The Financial - 18.02.2013

28

The FINANCIAL By MADONA GASANOVA F rom September 2012 till February 2013 the number of Russian tour- ists in Georgia in- creased by 72% compared to the same period of the year before. During the past five months Georgia has hosted 204,495 Russian visitors, of which almost half are friends and relatives of Georgian residents. The number of Russian tourists in Georgia during the same period of 2011/2012 was 119,053. “41% of Russian residents come to Georgia to visit friends and family,” Rusudan Mamat- sashvili, Head of the Planning and Development Department at Georgian National Tourism Administration (GNTA), told The FINANCIAL. © 2013 The FINANCIAL. INTELLIGENCE BUSINESS PUBLICATION WRITTEN EXPRESSLY FOR OPINION LEADERS AND TOP BUSINESS DECISION-MAKERS Feb. 16 Feb. 9 1 USD 1.6568 1.6561 1 EUR 2.2097 2.2213 100 RUB 5.5018 5.4915 1 TRY 0.9372 0.9358 CURRENCIES See on p. 17 See on p. 15 PRIME ADS http://www.finchannel.com 18 February, 2013 News Making Money GEORGIAN WEBSITE http://www.financial.ge Read on p. 23 MONEY TRANSFERS IN JANUARY see on page 4 | WORLD ECONOMIC CLIMATE IMPROVES, SURVEY SHOWS see on page 12 Continued on p. 4 Continued on p. 12 Continued on p. 14 Institutional Trust and Efficacy Frank Klobucar, GORBI Daan Harmsen, GeoCapital Read on p. 6 New Flow of Russian Tourists to Georgia The FINANCIAL S ince the parliamen- tary elections, com- panies operating on the Georgian market have reduced their activities. The business sector has become comparatively pas- sive in recent times, a fact that is confirmed by the latest statis- tics. An almost 20 percent de- crease was observed in register- ing business in 2012 compared to 2011 according to the Public Registry Service. Experts say that the reason for the decrease in registering business is due to the unstable political situation. Besides the elections and relatively unstable political situation, another reason for companies’ relative inactiv- ity is that the current govern- ment intends to revise all of the projects that were started under the previous govern- ment, experts say. Business Activities in Decline since Parliamentary Elections Continued on p. 6 More Than 15,000 Companies Participating in European Business Awards The FINANCIAL By MARIAM PAPIDZE T he European Busi- ness Awards is a European awards programme started in 2006. Since then the European Business Awards has established itself as the ul- timate platform for outstanding businesses in the EU. Designed to celebrate exceptional results across a variety of categories, the EBAs are a global showcase for the best in the business. Continued on p. 8 World Economic Climate Improves, Survey Shows The FINANCIAL T he world economy is showing signs of brightening after six months of stag- nation, according to a global survey of economic experts by the International Chamber of Commerce (ICC) and the Munich-based Ifo in- stitute for economic research. New Labour Code Terminates “Annulment of Contract” The FINANCIAL A ccording to the new version of Labor Code dis- crimination (gen- der, racial, eth- nic, religious, etc.) made by the employer shall be prohib- ited not only during the labor relations (while the employee works), but also during the pre-contractual relations. In such a case, if a person makes a complaint, the burden of proof shall be placed on the employer. Preliminary Statistics Showing Reduction in Imported Shoes The FINANCIAL By MARIAM PAPIDZE T he number of pairs of shoes imported in Georgia in 2012 was 7,874,000, with a total value of USD 393,830,000, according to the National Statistics Of- fice of Georgia. Industrial Production Up By 0.7% in Euro Area How can Georgia stimulate innovative entrepreneurship?

-

Upload

cis-bankers -

Category

Economy & Finance

-

view

1.099 -

download

2

Transcript of The Financial - 18.02.2013

The FINANCIALBy MAdoNA GAsANovA

From September 2012 till February 2013 the number of Russian tour-ists in Georgia in-

creased by 72% compared to the same period of the year before. During the past five months Georgia has hosted 204,495 Russian visitors, of which almost half are friends and relatives of Georgian

residents.The number of Russian

tourists in Georgia during the same period of 2011/2012 was 119,053.

“41% of Russian residents come to Georgia to visit friends and family,” Rusudan Mamat-sashvili, Head of the Planning and Development Department at Georgian National Tourism Administration (GNTA), told The FINANCIAL.

© 2013 The FINANCIAL. INTeLLIgeNCe busINess pubLICATIoN written expressly for opinion leaders and top business decision-makers

Feb. 16 Feb. 9

1 USD 1.6568 1.65611 EUR 2.2097 2.2213100 RUB 5.5018 5.49151 TRY 0.9372 0.9358

CURRENCIES

see on p. 17 see on p. 15

prim

e a

ds

http://www.finchannel.com18 February, 2013 News Making MoneyGeorGIAN weBsITe http://www.financial.ge

Read on p. 23

MoNEY TRaNSfERS IN JaNUaRY see on page 4 | WoRlD ECoNoMIC ClIMaTE IMpRovES, SURvEY ShoWS see on page 12

Continued on p. 4

Continued on p. 12

Continued on p. 14

Institutional Trust and Efficacy

Frank Klobucar, GorbiDaan Harmsen, Geocapital

Read on p. 6

New Flow of Russian Tourists to Georgia

The FINANCIAL

Since the parliamen-tary elections, com-panies operating on the Georgian market have reduced their

activities. The business sector has become comparatively pas-sive in recent times, a fact that is confirmed by the latest statis-tics. An almost 20 percent de-crease was observed in register-ing business in 2012 compared to 2011 according to the Public

Registry Service. Experts say that the reason for the decrease in registering business is due to the unstable political situation.

Besides the elections and relatively unstable political situation, another reason for companies’ relative inactiv-ity is that the current govern-ment intends to revise all of the projects that were started under the previous govern-ment, experts say.

Business Activities in Decline since Parliamentary Elections

Continued on p. 6

More Than 15,000 Companies Participating in European Business Awards

The FINANCIALBy MArIAM PAPIdze

The European Busi-ness Awards is a European awards programme started in 2006. Since then

the European Business Awards

has established itself as the ul-timate platform for outstanding businesses in the EU. Designed to celebrate exceptional results across a variety of categories, the EBAs are a global showcase for the best in the business.

Continued on p. 8

World Economic Climate Improves, Survey Shows

The FINANCIAL

The world economy is showing signs of brightening after six months of stag-nation, according

to a global survey of economic experts by the International Chamber of Commerce (ICC) and the Munich-based Ifo in-stitute for economic research.

New LabourCode Terminates“Annulment of Contract”

The FINANCIAL

According to the new version of Labor Code dis-crimination (gen-der, racial, eth-

nic, religious, etc.) made by the employer shall be prohib-ited not only during the labor relations (while the employee works), but also during the pre-contractual relations. In such a case, if a person makes a complaint, the burden of proof shall be placed on the employer.

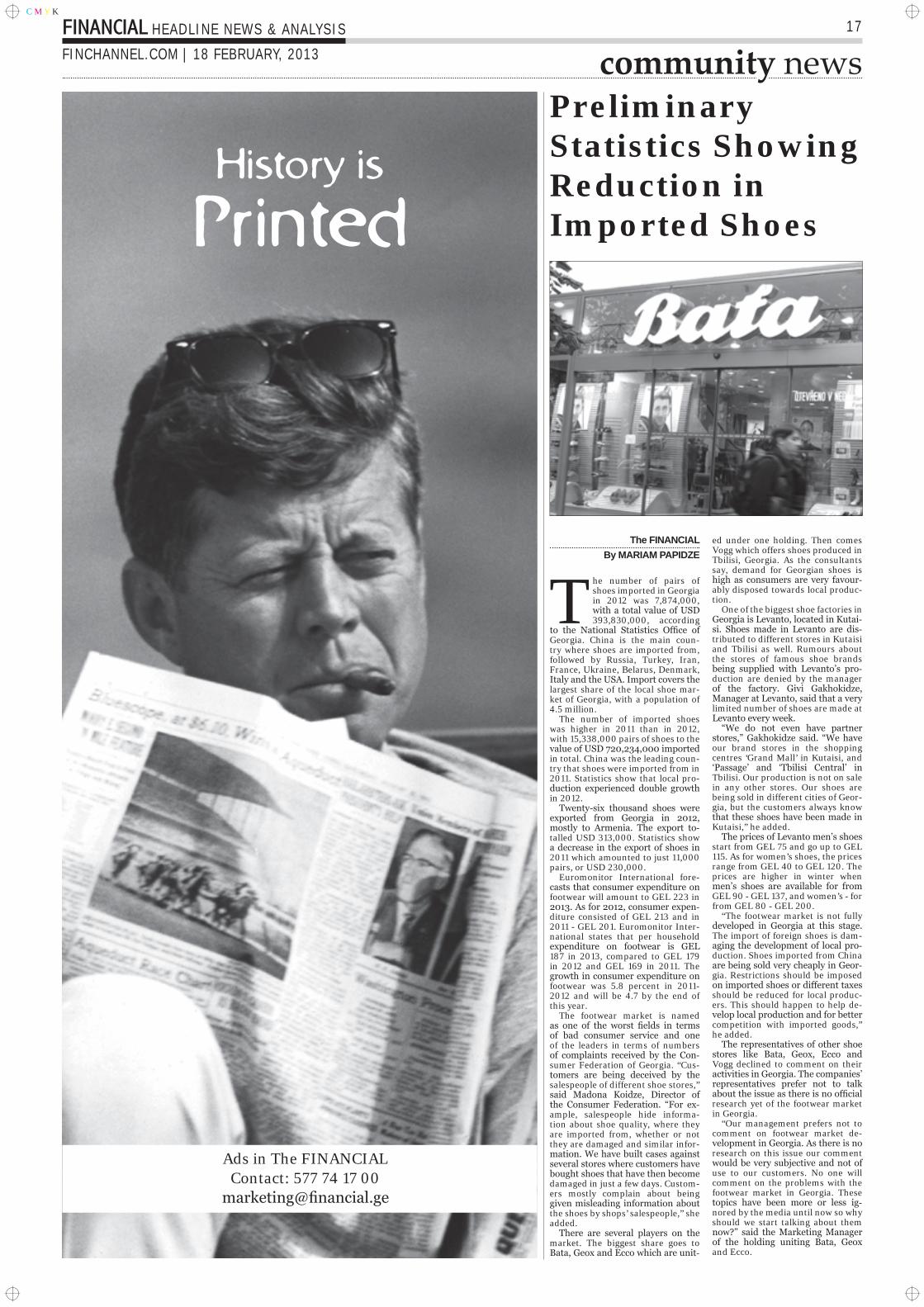

Preliminary Statistics Showing Reduction in Imported Shoes

The FINANCIALBy MArIAM PAPIdze

The number of pairs of shoes imported in Georgia in 2012 was 7,874,000, with a total value of

USD 393,830,000, according to the National Statistics Of-fice of Georgia.

Industrial Production Up By 0.7% in Euro Area

How can Georgia stimulate innovative entrepreneurship?

2 HEADLINE NEWS & ANALYSIS FINANCIAL18 FEbruArY, 2013 | FINcHANNEL.com

C M Y K

financial news

18 February, 2013

CopYRIghT aNDINTEllECTUal pRopERTY polICY

The FINANcIAL respects the intellectual property of others, and we ask our

colleagues to do the same. The material published in The FINANcIAL may not be reproduced without the written consent

of the publisher. All material in The FINANcIAL is protected by Georgian and international laws. The views expressed in The FINANcIAL are not necessarily

the views of the publisher nor does the publisher carry any responsibility for

those views.

pERMISSIoNS

If you are seeking permission to use The FINANcIAL trademarks, logos, service marks, trade dress, slogans, screen shots, copyrighted designs,

combination of headline fonts, or other brand features, please contact publisher. “&” is the copyrighted symbol used by

The FINANcIAL

FINANcIAL (The FINANcIAL) is regis-tered trade mark of Intelligence Group ltd in Georgia and ukraine. Trade mark registration by Sakpatenti - registration

date: october 24, 2007; registration N: 85764; Trade mark registratrion by ukrainian State register body - regis-

tration date: November 14, 2007.

aDvERTISINg

All Advertisements are accepted subject to the publisher’s standard conditions of insertion. copies may be obtained from advertisement and marketing

department. To GET the ADVErTISING rATE cArD

please contact marketing at:[email protected]

see financial media kit onlinewww.finchannel.com/MediaKit

DISTRIBUTIoN

The FINANcIAL distribution network covers 80 % of key companies operating in Georgia. 90 % is

distributed in Tbilisi, batumi and Poti. Newspaper delivered free of charge to more than 600 companies and their

managers. To be included in the list please contact

distribution department at: [email protected]

CoNTaCT US

EDITor-IN-cHIEFzvIaD poChKhUa

E-mAIL: [email protected]@finchannel.com

Phone: (+995 32) 2 252 275

hEAD OF MARKETING lalI JavaKhIa

E-MAIL: [email protected] [email protected]: (+995 577) 74 17 00

coNSuLTANTMaMUKa poChKhUa

E-MAIL: [email protected]: (+995 599) 29 60 40

HEAD oF DISTrIbuTIoN DEPArTmENT TEMUR TaTIShvIlI

E-MAIL: [email protected]: (+995 599) 64 77 76

coPY EDITor:IoNa MaClaREN

commuNIcATIoN mANAGEr: EKa BERIDzE

Phone: (+995 577) 57 57 89

PHoTo rEPorTEr:KhaTIa pSUTURI

MaIlINg aDDRESS:17 mtskheta Str.Tbilisi, Georgia

oFFIcE # 4PHoNE: (+995 32) 2 252 275

FAx: (+95 32) 2 252 276E-mail: [email protected] on the web: www.financial.ge

daily news: www.finchannel.com

Intelligence Group ltd. 2013

ISSUE: 7 (336)© 2013 INTELLIGENCE GROUP LTD

Prices in GELSuper 2.22Premium 2.17Euro Regular 2.05Regular 2.03Euro Diesel 2.26Diesel 2.02CNG 1.10

Prices in GEL

API Super 2.25API Premium 2.20API Diesel 2.25Euro Regular 2.08Regular Energy 2.05Diesel Energy 2.05

Prices in GEL

Eurosuper 2.22Premium Avangard 2.15EuroPremium 0.00Euroregular 2.00Eurodeasel 2.17

Prices in GEL

Super Unleaded 98 2.25Premium Unleaded 96 2.18Euro regular 2.04Regular Unleaded 93 2.02Euro Diesel 5 10 PPM 2.25Diesel L-62 2.02

Prices in GEL

Euro Super 2.25Efix Euro Premium 2.16Euro Regular 93 2.05Efix Euro Diesel 2.22Euro Diesel 2.08

current prices on Gasoline and diesel 18 February, 2013, GeorGia

Gasoline prices presented by BusinessTravelComHotel and airticket bookinG: 2 999 662 | sky.Ge

KhachapuriIndex

KhachapurI Index Is exclusIvely provIded to THe FINANCIAL by IseT

January 2013

KHACHApuRI INDeX: geoRgIAN

CoNsuMeRs eNJoY pRICe sTAbILITY

Florian Biermann is an assistant profes-sor at ISET. He got his Ph.D. in mathematical economics at the Hebrew University of Jeru-salem in Israel

The cost of cooking one standard Imeretian khachapuri in January 2013 averaged 3.44 GEL, which is about 0.3% higher compared to previous month and 1.7% lower compared to January 2012 (i.e. y/y).

Kh-index finding are very similar to those official estimates. According to GeoStat data, annual inflationstands at -1.6%. In other words, Consumer Price Index is currently lower (by 1.6%) than at exactly the same time in 2012. On average, prices have not changed compared to the previous month either. Geo-Stat’s estimate of monthly inflation for Janu-ary is a miniscule 0.2%.

In y/y terms prices of food and non-alcohol-ic beverages declined by 2.7%. Housing, water, electricity and gas commodity group also expe-rienced significant decrease in price (down by 6.5%). These declines were partially balanced out by modest rise in a few other categories: health (up by 2.7%) and Restaurants and ho-tels (up by 3.1%). Overall, considering bigger weight of food category in consumer basket, gen-eral price level declinedin annual terms.

Ever since May 2011, when inflation peaked given the state of frenzy in the global commod-ity markets, inflation has literally come to a halt: since early 2012, monthly inflation rates are fluctuating around the zero trend, in the [-0.9%; 0.9%] range. Annual inflation rates are fluctuating in the [-3.3%; 0.6%] range.Thus we can say that Georgian consumers are enjoying stable (even lower) prices.

eCoNoMIC LessoN oF THe WeeK: THe FuTuRe

oF LAboRAccording to standard economic theory, la-

bor is a good like any other, traded on the labor market. Like with all other markets, the price for labor, which is the wage, ensures that sup-ply meets demand. When there is a shortage of labor, the price of labor goes up, and more people offer their labor on the market. When there is an abundance of labor, a decrease in the price of labor prevents unemployment.

Economics recognizes that there is not just one market for labor, and whenever necessary, one considers special labor markets which are usually defined by the special kind of la-bor traded. In this sense, we speak of “labor market for medical doctors”, the “market for unskilled labor’, or the “market for university graduates”.

obsoLeTe AND NeW LAboR MARKeTs

As it turned out, many labor markets dis-appeared in the course of history. There is no market for blacksmiths and wheelwrights any-more, but the frequent surnames “Smith” and “Wright” in England suggest that in the past, these were common professions. In Georgia one still has gatekeepers who open and close railway crossing gates, but it is likely that this job will disappear in the next years. In devel-oped countries, the railway crossing gates are opened and closed automatically, without a human being actively involved.

On the other hand, also new labor markets emerge. For example, before the raise of com-puter technology, there was hardly a market for computer programmers.

WILL THeRe ALWAYs be DeMAND FoR LAboR?Unemployment is a common phenomenon

in most market economies. Economics has different explanations for unemployment, like market frictions and qualification mismatch. Yet the most common and most fundamental reason for unemployment is usually identified to be too high or too rigid labor costs, which in most cases are made up primarily by wages. Is this explanation convincing? Would the de-mand for blacksmiths and wheelwrights go up if their wages would go down? Nobody would make such a contention. But if the demand for entire professions can virtually disappear, how can we be sure that there is always enough de-mand for labor in general?

A HYpoTHesIs As oLD As CApITALIsM

Starting with the industrial revolution, people feared that the demand for labor might vanish. In the early 19th century, a violent political movement called “The Luddites” in-vaded factory halls in England and destroyed the machines. They felt that the ongoing auto-mation of production processes would make it difficult for them to sell their labor at reason-able prices. Given the rudimentary technol-ogy available in the early 19th century and the enormous productivity gains which occurred ever since, from today’s point of view their concerns seem rather funny. The demand for labor did not fade in the last 200 years. Yet they were right that in principle, there is no mechanism in a market economy which en-sures that there will always be (sufficient) demand for labor. In their book “Race against the Machine”, MIT economists Erik Bryn-jolfsson and Andrew McAfee look at this old question in light of the computer revolution. The argument that we will run out of labor de-mand is centuries old but always turned out to

be wrong. Therefore nobody, including Byn-jolfsson and McAfee, dares to predict the end of labor yet another time. Nonetheless, it is clear that many jobs which were recently con-sidered to be solid sources of income might soon become obsolete. Last time that I was in Germany, my parents surprised me with their new vacuum cleaner robot – the robot vacuum cleans the whole house automatically, one just has to switch it on. Will there be demand for cleaning personnel in 10 years? I myself was a bit worried when I read about a software which constructs mathematical proofs au-tomatically. Will there be demand for math-ematical economists in 20 years?

WHAT IF LAboR beCoMes obsoLeTe?If demand for human labor really declines

for these fundamental reasons, we run into various problems. First of all, the biggest part of the economic output (about 60%) is dis-tributed to the people as wages. How will we distribute the fruits of the production process when work input and performance cannot be the criterion anymore?

Secondly, for most people labor has more functions than just being the source of income. What will ordinary people do when they are not needed in the production process any-more? Not everyone is an artist or a Bohemian who has plenty of rewarding options how to spend time. For many people, their work struc-tures their days, and their workplaces are of-ten hotspots of social interaction. Unemployed people tend to degenerate and to lose social connectivity.

As I see it, economics does not have an an-swer how to tackle such a situation. Let’s just hope that we can go on for another 200 years without labor demand running short!

THe IseT KHACHApuRI INDeX

The ISET Policy Institute (ISET-PI, www.iset-pi.ge) is an independent think-tank as-sociated with the International School of Economics at TSU (ISET). ISET-PI designed a simple and robust way of tracking inflation and the differences in the cost of living across Georgia’s major cities. Unlike traditional “consumer baskets” used for monitoring price inflation, our “basket” includes only those in-gredients that are needed to cook one Imere-tian khachapuri (cheese, butter, flour, yeast, eggs, and milk) and energy inputs (gas and electricity). We conduct a monthly survey of the major markets in Tbilisi, Kutaisi, Batumi and Telavi to measure the differences in the cost of living across Georgia and to track the monthly fluctuations in the prices of all rel-evant ingredients.

Author: Florian Biermann .

146

148

150

152

154

156

158

160

162

0

1

1

2

2

3

3

4

4

May

/11

Jun/

11

Jul/1

1

Aug/

11

Sep/

11

Oct

/11

Nov

/11

Dec/

11

Jan/

12

Feb/

12

Mar

/12

Apr/

12

May

/12

Jun/

12

Jul/1

2

Aug/

12

Sep/

12

Oct

/12

Nov

/12

Dec/

12

Jan/

13

CPI

Kh-In

dex

Khachapuri Index (Kh-Index) and Consumer Price Index (CPI)

Kh-Index

CPI

3HEADLINE NEWS & ANALYSISFINANCIALFINcHANNEL.com | 18 FEbruArY, 2013

C M Y K

Advertiser: VTB Bank. Contact FINANCIAL Ad Dep at [email protected]

publicity

4 HEADLINE NEWS & ANALYSIS FINANCIAL18 FEbruArY, 2013 | FINcHANNEL.com

C M Y K

financial news

NuMbeR oF TouRIsTs FRoM

NoRTHeRN NeIgHbouR

INCReAseD bY 72% sINCe vICToRY oF

IvANIsHvILIThe FINANCIAL

By MAdoNA GAsANovA

From September 2012 till February 2013 the number of Russian tourists in Geor-gia increased by 72% com-pared to the same period of

the year before. During the past five months Georgia has hosted 204,495 Russian visitors, of which almost half are friends and relatives of Georgian residents.

The number of Russian tourists in Georgia during the same period of 2011/2012 was 119,053.

“41% of Russian residents come to Georgia to visit friends and family,” Rusudan Mamatsashvili, Head of the Planning and Development Depart-ment at Georgian National Tourism Administration (GNTA), told The FI-NANCIAL. “Leisure and recreation is the main purpose of foreign nation-als when visiting Tbilisi. Thirty-two percent of Russians visited Georgia for leisure and recreation while 5% travelled for business,” Mamatsash-vili said.

To restore relations with Geor-gia’s northern neighbour was one of the main promises made by Bid-zina Ivanishvili, currently holding the seat of Prime Minister. Russia has taken steps to resume the import of Georgian-produced wine and mineral water, originally banned by Russia in 2006.

Some think Mr. Ivanishvili has

struggled to meet the expectations that swept him to power in October, ending the nine-year political domi-nance of President Mikheil Saakash-vili and his party. Many voters ex-pected his election to be followed by immediate financial relief and a turn-around in relations with Russia.

Leading Georgian hotels, Radisson Blu Iveria and Tbilisi Marriott Hotel have, however, seen an increase in guests of Russian origin.

“The number of Russian guests at our hotel has doubled since October 2012 in comparison with the previous year,” said Nina Asatiani, Director of Sales and Marketing at Radisson Blu Iveria. “The total number of Russian guests at the Hotel in 2012 was 5,857. During the whole year the Hotel host-ed the largest number of Russians in October, when their number reached 869,” said Asatiani.

Russians are the second largest group of foreign nationals among the guests of Radisson Blu Iveria. Ameri-can guests make up around 19%, tak-ing first place.

“The number of Russian guests increased by 12% from October 2012 compared with the same period of last year. The majority of our guests visit the country for business,” said Alex-ander Kvaratskhelia, Cluster Director of Sales and Marketing at Tbilisi Mar-riott Hotel.

The leading guest nationalities by numbers at Tbilisi Marriott Hotel are US, British, Russian, German, Ukrai-nian, Azerbaijani and Armenian. Tbilisi Marriott Hotel has 127 rooms, while Courtyard by Marriott has 118.

According to GNTA, more than half of Russian travellers - 52% - visited the homes of friends or relatives while in the country. Almost a quarter - 23%

- stayed in private accommodation. As for hotels and guest houses, 14% and 5% of Russian visitors respectively stayed there. It should be noted that in comparison with the nationals of other countries, Russian travellers rarely stay in paid accommodation while in Georgia.

According to research conducted by GNTA from May 2011 - April 2012, the average duration of stay of Rus-sian tourists in Georgia is 26 days. This figure is high compared to other countries. A significant share of visi-tors - 16% - visit Georgia for just a sin-gle day. About one fifth - 21% - remain in the country for more than a month. Russian residents spend on average GEL 790 during visits to Georgia.

Forty-two percent of Russian trav-ellers used air travel as the mode of transport to reach the country, out of which 12% used Georgian air com-

panies and 30% - foreign. About one fifth - 19% - travelled by car.

The majority of Russian residents - 54% - travelled to Georgia alone. Ap-proximately 34% visited the country with other family members. Just 10% arrived in Georgia with friends.

The number of Russians who had organized their trip themselves was 72%, 15% of trips were arranged by friends/relatives, and just 4% were organized by companies or people’s places of work.

Tbilisi with 67% and Batumi with 40% are the most popular destina-tions for Russians in Georgia. Other popular destinations within Georgia include Mtskheta - 9%, Kutaisi - 8% and Kobuleti - 6%.

The Russian websites www.kom-mersant.ru/money and finam.ru ran online surveys on their respective sites asking readers to vote on wheth-er they would like to visit Georgia. From 30 January to 7 February a total of 3,672 visitors voted on the kom-mersant website. 56.94% said that they would like to visit Georgia while 43.06% said that they would not.

The website www.finam.ru ran a survey with the same question. In total 1,554 of the webpage’s visitors voted. Out of them 31.21% confirmed that they would want to visit Georgia while the majority of voters - 68.79% - said ‘no’.

From October to December 2012, 62 Russian companies were regis-tered in Georgia. The number for the same period of the previous year was 48. Against the background of a signif-icantly increased number of registered Russian companies the total num-ber of new businesses in Georgia has dropped since the 1 October elections. The amount of registered companies from October till January 2012 was 10,001, while for the year before it was 14,071. This statistical data was pro-vided to The FINANCIAL by the Na-tional Agency of the Public Registry.

The total number of companies reg-istered in Georgia in 2012 was 43,934 while in 2011 it was 54,081.

New Flow of Russian Tourists to Georgia

Adv

ertis

er: R

adio

Com

mer

sant

. Con

tact

FIN

AN

CIA

L A

d D

ep a

t mar

ketin

g@fin

chan

nel.c

om

biznesis personaluri radio

[email protected]+995 32 2505 955

biznesis personaluri radio

[email protected]+995 32 2505 955

Money Transfers In January

In January 2013, the volume of money transfers from abroad con-stituted 94.1 million USD (156.1 million GEL), which is 9.7 million USD (16.2 million GEL), or 11.5

percent more than the same amount for January 2012.

93.2 percent of total money transfers from abroad fall on those 11 big donor countries, from which the volume of such transfers exceeded 1 million USD in January. In January 2012 the share of these 11 countries constituted 91.4 per-cent of the total volume of money trans-fers.

In January 2013, 9.5 million USD (or 15.7 million GEL) were transferred from Georgia instead of 6.9 million USD (or 11.5 million GEL) in January 2012.

In the reference month, the structure of remittances by electronic wire sys-tems is shown on the graph below.

volume of money transfers

in January, 2013 Million US Dollars

Structure of money transfers by the biggest donor countries %

January, 2012

January, 2013

Total 94.1 100.0 100.0

russia48.7 49.4 51.7

Greece12.7 13.5 13.5

Italy8.3 9.7 8.8

uSA5.1 6.6 5.4

ukraine3.8 3.8 4.1

Turkey2.2 2.0 2.3

Spain1.8 2.7 1.9

United Kingdom1.7 1.2 1.8

Israel1.3 1.1 1.3

Germany1.1 0.9 1.2

Azerbaijan1.1 0.6 1.1

Cooking to Become Compulsory Part of School Curriculum

The FINANCIAL

Cooking lessons will become a compulsory part of the school curriculum in UK, with chil-dren as young as eight learning how to cook nutritionally bal-

anced food.Those are the plans under the new draft

national curriculum, which would also see secondary school pupils learning a range of cooking techniques.

Although “food technology” is part of the design and technology syllabus at the mo-ment, it is not an independent part of the national curriculum.

“For the first time ever cookery will be a compulsory part of the curriculum from Key Stages 1 to 3”, A spokesman for the Department for Education said. “The new design and technology curriculum is about giving pupils the knowledge needed for their daily lives. Given the obesity is-sues that face our children today, it is vital that they know as much as possible about healthy eating and what constitutes a bal-anced diet.

“It’s also important that they can devel-op an interest and understanding of good food. By bringing this into the curriculum, we want to encourage children to develop a love of food and cooking that will stay with them as they grow up.”

photo by outdoorukraine.jpg

5HEADLINE NEWS & ANALYSISFINANCIALFINcHANNEL.com | 18 FEbruArY, 2013

C M Y K

Advertiser: Eristavi Law Group. Contact FINANCIAL Ad Dep at [email protected]

publicity

6 HEADLINE NEWS & ANALYSIS FINANCIAL18 FEbruArY, 2013 | FINcHANNEL.com

C M Y K

financial news

FrANk kLoBuCArGorBI

Georgians are generally untrusting of most of their national institutions, such as the me-dia, though not so much as some other ex-soviet countries. In this recent poll conducted by Georgian Opinion Research Business In-ternational, we asked respondents about their trust in a few broad categories of public insti-tutions in their respective countries, includ-ing newspapers, TV and radio, and the police. This trust was measured on a ten point scale, where one represents absolute distrust and ten means the respondents trusts the institu-tion “completely.” In the asking, we discovered that Georgians trust their media, both print and broadcast, less than every other surveyed country save for Russia and Ukraine.

On the other hand, the police enjoy a well-above-average level of faith from Georgians, most likely as a result of the massive overhaul under President Saakashvili and the resultant disappearance of low-level corruption. Only Azeris trust their police more, but then again, Azeris trust everyone more, being the most confident in all their institutions. The only ex-

ception is how trusting the Kazakhs are of their newspapers. Ukrainians were the least trust-ing of every institution, and gave their police a particularly low score (3.58).

Newspaper TV/ radio PoliceArmenia 5.64 5.93 5.73

Azerbaijan 5.90 6.87 7.20

Belarus 5.57 5.76 6.04

Georgia 4.93 5.32 6.75

Kazakhstan 6.1 6.55 5.86

Moldova 4.97 5.59 3.96

Russia 4.67 5.14 4.46

Ukraine 4.65 5.11 3.58

So if people don’t like their public institu-tions, why don’t they take democratic action to change them? Aside from the fact that even in the most democratically developed country in this survey still suffers from “one man show” syndrome and other major speed-bumps to democracy, it seems that the vast majority of citizens don’t feel that it’s even possible to af-

fect change on a national level. We asked re-spondents in each country to agree or disagree with the statement, “I can influence my na-tional government.” In total, only about 15% agreed in any sense, the rest affirming their lack of efficacy.

Russians had the least faith in their democ-racy, with 9% feeling they could influence their government, while Armenians had the most, at 21%. Georgians had essentially the same low efficaciousness as Russians, only 10% agreed with the statement. However, keep in mind that this poll was conducted prior to the most recent elections; Georgia is a constantly changing place, and several of these numbers may have already begun to change.

“I can influence my national government”

Agree DisagreeArmenia 21% 79%

Azerbaijan 18% 82%

Belarus 18% 82%

Georgia 10% 90%

Kazakhstan 19% 81%

Moldova 14% 86%

Russia 9% 91%

Ukraine 14% 86%

With a real and recognized democratic tran-sition of power, Georgians may have begun to think of themselves as members of a true democracy. With the release of thousands of prisoners, and the nearly inevitable jump in crime rates, Georgians may start doubting the police’s ability to keep them safe. So stay tuned - over the coming months GORBI will continue to conduct our regular polling, and we’ll begin to see just how these recent changes will affect Georgia’s public trust and efficacy. Visit our website at gorbi.com for more articles and ar-chives.

Institutional Trust and Efficacy

The FINANCIALBy MArIAM PAPIdze

Since the parliamentary elections, companies op-erating on the Georgian market have reduced their activities. The business

sector has become comparatively passive in recent times, a fact that is confirmed by the latest statistics. An almost 20 percent decrease was observed in registering business in 2012 compared to 2011 according to the Public Registry Service. Experts say that the reason for the decrease in registering business is due to the unstable political situation.

Besides the elections and rela-tively unstable political situation, another reason for companies’ rela-tive inactivity is that the current gov-ernment intends to revise all of the projects that were started under the previous government, experts say.

“Declines in foreign investments, export and import have been statisti-cally confirmed, and are supposedly the result of a cautious attitude in re-sponse to the recent political chang-es,” said Paata Sheshelidze, economic expert and President at New Eco-nomic School - Georgia. “It seems to be largely a decline of the activities of those companies who were involved in various projects of the previous government. Governmental interfer-ence in business is changing due to the new government - a number of fields are now financially dependent on government funds or budgets. The way out is economic liberty, tax cuts and reduction of state costs. It is important that the Georgian Lari is guaranteed by gold, which will elimi-nate inflation,” he added.

“The United National Movement government’s narrative was that Georgia was modern and forward-thinking, cheaper to operate in than Europe and less corrupt than Bul-garia/Romania,” a US businessman in Georgia, who wants to remain anonymous, told The FINANCIAL. This person is currently holding ne-gotiations on multimillion projects with the Government.

“The winning party declared that

Georgia was a corrupt police state and that businesses here were liv-ing in fear. During the lead-up to the elections, foreign financiers and investors stopped providing funds for Georgian commercial activity. The winning party informed foreign press that the UNM was raising pri-vate armies for a civil war in Same-grelo, and that turned a lot of inves-tors off. After the elections, business has been stagnant in some sectors. Anything related to large scale in-frastructure or construction is at a complete standstill,” he said.

“Investment activities dependent on foreign investment have mostly halted, apart from those businesses backed by Russian investors. In our case, investors who had signed our term sheets for substantial labour-intensive investment projects have backed out of investment deals, cit-ing unacceptably high sovereign risk and political uncertainty. These

investors are from the Netherlands, China and Japan. In the case of our operations, USD 20 million worth of investment for 2013 has been can-celled, which would have employed over 300 people in development and 150 people permanently,” he added.

“Service companies that provide support to large infrastructure and construction projects are hit very hard, as many hydro projects have been suspended by the new govern-ment. One friend who owns such a company has had to sack half his staff this week; his firm is well estab-lished and has been operating suc-cessfully for a decade. Another friend in the same situation is considering closing his business, dismissing his twenty local staff and relocating to the EU. A third friend in the same sector sees no further potential for growth in his Georgian business and is investing in Kazakhstan to secure the future of his company,” he said.

“Another problem is that binding contracts signed with the previous government are not being honoured by the new government; the phrase “review of previous contracts” is used to delay payment for an unac-ceptable period, causing distress to companies owed large sums of mon-ey. Bad debts left by the previous government are not being settled by the new government either, despite promises to do so,” he said.

“There is a macro-economic risk that the government honouring its huge public spending promises will drain the budget, and additional taxes will be levied on business to pay for it, which will be very nega-tive. The old concept of needing an intermediary to meet with ministers seems to be making a comeback, which in such a small country is unnecessary. It damages efficiency and is a recipe for corruption. If the Government can tackle high-level

corruption, collusion and nepotism as promised, while maintaining a light regulatory touch, and a low-tax environment, then strong capital in-flows into the private sector should restart,” he said.

Fifteen out of twenty companies asked to comment about the dynam-ics of business activities since the parliamentary election, preferred to keep silent.

“We would prefer that any com-ments that we make focus purely on our project and/or the retail market. Therefore we prefer not to comment on this issue,” said Tim Wilkinson, Managing Partner at Redstone Asset Management.

“I do not have reliable informa-tion about declining companies’ activities in Georgia,” said Mamuka Shurgaia, CFO at SRG Investments LLC. “Accordingly, I cannot give you any examples regarding this is-sue and cannot confirm whether this information is correct or not. At our company such a thing has not hap-pened,” he added.

“At Magticom we are seeing an increase in activity since the elec-tions,” said David Lee, the President of Magticom and Chairman of the Eurasia Partnership Foundation. “I think that the political challenges will result in caution with regard to new long-term investments until the poli-cies of the new government become clearer and co-habitation becomes less fraught. However the recent progress in the Deep and Compre-hensive Free Trade Agreement, the improving trade relations with Rus-sia and the new agricultural develop-ment plans are big ticket items that should quickly improve confidence in many sectors,” he added.

“We are making huge gains in our Satellite TV business and de-mand for internet continues to grow strongly, particularly in the regions. As the agricultural investments this year “take root” there should be real growth in the regions. I see more up-side than downside right now, prob-lems are being addressed. Business-es need to plan and feel confident of the future and the new government is doing a lot to make this happen,” Lee added.

Business Activities in Decline since Parliamentary Elections

7HEADLINE NEWS & ANALYSISFINANCIALFINcHANNEL.com | 18 FEbruArY, 2013

C M Y K

publicity

Advertiser: Archi Group. Contact FINANCIAL Ad Dep at [email protected]

8 HEADLINE NEWS & ANALYSIS FINANCIAL18 FEbruArY, 2013 | FINcHANNEL.com

C M Y K

financial news

The FINANCIALBy MArIAM PAPIdze

The European Business Awards is a European awards programme started in 2006. Since then the European Busi-

ness Awards has established itself as the ultimate platform for outstand-ing businesses in the EU. Designed to celebrate exceptional results across a variety of categories, the EBAs are a global showcase for the best in the business.

The main principles behind the Awards are Innovation, Finan-cial Success, Business Ethics and having an International Mindset. These principles enable compa-nies of all sizes and industries to be judged on an equal standing and highlight the characteristics of long term successful businesses.

The Awards are judged by more than 200 very senior people who are drawn from business, aca-demia, government and the media. The panel includes CEOs, entrepre-neurs, management consultants, editors, ministers and prime min-isters, past and present. From Yves Leterme (ex-prime minister of Bel-gium) and José Maria Anzar (ex-prime minister of Spain) through to Fleming Lindelov (ex-CEO Carls-berg) and Luc Bardin (Group Vice President of BP).

Since 2010 the European Busi-ness Awards has been supported by The FINANCIAL. Zviad Poch-khua, Editor-in-Chief, is one of the judges.

“In my early 20s I founded and built up a publishing and me-dia business that I sold in 2007,” Adrian Tripp, CEO, EBA. “After the sale of my previous business I wanted to found a social enterprise that would work towards creating a stronger and more successful busi-ness community in Europe, a busi-ness community that could support our social and healthcare systems and provide prosperity for the citi-zens of Europe for generations to come.”

“We live in an increasingly glo-balised world, which provides great opportunity but also brings much greater competition. I believe it is important that we recognize inno-vative, ethical, financially success-ful businesses that have a strong in-ternational mindset. Those are the types of businesses that we will be able to build successful economies around.”

“By showcasing and bringing at-tention to the very best businesses

we help them to succeed and pros-per by providing excellent visibility and endorsement. They in turn will create more jobs and pay more tax-es which is good for society.”

“We also look at what makes those businesses successful and share those learnings with the rest of the business community. And

lastly we use the Awards and the companies featured to stimulate the debate within society around what the future shape, form and substance of the economies of Eu-rope should be. As the competition has grown so significantly over the last few years, we are more and more able to achieve the goals and objectives outlined above.”

Q. What do businesses gain from the Awards? What are the biggest benefits for com-panies participating in the Awards ceremony?

A. With over 15,000 companies engaged in the programme across 30 countries every year, 5 stages of judging and more than 200 judges, with participating companies hav-ing a combined turnover of more than EUR 1 trillion, this makes the European Business Awards very highly regarded and gives it excel-lent levels of visibility.

There are many benefits of enter-ing; the entry process is a very pow-

erful and robust way of reviewing exactly what has made the entrants successful. It also enables them to benchmark their performance against the most successful busi-nesses in Europe.

It also shows to staff, investors and clients that the leaders of the business are proud of what they as a business have achieved.

If companies get through and become award winners the acco-lade has very powerful business benefits, many of our previous win-ners have: generated new business and partnerships; have secured new investment to help them grow; some have undertaken mergers and acquisitions on the back of their achievements. They all benefit from significant international exposure and visibility.

Q. What should Georgian companies do to take part in this competition and in gen-eral to increase their competi-tiveness globally?

A. It is a great way for Georgian companies to create better visibil-ity on a European and global stage. The Awards are also a very effective platform for Georgian companies to build relationships with other very successful businesses throughout Europe. Every year we see many partnerships and much business done between European Business Awards finalist companies.

Q. What are the typical characteristics of Georgian companies that make them different from European ones?

A. Well-run businesses all over the world have similar character-istics, they have strong and driven management teams, they are con-stantly innovating to improve their competitive position in the market and are very sensitive to the needs of their clients. The best Georgian companies have the same charac-teristics.

Q. In your opinion how is the business environment im-proving in Europe and what are the main challenges still?

A. A more stable outlook for the Euro and Greece has taken away some of the uncertainty business leaders were facing when making important investment and expan-sion decisions, which is good. On the other hand, the macroeconomic conditions prevalent throughout Europe are still very challenging. We have seen this year across all of the entrants in the Awards signifi-cant pressure on margins. This in turn has an impact on investment and medium-term growth.

Q. Which are the most dy-namic companies and sectors in Europe so far? Why?

A. In every industry, both new and old, highly competitive to emerging, there are great compa-nies doing amazing work. From H&M (Sweden) to Pirelli (Italy), Sener (Spain) to Mercator (Slove-nia) they have all found a way to unlock value and are prospering.

The digital space in all its forms shows high levels of innovation and activity as does the biotech and renewable energy industries. Although all would do significantly better if there was a better-func-tioning investment environment.

More Than 15,000 Companies Participating in European Business Awards

“Companies like Goodwill, GM Pharmaceuticals, M Group and MediClubGeorgia have been very successful in making it as finalists of the Awards. As yet we have not had a European Business Awards Category Winner,” Adrian Tripp, CEO of the European Business Awards

“Six years ago we started with just 200 companies engaging in the Awards, this year there will be more than 15,000”

MoRe THAN oNe IN FouR RespoNDeNTs

RepoRT THeIR oRgANIzATIoNs WeRe THe vICTIMs oF AT LeAsT oNe

CYbeRATTACKThe FINANCIAL

More than one in four (28 percent) of re-spondents surveyed report their organiza-tions were the victims

of at least one cyberattack in the past year; nine percent report multiple breaches and an alarming 17 percent were not confident that their organi-zations could even detect an attack, according to a Deloitte Tech Trends poll of 1,749 business professionals.

“It’s no longer a discussion about if an organization will get hacked, but only a matter of when, and how quick-ly and effectively it will respond,” said Mark White, principal and chief technology officer, Deloitte Consult-ing LLP. “Organizations across many industries need to change the lens through which they view cyber risk – not only relying on traditional secu-rity controls to reveal tell-tale signs of an effective attack – but by consider-ing transforming the way they defend, detect and even manage security by leveraging cyber intelligence and ad-vanced techniques to help identify the coming threat and proactively re-spond.”

Additional findings from the poll include:

Response times to identify and ad-dress breaches vary, with plenty of room for improvement. Almost half (48 percent) of respondents polled said their organizations identified and triaged threats within hours, while approximately one in five (21 percent) reported their organizations did so within a week, and nearly one in 10 (9 percent) said it took more than a week.

People, process and technology are ALL critical to cyber threat programs.

Respondents said the following concerned their organizations the most regarding their cyber threat pro-grams:

infrastructure and technology (28 percent);

right talent/right skills (26 per-cent);

effective operational processes (24 percent) and adequate resourcing/funding (22 percent).

Consumer/personal information is highly valued by cyber criminals and organizations invest heavily trying to protect it.

Respondents put a high price tag on consumer/personal information, with approximately half (49 percent) reporting that this type of data would be of most value to cyber-criminals, followed by intellectual property (27 percent); corporate strategy informa-tion (13 percent) and financial perfor-mance information (11 percent).

Consistent with this data, more than half (55 percent) of respondents said their organizations most heavily invested in protecting consumer/per-sonal information, followed by intel-lectual property (23 percent).

“Cyber security may sound techni-cal in nature, but at its core it is a busi-ness issue. Any company’s competi-tive position and financial health may be at stake. Business and technology leaders need to engage in effective dialog about what the business val-ues most, how the company can drive a competitive advantage and which information and other digital assets are the most sensitive. Brand, cus-tomer trust and strategic positioning may be at risk,” said Kieran Norton, principal, Deloitte & Touche LLP and leader of Deloitte’s U.S. cyber threat management practice. “There may be no such thing as hacker-proof, but there’s a chance to reduce your cyber beacon, be less inviting to attack and proactively establish outward- and inward-facing measures around your most valued assets.”

You’ve Been Hacked, Now What?

9HEADLINE NEWS & ANALYSISFINANCIALFINcHANNEL.com | 18 FEbruArY, 2013

C M Y K

publicity

Advertiser: CIS Bankers. Contact FINANCIAL Ad Dep at [email protected]

Speakers and Master ClassesMovenbank, USA

ABN AMRO Bank, NetherlandsUniCredit Bank, Italy

ICC Banking Commission, FranceBank of Georgia, Georgia

TBC Bank, GeorgiaLiberty Bank, Georgia

Bank Standard, AzerbaijanAG Bank, AzerbaijanUnibank, AzerbaijanVTB Bank, Russia

Promsvyazbank, RussiaEskhata Bank, Tajikistan

ING Bank, Ukraine

Armenia • Azerbaijan • Belarus • Georgia • Kazakhstan • Kyrgyzstan • Moldova • Russia • Tajikistan • Turkmenistan • Ukraine • Uzbekistan

International Banking Conference & Exhibition3-7 June, Radisson Blu Iveria Hotel, Tbilisi, Georgia

Brett KingKeynote & Master Class

Bank 3.0Brett King is a three times best-selling author, public speaker and founder of the new retail banking and lifestyle concept, Moven. In BANK 3.0, Brett King looks at the latest trends that are redefining financial services and payments.

Caucasus & CIS: Local and Regional Opportunities

Risk & Compliance: Banking rules and regulations road map to 2020

Retail Banking: Reducing the cost of servicing your clients

Human Capital: Improving Staff Performance

Banking Technology: Innovations & Trends

Social Media: Opportunities & Risks

Past Sponsors & Partners Gold Sponsor General Media Partner

Media Partners

Contact us for sponsorship information and speaking opportunities: [email protected]

Advertisement.indd 1 11/02/2013 00:32

10 HEADLINE NEWS & ANALYSIS FINANCIAL18 FEbruArY, 2013 | FINcHANNEL.com

C M Y K

financial news

“INTeResT RATes oN LoANs AND DeposITs

WILL DRop DoWN bY 1-1.5 peRCeNT IN 2013”, CHIeF ReTAIL bANKINg oFFICeR

sAYs

The FINANCIALBy NANA MGheBrIshvILI

Interest rates on loans and de-posits will drop down by 1-1.5 percent in 2013, Valerian Gabu-nia, Chief Retail Banking Of-ficer at VTB Georgia told The

FINANCIAL. “This is a very important change for the banks but sometimes such changes seem trivial to custom-ers”, he believes.

VTB Georgia which was listed among the best banks in Georgia in terms of service quality in 2012, is go-ing to broaden its small network. The bank is going to be maximally involved in agri-projects which are already sup-ported by new Georgian Government.

“We are acting very aggressively in all markets. As a result we hold first place in growth out of VTB’s global group, (apart from Stat-up projects in newly entered countries)” said Va-lerian Gabunia, Chief Retail Banking Officer at VTB Georgia. “Our bank as well as the market is small compared to others. We can’t compete with them by size, but by quality and growth rates we do.”

“This problem is especially appar-ent in the regions. We currently have 22 branches in the whole country, a number which is not corresponding to our growth rate. We are going to add minimum 6 new branches in Georgia in 2013. VTB is annually investing in the growth of its chain,” he noted.

VTB Georgia experienced 51 per-cent growth in retail in 2012 while the whole market grew by 16 percent dur-ing the same period. In total the Bank issued up to GEL 250 million worth of loans in the retail & SME sector. At the same time the deposits form individual customers grew by 45 percent, which is almost twice more than the total mar-ket as it experienced growth of just 23

percent. The SME credit market in-creased by approximately 11 percent in 2012 and VTB’s corporate credit port-folio - by 26 percent.

“2012 was definitely successful but we will not be able to maintain a similar percentage of growth in 2013. Still we will grow twice more than the market. Generally speaking, the bigger the business is the smaller the growth. Brand awareness of VTB bank grew significantly last year and this will cer-tainly have positive impact on 2013 re-sults of VTB Bank.

Q. VTB Bank has changed its main focus and is now focusing more on the retail than corpo-rate segment. Was it this that caused the large growth of the Bank?

A. VTB Georgia has been oriented on corporate business for a long time. We always had a retail segment, but it made up only 30 percent of total activi-ties. About two years ago we changed our focus and made the Bank more universal. We then later turned more to the retail segment. Still we are main-taining strong positions in the corpo-rate sphere, but this segment is some-how limited in Georgia. At present the retail segment makes up 55 percent and we are trying to increase it up to 60 by the end of 2013.

Q. You entered the Pos.Credit market at the end of 2012. What are the prospects of this sector for VTB?

A. We are very active in this market as the potential seems great. There are several large, established banks that have been operating in this direc-tion for several years, but we are suc-cessfully competing with them. We have an innovative attitude toward this. Our officers are dressed less for-mally. They are working with tablets and don’t have desks in the branches. This makes their activity faster and more convenient and approachable for customers. The process of filling out a leasing application is simplified as well.

VTB has no analogue in terms of fast products like Pos. Credits and auto loans. We are the quickest and the most flexible so we strongly believe that clients appreciate that.

Q. What are the other innova-tive products that you offer?

A. We offered a unique credit card several weeks ago. This segment is es-

sential for us as well. All banks are very active in this direction but we offer the best terms. The tariffs are lower com-pared to others and the interest rate is the lowest. We offer a credit card for just 30 percent of annual interest rate. The rate at other banks starts from 36 percent. Our calculations are very posi-tive and we are more than managing to compete with the other big players.

We also plan to become more ac-tive in the consumer loans segment as this is the most popular product in the Georgian banking market.

Q. VTB focuses on SMEs as well. How do you attract busi-nesses? What tools do you use that help in gaining success?

A. We recently ran the campaign - ‘Minus 3’. We offered businesses the opportunity to switch their loans to VTB for a minus 3 interest rate and better terms. The product was found to be in great demand as we gained about 200 new SME clients who all trans-ferred from other banks.

Q. Whom do you consider to be your main competitors in the market? Microfinance organiza-tions focus on small and medium loans as well. Does this influence your business?

A. We don’t feel any competition with microfinance organizations. They have higher interest rates than any bank and ask for bigger collateral. Still the segment is developing successfully. Microfinance organizations help busi-nesses to start up, which then later could become the clients of us banks. In my opinion, this is quite a good practice.

As for the banks, Bank of Georgia and TBC Bank are our main competi-tors in terms of retail and corporate clients. ProCredit Bank is our main ri-val and donor for crediting SMEs. We, along with the other banks, are trying to win over their clients as it is the leading bank in this direction.

Q. Have the government changes influenced your busi-ness in any way?

A. They have not influenced VTB Bank at all. The retail sector continued its usual activities, both in the run-up to, and since, the election period. The SME segment tended to be a little bit passive during this period but they have since become very active in a short period of time. Even January was a very active period.

VTB Georgia Experienced Biggest Growth in VTB Group

Valerian Gabunia

The FINANCIAL

U.S. consumers de-rive more value from media online—net of the associated costs—than they receive

from offline media, according to new research by The Boston Con-sulting Group.

BCG calculates that the aver-age U.S. connected consumer, or online user, receives a “consumer surplus” from online media of ap-proximately $970 per year—or about 2.5 percent of the average U.S. annual income—compared with approximately $900 for of-fline media. Consumer surplus is defined as the value consumers themselves place on a media-re-lated activity or product over and above what they pay for it.

The BCG study—detailed in the report Follow the Surplus: How U.S. Consumers Value Online Media—examined the surplus consumers derive from each of seven categories—books, radio and music, U.S. newspapers and magazines, TV and movies, video games, international newspapers and magazines, and user-generat-ed content (UGC) and social net-works.

The highest consumer surplus ($311), accounting for about one-third of the online total, comes from UGC and social networks accessed through such platforms as Facebook and YouTube. Books fall at the opposite end of the spec-trum: they generate the greatest offline surplus, even taking into account fast-selling e-books.

“The fact that the consumer surplus is already higher for on-line media is somewhat extraor-dinary, given that online revenues represent less than 15 percent of the total media industry pie,” said John Rose, a BCG senior partner and coauthor of the report. “This surplus will only continue to grow, driven by consumers’ appreciation for an expanding array of high-quality content and the prolifera-tion of devices.”

The BCG study found that de-vice ownership is increasing, with proliferation driven first by the desire for mobile access, then by fragmentation of use—that is, con-sumers using different devices for different purposes in different sit-uations throughout the day.

The average consumer today

owns 2.9 devices—almost double the figure from three years ago—and expects to own 4.1 devices in three years’ time. The number of hours spent consuming online media jumps 50 percent when people start using a second con-nected device, which is often their first mobile device. It rises again for consumers owning five or more devices, by as much as 25 percent. Owners of multiple devices report big increases in value from online media consumption.

“Shrewd media companies that build effective digital capabilities will enjoy opportunities to extract some of this growing consumer surplus for themselves,” said Neal Zuckerman, a BCG partner and coauthor of the report. “They will need to develop products that work across the growing range of devices and capitalize on both new and existing models of com-mercialization, including adver-tising, new products and services, an increasing ability to charge for online content, and the still-evolv-ing ecosystem for monetizing the massive volumes of consumer data that the Internet serves up.”

Study also showed: More than two-thirds (68 percent) of con-sumers say they have more access to higher-quality online content today than three years ago.

Nearly two-thirds (62 percent) cite the unique nature of such con-tent as a major reason to go online.

The same percentage believes that the Internet promotes U.S. culture abroad.

More than three-quarters (77 percent) feel that it is their own responsibility to filter for accurate online content, and they believe they have the capability to do so effectively.

By a margin of some five to one, U.S. consumers are more excited about the Internet’s potential re-wards than they are worried about the potential risks.

The patterns of media consump-tion in the U.S. are remarkably consistent—especially for online media—across age, gender, and region. But what people are do-ing while they are online can vary. For example, men and women consume the same amount of on-line media—12 hours a week (men consume slightly more offline me-dia)—but men listen to significant-ly more music online while women enjoy more online interaction through UGC and games.

U.S. Consumers Get More Value from Online Media than Offline, BCG Study Finds

11HEADLINE NEWS & ANALYSISFINANCIALFINcHANNEL.com | 18 FEbruArY, 2013

C M Y K

publicity

Advertiser: DRC. Contact FINANCIAL Ad Dep at [email protected]

12 HEADLINE NEWS & ANALYSIS FINANCIAL18 FEbruArY, 2013 | FINcHANNEL.com

C M Y K

financial news

The FINANCIALBy NANA MGheBrIshvILI

Retail development re-mains one of the top sectors to finance for Bank of Georgia. Two new residential build-

ings at 19 Ingorokva Street and 5 Ingorokva Street, two of the best recently-finished residential houses in Tbilisi, built with Bank of Georgia loan, are ready to receive the dwell-ers.

“This is an example of a success-ful project financed with our loan,” said Archil Gachechiladze, Deputy CEO at Bank of Georgia. “We issued a loan of up to USD 10 million for the two housing projects. Overall Bank of Georgia financed the construction sector with more than USD 20 mil-lion in 2012.”

“In total we financed 6 projects in this sector last year. As of today, the number of the projects financed by Bank of Georgia loan that are close to being finished, or are in the ac-tive phase of construction, is close to 15. Bank of Georgia is continuing to finance all adequately-planned construction projects in 2013, as it is one of our priorities,” he added.

The residential building in 19 In-gorokva Street, known as ‘House near the Parliament’, has total space of 35,000 square metres. The prices of the flats vary from USD 1,500 to USD 1,800 per square metre. Flats are available from 100 square me-tres to 500. The building contains 91

flats, 84 garages, 11 shopping and 32 office spaces. The building will soon have a café, fitness centre, children’s entertainment room and other fa-cilities. The design of the residential house is outstanding as well.

“60 percent of the flats are already sold,” said Bezhan Tsakadze, one of the founders of Georgian Develop-ment Group (GDG). “Our coopera-tion with Bank of Georgia is bilateral and some of our clients have mort-gage loans at the Bank. Generally speaking, we couldn’t have finished the building without the support of Bank of Georgia. Working with the Bank has been very fruitful and con-venient as well as easy for us.”

The other residential building, in 5 Ingorokva Street, counts 27 flats and one commercial space.

These two residential houses are not the only projects of GDG that are supported by Bank of Georgia. A building in Bagebi will be finished in May 2013 and another house on Nutsubidze Street will be completed in a month and a half. According to Tsakadze, the company plans to build an ultra-modern house near Vake Park, and they will be cooper-ating with Bank of Georgia on this project as well.

While banks have been heavily blamed for not financing the devel-opment sector sufficiently, Bank of

Georgia has been intensively issu-ing loans for the building of new residential houses. The Bank has financially supported projects by such companies as Arsi (in Ortacha-la and Avlabari), Kalasi, Tiflis De-velopment, Kera+, Saba+, D+ and others. Bank of Georgia is also par-ticipating in the projects of Tbilisi Hall known as The Rehabilitation of Old Tbilisi.

“Unlike the pre-crisis period, after the crisis we initiated and created a special engineering monitoring group, which observes the spending of the financing during the construc-tion process. This helps the projects to be finished on time,” Gachechi-ladze explained. “Thanks of this, we know precise information about when the building will be finished and the issuing of mortgage loans becomes easier for the Bank as well. Demand for mortgage loans has been gradually growing since 2009. We suppose that it will grow further, concurrently with the economic growth in the country.”

“As for the criteria for financing the developers, there are several factors. First, is that the companies should have a downpayment. It is required that the company owns the land it wants to build on. The com-pany’s capital and experience are essential for cooperation as well. Unfortunately, the number of such businesses in Georgia is not big,” he added.

Bank of Georgia continues to fi-nance developers and construction business in 2013.

Bank of Georgia Continues to Finance Construction Business

The FINANCIAL

Love is in the air and with Valentine’s Day just past, coupled-up men wanting to pop the question on the most romantic day of the

year may be inclined to think that the more expensive the ring, the more appreciative their fiancée will be.

Research from London Business School, however, shows that a shows that a woman’s appreciation of her ring is not strongly based on cost.

A study co-authored by Dr Gabri-

elle Adams, Assistant Professor of Organisational Behaviour at London Business School, discovered that men believe the more they spend on an engagement ring, the more ap-preciative the receiver will be. How-ever, in reality women are not more appreciative if the cost is more, ac-cording to the outcomes of the study.

Dr Adams said: “Our study sug-gests that men may not need to spend as much as they think they do on an engagement ring. Women’s appreciation levels were less strong-ly correlated with the estimated price of the ring.”

The study asked recently engaged Americans from a popular weddings website to complete a survey, assuring participants that their answers would not be shared with their fiancée. In the study, ring-givers predicted high-er feelings of appreciation from price than the receivers, who reported no difference in appreciation for an ex-pensive ring than an inexpensive ring.

With research suggesting that men can often spend the equivalent of three month’s salary on an engage-ment ring, the study offers some timely comfort to those shopping on more of a budget this Valentine’s Day.

‘Thanks for the diamond ring, but you shouldn’t have spent so much!’

The FINANCIAL

The world economy is showing signs of bright-ening after six months of stagnation, according to a global survey of eco-

nomic experts by the International Chamber of Commerce (ICC) and the Munich-based Ifo institute for economic research.

The latest ICC-Ifo World Econom-ic Survey (WES) shows a climate indicator of 94.1 for the first quarter of 2013, up from 82.4 at the end of 2012 after two quarters of decline. The new global rise was driven by a significant increase in experts’ op-timism for the six-month economic outlook. Meanwhile, assessments of the current economic situation im-proved only slightly.

ICC Secretary General Jean-Guy Carrier was encouraged by the sur-vey results, but remained cautious. “While the signs of a renewed eco-nomic optimism are a boost to con-fidence, fresh approaches by govern-ment and business are still urgently needed to drive economic growth,” he said.

Ifo said positive business data from China and the US, after the first fiscal cliff had been averted, had helped lift the gloom. Another comfort was European Central Bank President Mario Draghi’s pledge last year to do “whatever it takes” to pro-tect the eurozone from collapse.

Asia brightens -- The sharpest im-provement in economic climate was seen in Asia, where the ICC-Ifo eco-nomic climate indicator rose above its long-term average. Since the end of 2012, experts have become more upbeat about Asia’s economic situ-ation and expectations have surged.

The economic indicator for North America rose too, mainly due to the view that the current economic situ-ation had improved, although it was still “not completely satisfactory”.

Euro zone’s glimmer of hope -- Hans-Werner Sinn, President of the Ifo institute, said: “Assessments of the euro zone’s six-month economic outlook are now at their most posi-tive for nearly two years which sig-

nals a glimmer of hope for the euro area’s economic situation.”

Overall, the survey showed the economic climate in Western euro areas to be poor but improving. This is mainly because of significantly brighter six-month expectations – in all euro countries apart from Esto-nia.

Survey respondents described the economies of Greece, Italy, Portugal, Spain and Cyprus as “ailing”, only slightly behind their euro neigh-bours. Only Germany and Estonia received positive assessments.

Inflation -- The World Economic Survey’s 1,169 economic experts in 124 countries were also quizzed on inflation. This gave a global aver-age inflation estimate of 3.3% for 2013, down from 3.6% last year. Estimates for the euro area fell to 2.1% for 2013, from 2.4% last year. Short-term interest rates, set by cen-tral banks, are expected to remain largely unchanged over the next six months. And long-term interest rates, those affected mainly by the capital market, look set to rise only slightly.

WES participants expect the value of the US dollar to grow moderately over the next six months and the euro/US dollar exchange rate to re-main stable.

Spotlight on SMEs -- An ICC spe-cial question included in the survey revealed a broad worldwide consen-sus on the economic importance of small- and medium-sized enterpris-es (SMEs). Support was particularly strong in Europe where, according to the European Commission, SMEs provide two thirds of private sec-tor jobs and account for 99% of all European business. Nearly all WES experts surveyed in Western Europe see a substantial and healthy SME sector as “essential for the national economy”.

Survey analysts pointed out that the short supply of bank credit, mainly in Europe, was a heavy con-straint not just for SMEs, but for entire economies, particularly Italy, the UK, Hungary, Albania, Slovenia, Portugal, Ireland, Romania, Spain and Greece.

World Economic Climate Improves, Survey Shows

13HEADLINE NEWS & ANALYSISFINANCIALFINcHANNEL.com | 18 FEbruArY, 2013

C M Y K

publicity

Advertiser: SilkNet. Contact FINANCIAL Ad Dep at [email protected]

14 HEADLINE NEWS & ANALYSIS FINANCIAL18 FEbruArY, 2013 | FINcHANNEL.com

C M Y K

The FINANCIAL

According to the new version of Labor Code discrimination (gen-der, racial, ethnic, re-ligious, etc.) made by

the employer shall be prohibited not only during the labor relations (while the employee works), but also during the pre-contractual relations. In such a case, if a person makes a complaint, the burden of proof shall be placed on the employer.

The current version shows that discrimination made by the employ-er is only prohibited during engaged labor relations.

Proposed changes were analyzed recently by Transparency Interna-tional.

Another change is that the em-ployer becomes obliged to provide the job candidate with full infor-mation about the work to be per-formed; the form and term of the labor contract; the working condi-tions; the legal position of the future employee during the labor relations; and the remuneration. Currently the employer is not obliged to provide the candidate with the said informa-tion; the candidate has the right to obtain the information on his/her initiative.

The labor contract shall be con-cluded for a definite or indefinite term. It shall be concluded for a definite term only in cases when it is related to: fulfilling a concrete job; seasonal work; temporary increase in the amount of work; replacing an employee during his/her temporary absence; other objective circum-stances.

It is changing the duration of working time according which the working time determined by the em-ployer during which the employee performs the obligations imposed by the contract shall not exceed 41 hours per week. The working time does not include a break and rest time. The working time for minors aged between 16 to 18 and persons employed to perform hard, harm-ful, or dangerous work has also been limited, and it shall not exceed 36 hours per week. Also, the working time of minors aged between 14 to 16 shall not exceed 24 hours per week.

As for the overtime work it should be remunerated if it exceeds 48 hours per week. Overtime work shall be remunerated with a rate that ex-ceeds the average hourly rate by at least 25%.

The employee shall be entitled to a paid leave of at least 24 working days per year, according to the new changes while the old one says al-most the same.

Disability is considered as tempo-rary if its duration does not exceed 60 calendar days on succession or if the entire duration over six months does not exceed 90 calendar days. It should be noted that determining the terms of temporary disability is very important for the protection of the employee’s labor rights, since the employer does not have the right to

dismiss him/her during this period. According to the current code, tem-porary disability shall not exceed 30 calendar days on succession or the entire duration over six months shall not exceed 50 calendar days.

The main change in termination of a contract is that the concept of “annulment of contract” (which implied termination of contract on the initiative of one of the parties) has completely disappeared, and it no longer constitutes grounds for terminating a contract. Therefore, the employer is no longer entitled to dismiss an employee without in-dicating the grounds (it should be noted that an employee may leave the job without naming a cause), and these grounds must be envisaged in this code.

One of the most important novel-ties of the draft code is included in Part 4 of Article 38. According to this norm, the employer is obliged to substantiate the grounds for ter-minating the contract in writing within seven calendar days of the employee’s demand. The employee has the right to appeal the substanti-ated decision in court within a term of 30 days, and, if the employer fails to substantiate the decision on dis-missal in writing within seven days, the employee is entitled to appeal this decision of the employer within 30 days, in which case the burden of proof on factual circumstances is placed on the employer.

With a labor contract, the employ-er may obligate the employee not to use the knowledge and qualifica-tions acquired while performing the terms of the contract for the benefit of another, competitor employer. This restriction may not apply after the labor relations are terminated. According to the current code, the restriction is in force not only during labor relations, but also after their termination, but no longer than for three years.

In case of labor dispute the draft code differentiates between exami-nation of disputes that arise in in-dividual labor relations and of those arising in collective labor relations.

The mediator shall examine the dispute in accordance with “The rule of examining and settling of disputes that arise during collective labor re-lations” approved by the Minister. The Minister has the right to make a decision to stop conciliatory proce-dures at any stage. Participation in the procedures is obligatory for the parties. The parties may also agree to transfer the dispute to an arbitra-tion court at any stage.

According to the draft changes, the right to stage a strike or a lock-out at the time of collective labor re-lations only arises when conciliatory procedures end without a result; it is only after this that it becomes permitted to resort to such radical measures as a strike or a lockout. It is possible to conduct conciliatory procedures both though direct ne-gotiations of the parties and through a mediator appointed by the Minis-try. The participation of a mediator depends of the will of the parties or on the Minister’s initiative to get in-volved in a dispute. Accordingly, the conciliatory procedures can be con-ducted both with and without the in-volvement of a mediator appointed by the Ministry.

However, the changes envisaged in the draft code relate the origin of the right to stage a strike or a lock-out closely to a mediator appointed by the Ministry (it is permitted to ex-ercise the right to stage a strike only after 21 days from the day a party sends the Minister a request to ap-point a mediator or 21 days after the day the Minister appoints a media-tor on his/her own initiative) and it is only permitted to stage a strike if the conciliatory procedures involved a mediator of the Ministry.

New LabourCode Terminates“Annulment of Contract”

financial news

The FINANCIAL

An EBRD long-term loan of EUR 150 million will back the investments of Gestamp Automocion SA, one of the world’s

leading manufacturers of auto parts. It is aimed at upgrading its Rus-sian, Polish, Hungarian and Turkish plants which supply assembly lines set up by major international car manufacturers in these four mar-kets.

Gestamp, a Spanish-registered and family-controlled group, plans to invest EUR 255 million in capital expenditure up to 2016. This will en-able the company to move closer to its key customers in these countries, a key goal to increasing its competi-tiveness and part of a strategy to foster long-term relationships with such major clients on a global scale.

Highlighting the EBRD’s role in advancing the long-term funding such industrial investments require, the package includes a EUR 50 mil-lion loan which will provide for a bullet repayment at the end of seven years as well as a seven-year A loan of EUR 60 million with a two-year grace period under an EBRD A/B loan structure.

The remaining EUR 40 million has been syndicated to three inter-national banks under a five-year EBRD B loan with UniCredit Bank Austria AG taking a EUR 20 million participation, the Spanish subsidiary of France’s Société Générale group taking EUR 13 million and Spain’s Banco Bilbao Vizcaya Argentaria SA taking EUR 7 million.

The Bank remains the lender of