Diversification Strategies and Firm Performance: A Sample ...

MSc. in Finance and International Business Author: Selen Gül

Department of Business Administration Advisor: Valerie Smeets

The Effects of Integration Strategies on Firm Performance

An Empirical Study on Danish Manufacturing Firms

Abstract:

The firms’ diversification strategy choices and their impact on corporate performance have been the center of attention both empirically and theoretically in the fields of strategy and finance for more than 30 years. However in general, previous studies have analyzed the integration-performance relationship without differentiating the industries that the firms were operating in, but rather the samples were pooled across industries. The aim of this paper is to investigate the performance effects of vertical, horizontal, unrelated integration and un-diversification strategies, by using a sample of 147 Danish manufacturing companies distinguished among 5 large industries, through the years 2009 to 2005. Empirical evidence shows that horizontal (related) integrated companies are outperforming the corporate performance of unrelated diversified firms, and the structure of the market, the level of concentration have varying effects on performance for each type of industry. Out of 5 industries, the manufacture of food products has the highest average performance measure, and the empirical results underline the significant and positive effect of the horizontal integration strategy for the manufacture of food products and manufacture of machinery and equipment industries that were subject to be tested.

August 2011

Aarhus School of Business, Aarhus University

Selen Gül The Effects of Integration Strategies on Firm Performance

1

Table of Contents

1. Introduction ................................................................................................................ 3

1.1.Research Questions............................................................................................ 4

1.2.Structure of the Thesis ....................................................................................... 5

2. Literature Review ........................................................................................................ 6

2.1.Theories of Vertical Integration ........................................................................ 6

2.1.1. Make or Buy Decision ..................................................................... 6

2.1.2. The Transaction Cost Theory .......................................................... 7

2.1.3. The Property Rights Theory ............................................................ 8

2.1.3.1.Benefits and Costs of Contracts........................................... 9

2.1.4. The Theory of Relational Contracts ................................................ 10

2.1.5. Is Vertical Integration Beneficial for the Firm? .............................. 10

2.1.6. Empirical Evidence on Vertical Mergers ........................................ 11

2.2.Horizontal Integration ........................................................................................ 12

2.2.1. Economies of Scale and Scope ........................................................ 13

2.2.2. The Learning Economy ................................................................... 14

2.2.3. Empirical Evidence on Horizontal Mergers .................................... 15

2.3.Diversification ................................................................................................... 16

2.3.1. Product Diversification .................................................................... 17

2.3.2. Geographic Diversification .............................................................. 17

2.3.3. The Determinants and Motives for Diversification ......................... 18

2.3.4. The Resource-Based View .............................................................. 19

2.3.5. Diversification and Firm Performance ............................................ 20

2.3.6. Empirical Evidence on Diversification and Firm Performance ...... 22

3. Development of Hypotheses ........................................................................................ 24

4. Methodology ................................................................................................................. 26

5. Data Construction........................................................................................................ 28

5.1.Sample Selection ............................................................................................... 28

5.2.Variables Measurement ..................................................................................... 30

5.2.1. Performance Measures (Dependent Variables) .............................. 30

5.2.2. Independent Variables ..................................................................... 31

5.2.3. Control Variables ............................................................................. 32

Selen Gül The Effects of Integration Strategies on Firm Performance

2

5.3.Limitations ......................................................................................................... 36

6. General Descriptive Analysis of Each Industry ........................................................ 37

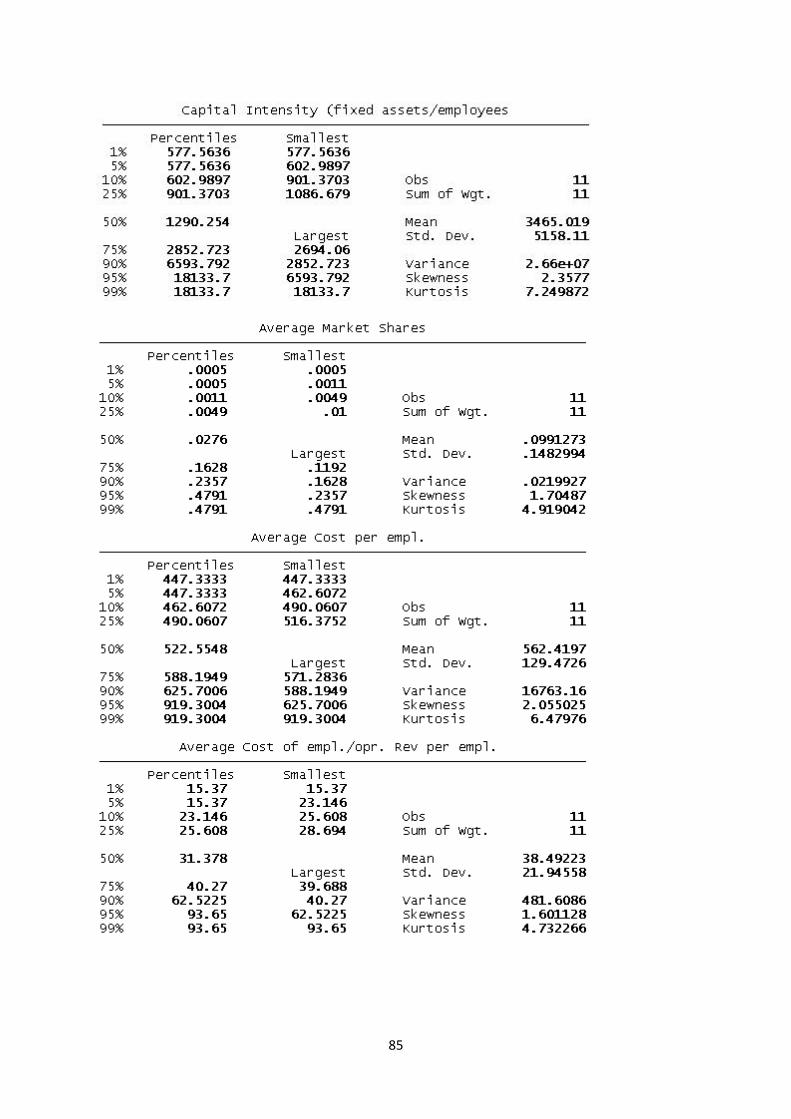

6.1.Manufacture of Basic Pharmaceuticals and Pharmaceutical Preparations ........ 37

6.2.Manufacture of Food Products .......................................................................... 41

6.3.Manufacture of Chemicals and Chemical Products .......................................... 44

6.4.Manufacture of Furniture ................................................................................... 46

6.5.Manufacture of Machinery and Equipment ....................................................... 48

7. Industry Comparisons ................................................................................................. 51

8. Empirical Findings and Discussion of Results .......................................................... 53

8.1.Manufacture of Food Industry ........................................................................... 53

8.2.Manufacture of Machinery and Equipment Industry ........................................ 57

8.3.Discussion of Results......................................................................................... 60

9. Conclusion .................................................................................................................... 63

References ........................................................................................................................... 65

Appendices ......................................................................................................................... 72

Selen Gül The Effects of Integration Strategies on Firm Performance

3

1. INTRODUCTION

In this new era, where technological innovations are growing at a fast pace leading to

a more globalized world, corporations are facing a change in their form, structure and scope.

These new technologies engendered goods to be produced at lower costs, compared to what

organizations could achieve using older technologies. In order to benefit from these

production opportunities, firms require reliable supplies of inputs, access to widespread

distribution and retail outlets. Based on these necessities, the relationships among

manufacturers, their suppliers, and their distributors have been affected by this product line

and volume expansion.

In relation to this phenomenon, the question of the diversification-performance

relation, has been generally the most studied in the literature. The scholars’ main focus has

been on the value enhancing or destructive effects of diversification, and the conclusions vary

based on the perspectives of the studies that are conducted. Santalo & Becerra (2008)

underline that, while several authors have found strong evidence of trading at a discount for

diversified firms, supporters indicate that diversified firms are more productive compared to

stand-alone businesses. Moreover, the early contributions of Rumelt (1974) and Penrose

(1995) indicate that, as firms diversify into more unrelated areas, a lower performance

outcome is more likely.

