The Evolution of the International Financial System Experience is the name we give to past mistakes,...

30

International Econom ics The Evolution of the International Financial System Experience is the name we give to past mistakes, reform that which we give to future ones. (Henry Wallach, 1972) Chapter 14

-

Upload

amelia-maxwell -

Category

Documents

-

view

214 -

download

0

Transcript of The Evolution of the International Financial System Experience is the name we give to past mistakes,...

International Economics

The Evolution of the International Financial System

Experience is the name we give to past mistakes, reform that which we give to future ones.

(Henry Wallach, 1972)

Chapter 14

International Economics

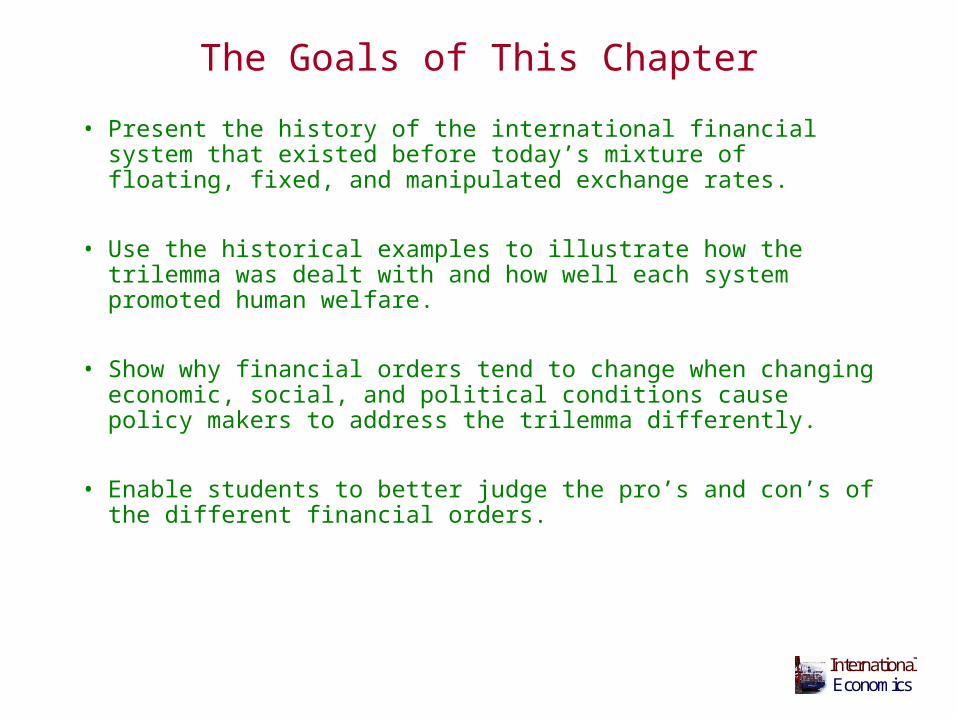

The Goals of This Chapter

• Present the history of the international financial system that existed before today’s mixture of floating, fixed, and manipulated exchange rates.

• Use the historical examples to illustrate how the trilemma was dealt with and how well each system promoted human welfare.

• Show why financial orders tend to change when changing economic, social, and political conditions cause policy makers to address the trilemma differently.

• Enable students to better judge the pro’s and con’s of the different financial orders.

International Economics

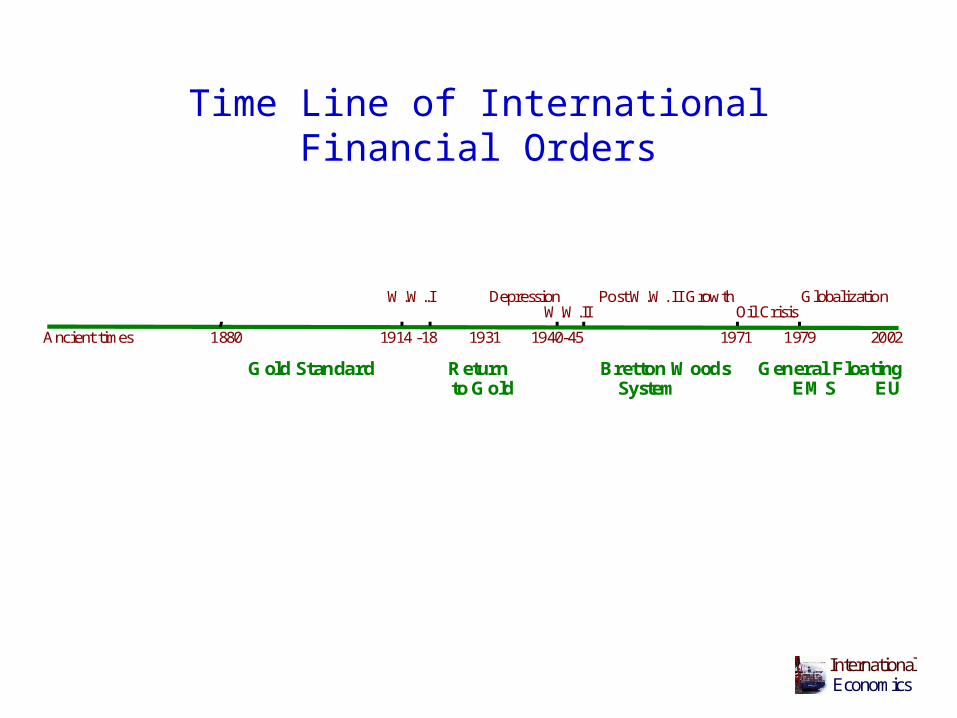

Time Line of International Financial Orders

Ancient times 1880 1914 -18 1931 1940-45 1971 1979 2002

Gold Standard Return Bretton Woods General Floating to Gold System EMS EU

W.W..I Depression Post W.W. II Growth Globalization W.W.II Oil Crisis

International Economics

The Rules of the Game

• The set of rules and other formal and informal incentives under which a financial system operates is called an order.

