The Board’s Role in Anticorruption Compliance - … · The Board’s Role in Anticorruption...

66

Page 1 The Board’s Role in Anticorruption Compliance OCTOBER 2015 The presentation will begin shortly. Learn Live Customer Support at: (888) 228-4188 or [email protected] Alternative audio option via phone: • Call: 1-855-233-5756 • Conference Code 446-460-6356# BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms. Maximizing Corporate Resources to Effectively Prevent, Detect, & Monitor Anticorruption Risks

Transcript of The Board’s Role in Anticorruption Compliance - … · The Board’s Role in Anticorruption...

Page 1

The Board’s Role in Anticorruption Compliance

OCTOBER 2015

The presentation will begin shortly.Learn Live Customer Support at: (888) 228-4188 or [email protected]

Alternative audio option via phone:• Call: 1-855-233-5756• Conference Code 446-460-6356#

BDO USA, LLP, a Delaware limited liability partnership, is the U.S.member of BDO International Limited, a UK company limited byguarantee, and forms part of the international BDO network ofindependent member firms.

Maximizing Corporate Resources to Effectively Prevent, Detect, & Monitor Anticorruption Risks

Page 2

CPE and Support

CPE Participation Requirements ‒ To receive CPE credit for this webcast:• You’ll need to actively participate throughout the program.• Be responsive to at least 75% of the participation pop-ups.

Certificate of Attendance: If you are logged for the entire time and respond to the requisiteparticipation pop-ups, you will be able to print your certificate from the“Participation” section at the end of the webcast.If you log out before printing your certificate:• Clients and Contacts and all other individual participants ‒ You will be

emailed instructions on how to access your certificate.• BDO USA professionals ‒ CPE will automatically be issued in CPE Tracking &

Reporting. A copy of your certificate will be sent after you have been issuedcredit.

Page 3

CPE and Support (Continued)

Group Participation ‒ To receive credit:• Sign-in sheets must list a Proctor name and CPA license number.• Clients and contacts ‒ Email sign-in sheets to [email protected] within 24 hours of

the webcast.• BDO Alliance USA ‒ Should proctor their own group participants. This process is

detailed in the LearnLive Participant Guide on the Alliance Portal > Resource Center. Call LearnLive Support for questions – 1-888-228-4088.

• BDO International ‒ Unfortunately, we cannot currently support group CPE for International Firms. Those wanting CPE must register and log in on their own computer.

• BDO USA ‒ Submit your sign-in sheets using a General Training & Development Request in BDO Service Now found at: https://apps.bdo.com > A to Z > BDO Service Now > Click “Request” in the upper right menu, then chose “Training & Development” from the Filter Category drop-down, click on “Training & Development Support”.

Page 4

CPE and Support (Continued)

Audio by Teleconference: Dial the teleconference number to listen to webcast audio by phone:• Dial: 1-855-233-5756• Enter Conference Code 446-460-6356#

Q&A: Submit all questions using the Q&A feature on the lower right corner of the screen. At the end of the presentation, the presenter(s) will review and answer all questions submitted.

Technical Support: If you should have technical issues, please contact LearnLive:• Click on the Live Chat icon under the Support tab, OR call: 1-888-228-4088

Page 5

Presenters

• Julia Bailey, Managing Director, Global Forensics Practice, BDO Consulting [email protected]

• Amy Rojik, Partner, National Assurance, BDO USA, LLP [email protected]

• Kirstie Tiernan, Director, Forensic Technology Services, BDO Consulting [email protected]

• Howard Weismann, Counsel, Compliance & Investigations Practice Group, Baker & McKenzie LLP [email protected]

Page 6

Anticorruption Corporate ComplianceAgenda

1. Overview

a. Key Elements

b. Government Guidance

c. The Board’s Role

2. Trends

a. Regulatory Environment & External Pressures

b. In-House Trends

c. Data Analytics

3. Key Risk Areas & Best Practices for Leveraging Resources

a. Overall elements

b. Internal Controls

c. Due Diligence: Third Parties & M & A

d. Gifts & Hospitality

e. Periodic Monitoring & Improvement

Page 7

Overview

• Key Elements• Government

Guidance• The Board’s

Role

Page 8

Anticorruption Background

Foreign Corrupt Practices Act (“FCPA”) 15 U.S.C., 78dd-1 et seq., 78m (1977)

•Anti-bribery provisions: Prohibit payments or offers or authorizations of payments of “anything of value” to foreign officials to obtain/retain business or business advantages

•Accounting and internal controls provisions: Require U.S. public companies to maintain good records and internal controls

•Enforcement: Civil and criminal liability for companies and individuals; Enforced by SEC and DOJ

•FCPA is substantially similar to other global anticorruption laws (e.g., UK Bribery Act)

Page 9

Sources of Anticorruption Compliance Guidance

Page 10

Other Anticorruption Compliance Guidance

• U.S. FCPA Resource Guide (2012)

• Asia-Pacific Economic Cooperation—Anti-Corruption Code of Conduct for Business

• International Chamber of Commerce—ICC Rules on Combating Corruption

• Transparency International—Business Principles for Countering Bribery;

• United Nations Global Compact—The Ten Principles World Bank—Integrity Compliance Guidelines

• World Economic Forum—Partnering Against Corruption–Principles for Countering Bribery

Page 11

5 Essential Elements of Anticorruption Compliance

LEADERSHIP

• Board of Directors & Sr. Executives must set proper tone of commitment to ethics and legal compliance.

• High-ranking compliance professionals with adequate authority & resources to manage & implement

RISK ASSESSMENT• Awareness of the nature & extent of risks• Processes for assessing risks

STANDARDS & CONTROLS

• Detailed written policies (more than just a piece of paper)

• Clear procedures & protocols for implementing

TRAINING & COMMUNICATION

• Training reaches key employees and includes live, annual training for high-risk personnel

• Tailored by country and updated frequently

MONITORING, AUDITING, & RESPONSE

• Continuous oversight and process of revision & improvement

• Reporting mechanisms • Protocols for internal investigations & disciplinary action

Page 12

The Board and Compliance Responsibility

• Board must be knowledgeable about the compliance and ethicsprogram, understand how it operates and “exercise reasonableoversight” with regard to the program implementation andeffectiveness.

- The U.S. Federal Sentencing Guidelines

• Board (or a sub-set of the Board) should receive direct reports fromthe senior individual with day-to-day responsibility for the complianceand ethics program.

– DoJ and SEC FCPA Guidance

• Audit Committee members must discuss risk assessment and riskmanagement policies.

– NYSE Corporate Governance Rules

Page 13

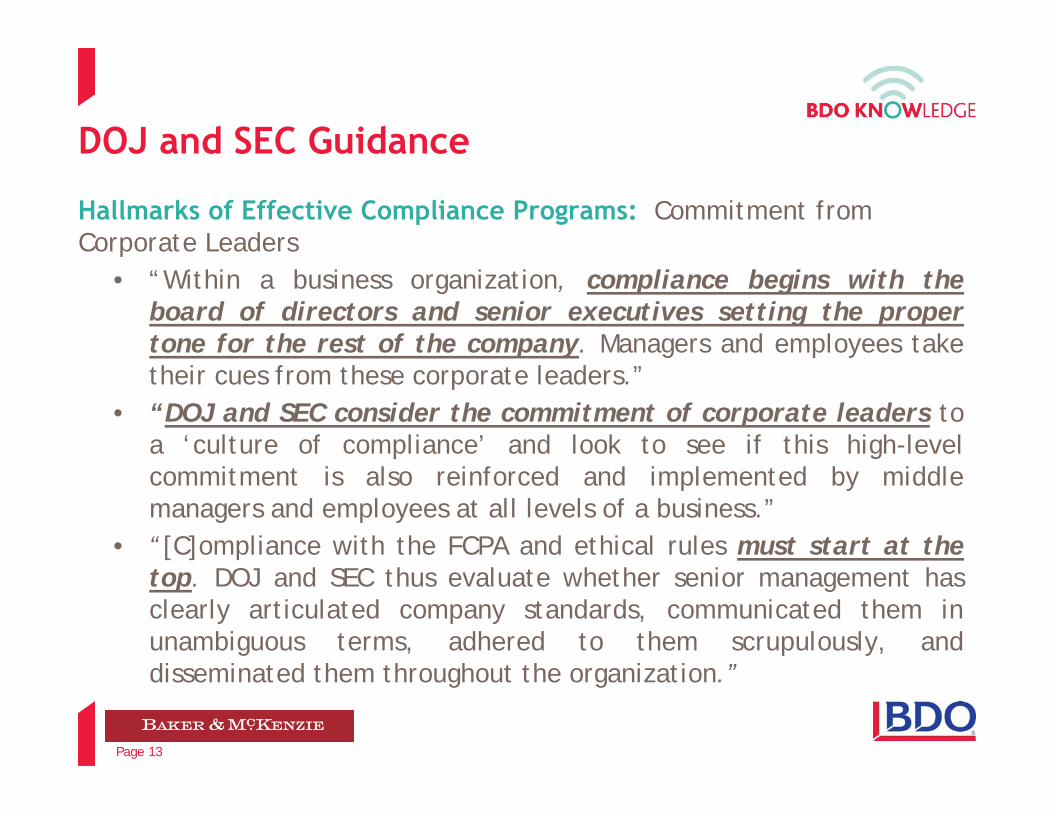

DOJ and SEC Guidance

Hallmarks of Effective Compliance Programs: Commitment from Corporate Leaders

• “Within a business organization, compliance begins with theboard of directors and senior executives setting the propertone for the rest of the company. Managers and employees taketheir cues from these corporate leaders.”

• “DOJ and SEC consider the commitment of corporate leaders toa ‘culture of compliance’ and look to see if this high-levelcommitment is also reinforced and implemented by middlemanagers and employees at all levels of a business.”

