UK Retail Banking Insights* - PwC€¦ · UK Retail Banking Insights which aims to address five...

24

Banking and Capital Markets UK Retail Banking Insights* Editor: Anne Obey, Director, Retail and Mortgage Banking Group Tel: 0117 928 1251 Email: [email protected] Distribution: If you would like to receive this publication by email or you would like to add your colleagues to the mailing list, please contact Carly Taylor on [email protected] Inside this issue 03 Precious Plastic 2007 – Consumer credit in the UK 08 Lenders face further scrutiny – the call for fairer practices 14 Building societies at a crossroad 18 Risk Appetite – The Starting Point for the ‘Use Test’ 21 EU Savings Directive – first year UK survey Welcome to the March issue of the PricewaterhouseCoopers UK Retail Banking Insights which aims to address five topical and challenging issues facing the retail banking industry. In this edition of the UK Retail Banking Insight, we look at a number of current hot topics in the sector, including analysis of the strategic options for the building society sector in Nick Page’s article on page 14 and of trends in consumer lending in ‘Precious Plastic 2007’. The subject of regulatory challenges is picked up by David Morey who examines three highly topical issues in TCF: PPI, mortgage exit fees and affordability and the regulatory focus continues with articles looking at some of the practicalities of Basel II implementation, and early experience of the EU Savings Directive. I hope you enjoy this edition. We continue to value your feedback and suggestions on topics for future editions. Copies are available from www.pwc.com/banking. Please contact me if you would like to discuss any of these issues in more detail. John Hitchins UK Banking Leader 020 7804 2497 [email protected] MARCH 2007

Transcript of UK Retail Banking Insights* - PwC€¦ · UK Retail Banking Insights which aims to address five...

Banking and Capital Markets

UK Retail Banking Insights*

Editor: Anne Obey,Director, Retail and Mortgage Banking GroupTel: 0117 928 1251Email: [email protected]

Distribution: If you would like toreceive this publication by email oryou would like to add your colleaguesto the mailing list, please contact CarlyTaylor on [email protected]

Inside this issue

03 Precious Plastic 2007 –Consumer credit in the UK

08 Lenders face further scrutiny– the call for fairer practices

14 Building societies ata crossroad

18 Risk Appetite – The StartingPoint for the ‘Use Test’

21 EU Savings Directive –first year UK survey

Welcome to the March issue of the PricewaterhouseCoopersUK Retail Banking Insights which aims to address five topicaland challenging issues facing the retail banking industry.

In this edition of the UK Retail Banking Insight, we look at a number of current hottopics in the sector, including analysis of the strategic options for the buildingsociety sector in Nick Page’s article on page 14 and of trends in consumer lendingin ‘Precious Plastic 2007’.

The subject of regulatory challenges is picked up by David Morey who examinesthree highly topical issues in TCF: PPI, mortgage exit fees and affordability and theregulatory focus continues with articles looking at some of the practicalities ofBasel II implementation, and early experience of the EU Savings Directive.

I hope you enjoy this edition. We continue to value your feedback and suggestionson topics for future editions. Copies are available from www.pwc.com/banking.

Please contact me if you would like to discuss any of these issues in more detail.

John HitchinsUK Banking Leader020 7804 [email protected]

MARCH 2007

The member firms of the PricewaterhouseCoopers network (www.pwc.com) provide industry-focused assurance, tax and advisoryservices to build public trust and enhance value for its clients and their stakeholders. More than 130,000 people in 148 countriesshare their thinking, experience and solutions to develop fresh perspectives and practical advice.

(Unless otherwise indicated, “PricewaterhouseCoopers” refers to PricewaterhouseCoopers LLP a limited liability partnershipincorporated in England. PricewaterhouseCoopers LLP is a member firm of PricewaterhouseCoopers International Limited.)

© 2007 PricewaterhouseCoopers LLP. All rights reserved. “PricewaterhouseCoopers” refers to PricewaterhouseCoopers LLP(a limited liability partnership in the United Kingdom) or, as the context requires, other member firms of PricewaterhouseCoopersInternational Limited, each of which is a separate and independent legal entity.

Designed by Court Three 0307.

Precious Plastic 2007 –Consumer credit in the UK

Only two years ago headlines were made when the total level ofindebtedness of the UK population reached £1 trillion. Despitecontinuing concerns, total household borrowing has continued toincrease, reaching a total of £1.2 trillion by the end of June 2006.

By Richard Thompson

What’s happening in theconsumer credit market?

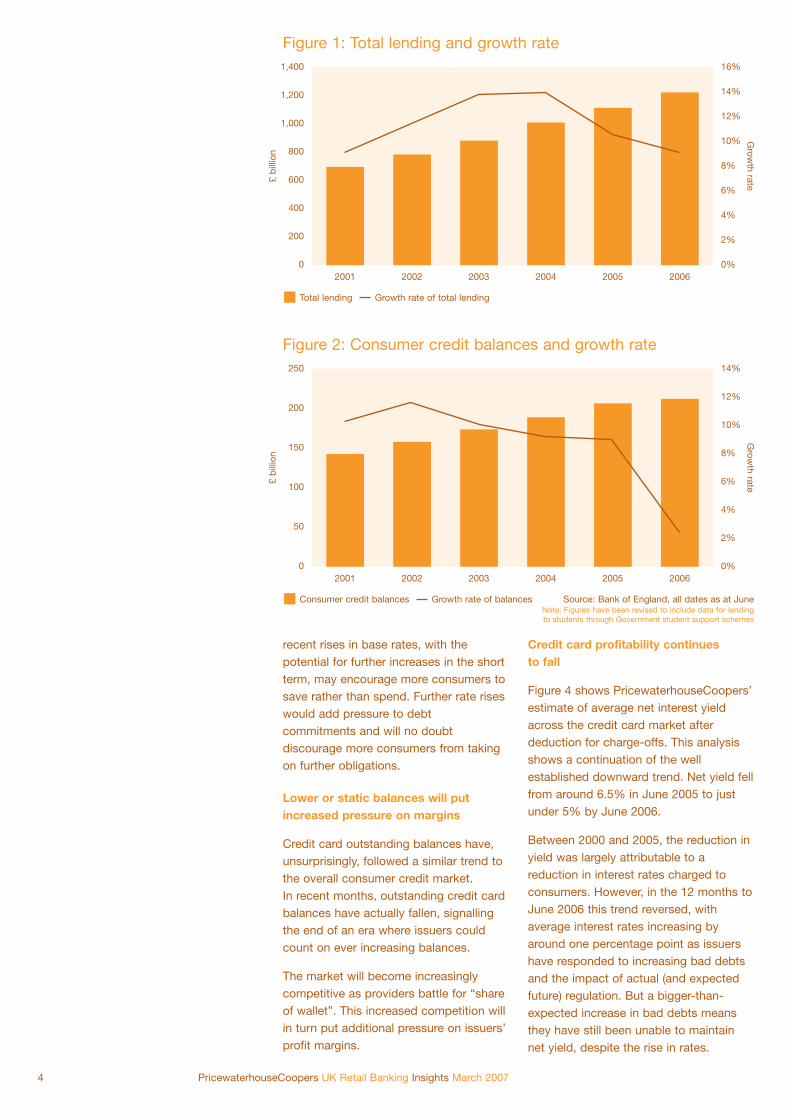

Total lending continues to increase

Only two years ago headlines were madewhen the total level of indebtedness ofthe UK population reached £1 trillion.Despite continuing concerns, totalhousehold borrowing has continued toincrease, reaching a total of £1.2 trillionby the end of June 2006.

However, over the past couple of yearsthe overall rate of growth has beendeclining. Recently this has been drivenby a slowdown in unsecured lendinggrowth (i.e. credit and store cards,personal loans and overdrafts) from 9.0%in 2005 to just over 2% in 2006.

Growth in consumer credit balances isclearly stalling

Last year we predicted a significantslowdown in growth rates of consumercredit balances, and they are nowfollowing a very different trend to the fiveprevious years, as shown in Figure 2overleaf. From 2000 to 2005 the averageannual growth rate was 10%, and it neverfell below 9% in any year. However, in the12 months to June 2006 there was asignificant slow down, with consumercredit balances growing by only 2.4%.Have we now reached a natural ceiling forconsumer credit balances?

It appears that the slow down is due toreduced demand rather than reducedsupply. Although increasing bad debtshave made lenders more cautious,extensive media coverage highlighting theproblems of over-indebtedness appearsto be influencing consumers’ willingnessto increase borrowings. In addition,

recent rises in base rates, with thepotential for further increases in the shortterm, may encourage more consumers tosave rather than spend. Further rate riseswould add pressure to debtcommitments and will no doubtdiscourage more consumers from takingon further obligations.

Lower or static balances will putincreased pressure on margins

Credit card outstanding balances have,unsurprisingly, followed a similar trend tothe overall consumer credit market.In recent months, outstanding credit cardbalances have actually fallen, signallingthe end of an era where issuers couldcount on ever increasing balances.

The market will become increasinglycompetitive as providers battle for “shareof wallet”. This increased competition will in turn put additional pressure on issuers’profit margins.

Credit card profitability continuesto fall

Figure 4 shows PricewaterhouseCoopers’estimate of average net interest yieldacross the credit card market afterdeduction for charge-offs. This analysisshows a continuation of the wellestablished downward trend. Net yield fellfrom around 6.5% in June 2005 to justunder 5% by June 2006.

Between 2000 and 2005, the reduction inyield was largely attributable to areduction in interest rates charged toconsumers. However, in the 12 months toJune 2006 this trend reversed, withaverage interest rates increasing byaround one percentage point as issuershave responded to increasing bad debtsand the impact of actual (and expectedfuture) regulation. But a bigger-than-expected increase in bad debts meansthey have still been unable to maintainnet yield, despite the rise in rates.

4 PricewaterhouseCoopers UK Retail Banking Insights March 2007

Figure 1: Total lending and growth rate

Total lending Growth rate of total lending

2001 2002 2003 2004 2005 2006£

bill

ion

Grow

th rate

1,400 16%

14%

12%

10%

8%

6%

4%

2%

0%

1,200

1,000

800

600

400

200

0

Figure 2: Consumer credit balances and growth rate

Consumer credit balances Growth rate of balances Source: Bank of England, all dates as at JuneNote: Figures have been revised to include data for lendingto students through Government student support schemes

2001 2002 2003 2004 2005 2006

£ b

illio

n

Grow

th rate

250 14%

12%

10%

8%

6%

4%

2%

0%

200

150

100

50

0

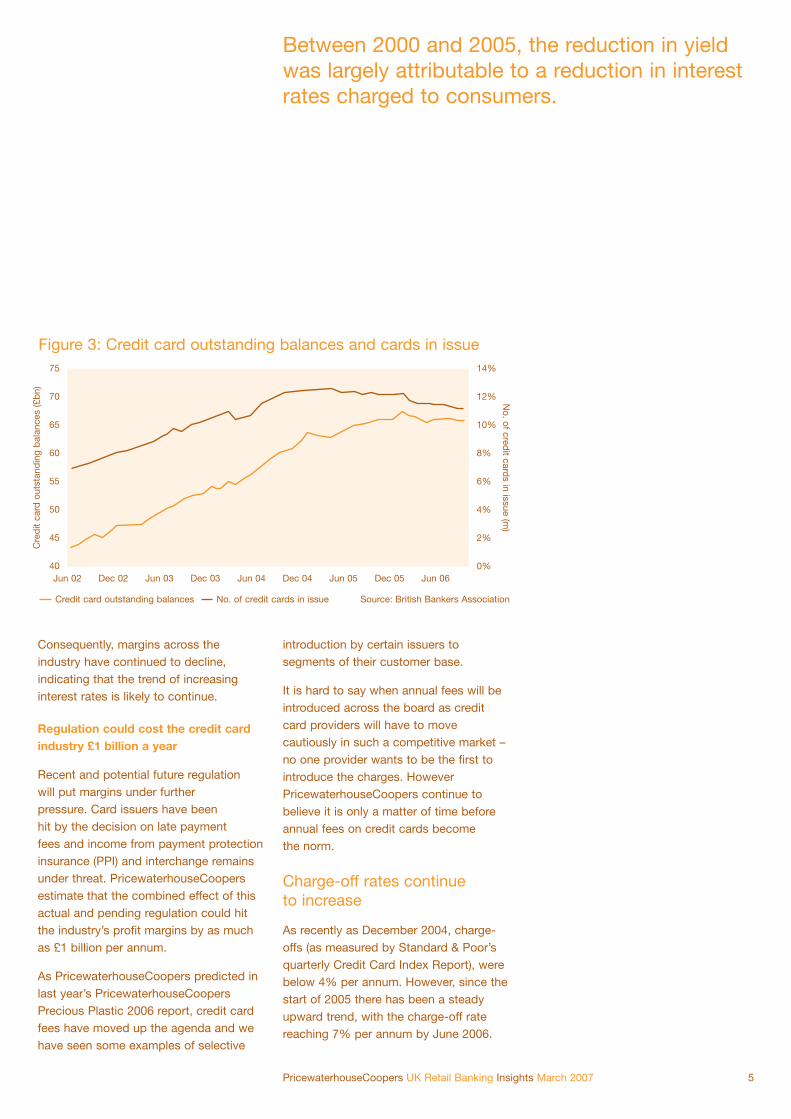

Between 2000 and 2005, the reduction in yieldwas largely attributable to a reduction in interestrates charged to consumers.

Consequently, margins across theindustry have continued to decline,indicating that the trend of increasinginterest rates is likely to continue.

Regulation could cost the credit cardindustry £1 billion a year

Recent and potential future regulationwill put margins under furtherpressure. Card issuers have beenhit by the decision on late paymentfees and income from payment protectioninsurance (PPI) and interchange remainsunder threat. PricewaterhouseCoopersestimate that the combined effect of thisactual and pending regulation could hitthe industry’s profit margins by as muchas £1 billion per annum.

As PricewaterhouseCoopers predicted inlast year’s PricewaterhouseCoopersPrecious Plastic 2006 report, credit cardfees have moved up the agenda and wehave seen some examples of selective

introduction by certain issuers tosegments of their customer base.

It is hard to say when annual fees will beintroduced across the board as creditcard providers will have to movecautiously in such a competitive market –no one provider wants to be the first tointroduce the charges. HoweverPricewaterhouseCoopers continue tobelieve it is only a matter of time beforeannual fees on credit cards becomethe norm.

Charge-off rates continueto increase

As recently as December 2004, charge-offs (as measured by Standard & Poor’squarterly Credit Card Index Report), werebelow 4% per annum. However, since thestart of 2005 there has been a steady upward trend, with the charge-off ratereaching 7% per annum by June 2006.

PricewaterhouseCoopers UK Retail Banking Insights March 2007 5

Figure 3: Credit card outstanding balances and cards in issue

Credit card outstanding balances No. of credit cards in issue Source: British Bankers Association

Jun 02 Dec 02 Jun 03 Dec 03 Jun 04 Dec 04 Jun 05 Dec 05 Jun 06

Cre

dit

card

out

stan

din

g b

alan

ces

(£b

n)

No. of cred

it cards in issue (m

)

75 14%

12%

10%

8%

6%

4%

2%

0%

70

65

60

55

50

45

40

The increase in Individual VoluntaryArrangements (IVAs) has been welldocumented, with someone now enteringa personal insolvency every minute ofevery working day. In the last three years,PricewaterhouseCoopers estimate theproportion of charge-offs due toinsolvencies has increased from around20% to 30%.

IVAs are beginning to be used as ameans of avoiding interest payments

PricewaterhouseCoopers has visibilityover a large proportion of the personalinsolvency market and we are now seeinga new trend – a growing proportion ofindividuals seem to be using IVAs as aneasy option to avoid interest payments.This group appears to have the capacityto repay the capital over a period oftime not dissimilar to the original termof their indebtedness, as witnessed bytheir proposed payment schedule underthe IVA.

Will personal insolvencies continueto increase?

When considering likely future trends itshould be borne in mind that externalinfluences, such as the introduction ofthe Simplified Individual VoluntaryArrangements (SIVA), interest rateincreases, and creditor attitudes couldhave a major bearing. On the one hand,the introduction of the SIVA could resultin a significant structural shift in themarket. On the other hand, creditor banksmay not allow the numbers to increase inthis way and could harden their stance onacceptable levels of dividend.

Regulation continues to be amajor issue for lenders

Store cards resolved, but unlikely tohave a major impact on the market

In March 2006, the CompetitionCommission (“CC”) published its finalreport on the store cards market andimposed a number of remedies.

Consumer groups responded that themeasures did not go far enough.However, It should be remembered thatthe average outstanding balance on astore card is just £150 and whilst therewill be a small proportion that rely tooheavily on store card credit the majorityof store card users do not. The impact ofany reduction in APR as a result of theremedies is therefore not meaningful to avery large proportion of store card users.As default rates across the industrycontinue to rise, institutions will be underpressure to reduce acceptance rates,particularly if the remedies in effect act asa price cap. This could potentially lead toa segment of the population unable toobtain store card credit and it is thissegment that is likely to have limitedaccess to other mainstream credit.

The interchange fee debate goeson and on

In September 2005, the OFT published adecision in which it determined that theinterchange fees for MasterCarddomestic UK transactions, in effectbetween 1 March 2000 and 18 November2005, violated UK and EU competitionlaw. In June 2006 the Competition

6 PricewaterhouseCoopers UK Retail Banking Insights March 2007

Figure 4: Net interest yield after charge-offs

Source: Standard & Poor’s, Bank of England, PricewaterhouseCoopers analysisNote: The Bank of England have restated their figures, which has changed the calculation from last year

Dec 00 Jun 01 Dec 01 Dec 02Jun 02 Jun 03 Dec 03 Jun 04 Dec 04 Jun 05 Dec 05 Jun 06N

et y

ield

per

cent

age

75

70

65

60

55

50

45

40

The OFT set a threshold for intervention at £12.Any default fee above that level would bepresumed unfair, and would be challengedunless there were “exceptional business factors”.

Appeals Tribunal set aside the OFT’sdecision after the OFT sought towithdraw it voluntarily. The OFT ended itsinvestigation of MasterCard’s pre-18November 2005 (multilateral) interchangefees but said it would continue toinvestigate MasterCard’s post-18November 2005 UK domestic interchangefees, which are now set unilaterally byMasterCard. The OFT is also investigatingVisa’s UK domestic interchange fees.The OFT said “we still believe that theinterchange fee arrangements that arenow in place could infringe competitionlaw and are harmful to consumers”.

Competition authorities in otherjurisdictions, including Australia,have taken a similar line to the OFT.In Australia, card associations haveargued that there is no proof retailershave cut prices to consumers followinga reduction in the interchange fee.

Lenders are likely to be hit by theinvestigation into PPI

In February 2007, the OFT referred themarket for PPI to the CC. The OFT’s initialestimate of the consumer savings thatcould be made by making the marketmore competitive was around £1bn.Changes in PPI arrangements couldresult in shifts in the lending market –with the potential for increases in interestrates as lenders seek to maintain levels ofprofitability. Any increase in unsecured personal loan rates could provide a boostto the second charge market.

The ruling on default fees has almostcertainly led to higher interest rates

In April 2006, the OFT stated that a fairdefault charge should not exceed thelevel of the administrative costs usuallyassociated with a default. It estimatedthat potentially unlawful penalty chargeswere currently in excess of £300 milliona year.

The OFT set a threshold for interventionat £12. Any default fee above thatlevel would be presumed unfair, andwould be challenged unless therewere “exceptional business factors”.Many card issuers stated that they didnot agree with the OFT’s assessment,but they nevertheless agreed to reducetheir charges. The debate has nowmoved on to the overdraft fees.

Overall approach

The consumer credit industryundoubtedly has some of the mostconsistently negative and one-sidedmedia reporting of any industry in the UK.This negative publicity and resultingpolitical pressure are likely to be a driverbehind recent regulatory initiatives.The consequences of continuingregulatory pressure will be lostrevenues and a further increase incompliance costs.

The consumer credit industry providesmajor benefits to consumers and to theeconomy as a whole and these benefitsneed to be properly explained. Regulationremains one of the key issues for theconsumer credit industry.

PricewaterhouseCoopers UK Retail Banking Insights March 2007 7

Contact us

Richard ThompsonPartner, Valuation & StrategyTel: 020 7213 1185Email: [email protected]

Lenders face further scrutiny– the call for fairer practicesWhilst the regulation of mortgages and general insurance hasbeen with us for some time now, the FSA is starting to direct itssearchlight on a number of specific areas with a particularemphasis on fairness. These include affordability in the creditsales process, the application of mortgage exit administrationfees and the sale of related payment protection insurance (PPI)to name a few.

By David Morey

This article looks at these three areas ofthe FSA’s current agenda. In those caseswhere Enforcement action has led to theissuance of a Final Notice, notably in thePPI arena, the FSA has been very clearas to the emphasis placed on Principles 6and 7, often with equal weight onPrinciples 2 and/or 3:

• Principle 6 – …pay due regard tointerests of customers and treatthem fairly

• Principle 7 – …information needsof clients, and communicateinformation…which is clear, fair andnot misleading

• Principle 2 – …due skill, careand diligence

• Principle 3 – …organise and controlaffairs responsibly and effectively…

Affordability – what’sthe issue?

The FSA’s recent commentary on theresults of its review of mortgageaffordability processes highlighted someconcerns about reliance on gross incomeand how this relates to the assessment ofaffordability. In the intermediary sector,the FSA’s thematic work has alsoidentified failings relating to affordabilityin the sale of, and advice on,self-certification mortgages and whetherborrowers were being encouraged to takeon larger mortgages than their incomewould justify.

Specifically, the FSA is looking for firmsto assess (demonstrably):

• Net income after tax and taking offcosts such as repayment of otherborrowing, maintenance and otherregular outgoings

Where the mortgage extends into retirement,and the borrower’s financial position changes,affordability also means taking account ofa customer’s likely income and expenditurein retirement.

• Whether the borrower can affordthe payments over time, such asat the end of any discount period orwhen rates change (the potentialimpact of possible future increases ininterest rates)

• Whether the borrower can repay thecapital amount (where the loan isinterest-only).

Where the mortgage extends intoretirement, and the borrower’s financialposition changes, affordability also meanstaking account of a customer’s likelyincome and expenditure in retirement.

Responsible lending

Affordability assessment approaches varyacross the industry. Responsible lendingdecisions require checks to be madeconcerning income and outgoings(typically using a combination of incomemultiples and affordability models) whenassessing ability to repay now and intothe future. Also the type of lendingundertaken and the type of borrower(for example, applicants with impaired orlow credit ratings) may require moredetailed assessments to be carried out.

Other (unregulated) lending

Mortgage lending is only part of theaffordability picture. Under the auspicesof Treating Customers Fairly (TCF),affordability assessments are equallyrelevant to other borrowing, includingpersonal loans and credit cards, and anumber of lenders are looking at how

their affordability assessment processesmay need to be strengthened for thesetypes of credit.

In an effort to strengthen existing rules,new Banking Code guidance concerningassessing affordability in relation tounsecured loans (overdrafts and otherborrowing) was issued by the BankingCode Standards Board in April 2006. Anyassessment should now include at leasttwo of the following:

• Income and financial commitments

• Repayment history

• Credit reference agency informationand past repayment history

• Credit scoring.

It is also worth noting that the Officeof Fair Trading’s recent guidance (‘theOFT Guidance’)(1) reinforces the need forfirms to have regard to its earlierguidance on non-status lending andconfirms its intention to consider furtherspecific guidance with regard toirresponsible lending and what thismay mean in different market sectorsand circumstances.

Responding to the concerns

The FSA has indicated that as part of itsretail agenda it will continue to focus onquality of advice processes in themortgage market. In responding to theseconcerns, firms will wish to consider howthe results of the FSA’s findings impacteach of their lending businesses:

PricewaterhouseCoopers UK Retail Banking Insights March 2007 9

Source:(1) Unfair relationships – Enforcement action underPart 8 of the Enterprise Act 2002 OFT guidance,December 2006

The FSA expects firms to “consider whethertheir terms might be unfair and provide evidenceof how decisions to increase MEAFs weretaken”. The FSA’s Statement of good practiceon mortgage exit administration fees (January2007) sets out what lenders should be doing.

• How extensive is the affordabilityprocess; does the advice processinclude an assessment of incomeand identifiable expenditure;anticipated changes in personalcircumstances (income/expenditurecomposition); impact of interest ratechanges and possible future increasesin interest rates?

• How do you deal with mortgagesextending into retirement?

• What steps are taken to ensure thatunderwriting processes (includingincome multiples and affordabilitymodels) reflect the differentcharacteristics and risk profilesof customers in different marketsectors (for example, sub-prime;non-conforming)?

• Have you carried out a recentassessment of your approach toaffordability (including affordabilitydecisioning models) to meet theregulatory as well as commercialdrivers impacting the business?

• What steps are taken concerning theassessment of the customer’s abilityto repay where ‘enhanced’ incomemultiples are used (and where the firmmay have insufficient, or outdated, datato measure the potential impact/risksof default)?

• What MI do you typically have tofacilitate the identification ofaffordability issues on a timely basis(for example, the performance of loanswhere ‘enhanced’ multiples have been

applied; at the end of any discountperiod; the level of arrears andrepossessions; lending introduced byintermediaries)?

Mortgage Exit AdministrationFees – a fair deal?

As with certain other costs associatedwith post sale credit activity, such asoverdraft fees and default charges,mortgage exit administration fees(MEAFs) are being challenged.Higher exit fees are receiving attention ontwo fronts – firstly in relation to aborrower’s understanding of the quantumof such charges when the mortgage wastaken out, and secondly in relation to theactual cost of administering the exit.

The key issues

The FSA is looking for firms to act fairly(charges should not be excessive,disproportionate or an unfair barrier torepaying a mortgage or switching lender)and consider:

• Variation clauses in existing contractsthat allow changes which the customerhas not agreed to in advance and thatdo not require the customer’sagreement (e.g. an increase in theMEAF amount)

• Variations only where there is a “validreason” (e.g. increases in chargesproportionate to any increase in theassociated cost of the administrationservices which a lender provides whencustomers exit a mortgage)

10 PricewaterhouseCoopers UK Retail Banking Insights March 2007

• Transparency: mortgage contractsshould be clear in explaining, in plainand intelligible language, which costswill be charged, and the basis of anyincreases, and at what point in the lifeof the contract.

Setting charges – what shouldfirm’s consider?

The FSA expects firms to “considerwhether their terms might be unfair andprovide evidence of how decisions toincrease MEAFs were taken”. The FSA’sStatement of good practice on mortgageexit administration fees (January 2007)sets out what lenders should be doing.

In setting charges, firms are likely to needto consider:

• The quantum of actual underlyingcosts involved and passed onto theborrower – the FSA is looking for firmsto demonstrably assess the actualcosts incurred and show how thecharge is derived and varied (the FSAhas indicated that such costs couldlegitimately include deed release fees,Land Registry charges, staff processingcosts and a reasonable proportion ofgeneral overheads)

• Analysing their mortgage products toidentify features, such as exit charges,that might be seen as disproportionateor an unfair barrier to changing productor lender (the FSA has indicated thatfirms are likely to be in breach ofPrinciple 6 where terms are known tobe unfair)

• Providing information at the point-of-sale about relevant costs (up-front andongoing charges) in order thatborrowers can understand the extent towhich exit charges are a feature of themortgage and the circumstances inwhich they become payable

• Providing information after thepoint-of-sale to help borrowers managetheir finances effectively, having regardto the full facts regarding likely costs.

Whilst the FSA has no remit to requireretrospective action under the UnfairTerms in Consumer ContractsRegulations 1999 (which it is currentlyusing when assessing the fairness ofMEAFs), a number of lenders will haveto refund elements of MEAFs wherecustomers have a valid complaint.

One of the principal changes of theConsumer Credit Act (“CCA”) 2006,which amends the CCA 1974, is theintroduction of the concept of an “unfairrelationship”. Under the Act, an unfairrelationship may arise by virtue of theterms of the credit agreement or anyrelated agreement (for example, alteringthe terms of a contract “unilaterally”without a valid reason and to thedetriment of the consumer, includingprice variation clauses if these are notrecognised as ‘core terms’ under theUnfair Terms in Consumer ContractsRegulations 1999). Whilst the unfairrelationship provisions do not apply toregulated mortgage contracts, theprinciples of fairness referred to inthe OFT Guidance can be readilymapped across.

PricewaterhouseCoopers UK Retail Banking Insights March 2007 11

Going forward, it looks as though thefocus on, and the consequential drive forcomparability, of MEAFs across theindustry will drive down those that arearguably on the high side.

Payment ProtectionInsurance – the good, the badand the ugly?

The sale of PPI has been a key area ofregulatory focus by the FSA during 2005and 2006; it will continue to attractregulatory scrutiny during 2007. The FSAhas been assessing how firms sell PPIagainst standards set out in the ICOBrules, and in the context of TreatingCustomers Fairly. In reality, most of thesales process issues identified by theFSA fall under the TCF umbrella.

Regulatory scrutiny

As a result of regulatory scrutiny,distributors and product providers havehad to respond to the ongoing challengesin a number of areas:

• Reassessment of the basis adoptedfor selling PPI (advised and non-advised sales)

• Elimination of risks associated withselling to ineligible customers

• Redesign of PPI suitability assessmentprocesses

• Redesign of core marketing andcustomer insurance documents

• Focussing on what TCF means forPPI distribution

• Design of new product propositions(alternative products, unbundling etc.).

What does all this meanfor businesses?

In practice this means that today’s sellingpractices are very different from 18months ago, as many lenders haveundertaken extensive work to improveprocesses. At its simplest, scrutiny bythe FSA has meant the adoption of newsales processes with new technologies(for example, automated suitabilityassessment models). This is likely to haverequired the roll-out of new training, newstaff remuneration arrangements, and theintroduction of new controls and MIreporting models.

In addition, some distributors havedecided that it is appropriate in theinterests of customer care and fairness,to identify cases where today’s standardssuggest that customers may not havebeen treated fairly and make these goodthrough compensation.

However, some distributors have hadspecific and extensive FSA Enforcement-driven remedial activity to handle;typically this revolves around bothprospective change and retrospectiveaction on previously sold PPI.

The FSA’s scrutiny of the PPI marketcontinues into 2007, with additional firmsbeing identified as part of both specific

12 PricewaterhouseCoopers UK Retail Banking Insights March 2007

Even for long-established product offerings,it is clear that nothing stays still. Aside fromregulation by the FSA, the market still needs torespond to the challenges of competitioninvestigation into the PPI market.

enquiry and PPI mystery shopping workto be undertaken by the FSA.

Some lenders have already engagedextensively with their providers as to howPPI products are to be designed forparticular target customers and whatalternatives are available. For others, thisdialogue is still ‘early days’.

Conclusion

What does this all mean? Even forlong-established product offerings, it isclear that nothing stays still. Aside fromregulation by the FSA, the market stillneeds to respond to the challengesof competition investigation into thePPI market.

As a minimum, it means managementteams (business unit leaders andcompliance) need to be alert to emergingand identified areas of regulatory focus –responding pro-actively to issues as theyarise will enable firms to stay in the game.

But is this sufficient? Maybe a betterstrategy is to actively engage in thefairness debate, identify opportunity fromit and seek to create space between youand your peers.

Contact us

David MoreyDirector, Regulatory PracticeTel: 020 7804 2684Email: [email protected]

PricewaterhouseCoopers UK Retail Banking Insights March 2007 13

Building societies ata crossroad

Mutuality offers building societies a valuable cost advantage inthe increasingly competitive savings and mortgage markets.Yet, rising funding costs and continuing margin erosion areleading to ever increasing pressure for consolidation,diversification and strategic re-orientation.

By Nick Page and Stuart Last

A decade ago, the building societymovement appeared to be at risk ofpassing into history as the mutualstatus of one society after another fellbefore an onslaught of takeovers,carpetbaggers and pressure frommembers. Yet following charitableassignment and other rule changes at theend of the 1990s, the remaining societieshave not just survived but prospered,increasing turnover in the wake of soaringmortgage demand and building firmsupport for mutuality among members.

Building societies lent £52.8 billion in2006, their best year yet. The total assetsof the sector’s 60 societies reached £305billion at the end of November 2006(mortgage assets were £200 billion,largely funded by savings balances of£190 billion). In a concentrated sector, thelargest ten societies hold more than 80%of overall assets. Of these, Nationwide isby far and away the largest, with assetsof some £120 billion.

Benefits of mutuality

The building society movement has beenable to make a commercial virtue of itsmutuality. Mutual ownership means thatsocieties do not have to pay dividends toprivate or institutional shareholders. Thesavings can be passed on to existing andprospective members. The net interestmargin (difference between the interestpaid to savers and charged to borrowers)of the sector’s top ten societies averaged1.03% at the 2005/2006 year-end,compared to around 2% for most banks.

As a result, building societies consistentlyfeature in the best mortgage buyingtables. In December 2006, for example,building societies topped the Times bestrates list for fixed (Derbyshire), flexible(Nationwide) and discount (Dunfermline).Recent press comment has praisedbuilding societies for not takingadvantage of the recent interest rate riseto increase spreads.

Building societies cannot afford to rest ontheir laurels at a time when internetcomparisons, aggressive cost cutting andmarketing by the banks and the ever increasingease of account transfer are intensifying thepressure of competition.

Mutuality can also prove to be a sourceof assurance and goodwill for customers.One sign of the trust that is such afeature of the building society ‘brand’ isthat they have attracted the bulk ofCash Child Trust Funds. Added tothis is customers’ identification withinstitutions that still predominantly servea particular home town or region and areoften important local employers in theirown right.

Margin pressure

However, building societies cannot affordto rest on their laurels at a time wheninternet comparisons, aggressive costcutting and marketing by the banks andthe ever increasing ease of accounttransfer are intensifying the pressure ofcompetition. Even with the potential rateadvantages of mutuality, buildingsocieties’ share of the savings market hasremained virtually unchanged (19.3% in2001 and 19.2% in the year to October2006). Their share of net mortgagelending actually fell from 26.6% in 2000to 19.2% in 2005, while their share ofgross mortgage advances declined from16.2% in 2001 to 15.6% in the year toOctober 2006.

The pressure on market share iscompounded by continued marginerosion. Funding costs are rising associeties find themselves no longer ableto rely on their deposits to finance theirlending. The proportion of fundingcoming from wholesale sources(syndicated loans, covered bonds andother non-retail deposit finance) in thesector was just 9.4% in 2001. By 2005,it had risen to 18.3%. Compliance costs

have also increased in the wake of arange of new demands including forsome the move to International FinancialReporting Standards and a growingregulatory burden (for example therequirements relating to ‘TreatingCustomers Fairly’).

On the income side, fierce marketcompetition means that societies have tooffer mortgage products at ever keenerand less profitable prices. The proportionof loan balances at standard variable ratesfell from 40% in 2001 to 23.3% in the finalquarter of 2005 as more customers optedfor fixed, capped and discounted variablerates. The rapid rise in house prices andthe need to offer ever more attractivedeals has also increased the default risk.In particular, the proportion of totaladvances exceeding three times singleincome and two and a half times jointincome rose from 36.1% in 2001 to54.3% in the final quarter of 2005.

Increases in base rates and their potentialimpact on mortgage demand, houseprices and defaults can only heighten thepressure on businesses whose revenuesare still largely dependent on mortgagelending. If mortgage margins continue toerode and/or there are any major ructionsin the housing market, there will be fewalternative sources of income to fall backon in a sector where only 40% ofinstitutions offer unsecured loans, only30% offer credit cards and less than 25%offer personal pensions, unit trusts orinvestment trusts. Even among theleading societies, fees are barely 25% ofrevenue compared to more than 30% ina comparable mid-sized bank.

PricewaterhouseCoopers UK Retail Banking Insights March 2007 15

Societies could source specialist products fromother mutuals as part of the development of auniversal building society brand. Some smallersocieties could also save costs by merging theirback offices or outsourcing operations to largerand better-resourced counterparts, whileretaining their local character and customer ties.

Strategic options

Cost control will clearly be critical in thesector’s ability to maintain itscompetitiveness. The Coventry BuildingSociety, the fifth largest, is one societyleading the way. Although branches are acritical part of the society’s brand andservice strategies, it has been ableto develop highly cost-effectivecontact centre and online delivery.Its cost/income ratio was 50.65% in2005, compared to an average for the topten of 59.68%.

Across the movement, the pressure onmargins is fuelling a growing drivetowards consolidation, following severalyears of relative inactivity. If managedwell, mergers can enable societies toenhance their product range and cutrunning costs through back-officeconsolidation and the closure of branchesin areas where there are overlaps. Largerorganisations could also attract cheaperwholesale funding.

The deals announced in 2006 includedNationwide’s planned merger with thePortman, the number three in the sector,following the latter’s earlier merger withthe Lambeth. Commenting on thedecision to merge with the Nationwide,Robert Sharpe, Chief Executive ofthe Portman, said that ‘if buildingsocieties are to continue to competesuccessfully with the retail banks, theyneed to enjoy comparable economiesof scale’. Others transactions includethe recently completed mergers of

regional competitors the Universaland the Newcastle, and the Leeds andthe Mercantile.

More societies, smaller ones in particular,may find themselves under pressure tomerge as competition, regulatorydemands and the difficulties of sustainingviable margins intensify. While thesmaller societies will continue to enjoythe loyalty of their existing members, theymay find that lack of scale makes itharder to control running costs and offersufficiently competitive rates to bring innew customers.

Running in parallel with the pressure onscale and expenses is the growingimpetus for product and servicediversification. A number of societies arealready seeking to carve out specialistniches that build on their lendingexpertise or develop more personalisedand sophisticated business lines thatleverage their trusted long-termrelationships with members.

An example is the Chelsea BuildingSociety, the sixth largest, which isdeveloping a strongly marketed presencein near-prime lending. In turn, theSkipton Building Society, the seventhlargest, now offers services ranging fromshare dealing to pension and inheritanceplanning. The wider Skipton Group nowbrings together 17 subsidiariesthat include market intelligence,conveyancing services and mortgageadministration outsourcing.

16 PricewaterhouseCoopers UK Retail Banking Insights March 2007

Growing openings

These competitive strategies could openup further opportunities for partnershipand product enhancement. Societiescould source specialist products fromother mutuals as part of the developmentof a universal building society brand.Some smaller societies could also savecosts by merging their back offices oroutsourcing operations to larger andbetter-resourced counterparts, whileretaining their local character andcustomer ties. There might even be astrong rationale for forging alliances withone of the larger former building societiessuch as the Alliance & Leicester.This could provide access to theexpertise and infrastructure of a sizeablebank, while still being able to sustainsome of the best elements of the buildingsociety ethos.

What is clear is that standing still is not aviable option. Margins in core businessesare likely to continue to erode. Althoughthe full impact of the latest base rate riseswill take some time to feed into themarket, it is apparent that the low-interestenvironment that helped fan themortgage lending boom is now a thing ofthe past. The building society movementis in a strong position to build on the rateand relationship benefits of its mutuality.However, the movement will need to bothsharpen its competitive edge throughmore efficient and cost-effective deliveryand also broaden its expertise andproduct range to attract and retain anincreasingly demanding customer base.

Contact us

Nick PagePartner, Transaction Services,Financial ServicesTel: 020 7213 1442Email: [email protected]

Stuart LastManager, Transaction Services,Financial ServicesTel: 020 7804 5288Email: [email protected]

PricewaterhouseCoopers UK Retail Banking Insights March 2007 17

Risk Appetite – The StartingPoint for the ‘Use Test’

Have the rules really changed for retail financial services in howthey manage their business? This article explores the foundationsfor passing the Use Test under Basel II.

By Tim Brooke and Richard Barfield

As firms direct their Basel II project teamstowards Pillars 2 and 3 away from thefocus on Pillar 1 and the subsequentwaiver application process, the topic thatnow seems to be top of the agenda ishow to demonstrate and embed ‘use’.

Following the significant volume of workunder Pillar 1, we are seeing many firmsstruggle with moving from a rathertechnical world confined to a smallnumber of knowledgeable staff, the Baselprogramme group, into the ‘Business asUsual’ environment, where decisionsneed to be taken in the context of theirimpact on risk and capital.

We are all acutely aware of the emphasisthat the regulator places on firms beingable to demonstrate that they have strongrisk management capabilities at all levels.The Use Test is one tangiblemanifestation of this, along with theeffective operation of the process

described in the firm’s ICAAP. Recentcommunications from the FSA on Basel IItake the opportunity to re-emphasise theimportance of “Use Test” evidence in theassessment process.

Testing the Use Test

So what does “use” mean in practiceand how will the regulator assesscompliance? This is one of the moreimportant issues facing Boards of retailfinancial institutions.

The starting point for applying andembedding use rests with the Board’sprocesses for determining its strategy.The annual round of discussion anddebate that most firms undertake todetermine and refine their longer termgoals should allow a clear opportunity toplace and decisions in the context of riskand document capital. A clear definitionof risk appetite is at the heart ofthis debate.

Risk appetite can mean different things todifferent organisations. A simple definition couldbe the amount of risk the firm is willing to take inthe pursuit of the execution of its strategy andbalancing the expectations and constraints ofthe investors, rating agencies and regulators.

Firms would argue that this is somethingthat the Board and executivemanagement perform routinely but thequestion still remains as to how well therisk and capital criteria for businessdecisions are evidenced.

Risk appetite can mean different things todifferent organisations. A simple definitioncould be the amount of risk the firm iswilling to take in the pursuit of theexecution of its strategy and balancingthe expectations and constraints of theinvestors, rating agencies and regulators.Risk appetite is a critical consideration fora firm’s overall strategy.

It is not the intention here to delve intothe detailed mechanics of risk appetitemeasurement and the nuances that areunique to individual firms’ approaches,but it should be clear that risk appetiteprovides the foundation for the Use Testunder Basel II. Given that the FSA’sstated intention is to take a top-downperspective during its Pillar 2assessments, it makes a lot of sense forfirms to have their risk appetites clearlyarticulated and appropriately measured.

Risk sensitive decisions

It’s worth reminding ourselves that BaselII can provide firms with a risk-sensitiveframework to analyse the risk capitaldynamics of different strategies andtactics. This allows the flexing of capitalusage, both current and anticipated, andfor the Board to decide how much risk towhich it is willing to commit the firm. Theagreed upon strategy is then a reflectionof the firm’s risk appetite, to which theBoard can assign a risk capital measure.

At the conclusion of the strategy processthe firm can have a perspective on therisk capital required and where its riskcapital is being deployed. Thisinformation is vital to allow the nextphase of the implementation ofrisk-based decision-making: theallocation of capital to business unitsand/or initiatives, and the setting ofoperating limits and hurdle rates.These affect routine decision-making inconnection with products, operationsand markets.

The use of return on risk adjusted capital,a tool that many firms use, directly linksthe management process to Basel Pillar 2requirements and the firm’s risk appetite.If the decision or activity uses capitalbeyond the plan or that which isavailable, the Board can decide eitherto relax its risk appetite, or to re-evaluateits capital resources or re-balancerisk profile.

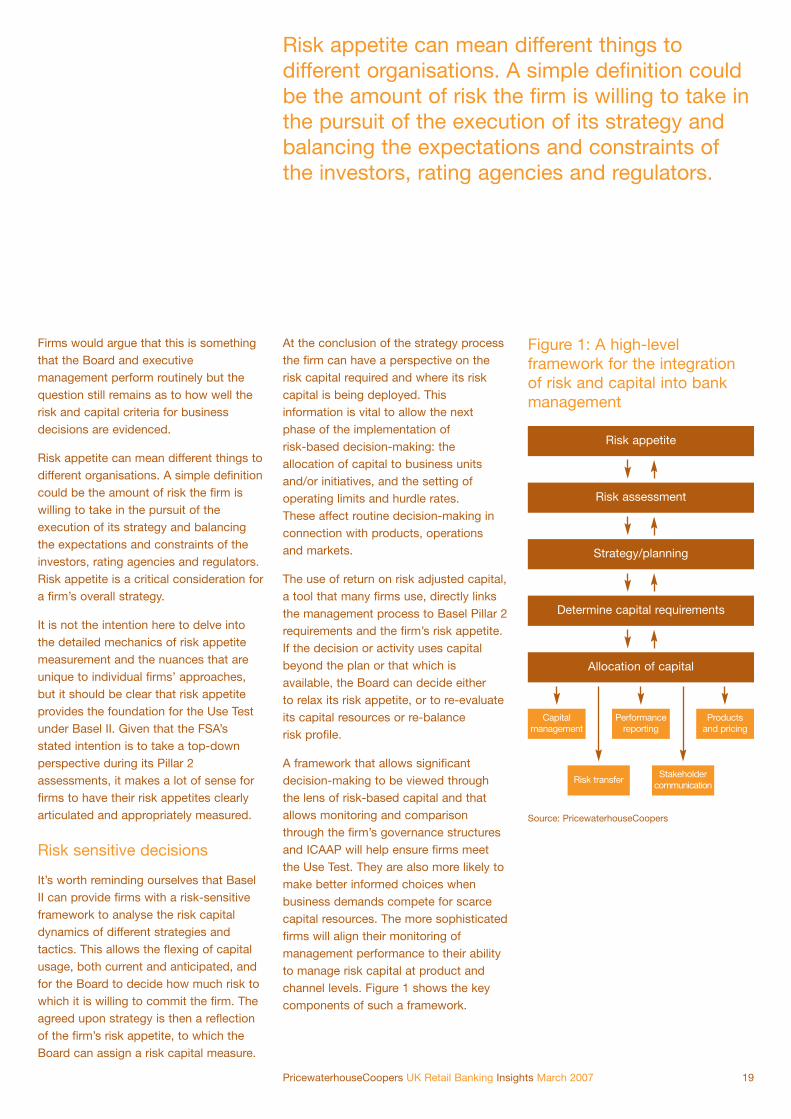

A framework that allows significantdecision-making to be viewed throughthe lens of risk-based capital and thatallows monitoring and comparisonthrough the firm’s governance structuresand ICAAP will help ensure firms meetthe Use Test. They are also more likely tomake better informed choices whenbusiness demands compete for scarcecapital resources. The more sophisticatedfirms will align their monitoring ofmanagement performance to their abilityto manage risk capital at product andchannel levels. Figure 1 shows the keycomponents of such a framework.

PricewaterhouseCoopers UK Retail Banking Insights March 2007 19

Figure 1: A high-levelframework for the integrationof risk and capital into bankmanagement

Risk appetite

Risk assessment

Strategy/planning

Determine capital requirements

Allocation of capital

Capitalmanagement

Risk transferStakeholder

communication

Performancereporting

Productsand pricing

Source: PricewaterhouseCoopers

Business as usual

Other challenges firms face as theybegin to refine their Pillar 2 processesand embed them within the organisationrelate to the level of understanding ofrisk-based decision-making within thebusiness. Basel project team membersare increasingly becoming coaches andeducators as they transfer the knowledgethat has been concentrated in theBasel programme to their businesscolleagues. 2007 will see the real workbegin as firms get to grips with using thenew information that Basel has createdand for some a major redesign of internalprocesses may be required. For otherretail banks this may not necessarilyrequire root and branch change; for a fewit will be more of an alignment of effectiveexisting practices to the language andprinciples of Basel II. For all lenders,though, the Use Test should be top ofthe agenda.

Contact us

Tim BrookeDirector, Risk Assurance Services (North)Tel: 0113 289 4008Email: [email protected]

Richard BarfieldDirector, Risk and Capital AdvisoryServices (London)Tel: 020 7804 6658Email: [email protected]

20 PricewaterhouseCoopers UK Retail Banking Insights March 2007

EU Savings Directive –first year UK survey In the January 2006 edition of this Newsletter, we discussed theimplications of the EU Savings Directive (EUSD) which came intoforce in 2005. The broad aim of the EUSD is to ensure that EUindividuals pay appropriate tax on their cross-border savingsincome, and its approach of requiring banks to pass customerinformation to relevant tax authorities represents one of the EU’srare forays into the direct taxation field.

By David Frood

EU member states are of courseresponsible for setting their own taxpolicies but the Directive is based on thesubsidiarity principle, which permits theEU to intervene when action to preventperceived market distortions – in thiscase, distortions resulting from identifiedcross-border tax evasion – is bestachieved at community level.

Its final shape as a reporting regime isvery different from that envisaged when itwas first proposed as a solution to theproblem of cross-border tax evasionwithin the EU – a problem which hadgrown, ironically, partly from the verysuccess in removing barriers to themovement of capital across EU bordersin pursuit of a single internal market.

The UK played a key role in formulatingEU thinking about the Directive, andconsulted widely with businesses inframing the approach to Directiveimplementation in the UK. Given this and

the importance of the UK’sfinancial sector within the EU,PricewaterhouseCoopers undertooka survey of the actual experience in theUK of the first year of the Directive.The findings of this survey revealed manypoints of practical significance to financialsector organisations emerging from theirexperience, and raised some importantquestions about the scope and shapeof the Directive.

The survey was carried out onlinein September 2006 and was aimedat UK organisations required to fileEUSD reports (‘paying agents’).Participants responded to a series ofquestions on their experience of theEUSD, any problems or concerns theyhad identified and their views on futuredevelopments for the Directive. Fifty sixorganisations participated in the survey,representing about 10% of the UKpaying agent population.

Imag

e co

urte

sy o

f A

idas

Zub

koni

s

It will be some time before information isavailable to measure the success of theEUSD in achieving its objectives – there iscertainly a great deal of data being generatedand exchanged.

Key Findings

The key findings of the survey were that:

1. The underlying aim of the Directivewas generally accepted byrespondents. However, the Directivewas regarded more as a political thanas a practical measure. The Directivewas seen as having manyinconsistencies – vague definitions,surprising gaps in its scope, yet alsoas overly prescriptive in parts – whichdid not make it easy to understand orcomply with. Respondents alsoexpressed considerable scepticismabout its likely effectiveness withalmost half of survey respondentssaying that they do not think that theDirective is fit for purpose.

2. Although the cost of implementationvaried widely, many respondentsfound preparing for the Directive wasexpensive, particularly from a systemsperspective. In a large minority ofcases the cost ran into hundreds ofthousands, or millions (and in twocases, tens of millions) of pounds, alevel which considerably exceededthe upper end estimates (of around£350,000 in total per organisation)predicted in the Government’s 2003Regulatory Impact Assessment. Thissignificant cost shift to the financialsector, in practice predominantlybanks, has not been widelyacknowledged by the tax authorities.

3. There was a widespread view that thecost of compliance with the Directivewas disproportionate to the value

gained by tax authorities from thedata reported. As one respondentcommented: “it’s difficult to see howthe hard won numbers could be usedby the overseas tax authority otherthan in a general warning capacity.”This becomes obvious when oneconsiders that UK institutionsreported income on a UK tax yearbasis, not on a foreign tax year basis,meaning that the chance of paymentsreported in the UK actually matchingfigures on overseas tax returns will beextremely remote. Many respondentsfelt a de minimis threshold should beintroduced, to avoid having to reportcompletely trivial amounts. Severalrespondents also expressed the viewthat tax authorities would derivesubstantially all of the benefitsintended if simply the existence of theaccount or income producing assetwas reported, without getting tied upin the numbers, and this would be afar cheaper solution for financialorganisations.

4. Survey respondents reported verylittle impact on customer behaviour inthe run up to the Directive, forexample in terms of account closures.Early speculation about the negativeimpact of the Directive on customerbusiness in the UK seems to haveproved unfounded, although this isnot altogether surprising since the UKdoes not have banking secrecytraditions and would not be the firstlocation of choice for those intent onavoiding disclosure.

22 PricewaterhouseCoopers UK Retail Banking Insights March 2007

5. It was found that, except in the moststraightforward cases, key Directiveterms did not correspond well withexisting data categories. Directiveterms of ‘beneficial ownership’,‘interest payments’ and ‘payingagents’ all carried specialisedmeanings which needed analysing.Data required about customers andproducts, for example residual entitiesand grandfathered bonds, did notmatch data already held, andobtaining information about otherfinancial products, particularly thirdparty funds, was a major challengein practice.

6. Survey respondents generallyfelt that, overall, HM Revenue &Customs (HMRC) implemented theDirective well in the UK through acombination of industry consultation,help visits and the production ofdetailed guidance. However, the factthat that the guidance frequentlychanged – there have been fiveversions of the guidance notesso far – was a source of frustration.Moreover, survey respondents felt thatHMRC could have been bolder inclarifying areas of uncertainty in theDirective, for example the conceptof residual entities.

7. Although HMRC may have had limitedfreedom of manoeuvre in relation tointerpreting Directive concepts, it wascertainly within HMRC’s power tospecify how information was to bereported in the UK, but many surveyrespondents felt that HMRC’s

reporting requirements were too rigid.Several respondents mentioned theirreturns were rejected by HMRC dueto formatting errors, even after testreturns were accepted.

8. Despite the compliance difficultiesmentioned, a large majority ofrespondents were neverthelessconfident that they had managed tofile complete and accurate Directivereports on time.

9. A clear majority of respondents didnot want to see any changes in theshort term to the scope of theDirective, to allow organisations timeto bed down their new processesproperly. Others expressed thedesirability of aligning the scope ofreporting under the existing domesticrules with reporting under theDirective. Unfortunately, thedifferences between these reportingregimes appears to be growing, forexample with Sharia compliantfinance products being brought withinthe scope of domestic reporting butremaining outside Directive reporting.

It will be some time before information isavailable to measure the success of theEUSD in achieving its objectives – there iscertainly a great deal of data beinggenerated and exchanged, but the realtest of success will be whether the EUSDwill actually change taxpayer behaviourby deterring EU individuals fromconcealing their offshore income andassets from the taxman in future.

PricewaterhouseCoopers UK Retail Banking Insights March 2007 23

If you would like a copy of thefull PricewaterhouseCooperssurvey or have any questionsabout the EUSD please contact:

David FroodTax Director, Banking & Capital MarketsTel: 020 7212 5545Email: [email protected]

Michael Andrews-ReadingSenior Manager, Tax InvestigationsTel: 020 7804 4359Email: [email protected]

www.pwc.com