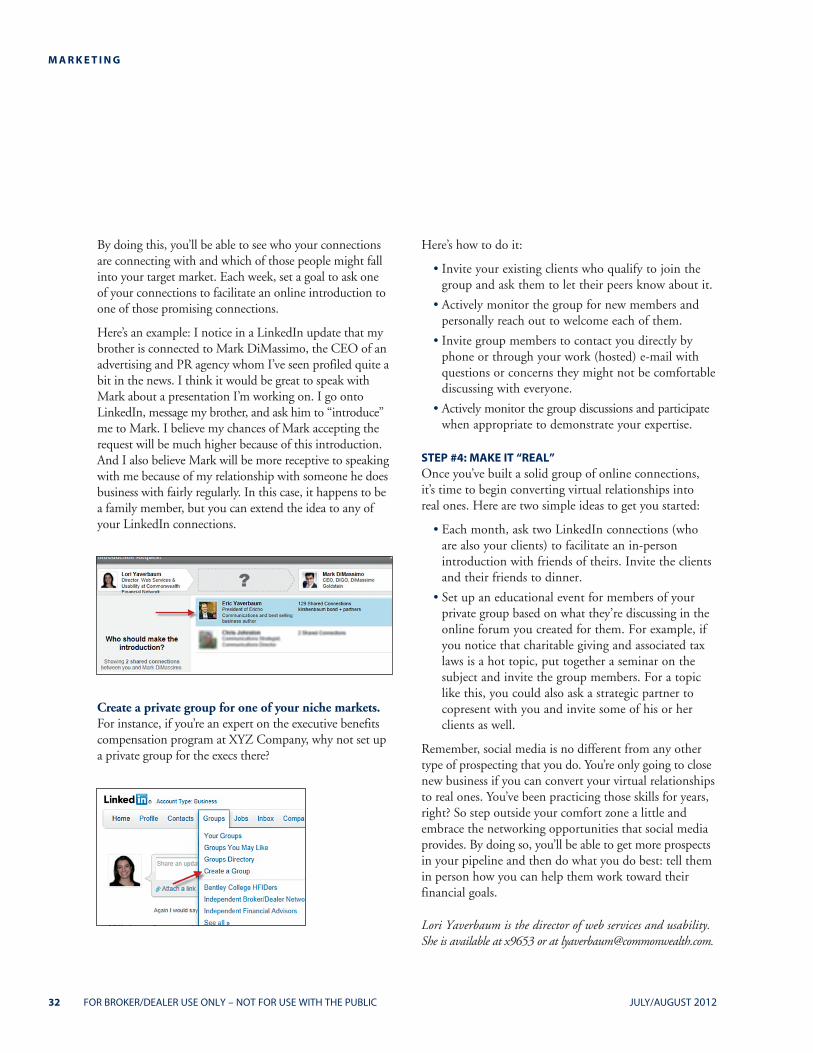

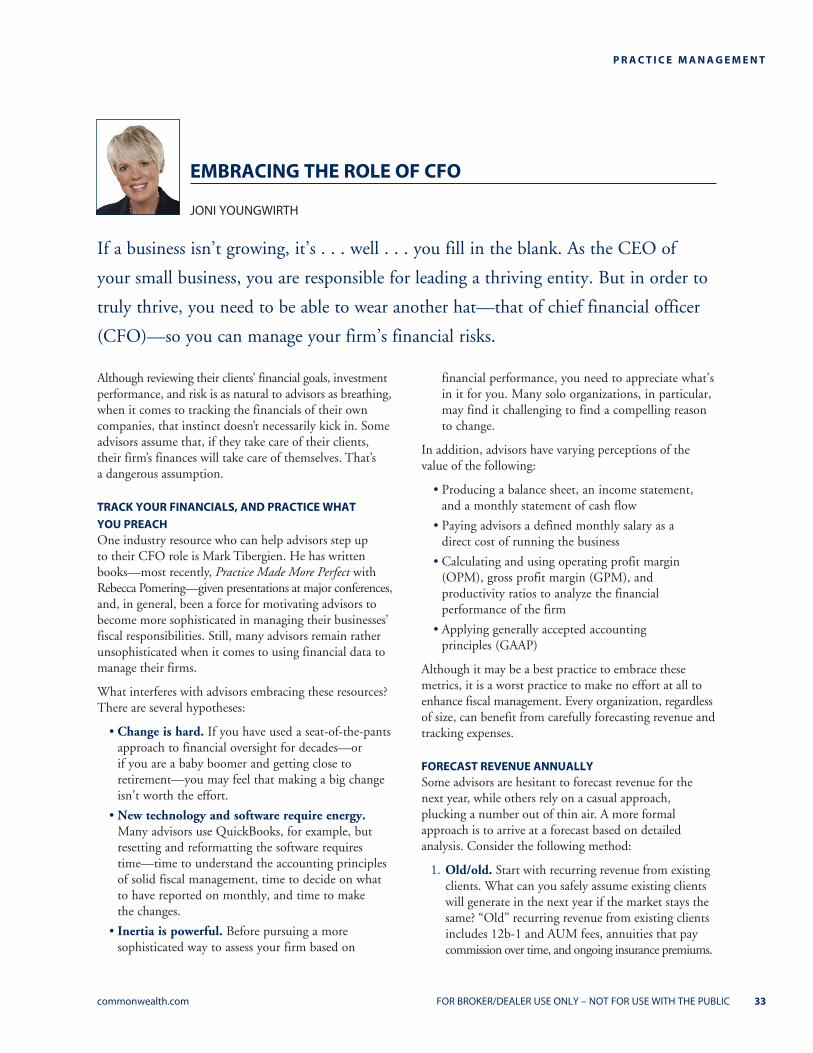

Test on Guest

52

CBR COMMONWEALTH BUSINESS REVIEW TAKING THE LEAD TO SECURE YOUR CLIENTS’ FINANCIAL WELL-BEING POWERFUL NEW TECHNOLOGY HELPS YOU STAY AT THE HEAD OF THE RETIREMENT PLAN PACK WHEN IT COMES TO INFORMATION SECURITY, KEEP AN EYE ON THE WEAKEST LINK EMBRACING THE ROLE OF CFO Don’t leave your firm’s fiscal management to chance. Adopting a more formal approach to forecasting and tracking your financials can help lead your business to greater prosperity. JULY/AUGUST 2012

-

Upload

commonwealth-financial-network -

Category

Documents

-

view

227 -

download

1

description

Test on Guest wifi

Transcript of Test on Guest

CBRCOMMONWEALTH BUSINESS REVIEW

TAKING THE LEAD TO SECURE YOUR CLIENTS’ FINANCIAL WELL-BEING

POWERFUL NEW TECHNOLOGY HELPS YOU STAY AT THE HEAD OF THE RETIREMENT PLAN PACK

WHEN IT COMES TO INFORMATION SECURITY, KEEP AN EYE ON THE WEAKEST LINK

EMBRACING THE ROLE OF CFO

Don’t leave your firm’s fiscal management to chance. Adopting a more formal approach to forecasting and tracking your financials can help lead your business to greater prosperity.

JULY/AUGUST 2012

F R O M T H E E D I T O R

CREATING A LEGACY OF LEADERSHIP

KATE FLOOD

The essence of leadership encompasses so much more than these simple words. It involves creating our own opportunities to learn and to grow. It is about having a vision and a purpose for moving forward. It means inspiring ourselves and others to make better decisions. And it’s about leveraging the talents of those around us to find newer and better ways to accomplish goals, whether they be financial, professional, or personal. The Commonwealth community is full of advisors (see p. 7) who embody these traits and have successfully led their organizations—and, more important, their clients—to financial freedom.

To help our advisors continue to hone these essential skills, the Commonwealth home office staff has contributed a collection of insights and ideas—running the gamut from risk management, to operational efficiency, to information security. Here’s a preview.

The biggest threat to a portfolio isn’t a market downturn; it’s a death, disability, or extraordinary medical or long-term

care expense. For many advisors, though, talking about insurance can be uncomfortable. But that doesn’t remove your obligation to identify your clients’ goals and the effect of common risks on those goals. By following some of the guidelines shared in “Taking the Lead to Secure Your Clients’ Financial Well-Being” (p. 8), you’ll be better prepared to counsel your clients to make better decisions.

New to the qualified plan marketplace? Looking for ways to make your existing retirement plan business more efficient? Commonwealth’s Retirement Plan Manager (RPM) can help. Combining a custom IPS engine, RFP portal, and CRM tool, RPM makes it easy to deliver the full range of services your plan sponsor clients need. Learn more in “Powerful New Technology Helps You Stay at the Head of the Retirement Plan Pack” (p. 24).

“When It Comes to Information Security, Keep an Eye on the Weakest Link” (p. 28) examines the current environment, in which cyber crooks are increasingly setting their sights on clients’ e-mail accounts, hoping to perpetrate wire fraud schemes. In light of recent attempts to defraud Commonwealth advisor offices in this way, it’s more essential than ever to educate your clients about protecting their e-mail accounts from hackers. Their best defense? A strong password.

Through the Commonwealth Business Review, we continue to provide you with the thought leadership you need to create a lasting legacy of leadership in your businesses and your lives. If you have questions or comments, or ideas for future stories, we’d love to hear from you.

Kate Flood is the editor of the CBR. She is available at x9606 or at [email protected].

As Commonwealth Chairman Joe Deitch discusses in this issue’s editorial,

it’s easy to refer to someone at the head of an organization as a leader

and to his or her actions as leadership. But what does that really mean?

Be sure to check out our online exclusives (highlighted on p. 4) for additional valuable content from our subject matter experts.