• “[C]ompliance with the FCPA and ethical rules must start at thetop. DOJ and SEC thus evaluate whether senior management hasclearly articulated company standards, communicated them inunambiguous terms, adhered to them scrupulously, anddisseminated them throughout the organization.”

Page 14

U.S. Sentencing Guidelines

• Board must be “knowledgeable about the content and operation of the compliance and ethics program and shall exercise reasonable oversight” with respect to its implementation and effectiveness.

• To receive a “culpability score reduction” during sentencing under the Guidelines, a company must show that its compliance officers can promptly report any matter involving criminal conduct directly to the board or appropriate board committee.

• Compliance officers should also report to the board on the implementation and effectiveness of the company’s compliance program at least once a year.

Page 15

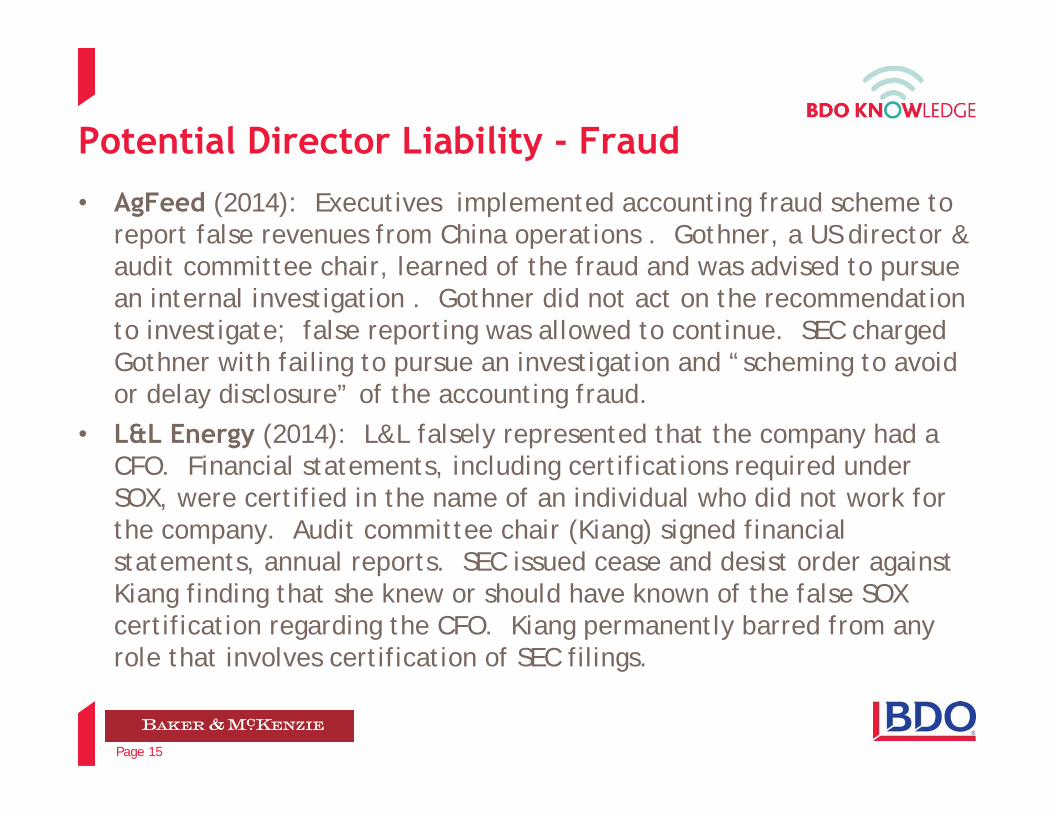

Potential Director Liability - Fraud• AgFeed (2014): Executives implemented accounting fraud scheme to

report false revenues from China operations . Gothner, a US director & audit committee chair, learned of the fraud and was advised to pursue an internal investigation . Gothner did not act on the recommendation to investigate; false reporting was allowed to continue. SEC charged Gothner with failing to pursue an investigation and “scheming to avoid or delay disclosure” of the accounting fraud.

• L&L Energy (2014): L&L falsely represented that the company had a CFO. Financial statements, including certifications required under SOX, were certified in the name of an individual who did not work for the company. Audit committee chair (Kiang) signed financial statements, annual reports. SEC issued cease and desist order against Kiang finding that she knew or should have known of the false SOX certification regarding the CFO. Kiang permanently barred from any role that involves certification of SEC filings.

Page 16

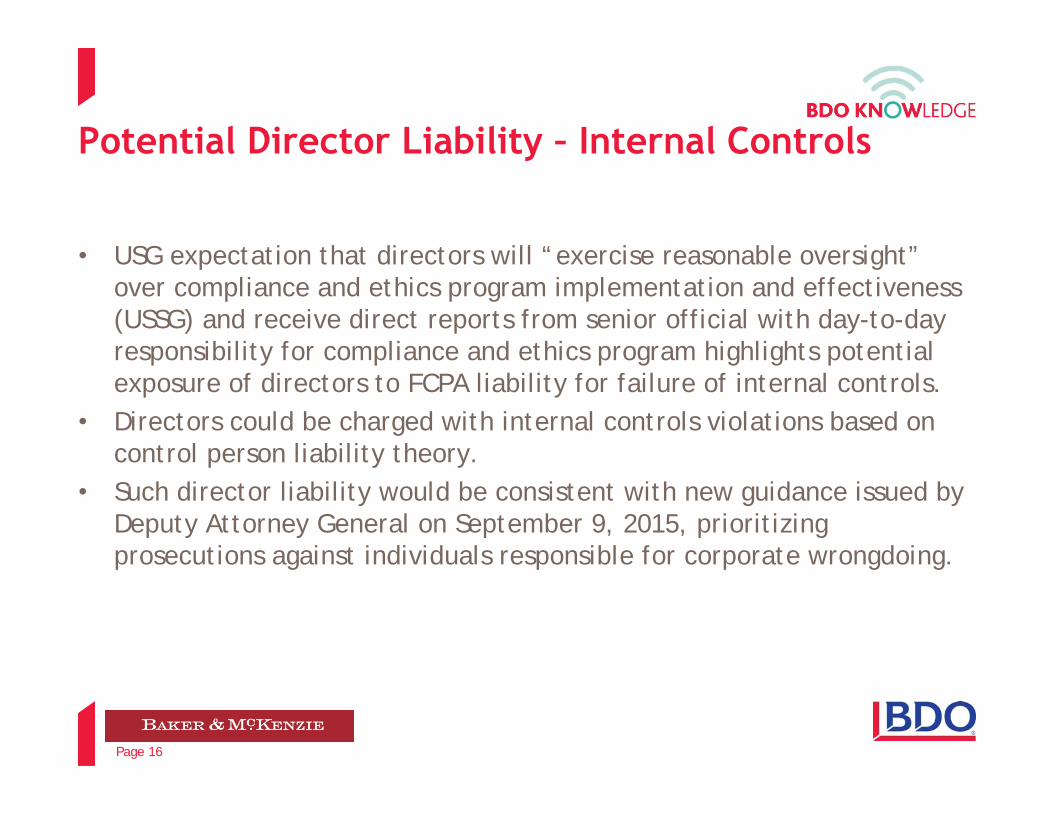

Potential Director Liability – Internal Controls

• USG expectation that directors will “exercise reasonable oversight” over compliance and ethics program implementation and effectiveness (USSG) and receive direct reports from senior official with day-to-day responsibility for compliance and ethics program highlights potential exposure of directors to FCPA liability for failure of internal controls.

• Directors could be charged with internal controls violations based on control person liability theory.

• Such director liability would be consistent with new guidance issued by Deputy Attorney General on September 9, 2015, prioritizing prosecutions against individuals responsible for corporate wrongdoing.

Page 17

Potential Director Liability – Internal Controls

• US v Total S.A. (2013): DOJ alleged that Total “knowingly circumvented and knowingly failed to implement a system of internal accounting controls sufficient to provide reasonable assurances that transactions and dispositions of Total’s assets complied with applicable law.”

• US v Orthofix International (2012): DOJ charged Orthofix with internal controls violations for failing to maintain an effective A/C compliance program and adequate financial controls.

• Nature’s Sunshine Products (2009): SEC enforcement action against two senior executives of Nature’s Sunshine Products. SEC alleged senior executives failed to adequately supervise their personnel, ensure that accurate books and records were kept, and ensure proper internal controls were being maintained.

Page 18

Potential Director Liability – Civil Shareholder Suits

• No private right of action under FCPA but anticorruption investigations are often followed by shareholder lawsuit. (E.g., recent cases: Och-Ziff Capital Management Group (2014), Hyperdynamics Corporation (2014), NuSkin (2014), Archer Daniels Midland (2014). )

• These cases often fail. (e.g., Avon Products (SDNY September, 2014)• Wal-mart (2014): Securities class action suit filed following Company’s

2011 SEC filing disclosure that it had begin an internal investigation into possible FCPA violations and had disclosed the same to the SEC and DoJ. • Shareholder plaintiffs alleged the disclosure was misleading because

it left investors with the impression that Wal-Mart had first learned of corruption in 2011, rather than in 2005 and 2006, when it actually learned of the possible corruption.

• Case survived defendants’ motion to dismiss.• Wal-mart is ongoing but will likely encourage a continuation of FCPA-

related shareholder lawsuits.

