![[Insights Secure – 2015] UPSC Mains Que...t Events_ 07 September 2015 - InSIGHTS](https://static.fdocuments.us/doc/165x107/563dba5c550346aa9aa4f0c4/insights-secure-2015-upsc-mains-quet-events-07-september-2015-insights.jpg)

[Insights Secure – 2015] UPSC Mains Que...t Events_ 07 September 2015 - InSIGHTS

Upload

natalie-longCategory

view

214download

1

TAXSCAPESA Journey of Ideas & Insights in a

Challenging Tax World

2015 Issues Forum

May 14-15, 2015

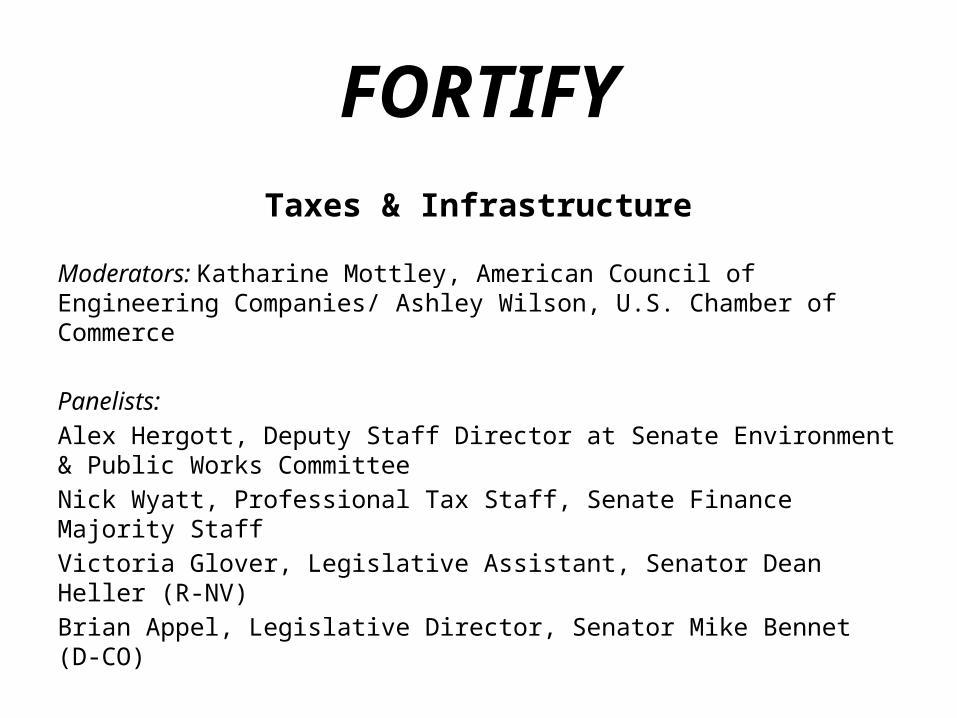

FORTIFY

Taxes & Infrastructure

Moderators: Katharine Mottley, American Council of Engineering Companies/ Ashley Wilson, U.S. Chamber of Commerce

Panelists:

Alex Hergott, Deputy Staff Director at Senate Environment & Public Works Committee

Nick Wyatt, Professional Tax Staff, Senate Finance Majority Staff

Victoria Glover, Legislative Assistant, Senator Dean Heller (R-NV)

Brian Appel, Legislative Director, Senator Mike Bennet (D-CO)

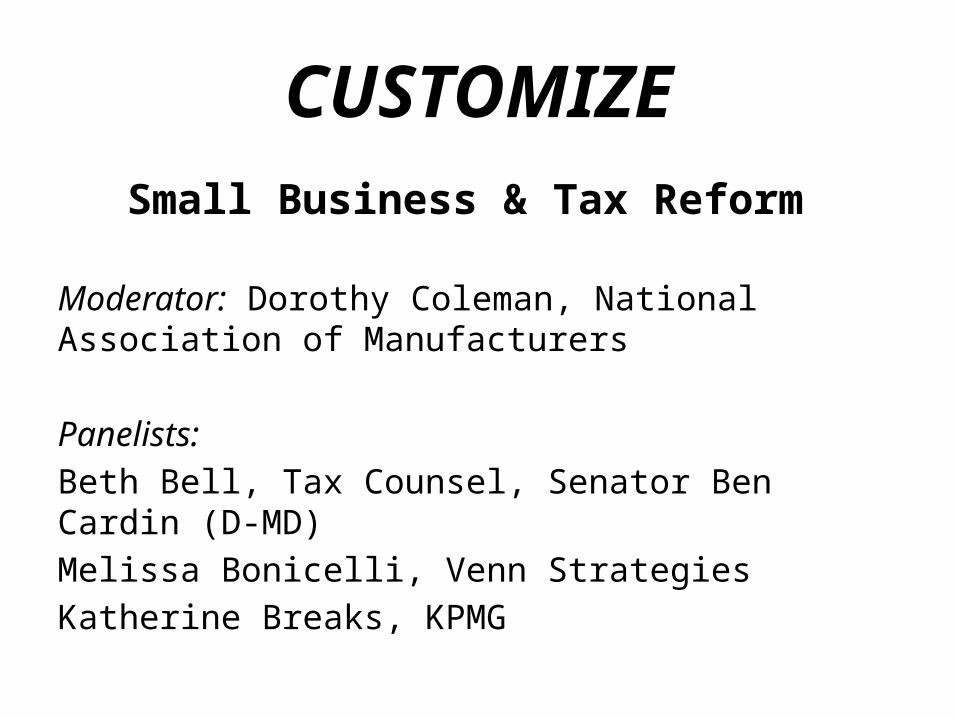

CUSTOMIZESmall Business & Tax Reform

Moderator: Dorothy Coleman, National Association of Manufacturers

Panelists:

Beth Bell, Tax Counsel, Senator Ben Cardin (D-MD)

Melissa Bonicelli, Venn Strategies

Katherine Breaks, KPMG

CUSTOMIZESmall Business & Tax Reform

Moderator: Dorothy Coleman, National Association of Manufacturers

Panelists:

Beth Bell, Tax Counsel, Senator Ben Cardin (D-MD)

Melissa Bonicelli, Venn Strategies

Katherine Breaks, KPMG

Tax Reform and Small Business

Issues Forum

Katherine M, Breaks

Tax Managing Director

Washington National Tax

Washington, DC

May 14, 2015

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

6

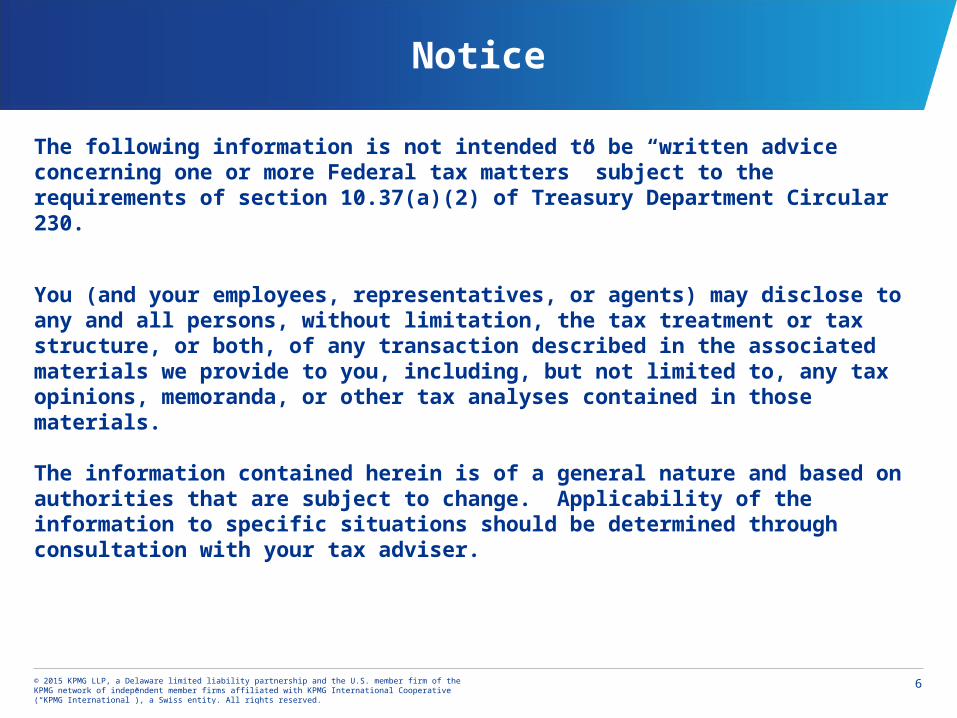

Notice

The following information is not intended to be “written advice concerning one or more Federal tax matters” subject to the requirements of section 10.37(a)(2) of Treasury Department Circular 230.

You (and your employees, representatives, or agents) may disclose to any and all persons, without limitation, the tax treatment or tax structure, or both, of any transaction described in the associated materials we provide to you, including, but not limited to, any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be determined through consultation with your tax adviser.

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

77

C Corporation

A C Corporation pays a maximum corporate tax rate of 35%: 15% of taxable income (TI) up to $50,000 25% of TI over $50,000 to $75,000 34% of TI over $75,000 up to $10 million 35% of TI over $10 million Personal service corporations are not eligible for graduated rates

Surtax on higher levels of taxable income creates flat 34 or 35% tax rate

Individuals that hold stock in U.S. C Corporation more than 12 months

and then receive a dividend pay maximum 15% tax rate (20% for

taxpayers with AGI in excess of $200k single/250k jt filers, adjusted for

inflation)

3.8% net investment tax if AGI over 200k singles/250k jt. filers

Maximum combined corporate/individual tax rate of 48% (without net

investment tax)

If C Corporation is more than 80% owned (by vote and value) by

another C corporation, there is a 100% DRD.