CONTENTS

EDITORIAL

5 Leadership: The Multiplier Effect

WEALTH MANAGEMENT

8 Taking the Lead to Secure Your Clients’

Financial Well-Being

11 The Light at the End of the Tunnel

14 Standing Watch: A New Era of Due Diligence

16 A Good Time, a Terrible Time, or Just in Time?

Notes on the Insurance Industry

18 Keeping Your Clients’ Beneficiary Designations

Up to Date—And Your Name Out of the Press

21 Fixed Income Research: Supporting Your

Investment Needs and Goals

RETIREMENT

24 Powerful New Technology Helps You Stay at the

Head of the Retirement Plan Pack

COMPLIANCE

26 Leading by Example Can Help Your Firm

Stay Compliant

TECHNOLOGY

28 When It Comes to Information Security,

Keep an Eye on the Weakest Link: Your Clients

MARKETING

30 Using Social Media to Get Real-Life Results

PRACTICE MANAGEMENT

33 Embracing the Role of CFO

36 You’ve Hired a New Employee—Now What?

39 Commonwealth Mentors: Advisor Stories of Success

and Inspiration

BULLETIN BOARD

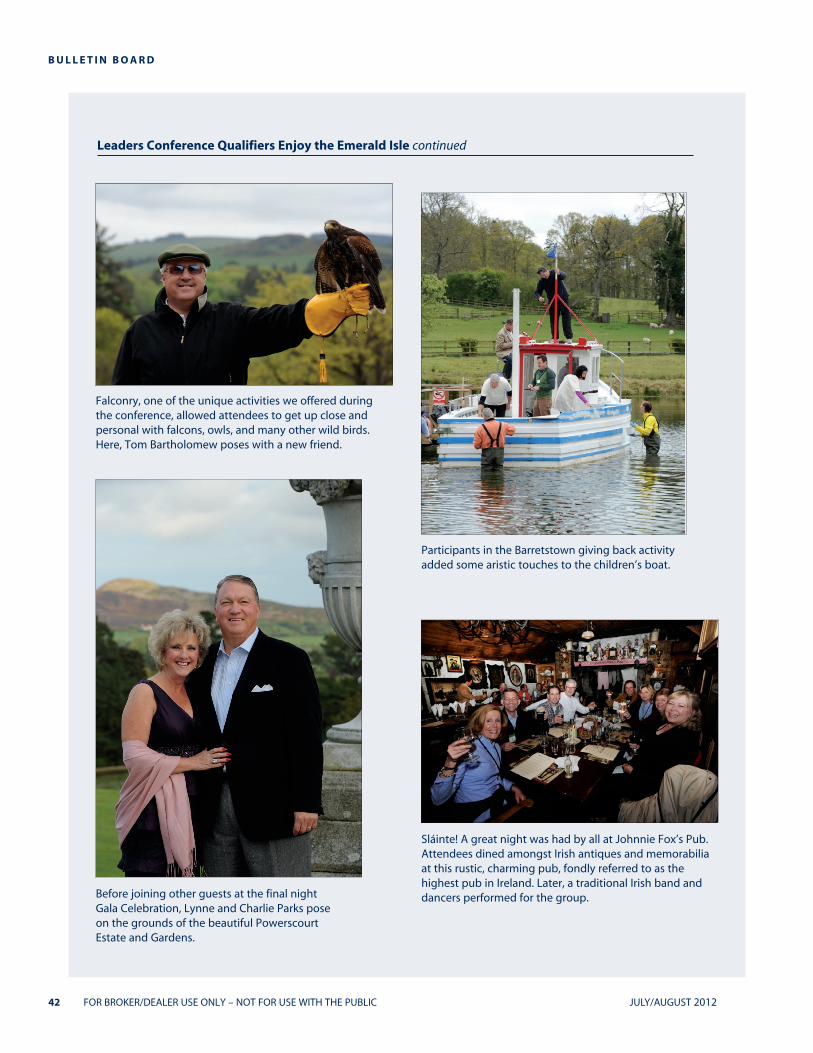

41 Leaders Conference Qualifiers Enjoy the Emerald Isle

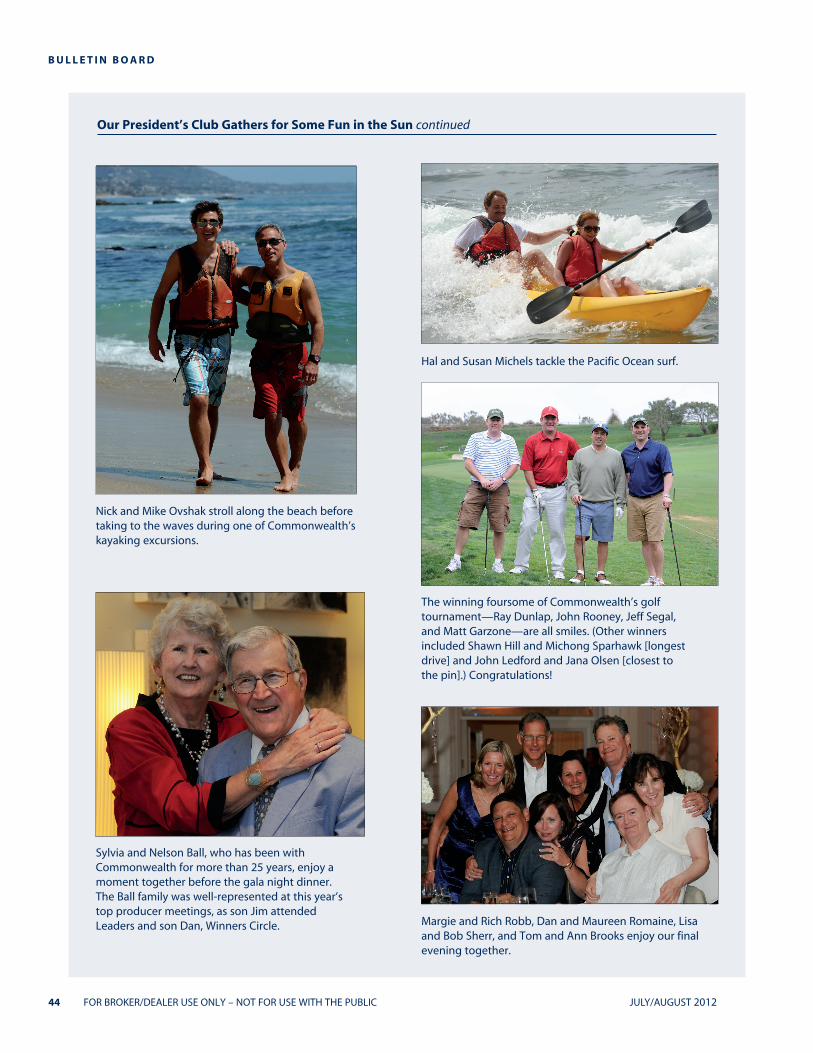

43 Our President’s Club Gathers for Some Fun in the Sun

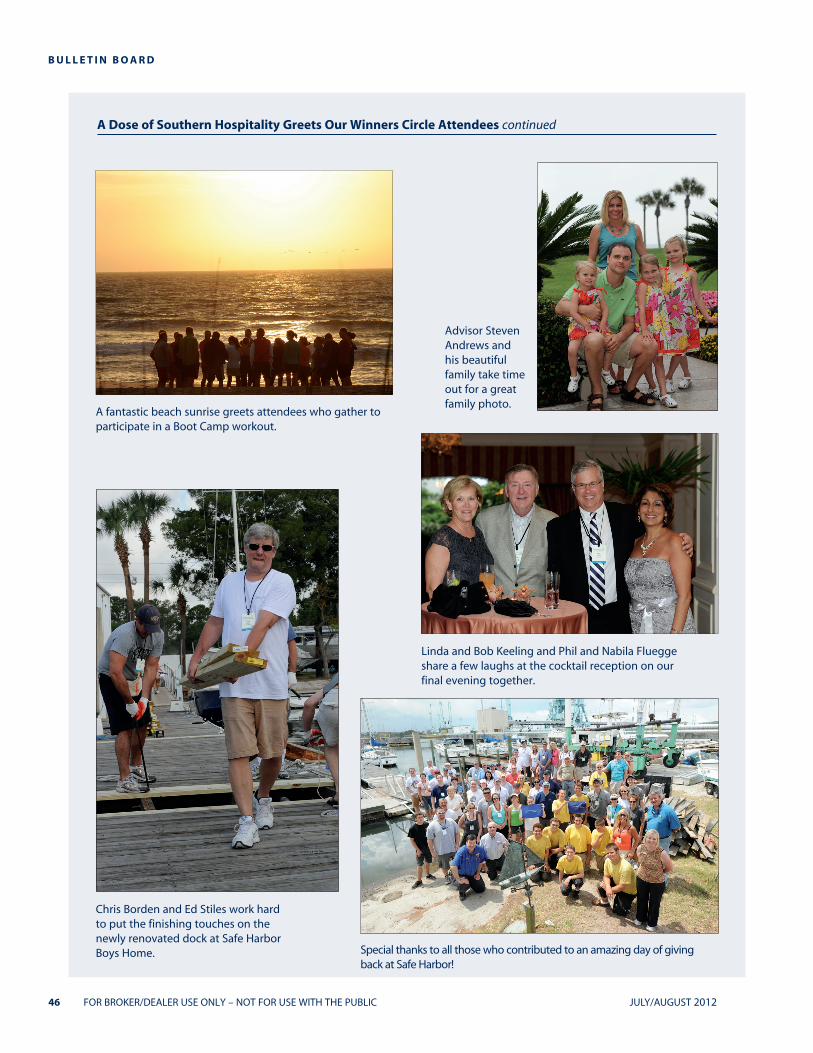

45 A Dose of Southern Hospitality Greets Our

Winners Circle Attendees

47 Commonwealth Cares Goes Macho for a Worthy Cause

48 A Welcome to New Advisors

49 Looking Forward to These Events . . .

49 2013 Top Producer Meeting Requirements

50 Top 10 Clubs

ON THE COVER:

Embracing the Role of CFO (p. 33)

Although reviewing their clients’ financial goals, investment performance, and risk is as natural to advisors as

breathing, when it comes to tracking the financials of their own companies, that instinct doesn’t necessarily kick in.

From forecasting revenue, to creating an annual budget, to benchmarking, these tips can help you embrace your

inner CFO so you can lead your firm to even greater prosperity.

JULY/AUGUST 2012CBRCOMMONWEALTH BUSINESS REVIEW

TITLE

AUTHOR

e C B R

wealth management | retirement | technology | compliance | practice management | bulletin board

BULLETIN BOARD

THERE’S MORE ONLINE!Looking for additional ideas and strategies for your business? Check out our online exclusives in the eCBR. (From the homepage of COMMunity Link®, click on More eCBR in the bottom right corner of the eCBR widget.)

WEALTH MANAGEMENT

Asset-Based Products: The Easy Long-Term Care Conversation— Susan Kobara, CLTC

As an advisor, one of your roles is to take an investment set aside for a specific purpose and move it into another investment set aside for the same purpose but with a potentially better outcome. And that’s just what asset-based long-term care products seek to do—provide a potentially better outcome for liquid assets set aside for emergency health care costs. Put that way, you may find the long-term care conversation less daunting than you imagined.

Bringing Fixed Income to the Unified Managed Account— Alicia Nisberg, CIMA®

Commonwealth’s Preferred Portfolio Services® Direct SMA/UMA platform has become an efficient choice for higher-net-worth investors, but it has been missing a key feature that many clients and advisors have asked for: the ability to hold bonds instead of fixed income mutual funds or ETFs. Now, with new technology, Envestnet, our overlay manager, can offer bond SMAs as sleeve options. Learn more about our first offering from Strategic Partners Investment Advisors.