Page 19

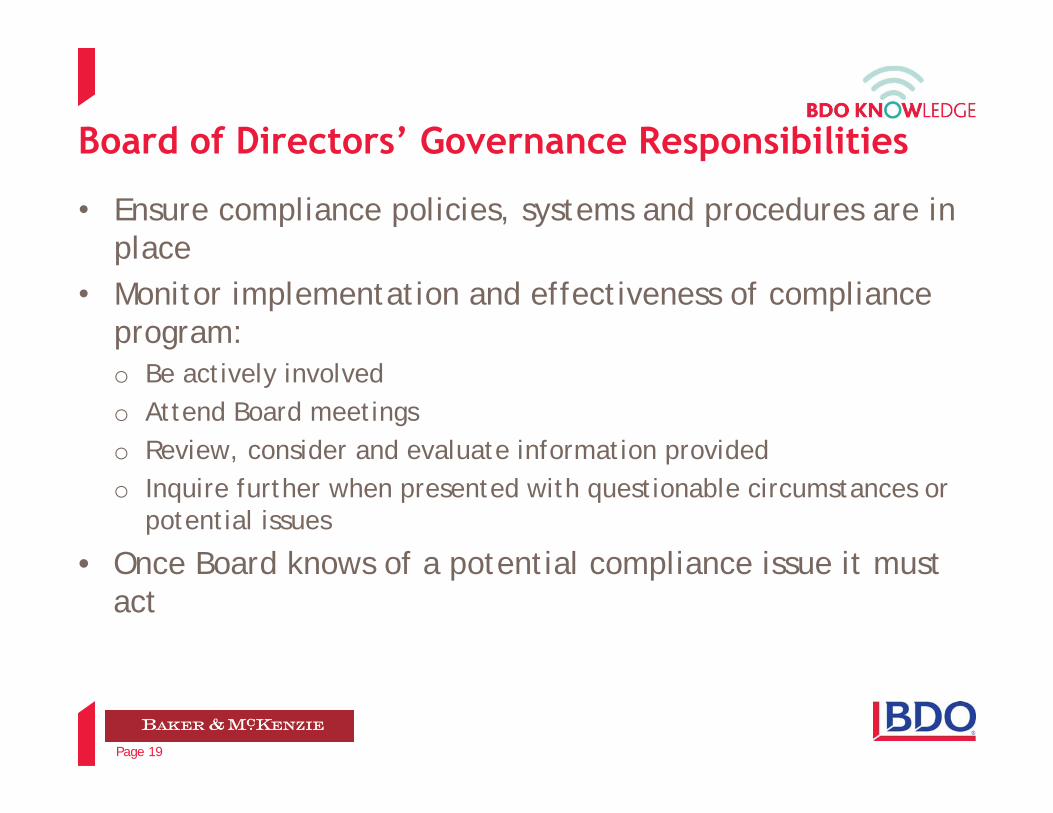

Board of Directors’ Governance Responsibilities

• Ensure compliance policies, systems and procedures are in place

• Monitor implementation and effectiveness of compliance program: o Be actively involved o Attend Board meetings o Review, consider and evaluate information provided o Inquire further when presented with questionable circumstances or

potential issues

• Once Board knows of a potential compliance issue it must act

Page 20

Board of Directors’ Governance Responsibilities (Continued)• Regularly receive compliance briefings and training

o While USG recommend compliance officers report to board at least annually on implementation and effectiveness of compliance program, Baker & McKenzie recommends quarterly presentations to board on: ongoing internal investigations, general developments in anticorruption laws and enforcement, compliance challenges company is facing and what is being done to address those challenges

o Board members should discuss risk assessment and risk management policies

o Maintain & demonstrate open line of communication between compliance team and Board.

Page 21

Trends

• Regulatory Environment & External Pressures

• In-House Trends

Page 22

Prospect name − Document title

Regulatory Environment

Page 23

External Pressures

Increases In… SEC, DoJ, and global enforcementGovernment resources Aggressive investigation techniques Prosecution of individuals, executives, &

“gatekeepers”Guilty pleas (fewer “DPAs”)Global government cooperation Penalties (in U.S. and globally)D/O liability casesWhistleblowers & incentives for them

Page 24

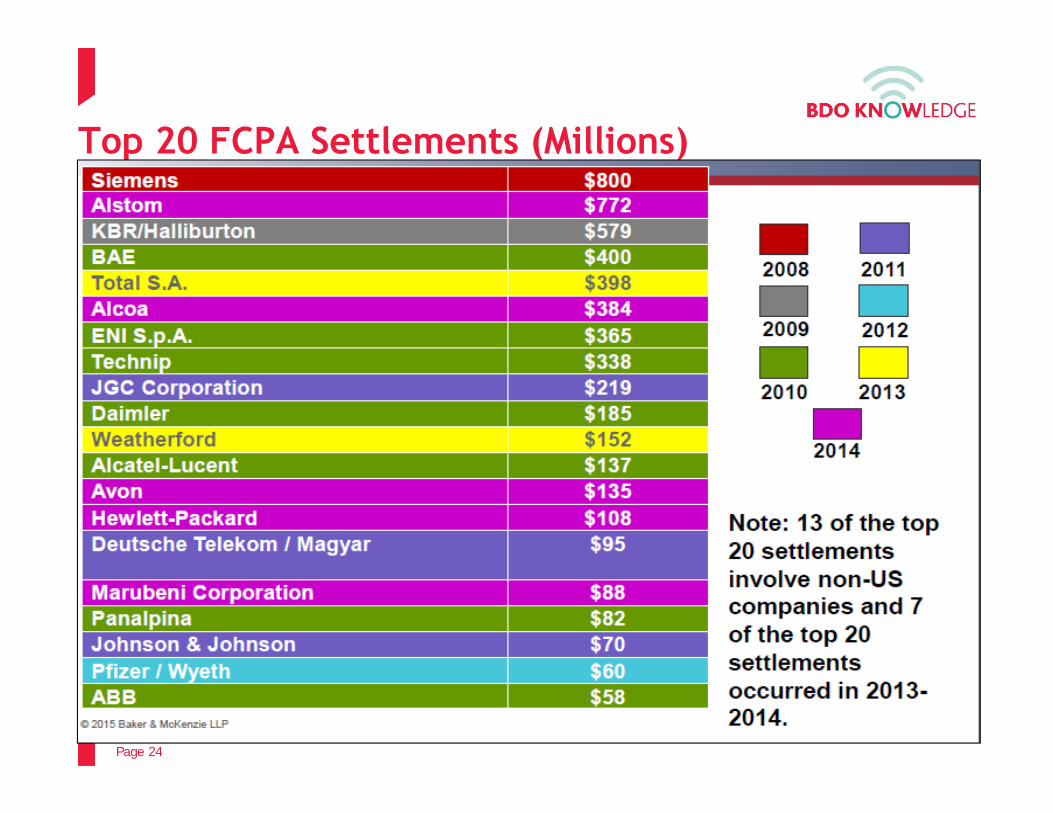

Top 20 FCPA Settlements (Millions)

Page 25

Prosecution of Corporate BriberyU.S. Foreign Corruption Practices Act Actions

Page 26

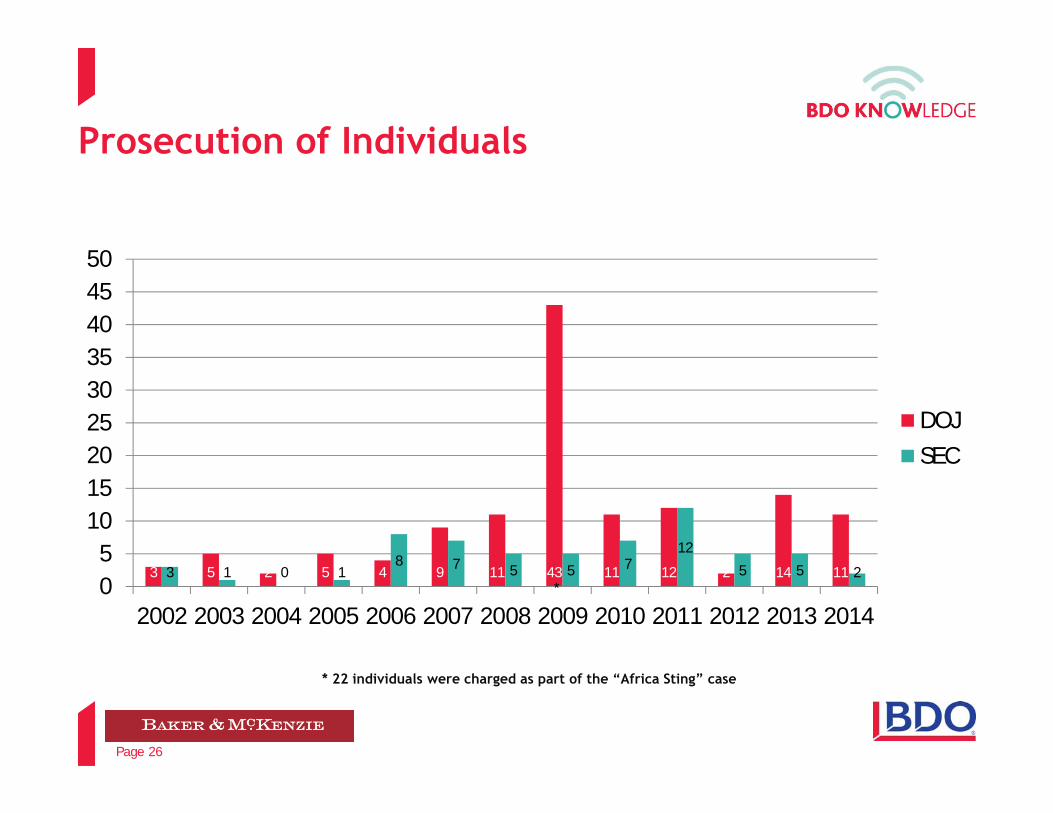

Prosecution of Individuals

3 5 2 5 4 9 11 43 11 12 2 14 113 1 0 18 7 5 5 7

12

5 5 205

101520253035404550

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

DOJSEC

*

* 22 individuals were charged as part of the “Africa Sting” case

Page 27

TECHNOLOGY

RISK ASSESSMENT & MONITORING

RESOURCES NEEDED

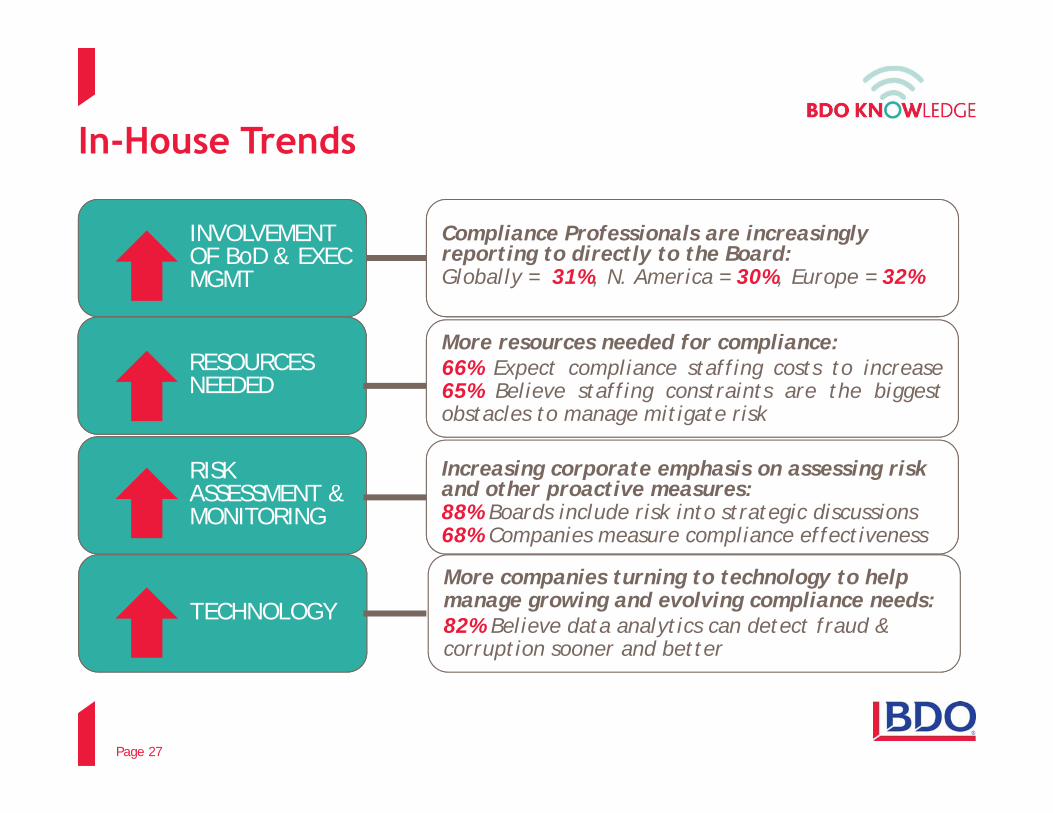

Compliance Professionals are increasingly reporting to directly to the Board: Globally = 31%, N. America = 30%, Europe = 32%

INVOLVEMENT OF BoD & EXEC MGMT

TECHNOLOGY

RISK ASSESSMENT & MONITORING

RESOURCES NEEDED

Compliance Professionals are increasingly reporting to directly to the Board: Globally = 31%, N. America = 30%, Europe = 32%

INVOLVEMENT OF BoD & EXEC MGMT

In-House Trends

More resources needed for compliance:66% Expect compliance staffing costs to increase65% Believe staffing constraints are the biggestobstacles to manage mitigate risk

Increasing corporate emphasis on assessing risk and other proactive measures: 88% Boards include risk into strategic discussions68% Companies measure compliance effectiveness

More companies turning to technology to help manage growing and evolving compliance needs:82% Believe data analytics can detect fraud & corruption sooner and better

Page 28

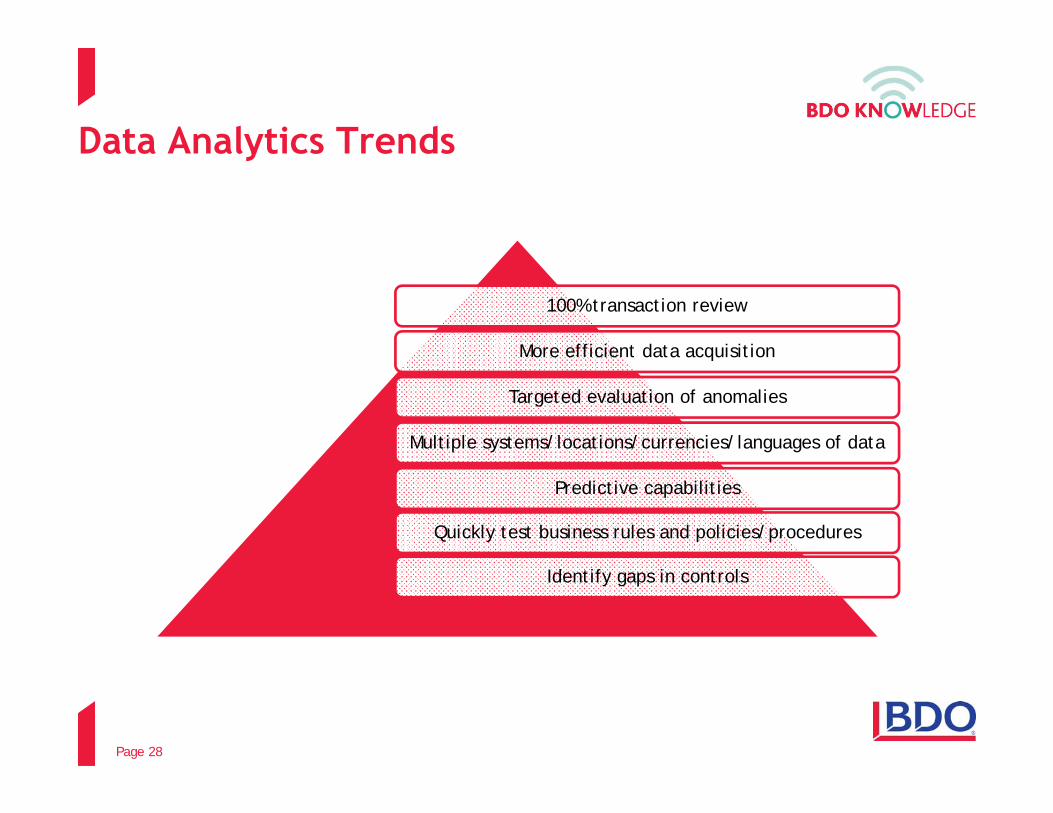

Data Analytics Trends

100% transaction review

More efficient data acquisition

Targeted evaluation of anomalies

Multiple systems/locations/currencies/languages of data

Predictive capabilities

Quickly test business rules and policies/procedures

Identify gaps in controls

Page 29

Examples of Data Analytics

Page 29

Human Resources & Payroll

Employee Expenses & Petty Cash

General Ledger / Journal Entries

Accounts Payable & Receivables

Employee verification; duplicate employees, unexpected relationships; high-risk transactions; unauthorized transactions

Procedural bypass; cash advances; key words that typically surround anti-corruption violations; transactions that continually approach authority levels

Entries made outside business hours; re-classifications; entries that write off receivables

Supplier Validation; duplicate suppliers; unexpected relationships; detailed transaction testing; review of unexpected relationships and detailed transaction testing

Page 30

Key Risk Areas

• Overall elements

• Governance

• Internal Controls

• Due Diligence: Third Parties & M & A

• Gifts/Hospitality

Page 31

Best Practices for Anticorruption Compliance

1. Governance & Oversight2. Written Policies &

Procedures3. Due diligence – Significant

3rd Parties/M&A Targets4. Facilitation Payments5. Gifts & Hospitality6. Charitable donations &

Political contributions7. Hiring & Termination

8. Books & Records / Internal Controls

9. Reporting & Hotlines10. Periodic Assessments &

Monitoring11. Training &

Communication12. Enforcement

Page 32

Best Practices for Anticorruption Compliance

1. Governance & Oversight2. Written Policies &

Procedures3. Due diligence – Significant

3rd Parties/M&A Targets4. Facilitation Payments5. Gifts & Hospitality6. Charitable donations &

Political contributions7. Hiring & Termination

8. Books & Records / Internal Controls

9. Reporting & Hotlines10. Periodic Assessments &

Monitoring11. Training &

Communication12. Enforcement

Page 33

Oversight & Governance

• Governing Authority must have reasonable oversight

• Specific high-level authority must have overall responsibility and:• appropriate authority • adequate autonomy • direct access to Governing