Besides the effects of unrelated diversification and firm value, the companies may

initially choose to either vertically or horizontally integrate. Manufacturing firms increasingly

choose to vertically integrate; meaning that, rather than relying on independent suppliers,

factors and agents, they choose to produce the raw materials themselves and even distribute

finished goods. Moreover, new production technologies have given firms the opportunity to

exert scope economies by producing a wider range of products at a lower cost, compared to

be produced separately, leading them to horizontally integrate. (Besanko et. al, 2007)

Through diversification within their areas of business, the companies desire to reduce costs

and improve market effectiveness by utilizing economies of scale and scope.

Besides these integration strategies, geographic diversification plays a key role in the

strategic behavior of the large companies and their corporate performance. The company’s

expansion to different geographic locations as to different global regions and countries would

define international diversification (Hitt et. al, 1997) Its importance comes from the utilization

of the foreign market opportunities.

The research on diversification and firm value has focused primarily on US and

European based companies, without taking the performance effects of vertical and horizontal

Selen Gül The Effects of Integration Strategies on Firm Performance

4

integration into consideration. In addition, there are few studies that have focused on a single

country, as Kahloul & Hallara (2010) evaluated the performance effects of the French firms.

This paper will evaluate the performance measures by combining the impacts of unrelated

diversification and as well as vertical, horizontal integration strategies and remaining

undiversified. Moreover, in order to specify the results and overcome the socio-cultural

differences among countries, the main focus will be on Danish manufacturing companies and

the outcomes are to be evaluated based on five different industries.

1.1. Research Questions

Based on the definitions mentioned above, it is crucial to highlight the relationship

between firm performance and its level of integration strategies. By extending the study of

diversification-firm performance analyzers (Penrose, 1995; Rumelt, 1974; Bettis, 1981), the

aim of this paper is to question whether firms with an unrelated diversification, horizontal

integration, vertical integration or un-diversification strategy perform better or worse

compared to each other, and how these choices affect the firm performance. Prior studies

generally have taken the effect of integration strategies homogenous across the industries,

whereas this study investigates the effect of the strategies on performance by differentiating

the industries. This homogenous approach is neglected since different industries bear different

structural characteristics, which will lead to various average profits in each industry (Bettis &

Hall, 1982), and the type of concentration and competition within an industry are the leading

factors that orientate the companies to integrate or not (Penrose, 1995). The questions to be

addressed are as follows:

• What is the dominant integration strategy that each industry embraces and

which one has the highest affect on performance?

• How does the level of concentration change among the industries and does it

have a relation with the strategies chosen?

• Does the integration strategies have an impact on corporate performance and

do these effects differ based on the industries?

• Does the number of countries the firm is operating in, have an impact on firm

operating performance?

Selen Gül The Effects of Integration Strategies on Firm Performance

5

1.2.Structure of the Thesis

The next section will highlight the theoretical and empirical findings on the topic.

Section 3 develops the hypothesis based on the theoretical and empirical arguments

mentioned in the literature review. Section 4 gives in depth information of the methodology

used, and Section 5 describes the data collection procedure. Section 6 presents the summary

statistics for the industries involved in the study. Section 7 illustrates the comparisons among

these industries based on their summary statistics. Section 8 presents the empirical findings

and the discussion of the results, and finally, Section 9 makes concluding remarks regarding

the study.

Selen Gül The Effects of Integration Strategies on Firm Performance

6

2. LITERATURE REVIEW 2.1.Theories of Vertical Integration

Coase (1937) suggests that the introduction of the firm is initially based on the

existence of the marketing costs. The number of transactions or the activities of the firm

within its boundaries is the determining component in assessing the size of the firm, rather

than its output. These boundaries are defined as the vertical boundaries since these activities

are related at the various levels of the supply chain. Sudarsanam (2010) defines vertical

integration as “the combination of successive activities in a vertical chain under common

coordination and control of a single firm.” (p. 153) Vertical integration defines the activities

that the company performs within its boundaries, compared to the purchases from

independent firms in the market (Besanko et.al, 2007). In other words, vertical merger

replaces two or more independent firms with a single firm, and rather than relying on arm’s

length market-based transactions or contractual dealings, it internalizes the coordination of the

successive activities of the firm. Fan & Goyal (2006) indicate that vertical mergers procure

acquiring companies with ownership and control over contiguous stages of production. These

mergers allow firms to substitute internal exchanges within the boundaries of the firm for

contractual or market exchanges. Although vast amounts of theoretical studies on vertical

integration exist, there is inadequate number of empirical work on vertical mergers, and the

ones conducted are based on small samples.

2.1.1. Make-or-Buy Decision

Make-or-Buy decisions address the questions of: Why do some firms prefer a

vertically integrated structure, while others specialize in one stage of production and

outsource the remaining stages to other companies? In other words, should a firm produce its

own inputs, buy them in the spot market or preserve the relationship with a specific supplier.

This decision determines the firm's level of vertical integration, since every decision identifies

which operations the firm will engage in and which it will outsource from the suppliers

(Walker & Weber, 1984). This notion is concerned with the decision whether to integrate

backwards, which is “to internalize production of an input rather than source it from an

external supplier.” (Sudarsanam, 2010, p. 158) Therefore the ‘make’ part of the decision

emphasizes that ownership is joint and control rights are integrated, whereas under the latter,

they are separate. Moreover, the costs and benefits of either alternative have to be taken into

consideration. For instance, this choice may depend on a range of factors such as; “the current

and future availability of spot markets for arm’s length transactions, the cost of sourcing from

Selen Gül The Effects of Integration Strategies on Firm Performance

7

the spot market, the direct and indirect costs of contracts and informal arrangements,

uncertainty and information asymmetry between buyer and seller and indirect costs of

internalizing production.” (p.158)

Based on these factors, the company can choose to perform the activities in-house or

buy them from the specialists in the market that are called market firms (Besanko et. al,

2007). There are many advantages and disadvantages of using the market firms to source the

upstream activities in the vertical change. The benefits would be achieving scale and learning

economies, as well as efficient division of labor and specialization from the supplier’s side.

On the other hand, the downsides would be the issue in coordinating the production process,

the leak of private information, agency and influence costs, moral hazard and disincentives for

innovation.

2.1.2. The Transaction-Cost Theory

The transaction costs theory (TC) can be traced back to Coase (1937) who indicated

that the production will take place within the firm when the cost of organizing the production

through the market exchange is larger than within the firm. In other words, the firms may

avoid the costs of transacting with the market firms by carrying out the activity in-house. This

cost of transacting with independent market firms is defined by Coase (1937) as the cost of

using the price mechanism. The size of the firm will be based on the cost of using the price

mechanism, in which “a firm will tend to expand until the costs of organizing an extra

transaction within the firm become equal to the costs of carrying out the same transaction by

means of exchange on the open market or the costs of organizing in another firm.” (p. 395)

Leiblein & Miller (2003) argue that, although the applicants of the theory generally assume

that markets ensure a more efficient mechanism for exchange compared to the hierarchy, in

certain situations the costs of the market exchange may be too high and surpass these

efficiencies procured by the market. Therefore, the theory focuses on determining the features

of exchanges that are best suited to the firms and the market. Williamson (1975) indicates that

these inefficiencies originate from small numbers of bargaining situations. “Due to the

bounded rationality of decision-makers, the asymmetric distribution of relevant information,

and the inability to completely specify behavior in the presence of multiple contingencies, the

theory maintains that all contracts are incomplete and therefore subject to renegotiation and

the possibility of opportunistic behavior.” (Leiblein & Miller, 2003, p. 842) Opportunistic

behavior is more apparent, when an exchange demands one or more parties to get involved in

Selen Gül The Effects of Integration Strategies on Firm Performance

8

significant transaction-specific investments, which in turn create quasi-rents1 that, may lead to

hold-up2. Such relation-specific investment creates difficulty in switching to a new customer

due to the increases in costs, thus locking the supplier into that relationship (Sudarsanam,

2010). Besanko et al. (2007) and Sudarsanam (2010) are underlining the types of specificities

as; site, physical characteristics, dedicated assets and human assets specific.

