Greece Debt Crisis Report_Section_B_Group_8

24

Submitted By Group 8 Gaurav Dasgupta – PGP/14/83 Gaurav Singh –PGP/14/84 Kavitha Jayaram-PGP/14/92 Magill Thomas-PGP/14/94 Parvathy L-PGP/14/103 Sandeep Tripathy-PGP/14/114

-

Upload

sandeep-tripathy -

Category

Documents

-

view

221 -

download

0

Transcript of Greece Debt Crisis Report_Section_B_Group_8

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 1/24

Submitted ByGroup 8 Gaurav Dasgupta – PGP/14/83

Gaurav Singh –PGP/14/84 Kavitha Jayaram-PGP/14/92

Magill Thomas-PGP/14/94 Parvathy L-PGP/14/103

Sandeep Tripathy-PGP/14/114

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 2/24

Report on Greece Debt Crisis

2

Table of Contents

Executive Summary .................................................................................................................. 3

Debt Crisis ............................................................................................................................. 4

Overview of Greece economy ..................................................................................................... 4

Overview of Euro and EuroZone .................................................................................................. 4

Formation of the EU.............................................................................................................. 5

History of the Euro ............................................................................................................... 6

EuroZone Members .............................................................................................................. 6

Changes brought about by the Euro ........................................................................................... 7

Euro Vs US Dollar over the years .............................................................................................. 8

How Greece got into this trouble ................................................................................................. 9

Cheaper borrowing from Eurozone ........................................................................................... 9

Increased credit with the help of Investment Bankers ..................................................................... 10

Credit Default Swap ............................................................................................................. 10

Excessive spending ............................................................................................................... 12

Large scale tax evasion .......................................................................................................... 13

Impact of Greece Debt Crisis ..................................................................................................... 14

Impact on Greece ................................................................................................................ 14

Impact on Eurozone ............................................................................................................. 14

Impact on World ................................................................................................................. 16

Crisis Mitigation ..................................................................................................................... 18

Debt Restructure ................................................................................................................. 18

Bailout by Other EU countries and IMF ..................................................................................... 18

Recovery Strategy ................................................................................................................... 18

Fiscal Austerity ................................................................................................................... 19

Revenue Mobilization ........................................................................................................... 19

Possible effects of recovery strategies ........................................................................................ 21

Future challenges .................................................................................................................... 22

PIIGS ............................................................................................................................... 22

Survival of Euro .................................................................................................................. 23

References ............................................................................................................................ 24

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 3/24

Report on Greece Debt Crisis

3

Executive Summary

One of the most reeling economies in the Eurozone is Greece. Though it constitutes less than 3% of the

GDP of the entire Eurozone, the troubled economy has raised too many questions that economists have

not been able to answer convincingly.

The biggest benefit a member of Eurozone gets is attract foreign investors easily because of common

powerful currency and had to pay a low interest rate for bonds. Other benefits that were associated

with being in Eurozone were increase in trade, tourism; reduction in risk due to exchange rate. Due to

these benefits, Greece fudged its accounts to enter Eurozone in 2000 which it publicly admitted in Nov

2004.

It never fulfilled the eligibility to enter Eurozone because of high public debt and budget deficit. Easy

access and reckless spending further increased the public debt and budget deficit. US investment

bankers also entered deals with the Greece government on currency swap derivatives that artificially

increased the credit of the country by $1 billion and further masked its deficit.

When the US recession spread across the world in 2008, Greece was also affected and its income was

significantly affected. But because of high public debt, investors speculated that Greece might default

and this led to the sale of investments (bonds, stocks) in Greece. Investment dried up and Greece found

it even difficult to maintain the budget deficit and put the country on a slow growth track. As a

contagion effect, other similar European economies e.g. Portugal, Italy, Spain and Ireland also became

the victim of speculation. Soon, investors across the world became wary of the financial crisis and

investment across the world reduced. As a result, bond prices fell and stock markets crashed all over the

world. Thus, even a small part of Eurozone resulted in a crisis that impacted the whole world.

Consequently, Greece asked for bailout from IMF and other strong Eurozone members so that it can

recover from the severe crisis. After declining the request citing various political and economic reasons,

a bailout package of $110 billion was sanctioned in May which was to be rolled out in three phases till2013. However, due to the austerity drive and debt reduction measures that come with bailout

package, economists opine that Greece will enter another recession that will take 8-9 years for

recovery.

Further, other troubled economies in PIIGS may also ask for bailout which may be difficult for IMF and

other Eurozone members because of the huge size of Spain and Italy as compared to Greece. In that

case, because of the austerity drive, another recession will hit the entire world which might be of a

larger scale than the US recession.

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 4/24

Report on Greece Debt Crisis

4

Debt CrisisA debt crisis is the crisis that occurs due to the inability to pay one’s debt. This happens when

one loan is taken to repay other loans and the process continues. Debt crisis generally happens in

developing countries due to various factors and affects many generations that follow. Developing

countries face low levels of income, high levels of unemployment, unstable currency, high poverty

levels etc. All these are caused due to the debt crisis that these countries face that hinder their

development. The debt crisis can effectively overcome by various strategies over different sectors of the

economy and a well-laid plan for handling this.

Overview of Greece economy

Greece is a capitalist economy and 40% of its GDP1 is accounted for by the public sector and its

per capita GDP is about two thirds that of the leading Euro economies.15% of GDP is being

contributed by tourism.20% of workforce is taken over by immigrants, mainly in unskilled and

agricultural jobs. Greece is one of the major beneficiaries of EU aid. Greece economy grew by over 4%

in years 2003-2007 mainly due to the Olympics games that happened in Athens in 2004 whoseinfrastructure spending was substantial and another reason was the increased availability of credit which

resulted in sustained levels of spending by consumer. This growth could not sustain itself for long

resulting in a fall by 2% in 2008 and recession followed in 2009 resulting in the decrease of growth by

another 2% caused by the financial crisis faced by the world, less credit and growing budget deficit and

lack of measures to tackle the same.

The EU’s Growth and Stability Pact quoting that budget deficit should not exceed 3% was

violated by Greece in 2007-08 though it was all going well from 2003-06.In 2009, the deficit increased

voluminously and touched 13.7% of GDP. Greece has its public debt, unemployment and inflation

above the EU average but per-capita income is below. The country has been rated very low in

international debt rating due to the eroding public finances, misrepresented statistics, consistentunderperformance in the reforms front. Due to the intense pressure from the EU and the international

market participants, Greece has taken some measures to decrease the tax evasion, improve health care

reforms, cut government spending, improve pension systems and improve competitiveness and

introduce better labor and product markets. Athens faces powerful vocal opposition due its unpopular

reforms. Greek labor unions are trying hard to bring in new austerity measures but the impact has been

limited so far.

In April 2010, a leading credit agency assigned Greece the lowest possible credit. In May, the

IMF and Eurozone governments provided Greece with loans worth $147 billion to repay its debt to

creditors. This was one of the largest bailouts and as an exchange, the government has announced

spending cuts and tax increases to generate $40 billion over 3 years in addition to the other measures.

Overview of Euro and EuroZone

EuroZone is the collective group of countries which have Euro as their accepted currency. The

EuroZone came to existence in 1999. It initially had 11 countries and this grew to 16 by 2009. This

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 5/24

Report on Greece Debt Crisis

5

does not include every country in the European Union. The members of EuroZone must use Euro as its

sole legal currency. The European Central Bank(ECB) is responsible for creating and maintaining the

monetary rules.

The countries in EuroZone are supposed to follow the convergence criteria

Inflation rates:

No more than 1.5 percentage points higher than the average of the three best performing(lowest inflation, which may be negative) member states of the EU.

Govt finance1:

o Annual government deficit: The ratio of the annual government deficit to GDP

must not exceed 3% at the end of the preceding fiscal year2.

o Government debt: The ratio of gross govt debt to GDP must not exceed 60% at the

end of the preceding fiscal year.

o Exchange rate: Applicant countries should have joined the exchange rate mechanism

under the European Monetary Sytem(EMS) for two consecutive years and should not

have devalued its currency during the period.

Long-term interest rates: The nominal long-term interest rate must not be more than 2 percentage points higher than in

the three lowest inflation member states.

The symbol for the euro is a modification of the English alphabet E-

rounded "E" with two cross lines - €. Euros are divided into eurocents, eacheurocent is one one-hundredth of a euro.

Formation of the EU

11 European Union states met the convergence criteria In 1998((Austria, Belgium, Finland, France,

Germany, Ireland, Italy, Luxembourg, Netherlands, Portugal, and Spain). The Eurozone came into

existence with the official launch of the euro on 1 January 1999. Greece qualified in 2000 and was

admitted on 1 January 2001. Physical coins and banknotes were introduced on 1 January 2002.

Currently, there are 16 member states with 329 million people in the eurozone. Euro is the Official

currency of the EuroZone. It is also the second largest reserve currency. It is the second largest traded

currency in the world after the US dollar. It is managed and administered by the ECB(European Central

Bank) which sets the monetary policy. Currently, only 16 of the 27 members of the EU are members of

the EuroZone.

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 6/24

Report on Greece Debt Crisis

6

History of the Euro

The Euro became the official currency of the EuroZone members on 1 Jan,1000.The European

Currency Unit(ECU) was replaced in a ratio of 1:1 by the Euro. Banknotes were launched only in 2002

in the EuroZone. The first nine years with the common currency Euro went well according to

expectations but then the financial crisis of Greece during 2009-2010 gave a lot of stress to the whole of

Europe due to the common currency.

EuroZone Members

Country Joining Date Population Austria 1 January 1999 8,356,707

Belgium 1 January 1999 10,741,048 Cyprus 1 January 2008 801,622 Finland 1 January 1999 5,325,115 France 1 January 1999 64,105,125

Germany 1 January 1999 82,062,249 Greece 1 January 2001 11,262,539 Ireland 1 January 1999 4,517,758

Italy 1 January 1999 60,090,430 Luxembourg 1 January 1999 491,702

Malta 1 January 2008 412,614 Netherlands 1 January 1999 16,481,139

Portugal 1 January 1999 10,631,800 Slovakia 1 January 2009 5,411,062 Slovenia 1 January 2007 2,053,393

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 7/24

Report on Greece Debt Crisis

7

Spain 1 January 1999 45,853,045 Changes brought about by the Euro

Trade

The Euro helped increase trade within the Eurozone from 5 to 10 %.

Investment

Studies have found that there has been a positive influence of the Euro on investment. FDI increased by

around 20% in the EuroZone in the first 4 years 2. Corporate investment also increased after the

introduction of the Euro because of the easier access. According to a study, the introduction of the Euro

accounts for 22% of the investment rate since 1998 for countries that had a weak currency.

Inflation

There has been a popular belief among people that the introduction of the Euro has caused an increase in

the prices, especially in the case of cheap goods which are frequently purchased.

Exchange rate risk

A common currency helps in reduction of the overall risk associated with exchange rate fluctuations.

Euro reduced the market risk exposures for nonfinancial firms both in and outside Europe.

Financial integration

The Euro has helped in financial integration by decreasing the cost of trade in equity,bonds and banking

assets in the EuroZone. There has been an integration in the investments in bond portfolios too because

the EuroZone countries lend and borrow amongst each other much more than with countries outside.

Effect on interest rates

The Euro has helped decrease the interest rates of the member countries especially those with a weak

currency. Thus the value of such firms have increased substantially.

Tourism

Tourism has increased by about 6.5% due to the introduction of the Euro.

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 8/24

Report on Greece Debt Crisis

8

Euro Vs US Dollar over the years

The ECB targets interest rates rather than exchange rates. It does not intervene on the foreign

exchange rate markets, because of the implications of the Mundell-Fleming Model which suggest that a

central bank cannot maintain interest rate and exchange rate targets simultaneously because increasing

the money supply results in a depreciation of the currency.

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 9/24

Report on Greece Debt Crisis

9

How Greece got into this trouble

The basic problem with the Greece economy since early 2000s has been excessive spending with

borrowed money and very low government revenue. Over the years, it has kept on increasing

government expenditure by borrowing huge amounts from investors which resulted in a steady Budget

Deficit. After a certain point, investors realized that the budget deficit of Greece is way beyond control

and it may not be able to make payments to the investors i.e. Greece might default. This significantlyimpacted the borrowing capacity of the country and investment dried out. Further, the 2008 US

recession caused substantial loss in income. This further questioned the ability of Greece to repay its

investors and this is called Greece sovereign debt crisis.

The various elements that contributed to the debt crisis are discussed below in detail.

a) Cheaper borrowing from Eurozone

b) Increased credit with the help of Investment Bankers

c) Credit Default Swap

d) Excessive spending

e) Large scale tax evasion

Cheaper borrowing from Eurozone

Though Eurozone was formed in Jan 1, 1999, Greece was unable to join at that time because of it failed

to meet the Euro convergence criteria of having a budget deficit not exceeding 3% of GDP and public

debt not exceeding 60% of GDP3. But later Greece proved compliance of the convergence criteria and

joined Eurozone in 1st Jan 2001 as its 12th and weakest member.

The single most important benefit of being a part of Eurozone is to adopt the common currency ‘Euro’

which was growing to become the most powerful currency of the world. Since Euro is the common

currency in the entire Eurozone which included powerful economies like France and Germany, entering

Eurozone meant cheaper borrowing.

This can be explained by the following relation.

where it= interest rate for bonds in domestic economy

it* = interest rate for bonds in foreign countries

Et

= current Exchange rate

Et+1

= expected Exchange rate in future

Since lending and borrowing in Eurozone will be in Euro only, exchange rate does not come into

picture and hence the interest rate in all member countries will be theoretically the same. Greece could

have borrowed at the same rate as Germany/France can despite the vast differences in their sizes and

structure.

*

1

( ) ( )1 + 1 + t

et t

t

E i i

E

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 10/24

Report on Greece Debt Crisis

10

Due to easy access to funds, Greece could borrow huge amounts and spent recklessly without being

scrupulous enough to see the return on investments.

Increased credit with the help of Investment Bankers

Investment banks from the United States entered a Currency swapping derivatives deal with the Greece

government that helped Greece mask its true deficit4.

Currency swapping derivatives are financial instruments that are generally used for refinancing an

economy. Generally such instruments help governments borrow money from other countries in foreign

currencies i.e. Yen, Dollars etc, but Euros are required to pay daily bills. Maturity amount is to be paid

in original foreign denomination.

However, in the special agreement between Goldman Sachs and Greece, the exchange rate that was

used was a fictional one which helped Greece borrow approximately $1 billion5 more than it would

have otherwise. Thus, Goldman Sachs arranged for an additional $1 billion credit for Greece and in turn

received a hefty commission for the deal.

Further, since this was a ‘Swap’ derivative, it did not appear in the accounts of Greece and hence didnot come to notice of Eurostat that checks the economic health of Eurozone member countries. Thus,

Greece was able to mask $1 billion of debt due to the Currency-swap derivative instrument.

Credit Default Swap

Gambling and speculations by Investment banks made it extremely difficult for Greece to borrow

money from investors.

Major Investment bankers speculated that Greece will not be able to buy make payments towards

maturity and coupons and is likely to default very soon. This led to the sale of insurance policies that

guards the interests of investors in case an economy fails.

These contracts termed credit-default swaps5, effectively allowed banks and hedge funds wager on a

default by a company or, in this case, an entire country i.e. Greece. If Greece fails to pay for its debts,

owners of these insurance policies can make profit.

Before the debt crisis came to headlines, JP Morgan Chase and about a dozen other banks created an

index that gave market players a platform to bet on whether Greece and other similar European nations

default on their huge debts. Such derivatives are said to have a significant role in Europe’s debt crisis, as

major players across the globe gambled on the failure of the economy of Greece.

This resulted in a vicious circle. As banks and investors rushed to buy such swaps, these swaps became

more and more costly. Alarmed by such ominous signals, Greece government bonds were shunned inthe market and thereby decreased its prices. This in turn resulted in high interest rates that Greece now

was required to pay and thus further increased speculations about default by Greece.

In late January and early February, as demand for swaps protection kept on soaring, investors in Greek

bonds abstained from the market, raising questions about whether Greece could find investors for

buying its bond.

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 11/24

Report on Greece Debt Crisis

11

The Markit index, which is established to trade such credit default swaps, is made up of fifteen most

heavily traded credit default swaps in Europe and covers similar other troubled countries like Italy,

Portugal and Spain. As questions about those countries’ debts moved markets around the world in

February, trading in the Markit index sky-rocketed6.

In February, demand for such swap instruments hit $109.3 billion, 100% more than its value of $52.9

billion in January. Since French banks held $75.4 billion of Greek debt, Swiss institutions held $64

billion and German banks’ exposure stands at $43.2 billion, they were among the major buyers of

Credit Default Swaps.

Massive purchase of credit default swaps kept on increasing Markit index which meant higher chances of

default and thus resulted in even higher cost of debt for Greece.

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 12/24

Report on Greece Debt Crisis

12

Excessive spending

Greece has always been a spendthrift country which kept on a high spending spree even with borrowed

funds. It paid its employees 14 month’s salary7 every year and also paid huge holiday bonuses even if it

was incurring a very high budget deficit.

[Workers' remittances and compensation of employees; paid (US dollar) in Greece ]

[ Greece Government Budget deficit as a percentage of GDP ]

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 13/24

Report on Greece Debt Crisis

13

Large scale tax evasion

One of the major problems that results in very low government income is large scale tax evasion.

Annual tax loss in Greece is estimated at $20.5 billion 8 which can help the struggling economy pay off a

significant chunk of its budget deficit.

[Shadow economy on account of tax evasion in Eurozone]

As it can be observed from the above graph, the economies that are struggling the most are the ones

which have highest tax evasion because of major loopholes in the tax collection system and special

rebates that are offered in many circumstances.

Evading taxes is a norm in Greece and citizens feel proud of tax evasion. This has made it even more

difficult for the government to curb the issue.

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 14/24

Report on Greece Debt Crisis

14

Impact of Greece Debt Crisis

The impact of Greece debt crisis was massive and it was not just limited to Greece and Eurozone, but

spread across the world.

Impact on Greece

Due to steady increase in Markit Index on account of high sale of Credit Default Swaps and

speculations, investors lost confidence in Greece. Credit rating agencies like Fitch and S&P downgraded

Greece’s credit rating to all time low levels. This badly hurt investment in Greece.

Further, investors all over the world started selling Greek investments which led to fall in bond prices.

High risk resulted in demand of high risk premium (interest rate) by the investors i.e. cost of debt

increased substantially for Greece. In April 2010, the bond interest rates were 650 basis points higher

than that of Germany.

When it was revealed that Greece was supposed to make payment of €54 billion 10 towards maturity and

coupon rates in 2010 , chances of default further increased.

Due to the cumulative impact of all these reasons, investors withdrew from Greece and investmentdried up which let to further problems in adjusting the debt crisis and greatly slowed down the

economy.

[Interest rates for 10 year bonds in Greece and Germany]

Impact on Eurozone

Due to the worrying economic condition in Greece and other PIIGS country in Europe (Portugal,

Ireland, Italy, Spain), investors became very cautious and felt that the crisis would spread to the entire

Eurozone and affect other economies even if they’re doing well. This is called Contagion or Dominion

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 15/24

Report on Greece Debt Crisis

15

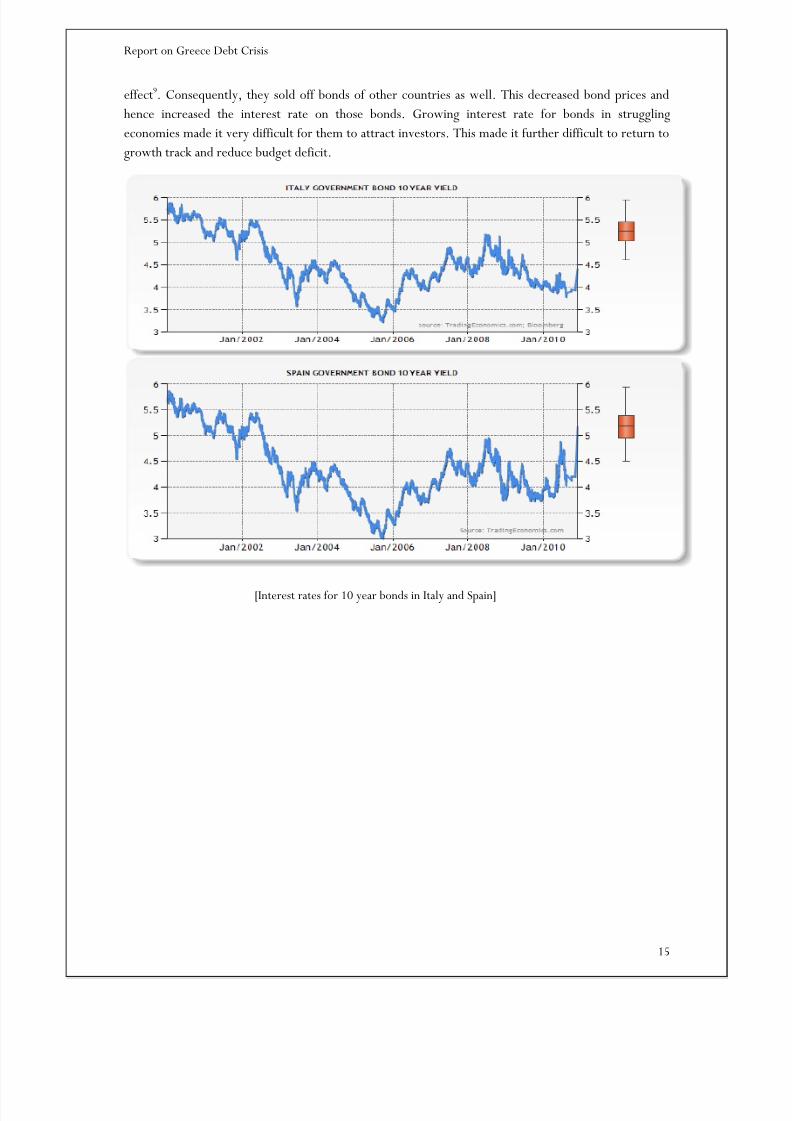

effect9. Consequently, they sold off bonds of other countries as well. This decreased bond prices and

hence increased the interest rate on those bonds. Growing interest rate for bonds in struggling

economies made it very difficult for them to attract investors. This made it further difficult to return to

growth track and reduce budget deficit.

[Interest rates for 10 year bonds in Italy and Spain]

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 16/24

Report on Greece Debt Crisis

16

Investors in stock markets also sold off their investments rapidly which led to severe crash in many

leading Eurozone stock exchanges e.g. France and Germany.

[Indices for stock market exchanges in Germany and France]

A severe liquidity crunch slowed down the growth of the entire Eurozone. All possible options for

attracting investors had failed.

Impact on World

Being the currency of some of the strongest economies in the world, depreciation on the value of Euro

caused heavy losses to countries/institutions that held high reserves of Euro. Suppose India held €1

billion of foreign reserves and Euro depreciates by 5%, then India loses $50 millions11.

Europeans constitute a major chunk among all tourists in the world. Because of this crisis, Europe was badly affected and hence tourism industry suffered huge losses across the world.

Many banks and financial institutions borrow money from London Interbank Market at LIBOR11

(London Interbank offer Rate ). Due to riskiness of the market and liquidity crunch in Eurozone,

floating LIBOR was increasing. This made foreign borrowing less lucrative and investment

opportunities reduced in other economies as well.

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 17/24

Report on Greece Debt Crisis

17

Similar to the Eurozone scenario, investors became risk-averse and started selling off investments in

stock markets all over the world. This made the stock markets plunge and investors incurred huge

losses.

[Nikkie 225 and Dow Jones Stock Indices, Source : Yahoo Finance]

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 18/24

Report on Greece Debt Crisis

18

Crisis Mitigation

By October, 2009 when George Papandreou became the Prime Minister of Greece it was quite clear

that the Greece Economy was on the verge of collapse and needed urgent restructuring. Pandereos’

Government unveiled a series of fiscal consolidation measures to reduce government expenditure but

the reduction in the Greece economic output and the large debts already owed by Greece made the

restructuring process ineffective. To add to that the yields on Greek bonds started increasing and it

became increasingly difficult for Greece to sell new bonds to pay back the debt which was maturing. By

March 29, 2010 Financial markets looses faith in Greece’s ability to service its debt and it becomes

increasingly clear that Greece will either have to restructure its debt or other EU countries will have to

bail it out. Let us study the two options which were available to Greece and the consequences of those

options

Debt Restructure

Debt Restructuring was the initial option which was considered by Greece as a way to come out of the

debt trap. But it was fraught with many risks. Once bond holders feel that sovereign debt issued by

small euro zone countries with high deficits is not secure there may be a run on other countries like

Ireland, Portugal etc, leading to their collapse and a financial contagion and possibly the collapse of the

Euro single currency. Also most of the bonds issued by Greece are held by European and American

banks. Banks whose balance sheets are already weak due to the mortgage crisis and the recession that

followed might go bankrupt if they are asked to restructure their Greek debt.

Bailout by Other EU countries and IMF

There was initial opposition to the idea of bailout both in the countries which will be bearing the cost of

the bailout and in Greece itself. The stronger countries like Germany and France who would have to

foot the major share of the cot felt that they had no obligation to clean up the mess that Greece had

created. There was also criticism that Greece had falsified its accounts to join the Euro Zone and had

very high government expenditure. Citizens in Greece felt that they were giving up their financial

sovereignty by agreeing to the strict terms of the bailout. But April 2010 both sides agree to a bailout as

a restructuring of the debt will cause a worldwide financial contagion and on April 23, 2010 a bailout

package of 110 Billion Euros is announced12.

Recovery Strategy

The bailout package devised by the EU and IMF had very strict conditions which Greece had to follow,

the main among them being a reduction in government deficit.

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 19/24

Report on Greece Debt Crisis

19

Fiscal Austerity

The Greece Government Unveiled a series of measures to bring down the Government Deficit from an

estimated 13.6% of GDP in 2009 to below 3% by 2012 13. Some of these measures were

1. 10% reduction in the remuneration of the Prime Minister, Ministers and Secretary Generals of Ministries

2. Hiring Freeze in20103. Wage freeze and 12% reduction in civil servant’s wage allowances coupled with the reduction

of Christmas, Easter and holiday bonuses by 30% (the so called 13th and 14th salary4. Abolition of executive bonuses in the public sector5. Freeze of all public sector pensions

Revenue Mobilization

The Greek government also started a revenue mobilization drive to increase it income. This drive was

important as the revenue collection of Greece government was particularly low mainly because of large

scale tax evasion and the black economy. The measure announced by the government were

1. Increase of VAT rates from 4,5%, 9% and 19% to 5%, 10% and 21% respectively14 2. Increase of excise tax on luxury goods (expensive cars, yachts etc)3. One-off tax of 1% on personal incomes above 100,000 Euros4. Introduction of an excise tax for electricity5. Increase of excise duties on tobacco, alcohol and fuel6. Increase of taxes on inheritances and bequests

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 20/24

Report on Greece Debt Crisis

20

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 21/24

Report on Greece Debt Crisis

21

Possible effects of recovery strategies

Most Economists expect the combined implementation of fiscal austerity and revenue mobilization

schemes to reduce the government deficits to manageable levels. Especially the increase vat rates and

increase in exercise duties on alcohol and tobacco are expected to be non-evadable and hence lead to

increased revenue generation.

But many economists also fear that Greece might go into a second recession because of the spending

cuts. They site three reasons for this

• Incidence of tax evasion is already very high in Greece. Increase in tax rates will cause evenmore evasion.

• Expansionary monetary policy to compensate for the reduction in fiscal spending is not possibleas the monetary policy is set by the European Central Bank.

• 40% of the Greek economy is based on government expenditure. A Sharp reduction ingovernment spending may send Greece into a severe recession.

Their fears can be summarized by the classic debt spiral theory. According to this government imposes

high taxes and drastic cuts in expenditure in order to reduce its debt. But this leads to a reduction in the

incomes of the people leading to a reduction in spending. This in turn leads to a reduction in the GDP

of the country and hence an Increase in the Debt to GDP ratio15.

[ Debt Spiral ]

High Debt toGDP ratio

High tax, lowsalaries & lowGov. spending

LowerDisposable

Income

Low

consumption

Low output

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 22/24

Report on Greece Debt Crisis

22

Future challenges

PIIGS

The PIIGS consists of Portugal Ireland Italy Greece and Spain. Together they make up 34% of the Euro

Zone economy and all have issues with high Government debt16. All these economies suffer from

Greece style economic problems but each is unique to some extent.

Ireland had a bubble economy due to high private investment which was supported by very lowtaxes. There was also a debt fueled construction boom which went to bust after the Lehmancollapse. The resultant effect on its banks required the government to bail them out puttingsevere strains on it finances

Italy was characterized by high wages and an uncompetitive manufacturing sector. The nearcollapse of Alitalia and its bailout also added to the government debt.

Spain was characterized by a huge housing bubble which rivaled that of the United States. It alsoran huge deficits with cheap imports making its manufacturing sector to contract.

Portugal had very high wages making it uncompetitive in manufacturing. This resulted in a lackof private investment and hence a slowing economy.

The very possibility of Greece defaulting on its debt lead to an increase in the bond yields of these

countries. This has been more so in recent days when Ireland also had to be bailed out with a 90 Billion

Euro package as shown by the following graphs.

[ Portugal 10 year Government Bond yields]

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 23/24

Report on Greece Debt Crisis

23

[ Spain 10 year Government Bond yields ]

The increase in the bond yields of these countries makes it difficult for them to borrow in the open

market and also increases the amount of money they have to payout as interest this automatically makes

their finances strained and hence making the investors ask for higher yields. This vicious circle may

cause the other countries in the PIIGS grouping to default or seek a bailout. And unlike Greece which a

relatively small economy and forms just 2% of the Euro Zone economy the other countries of PIIGS

when put together form 34% of the economic output of the Euro Zone. Hence bailing them will

require significant amounts of money, which the other EU states may find hard to raise.

Survival of Euro

Greece Debt crisis has raised questions regarding the feasibility of the European Monetary Union. Euro

skeptics have pointed out that the monetary union is not backed by a larger political union causing each

nation to set its own Fiscal policy. There is also criticism that one of the main criterions for a monetary

union to work i.e. high mobility of Labour is not satisfied in the Euro Zone. But others feel that the

crisis talks of a need to have better integration between the member countries and a stricter enforcing of

the Stability and Growth Pact. Some even advocate the implementation of a Euro wide Fiscal policy in

order to prevent a Greek style crisis in the future17.

The Greece crisis also brought to the front he imbalances between the northern economies like

Germany who have led an export led growth model and high fiscal prudence which resulted in high

saving and that of countries like Greece who led an debt financed consumption led economy. It is

expected that going ahead countries like Germany will spur its domestic consumption and peripheralcountries like Greece will make their economies more competitive and spur the development of export

industries.

8/8/2019 Greece Debt Crisis Report_Section_B_Group_8

http://slidepdf.com/reader/full/greece-debt-crisis-reportsectionbgroup8 24/24

Report on Greece Debt Crisis

References

1. “Greece's budgetary woes, A long odyssey” Nov 18 2010. Dec 2 2010.

http://www.economist.com/node/17522434

2. “MELISSA EDDY and DEREK GATOPOULOS” The ABC News. May 3 2010. Nov 24 2010

http://abcnews.go.com/Business/wireStory?id=10536767&page=1

3. “DAVID MUIR and BRADLEY BLACKBURN “The ABC News. May 5 2010. Nov 24 2010http://abcnews.go.com/WN/greeks-streets-violent-protests-economic-

problems/story?id=10567233

4. “Shelley DuBois” CNN Money. March 4 2010. Nov 25 2010.

http://money.cnn.com/2010/03/04/news/international/greece_pay.fortune/index.htm

5. “Beat Balzli” Spiegel Online International. August 2 2010. Nov 30 2010

http://www.spiegel.de/international/europe/0,1518,676634,00.html

6. “http://www.ft.com/indepth/greece-debt-crisis

7. http://www.guardian.co.uk/business/2010/may/05/greece-debt-crisis-timeline

8. http://www.nytimes.com/2010/05/08/world/europe/08europe.html

9.

“Peter_Schiff “ The Market Oracle. April 09 2010. Nov 26 2010.http://www.marketoracle.co.uk/Article18529.html

10. “Matthew Bandyk” US News. March 11 2010. Nov 28 2010

http://money.usnews.com/money/business-economy/articles/2010/03/11/how-greeces-

debt-crisis-affects-america.html

11. “Justin Fox” Time Magazine. Feb 22 2010. Nov 25 2010

http://www.time.com/time/magazine/article/0,9171,1963732,00.html

12. “Greece Debt Crisis” Financial Times May 24 2010 Nov 27 2010

http://www.ft.com/greece

13. “Tax Evasion in Greece Seems a Popular Sport” Economy Watch. May 13 2010. Nov 28 2010

14. http://www.economywatch.com/in-the-news/tax-evasion-in-greece-seems-a-popular-sport-

13.05.html

15. “Simon Johnson and James Kwak” PNR February 4 2010. November 28 2010

http://www.npr.org/templates/story/story.php?storyId=99927343

16. “Neil Irwin“ The Washington Post May 7 2010. Nov 30 2010

http://www.washingtonpost.com/wp-

dyn/content/article/2010/05/07/AR2010050700642.html

17. “Greece Crisis: Impact ON Emerging Economies” Money Butjaz . May 27 2010. Dec 2

2010http://money.butjazz.com/greece-crisis-impact-on-emerging-economies-india-china/#

18. Morgan Stanley Research ,Economics and Interest rate strategy, November 2010

19. www.tradingeconomics.com

Word Count: 4,527

![CRS - Greece Debt Crisis[1]](https://static.fdocuments.us/doc/165x107/577d299a1a28ab4e1ea74861/crs-greece-debt-crisis1.jpg)