Authority• sufficient resources

• Specific individual(s) delegated day-to-day operational responsibility

Page 34

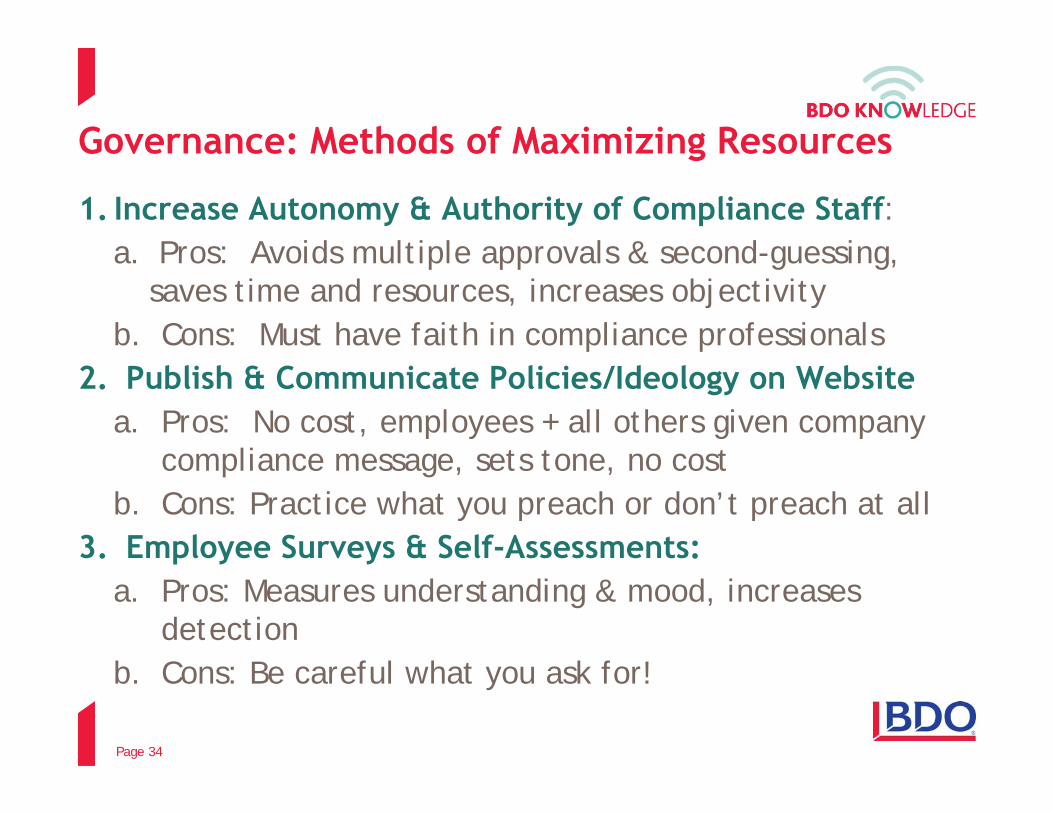

Governance: Methods of Maximizing Resources

1. Increase Autonomy & Authority of Compliance Staff: a. Pros: Avoids multiple approvals & second-guessing,

saves time and resources, increases objectivityb. Cons: Must have faith in compliance professionals

2. Publish & Communicate Policies/Ideology on Website a. Pros: No cost, employees + all others given company

compliance message, sets tone, no costb. Cons: Practice what you preach or don’t preach at all

3. Employee Surveys & Self-Assessments:a. Pros: Measures understanding & mood, increases

detectionb. Cons: Be careful what you ask for!

Page 35

Books & Records / Internal Controls

• Coordination & cross-referencing with Audit and Accounting Policies and Roles/Responsibilities is crucial.

• Books and Records: In reasonable detail that accurately reflects transactions and dispositions of assets.• The Al Capone folly: Easy to stumble on this one• Is the substance of books/records as important as the form?

• Internal Control: Sufficient enough to provide reasonable assurances that management has adequate oversight of transactions involving company assets.• Are cash disbursements (A/P), vendor management, and

invoicing tightly controlled or easy to override?• Are approvers aware of what they are approving?

Page 36

Internal Controls: Methods of Maximizing Resources

1. Risk Assessments: e.g., BDO, In-housea. Pros: Proactive – before offer, USG mandatesb. Cons: Cost, experience & scope matters

2. Internal Audits: e.g., BDO, In-housea. Pros: May already be required, b. Cons: Relies on sampling, GAAP audits do not require

tests for fraud/corruption, auditing policy/procedure adherence not good at detecting corruption

3. Data Analytics: e.g., IDEA, ACL, Tableau, SQL Servera. Pros: Excellent detection; cost efficient b. Cons: Depends on completeness and reliability of data

(e.g., legacy systems, human error/integrity, etc.)

Page 37

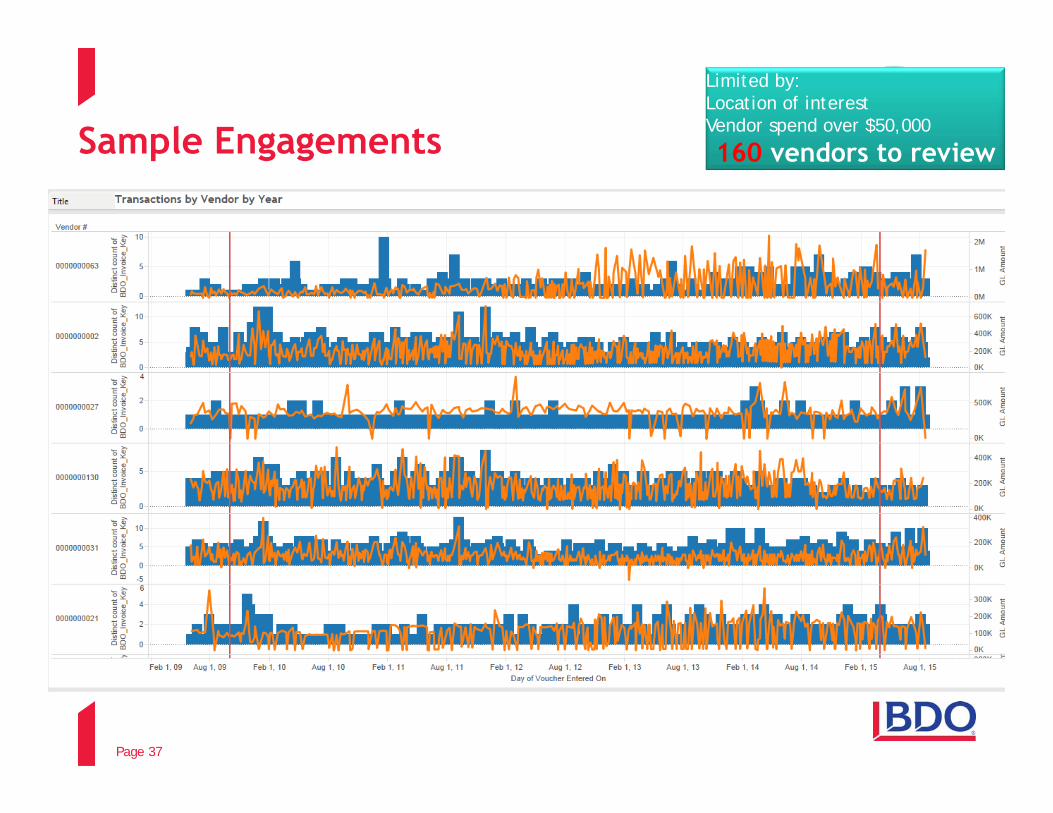

Sample Engagements

Limited by:Location of interestVendor spend over $50,000

160 vendors to review

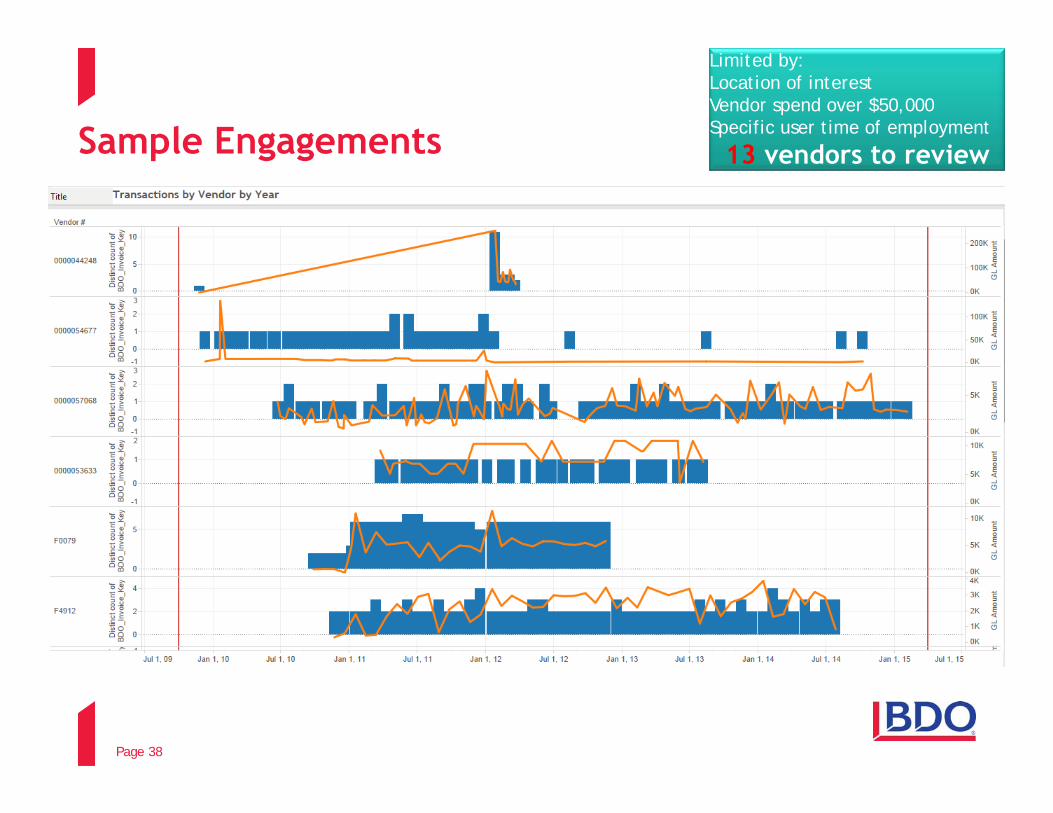

Page 38

Sample Engagements

Limited by:Location of interestVendor spend over $50,000Specific user time of employment