Therefore, based on these downsides of contracts, vertical integration is thought to be

beneficial, where hold-up concerns are severe. Firms are expected to depend on in-house

production when the transactions are complex, specific investments are included, those

specific assets are unceasing, the quality of those assets are hard to be verified, the

environment is uncertain and when the quasi-rents based on the relationship are large.

2.1.3. The Property-Rights Theory

The property-rights theory, which has been developed by Grossman & Hart (1986),

emphasizes how asset ownership can change investment incentives. They propose two types

of contractual rights as; the specific rights and residual rights of control. “When it is too

costly for one party to specify a long list of the particular rights it desires over another’s

party’s assets, it may be optimal for that party to purchase all the rights except for those

specified in the contract.” (p. 692) The purchase of the residual rights of control is called

ownership. All the residual control rights of the physical assets in question are held by the

entity under integration, whereas under non-integration, the assets are owned individually

(Hubbard, 2008). Moreover, Grossman & Hart (1986) present that the allocation of residual

control rights to one party strengthens the investment incentives of that party, while

weakening the counter party’s investment incentives. “Integration shifts the incentives for

opportunistic and distortionary behavior, but it does not remove these incentives.” (p. 716)

Therefore, both costs and benefits from integration will exist. One of the concluding remarks

of Grossman & Hart (1986) is that, integration is suggested when one party’s investment

incentives is relatively more important to the other firm’s incentives. On the other hand, when

both investment decisions are equally and somewhat crucial, non-integration is preferable.

Compared to the TC literature, the PR literature does not underline the ex post

haggling, renegotiation and opportunistic behavior. “Instead it stresses contractual

incompleteness and develops formal models that show how ex post bargaining affects ex ante

investment in non-contractible assets.” (Lafontaine & Slade, 2007, p. 650) Kim & Mahoney 1 Quasi-rent would be “the extra profit that you get if the deal goes ahead as planned, versus the profit you would get if you had to turn to your next-best alternative.” (Besanko et. Al, 2007, p. 126) 2 The term hold-up will be explained more in detail under section 2.1.3.1.

Selen Gül The Effects of Integration Strategies on Firm Performance

9

(2005) further indicate the importance of property rights theory, as that various specifications

of property rights arise in response to the economic problem of allocating scarce resources,

and how it affects the economic behavior and economic outcomes in return.

2.1.3.1. Benefits and Costs of Contracts

According to the theories mentioned above, the existence of market failures may lead

the firms to source its inputs from suppliers by negotiating contracts. The duration of these

contracts may be short or long-term in nature. Williamson (1971) introduces three alternatives

to be considered: a life time contract, a series of short-term contracts, and vertical integration.

The once-for-all type of contracts are facing the dilemma of the redesign issues due to

changing technology, in which sequential decision process is needed. “If, however,

contractual revisions or amendments are regarded as an occasion to bargain opportunistically,

which predictably they will be, the purchaser will defer and accumulate adaptations, if by

packaging them in complex combinations their true value can better be disguised; some

adaptations may be forgone altogether.” (Williamson, 1971, p. 116) Therefore, short-term

contracts may be more preferable due to sequential decision making and adaptation. However,

the downsides would be the necessity of relation-specific investments and the existence of a

first-mover advantage for one of the parties (Williamson, 1971). These downsides would

generate the hold-up problem or behaving opportunistically, in which it occurs when one of

the parties would attempt to renegotiate the terms of the contract. The party that has been

held-up could be either the buyer or the supplier, but most likely the one that has engaged in a

relation-specific investment (Besanko et. al, 2007). In order to eliminate this hold-up problem,

Williamson (1971) suggests the firms to vertically integrate, in which the disadvantages of

long and short term contracts would be avoided. “Sequential adaptations become an occasion

for cooperative adjustment rather than opportunistic bargaining; risks may be attenuated;

differences between successive stages can be resolved more easily by the internal control

machinery.” (Williamson, 1971, p. 116)

Besides the solution of vertical integration, only a complete contract can eliminate

opportunistic behavior. Besanko et al. (2007) argue the applicability of complete contracts,

and underline that this type of contracts would be feasible only if the parties are able to

specify each contingency to be occurred and the set of actions to be taken. Therefore,

contracts in the real-world are incomplete, which involve some degree of open-endedness or

ambiguity. The literature on transactions costs highlights that incomplete contracts can cause

a non-integrated relationship to yield outcomes that is inferior compared to complete

Selen Gül The Effects of Integration Strategies on Firm Performance

10

contracts. The three fundamental factors preventing to achieve complete contracting are;

bounded rationality, difficulties specifying or measuring performance and asymmetric

information.

2.1.4. The Theory of Relational Contracts

In relation to this phenomenon of contracts, the third insight is formed by Baker et al.

(2002) indicating that “relational contracts are informal agreements and unwritten codes of

conduct that powerfully affect the behaviors of individuals within firms.” (p. 39) These

relational contracts affect the behaviors of firms in their business relations with other firms,

whether vertical or horizontal. Baker et al. (2002) underline in their study the ease of

relational contracts between and within the firms, compared to the difficulties encountered in

formal contracting. “For example, a formal contract must be specified ex ante in terms that

can be verified ex post by the third party, whereas a relational contract can be based on

outcomes that are observed by only the contracting parties ex post, and also on outcomes that

are prohibitively costly to specify ex ante.” (p. 40) Therefore, a relational contract empowers

the parties to exploit their detailed knowledge to their particular situation and to adapt this

situation to new information as it becomes available. Based on these advantages of relational

contracts, the authors are adding dynamics to the previous models and illustrate how these

dynamics will affect the vertical integration decisions by introducing game theory models

such as; trust games, repeated trust games and trigger strategies.

2.1.5. Is Vertical Integration Beneficial for the Firm?

According to Sudarsanam (2010), vertical integration increases technical efficiencies

in some ways; however arises inefficiencies in some other ways. The author describes these

technical efficiencies as coordinating, monitoring, and enforcement in the process of

production. On the other hand, interdivisional rivalry may lead to opportunism and an

increase in influence costs. Moreover, information asymmetry in integrated firms may exist

between various levels of management and divisions. “In particular, a firm that purchases its

supplier, thereby removing residual rights of control from the manager of the supplying

company, can distort the manager's incentives sufficiently to make common ownership

harmful.” (Grossman & Hart, 1986, p. 692) When the residual rights are captured by one

party, they are lost for the contrary party that may lead to distortions. On the other side, by

vertically integrating no alternative use of the good will exists, leading to a value of zero

quasi-rent and no hold-up problems (Williamson, 1971).

Selen Gül The Effects of Integration Strategies on Firm Performance

11

2.1.6. Empirical Evidence on Vertical Mergers

The efficiencies of vertical integration have been subject to be tested by several

scholars in order to illustrate why firms take parts production in-house and what types of

specificities are affecting vertical integration (Monteverde & Teece, 1982; Masten, 1984) ,

and how the duration of the contracts are affecting the choice to vertically integrate (Joskow,

1985). Monteverde & Teece (1982) have explained vertical integration by examining the U.S.

automobile industry for the two firms, GM and Ford. The study observed a significant and a

positive effect on the engineering effort and specificity coefficients, meaning that a high level

of engineering effort and the specificity of the component will more likely lead the

component to be produced in-house. “GM and Ford are more likely to bring component

design and manufacturing in-house if relying on suppliers for preproduction development

service will provide suppliers with an exploitable first-mover advantage.” (p. 212) Moreover

Masten (1984) has followed a similar approach by analyzing the variables on vertical

integration by using a sample from the U.S. aerospace industry of 1,887 aerospace

components. The author has found a significant positive effect for specialization and

complexity coefficients, in which the higher the complexity and specialization of the inputs,

the higher the probability to vertically integrate. In addition, Joskow (1985) has conducted a

study by examining the U.S. coal-burning electric generating plants in order to identify the

role of contract duration on vertical integration decisions. The author points out that the

variation in the contract duration is based on the level of relation-specific investments, in

which longer commitments are engaged where relation-specific investments are more

important. Moreover, in the studies of Fan & Goyal (2006), the authors give the basic idea of

a vertical merger as, the two industries are vertically related if one of the firms uses the

other’s output for its own production or if the firm can supply its product or services as the

other’s input. This measure can be captured by Input-Output tables and is applicable to

measure the vertical relations in large samples. Therefore, where merging firms are from the

same Input-Output industries, the merger is categorized as vertical.