Yield of Dreams: Finding Income in a Low-Yield Environment— Brian Glazer

With current interest rates close to zero, the need for investments that can generate retirement income is higher than ever. But that doesn’t mean that investors should blindly reach for yield. Here, we highlight various types of investments—including equity-income mutual funds, dividend-paying ETFs, and individual stocks—that have the potential to produce “safer and realistic” income, listing their pros and cons and when you might want to consider them for a portfolio.

PRACTICE MANAGEMENT

10-Point Financial Check-Up— Kenton Shirk

Practice Management has introduced a new tool to help you assess 10 critical levers that impact your firm’s profitability, including gross profit margin, operating profit margin, client revenue distribution, and other productivity measures. Each report is customized for your firm and compares your metrics with those of other financial advisory firms within a similar revenue range.

BULLETIN BOARD

Names in the News— Emily Guadagnoli

Read about Commonwealth advisors who have been recognized by and quoted in the financial industry press.

ARCHIVES Our comprehensive archive of online exclusives and print stories dates back to 2006. You can search by topic, author, or other keywords, or simply browse through historic content. Printer-friendly versions of articles are available at the click of a button. You’ll also find downloadable PDFs of our print issues.

Leaders possess a powerful combination of passion and purpose, and the more effective ones seem to be able to multiply the results of their followers more so than managers can. Given the enormous effect leaders can have, perhaps we need a better approach for understanding and learning from them—so we can emulate their positive attributes and apply them to our own lives, families, and businesses.

This discussion raises certain questions, such as:

• What’s the difference between a great leader and a great manager?

•Is leadership an innate talent or can it be taught?

•How do we measure leadership?

•How do we teach it?

•How do we ourselves become better leaders?

BACK TO SCHOOLThese issues became a priority for me last year when I received approval to create a leadership institute at my high school, Boston Latin School. Established in 1635, Boston Latin is the oldest public school in the U.S. Its halls are filled with the names and pictures of many of our country’s founding fathers . . . because that’s where they went to school!

As a kid growing up in the poor part of Boston, I thought this was pretty normal. In retrospect, I can say only that it was my normal. Regardless of where we see their names—on school walls or in books, on TV or on the Internet—all of us are surrounded by innumerable examples of leaders and leadership. So where do we go and what do we do with this information? This leads me to some basic observations about how we manifest leadership in our lives.

THE ESSENCE OF LEADERSHIPLeadership is about choice. In almost every aspect of our lives, we get to choose how and what we do or don’t do. We may stick our heads in the sand and accept the

status quo, but make no mistake: that is a choice, too. Leaders seem to understand more than most people not only that we have choices, but also that we have opportunities—and that we can choose to create more.

Leadership is about vision—and vision leads to purpose. People often refer to visionaries as those who can see beyond the constraints of their current situation. Is it a special talent? A sixth sense? Is it fueled by a desire to move toward or away from something? Can vision be learned?

Through my own experience, I have come to understand that we are much more than just a brain and much more than just a body. I was in my 30s when I became aware of how my entire being was designed to create a greater level of awareness. My biological computer wasn’t confined to my skull; it encompassed my entire body. I just had to learn to listen to it and use it better. And with increased awareness and practice came increased understanding.

But our powers aren’t confined to our physical being. We are electromagnetic entities. We emit and receive energy constantly. So does everything and everyone around us. The more we become attuned to this energy, the better we can see. There’s a tendency to ascribe such insights to some mysterious realm. Some call it intuition while others may explain it in more spiritual terms. Regardless of how we choose to describe it, we are absolutely part of something beyond the physical. And, like any other muscle, the more we choose to exercise and grow our awareness, the stronger this ability gets.

Leadership is about inspiration. Vision leads to both passion and purpose. Managers understand, organize, and execute. Leaders inspire. Managers operate mountains. Leaders move them! Both are valuable talents, but they are inherently different. The currency of leadership is energy. Energy can be communicated, but it’s much more than information—it is nourishment. Leaders get others to tap into this energy, to believe and then to act. And then, acting together, and with their energy multiplied, they effect change.

E D I T O R I A L

Leadership is a word that gets tossed around a lot. We tend to think of people at the

helm of an organization as leaders, and what they do to run the organization is

therefore leadership. But it’s much more than that.

commonwealth.com FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC 5

LEADERSHIP: THE MULTIPLIER EFFECT

JOSEPH DEITCH

6 FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC JULY/AUGUST 2012

E D I T O R I A L

That’s when the real magic happens! Because when we realize that we can go above and beyond, our beliefs increase to accommodate this new reality. Pretty soon, these new beliefs and realizations are creating new realities. As someone once taught me, “Whatever you can conceive and believe, you can achieve.”

Leadership doesn’t always involve others, though. The flame starts within, and one person can accomplish an enormous amount simply by putting his or her mind and imagination to work. Frankly, most of the time it’s ourselves we need to inspire! As individual entrepreneurs, there is no one there to lead and manage us.

Leadership is about leverage. This is the multiplier effect. As Archimedes said, “Give me a lever and I can move the world.” Whether you leverage and multiply your efforts by enlisting others or by creating new solutions (or both!), leadership is about getting more done. Certainly more than we could accomplish by accepting the status quo. By having a bold vision, by inspiring ourselves and others, and by creating new and improved methods, we can move mountains.

LEADERSHIP LABAt Boston Latin, our initial challenge in creating the leadership institute was a lack of time. Each day was filled with required classes, sports, clubs, jobs, and family responsibilities. Adding another course would mean deleting something else—and that would be a long, unpleasant battle. So, we came up with the perfect solution: learning by doing. You may want to try it yourself.

The lessons of leadership are relatively straightforward, and our goal is to show the students how to improve what they are already doing. In a sense, their lives are the leadership lab. And so is yours.

Leadership is not rocket science, and it actually helps to keep it simple. The following list is a good start. It only remains to put these lessons to work, or at least to better use:

•Choose to make a difference. Think big.

• Look within. Act in concert with your inner yearnings and intuition.

• Be more aware of your environment. Knowledge is power.

•Recruit team members, mentors, and supporters.

• Brainstorm. Play with ideas and possibilities. Let your minds expand and roam, and then identify and pursue the best options.

• Be aware of what motivates you and others, and then manage everyone accordingly.

• Make goals attainable and then make them happen. Create a sense of success and then a reality of success. Help yourself and others believe.

•Constantly refine and improve.

At Latin, as part of the leadership institute, we are inviting celebrated and successful alumni to visit and share their success stories and to be facilitators and mentors. We’re also sponsoring summer internships at a variety of businesses, as well as creating a mini grant program to fund inspirational student ideas that are intended to create change and foster leadership.

A website is in the works to serve as both a resource for information and archival experiences, as well as a platform for interaction. Often, it is the reinforcing of a lesson or an experience through exploration and sharing that helps it take root and then grow to the next level. For example, a recent luncheon at the school brought together the leaders of various teams and clubs to discuss their leadership experiences and compare notes. Amazing what the head of the school orchestra and the captain of the football team had to offer each other!

LEADERSHIP AT COMMONWEALTHCommonwealth offers similar resources through our corporate networking events, the Commonwealth Forum, and Practice Management programs, plus you may have noticed that we’ve been reaching out to you more over the past few years. This issue of the CBR, for example, is filled with many powerful examples of what we do and how we can help. And you can expect our commitment to continue to increase in the future, as our world and our business become ever more complex.

Any success story is filled with many leaders—and leaders abound both in our home office and in the field (see sidebar). We have a lot to learn from one another, and it all starts with a decision to engage in the process.

Joseph Deitch is the founder and chairman of Commonwealth Financial Network .®

E D I T O R I A L

commonwealth.com FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC 7

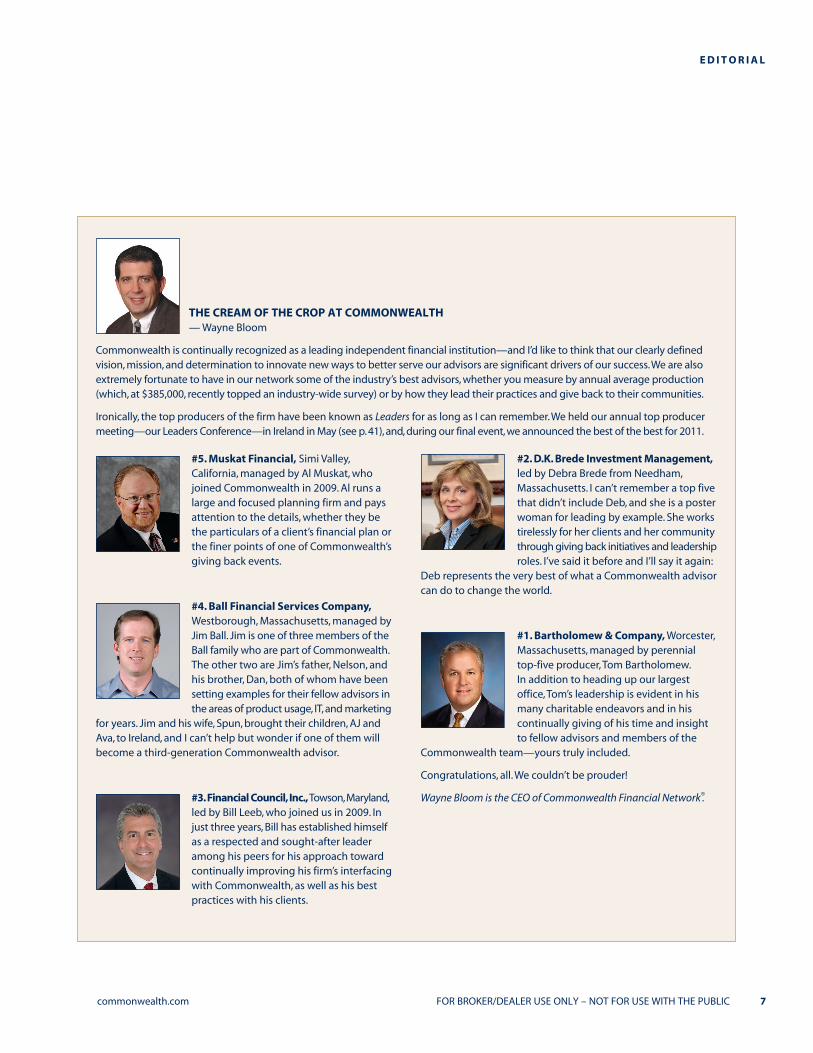

#5. Muskat Financial, Simi Valley, California, managed by Al Muskat, who joined Commonwealth in 2009. Al runs a large and focused planning firm and pays attention to the details, whether they be the particulars of a client’s financial plan or the finer points of one of Commonwealth’s giving back events.

