Alternative UCITS Barometer - Hedge ConnectionCapital... · Introduction 2 ML Capital Asset...

14

Alternative UCITS Barometer Quarter 3, 2014

Transcript of Alternative UCITS Barometer - Hedge ConnectionCapital... · Introduction 2 ML Capital Asset...

Alternative UCITS Barometer

Quarter 3, 2014

Introduction

2

ML Capital Asset Management, the investment manager and promoter of the MontLake UCITS Platform, is delighted topresent the 15th edition of the quarterly ML Capital Alternative UCITS Barometer (Barometer).

The Barometer is designed to help identify and anticipate key trends in the demand for the major strategies within theAlternative UCITS sector.

The capital introductory team at ML Capital survey a diverse range of 60 investors who collectively manage almost $95billion and today invest upwards of $35 billion into Alternative UCITS, reflecting the widening of the investor base forregulated alternative products in Europe. Respondents range from insurance and pension funds to private bankingorganisations, with a significant constituent of financial advisers that deal with the primary source of Alternative UCITSinflows, the mid-net-worth investor.

Commenting on the highlights of the latest Barometer, John Lowry, Co - Founder & CIO of ML Capital;

“With markets near all-time highs, investors are increasingly looking for Multi-Strategy funds which have the ability todeliver returns less dependent on market movements. Our latest Barometer shows a sustained high level of interest forLong Short funds focussed on the following areas, US equities, Global equities and those that concentrate on investingin the Emerging Markets. In the non-equity sector, for the family offices, wealth managers and other institutions thatwe interact with, there is also a strong demand for less correlated strategies such as Global Macro and Multi-Strategyfunds.

With asset levels at all-time highs in the overall hedge fund industry, a large number of well-respected US managersare now expanding their product ranges through launching a regulated UCITS product to support the widening ofdemand for investment products that are not fully dependent on the direction of the stock-markets".

We hope that the Barometer will provide a useful insight into current appetite levels across some of the major sectorsof the regulated fund universe.

Should you have any questions then please do not hesitate to contact a member of our Cap Intro or Fund Hostingteams.

Cyril Delamare, CEO

Q3 Barometer Highlights

3

16% 2%

63%

18%

Participant Location

Continental Europe

Scandinavia

UK

Switzerland

Sharp Rise in Interest for Multi-Strategy Funds

The most dramatic result by far this quarter is for Multi-Strategy funds, which

show an almost five fold rise in the levels of demand over last quarters result.

There has been a large spike in the level of allocators to Alternative UCITS planning

to increase the size of their Multi-Strategy holdings this quarter. Almost half of our

respondents (47%) are looking to allocate to the space, with a cautious eye on the

relatively highly priced equity and bond markets.

Bullish views on both US and Global Long Short Funds

Highest level of interest for US Long Short strategies since the inception of the

Alternative UCITS Barometer. Following a drop in interest towards the tail end of

2013, sentiment towards the US L/S space has somewhat changed and interest has

rallied going into Q3.

Furthermore, whilst UK Long Short slides out of favour, 51% of respondents plan to

increase exposures to Global Long Short Funds.

Healthy Upswing towards Emerging Markets

There is a healthy move back towards the Emerging Markets shown this quarter.

Our research has highlighted that there is emphatic support for Globally diversified

funds (39%) as opposed to the more targeted regional products.

16%

18%

12%4%

49%

Participant Type

Bank/institution

Family Office

Fund of Funds

Private bank

Wealth manager / IFA

4

Looking to launch a regulated fund?

ML Capital can help you.

Whether it is a standalone fund structure or a new sub-fund of an existing umbrella,ML Capital’s structuring team will be able to advise you on the best way forward.

Investment Manager and Promoter to Regulated Funds

Dedicated UCITS platform with access to top tier service providers

Structuring expertise - Re-domiciliation, Mergers

UCITS & QIAIF infrastructure support, enabling you to focus on your investment

strategy

Cross border distribution expertise and fund registration

Experienced sales team for retail and institutional distribution

ML Capital: your one stop shop for investment managers looking to launch a Europeanregulated fund.