Moreover Sudarsanam (2010) specifies that the empirical evidence on vertical mergers

and their value effects is rare, compared to the ones that have analyzed horizontal and

diversifying mergers. Colangelo (1995) has studied the effect of pre-emptive merging for

vertical vs. horizontal integration and underlined that the overall gain from a vertical

integration is generally greater than that from a horizontal integration. “In our context vertical

integration gives rise to three different gains: (a) it eliminates double marginalization; (b) it

Selen Gül The Effects of Integration Strategies on Firm Performance

12

enables price discrimination against non-integrated rivals; (c) it avoids the loss coming from

being non-integrated after a horizontal merger.” (p. 324) In addition, the findings of Leiblein

& Miller (2003) regarding the semiconductor industry point out that, the vertical boundary

choices are affected significantly depending on the firm-level competences and strategies. For

instance, the companies with greater experience in a specific type of technology have the

tendency to internalize the manufacturing activities than firms without such production know-

how. “Similarly, firms with high levels of sourcing experience are more likely to outsource

their production than firms that do not have such experience.” (p. 854) To sum up, firms

internalize transactions when it is expected that they will need to renegotiate supplier

contracts due to high asset specificity.

2.2.Horizontal Integration

Besanko et al. (2007) indicate that a firm’s horizontal boundaries determine the

quantities and varieties of products and services that it produces. It refers to a merger of two

or more firms producing the same good under one consolidated firm (Chakravarty, 1998).

Horizontal boundaries vary obviously across industries and across the firms within them. The

optimal horizontal boundaries of the firms are appertaining crucially to economies of scale

and scope. Economies of scale and scope exist whenever large-scale production, distribution,

or retail operations have a cost advantage over smaller operations. “Economies of scale and

scope not only affect the sizes of the firms and the structure of markets, but they are also

central to many issues in business strategy.” (Besanko et al., 2007, p. 75) Economies of scale

and scope are the essence for merger and diversification strategies. They have an effect on

entry and exit, pricing, and the capability of the firm to protect its long-term sustainable

advantage.

Sudarsanam (2010) underlines that, a number of firms in wide-ranging sectors such as

utility, electricity, banking, pharmaceuticals, insurance, oil and gas, automobiles, food and

drinks, steel and healthcare have merged with one another, in the recent years. Such mergers

are defined as horizontally related mergers. Where the firms selling the identical product

merge, it is described as a pure horizontal merger. “Where firms selling products that are not

identical in terms of end use but nevertheless share certain commonalities, such as

technology, markets, marketing channels, branding or knowledge base, merge, we refer to

such mergers as related mergers.” (p.123) For simplicity, Sudarsanam (2010) refers to the

Selen Gül The Effects of Integration Strategies on Firm Performance

13

term horizontal merger as to both pure horizontal mergers and related mergers3 of firms

selling a range of similar products. Horizontal mergers often qualify industries and markets

whose products are generally in the mature or declining stages of the production life cycle.

These markets have a low overall growth rate, and firms have accumulated production

capacity that far exceeds the demand. This combination of low market growth and excess

capacity engenders difficulties on firms to attain cost efficiencies through consolidating

mergers. Such efficiencies may be achieved from scale, scope and learning economies.

2.2.1. Economies of Scale and Scope

The origin of costs may have crucial inferences for industry structure and the behavior

of the companies. Besanko et al. (2007) denote that “the production process for specific good

or service exhibits economies of scale over a range of output when average cost declines over

that range.” (p.75) Moreover, economies of scale exist if the firm attains unit-cost savings as

it raises the production of a given good or service. In order to achieve these scale economies,

the associated costs, risks and the extent of cost savings have to be taken into notice

(Sudarsanam, 2010). Therefore, firms should be conscious about diseconomies of scale,

which arise from complexities of monitoring, diffusion of control, ineffectiveness of

communication, and numerous layers of management. In addition to these disadvantages,

Besanko et al. (2007) also underline the limits to economies of scale, in which beyond a

certain size, bigger is no longer better and may even lead to worse outcomes. The most

important reasons for these limits are; labor cost and firm size, conflicting out, spreading

specialized resources too thin, and incentive and bureaucracy effects. Moreover, economies of

scale may be more crucial for the manufacturing organizations, “since the high capital costs of

plant need to be recovered over a high volume of output.” (Johnson et al. 2008, p. 99) The

manufacturing sectors that have been generally important have been motor vehicles,

chemicals and metals. In terms of distribution and marketing other industries such as drinks,

tobacco and food, the scale economies would be crucial (Johnson et al. 2008).

Economies of scope exist, if an increase of production in the variety of goods and

services saves the firm from the costs it bears. “Whereas economies of scale are usually

defined in terms of declining average cost functions, economies of scope are usually defined

in terms of the relative total cost of producing a variety of goods and services together in one

firm versus separately in two or more firms.” (Besanko et al., 2007, p. 76) In other words,

Panzar & Willig (1981) point out to the existence of economies of scope where it is less

3 This paper will handle related diversification under the term ‘horizontal integration’.

Selen Gül The Effects of Integration Strategies on Firm Performance

14

costly to merge two or more product lines in one firm compared to supplying them separately.

Based on the definitions above, scope economies are available only for multi-product firms.

Certainly, both economies may be recognized by the increase of the output of individual

products as well as the total output of all the firm’s products. The research on the extent of

scope economies is scarce, in contrast to the literature on scale economies. One possible

explanation is that until recently product costing did not allocate costs to the different

products correctly, based on the related activities. Activity-based costing (ABC) mitigates this

issue; however the problem of how to compare these product costs in the merged firm with

the costs on the similar products produced separately by different companies still exists

(Sudarsanam, 2010).

2.2.2. The Learning Economy

Experience is an important determinant to fulfill the tasks faster and attain the output.

The magnitude lies under the idea of the learning curve. Besanko et al. (2007) determine that

economies of scale points out to the advantages that flow from increase in production to a

larger output at a given point in time. “The learning curve refers to advantages that flow from

accumulating experience and know-how.” (p. 94) Sudarsanam (2010) specifies that the

economy of learning comes to light when workers and managers become more experienced

and effective over time in using the available resources of the firm, and help decrease the cost

of production. “The time required to do a job will decrease each time the job is done, that the

time per unit will decrease at a decreasing rate, and that the time reduction will be

predictable.” (Lindsey & Neeley, 2010, p. 73) It is a function of cumulative output over

several periods, and increasing cumulative output raises the motivation to learn more efficient

and effective ways of producing each unit of the output for the managers and workers.

Employees learn not only from their personal experience but also from that of their

colleagues. The limit to learning and its affect on cost reduction is designated by the minimum

efficient learning scale (MELS). At this level, maximum learning has been procured (Besanko

et al., 2007).

Based on the studies conducted, the semiconductors and aircraft production are some

of the industries that the learning economy may be more crucial. The learning rates averaged

about 20 to 40 percent respectively. Learning curve efficiency entails that the firms have a

large sales quantity and therefore a relatively large market share. “Therefore, the cost of

acquisition of the increased market share needs to be balanced against the subsequent cost

savings from increased learning efficiency.” (Sudarsanam, 2010, p. 138) Moreover, Besanko

Selen Gül The Effects of Integration Strategies on Firm Performance

15

et al. (2007) emphasize that learning occurs at different rates for different organizations and

processes, according to the variation in slopes across firms and products. Although

organizational learning is highlighted as the essence of the process, primarily it is individuals

who learn. While individuals do the learning, the firms can take the steps to enhance learning

and the maintenance of knowledge in the organization.