#4. Ball Financial Services Company, Westborough, Massachusetts, managed by Jim Ball. Jim is one of three members of the Ball family who are part of Commonwealth. The other two are Jim’s father, Nelson, and his brother, Dan, both of whom have been setting examples for their fellow advisors in the areas of product usage, IT, and marketing

for years. Jim and his wife, Spun, brought their children, AJ and Ava, to Ireland, and I can’t help but wonder if one of them will become a third-generation Commonwealth advisor.

#3. Financial Council, Inc., Towson, Maryland, led by Bill Leeb, who joined us in 2009. In just three years, Bill has established himself as a respected and sought-after leader among his peers for his approach toward continually improving his firm’s interfacing with Commonwealth, as well as his best practices with his clients.

#2. D.K. Brede Investment Management, led by Debra Brede from Needham, Massachusetts. I can’t remember a top five that didn’t include Deb, and she is a poster woman for leading by example. She works tirelessly for her clients and her community through giving back initiatives and leadership roles. I’ve said it before and I’ll say it again:

Deb represents the very best of what a Commonwealth advisor can do to change the world.

#1. Bartholomew & Company, Worcester, Massachusetts, managed by perennial top-five producer, Tom Bartholomew. In addition to heading up our largest office, Tom’s leadership is evident in his many charitable endeavors and in his continually giving of his time and insight to fellow advisors and members of the

Commonwealth team—yours truly included.

Congratulations, all. We couldn’t be prouder!

Wayne Bloom is the CEO of Commonwealth Financial Network .®

THE CREAM OF THE CROP AT COMMONWEALTH— Wayne Bloom

Commonwealth is continually recognized as a leading independent financial institution—and I’d like to think that our clearly defined vision, mission, and determination to innovate new ways to better serve our advisors are significant drivers of our success. We are also extremely fortunate to have in our network some of the industry’s best advisors, whether you measure by annual average production (which, at $385,000, recently topped an industry-wide survey) or by how they lead their practices and give back to their communities.

Ironically, the top producers of the firm have been known as Leaders for as long as I can remember. We held our annual top producer meeting—our Leaders Conference—in Ireland in May (see p. 41), and, during our final event, we announced the best of the best for 2011.

W E A L T H M A N A G E M E N T

8 FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC JULY/AUGUST 2012

Should I assume that, if they were in fact a health concern, my dentist would have referred me to a doctor? Or did he limit his comments strictly to my dental health?

Like a dentist or doctor, you’re a trusted professional in your field. You may consider yourself a specialist in investment advice, asset management, and retirement planning, leaving insurance, estate planning, and the like to others. But is that how your clients see you? They may well assume that, since you have all the information right in front of you, you would alert them to a potential risk or concern in any area of their financial lives.

ARE YOU DOING ENOUGH TO PROTECT YOUR CLIENTS? The sad truth is that many advisors, even those who call themselves financial planners, don’t always alert their clients to significant and evident risks to their financial well-being. The biggest threat to a portfolio isn’t a market downturn; it’s a death, disability, or extraordinary medical or long-term care expense.

Of course, advisors have plenty of reasons for not discussing insurance with their clients:

• I meant to, but we ran out of time in the appointment.

• Clients would rather talk about making money, not spending money.

• No one wants to talk about death, wheelchairs, or nursing homes.

• The client came to me for investment advice; life insurance is a poor investment.

• I don’t want to be viewed as a “product pusher.”

• If the underwriting goes south, my client might move his investment accounts.

• Insurance is too complicated. I can’t keep up with it.

It all boils down to one excuse, doesn’t it? Many planners simply aren’t comfortable talking about insurance. Even if you are purely an investment advisor, identifying your clients’ goals and the effect of common risks on those goals should be a core competency. Your clients expect and deserve your leadership and counsel.

“One of the great tests of leadership is the ability to recognize a problem before it becomes an emergency.” — Arnold Glasow

I hear many sad stories about clients’ lives that are cut short due to sudden death or acute illness, leaving families in emotional, if not financial, stress. One that comes to mind concerned a widow with two young children. Her advisor relayed his disgust with a local bank that fired the widow because she was taking too much time off, often leaving in the middle of the day. After taking several months of bereavement leave, she had returned to work full-time. Her children, particularly the boy in middle school, were having trouble dealing with grief. Several times a week, she was called away to deal with a child’s sudden illness, depression, or behavior problems. Meanwhile, the advisor was wrestling with how to pay the family’s bills without jeopardizing her retirement or the children’s education.

As I listened to the advisor tell the story, I wondered if he was deflecting his anger at himself onto the bank. Yes, the employer may have been callous, but what about the widow’s life insurance? If the family failed to plan the first time around, what steps had the advisor taken to ensure that it wouldn’t happen again? And what steps would he take to ensure that another client’s family isn’t faced with the same hard choices?

Recently, my dentist asked me to update my medical information and included a list

of possible symptoms and conditions. I checked off that I frequently get cramps in my

feet. After I left the office, it occurred to me that he hadn’t mentioned the cramps.

TAKING THE LEAD TO SECURE YOUR CLIENTS’ FINANCIAL WELL-BEING

TERE D’AMATO, CFP®, CLU®, CHFC®, MSFS

W E A L T H M A N A G E M E N T

commonwealth.com FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC 9

“A leader takes people where they want to go. A great leader takes people where they don’t necessarily want to go but ought to be.” — Rosalynn Carter

We wouldn’t be human if we didn’t try to avoid uncomfortable conversations. In his previous life as a corporate trainer, David Juliano of Commonwealth’s Advanced Planning team helped employees overcome this tendency using a concept called “comfortable versus right.” As David explains, “The idea was to get people to recognize that, in the regular course of conducting themselves in their jobs, they will repeatedly encounter situations where they have to decide what to do. Sometimes it might be tempting to take an easier course because it’s more comfortable, but that route may not be what’s right for the client. This philosophy helped people to pause in those situations and challenge themselves to always do what’s right, even though it might not be the most comfortable.”

Certainly, no one wants to lead clients through the uncomfortable conversation about death, wheelchairs, and nursing homes. But helping them make decisions about the best way to protect their financial futures is simply the right thing to do.

“Leadership should be born out of the understanding of the needs of those who would be affected by it.” — Marian Anderson

Discussing a client’s insurance needs is not the same as “selling insurance.” Although many advisors were introduced to financial services through an insurance company, today’s approach has moved away from “overcoming objections” to consultative selling. Try starting the conversation with open-ended questions like these:

• Is there something going on now that concerns you—an aging parent, a special needs child, health challenges, impending retirement?

• How do you feel this has affected or will affect your financial security?

• Are the consequences of these risks to your investments too large to ignore?

• Do you think your current level of insurance coverage is about right?

• Are your beneficiary selections still valid?

• What do you like about the insurance products you currently own?

•What would you change?

The answers to these questions can reveal the client’s preferences and biases, helping you make better recommendations. Most clients don’t know if their insurance coverage is adequate and will welcome a review.

As you initiate these conversations, don’t discount the sense of security that insurance can provide. I learned this lesson one December day as a young life insurance agent. A stranger walked into my office asking to buy life insurance as a holiday present for his spouse. It won’t surprise you that I was skeptical this gift would meet her expectations. I also suspected that if this stranger wasn’t contemplating suicide, he was scheduled for a major operation. I was wrong. When the policy was issued, the insured asked me to hand-deliver it that night to his wife. As I sat at the dining room table, he turned to me and asked me to tell his wife why he bought the policy. I was about to clumsily say, “It’s your Christmas present!” when he interrupted me. During this holiday season, he wanted her to have as much love, warmth, and security as he and their children received from her. He promised to always

W E A L T H M A N A G E M E N T

be there for her in every way, but if he couldn’t, she would never have to worry about money. She cried; I cried. And they continued to be my very favorite clients through the years.

“Successful leaders . . . don’t tackle things they are not good at. They make sure necessities get done, but not by them. Successful leaders make sure they succeed!” — Peter Drucker

Imagine that a storm is coming. As you go around the house, you find one window stuck open. No matter how much effort you exert, nothing will make it budge. Would you stop there, throw up your hands, and ignore the rest of the open windows? Of course not. You would close the rest of the windows and take measures to minimize the damage from the open one.

Likewise, if you’re not comfortable with your insurance expertise, seek advice from advisors who are. Attend the Commonwealth Insurance Institute, connect with others on the Commonwealth Forum, or turn to Commonwealth’s

Insurance department for point-of-sale support contacts. If you really believe that the client would be better served by someone else, refer him or her to the best professionals in your community.

“You cannot be a leader, and ask other people to follow you, unless you know how to follow, too.” — Sam Rayburn

When was the last time you created a comprehensive financial plan for you and your family? When Commonwealth advisor John Augustine was asked what he would say to someone looking to integrate insurance into the financial planning process, he replied, “Do you own it yourself? Ask yourself who you love and care about; what would life be like for these people if you died or needed 24-hour care? Have you adequately provided for them? If not, insurance can do something that no other financial product can—create money when it is most needed.”

Tere D’Amato is the vice president of advanced planning. She is available at x9168 or at [email protected].

10 FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC JULY/AUGUST 2012

Simple can be harder than complex: You have to

work hard to get your thinking clean to make it

simple. But it’s worth it in the end because once

you get there, you can move mountains.

— Steve Jobs

W E A L T H M A N A G E M E N T

commonwealth.com FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC 11

W E A L T H M A N A G E M E N T

As we look at the trajectory of the U.S. economic recovery, once again this year we

see a light at the end of the tunnel and wonder if it is an oncoming train. Although

improvements in 2010 and 2011 did indeed end up derailing, it looks, at this point,

as if 2012 may bring the start of sustainable growth. The end result remains vulnerable

to outside influences, though, so the real question here is, How will we know?

THE LIGHT AT THE END OF THE TUNNEL

BRAD MCMILLAN, CFA®, CAIA, MAI, AIF®

THE BRIGHT SPOTS: EMPLOYMENT AND HOUSINGWhen it comes to sustainable growth, the key indicator I focus on is employment, as employment generates wage income, which is the base of consumption. Because consumption accounts for over two-thirds of our economy, without growing employment, nothing else can grow with any lasting momentum.

