issued an opinion on its reviewof the said guidelines.

ESMA’s guidelines set out a two-tiered approach for adefinition of European money market funds:

• Short term money market fund• Money market fund

Both short term MMFs and MMFs must comply with general guidelines and also have to comply with specific guidelines relating to their category.

EY supports asset managers and investment fund houses in the regulatory assessment and formation of bespoke investment funds.

12 Specific types of UCITS structures

The Malta UCITS Investment Funds | 41

A MMF must indicate in its offering documentation whether it is a short term MMF or a MMF. In both cases, specific disclosure is required to draw the attention to the difference between the MMF and investment in a bank deposit. It should be clear, for example, that an objective to preserve capital is not a capital guarantee.

12.3 UCITS exchange traded funds (ETFs)

UCITS exchange traded funds (ETF) are subject to ESMA’s guidelines on ETFs and other UCITS issues issued in July 2012.

A UCITS ETF is a UCITS at least one unit or share class of which is traded throughout the day on at least one regulated market or multilateral trading facility with at least one market maker which takes action to ensure that the stock exchange value of its units or shares does not significantly vary from its net asset value and where applicable its indicative net asset value.

These guidelines require:

• Use of the “UCITS ETF” identifier in the name, constitutional documents, prospectus, KIID and any other marketing documentation. A UCITS which is not a UCITS ETF is not allowed to use the identifier term or any derivations thereof (e.g., ETF)• Prospectus, KIID and marketing-related documents disclosure on portfolio transparency and where information on the portfolio may be obtained and the indicative net asset value (NAV) may be obtained• Prospectus disclosure on how the indicative NAV is calculated and the frequency of calculation• Prospectus, KIID and marketing-related documents for actively-managed UCITS ETF: • That it is actively managed • How it will meet the stated investment policy and any intention to outperform an index

Requirements applicable to MMF

Objective

Valuation method

Type of NAV

Dealings

Eligible assets

Short-term MMF MMF

Having the primary investment objective of maintaining the principal of the UCITS and aim to provide a return in line with money market rates

Constant net asset value (NAV) or variable NAV Variable NAV

Marking-to-market or Amortised cost Marking-to-market

Daily subscription and redemption (unless marketed solely as an employee savings scheme)

• Money market instruments which comply with the criteria for money market instruments as set out in the rules (requirements outlined hereunder)• Deposits with credit institutions• Derivatives used in line with money market investment strategy of the fund. Derivatives which give exposure to foreign exchange may only be used for hedging purposes. Investment in non-base currency securities is allowed provided the currency exposure is fully hedged.

• Other investment funds that comply with the definition • Other investment funds that comply of a short-term money market fund with the definitions of a short-term money market fund or a money market fund

• Treatment of secondary market investors: • Risk warning in prospectus and market-related documents on the effect on units purchased on the secondary market are generally not redeemable from the UCITS ETF • Units purchased on the secondary market cannot be sold directly back to UCITS ETF. Investors must buy and sell units/shares on a secondary market with the assistance of an intermediary (e.g., a stockbroker) and may incur fees for doing so. Investors may pay more than the current NAV when buying units and may receive less than the current NAV when selling them

12.4 Index-tracking UCITS

For index-tracking UCITS, ESMA’s guidelines on ETFs and other UCITS issues require:

• Prospectus disclosure on the description of the index and information on underlying components; how the index will be tracked and the implications of the chosen method for investors; anticipated level of tracking error; factors that are likely to affect the ability of index-tracking UCITS to track the performances of the index• Summary in KIID on how the index will be tracked and implications of any divergence with anticipated tracking error • Annual and half-yearly report disclosure on actual tracking error with annual report to disclose the actual divergence between anticipated and realised tracking error and difference in performance of UCITS and the performance of the index tracked

42 | The Malta UCITS Investment Funds

For index-tracking leverage UCITS, the guidelinesrequire:

• Prospectus and KIID disclosure on the leverage policy, how this is achieved (i.e., whether the leverage is at the level of the index or arises from the way in which the UCITS obtains exposure to the index), the cost of the leverage (where relevant) and the risks associated with this policy; a description of the impact of any reverse leverage if any; and a description of how the performance of the UCITS may differ significantly from the multiple of the index performance over the medium to long term• Compliance with limits and rules on global exposure using either the commitment approach or the relative VaR approach

A UCITS should not invest in a financial index which has a single component that has an impact on the overall index return which exceeds the relevant diversification requirements i.e., 20%/35%.

The Malta UCITS Investment Funds | 43

13.1 Investor information

A UCITS is required to publish:

• A prospectus and relevant offering supplement for each sub-fund (if a multi-fund UCITS)