The Early Days of Disruption: the Online Insurance Industry

16

PRODUCED BY ALAN ALDEN I SERIES-A PARTNERS LLC The Early Days of Disruption: t he Online Insurance Industry Produced By: Alan Alden [email protected] @SeriesAPartners www.series-a.com

-

Upload

alan-tikwart-alden -

Category

Internet

-

view

487 -

download

1

Transcript of The Early Days of Disruption: the Online Insurance Industry

PRODUCED BY ALAN ALDEN I SERIES-A PARTNERS LLC

The Early Days of Disruption:

the Online Insurance Industry

Produced By:

Alan [email protected]

@SeriesAPartners

www.series-a.com

PRODUCED BY ALAN ALDEN – SERIES-A PARTNERS

Page 2

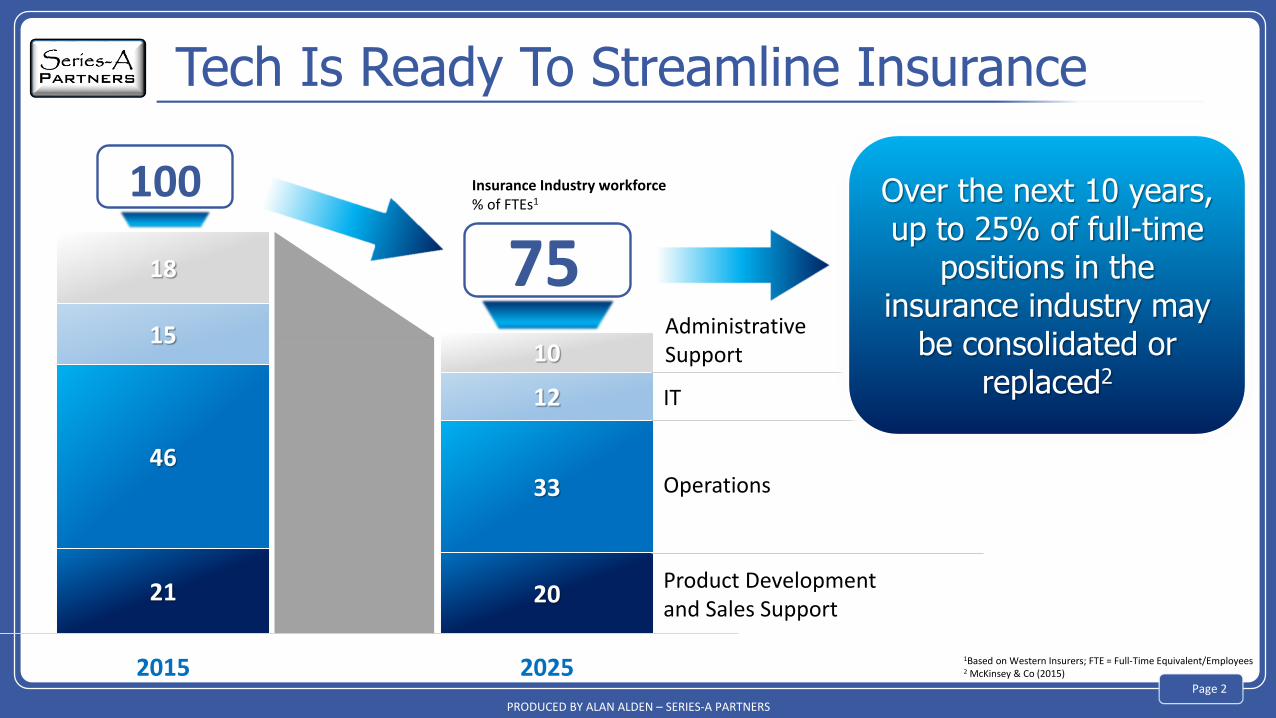

21 20

4633

15

12

18

10

2015 2025

100

Product Development and Sales Support

Operations

Administrative Support

IT

Insurance Industry workforce% of FTEs1 Over the next 10 years,

up to 25% of full-time positions in the

insurance industry may be consolidated or

replaced2

1Based on Western Insurers; FTE = Full-Time Equivalent/Employees2 McKinsey & Co (2015)