The 2012 employment picture has been encouraging, and, despite some recent weakness, the numbers seem to indicate that the recovery is still on track. Unemployment currently stands at 8.2 percent, and the economy continues to add jobs, albeit at a sometimes anemic rate. These increases in employment have been accompanied by growth in incomes, which has helped to support an increase in consumer spending. While there has also been some drawdown in the savings rate, it is not yet at a problematic level. To me, this suggests that continued income growth will allow continued spending growth, at the same time as saving continues.

Employment isn’t the only bright spot, however. Other positive factors in our economy include the apparent stabilization of the housing market, which has been hovering at depressed levels for several years. Housing is a foundational component of any recovery, and we’re starting to see rising prices in some markets, as well as

an uptick in housing starts. Combine that with current record-high affordability levels, record-low mortgage rates, and rising rents, and you’ve got a recipe for a continued recovery.

Similarly, demand for durable goods, such as cars, also seems to be recovering. This is due, in part, to deferred

demand. You may not need a new car every year, but you will eventually, and it seems that many Americans are digging into their pockets to fund these big-ticket purchases again.

But is it all sustainable? I think it could be. Employment growth at the current level seems to be sustainable around a trend line that would promote continued recovery. Continued growth

in spending would follow as a result. The housing recovery and growth in durable goods demand should also be able to continue their forward trajectory. When you also factor in a gradual recovery in government spending and slow growth in business investment—both of which are occurring—the recovery appears to be on track.

So what could derail it?

THE OBSTACLES: POLITICAL VS. ECONOMIC Major obstacles to the ongoing economic recovery would be external events—a war in the Middle East, a European economic collapse, or a significant political event in the U.S., for example. Of the three, the most probable seems to be the last (although renewed talks about Greece’s exit from the euro have certainly added to market volatility). Notably, however, all three examples are political, not economic, events. That political events now trump

MAJOR OBSTACLES TO THE ONGOING ECONOMIC

RECOVERY WOULD BE EXTERNAL EVENTS—A WAR IN THE

MIDDLE EAST, A EUROPEAN ECONOMIC COLLAPSE, OR A

SIGNIFICANT POLITICAL EVENT IN THE U.S., FOR EXAMPLE.

W E A L T H M A N A G E M E N T

12 FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC JULY/AUGUST 2012

economic ones is a reflection of the new world order. In some sense, though, this is just a reversion to the origins of the economics discipline, when it was known as political economy.

It also reflects a reversion to the real rather than the financial. The past 30 years have been an exceptional period in world history, with unprecedented growth in finance and financial markets. Now, politics and the real economy are reasserting themselves against the primacy of finance.

We might also examine this situation by considering the effects of nationalism and geography on recent economic developments. The Middle East and the oil price, the European financial crisis and the Greek and French elections, turmoil in Russia and its effect on natural gas prices across Europe . . . all show that the return of the real is not limited to the U.S. In order to start to understand where we as a country now are economically, we must take a wider perspective than we have done during the past couple of decades.

There are two dimensions we need to look at in this analysis. The first is whether a country is a consumer or a producer of key items, such as capital, raw materials, and manufactured goods. The second is the key dependencies of a country, whether they are capital, energy, market access, or other factors. The first dimension looks at how a country operates, the second at its vulnerabilities.

Compare Germany with Greece. Both are European countries, but the similarities end there. Germany produces capital; Greece consumes it. Germany manufactures goods; Greece imports them. Both consume raw materials, but Germany uses them more efficiently. Overall, Germany depends on market access and raw materials, while Greece depends on access to capital, imports, raw materials, and other factors. Unsurprisingly, Greece has been more economically vulnerable.

Running this analysis on the U.S., we find that, overall—and with one big exception—we are in a strong position. The big exception, of course, is capital. The U.S. has been running large deficits for some time, depending on foreign capital for continued operation. In other areas, including manufacturing, demographics, geography, and even energy, the U.S. remains relatively strong. Because our capital

dependency stands out in a generally healthy picture, it has, unsurprisingly, become a focus of national concern and policy debate under the name of the deficit.

THE ONCOMING TRAIN? Which brings us to the major outstanding economic and political issue of our day. The U.S. capital dependency means that this year’s presidential election will determine the government that will have to make long-term decisions about how to deal with the country’s budget problems—because we can no longer continue to kick the can down the road. To understand the basis of the decisions they will make, we must first understand the underlying facts.

We currently spend about 50 percent more than we raise in taxes—that is, taxes cover about two-thirds of spending and borrowing accounts for about one-third. Approximately 37 percent of the spending is discretionary (defense and other government programs), about 57 percent is mandatory (Social Security, Medicare and Medicaid, etc.), and about 7 percent is net interest on the accrued debt.

In order to balance the budget, we have two options: reduce spending or raise taxes. The numbers above mean that if we raised taxes without cutting spending, taxes would have to go up by about 50 percent. Everyone in the country would be paying half again as much as they now do.

If, on the other hand, we balanced the budget by cutting spending alone, we would either have to substantially eliminate the discretionary spending—all of defense and everything else we typically associate with the federal government—or, for example, cut discretionary spending by half and Social Security and Medicare by about one-third. The details can vary, but this is broadly what it would take. I don’t have to tell you that neither “solution” would sit well with U.S. citizens; just look at what happened in Greece.

This suggests, then, that any resolution for our budget woes will probably require a mix of tax increases and spending cuts. The details, as always, are what we want to know, but, at this point in the election campaign, we don’t have any. A review of both parties’ proposals thus far suggests that neither has a credible plan for getting the problem under control.

There is another complicating factor to consider as well: the numerous looming changes coming toward the end of this year. The expiration of the Bush tax cuts and the sequestration of government spending will both hit at the end of 2012. Worse, the debt ceiling debate will fire up

again, quite possibly even before the election. Any one of these would have significant political and economic effects, but if they all come at the same time—with a presidential election mixed in—we could be facing some extreme uncertainty and the possible derailment of the economic improvements we’ve seen thus far.

COMMONWEALTH RESOURCESCommonwealth has provided support in similar situations in the past—the Turbulent Market materials from 2008 and 2009 and the extensive commentaries on the last debt ceiling debacle and U.S. credit rating downgrade, among others—and we will continue to do so. More, since we know this is coming, we will be providing materials to get ahead of the storm as the election nears and more details become available. In the meantime, we’ll keep an eye on the light in the tunnel and hope for the best.

As always, feel free to contact me or another member of Investment Research if we can provide any assistance.

Brad McMillan is Commonwealth’s chief investment officer. He is available at x9269 or at [email protected].

W E A L T H M A N A G E M E N T

commonwealth.com FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC 13

Keeping a little ahead of conditions is one of the

secrets of business; the trailer seldom goes far.

— Charles Schwab

Recognizing this risk, Batman has made it his personal mission to stand watch over the city and protect its citizens from criminal mischief. Ironically, the financial services industry currently finds itself in a similar scenario, searching for its own Batman to stand watch over its citizens (i.e., its investors) and protect them from financial malfeasance.

Recent investment scandals and financial debacles have highlighted the need for more stringent oversight and put the process of assessing and monitoring risk at the top of the list of regulators’ priorities. Consequently, due diligence programs are evolving from their previously narrow focus toward a more holistic analysis of both products and sponsors. Industry experts believe that this dual level of review will reduce overall risk while ensuring that broker/dealers engage in an ongoing effort to protect their customers.

WHAT DOES IT MEAN FOR COMMONWEALTH?Broker/dealers have always been required to perform due diligence on the products they make available to their advisors and clients. But in this environment of heightened sensitivity, the regulators have begun asking B/Ds to evidence their due diligence programs through written supervisory procedures and documented backup. The SEC and FINRA have gone so far as to announce that they are making due diligence a key focus of the 2012 exam cycle. As a result, B/Ds that are unable to evidence sufficient due diligence procedures may face enforcement actions, fines, suspensions, and even expulsions.

Clearly, from a regulatory perspective, it’s important that Commonwealth maintain an appropriate due diligence program. But it’s also important from an advisor perspective in that it:

1. Affirms our commitment to running a compliant firm and ensuring that we have effective procedures in place to properly analyze sponsors and their products

2. Gives advisors more confidence in the products they ultimately recommend to their clients

Commonwealth’s due diligence program is managed through the collaborative efforts of our Investment Research, Compliance, and Legal teams—and led by our dedicated due diligence officer (that’s me).

OUR VERY OWN BATMANCommonwealth’s Wealth Management division already had a robust due diligence program that encompassed many layers of analysis. Product managers and analysts monitored products to help ensure that our platform offerings met appropriate guidelines for quality and oversight. In recent years, however, it became clear that we would benefit from a dedicated position that could be bridge between Compliance and Wealth Management. By establishing a leadership role for the entire process, we would help alleviate the procedural burden our analysts faced in documenting, tracking, and maintaining this centralized due diligence program. And with more time on their hands, our analysts could devote more of it to consulting with advisors and helping them find the most appropriate investments for their clients’ portfolios.

While I don’t claim to have an alter ego who prowls the streets in a car shaped like a bat, as Commonwealth’s due diligence officer, it is my personal mission—with support from my partners in Research, Compliance, and Legal—to stand watch and be ready to identify regulatory, product, and operational risks.

THE DUE DILIGENCE REVIEWHere at Commonwealth, the due diligence program encompasses a multistage review process that starts with a due diligence questionnaire. We ask questions to gather information on the firm’s history, product results, existing compliance oversight, any regulatory updates, operational process, and financial procedures. Sponsors are required to complete the comprehensive questionnaire during the

I’ve always been fascinated with comic book superheroes, especially Batman. As any

comic book fan knows, Gotham is filled with criminals seeking to disrupt the city

by spreading fear, chaos, and uncertainty.

STANDING WATCH: A NEW ERA OF DUE DILIGENCE

FRED SHANE

W E A L T H M A N A G E M E N T

14 FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC JULY/AUGUST 2012

W E A L T H M A N A G E M E N T

commonwealth.com FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC 15

RFP phase, as well as annually. We then review these questionnaires and any supporting documents provided in order to fully understand a sponsor’s internal controls, organizational effectiveness, and products.

Throughout the year, we conduct random spot checks, analyzing legal and regulatory updates to identify any potential red flags, such as regulatory fines, headline risk, pending lawsuits, or legal decisions that would negatively impact the firm. In addition, I, along with our product managers and analysts, hold periodic on-site meetings with select groups of sponsors, digging deeper into their internal controls, compliance program, operational infrastructure, and financial condition. This allows us to analyze a firm’s infrastructure beyond the due diligence questionnaire while building stronger relationships with our sponsors.

Besides this sponsor-level review, our product managers and analysts review sponsors’ products on an ongoing basis utilizing various research tools, product documents, and analytical techniques to ensure that management teams are adhering to their processes and mandates.

