The future challenges of Healthcare - Roche - Doing now ...31660fae-5f86-46d3-b3f5-14aeda047e… ·...

12

1 r The future challenges of Healthcare Dr. Erich Hunziker CFO – F. Hoffmann La Roche Ltd. San Francisco, January, 2006 r 2 This presentation contains certain forward-looking statements. These forward-looking statements may be identified by words such as “believes”, “expects”, “anticipates”, “projects”, “intends”, “should”, “seeks”, “estimates”, “future” or similar expressions or by discussion of strategy, goals, plans or intentions. Various factors may cause actual results to differ materially in the future from those reflected in forward-looking statements contained in this presentation among others: 1. Pricing and product initiatives of competitors; 2. Legislative and regulatory developments and economic conditions; 3. Delay or inability in obtaining regulatory approvals or bringing products to market; 4. Fluctuations in currency exchange rates and general financial market conditions; 5. Uncertainties in the discovery, development or marketing of new products or new uses of existing products; 6. Increased government pricing pressures; 7. Interruptions in production; 8. Loss of or inability to obtain adequate protection for intellectual property rights; 9. Litigation; 10. Loss of key executives or other employees; and... 11. Adverse publicity or news coverage For marketed products discussed in this presentation, please see full prescribing information on our website – www.roche.com

Transcript of The future challenges of Healthcare - Roche - Doing now ...31660fae-5f86-46d3-b3f5-14aeda047e… ·...

1

r

The future challenges of Healthcare

Dr. Erich Hunziker CFO – F. Hoffmann La Roche Ltd.

San Francisco, January, 2006

r

2

This presentation contains certain forward-looking statements.These forward-looking statements may be identified by words such as “believes”, “expects”, “anticipates”, “projects”, “intends”, “should”, “seeks”, “estimates”, “future”or similar expressions or by discussion of strategy, goals, plans or intentions. Various factors may cause actual results to differ materially in the future from those reflected in forward-looking statements contained in this presentation among others:

1. Pricing and product initiatives of competitors;2. Legislative and regulatory developments and economic conditions;3. Delay or inability in obtaining regulatory approvals or bringing products to market;4. Fluctuations in currency exchange rates and general financial market conditions;5. Uncertainties in the discovery, development or marketing of new products or new uses of

existing products;6. Increased government pricing pressures;7. Interruptions in production;8. Loss of or inability to obtain adequate protection for intellectual property rights;9. Litigation;10. Loss of key executives or other employees; and...11. Adverse publicity or news coverage

For marketed products discussed in this presentation, please see full prescribing information on our website – www.roche.com

2

r

3"Healthcare events" dominate or at least influence the life of most people

consultation with themedical community

self testing / self medication

researchactivities

diagnostics events prescriptions /consumption

of drugs

medical therapies

No change from the past:Health remains a basic need of mankind

r

4

The view of Pharma has changed

• Strong demand for drugs

• Strong earnings growth: sales growth drives margins expansion

• Pharma low risk: defensive qualities

• Blockbuster business model: in particular for GP drugs

• Growth rates slowing down in average

• Price pressure: limited budgets for health care systems

• Investors more focusing on risks: patent, regulatory and liability

• Blockbuster also in specialty care

From sector approach to evaluation of individual companies

From sector approach to evaluation of individual companies

In the nineties In the nineties and nowadays and nowadays

3

r

5

no. of healthcare events

today 2020

Access to healthcare

Health awareness

Higher life expectancy

Population growth

Researchactivities

No change from the past:There is an big increase in demand for healthcare

r

6

Incidence of cancer increasing

Cancer Disease: All sites but non-melanoma skin

0

100

200

300

400

500

600

700

1953

1954

1955

1956

1957

1958

1959

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

Age Standardised Rate (World)

Year

Czech Republic

Denmark

England, South Thames Region

Finland

Germany, Saarland

Netherlands, Eindhoven

Norway

Poland, Cracow City

Sweden

SubCountry

Source: A pan European comparison regarding patient access to cancer, Karolinska Institute 2005

4

r

7

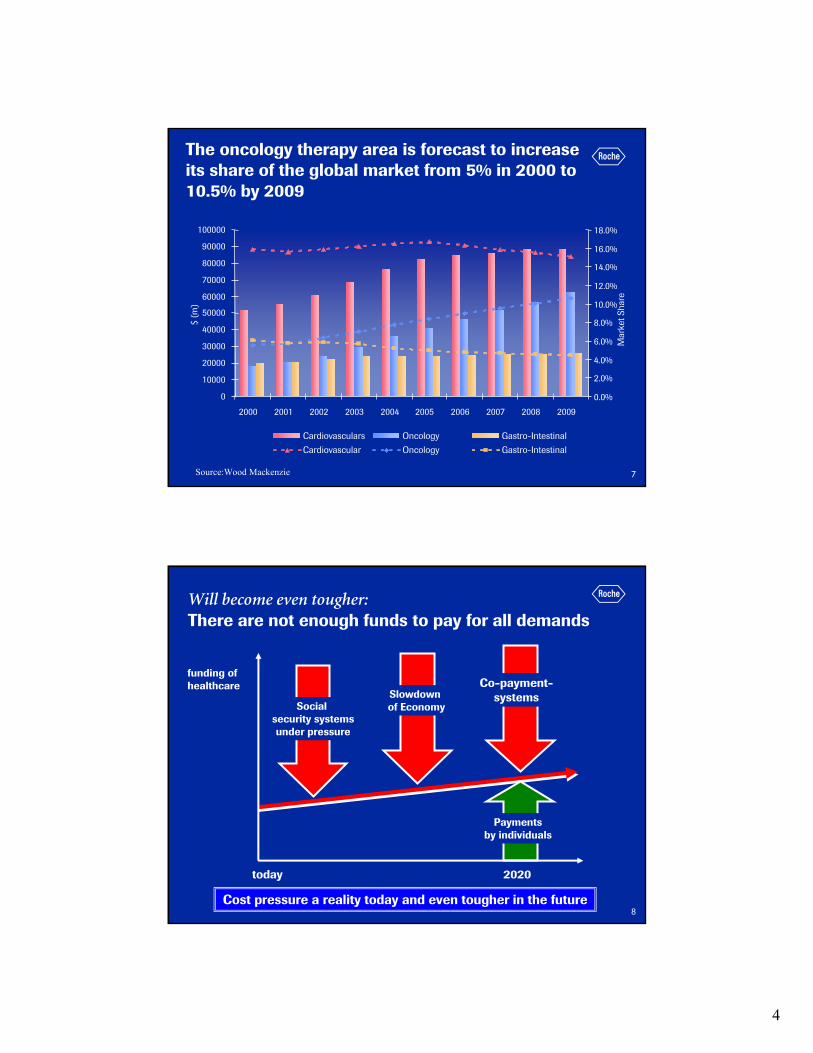

The oncology therapy area is forecast to increase its share of the global market from 5% in 2000 to 10.5% by 2009

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

$ (m

)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Mar

ketS

hare

Cardiovasculars Oncology Gastro-Intestinal

Cardiovascular Oncology Gastro-Intestinal

Source:Wood Mackenzie

r

8

today 2020

Paymentsby individuals

Co-payment-systemsSlowdown

of EconomySocial security systemsunder pressure

funding of healthcare

Will become even tougher:There are not enough funds to pay for all demands

Cost pressure a reality today and even tougher in the future

5

r

9

Cancer- a similar burden to society as cardiovascular disease

6.78.43,167,6755.97.83,523,243Respiratory disease

7.79.63,644,6208.711.25,099,011Injuries

16.921.17,989,86416.721.79,839,035Cancer

16.220.17,637,49317.122.210,088,093Cardiovascular disease

26.332.712,379,28225.332.814,857,720Mental disease

100124.247,092,868100129.758,807,846All disease groups

%DALY /1000Total DALYs%DALY /1000Total DALYs

EU 15EU 25

DALY: Disability – Adjusted Life Years. Integrated measure of mortality and disability developed by the WHO. One DALY is one lostyear of ‘healthy’ life and the burden of disease as a measurement of the gap between actual health and an ideal situation

Source: A pan European comparison regarding patient access to cancer, Karolinska Institute 2005

r

10

But still a comparably low public expenditures on oncology

Source: Wood Mackenzie

2004

2009

CAGR – 2004/2009

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

Cardiovasculars

Central Nervo

us System

Anti-Infective

s

Metabolism

Oncology

Musculoskeletal/Pain

Respiratory

Gastro-Intestin

al

Genito-Urinary

Dermatology

Vaccines

Ophthalmology

Transplant

Sale

s ($

m)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

CA

GR

6

r

11

Premium for innovation’ must be earned by ‘medical differentiation’

high

low

low high

Med

ical

Diff

eren

tati

on

Premium for innovation

Value stra

tegy

high value eve

nts

e.g. Onco

logy

Volume strategy high volume events

e.g. Generics

Roche FocusRoche Focus

r

12

New treatment options offer substantial benefits to patients. Example: Early Breast Cancer:

Relative risk reduction of recurrence (%)0 10 20 30 40

17%

42%

46%

31%

CEF vs CMFLevine 2005

AC → T vs ACHenderson 2003

Chemo → Herceptin vschemo Piccart 2005

Tamoxifen vs placeboFisher 2004

DAC vs FACMartin 2005

28%

HER2+

HER2+&

HER2-

A = doxorubicin; C = cyclophosphamide; D = docetaxel; E = epirubicin; F = 5-fluorouracil; M = methotrexate; T = paclitaxel

Chemo + Herceptin vs chemoRomond 2005

50

52%

Best chance of a cure with new adjuvant treatment optionsBest chance of a cure with new adjuvant treatment options

7

r

13

Innovation

Marketingpower

1. Innovative products continue to command high prices and reimbursement,

2. Selling “average /me-too” products by sheer marketing power becomes more and more difficult

Roche strategic choice: Innovation is key !

Only if we create relevant proven benefit for the customer = medically differentiated products, we will be able to create high value returns

r

14

From „traditional Pharma“ to „individualized medicine“

Efficiency gains and

value contributions to healthcare

time

„traditional Pharma“

„size matters“

individualized medicine /

targeted therapy

2004 ?

basic research and molecular diagnostics are already on the next s-curve

8

r

15

Where does size really matter ?

DiscoveryResearch

Develop-ment

Manu-facturing

MarketingSelling

Intellectintensive

Capital intensive

Size does not increase productivity beyond a certain critical level!

Size is critical to optimize investment, speed and coverage!

Economies of scope Economies of scale: Size matters

•More trials•More patients•Investigator networks•In-licensing power

•More launches•Larger products•Market entry speed•Sales force flexibility

Source: Decision resources Spectrum May 03; MacKinsey 01

r

16

Joint learning (e.g. identifyingthe right technology at the

right point in time)

Roche as one partner of choicefor the scientific community

(e.g. deCODE) and for top talent

Diagnostics+ Pharma =Value added

Roche as a

key producer

of biologics

Diagnostics and

Pharma to

exploit the

same

technology

know-how (e.g.

Genomics,

Genetics)

A unique Roche advantage: two high tech businesses joining forces where it adds value

9

r

17

"Pharmaceutical" companies

We are open to innovation generated bythird parties

ResearchDevelop-ment

Marke-ting +Distri-bution

Pro-duction

"Biotech" companies

CustomerbenefitInnovation

r

18

The unique Roche innovation cosmos

Alliances, collaborations and In-Licensing

Spin-offs

r

Pha

rmac

eutic

als

r

Dia

gnos

tics

volatility

innovation advantage short-lived

value in software

networks

10

r

19

A lot is speculated about the fight for „information leadership“ in healthcare

innovation advantageshort-lived

channel power

individual decideson value spending

individual has accessto original information

volatility

networks

value in software

cost leadership is key

Will decision processeschange dramatically?

Will Microsoft, G

E, Siemens,

IBM be the key competitors?

With Diagnostics we havea „foot in the door“ to be a playerin actionable health information

r

20

Will Roche be marginalised geographically because we focus on high value business?

innovation advantageshort-lived

channel power

individual decideson value spending

individual has accessto original information

volatility

networks

value in software

cost leadership is key

economic value generationin US, Europe, Asia

population centers US, Asia, Latin America

Roche is strongin the emerginggrowth centres

of the world

11

r

21

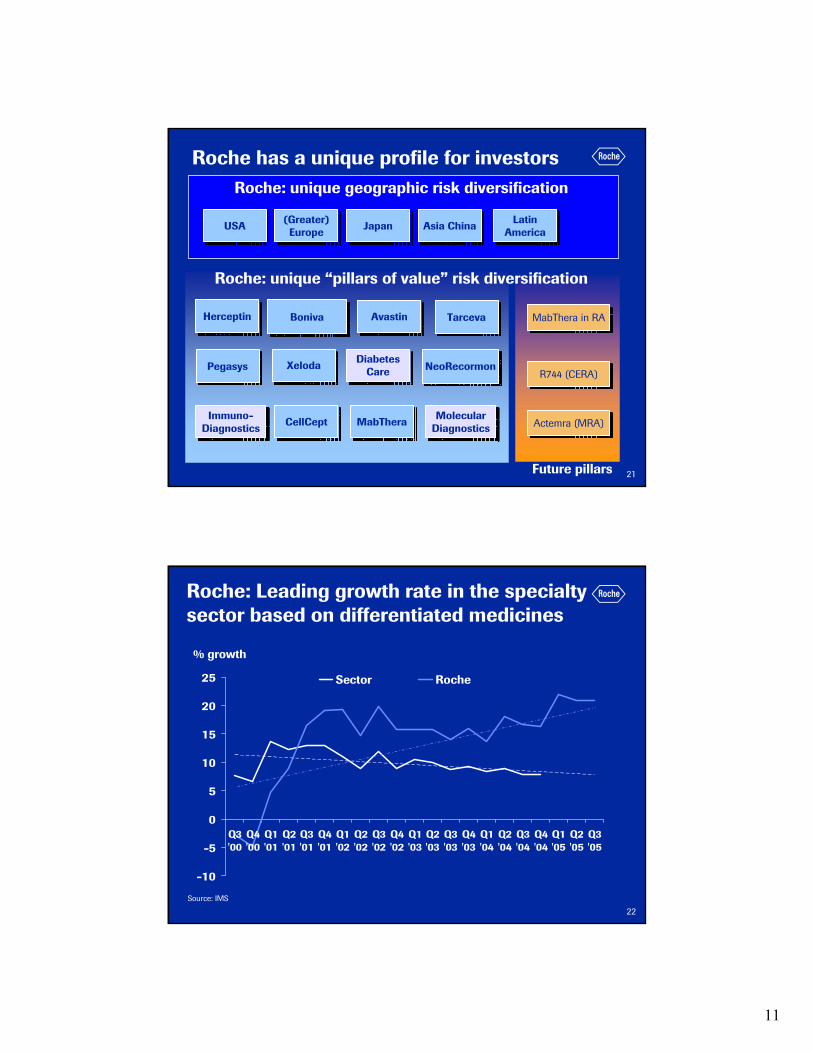

Roche has a unique profile for investors

CellCeptCellCept

PegasysPegasys NeoRecormonNeoRecormon

HerceptinHerceptin

XelodaXeloda

MabTheraMabThera

AvastinAvastin

Future pillars

Actemra (MRA)Actemra (MRA)

BonivaBoniva MabThera in RAMabThera in RA

Diabetes Care

Diabetes Care

Molecular DiagnosticsMolecular

DiagnosticsImmuno-

DiagnosticsImmuno-

Diagnostics

R744 (CERA)R744 (CERA)

USAUSA (Greater)Europe

(Greater)Europe JapanJapan Asia ChinaAsia China Latin

AmericaLatin

America

TarcevaTarceva

Roche: unique geographic risk diversification

Roche: unique “pillars of value” risk diversification

r

22

Roche: Leading growth rate in the specialty sector based on differentiated medicines

-10

-5

0

5

10

15

20

25

Q3'00

Q4'00

Q1'01

Q2'01

Q3'01

Q4'01

Q1'02

Q2'02

Q3'02

Q4'02

Q1'03

Q2'03

Q3'03

Q4'03

Q1'04

Q2'04

Q3'04

Q4'04

Q1'05

Q2'05

Q3'05

Sector Roche

% growth

Source: IMS

12

r

23

Roche ambition: to be a unique investment opportunity in the healthcare industry

“big pharma”

”biotech”

global hightech/biotech

Roche – a unique investment opportunity

with a “foot in the door” to

Individualized healthcare

Pharm

aB

iotech

Informationtechnology

Pfizer

r

![· 2019-02-27 · C[DR\§FRFI" p¿Z U]HZFT I]lGJl;"8L NAAC A (3.02) State University 5F[PAF[PG\PvZ!4 I]lGJl;"8L ZF[04 5F86 spPU]Pf #($Z&5 OF[Gos_Z*&&f ZZZ*$54 Z#_5Z)4 Z#_*$#4 Z##&$(](https://static.fdocuments.us/doc/165x107/5e28c53317fadd3fa308fb19/2019-02-27-cdrfrfi-pz-uhzft-ilgjl8l-naac-a-302-state-university.jpg)

![masc.co.in · 2019-03-07 · C[DR\§FRFI" p¿Z U]HZFT I]lGJl;"8L NAAC A (3.02) State University 5F[PAF[PG\PvZ!4 I]lGJl;"8L ZF[04 5F86 spPU]Pf #($Z&5 OF[Gos_Z*&&f ZZZ*$54 Z#_5Z)4 Z#_*$#4](https://static.fdocuments.us/doc/165x107/5e71c50126756d35cf4aa6cd/masccoin-2019-03-07-cdrfrfi-pz-uhzft-ilgjl8l-naac-a-302.jpg)

![C[DR\§FRFI" p¿Z U]HZFT I]lGJl;"8L NAAC A (3.02) State University 5F[PAF[PG\PvZ!4 I]lGJl;"8L ZF[04 5F86 spPU]Pf #($Z&5 OF[Gos_Z*&&f ZZZ*$54 …](https://static.fdocuments.us/doc/165x107/5e2e2cf33f4ada6d82462e42/cdrfrfi-pz-uhzft-ilgjl8l-naac-a-302-state-university-5fpafpgpvz4.jpg)

![§FRFI pœZ U]HZFT I]lGJl;8L · 2020. 4. 8. · (p d]bi lc;fal vlwsfzlzl sdc[sdf4 c[dr\n=frfi" pttz u]hzft i]lgjl;"8l4 5f86 tzov5lz5+gl of., vy[" )P l;,[S8 OF.,[v sZ GS,f +(0&+$'5$&+$5](https://static.fdocuments.us/doc/165x107/610e8872aed6a632300dc82c/frfi-pz-uhzft-ilgjl8l-2020-4-8-p-dbi-lcfal-vlwsfzlzl-sdcsdf4-cdrnfrfi.jpg)