13 vendors to review

Page 39

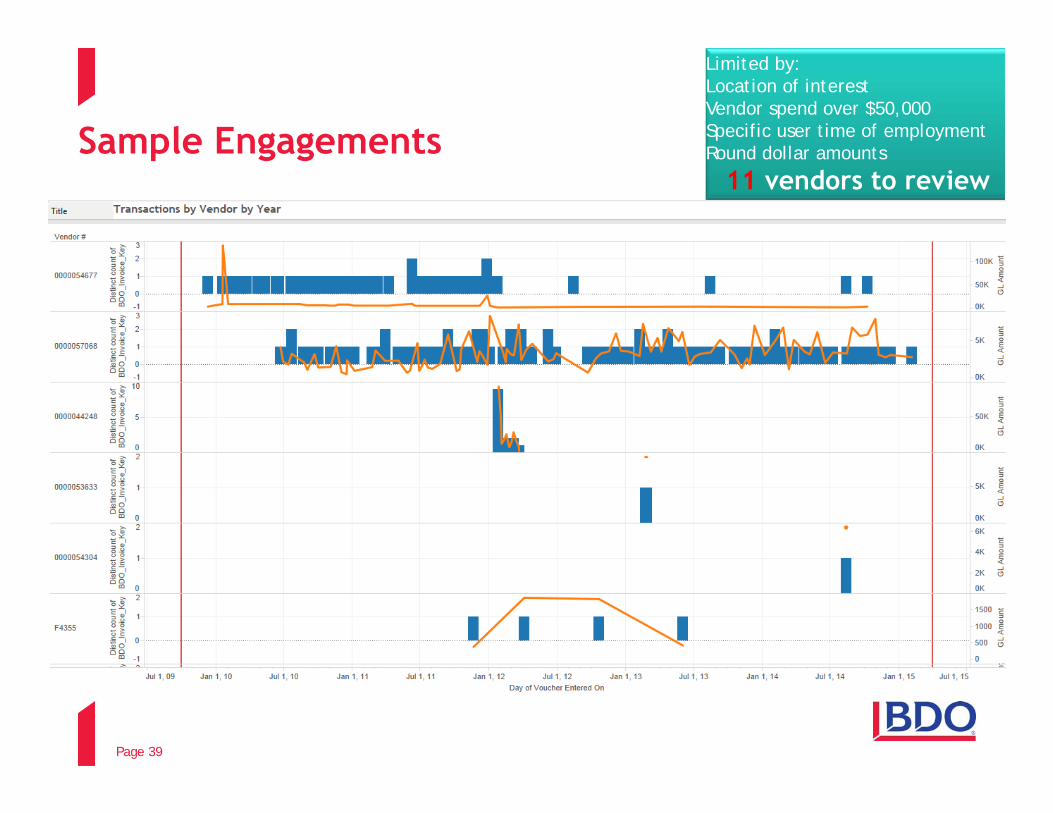

Sample Engagements

Limited by:Location of interestVendor spend over $50,000Specific user time of employmentRound dollar amounts

11 vendors to review

Page 40

Sample Engagements

1 Ghost Vendor from 2010 – 2015

Over $350,000 in False Payments

Page 41

Sample Engagements

Page 42

Sample Engagements

Page 43

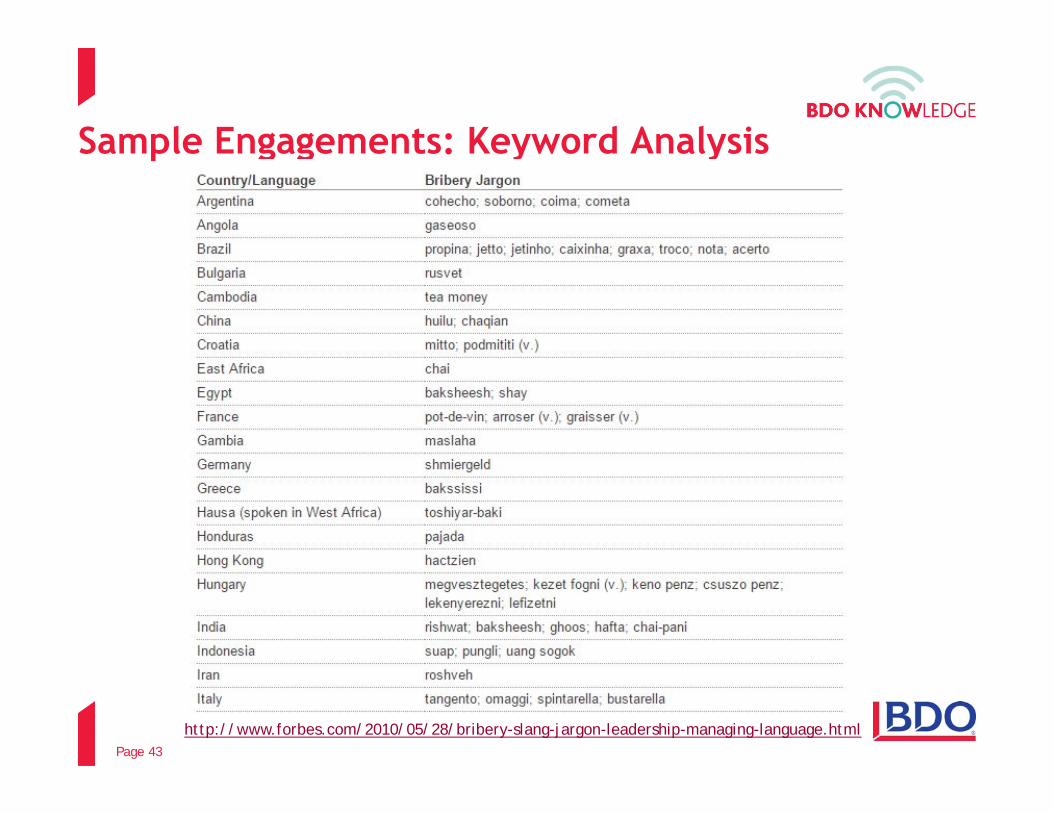

Sample Engagements: Keyword Analysis

Page 43http://www.forbes.com/2010/05/28/bribery-slang-jargon-leadership-managing-language.html

Page 44

Sample Engagements: Keyword Analysis

Page 44http://www.forbes.com/2010/05/28/bribery-slang-jargon-leadership-managing-language.html