Tech Is Ready To Streamline Insurance

75

PRODUCED BY ALAN ALDEN – SERIES-A PARTNERS

Page 3

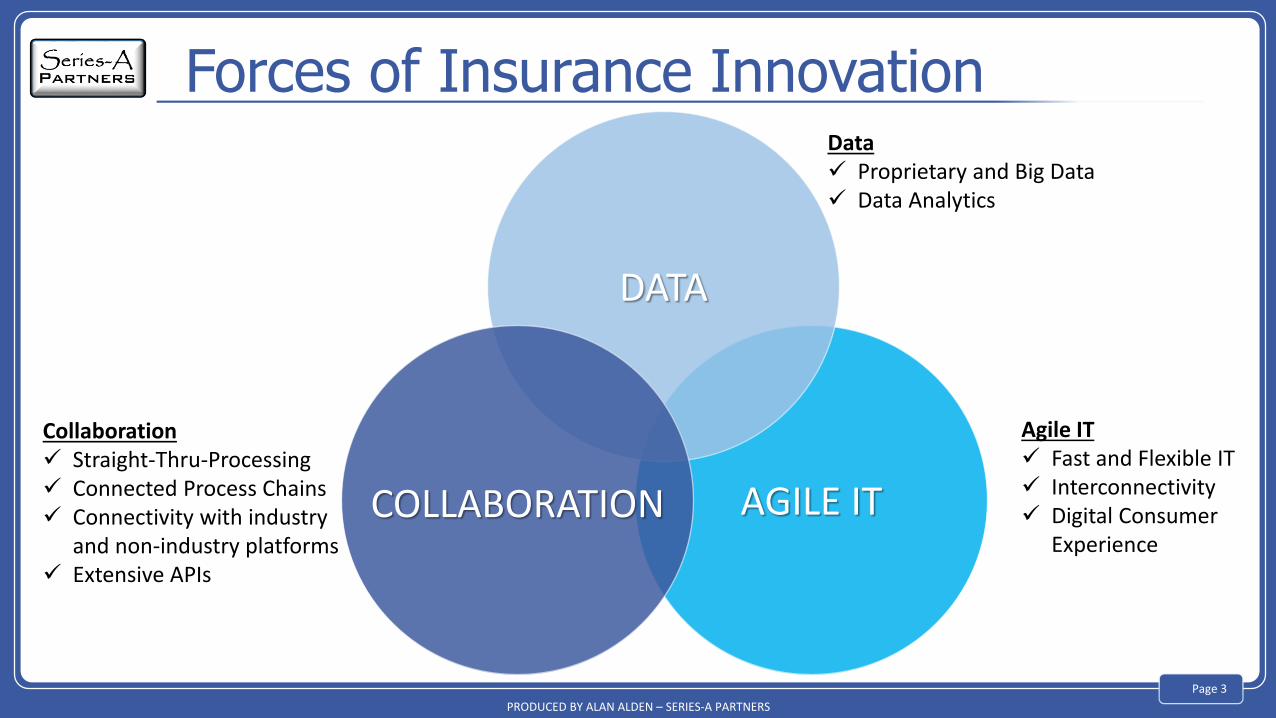

Forces of Insurance Innovation

AGILE IT

DATA

Data Proprietary and Big Data Data Analytics

Collaboration Straight-Thru-Processing Connected Process Chains Connectivity with industry

and non-industry platforms Extensive APIs

Agile IT Fast and Flexible IT Interconnectivity Digital Consumer

Experience

COLLABORATION

Page 4

PRODUCED BY ALAN ALDEN I SERIES-A PARTNERS LLC

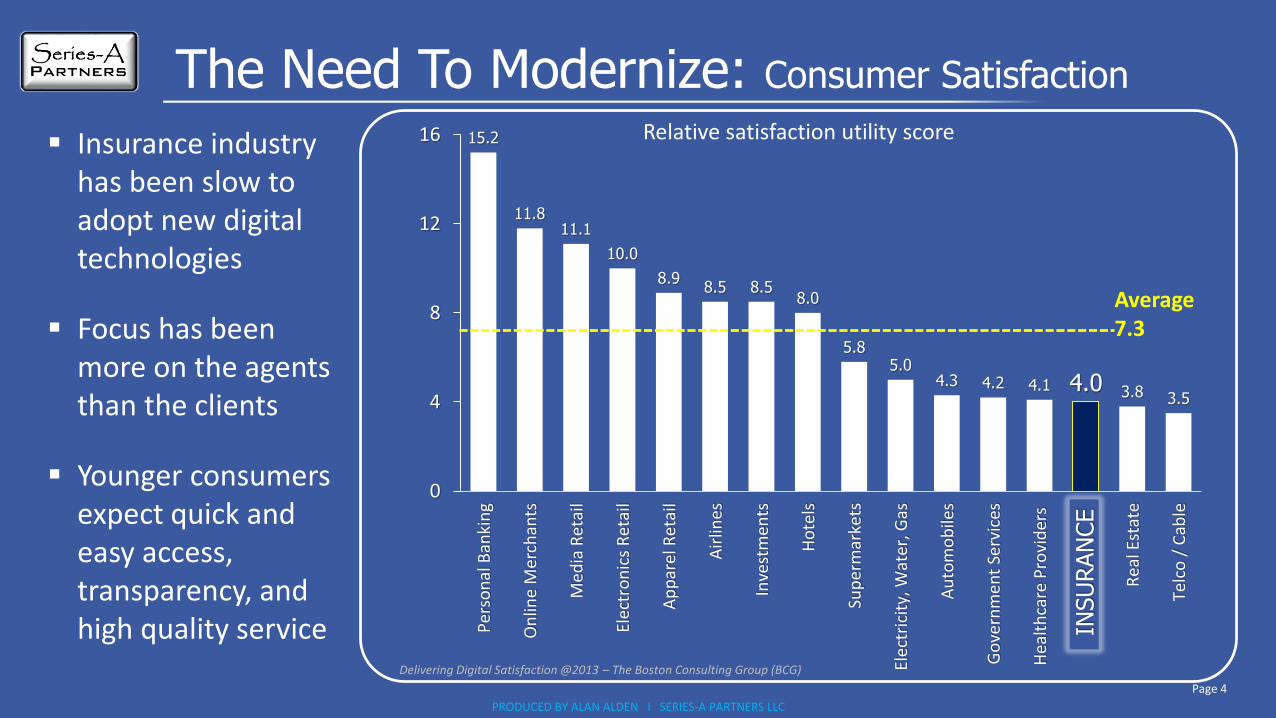

The Need To Modernize: Consumer Satisfaction

Insurance industry has been slow to adopt new digital technologies

Focus has been more on the agents than the clients

Younger consumers expect quick and easy access, transparency, and high quality service

15.2

11.811.1

10.0

8.98.5 8.5

8.0

5.85.0

4.3 4.2 4.1 4.0 3.8 3.5

0

4

8

12

16

Per

son

al B

anki

ng

On

line

Mer

chan

ts

Med

ia R

eta

il

Elec

tro

nic

s R

etai

l

Ap

par

el R

etai

l

Air

lines

Inve

stm

ents

Ho

tels

Sup

erm

arke

ts

Elec

tric

ity,

Wat

er, G

as

Au

tom

ob

iles

Go

vern

men

t Se

rvic

es

Hea

lth

care

Pro

vid

ers

INSU

RA

NC

E

Rea

l Est

ate

Telc

o /

Cab

le

Average7.3

INSU

RAN

CE

Relative satisfaction utility score

Delivering Digital Satisfaction @2013 – The Boston Consulting Group (BCG)

Page 5

PRODUCED BY ALAN ALDEN I SERIES-A PARTNERS LLC

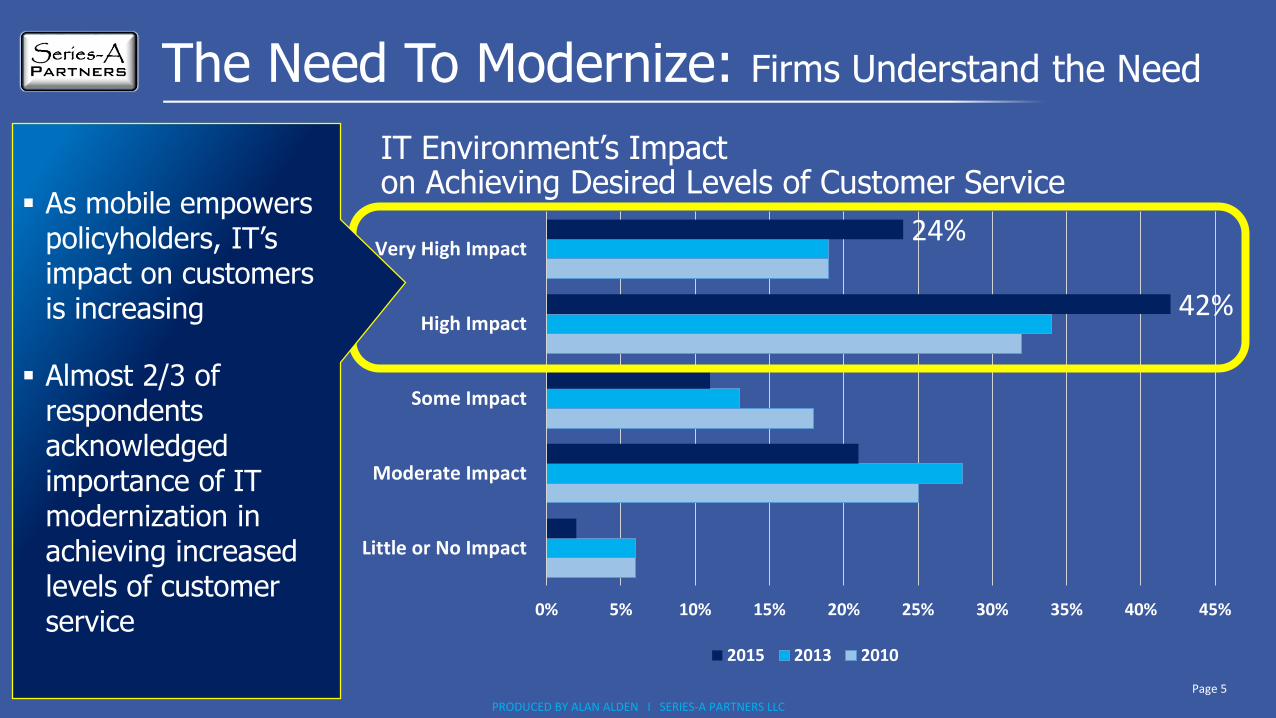

The Need To Modernize: Firms Understand the Need

42%

24%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Little or No Impact

Moderate Impact

Some Impact

High Impact

Very High Impact

2015 2013 2010

IT Environment’s Impact on Achieving Desired Levels of Customer Service

As mobile empowers policyholders, IT’s impact on customers is increasing

Almost 2/3 of respondents acknowledged importance of IT modernization in achieving increased levels of customer service

Page 6

PRODUCED BY ALAN ALDEN I SERIES-A PARTNERS LLC

The Opportunity

$175Billion

2015

$189.2Billion

2017

Global Insurance IT Spending

4% CAGR

Page 7

PRODUCED BY ALAN ALDEN I SERIES-A PARTNERS LLC

Country / Region 2013 2014 2015 2016 2017

US (7.1%) (1.7%) 1.3% 1.0% 2.3%

Canada 3.0% 7.6% 2.4% 3.5% 3.8%

UK (5.9%) (10.4%) 2.2% 3.5% 3.2%

Japan 6.8% 7.1% 2.7% 3.0% 3.7%

Australia 9.8% 26.5% (5.8%) 4.1% 2.1%

France 3.6% 8.4% 4.2% 2.6% 2.5%

Germany 2.5% 2.7% 3.1% 0.9% 0.9%

Italy 20.6% 29.5% 2.8% 2.2% 2.3%

Spain (4.3%) (2.5%) (11.6%) 0.3% 0.6%

Netherlands -5.9%) (5.2%) (10.0%) 2.2% 1.7%

Advanced Markets -2.5% 4.2% 1.9% 2.4% 2.6%

World -1.5% 4.7% 3.3% 4.0% 4.2%

Emerging Markets 4.0% 7.4% 10.6% 10.7% 10.7%

With Great Growth Ahead….

Emerging Markets 4.0% 7.4% 10.6% 10.7% 10.7%

PRODUCED BY ALAN ALDEN – SERIES-A PARTNERS

Page 88

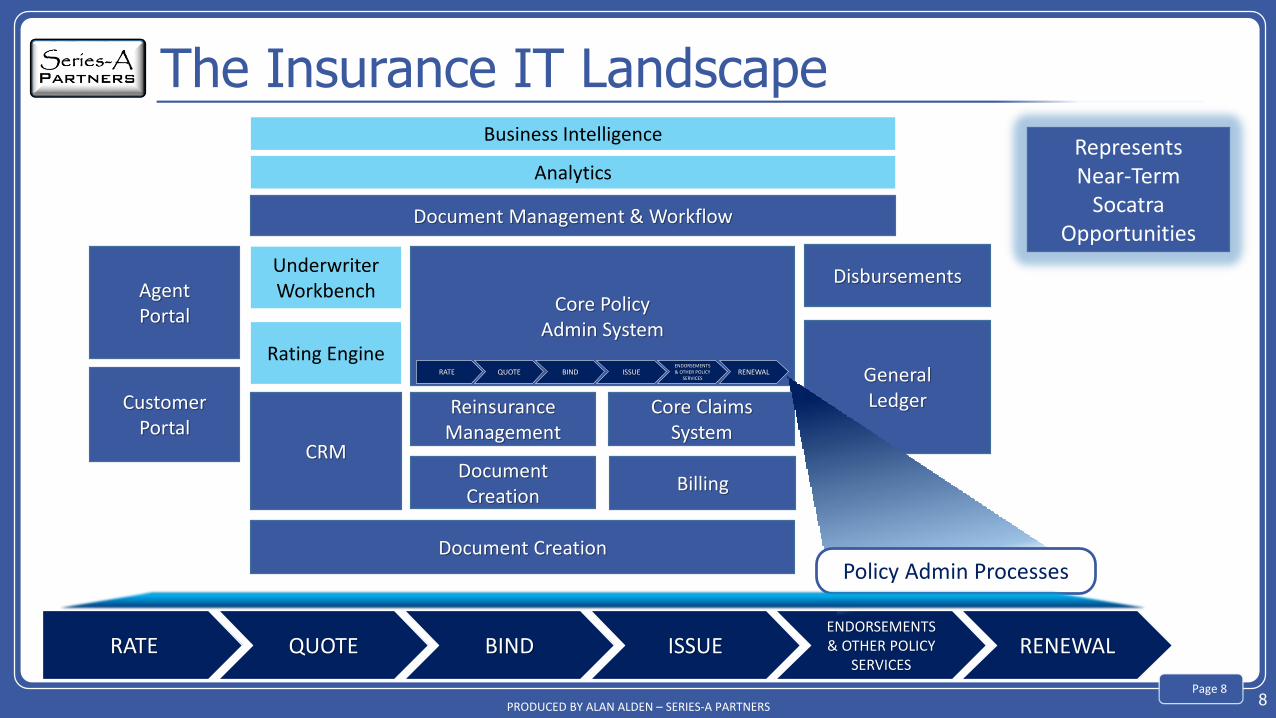

The Insurance IT Landscape

Represents Near-Term

Socatra Opportunities

RATE QUOTE BIND ISSUEENDORSEMENTS & OTHER POLICY

SERVICESRENEWAL

Core Policy Admin System

Document Creation

Billing

GeneralLedger

Document Management & Workflow

Business Intelligence

Analytics

Reinsurance Management

Core ClaimsSystem

Disbursements

CRM

Rating Engine

UnderwriterWorkbench

Document Creation

CustomerPortal

AgentPortal

RATE QUOTE BIND ISSUEENDORSEMENTS & OTHER POLICY

SERVICESRENEWAL

Policy Admin Processes

PRODUCED BY ALAN ALDEN – SERIES-A PARTNERS

Page 9

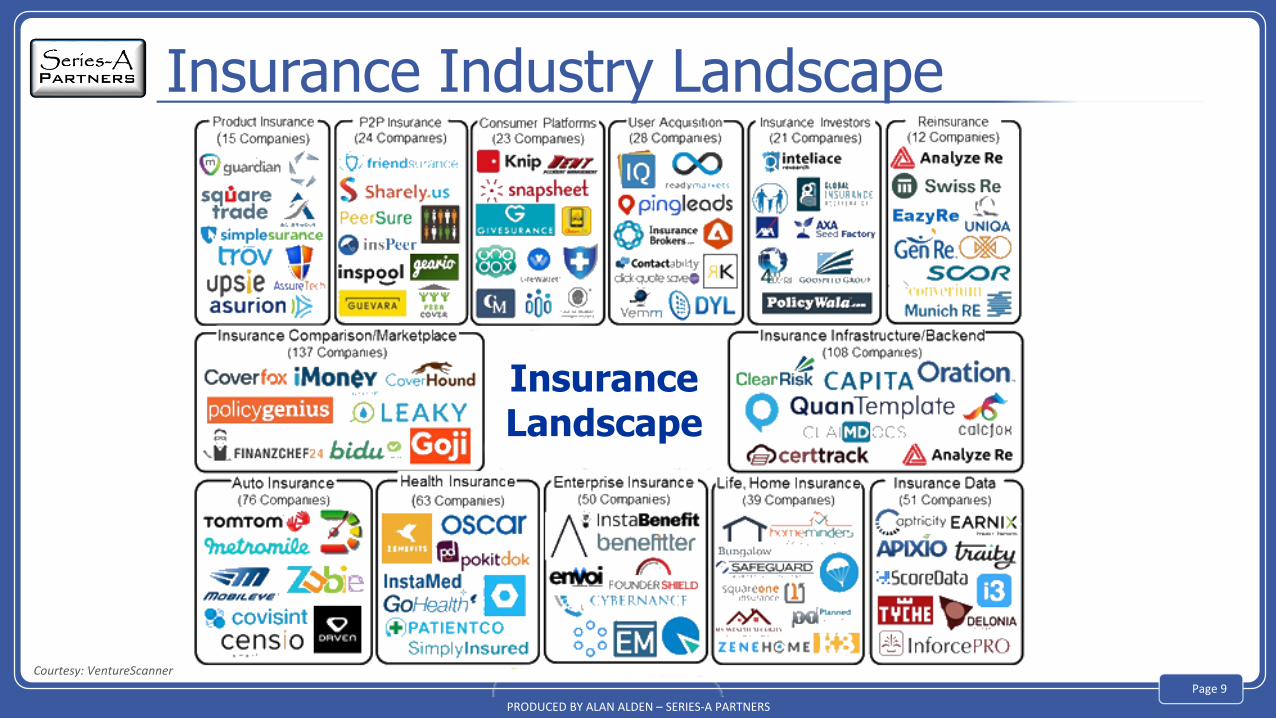

Insurance Industry Landscape

Insurance Landscape

Courtesy: VentureScanner

PRODUCED BY ALAN ALDEN I SERIES-A PARTNERS LLC

Insurance IndustryEmerging Markets

Opportunity Overview

Page 11

PRODUCED BY ALAN ALDEN I SERIES-A PARTNERS LLC

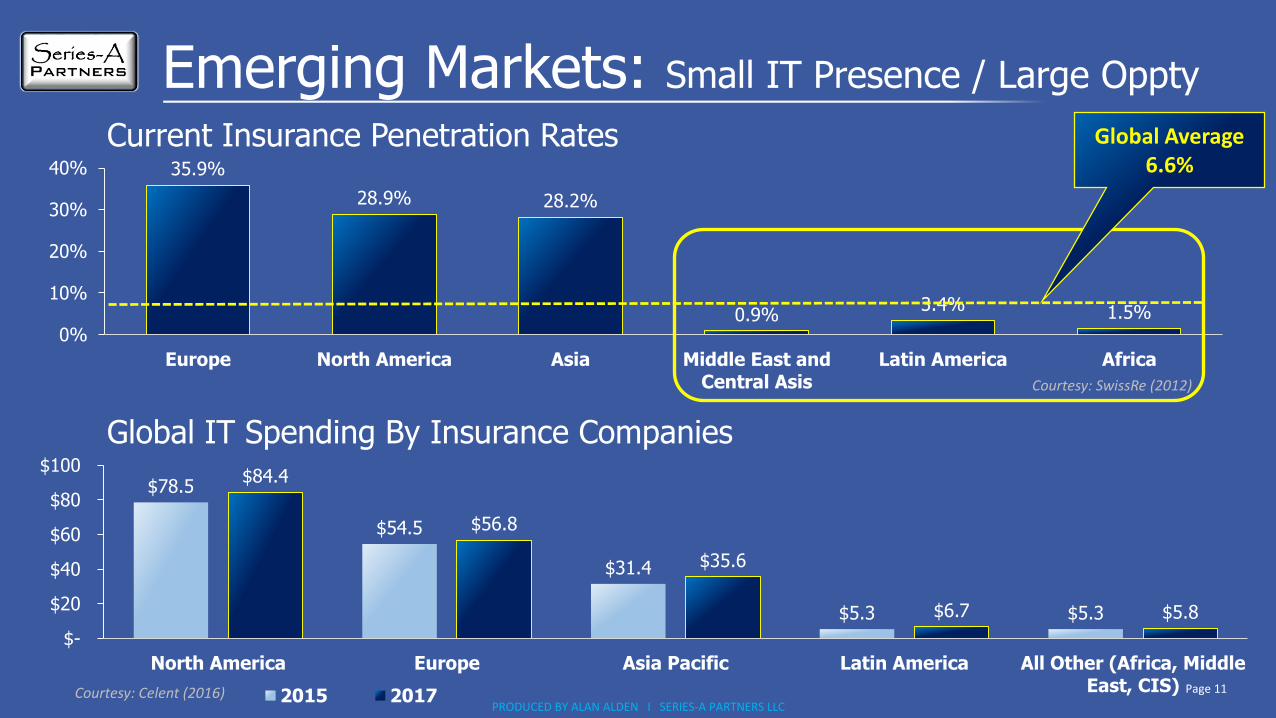

Emerging Markets: Small IT Presence / Large Oppty

35.9%

28.9% 28.2%

0.9%3.4% 1.5%

0%

10%

20%

30%

40%

Europe North America Asia Middle East andCentral Asis

Latin America Africa

Current Insurance Penetration Rates

$78.5

$54.5

$31.4

$5.3 $5.3

$84.4

$56.8

$35.6

$6.7 $5.8

$-

$20

$40

$60

$80

$100

North America Europe Asia Pacific Latin America All Other (Africa, MiddleEast, CIS)

2015 2017

Courtesy: SwissRe (2012)

Global Average6.6%

Courtesy: Celent (2016)

