Technologies -...

17

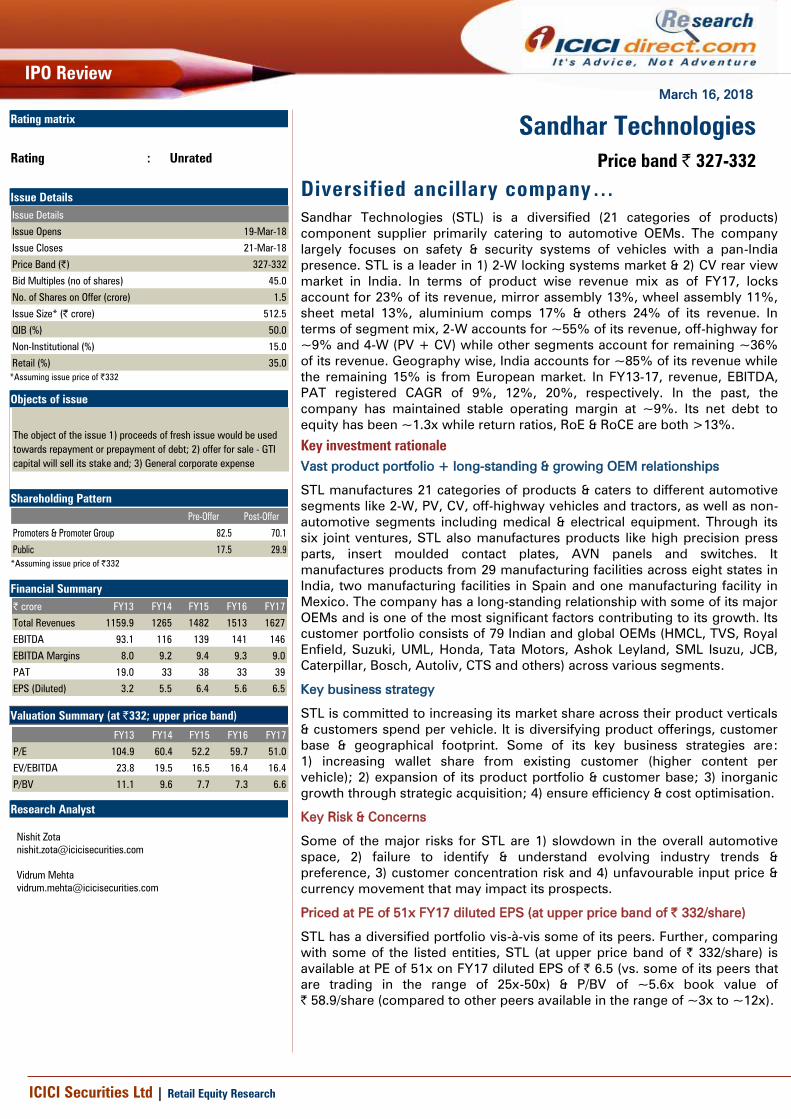

March 16, 2018 IPO Review ICICI Securities Ltd | Retail Equity Research Diversified ancillary company… Sandhar Technologies (STL) is a diversified (21 categories of products) component supplier primarily catering to automotive OEMs. The company largely focuses on safety & security systems of vehicles with a pan-India presence. STL is a leader in 1) 2-W locking systems market & 2) CV rear view market in India. In terms of product wise revenue mix as of FY17, locks account for 23% of its revenue, mirror assembly 13%, wheel assembly 11%, sheet metal 13%, aluminium comps 17% & others 24% of its revenue. In terms of segment mix, 2-W accounts for ~55% of its revenue, off-highway for ~9% and 4-W (PV + CV) while other segments account for remaining ~36% of its revenue. Geography wise, India accounts for ~85% of its revenue while the remaining 15% is from European market. In FY13-17, revenue, EBITDA, PAT registered CAGR of 9%, 12%, 20%, respectively. In the past, the company has maintained stable operating margin at ~9%. Its net debt to equity has been ~1.3x while return ratios, RoE & RoCE are both >13%. Key investment rationale Vast product portfolio + long-standing & growing OEM relationships STL manufactures 21 categories of products & caters to different automotive segments like 2-W, PV, CV, off-highway vehicles and tractors, as well as non- automotive segments including medical & electrical equipment. Through its six joint ventures, STL also manufactures products like high precision press parts, insert moulded contact plates, AVN panels and switches. It manufactures products from 29 manufacturing facilities across eight states in India, two manufacturing facilities in Spain and one manufacturing facility in Mexico. The company has a long-standing relationship with some of its major OEMs and is one of the most significant factors contributing to its growth. Its customer portfolio consists of 79 Indian and global OEMs (HMCL, TVS, Royal Enfield, Suzuki, UML, Honda, Tata Motors, Ashok Leyland, SML Isuzu, JCB, Caterpillar, Bosch, Autoliv, CTS and others) across various segments. Key business strategy STL is committed to increasing its market share across their product verticals & customers spend per vehicle. It is diversifying product offerings, customer base & geographical footprint. Some of its key business strategies are: 1) increasing wallet share from existing customer (higher content per vehicle); 2) expansion of its product portfolio & customer base; 3) inorganic growth through strategic acquisition; 4) ensure efficiency & cost optimisation. Key Risk & Concerns Some of the major risks for STL are 1) slowdown in the overall automotive space, 2) failure to identify & understand evolving industry trends & preference, 3) customer concentration risk and 4) unfavourable input price & currency movement that may impact its prospects. Priced at PE of 51x FY17 diluted EPS (at upper price band of | 332/share) STL has a diversified portfolio vis-à-vis some of its peers. Further, comparing with some of the listed entities, STL (at upper price band of | 332/share) is available at PE of 51x on FY17 diluted EPS of | 6.5 (vs. some of its peers that are trading in the range of 25x-50x) & P/BV of ~5.6x book value of | 58.9/share (compared to other peers available in the range of ~3x to ~12x). Sandhar Technologies Price band | 327-332 Rating matrix Rating : Unrated Issue Details Issue Details Issue Opens 19-Mar-18 Issue Closes 21-Mar-18 Price Band (|) 327-332 Bid Multiples (no of shares) 45.0 No. of Shares on Offer (crore) 1.5 Issue Size* (| crore) 512.5 QIB (%) 50.0 Non-Institutional (%) 15.0 Retail (%) 35.0 *Assuming issue price of |332 Objects of issue The object of the issue 1) proceeds of fresh issue would be used towards repayment or prepayment of debt; 2) offer for sale - GTI capital will sell its stake and; 3) General corporate expense Shareholding Pattern Pre-Offer Post-Offer Promoters & Promoter Group 82.5 70.1 Public 17.5 29.9 *Assuming issue price of |332 Financial Summary | crore FY13 FY14 FY15 FY16 FY17 Total Revenues 1159.9 1265 1482 1513 1627 EBITDA 93.1 116 139 141 146 EBITDA Margins 8.0 9.2 9.4 9.3 9.0 PAT 19.0 33 38 33 39 EPS (Diluted) 3.2 5.5 6.4 5.6 6.5 Valuation Summary (at |332; upper price band) FY13 FY14 FY15 FY16 FY17 P/E 104.9 60.4 52.2 59.7 51.0 EV/EBITDA 23.8 19.5 16.5 16.4 16.4 P/BV 11.1 9.6 7.7 7.3 6.6 Research Analyst Nishit Zota [email protected] Vidrum Mehta [email protected]

Transcript of Technologies -...

March 16, 2018

IPO Review

ICICI Securities Ltd | Retail Equity Research

Diversified ancillary company…

Sandhar Technologies (STL) is a diversified (21 categories of products)

component supplier primarily catering to automotive OEMs. The company

largely focuses on safety & security systems of vehicles with a pan-India

presence. STL is a leader in 1) 2-W locking systems market & 2) CV rear view

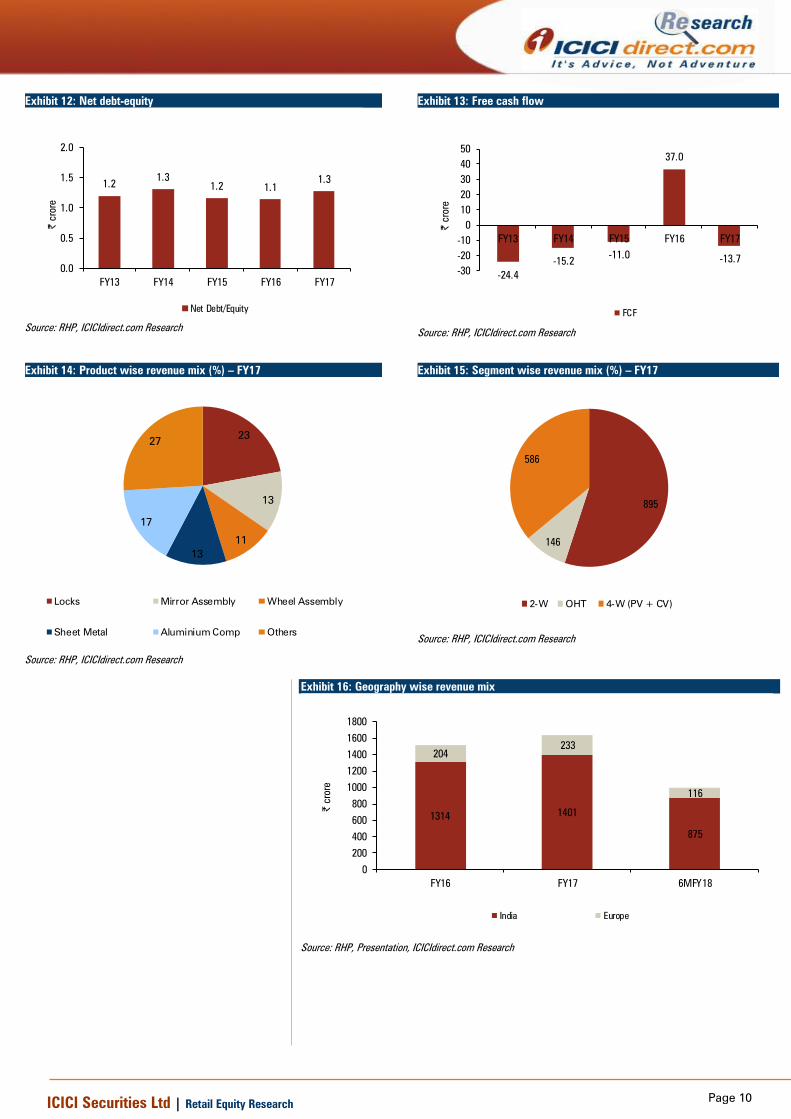

market in India. In terms of product wise revenue mix as of FY17, locks

account for 23% of its revenue, mirror assembly 13%, wheel assembly 11%,

sheet metal 13%, aluminium comps 17% & others 24% of its revenue. In

terms of segment mix, 2-W accounts for ~55% of its revenue, off-highway for

~9% and 4-W (PV + CV) while other segments account for remaining ~36%

of its revenue. Geography wise, India accounts for ~85% of its revenue while

the remaining 15% is from European market. In FY13-17, revenue, EBITDA,

PAT registered CAGR of 9%, 12%, 20%, respectively. In the past, the

company has maintained stable operating margin at ~9%. Its net debt to

equity has been ~1.3x while return ratios, RoE & RoCE are both >13%.

Key investment rationale

Vast product portfolio + long-standing & growing OEM relationships

STL manufactures 21 categories of products & caters to different automotive

segments like 2-W, PV, CV, off-highway vehicles and tractors, as well as non-

automotive segments including medical & electrical equipment. Through its

six joint ventures, STL also manufactures products like high precision press

parts, insert moulded contact plates, AVN panels and switches. It

manufactures products from 29 manufacturing facilities across eight states in

India, two manufacturing facilities in Spain and one manufacturing facility in

Mexico. The company has a long-standing relationship with some of its major

OEMs and is one of the most significant factors contributing to its growth. Its

customer portfolio consists of 79 Indian and global OEMs (HMCL, TVS, Royal

Enfield, Suzuki, UML, Honda, Tata Motors, Ashok Leyland, SML Isuzu, JCB,

Caterpillar, Bosch, Autoliv, CTS and others) across various segments.

Key business strategy

STL is committed to increasing its market share across their product verticals

& customers spend per vehicle. It is diversifying product offerings, customer

base & geographical footprint. Some of its key business strategies are:

1) increasing wallet share from existing customer (higher content per

vehicle); 2) expansion of its product portfolio & customer base; 3) inorganic

growth through strategic acquisition; 4) ensure efficiency & cost optimisation.

Key Risk & Concerns

Some of the major risks for STL are 1) slowdown in the overall automotive

space, 2) failure to identify & understand evolving industry trends &

preference, 3) customer concentration risk and 4) unfavourable input price &

currency movement that may impact its prospects.

Priced at PE of 51x FY17 diluted EPS (at upper price band of | 332/share)

STL has a diversified portfolio vis-à-vis some of its peers. Further, comparing

with some of the listed entities, STL (at upper price band of | 332/share) is

available at PE of 51x on FY17 diluted EPS of | 6.5 (vs. some of its peers that

are trading in the range of 25x-50x) & P/BV of ~5.6x book value of

| 58.9/share (compared to other peers available in the range of ~3x to ~12x).

Sandhar Technologies

Price band | 327-332

Rating matrix

Rating : Unrated

Issue Details

Issue Details

Issue Opens 19-Mar-18

Issue Closes 21-Mar-18

Price Band (|) 327-332

Bid Multiples (no of shares) 45.0

No. of Shares on Offer (crore) 1.5

Issue Size* (| crore) 512.5

QIB (%) 50.0

Non-Institutional (%) 15.0

Retail (%) 35.0

*Assuming issue price of |332

Objects of issue

The object of the issue 1) proceeds of fresh issue would be used

towards repayment or prepayment of debt; 2) offer for sale - GTI

capital will sell its stake and; 3) General corporate expense

Shareholding Pattern

Pre-Offer Post-Offer

Promoters & Promoter Group 82.5 70.1

Public 17.5 29.9

*Assuming issue price of |332

Financial Summary

| crore FY13 FY14 FY15 FY16 FY17

Total Revenues 1159.9 1265 1482 1513 1627

EBITDA 93.1 116 139 141 146

EBITDA Margins 8.0 9.2 9.4 9.3 9.0

PAT 19.0 33 38 33 39

EPS (Diluted) 3.2 5.5 6.4 5.6 6.5

Valuation Summary (at |332; upper price band)

FY13 FY14 FY15 FY16 FY17

P/E 104.9 60.4 52.2 59.7 51.0

EV/EBITDA 23.8 19.5 16.5 16.4 16.4

P/BV 11.1 9.6 7.7 7.3 6.6

Research Analyst

Nishit Zota

Vidrum Mehta

Page 2 ICICI Securities Ltd | Retail Equity Research

Exhibit 1: Consolidated Key Financials

| crore FY13 FY14 FY15 FY16 FY17

Total Revenues 1159.9 1265.0 1482.1 1513.2 1626.8

EBITDA 93.1 116.3 139.1 141.3 145.8

EBITDA Margins (%) 8.0 9.2 9.4 9.3 9.0

PAT 19.0 33.1 38.3 33.4 39.2

PAT Margins (%) 1.6 2.6 2.6 2.2 2.4

Diluted EPS 3.2 5.5 6.4 5.6 6.5

RoE 10.6 16.0 14.8 12.2 13.0

RoCE 15.2 16.9 16.3 15.4 13.4

Source: RHP, ICICIdirect.com Research

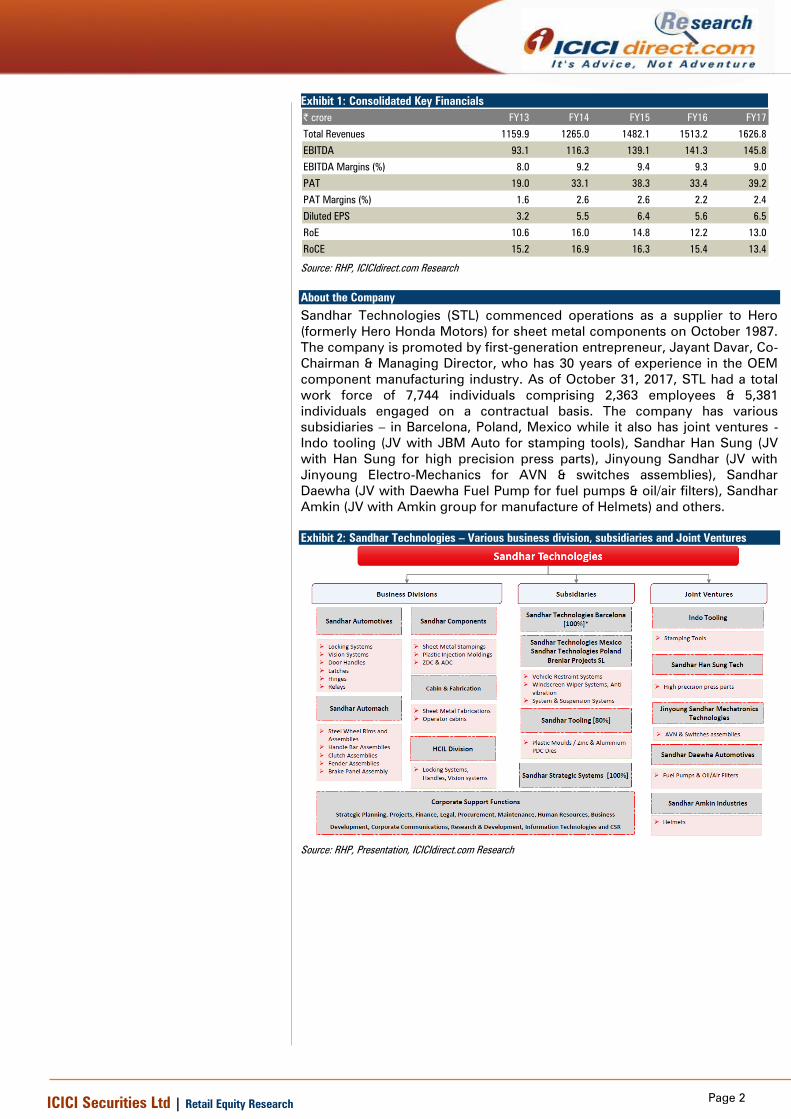

About the Company

Sandhar Technologies (STL) commenced operations as a supplier to Hero

(formerly Hero Honda Motors) for sheet metal components on October 1987.

The company is promoted by first-generation entrepreneur, Jayant Davar, Co-

Chairman & Managing Director, who has 30 years of experience in the OEM

component manufacturing industry. As of October 31, 2017, STL had a total

work force of 7,744 individuals comprising 2,363 employees & 5,381

individuals engaged on a contractual basis. The company has various

subsidiaries – in Barcelona, Poland, Mexico while it also has joint ventures -

Indo tooling (JV with JBM Auto for stamping tools), Sandhar Han Sung (JV

with Han Sung for high precision press parts), Jinyoung Sandhar (JV with

Jinyoung Electro-Mechanics for AVN & switches assemblies), Sandhar

Daewha (JV with Daewha Fuel Pump for fuel pumps & oil/air filters), Sandhar

Amkin (JV with Amkin group for manufacture of Helmets) and others.

Exhibit 2: Sandhar Technologies – Various business division, subsidiaries and Joint Ventures

Source: RHP, Presentation, ICICIdirect.com Research

Page 3 ICICI Securities Ltd | Retail Equity Research

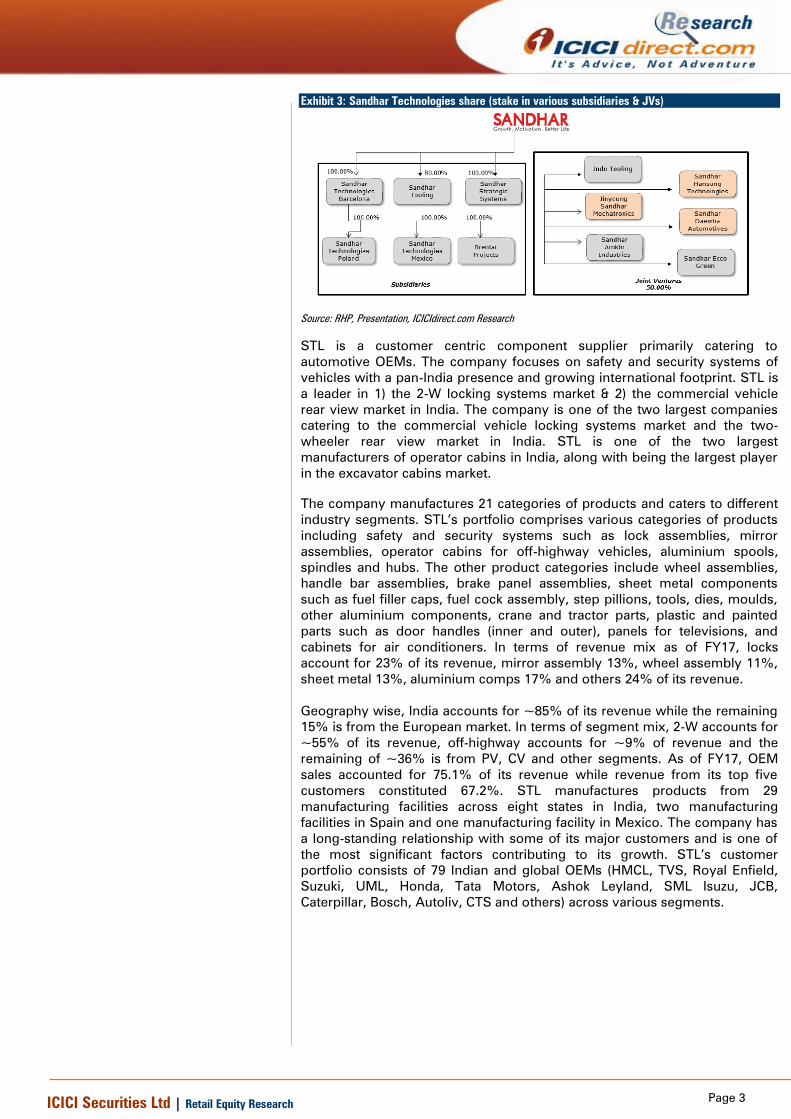

Exhibit 3: Sandhar Technologies share (stake in various subsidiaries & JVs)

Source: RHP, Presentation, ICICIdirect.com Research

STL is a customer centric component supplier primarily catering to

automotive OEMs. The company focuses on safety and security systems of

vehicles with a pan-India presence and growing international footprint. STL is

a leader in 1) the 2-W locking systems market & 2) the commercial vehicle

rear view market in India. The company is one of the two largest companies

catering to the commercial vehicle locking systems market and the two-

wheeler rear view market in India. STL is one of the two largest

manufacturers of operator cabins in India, along with being the largest player

in the excavator cabins market.

The company manufactures 21 categories of products and caters to different

industry segments. STL’s portfolio comprises various categories of products

including safety and security systems such as lock assemblies, mirror

assemblies, operator cabins for off-highway vehicles, aluminium spools,

spindles and hubs. The other product categories include wheel assemblies,

handle bar assemblies, brake panel assemblies, sheet metal components

such as fuel filler caps, fuel cock assembly, step pillions, tools, dies, moulds,

other aluminium components, crane and tractor parts, plastic and painted

parts such as door handles (inner and outer), panels for televisions, and

cabinets for air conditioners. In terms of revenue mix as of FY17, locks

account for 23% of its revenue, mirror assembly 13%, wheel assembly 11%,

sheet metal 13%, aluminium comps 17% and others 24% of its revenue.

Geography wise, India accounts for ~85% of its revenue while the remaining

15% is from the European market. In terms of segment mix, 2-W accounts for

~55% of its revenue, off-highway accounts for ~9% of revenue and the

remaining of ~36% is from PV, CV and other segments. As of FY17, OEM

sales accounted for 75.1% of its revenue while revenue from its top five

customers constituted 67.2%. STL manufactures products from 29

manufacturing facilities across eight states in India, two manufacturing

facilities in Spain and one manufacturing facility in Mexico. The company has

a long-standing relationship with some of its major customers and is one of

the most significant factors contributing to its growth. STL’s customer

portfolio consists of 79 Indian and global OEMs (HMCL, TVS, Royal Enfield,

Suzuki, UML, Honda, Tata Motors, Ashok Leyland, SML Isuzu, JCB,

Caterpillar, Bosch, Autoliv, CTS and others) across various segments.

Page 4 ICICI Securities Ltd | Retail Equity Research

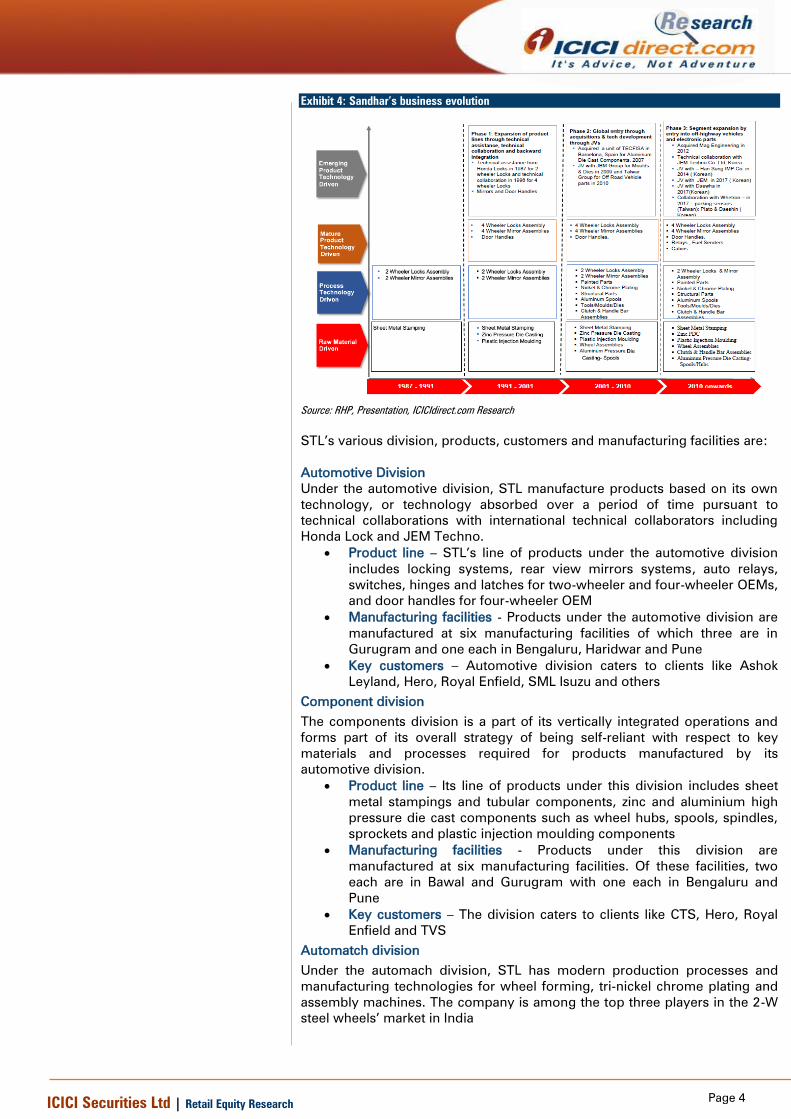

Exhibit 4: Sandhar’s business evolution

Source: RHP, Presentation, ICICIdirect.com Research

STL’s various division, products, customers and manufacturing facilities are:

Automotive Division

Under the automotive division, STL manufacture products based on its own

technology, or technology absorbed over a period of time pursuant to

technical collaborations with international technical collaborators including

Honda Lock and JEM Techno.

Product line – STL’s line of products under the automotive division

includes locking systems, rear view mirrors systems, auto relays,

switches, hinges and latches for two-wheeler and four-wheeler OEMs,

and door handles for four-wheeler OEM

Manufacturing facilities - Products under the automotive division are

manufactured at six manufacturing facilities of which three are in

Gurugram and one each in Bengaluru, Haridwar and Pune

Key customers – Automotive division caters to clients like Ashok

Leyland, Hero, Royal Enfield, SML Isuzu and others

Component division

The components division is a part of its vertically integrated operations and

forms part of its overall strategy of being self-reliant with respect to key

materials and processes required for products manufactured by its

automotive division.

Product line – Its line of products under this division includes sheet

metal stampings and tubular components, zinc and aluminium high

pressure die cast components such as wheel hubs, spools, spindles,

sprockets and plastic injection moulding components

Manufacturing facilities - Products under this division are

manufactured at six manufacturing facilities. Of these facilities, two

each are in Bawal and Gurugram with one each in Bengaluru and

Pune

Key customers – The division caters to clients like CTS, Hero, Royal

Enfield and TVS

Automatch division

Under the automach division, STL has modern production processes and

manufacturing technologies for wheel forming, tri-nickel chrome plating and

assembly machines. The company is among the top three players in the 2-W

steel wheels’ market in India

Page 5 ICICI Securities Ltd | Retail Equity Research

Product line – STL’s line of products under this division includes

wheel rims and wheel assemblies, handle bars, clutch and brake

panels and fender assemblies

Manufacturing facilities - Products under this division are

manufactured at six manufacturing facilities in Bengaluru, Chennai,

Hosur, Mysuru, Oragadam (Chennai) and Nalagarh

Key customers – The division caters to clients like include Hero, Royal

Enfield, Suzuki and TVS

Cabins and fabrication division

Under the cabins and fabrication division, STL caters to the off-highway

vehicles segment. This has been achieved by acquiring Mag Engineering in

FY13 and the cabin business of Arkay Fabsteel in FY15

Product line – STL’s line of products under this division includes

operator cabins, canopies, housings, panels, switchboards, control

cabinets and other high precision sheet metal components for back

hoe loaders, excavators, wheel loaders, cranes and tractors

Manufacturing facilities - Products under this division are

manufactured in four facilities of which two are in Bengaluru and one

each in Pune and Jaipur

Key customers – The division caters to clients like Atlas Copco,

Caterpillar, Doosan Bobcat, JCB, Kobelco, Komatsu, LeeBoy India,

Potain India, TAFE, and Tata Hitachi

HSCI division

Under the HSCI division, STL predominantly cater to Honda Cars. The

company has a 30-year-old relationship with Honda Cars. In 1987, the

company entered into a technical assistance arrangement for supply of 2-W

locks to Honda Lock, which progressed further into a technical collaboration

for 4-W lock assemblies, mirror assemblies and door handles in 1996.

Product line – STL’s line of products under this division includes lock

assemblies, door handles, mirror assemblies and painted products for

passenger vehicles as well as painted products for two-wheelers

Manufacturing facilities - Products under this division are

manufactured at Gurugram and Pathredi, Alwar

Key customers – The division caters to Honda

Some key subsidiaries & joint ventures -

Sandhar Technologies Barcelona, SL

In FY08, STL acquired the business of TECFISA, Spain, which was primarily

engaged in the business of aluminium die of small parts and mould design,

and is named Sandhar Technologies Barcelona, SL (STBSL). It has further

three wholly-owned subsidiaries, ST Mexico, ST Poland and Breniar Projects.

The company caters to some of its key customers including Bosch, Autoliv

and other global auto component manufacturers.

Sandhar Tooling

Sandhar Tooling was incorporated in 2002 as a joint venture between STL

and Steady Stream. The JV largely caters to OEMs while the manufacturing

facility is in Manesar.

Sandhar Strategic Systems

Sandhar Strategic Systems was incorporated on September 9, 2016 as an

MSME for carrying out manufacturing activities in, inter alia, the defence and

aerospace sector. The company is yet to commence its operations.

Page 6 ICICI Securities Ltd | Retail Equity Research

Indo Toolings

Indo Tooling is a joint venture between STL & JBM Auto. Indo Toolings

primarily undertakes commercial tooling activities. STL holds 50% of the

equity share capital of Indo Toolings. The remainder is held by JBM Auto.

Indo Toolings operates under an operation, maintenance and management

agreement entered into with Pithampur Auto Cluster. The company’s key

customers include commercial vehicle OEMs. Its manufacturing facility is in

Indore and Bhopal.

Sandhar Han Sung

Sandhar Han Sung is a joint venture between STL and Han Sung. Sandhar

Han Sung primarily undertakes the manufacture of high precision press parts,

insert moulded contact plates and switches. STL holds 50% of the equity

capital of Sandhar Han Sung. The remainder is held by Han Sung. The key

customers of Sandhar Han Sung include a major electrical equipment

manufacturer and a South Korean automotive component supplier. The

manufacturing facility is in Gurugram and Oragadam.

Jinyoung Sandhar Mechatronics (JSM)

Jinyoung Sandhar Mechatronics is a joint venture between STL and Jinyoung

Electro-Mechanics. JSM primarily undertakes the assembly of AVN panels,

and switches. STL holds 50% of JSM’s equity share capital. The remainder is

held by Jinyoung Electro-Mechanics. A key customer of JSM includes a

South Korean automotive components manufacturer, which supplies to the

only South Korean OEM in the Indian auto industry. The manufacturing

facility operated by JSM is located at Oragadam, Chennai.

Sandhar Daewha

Sandhar Daewha is a joint venture between STL and Daewha Fuel Pump.

Sandhar Daewha had been set up to undertake the manufacture and

assembly of oil fuel modules, fuel filters, starter motors, and wiper blades.

STL holds 50% of Sandhar Daewha’s equity share capital. The remainder is

held by Daewha Fuel Pump.

Sandhar Amkin

Sandhar Amkin is a joint venture between STL and the Amkin Group. Sandhar

Amkin has been set up to undertake the manufacture of safety helmets and

other headgears for 2-W. STL holds 50% of Sandhar Amkin’s equity share

capital. The remainder is held by the Amkin Group.

Sandhar Ecco-Green Energy

Sandhar Ecco-Green Energy is a joint venture between STL, ECCO Green

Energy, DMRG, and Tarun Agrawal. Sandhar Ecco-Green Energy primarily

undertakes solar power installation engineering project contracts for captive

use by the company. STL holds 50% of Sandhar Ecco-Green Energy’s equity

share capital. The remainder is held by ECCO Green Energy, DMRG, and

Tarun Agrawal.

Page 7 ICICI Securities Ltd | Retail Equity Research

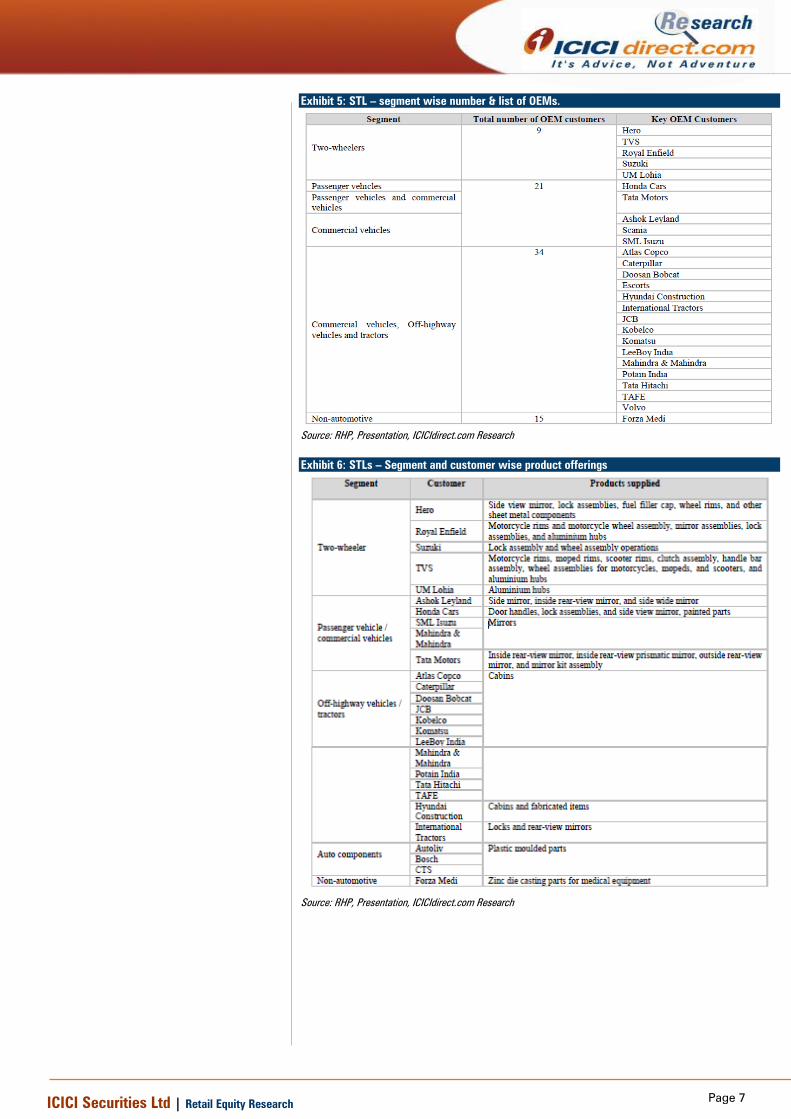

Exhibit 5: STL – segment wise number & list of OEMs.

Source: RHP, Presentation, ICICIdirect.com Research

Exhibit 6: STLs – Segment and customer wise product offerings

Source: RHP, Presentation, ICICIdirect.com Research

Page 8 ICICI Securities Ltd | Retail Equity Research

Exhibit 7: STL’s– Product category wise peers

Source: RHP, Presentation, ICICIdirect.com Research

Investment Rationale

Long-standing, growing relationships with major OEMs

STL has long-standing relationships with 79 Indian & global OEM customers,

which include some leading companies such as Ashok Leyland, Doosan

Bobcat, Hero, Honda Cars, Komatsu, Scania, TAFE, Tata Motors, TVS, UM

Lohia and Volvo. It has grown its client base over the last few years to include

OEMs such as Caterpillar, CTS, Hyundai Construction, International Tractors,

JCB, Kobelco, SML Isuzu and others. STL’s consistent delivery of quality and

cost competitive products over the years, irrespective of the size and scale of

demand, has helped it in receiving orders from multiple OEMs and locations

globally. Its relationship with its customers provides it with the opportunity to

cross sell multiple products to them.

Diversified product portfolio

STL commenced its business by manufacturing sheet metal components

which accounted for 100% of its revenue. However, the revenue contribution

from the same is at 13.8% as of FY17. This is mainly after STL diversified into

various products and across segments. At present, STL manufactures 21

categories of products with varieties, which cater to different automotive

segments such as 2-W, PV, CV, off-highway vehicles and tractors, as well as

non-automotive segments including medical and electrical equipment. Its

current portfolio comprises various categories of products including safety &

security systems such as lock assemblies, mirror assemblies, operator cabins

for off-highway vehicles, aluminium spools, spindles, and hubs. The company

also manufactures other product categories including wheel assemblies,

handle bar assemblies, brake panel assemblies, sheet metal components

such as fuel filler caps, fuel cock assembly, step pillions, tools, dies, moulds,

other aluminium components, crane and tractor parts, plastic and painted

parts such as door handles (inner and outer), panels for televisions, and

cabinets for air conditioners. Through its six joint ventures, Sandhar also

manufactures products like high precision press parts, insert moulded contact

plates, AVN panels and switches.

Production facilities close to customers based on philosophy ‘Be Glocal’

STL’s strategy has been to invest in locations close to its OEM customers’

plants, which has been a key factor in aiding a strong relationship with OEM

customers. Its manufacturing facilities at Gurugram, Chennai & Bengaluru are

close to plants of Hero, Royal Enfield & TVS, respectively. Further, the

company also has manufacturing facilities in Mexico & Spain, and an

assembly and packaging centre in Poland, to cater to customers in Western

Europe, Eastern Europe and Nafta markets. It has expanded its operations

from four manufacturing facilities in India as on FY05 to 31 facilities in India,

two manufacturing facilities in Spain and one in Mexico.

Page 9 ICICI Securities Ltd | Retail Equity Research

Vertical, horizontal integration of its operations from product designing to

supply solutions

STL is present across levels of the automotive component critical value chain.

It provides products & services that range from product design and

prototyping to tool manufacturing, assembly, as well as production of

integrated components. As part of its vertical integration strategy, the

company has established multiple processes like zinc die casting, aluminium

die-casting, plastic injection moulding and an in-house robotic paint shop that

are used in manufacturing and assembly of locking systems. Its integration

strategies reduce the dependence on third party suppliers for a number of

products & services. The company has various in-house R&D activities that

primarily work on development of new products, designing, prototyping, and

product upgrades. STL also has six JVs that manufacture products like high

precision press parts, insert moulded contact plates, AVN panels and

switches. The company also has a technical collaboration with Honda Lock

and JEM Technologies.

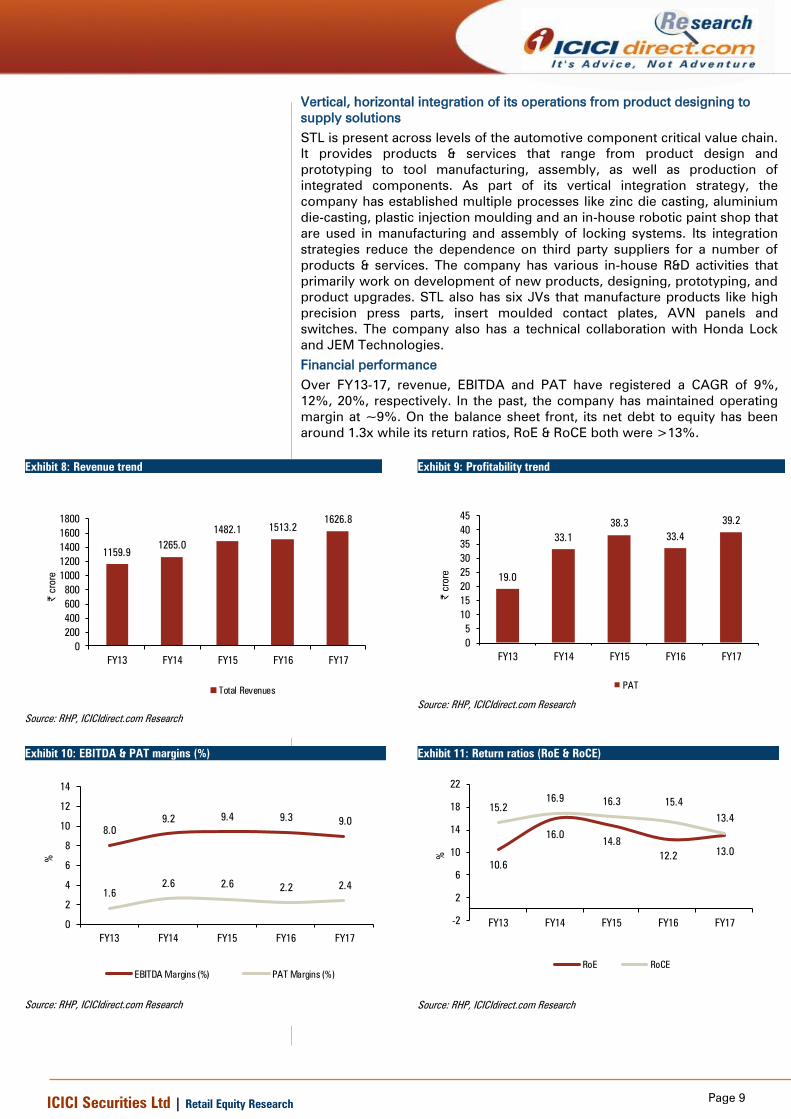

Financial performance

Over FY13-17, revenue, EBITDA and PAT have registered a CAGR of 9%,

12%, 20%, respectively. In the past, the company has maintained operating

margin at ~9%. On the balance sheet front, its net debt to equity has been

around 1.3x while its return ratios, RoE & RoCE both were >13%.

Exhibit 8: Revenue trend

1159.9

1265.0

1482.1 1513.2

1626.8

0

200

400

600

800

1000

1200

1400

1600

1800

FY13 FY14 FY15 FY16 FY17

| crore

Total Revenues

Source: RHP, ICICIdirect.com Research

Exhibit 9: Profitability trend

19.0

33.1

38.3

33.4

39.2

0

5

10

15

20

25

30

35

40

45

FY13 FY14 FY15 FY16 FY17

| crore

PAT

Source: RHP, ICICIdirect.com Research

Exhibit 10: EBITDA & PAT margins (%)

8.0

9.2 9.4 9.39.0

1.6

2.6 2.62.2 2.4

0

2

4

6

8

10

12

14

FY13 FY14 FY15 FY16 FY17

%

EBITDA Margins (%) PAT Margins (%)

Source: RHP, ICICIdirect.com Research

Exhibit 11: Return ratios (RoE & RoCE)

10.6

16.014.8

12.213.0

15.2

16.916.3 15.4

13.4

-2

2

6

10

14

18

22

FY13 FY14 FY15 FY16 FY17

%

RoE RoCE

Source: RHP, ICICIdirect.com Research

Page 10 ICICI Securities Ltd | Retail Equity Research

Exhibit 12: Net debt-equity

1.21.3

1.2 1.1

1.3

0.0

0.5

1.0

1.5

2.0

FY13 FY14 FY15 FY16 FY17

| crore

Net Debt/Equity

Source: RHP, ICICIdirect.com Research

Exhibit 13: Free cash flow

-24.4

-15.2-11.0

37.0

-13.7

-30

-20

-10

0

10

20

30

40

50

FY13 FY14 FY15 FY16 FY17

| crore

FCF

Source: RHP, ICICIdirect.com Research

Exhibit 14: Product wise revenue mix (%) – FY17

23

13

11

13

17

27

Locks Mirror Assembly Wheel Assembly

Sheet Metal Aluminium Comp Others

Source: RHP, ICICIdirect.com Research

Exhibit 15: Segment wise revenue mix (%) – FY17

895

146

586

2-W OHT 4-W (PV + CV)

Source: RHP, ICICIdirect.com Research

Exhibit 16: Geography wise revenue mix

13141401

875

204

233

116

0

200

400

600

800

1000

1200

1400

1600

1800

FY16 FY17 6MFY18

| crore

India Europe

Source: RHP, Presentation, ICICIdirect.com Research

Page 11 ICICI Securities Ltd | Retail Equity Research

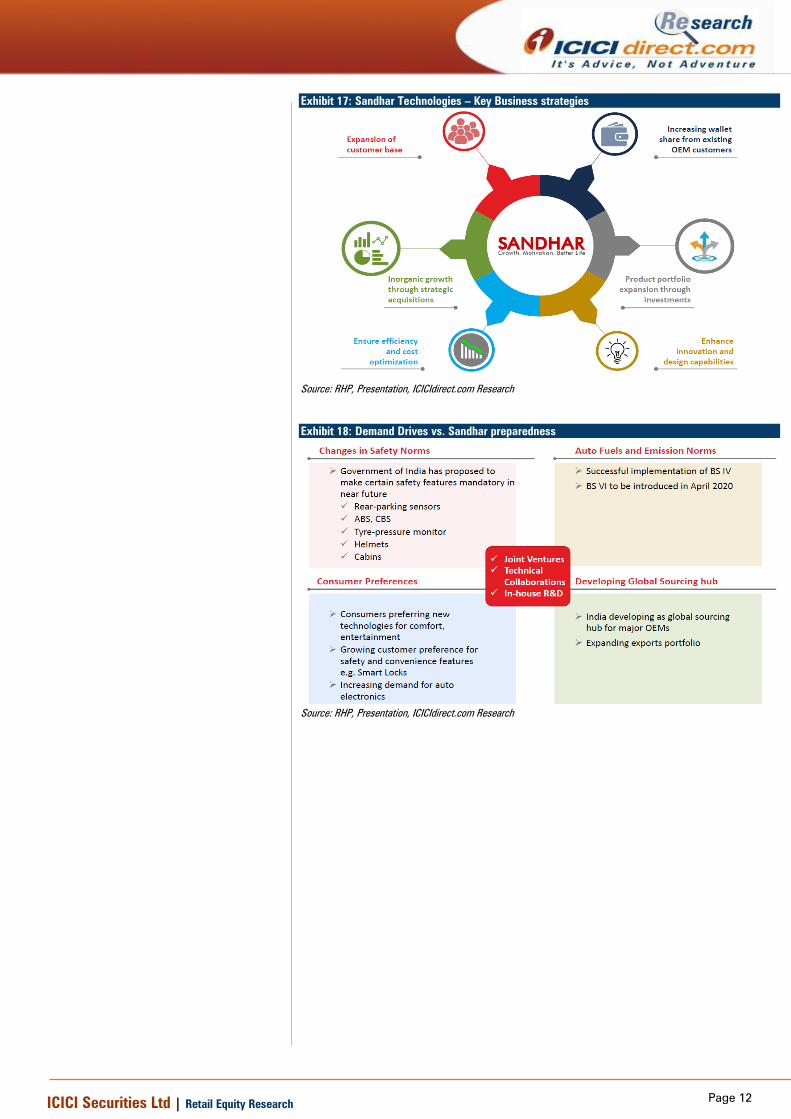

Key business strategy

STL is committed to increasing its market share across its product verticals &

customers spend per vehicle. The company is diversifying product offerings,

customer base and geographical footprint. The following are some of its key

business strategies:

Expansion of product portfolio through investment in new products, business

with high growth potential

The company plans to leverage current trends in the automotive sector such

as increasing focus on safety, fuel efficiency, comfort, customisation,

entertainment and communication, as well as auto electronics to develop

products that meet its OEM customers’ requirements in these areas. The

company is exploring & testing the feasibility of various technology driven

and high margin products such as smart keys, auto relays, switches, USB

chargers, parking assistant systems, fuel filters, fuel modules, fuel senders,

starter motors and shark-finned antennas, among others in partnership with

its OEM customers. STL aims to capture dominant market share in each of its

new products and at the same time, also intends to continuously upgrade its

existing products and customise them according to the needs of its OEM

customers.

Expand customer base

The company continues to focus on increasing its customer base by

marketing existing products to new customers, together with developing new

products. It has increased its customer base in the past through new products

and segments as well as through acquisitions. The number of OEMs

customer base has grown from 58 in FY13 to 79 in FY17.

Increase wallet share from existing OEM customers

STL focuses on increasing its contribution per vehicle (i.e. the number and

value of components supplied by STL in vehicles produced by its OEM

customers) and also works closely with its OEM customers to develop a

broader portfolio of products, which meet their requirements. Over the years,

STL has been able to increase its customers’ contribution to its revenue. For

instance – its revenue from Royal Enfield was | 18.74 crore in FY13, which

increased to | 69.74 crore in FY17. Further, its revenue from Honda Cars was

at | 46.82 crore in FY13, which increased to | 130.5 crore in FY17. STL

intends to continue focus on increasing its contribution per vehicle and work

closely with OEM customers to develop a broader portfolio of products,

which meet their requirements.

Inorganic growth through strategic acquisitions

The company has a successful track record of acquiring assets and ensuring

two-way transfer of best practices. STL evaluate potential acquisitions on

several criteria including access to technology, new customer access,

new/adjacent product portfolio, new market access, size of the acquisition

and profitability. The company endeavours to target segments where it can

leverage its existing expertise and competencies to build new capabilities.

Ensure efficiency, cost optimisation & enhance innovation/design capabilities

The company constantly endeavours to reduce the costs of its operations

while ensuring the quality of products. STL already has central planning,

marketing and raw material procurement teams that helps company to

reduce cost and achieve operational efficiencies and economies of scale.

Further ensuring cost rationalisation in its manufacturing processes continues

to be one of its key strategies. The company intends to focus on adopting

strategies to establish a standardised platform across its business units for

the processes, hardware and software infrastructure and workforce.

Page 12 ICICI Securities Ltd | Retail Equity Research

Exhibit 17: Sandhar Technologies – Key Business strategies

Source: RHP, Presentation, ICICIdirect.com Research

Exhibit 18: Demand Drives vs. Sandhar preparedness

Source: RHP, Presentation, ICICIdirect.com Research

Page 13 ICICI Securities Ltd | Retail Equity Research

Key Risk & Concerns

Slowdown in overall demand environment (automotive space)

STL’s performance is largely dependent on the automotive space and any

slowdown in the space could directly impact its performance. Though the

company has a presence across segments, it has a higher dependence on the

2-W segment, which accounts for ~54.6% of its revenue as of FY17. In the

event of a decline in 2-W demand, or any other developments that make the

sale of components in the 2-W market less economically beneficial, the same

can adversely affect its business, results of operations and prospects.

Failure to identify, understand evolving industry trends & preference

The changes in regulatory/industry requirement or in competitive

technologies may render few of its product obsolete or less attractive. The

ability to anticipate changes in technology and regulatory standards and

successfully develop and introduce new and enhanced products on a timely

basis is a significant factor.

High customer concentration risk

STL has higher customer concentration risk, which could impact its financial

performance. As of FY17, OEM sales accounted for 75.1% of its revenue

while revenue from its top five customers constituted 67.2%. The company

does not have any firm commitment for supplying component to its

customers. Thus, it has to rely on purchase orders that may be amended or

cancelled prior to finalisation. Also, loss of any of its key customers or a

significant reduction in demand from its customers may have an adverse

effect on their business.

Unable to manage its raw material requirement

STL is highly depended on zinc, sheet metal parts and aluminium that

account for 41.5% of its revenue. It sources its glass requirement from one of

its major suppliers, which accounts for 90% of its glass requirement. If STL is

unable to manage its raw material procurement (price, availability & quality) it

may impact its production and business. Also, the purchase of goods

(bought-out parts) constituted ~28.3% of its overall raw material cost.

Adverse currency movement may impact its performance

STL’s consolidated results of operations are in rupee while its subsidiaries

report their financial results in their respective local currencies of France,

Spain, Mexico and others. Hence, there could be an impact on consolidation

of its financials primarily due to currency movement. As of FY17, revenue

from Europe and other location (outside India) were at | 232.8 crore (~14.3%

of its total revenue). Thus, exchange rate fluctuations may have an adverse

effect on its reported revenues and financial results.

Page 14 ICICI Securities Ltd | Retail Equity Research

Objects of issue

The object of the issue 1) proceeds of fresh issue (| 300 crore) would be used

towards repayment or prepayment of debt (around | 225 crore); 2) offer for

sale (64 lakh equity share at upper price band of | 332/share will result into

overall value of | 212.50 crore) by GTI Capital Beta (currently holds 89.34 lakh

share or 17.47% stake in the company with average cost of acquisition at |

84/share) and; 3) general corporate expense. Thus, the overall offer size (at

upper price band of | 332/share) will be around | 512.5 crore.

Valuations

STL has a diversified product portfolio vis-à-vis its peers. Comparing with

some of the listed entity, which are into similar kind of business, STL (at

upper price band of | 332/share) is available at 51x on FY17 diluted EPS of

| 6.5 compared to some of its other ancillary players that trade in the range of

25-50x their FY17 EPS. On the book value front, STL will be available (at

upper price band of | 332/share) at ~5.6x on FY17 book value of | 58.9/share

compared to some of its other peers available in the range of ~3-12x.

Page 15 ICICI Securities Ltd | Retail Equity Research

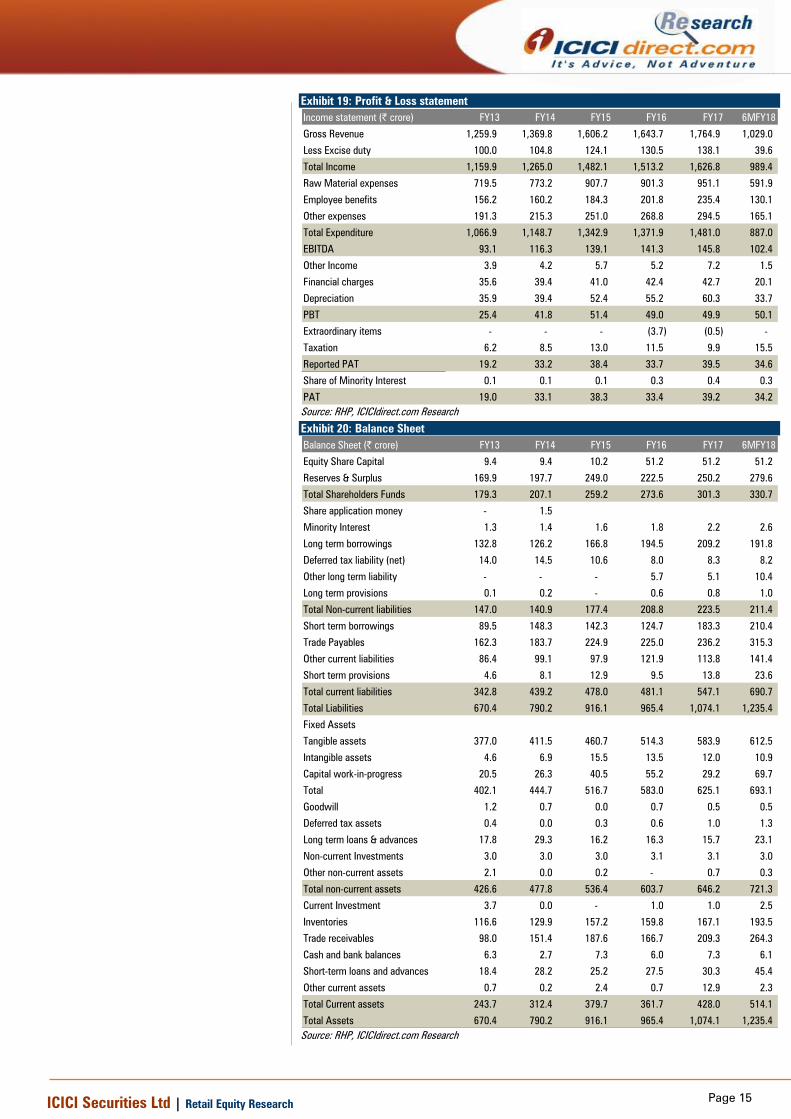

Exhibit 19: Profit & Loss statement

Income statement (| crore) FY13 FY14 FY15 FY16 FY17 6MFY18

Gross Revenue 1,259.9 1,369.8 1,606.2 1,643.7 1,764.9 1,029.0

Less Excise duty 100.0 104.8 124.1 130.5 138.1 39.6

Total Income 1,159.9 1,265.0 1,482.1 1,513.2 1,626.8 989.4

Raw Material expenses 719.5 773.2 907.7 901.3 951.1 591.9

Employee benefits 156.2 160.2 184.3 201.8 235.4 130.1

Other expenses 191.3 215.3 251.0 268.8 294.5 165.1

Total Expenditure 1,066.9 1,148.7 1,342.9 1,371.9 1,481.0 887.0

EBITDA 93.1 116.3 139.1 141.3 145.8 102.4

Other Income 3.9 4.2 5.7 5.2 7.2 1.5

Financial charges 35.6 39.4 41.0 42.4 42.7 20.1

Depreciation 35.9 39.4 52.4 55.2 60.3 33.7

PBT 25.4 41.8 51.4 49.0 49.9 50.1

Extraordinary items - - - (3.7) (0.5) -

Taxation 6.2 8.5 13.0 11.5 9.9 15.5

Reported PAT 19.2 33.2 38.4 33.7 39.5 34.6

Share of Minority Interest 0.1 0.1 0.1 0.3 0.4 0.3

PAT 19.0 33.1 38.3 33.4 39.2 34.2

Source: RHP, ICICIdirect.com Research

Exhibit 20: Balance Sheet

Balance Sheet (| crore) FY13 FY14 FY15 FY16 FY17 6MFY18

Equity Share Capital 9.4 9.4 10.2 51.2 51.2 51.2

Reserves & Surplus 169.9 197.7 249.0 222.5 250.2 279.6

Total Shareholders Funds 179.3 207.1 259.2 273.6 301.3 330.7

Share application money - 1.5

Minority Interest 1.3 1.4 1.6 1.8 2.2 2.6

Long term borrowings 132.8 126.2 166.8 194.5 209.2 191.8

Deferred tax liability (net) 14.0 14.5 10.6 8.0 8.3 8.2

Other long term liability - - - 5.7 5.1 10.4

Long term provisions 0.1 0.2 - 0.6 0.8 1.0

Total Non-current liabilities 147.0 140.9 177.4 208.8 223.5 211.4

Short term borrowings 89.5 148.3 142.3 124.7 183.3 210.4

Trade Payables 162.3 183.7 224.9 225.0 236.2 315.3

Other current liabilities 86.4 99.1 97.9 121.9 113.8 141.4

Short term provisions 4.6 8.1 12.9 9.5 13.8 23.6

Total current liabilities 342.8 439.2 478.0 481.1 547.1 690.7

Total Liabilities 670.4 790.2 916.1 965.4 1,074.1 1,235.4

Fixed Assets

Tangible assets 377.0 411.5 460.7 514.3 583.9 612.5

Intangible assets 4.6 6.9 15.5 13.5 12.0 10.9

Capital work-in-progress 20.5 26.3 40.5 55.2 29.2 69.7

Total 402.1 444.7 516.7 583.0 625.1 693.1

Goodwill 1.2 0.7 0.0 0.7 0.5 0.5

Deferred tax assets 0.4 0.0 0.3 0.6 1.0 1.3

Long term loans & advances 17.8 29.3 16.2 16.3 15.7 23.1

Non-current Investments 3.0 3.0 3.0 3.1 3.1 3.0

Other non-current assets 2.1 0.0 0.2 - 0.7 0.3

Total non-current assets 426.6 477.8 536.4 603.7 646.2 721.3

Current Investment 3.7 0.0 - 1.0 1.0 2.5

Inventories 116.6 129.9 157.2 159.8 167.1 193.5

Trade receivables 98.0 151.4 187.6 166.7 209.3 264.3

Cash and bank balances 6.3 2.7 7.3 6.0 7.3 6.1

Short-term loans and advances 18.4 28.2 25.2 27.5 30.3 45.4

Other current assets 0.7 0.2 2.4 0.7 12.9 2.3

Total Current assets 243.7 312.4 379.7 361.7 428.0 514.1

Total Assets 670.4 790.2 916.1 965.4 1,074.1 1,235.4

Source: RHP, ICICIdirect.com Research

Page 16 ICICI Securities Ltd | Retail Equity Research

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns

ratings to its stocks according to their notional target price vs. current market price and then categorises them

as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional

target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

Page 17 ICICI Securities Ltd | Retail Equity Research

ANALYST CERTIFICATION

We /I, Nishit Zota, MBA & Vidrum Mehta, MBA Research Analyst, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately

reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this

report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities

Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has

its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which

are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking

and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts

and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without

prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current.

Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended

temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this

company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate

the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any

loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the

risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any

compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts

and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Nishit Zota, MBA & Vidrum Mehta, MBA Research Analyst, of this report have not received any compensation from the companies mentioned in the report in the preceding twelve

months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month

preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

It is confirmed that Nishit Zota, MBA & Vidrum Mehta, MBA Research Analyst, do not serve as an officer, director or employee of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and

to observe such restriction.

ICICI Securities Limited has been appointed as one of the Book Running Lead Managers to the initial public offer of Sandhar Technologies Ltd. This report is prepared on the basis of publicly available

information.