Horizontal mergers lead to the consequence of a sudden increase in the quantity of

output when the output of each merging firm is combined. While each firm has the

opportunity to learn from the experience of the other firm, this learning may not engender the

cumulative output of the merged entity to increase more. In the period subsequent the merger

this output may increase, hence creating opportunity for further learning. However, if the

output of the merged company is already large, it is expected to have passed the minimum

efficient learning scale (MELS) of cumulative output (Sudarsanam, 2010). For instance,

“mergers involving complex technological processes such as drug discovery may yield

potentially valuable learning opportunities, but they are also problematic because of the

coordination and management problems.” (p. 139)

2.2.3. Empirical Evidence on Horizontal Mergers

Lipczynski et al. (2005) signify that the empirical evidence on the increased

profitability through increased market power or cost savings of horizontal mergers is rather

conflicting and inconclusive. For instance, Cosh et al. (1980) examine 211 mergers in the UK

between the years 1967 and 1969, comparing profitability during a five-year period before the

merger, with profitability during the five years subsequent the merger. The merged firms are

observed to have experienced an increase in average profitability. On the contrary, Meeks

(1977) detects a fall on average profitability during the seven-year period following the

merger in a study of mergers in the UK between 1964 and 1972. In addition to these studies,

Ravenscraft & Scherer (1987) examine the pre-merger profitability of 634 US target firms in

the late 1960s and early 1970s. The target firms’ profitability (the ratio of operating income to

assets) was observed to be 20 percent, which is much greater than the average profitability of

all firms of 11 percent.

Moreover, Weiss (1965) inspects the impacts of horizontal mergers on seller

concentration for six manufacturing industries for the period 1926-1959. “Changes in

concentration ratios over approximate 10-year intervals are decomposed into effects arising

from the internal growth of firms, the exit of incumbent firms, mergers, and turnover or

changes in the identity of the largest firms in each industry.” (Lipczynski et al., 2005, p. 263)

Selen Gül The Effects of Integration Strategies on Firm Performance

16

Therefore, internal growth and exit seem to have a more crucial role than mergers in affecting

the changes in concentration.

Finally, Colangelo (1995) underlines the gains from horizontal integration as: it leads

to an increase in the market power due to the internalization of the cross-price effect on

demand, and it prevents the loss coming from being non-integrated after a vertical integration.

2.3.Diversification

The incentive and consequences of diversification on firms has been committed to a

vast amount of studies by both economists and business researchers. However, these two

groups approached the phenomenon from different perspectives. “Economists have treated the

extent of a firm’s diversification as determined by structural variables in the industries in

which the firm operated and the economics of the organization of activity within the firm

operated and the economics of the organization of activity within the firm compared to via the

market.” (Lecraw, 1984, p. 179) On the other hand, business researchers have paid attention

on the human and physical assets of the firm, by taking its internal strengths and weaknesses

into consideration in determining its diversification strategy. This paper will have the focus of

the economists’ perspective in identifying the companies’ diversification strategies, in which

the structural variables of the industry and the activity of the firm within this industry will be

highlighted.

Lipczynski et al. (2005) define a diversified firm or a conglomerate as; to being

involved in the production of a number of various goods and services, making it a multi-

product firm. According to the authors, the types of diversification can take the forms as

product extension, market extension and pure diversification. Product extension would be

achieved if a firm can diversify by producing a new product that is strongly related to its

existing products. Market extension involves diversifying into a new geographic market with

the same line of products, and a pure diversification strategy involves a transition into

unrelated areas of business activity. Rumelt (1982) depicts the first and the last components of

the strategies respectively as related4 and unrelated business companies.

Lipczynski et al. (2005) further indicate two ways in which a diversification strategy

can be performed; either through internally generated expansion, or through mergers and

acquisitions. “Conglomerate merger involves the integration of firms that operate in different

product markets, or in the same product market but in different geographic markets, whereas

internally generated expansion is likely to require the simultaneous extension of the firm’s

4 Recall that this paper takes “related diversification” strategy under the name of horizontal integration.

Selen Gül The Effects of Integration Strategies on Firm Performance

17

plant and equipment, workforce and skills base, supplies and raw materials, and the technical

and managerial expertise of its staff.” (p. 593) Diversifying through a conglomerate merger

may be less demanding in this matter.

2.3.1. Product Diversification

As indicated above, the strategies of related and unrelated integration are defined

under product diversification. Although this paper will refer to the concepts as horizontal

integration and unrelated integration strategies, it is worth mentioning this broad definition

and its performance effects. Ravichandran et al. (2009) notes that, product diversification

which illustrates the scope of the multiple and distinct product markets that the firm is

operating in, has been lately under the focus of strategic management researchers. Geringer et

al. (2000) indicate “the relationship of performance and the product mode of diversity is well

established by studies in two related directions — type of diversification and degree of

diversity.” (p. 54) Rumelt (1974) found differences across his “relatedness” categories, in the

seminal study of qualitative types of diversification. The author divided the integration

strategies into 7 categories; which were single business, dominant vertical, dominant

constrained, dominant linked-unrelated, related constrained, related linked and unrelated

business. In order to specify the strategy that a company possesses, Rumelt (1974)

constructed intervals of ratio specification. Based on these intervals of ratios (specialization

ratio, related-core ratio, related ratio and vertical ratio) the companies’ strategies were

specified. Following studies using his methodology have generally underlined that related

diversification generated higher performance levels than unrelated diversification, although

industry effects and other firm-level variables tend to eliminate much of the effect of the

diversification type. Therefore, the general outcome of the studies is that related

diversification is associated with a profitability advantage (Geringer et al., 2000).

2.3.2. Geographic Diversification

Geographic diversification is identified as the firm’s expansion into various

geographic locations or markets across the borders of regions and countries (Hitt et al., 1997).

“Thus, a firm's level of international diversification is reflected by the number of different

markets in which it operates and their importance to the firm (as measured, for instance, by

the percentage of total sales represented by each market).” (p. 767) This type of

diversification strategy has its motivations as well as downsides. Denis et al. (2002) identify

several motivations as; global diversification is a mechanism that combines the information-

Selen Gül The Effects of Integration Strategies on Firm Performance

18

based assets of buyers and sellers within the same firm. It generates value by creating

flexibility within the firm, by giving the ability to respond to changes in relative prices. In

addition, investors’ diversification choices can result as the benefit of geographic

diversification. Ravichandran et al. (2009) adds the scope and scale economies, enhanced

market power, and the ability to supply lower-cost factor inputs to the benefits of global

diversification. Moreover, “increased operational flexibility by global diversification reduces

the risks across the markets.” (Kim & Mathur, 2008, p. 749) However as from the downside

perspective, a globally diversified entity is more complex compared to a purely domestic

firm. The costs of information asymmetry between corporate headquarters and the difficulty

of monitoring managerial decision-making may give rise (Denis et al., 2002).

Based on the empirical studies conducted, Ravichandran (2009) and his colleagues

specify that, “multinational corporations (MNCs) experienced a positive valuation effect

relative to purely domestic firms because of their role as financial intermediaries.” (p. 210)

Moreover, Lepetit et al. (2004) illustrate that the announcements of the mergers and

acquisitions beyond regions and countries have a positive effect on the market. On the other

hand, the effect on firm performance may be negative due to high transaction costs and

managerial-information processing demands. Moreover, Delios & Beamish (1999) have

found a positive relationship between the geographic scope and firm’s performance by

collecting a data of 399 Japanese manufacturing firms. Their findings illustrate that expanding

into new geographic markets is an effective strategy for developing the performance of

Japanese companies. However, in the study of Kim & Mathur (2008) where a sample of

28,050 firm year observations from 1990 to 1998 was used, a firm value decrease was

associated for both industrial and geographic diversification. “We find that geographically

diversified firms have higher R&D expenditures, advertising expenses, operating income,

ROE and ROA than those of industrially diversified firms.” (p. 764)

2.3.3. The Determinants and Motives for Diversification

In exploring the determinants of diversification, Rondi et al. (1996) focuses on three

theories of diversification. The first, attributed to Marris (1964) and Penrose (1995), propose

that the managers seek to maximize the growth of the firm. The operation of specific assets

such as marketing skills and technical enterprise in other industries offers a convenient

vehicle in order to achieve the growth objective. The second theory attributed to Bain (1959),

puts emphasis on the conditions that yield entry possible or attractive. These incorporate

industry-level characteristics such as growth and concentration, average profitability, as well

Selen Gül The Effects of Integration Strategies on Firm Performance

19

as barriers to entry. The third theory, attributed to Rumelt (1974) and Williamson (1975),

focuses on relatedness between industries that makes diversification attractive, in which

relatedness refers to the similarities between markets, technologies, and organizational

structures (Lipczynski et al., 2005). The scope of this paper generally refers to the third theory

where relatedness is the underlying concept.

As mentioned above under the heading of horizontal boundaries, related

diversification represents the horizontally integrated mergers. Therefore, this part will

consider the value creation for the acquisitions of unrelated businesses. Sudarsanam (2010)

underlines the motives of value creation as having an increased market power or operating an

efficient internal capital market. “Market power is the ability of a firm in a market to pursue

anticompetitive behavior against its current rivals or potential entrants.” (p. 184) This power

is not obtained from the monopoly position in that market, but from the range of the firm’s

activities and its size. Based on this market power, the conglomerates assign investment funds

to a wide range of individual entities. If these entities were stand-alone, independent firms,

their funds would be supplied directly from the capital markets. Thus, the conglomerate firm

serves the role of capital markets. The firm will create value, in case it possesses an effective

performance compared to the external capital market. Moreover, Lipczynski et al. (2005)

add more motives such as; saving costs, reduction of transaction costs and the managerial

motives for diversification.

2.3.4. The Resource-Based View

A vast amount of the management literature on diversification follows the resource-

based view of the firm. “The resource view argues that rent-seeking firms diversify in

response to excess capacity in productive factors, here called resources.” (Montgomery, 1994,

p. 167) Under this perspective, firms acquire companies to keep the balance among the

required competitive profile and competences, and their current endowments of resources.

However, the amount of resources available are limited, therefore firms are not limitless in

their ability to pursue new investment opportunities (Wiersema & Bowen, 2008). Apart from

this limitation, conglomerate acquisition may be undertaken by the same motives for

acquiring competitive profile and competences. Other reasons may be the need for growth,

and to utilize the excess capacity the firm possesses. These idle resources should be reused in

more productive and profitable areas. Therefore the question to be answered is, how best the

firm can exploit these resources outside of its current operations. In the book of Silverman

(2002), three sets of factors are pointed out as the firm’s diversification behavior. Initially is

Selen Gül The Effects of Integration Strategies on Firm Performance

20

the specific range of applications to which the firm’s current resources may be useful. These

depict the possible set of businesses in which the firm’s resource base will provide

competitive advantage. The second is the scope of transaction costs in the relevant markets

for the firms existing resources. These determine the firm’s ability to exploit its resources

through contractual arrangements, which can prevent the need for expansion of the firm’s

boundaries. The third set of factors deal with the sustainability of the competitive advantage

furnished by the firm’s resources. For the reason of prioritization, a firm will decide on to

focus first on the exploitation of those resources that offer the most sustainable competitive

position, since it cannot use all of its resources at once. Finally, “in order to generate

sustainable competitive advantage, it has been argued that firms’ resources and capabilities

should be rare, valuable, difficult to imitate, non-substitutable and non-transferable in that

they cannot be easily purchased in resource markets.” (Matraves & Rondi, 2007, p. 38)

2.3.5. Diversification and Firm Performance

Firm diversification has been extensively researched both empirically and

theoretically in the fields of strategy and finance for more than 30 years. The literature on

diversification generally focuses on the economic rationale behind the diversification-

performance relationship, and the main common objective of this work has been to verify the

effect of diversification on the creation or destruction of firm value. Thus, the researches’

center of attention has been on the performance of the diversified firms compared to

specialized firms (Santalo & Becerra, 2008).

Many researchers have studied the effects of operating performance on diversified

firms compared to undiversified, which is measured by accounting profits or productivity.

They have found the relationship between performance and corporate diversity to be

ambiguous. “Profits were more likely to be determined by industry profitability, coupled with

how the firm related new businesses to old ones, rather than diversification per se.”(Besanko

et al., 2007, p. 180)

Ravichandran et al. (2009) specify that firms may choose to diversify into related or

unrelated markets, based on the similarity or relatedness of the new business. “Related

diversification is believed to lead to better performance than unrelated diversification because

the former leverages significant business synergies while the latter suffers from agency costs

and inefficient resource allocation.” (p. 206) This belief has been widely studied by many

scholars. Prahalad & Bettis (1986) explain this logic more in depth, by indicating the four

major and nine minor categories that Rumelt (1982) has used to identify the diversification

Selen Gül The Effects of Integration Strategies on Firm Performance

21

strategies of the firms. The major categories are to be single business, dominant business,

related business and unrelated business. Rumelt (1982) has used statistical models to relate

diversification strategy to performance and pointed out that capital productivity is greater in

moderately diversified firms. However the firms in between moderate and high levels of

unrelated diversification acquired moderate or poor productivity. In other words, on the

average related diversification strategies outperformed the other diversification strategies. On

the other side, the unrelated business strategy was observed to be the lowest performing

(Prahalad & Bettis, 1986, p. 486). Moreover, “Noel Capon (1988) and his colleagues found

that firms that restricted their diversification to narrow markets performed better than did

broader firms, presumably because of their learning particular market demands.” (Besanko et

al., 2007, p. 180) Although the theoretical and empirical findings on the area of diversification

are quite rich, the results have not been consistent. Despite the inconclusive results,

diversification has been an effective firm strategy for growth (Ravichandran et al., 2009).

Lately, Nathanson & Cassano (1982) conducted a statistical study of diversity and

performance with a sample of 206 firms through years 1973 and 1978. They utilized two

factors which are market and product diversity to distinguish the diversification strategy that

improves Rumelt’s categories. The findings illustrated that, an increase in product diversity

decreased the average returns, whereas the returns remained rather stable for an increase in

market diversity. Also, they discovered that size plays a crucial role on the relationships. “For

both the market and product diversity, smaller firms did well relative to larger firms in

categories marked by no diversification and in categories of extremely high diversification,

and larger firms did significantly better than smaller firms in the in-between categories—

those characterized by intermediate levels of diversification.” (Prahalad & Bettis, 1986, p.

486) In both these studies of Rumelt (1982) and Nathanson & Cassano (1982), the key point

is to decide on the generic strategy of diversification (the level of relatedness) in order to

achieve performance (Prahalad & Bettis, 1986). According to this phenomenon Kiker &

Banning (2008) support that, diversification is an issue of creating fit with the most

significant contingencies and an effective fit will improve the overall performance of the firm.

According to this view, diversification does not necessarily lead to increased overall firm

performance; rather it relies upon how effective the diversification fits the particular

contingencies of the firm. “Research from this perspective has generally found that this occurs

to the extent that firms diversify only in a direction which is related to their core

competencies.” (Kiker & Banning, 2008, p. 20)

Selen Gül The Effects of Integration Strategies on Firm Performance

22

2.3.6. Empirical Evidence on Diversification and Firm Performance

A vast number of researches have been conducted in order to examine the relationship

between diversification and firm performance, by utilizing industry structure variables like

concentration, scale, industry growth, etc. In these studies, accounting indices, such as return

on equity or return on invested capital have been generally used to measure performance. The

common measure for diversification has been the Herfindahl index; for instance, one minus

the sum of the squared percentages of a firm's total revenues in each of its markets. “These

studies nearly always find a neutral or negative, not a positive, relationship between

diversification and firm performance.” (Montgomery, 1994, p. 169) Montgomery &

Wernerfelt (1988) and Lang & Stulz (1994) presented a similar analysis using Tobin's q, from

the perspective of the stock price performance (the capital market value of the firm divided by

the replacement value of its assets) to measure performance. Their findings illustrated a

reduction on the firms’ profitability as the level of diversification increased (Montgomery,

1994). In other words, “highly diversified firms are consistently valued less than specialized

firms.” (Lang & Stulz, 1994, p. 1278)

Schoar (2002) has examined the effect of productivity on firm performance and found

that diversification has caused to a destructive ‘new toy’ effect. “While the newly acquired

plants increase their productivity by three percent, incumbent plants show productivity

declines of almost two percent.” (p. 2380) This study is also supported by Lichtenberg (1992)

who underlines the fall of the productivity of plants as the level of diversification increases

(Schoar, 2002).

