Tax Increment Financing Update - TN Comptroller · PDF fileTax Increment Financing Update...

27

Tax Increment Financing Update Presentation will begin at 12:15 PM Betsy Knotts, Office of General Counsel Kelsie Jones, State Board of Equalization

Transcript of Tax Increment Financing Update - TN Comptroller · PDF fileTax Increment Financing Update...

Tax Increment Financing Update

Presentation will begin at 12:15 PM

Betsy Knotts, Office of General Counsel

Kelsie Jones, State Board of Equalization

Today’s Agenda:

Introduction to Tax Increment Financing (TIF)

Comptroller’s Statutory Duties Related to TIF

Q & A—Partnering with Local Governments

2

3

Basics of Tax Increment Financing

TIF is the act of borrowing

against a future value

In other words, upfront cash to construct a project

4

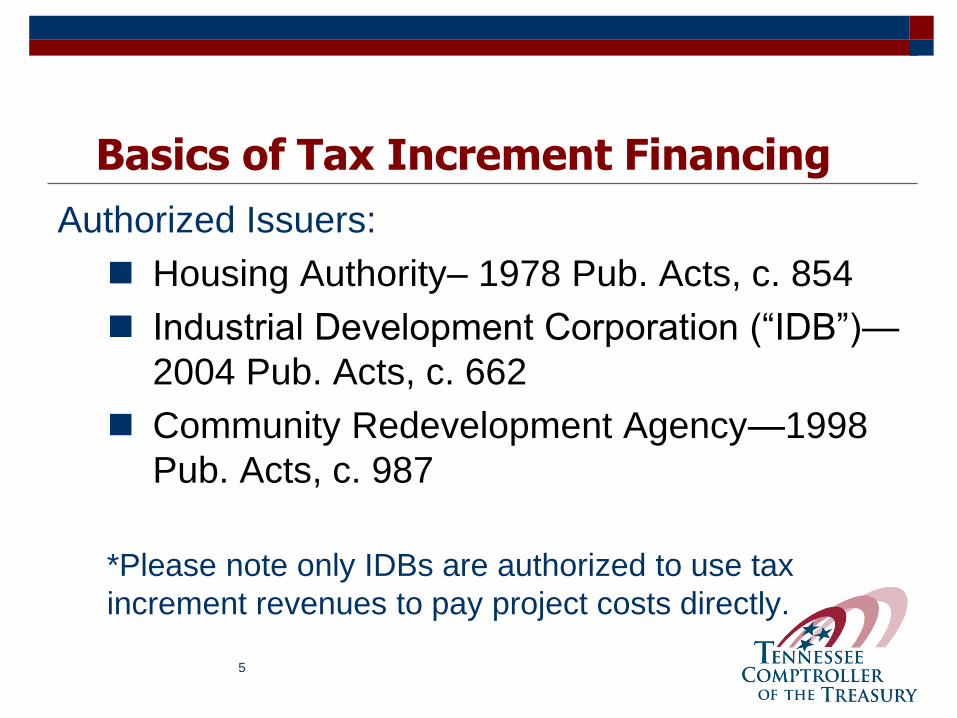

Basics of Tax Increment Financing

Authorized Issuers:

Housing Authority– 1978 Pub. Acts, c. 854

Industrial Development Corporation (“IDB”)—

2004 Pub. Acts, c. 662

Community Redevelopment Agency—1998

Pub. Acts, c. 987

*Please note only IDBs are authorized to use tax

increment revenues to pay project costs directly.

5

Tax Increment Financing in theTennessee Code Annotated (T.C.A.)

1978

T.C.A. § 13-20-202, Housing Authority

2004

T.C.A. § § 7-53-312 and -314, Industrial Dev. Board

2012

T.C.A. § 9-23-101 et seq., TIF Uniformity Act

6

Typical documents in a TIF transaction:

Authorizing Documents

Financing Documents

7

TIF Approval Process

IDB Approves Economic Impact Plan

City Approves the Plan

Formal Creation of Tax Increment Area

Incremental Increases Transferred to TIF Agency

County Approves the Plan

COT and ECD Approve the Extended Plan Term or Project

8

Examples of Financing Documents:

Tax Increment Plan

Economic Impact Plan

Redevelopment Plan

Tax Increment Revenue Note

Development Agreement

Guaranty Agreement

9

Authorized TIF Projects

Housing Authority

Redevelopment and Urban Renewal

Remove or reduce blight

Rehabilitation or conservation work

Industrial Development Board

Project defined at T.C.A. § 7-53-101(13)

24 Subparts defining economic development

BROAD

10

The Uniformity in Tax Increment Financing Act of 2012 (TCA Section 9-23-101 et seq.)

The 2012 Act addressed the following issues:

No state oversight

TIF revenues accumulated off budget

Inconsistent reporting requirements

The 2012 Act applies to newly created or amended tax increment plans for which public hearings are held on or after March 21, 2012.

11

The Uniformity in Tax Increment Financing Act of 2012 (TCA Section 9-23-101 et seq.)

Best Interest Determination Required Plan Term Extends beyond 20 or 30 years

IDB uses TIF to finance a privately-owned project other

than parking and storm water improvements and for

general economic development purposes

TCA § 9-23-103(a)(2)(B)Excess taxes beyond amounts necessary to fund or reserve for

eligible expenditures under the applicable tax increment

statute, may be applied to principal and interest of debt

incurred to finance such eligible expenditures, or shall revert

to the taxing agency general fund.

12

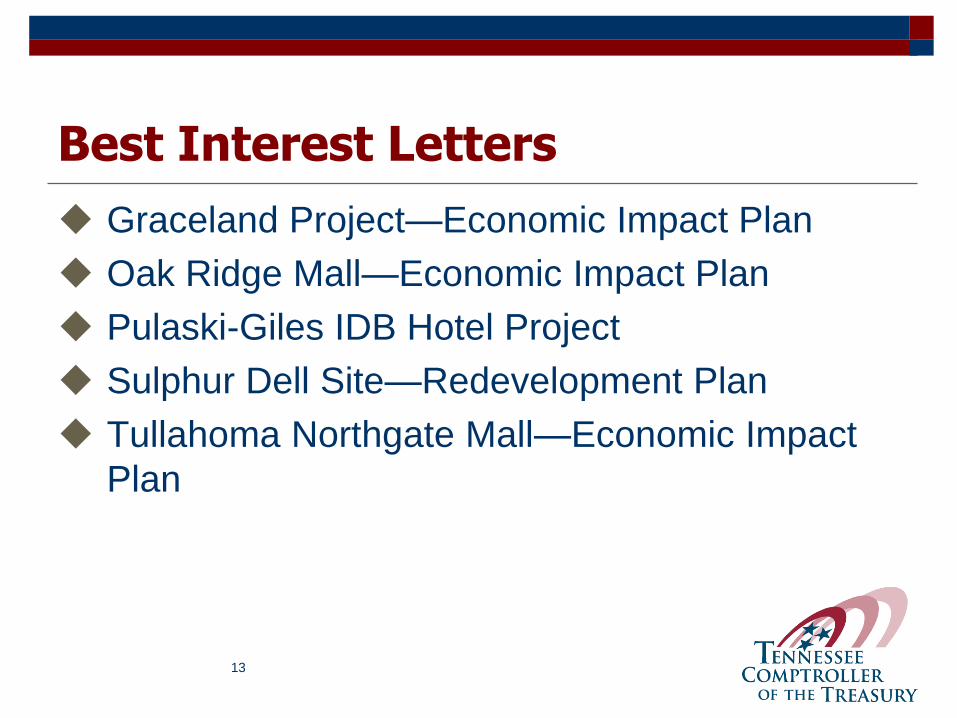

Best Interest Letters

Graceland Project—Economic Impact Plan

Oak Ridge Mall—Economic Impact Plan

Pulaski-Giles IDB Hotel Project

Sulphur Dell Site—Redevelopment Plan

Tullahoma Northgate Mall—Economic Impact

Plan

13

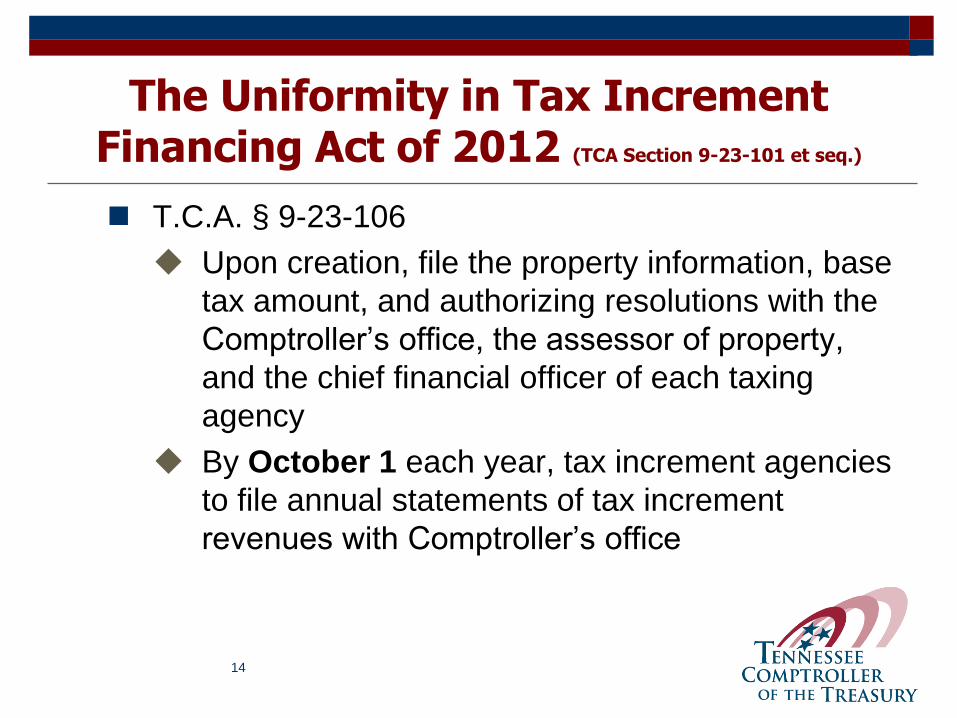

The Uniformity in Tax Increment Financing Act of 2012 (TCA Section 9-23-101 et seq.)

T.C.A. § 9-23-106

Upon creation, file the property information, base

tax amount, and authorizing resolutions with the

Comptroller’s office, the assessor of property,

and the chief financial officer of each taxing

agency

By October 1 each year, tax increment agencies

to file annual statements of tax increment

revenues with Comptroller’s office

14

Additional Information

15

TIF Plan Filing and Annual Increment Reporting Status

As stated earlier, the TIF development plan and annual increment received are to be filed with the Comptroller’s office

Compliance level is lower than desired but currently improving

Annual correspondence reminders from the Comptroller’s office

Working with every county to assemble a complete statewide database

16

Graceland Economic Impact Plan, 2015

17

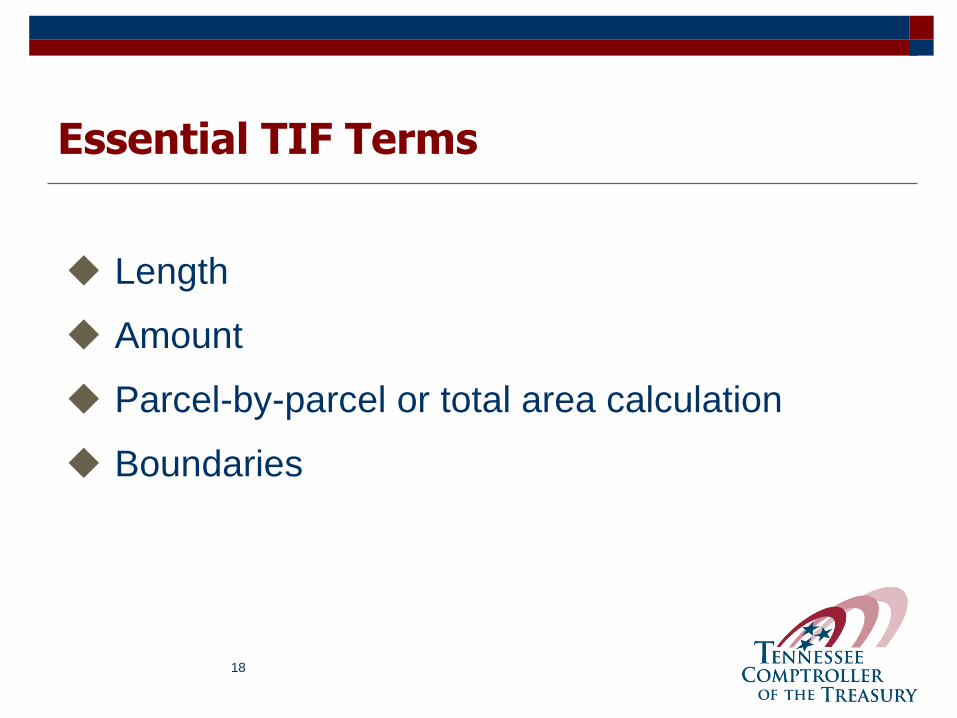

Essential TIF Terms

Length

Amount

Parcel-by-parcel or total area calculation

Boundaries

18

Graceland Economic Impact Plan

Privately-owned archive studio, hotel and conference

center, museum attractions and retail

Passed “but for” test

Boundaries limited to 120 acre Graceland Campus

Only 50% of the tax increment revenues generated in

the plan area will be utilized for project purposes; the

remaining 50% will be distributed to the local

governments

Pooled incremental sales and property tax revenues,

borrower payments, and tourism surcharges.

19

Measuring TIF Effectiveness

Get updates from the finance director on

amounts outstanding and receive a list of active

plan areas with estimated end dates

Do your own “but for” or necessity test

Ask questions about the projected values

Remember only IDBs may use incremental

revenues to pay project costs directly

20

TIF at a Turning Point

GASB Statement No. 77, Tax Abatement

Disclosures, approved August 2015

New financial statement disclosures required for

state and local governments for fiscal year

beginning July 1, 2016 and ending June 30,

2017

New disclosure requirements supplement

existing state reporting requirements

Economic Development Policies21

Your Questions…Accountability

Should policies be required?

How should the established criteria be

communicated to the authorizing entity prior to

receiving any formal approval?

Should TIF projects be targeted and

temporary? How do we know when they end?

22

Your Questions…Transparency

What are TIF best practices in Tennessee?

Are TIF discussions conducted in the

“sunshine”?

23

Your Questions…Duration

What are the pros and cons of reauthorizing a

tax increment allocation when the original plan

has run its course?

If the decision is made to amend the plan to

keep developing the area, what questions

should the authorizing entity ask?

24

Partnering with Local Governments

What oversight authority does the Comptroller

have, when is it exercised, and what prompts it

to be used?

What other resources are available to help

facilitate the proper creation of tax increment

areas?

25

TIF Brochure

26

Contact Information

Betsy KnottsAssistant General CounselComptroller of the Treasury Suite 1700, James K. Polk Bldg.505 Deaderick St.Nashville, TN 37243Phone: (615) [email protected]

Kelsie JonesExecutive SecretaryState Board of Equalization9th Floor, Snodgrass TN Tower312 Rosa L. Parks AvenueNashville, TN 37243-1102Phone: (615) [email protected]

27