Global IT Spending By Insurance Companies

Page 12

PRODUCED BY ALAN ALDEN I SERIES-A PARTNERS LLC

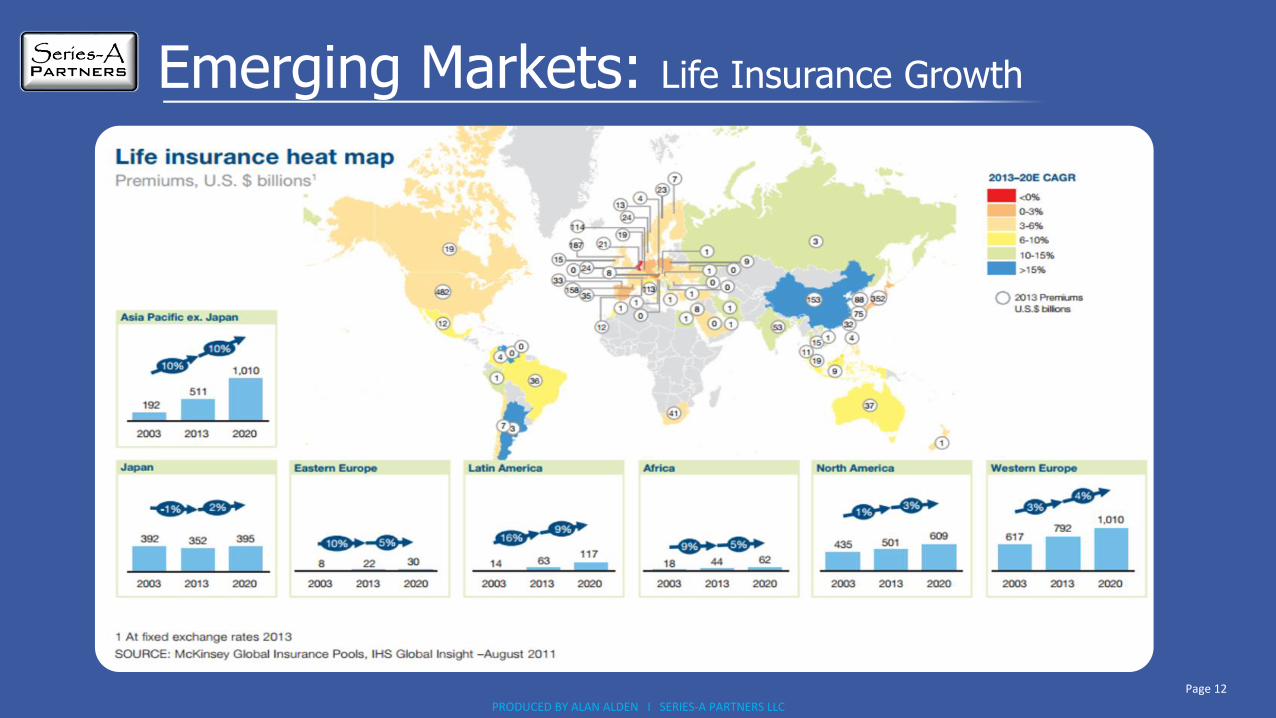

Emerging Markets: Life Insurance Growth

Page 13

PRODUCED BY ALAN ALDEN I SERIES-A PARTNERS LLC

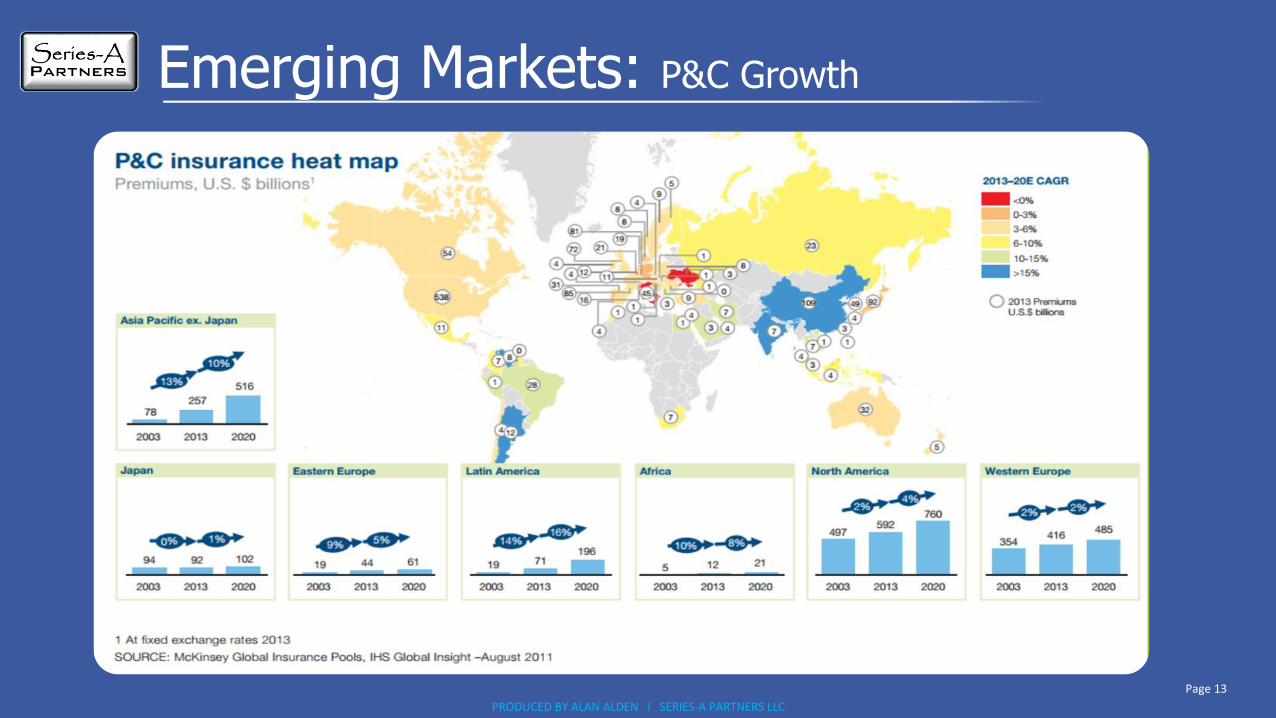

Emerging Markets: P&C Growth

PRODUCED BY ALAN ALDEN – SERIES-A PARTNERS

Page 14

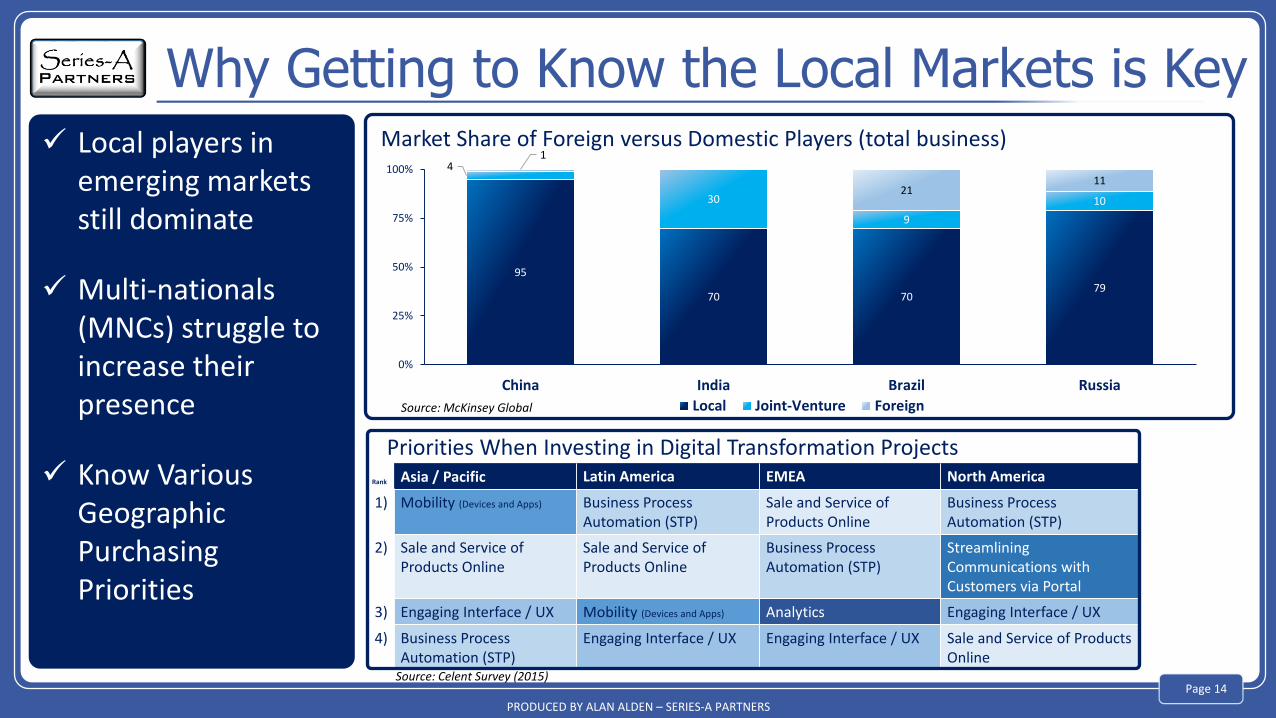

Why Getting to Know the Local Markets is Key

Local players in emerging markets still dominate

Multi-nationals (MNCs) struggle to increase their presence

Know Various Geographic Purchasing Priorities

95

70 7079

4

30

9

10

1

2111

0%

25%

50%

75%

100%

China India Brazil Russia

Local Joint-Venture ForeignSource: McKinsey Global

Market Share of Foreign versus Domestic Players (total business)

Priorities When Investing in Digital Transformation ProjectsRank Asia / Pacific Latin America EMEA North America

1) Mobility (Devices and Apps) Business Process Automation (STP)

Sale and Service of Products Online

Business Process Automation (STP)

2) Sale and Service of Products Online

Sale and Service of Products Online

Business Process Automation (STP)

StreamliningCommunications with Customers via Portal

3) Engaging Interface / UX Mobility (Devices and Apps) Analytics Engaging Interface / UX

4) Business Process Automation (STP)

Engaging Interface / UX Engaging Interface / UX Sale and Service of Products Online

Source: Celent Survey (2015)

Page 15

PRODUCED BY ALAN ALDEN I SERIES-A PARTNERS LLC

Go-to-Market Key Considerations

Most insurers are spending are spending between 1-6% of direct written premiums on IT*

Average is 3.2%

~25% is spent on external software and an additional 22% is spent on external services

More than 70% of vendors opt for vendor solutions (vs building own)

Growth and retention, process optimization (faster, leaner and smarter business processes), and meeting regulatory requirements are the top three drivers for IT investment at Asian insurers

* Source: Celent Asia Pacific Insurance CIO survey 2014

Page 16

Thank You

Contact Information:

Alan Alden

PRODUCED BY ALAN ALDEN I SERIES-A PARTNERS LLC

@SeriesAPartners

www.series-a.com

INVESTMENT BANKING I STRATEGYINTERNATIONAL CORPORATE DEVELOPMENT