• An international monetary order is sometimes referred to in the international finance literature as “the rules of the game,” a term reportedly coined by John Maynard Keynes.

• A monetary order is to a monetary system somewhat like a constitution is to a political system.

International Economics

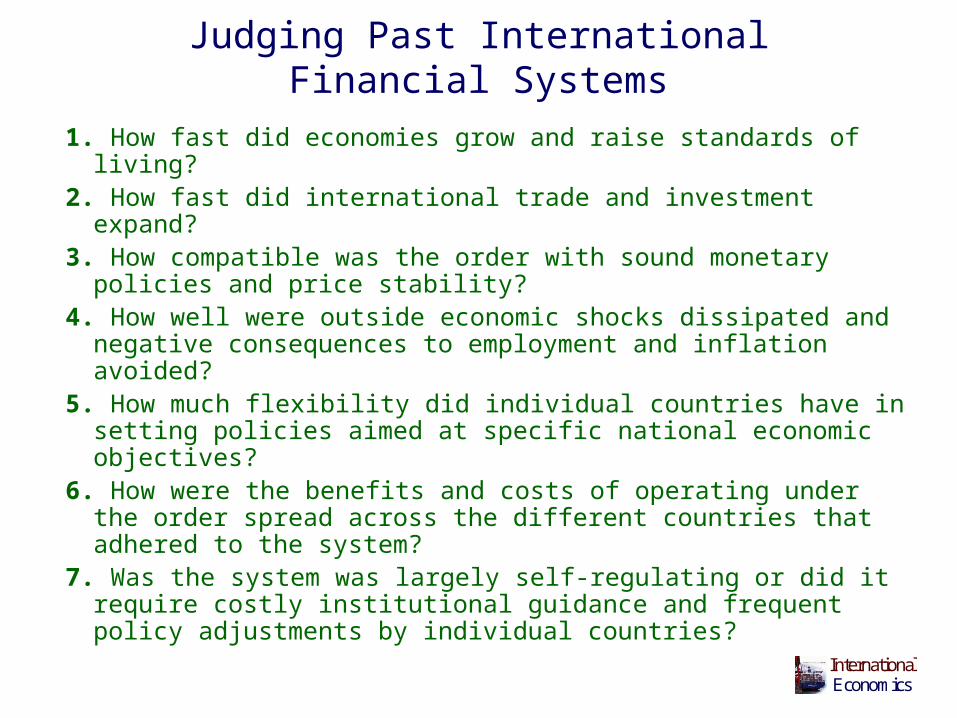

Judging Past International Financial Systems

1. How fast did economies grow and raise standards of living?2. How fast did international trade and investment expand?3. How compatible was the order with sound monetary policies

and price stability?4. How well were outside economic shocks dissipated and

negative consequences to employment and inflation avoided?5. How much flexibility did individual countries have in setting

policies aimed at specific national economic objectives?6. How were the benefits and costs of operating under the order

spread across the different countries that adhered to the system?

7. Was the system was largely self-regulating or did it require costly institutional guidance and frequent policy adjustments by individual countries?

International Economics

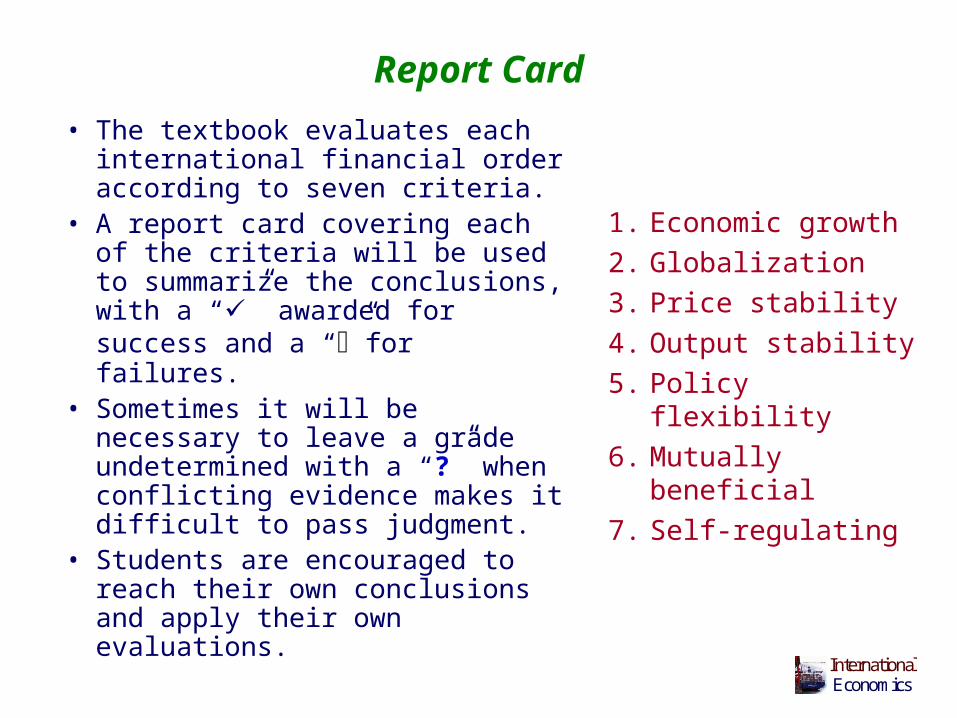

Report Card

• The textbook evaluates each international financial order according to seven criteria.

• A report card covering each of the criteria will be used to summarize the conclusions, with a “” awarded for success and a “”for failures.

• Sometimes it will be necessary to leave a grade undetermined with a “?” when conflicting evidence makes it difficult to pass judgment.

• Students are encouraged to reach their own conclusions and apply their own evaluations.

1. Economic growth

2. Globalization

3. Price stability

4. Output stability

5. Policy flexibility

6. Mutually beneficial

7. Self-regulating

International Economics

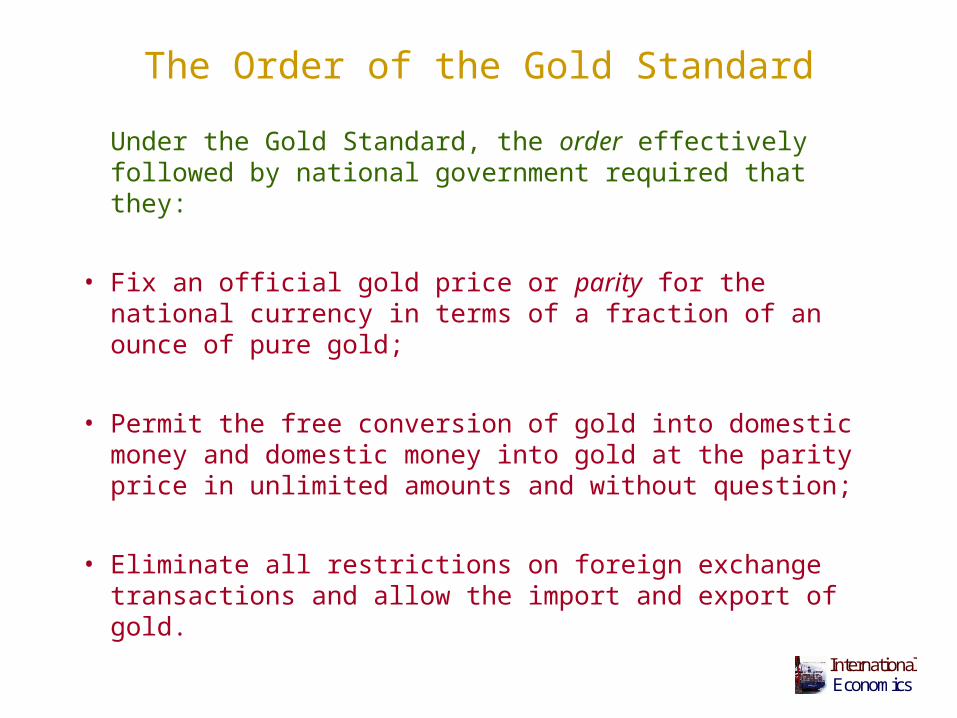

The Order of the Gold Standard

Under the Gold Standard, the order effectively followed by national government required that they:

• Fix an official gold price or parity for the national currency in terms of a fraction of an ounce of pure gold;

• Permit the free conversion of gold into domestic money and domestic money into gold at the parity price in unlimited amounts and without question;

• Eliminate all restrictions on foreign exchange transactions and allow the import and export of gold.

International Economics

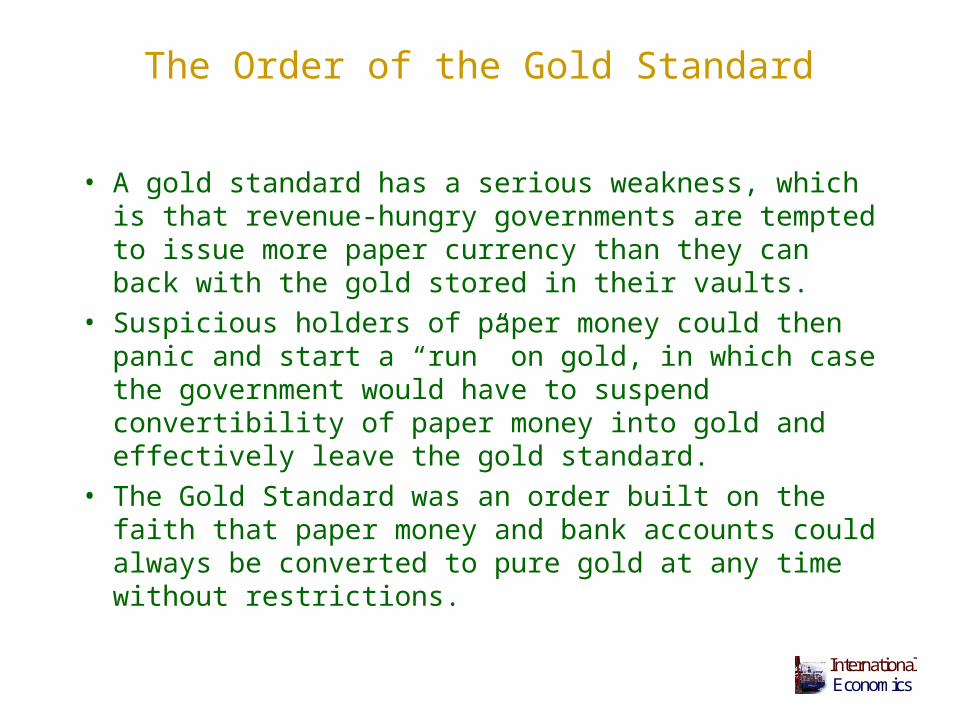

The Order of the Gold Standard

• A gold standard has a serious weakness, which is that revenue-hungry governments are tempted to issue more paper currency than they can back with the gold stored in their vaults.

• Suspicious holders of paper money could then panic and start a “run” on gold, in which case the government would have to suspend convertibility of paper money into gold and effectively leave the gold standard.

• The Gold Standard was an order built on the faith that paper money and bank accounts could always be converted to pure gold at any time without restrictions.

International Economics

The Order of the Gold Standard

To enhance faith in the system, several other “rules of the game” had to be respected by governments:

• Back domestic coin and currency fully with gold reserves, and link the growth of domestic money to the availability of reserves.

• Effectively allow the domestic price level to be determined by the worldwide supply and demand for gold.

• If the central bank must serve as a lender of last resort in the case of short-term credit crises in the domestic banking sector, always charge interest rates well above market.

International Economics

The Gold Standard and Exchange Rates

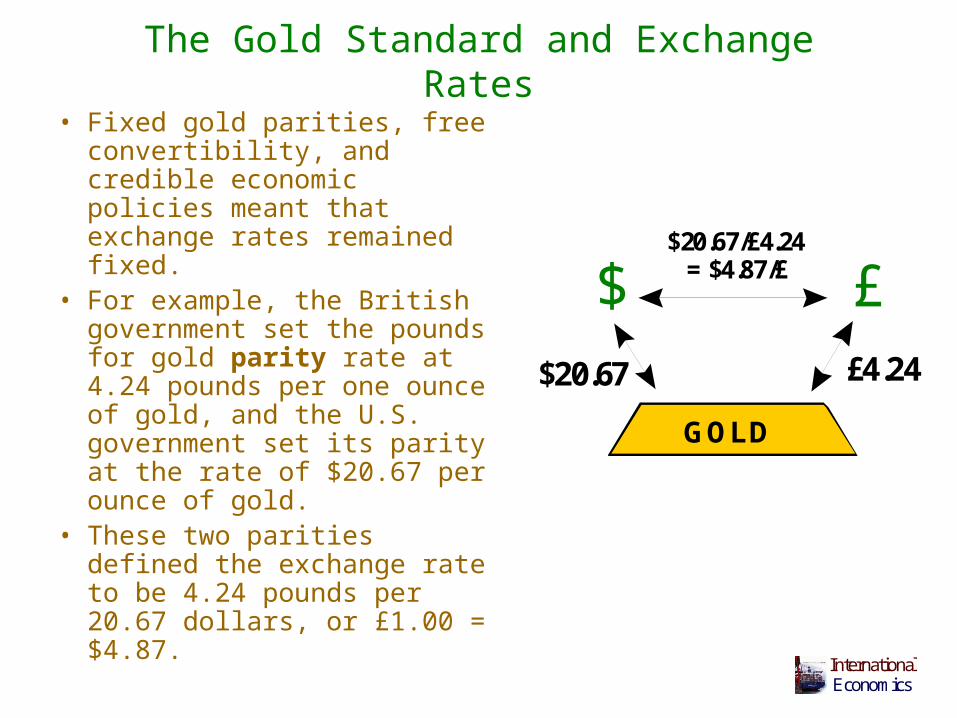

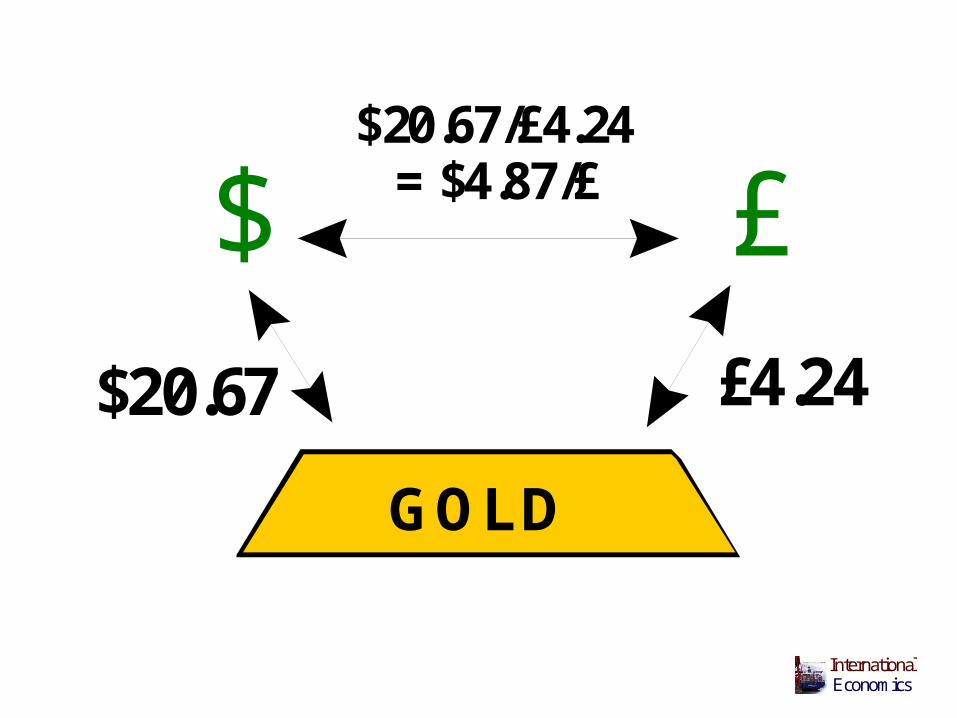

• Fixed gold parities, free convertibility, and credible economic policies meant that exchange rates remained fixed.

• For example, the British government set the pounds for gold parity rate at 4.24 pounds per one ounce of gold, and the U.S. government set its parity at the rate of $20.67 per ounce of gold.

• These two parities defined the exchange rate to be 4.24 pounds per 20.67 dollars, or £1.00 = $4.87.

£$$20.67 £4.24

$20.67/£4.24 = $4.87/£

GOLD

International Economics

£$$20.67 £4.24

$20.67/£4.24 = $4.87/£

GOLD

International Economics

The Gold Standard and Exchange Rates

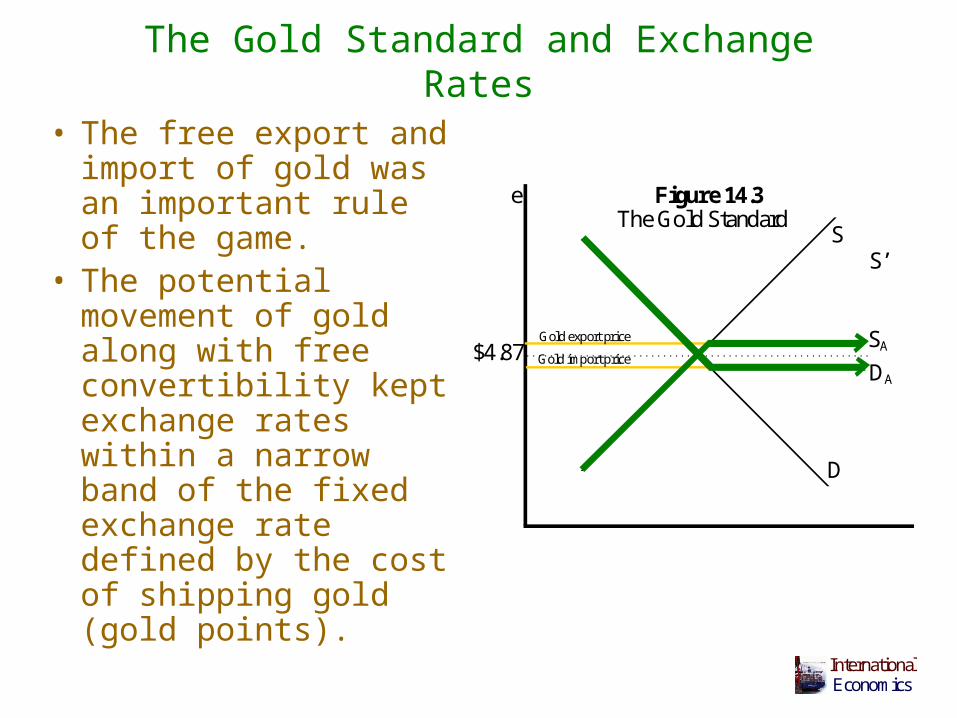

• The free export and import of gold was an important rule of the game.

• The potential movement of gold along with free convertibility kept exchange rates within a narrow band of the fixed exchange rate defined by the cost of shipping gold (gold points).

$4.87

S

D

S’

Gold export price

Gold import price

e Figure 14.3 The Gold Standard

DA

SA

International Economics

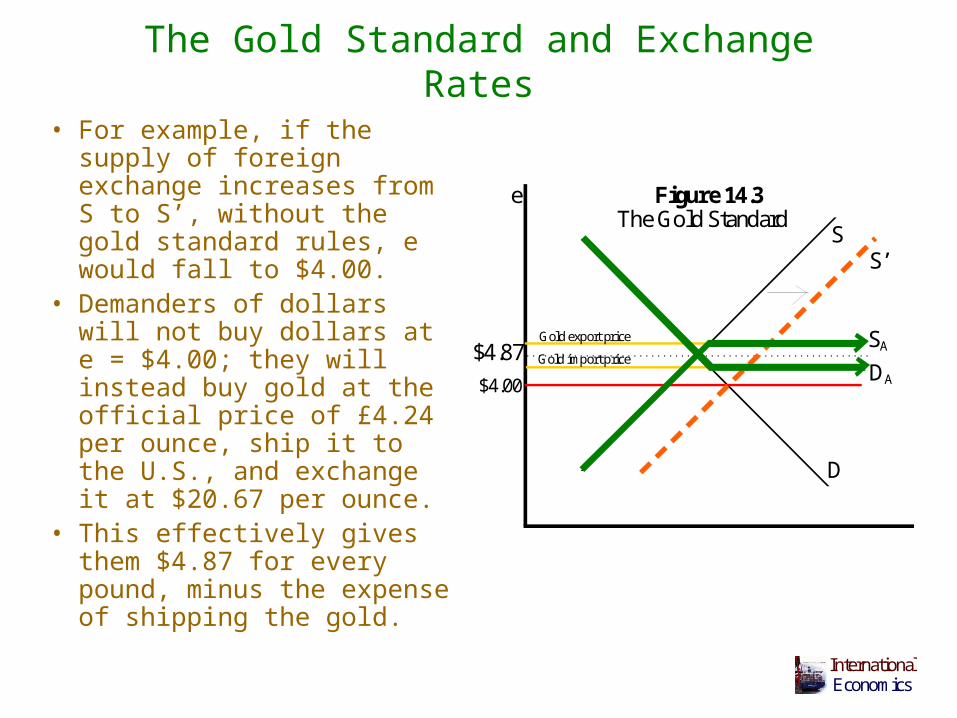

The Gold Standard and Exchange Rates

• For example, if the supply of foreign exchange increases from S to S’, without the gold standard rules, e would fall to $4.00.

• Demanders of dollars will not buy dollars at e = $4.00; they will instead buy gold at the official price of £4.24 per ounce, ship it to the U.S., and exchange it at $20.67 per ounce.

• This effectively gives them $4.87 for every pound, minus the expense of shipping the gold.

$4.87

S

D

$4.00

S’

Gold export price

Gold import price

e Figure 14.3 The Gold Standard

DA

SA

International Economics

Hume’s Specie-Flow Mechanism

• The specie flow mechanism and was first described as far back as 1752 by David Hume, before the establishment of the gold standard.

• Hume’s reasoning was used to argue that the gold standard was self-correcting.

• If a trade deficit caused gold to flow out of a country, its money supply would fall and prices would decline, thus restoring international competitiveness without changing the exchange rate.

• Similarly, a trade surplus would cause gold to flow into the country, increasing the money supply, and eventually reducing exports and increasing imports.

International Economics

Report CardThe Gold Standard

1. Economic growth 2. Globalization

3. Price stability

4. Output stability 5. Policy flexibility 6. Mutually beneficial ?

7. Self-regulating ?

International Economics

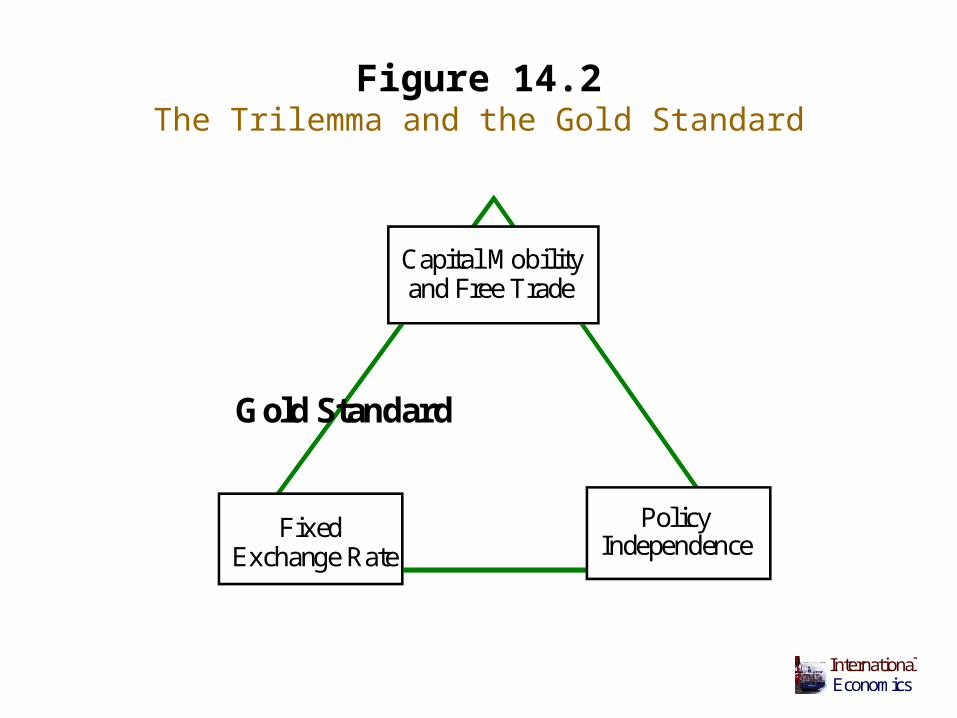

Figure 14.2The Trilemma and the Gold Standard

Capital Mobility and Free Trade

Fixed Exchange Rate

PolicyIndependence

Gold Standard

International Economics

Returning to the Gold Standard under Changed Circumstances After World War I

• Inflation during the war years meant that countries would have to deflate if they were to return to the gold standard under the old gold parities.

• John Maynard Keynes argued that the tight monetary policies required to restore the real value of gold relative to the world’s money supplies cost too much in terms of unemployment, falling investment, and lost output.

• He suggested that countries forget trying to return to the gold standard under the old gold parities and that they should set new parities and simply seek to maintain price stability at the higher price levels instead of trying to deflate prices.

International Economics

Returning to the Gold Standard under Changed Circumstances After World War I

• A strong case can be made that the deflationary policies of the 1920s, driven by the desire to return to the gold standard under the traditional gold parities, caused the Great Depression.

• According to Nobel-laureate Robert Mundell:Had the price of gold been raised in the late

1920's, or, alternatively, had the major central banks pursued policies of price stability instead of adhering to the gold standard, there would have been no Great Depression, no Nazi revolution, and no World War II.

• Policy makers would design a very different financial order after World War II.

International Economics

Report CardThe Inter-War Period

1. Economic growth 2. Globalization

3. Price stability 4. Output stability 5. Policy flexibility 6. Mutually beneficial 7. Self-regulating

International Economics

The Extraordinary Bretton Woods Conference

• In July of 1944, while the Second World War was still raging, the economic policy makers from the allied countries met in the U.S. to establish the order that would guide the post-World War II international system.

• The motivation for the Bretton Woods Conference was to reverse the trend toward economic isolation and growth-retarding economic policies during the inter-war years.

• The purpose of the Bretton Woods conference was to design a world economic order that would minimize economic conflict, encourage sound macroeconomic policies to generate growth and employment in all economies, and restore the flow of goods and investments between countries.

International Economics

The Bretton Woods Order

1. Countries other than the U.S. intervene in the foreign exchange market to keep their exchange rate within 1% of the dollar peg.

2. The U.S. does not intervene in the foreign exchange markets, but will convert dollars to gold at $35/oz. for foreign central banks.

3. The International Monetary Fund (IMF) serves as the central bankers’ central bank, providing liquidity to intervene in the foreign exchange markets.

4. Pegs should be adjusted in the exceptional circumstances of a fundamental disequilibrium; otherwise adjust domestic monetary policies to keep the exchange rate fixed.

5. The U.S. and its large economy effectively anchors the world price level with its monetary policy.

6. Currency should be freely convertible for current account transactions.

International Economics

Devaluation? Depreciation?What’s the Difference?

• The term depreciation (appreciation) refers to a decline (rise) in value of a currency relative to other currencies under a regime of floating exchange rates.

• The term devaluation (revaluation) refers to an intentional one-time lowering (raising) of the fixed value of a currency under a fixed exchange rate arrangement.

International Economics

Figure 14.7The Trilemma and the Bretton Woods System

Capital Mobility and Free Trade

Fixed Exchange Rate

PolicyIndependence

Bretton Woods: 1959-1971

Early Bretton Woods 1944-1958

International Economics

Report Card Bretton Woods

1. Economic growth 2. Globalization 3. Price stability ?4. Output stability ?5. Policy flexibility 6. Mutually beneficial ?7. Self-regulating

International Economics

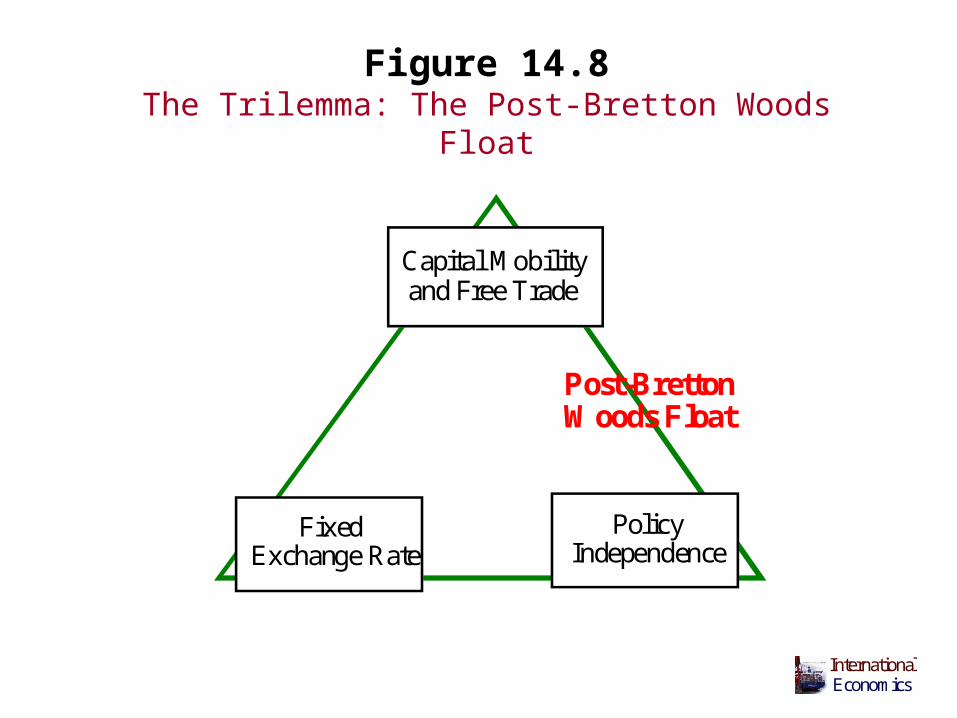

Figure 14.8The Trilemma: The Post-Bretton Woods Float

Capital Mobility and Free Trade

Fixed Exchange Rate

PolicyIndependence

Post-Bretton Woods Float

International Economics

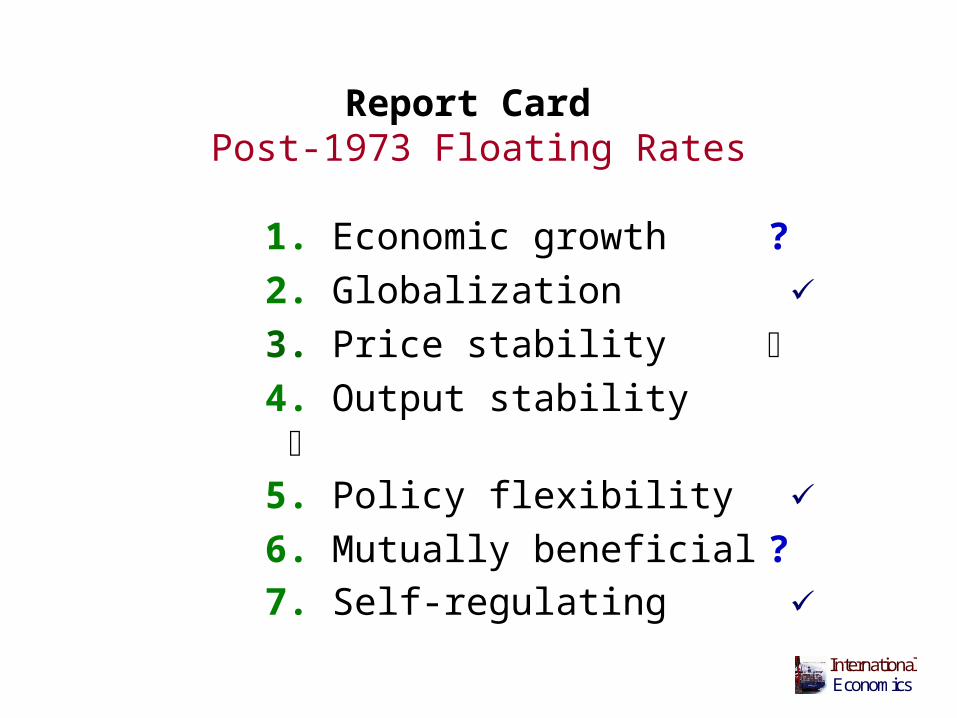

Report Card Post-1973 Floating Rates

1. Economic growth ?

2. Globalization

3. Price stability 4. Output stability 5. Policy flexibility

6. Mutually beneficial ?

7. Self-regulating

International Economics

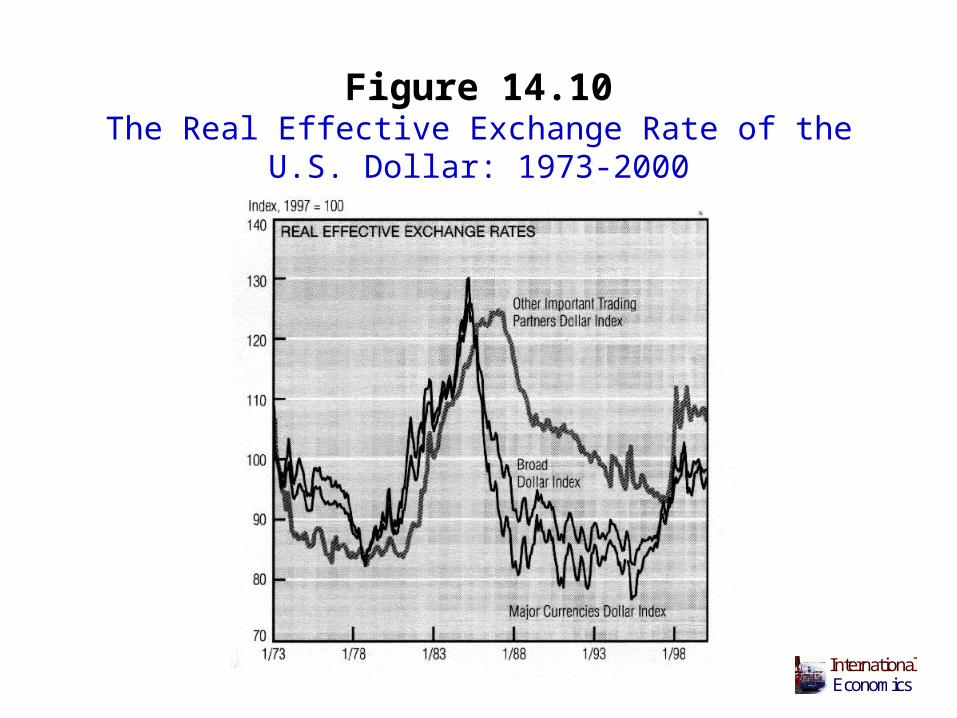

Figure 14.10The Real Effective Exchange Rate of the U.S. Dollar:

1973-2000

International Economics

Establishing a European Monetary Union

• At a meeting in Madrid in December of 1995, the European Union, jus having expanded to 15 members, reconfirmed its intent to create a single currency.

• The new currency was to be called the euro and denoted by the symbol i.

• European governments agreed to a three-step procedure for moving toward a single currency.

• Most importantly, a set of specific economic goals were set, and these goals would have to be met by a country before it could become part of the single currency area.

• At the start of 2002, the euro became the currency of Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxemburg, the Netherlands, Portugal, and Spain.

International Economics

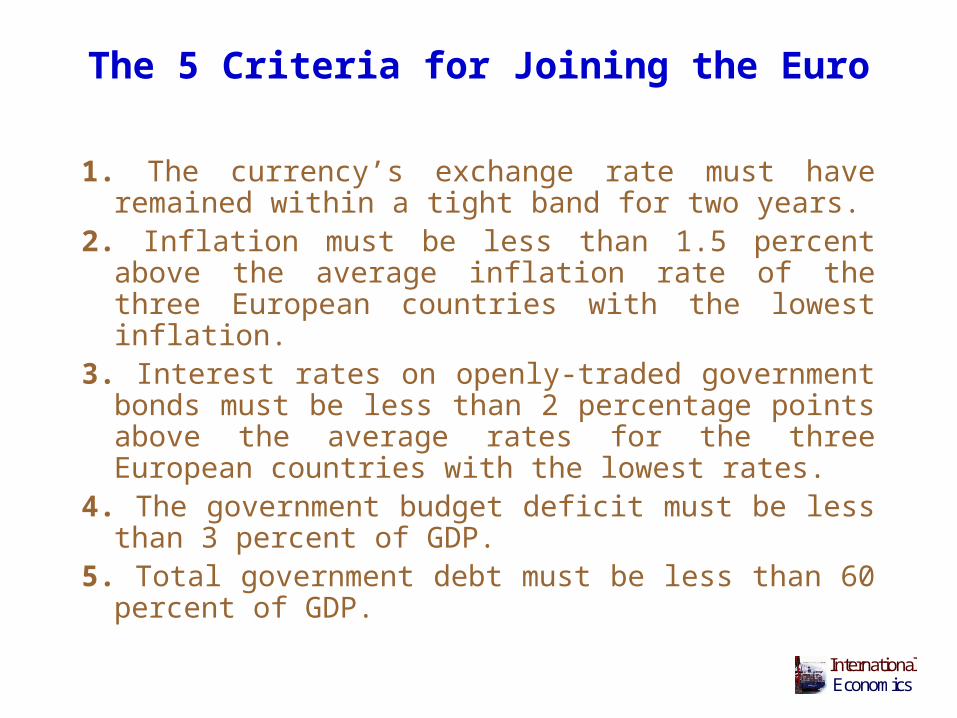

The 5 Criteria for Joining the Euro

1. The currency’s exchange rate must have remained within a tight band for two years.

2. Inflation must be less than 1.5 percent above the average inflation rate of the three European countries with the lowest inflation.

3. Interest rates on openly-traded government bonds must be less than 2 percentage points above the average rates for the three European countries with the lowest rates.

4. The government budget deficit must be less than 3 percent of GDP.

5. Total government debt must be less than 60 percent of GDP.

International Economics

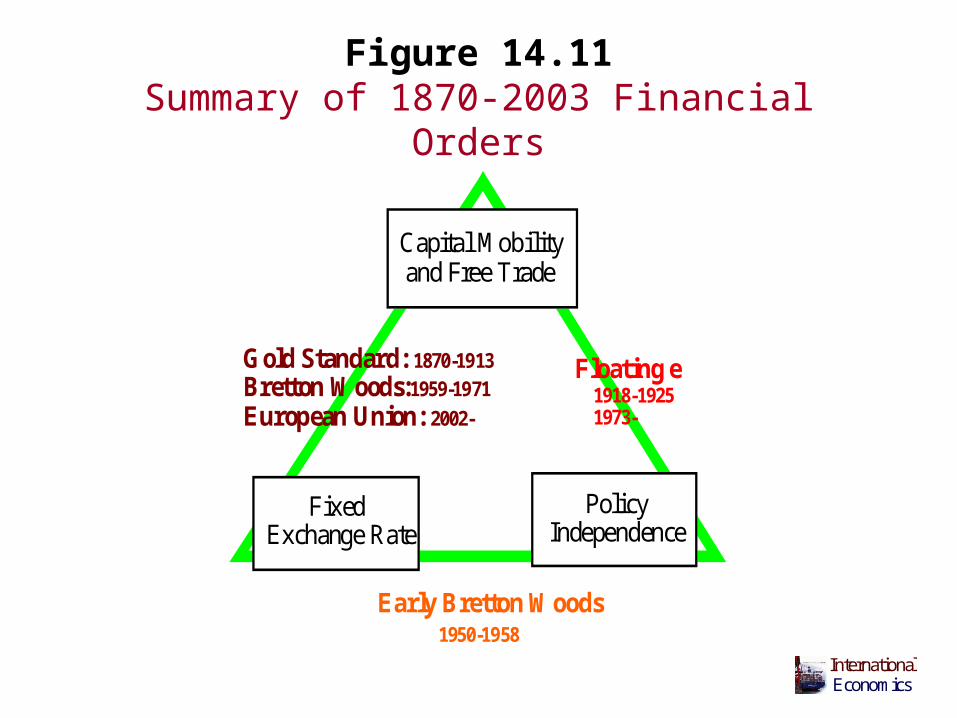

Figure 14.11Summary of 1870-2003 Financial Orders

Capital Mobility and Free Trade

Fixed Exchange Rate

PolicyIndependence

Gold Standard: 1870-1913Bretton Woods:1959-1971

European Union: 2002-

Floating e 1918-1925 1973-

Early Bretton Woods 1950-1958