The Genworth CLTC Sales Model Making Long Term Care Sales SIMPLE Presented by: Robert Burke, RVP...

54

The Genworth CLTC Sales The Genworth CLTC Sales Model Model Making Long Term Care Sales Making Long Term Care Sales SIMPLE SIMPLE Presented by: Presented by: Robert Burke, RVP Robert Burke, RVP Genworth LTC Genworth LTC

-

Upload

jarred-odgers -

Category

Documents

-

view

219 -

download

2

Transcript of The Genworth CLTC Sales Model Making Long Term Care Sales SIMPLE Presented by: Robert Burke, RVP...

The Genworth CLTC Sales The Genworth CLTC Sales ModelModel

Making Long Term Care Sales SIMPLEMaking Long Term Care Sales SIMPLE

Presented by:Presented by:

Robert Burke, RVPRobert Burke, RVP

Genworth LTCGenworth LTC

Lets make this Simple…Lets make this Simple…

SSee the Clientee the Client

IImpart the Riskmpart the Risk

MMake a Planake a Plan

PPresent the Planresent the Plan

LLook at Benefitsook at Benefits

EExamine Underwritingxamine Underwriting

See the ClientSee the Client

In a 2004 LIMRA study of In a 2004 LIMRA study of buyers and non buyersbuyers and non buyers Only 30 % of the people who received info in Only 30 % of the people who received info in

the mail used it in combination with other info the mail used it in combination with other info to buy LTCIto buy LTCI

Another 53% who received info by mail Another 53% who received info by mail decided not to buydecided not to buy

The remaining 17% were still deciding.The remaining 17% were still deciding.

Impart the riskImpart the risk

1. It must be established beyond a reasonable 1. It must be established beyond a reasonable doubt that the client believes he may live a long doubt that the client believes he may live a long life and when he does he may need care.life and when he does he may need care.

2. It must be established beyond reasonable 2. It must be established beyond reasonable doubt that the client understands the impact doubt that the client understands the impact providing care will have on his family and best providing care will have on his family and best thought out retirement plan. This allows for the thought out retirement plan. This allows for the drafting of a plan.drafting of a plan.

3. It must be established beyond a reasonable 3. It must be established beyond a reasonable doubt that nothing will pay for that plan except doubt that nothing will pay for that plan except LTCiLTCi

Establishing a plan for long-Establishing a plan for long-term care: The 3-step term care: The 3-step

process…process…

Step One:Step One:

Establishing beyond a Establishing beyond a reasonable doubt that the reasonable doubt that the

client may live a long life and client may live a long life and very well may need care.very well may need care.

Believes they will live a long lifeBelieves they will live a long life PeriodPeriod Your clients believe they will live a Your clients believe they will live a

long life also. That’s why they make long life also. That’s why they make you promise not to outlive their life you promise not to outlive their life savingssavings

Everyone in this room…Everyone in this room…

When you don’t die…When you don’t die…

You liveYou live

When you live, you get oldWhen you live, you get old

When you get old you get frailWhen you get old you get frail

When you get frail you get sick and need careWhen you get frail you get sick and need care

If the client argues this point If the client argues this point there can be no possibility of there can be no possibility of putting together a plan for putting together a plan for care and protecting it with care and protecting it with

LTCi…LTCi…

Leave immediatelyLeave immediately

Step 2:Step 2:

Establishing beyond a Establishing beyond a reasonable doubt that long-reasonable doubt that long-term care is a family issue term care is a family issue

therefore requiring a therefore requiring a plan to plan to protect the family…protect the family…

Why do people buy Long Why do people buy Long Term Care Insurance?Term Care Insurance?

New thinking…New thinking…

Long-term care has Long-term care has nothing to do with your nothing to do with your

client…client…

The question is not who will take care of your The question is not who will take care of your client, his family will, but rather what providing client, his family will, but rather what providing that care will do to his family and finances that care will do to his family and finances

Families provide the majority of care. “Family” Families provide the majority of care. “Family” is defined as children which often means the is defined as children which often means the daughter daughter

Caregiver stress results in severe tension Caregiver stress results in severe tension between the siblings because the responsibility between the siblings because the responsibility is not shared equallyis not shared equally

Long-term care rarely brings families together, Long-term care rarely brings families together, it tears them apartit tears them apart

It’s a family issue…It’s a family issue…

LTCi never replaces what LTCi never replaces what families do. Rather it builds families do. Rather it builds on an existing infrastructure on an existing infrastructure of support thus allowing the of support thus allowing the

caregivers to provide the caregivers to provide the care care better and longerbetter and longer

Children don’t want to take care of their parents Children don’t want to take care of their parents but will because they love them and are but will because they love them and are concerned for their safetyconcerned for their safety

Suggesting that they will provide care if Suggesting that they will provide care if necessary only reinforces your credibility and necessary only reinforces your credibility and allows for a discussion of what LTCi really does…allows for a discussion of what LTCi really does…

It allows them to provide the care better and It allows them to provide the care better and longer by paying for the type of services children longer by paying for the type of services children find the most embarrassing and difficult to find the most embarrassing and difficult to performperform

What the professional has just done is get the What the professional has just done is get the children off the hook and turned them into children off the hook and turned them into proponents of LTCi. Many will even pay for the proponents of LTCi. Many will even pay for the costcost

Step 3:Step 3:

Establishing beyond a Establishing beyond a reasonable doubt that reasonable doubt that

nothing will pay to protect nothing will pay to protect that plan except LTCithat plan except LTCi

““You have made it clear that the principal You have made it clear that the principal must be preserved because of the must be preserved because of the

possibility of something happening in the possibility of something happening in the future.”future.”

“We will use those assets to generate “We will use those assets to generate sufficient income at retirement. When sufficient income at retirement. When

combined with social security and pension combined with social security and pension benefits, it will allow you to sustain your benefits, it will allow you to sustain your pre-retirement lifestyle as well as keep pre-retirement lifestyle as well as keep

prior financial commitments.”prior financial commitments.”

Up till now those assets have Up till now those assets have been protected by insurance been protected by insurance

which allows them to be which allows them to be available for retirement…available for retirement…

Ex) $750,000Ex) $750,000 Home, Car, Cabin, Home, Car, Cabin,

Stocks, Bonds, Life Stocks, Bonds, Life Insurance Cash Value, Insurance Cash Value, AnnuitiesAnnuities

Homeowners Insurance

AutoHealth

Long Term Care

Good Health

LIFE

You’ve allocated assets You’ve allocated assets and created income for and created income for

retirement…retirement…

What income or assets What income or assets have you allocated to pay have you allocated to pay

for for long-term care? long-term care?

Not doing so means the Not doing so means the client has to rely on a client has to rely on a

government program or use government program or use retirement funds to pay for retirement funds to pay for

carecare

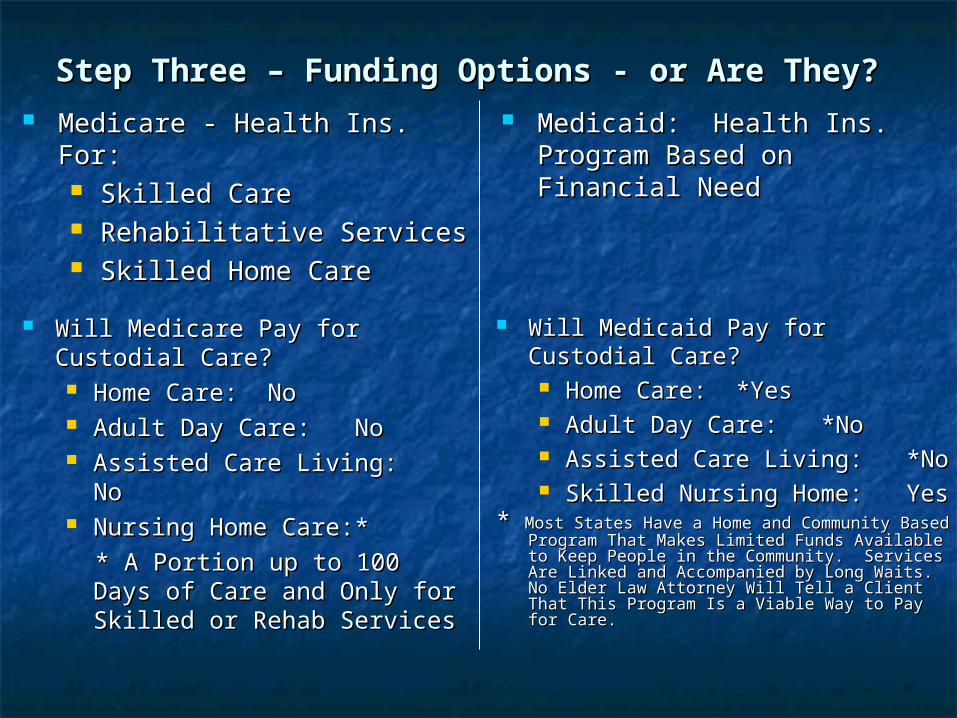

Step Three – Funding Options - or Are They? Step Three – Funding Options - or Are They? Medicare - Health Ins. For:Medicare - Health Ins. For:

Skilled CareSkilled Care Rehabilitative ServicesRehabilitative Services Skilled Home CareSkilled Home Care

Will Medicare Pay for Will Medicare Pay for Custodial Care?Custodial Care? Home Care: Home Care: NoNo Adult Day Care:Adult Day Care:

NoNo Assisted Care Living:Assisted Care Living: NoNo Nursing Home Care:Nursing Home Care: * *

* A Portion up to 100 Days * A Portion up to 100 Days of Care and Only for Skilled of Care and Only for Skilled or Rehab Servicesor Rehab Services

Medicaid: Health Ins. Medicaid: Health Ins. Program Based on Program Based on Financial NeedFinancial Need

Will Medicaid Pay for Custodial Will Medicaid Pay for Custodial Care?Care? Home Care: Home Care: *Yes*Yes Adult Day Care:Adult Day Care: *No*No Assisted Care Living:Assisted Care Living: *No*No Skilled Nursing Home:Skilled Nursing Home: Yes Yes

* * Most States Have a Home and Community Based Most States Have a Home and Community Based Program That Makes Limited Funds Available to Program That Makes Limited Funds Available to Keep People in the Community. Services Are Keep People in the Community. Services Are Linked and Accompanied by Long Waits. No Elder Linked and Accompanied by Long Waits. No Elder Law Attorney Will Tell a Client That This Program Law Attorney Will Tell a Client That This Program Is a Viable Way to Pay for Care.Is a Viable Way to Pay for Care.

““I’m a Veteran. The VA Will Pay for My Care…”I’m a Veteran. The VA Will Pay for My Care…” The VA will only cover 100% of your expenses if the The VA will only cover 100% of your expenses if the

cause of your care need is directly related to a cause of your care need is directly related to a service injuryservice injury

In 2001, the Federal Long Term Care Insurance In 2001, the Federal Long Term Care Insurance Program Was Launched, Recognizing That the VA Program Was Launched, Recognizing That the VA Does Not Offer Comprehensive Long Term Care to Does Not Offer Comprehensive Long Term Care to Most BeneficiariesMost Beneficiaries

¹ GAO Report: ¹ GAO Report: VA Health Care: Better Data Needed to Effectively Use Limited Nursing Home ResourcesVA Health Care: Better Data Needed to Effectively Use Limited Nursing Home Resources , , Hrd-97-27, 1996Hrd-97-27, 1996

Step Three – Funding Options?Step Three – Funding Options?

Self funding the cost of Self funding the cost of long-term care…long-term care…

““I read in I read in Consumer Consumer ReportsReports that my clients that my clients don’t need LTCI if they don’t need LTCI if they

have $1,000,000 or have $1,000,000 or more”more”

I HaveI Have$1,000,000$1,000,000

Income for remaining Income for remaining SpouseSpouse

Find NursesFind Nurses Hire Nursing AssistantsHire Nursing Assistants Schedule House CleaningSchedule House Cleaning Buy GroceriesBuy Groceries Cook MealsCook Meals Schedule and transport to Schedule and transport to

adult daycareadult daycare Install a ramp and grab Install a ramp and grab

bars, widen doorways, buy bars, widen doorways, buy a hospital beda hospital bed

I HaveI Have$500,000$500,000

Income for remaining Income for remaining SpouseSpouse

Find NursesFind Nurses Hire Nursing AssistantsHire Nursing Assistants Schedule House CleaningSchedule House Cleaning Buy GroceriesBuy Groceries Cook MealsCook Meals Schedule and transport to Schedule and transport to

adult daycareadult daycare Install a ramp and grab Install a ramp and grab

bars, widen doorways, buy bars, widen doorways, buy a hospital beda hospital bed

Please don’t confuse having money with getting old, getting Please don’t confuse having money with getting old, getting sick, and needing care. They are really two completely sick, and needing care. They are really two completely

different thingsdifferent things

““I’ll give my money to I’ll give my money to my kids.”my kids.”

In the final analysis LTCI, like In the final analysis LTCI, like any other type of insurance any other type of insurance

protects a plan. In this case it protects a plan. In this case it allows your client’s retirement allows your client’s retirement

plan to execute for the plan to execute for the purpose for which it was purpose for which it was

intended:intended:

Retirement, not paying for Retirement, not paying for long-term carelong-term care

Make a PlanMake a Plan(Plan design rules)(Plan design rules)

1. Buy what you know1. Buy what you know1.1. Insure 80% of the cost of a Nursing HomeInsure 80% of the cost of a Nursing Home2.2. Buy Compound Inflation Protection for clients Buy Compound Inflation Protection for clients

under 70under 703.3. Buy best home care availableBuy best home care available4.4. Zero Day Home Care Benefit is a mustZero Day Home Care Benefit is a must

Benefit AnalysisBenefit Analysis

Benefit typeBenefit type Average Average staystay

Nursing HomeNursing Home 1079 Days1079 Days

Assisted LivingAssisted Living 721 Days721 Days

Home Health Home Health CareCare

523 Days523 Days

% of claims% of claims

11.2 %11.2 %

10.6 %10.6 %

77.9%77.9%

1. Buy what you know1. Buy what you know Insure 80% of the cost of a Nursing Home Insure 80% of the cost of a Nursing Home Buy Compound Inflation Protection for clients under Buy Compound Inflation Protection for clients under

7070 Buy best home care availableBuy best home care available Zero Day Home Care Benefit is a mustZero Day Home Care Benefit is a must

2. Buy as much of what you don’t know as 2. Buy as much of what you don’t know as you can affordyou can afford

Make a PlanMake a Plan(Plan design rules)(Plan design rules)

Present the PlanPresent the Plan(Privileged Choice Shared)(Privileged Choice Shared)

4 4

8

6

6

Built-in Joint Waiver of Premium

Built-in Survivorship Benefit

No Claims Offset Compounding

No Claims Offset No Claims Offset CompoundingCompounding

Without Claims vs. With Claims

Benefits May Last Longer with Benefits May Last Longer with

Privileged ChoicePrivileged Choice®®

Not Reduced by Claims PaidNot Reduced by Claims Paid

This example assumes 100% of the monthly maximum benefit is paid continuously until all benefits exhausted.

Present the PlanPresent the Plan(Privileged Choice Shared)(Privileged Choice Shared)

4 4

8

6

6

Built-in Joint Waiver of Premium

Built-in Survivorship Benefit

No Claims Offset Compounding

10

4

By the Way…..Standard HealthApples to Apples BenefitsHusband and Wife Same AgeMonthly Benefit: $4500, 90 days-Zero Day Elim Home Care, Compound

AgeAge Genworth Genworth

8 YR8 YRGenworth Genworth

10 YR10 YRMet VIP IIMet VIP II John John

HancockHancock

5050 $3150$3150 $3,42$3,4200

$5,00$5,0022

$4,08$4,0888

5555 $3,33$3,3300

$3,60$3,6000

$5,41$5,4188

$4,43$4,4388

6060 $4,14$4,1400

$4,68$4,6800

$6,83$6,8366

$5,41$5,4199

6565 $5,58$5,5800

$6,39$6,3900

$9,16$9,1666

$6,80$6,8022

Simplicity of StorySimplicity of StorySimplicity of Plan DesignSimplicity of Plan Design

Look at BenefitsLook at Benefits

Nursing HomeNursing Home Assisted LivingAssisted Living Home Health CareHome Health Care

Facility Choices for Aging Facility Choices for Aging Relatives Relatives

Assisted living facilities:Assisted living facilities: Residential care setting with Residential care setting with minimal care needsminimal care needs

Skilled nursing facility:Skilled nursing facility: Medical Medical and substantial physical care needsand substantial physical care needs

Alzheimer’s facilities:Alzheimer’s facilities: Specialized Specialized carecare

Hospice care:Hospice care: In home or facility- In home or facility-basedbased

Bed reservation benefitBed reservation benefit

Not just for Nursing Home Care:Not just for Nursing Home Care:

Nurses, Nursing Assistants and TherapistsNurses, Nursing Assistants and Therapists Informal CaregiversInformal Caregivers Homemaker/Chore ServicesHomemaker/Chore Services Assistance with shopping, housekeeping, Assistance with shopping, housekeeping,

chore services and meal preparationchore services and meal preparation Home modificationsHome modifications Adult Day Care and HospiceAdult Day Care and Hospice Alternative Plan of CareAlternative Plan of Care

Today’s long term care insurance is more than nursing home care coverage; it can also cover you in your home and community, using benefits such as:

*These services not available in all states.

Additional Features To Look Additional Features To Look ForFor

Monthly BenefitMonthly Benefit

Waiver of Premium Waiver of Premium

International Coverage International Coverage

Survivorship benefitSurvivorship benefit

Couples, good health discountCouples, good health discount

Care CoordinationCare Coordination

The Care CoordinatorProvides the Plan of

Care

Counseling

Monitoring of On-going Services

Care Referral

Coordination With Providers

Is a Licensed Health Care Practitioner

(LHCP)

Coordination With

Free Services

Care Coordinator

Examine UnderwritingExamine Underwriting

Set a TimetableSet a Timetable Today we will do an applicationToday we will do an application The company may request medical records or The company may request medical records or

health interviewshealth interviews Once a policy is issued we will sit back down Once a policy is issued we will sit back down

and make the final evaluation of putting this and make the final evaluation of putting this plan in placeplan in place

At that time you will have 30 days to free look At that time you will have 30 days to free look the policythe policy

So lets make this Simple…So lets make this Simple…

SSee the Clientee the Client

IImpart the Riskmpart the Risk

MMake a Planake a Plan

PPresent the Planresent the Plan

LLook at Benefitsook at Benefits

EExamine Underwritingxamine Underwriting

Selling to Younger CouplesSelling to Younger Couples(Sales idea of the day)(Sales idea of the day)

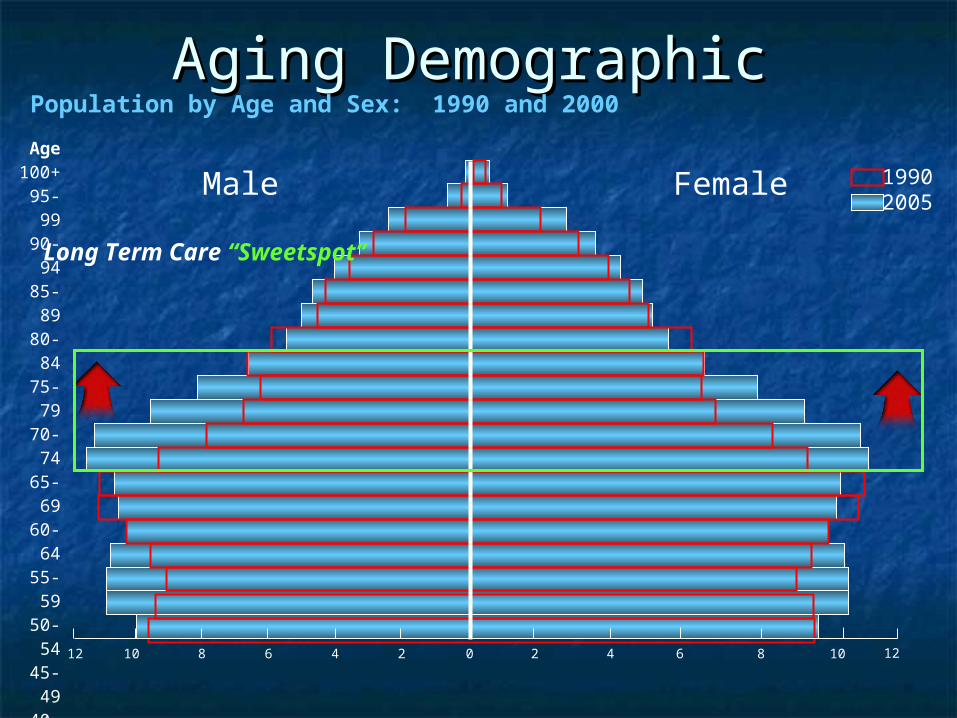

Aging DemographicAging Demographic

19902005

Male Female

Population by Age and Sex: 1990 and 2000

12 1210 108 86 64 42 20

Age100+

95-9990-9485-8980-8475-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-14

5-9

Long Term Care “Sweetspot”

““It’s Not Affordable”It’s Not Affordable”

Forbes Study1 Indicates Prices Consumers Are Willing to Pay For Long Term Care Insurance:

Ages 40-49: $1,000Ages 50-59: $1,305Ages 60-74: $2,100

Price Points Maximize Willingness to Buy1. Forbes Consulting Group, January, 2005

What We Have LearnedWhat We Have Learned

1. Long-Term Care Claims - Milliman, April, 2005

2. Claims Utilization Data - Genworth Financial

Benefit Exhaustion

Benefit Period

% E

xhau

stin

g B

enef

its

For Policies With 3-year Benefit For Policies With 3-year Benefit Period, Only 8 in 100 Claimants Period, Only 8 in 100 Claimants Exhausted Their BenefitsExhausted Their Benefits11

Consider Alzheimer’s Family HistoryConsider Alzheimer’s Family History

8580

55

010

2030

4050

6070

8090

NH ALF HHC

Daily Benefit Utilization

Benefit Type

% D

aily

Ben

efi

t M

ax U

sedOn Average, Our Claimants On Average, Our Claimants Utilized 55% of a Daily Benefit Utilized 55% of a Daily Benefit Maximum for Home Health Maximum for Home Health CareCare22

NH = Nursing Home

ALF = Assisted Living Facility

HHC = Home Health Care

2 Strategies for Plan Design2 Strategies for Plan DesignStack the Coverage

Buy a first chunk today based on Buy a first chunk today based on affordability with the affordability with the Implicit Implicit understandingunderstanding that a second policy will that a second policy will be necessary to offer adequate be necessary to offer adequate coverage in retirementcoverage in retirement

Plan purchase of second policy when Plan purchase of second policy when offer as a group at your employment or offer as a group at your employment or near retirement when income and near retirement when income and retirement expense estimates are retirement expense estimates are more accuratemore accurate

Buying a quality individual policy first Buying a quality individual policy first gives the client the Cadillac in the gives the client the Cadillac in the garage and makes the Ford more of a garage and makes the Ford more of a utility planutility plan

One and Done

Buy what you need and what you Buy what you need and what you can all at once based on can all at once based on affordabilityaffordability

Use with current or near-retirement Use with current or near-retirement people who know or have a fairly people who know or have a fairly good idea what their income will be good idea what their income will be during retirementduring retirement

Value of early retirement Value of early retirement planningplanning

Stacking Coverage

Stacking Stacking allows this to allows this to only only consume consume 4.2% of the 4.2% of the retirement retirement incomeincome

$70,000 Annual Income

$1488 1st Premium

$1452 2nd Premium

11stst policy bought at policy bought at 45- 4yr, $3000 MB45- 4yr, $3000 MB

22ndnd policy bought policy bought at 65 – 4 yr $1,500 at 65 – 4 yr $1,500 MBMB

Goal: 4 yrs of coverage $9,000 MB at retirement (65) from age 45 Goal: 4 yrs of coverage $9,000 MB at retirement (65) from age 45 starting todaystarting today

Waiting to Buy at Retirement

Single policy Single policy purchase will purchase will consume 12.5% consume 12.5% of the retirement of the retirement income. income.

$70,000 Annual Income

$8,712 Annual

Premium

1 policy bought 1 policy bought at 65- 4yr, at 65- 4yr, $9,000 MB$9,000 MB

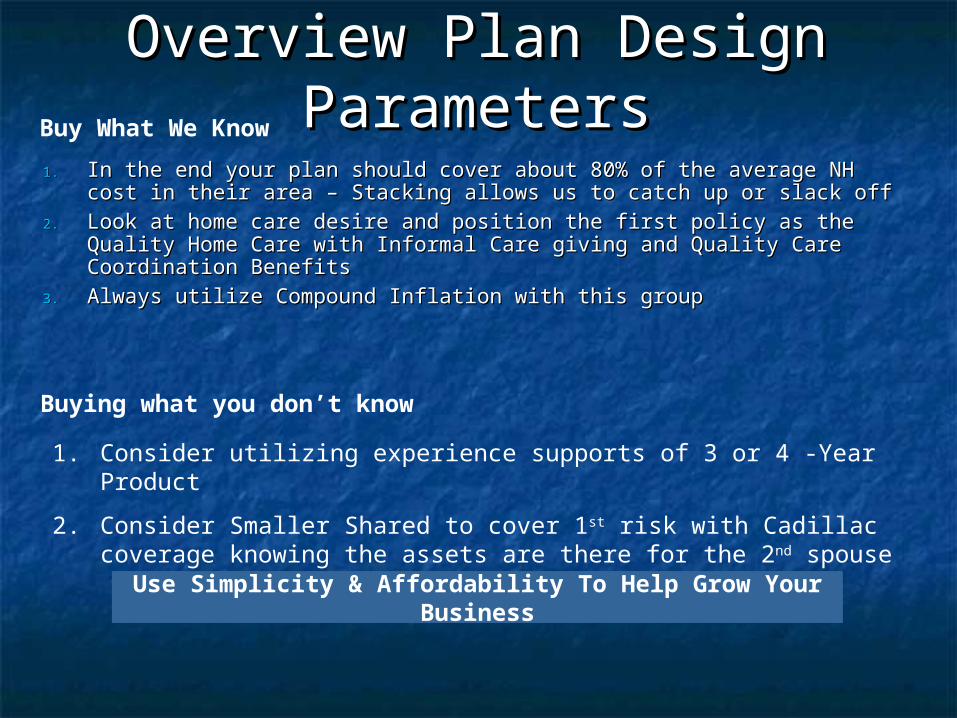

1.1. In the end your plan should cover about 80% of the average NH In the end your plan should cover about 80% of the average NH cost in their area – Stacking allows us to catch up or slack offcost in their area – Stacking allows us to catch up or slack off

2.2. Look at home care desire and position the first policy as the Quality Look at home care desire and position the first policy as the Quality Home Care with Informal Care giving and Quality Care Coordination Home Care with Informal Care giving and Quality Care Coordination BenefitsBenefits

3.3. Always utilize Compound Inflation with this groupAlways utilize Compound Inflation with this group

Overview Plan Design Overview Plan Design ParametersParametersBuy What We Know

Buying what you don’t know

1. Consider utilizing experience supports of 3 or 4 -Year Product

2. Consider Smaller Shared to cover 1st risk with Cadillac coverage knowing the assets are there for the 2nd spouse

Use Simplicity & Affordability To Help Grow Your Business