Page 45

Sample Engagements: Keyword Analysis

Page 45

Page 46

Sample Engagements – Vendor Geographic Review

Page 47

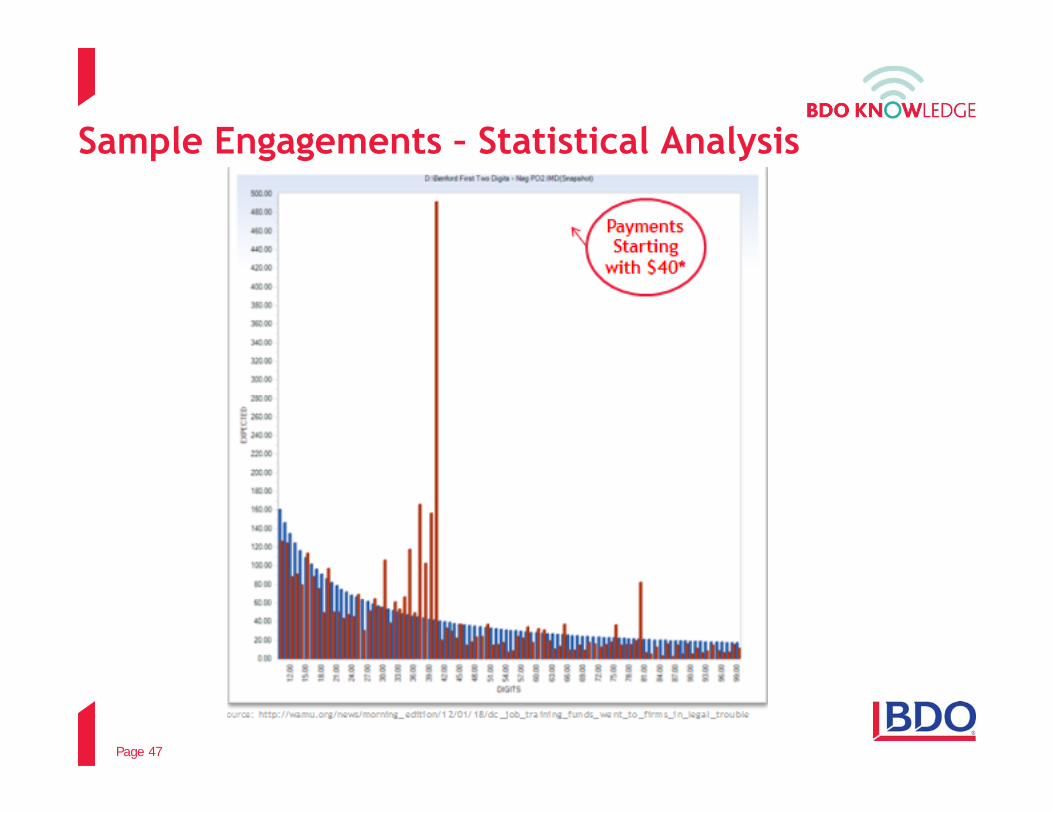

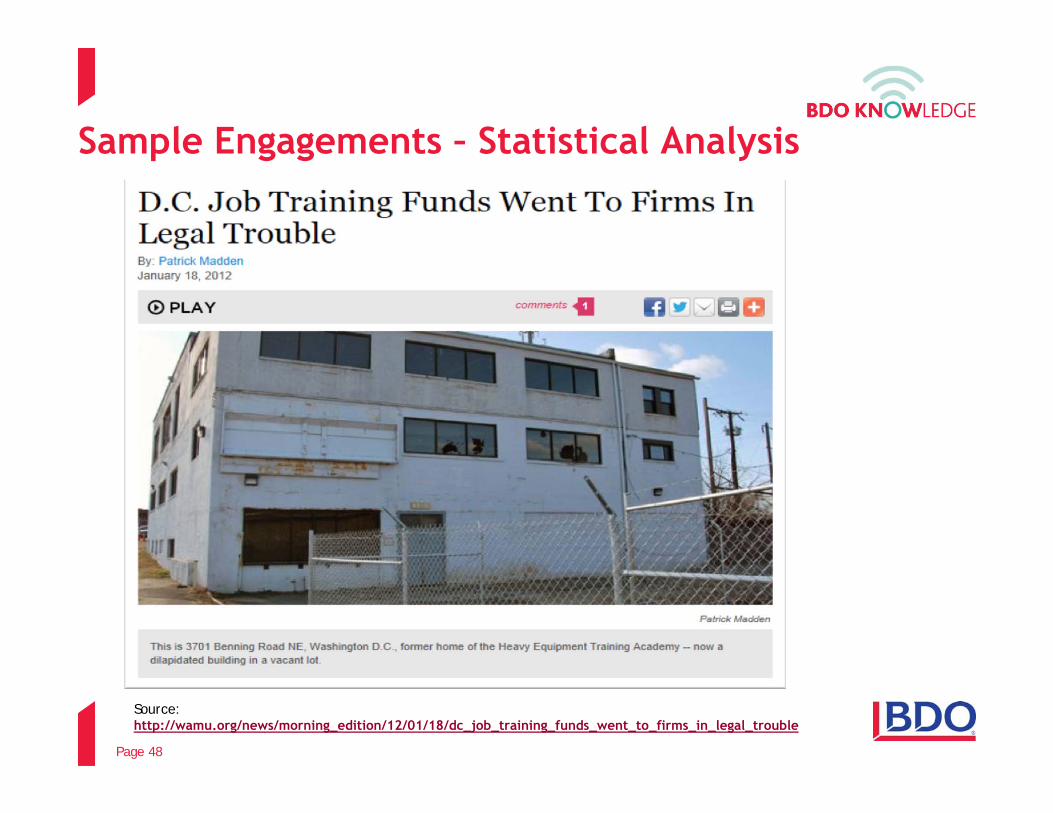

Sample Engagements – Statistical Analysis

Page 47

Page 48

Sample Engagements – Statistical Analysis

Page 48

Source: http://wamu.org/news/morning_edition/12/01/18/dc_job_training_funds_went_to_firms_in_legal_trouble

Page 49

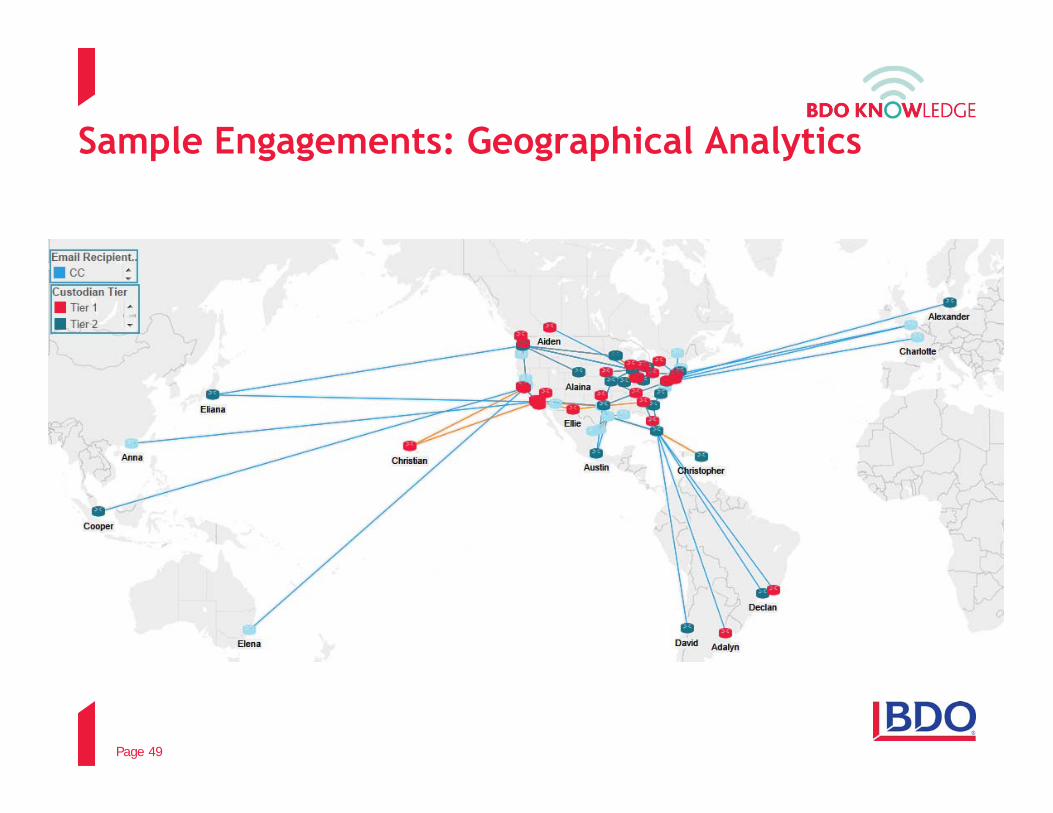

Sample Engagements: Geographical Analytics

Page 50

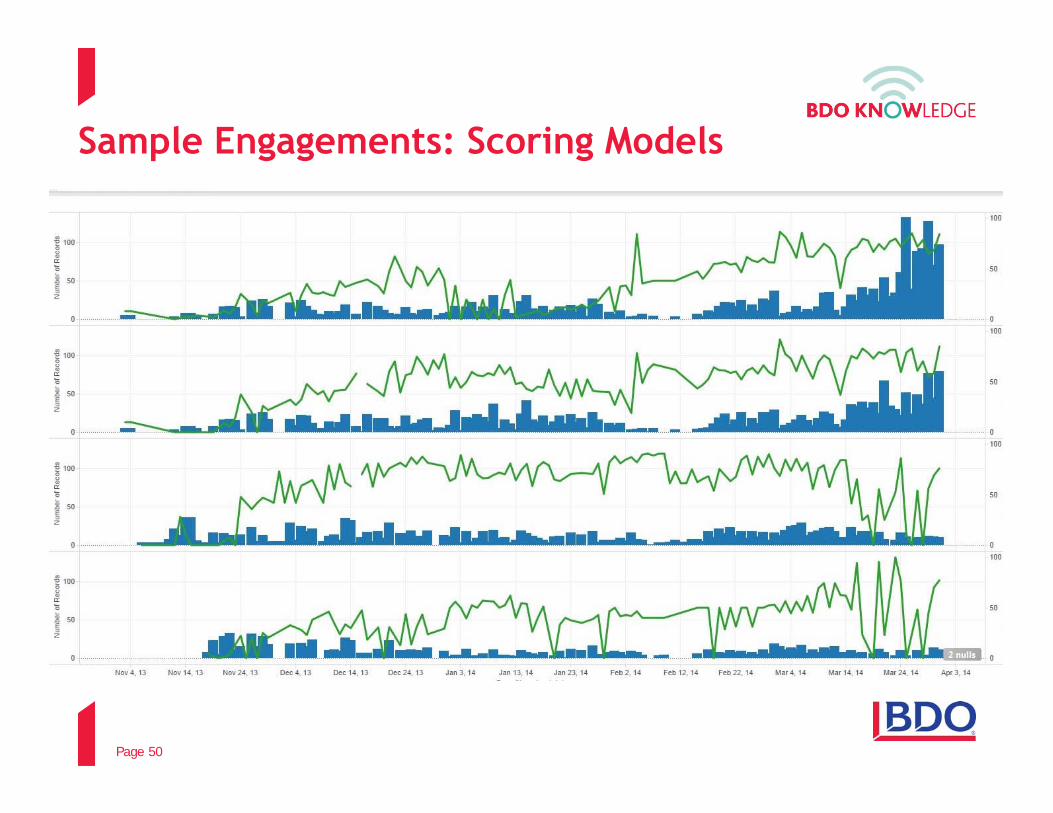

Sample Engagements: Scoring Models

Page 50

Page 51

Due Diligence – Significant Third Parties• Risk-based, considering:

o Type of Engagement o Risk of Transactiono Qualifications & associations of

3rd party: Reputation & Legitimacy Experience/Education Relationships with

government officialso Understanding of business

rationale for appointment Role vs. legitimate business

purpose Timing of business need Payment terms (country,

timing, currency) Compensation (vs. amt of

work, industry, country)

• Ongoing monitoringo Update DD periodicallyo Exercise audit rightso Annual certificationso Activity reports o Payments and banks

• Awareness of Company Programo Certification of compliance o Periodic Training

• Approvals of persons with 1st-Hand Knowledge of:

o Qualifications of 3rd Party & Business

o Due diligenceo (For payments) Performance and

activity reported

Page 52

Due Diligence: M&A Target or JV Partners

Pre-Transaction Due Diligence:• If Company has “control” over

resulting entity, then higher level of due diligence• “Control”: 50% or more

ownership OR Managerial control (i.e., responsibility for governance of entity)

• Vet all third- parties if possible• If corruption, • Negotiate for cost of bribery• Voluntarily disclose• Cooperate in investigation

Post-Transaction Due Diligence:• Incorporate acquired company

into anticorruption program asap• Train new employees• Evaluate target’s third parties

under company standards• Audits of new business units

Page 53

Due Diligence: Methods of Maximizing Resources

1. Outsourcing: BDO, Baker & McKenzie, TRACE, Red Flag Group, Kroll, etc.a. Pros: Experience, alleviates workload, objectivityb. Cons: Cost, lacking knowledge of business purpose,

remuneration & industry 2. Toolkits:

a. Pros: Cost, provides best practices, templatesb. Cons: No substitute for expertise

3. Data Analytics:a. Pros: Excellent ongoing monitoring, flags information

that cannot be spotted in due diligenceb. Cons: Not a substitute but a supplement to due

diligence

Page 54

GiftsBusiness Purpose: • Before, during, after meeting• Never right before an award of

business• For traditional season and holiday

gift givingMust be reasonable and customary:• Never cash• Generally, no more than 4x per

year• Market value less than $40• Promotional items (hats, pens,

etc. with logo) generally okay• Rule of Thumb For “Reasonable”

Gifts: Company promo catalog

Must be legal in country!• Many countries prohibit any gift

to government officials (e.g.,US)

Review & Approval: Requirement to seek approval from Law/Compliance before: • Giving gifts to “Government

Officials” or • to anyone if outside guidance

Page 55

Hospitality (i.e., Travel & Entertainment)

Business Purpose: • Contract negotiation or

demonstration/explanation of products or services

• Never offered to wrongfully influence recipient for biz advantage

Must be legal in country! • Many countries prohibit or limit

gifts/hospitality to government officials or private customers

• Many online resources for legal guidance

Must be reasonable & customary• All invitees must be relevant to

business purpose (no spouses)• Reimbursement or per diems to

invitees should not allowed• Meals: Generally …• No more than 2x per month • Maximum amounts per country?

Public sources are available (e.g., State Department per diem rates)

Review & Approval:• Requirement to seek approval from

Law/Compliance before: o Long distance travel, lodging or

entertainment for “Government Officials”

o To anyone if outside guidelines

Page 56

Gifts/Hospitality: Methods of Maximizing Resources

1. Country Guides: e.g., BDO, Baker & McKenzie, TRACE, In-Housea. Pros: Proactive – before offer, legal precisionb. Cons: Difficult to implement - “one size fits all” may be

easier to understand & audit2. Ongoing Auditing/Monitoring: IT controls (e.g., Concur),

data analytics (IDEA, ACL, Tableau, SQL Server)a. Pros: Proactive control – before recording, cost savings,

better prevention/detectionb. Cons: Depends on completeness and reliability of data

(e.g., due to legacy systems, differences in fields, human error/integrity when inputting data)

Page 57

Sample Engagements: Expense Fraud

Page 57

Page 58

Periodic Assessments & Monitoring• Understand risk to allocate resources appropriately• Consider risk factors :

o Country and industry sectoro Size and type of business opportunity o Potential business partnerso Level of involvement with governments o Amount of government regulation and oversight, o Exposure to customs and immigration in conducting business

affairs• Require regular review & improvement

o Employee surveys & self assessmentso Control testing (“specific audits”)o Risk Assessmentso Data analytics

Page 59

Julia K. Bailey serves as a Managing Director with nearly 20 years ofexperience in providing international, political and regulatory complianceservices.Prior to joining BDO, Julia held counsel and compliance leadership roleswith several Fortune 100 corporations. She served as Assistant GeneralCounsel, International Transactions and Compliance of HoneywellInternational, Inc., where she managed all aspects of global anti-corruption and political compliance programs. She also served as AssociateGeneral Counsel of International & Domestic Compliance at BAE Systems,Inc. and as Special Counsel, International for Northrop GrummanCorporation. Julia is a regular speaker on topics ranging from anti-corruption, ethics and compliance, international trade, and corporatepolitical activities, among others.Julia is a licensed attorney, certified Six Sigma Black Belt, and corporateleader with a focus on developing and implementing proactive compliancemeasures, as well as anticorruption due diligence, risk assessments andinvestigations for Fortune 100 organizations, domestically and abroad.

Julia K. Bailey, JD, MBA, BA

Managing Director, BDO ConsultingWashington, DC

T + 1 202 644 [email protected]

Presenter

Page 60

Howard Weissman is a counsel in Baker & McKenzie's Compliance &Investigations Practice Group in Washington, DC. He has decades ofexperience in advising on US laws and regulations directly impactinginternational business operations such as the Foreign Corrupt PracticesAct (FCPA) and US antiboycott laws, International Traffic in ArmsRegulations, Export Administration Regulations, and foreign agency andanti-bribery laws. Howard has designed and implemented corporate anti-corruption compliance programs and training programs. He served as vicepresident and associate general counsel at Lockheed Martin Corporation,where he worked for more than 25 years.Howard advises on the structuring of transactions to comply with theFCPA and related laws. He also supervises and participates in conductinginternal investigations and audits to determine compliance with suchlaws and regulations, and advises on the consequences of suchinvestigations and audits, including the development of appropriatedefenses, disclosures, disciplinary actions and compliance policies. Hehas conducted FCPA due diligence for numerous proposed acquisitions, aswell as on proposed international joint venture partners, teammates,consultants, distributors, and other third parties and also advises on USantiboycott laws and on international consultant-related matters.

Howard O.Weissman

Baker & McKenzie LLPWashington, DC

T + 1 202 452 [email protected]

Presenter

Page 61

Kirstie L. Tiernan is a Director in BDO Consulting’s Chicago office withover 10 years of experience providing data analysis, IT consulting, digitalforensics and e-discovery services. A Certified Fraud Examiner and anOracle Certified Associate, Kirstie regularly conducts fraud investigationsand Foreign Corrupt Practices Act compliance reviews, in addition toproviding fraud prevention services across various industries.

Kirstie is experienced in managing fraud detection and preventionanalysis projects requiring the collection of entire general ledger systemsdata from multiple sources such as Peoplesoft, SAP and Oracle. Sheapproaches projects with a focus on process efficiency, regularlyimplementing technological advancements within systems and databasesin order to improve and accelerate time-consuming clientprocesses. Kirstie also conducts anti-bribery compliance reviews, havingmanaged engagements at several Fortune 500 companies, as well as aninternational review at a Fortune 10 client that resulted from allegationsof Foreign Corrupt Practices Act violations.

Kirstie TiernanCFE, OCA

Director, BDO ConsultingChicago, IL

312-616-4638T + 1 312 616 [email protected]

Presenter

Page 62

Additional resources accessible via BDO Board Governance:https://www.bdo.com/services/assurance/board-governance/overview

Recent BDO Publications:• SEC Adopts Rule for Pay Ratio Disclosure• Continuous Monitoring• Q2 2015 Significant Accounting and

Reporting Matters• SEC Proposed Rules Requiring Clawback of

Executive Compensation• 2015 BDO IPO Halftime Report• SEC Issues Concept Release Seeking

Comment on Possible Revisions to Audit Committee Disclosures

• PCAOB Issues Proposals to Improve Transparency and Provide Insight Into Audit Quality

• PCAOB Audit Committee Dialogue and Other Resources

• SEC Adopts Amendments to Regulation A• External Auditor Assessment Tools• Audit Committee Disclosure Resources• SEC Proposal on Pay vs. Performance

Disclosures• FASB ASU on Going Concern• PCAOB AS 18 – Related Party Transactions• Center for Audit Quality Approach to Audit

Quality Indicators

BDO Board Governance

For a complete listing of BDO publications, refer to: https://www.bdo.com/insights/

Page 63

BDO Board GovernanceUpcoming BDO Governance and Financial Reporting Knowledge Webinars: • Quarterly Technical update (Q3 2015) – October 7, 8, and 9• Establishing an Effective Internal Audit Function* - October 22• Effective Audit Committees – November 9*• Quarterly Technical Update (Q4 2015)* - January 7, 8, and 11

*Registration will be available shortly on https://www.bdo.com/events

Recent Archived Webinars: • Revenue Recognition Transition Resource Group 2015 Update• Quarterly Technical Update (Q2 2015)• Data Analytics and Risk Management – A Board Primer

Page 64

Evaluation

We continually try and improve our programming and appreciate constructive feedback.

Following the program, we will be sending out a thank you e-mail that contains a link to a brief evaluation.

Thank you in advance for your participation!

Page 65

ConclusionThank you for your participation!Certificate Availability – If you participated the entire time and responded to at least 75% of the polling questions, click the Participation tab to access the print certificate button.

Group Participation Reminder – to receive credit:• Sign-in sheets must list a Proctor name and CPA license number.• Clients and Contacts – Email sign-in sheets to [email protected] w/in 24 hours of the webcast.• BDO Alliance USA – Should proctor their own group participants. This process is detailed in

the LearnLive Participant Guide on the Alliance Portal > Resource Center. Call LearnLive Support for questions – 1-888-228-4088.

• BDO International - Unfortunately, we cannot currently support group CPE for International Firms. Those requesting CPE must have registered and participated from their own computer.

• BDO USA ‒ Submit your sign-in sheets using a General Training & Development Request in BDO Service Now found at: https://apps.bdo.com > A to Z > BDO Service Now > Click “Request” in the upper right menu, then chose “Training & Development” from the Filter Category drop-down, click on “Training & Development Support”.

Please exit the interface by clicking the red “X” in the upper right hand corner of your screen.

Page 66

BDO is the brand name for BDO USA, LLP, a U.S. professional services firm providing assurance, tax, financial advisory and consulting services to a wide range of publicly traded and privately held companies. For more than 100 years, BDO has provided quality service through the active involvement of experienced and committed professionals. The firm serves clients through 58 offices and more than 400 independent alliance firm locations nationwide. As an independent Member Firm of BDO International Limited, BDO serves multi-national clients through a global network of 1,328 offices in 152 countries.

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms. BDO is the brand name for the BDO network and for each of the BDO Member Firms. For more information please visit: www.bdo.com.

Material discussed is meant to provide general information and should not be acted on without professional advice tailored to your firm’s individual needs.

© 2015 BDO USA, LLP. All rights reserved.