Products that are currently vetted through this due diligence process include:

•SMAs/UMAs

•Third-party asset managers

•Alternatives

•Real estate

•Leasing programs

•Variable annuity/life core sponsors

•Mutual fund core sponsors

•Commonwealth’s Mutual Fund Recommended List

•PPS Select models comprising mutual funds

•UITs

•Retirement (to be activated fall of 2012)

Finally, through an extensive network of tracking documents, authorized stakeholders are able to obtain information on all of our products and sponsors whenever it is needed—and so we can evidence our due diligence efforts should the regulators come calling.

WHAT IS IN STORE IN THE FUTURE?We will continue to review, analyze, and enhance the firm’s due diligence program to ensure that it remains viable and adheres to regulatory requirements. In addition, we will expand the program into various aspects within Wealth Management as new risks are identified. As our program grows, other departments within Commonwealth are beginning to leverage the process to help identify opportunities for improvement within their own areas.

FINAL THOUGHTSThe success of Commonwealth’s due diligence program is due to the collaborative efforts of members of Research, Compliance, and Legal—the superheroes who stand watch and help protect the interests of Commonwealth, our advisors, and their clients.

And it’s just one more way in which Commonwealth lives and breathes our client-forward™ philosophy. As a sponsor recently shared with me: “Honestly, I think it is terrific that the advisors at Commonwealth have a diligence person like you protecting their clients. I can attest that it is more thorough than what we see from many firms.”

Fred Shane is a due diligence officer in Investment Research. He is available at x9931 or at [email protected].

CentralizationMultistage

Review

Collaboration

Tracking

Transparency

W E A L T H M A N A G E M E N T

16 FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC JULY/AUGUST 2012

While not as bad as the panic of 2008, where many justifiably feared the survival of weaker carriers, the current state of affairs offered little to feel optimistic about. The speaker outlined numerous contributing factors: an aging sales force, declining revenues, and unhedged variable annuity business. But the main negative factor was the low-interest-rate environment, which hamstrung insurance companies’ ability to invest premium dollars in fixed income.

At the time, the 10-year Treasury was yielding around 3.5 percent, and, despite the gloomy mood, the speaker and others felt it couldn’t possibly get any worse. And yet, today, the 10-year Treasury hovers below 2 percent and carriers have responded accordingly by restricting or eliminating products or leaving the business altogether. What does this mean for clients who need to manage risk in such an uncertain and unprecedented environment? Are there any opportunities now, or should advisors wait until it gets better?

WHERE WE STAND TODAYOn a positive note, the carriers that have left the business or limited their products are still financially strong, according to ratings agencies. For clients with existing policies, particularly those with guarantees, their protection remains. And because those products were sold at a time of higher interest rates, the premium dollars they previously paid were invested in higher-yielding assets than are available today. A contractually guaranteed income benefit or death benefit often remains the same as the day it was bought.

On the flip side, products without guarantees could be at risk, as underlying fixed accounts may now be at or near contractual lows. During your quarterly and annual reviews, be sure to evaluate these products using in-force illustrations to ensure that they’re still on track to be there when your

clients need them. Commonwealth’s Insurance and Annuity Research teams can help with this analysis, providing insight and potential alternatives to your clients’ current coverage. But thankfully, in most cases, clients who have already bought the coverage they need are in products better than what’s available today.

COMPANIES ARE HUNGRY FOR BUSINESSOf course, carriers that remain in the business still want and need new sales, especially of products with systematic premium payments rather than lump-sum premiums. Insurance is inherently a long-term product, and carriers, particularly mutual carriers, see the long-term opportunity for revenue. With sales numbers at historic lows, many are willing to compete on price, underwriting, or compensation to win market share and stay on target to meet their goals. Commonwealth’s Insurance team has helped many advisors shop the dozens of available carriers to find cost-effective solutions for clients, pinpointing those with the best chance of winning the case.

Take a look at indexed life and traditional whole life. With companies eliminating some of their guaranteed no-lapse universal life products, and others raising costs on such policies, indexed life and traditional whole life insurance have both picked up the slack for many advisors. Although each product takes a very different approach to cash value—indexed products offer a cap and floor return tied to an index like the S&P 500, and whole life pays fixed rates and dividends—they have had similar historical returns and volatility. Both products offer fixed income-like returns and risk, though neither has the risk to principal carried by fixed income funds or individual bonds when interest rates do eventually rise.

Although carriers and advisors can debate whether life insurance deserves to be called an asset class, both of these products can help diversify your clients’ holdings while providing valuable protection. In addition, such products give clients options if they later decide to 1035 or surrender their contracts, whereas most no-lapse universal life policies and term contracts have no such equity built up in later years.

CLIENTS NEED INSURANCE MORE THAN EVERAlthough investing may allow for a wait-and-see approach, insurance planning for most clients can’t wait. A premature

In March of last year, I sat in a packed

audience listening intently while a

former insurance company CFO

explained why this was a terrible time

to be in the insurance business.

A GOOD TIME, A TERRIBLE TIME, OR JUST IN TIME? NOTES ON THE INSURANCE INDUSTRY

BRIAN HARRISON, CFP®, CLU®, CHFC®, CLTC

W E A L T H M A N A G E M E N T

commonwealth.com FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC 17

death, disability, or long-term care event would bankrupt most families. And with life insurance ownership at historic lows, according to LIMRA, clients’ needs are as great as they’ve ever been. A recent Genworth study found the following: “Over 42 percent of American adults with household incomes between $50,000 and $250,000 do not have life insurance. Even for those who do own life insurance, 40 percent recognize that they need more. This is likely due to the fact that the average Main Street American only has enough life insurance to cover 3.6 years of income . . . the average amount of coverage is $155,000. 69 percent of single adults with children are uninsured.”

Conduct a simple needs analysis. The Genworth study also found that clients would welcome a needs analysis and annual insurance review, but they want the process to be quick and easy. Commonwealth’s interactive Life Insurance Needs Analysis Tool can help you quickly determine the right amount of coverage for a client; it’s as simple as inputting some basic information. (You can access the tool on COMMunity Link® at Products > Insurance > Request a Proposal.) For term life insurance, our one-click quote engine lets you see how much it would cost in a matter of seconds. And then, through our App Assistant program, you can delegate all of the paperwork to us.

Consider this: one average term life insurance policy per week could add more than $50,000 to your top-line revenue while protecting your clients against a financial tragedy. The Genworth statistics make a compelling case, and with the number of traditional insurance agents in decline, you may be the only person to bring up the topic, perform a needs analysis, and get clients the coverage they need.

ESTATE TAX OPPORTUNITIES WON’T LAST FOREVERFor higher-end clients, the current estate tax rules may present a once-in-a-lifetime opportunity to remove assets from a large estate. Until year-end, the federal lifetime gift tax exemption is unified with the federal estate tax and generation-skipping transfer tax exemptions, for a total possible exemption of $5.12 million; the maximum tax rate on anything above that amount is 35 percent. Thus, during life and at death, a client may make total taxable gifts (other than annual exclusion amounts or transfers for medical or educational purposes) of up to $5 million before owing gift taxes. And life insurance provides an opportunity to leverage that gift substantially.

Time is of the essence, however. Unless Congress acts to extend the current law (a big uncertainty considering the persistent gridlock in DC), the exemption limit will decrease to $1 million and the tax rate will rise to 55 percent in 2013.

Talk to your high-net-worth clients now. By taking advantage of life insurance, healthy clients can give away $5 million in assets without writing a check for $5 million. Guaranteed products offer the chance to pass on wealth today with “discounted dollars,” creating a substantial legacy and preventing the challenging fire sale that could occur should clients die without proper planning. For example, a $1 million gift into a Penn Mutual Survivorship Plus Indexed Universal Life policy for two very healthy 55-year-olds would guarantee in excess of $7.8 million in death benefits; thanks to the cash value’s indexed opportunity for growth, it could be even be more. Business owners who have a sizable illiquid asset in their companies may benefit the most from such a strategy. Estate planners and insurance companies should be busy at year-end; now is the time to start the conversation with your clients.

A GREAT TIME FOR ADVISORSWith the combination of favorable tax laws, carriers desperate for business, and a vastly underinsured population, you have a tremendous opportunity over the next few months. And Commonwealth has the resources to make the process easy. We can design the case, take the application, and usher it through underwriting. All you need to do is have a conversation with your clients about the risks that remain in their financial plans. From the kids of a client who just had their first child to your wealthiest clients, you can make a meaningful difference in their lives. While it may not be a good time to be an insurance company, it’s a great time to be an advisor who makes risk management part of his or her practice.

Commonwealth Financial Network® does not provide legal or tax advice.

Brian Harrison is the director of insurance and financial planning marketing. He is available at x9174 or at [email protected].

The story has the usual cast of characters: a wealthy client (a lawyer) and his broker, ex-wife, and widow. After a bitter divorce, Newman Trowbridge Jr. presumably didn’t intend to retain his former wife as his IRA beneficiary. When he died unexpectedly in 2009, however, the beneficiary designation on the IRA hadn’t been updated, leaving the account’s considerable holdings to his ex-wife.

Citing the securities industry’s Know Your Customer rule, Trowbridge’s estate sued the broker and broker/dealer, alleging that they were guilty of negligence and a breach of fiduciary duty. (“Estate Sues B/D and Broker Over Lawyer’s Designation of Ex-Wife as IRA Beneficiary,” the Forbes.com headline read.) The suit claimed that the broker failed to regularly review Trowbridge’s accounts and to advise Trowbridge to designate his current spouse as his IRA beneficiary after he remarried. Ultimately, the FINRA arbitration panel found that the burden lay with Trowbridge, a sophisticated attorney who routinely oversaw his own investment and estate planning decisions. Although no one seemed to think his ex-wife was the intended beneficiary, she received the money.

Although it may seem that the B/D and the broker won this case, the reality isn’t quite so rosy. Nobody embroiled in a lawsuit comes out a winner after spending large sums of money on his defense. And would you want the terms defendant, breach of fiduciary duty, and FINRA arbitration panel associated with your name and practice?

IRA BENEFICIARY FAQSFortunately, when it comes to conducting beneficiary reviews, Commonwealth advisors are ahead of the game. I don’t need to tell you that regular reviews are essential to keeping your clients’ estate and financial plans current and in line with their wishes. Based on my daily conversations with advisors, most of you are already providing this important service. In fact, many of you are calling for advice on complex beneficiary issues so that you can guide clients in working with their attorneys and tax advisors. Here’s a sampling of questions I commonly hear from advisors regarding IRA options in estate planning.

