THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT...

65

THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

Transcript of THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT...

THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

The Gambia cashew sector development and export strategy was developed on the basis of the process, methodology and technical assistance of the International Trade Centre ( ITC ). The views expressed herein do not reflect the official opinion of ITC. This document has not been formally edited by ITC.

The International Trade Centre ( ITC ) is the joint agency of the World Trade Organization and the United Nations

Street address: ITC 54-56, rue de Montbrillant 1202 Geneva, Switzerland

Postal address: ITC Palais des Nations 1211 Geneva 10, Switzerland

Telephone: +41-22 730 0111

Fax: +41-22 733 4439

E-mail: [email protected]

Internet: http://www.intracen.org

Layout : Jesús Alés ( sputnix.es )Photo next page : Artizone

THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

Source: Atamari, via Wikimedia Commons.

IIITHE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

ACKNOWLEDGEMENTS

The cashew sector development and export of The Gambia was made possible with the support of the Enhanced Integrated Framework (EIF); the commitment of the Ministry of Trade, Industry, Regional Integration and Employment (MOTIE) and the Ministry of Agriculture (MOA); as well as the active participation of various inter-mediary organizations including the National Agricultural Research Institute (NARI), Gambia Investment and Export Promotion Agency (GIEPA), International Relief and Development (IRD), national cashew farmers asso-ciations and federation, and the Cashew Alliance of The Gambia (CAG).

This document represents the ambitions of the private and public sector stakeholders who devoted themselves extensively to defining the enhancements and future ori-entations for the sector to raise its growth and export performance.

Technical support and guidance from International Trade Centre (ITC) was rendered through Mr. Charles Roberge and Mr. Isaac Ndungú. Mr. Fafading Fatajo was the national consultant and coordinated stakeholders' consultations.

The efforts and contributions of all cashew sector stake-holders, particularly the members of the cashew sector strategy design committee and the Cashew Alliance of The Gambia, towards the development of the sector strat-egy are highly appreciated.

IV THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

FOREWORD BY ARANCHA GONZÁLEZ, EXECUTIVE DIRECTOR, ITC

Cashews offer one of the most dynamic alternatives to The Gambia’s main export commodity - groundnuts. Not only does The Gambia already produce and export a significant volume of cashews, but high quality Gambian cashews currently command a premium from internation-al buyers. Add to these advantages a supportive overall business environment and one of West Africa’s most ef-ficient ports, and there is no reason why The Gambia, currently the 15th largest exporter of cashews, should be limited to a 0.1 % share of global cashew markets.

This cashew sector development and export strategy provides a realistic roadmap to strengthen the growing potential of Gambian cashews. With less than 5 % of to-tal raw cashew nuts ( RCN ) processed in 2012, there is a clear opportunity to increase in-country value added and take advantage of demand from hotels and restaurants catering to the growing Gambian tourism industry. Along the value chain, environmental considerations such as intercropping and reducing waste offer equally important ways of adding value in sustainable ways.

The strategy is aligned with and builds on national devel-opment plans including the National Development Vision 2020, The Gambian National Agricultural Investment Plan ( GNAIP ) 2011-2015, Program for Accelerated Growth and Employment ( PAGE ) 2012-2015, the National Trade Policy and the National Export Strategy. With the commitment of the Ministry of Trade, Industry, Regional Integration and Employment ( MOTIE ), the Ministry of Agriculture ( MOA ), and the private sector, this cashew strategy aims to make The Gambia a regional centre of excellence in cashew production and value-addition that is integrated into re-gional and global value chains.

The participative design process of this ITC-facilitated sector strategy involved close cooperation with the public and the private sectors and has secured stakeholders’ ownership of the strategy. The strategy design process has also enabled new outcomes including a strength-ened Cashew Alliance of The Gambia, a newly estab-lished Cashew Traders Association, and an enhanced dialogue between public and private cashew stakehold-ers. These are well attuned to intensifying the dynamism of The Gambian cashew sector.

But the success of the strategy will now depend on its implementation. Without effective implementation of the strategy’s plan of action, the potential described in the strategy will remain unrealised. The public and private coordination efforts deployed during the design of the strategy now need to shift focus to mobilizing resources and managing and monitoring the implementation of the strategy. ITC is delighted to have partnered in this initiative and stands ready to continue with its engagement and extending assistance in the transition to implementation of the cashew sector strategy.

Arancha GonzálezITC Executive Director

VTHE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

OFFICIAL STATEMENT FROM THE MINISTER OF TRADE, INDUSTRY, REGIONAL INTEGRATION AND EMPLOYMENT

The Gambian cashew sector has huge potential and this cashew sector strategy is designed to promote the de-velopment of the sector to diversify The Gambia’s export base from its current concentration on groundnuts and fishery products. The Ministry of Trade, Industry, Regional Integration and Employment strongly endorses the prep-aration of this strategy which is in line with the spirit of the National Trade Policy and the National Export Strategy ( NES ) for the promotion of exports of Gambian cashew.

The formulation of the strategy followed a participatory process involving the public and private sectors and this will promote private sector participation in the sector. The strategy aims at addressing issues of competitiveness through improving productivity, enhancing value addition and strengthening capacity of all stakeholders along the value chain for increased exports.

The Government of The Gambia looks forward to the thorough execution of the strategy and will continue its efforts in maintaining macroeconomic stability, improving the competitiveness of the economy and encouraging private investment in production and processing cashew to achieve the vision of strategy : “To be the regional centre of excellence in cashew value-addition, leading the way in production, processing, exports and research and development”.

The National Coordination Committee for the cashew sec-tor will also be closely linked to the NES Implementation Committee to ensure effective coordination and moni-toring of the implementation of the strategy as well as to ensure synergy in the national efforts to promote develop-ment of the cashew sector in The Gambia.

The Government of The Gambia looks forward to effec-tive partnership with all relevant private stakeholders, key financial and technical partners, donors and investors in the implementation of the strategy.

Finally, I also wish to extend my thanks and gratitude to ITC, and all other institutions and individuals who sup-ported the preparation of this strategy.

Hon. Abdou KolleyMinister of Trade, Industry, Regional

Integration and Employment

VI THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

OFFICIAL STATEMENT FROM THE MINISTER OF AGRICULTURE

The agricultural sector is guided by the Agriculture and Natural Resources ( ANR ) Policy and Gambia National Agriculture Investment Programme ( GNAIP ) to achieve the development goals of the agricultural sector in The Gambia. Considering that there is a great need for in-creased and focused investment in the agriculture sector, the GNAIP is an important strategy to mobilise the much needed investment to help increase agricultural produc-tion, productivity and most importantly, ensure food and income security, and reduce poverty. The development of agricultural chains and market promotion is an important sub-component of the GNAIP comprising the develop-ment of food processing chains, strengthening of national operator support services and promotion of intra-regional and extra-regional trade.

The Gambia sector development and export strategy-cashew developed under the Sector Competitiveness and Export Diversification Project therefore, compliments and contributes to the realization of the goals of both the GNAIP and ANR Policy by intervening in the development of the cashew sector.

The development of this strategy document particularly took an approach which included a value chain analy-sis and diagnostic of the sector, defined strategic ori-entations and developed detailed plan of action with clear objectives, activities, target measures, and roles for implementing institutions. It is also important to note that all these involved the active participation of sector stakeholders.

Therefore, it is strongly believed that the contents of this sector strategy carries the collective thoughts on the chal-lenges of the sector and what actions need to be taken to reach our common objective.

Hence, the Ministry of Agriculture gives its full support and also call on all its partners to provide support in what-ever form to the full implementation of the strategy to contribute to the development of the agriculture sector in general and the cashew sector in particular.

Hon. Solomon OwensMinister of Agriculture

VIITHE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

STATEMENT FROM THE CASHEW ALLIANCE OF THE GAMBIA

Cashew is fast becoming a major export crop and is of vital importance to the socio-economic development of The Gambia. The growing cashew sector has been mainly driven by its commercial viability, conducive busi-ness environment and a dynamic private sector in which Cashew Alliance of The Gambia ( CAG ) members are at the forefront.

CAG is a national association of all cashew stakehold-ers including farmers, processors, traders, Government representatives and exporters. It was registered as a non-profit organization in 2010 as the apex body for the cashew industry and to further the interests of the cashew sector in The Gambia. CAG also represents the interest of the African Cashew Alliance ( ACA ) in The Gambia.

The cashew sector development committee estab-lished under the Sector Competitiveness and Export Diversification Project ( SCEDP ) was tasked with the responsibility of overseeing and coordinating the de-velopment and implementation of a sector strategy for cashew nuts. CAG was given the honor of chairing the committee and was well represented in all the commit-tee deliberations. During the year cashew stakeholders who are members of the committee met on several oc-casions to design the cashew sector strategy. Multi-stakeholder workshops were conducted to diagnose the value chain and the sector constraints, defined the overall development visions of the sector and proposed strategic objectives. Also, validation of the cashew problem tree, action plans and prioritization of objec-tives were undertaken to enable the project to devel-op the sector strategy. The sector strategy proposed

has finally been validated by the stakeholders pending Government endorsement.

The project has immensely contributed to the building of capacities of CAG members and other cashew stake-holders. With the setting up of a strategy implementation committee coupled with the strengthening of the CAG, implementation of the sector strategy will be much more successful. This will form the basis for the mobilization of funds to implement projects proposed.

CAG would like to thank the Government of The Gambia through the Ministry of Trade, Industry, Regional Integration and Employment as well as the Enhanced Integrated Framework for bringing such a vital project to the country. Also the International Trade Centre ( ITC ) for a very good implementation of the project to such a successful outcome.

It is hoped that the cashew strategy when implemented will contribute immensely to the development of a sustain-able cashew sector that would enhance export competi-tiveness, raise rural income and reduce poverty.

Momodou A. Ceesay (MR) President – Cashew Alliance

of The Gambia

VIII THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

ACKNOWLEDGEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . III

FOREWORD BY ARANCHA GONZÁLEZ, EXECUTIVE DIRECTOR, ITC . . . . . . . . . . . . . IV

OFFICIAL STATEMENT FROM THE MINISTER OF TRADE, INDUSTRY, REGIONAL INTEGRATION AND EMPLOYMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . V

OFFICIAL STATEMENT FROM THE MINISTER OF AGRICULTURE. . . . . . . . . . . . . . . . . VI

STATEMENT FROM THE CASHEW ALLIANCE OF THE GAMBIA . . . . . . . . . . . . . . . . . . VII

ACRONYMS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . XI

EXECUTIVE SUMMARY 1

INTRODUCTION 4

WHERE WE ARE NOW 5

HISTORICAL PERSPECTIVE OF THE SECTOR . . . . . . . . . . . . . . . . . . . . . . . . . 5

CURRENT CONTEXT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

VALUE CHAIN OPERATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

CURRENT VALUE CHAIN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

SECTOR IMPORTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

GLOBAL PERSPECTIVE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

THE GAMBIA’S CASHEW TRADE PERFORMANCE . . . . . . . . . . . . . . . . . . . . . 13

THE INSTITUTIONAL PERSPECTIVE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

RELEVANT DEVELOPMENT STRATEGIES AND PROGRAMMES . . . . . . . . . . 20

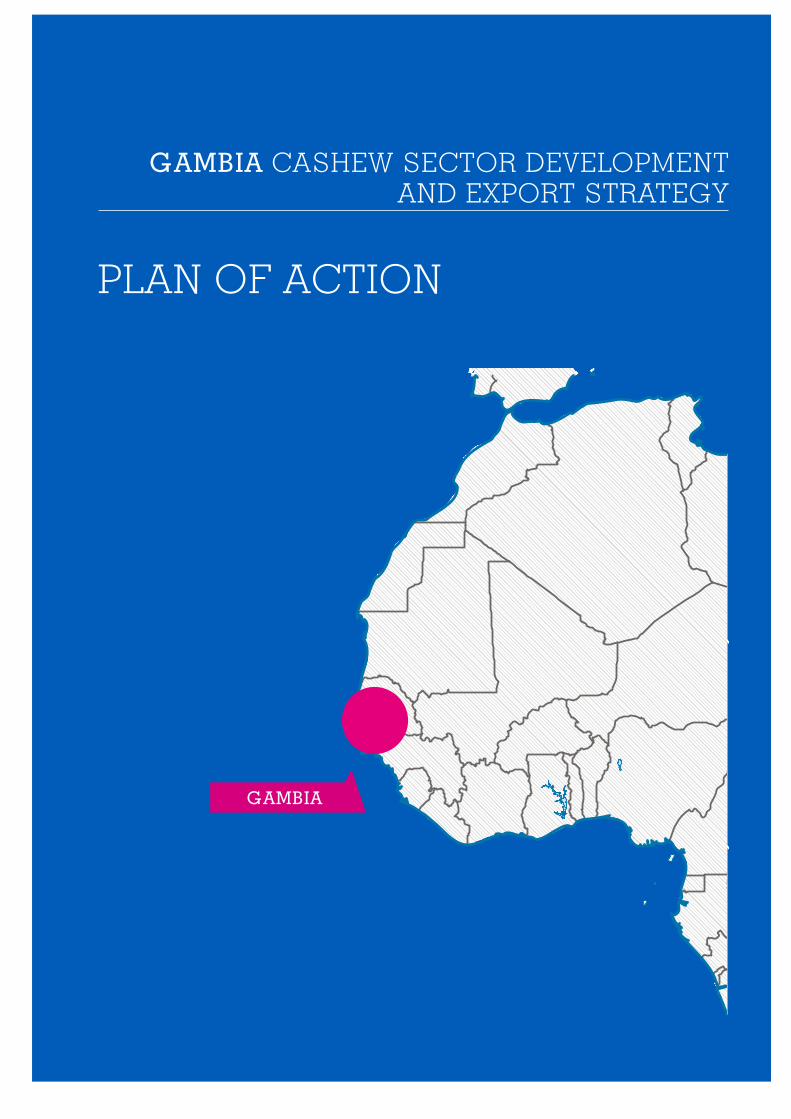

TRADE COMPETITIVENESS ISSUES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

WHERE WE WANT TO GO 27

VISION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

FUTURE VALUE CHAIN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

MARKET IDENTIFICATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

STRATEGIC OPPORTUNITIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

CONTENTS

IXTHE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

HOW TO GET THERE 33

STRATEGIC OBJECTIVES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

IMPORTANCE OF COORDINATED IMPLEMENTATION . . . . . . . . . . . . . . . . . . 33

PLAN OF ACTION 35

BIBLIOGRAPHY 45

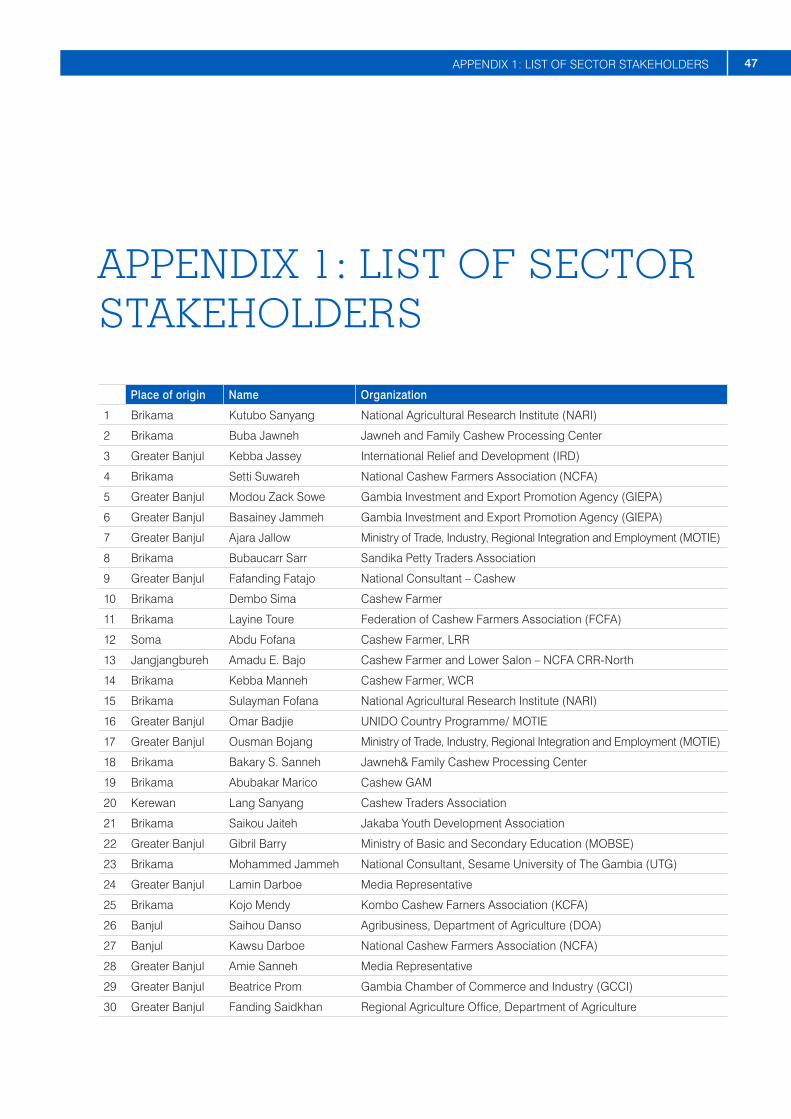

APPENDIX 1 : LIST OF SECTOR STAKEHOLDERS 47

LIST OF FIGURES

Figure 1 : Growth trends for global imports of cashew kernels between 2007 and 2011 ( US $ billions ) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Figure 2 : Total value of imports and exports for The Gambia ( 2007–2011 ) . . . . . . . . . . 13

Figure 3 : Gambia fluctuation of RCN exports in value and quantities, mirror data, 2005–2012 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Figure 4 : Sources of India’s RCN 2012 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Figure 5 : Changing trends in India’s cashew sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Figure 6 : Products and sub-products of the cashew tree . . . . . . . . . . . . . . . . . . . . . . . . . 24

X THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

TABLES

Table 1 : Quantity of raw cashew nuts processed in The Gambia, 2005 to 2011 . . . . . 6

Table 2 : Global production levels of cashews ( top five producers ) 2007 to 2011 . . . . 6

Table 3 : Major importers of cashew nuts in shell and without shell, 2011 and 2012 . 11

Table 4 : Major exporters of cashew nuts in shell and without shell, 2011 and 2012. . 12

Table 5 : Gambian RCN exports, mirror data, 2008-2012 . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Table 6 : Gambian RCN exports, direct data, 2008–2012 . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Table 7 : Gambian cashew sector policy support network . . . . . . . . . . . . . . . . . . . . . . . . 16

Table 8 : Gambian cashew sector trade support network . . . . . . . . . . . . . . . . . . . . . . . . . 16

Table 9 : Gambian cashew sector business services network . . . . . . . . . . . . . . . . . . . . . 17

Table 10 : Gambian cashew sector civil society network . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Table 11 : Perception of Gambian cashew sector TSIs – influence vs. capability . . . . 19

XITHE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

ACRONYMS

ACA African Cashew Alliance

ANRP Agriculture and Natural Resource Policy

CAG Cashew Alliance of The Gambia

CEP Cashew Enhancement Project

CNSL Cashew Nut Shell Liquid

DOA Department of Agriculture

ECOWAS Economic Community of West African States

EIF Enhanced Integrated Framework

EU European Union

FAO Food and Agriculture Organization of the United Nations

FSQA Food Safety and Quality Authority

GAP Good Agricultural Practices

GCCI Gambia Chamber of Commerce and Industry

GDP Gross Domestic Product

GIEPA Gambia Investment and Export Promotion Agency

GRA Gambia Revenue Authority

GSB Gambia Standards Bureau

GTA Gambia Tourism Authority

HACCP Hazard Analysis and Critical Control Point

IRD International Relief and Development

ISO International Organization for Standardization

ITC International Trade Centre

MOA Ministry of Agriculture

MOBSE Ministry of Basic and Secondary Education

MOFEA Ministry of Finance & Economic Affairs

MOJ Ministry of Justice

MOTIE Ministry of Trade, Industry, Regional Integration and Employment

MoU Memorandum of Understanding

NACOFAG National Coordinating Organisation for Farmers Associations

NARI National Agricultural Research Institute

NES National Export Strategy

NFP National Farmers Platform

NGO Non-Governmental Organization

PAGE Program for Accelerated Growth and Development

PoA Plan of Action

RCN Raw Cashew Nuts

SCEDP Sector Competitiveness and Export Diversification Project

TSI Trade Support Institution

TSN Trade Support Network

UN United Nations

VISACA Village Savings & Credit Associations & Programs

Source: © Enhanced Integrated Framework

1EXECUTIVE SUMMARY

EXECUTIVE SUMMARY

The cashew sector development and export strategy has been designed following a participatory process involving the public and private sectors. Using the technical guid-ance and support of the International Trade Centre ( ITC ), the strategy analyses key constraints facing the sector to determine realistic strategic opportunities to improve and sustain the competitiveness of the sector.

The Gambian cashew sector has shown tremendous potential in the last 20 years as an alternative crop to diversify production and exports from the current con-centration on groundnuts. The sector’s performance has grown steadily in the last few years, sustained by the global demand for cashews. Future development hinges on the ability of sector stakeholders to address and cor-rect key constraints and seize emerging opportunities.

CURRENT PERFORMANCE

Gambian cashew nut farming has gained most of its mo-mentum in the Western and North Bank regions. It is esti-mated that by 2011 there were about 2.3 million cashew trees planted on 23,529 hectares ( ha ). During the period 2005–2011 raw cashew nut production rose by approxi-mately 700 %, sustained by good local market prices.

It is estimated that cashew kernel processing accounted for only 5–10 tons in 2012. Kernel processing is mainly undertaken by a few small-scale factories which have limited capacity and resources. However, the develop-ment of two new large processing plants in 2013 has increased the total processing capacity to approximately 10,000 tons.

The Gambia only exports raw cashew nuts and does not export cashew nuts without shells. It has become the 15th leading exporter globally, although its exports vary sub-stantially from one year to the next. According to United Nations Comtrade data ( mirror data ), the total export value of raw cashew nuts from The Gambia surpassed US $ 25 million in 2008 and 2010. The variability in export value and quantities exemplifies Gambian challenges in

supplying international markets with adequate volumes and regular consistency. Much of what is exported from The Gambia through Banjul port is sourced from coun-tries of the subregion.

Despite its recent dynamism, the performance of the cashew sector has been hampered by a wide range of supply-side issues such as the limited use of good plan-tation management techniques, insufficient business management skills across the value chain, the absence of improved varieties of cashew seedlings, and limited processing of raw cashew nuts ( RCN ). Furthermore, in-sufficient capacity to organize the sector’s development ; limited public support for the sector ; the unstructured na-ture of public–private dialogue ; low knowledge of buyer requirements and market trends ; difficulty implementing and maintaining quality controls ; and the limited promo-tion of cashew products have all been identified as chal-lenges to be addressed by the sector.

STRATEGIC ORIENTATION

The strategy design process has defined a number of market and strategic opportunities available to sector stakeholders to stimulate the sector’s growth.

In terms of short-term market opportunities, this strategy proposes to continue exports of Gambian cashews to India since there are well-established trade relations in this growing market. Viet Nam is considered an excel-lent opportunity to diversify export destinations. It is also envisaged to develop the local Gambian market for pro-cessed cashew products by supplying local hotels and restaurants.

In the longer term the strategy proposes to explore ex-ports of RCN to large importing countries such as Brazil or fast emerging processors such as Middle Eastern countries. In the long term, and with quality enhancement, it is proposed to export processed cashew products to the diaspora and selected markets in the European Union ( EU ).

2 THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

The strategy proposes structural enhancements to the sector such as intercropping other produce between cashew rows to increase revenues of farmers ; improving linkages with the tourism sector ; reducing waste at differ-ent levels of the value chain ; designing special integra-tion programmes for youth and women ; and harnessing cashew trees in public places.

ROADMAP FOR SECTOR DEVELOPMENT

In order to realise the development and export potential of The Gambian cashew sector, the following vision has been adopted.

“ To be the regional centre of excellence in cashew value-addition, leading the way in production, processing,

exports and research & development.1 ”1. This vision is the same as the NES vision for the cashew sector and was selected to ensure alignment.

To achieve this vision the strategy will reduce binding constraints on trade competitiveness and capitalize on strategic options identified for The Gambian cashew sec-tor. The sector strategy vision will be achieved through the implementation of the Plan of Action ( PoA ). This PoA revolves around the following four strategic objectives, each spelling out specific sets of activities intended to address both challenges and opportunities facing the cashew sector in The Gambia :

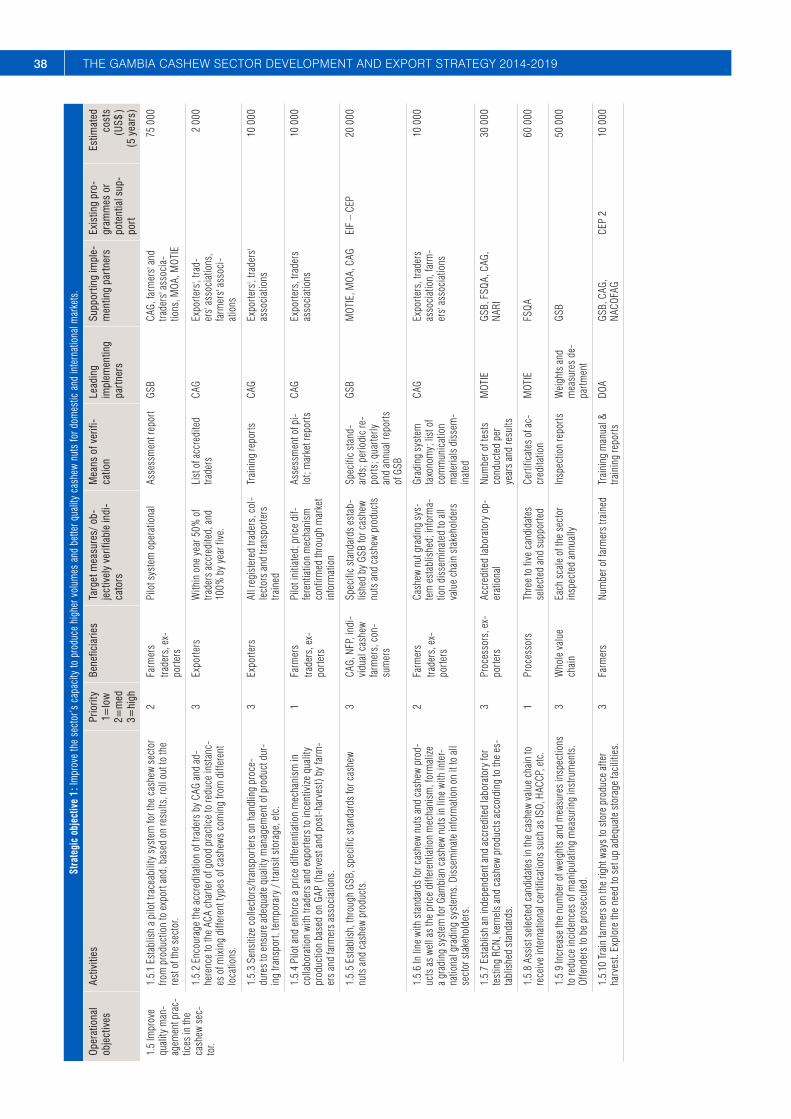

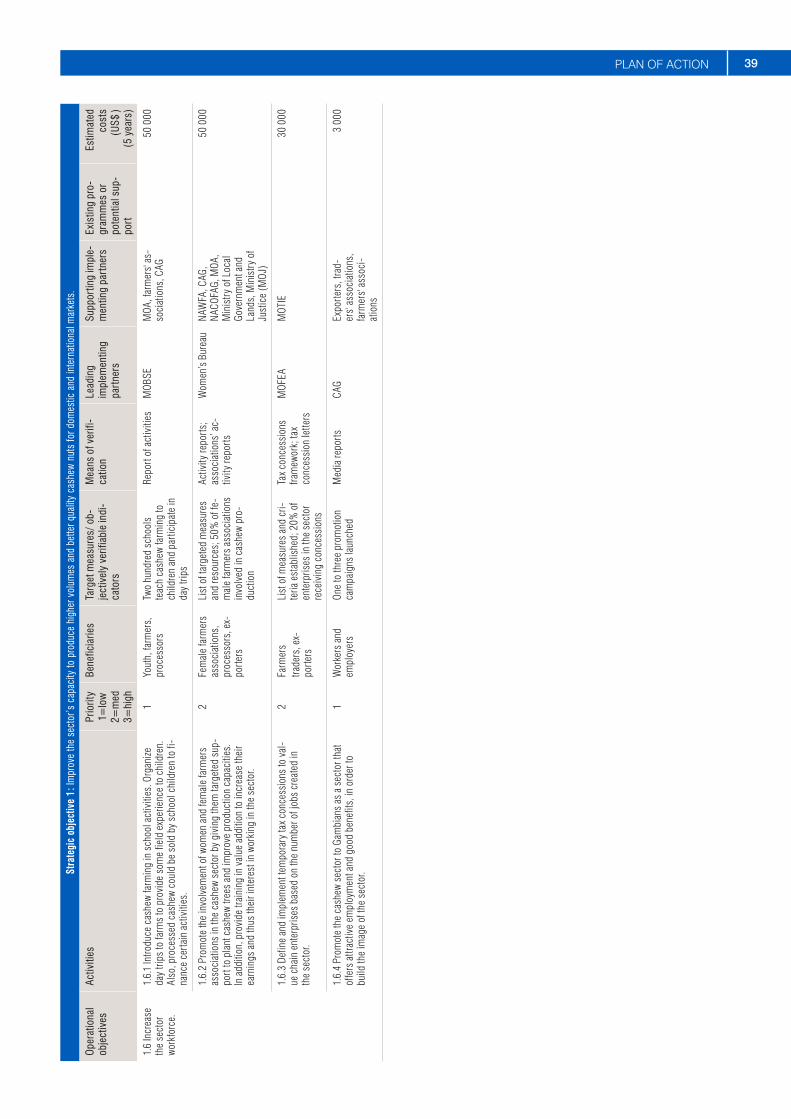

� Improve the sector’s capacity to produce higher vol-umes and better quality cashew nuts for domestic and international markets ;

� Strengthen the organization and coordination of the sector and its support services to enable structured development ;

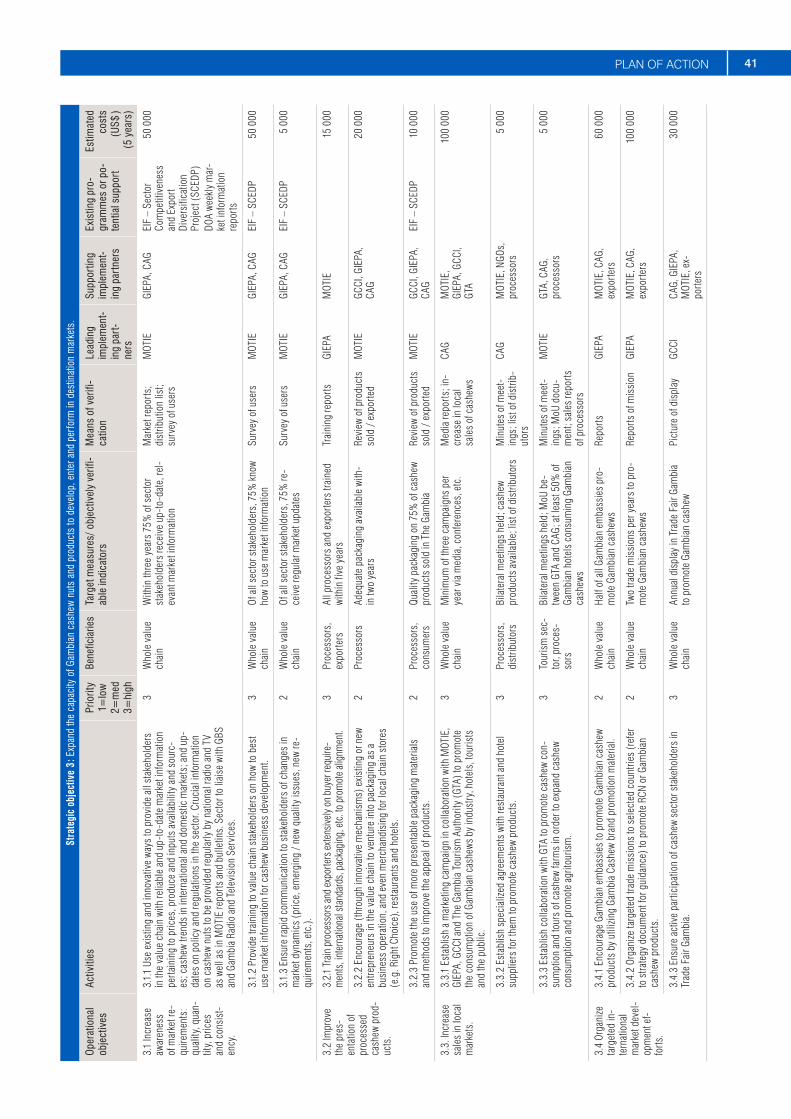

� Expand the capacity of Gambian cashew nuts and products to develop, enter and perform in destination markets ;

� Increase capacity to add value to the sector’s products and by-products.

To build the desired competitiveness, the sector requires credible institutional support systems in both the govern-ment and the private sector. The Cashew Alliance of The Gambia ( CAG ) as an umbrella body is instrumental to coordinating the sector’s future growth prospects. The ex-isting initiatives in the country, such as the Agriculture and Natural Resource Policy ( ANRP ), Program for Accelerated

Growth and Development ( PAGE ), Seed Policy, National Export Strategy ( NES ) and GIEPA’s investment promotion efforts, will need to be stepped up to facilitate improve-ments in quality and the expansion of production and marketing efforts locally to penetrate the tourism sector and international markets.

IMPLEMENTATION MANAGEMENT

The achievement of these ambitious objectives will re-quire continuous and coordinated efforts from all relevant private and public stakeholders as well as support from key financial and technical partners, donors and inves-tors. Several institutions are designated to play a leading role in the implementation of the sector’s PoA and bear the overall responsibility for successful execution of the strategy. Each institution mandated to support the export development of the cashew sector is clearly identified in the strategy PoA.

The proposed National Coordination Committee for the cashew sector and its secretariat will play a coordinating and monitoring role in the implementation of the cashew strategy, in line with the overall framework of the NES. In particular, the National Coordination Committee will be tasked with coordinating the implementation of activities in order to optimize the allocation of both resources and efforts across the wide spectrum of stakeholders.

Source: © IRD Voices.

3EXECUTIVE SUMMARY

Box 1 : Methodological note

The approach used by ITC in the strategy design process relies on a number of analytical elements such as value chain analysis, trade support network ( TSN ) analysis, problem tree, and strategic options selection, all of which form major building blocks of this sector export strategy document.

Value chain analysis : A comprehensive analysis of the sector’s value chain is an integral part of the strategy development process. This analysis results in the identification of all players, processes and linkages within the sector. The process served as the basis for analysing the current performance of the value chain and for deliberating on options for the future development of the sector.

TSN analysis : The trade support network comprises the support services available to the primary value chain players discussed above. It is constituted of policy institutions, trade support organisations, business services providers and civil society. An analysis of the quality of service delivery and constraints affecting the constitu-ent trade support institutions ( TSIs ) is an important input to highlight gaps in service delivery relative to specific sector needs. A second analysis of TSIs assessed their level of influence ( i.e. their ability to influence public policy and other development drivers in the country and therefore make things happen or change ) and their level of capacity to respond to the sector’s needs.

Problem tree analysis : The problem tree analysis used is based on the principles of root causes analysis. The problem tree provides a deeper understanding of what is causing the sector’s constraints and where solution-seeking activities should be directed. As a critical step in the analytical phase of the sector’s performance, the problem tree guides the design of realistic activities in the strategy’s plan of action.

Strategic orientations : The strategic options for the development of the sector are reflected in the future value chain, which is the result of consultations, surveys and analysis conducted as part of the sector strategy design process. The future perspective has two components:

� A market-related component involving identification of key markets in the short and medium- to-long term for Gambian exporters, and ;

� Structural changes to the value chain that result in either strengthening of linkages, or introduction of new linkages.

Realistic and measurable plans of actions : The definition of recommendations and strategic directions for the development of the sector is essential to guide its development, but is not enough. It is important to clearly define the actions to be implemented to stimulate growth. The development of a detailed action plan, defining which activities need to be undertaken by sector stakeholders is necessary to the effective implementation of the strategy. An action plan, developed with the support of ITC, includes performance indicators to ensure ef-fective monitoring and evaluation of the strategy’s implementation.

4 THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

INTRODUCTION

The cashew sector analysis and strategy presented in this document have been elaborated as part of the Sector Competitiveness and Export Diversification Project of the Enhanced Integrated Framework ( EIF ). The project is be-ing elaborated and implemented in full cooperation with the Government of Gambia. The initiative has also been fully supported by the sector’s private sector operators.

This sector and export strategy is based on the findings and recommendations of the NES of The Gambia. Its analysis and PoA expand and strengthen the orientations of the cashew component of the NES. This cashew sec-tor strategy has been elaborated with the support of the members of the NES team in charge of elaborating the cashew component of the NES.

The Gambian cashew sector has shown tremendous potential in the last 20 years as an alternative crop to diversify production and exports from the current con-centration on groundnuts. The sector’s performance has grown steadily in the last few years, sustained by the global demand for cashews. The sector’s future devel-opment hinges on the ability of sector stakeholders from both public and private sectors to address and correct key constraints and seize emerging opportunities. This document presents the expectations of the private and public sectors for improvement of the cashew sector in The Gambia. Without concerted efforts to address critical issues and identified market development opportunities the sector’s potential will remain untapped instead of lev-eraging its potential and capacity. The five year plan of action of the strategy proposes realistic and achievable activities that will contribute to accelerating the growth of the cashew sector.

Source: Atamari, via Wikimedia Commons.

5WHERE WE ARE NOW

WHERE WE ARE NOW

HISTORICAL PERSPECTIVE OF THE SECTORCashew was first introduced in The Gambia in the 1960s as an agroforestry crop, planted around forestry boundaries as a firebreak. In the 1980s the Ministries of Agriculture and Forestry promoted the cultivation of the crop on a large scale as a means of protecting the envi-ronment and providing an economic benefit to farmers. Farmers were advised to plant cashew along the borders of their farmland and forests to contain growth of grass and curtail intrusion of fires into farm areas.

The Gambian cashew sector was mostly developed through private sector efforts in the late 1980s. In the early 1990s the private sector commenced distribution of seeds of locally improved varieties. Seeds were distrib-uted along with a cashew grower’s manual.

The production of raw cashew nuts steadily increased from a low 200 tons in 1998 to 2,000 tons in 2007. At the same time, the number of cashew exporters grew from two exporters in 2003 to more than 15 in 2007, confirm-ing the vitality of the sector. At that time the exports of cashews from the Port of Banjul exceeded 30,000 tons, while production of Gambian cashew nuts was merely 2,000 tons.2 The vitality of the sector in The Gambia, the high concentration of exporters and the port infrastruc-ture drew cashews from Senegal and Guinea-Bissau. Leadership from the private sector has led to the sec-tor’s growth in The Gambia.

Cashew growers associations and cooperatives have emerged with the development of the sector.3 At the mo-ment there are five cashew farmers associations operat-ing in The Gambia. In 2012, the Federation of Gambian

2. ComAfrique Ltd ( 2007 ). Gambia Cashew profile for African Cashew Alliance.3. There are five functional growers’ associations active : Kombo Cashew Farmers Association, National Cashew Farmers Association, Soomo Cashew Farmers Association, NDAR cashew and Hakilinyma Cashew Farmers Association.

Cashew Farmers Associations was established to repre-sent the interests of all the cashew farmers associations and facilitate dialogue with other sector stakeholders.4 An apex body for the sector – the Cashew Alliance of The Gambia – was also established 2011 to represent the vari-ous private sector interests of the sector.

In sum, the sector has grown organically from humble beginnings to become in 2011 the sixth most important export sector of The Gambia.5 For a long time there was little government assistance but that situation is chang-ing, with government leaders speaking favourably about the need to develop cashew production.6

CURRENT CONTEXTAccording to a recent survey the majority of cashew farm-ers are individual land owners with average holdings of 1-3 ha.7 The majority of the sector’s operations are man-aged by cashew farmers, local traders, collectors, export-ers and a few processors.

PRODUCTION

There is no official data on Gambian cashew nut produc-tion from either official sources or international organiza-tions such as the Food and Agriculture Organization of the United Nations ( FAO ). The following figures are based on data collected through various sources.

4. Point Newspaper, The ( 2012 ). Federation of Gambian Cashew Farmers Association launched, 10 July. Available from http : / / thepoint.gm / africa / gambia / article / federation-of-gambian-cashew-farmers-association-launched5. ITC calculations based on Comtrade data.6. Gomez, G., Jaeger, P. and Peters, J. ( 2011 ). Analysis of the Cashew Value Chain in Senegal and The Gambia – African Cashew initiative. Germany, GIZ.7. Ibid. p.25, and IRD baseline data.

6 THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

Table 1 : Quantity of raw cashew nuts processed in The Gambia, 2005 to 2011

2005 2006 2007 2008 2009 2010 2011 Average 2005-2011

Production, tons 1 250 1 750 2 000 3 000 6 500 8 000 10 000 4 643

Harvested area ( ha ) 3 187 4 375 5 000 7 058 15 294 17 777 23 529 10 889

Yield, kg / ha 400 400 400 425 425 450 450 421

Exports ( tons ) 12 498 22 891 22 521 24 095 27 367 12 223 24 869 20 923

Source : ITC calculations and IRD data

Table 2 : Global production levels of cashews ( top five producers ) 2007 to 2011

2007 2008 2009 2010 2011

Viet Nam 1 249 600 1 234 000 1 165 600 1 242 000 1 237 300

Nigeria 660 000 727 603 800 000 830 000 835 000

India 620 000 665 000 695 000 613 000 674 600

Côte d’Ivoire 280 000 330 000 350 000 380 000 393 000

Brazil 140 675 243 253 220 505 104 342 230 785

Source : FAO Statistics

Gambian cashew nut farming has gained most of its mo-mentum in the Western and North Bank regions. It is esti-mated that by 2011 there were about 2.3 million cashew trees planted on 23,529 ha.8 Table 1 shows production and processing for the period 2005-2011. During this pe-riod 9 raw cashew nut production rose by approximately 700 %, sustained by good local market prices.

Gambian cashew production is relatively small com-pared to the world leaders in raw cashew nut produc-tion. World raw cashew output is estimated to have increased by about 3 % per year over the past five sea-sons, from 2,130,000 tons in 2006 / 2007 to 2,490,000 tons in 2010 / 2011. 10 Viet Nam and India are two of the world leaders in cashew production, as well as two of the larg-est processors of kernels. As indicated in Table 2, The Gambia is in the vicinity of two of the largest producers in the world. The production of Nigeria and Côte d’Ivoire ranges from 835,000 tons to 393,000 tons respectively. The current production of The Gambia, if it is confirmed, would rank the country at 16th in terms of global produc-tion volume.

Cashew grows across virtually the entire country but production and quality differs greatly from one region

8. 10,000 tons estimated production in 2011 / 400kg / ha. Estimated area cultivated was 23,529 ha and, based on the assumption of approximately 100 trees per ha, the total estimated number of cashew trees in the country is 2,352,900.9. During this period cashew nut production increased from 1,250 to 10,000 tons.10. International Trade Centre ( 2011 ). Cashew MNS BULLETIN, November.

to another. The average yield of cashew production in The Gambia is estimated at 450kg / ha, which is low when compared with the world average of 840kg / ha.11 The av-erage yields in The Gambia are partly explained by limited use of good agricultural practices ( GAP ) and post-har-vest losses caused by inadequate handling practices.

PROCESSING

It is estimated that cashew kernel processing accounted for only 10-20 tons in 2012.12 Kernel processing is mainly undertaken by a few small-scale factories 13 which have limited capacity and resources. The development of two new large processing plants in 2013 has increased total processing capacity to approximately 10,000 tons.

The challenge with cashew processing, though not pecu-liar to The Gambia, is that to be economically viable there must be enough output of processed kernels.14 This im-plies the need for a calculated expansion either in the size of existing farms, the entering of new farmers into cash-

11. Gomez, G., Jaeger, P. and Peters, J. ( 2011 ). Analysis of the Cashew Value Chain in Senegal and The Gambia – African Cashew initiative. Germany, GIZ, p.24 and Sustainable Trade Initiative ( n.d. ). Cashew. Available from http : / / www.idhsustainabletrade.com / cashew12. Bilateral meetings with IRD and Gambia Horticultural Enterprises.13. There are three main micro-processors of cashew kernels : Gambia Horticultural Enterprises, Jawneh & family enterprise, and Group Juboo. Two larger plants became operational in 2013 with a processing capacity of 2,500 tons per year and 7,000 tons per year.14. Government of Gambia ( 2012 ). Gambia National Export Strategy 2013–2017, p.14.

7WHERE WE ARE NOW

ew production, or an increase in imports of RCN from the subregion to ensure processing plants can achieve economically sustainable operations. In increasing the availability of RCN for processing it will also be impor-tant to ensure quality requirements are maintained, which could mean excluding sourcing from some zones of the subregion 15 such as Mali. Expansion of cultivation in the east of Gambia should also be undertaken with caution.

The processing of cashew also includes the transforma-tion of the cashew apple. At the moment cashew apples are mainly transformed at the household level into jams, alcohol, dried fruit and other sub-products, and there is very little commercialization of products, with the excep-tion of fresh apples sold in markets.

VALUE CHAIN OPERATIONSA report by Gomez, Jaeger and Peters 16 described the chain as simple and direct, with harvest passing from the farmers to buying agents working for collectors, who in turn supply the exporters.

RESEARCH AND DEVELOPMENT

In the past there was not much work done in cashew research due to limited government intervention in the sector. The National Agricultural Research Institute ( NARI ) is considering doing research on cashew, especially look-ing into the characteristics of the varieties available in the country and their genetic potential ( discussions with the Programme Leader, Agroforestry Programme and NARI, October 2012 ). The IRD has done some research seek-ing to introduce high-yielding varieties and to expand value addition by increasing the amount of processing done and the variety of products. Currently ( 2013 ) IRD is engaged in research work on cashew covering Gambia and Senegal.17

SEED SELECTION 18

According to IRD, when planting a cashew tree one must investigate the best seed variety suitable for the region. Seeds for planting should be obtained from healthy moth-er trees of a recognized high yielding variety, aged 8-15

15. According to sector stakeholders, certain production zones in East Gambia, Senegal and Mali produce RCN of lower quality, mainly because of climatic conditions.16. Gomez, G., Jaeger, P. and Peters, J. ( 2011 ). Analysis of the Cashew Value Chain in Senegal and The Gambia – African Cashew initiative. Germany, GIZ.17. Interview with IRD.18. International Relief and Development ( 2011 ). Cashew Business Basics – The Gambia River Basin Cashew Value Chain Enhancement Project ( CEP ).

years. It is recommended to scout for several cashew trees with good flowering and following them through to maturity.

PLANTING

There are two ways to grow cashew seeds. One way is to plant the seed directly in the desired location. Trees planted in such manner are easily eaten by pests. They also require watering, which could be difficult, especially on a large scale. Another method is to plant the seed in a plastic bag and then transfer the young tree seedling ( about three months old ) to the desired location. This method has higher chances of survival and good growth.

PRODUCTION

The cultivation of cashew in The Gambia is restricted to rain-fed production due to economic limitations and sa-line intrusion upstream.19 Cashew does not do well in saline soil ( salty soil ).

Production involves planting, weed management, pruning and grafting. These are followed by fire belting, collecting the nuts and drying. The key inputs into the production process are seeds, seedlings, pruning and grafting tools, weeding tools, collection containers, drying material and storage bags. There is rare use of fertilizers in the sector except by commercial farmers, who are few. The simple materials used for the above processes are imports re-tailed locally. Fencing is required to protect against theft and animal invasion. Frequent visits to the farm are rec-ommended as fencing alone does not fully deter thieves and animals.

HARVESTING

The cashew in The Gambia is not harvested from the tree ; apples are allowed to fall and are picked for separation of nuts from the apple under hygienic conditions. The ground should be kept free of weeds. Nuts and apples are separated within 24 hours. Nuts are dried under the sun for 3-4 days while guarding against moisture and insects.

NUT COUNT TEST

This test is done to give an indication of the size of the raw nut by counting the number of raw nuts per kilo. Nuts selected randomly from the bags are placed on a scale until the scale reads 1 kg. Then the number of nuts is

19. Gomez, G., Jaeger, P. and Peters, J. ( 2011 ). Analysis of the Cashew Value Chain in Senegal and The Gambia – African Cashew initiative. Germany, GIZ.

8 THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

counted. It will take more small nuts to add up to a kilo. The larger the nuts, the fewer nuts it takes to make a kilo. The fewer the nuts the better.20

PROCESSING

By 2012 there were four processors, with two being regu-larly active and with the total amount processed ranging between 10 and 20 tons per year. There is reported sub-stantial artisanal processing activity with an estimated 46 % of households reported to be doing some process-ing for household consumption.21 The vast majority of cashew is exported raw, mainly to India. There every part of the cashew is used or processed to generate income. This includes the nut, the peel inside the shell and the liquid inside the shell, as well as the outer shell and the cashew apple.22

EXPORTING

Products from The Gambia and the subregion ( mainly Senegal and Guinea-Bissau ) are aggregated at Banjul and shipped to export markets. They are packed in jute bags and shipped to the export market. As described in the export section, most Gambian cashew is exported raw to India.

SERVICES AND SUPPORT

The support services required in the value chain include :

� Research ; � Training in good methods ; � Quality and standards management ; � Prompt and regular dissemination of accurate relevant

market and production information ; � Financial services ; � Labour ; � Transport, storage and handling ; � Cross-border facilitation ; � Packaging ; and � Export promotion.

20. International Relief and Development ( 2011 ). Cashew Business Basics – The Gambia River Basin Cashew Value Chain Enhancement Project ( CEP ).21. Gomez, G., Jaeger, P. and Peters, J. ( 2011 ). Analysis of the Cashew Value Chain in Senegal and The Gambia – African Cashew initiative. Germany, GIZ.22. International Relief and Development ( 2011 ). Cashew Business Basics – The Gambia River Basin Cashew Value Chain Enhancement Project ( CEP ).

The Government of Gambia has not intervened much in the sector but this appears bound to change with growing interest from policymakers. Cashew production and pro-cessing is recognized in many policy documents, such as the NES, as an important crop for socioeconomic devel-opment. There is one donor activity, namely The Gambia River Basin Cashew Value Chain Enhancement Project ( CEP ), which is supporting activities along the value chain. Some limited business development services are provided by numerous sector associations.

Labour, finance and transport are the key services re-quired. Storage is usually on the farmers’ premises. Packaging is not an issue right now as the bulk of The Gambian cashew is exported raw (in shell). There are numerous sector associations but their ability to improve competitiveness has been hindered by a lack of resourc-es and limited government intervention. Thus there is limited lobbying and advocacy for the required services listed above to be made available.

OTHER ACTIVITIES ALONG THE VALUE CHAIN

Intercropping with food and other cash crops is possi-ble. Beekeeping has also been noted by IRD as a viable operation. Other possibilities including use of the apple to make juice and alcohol, and making jams, cakes and candles ( IRD ). These are all done on limited a scale at household level. Scarcity of production data makes it dif-ficult to quantify values along the value chain.

Source: © Enhanced Integrated Framework

Nat

iona

l com

pone

nt

Inpu

ts u

sed

by fa

rmer

s

Sub-

regi

on

impo

rted

RCN

Har

vest

Stor

age

Pack

agin

g

Prod

uctio

n

Dry

ing

NAR

IG

ambi

a Bu

reau

of S

tatis

tics

Gam

bia

Stan

dard

s Bu

reau

Food

Saf

ety

and

Qua

lity

Auth

ority

Gam

bia

Port

s Au

thor

ity

Sect

or a

ssoc

iatio

nsM

oAM

OTI

EG

IEPA

GRA

Prim

ary

supp

ort s

ervi

ces

Farm

pro

duct

ion

Mid

dlem

en

Tran

spor

ters

Loca

l Sho

psAg

ents

War

ehou

ses

Colle

ctor

s

Pack

agin

gG

radi

ng

Smal

l and

larg

esc

ale

Proc

esso

rsLo

cal m

arke

t(k

erne

ls)

Qua

lity

chec

ks

Expo

rter

s

Cash

ew A

llian

ce o

f The

Gam

bia

Fina

ncia

l ser

vice

s: C

omm

erci

al b

anks

; mic

ro-le

nder

s; b

ig b

uyer

s; s

elf-

help

gro

ups

/ VIS

ACA

Indi

a

Roas

ter

/ pac

ker

Who

lesa

le

Reta

il

Impo

rter

Re-e

xpor

t

Ger

man

y

Roas

ter

/ pac

ker

Who

lesa

le

Reta

il

Impo

rter

Viet

nam

Roas

ter

/ pac

ker

Who

lesa

le

Reta

il

Impo

rter

Re-e

xpor

t

Seed

ings

Loca

l lab

our

Agro

chem

ical

s

Farm

impl

emen

ts

Lege

nd

Inte

rnat

iona

l com

pone

nt

9WHERE WE ARE NOWC

UR

RE

NT

VA

LUE

CH

AIN

So

urc

e: G

amb

ian

cash

ew s

take

hold

ers

dur

ing

the

stra

teg

y d

esig

n p

roce

ss

10 THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

SECTOR IMPORTS

Cashews kernel processed in The Gambia are mainly sold in specific shops or by street vendors. However, some cashew kernels – packaged according to packag-ing and quality requirements – are also available in su-permarkets. According to USAID, 75 % of supermarkets import their cashews from Europe or Senegal.23

As indicated in the trade data, significant volumes of RCN are imported to The Gambia for re-export through the port of Banjul. The vast majority of export from The Gambia represents imported RCN from Senegal, Guinea-Bissau and even Mali. This situation creates a quality management problem as it is extremely difficult to trace the origin of the nuts. At the moment, Gambian RCN with an outturn ratio of 49-52 are receiving a premium from international buyers. The formal and informal imports of RCN from the subregion are difficult to trace and monitor, which often leads to the mixing of good quality Gambian nuts with lower quality imported nuts. This critical issue needs to be addressed in order to maintain the premi-um on Gambian cashew nuts. The high volume of RCN imported from neighbouring countries can contribute to satisfying the volume requirements of emerging process-ing enterprises in The Gambia. In addition to RCN critical inputs such as chemicals, tools and packaging materials are also imported.

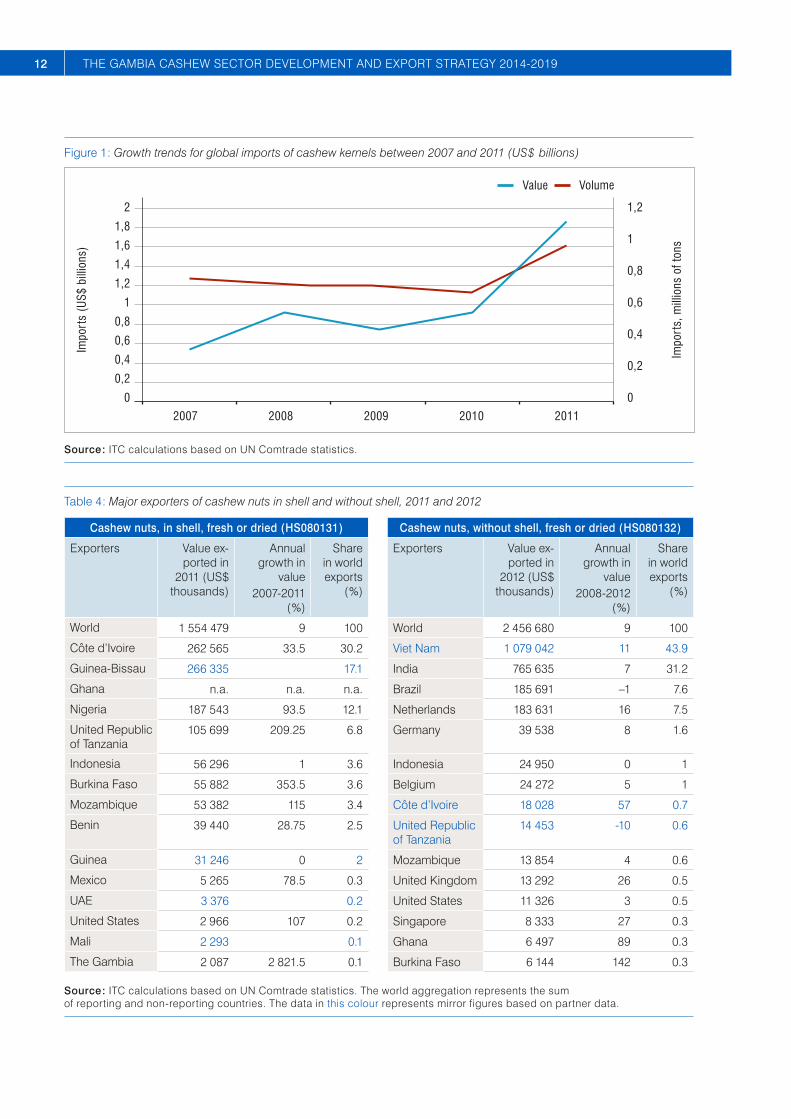

GLOBAL PERSPECTIVEThe global cashew nut industry is a fast growing industry worth US $ 4.9 billon, as shown in Tables 3 and 4 below.

23. See : USAID ( 2007 ). Cashew marketing & consumption in West Africa : current status and opportunities. West Africa Trade Hub Technical Report No. 22. No trade data is reported for this import on Comtrade.

MAJOR IMPORTERS

The import market for RCN ( HS 080131 ) is worth approxi-mately US $ 1.8 billion ( 2011 ), with an average growth rate of 37 % for the 2008-2012 period.

In 2011 India was the leading importer of RCN with total imports of US $ 1.1 billion. Its market represents 62 % of total world RCN imports. Indian imports of RCN have grown by 33 % on average since 2007. Viet Nam is the second largest global importer of cashews with imports of US $ 557 million. Viet Nam started from a smaller import base of US $ 239 million in 2008 and has made important efforts to develop its processing capacity. Brazil’s new processing factories are also competing for RCN with Viet Nam and India. Brazil’s nascent industry is seeking to import cashew nuts in large volumes, which explains the impressive growth of imports over the last five years. The three largest importers’ share of world RCN imports represents more than 96 % of global imports. It should be noted that smaller markets like China, Belgium, the United Arab Emirates ( UAE ) and Sri Lanka are also showing signs of rapid growth in RCN imports.

The import market for RCN is highly concentrated, with limited opportunities for exporters to seek new clients. The three largest buyers of cashew are currently compet-ing for nuts in order to keep their industries functioning. This situation increases the value of RCN exports and creates a global scarcity which is leading to the closure of smaller processing facilities incapable of acquiring RCN at a reasonable price.

The import market for cashew kernels ( without shell ) is valued at US $ 2.5 billon ( 2012 ) with an average growth rate of 9 % for the 2008-2012 period.

The United States of America is the largest importer of processed cashew nuts with an import value of US $ 817 million ( 2012 ). This important market has been the lead-ing importer of kernels for many years and is growing at the average global rate of 9 %. The Netherlands ranks as the second largest importer globally but is growing more slowly than the world average. Large import mar-kets growing rapidly include Saudi Arabia ( 29 % growth ), Thailand ( 26 % ), Italy ( 24 % ), Germany ( 18 % ) and Japan ( 14 % ). All of these markets are growing at rates higher that the global average, therefore gaining market shares.

The current top five largest importers of kernels represent more than 60 % of total imports. The import market for ker-nels is not as concentrated as the market for RCN. Even though the United States and the Netherlands represent key destinations for kernels, other smaller markets are emerging rapidly. This signifies a growing demand for cashew kernels.

11WHERE WE ARE NOW

Table 3 : Major importers of cashew nuts in shell and without shell, 2011 and 2012

Cashew nuts, in shell, fresh or dried ( HS080131 ) Cashew nuts, without shell, fresh or dried ( HS080132 )

Importers Value import-ed in 2011

( US $ thou-sands )

Annual growth in

value2007-2011

( % )

Share in world imports

( % )

Importers Value im-ported in

2012 ( US $ thousands )

Annual growth in

value2008-2012

( % )

Share in world im-ports ( % )

World 1 838 604 36 100 World 2 504 667 9 100

India 1 142 633 33 62.2 United States 817 463 9 32.6

Viet Nam 557 718 44 30.3 Netherlands 278 622 7 11.1

Brazil 57 393 105 3.1 Germany 216 170 18 8.6

France 18 403 13 1 Australia 112 138 11 4.5

United States 10 643 12 0.6 United Kingdom

97 396 1 3.9

UAE 9 566 156 0.5 UAE 86 068 2 3.4

United Kingdom

8 021 65 0.4 Canada 73 132 9 2.9

Nigeria 6 046 348 0.3 Japan 61 490 14 2.5

Indonesia 5 476 107.75 0.3 Russian Federation

53 524 10 2.1

Saudi Arabia 4 485 n.a. 0.2 France 48 767 7 1.9

South Africa 1,848 -24.25 0.1 Thailand 46 704 26 1.9

Italy 1 632 27.75 0.1 Saudi Arabia 44 243 29 1.8

Canada 1 437 19.75 0.1 Belgium 42 678 5 1.7

Sources : ITC calculations based on UN Comtrade statistics. The world aggregation represents the sum of reporting and non-reporting countries. The data in this colour represent mirror figures based on partner data.

MAJOR EXPORTERS

The export market for raw cashew nuts ( RCN ) ( HS 080131 ) is worth approximately US $ 1.5 billion ( 2011 )24 with an an-nual average growth rate of 31.9 % for 2007–2011.

African countries dominate the exports of RCN with nine of the top ten exporters. Côte d’Ivoire exported 61.2 % of its production and provided 30 % of global exports in 2011. Guinea-Bissau is, according to mirror data, the sec-ond largest exporter of RCN with a 17.4 % market share. Taken together the top three African ( excluding Ghana for statistical reasons ) exporters represent almost 60 % of global RCN exports. Other major producers such as Viet Nam, India and Brazil almost entirely process their production with limited exports. As will be discussed be-low, The Gambia is the 15 th largest exporter of cashews in the world but only has a 0.1 % market share.

24. For RCN imports and exports 2011 data is used as a reference due to inconsistencies with the 2012 data.

The export market for cashew kernels ( HS080132 ) is worth US $ 2.4 billion globally ( 2012 ), with an annual av-erage growth rate of 9 % for 2008–2012.

Viet Nam has been the largest exporter of cashew ker-nels since 2008. In 2012, it exported US $ 1 billion worth of kernels and was continuing to grow its exports above the global average of 9 %, thereby confirming its domi-nant position in this market. India was, until 2008, the world leader in kernel exports and has now become the second most important with exports of US $ 765 million. India is currently growing below the world average and losing some market share to other fast growing exporters.

12 THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

Figure 1 : Growth trends for global imports of cashew kernels between 2007 and 2011 ( US $ billions )

Impo

rts

(US$

bill

ions

)

Impo

rts,

mill

ions

of t

ons

2010200920082007

0

0,2

0,4

0,6

0,8

1

1,2

0

0,2

0,4

0,6

0,8

1

1,2

1,4

1,6

1,8

2

2011

Value Volume

Source : ITC calculations based on UN Comtrade statistics.

Table 4 : Major exporters of cashew nuts in shell and without shell, 2011 and 2012

Cashew nuts, in shell, fresh or dried ( HS080131 ) Cashew nuts, without shell, fresh or dried ( HS080132 )

Exporters Value ex-ported in

2011 ( US $ thousands )

Annual growth in

value2007-2011

( % )

Share in world exports

( % )

Exporters Value ex-ported in

2012 ( US $ thousands )

Annual growth in

value2008-2012

( % )

Share in world exports

( % )

World 1 554 479 9 100 World 2 456 680 9 100

Côte d’Ivoire 262 565 33.5 30.2 Viet Nam 1 079 042 11 43.9

Guinea-Bissau 266 335 17.1 India 765 635 7 31.2

Ghana n.a. n.a. n.a. Brazil 185 691 –1 7.6

Nigeria 187 543 93.5 12.1 Netherlands 183 631 16 7.5

United Republic of Tanzania

105 699 209.25 6.8 Germany 39 538 8 1.6

Indonesia 56 296 1 3.6 Indonesia 24 950 0 1

Burkina Faso 55 882 353.5 3.6 Belgium 24 272 5 1

Mozambique 53 382 115 3.4 Côte d’Ivoire 18 028 57 0.7

Benin 39 440 28.75 2.5 United Republic of Tanzania

14 453 -10 0.6

Guinea 31 246 0 2 Mozambique 13 854 4 0.6

Mexico 5 265 78.5 0.3 United Kingdom 13 292 26 0.5

UAE 3 376 0.2 United States 11 326 3 0.5

United States 2 966 107 0.2 Singapore 8 333 27 0.3

Mali 2 293 0.1 Ghana 6 497 89 0.3

The Gambia 2 087 2 821.5 0.1 Burkina Faso 6 144 142 0.3

Source : ITC calculations based on UN Comtrade statistics. The world aggregation represents the sum of reporting and non-reporting countries. The data in this colour represents mirror figures based on partner data.

13WHERE WE ARE NOW

Figure 2 : Total value of imports and exports for The Gambia ( 2007–2011 )

–400

–300

–200

–100

0

100

200

Exports (US$ M) 13 14 66 35 95

-320 -329 -303 -285 -343

2007 2008 2009 2010 2011

Imports (US$ M)

US$

Mill

ions

Source : ITC calculations based on UN Comtrade data.

Figure 3 : Gambia fluctuation of RCN exports in value and quantities, mirror data, 2005–2012

US$

thou

sand

s

Tons

201020092008200720062005

0

5000

10000

15000

20000

25000

30000

0

5000

10000

15000

20000

25000

30000

35000

40000

2011 2012

Value Quantities

Source : ITC Calculations based on UN Comtrade data

A number of new countries are emerging at the global lev-el as exporters of kernels. In West Africa, the impressive growth rates of Burkina Faso, Ghana and Côte d’Ivoire should be noted. This growth is in line with the African Cashew Alliance ( ACA ) objective to process 100,000 tons by 2020 25 in Africa. In 2011 the West African economic community exported 32,000 tons of kernels.

25. Ghanaian Chronicle ( n.d. ). ACA Announces Ambitious Cashew Production Target. Available from http : / / thechronicle.com.gh / aca-announces-ambitious-cashew-production-target /

THE GAMBIA’S CASHEW TRADE PERFORMANCE

The Gambia’s liberal market-based economy and memberships in the World Trade Organization and the Economic Community of West African States ( ECOWAS ) provide the country with a good reputation for low import duties and trade-friendly regulations. The efficiency of Banjul’s port in in the subregion presents a critical gate-way for trade. Figure 3 underlines a concerted need to develop The Gambia’s exports. The global growth rate of 9 % ( imports ) for RCN and 9 % for cashew kernels of-fers an opportunity for The Gambian cashew sector to emerge and support the country’s export development.

14 THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

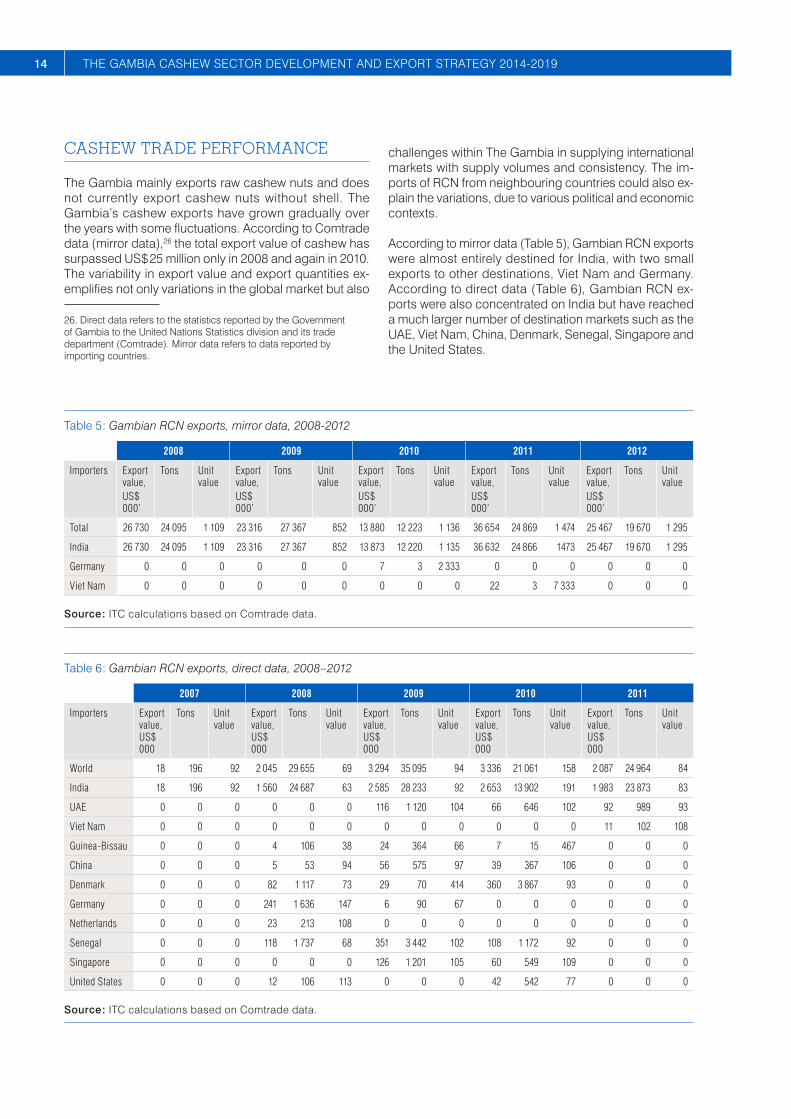

CASHEW TRADE PERFORMANCE

The Gambia mainly exports raw cashew nuts and does not currently export cashew nuts without shell. The Gambia’s cashew exports have grown gradually over the years with some fluctuations. According to Comtrade data ( mirror data ),26 the total export value of cashew has surpassed US $ 25 million only in 2008 and again in 2010. The variability in export value and export quantities ex-emplifies not only variations in the global market but also

26. Direct data refers to the statistics reported by the Government of Gambia to the United Nations Statistics division and its trade department ( Comtrade ). Mirror data refers to data reported by importing countries.

challenges within The Gambia in supplying international markets with supply volumes and consistency. The im-ports of RCN from neighbouring countries could also ex-plain the variations, due to various political and economic contexts.

According to mirror data ( Table 5 ), Gambian RCN exports were almost entirely destined for India, with two small exports to other destinations, Viet Nam and Germany. According to direct data ( Table 6 ), Gambian RCN ex-ports were also concentrated on India but have reached a much larger number of destination markets such as the UAE, Viet Nam, China, Denmark, Senegal, Singapore and the United States.

Table 5 : Gambian RCN exports, mirror data, 2008-2012

2008 2009 2010 2011 2012

Importers Export value,US $ 000’

Tons Unit value

Export value,US $ 000’

Tons Unit value

Export value,US $ 000’

Tons Unit value

Export value,US $ 000’

Tons Unit value

Export value,US $ 000’

Tons Unit value

Total 26 730 24 095 1 109 23 316 27 367 852 13 880 12 223 1 136 36 654 24 869 1 474 25 467 19 670 1 295

India 26 730 24 095 1 109 23 316 27 367 852 13 873 12 220 1 135 36 632 24 866 1473 25 467 19 670 1 295

Germany 0 0 0 0 0 0 7 3 2 333 0 0 0 0 0 0

Viet Nam 0 0 0 0 0 0 0 0 0 22 3 7 333 0 0 0

Source : ITC calculations based on Comtrade data.

Table 6 : Gambian RCN exports, direct data, 2008–2012

2007 2008 2009 2010 2011

Importers Export value, US $ 000

Tons Unit value

Export value, US $ 000

Tons Unit value

Export value, US $ 000

Tons Unit value

Export value, US $ 000

Tons Unit value

Export value, US $ 000

Tons Unit value

World 18 196 92 2 045 29 655 69 3 294 35 095 94 3 336 21 061 158 2 087 24 964 84

India 18 196 92 1 560 24 687 63 2 585 28 233 92 2 653 13 902 191 1 983 23 873 83

UAE 0 0 0 0 0 0 116 1 120 104 66 646 102 92 989 93

Viet Nam 0 0 0 0 0 0 0 0 0 0 0 0 11 102 108

Guinea-Bissau 0 0 0 4 106 38 24 364 66 7 15 467 0 0 0

China 0 0 0 5 53 94 56 575 97 39 367 106 0 0 0

Denmark 0 0 0 82 1 117 73 29 70 414 360 3 867 93 0 0 0

Germany 0 0 0 241 1 636 147 6 90 67 0 0 0 0 0 0

Netherlands 0 0 0 23 213 108 0 0 0 0 0 0 0 0 0

Senegal 0 0 0 118 1 737 68 351 3 442 102 108 1 172 92 0 0 0

Singapore 0 0 0 0 0 0 126 1 201 105 60 549 109 0 0 0

United States 0 0 0 12 106 113 0 0 0 42 542 77 0 0 0

Source : ITC calculations based on Comtrade data.

15WHERE WE ARE NOW

Box 2 : Indian market in perspective

India is the leading global importer of raw cashew nuts and the main destination market for Gambian cashews. India imports cashew from various countries, namely Côte d’Ivoire, Benin, the United Republic of Tanzania and Guinea-Bissau. Gambia’s cashew represents only 2 % of the total imports of India. India imports a growing volume of cashew nuts in order to satisfy a growing domestic demand for cashew kernels. Therefore the Indian market will remain a key destination market for Gambian cashews over the next few years.

Figure 4 : Sources of India’s RCN 2012

Côte d’Ivoire30%

Benin19%United Republic

of Tanzania14%

Guinea-Bissau

11%

Ghana10%

Indonesia5%

Gambia2% Senegal

1%

Others4%

Guinea1%

Nigeria3%

Source : ITC calculations based on UN Comtrade statistics

Figure 5 : Changing trends in India’s cashew sector

Imports

566 544 495572 573

489

599 620

480

649 665

462

728 695

446

Production Exports

2005 2006 2007 2008 2009

India est raw cashew production, imports, and exportsin million kgs

Source : Red River Foods, 2010

The important difference between direct and mirror data indicates a clear need to enhance data collection for the cashew sector. In either case, India remains the main destination market for Gambian RCN as it absorbs more than 95 % of exports.

As indicated earlier, The Gambia is world’s 15th largest exporter with a 0.1 % market share in the global RCN mar-ket. This performance is mostly due to constant exports of RCN, mainly to India, in the last few years. The good performance of The Gambia remains precarious as new ports are gaining importance in West Africa and will most certainly compete to attract some of the cashew export business. If they are successful then re-exports from The Gambia would be challenged and total export volume reduced. As indicated in the competitiveness constraints section, a number of key challenges at all levels of the value chain need to be addressed in order to maintain and expand the cashew business in The Gambia.

THE INSTITUTIONAL PERSPECTIVEThe Gambia is yet to build an elaborate network of trade support institutions ( TSIs ) which can reliably support trade development operations. In the case of cashew,

the situation is positive since a number of private, non-for-profit organizations and sector associations are effec-tively supporting the development of the sector.

The TSIs providing important services to The Gambian cashew sector can be categorized according to the fol-lowing support areas :

� Policy support network � Trade services network � Business services network � Civil society network.

Tables 7 to 10 identify the main TSIs whose service deliv-ery affects the cashew sector in The Gambia. An assess-ment of the TSIs along three key dimensions – importance of the TSI to sector development, current level of respon-siveness to the sector’s needs, and resource availability – was completed. The ranking ( high / medium / low ) for each TSI was completed by sector stakeholders on the basis of their perception.

16 THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

POLICY SUPPORT NETWORK

The institutions in the policy support network represent ministries and competent authorities responsible for in-fluencing or implementing policies at the national level.

Table 7 : Gambian cashew sector policy support network

Name DescriptionImportance of TSI to sector development

Level of responsiveness to sector needs

Resources available

to support the sector

Ministry of Agriculture ( MOA )

MOA is in charge of driving the government agen-da with respect to agriculture and all related activ-ities. It oversees the activities of national agencies involved in agricultural development such as NARI and Departments of Agriculture for the imple-mentation of agricultural-based policies and pro-grammes. MOA collects agricultural data on area, yield and production, and trains farmers.

H L M

Ministry of Trade, Regional Integration & Employment ( MOTIE )

MOTIE is responsible for trade policy, industrial de-velopment, employment creation, export develop-ment and overall private sector development.

H M L

Ministry of Finance & Economic Affairs ( MOFEA )

The main responsibilities of MOFEA are fiscal and monetary policy management including budget al-locations, prioritization of development projects, revenue generation ( taxes and customs duties ) and focal institution projects.

M L H

Ministry of Basic and Secondary Education ( MOBSE )

MOBSE is responsible for the education of children and youth in The Gambia. As part of their work they have 200 farms of 0.5 ha that can be used as training grounds. Furthermore, MOBSE can act as a transmission channel for information.

M M H

TRADE SUPPORT NETWORK

These institutions or agencies provide a wide range of trade related services to both government and enterprises.

Table 8 : Gambian cashew sector trade support network

Name Description

Importance of TSI

to sector development

Level of responsiveness to sector needs

Resources available

to support the sector

Gambia Chamber of Commerce and Industry ( GCCI )

GCCI supports exporters and provides them with certificates of origin, and promotes export trade. Several cashew traders are members of GCCI. It also assists with advocacy, lobbying and arbitration.

H M M

Gambia Investment and Export Promotion Agency ( GIEPA )

GIEPA is the investment and export development institution of The Gambia. It is leading implementa-tion of the government’s NES and is well positioned to assist export development of the cashew sector.

H M M

17WHERE WE ARE NOW

Name Description

Importance of TSI

to sector development

Level of responsiveness to sector needs

Resources available

to support the sector

Gambia Standards Bureau ( GSB )

The Gambia Standards Bureau was set up by The Gambia Standards Bureau Act of 2010. GSB was established to develop and promulgate standards, offer services in the field of metrology, and conduct conformity assessments. For the cashew sector it is establishing a standard for cashew nut exports, and can proceed to controls of weights and con-duct quality testing. GSB is not responsible for ac-creditation.

H L L

Food Safety and Quality Authority ( FSQA )

FSQA, under the Office of the Vice President, is re-sponsible for food quality and safety to ensure that food that enters and exits the country is of high standard and good quality.

H L L

Gambia Bureau of Statistics ( GBOS )

The Gambia Bureau of Statistics is the highest au-thority on all statistics in the country, including crop area, yield and production. It is responsible, with MOA, to compile reliable data about cashew pro-duction.

H L H

National Agriculture Research Institute ( NARI )

NARI is responsible for undertaking research on cashew varieties ; is in charge of seedling selection, multiplication and certification ; and provides exten-sion services to farmers.

H L L

Gambia Ports Authority ( GPA )

The Gambia Ports Authority is responsible for the functioning and efficiency of the Port of Banjul. Port efficiency is critical to the cashew export business.

H H M

Gambia Revenue Authority ( GRA )

For the cashew sector, GRA is responsible for promptly assessing, collecting and accounting for all revenues due to the government and for simpli-fying and standardizing procedures and legislation without increasing the compliance burden or hin-dering trade.

H M H

BUSINESS SERVICES NETWORK

These are associations, or major representatives, of com-mercial service providers used by exporters to carry out international trade transactions.

Table 9 : Gambian cashew sector business services network

Name DescriptionImportance of TSI to sector development

Level of responsiveness to sector needs

Resources available

to support the sector

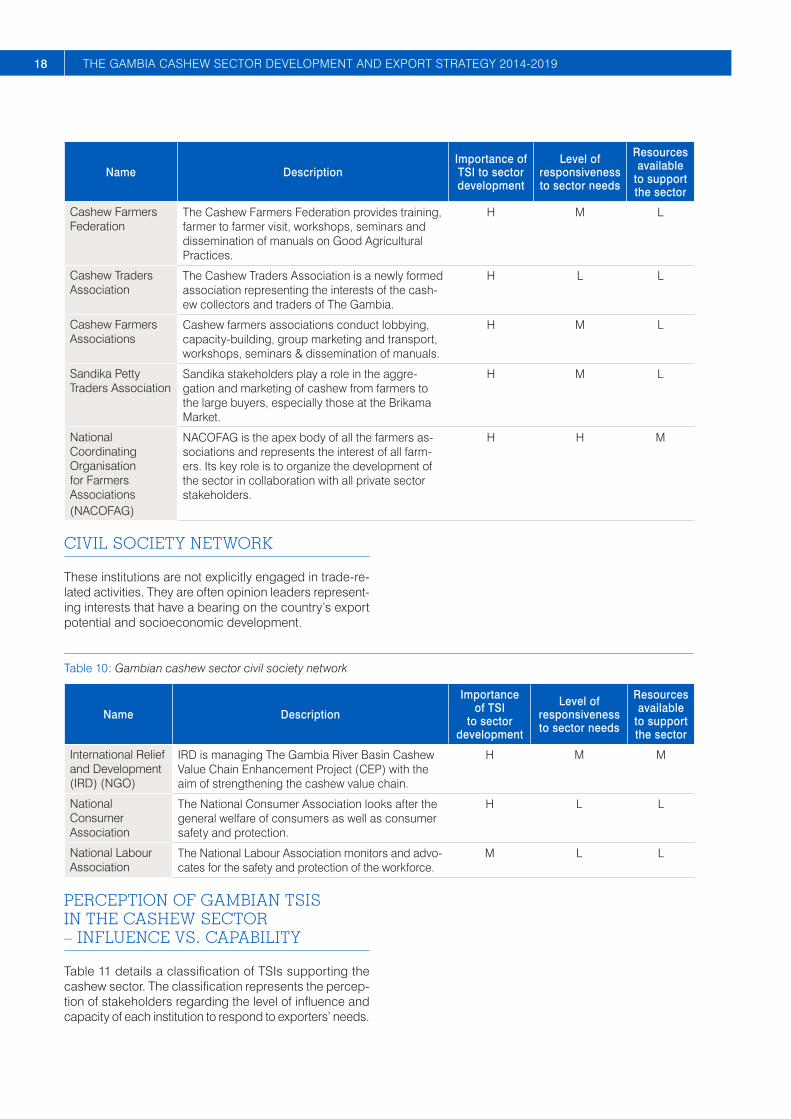

Cashew Alliance of The Gambia ( CAG )

CAG is the apex body of the cashew sector and represents the interests of all sector stakeholders, namely the members of the alliance. It key role is to organize the development of the sector in col-laboration with all private sector stakeholders

H L L

18 THE GAMBIA CASHEW SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

Name DescriptionImportance of TSI to sector development

Level of responsiveness to sector needs

Resources available

to support the sector

Cashew Farmers Federation

The Cashew Farmers Federation provides training, farmer to farmer visit, workshops, seminars and dissemination of manuals on Good Agricultural Practices.

H M L

Cashew Traders Association

The Cashew Traders Association is a newly formed association representing the interests of the cash-ew collectors and traders of The Gambia.

H L L

Cashew Farmers Associations

Cashew farmers associations conduct lobbying, capacity-building, group marketing and transport, workshops, seminars & dissemination of manuals.

H M L

Sandika Petty Traders Association

Sandika stakeholders play a role in the aggre-gation and marketing of cashew from farmers to the large buyers, especially those at the Brikama Market.

H M L

National Coordinating Organisation for Farmers Associations( NACOFAG )

NACOFAG is the apex body of all the farmers as-sociations and represents the interest of all farm-ers. Its key role is to organize the development of the sector in collaboration with all private sector stakeholders.

H H M

CIVIL SOCIETY NETWORK

These institutions are not explicitly engaged in trade-re-lated activities. They are often opinion leaders represent-ing interests that have a bearing on the country’s export potential and socioeconomic development.

Table 10 : Gambian cashew sector civil society network

Name Description

Importance of TSI

to sector development

Level of responsiveness to sector needs

Resources available

to support the sector

International Relief and Development ( IRD ) ( NGO )

IRD is managing The Gambia River Basin Cashew Value Chain Enhancement Project ( CEP ) with the aim of strengthening the cashew value chain.

H M M

National Consumer Association

The National Consumer Association looks after the general welfare of consumers as well as consumer safety and protection.

H L L

National Labour Association

The National Labour Association monitors and advo-cates for the safety and protection of the workforce.

M L L

PERCEPTION OF GAMBIAN TSIS IN THE CASHEW SECTOR – INFLUENCE VS. CAPABILITY

Table 11 details a classification of TSIs supporting the cashew sector. The classification represents the percep-tion of stakeholders regarding the level of influence and capacity of each institution to respond to exporters’ needs.

19WHERE WE ARE NOW

Table 11 : Perception of Gambian cashew sector TSIs – influence vs. capability

Capacity of institution to respond to sector’s needs

Low High

Level of influence

on the sector

High

• Ministry of Agriculture• Ministry of Trade, Regional Integration & Employment• Gambia Chamber of Commerce & Industry• Gambia Investment and Export Promotion Agency• Gambia Standards Bureau• National Agriculture Research Institute• Cashew Farmers Federation• Cashew Traders Association• Cashew Farmers Associations• Sandika Petty Traders Association

• International Relief and Development• Gambia Ports Authority• Gambia Revenue Authority

Low

• Food Safety and Quality Authority• Cashew Alliance of The Gambia• National Consumer Association• National Labour Association

• Gambia Bureau of Statistics• Ministry of Finance and Economic Af-

fairs• Ministry of Basic and Secondary Edu-

cation

Three institutions are perceived as having both strong in-fluence and resources ( capacity ) to respond to the needs of the cashew sector. IRD is seen as being proactive to sector members’ interests. The Gambia Ports Authority is considered efficient and is seen as playing its role of facilitating exports well. GRA is also seen as influential and well-resourced in enhancing the processing of cus-toms documentation, checking compliance and avoiding cumbersome procedures.