For more information please contact [email protected] or +44 207 925 2748

Long/Short Equities Trending

5

Global Long/Short

US Long/Short

UK Long/Short

Japan Long/Short

• MORE • SAME • LESS • MORE • LESS

51%35%

14%

61%31%

8%

8%

69%

22%

0%

10%

20%

30%

40%

50%

60%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Pe

rce

nta

ge C

han

ge

0%

10%

20%

30%

40%

50%

60%

70%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Pe

rce

nta

ge C

han

ge

0%

10%

20%

30%

40%

50%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Pe

rce

nta

ge C

han

ge

16%

65%

18%

0%

10%

20%

30%

40%

50%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Pe

rce

nta

ge C

han

ge

Long/Short Equities Trending

European Long/Short

6

This quarter, most Equity strategies continue to receive substantial interest from investors, with the biggest spike in demand

experienced for US and Global Long Short funds. A slight majority (51%) are forecasting that they will be moving more of their asset

base towards Globally diversified products this quarter, whilst over 60% plan to further increase their holdings of US Equity funds.

After such a strong and sustained rally in equities and with global stock markets near or at their all-time highs, a degree of profit

taking can be regarded as healthy. Whilst central banks continue to support stocks globally, some investors make the point that

relative to bond prices equity markets continue to offer some value. Nevertheless, the next phase of the market cycle may well favour

managers that adopt a more opportunistic, trading focused investment approach.

Demand levels for European strategies, although still strong, have fallen back to a degree this quarter. Last time out, European funds

were the most popular of all Equity strategies but have now been superseded by both the US and Global categories. Clearly many

investors have significant concerns over the ongoing Eurozone situation. Despite these issues, the demand levels for European

focussed Equity funds remains healthy with almost half of respondents (47%) expecting to raise their commitment levels.

The fortunes of funds dedicated to the UK and Japan appear to be going in opposite directions, with a healthy upward spike towards

Japan funds contrasting with a more muted interest level for UK strategies.

Commentary

47%47%

6%

0%

10%

20%

30%

40%

50%

60%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Pe

rce

nta

ge C

han

ge• MORE • SAME • LESS • MORE • LESS

Global Emerging

Pan-Asia

Commentary

Latin America

7

Emerging Markets Trending

A significant trend back towards Emerging Markets, with some respondents viewing the current levels as an interesting entry or re-

entry point following a difficult 2 year period. While still off its historic level of demand of 60% at the start of 2013, today almost 2 in

5 of respondents are looking to up their exposure levels to globally diversified EM products. However, somewhat of a contrarian or

controversial viewpoint, as at the same time as 40% are looking to increase, one third of investors are in fact planning to reduce

exposures to the very same strategy. It will be very interesting to see who has called this one correctly over the coming months.

Emerging market economies are beginning to see the positive knock on effects from the economic recoveries in the developed world,

led by the US and the UK. Many emerging markets have seen significant and painful depreciation in their currencies over the past 18

months. These devaluations have resulted in greatly improved levels of export competitiveness which should result in a strong export

lead recovery in many of the economies of the developing world. Globally diversified funds are by far and away the most popular type

of EM product, with a far lower level of interest shown to dedicated Asian and Latin American products, with the Lat Am space only

showing a 2% level of interest.

39%

29%

33%

8%

67%

24%

2%

51%47%

0%

10%

20%

30%

40%

50%

60%

70%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Pe

rce

nta

ge C

han

ge

0%

10%

20%

30%

40%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Pe

rce

nta

ge C

han

ge

0%

10%

20%

30%

40%

50%

60%

70%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Pe

rce

nta

ge C

han

ge• MORE • SAME • LESS • MORE • LESS

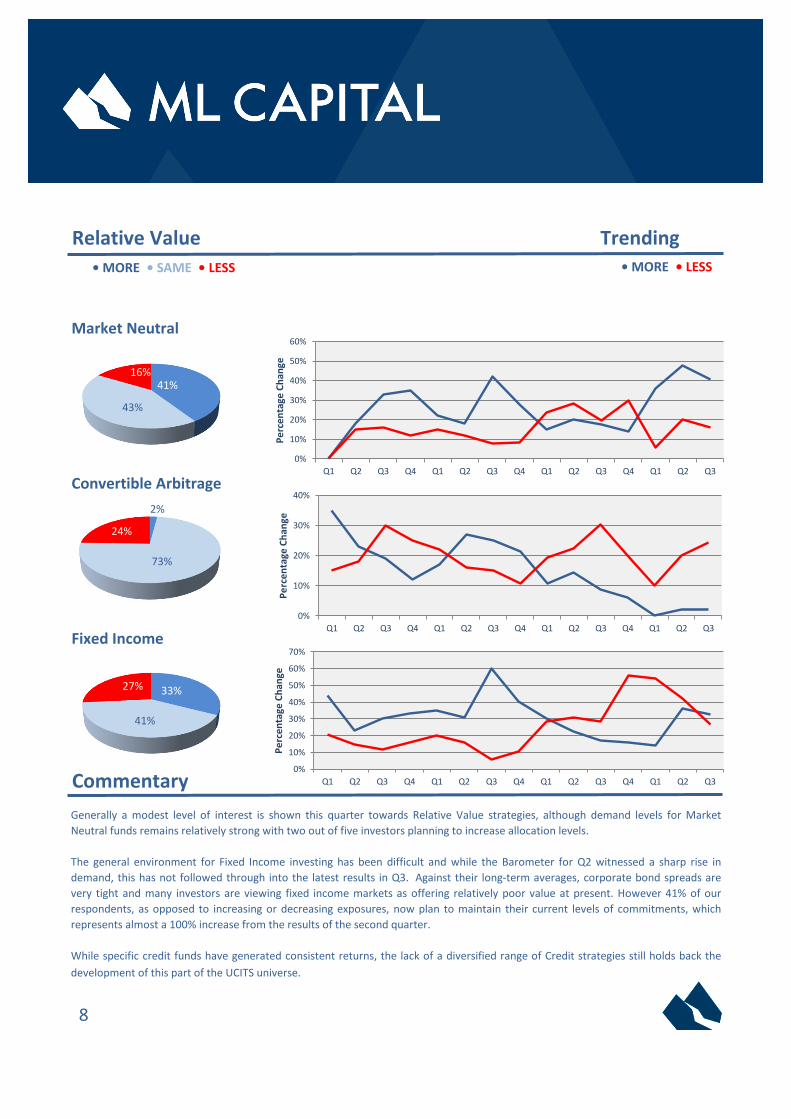

Fixed Income

Relative Value Trending

Market Neutral

Convertible Arbitrage

Commentary

Generally a modest level of interest is shown this quarter towards Relative Value strategies, although demand levels for Market

Neutral funds remains relatively strong with two out of five investors planning to increase allocation levels.

The general environment for Fixed Income investing has been difficult and while the Barometer for Q2 witnessed a sharp rise in

demand, this has not followed through into the latest results in Q3. Against their long-term averages, corporate bond spreads are

very tight and many investors are viewing fixed income markets as offering relatively poor value at present. However 41% of our

respondents, as opposed to increasing or decreasing exposures, now plan to maintain their current levels of commitments, which

represents almost a 100% increase from the results of the second quarter.

While specific credit funds have generated consistent returns, the lack of a diversified range of Credit strategies still holds back the

development of this part of the UCITS universe.

8

41%

43%

16%

73%

24%

2%

33%

41%

27%

0%

10%

20%

30%

40%

50%

60%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Pe

rce

nta

ge C

han

ge

0%

10%

20%

30%

40%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Pe

rce

nta

ge C

han

ge

0%

10%

20%

30%

40%

50%

60%

70%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Pe

rce

nta

ge C

han

ge• MORE • SAME • LESS • MORE • LESS

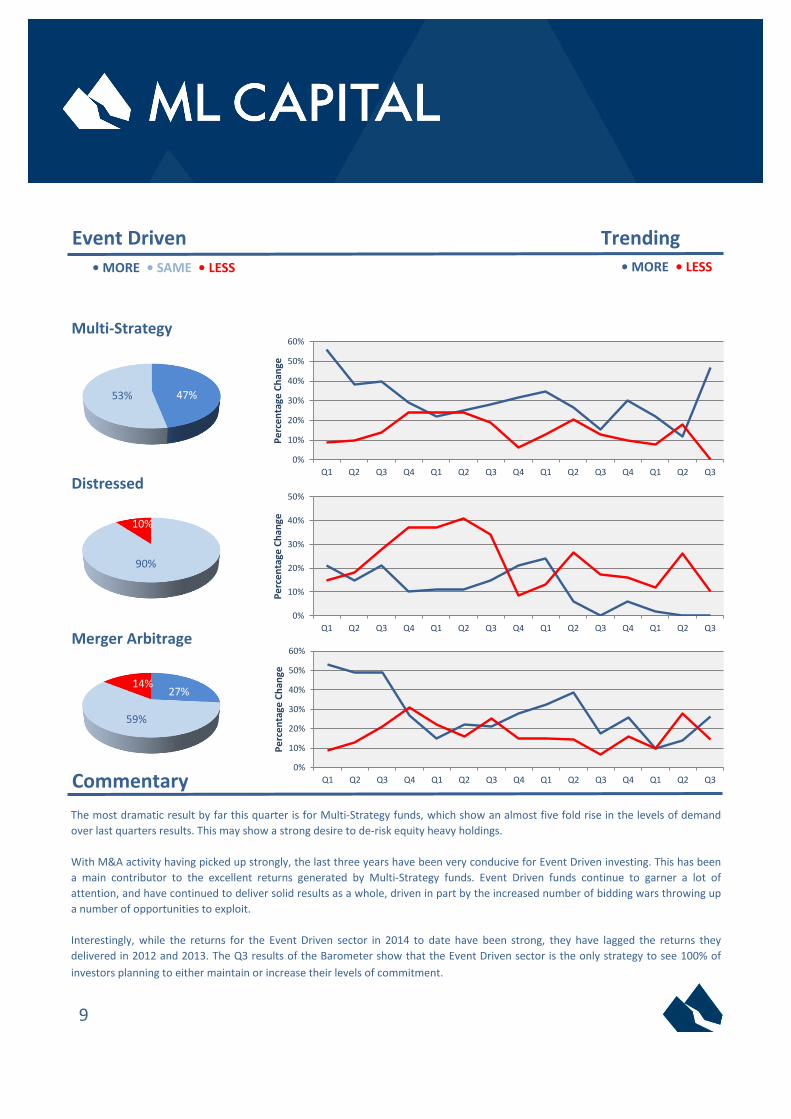

Commentary

Distressed

Event Driven Trending

Multi-Strategy

Merger Arbitrage

9

The most dramatic result by far this quarter is for Multi-Strategy funds, which show an almost five fold rise in the levels of demand

over last quarters results. This may show a strong desire to de-risk equity heavy holdings.

With M&A activity having picked up strongly, the last three years have been very conducive for Event Driven investing. This has been

a main contributor to the excellent returns generated by Multi-Strategy funds. Event Driven funds continue to garner a lot of

attention, and have continued to deliver solid results as a whole, driven in part by the increased number of bidding wars throwing up

a number of opportunities to exploit.

Interestingly, while the returns for the Event Driven sector in 2014 to date have been strong, they have lagged the returns they

delivered in 2012 and 2013. The Q3 results of the Barometer show that the Event Driven sector is the only strategy to see 100% of

investors planning to either maintain or increase their levels of commitment.

47%53%

90%

10%

27%

59%

14%

0%

10%

20%

30%

40%

50%

60%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Pe

rce

nta

ge C

han

ge

0%

10%

20%

30%

40%

50%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Pe

rce

nta

ge C

han

ge

0%

10%

20%

30%

40%

50%

60%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Pe

rce

nta

ge C

han

ge• MORE • SAME • LESS • MORE • LESS

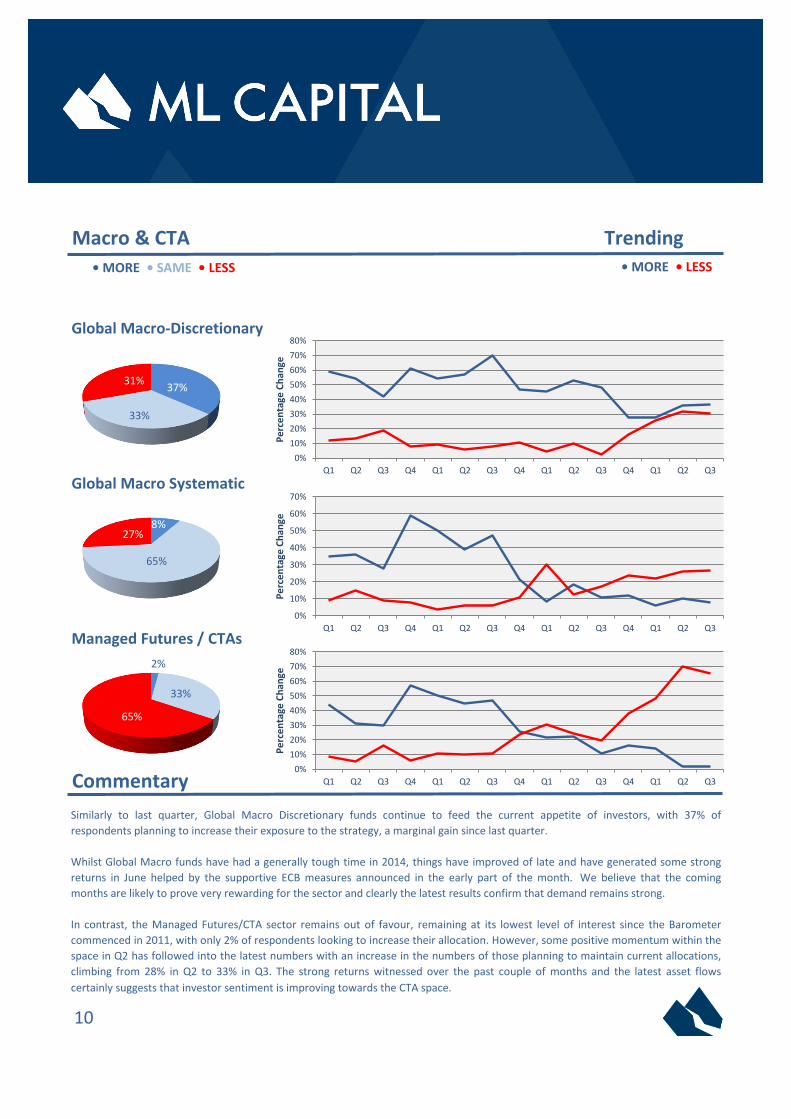

10

Managed Futures / CTAs

Commentary

Macro & CTA Trending

Global Macro-Discretionary

Global Macro Systematic

Similarly to last quarter, Global Macro Discretionary funds continue to feed the current appetite of investors, with 37% of

respondents planning to increase their exposure to the strategy, a marginal gain since last quarter.

Whilst Global Macro funds have had a generally tough time in 2014, things have improved of late and have generated some strong

returns in June helped by the supportive ECB measures announced in the early part of the month. We believe that the coming

months are likely to prove very rewarding for the sector and clearly the latest results confirm that demand remains strong.

In contrast, the Managed Futures/CTA sector remains out of favour, remaining at its lowest level of interest since the Barometer

commenced in 2011, with only 2% of respondents looking to increase their allocation. However, some positive momentum within the

space in Q2 has followed into the latest numbers with an increase in the numbers of those planning to maintain current allocations,

climbing from 28% in Q2 to 33% in Q3. The strong returns witnessed over the past couple of months and the latest asset flows

certainly suggests that investor sentiment is improving towards the CTA space.

37%

33%

31%

8%

65%

27%

2%

33%

65%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Pe

rce

nta

ge C

han

ge

0%

10%

20%

30%

40%

50%

60%

70%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Pe

rce

nta

ge C

han

ge

0%

10%

20%

30%

40%

50%

60%

70%

80%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Pe

rce

nta

ge C

han

ge• MORE • SAME • LESS • MORE • LESS

Global Macro Discretio'

Market Neutral 40.8% 42.9% 16.3%

Multi-Strategy 46.9% 53.1% 0.0%

Global Macro Systemat' 8.2% 65.3% 26.5%

More Same Less

Macro & CTA

Distressed 0.0% 89.8%

Managed Futures/CTA

Source Data

More Same Less

Global L/S Equity

UK L/S Equity

US L/S Equity

European L/S Equity

Japan L/S Equity

51.0%

8.2%

34.7% 14.3%

69.4% 22.4%

61.2% 30.6%

More Same

11

Convertible Arbitrage 2.0% 73.5% 24.5%

More Same Less

2.0% 32.7% 65.3%

36.7% 32.7% 30.6%

10.2%

Merger Arbitrage 26.5%

18.4%

Latin America

8.2%

46.9%

Long / Short EquityEmerging Markets

Relative Value

More Same

46.9%

Less

Global Emerging 38.8% 28.6% 32.7%

2.0% 51.0%

Pan-Asia 8.2% 67.3% 24.5%

6.1%

16.3% 65.3%

Lowest Surveyed Hedge Allocation USD $ 25 m

Highest Surveyed Alt UCITS Allocation USD $ 6 bn

Lowest Surveyed Alt UCITS Allocation USD $ 10 m

Highest Surveyed Avg Alt UCITS Ticket USD $ 302 m

Lowest Surveyed Avg Alt UCITS Ticket USD $ 50 k

Highest Surveyed Hedge Allocation USD $250 bn

Barometer Participants

Barometer Surveyed Alt UCITS Assets USD $ 35 bn

59.2% 14.3%

Less

Barometer Surveyed Hedge Fund Assets USD $ 513 bn

Further Statistics

Total Press Reported Hedge Fund Assets USD $3,000 bn

Press Reported

Total Press Reported Alt UCITS Assets USD $ 265 bn

Event Driven

Fixed Income 32.7% 40.8% 26.5%

46.9%

About ML Capital

About The MontLake UCITS Platform

12

ML Capital is a forward looking and leading independent investment management firm specializing in European regulated fundstructures, headquartered in Dublin, Ireland. As an award winning platform provider, we partner with the very best of investmentmanagers to bring to market the latest most appropriate fund structures to comply with the raft of incoming regulatoryrequirements, whilst meeting the ever increasing expectations of investors.

ML Capital handles all aspects of the fund structuring and launch on investment managers’ behalf. Through our dedicated networkwe offer fund sales and distribution if required and have had comprehensive coverage of investors in all key European markets forthe past 20 years.

Our goal is to provide the most appropriate fund structures to maximize distribution opportunities across all key markets. Oursolutions bring together market leading service providers with some of the very best minds in the regulated fund space; providingwell managed European investment products with the highest levels of service and governance. We ensure that all incominginvestors and partners come in with the full knowledge that they are investing into structures that are designed to protect and

preserve investor interest.

The MontLake UCITS Platform, domiciled in Ireland and regulated by the Central Bank of Ireland provides investment managerswith a turnkey solution for launching a UCITS fund under its umbrella structure. Typical time to market is 10 weeks, or less, withthe platform offering immediate access to a wide range of investors through ML Capital’s distribution network.

Funds placed on the platform by ML Capital will benefit from top-tier service providers including Citi for custody, administrationand trustee services, KPMG for audit, and Bridge Consulting for oversight and directorships. ML Capital has also ensured thatmanagers utilising the MontLake UCITS Platform will have unfettered access to a network of the leading prime brokerage firms.

For more information on ML Capital please visit our website www.mlcapital.com or our platform website www.montlakeucits.com.

IRELAND

26 Upper Fitzwilliam Street Dublin 2Ireland

+353 1535 0912

MALTA

Suite 5Tigne PalaceBisazza StreetSliema

+356 2133 4801

www.mlcapital.com

SWITZERLAND

Rue de la Cloche 81201Geneva

+41 (0) 22 318 56 70

UK

30 St James's SquareLondonSW1Y 4AL

+44 (0)207 9252 748

DISCLAIMER

14

FOR INVESTMENT PROFESSIONALS ONLY

This financial promotion is issued by ML Capital Limited. This document is not intended as an

offer to acquire or dispose of any security. Information given in it has been obtained from, or

based upon, sources believed by us to be reliable and accurate although ML does not accept

liability for the accuracy of the contents. This information is not intended to constitute a basis

for any specific investment decision.

For Addressee only. The distribution of this report does not constitute an offer or solicitation.

Past performance is not a guide to future performance. The value of investments can fall as

well as rise. You should ensure you understand the risk profile of the products or services you

plan to purchase. The services provided by ML Capital Limited are available only to investors

who come within the category of the Eligible Counterparty or Professional Client as defined in

the Financial Services Authority’s Handbook they are not available to individual investors,

who should not rely on this communication. Information given in this document has been

obtained from, or based upon, sources believed by us to be reliable and accurate although

ML Capital does not accept liability for the accuracy of the contents. ML Capital does not

offer investment advice or make recommendations regarding investments.