Ravichandran et al. (2009) focused on the effects of IT technology spending to

product and geographic diversification and firm performance. They have defined the firm

profitability by using the accounting-based measure of return on assets (ROA) and the

measure of Tobin’s q for firm valuation. The authors’ concluding remarks were; IT needs to

be viewed as a valuable asset by the managers in highly diversified firms, based on the

performance critical role when implemented with diversification. However, they must be

attentive that the impacts on performance are dependent on types of diversification. “In firms

with unrelated product diversification or with high geographic diversification, IT may not

contribute to performance as much as in related diversifiers and in low geographic

diversification contexts.” (p. 233) These findings are also supporting the work of Miller

(2006), which specifies the greater value creation from technological diversity of the multi-

business firms compared to single-segment firms, and the greater performance of diversified

as technological diversity increases.

Selen Gül The Effects of Integration Strategies on Firm Performance

23

Another perspective in assessing the performance-diversification linkage is

highlighted in the study of Santalo & Becerra (2008), in which this linkage is examined by

differentiating the industries. Their evidence illustrates that the effect of diversification on

performance is not homogenous across industries. “Diversified firms observe a diversification

discount if and only if they compete in industries with a large number of single-segment

companies or, equivalently, when specialists hold a considerable market share.” (p. 851) On

the other hand, industries that bear only a few non-diversified firms competing, leads the

diversified firms enjoy a premium in those industries in which specialists acquire a small

market share.

In addition, Bettis (1981) has conducted a study using a sample of 80 firms, in order to

investigate the performance differences between related and unrelated diversified firms. By

regressing the return on assets to advertising, R&D, plant investment, size, risk and

diversification strategy, the author concluded that, on average related diversified firms

perform better than unrelated diversified firms by about one to three percentage points of

return on assets.

Moreover, Denis (2002) and his colleagues examined the effects of global and

industrial diversification on the firm value, by using a sample of 44,288 firms through years

1984 and 1997. The findings highlight an increase in global diversification over time, whereas

a reduction for industrial diversification. However both global and industrial diversification is

associated with valuation discounts, which are statistically significant compared to purely-

domestic firms. Moreover, the authors have found no evidence of tendency to replace the

global diversification strategy for industrial diversification by the individual firms.

Finally, Capar (2009) examined a sample of 196 firms through years 1995-2000,

based on the effects of international and product diversification on innovation assets and firm

performance. The results are found to be significant for the effects of international

diversification on innovation assets and a negative effect for an increase of product

diversification. Therefore, “the present study provided strong evidence that innovation assets

lead to higher performance.” (p. 6)

Selen Gül The Effects of Integration Strategies on Firm Performance

24

3. DEVELOPMENT OF HYPOTHESES

Based on the prior research on the effects of the integration strategies on firm’s

performance, this section outlines the hypotheses that are subject to be tested. This paper will

focus on the two industries (manufacture of food products and manufacture of machinery and

equipment) out of the 5 industries in computing the regression models, due to the

adequateness of the amount of data. In order to examine if the results obtained will be related

to the previous studies, two separate hypotheses have been developed for manufacture of food

products and manufacture of machinery and equipment industries respectively.

Bettis & Hall (1982) underline the importance of the differences among industries.

Since this paper is analyzing the effects of the integration strategies by differentiating the

industries that the firms compete in, it is crucial to note that “the different industries have

different structural characteristics (in the industrial organization economics sense), and these

different structural characteristics result in different average (and potential) profits in each

industry.” (Bettis & Hall, 1982, p. 255) In relation to this phenomenon, it is expected that the

effects of the integration strategies on firm’s profitability may vary among the industries.

Moreover, Besanko et al. (2007) ask the question of whether they will encounter considerable

differences in profitability of business units within industries and a modest variation in

profitability across the industries. “If so, the effect of the market environment on profitability

is unimportant, but the effect of a firm’s competitive position in the industry is important.” (p.

349) The question can be asked vice versa, and the authors conclude that both the market and

the firm’s competitive position in the industry can explain profitability. McGahan & Porter

(1997) indicate that the industry is responsible for about 19 percent of the variation in profit

across industries, whereas the percentage is 32 for the business-specific effects.

In relation to these differences, the effects of the integration strategies can be tested

based on the theories presented above. Prior research indicates that, in order to prevent the

hold-up problem, firms tend to vertically integrate when their investment incentives are more

crucial compared to the counter party’s incentives (Grossman & Hart, 1986). Since the firms

tend to internalize their transactions in order to avoid the renegotiations of contracts and

investing huge amounts on the relation-specific assets, the following hypothesis is formed:

H1: Vertical integration strategies have a positive effect on firm’s performance.

The findings of the early studies of Rumelt (1982) designate that firms were different

not only in terms of their product diversity but also in the patterns of relationships they

created among various lines of businesses. Moreover, the different types of strategies of

Selen Gül The Effects of Integration Strategies on Firm Performance

25

diversification were associated with differing corporate profitability based on the strategy

chosen. “The highest levels of profitability were exhibited by those having a strategy of

diversifying primarily into those areas that drew on some common core skill or resource.” (p.

359) On the other hand, the lowest levels were those of vertically integrated businesses and

firms following strategies of diversification into unrelated businesses (Rumelt, 1982).

Besides the findings of Rumelt, the general empirical evidence has a strong support in

highlighting the related diversified firms are outperforming the unrelated diversified

companies (Montgomery, 1994; Lang & Stulz, 1994; Bettis, 1981). For instance, Chang &

Wang (2007) have examined a sample of 2,402 U.S. firms through years 1996 to 2002, and

found strong support that related product diversification leads to positive performance effects.

“Conversely, unrelated product diversification not only has a weaker influence than related

product diversification, it actually damages the performance of multinational firms” (p. 77)

Since this paper takes the related diversification strategy under the definition of ‘horizontal

integration’ the second hypothesis will be:

H2: Horizontal integration strategies outperform unrelated diversification strategies.

Based on the value-reducing and enhancing effects of global diversification, the prior

studies indicate conflicting evidence of geographic diversification on the firm’s value.

Researchers found that wide-ranging multinational operations were associated with higher

performance (Delios & Beamish, 1999; Hitt et al., 1997) and lower levels of risk. “However,

given that international operations encumber a firm because of the increased difficulty and

costs found in operating in foreign markets, it remained a question whether the higher

performance of multinational firms was attributable to a firm’s possession of superior

resources (i.e. proprietary assets5), or to other benefits of international operations.” (Delios &

Beamish, 1999, p. 723) The third hypothesis will test the positive aspect of geographic

diversification, taking into account that the geographically diversified firms have higher

values of performance measures such as operating income and ROA, compared to industrially

diversified firms ( Kim & Mathur, 2007).

H3: Geographic diversification has positive effects on firm’s performance.

5 Proprietary asset, usually, is any asset that is considered in the realm of intellectual property that should not be disclosed. These assets may include trade secrets and undisclosed inventions (VentureLine).