How do I know the right beneficiary is named? The only way to be sure is to gather all the facts and review the client’s estate planning documents. While it’s important to consider tax consequences and ways to keep distribution options open, it’s equally important to understand the client’s planning goals. Does he or she have minor children, spendthrift concerns, children from a prior marriage, or worries about children getting divorced? If so, the client may be willing to sacrifice a beneficiary’s flexibility in terms of taking distributions or maximizing tax advantages. Estate planning isn’t a perfect world. More often than not, clients will have to make a choice between control, flexibility, and tax savings.

How important is it to keep tabs on your clients’ beneficiary designations? As one

recent case shows, it’s an area advisors shouldn’t overlook.

W E A L T H M A N A G E M E N T

18 FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC JULY/AUGUST 2012

IT’S POSSIBLE TO BYPASS EXPENSIVE AND

TIME-CONSUMING PROBATE PROCEEDINGS

BY INITIATING A DIRECT TRUSTEE-TO-TRUSTEE

TRANSFER FROM THE DECEASED SPOUSE’S

IRA TO THE SURVIVING SPOUSE’S IRA.

KEEPING YOUR CLIENTS’ BENEFICIARY DESIGNATIONS UP TO DATE—AND YOUR NAME OUT OF THE PRESS

ROSE WATSON, ESQ.

W E A L T H M A N A G E M E N T

commonwealth.com FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC 19

Don’t bad things happen when a trust is named as beneficiary? Not really. In order for IRA proceeds to be distributed via a life expectancy payout, there must be a designated beneficiary, which the IRS defines as an individual. A trust can qualify as a designated beneficiary to take required minimum distributions (RMDs) if it meets the IRS’s “see-through” rules, which are outlined in the next section. In this case, the trustee may take RMDs over the life expectancy of the oldest individual beneficiary. (The other options are a lump-sum distribution or a full distribution within five years.) In comparison, if individual beneficiaries are named, they may set up their own IRA beneficiary designation accounts for their shares and take RMDs over their own life expectancies.

Clients who are considering naming a trust as an IRA beneficiary should keep the following points in mind:

• Separate account treatment is never available. If the trust beneficiaries range widely in age, the trust may end up taking distributions on a much more accelerated time frame than if the youngest individual were named.

• A trust, even a see-through trust, cannot exercise the spousal rollover option. If a surviving spouse is the income beneficiary with children as remainders, upon the surviving spouse’s death, the trust must continue with RMDs based on the surviving spouse’s life expectancy, consuming the IRA assets more quickly.

Clients may find it easier to swallow these potential limitations if designating a trust allows them to achieve their primary planning goals, such as asset protection and control from the grave.

How do I know if this is a see-through trust? There is no specific language that determines a see-through trust. Instead, four criteria must be met:

1. The trust must be valid under state law;

2. The trust must be irrevocable or become irrevocable upon the participant’s death;

3. The trust beneficiaries with respect to the trust’s interest in the IRA must be identifiable from the trust instrument; and

4. Certain documentation must be provided to the plan administrator.

If the trust satisfies these four requirements, the trust beneficiaries will be treated as designated beneficiaries of the IRA for most, but not all, purposes. Keep in mind that all trust beneficiaries must be designated beneficiaries (i.e., individuals). If the trust has beneficiaries that do not qualify as designated beneficiaries, such as charitable organizations, it must be carefully reviewed to determine if it qualifies as a see-through trust.

What are the differences between the IRS’s RMD rules and the trust distribution provisions? A trust is governed by two sets of rules. The first are the IRS regulations that determine the schedule the trust must follow to take distributions from the IRA. Once the trustee has taken the IRA distributions, the trust document itself determines the beneficiaries’ access to the trust assets.

How do I include an IRA in a testamentary trust and preserve the designated beneficiary? If the IRA benefits are payable to the estate, there is no designated beneficiary, even if all the beneficiaries of the estate are individuals. The executor can transfer the inherited IRA to the estate beneficiaries, but the estate beneficiaries can’t use their own life expectancies to compute RMDs. If the client has a testamentary trust and wishes to preserve the IRA’s designated beneficiary status, the testamentary trust should be named in the beneficiary designation. (For example, “John Doe, Trustee of the Trust Established Under the Jane Doe Last Will and Testament, dated January 1, 2012.”)

What if the surviving spouse is the sole beneficiary of the deceased spouse’s estate? A long line of IRS rulings establishes that, if the IRA benefits are paid to the estate, the surviving spouse can roll over the benefits to his or her own IRA, provided certain conditions are met. In fact, it’s

W E A L T H M A N A G E M E N T

20 FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC JULY/AUGUST 2012

possible to bypass expensive and time-consuming probate proceedings by initiating a direct trustee-to-trustee transfer from the deceased spouse’s IRA to the surviving spouse’s IRA, a procedure blessed by the IRS in a similar situation in Private Letter Ruling 201211034 (December 22, 2011).

Why is it often recommended to “name the spouse as primary and the trust as contingent”? A widow or widower who inherits IRA benefits from his or her deceased spouse has two options that are not available to other beneficiaries. The surviving spouse can take a life expectancy payout with the life expectancy recalculated every year, or the spouse can roll the whole amount over to his or her own IRA. Thus, the goal of naming the spouse as the primary beneficiary and the trust as secondary is to maximize flexibility for the spouse while preserving some protection and control in the event the spouse dies first or disclaims the asset.

Can clients name an UTMA or UGMA account for minor beneficiaries? If a client wishes to benefit a minor directly, he or she may do so. (NFS does not permit a custodial designation.) One benefit of using an UTMA or UGMA account for minor beneficiaries is that the client avoids the expense of drafting a trust. For IRAs with smaller balances, this approach may be preferable. Another benefit of using an UTMA or UGMA account is that, until the beneficiary reaches the age of majority, the account’s custodian has control over the funds. The age of majority varies from state to state between 18 and 21. The major drawback is that, once beneficiaries come of age, the money is theirs to use as they wish.

Why do estate planning attorneys rely on advisors? It’s simple: you’re competent and they need your help. Plus, they know your clients trust you. In most cases, you probably know more about the client’s financial plan than the attorney, and you may also be more familiar with the complex IRS rules governing IRAs. Clients are sometimes reluctant to pay legal fees to have an attorney help review their beneficiary designations, and the attorney may rely on you to see that everything is wrapped up. Working with the attorney to ensure that the client’s estate is in order is a great way to build a strong foundation for future referrals.

TOOLS TO USE WITH YOUR CLIENTSFor additional resources to assist your clients with their beneficiary designations, visit the Financial Planning Playbook on COMMunity Link® at Planning & Research > Financial Planning > Playbook > Estate Planning > Coach Your Clients. There, you’ll find our Reviewing Your Beneficiary Designations worksheet and a new client-approved piece titled “FAQs: IRA and Trust Basics.” We hope you’ll find these resources useful during your regular beneficiary reviews. Remember, asking the right questions can go a long way toward protecting your clients’ assets and your own good name.

Commonwealth Financial Network® does not provide legal or tax advice.

Rose Watson is an advanced planning consultant. She is available at x9891 or at [email protected].

PULL QUOTE

W E A L T H M A N A G E M E N T

commonwealth.com FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC 21

From a high level, our team specializes in the analysis of individual credits across the fixed income universe, including Treasury, agency, mortgage, municipal, investment-grade, high-yield, and preferred securities. We also provide regular market commentary through a weekly publication, Across the Curve, as well as via the Investment Research team’s quarterly conference call.

To date, we have had the opportunity to work with more than 500 Commonwealth advisors in various capacities, and, through this article, we hope to introduce our team to an even broader base. Read on to learn how you can leverage our team to meet your clients’ fixed income investment needs and goals.

ANALYTICAL SUPPORT AND INSIGHTDuring the past three years, our team has served as a highly specialized resource for advisors seeking insight or analytical support across fixed income markets and individual securities. We provide a broad range of capabilities to advisors for both existing and prospective clients, offering analytical solutions that are specifically customized in accordance with advisor needs, client risk tolerance and investment objectives, and any unique analytical goals.

Here are some specific ways you can leverage our team:

The evaluation of an existing fixed income portfolio or security. This analysis may include a written report summarizing the market environment of the associated asset class, an aggregated portfolio overview and relative comparison to the broader asset class, and individual credit analysis, which focuses on fundamental issuer credit quality and unique security structure. The goal is to identify key risks within a portfolio and assess whether or not existing holdings, in aggregate, appear to best reflect the client’s targeted risk tolerance and investment objectives.

Appraisal of a prospective client’s existing portfolio and proposal for alternative fixed income investment solutions. This analysis may include a written report similar to that noted above. In addition, we seek to provide you with value-added solutions that you can present to your potential new client, including suggestions on portfolio realignment, possible investment strategies, and appropriate fixed income strategies given the investor’s articulated goals.

Portfolio construction and/or strategic repositioning. In this endeavor, the team works closely with the Fixed Income Trade Desk to assist advisors in constructing customized fixed income portfolios or strategically liquidating existing positions to effectively reposition a portfolio. We may also collaborate with you to build a personalized bond ladder based on the client’s needs. When appropriate, different potential portfolio illustrations may be provided to depict varying income generation opportunities that may be available through alternative fixed income strategies. These illustrations are meant to serve as examples of

Since its establishment in the spring of 2009, Commonwealth’s Fixed Income Research

team and capabilities have expanded in an ongoing effort to meet the evolving needs of

our advisors for information and insight related to individual fixed income securities.

FIXED INCOME RESEARCH: SUPPORTING YOUR INVESTMENT NEEDS AND GOALS

MEAGAN SWANSON, CFA®

risk/reward opportunities in the current market environment, as well as to provide you with material and talking points for navigating conversations and framing expectations with existing and potential clients.

Idea generation associated with new potential investment opportunities. Through this analytical process, we seek to identify new potential individual fixed income investments given a set of client constraints and objectives. This screening process can be completed on an ad hoc basis or periodically, depending on your needs. The level of detail we provide can also vary, ranging from a basic security screen to a highly detailed, individual credit analysis by security.

Formulation and implementation of fixed income strategies. This process involves the collaboration of the Fixed Income Research team, the Trade Desk, and the advisor. We will work closely with you to help you take advantage of market dislocations with an aim to opportunistically maximize yield and minimize cost basis while gradually building out portfolios. The goal is to marry credit analysis, portfolio construction, and effective trading strategies.

Prospective account proposals. Through this analytical exercise, we strive to provide advisors with the information and presentation material necessary for initial and ongoing meetings and conversations with prospective clients. The effort typically begins with an introductory discussion to gather information about the client’s unique investment goals and objectives, risk tolerance, broader investment portfolio, and net worth composition. Then, we work with you to identify appropriate asset class allocations and potential investment opportunities. We may also

leverage the broader Investment Research team for additional analysis.

Market commentary and insight. Our team produces a weekly publication, Across the Curve, which includes commentary on the fixed income markets, Federal Reserve policy, new issuance trends, and market performance. Additionally, we collaborate with the Investment Research team to produce a weekly client-approved market commentary. We also provide periodic commentary on market-moving events (e.g., the U.S. Treasury downgrade; municipal market “60 Minutes” response). As we are consistently following various fixed income market trends and news-related items, we aim to be a resource for advisors seeking to discuss the general fixed income asset classes, current trends, and near-term outlooks.

These are just a few ways in which our team works to consistently support the growing analytical needs of Commonwealth advisors in the individual security fixed income space. That said, we know that the markets—and, thus, clients’ investment needs—are always in flux, so please feel free to reach out to us directly with any unique question or request that relates to individual fixed income securities. If we do not have a solution already, we are happy to work with you to create new tools and processes to support the evolution of your investment management practice.

E-mail us at [email protected].

Meagan Swanson is a senior fixed income analyst. She is available at x9968 or at [email protected].

22 FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC JULY/AUGUST 2012

W E A L T H M A N A G E M E N T

commonwealth.com FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC 23

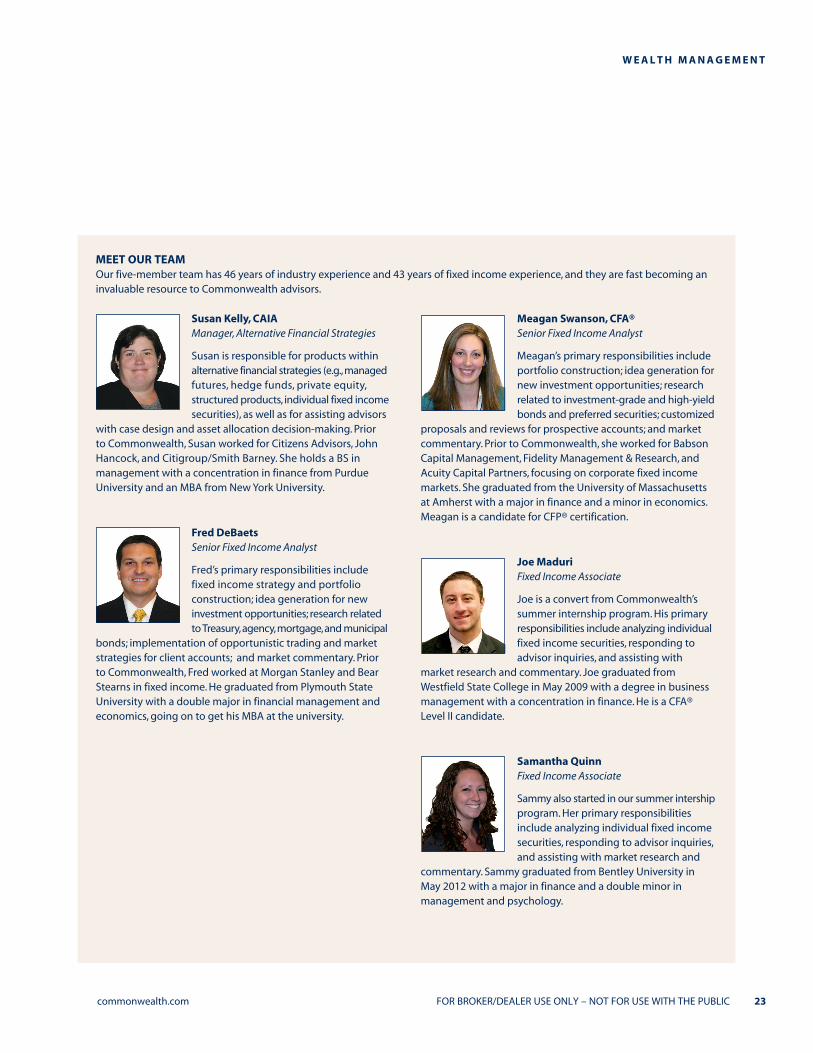

Susan Kelly, CAIA Manager, Alternative Financial Strategies

Susan is responsible for products within alternative financial strategies (e.g., managed futures, hedge funds, private equity, structured products, individual fixed income securities), as well as for assisting advisors

with case design and asset allocation decision-making. Prior to Commonwealth, Susan worked for Citizens Advisors, John Hancock, and Citigroup/Smith Barney. She holds a BS in management with a concentration in finance from Purdue University and an MBA from New York University.

Fred DeBaets Senior Fixed Income Analyst

Fred’s primary responsibilities include fixed income strategy and portfolio construction; idea generation for new investment opportunities; research related to Treasury, agency, mortgage, and municipal

bonds; implementation of opportunistic trading and market strategies for client accounts; and market commentary. Prior to Commonwealth, Fred worked at Morgan Stanley and Bear Stearns in fixed income. He graduated from Plymouth State University with a double major in financial management and economics, going on to get his MBA at the university.

Meagan Swanson, CFA® Senior Fixed Income Analyst

Meagan’s primary responsibilities include portfolio construction; idea generation for new investment opportunities; research related to investment-grade and high-yield bonds and preferred securities; customized

proposals and reviews for prospective accounts; and market commentary. Prior to Commonwealth, she worked for Babson Capital Management, Fidelity Management & Research, and Acuity Capital Partners, focusing on corporate fixed income markets. She graduated from the University of Massachusetts at Amherst with a major in finance and a minor in economics. Meagan is a candidate for CFP® certification.

Joe Maduri Fixed Income Associate

Joe is a convert from Commonwealth’s summer internship program. His primary responsibilities include analyzing individual fixed income securities, responding to advisor inquiries, and assisting with

market research and commentary. Joe graduated from Westfield State College in May 2009 with a degree in business management with a concentration in finance. He is a CFA® Level II candidate.

Samantha Quinn Fixed Income Associate

Sammy also started in our summer intership program. Her primary responsibilities include analyzing individual fixed income securities, responding to advisor inquiries, and assisting with market research and

commentary. Sammy graduated from Bentley University in May 2012 with a major in finance and a double minor in management and psychology.

W E A L T H M A N A G E M E N T

MEET OUR TEAMOur five-member team has 46 years of industry experience and 43 years of fixed income experience, and they are fast becoming an invaluable resource to Commonwealth advisors.

24 FOR BROKER/DEALER USE ONLY – NOT FOR USE WITH THE PUBLIC JULY/AUGUST 2012

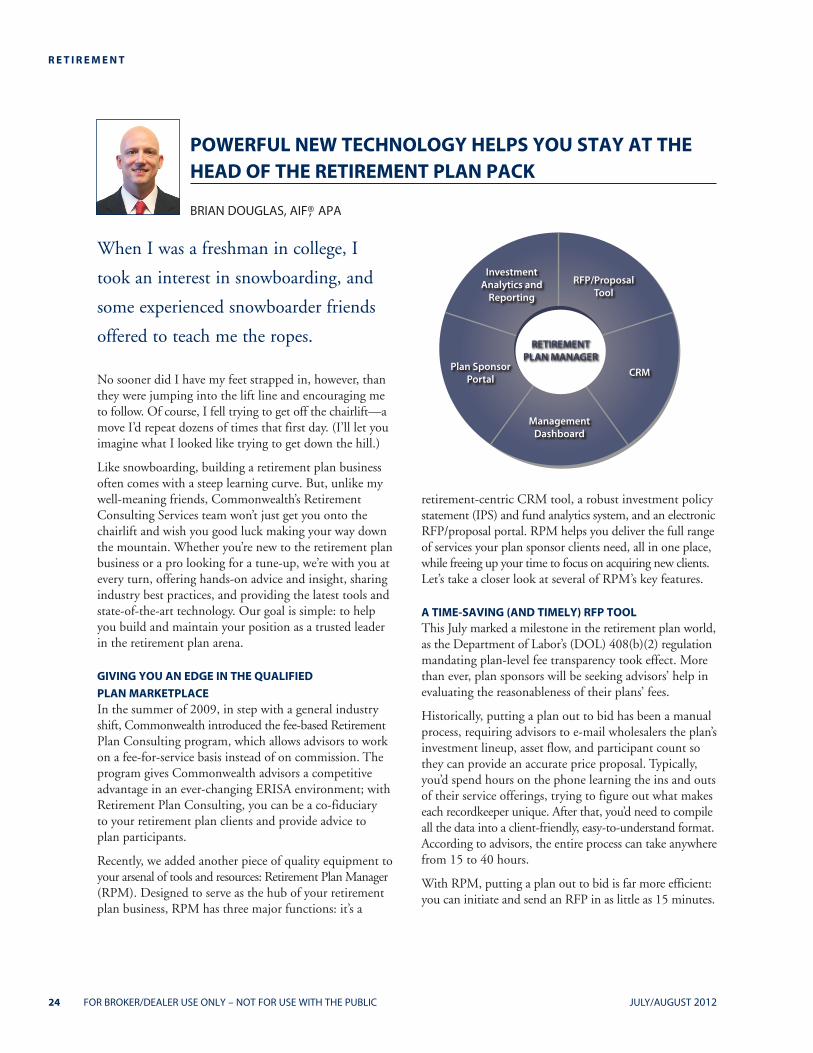

R E T I R E M E N T

No sooner did I have my feet strapped in, however, than they were jumping into the lift line and encouraging me to follow. Of course, I fell trying to get off the chairlift—a move I’d repeat dozens of times that first day. (I’ll let you imagine what I looked like trying to get down the hill.)

Like snowboarding, building a retirement plan business often comes with a steep learning curve. But, unlike my well-meaning friends, Commonwealth’s Retirement Consulting Services team won’t just get you onto the chairlift and wish you good luck making your way down the mountain. Whether you’re new to the retirement plan business or a pro looking for a tune-up, we’re with you at every turn, offering hands-on advice and insight, sharing industry best practices, and providing the latest tools and state-of-the-art technology. Our goal is simple: to help you build and maintain your position as a trusted leader in the retirement plan arena.

GIVING YOU AN EDGE IN THE QUALIFIED

PLAN MARKETPLACEIn the summer of 2009, in step with a general industry shift, Commonwealth introduced the fee-based Retirement Plan Consulting program, which allows advisors to work on a fee-for-service basis instead of on commission. The program gives Commonwealth advisors a competitive advantage in an ever-changing ERISA environment; with Retirement Plan Consulting, you can be a co-fiduciary to your retirement plan clients and provide advice to plan participants.