If C corporation is more than 20% but less than 80% owned by another

C corporation, 80% DRD

If C Corporation is less than 80% owned, 70% DRD.

C Corporation

Individual Shareholders

Source: IRC section 11, 1(h).

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

88

S Corporation

With a few exceptions, not discussed here, an S Corporation is a flow-through entity for tax purposes.

The S Corporation’s taxable income is reported on the individual shareholder’s individual income tax return.

The shareholders pay tax on the taxable income of the S Corporation regardless of whether the S Corporation makes any cash distributions.

Rate brackets (2015 joint filers): Taxable income (TI) not over $18,450 – 10% TI over $18,450 but not over $74,900 – 15% TI over $74,900 but not over $151,200 – 25% TI over $151,200 but not over $230,450 – 28% TI over $230,450 but not over $411,500 – 33% TI over $411,500 but not over $464,850 –35% TI over $464,850 – 39.6%

For shareholders that don’t “materially participate,” in the business of the S Corporation, 3.8% net investment tax if AGI over 200k singles/250k jt. filers

S Corporation

Individual Shareholders

Source: Rev. Proc. 2014-61, 2014-47 I.R.B. 860.

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

99

Partnerships

The partnership’s taxable income is claimed on the individual partner’s income tax return.

Partner’s share of the partnership’s taxable income is reported on a K-1.

The partners pay tax on the taxable income regardless of whether the partnership makes any cash distribution.

Rate brackets: Same as prior slide

For a corporate partner, the partnership’s taxable income is claimed on the corporate income tax return.

Income included in corporate taxable income.

Partnership

Individual Partners

© 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

10

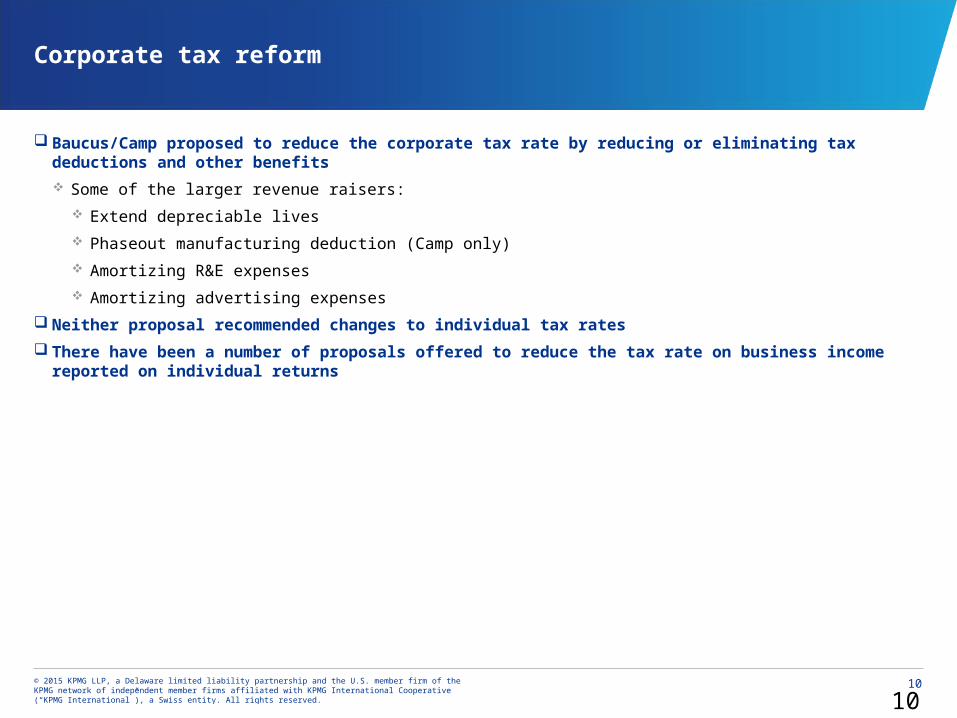

Corporate tax reform

Baucus/Camp proposed to reduce the corporate tax rate by reducing or eliminating tax deductions and other benefits

Some of the larger revenue raisers:

Extend depreciable lives

Phaseout manufacturing deduction (Camp only)

Amortizing R&E expenses

Amortizing advertising expenses

Neither proposal recommended changes to individual tax rates

There have been a number of proposals offered to reduce the tax rate on business income reported on individual returns

10

Thank you

Presentation by Katherine M. Breaks

• © 2015 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

• The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

CENTERModerator: Jodi Knauer, Bula Wellness

IMAGINEThe Challenges of Entrepreneurship

Moderator: Anne Canfield, President, Canfield & Associates; Managing Director, Canfield Press

Panelists:

Anjali Kataria, President, Mytonomy

Amy Millman, President and Founder, Springboard Enterprises

RESOLVEKeynote Panel

The United States Tax Court

Moderator: Libby Coffin, United Technologies

Panelists:

Hon. Tamara Ashford, U.S. Tax Court

Hon. Kathleen Kerrigan, U.S. Tax Court

Hon. Cary Pugh, U.S. Tax Court

INFLUENCE Congressional Leadership Staff

Moderator: Arshi Siddiqui, Akin Gump

Panelists:

Brendan Dunn, Policy Advisor and Counsel, Office of Senate Majority Leader, Mitch McConnell (R-KY)

Ellen Doneski, Chief Advisor on Tax and Economic Policy, Office of the Senate Minority Leader, Harry Reid (D-NV)

Brad Bailey, Assistant to the Speaker for Policy, Office of House Speaker John Boehner (R-OH)

Katherine Monge, Counsel, Office of the Democratic Leader Nancy Pelosi (D-CA)

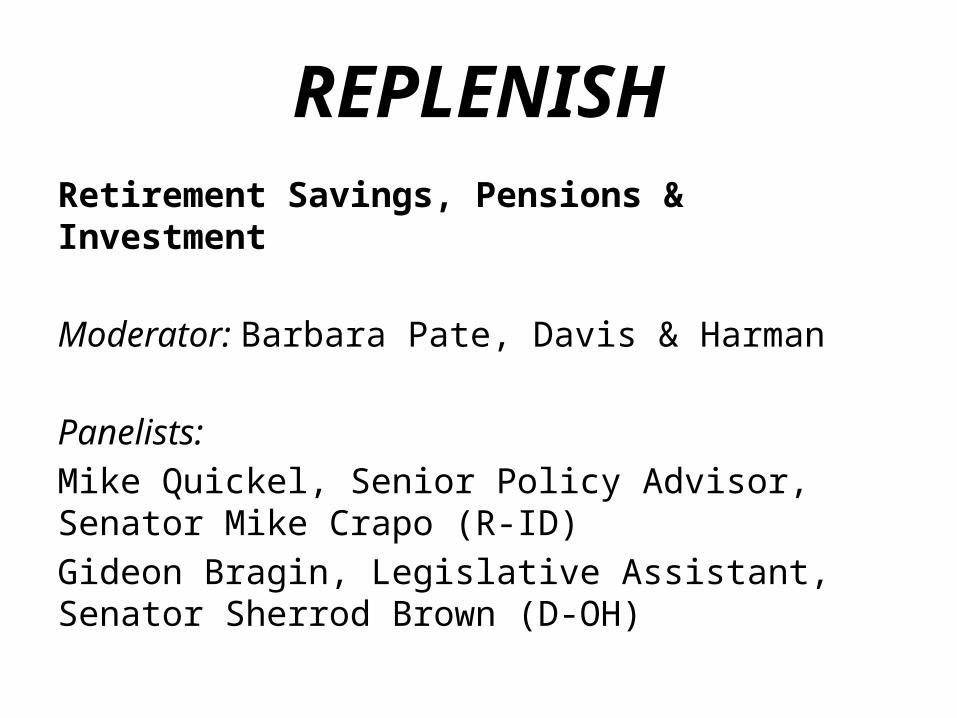

REPLENISHRetirement Savings, Pensions & Investment

Moderator: Barbara Pate, Davis & Harman

Panelists:

Mike Quickel, Senior Policy Advisor, Senator Mike Crapo (R-ID)

Gideon Bragin, Legislative Assistant, Senator Sherrod Brown (D-OH)

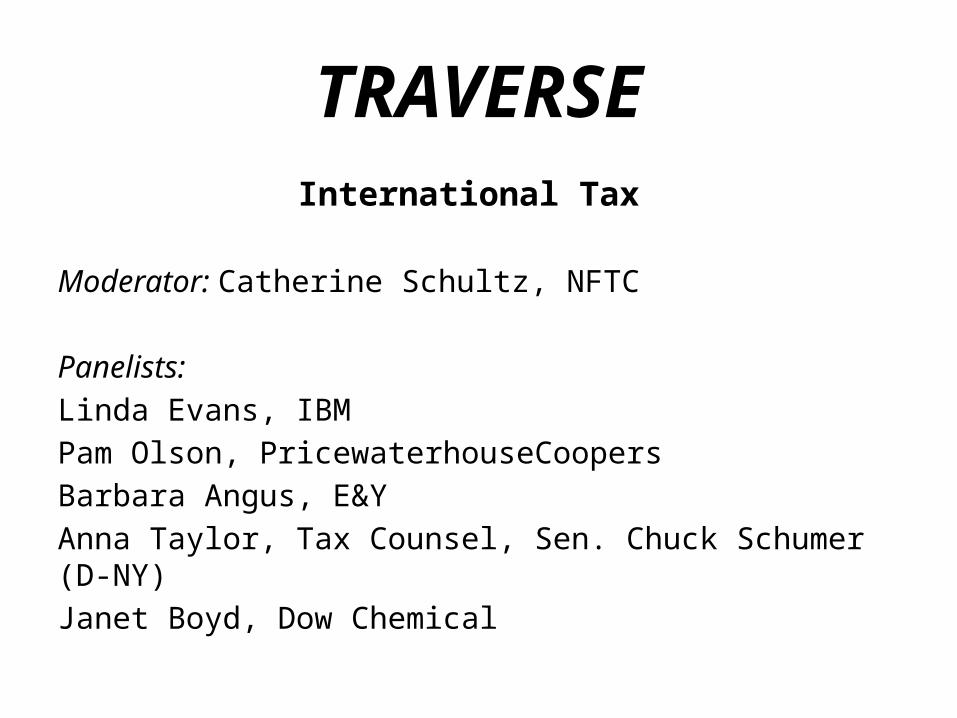

TRAVERSEInternational Tax

Moderator: Catherine Schultz, NFTC

Panelists:

Linda Evans, IBM

Pam Olson, PricewaterhouseCoopers

Barbara Angus, E&Y

Anna Taylor, Tax Counsel, Sen. Chuck Schumer (D-NY)

Janet Boyd, Dow Chemical

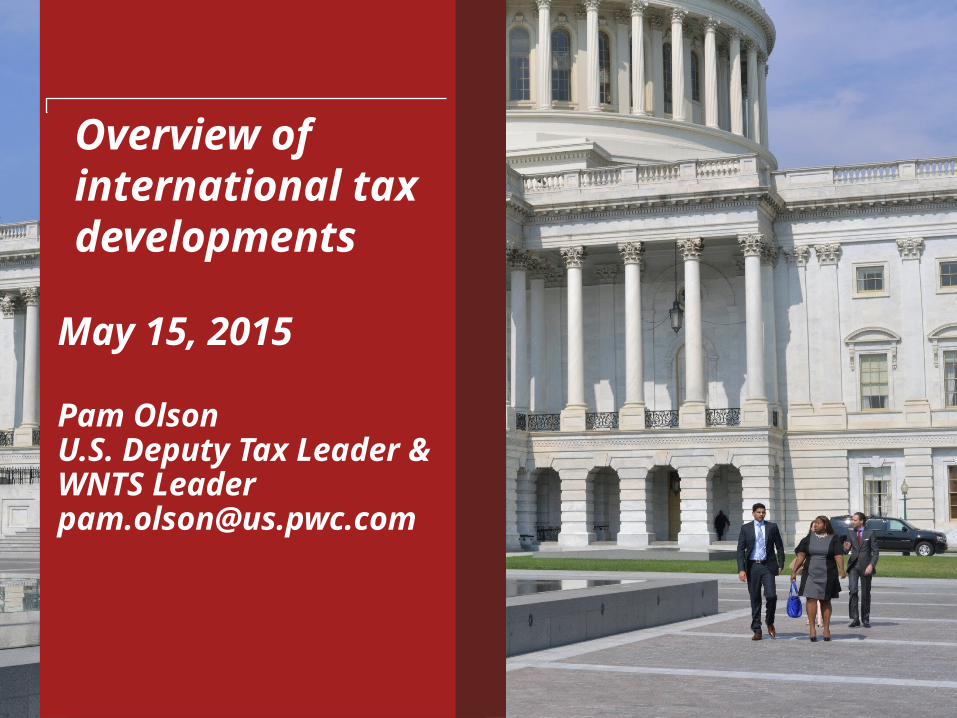

PwC

Overview of international tax developments

May 15, 2015

Pam OlsonU.S. Deputy Tax Leader & WNTS [email protected]

PwC

Business tax reform has been a global trend

Lower tax rate

Exemption system (“territorial”)

Consumption taxes used to fund tax reform

Primaryfeatures of reform

20

PwC

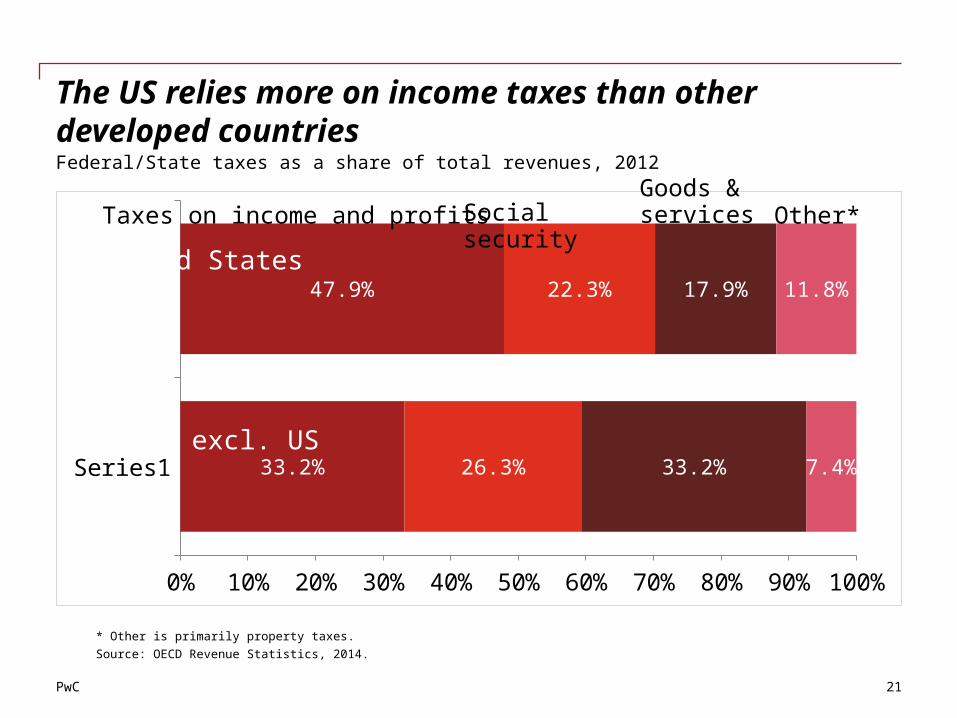

The US relies more on income taxes than other developed countries

Series1

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

33.2%

47.9%

26.3%

22.3%

33.2%

17.9%

7.4%

11.8%

21

OECD, excl. US

Taxes on income and profits Social securityGoods & services Other*

United States

Source: OECD Revenue Statistics, 2014.

Federal/State taxes as a share of total revenues, 2012

* Other is primarily property taxes.

PwC

International competitiveness

22

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

20

25

30

35

40

45

50

39.1

24.8

Top Statutory (Federal and State) Corporate Tax Rates, OECD 1981-2014

United States

OECD Average Excluding US

Since 1988, the average OECD statu-tory corporate tax rate (excl. US) has fallen by over 19 percentage points, while the US rate has increased by half a percentage point.

Source: OECD Tax Database and PwC Calculations

PwC

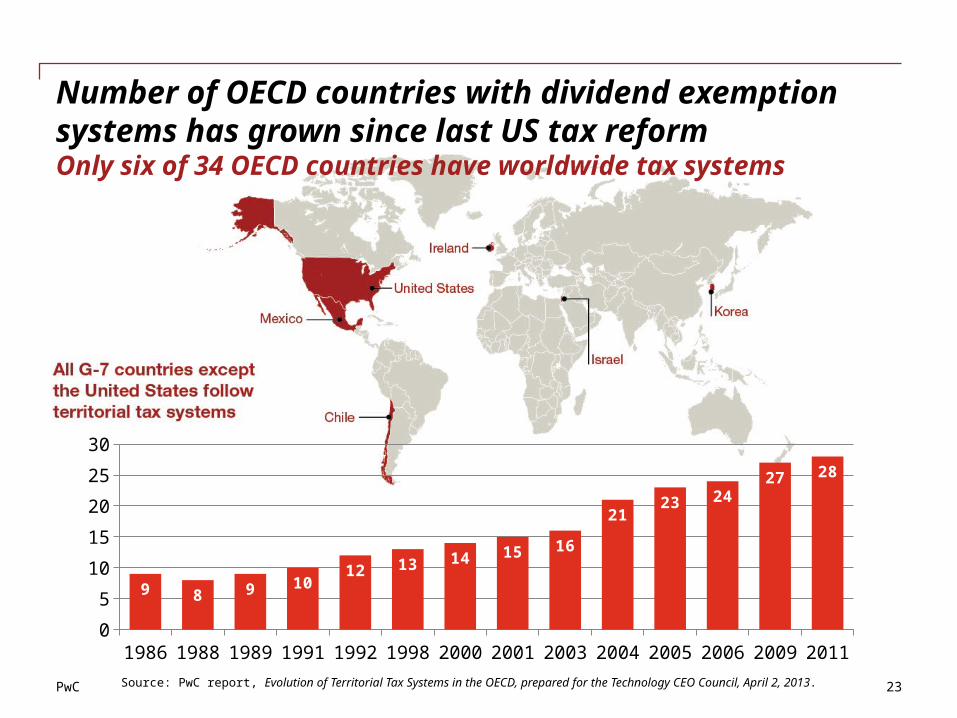

1986 1988 1989 1991 1992 1998 2000 2001 2003 2004 2005 2006 2009 20110

5

10

15

20

25

30

9 8 9 1012 13 14 15 16

2123 24

27 28

23Source: PwC report, Evolution of Territorial Tax Systems in the OECD, prepared for the Technology CEO Council, April 2, 2013.

Number of OECD countries with dividend exemption systems has grown since last US tax reformOnly six of 34 OECD countries have worldwide tax systems

PwC

Research credits & patent box regimes

24

Indi

a

Spain

Denm

ark

Brazil

Norway

Turke

y

Canad

a

Belgi

um

Nethe

rland

s

Japa

nIta

ly

Unite

d Kin

gdom

South

Kor

ea

Unite

d Sta

tes*

Chile

Icela

ndIsr

ael

Mex

ico

Slova

k Rep

ublic

Switzer

land

New Z

eala

nd

-10%

0%

10%

20%

30%

40%

50%

US is 27th out of 41 countries

Countries with solid bars have patent box regimes (Ireland's Knowledge Development Box is under development). R&D tax subsidy rate does not reflect patent box. US rate is a weighted average of alternative simplified and regular research tax credits.

Source: Information Technology and Innovation Institute, "The United States Lags Far Behind in R&D Tax Incentive Generosity," July 2012

PwC

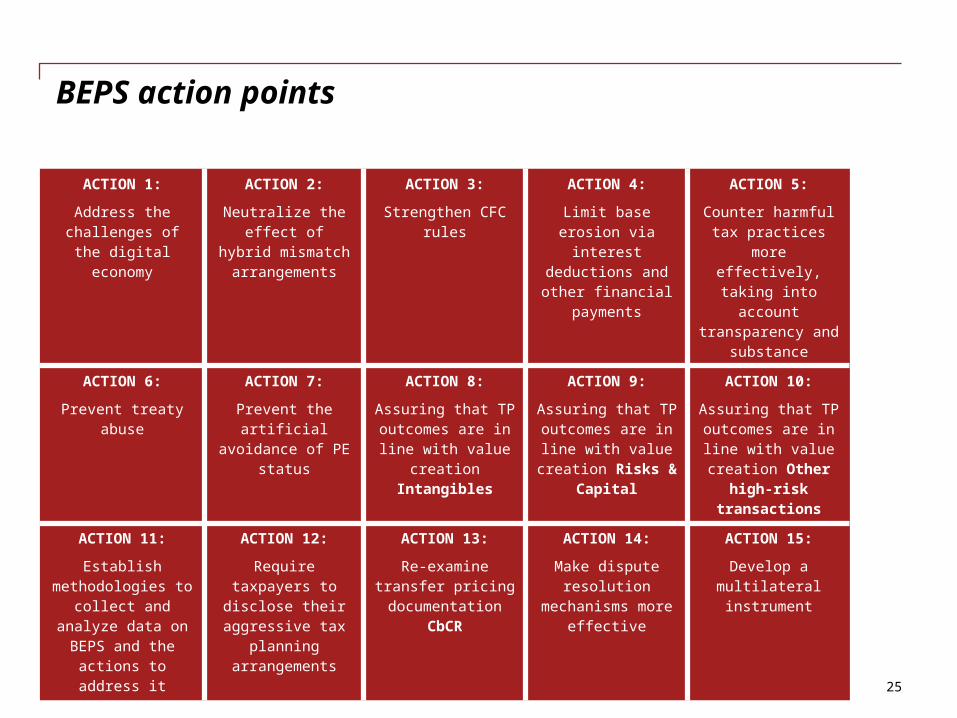

BEPS action points

ACTION 1:

Address the challenges of the digital economy

ACTION 2:

Neutralize the effect of hybrid

mismatch arrangements

ACTION 3:

Strengthen CFC rules

ACTION 4:

Limit base erosion via interest

deductions and other financial

payments

ACTION 5:

Counter harmful tax practices more effectively, taking

into account transparency and

substance

ACTION 6:

Prevent treaty abuse

ACTION 7:

Prevent the artificial

avoidance of PE status

ACTION 8:

Assuring that TP outcomes are in line with value

creation Intangibles

ACTION 9:

Assuring that TP outcomes are in line with value

creation Risks & Capital

ACTION 10:

Assuring that TP outcomes are in line with value creation Other

high-risk transactions

ACTION 11:

Establish methodologies to

collect and analyze data on BEPS and

the actions to address it

ACTION 12:

Require taxpayers to disclose their aggressive tax

planning arrangements

ACTION 13:

Re-examine transfer pricing documentation

CbCR

ACTION 14:

Make dispute resolution

mechanisms more effective

ACTION 15:

Develop a multilateral instrument

25

PwC

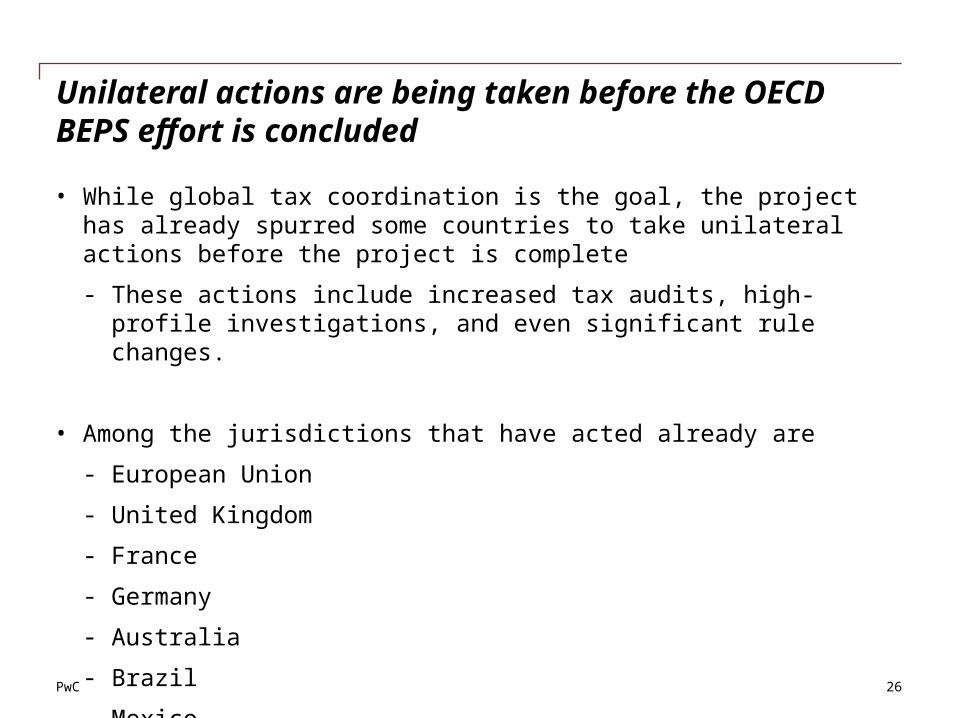

Unilateral actions are being taken before the OECD BEPS effort is concluded

• While global tax coordination is the goal, the project has already spurred some countries to take unilateral actions before the project is complete

- These actions include increased tax audits, high-profile investigations, and even significant rule changes.

• Among the jurisdictions that have acted already are

- European Union

- United Kingdom

- France

- Germany

- Australia

- Brazil

- Mexico 26

PwC

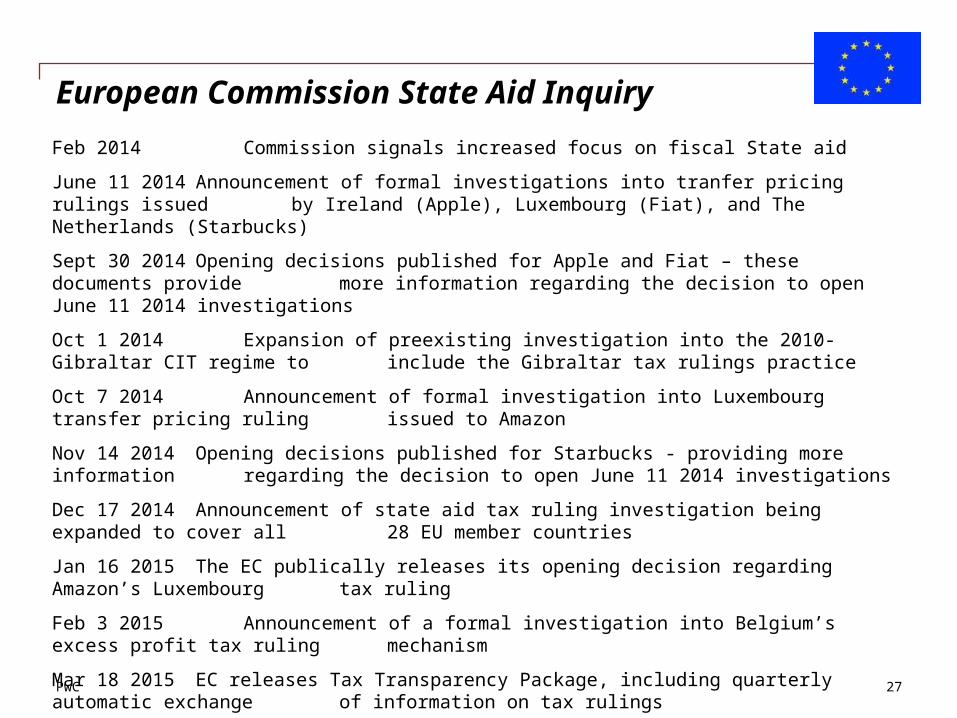

European Commission State Aid Inquiry

27

Feb 2014 Commission signals increased focus on fiscal State aid

June 11 2014 Announcement of formal investigations into tranfer pricing rulings issued by Ireland (Apple), Luxembourg (Fiat), and The Netherlands (Starbucks)

Sept 30 2014 Opening decisions published for Apple and Fiat – these documents provide more information regarding the decision to open June 11 2014 investigations

Oct 1 2014 Expansion of preexisting investigation into the 2010-Gibraltar CIT regime to include the Gibraltar tax rulings practice

Oct 7 2014 Announcement of formal investigation into Luxembourg transfer pricing ruling issued to Amazon

Nov 14 2014 Opening decisions published for Starbucks - providing more information regarding the decision to open June 11 2014 investigations

Dec 17 2014 Announcement of state aid tax ruling investigation being expanded to cover all 28 EU member countries