Selen Gül The Effects of Integration Strategies on Firm Performance

26

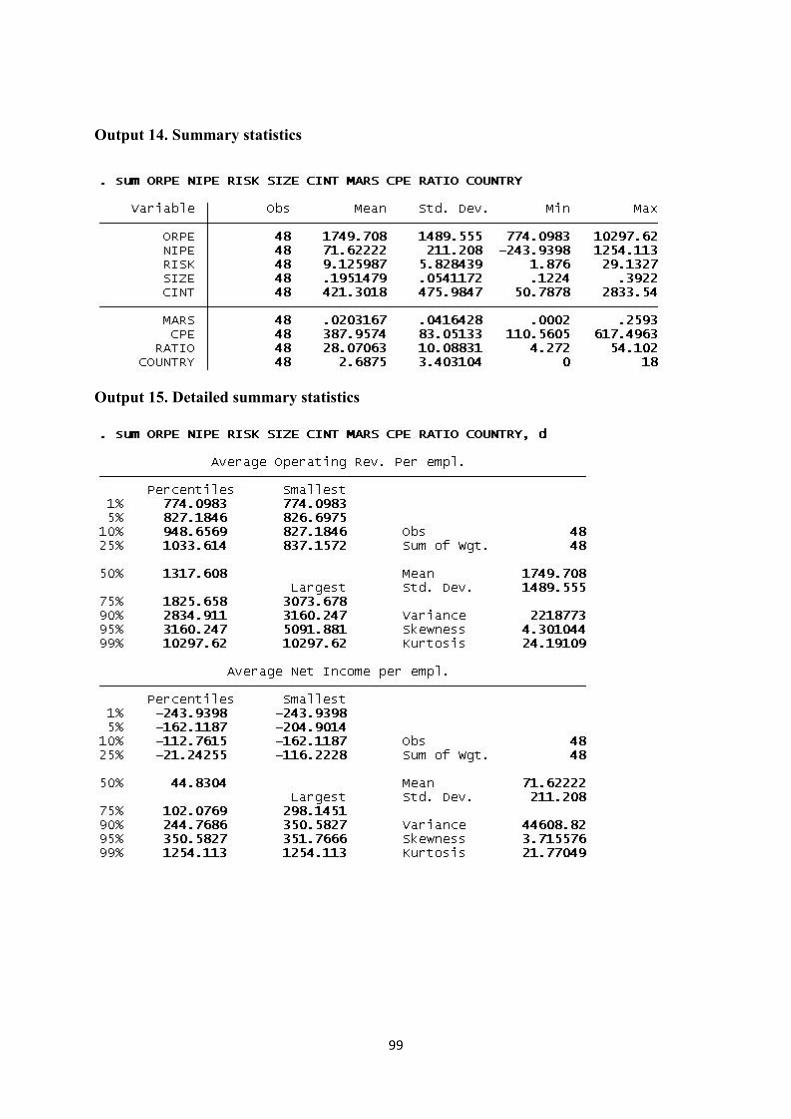

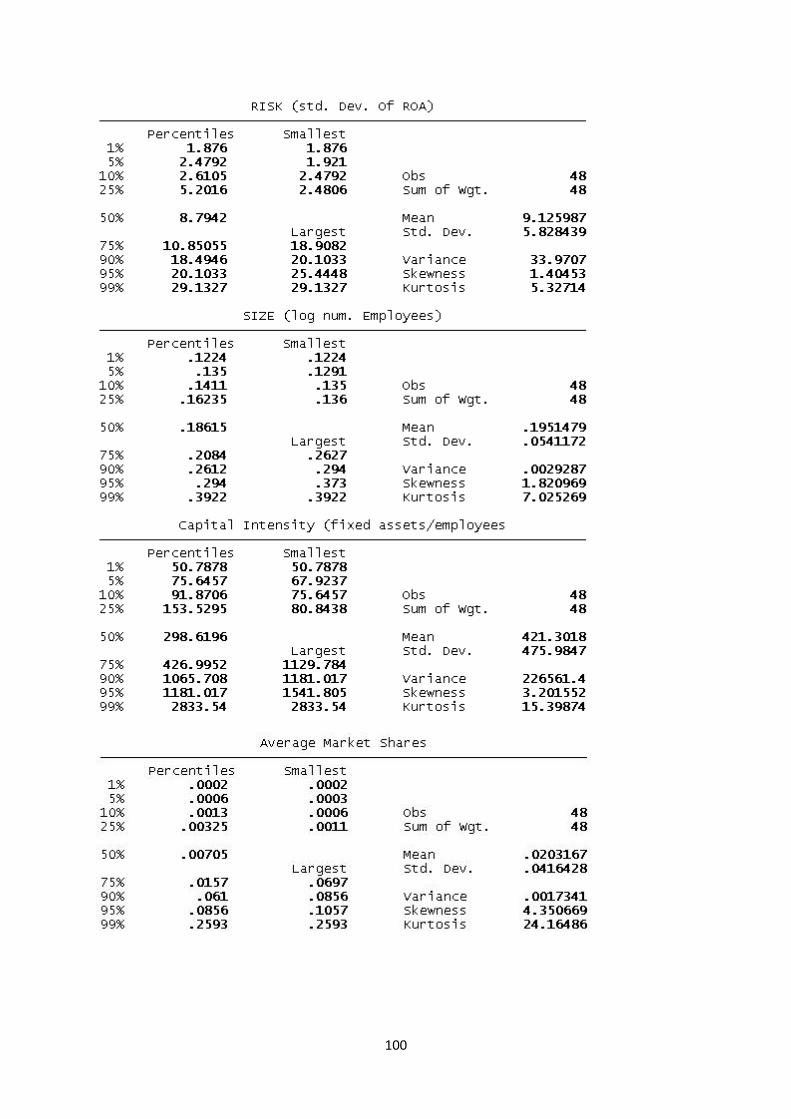

4. METHODOLOGY The study involves the analysis of 147 Danish firms between the years 2005-2009,

based on the 5-year average values. The recent empirical studies mostly focus on market share

prices and event studies in analyzing the diversification-performance linkage, whereas this

paper will focus on the operating performance perspective. Performance is measured as

operating revenue per employee (ORPE) and net income per employee (NIPE), which are

used as the dependent variables. The independent variables would be horizontal integration

(HI), vertical integration (VI), unrelated diversification (UR) and un-diversification (UD)

strategies which were explained with binary (dummy) variables that take on the values 1 and

0 depending on the type of strategy. Moreover, the analysis will examine the effects of global

diversification (COUNTRY) by focusing on the number of subsidiaries. Control variables

involve the firm specific characteristics such as: risk (RISK), size (SIZE), capital intensity

(CINT), market share (MARS), cost per employee (CPE) and the ratio of the cost of

employee to operating revenue (RATIO). Apart from these measures, this study has

conducted the Herfindahl index, entropy measure, concentration ratio and the relative measure

for the four largest firms in order to illustrate how concentrated and diversified the industries

are. These measures will not be included in the regression analysis, since the concentration

indices are calculated for all the years (2009-2005) rather than computing averages.

The analysis will begin by distinguishing each of the 5 industries and presenting their

descriptive statistics. This separation is crucial, since a computation of the summary statistics

of the whole sample would be misleading based on the differences among the industries.

In addition to these summary statistics, the study will present two regression models

with the inclusion and exclusion of the interaction effects (Bettis, 1981). The data for the

regression analysis will be conducted for only two industries separately, due to having

sufficient number of companies. These industries would be the manufacture of food and the

manufacture of machinery and equipment industries, with 54 and 48 companies respectively.

It will be designed to explore the performance differences between vertically integrated,

horizontal integrated, unrelated diversified and un-diversified firms. The models will be

estimated with the simple OLS regression, by conducting for ORPE and NIPE performance

measures separately. Below the models are briefly identified:

Model without the interaction effects: ORPE = β0 + β1 (SIZE) + β2 (RISK) + β3 (CINT) + β4 (MARS) + β5 (CPE) + β6 ( RATIO) + β7 (COUNTRY) + β8 (VI) + β9 (HI) + β10 (UR) + e

Selen Gül The Effects of Integration Strategies on Firm Performance

27

NIPE = β0 + β1 (SIZE) + β2 (RISK) + β3 (CINT) + β4 (MARS) + β5 (CPE) + β6 ( RATIO) + β7 (COUNTRY) + β8 (VI) + β9 (HI) + β10 (UR) + e In this model VI, HI and UR are dummy variables, in which the un-diversification

variable is excluded from the model. "This was done since if all the binary variables are

included, the normal regression equations are not independent and thus not have a unique

solution." (Bettis, 1981, p. 384) Therefore, β0 embraces the effects of the un-diversification

strategy (Bettis, 1981).

The second model includes the interactive terms in order to explore more the reasons

for differences in performance effects between different diversification strategies. In this type

of model the forward stepwise regression procedure was used (Bettis, 1981), in order to

“include every potentially useful predictor in the model and then delete those terms not

making significant partial contributions at some pre-assigned significance level.” (Agresti &

Finlay, 1997, p. 528) The forward selection begins with none of the variables and adds one

variable at a time to the model until it reaches a point where an inclusion of the remaining

variable does not make a significant contribution in predicting Y. In order to further modify

the forward selection, stepwise regression leaves the variables out from the model, in case

they lose their significance as other variables are added. Therefore, a variable previously

entered into the model at some point may be eliminated due to the overlap with other

variables that have entered at later stages (Agresti & Finlay, 1997). The interactive regression

model to be tested under this forward stepwise procedure is constructed as follows6: