Hikal Ltd. ( HIKCHE) -...

24

ICICI Securities – Retail Equity Research Initiating Coverage March 19, 2019 CMP: | 166 Target: | 200 ( 21%) Target Period: 12 months Hikal Ltd. ( HIKCHE) BUY Unique blend of pharma and crop protection… Established in 1988 by first generation promoter Jay Hiremath, Hikal has a unique business model with ‘pharma’ and ‘crop protection’ as separate growth engines. The company has evolved as a B2B player catering to global crop protection and specialty chemical companies besides pharmaceutical and animal health players. For 9MFY19, pharma and crop protection accounted for 60% and 40%, respectively, of total operating revenues. We are initiating coverage on the company as we find a compelling risk-reward proposition at the current level considering the capability of the company in both pharma and crop protection along with future growth prospects based on client stickiness and calibrated capex. Expertise in APIs to drive pharma growth Hikal ventured into the pharma API business by virtue of acquisition of Novartis’ Panoli plant in the year 2000. In a short span of time, banking on its chemistry skills, the company has been able to tap incremental customers via the CDMO route. Hikal also operates as a dedicated API supplier as it expands its portfolio. We expect the pharma segment to grow at a CAGR of 15.5% in FY19-21E to | 1250 crore on the back of new offerings and repeat business from CDMO customers. Crop protection growth to piggyback on client relationship Hikal started operations as a crop protection company in 1991 after acquiring Merck’s facility in Mahad. Since then, it has come a long way with a predominantly CDMO focused business model catering mainly to global innovators. Over the years, the company has increased its product offerings with a foray into niche products and specialty chemicals. We expect crop protection segment to grow at 12.5% CAGR in FY19-21E to | 773 crore due to sustained product offerings and optimum capacity utilisation. Experience in high profile clients servicing to the fore… For years, the company has been dealing with high profile MNCs like Merck & Co, Bayer, Syngenta, BASF, Pfizer to name a few. With proven capabilities and management pedigree, we believe Hikal offers a compelling value proposition as it continues to expand in both pharma and crop protection segments with separate focus and a calibrated approach. This bodes well in the current scenario when Chinese supply disturbances are likely to create opportunities for Indian players both in APIs and crop protection CDMO. The company has spent ~| 500 crore over the last five years to augment capacities. After years of volatility in growth, Hikal has been witnessing a relatively stable growth trajectory. We expect sales, EBITDA, PAT to grow at a CAGR of 15%, 18%, 30%, respectively, in FY19-21E on the back of new launches and better operating leverage. Simultaneously, we also expect a 330 bps RoCE improvement to 17.3% through FY21. We arrive at a valuation of | 200 based on 15x FY21E EPS of | 13.3. Key Financial Summary (Year-end March) FY18 FY19E FY20E FY21E Revenues (| crore) 1296.1 1,548.1 1,783.7 2,051.3 EBITDA (| crore) 241.7 293.7 345.0 409.7 EBITDA Margins (%) 18.6 19.0 19.3 20.0 Net Profit (| crore) 77.2 97.3 127.4 164.4 EPS (|) 6.3 7.9 10.3 13.3 PE (x) 26.5 21.0 16.0 12.4 EV to EBITDA (x) 11.0 9.2 8.0 6.7 Price to book (x) 3.1 2.7 2.4 2.1 RoE (%) 11.5 13.0 15.0 16.8 RoCE (%) 12.2 14.0 15.3 17.3 Source: ICICI Direct Research, Company Particulars Particular Market Cap Debt (FY18) Cash (FY18) EV 52 week H/L (|) 207/134 Equity capital Face value | 2 MF Holdings (%) 1.5 FII Holdings (%) 4.2 Amount | 2044 crore | 635 crore | 27 crore | 2652 crore | 24.7 crore Key Highlights Hikal has a unique business model, with crop protection and pharma as separate growth engines Expertise in APIs is expected to drive pharma growth Crop protection growth to piggyback on client relationship After years of volatility in growth, the company is witnessing a relatively stable growth trajectory Price movement Source: ICICI Direct Research, Company Research Analyst Siddhant Khandekar [email protected] MItesh Shah [email protected] 0.0 100.0 200.0 300.0 0 4000 8000 12000 16000 Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18 Mar-19 CNX Pharma Hikal

Transcript of Hikal Ltd. ( HIKCHE) -...

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

Init

iatin

g C

overage

March 19, 2019

CMP: | 166 Target: | 200 ( 21%) Target Period: 12 months

Hikal Ltd. ( HIKCHE)

BUY

Unique blend of pharma and crop protection…

Established in 1988 by first generation promoter Jay Hiremath, Hikal has a

unique business model with ‘pharma’ and ‘crop protection’ as separate

growth engines. The company has evolved as a B2B player catering to

global crop protection and specialty chemical companies besides

pharmaceutical and animal health players. For 9MFY19, pharma and crop

protection accounted for 60% and 40%, respectively, of total operating

revenues. We are initiating coverage on the company as we find a

compelling risk-reward proposition at the current level considering the

capability of the company in both pharma and crop protection along with

future growth prospects based on client stickiness and calibrated capex.

Expertise in APIs to drive pharma growth

Hikal ventured into the pharma API business by virtue of acquisition of

Novartis’ Panoli plant in the year 2000. In a short span of time, banking on

its chemistry skills, the company has been able to tap incremental customers

via the CDMO route. Hikal also operates as a dedicated API supplier as it

expands its portfolio. We expect the pharma segment to grow at a CAGR of

15.5% in FY19-21E to | 1250 crore on the back of new offerings and repeat

business from CDMO customers.

Crop protection growth to piggyback on client relationship

Hikal started operations as a crop protection company in 1991 after

acquiring Merck’s facility in Mahad. Since then, it has come a long way with

a predominantly CDMO focused business model catering mainly to global

innovators. Over the years, the company has increased its product offerings

with a foray into niche products and specialty chemicals. We expect crop

protection segment to grow at 12.5% CAGR in FY19-21E to | 773 crore due

to sustained product offerings and optimum capacity utilisation.

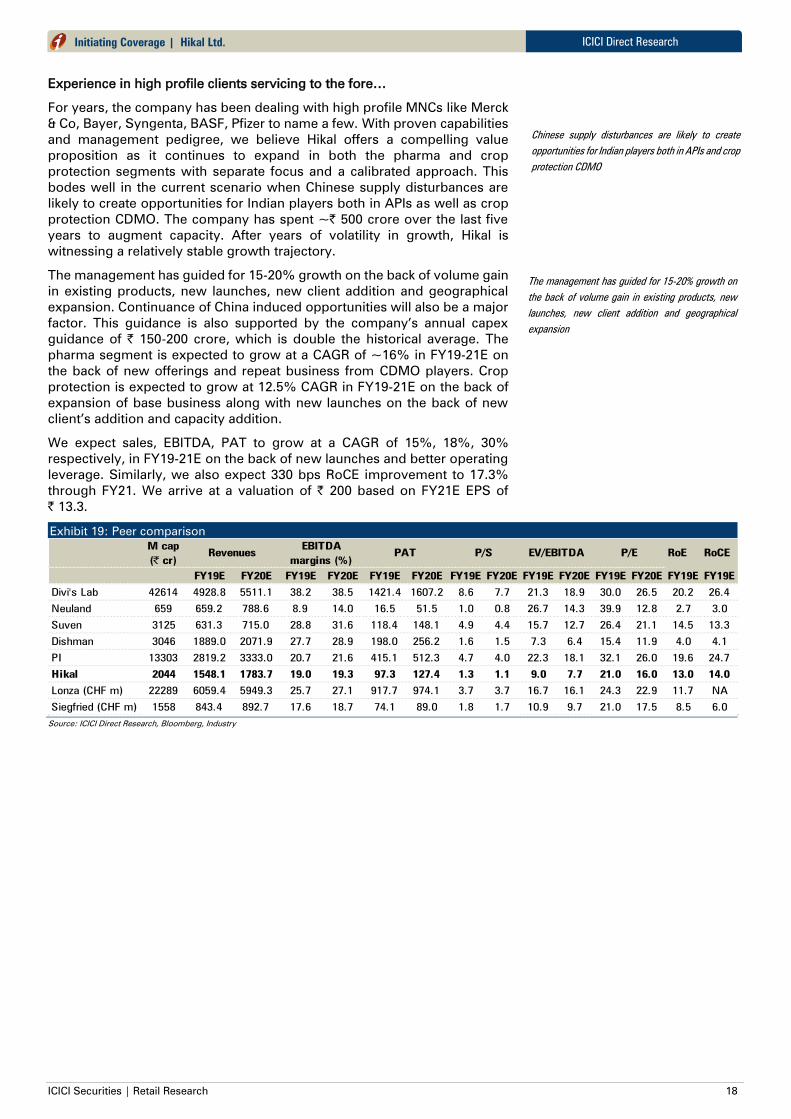

Experience in high profile clients servicing to the fore…

For years, the company has been dealing with high profile MNCs like Merck

& Co, Bayer, Syngenta, BASF, Pfizer to name a few. With proven capabilities

and management pedigree, we believe Hikal offers a compelling value

proposition as it continues to expand in both pharma and crop protection

segments with separate focus and a calibrated approach. This bodes well in

the current scenario when Chinese supply disturbances are likely to create

opportunities for Indian players both in APIs and crop protection CDMO. The

company has spent ~| 500 crore over the last five years to augment

capacities. After years of volatility in growth, Hikal has been witnessing a

relatively stable growth trajectory. We expect sales, EBITDA, PAT to grow at

a CAGR of 15%, 18%, 30%, respectively, in FY19-21E on the back of new

launches and better operating leverage. Simultaneously, we also expect a

330 bps RoCE improvement to 17.3% through FY21. We arrive at a valuation

of | 200 based on 15x FY21E EPS of | 13.3.