Jan 16 2015 The EC publically releases its opening decision regarding Amazon’s Luxembourg tax ruling

Feb 3 2015 Announcement of a formal investigation into Belgium’s excess profit tax ruling mechanism

Mar 18 2015 EC releases Tax Transparency Package, including quarterly automatic exchange of information on tax rulings

OECD BEPS project – Status, 2015 outlook, and next steps

15 May 2015

Page 29

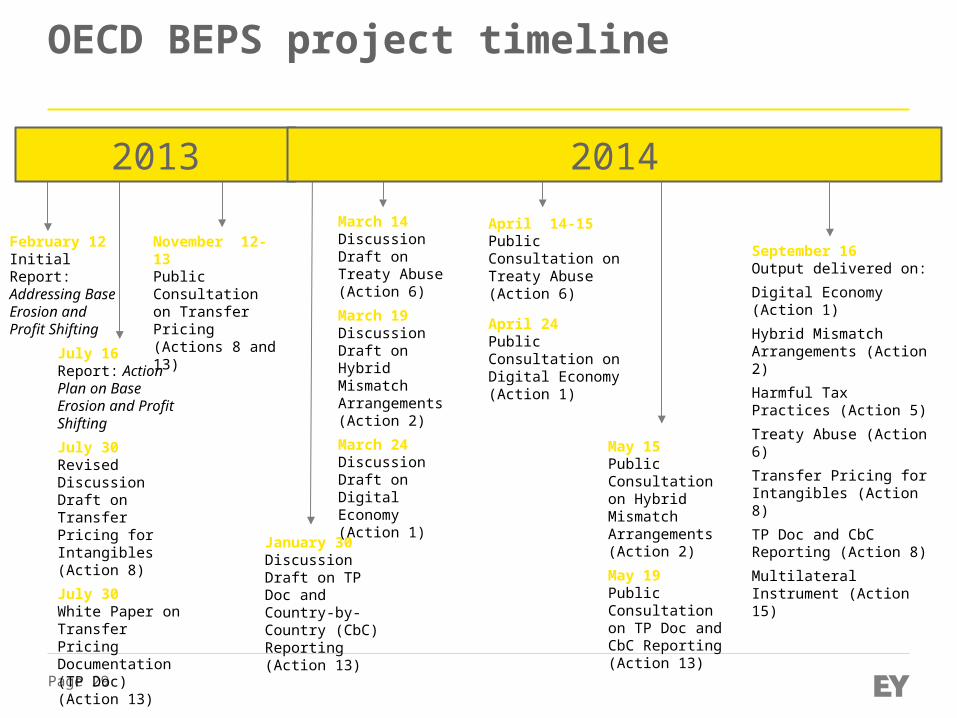

OECD BEPS project timeline

2013

February 12Initial Report: Addressing Base Erosion and Profit Shifting

July 16Report: Action Plan on Base Erosion and Profit Shifting

July 30Revised Discussion Draft on Transfer Pricing for Intangibles (Action 8)

July 30White Paper on Transfer Pricing Documentation (TP Doc) (Action 13)

November 12-13Public Consultation on Transfer Pricing (Actions 8 and 13)

January 30Discussion Draft on TP Doc and Country-by-Country (CbC) Reporting (Action 13)

2014

March 14Discussion Draft on Treaty Abuse (Action 6)

March 19Discussion Draft on Hybrid Mismatch Arrangements (Action 2)

March 24Discussion Draft on Digital Economy (Action 1)

September 16Output delivered on:

Digital Economy (Action 1)

Hybrid Mismatch Arrangements (Action 2)

Harmful Tax Practices (Action 5)

Treaty Abuse (Action 6)

Transfer Pricing for Intangibles (Action 8)

TP Doc and CbC Reporting (Action 8)

Multilateral Instrument (Action 15)

April 14-15Public Consultation on Treaty Abuse (Action 6)

April 24Public Consultation on Digital Economy (Action 1)

May 15Public Consultation on Hybrid Mismatch Arrangements (Action 2)

May 19Public Consultation on TP Doc and CbC Reporting (Action 13)

Page 30

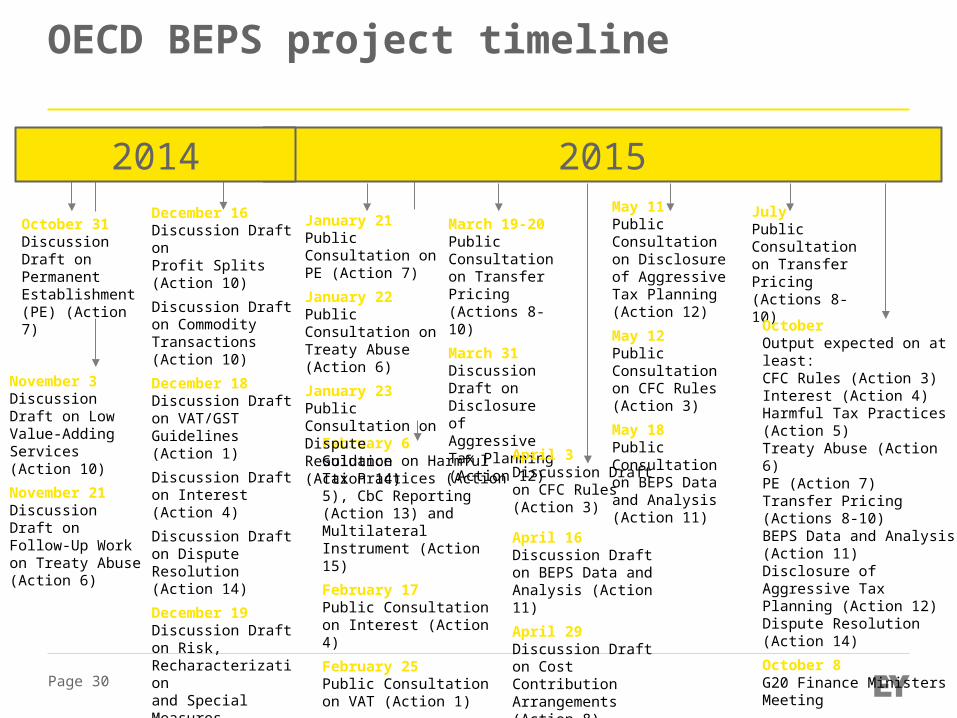

OECD BEPS project timeline

2015

February 6Guidance on Harmful Tax Practices (Action 5), CbC Reporting (Action 13) and Multilateral Instrument (Action 15)

February 17Public Consultation on Interest (Action 4)

February 25Public Consultation on VAT (Action 1)

March 19-20Public Consultation on Transfer Pricing (Actions 8-10)

March 31Discussion Draft on Disclosure of Aggressive Tax Planning (Action 12)

April 3Discussion Draft on CFC Rules (Action 3)

April 16Discussion Draft on BEPS Data and Analysis (Action 11)

April 29Discussion Draft on Cost Contribution Arrangements (Action 8)

May 11Public Consultation on Disclosure of Aggressive Tax Planning (Action 12)

May 12Public Consultation on CFC Rules (Action 3)

May 18Public Consultation on BEPS Data and Analysis (Action 11)

JulyPublic Consultation on Transfer Pricing (Actions 8-10)

October Output expected on at least:CFC Rules (Action 3)Interest (Action 4)Harmful Tax Practices (Action 5)Treaty Abuse (Action 6)PE (Action 7)Transfer Pricing (Actions 8-10)BEPS Data and Analysis (Action 11)Disclosure of Aggressive Tax Planning (Action 12)Dispute Resolution (Action 14)

October 8G20 Finance Ministers Meeting

January 21Public Consultation on PE (Action 7)

January 22Public Consultation on Treaty Abuse (Action 6)

January 23Public Consultation on Dispute Resolution (Action 14)

October 31 Discussion Draft on Permanent Establishment (PE) (Action 7)

November 3 Discussion Draft on Low Value-Adding Services (Action 10)

November 21Discussion Draft on Follow-Up Work on Treaty Abuse (Action 6)

December 16Discussion Draft on Profit Splits (Action 10)

Discussion Draft on Commodity Transactions (Action 10)

December 18Discussion Draft on VAT/GST Guidelines (Action 1)

Discussion Draft on Interest (Action 4)

Discussion Draft on Dispute Resolution (Action 14)

December 19Discussion Draft on Risk, Recharacterization and Special Measures (Actions 8-10)

2014

Page 31

OECD BEPS Action Plan – September 2014 developments

► OECD issued reports on all seven 2014 BEPS focus areas on 16 September 2014:

► Action 1 (Digital economy)► Action 2 (Hybrid mismatch arrangements)► Action 5 (Harmful tax practices)► Action 6 (Treaty abuse)► Action 8 (Transfer pricing for intangibles)► Action 13 (Transfer pricing documentation and country-by-country

(CbC) reporting)► Action 15 (Multilateral instrument)

► Further work in all these areas continues in 2015► 2015 BEPS focus areas involve more fundamental

concepts and more challenging issues, but G20 committed to completion of BEPS project in 2015

Page 32

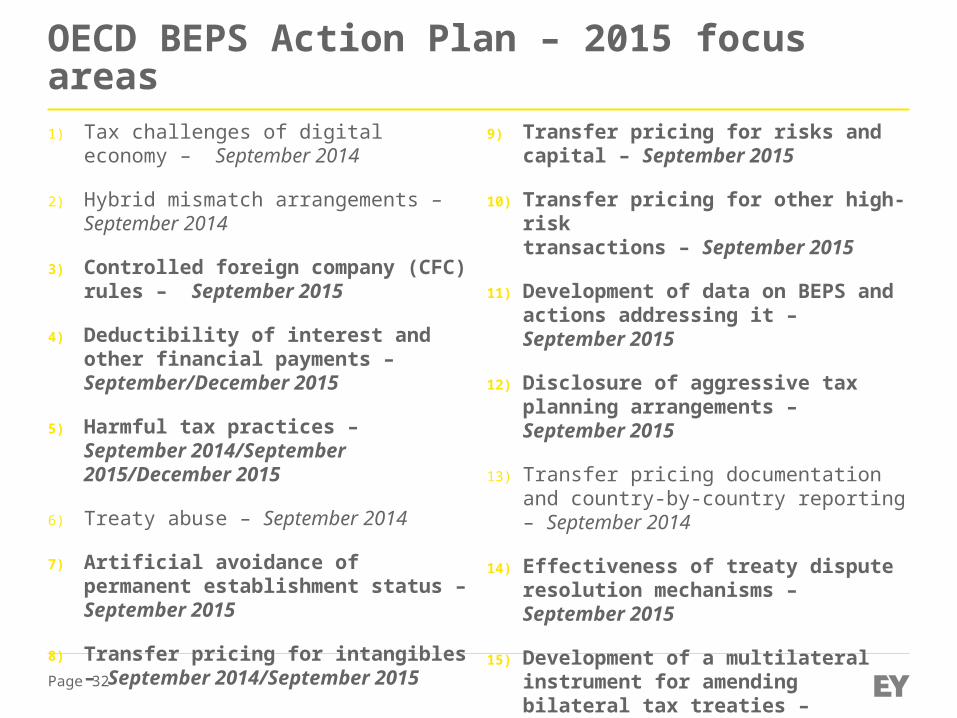

OECD BEPS Action Plan – 2015 focus areas

1) Tax challenges of digital economy – September 2014

2) Hybrid mismatch arrangements – September 2014

3) Controlled foreign company (CFC) rules – September 2015

4) Deductibility of interest and other financial payments – September/December 2015

5) Harmful tax practices – September 2014/September 2015/December 2015

6) Treaty abuse – September 2014

7) Artificial avoidance of permanent establishment status – September 2015

8) Transfer pricing for intangibles – September 2014/September 2015

9) Transfer pricing for risks and capital – September 2015

10) Transfer pricing for other high-risktransactions – September 2015

11) Development of data on BEPS and actions addressing it – September 2015

12) Disclosure of aggressive tax planning arrangements – September 2015

13) Transfer pricing documentation and country-by-country reporting – September 2014

14) Effectiveness of treaty dispute resolution mechanisms – September 2015

15) Development of a multilateral instrument for amending bilateral tax treaties – September 2014/December 2015

Page 33

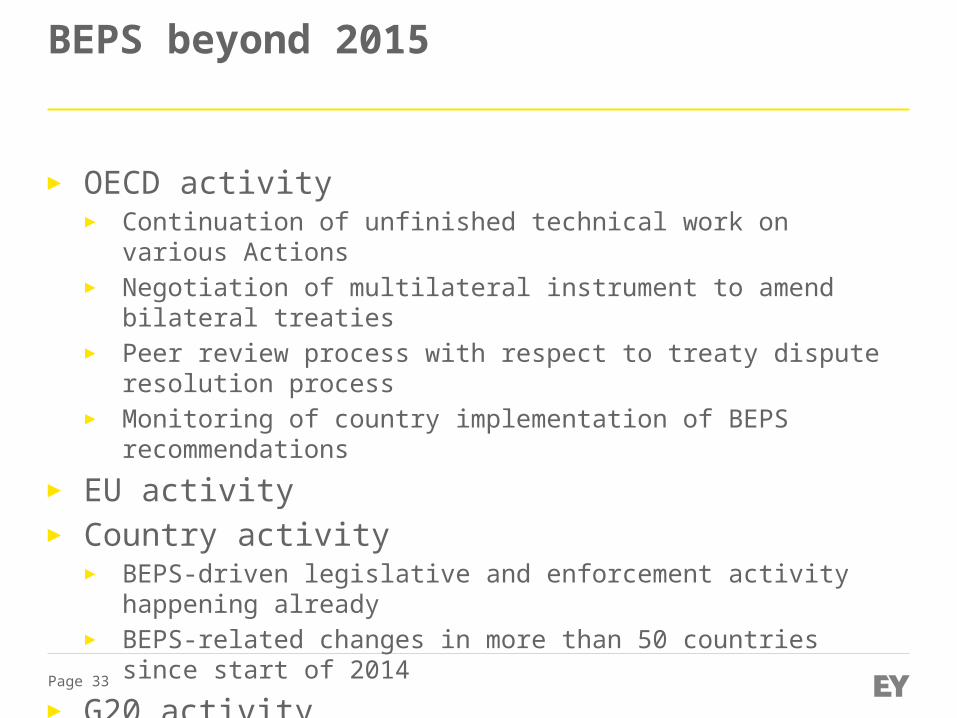

BEPS beyond 2015

► OECD activity► Continuation of unfinished technical work on various Actions► Negotiation of multilateral instrument to amend bilateral treaties► Peer review process with respect to treaty dispute resolution process► Monitoring of country implementation of BEPS recommendations

► EU activity► Country activity

► BEPS-driven legislative and enforcement activity happening already► BEPS-related changes in more than 50 countries since start of 2014

► G20 activity► Public and press reaction

© 2015 IBM Corporation

Tax Coalition Issues Forum - International Tax Panel May 2015

Digital Global Tax Developments Linda Evans, Director Global Tax Policy

IBM Government and Regulatory Affairs

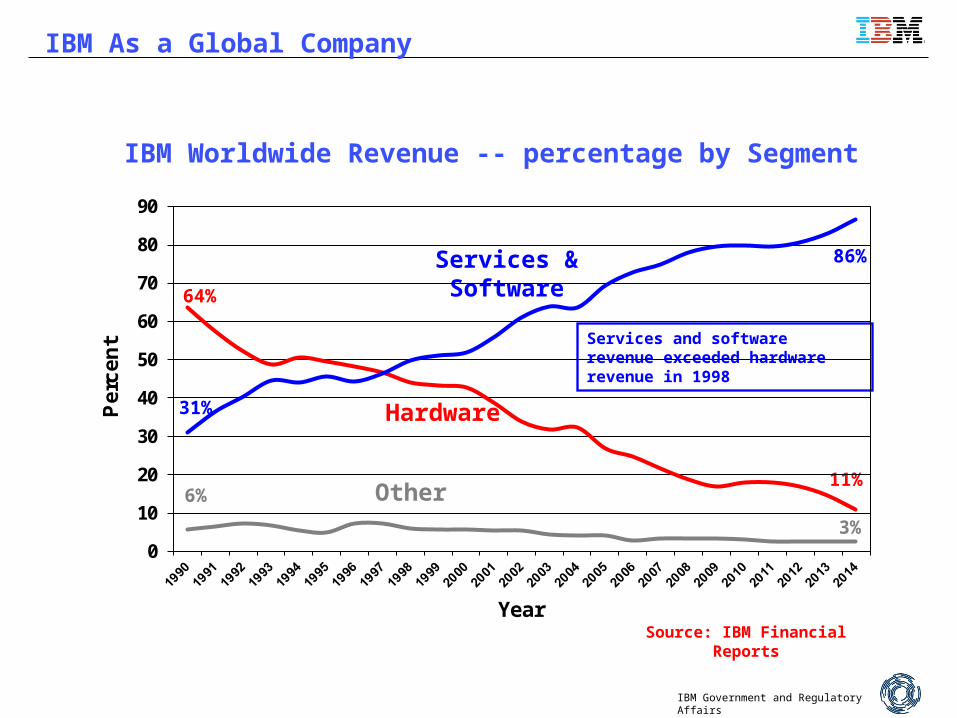

IBM As a Global Company

0

10

20

30

40

50

60

70

80

90

Pe

rce

nt

YearSource: IBM Financial Reports

Hardware

Services & Software

Other

86%

31%

64%

11%6%

3%

Services and software revenue exceeded hardware revenue in 1998

IBM Worldwide Revenue -- percentage by Segment

IBM Government and Regulatory Affairs

36

Global tax developments and digital

Background– Apparent perception that digital and mobile IP/ intangible income drive

aggressive tax avoidance and offshore planning– Global efforts to treat differently income from digital goods and

services as compared different from that for “physical goods”• “Virtual PE” and profit attribution • Gross basis versus net taxation

– US MNCs, particularly internet ones have been targeted– Global initiatives proposed by OECD, EU and specific countries

including the US – Challenge: Global efforts include developing countries that have

divergent views on tax policy and revenue needs– Result: Increased disputes, aggressive audits and less favorable

climate for FDI

IBM Government and Regulatory Affairs

Global tax developments and digital

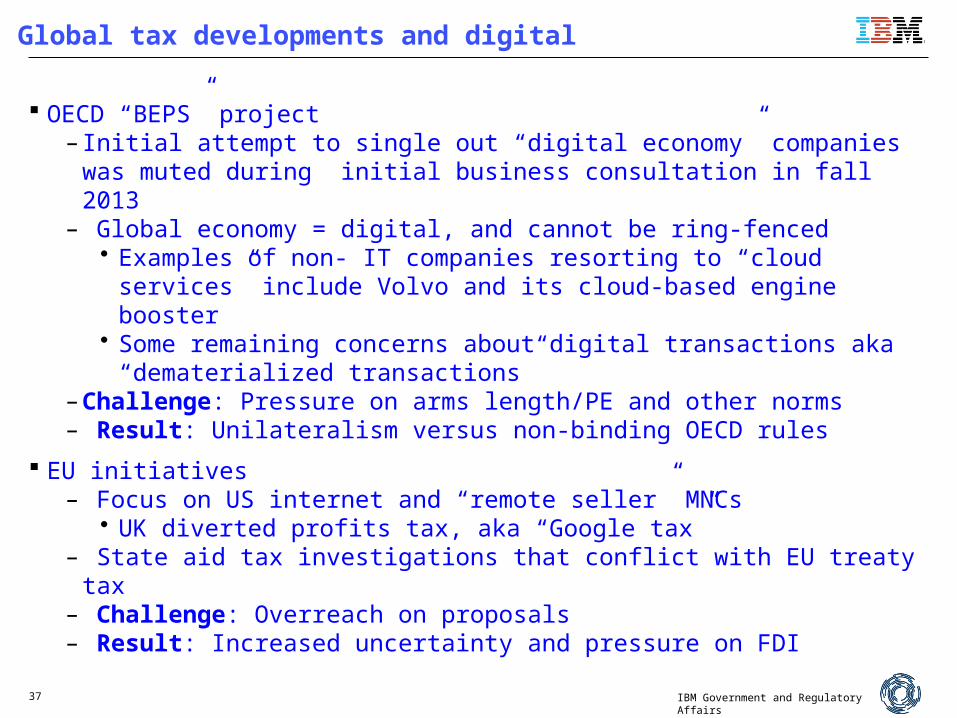

OECD “BEPS” project– Initial attempt to single out “digital economy” companies was muted during

initial business consultation in fall 2013 – Global economy = digital, and cannot be ring-fenced

• Examples of non- IT companies resorting to “cloud services” include Volvo and its cloud-based engine booster

• Some remaining concerns about digital transactions aka “dematerialized transactions”

– Challenge: Pressure on arms length/PE and other norms – Result: Unilateralism versus non-binding OECD rules

EU initiatives – Focus on US internet and “remote seller” MNCs

• UK diverted profits tax, aka “Google tax”– State aid tax investigations that conflict with EU treaty tax – Challenge: Overreach on proposals – Result: Increased uncertainty and pressure on FDI

37

IBM Government and Regulatory Affairs

Global tax developments and digital

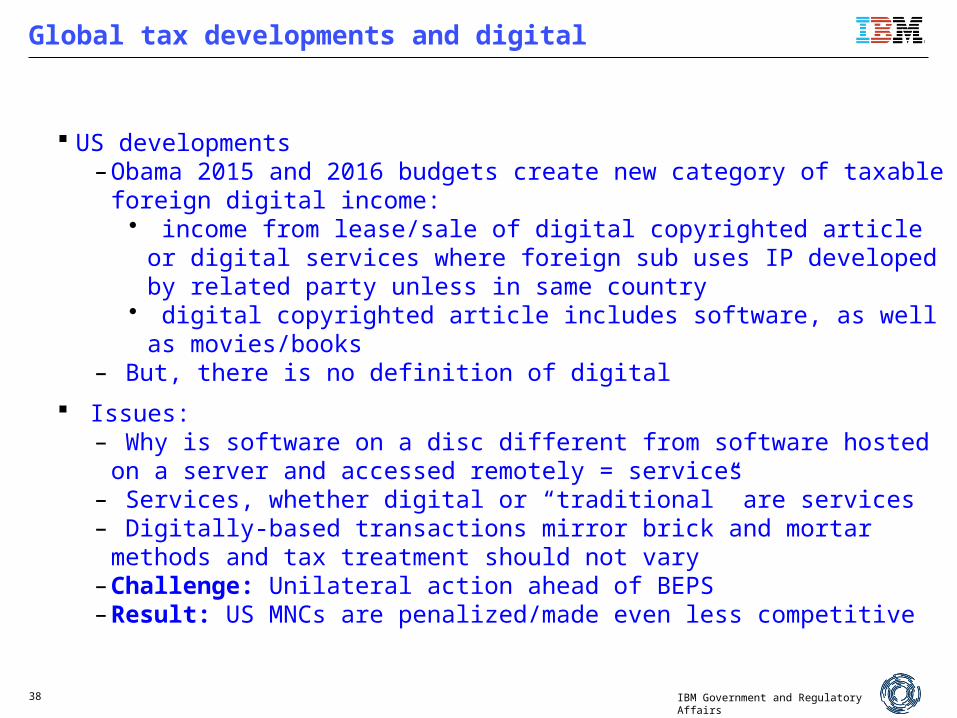

US developments – Obama 2015 and 2016 budgets create new category of taxable foreign digital

income:• income from lease/sale of digital copyrighted article or digital services

where foreign sub uses IP developed by related party unless in same country

• digital copyrighted article includes software, as well as movies/books– But, there is no definition of digital

Issues:– Why is software on a disc different from software hosted on a server and

accessed remotely = services– Services, whether digital or “traditional” are services– Digitally-based transactions mirror brick and mortar methods and tax

treatment should not vary – Challenge: Unilateral action ahead of BEPS– Result: US MNCs are penalized/made even less competitive

38

IBM Government and Regulatory Affairs39

There will likely be greater sensitivity to tax planning to avoid perception of overreach and blows to public image and reputation; also increasing pressure on audits and dispute resolution

Page 40Page 40

Global Tax Developments for Manufacturers

Janet Boyd, Director of Government Relations and Legislative Council

Tax Coalition Issues Forum - International Tax Panel May 15, 2015

Page 41Page 41

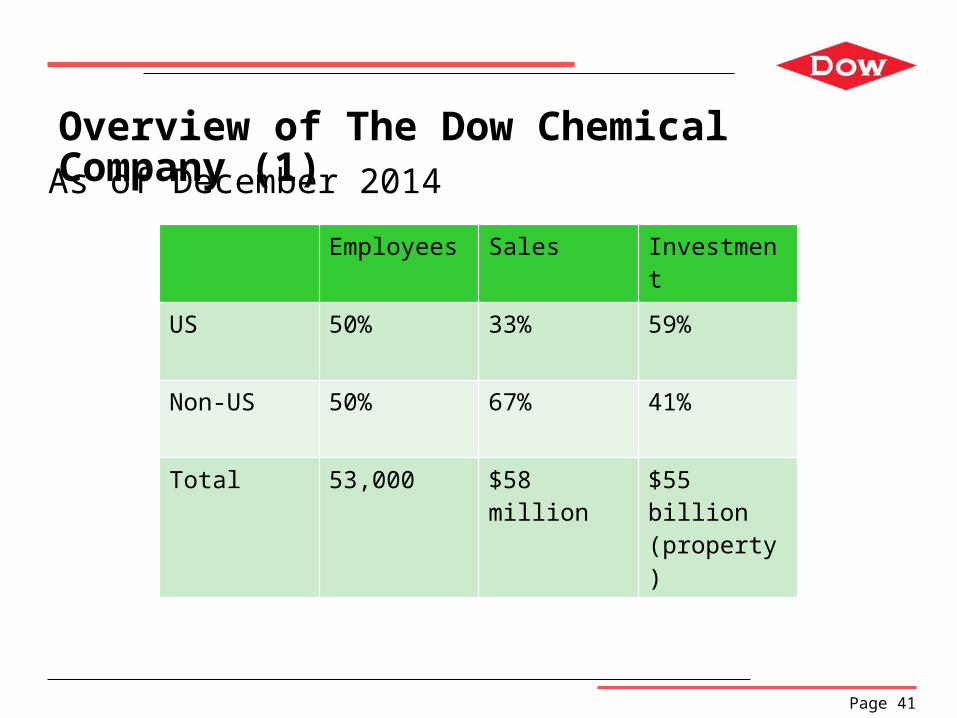

Overview of The Dow Chemical Company (1)As of December 2014

Employees Sales Investment

US 50% 33% 59%

Non-US 50% 67% 41%

Total 53,000 $58 million $55 billion (property)

Page 42DOW CONFIDENTIAL - Do not share without permission Page 42

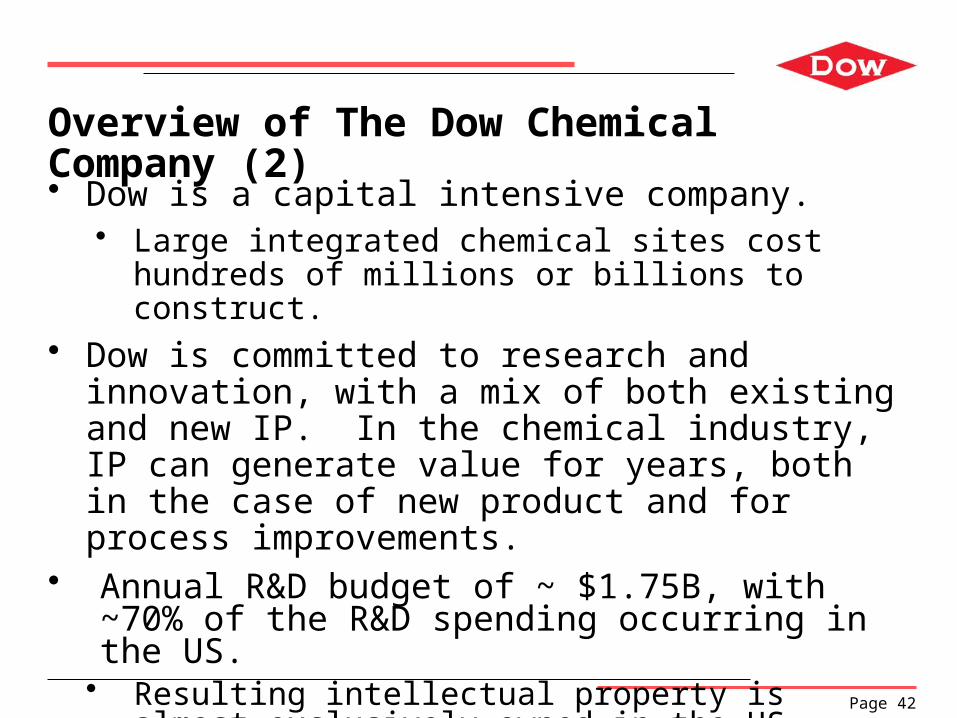

Overview of The Dow Chemical Company (2)

• Dow is a capital intensive company. • Large integrated chemical sites cost hundreds of millions or billions

to construct.• Dow is committed to research and innovation, with a mix of both

existing and new IP. In the chemical industry, IP can generate value for years, both in the case of new product and for process improvements.

• Annual R&D budget of ~ $1.75B, with ~70% of the R&D spending occurring in the US.

• Resulting intellectual property is almost exclusively owned in the US.

DOW CONFIDENTIAL - Do not share without permission

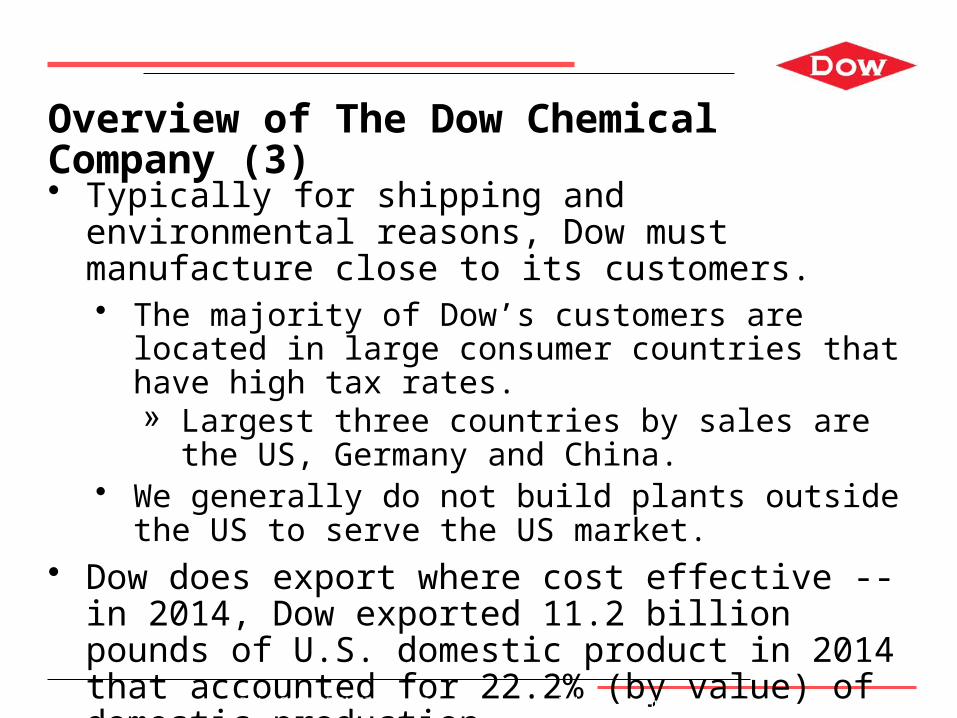

Overview of The Dow Chemical Company (3)

• Typically for shipping and environmental reasons, Dow must manufacture close to its customers. • The majority of Dow’s customers are located in large consumer

countries that have high tax rates. » Largest three countries by sales are the US, Germany and

China.• We generally do not build plants outside the US to serve the US

market.• Dow does export where cost effective -- in 2014, Dow exported

11.2 billion pounds of U.S. domestic product in 2014 that accounted for 22.2% (by value) of domestic production.

Page 43

Dow’s competitors are foreign-owned and state-owned

• Dow is currently the 3rd largest chemical company in the world. Numbers1 and 2 are foreign-owned: BASF and Sinopec. From 2003 through 2005, Dow was the top company with BASF number 2.

• In 1990, Saudi Basic Industries, founded by royal decree in 1976, was number 34 on the Global Top 50. Ten years ago, as SABIC, it had climbed to number 12. Currently, SABIC has moved up to number four, trailing only BASF, Dow, and China’s Sinopec.

DOW CONFIDENTIAL - Do not share without permission Page 44

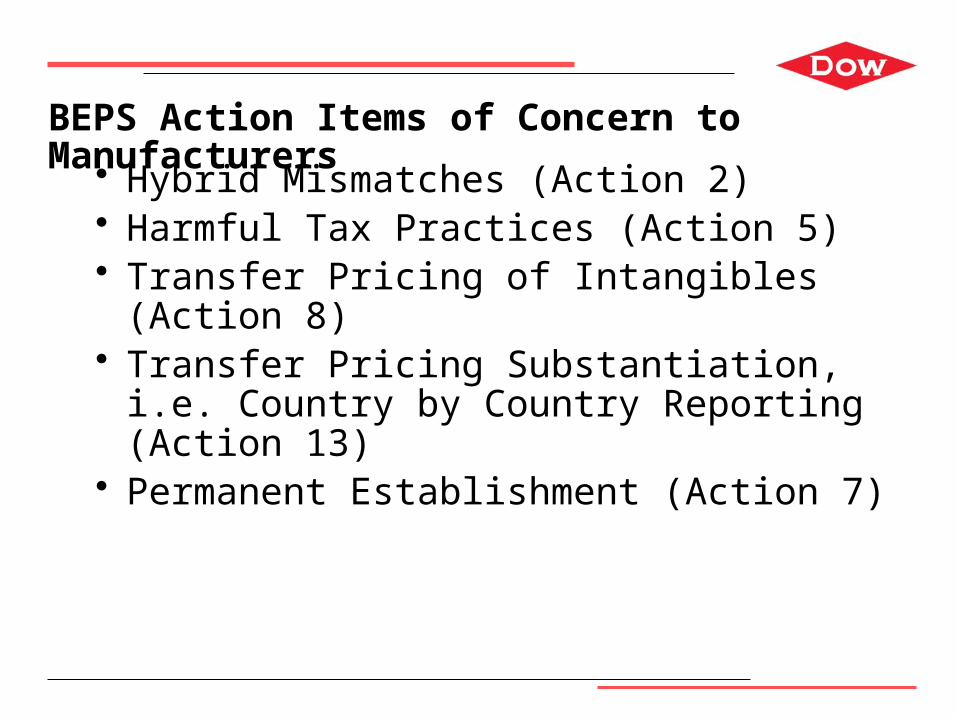

BEPS Action Items of Concern to Manufacturers

• Hybrid Mismatches (Action 2)• Harmful Tax Practices (Action 5)• Transfer Pricing of Intangibles (Action 8)• Transfer Pricing Substantiation, i.e. Country by Country

Reporting (Action 13)• Permanent Establishment (Action 7)

Page 45

BEPS Action Items of Concern to Manufacturers

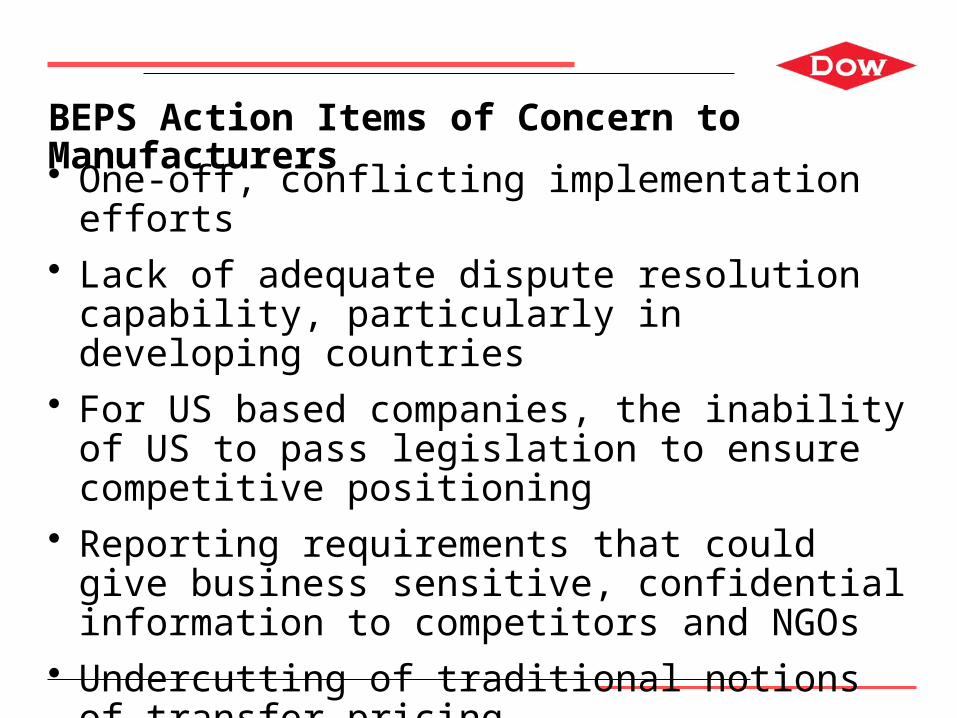

• One-off, conflicting implementation efforts• Lack of adequate dispute resolution capability, particularly in

developing countries• For US based companies, the inability of US to pass

legislation to ensure competitive positioning • Reporting requirements that could give business sensitive,

confidential information to competitors and NGOs• Undercutting of traditional notions of transfer pricing• Conflicting rules on interest deductions

Page 46

ENERGIZEKeynote Speaker

Olga Hartwell, Senior Vice President & Tax Director, GE

Introduction by Lisa Wolski, GE

THANK YOU!!

![[Insights Secure – 2015] UPSC Mains Que...t Events_ 10 September 2015 - InSIGHTS](https://static.fdocuments.us/doc/165x107/563dba5c550346aa9aa4efab/insights-secure-2015-upsc-mains-quet-events-10-september-2015-insights.jpg)