“The International Financial Crisis and Greece” - hba.gr€œThe International Financial Crisis...

23

1 G. Hardouvelis, 18/11/2008 “ “ The International The International Financial Crisis and Financial Crisis and Greece” Greece” Gikas A. Hardouvelis Gikas A. Hardouvelis * * Athens, November 18, 2008 Athens, November 18, 2008 ECONOMIA CONFERENCE ECONOMIA CONFERENCE Athens, Athens, Karantzas Karantzas Megaron Megaron * * Chief Economist, Eurobank EFG Group Chief Economist, Eurobank EFG Group Professor, Department of Banking and Financial Management, Un. o Professor, Department of Banking and Financial Management, Un. o f Piraeus f Piraeus

Transcript of “The International Financial Crisis and Greece” - hba.gr€œThe International Financial Crisis...

1G. Hardouvelis, 18/11/2008

““The International The International Financial Crisis and Financial Crisis and

Greece”Greece”

Gikas A. HardouvelisGikas A. Hardouvelis**Athens, November 18, 2008Athens, November 18, 2008

ECONOMIA CONFERENCEECONOMIA CONFERENCEAthens, Athens, KarantzasKarantzas MegaronMegaron

* * Chief Economist, Eurobank EFG GroupChief Economist, Eurobank EFG GroupProfessor, Department of Banking and Financial Management, Un. oProfessor, Department of Banking and Financial Management, Un. of Piraeusf Piraeus

2G. Hardouvelis, 18/11/2008

I. Will Greece keep convergingto the EU-15 average despite the crisis?

Real growth rates, 1990–2009

Investment: the main driver of growth, with growth rates higher than those of consumptionUntil 2005, investment in equipment higher than investment in residential constructionIs the party over now?

Source: European Commission

GDP per capitaPPS, EU-15=100

5.04.6

0.8

1.6

2.6

0.1

4.2

3.8

2.1

-1.6

0.7

2.0

2.43.6

3.4 3.4

4.5 4.5

4.0 3.3

2.5

3.9

0.9

2.8

1.4

-0.8

2.62.5

1.5

2.6 2.83.0

3.8

1.9

2.1

1.3

-2

-1

0

1

2

3

4

5

6

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

% Greece

EA

EU forecastsfor 2009

71.0

91.3

50556065707580859095

1995 2009

3G. Hardouvelis, 18/11/2008

I. Greece at a crossroads

• Greece’s problems are long-term, with competitiveness carrying a large blame

• Surprisingly, Greece can withstand the crisis better than its European counterparts, thanks to its relatively strong banking system, with a projected 2009 rate of growth slightly above 2%

• Yet, if officials remain sluggish to the elevated demands for active policy, the crisis may also bring a nightmare scenario of negative growth

• If the recession scenario prevails, then subsequently the lack of policy tools and the long-run problems are bound to depress the economy for a long time

4G. Hardouvelis, 18/11/2008

II.Competitiveness:

The Greek Economy’sDeepest Problem

5G. Hardouvelis, 18/11/2008

II. Competitiveness and Ease of Doing Business

Competitiveness is the deepest thorn in the Greek economyWorld Bank - Doing Business 2009 report: Greece ranks 96th in 2008 among 181 economies in the ease of doing business, rising 10 places from the 106th in 2007. Greece remains last among EU-27 countries

No 1: Singapore

Source: WEF

Ease of Doing Business Rankings 2007 – 2008(rankings in reverse order)

Improvement

Deterioration

0

20

40

60

80

100

120

140

160

180

200

0 20 40 60 80 100 120 140 160 180 200

2007

2008

Greece (+10)

No. 181: Congo

Ease of...Doing

Business 2008rank

Change in rankfrom 2007

Doing Business 96 +10Starting a Business 133 +17Dealing with Construction Permits 45 +1

Employing Workers 133 +10

Registering Property 101 -5

Getting Credit 109 -7

Protecting Investors 150 +11

Paying Taxes 62 +32Trading Across Borders 70 -4

Enforcing Contracts 85 -1

Closing a Business 41 0

6G. Hardouvelis, 18/11/2008

ΙI. Competitiveness is way below Greece’s level of development

Source: WEF, IMF

GDP per capita, in $ PPP

Co

mp

eti

tiven

ess

Ran

kin

gs,

(rev

erse

d or

der)

Greece

Gap: 54 placesBrunei

NorwaySingaporeNew Zealand

ThailandGeorgia

y = 31,13Ln(x) - 180,36R2 = 0,5871

0

20

40

60

80

100

120

140

160

180

200

0 10.000 20.000 30.000 40.000 50.000

Based on its standard of living, Greece should have ranked 42nd instead of 96th

7G. Hardouvelis, 18/11/2008

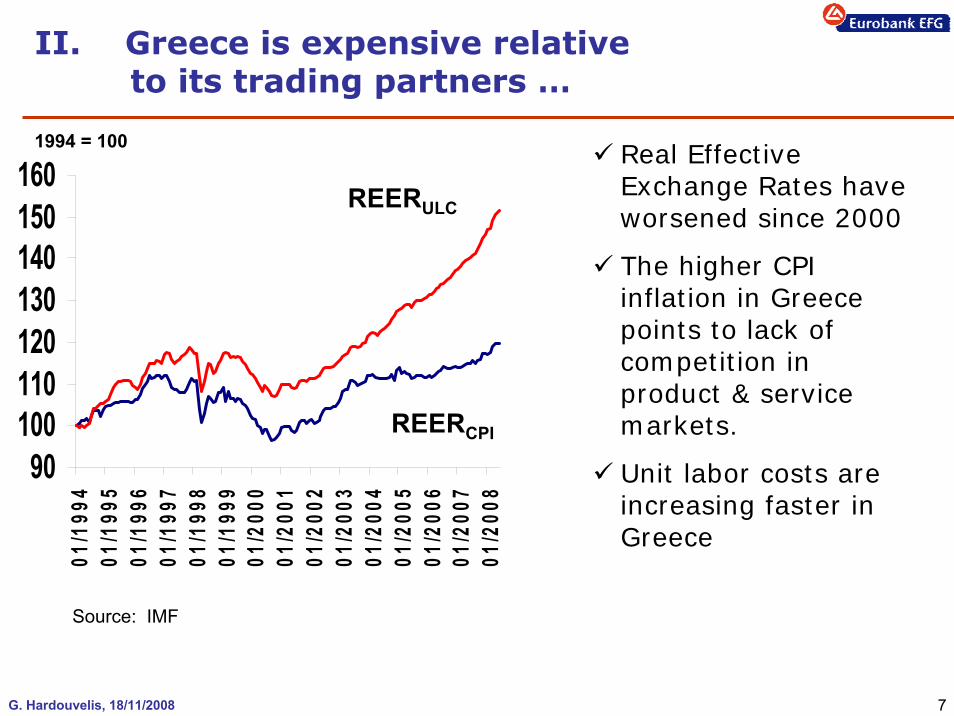

ΙI. Greece is expensive relative to its trading partners …

90100110120130140150160

01/1

994

01/1

995

01/1

996

01/1

997

01/1

998

01/1

999

01/2

000

01/2

001

01/2

002

01/2

003

01/2

004

01/2

005

01/2

006

01/2

007

01/2

008

REERULC

REERCPI

1994 = 100 Real Effective Exchange Rates have worsened since 2000

The higher CPI inflation in Greece points to lack of competition in product & service markets.

Unit labor costs are increasing faster in Greece

Source: IMF

8G. Hardouvelis, 18/11/2008

II. … hence, Greece’s current account is getting worse

CA deficit has tripled relative to the pre-EMU period, while the growth in aggregate demand is the same as beforeCA deficit can lead to an abrupt future recession

Source: Bank of Greece

-5.8 -7.4-11.1

-6.6

-14.1

-2.8 -7.8 -7.3 -6.8-3.8-3.9

-26

-21

-16

-11

-6

-1

4

9

14

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007-26

-21

-16

-11

-6

-1

4

9

14

Income ServicesGoods TransfersCurrent Account Balance

% GDP % GDP

9G. Hardouvelis, 18/11/2008

III.

The global financial crisis

and the relative position

of the Greek financial system

10G. Hardouvelis, 18/11/2008

III. How large is the short-run correction? The two problems of the global crisis

1) Insolvency2) Lack of liquidity

The next 15 months will provide a stress test of the Greek economyTwo problems underpin the global financial crisis:

Fortunately, structural reforms did occur in the Greek banking sector and Greek banks are very strong and healthy relative to their European peers, i.e., are well-capitalized

Yet, Greek banks are affected by the second factor, lack of liquidity

Which may lead to de-leveraging, i.e. the transmission of the crisis to the real economy

11G. Hardouvelis, 18/11/2008

III. Insolvency: Getting better

Total Write-downs: $ 708.5Total Capital Raised: $ 713.7Total Gap: $ -5.2

334

232

24

235

176

22

99

56

20

50100150200250300350

US Europe Asia

Writedowns Capital Raised Gap

bn USD

Total Writedowns: $ 590.2Total Capital Raised: $ 433.7Total Gap: $ 156.5

Sept. 30, 2008

Source: Bloomberg

The gap between total write-downs and capital increases has declined sharply in recent weeks due to governments’ recapitalizationsIMF: Estimates write-downs for all FIs to reach $1.4 trillion

Banking sector only

426

255

28

377

296

4149

-41-13

-90-1070

150230310390

US Europe Asia

Writedowns Capital Raised Gap

bn USDNov.18, 2008

12G. Hardouvelis, 18/11/2008

III. Insolvency: Greek banks better capitalized than most European banks

0123456789

Germ

any

Switz

erla

ndFr

ance

Swed

en

Denm

ark UK

Belgiu

mIc

elan

dSpa

in

Portu

gal

Norw

ayIr

elan

dFi

nland

Austr

ia

Ital

y Gre

ece US

30/6/2008

%

Best:EFG Intern/al 13.52% in Switzerland

Worst:DEXIA 1.67%in Belgium

Ranking of individual banks

Capital / Asset Ratio

13G. Hardouvelis, 18/11/2008

Euro Area U.S.A.III. Liquidity: Worsening not yet solved in Europe

020406080

100120140160180

May

-07

Jun-

07Ju

l-07

Aug

-07

Sep-

07O

ct-0

7N

ov-0

7D

ec-0

7Ja

n-08

Feb-

08M

ar-0

8A

pr-0

8M

ay-0

8Ju

n-08

Jul-0

8A

ug-0

8Se

p-08

Oct

-08

Nov

-08

17/11/2008: 92.1

10/10/2008: 162.1

1m Euribor - EONIA

0

50

100

150

200

250

300

350

400

May

-07

Jun-

07Ju

l-07

Aug

-07

Sep-

07O

ct-0

7N

ov-0

7D

ec-0

7Ja

n-08

Feb-

08M

ar-0

8A

pr-0

8M

ay-0

8Ju

n-08

Jul-0

8A

ug-0

8Se

p-08

Oct

-08

Nov

-08

17/11/2008: 99.6

10/10/2008: 337.8

1m Libor - OIS

Uncovered minus covered 1-month inter-bank rates

0

20

40

60

80

100

120

May

-07

Jun-

07Ju

l-07

Aug

-07

Sep-

07O

ct-0

7N

ov-0

7D

ec-0

7Ja

n-08

Feb-

08M

ar-0

8A

pr-0

8M

ay-0

8Ju

n-08

Jul-0

8A

ug-0

8Se

p-08

Oct

-08

Nov

-08

17/11/2008: 22.0

8/10/2008: 105.1

1w Euribor - EONIA

0

50

100

150

200

250

300

350

400

May

-07

Jun-

07Ju

l-07

Aug

-07

Sep-

07O

ct-0

7N

ov-0

7D

ec-0

7Ja

n-08

Feb-

08M

ar-0

8A

pr-0

8M

ay-0

8Ju

n-08

Jul-0

8A

ug-0

8Se

p-08

Oct

-08

Nov

-08

17/11/2008: 47.0

13/10/2008: 346.4

Uncovered minus covered 1-week inter-bank rates

1w Libor - OIS

14G. Hardouvelis, 18/11/2008

III. Liquidity: European banks are hoarding cash

0

50

100

150

200

250

300

Jun-

07

Jul-0

7

Aug

-07

Sep-

07

Oct

-07

Nov

-07

Dec

-07

Jan-

08

Feb-

08

Mar

-08

Apr

-08

May

-08

Jun-

08

Jul-0

8

Aug

-08

Sep-

08

Oct

-08

Nov

-08

19/9/2008: € 1.8 bn

7/11/2008: € 225.5 bn

EUR Billion

Source: ECB

Deposit Facility

15G. Hardouvelis, 18/11/2008

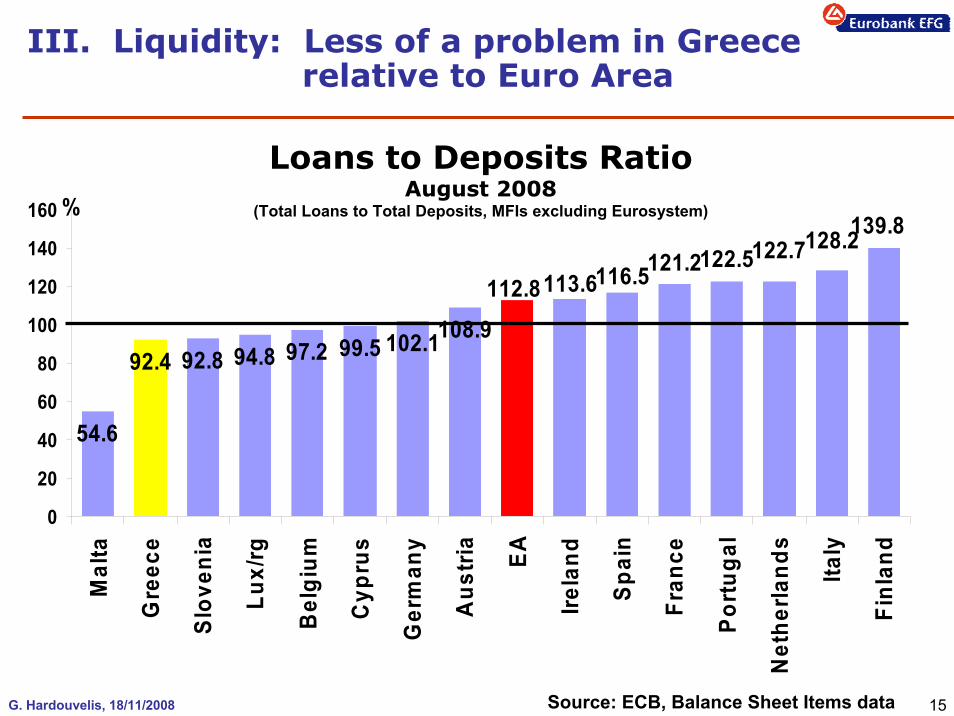

ΙII. Liquidity: Less of a problem in Greece relative to Euro Area

Source: ECB, Balance Sheet Items data

Loans to Deposits RatioAugust 2008

(Total Loans to Total Deposits, MFIs excluding Eurosystem)

54.6

92.4 92.8 94.8 97.2 99.5 102.1108.9

139.8128.2122.7122.5121.2116.5113.6112.8

0

20

40

60

80

100

120

140

160

Mal

ta

Gre

ece

Slov

enia

Lux/

rg

Bel

gium

Cyp

rus

Ger

man

y

Aus

tria

EA

Irela

nd

Spai

n

Fran

ce

Portu

gal

Net

herla

nds

Italy

Finl

and

%

16G. Hardouvelis, 18/11/2008

III. Rescue measures …

Greece has offered half the EU-27 package

Measures have to be voted into Laws to be operational. Laggards as of 17/11/2008: Greece & Austria

Then, we hope to see renewed liquidity in the inter-bank market

Package Amount

% of 2009 GDP

PartialAdoption

Italy € 40 bn 2.5%

Belgium € 9.7 bn 2.7%

US $ 700 bn 4.8%

Greece € 28 bn 10.8% NOPortugal € 20 bn 11.6%

Spain € 150 bn 13.4%

France € 360 bn 18.0%

Germany € 500 bn 19.5%

UK £ 500 bn 33.8%

Austria € 100 bn 34.2% NONetherlands € 220 bn 36.3%

Sweden SEK 1,500 bn 47.7%

Ireland € 400 bn 214.8%Total EU-27 € 2,580 bn 20.0%

17G. Hardouvelis, 18/11/2008

* Sorted from largest (=1) to smallest (=13)

III. … related to the size of the problem

0123456789

1011121314

0 2 4 6 8 10

Greece

Italy

US

Spain

Portugal

Austria

Ireland

Germany

France

UK

Sweden

Belgium

Netherlands

HIGH PROBLEMHIGH PACKAGE

LOW PROBLEMLOW PACKAGE

Capital / Asset Ratio (%)

y = 2.28 + 0.88xR2 = 20%

Ran

kin

g o

f re

scu

e m

easu

res/

GD

P*

18G. Hardouvelis, 18/11/2008

IV.

How much will Greecebe affected by the crisis

in 2009?

Growth slowdownA nightmare scenario can be avoided only through active policy intervention

19G. Hardouvelis, 18/11/2008

ΙV. Greece: Channels of negative influence

1) Lower economic activity abroad → less exports, lower tourist receipts, less foreign buying of property, lower shipping rates

2) Higher interest rates due to liquidity considerations → less credit expansion, lower consumption & investment

Greece will avoid:

Large bank failures and abrupt restriction of credit due to solvency reasons to the same degree observed abroad

9,00

9,50

10,00

10,50

11,00

11,50

12,00

Μαϊ-0

4Αυ

γ-04

Νοε-0

4Φε

β-05

Μαϊ-0

5Αυ

γ-05

Νοε-0

5Φε

β-06

Μαϊ-0

6Αυ

γ-06

Νοε-0

6Φε

β-07

Μαϊ-0

7Αυ

γ-07

Νοε-0

7Φε

β-08

Μαϊ-0

8Αυ

γ-08

Bill

ions Jan 2008 - Aug 2008: 5% yoy

Tourist receipts

€ bn

0100020003000400050006000700080009000

10000110001200013000

Νοε

-99

Μαρ

-00

Ιουλ

-00

Νοε

-00

Μαρ

-01

Ιουλ

-01

Νοε

-01

Μαρ

-02

Ιουλ

-02

Νοε

-02

Μαρ

-03

Ιουλ

-03

Νοε

-03

Μαρ

-04

Ιουλ

-04

Νοε

-04

Μαρ

-05

Ιουλ

-05

Νοε

-05

Μαρ

-06

Ιουλ

-06

Νοε

-06

Μαρ

-07

Ιουλ

-07

Νοε

-07

Μαρ

-08

Ιουλ

-08

Νοε

-08

17/11/2008: 856

20/5/2008: 11793

Baltic Dry Index

20G. Hardouvelis, 18/11/2008

IV. Bearish markets are harsh on Greece

Recent increase in gov. bond spread is consistent with historical behavior (thus not due to the package): It is explained by similar increases in other EA spreads plus EMBI+

Markets do not see the better position of Greek banks: Banking stocks hard hit

Nov 17: GR 33.04EA 32.97USA 38.44

30

40

50

60

70

80

90

100

110

120

29/6

/200

7

29/7

/200

7

29/8

/200

7

29/9

/200

7

29/1

0/20

07

29/1

1/20

07

29/1

2/20

07

29/1

/200

8

29/2

/200

8

29/3

/200

8

29/4

/200

8

29/5

/200

8

29/6

/200

8

29/7

/200

8

29/8

/200

8

29/9

/200

8

29/1

0/20

08

Greece EuroArea USA

Banking Stock indices since 29/6/2007

020406080

100120140160180

May

-07

Jul-0

7

Sep-

07

Nov

-07

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep-

08

Nov

-08

b.p.

17/3/2008: 71.0 b.p.

17/11/2008: 148.1 b.p.

29/6/2007: 25.0 b.p.

10-y Gov. Bond Spread: Greece-Germany

21G. Hardouvelis, 18/11/2008

IV. Greece: Will the good scenario prevail?

THE GOOD SCENARIO:yoy growth in constant prices

Weights(2007) EU 2008 EU 2009 GH 2009

GDP 100.0% 3.1 2.5 2.1

Pr. Consumption 71.2% 2.6 2.2 2.0

Pub. Consumption 16.7% 2.9 2.7 2.4

Investment 22.5% 3.2 2.8 2.1

Exports 23.0% 4.2 3.1 2.6

Imports 33.5% 2.6 2.5 2.1

HCPI 4.4 3.5 3.3

Budget deficit (% GDP) -2.5 -2.2 -2.9

Public debt (% GDP) 93.4 92.2 93.0

Unemployment rate 9.0 9.2 8.7

Current account (% GDP) -14.3 -15.0 -14.0

YES, if: 1. Loan expansion resumes by year-end2. Investment growth fills in the slack3. Consumption growth declines and imports decline

for a longer period than the current global recession

22G. Hardouvelis, 18/11/2008

V. ConclusionsThe current crisis has delayed affecting Greece because of the health of its financial sector. Is the worst in front of us?Two possibilities for 2009:I. Good scenario of growth slightly > 2%,II. Nightmare scenario of growth < 0, as past experience shows that

Greek recessions are the worst ones in the OECD, with a total mean output loss of -6.45% of GDP (2 times bigger the mean OECD country loss and 3 times the median loss)

Two main risk drivers will determine which scenario will unfold:I. The liquidity issue, as Greece & Austria remain the two countries with no

government measures that have become Law II. The need for aggressive fiscal expansion, mainly though investment

projects co-financed with the EU

In a future environment of low growth, it may be more difficult to carry on with those structural reforms needed to improve competitiveness.In a possible nightmare scenario, our limited macro-economic tools and the long-run imbalances imply that once in a recession A long period of stagnation may follow

23G. Hardouvelis, 18/11/2008

For more info, please consult the Eurobank website:

http://www.eurobank.gr/research

THANK YOU FOR YOUR ATTENTION!!My thanks to the Research department of Eurobank EFG

for able research assistance and support

New Europe:

Οικονομία & Αγορές:

Global Economic & Market Outlook:

A quarterly analysis of the countries of New Europe

Μηνιαία έκδοση με θέματα για την ελληνική και παγκόσμια οικονομία

A quarterly in-depth analysis of major market and economic trends across the globe with our detailed forecasts