Key Financial Summary

(Year-end March) FY18 FY19E FY20E FY21E

Revenues (| crore) 1296.1 1,548.1 1,783.7 2,051.3

EBITDA (| crore) 241.7 293.7 345.0 409.7

EBITDA Margins (%) 18.6 19.0 19.3 20.0

Net Profit (| crore) 77.2 97.3 127.4 164.4

EPS (|) 6.3 7.9 10.3 13.3

PE (x) 26.5 21.0 16.0 12.4

EV to EBITDA (x) 11.0 9.2 8.0 6.7

Price to book (x) 3.1 2.7 2.4 2.1

RoE (%) 11.5 13.0 15.0 16.8

RoCE (%) 12.2 14.0 15.3 17.3

Source: ICICI Direct Research, Company

Particulars

Particular

Market Cap

Debt (FY18)

Cash (FY18)

EV

52 week H/L (|) 207/134

Equity capital

Face value | 2

MF Holdings (%) 1.5

FII Holdings (%) 4.2

Amount

| 2044 crore

| 635 crore

| 27 crore

| 2652 crore

| 24.7 crore

Key Highlights

Hikal has a unique business model,

with crop protection and pharma as

separate growth engines

Expertise in APIs is expected to drive

pharma growth

Crop protection growth to piggyback

on client relationship

After years of volatility in growth, the

company is witnessing a relatively

stable growth trajectory

Price movement

Source: ICICI Direct Research, Company

Research Analyst

Siddhant Khandekar

MItesh Shah

0.0

100.0

200.0

300.0

0

4000

8000

12000

16000

Mar-16

Sep-16

Mar-17

Sep-17

Mar-18

Sep-18

Mar-19

CNX Pharma Hikal

ICICI Securities | Retail Research 2

ICICI Direct Research Initiating Coverage | Hikal Ltd.

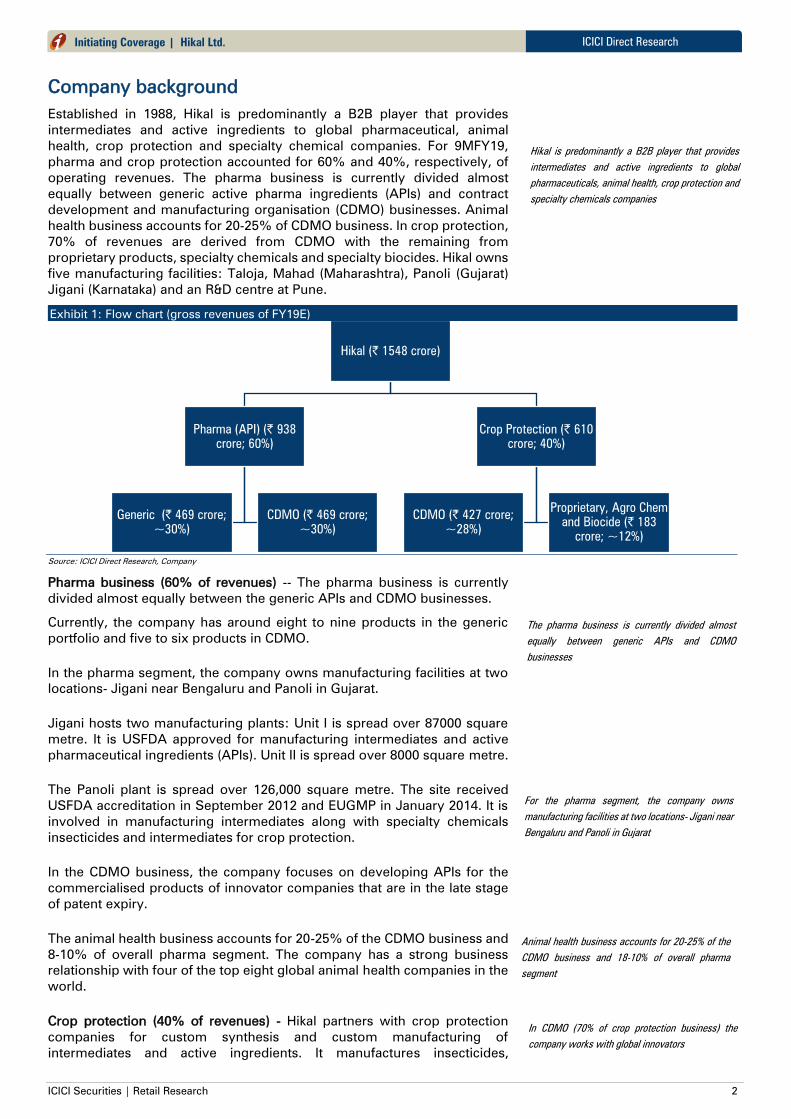

Company background

Established in 1988, Hikal is predominantly a B2B player that provides

intermediates and active ingredients to global pharmaceutical, animal

health, crop protection and specialty chemical companies. For 9MFY19,

pharma and crop protection accounted for 60% and 40%, respectively, of

operating revenues. The pharma business is currently divided almost

equally between generic active pharma ingredients (APIs) and contract

development and manufacturing organisation (CDMO) businesses. Animal

health business accounts for 20-25% of CDMO business. In crop protection,

70% of revenues are derived from CDMO with the remaining from

proprietary products, specialty chemicals and specialty biocides. Hikal owns

five manufacturing facilities: Taloja, Mahad (Maharashtra), Panoli (Gujarat)

Jigani (Karnataka) and an R&D centre at Pune.

Exhibit 1: Flow chart (gross revenues of FY19E)

Source: ICICI Direct Research, Company

Pharma business (60% of revenues) -- The pharma business is currently

divided almost equally between the generic APIs and CDMO businesses.

Currently, the company has around eight to nine products in the generic

portfolio and five to six products in CDMO.

In the pharma segment, the company owns manufacturing facilities at two

locations- Jigani near Bengaluru and Panoli in Gujarat.

Jigani hosts two manufacturing plants: Unit I is spread over 87000 square

metre. It is USFDA approved for manufacturing intermediates and active

pharmaceutical ingredients (APIs). Unit II is spread over 8000 square metre.

The Panoli plant is spread over 126,000 square metre. The site received

USFDA accreditation in September 2012 and EUGMP in January 2014. It is

involved in manufacturing intermediates along with specialty chemicals

insecticides and intermediates for crop protection.

In the CDMO business, the company focuses on developing APIs for the

commercialised products of innovator companies that are in the late stage

of patent expiry.

The animal health business accounts for 20-25% of the CDMO business and

8-10% of overall pharma segment. The company has a strong business

relationship with four of the top eight global animal health companies in the

world.

Crop protection (40% of revenues) - Hikal partners with crop protection

companies for custom synthesis and custom manufacturing of

intermediates and active ingredients. It manufactures insecticides,

Hikal (| 1548 crore)

Pharma (API) (| 938

crore; 60%)

Generic (| 469 crore;

~30%)

CDMO (| 469 crore;

~30%)

Crop Protection (| 610

crore; 40%)

CDMO (| 427 crore;

~28%)

Proprietary, Agro Chem

and Biocide (| 183

crore; ~12%)

Hikal is predominantly a B2B player that provides

intermediates and active ingredients to global

pharmaceuticals, animal health, crop protection and

specialty chemicals companies

The pharma business is currently divided almost

equally between generic APIs and CDMO

businesses

For the pharma segment, the company owns

manufacturing facilities at two locations- Jigani near

Bengaluru and Panoli in Gujarat

Animal health business accounts for 20-25% of the

CDMO business and 18-10% of overall pharma

segment

In CDMO (70% of crop protection business) the

company works with global innovators

ICICI Securities | Retail Research 3

ICICI Direct Research Initiating Coverage | Hikal Ltd.

fungicides and herbicides for customers with a major chunk from

insecticides. In CDMO (70% of crop protection business) the company

works with global innovators, which involves developing crop protection

products from gram to kilo to tonne scale at its kilo lab, pilot plants and

commercial plants meeting the stringent regulatory and customer

requirement. Majority of the crop protection business is export oriented.

The company has around nine to 11 products in the CDMO business and

about five to six own products. No single product in the CDMO business

comprises more than 15% of the business. Hikal is also working on a few

niche patented products in this segment. The company has about one or

two products that are in late stages of registration and launch.

In the specialty chemicals business (~20% of crop protection business), the

company offers specialty biocides and antimicrobial actives and additives.

These products are predominantly used in industries like leather, paint,

paper, water treatment, personal care, building materials and textiles.

The company has three sites dedicated to crop protection, Mahad, Taloja

and Panoli. The 27000 square metre Mahad facility is the first manufacturing

site of Hikal that was established in 1991. This site facilitates manufacturing

of specially chemicals, fungicides, herbicides and intermediates. Another

site is in Taloja (60,000 square metre), Maharashtra that was commissioned

in 1997 in a technical collaboration with US based Merck & Co. The site

facilitates manufacturing of fungicides, insecticides and intermediates. This

site also manufactures patent API for innovator companies.

The company spends 3-4% of total revenues in R&D filing and developing

own proprietary products in both pharma and crop protection segments.

Hikal has also developed a new API for Pregabalin (CNS) using an enzymatic

process that is both cost-effective and environmental friendly.

Exhibit 2: Time Line

Year Milestone

1988 Hikal incorporated

1991 First manufacturing at Mahad, begins operations - signs long term agreement with Hoechst India

1995 Signs long term manufacturing and supply agreement with Merck, US for large volume Agrovet active ingredient

1997 Manufacturing of active ingredient for Merck begins at Taloja site

2000 Acquires manufacturing site from Novartis in Panoli, Gujarat

2001 Acquires R&D and manufacturing site in Bangalore. Maiden entry in pharmaceutical business

2002 First pharmaceutical API DMF filed in US

2003 New API plant commissioned at Bangalore. Multi-purpose pharmaceutical intermediate plant commissioned at Panoli

2005 Signs long term supply agreement with a multinational crop protection company

2006 Signs long term supply contract with global innovator company for commercial supply of APls

2007 Signs long term contract API manufacturing supply agreement with leading animal health company

2008 IFC (World Bank) invests 8.27% equity into company

2009 Acoris (R&D centre), Pune becomes operational

2009 Signs long term supply contract for on patent molecule with global crop protection innovator company

2013 Signs long term supply agreement for human health products with global biopharmaceutical company

2014 Pharmaceutical sites Panoli & Bangalore receive EUGMP approval

2015 New development & launch plant in Bangalore commissioned for new products from pharmaceutical division

2017 Commissions new state-of-the-art plant at Mahad for leading global crop protection innovator company

Source: ICICI Direct Research, Company

The company has around nine to 11 products in the

CDMO business and about five to six of own

products

The company has three sites dedicated to crop

protection- Mahad, Taloja and Panoli

The company spends 3-4% of total revenues in R&D

filing and developing own proprietary products in

both pharma and crop protection segments

ICICI Securities | Retail Research 4

ICICI Direct Research Initiating Coverage | Hikal Ltd.

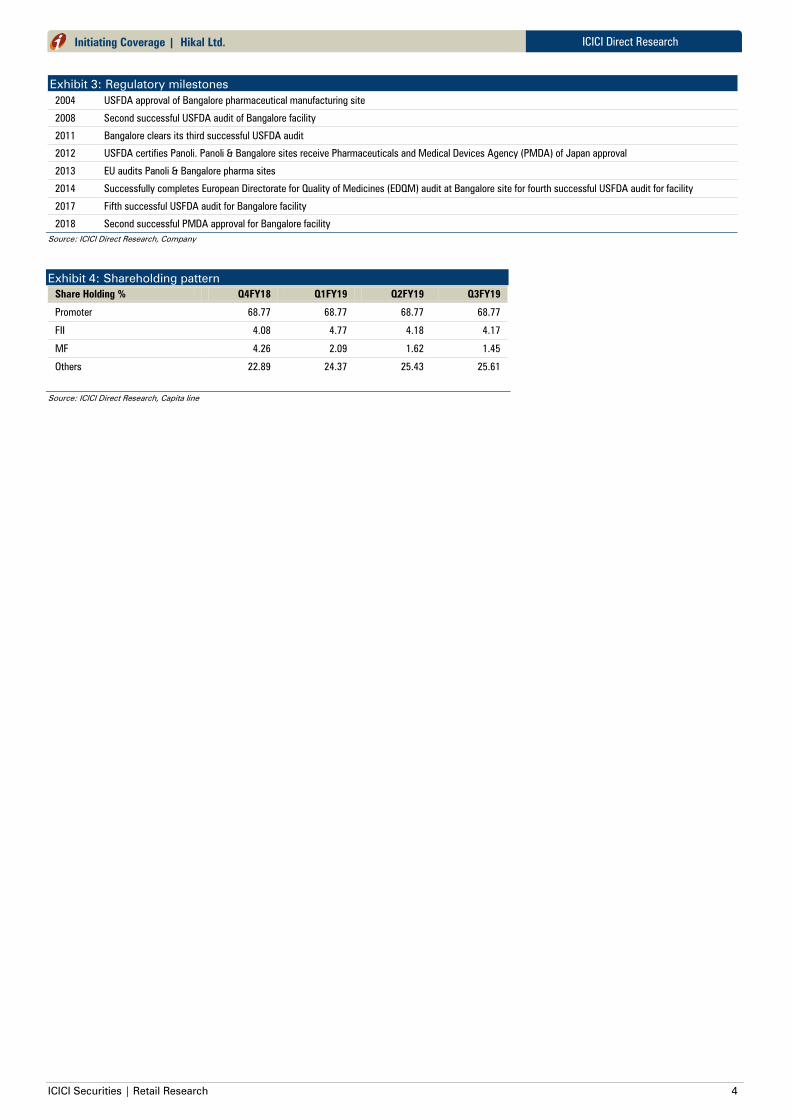

Exhibit 3: Regulatory milestones

2004 USFDA approval of Bangalore pharmaceutical manufacturing site

2008 Second successful USFDA audit of Bangalore facility

2011 Bangalore clears its third successful USFDA audit

2012 USFDA certifies Panoli. Panoli & Bangalore sites receive Pharmaceuticals and Medical Devices Agency (PMDA) of Japan approval

2013 EU audits Panoli & Bangalore pharma sites

2014 Successfully completes European Directorate for Quality of Medicines (EDQM) audit at Bangalore site for fourth successful USFDA audit for facility

2017 Fifth successful USFDA audit for Bangalore facility

2018 Second successful PMDA approval for Bangalore facility

Source: ICICI Direct Research, Company

Exhibit 4: Shareholding pattern

Share Holding % Q4FY18 Q1FY19 Q2FY19 Q3FY19

Promoter 68.77 68.77 68.77 68.77

FII 4.08 4.77 4.18 4.17

MF 4.26 2.09 1.62 1.45

Others 22.89 24.37 25.43 25.61

Source: ICICI Direct Research, Capita line

ICICI Securities | Retail Research 5

ICICI Direct Research Initiating Coverage | Hikal Ltd.

Investment Rationale-

Expertise in APIs to drive pharma growth

Having got established as a crop protection B2B player, Hikal ventured into

the pharma API business by virtue of acquisition of Novartis’ Panoli plant in

2000. The company later acquired another manufacturing and R&D facility

at Jigani near Bangalore in 2001. Since then, Hikal has developed and filed

as many as 28 drug master files (DMFs) with the USFDA for the US market.

The company has also filed product dossiers for other regulated markets.

As mentioned earlier, the business was divided almost equally between

generic APIs and CDMO.

Currently, the company has around eight to nine products in the generic

portfolio and five to six products in CDMO. Gabapentin (CNS) is the largest

product that contributes ~40% to total pharma sales. The pharma business

is mainly export-oriented with ~55% of sales derived from the US, 30% from

Europe and the balance from the rest of the world (RoW).

During FY16-19E, pharma segment grew at ~18% CAGR YoY due to 1)

timely addition of capacity, 2) new launches, 3) improved market share in

existing products, 4) windfall on account of API supply constraints from

China and 5) favourable currency. The company is mainly focusing on

Central Nervous System (CNS) and anti-diabetic segments.

Exhibit 5: Strong growth in FY16-19E (| crore)

Source: ICICI Direct Research, Company

Generic (APIs) – Hikal manufactures APIs and intermediates for global

innovator and generic companies.

The company has followed a three-pronged strategy for API development

(already generic, to be generic and future generic) to generate revenues in

the short-term, as well as build a pipeline from a long-term perspective. It

identifies products by a combination of client requirements and niche

molecules where the company has a technological edge, backed by its

expertise in advanced chemistry and backward integration.

The company has a small but strong product pipeline. Currently, Hikal has

around eight to nine products in the generic portfolio. The company

normally targets | 50 crore+ opportunity for each product. For this, Hikal

typically identifies products that have clocked billion dollar sales at their

peak with high volume.

Leveraging on strong cost efficiency, manufacturing capability and

chemistry background, the company is able to generate sizeable revenues

even from commoditised generic products. Its flagship Gabapentin (CNS) is

a clear example of the company’s ability to garner higher market share in a

product despite steep competition (more than 25 DMF filings). Gabapentin

contributes ~40% to the company’s pharma revenues and 15-16% of overall

revenues. Hikal is the largest supplier for Gabapentin globally. The company

569.1610.7

752.8

937.6

0

200

400

600

800

1000

FY16 FY17 FY18 FY19E

Pharma

Pharma bifurcation

Source: ICICI Direct Research, Company

During FY16-19E, growth was driven by 1) timely

addition of capacity, 2) new launches, 3) improved

market share in existing products, 4) windfall on

account of API supply constraints from China and 5)

a favourable currency

The company has followed a three-pronged strategy

for API development (already generic, to be generic

and future generic)

Currently, the company has around eight to nine

products in the generic portfolio

Gabapentin contributes ~40% to the company’s

pharma revenues and 15-16% of overall revenues

APIs

~50%

CDMO

~50%

CAGR 18.1%

ICICI Securities | Retail Research 6

ICICI Direct Research Initiating Coverage | Hikal Ltd.

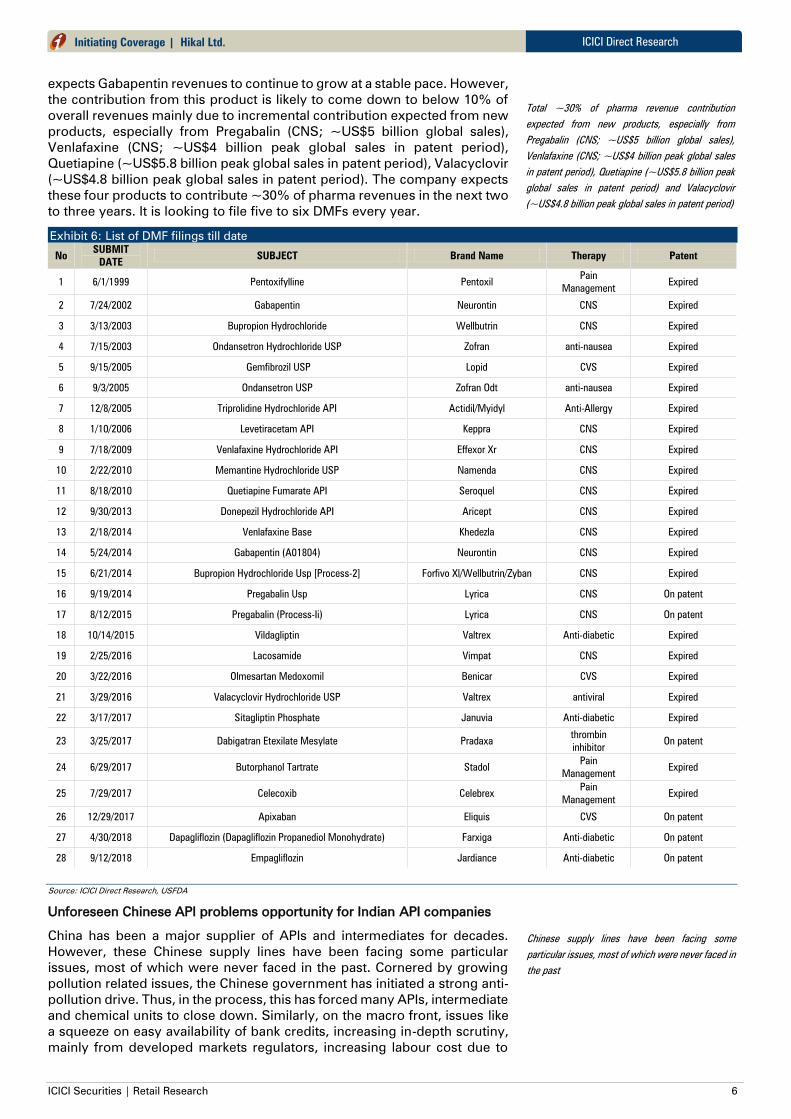

expects Gabapentin revenues to continue to grow at a stable pace. However,

the contribution from this product is likely to come down to below 10% of

overall revenues mainly due to incremental contribution expected from new

products, especially from Pregabalin (CNS; ~US$5 billion global sales),

Venlafaxine (CNS; ~US$4 billion peak global sales in patent period),

Quetiapine (~US$5.8 billion peak global sales in patent period), Valacyclovir

(~US$4.8 billion peak global sales in patent period). The company expects

these four products to contribute ~30% of pharma revenues in the next two

to three years. It is looking to file five to six DMFs every year.

Exhibit 6: List of DMF filings till date

No SUBMIT

DATE SUBJECT Brand Name Therapy Patent

1 6/1/1999 Pentoxifylline Pentoxil Pain

Management Expired

2 7/24/2002 Gabapentin Neurontin CNS Expired

3 3/13/2003 Bupropion Hydrochloride Wellbutrin CNS Expired

4 7/15/2003 Ondansetron Hydrochloride USP Zofran anti-nausea Expired

5 9/15/2005 Gemfibrozil USP Lopid CVS Expired

6 9/3/2005 Ondansetron USP Zofran Odt anti-nausea Expired

7 12/8/2005 Triprolidine Hydrochloride API Actidil/Myidyl Anti-Allergy Expired

8 1/10/2006 Levetiracetam API Keppra CNS Expired

9 7/18/2009 Venlafaxine Hydrochloride API Effexor Xr CNS Expired

10 2/22/2010 Memantine Hydrochloride USP Namenda CNS Expired

11 8/18/2010 Quetiapine Fumarate API Seroquel CNS Expired

12 9/30/2013 Donepezil Hydrochloride API Aricept CNS Expired

13 2/18/2014 Venlafaxine Base Khedezla CNS Expired

14 5/24/2014 Gabapentin (A01804) Neurontin CNS Expired

15 6/21/2014 Bupropion Hydrochloride Usp [Process-2] Forfivo Xl/Wellbutrin/Zyban CNS Expired

16 9/19/2014 Pregabalin Usp Lyrica CNS On patent

17 8/12/2015 Pregabalin (Process-Ii) Lyrica CNS On patent

18 10/14/2015 Vildagliptin Valtrex Anti-diabetic Expired

19 2/25/2016 Lacosamide Vimpat CNS Expired

20 3/22/2016 Olmesartan Medoxomil Benicar CVS Expired

21 3/29/2016 Valacyclovir Hydrochloride USP Valtrex antiviral Expired

22 3/17/2017 Sitagliptin Phosphate Januvia Anti-diabetic Expired

23 3/25/2017 Dabigatran Etexilate Mesylate Pradaxa thrombin

inhibitor On patent

24 6/29/2017 Butorphanol Tartrate Stadol Pain

Management Expired

25 7/29/2017 Celecoxib Celebrex Pain

Management Expired

26 12/29/2017 Apixaban Eliquis CVS On patent

27 4/30/2018 Dapagliflozin (Dapagliflozin Propanediol Monohydrate) Farxiga Anti-diabetic On patent

28 9/12/2018 Empagliflozin Jardiance Anti-diabetic On patent

Source: ICICI Direct Research, USFDA

Unforeseen Chinese API problems opportunity for Indian API companies

China has been a major supplier of APIs and intermediates for decades.

However, these Chinese supply lines have been facing some particular

issues, most of which were never faced in the past. Cornered by growing

pollution related issues, the Chinese government has initiated a strong anti-

pollution drive. Thus, in the process, this has forced many APIs, intermediate

and chemical units to close down. Similarly, on the macro front, issues like

a squeeze on easy availability of bank credits, increasing in-depth scrutiny,

mainly from developed markets regulators, increasing labour cost due to

Total ~30% of pharma revenue contribution

expected from new products, especially from

Pregabalin (CNS; ~US$5 billion global sales),

Venlafaxine (CNS; ~US$4 billion peak global sales

in patent period), Quetiapine (~US$5.8 billion peak

global sales in patent period) and Valacyclovir

(~US$4.8 billion peak global sales in patent period)

Chinese supply lines have been facing some

particular issues, most of which were never faced in

the past

ICICI Securities | Retail Research 7

ICICI Direct Research

Initiating Coverage | Hikal Ltd.

higher standard of living and last, but not the least, the US-China trade war

have impacted API exports to the US. Although Chinese goods have not

been altogether out of the game, the void has provided other global players,

especially Hikal and other Indian API manufacturers, an opportunity to fill the

gap, to a greater extent.

Some of China’s loss can be India’s gains…

The once unparalleled Chinese bulk manufacturing capability and capability

in APIs is facing headwinds for the first time. Even though most of the lost

ground is likely to be restored, the remaining vacuum still presents a good

opportunity for Indian players to step in. What can be termed as a new

opportunity for Indian players is the strategic shift of global players from

single sourcing to multiple sourcing of APIs and intermediates to counter

the uncertainties in future. India can be a perfect strategic fit due to dual

sourcing for global customers, mainly on legacy adherence to stringent

compliance (1298 UAFDA approved API units) and zero-discharge

compliance adopted by most players at the behest of state governments

besides technical capability and local sourcing.

Another advantage for sourcing APIs from India can be its legacy proficiency

in formulations (where China lags), thus providing an end-to-end solution

for customers. The Indian formulations market is the third largest in terms

of volume and thirteenth largest in terms of value globally. The Indian

pharma industry supplies 40% of generic demand in the US and 25% of all

medicine in the UK. Companies like Hikal are poised to benefit in this sort of

a scenario as they can be potential suppliers to global and Indian players.

Exhibit 7: Potential incremental opportunity for Indian players (10% assumption)

Source: ICICI Direct Research, Industry

CDMO

Hikal approaches innovator companies targeting their late stage

commercialised products, which are likely to face steep competition post

patent expiry in the near term, for value proposition. Similarly, the company

also offers early-stage R&D services such as synthesis, scale-up, API

development, stability studies and method development all the way through

manufacturing services, ranging from preclinical R&D material for clinical

trial purposes and commercial production, Phases I through III. For this

business, the company has a dedicated business development team for the

US, Europe and Japan to identify large and virtual companies for CDMO of

intermediates and APIs that are in different stages of development.

Currently, the company is working on five to six products in CDMO segment.

Following are some key contracts the company is pursuing currently

US innovator client: Hikal is the contract manufacturer of two large volume

molecules, a neuropathic pain reliever and an anti-cholesterol molecule

exclusively for a leading US-based innovator company. These products

have stringent technical specification requirements. As per the

management, both these products are for life-cycle extension. The volumes

of both these molecules increased this year. The trend is expected to

continue next year as well.

What can be termed as a new opportunity for Indian

players is the strategic shift of global players from

single sourcing to multiple sourcing of APIs and

intermediates to counter the uncertainties in the

future

The company has a dedicated business

development team for the US, Europe and Japan to

identify large and virtual companies for CDMO of

intermediates and APIs that are in different stages of

development

India ,

US$3 bn

RoW,

US$3 bn

China,

US$30 bn

ICICI Securities | Retail Research 8

ICICI Direct Research Initiating Coverage | Hikal Ltd.

European innovator client: Hikal has an exclusive long-term contract

manufacturing agreement with a leading European innovator for two

molecules. Based on the forecast provided by the client, these products are

expected to grow further in the next year as well. One of these molecules is

an anti-epilepsy drug that is widely used to control seizures while the other

is a drug used for memory enhancement.

Business in Japan: The company is working on several products that have

come through R&D and progressed to the semi-commercial stage. In FY20,

the company expects a repeat order of two intermediates going into a new

generation API to be launched in Japan.

Intermediate contracts – Hikal has supplied an intermediate to a US-based

biotechnology company, which, in turn will supply the same as food additive

for a global FMCG conglomerate. The company expects a repeat order of

higher quantity from this product. Hikal delivered another intermediate to a

leading US company for one of its APls under development. Apart from this,

the company expects a repeat order of two intermediates going into a new

generation API to be launched in Japan. Business for the supply of an

intermediate going into high-value Prostaglandin API is also expected. It will

supply an intermediate going into Phase 1 of the oncology product used for

treatment of breast cancer and investigated for different types of cancer

developed by a biotech company. The company has also entered into a

contract with a US-based company for process development services for a

food ingredient.

Animal health business - In the animal health business (20-25% of CDMO

revenues), the company manufactures a non-antibiotic veterinary drug API

that is used to prevent coccidiosis, a disease that threatens newly arrived

cattle that often have a compromised immune system. This is under an

exclusive manufacturing contract with a leading US-based veterinary drug

innovator. Hikal has also developed two APls in this segment. One of them

has a dual application and is also used as a human health product.

Additionally, the company has filed a USDMF in FY18 and plans to file

another DMF in the near term.

We expect the pharma segment to grow at 15.5% CAGR in FY19-21E on the

back of new offerings and repeat business from CDMO players. Continuance

of China induced opportunities will also be a major factor.

Exhibit 8: Pharma growth likely to remain strong

Source: ICICI Direct Research, Company

569.1610.7

752.8

937.6

1087.1

1250.2

0

200

400

600

800

1000

1200

1400

FY16 FY17 FY18 FY19E FY20E FY21E

Pharma

18.1% CAGR

15.5% CAGR

ICICI Securities | Retail Research 9

ICICI Direct Research Initiating Coverage | Hikal Ltd.

Crop protection growth to piggyback on client relationship and capabilities-

In crop protection, partnering with global innovators has been the hallmark

for Hikal since inception. It all began in 1991 when the company signed a

long term supply agreement with Hoechst India from the then newly

established Mahad (Maharashtra) facility. Again in 1997, as a part of

backward integration policy, the company commissioned a manufacturing

facility at Taloja (Maharashtra) in technical collaboration with Merck & Co.

Inc. US. Since then, Hikal has been involved with innovators on a fairly

regular basis.

During FY16-19E, the crop protection business grew ~20% YoY due to 1)

successful commercialisation of new products, 2) diversification into

specialty chemicals and specialty biocides, 3) windfall on account of Chinese

supply constraints of key crop protection ingredients, 4) additional product

offerings to existing customers and 5) favourable currency.

Exhibit 9: Strong growth through FY16-19E

Source: ICICI Direct Research, Company

Hikal partners with crop protection companies for CDMO of intermediates

and active ingredients. The company has a successful track record of

developing crop protection products from gram to kilo to tonne scale as per

requirement. It manufactures insecticides, fungicides and herbicides for

customers with a major chunk from Insecticides. Hikal also has its own

portfolio of products for the specialty chemical and biocide industry. CDMO

contributes ~70% with the balance contributed by specialty chemicals and

biocides besides Hikal’s proprietary products. It is currently working for 20-

25 clients including top five out of seven in global crop protection business.

As per the management, competition in this segment is lower than pharma

mainly due to fewer players and consolidation among large players. In crop

protection, the company has around 10 to 11 products in the CDMO

business and about five to six own products. No single product in the CDMO

business constitutes more than 15% of the business.

Strategically, the company has also diversified into specialty chemicals

which includes specialty biocides, antimicrobial actives and additives that

contribute ~20% of total crop protection sales. These products are used in

industries like leather, paint, paper, water treatment, personal care, building

materials and textile industry. The company is expecting good demand for

specialty biocides, especially in the domestic market on account of

shortages from China.

The company focuses on a broad spectrum of products in the fungicides,

insecticide and herbicides space. Following are a few instances wherein the

company has engaged with global innovators

Key herbicides products

On–patent herbicide intermediate for global innovator – In FY18, the

company commissioned a new plant in Mahad to manufacture an exclusive

356.5

423.3

547.3

610.3

0

100

200

300

400

500

600

700

FY16 FY17 FY18 FY19E

(|

crore)

Crop Protection

Crop protection bifurcation

ICICI Direct Research, Company

During FY16-19E, the crop protection business grew

~20% YoY due to 1) successful commercialisation

of new products, 2) diversification into specialty

chemicals and specialty biocides, 3) windfall on

account of Chinese supply constraints of key crop

protection ingredients, 4) additional product

offerings to existing customers and 5) favourable

currency

Hikal is currently working for 20-25 clients including

top five out of seven in global crop protection

business

No single product in the CDMO constitutes more

than 15% of the business

Specialty products are used in industries like leather,

paint, paper, water treatment, personal care,

building materials and textile industry

CDMO

~70%

Proprietary

& Others

~30%

CAGR 19.6%

ICICI Securities | Retail Research 10

ICICI Direct Research

Initiating Coverage | Hikal Ltd.

and high volume product for one of its global innovator customers. Based

on the company’s on-time delivery, quality and successful scale up, the

client has awarded an exclusive supply contract to make the precursor of

this product to the company.

Two on-patent herbicide products for Japanese innovator –These products

are used predominantly for controlling broad-leaved weeds in water-seeded

rice and for seed treatment in cotton crop. The volume of one of these

products grew strongly in FY18 due to successful commercialisation and

scale-up and the company expects to achieve similar growth in FY19.

Key fungicide products

On-patent fungicide product for global innovator— This product is used to

prevent late blight and downy mildew on vine, potato, fruit and vegetables.

The product has shown a significant increase in volumes in FY18 mainly due

to increased demand from the global Innovator for whom the company

manufactures this product exclusively. The increase in demand was due to

the de-stocking of inventories and multiple new registrations across various

geographies along with introduction of a new combination of products.

Versatile fungicide for leading Japanese innovator -- This fungicide has

preventative, systemic and curative properties for soil-borne and other

diseases in almonds, peaches, plums, apricots, other fruits and vegetables,

golf courses, professional sports fields and lawns. Sales of this product was

impacted in FY18 due to unavailability of key raw materials due to a volatile

supply chain situation involving Chinese suppliers. However, with the

improved and positive change in raw material availability, the company

expects to grow volumes significantly in FY19 and make good both last

year’s pending orders as well as fresh orders.

Niche fungicide for Japanese innovator -- This special product is a selective

new compound with new modes of action for protection from fungal

diseases, especially in rice crops. In FY18, due to capacity constraint, Hikal

could not fulfil customer demand. However, the company has

debottlenecked plants and will supply the backlogged quantities apart from

additional requirements in FY19.

Exclusive fungicide product for European innovator – This product is used

to control Oomycete disease, for late blight control in potatoes, tomatoes

and for downy mildew in vegetables. It witnessed a substantial increase in

volume last year. The company exclusively manufactures this product under

contract for a leading European innovator. Based on the projections given

by the innovator, the company is expecting strong volume growth in FY19.

Thiabendazole– This product accounts for less than 15% of the crop

protection sales and is one of the company’s legacy crop protection

products. The product is versatile and used in both crop protection to

control mould and other fungal diseases in fruits and vegetables, as well as

an anti-parasitic to control roundworms. It is also used in the material

protection industry to prevent fungal growth.

Key insecticide products

Low volume margin accretive insecticide product for Japanese innovator --

This product increases colouration of fruits as well as enhances fruit quality

by increasing the citric acid content. In FY16, the company had

commercialised the product for a leading Japanese innovator company.

Since the client was in the process of developing the market for this

innovative product, the company could not achieve scalability in the last two

ICICI Securities | Retail Research 11

ICICI Direct Research Initiating Coverage | Hikal Ltd.

years. However, the company expects revenue from this product from FY19

onwards.

New insecticide for European customer – This product is used to control a

wide range of insects on rape, maize, fruits & vegetables along with pome

fruit and also as a wood preservative to control termites, wood boring

beetles and other insects. The volume of this product is likely to increase

substantially in FY19 due to the ban on some of the products of competitors

in the European Union.

Biocides, specialty chemicals businesses - To diversify into new and allied

business areas, the company has entered the specialty biocides and

specialty chemicals businesses. Contribution from these products has gone

up to~20% from a low single digit in past three years. These products are

used in industries like leather, paint, paper, water treatment, personal care,

building materials and textile industry.

New product development

Hikal owns a research and technology (R&T) centre in Pune for crop

protection, biocides and specialty chemicals products. The company has

several new products in the pipeline, both for customers in contract

manufacturing and own development. Hikal is developing a versatile

product that is used as a microbiocides as well as a fungicide. It has a wide

range of applications as a preservative in varnishes, adhesives, inks, laundry

detergents, stain removers, fabric softeners, leather processing solutions,

fluid preservation and in emulsion paints. The company expects to scale up

and further commercialise these products in the near future.

The company is also working on developing a commercially viable process

for a complex crop protection product, which has recently gone off-patent.

This product is used to control a wide range of diseases by pests on

soybean, cereals, fruits and vegetables. One more key product in the

pipeline is used to control a wide range of pests on cereals, rape and

soybean. Both these products involve complex chemistry and technology.

Hikal is expecting to complete the complex process development by FY19.

On the specialty chemicals front, it is working on the development of two

products with wide usage in the chemical industry. These products have a

wide range of applications including that of an antiseptic disinfectant. Hikal

expects to commercialise both these products in the near future.

Stagnant global crop protection market scenario conducive for CDMO

evolution

Overall global growth has been stagnant over the past few years due to 1)

patent expiry of some ley molecules, 2) climatic and crop pattern changes

in different parts of the world, 3) broadly muted food grain prices affecting

farmers’ income and 4) higher use of genetically modified crops with better

insects and herbs resistance. The overall market has grown at a CAGR of

just 1% in CY12-18. The market is well diversified (Asia Pacific- 30%, Latin

America- 24%, Europe- 22% and North America 20%), which suggests that

in any particular year, besides patent expiry, any headwinds in a particular

geography would slow down overall growth.

The company is developing a versatile product that

is used as a microbiocides as well as a fungicide

The company is also working on developing a

commercially viable process for a complex crop

protection product which has recently gone off-

patent.

The global crop protection market has grown at a

CAGR of just 1% during CY12-18

ICICI Securities | Retail Research 12

ICICI Direct Research Initiating Coverage | Hikal Ltd.

Exhibit 10: Global crop protection market value (US$ million)

Sales (US$ million) Crop Protection Non-Crop Total Crop

Protection

2012 52,617 6,520 59,137

2013 54,075 6,512 60,587

2014 58,746 6,515 65,261

2015 56,160 6,882 63,042

2016 52,882 7,106 59,988

2017 54,219 7,311 61,530

2018 (P) 56,500 7,538 64,038

Source: ICICI Direct Research, ICRA

Some challenges faced by global crop protection industry

Demand for crop protection is mainly driven by a desire to enhance crop

yield, increase plant growth and protect crops against pests and other

harmful aspects. Globally, farmers use various kind of crop protection

including herbicides, insecticides, fungicides, and seed treatment chemicals

to optimise their agricultural output. Besides this, the global consumption of

crop protection is also growing as arable land is shrinking due to rapid

industrialisation and population expansion. That said, the crop protection

market has its own set of challenges. They are discussed in brief below-

Regulations

Globally, the crop protection market is governed by many national and

international laws, which are increasing the cost of developing new

products. Since manufacturers have to consider numerous regulations,

there is a delay in the introduction of new products in the market. A case in

point is Herbicide Glyphosate, which faced stiff regulatory challenges in

Europe and Brazil. Additionally, different countries will have varying product

filling requirements. As a result, global players need to submit technical

grade registrations with the full dossier. Such processes further increase the

complexities for overseas suppliers that have to conduct additional tests and

studies to obtain approval for selling the crop protection within the region.

Europe in particular is highly regulated.

High R&D costs

Developing a typical crop protection molecule takes nine years on an

average with average spending of US$180 million. During the same time,

the market may witness newer innovations or competitors may come up

with better chemicals. As a result, manufacturers in the crop protection

industry are struggling to cope with such high R&D costs.

Growing usage of GM crops

Progress in genetic science has enabled genetically modified crops (GM

crops) to develop resistance to pests. As a result, such GM crops do not

need crop protection and pesticides for them to grow. Pest-resistant GM-

maize crops are widely used in the US and are further used in industrial-

scale biofuel. The development and growth of such crops can pose a threat

to the growth of the global crop protection market as they would not be

required to be applied to GM crops.

Upheaval on account of consolidation in global crop protection space- Over

the past few years, a number of global crop protection conglomerates have

acquired or merged their business operations to counter fluctuations in

currencies, crop prices and crude oil prices that had adversely affected the

sales and profit margins. The trend was initiated ~by the US$130 billion

merger announcement between Dow Chemicals & Du-Pont, followed by

~US$44 billion acquisition of Syngenta by ChemChina. The last in the

pipeline was acquisition of Monsanto by Bayer AG for ~US$63 billion. These

merged entities together account for 75-80% of market share. The trigger

Different countries will have varying product filling

requirements

Crop protection molecule takes nine years on an

average with average spending of US$180 million

The development and growth of GM crops can pose

a threat to the growth of the global crop protection

market

Merged entities together account for 75-80% of

market share

They have expanded their scope from being a

standalone crop protection or seed provider to a

much broader solution provider for global farming

ICICI Securities | Retail Research 13

ICICI Direct Research

Initiating Coverage | Hikal Ltd.

for these companies to merge their business operations was to boost

margins, lower cost & development time, streamline workflows and increase

the efficiency of the R&D process. Similarly, they have expanded their scope

from being a standalone crop protection or seed provider to a much broader

solution providers for global farming.

Other global developments- China issues and Japanese potential

China impact

Chinese policies have become increasingly stringent in the last few months.

A case in point is the 2017 release of new regulations on pesticides

administration. These new regulations have made major adjustments in

pesticide production, registration, operation, application and penalties.

These regulations provide a solid legal basis for safeguarding the quality and

safety of China's agricultural products and promoting the development of

resource-saving and environment-friendly modern agriculture.

This is likely to have significant impact on the production and export of

technical materials. This may expand to formulation products and even

pesticide application in coming years. The Chinese government has

circulated a series of policies, such as the Soil Pollution Control Action Plan,

Water Pollution Control Action Plan and Gas Pollution Control Action Plan.

The new environmental protection standards are likely to substantially

increase the cost for companies in the future. The environmental protection

policies are a way for the government to eliminate backward production

capacity and non-compliant enterprises. This suggests that the crackdown

is mainly on intermediates & APIs along with other chemicals.

Many customers on the innovator side had moved to China in a big way. A

lot of them have been having major supply issues with China. Hence, they

are looking at Indian companies as alternative source on a permanent basis.

Japanese potential- Tough market to crack but opening up…

Japanese companies boast strong R&D strengths, with 40% of the world’s

patented crop protection products coming from Japanese enterprises.

Japan has nearly 20 new agro-chemical products that are poised for

registration before entering the international market. These macros suggest

that Japan remains a potentially significant market for sustained growth.

However, post recent tsunamis, Japanese companies are looking at

outsourcing capabilities outside Japan to de-risk themselves. As in pharma,

Japanese companies are very strict about confidentiality and intellectual

property protection in crop protection. Some of them have seen an

opportunity in India and are now creating a base here. Secondly, Hikal

already has an engagement with Japanese players for five to six products.

Normalised growth still significant

Being an export driven company, Hikal’s fortunes are directly dependent on

structural changes at the global level especially over the last three years,

besides legacy industry dynamics. With the global crop protection industry

growth being stuck in low single digits (CAGR of just 1% in CY12-18), Hikal

has maintained its mid-teen growth tempo, especially since FY16. This

suggests an increasing trend of outsourcing in the backdrop of falling

revenues and squeezing margins for top tier global players after the patent

expiry of major products in the last few years. By 2020, some more brands

worth US$3 billion are scheduled to go off-patent. This has led to massive

consolidation in the global landscape with added focus on cost control

measures. This, along with issues in China, have led to incremental ex-China

outsourcing, which is reflected in the performances of most crop protection

B2B players including Hikal. While replicating the FY16-19E growth looks

unlikely, we believe the expansion of base business along with new

launches on the back of new clients’ addition and capacity augmentation will

drive growth henceforth. We expect the crop protection segment to grow at

12.5% CAGR in FY19-21E.

New regulations have made major adjustments in

pesticide production, registration, operation,

application and penalties

The new environmental protection standards are

likely to substantially increase the cost for Chinese

companies in future

Post the recent tsunamis, Japanese companies are

looking to outsource capabilities outside Japan to

de-risk themselves

We expect crop protection segment to grow at a

CAGR of 12.5% in FY19-21E on the back of new

clients’ addition and capacity augmentation

ICICI Securities | Retail Research 14

ICICI Direct Research

Initiating Coverage | Hikal Ltd.

Exhibit 11: Crop protection business expected to grow at 12.5% over FY19-21E

Source: ICICI Direct Research, Company

356.5

423.3

547.3

610.3

672.2

773.0

0

1000

FY16 FY17 FY18 FY19E FY20E FY21E

(|

crore)

Crop Protection

CAGR 12.5%

CAGR 19.6%

ICICI Securities | Retail Research 15

ICICI Direct Research

Initiating Coverage | Hikal Ltd.

Financial highlights

Revenues expected to grow at CAGR of 15% over FY19-21E

The 9MY19 revenues grew 24.5% YoY to | 1132 crore on the back of robust

performance across segments. Volume growth was 13-15% while the

remaining growth was attributable to favourable currency movement and

higher realisation. This, in turn, was possible due to passing on of

incremental raw material cost to customers. Raw material prices increased

mainly due to raw material supply constraints from China.

Segment wise, the pharma segment grew 26.4% YoY to | 680 crore owing

to 1) direct advantage of APIs supply constraint from China, 2) volume

growth in existing products and 3) new launches. Crop protection has also

grown 21.7% YoY to | 452 crore due to 1) commercialisation of new

products 2) strong volume growth from existing products led by

geographical expansion and market share gain and 3) higher contribution

from specialty biocides and specialty chemicals segments. The company

also entered into a partnership with new players, which has started

contributing to growth. Looking at the company’s strong product pipeline,

capacity expansion, timely execution and order positions, we expect growth

momentum to continue, going ahead. Currently, 15-20% of reported sales

are via new products both in pharma and crop protection. The management

expects this percentage to go up to 25% per year, going forward. We expect

revenues to grow at a CAGR of 15.1% YoY to | 2051 crore.

Exhibit 12: Revenues expected to grow at 15.1% CAGR over FY19-21E

Source: ICICI Direct Research, Company

Exhibit 13: Pharma to grow at 15.5% over FY19-21E

Source: ICICI Direct Research, Company

Exhibit 14: Crop protection to grow at 12.5% (FY19-21E)

Source: ICICI Direct Research, Company

925.71013.9

1296.1

1547.7

1783.6

2051.2

0

500

1000

1500

2000

2500

FY16 FY17 FY18 FY19E FY20E FY21E

(|

crore)

Revenues

CAGR 15.1%

569.1610.7

752.8

937.6

1087.1

1250.2

0

200

400

600

800

1000

1200

1400

FY16 FY17 FY18 FY19E FY20E FY21E

Pharma

356.5

423.3

547.3

610.3

672.2

773.0

0

100

200

300

400

500

600

700

800

900

FY16 FY17 FY18 FY19E FY20E FY21E

Crop Protection

Currently, around 15-20% of reported sales are via

new products both in pharma and crop protection.

This is expected to go to 25%

The company also entered into a partnership with

new players, which has started contributing to

growth

CAGR 18.7%

ICICI Securities | Retail Research 16

ICICI Direct Research

Initiating Coverage | Hikal Ltd.

EBITDA margins expected to improve 100 bps to 20.0% by FY21E

While revenue growth was solid, hindrances arising from availability of

certain key raw materials and advanced intermediates from China remain an

issue, (albeit on a lower scale). This has materially impacted gross margins.

However, the company has managed to pass on a majority of the price

increases to customers and make up the remaining with process

improvements and manufacturing efficiencies.

In a way, for ~60% of the overall business (pharma CDMO + crop protection

CDMO), the company manages to pass on 100% of fluctuation in raw

material prices. To mitigate the risk for the remaining 40% pie, the company

is planning to source from local vendors and making raw materials in-house

through backward integration. With all these measures, coupled with

stabilising raw material supplies from China, we expect gross margins to go

up to the historical level of ~50% from FY20. We also expect EBITDA

margins to improve 100

bps over FY19-21E to 20.0%.

Exhibit 15: EBITDA and EBITDA margins trend

Source: ICICI Direct Research, Company

Improvement in operational margins to drive net profit

Net profit growth is likely to be driven by an improvement in operating

margin performance and better operational leverage. We expect net profit

to grow 30.0% in FY19-21E to | 164.4 crore.

Exhibit 16: Net profit trend

Source: ICICI Direct Research, Company

Return ratios to improve on the back of better asset turnover

Return ratios remained muted in FY14-18 in line with a decline in margins,

which were impacted due to a spike in raw material prices. However, on the

back of a persistent improvement in gross margins coupled with an

improvement in assets turnover, we expect improvement in return ratios.

180.8194.3

241.7

293.7

345.0

409.7

19.5

19.2

18.6

19.0

19.3

20.0

17.5

18.0

18.5

19.0

19.5

20.0

20.5

0

50

100

150

200

250

300

350

400

450

FY16 FY17 FY18 FY19E FY20E FY21E

(|

crore)

EBITDA EBITDA Margins (%)

41.2

67.7

77.2

97.3

127.4

164.4

0

20

40

60

80

100

120

140

160

180

FY16 FY17 FY18 FY19E FY20E FY21E

(|

crore)

Net Profit

The company manages to pass on 60% of the price

increase in raw materials to customers due to CDMO

factor

CAGR 30.0%

CAGR 33.2%

ICICI Securities | Retail Research 17

ICICI Direct Research

Initiating Coverage | Hikal Ltd.

Future capex mainly for brownfield expansion and debottlenecking

The company has substantial additional space in its existing facilities. To

cater to the strong volume growth, the company is spending | 250 crore in

the next 18 months to 24 months in brownfield expansion and

debottlenecking in current capacities. All the future capex is revenue

generating. This incremental capacity has the capability to generate 1.5-1.7x

asset turnover.

Exhibit 17: RoE and RoCE trend

Source: ICICI Direct Research, Company

Exhibit 18: Free cash flow

Source: ICICI Direct Research, Company

10.7 10.6

12.2

14.0

15.3

17.3

7.3

11.2

11.5

13.0

15.0 16.8

0

2

4

6

8

10

12

14

16

18

20

FY16 FY17 FY18 FY19E FY20E FY21E

(%

)

RoCE (%) RoE (%)

103.2

53.6

126.8

58.2

32.8

6.5

49.6

87.1

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Free Cash flow

ICICI Securities | Retail Research 18

ICICI Direct Research Initiating Coverage | Hikal Ltd.

Experience in high profile clients servicing to the fore…

For years, the company has been dealing with high profile MNCs like Merck

& Co, Bayer, Syngenta, BASF, Pfizer to name a few. With proven capabilities

and management pedigree, we believe Hikal offers a compelling value

proposition as it continues to expand in both the pharma and crop

protection segments with separate focus and a calibrated approach. This

bodes well in the current scenario when Chinese supply disturbances are

likely to create opportunities for Indian players both in APIs as well as crop

protection CDMO. The company has spent ~| 500 crore over the last five

years to augment capacity. After years of volatility in growth, Hikal is

witnessing a relatively stable growth trajectory.

The management has guided for 15-20% growth on the back of volume gain

in existing products, new launches, new client addition and geographical

expansion. Continuance of China induced opportunities will also be a major

factor. This guidance is also supported by the company’s annual capex

guidance of | 150-200 crore, which is double the historical average. The

pharma segment is expected to grow at a CAGR of ~16% in FY19-21E on

the back of new offerings and repeat business from CDMO players. Crop

protection is expected to grow at 12.5% CAGR in FY19-21E on the back of

expansion of base business along with new launches on the back of new

client’s addition and capacity addition.

We expect sales, EBITDA, PAT to grow at a CAGR of 15%, 18%, 30%

respectively, in FY19-21E on the back of new launches and better operating

leverage. Similarly, we also expect 330 bps RoCE improvement to 17.3%

through FY21. We arrive at a valuation of | 200 based on FY21E EPS of

| 13.3.

Exhibit 19: Peer comparison

M cap

(| cr)

RoE RoCE

FY19E FY20E FY19E FY20E FY19E FY20E FY19E FY20E FY19E FY20E FY19E FY20E FY19E FY19E

Divi's Lab 42614 4928.8 5511.1 38.2 38.5 1421.4 1607.2 8.6 7.7 21.3 18.9 30.0 26.5 20.2 26.4

Neuland 659 659.2 788.6 8.9 14.0 16.5 51.5 1.0 0.8 26.7 14.3 39.9 12.8 2.7 3.0

Suven 3125 631.3 715.0 28.8 31.6 118.4 148.1 4.9 4.4 15.7 12.7 26.4 21.1 14.5 13.3

Dishman 3046 1889.0 2071.9 27.7 28.9 198.0 256.2 1.6 1.5 7.3 6.4 15.4 11.9 4.0 4.1

PI 13303 2819.2 3333.0 20.7 21.6 415.1 512.3 4.7 4.0 22.3 18.1 32.1 26.0 19.6 24.7

Hikal 2044 1548.1 1783.7 19.0 19.3 97.3 127.4 1.3 1.1 9.0 7.7 21.0 16.0 13.0 14.0

Lonza (CHF m) 22289 6059.4 5949.3 25.7 27.1 917.7 974.1 3.7 3.7 16.7 16.1 24.3 22.9 11.7 NA

Siegfried (CHF m) 1558 843.4 892.7 17.6 18.7 74.1 89.0 1.8 1.7 10.9 9.7 21.0 17.5 8.5 6.0

EV/EBITDA P/ERevenuesEBITDA

margins (%)

PAT P/S

Source: ICICI Direct Research, Bloomberg, Industry

Chinese supply disturbances are likely to create

opportunities for Indian players both in APIs and crop

protection CDMO

The management has guided for 15-20% growth on

the back of volume gain in existing products, new

launches, new client addition and geographical

expansion

ICICI Securities | Retail Research 19

ICICI Direct Research

Initiating Coverage | Hikal Ltd.

Exhibit 20: One year forward PE

Source: ICICI Direct Research, Bloomberg

Exhibit 21: One year forward PE of company vs. Nifty Pharma Index

Source: ICICI Direct Research, Bloomberg

Risk & Concerns

1. Estimation risk- peculiar phenomenon for B2B players

Verifying the revenue stream from third party and independent

sources is always a difficult task to estimate revenues of B2B players

compared to B2C players. On account of client confidentiality, most

of these players are reluctant to divulge important details. Similarly,

there can be significant quarterly gyrations (or even yearly) in the

performances due to the contractual nature of the revenue stream.

Hence, the only reliable source is the broader management

guidance.

2. Regulatory risk – 85% of pharma revenues come from developed

markets

In the current scenario, the major risk for the pharmaceutical

industry is regulatory risk, especially for a company that has high

dependency on regulatory market revenues. Total ~85% of Hikal’s

pharma revenues are generated from developed markets (US –55%,

Europe –30%). Although the company has a strong compliance track

record vis-à-vis regulatory authorities from the US, Europe and

Japan, any scaling up of future operations entails high risk.

In the crop protection business, the company operates in a highly

regulated markets where it faces extensive regulations and stringent

registration conditions. Penalties for non-compliance with these

regulations can vary from revocation or suspension of the

registration to imposition of fines or confiscation of such jurisdiction.

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0M

ar-16

Sep-16

Mar-17

Sep-17

Mar-18

Sep-18

Mar-19

|

Price 33.7x 13.5x 25.1x 19.3x 16.4x

0.00

9.00

18.00

27.00

36.00

45.00

Mar-16

Sep-16

Mar-17

Sep-17

Mar-18

Sep-18

Mar-19

(x)

Hikal CNX Pharma

17% Discount

ICICI Securities | Retail Research 20

ICICI Direct Research

Initiating Coverage | Hikal Ltd.

3. Product concentration risk – Hikal derives ~40% of pharma

revenues from Gabapentin and less than 15% of crop protection

revenues from Thiabendazole. Although the company expects the

dependency of single product to come down to less than 10% of

total revenues in the next two to three years, any adverse impact on

any of these products in the near term could impact future growth

4. Risk of raw material supply – FY18 gross margins declined 369 bps

to 46.1% mainly due to a sudden shoot up in raw material prices

leading to supply constraint from China. The company procures 30-

35% of raw materials from China. However, indirectly also most of

the raw material supply and prices were impacted by China issues.

Hikal is looking at backward integration and alternative sources to

mitigate this risk. The company also has the ability to pass on a

majority of the increase in raw material prices to the end user albeit

with lags. However, we are not denying such raw material volatility

in future, which may impact Hikal’s profitability.

5. Seasonality risk – The crop protection business is heavily dependent

on the agricultural industry, which, in turn, is subject to soil and

climatic conditions, rainfall, seasonal and other weather factors. This

renders the performance of the agricultural sector, as a whole, or the

levels of production of a particular crop relatively unpredictable.

Further, global warming and other changes to the weather pattern

are being witnessed globally. This may make it difficult for the

company to rely on weather forecasts and growth opportunities. The

weather can affect the presence of diseases and pest infestations in

the short-term on a regional basis. Accordingly, it may negatively

affect the demand. Further, on account of seasonality of the

agricultural industry, the company’s operating results may fluctuate

from quarter to quarter.

ICICI Securities | Retail Research 21

ICICI Direct Research

Initiating Coverage | Hikal Ltd.

Financials

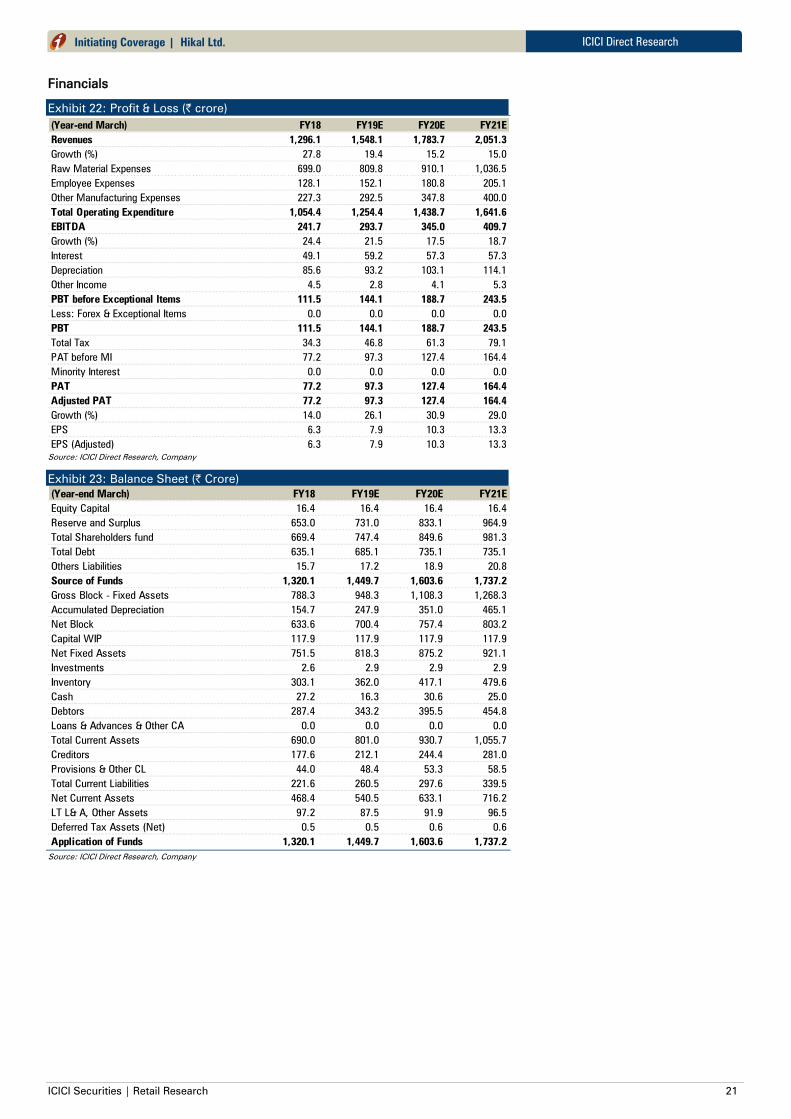

Exhibit 22: Profit & Loss (| crore)

(Year-end March) FY18 FY19E FY20E FY21E

Revenues 1,296.1 1,548.1 1,783.7 2,051.3

Growth (%) 27.8 19.4 15.2 15.0

Raw Material Expenses 699.0 809.8 910.1 1,036.5

Employee Expenses 128.1 152.1 180.8 205.1

Other Manufacturing Expenses 227.3 292.5 347.8 400.0

Total Operating Expenditure 1,054.4 1,254.4 1,438.7 1,641.6

EBITDA 241.7 293.7 345.0 409.7

Growth (%) 24.4 21.5 17.5 18.7

Interest 49.1 59.2 57.3 57.3

Depreciation 85.6 93.2 103.1 114.1

Other Income 4.5 2.8 4.1 5.3

PBT before Exceptional Items 111.5 144.1 188.7 243.5

Less: Forex & Exceptional Items 0.0 0.0 0.0 0.0

PBT 111.5 144.1 188.7 243.5

Total Tax 34.3 46.8 61.3 79.1

PAT before MI 77.2 97.3 127.4 164.4

Minority Interest 0.0 0.0 0.0 0.0

PAT 77.2 97.3 127.4 164.4

Adjusted PAT 77.2 97.3 127.4 164.4

Growth (%) 14.0 26.1 30.9 29.0

EPS 6.3 7.9 10.3 13.3

EPS (Adjusted) 6.3 7.9 10.3 13.3

Source: ICICI Direct Research, Company

Exhibit 23: Balance Sheet (| Crore)

(Year-end March) FY18 FY19E FY20E FY21E

Equity Capital 16.4 16.4 16.4 16.4

Reserve and Surplus 653.0 731.0 833.1 964.9

Total Shareholders fund 669.4 747.4 849.6 981.3

Total Debt 635.1 685.1 735.1 735.1

Others Liabilities 15.7 17.2 18.9 20.8

Source of Funds 1,320.1 1,449.7 1,603.6 1,737.2

Gross Block - Fixed Assets 788.3 948.3 1,108.3 1,268.3

Accumulated Depreciation 154.7 247.9 351.0 465.1

Net Block 633.6 700.4 757.4 803.2

Capital WIP 117.9 117.9 117.9 117.9

Net Fixed Assets 751.5 818.3 875.2 921.1

Investments 2.6 2.9 2.9 2.9

Inventory 303.1 362.0 417.1 479.6

Cash 27.2 16.3 30.6 25.0

Debtors 287.4 343.2 395.5 454.8

Loans & Advances & Other CA 0.0 0.0 0.0 0.0

Total Current Assets 690.0 801.0 930.7 1,055.7

Creditors 177.6 212.1 244.4 281.0

Provisions & Other CL 44.0 48.4 53.3 58.5

Total Current Liabilities 221.6 260.5 297.6 339.5

Net Current Assets 468.4 540.5 633.1 716.2

LT L& A, Other Assets 97.2 87.5 91.9 96.5

Deferred Tax Assets (Net) 0.5 0.5 0.6 0.6

Application of Funds 1,320.1 1,449.7 1,603.6 1,737.2

Source: ICICI Direct Research, Company

ICICI Securities | Retail Research 22

ICICI Direct Research

Initiating Coverage | Hikal Ltd.

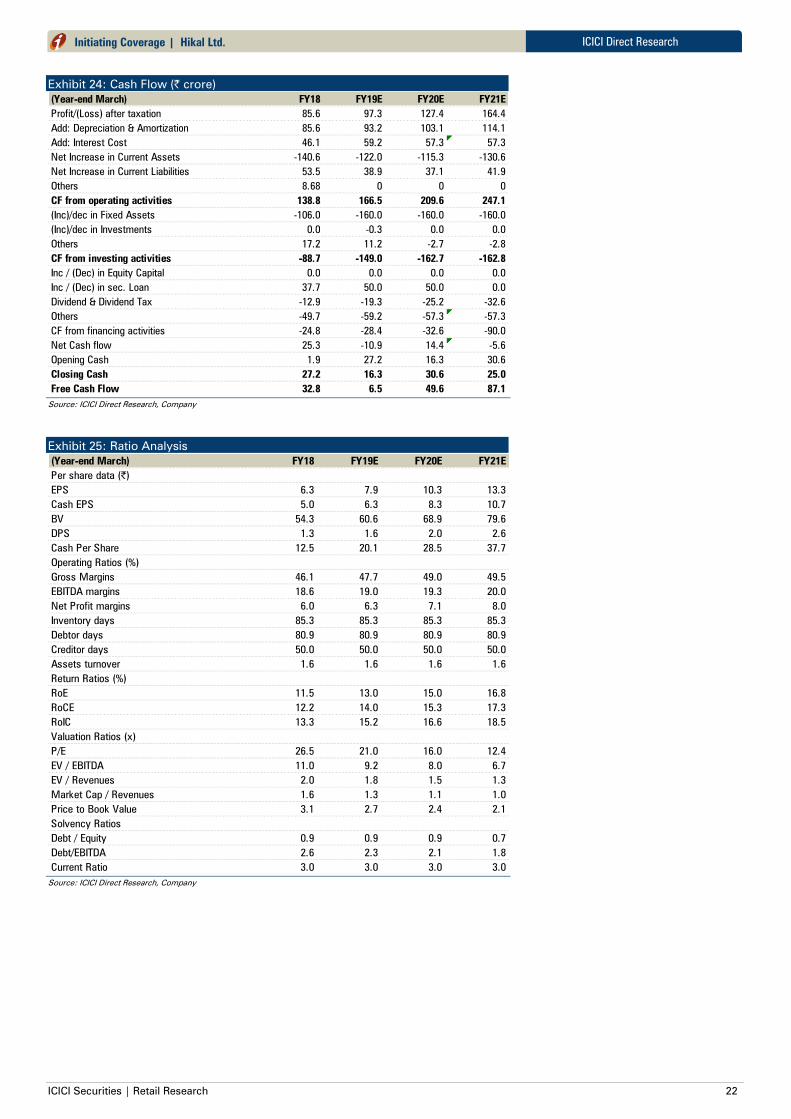

Exhibit 24: Cash Flow (| crore)

(Year-end March) FY18 FY19E FY20E FY21E

Profit/(Loss) after taxation 85.6 97.3 127.4 164.4

Add: Depreciation & Amortization 85.6 93.2 103.1 114.1

Add: Interest Cost 46.1 59.2 57.3 57.3

Net Increase in Current Assets -140.6 -122.0 -115.3 -130.6

Net Increase in Current Liabilities 53.5 38.9 37.1 41.9

Others 8.68 0 0 0

CF from operating activities 138.8 166.5 209.6 247.1

(Inc)/dec in Fixed Assets -106.0 -160.0 -160.0 -160.0

(Inc)/dec in Investments 0.0 -0.3 0.0 0.0

Others 17.2 11.2 -2.7 -2.8

CF from investing activities -88.7 -149.0 -162.7 -162.8

Inc / (Dec) in Equity Capital 0.0 0.0 0.0 0.0

Inc / (Dec) in sec. Loan 37.7 50.0 50.0 0.0

Dividend & Dividend Tax -12.9 -19.3 -25.2 -32.6

Others -49.7 -59.2 -57.3 -57.3

CF from financing activities -24.8 -28.4 -32.6 -90.0

Net Cash flow 25.3 -10.9 14.4 -5.6

Opening Cash 1.9 27.2 16.3 30.6

Closing Cash 27.2 16.3 30.6 25.0

Free Cash Flow 32.8 6.5 49.6 87.1

Source: ICICI Direct Research, Company

Exhibit 25: Ratio Analysis

(Year-end March) FY18 FY19E FY20E FY21E

Per share data (|)

EPS 6.3 7.9 10.3 13.3

Cash EPS 5.0 6.3 8.3 10.7

BV 54.3 60.6 68.9 79.6

DPS 1.3 1.6 2.0 2.6

Cash Per Share 12.5 20.1 28.5 37.7

Operating Ratios (%)

Gross Margins 46.1 47.7 49.0 49.5

EBITDA margins 18.6 19.0 19.3 20.0

Net Profit margins 6.0 6.3 7.1 8.0

Inventory days 85.3 85.3 85.3 85.3

Debtor days 80.9 80.9 80.9 80.9

Creditor days 50.0 50.0 50.0 50.0

Assets turnover 1.6 1.6 1.6 1.6

Return Ratios (%)

RoE 11.5 13.0 15.0 16.8

RoCE 12.2 14.0 15.3 17.3

RoIC 13.3 15.2 16.6 18.5

Valuation Ratios (x)

P/E 26.5 21.0 16.0 12.4

EV / EBITDA 11.0 9.2 8.0 6.7

EV / Revenues 2.0 1.8 1.5 1.3

Market Cap / Revenues 1.6 1.3 1.1 1.0

Price to Book Value 3.1 2.7 2.4 2.1

Solvency Ratios

Debt / Equity 0.9 0.9 0.9 0.7

Debt/EBITDA 2.6 2.3 2.1 1.8

Current Ratio 3.0 3.0 3.0 3.0

Source: ICICI Direct Research, Company

ICICI Securities | Retail Research 23

ICICI Direct Research

Initiating Coverage | Hikal Ltd.

RATING RATIONALE

ICICI Direct endeavours to provide objective opinions and recommendations. ICICI Direct assigns ratings to its

stocks according to their notional target price vs. current market price and then categorises them as Strong Buy,

Buy, Hold and Sell. The performance horizon is two years unless specified and the notional target price is defined

as the analysts' valuation for a stock

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICI Direct Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

ICICI Securities | Retail Research 24

ICICI Direct Research Initiating Coverage | Hikal Ltd.

ANALYST CERTIFICATION

We /I, Siddhant Khandekar (Inter CA), Mitesh Shah, MS (Finance) Analysts, authors and the names subscribed to this report; hereby certify that all of the views expressed in this research report accurately reflect our views about the

subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. It is also confirmed that above mentioned

Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months and do not serve as an officer, director or employee of the companies mentioned in the report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities Limited is a Sebi registered

Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities Limited Sebi Registration is INZ000183631 for stock broker. ICICI Securities is a subsidiary of ICICI Bank which is India’s largest private sector bank

and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which are available on

www.icicibank.com

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and other business relationship

with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the

securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected

recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would

endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI

Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in

circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein