Task A: Sector performance and structural sector...

92

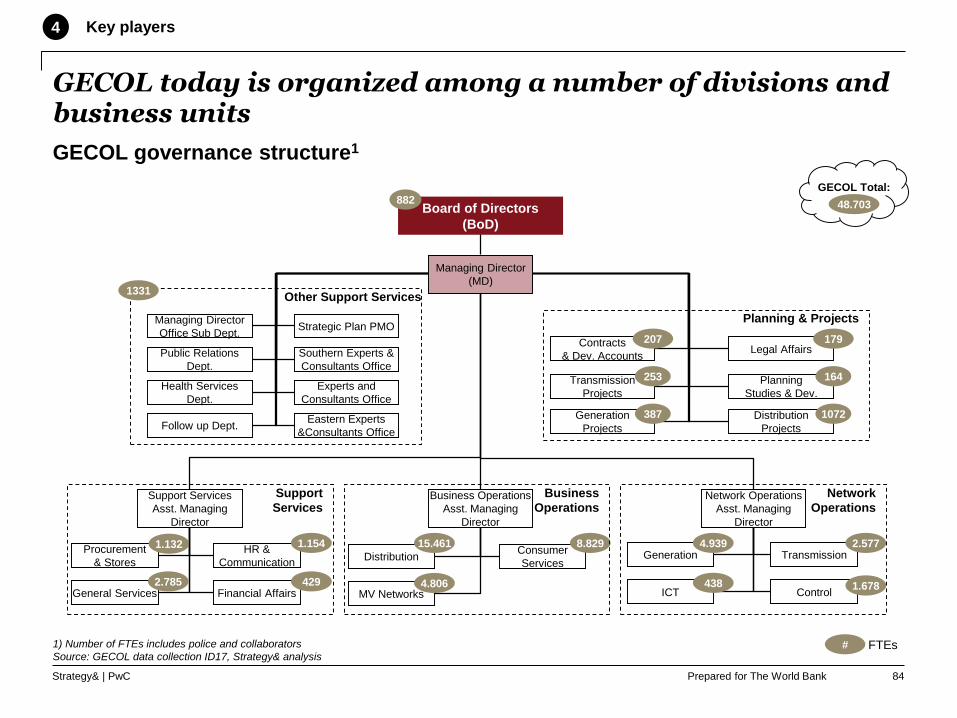

Deliverable 2: Rapid assessment of the sector performance Task A: Sector performance and structural sector reform April 2017 REVISED FINAL REPORT Report produced in April 2017 Data & analyses up-dates available within Task C and Task A final reports and within Task C Technical & Financial improvements reports Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized ed

Transcript of Task A: Sector performance and structural sector...

Deliverable 2: Rapid assessment of the sector performance

Task A: Sector performance and

structural sector reform

April 2017

REVISED FINAL REPORT

Report produced in April 2017

Data & analyses up-dates available within Task C and Task A final reports

and within Task C Technical & Financial improvements reports

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Prepared for The World BankStrategy& | PwC

Disclaimer and copyright note

This document has been prepared only for the International

Bank of Reconstruction and Development ("IBRD") and solely

for the purpose and on the terms agreed with the IBRD in our

agreement dated 21 March 2017 relating to Task A.

The scope of our work was limited to a review of documentary

evidence made available to us. We have not independently

verified any information given to us relating to the services.

We accept no liability (including for negligence) to anyone else

in connection with this document. We have agreed with you

that the report will be provided by you to GECOL for their

consideration. We would ask that it not be provided to anyone

else unless otherwise agreed in writing by us.

This is a draft prepared for discussion purposes only and

should not be relied upon; the contents are subject to

amendment or withdrawal and our final conclusions and

findings will be set out in our final deliverable.

© 2017

PricewaterhouseCoopers

LLP

All rights reserved. In this

document, 'PwC' refers to the

UK member firm, and may

sometimes refer to the PwC

network. Each member firm

is a separate legal entity.

Please see

www.pwc.com/structure for

further details

1

Prepared for The World BankStrategy& | PwC

Objective is to rapidly identify the issues affecting the sector – Analyses are then further deep-dived in following reports

Considerations on current report

Document objectives

• Revise the Libyan electricity demand towards 2030

• Review the Libyan electricity sector, by business area (generation, transmission, distribution & supply)

• Identify preliminary considerations on the country’s supply & demand balance

• Provide an high-level overview of the sector governance and structure

Document intends to: The document is NOT

• Review the electricity demand projections

towards 2030

• Rapidly identify at a high-level the issues

affecting the Libyan electricity sector in order

to provide to the project team members with

an overview and the preliminary directions on

which to focus on with the next deliverables

(including Task B and Task D)

• Allow project team members and

stakeholders to initiate discussions on the real

issues affecting the Libyan sector today

• The document does not represent the final

assessment of the Libyan sector performance

(this assessment is to be made with the following

deliverables planned within Task A and Task C)

2

Prepared for The World BankStrategy& | PwC

Demand

Generation

Transmission

Distribution and supply

Supply / demand balance

Governance and sector structure

References for analysis update

3

Prepared for The World BankStrategy& | PwC

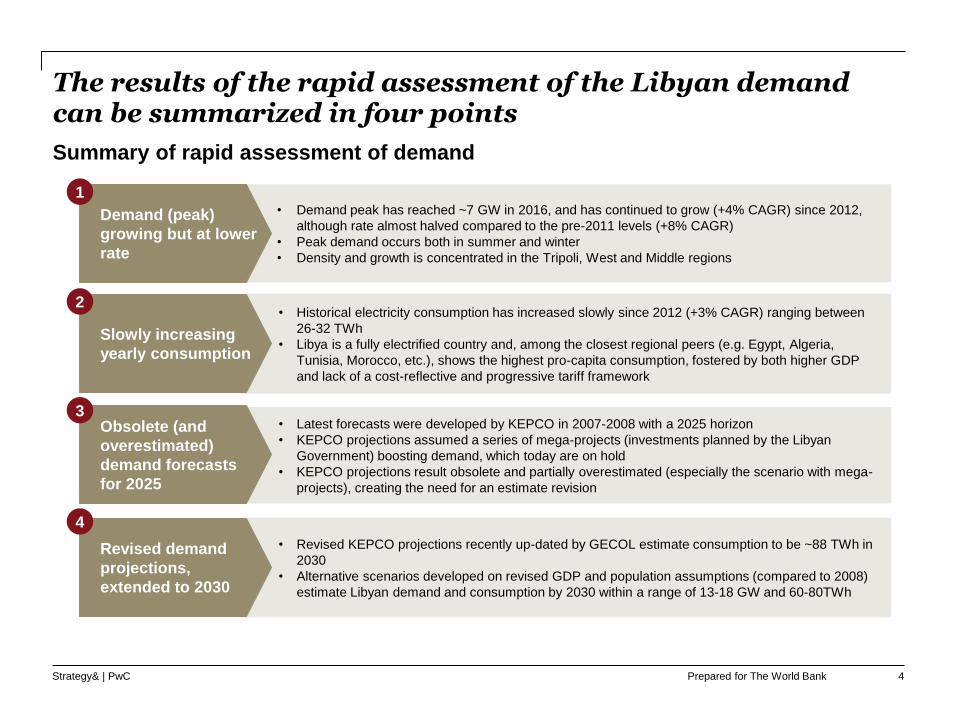

The results of the rapid assessment of the Libyan demand can be summarized in four points

Summary of rapid assessment of demand

• Demand peak has reached ~7 GW in 2016, and has continued to grow (+4% CAGR) since 2012,

although rate almost halved compared to the pre-2011 levels (+8% CAGR)

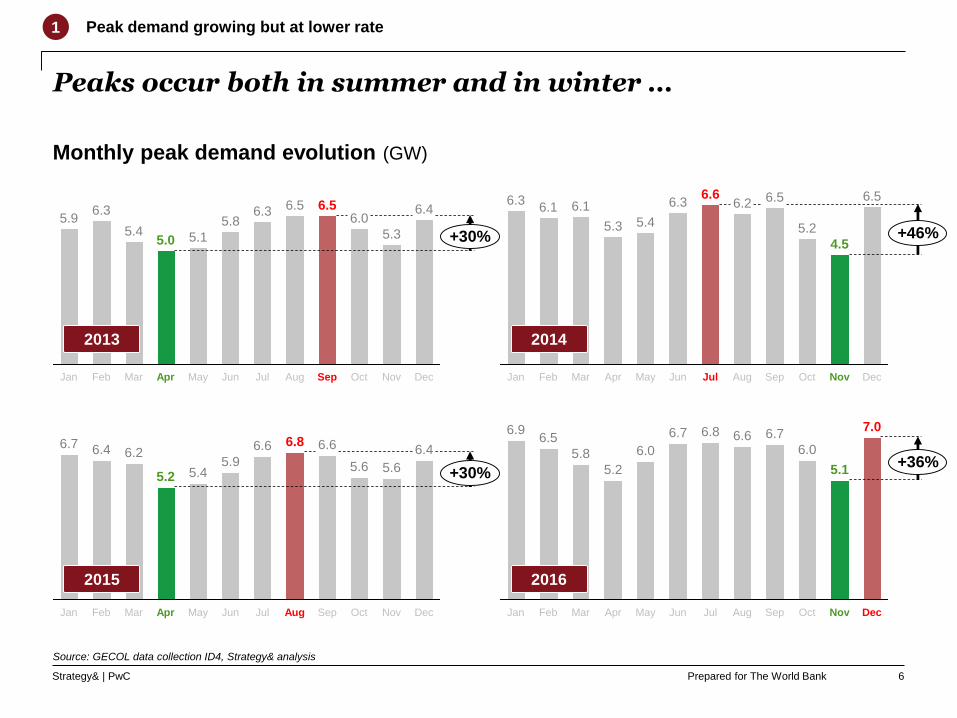

• Peak demand occurs both in summer and winter

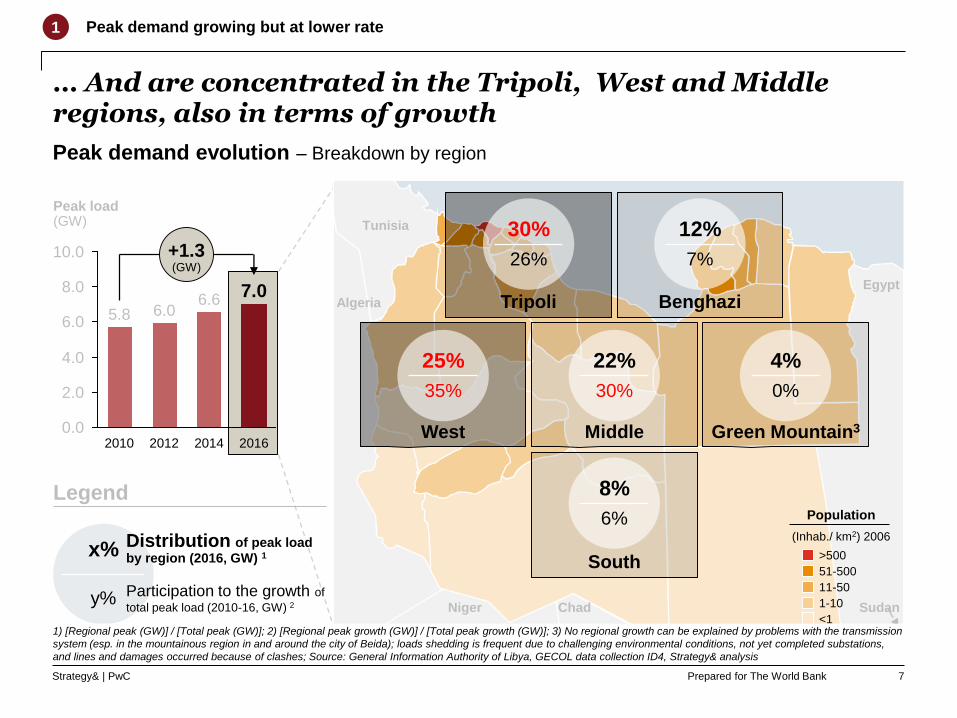

• Density and growth is concentrated in the Tripoli, West and Middle regions

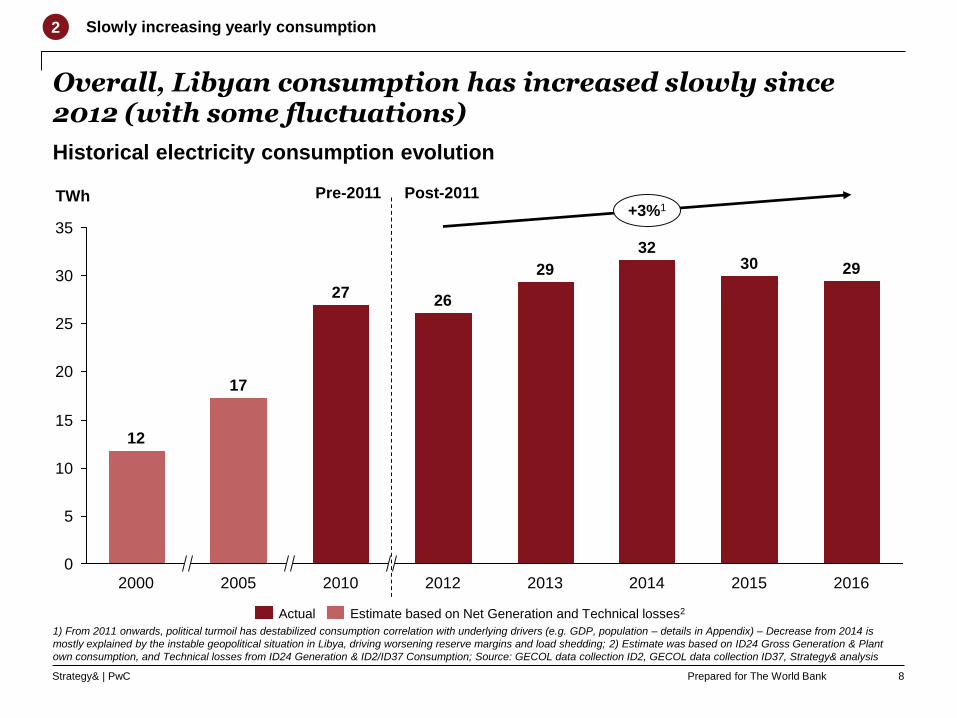

• Historical electricity consumption has increased slowly since 2012 (+3% CAGR) ranging between

26-32 TWh

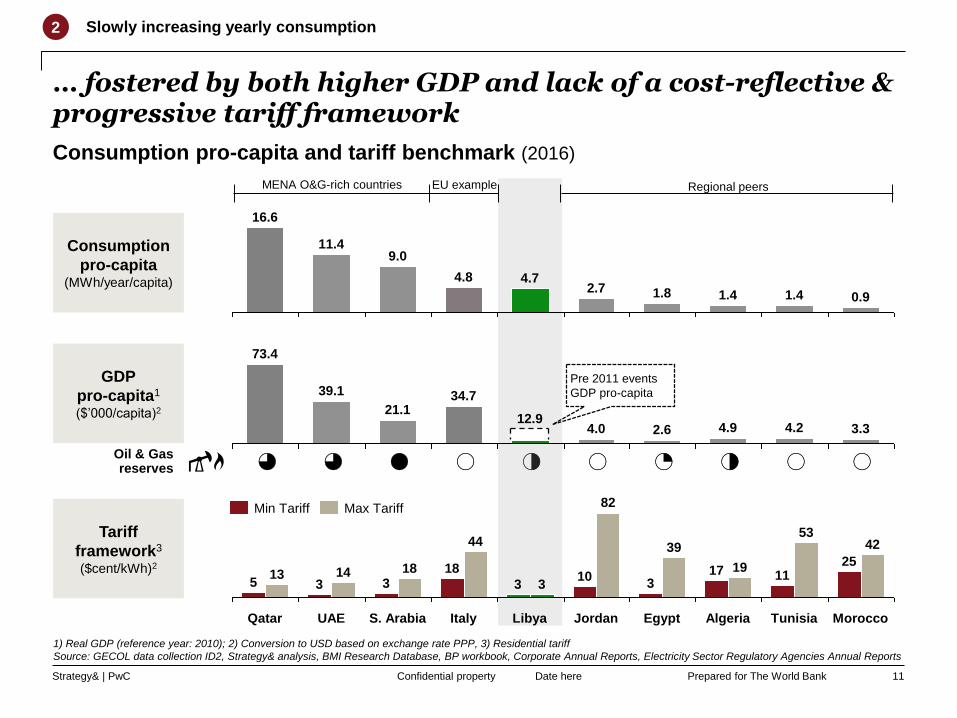

• Libya is a fully electrified country and, among the closest regional peers (e.g. Egypt, Algeria,

Tunisia, Morocco, etc.), shows the highest pro-capita consumption, fostered by both higher GDP

and lack of a cost-reflective and progressive tariff framework

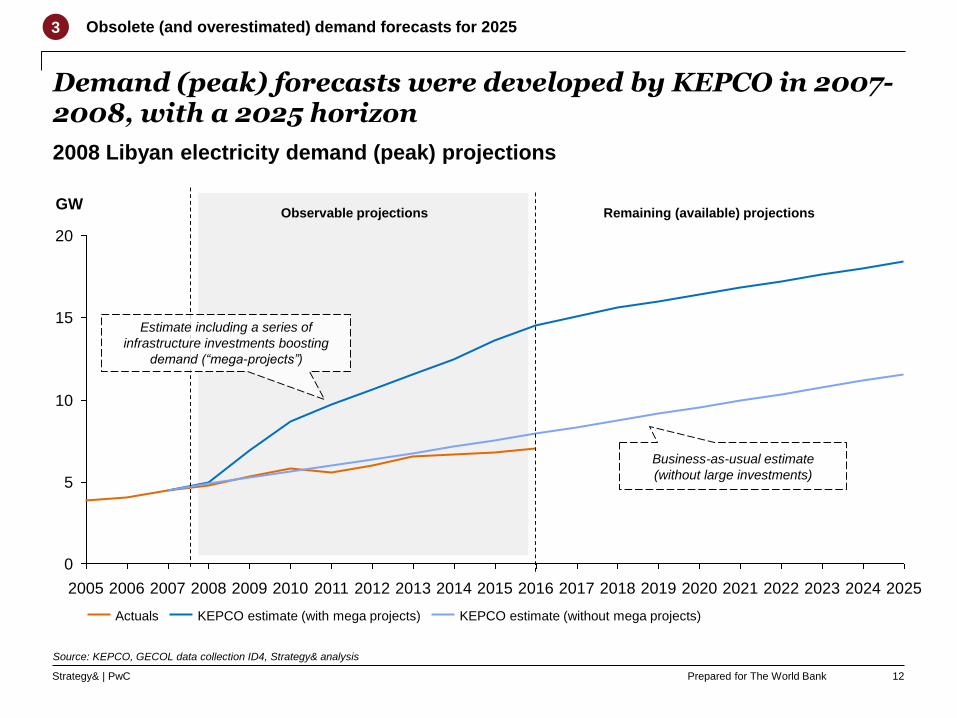

• Latest forecasts were developed by KEPCO in 2007-2008 with a 2025 horizon

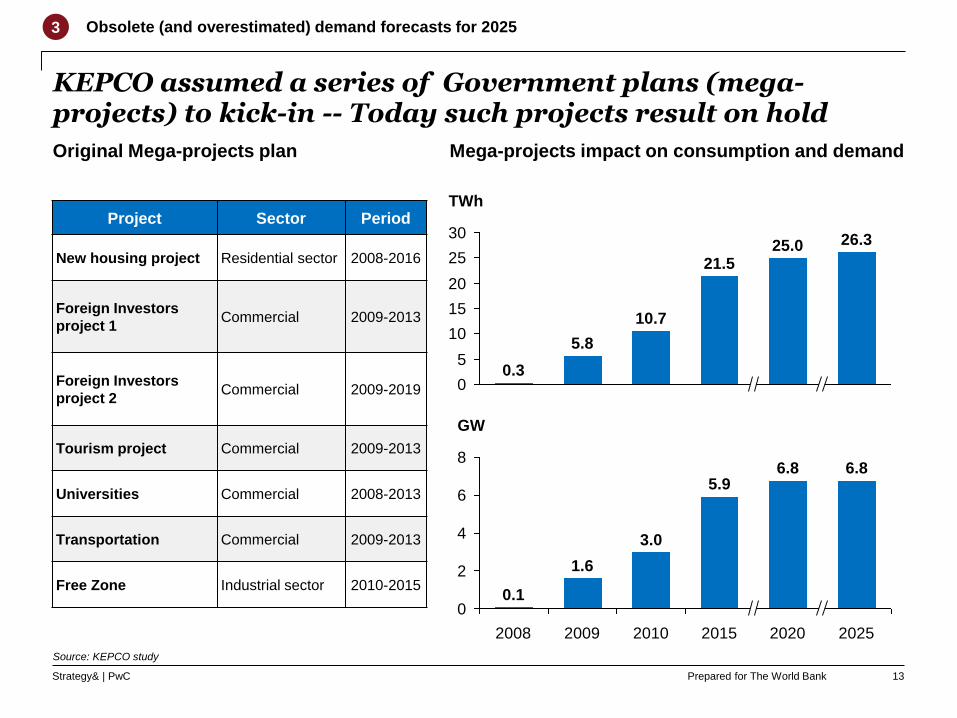

• KEPCO projections assumed a series of mega-projects (investments planned by the Libyan

Government) boosting demand, which today are on hold

• KEPCO projections result obsolete and partially overestimated (especially the scenario with mega-

projects), creating the need for an estimate revision

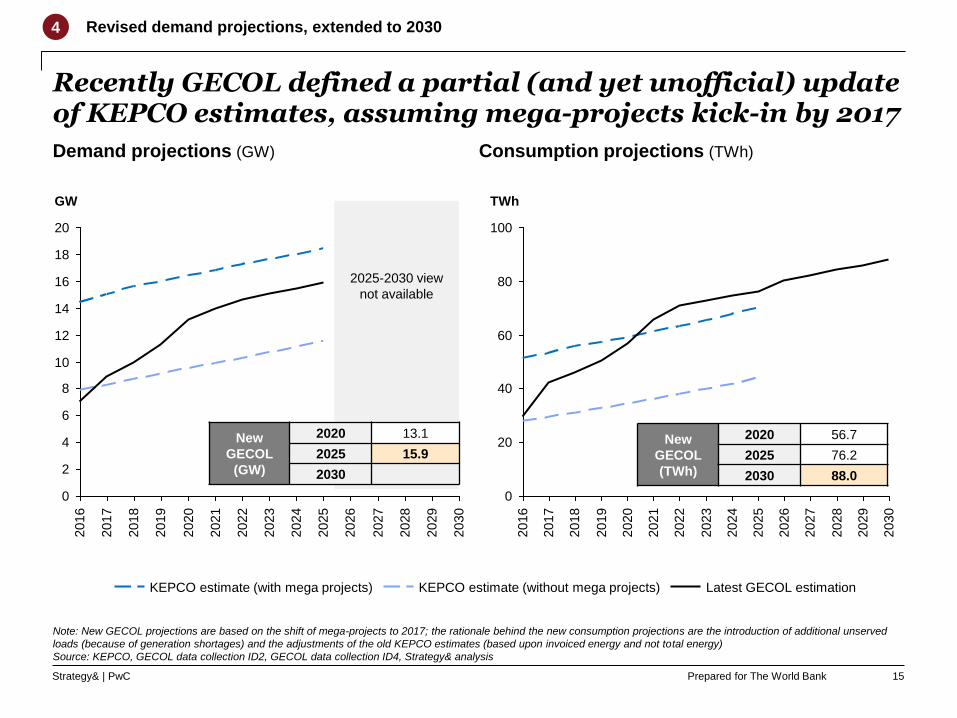

• Revised KEPCO projections recently up-dated by GECOL estimate consumption to be ~88 TWh in

2030

• Alternative scenarios developed on revised GDP and population assumptions (compared to 2008)

estimate Libyan demand and consumption by 2030 within a range of 13-18 GW and 60-80TWh

Slowly increasing

yearly consumption

Obsolete (and

overestimated)

demand forecasts

for 2025

Revised demand

projections,

extended to 2030

Demand (peak)

growing but at lower

rate

1

2

3

4

4

Prepared for The World BankStrategy& | PwC

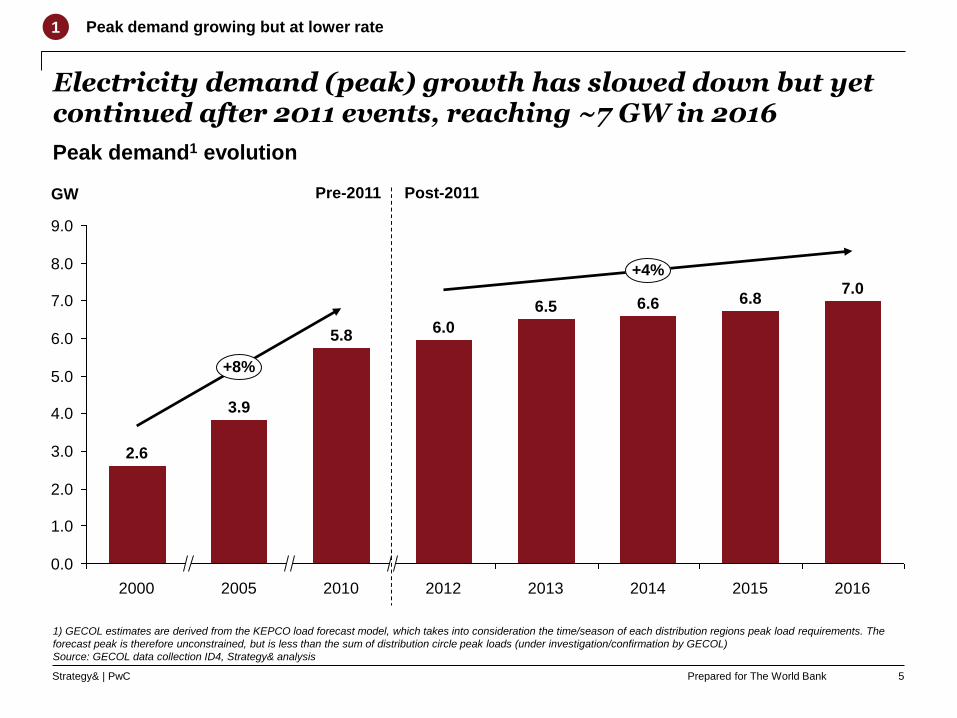

Electricity demand (peak) growth has slowed down but yet continued after 2011 events, reaching ~7 GW in 2016

9.0

4.0

7.0

5.0

3.0

1.0

6.0

8.0

2.0

0.0

2005

5.8

GW

6.5

20162010 20152000

6.6

3.9

2012

6.8

6.0

2.6

2014

+4%

+8%

2013

7.0

1) GECOL estimates are derived from the KEPCO load forecast model, which takes into consideration the time/season of each distribution regions peak load requirements. The

forecast peak is therefore unconstrained, but is less than the sum of distribution circle peak loads (under investigation/confirmation by GECOL)

Source: GECOL data collection ID4, Strategy& analysis

Peak demand growing but at lower rate1

Post-2011Pre-2011

Peak demand1 evolution

5

Prepared for The World BankStrategy& | PwC

Peaks occur both in summer and in winter …

Aug Sep

6.56.0

6.4

+30%

DecNov

5.3

Oct

6.35.8

5.0

MarFeb

5.4

JulJun

5.1

Jan

6.3

Apr May

5.96.5

5.3

Jan AprFeb

6.36.1

5.4

Mar

6.1

May

6.26.6

Jun Jul

6.3 6.5

DecNov

5.2

4.5

Oct

+46%

Sep

6.5

Aug

DecNovOct

5.6

Aug

6.66.8

5.6

Sep

+30%

6.66.26.4

5.2

Apr

5.9

JulJunJan May

5.4

MarFeb

6.7 6.4

Nov

6.8

Jun

5.1

DecOct

6.0

Sep

6.76.7 7.0

+36%

Aug

6.6

JulAprMar May

6.0

5.2

5.8

Feb

6.56.9

Jan

2013 2014

2015 2016

Monthly peak demand evolution (GW)

1

Source: GECOL data collection ID4, Strategy& analysis

Peak demand growing but at lower rate

6

Prepared for The World BankStrategy& | PwC

… And are concentrated in the Tripoli, West and Middle regions, also in terms of growth

Peak demand evolution – Breakdown by region

Algeria

Niger Chad

Tunisia

Sudan

Egypt

Tripoli Benghazi

West Middle Green Mountain3

South >500

51-500

11-50

1-10

<1

Population

(Inhab./ km2) 2006

30%

26%

12%

7%

22%

30%

8%

6%

25%

35%

4%

0%

Legend

x%

y%

Distribution of peak load

by region (2016, GW) 1

Participation to the growth of

total peak load (2010-16, GW) 2

1 Peak demand growing but at lower rate

1) [Regional peak (GW)] / [Total peak (GW)]; 2) [Regional peak growth (GW)] / [Total peak growth (GW)]; 3) No regional growth can be explained by problems with the transmission

system (esp. in the mountainous region in and around the city of Beida); loads shedding is frequent due to challenging environmental conditions, not yet completed substations,

and lines and damages occurred because of clashes; Source: General Information Authority of Libya, GECOL data collection ID4, Strategy& analysis

7

10.0

6.0

8.0

4.0

2.0

0.0

Peak load(GW)

20122010

6.05.8

+1.3(GW)

7.0

20162014

6.6

Prepared for The World BankStrategy& | PwC

Overall, Libyan consumption has increased slowly since 2012 (with some fluctuations)

5

15

20

0

10

35

30

25

TWh

2015

+3%1

2016

29

2012

32

2010

27

17

26

20142005

3029

12

20132000

Historical electricity consumption evolution

1) From 2011 onwards, political turmoil has destabilized consumption correlation with underlying drivers (e.g. GDP, population – details in Appendix) – Decrease from 2014 is

mostly explained by the instable geopolitical situation in Libya, driving worsening reserve margins and load shedding; 2) Estimate was based on ID24 Gross Generation & Plant

own consumption, and Technical losses from ID24 Generation & ID2/ID37 Consumption; Source: GECOL data collection ID2, GECOL data collection ID37, Strategy& analysis

2 Slowly increasing yearly consumption

Actual Estimate based on Net Generation and Technical losses2

Post-2011Pre-2011

8

Prepared for The World BankStrategy& | PwC

Similarly to peak demand, density is concentrated in the Tripoli, West and Middle areas

Consumption evolution – Breakdown by region1

Algeria

Niger Chad

Tunisia

Sudan

Egypt

Tripoli4 Benghazi

West5 Middle6 Green Mountain7

South >500

51-500

11-50

1-10

<1

Population

(Inhab./ km2) 2006

37%

145%

15%

-33%

16%

76%

7%

-53%

17%

-63%

8%

30%

0.0

30.0

20.0

40.0

10.0

2014

Consumption(TWh) +2.5

(TWh)

2016

29.527.0

20122010

31.7

26.2

Legend

x%

y%

Distribution of consumption by region (2016, TWh) 2

Participation to the growth of

total consumption (2010-16, TWh) 3

2 Slowly increasing yearly consumption

1) Based on Energy supplied to 11kV distribution network (consumption data breakdown by region still to be provided); 2) [Regional consumption (TWh)] / [Total consumption

(TWh)]; 3) [Regional consumption growth (TWh)] / [Total consumption growth (TWh)]; 4) Includes the central government and Jfara; 5) Includes Western Mountain and Gharyan;

6) Includes Tarhouna ; 7) Includes Green Mountain and Derna; Source: General Information Authority of Libya, GECOL data collection ID21, Strategy& analysis

9

Prepared for The World BankStrategy& | PwC

Compared to its regional peers, Libya shows the highest pro-capita and residential electricity consumption …

Date hereConfidential property 10

48%62% 56% 61% 53% 59%

38% 41%47%39%44%52%

100%

Algeria MoroccoTunisia2Libya EgyptJordan

ResidentialOther

0

1

2

3

4

5 4.8

1.3

2.5

Egypt

1.31.7

Libya AlgeriaJordan Morocco

0.9

Tunisia

Slowly increasing yearly consumption2

1) Electrification rate stands for % of population access to electricity. Data refers to 2015, latest historical data-point available

2) Data refers to 2014, latest historical data-point available

Source: GECOL data collection ID2, Strategy& analysis, BMI Research Database, Corporate Annual Reports, Electricity Sector Regulatory Agencies Annual Reports

Consumption

pro-capita(MWh/year/capita)

Share of

residential

consumption(%)

Consumption pro-capita regional benchmark (2015)

Electrification

Rate1100% 99.9% 100% 99.1% 99.8%2 99.2%

Libyan pre 2011 events

share of residential

consumption 35%

Prepared for The World BankStrategy& | PwC

3 3 4 0 2 0 1 2 0 0

… fostered by both higher GDP and lack of a cost-reflective & progressive tariff framework

Date hereConfidential property 11

0.91.4

4.74.8

9.0

1.41.82.7

11.4

16.6

Consumption pro-capita and tariff benchmark (2016)

1) Real GDP (reference year: 2010); 2) Conversion to USD based on exchange rate PPP, 3) Residential tariff

Source: GECOL data collection ID2, Strategy& analysis, BMI Research Database, BP workbook, Corporate Annual Reports, Electricity Sector Regulatory Agencies Annual Reports

Consumption

pro-capita(MWh/year/capita)

Oil & Gasreserves

Pre 2011 events

GDP pro-capita

Slowly increasing yearly consumption2

4.9 4.2 3.32.64.012.9

34.7

73.4

21.1

39.1GDP

pro-capita1

($’000/capita)2

Tariff

framework3

($cent/kWh)2

Algeria

17

Egypt Morocco

2511

Qatar UAE

35

Libya Jordan

310

3

Italy

183

S. Arabia Tunisia

42

13

44

14 18 19

39

3

82

53

Min Tariff Max Tariff

MENA O&G-rich countries Regional peersEU example

Prepared for The World BankStrategy& | PwC

Demand (peak) forecasts were developed by KEPCO in 2007-2008, with a 2025 horizon

Source: KEPCO, GECOL data collection ID4, Strategy& analysis

2008 Libyan electricity demand (peak) projections

2019 20222014 20232017

0

2016 2021 2025202420202018201520132012201120102007 20082006 20092005

10

15

20

5

GW

KEPCO estimate (without mega projects)Actuals KEPCO estimate (with mega projects)

Obsolete (and overestimated) demand forecasts for 20253

Observable projections Remaining (available) projections

Estimate including a series of

infrastructure investments boosting

demand (“mega-projects”)

Business-as-usual estimate

(without large investments)

12

Prepared for The World BankStrategy& | PwC

KEPCO assumed a series of Government plans (mega-projects) to kick-in -- Today such projects result on hold

Project Sector Period

New housing project Residential sector 2008-2016

Foreign Investors

project 1Commercial 2009-2013

Foreign Investors

project 2Commercial 2009-2019

Tourism project Commercial 2009-2013

Universities Commercial 2008-2013

Transportation Commercial 2009-2013

Free Zone Industrial sector 2010-2015

0

25

15

5

10

20

3025.0 26.3

21.5

5.8

0.3

10.7

TWh

Source: KEPCO study

Obsolete (and overestimated) demand forecasts for 20253

Original Mega-projects plan Mega-projects impact on consumption and demand

13

2

0

4

6

86.8

3.0

2025

GW

6.8

20202015

5.9

2010

1.6

0.1

20092008

Prepared for The World BankStrategy& | PwC

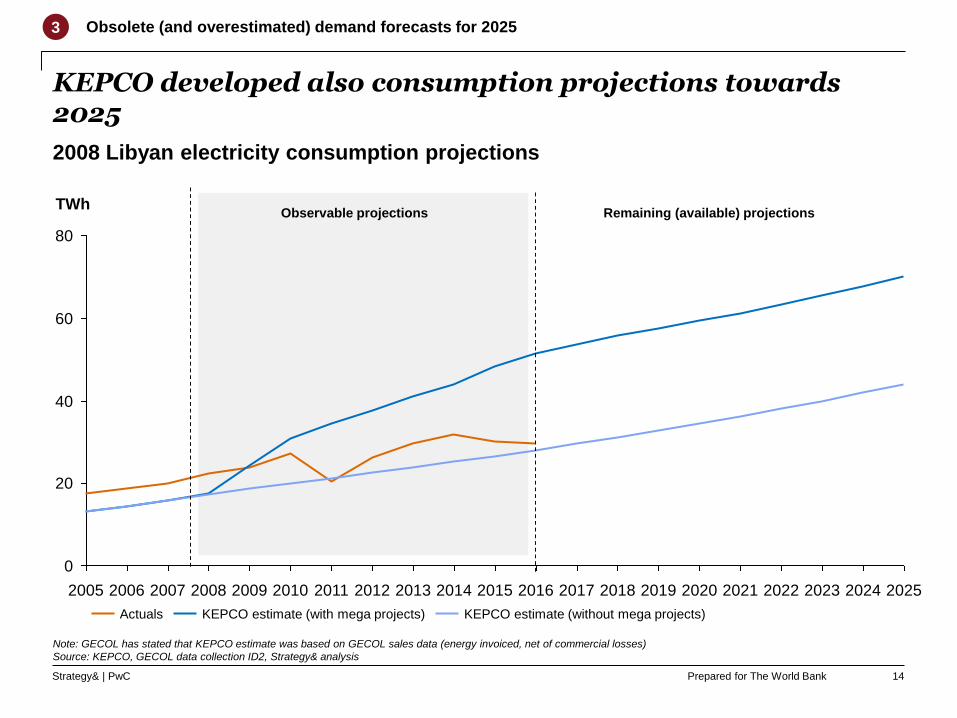

KEPCO developed also consumption projections towards 2025

Note: GECOL has stated that KEPCO estimate was based on GECOL sales data (energy invoiced, net of commercial losses)

Source: KEPCO, GECOL data collection ID2, Strategy& analysis

2008 Libyan electricity consumption projections

60

2020 2025

0

2015

20

80

40

20102005 20192017 20232014 20242012 20132006 20092007 2008 2011 2016 2018 2021 2022

TWh

KEPCO estimate (with mega projects)Actuals KEPCO estimate (without mega projects)

Obsolete (and overestimated) demand forecasts for 20253

Remaining (available) projectionsObservable projections

14

Prepared for The World BankStrategy& | PwC

Recently GECOL defined a partial (and yet unofficial) update of KEPCO estimates, assuming mega-projects kick-in by 2017

Demand projections (GW) Consumption projections (TWh)

2025

18

16

12

14

4

6

2029

2

2027

2026

0

20

2024

10

8

2028

2030

2023

2022

2021

2020

2019

2018

2017

2016

GW

KEPCO estimate (without mega projects) Latest GECOL estimationKEPCO estimate (with mega projects)

2017

2018

2016

100

40

2030

2029

2028

20

2026

2025

2024

2023

2027

2021

2022

2020

2019

80

60

0

TWh

Note: New GECOL projections are based on the shift of mega-projects to 2017; the rationale behind the new consumption projections are the introduction of additional unserved

loads (because of generation shortages) and the adjustments of the old KEPCO estimates (based upon invoiced energy and not total energy)

Source: KEPCO, GECOL data collection ID2, GECOL data collection ID4, Strategy& analysis

New

GECOL

(TWh)

2020 56.7

2025 76.2

2030 88.0

2025-2030 view

not available

New

GECOL

(GW)

2020 13.1

2025 15.9

2030

4 Revised demand projections, extended to 2030

15

Prepared for The World BankStrategy& | PwC

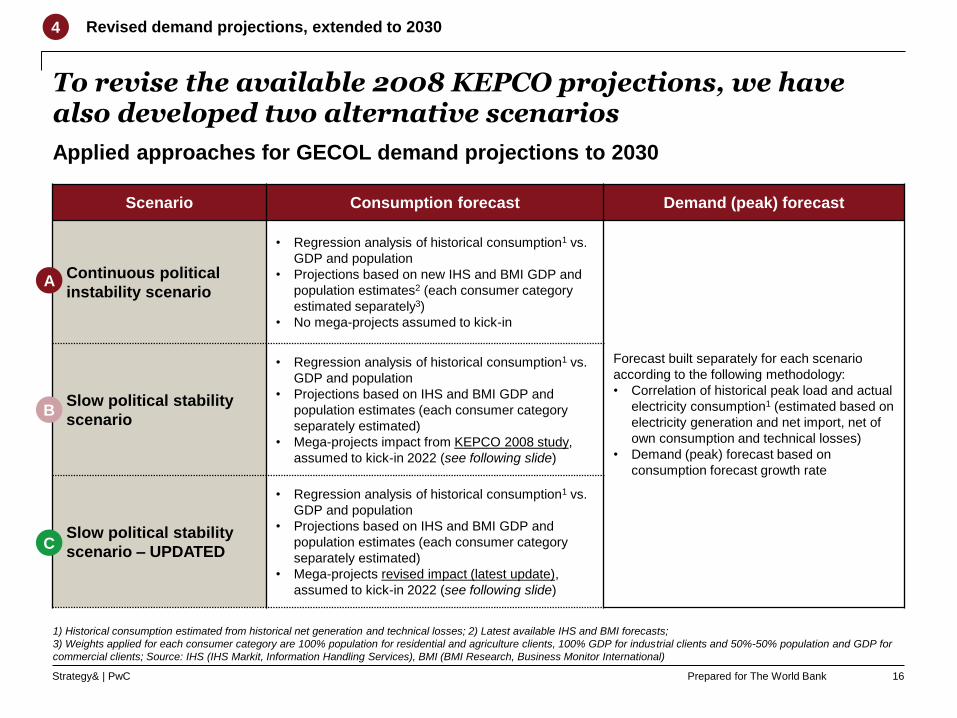

To revise the available 2008 KEPCO projections, we have also developed two alternative scenarios

1) Historical consumption estimated from historical net generation and technical losses; 2) Latest available IHS and BMI forecasts;

3) Weights applied for each consumer category are 100% population for residential and agriculture clients, 100% GDP for industrial clients and 50%-50% population and GDP for

commercial clients; Source: IHS (IHS Markit, Information Handling Services), BMI (BMI Research, Business Monitor International)

Applied approaches for GECOL demand projections to 2030

4 Revised demand projections, extended to 2030

Scenario Consumption forecast Demand (peak) forecast

Continuous political

instability scenario

• Regression analysis of historical consumption1 vs.

GDP and population

• Projections based on new IHS and BMI GDP and

population estimates2 (each consumer category

estimated separately3)

• No mega-projects assumed to kick-in

Forecast built separately for each scenario

according to the following methodology:

• Correlation of historical peak load and actual

electricity consumption1 (estimated based on

electricity generation and net import, net of

own consumption and technical losses)

• Demand (peak) forecast based on

consumption forecast growth rate

Slow political stability

scenario

• Regression analysis of historical consumption1 vs.

GDP and population

• Projections based on IHS and BMI GDP and

population estimates (each consumer category

separately estimated)

• Mega-projects impact from KEPCO 2008 study,

assumed to kick-in 2022 (see following slide)

Slow political stability

scenario – UPDATED

• Regression analysis of historical consumption1 vs.

GDP and population

• Projections based on IHS and BMI GDP and

population estimates (each consumer category

separately estimated)

• Mega-projects revised impact (latest update),

assumed to kick-in 2022 (see following slide)

A

B

16

C

Prepared for The World BankStrategy& | PwC

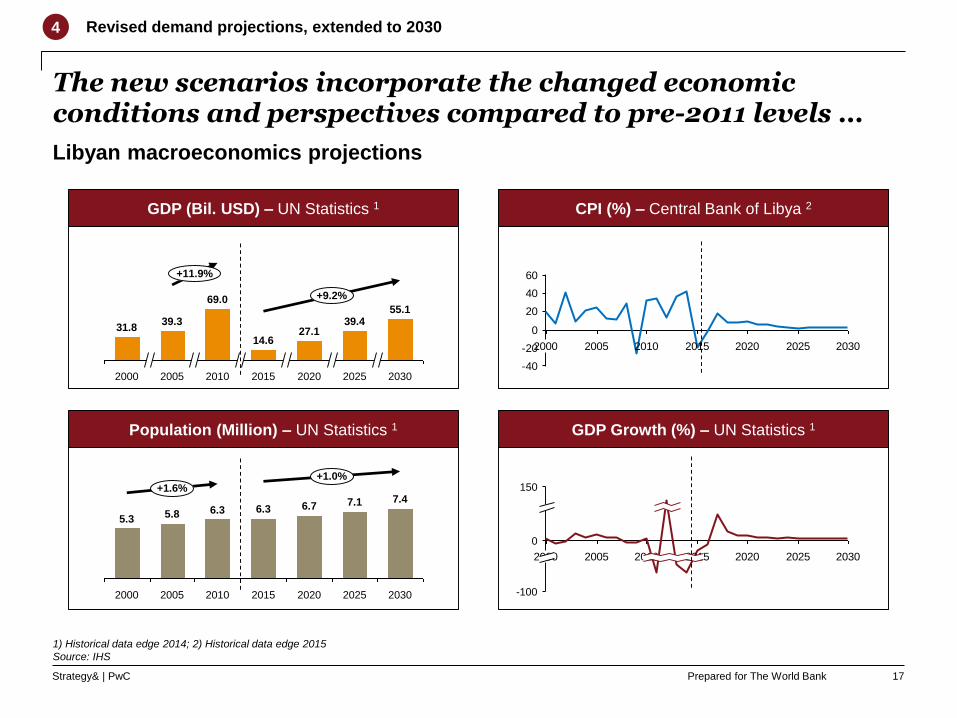

The new scenarios incorporate the changed economic conditions and perspectives compared to pre-2011 levels …

CPI (%) – Central Bank of Libya 2

GDP Growth (%) – UN Statistics 1

-40

-20

0

20

40

60

2000 2005 2010 2015 2020 2025 2030

2000 2005 2010 2015 2020 2025 2030

150

-100

0

Libyan macroeconomics projections

GDP (Bil. USD) – UN Statistics 1

Population (Million) – UN Statistics 1

2000 2025

7.1

+1.6%

20102005

5.36.3

7.4

2020

6.7

2015 2030

6.35.8

+1.0%

2005

39.355.1

+9.2%

39.4

14.6

2015

+11.9%

2020

27.1

2010

69.0

20252000

31.8

2030

1) Historical data edge 2014; 2) Historical data edge 2015

Source: IHS

4 Revised demand projections, extended to 2030

17

Prepared for The World BankStrategy& | PwC

12

14

10

24

20

4

6

0

8

2

16

22

18

20292028

TWh

2030

23.3

21.5

0.0

20272025

10.7

15.1

20232022

0.3

13.1

18.7

2026

5.8

17.1

2020 20242021

0.0

2019

0.0

2018

0.0

2017

0.0

Period of renewed political stability and public investments

16

12

10

8

18

6

4

2

0

22

20

14

24

20272026

6.75.7

202320222020

0.0

2019

0.0 0.0

2018

0.0

2017

10.2

2.5

0.1

7.5

9.58.2

2025 20292028

TWh

2024

4.7

2021

0.0

2030

… And include an updated view on “mega-projects” ramp-up (now estimated to start in 2022) and impact

“Mega-projects” ramp-up projections

Source: KEPCO, IHS, Strategy& analysis

4 Revised demand projections, extended to 2030

18

Political instability

period conservatively

assumed to last for five

more years

Revision of the impact

of the 650 development

projects in GECOL’s

database

Scenario B

Scenario C

Mega-projects

(KEPCO 2008

impact)

Mega-projects

(latest update)

Prepared for The World BankStrategy& | PwC

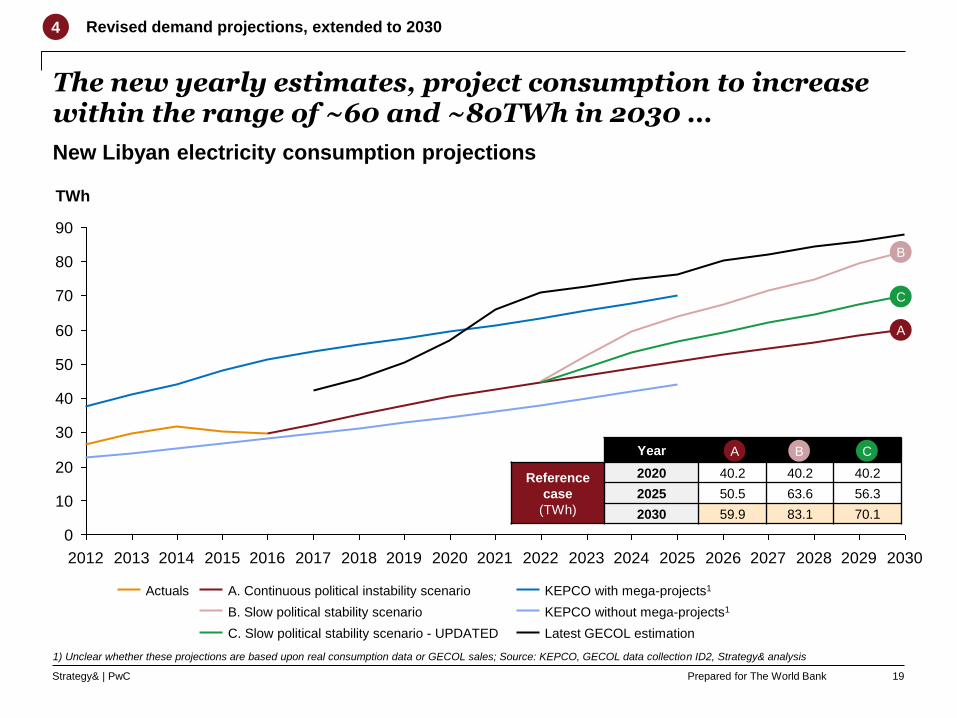

The new yearly estimates, project consumption to increase within the range of ~60 and ~80TWh in 2030 …

New Libyan electricity consumption projections

4

1) Unclear whether these projections are based upon real consumption data or GECOL sales; Source: KEPCO, GECOL data collection ID2, Strategy& analysis

Revised demand projections, extended to 2030

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

70

40

90

80

50

60

30

20

10

0

TWh

KEPCO with mega-projects1A. Continuous political instability scenario

KEPCO without mega-projects1

Latest GECOL estimation

B. Slow political stability scenario

Actuals

C. Slow political stability scenario - UPDATED

Year A B C

Reference

case

(TWh)

2020 40.2 40.2 40.2

2025 50.5 63.6 56.3

2030 59.9 83.1 70.1

B

A

A B

19

C

C

Prepared for The World BankStrategy& | PwC

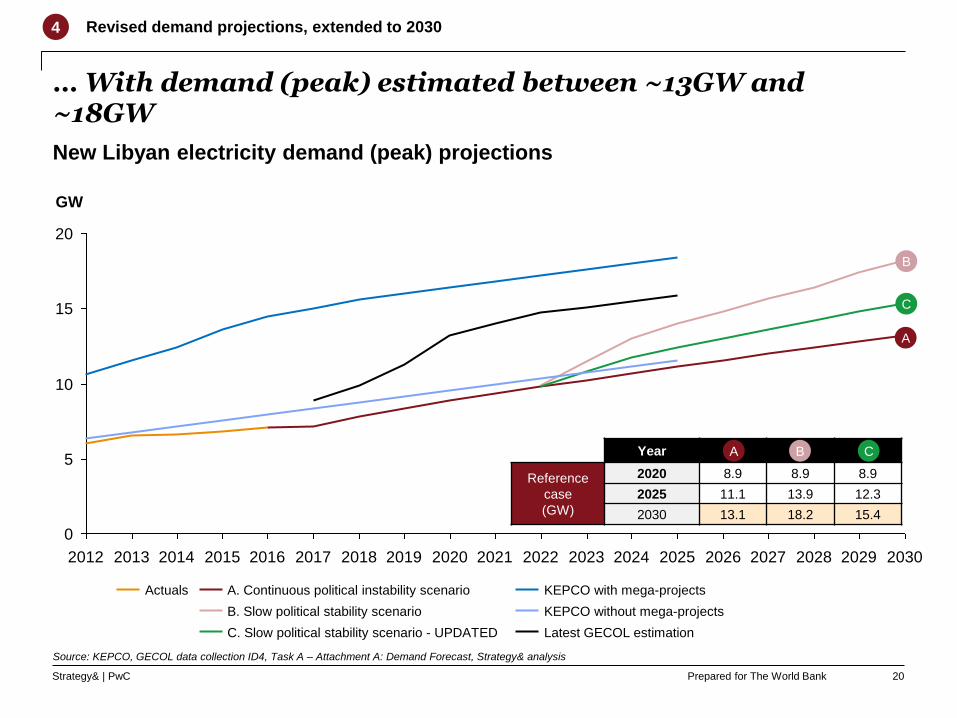

… With demand (peak) estimated between ~13GW and ~18GW

New Libyan electricity demand (peak) projections

4

Source: KEPCO, GECOL data collection ID4, Task A – Attachment A: Demand Forecast, Strategy& analysis

Revised demand projections, extended to 2030

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

20

0

5

15

10

GW

C. Slow political stability scenario - UPDATED

B. Slow political stability scenario

Actuals

KEPCO without mega-projects

Latest GECOL estimation

KEPCO with mega-projectsA. Continuous political instability scenario

Year A B C

Reference

case

(GW)

2020 8.9 8.9 8.9

2025 11.1 13.9 12.3

2030 13.1 18.2 15.4

A

B

A B

20

C

C

Prepared for The World BankStrategy& | PwC

Demand

Generation

Transmission

Distribution and supply

Supply / demand balance

Governance and sector structure

References for analysis update

21

Prepared for The World BankStrategy& | PwC

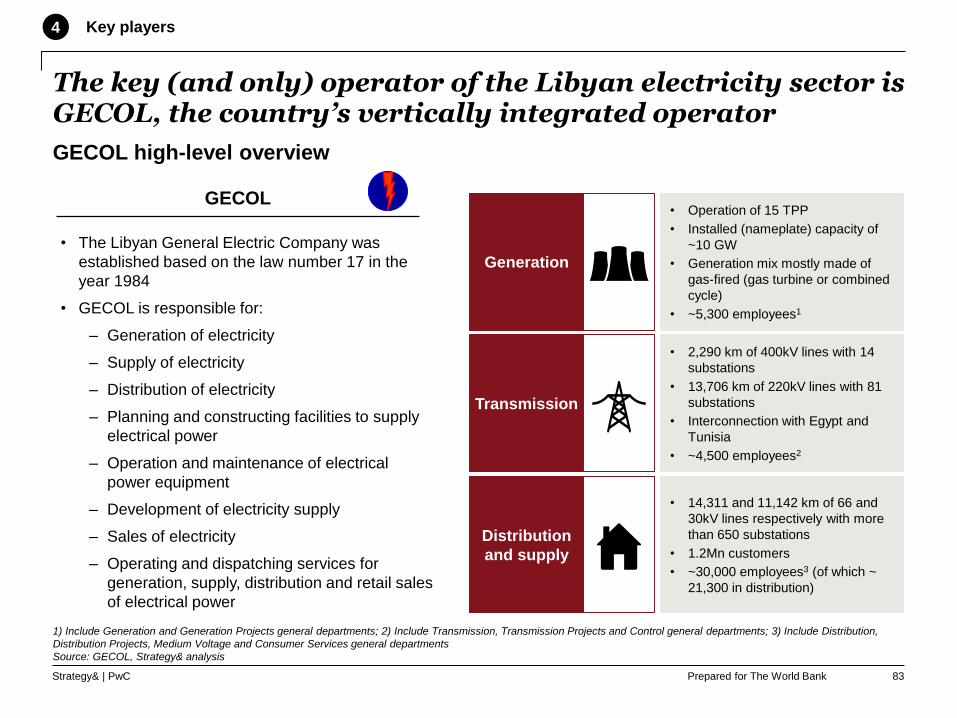

Libyan generation sector today is fully managed by GECOL, who produces electricity through 15 thermal power plants

Libyan power generation overview

Sources: GECOL data collection ID1, GECOL data collection ID12, GECOL data collection ID17, GECOL data collection ID22, Strategy& analysis

Steam turbine Gas turbine Combined Cycle

Technology

Libyan power generation in a nutshell

Generation capacity

(2016)

• Nameplate: 10.3 GW

• Installed: 7.5 GW

Technology mix

(% of installed capacity

by technology, 2016)

• Steam turbine: 14%

• Gas turbine: 48%

• Combined Cycle: 38%

No. of units

(2016)

68 (of which active 61),

15 thermal power plants

Sector operator 100% GECOL

No. of FTE employed

in the generation

sector (2016 y/e)

5,326 employees (11% of total

FTEs)

Generation

asset value

(Net asset value, 2014)

1.28 Bn LD

Number of FTEs per

MW installed capacity

(2016)

0.52 FTEs / MW

Zawia Tripoli

Khoms

Misurata

Benghazi

Derna

Sarir

ZwetinaWest Mountain

Khaleej

Tobruk

22

Prepared for The World BankStrategy& | PwC

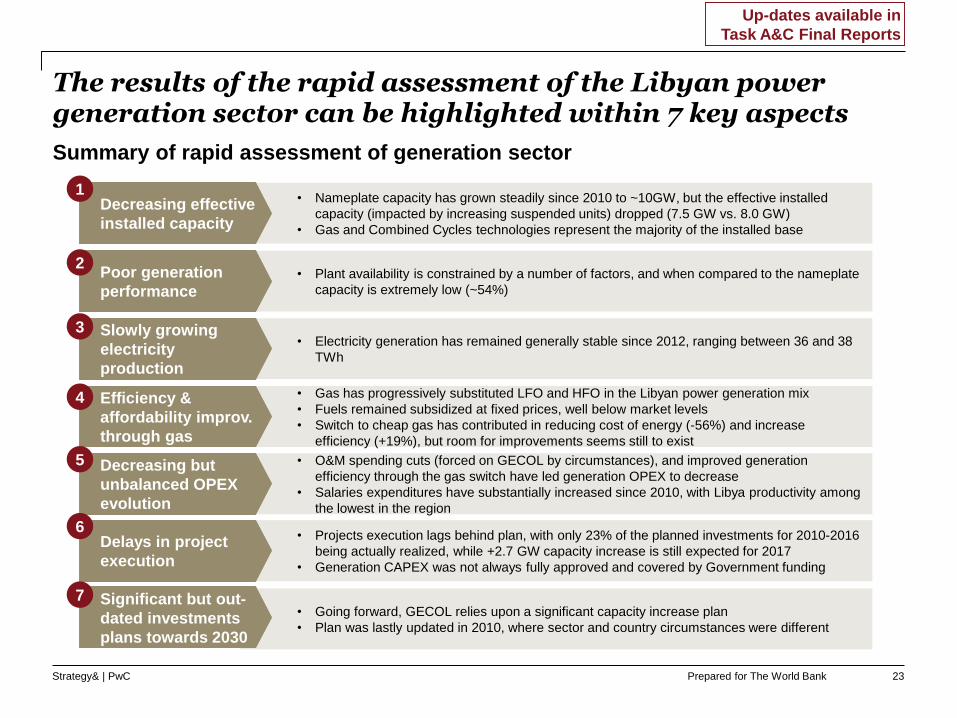

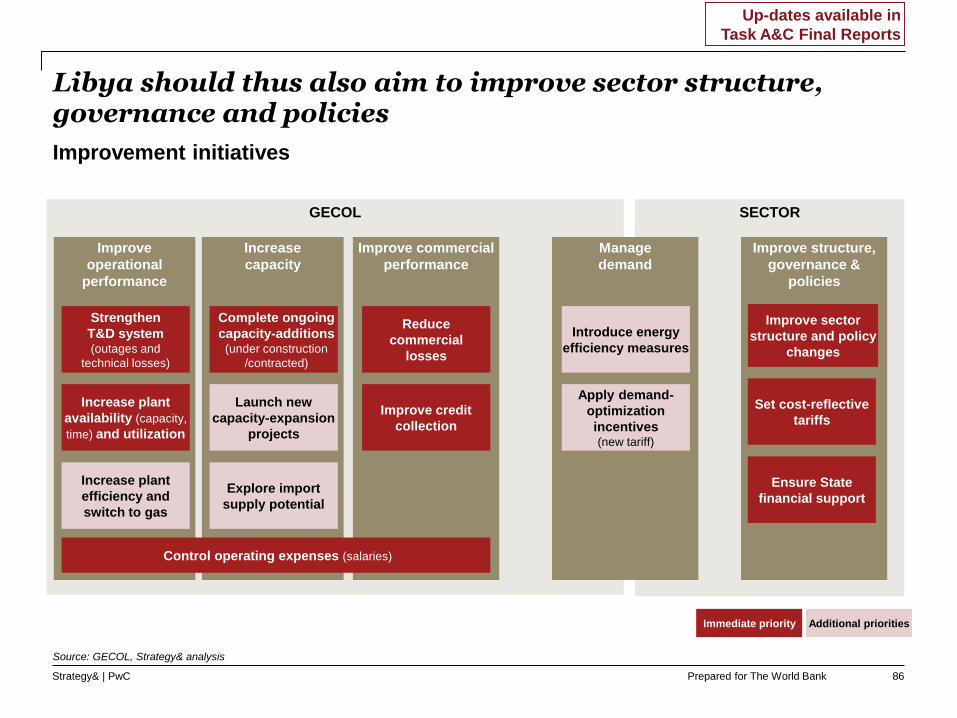

• Going forward, GECOL relies upon a significant capacity increase plan

• Plan was lastly updated in 2010, where sector and country circumstances were different

• Nameplate capacity has grown steadily since 2010 to ~10GW, but the effective installed

capacity (impacted by increasing suspended units) dropped (7.5 GW vs. 8.0 GW)

• Gas and Combined Cycles technologies represent the majority of the installed base

The results of the rapid assessment of the Libyan power generation sector can be highlighted within 7 key aspects

Summary of rapid assessment of generation sector

Decreasing effective

installed capacity

• Plant availability is constrained by a number of factors, and when compared to the nameplate

capacity is extremely low (~54%)

Poor generation

performance

• O&M spending cuts (forced on GECOL by circumstances), and improved generation

efficiency through the gas switch have led generation OPEX to decrease

• Salaries expenditures have substantially increased since 2010, with Libya productivity among

the lowest in the region

Decreasing but

unbalanced OPEX

evolution

• Projects execution lags behind plan, with only 23% of the planned investments for 2010-2016

being actually realized, while +2.7 GW capacity increase is still expected for 2017

• Generation CAPEX was not always fully approved and covered by Government funding

Delays in project

execution

Significant but out-

dated investments

plans towards 2030

• Electricity generation has remained generally stable since 2012, ranging between 36 and 38

TWh

Slowly growing

electricity

production

1

6

7

2

• Gas has progressively substituted LFO and HFO in the Libyan power generation mix

• Fuels remained subsidized at fixed prices, well below market levels

• Switch to cheap gas has contributed in reducing cost of energy (-56%) and increase

efficiency (+19%), but room for improvements seems still to exist

Efficiency &

affordability improv.

through gas

5

4

3

23

Up-dates available in

Task A&C Final Reports

Prepared for The World BankStrategy& | PwC

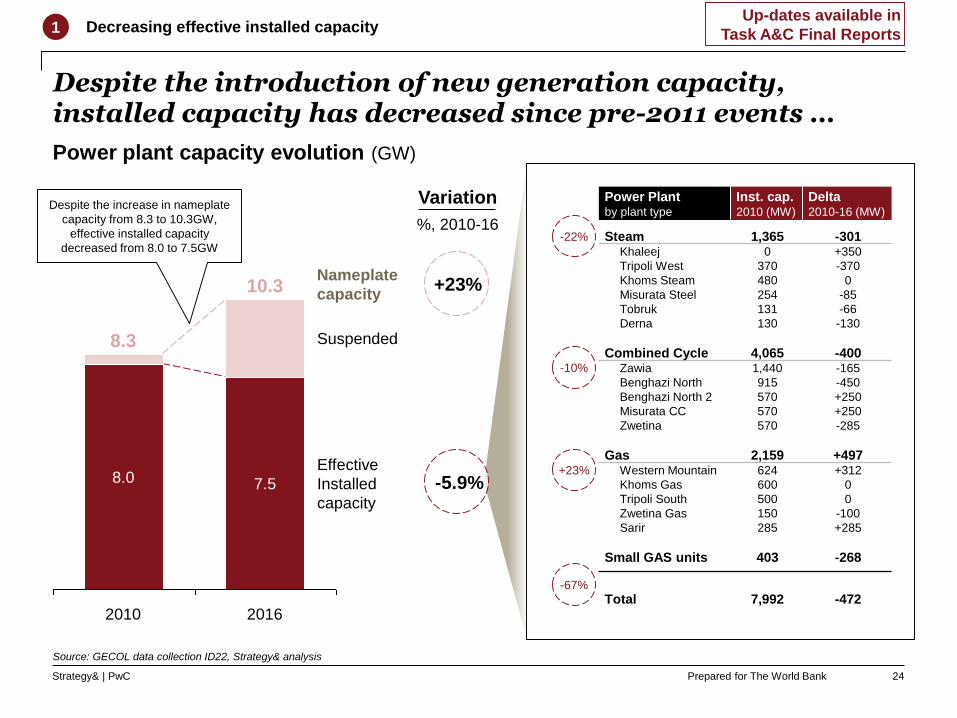

Despite the introduction of new generation capacity, installed capacity has decreased since pre-2011 events …

Source: GECOL data collection ID22, Strategy& analysis

Decreasing effective installed capacity1

Power plant capacity evolution (GW)

8.3

2016

10.3

8.0 7.5

2010

Effective

Installed

capacity

Suspended

Power Plantby plant type

Inst. cap.2010 (MW)

Delta2010-16 (MW)

Steam 1,365 -301Khaleej 0 +350

Tripoli West 370 -370

Khoms Steam 480 0

Misurata Steel 254 -85

Tobruk 131 -66

Derna 130 -130

Combined Cycle 4,065 -400Zawia 1,440 -165

Benghazi North 915 -450

Benghazi North 2 570 +250

Misurata CC 570 +250

Zwetina 570 -285

Gas 2,159 +497Western Mountain 624 +312

Khoms Gas 600 0

Tripoli South 500 0

Zwetina Gas 150 -100

Sarir 285 +285

Small GAS units 403 -268

Total 7,992 -472

-22%

-10%

+23%

-67%

+23%

Variation

%, 2010-16

Nameplate

capacity

-5.9%

Despite the increase in nameplate

capacity from 8.3 to 10.3GW,

effective installed capacity

decreased from 8.0 to 7.5GW

24

Up-dates available in

Task A&C Final Reports

Prepared for The World BankStrategy& | PwC

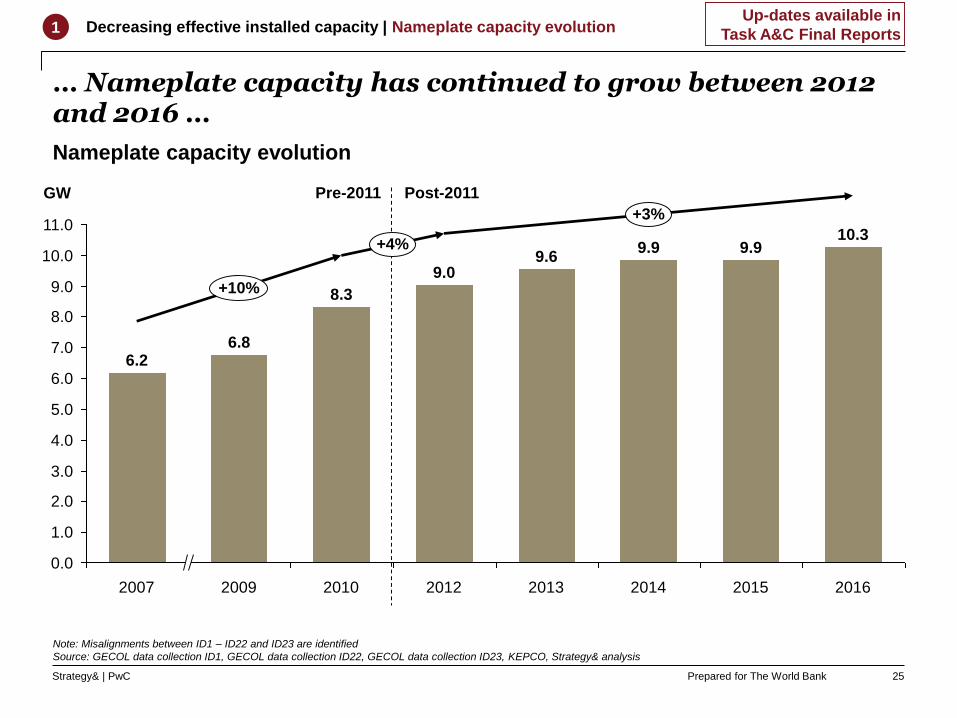

… Nameplate capacity has continued to grow between 2012 and 2016 …

11.0

10.0

4.0

1.0

9.0

5.0

8.0

6.0

7.0

3.0

2.0

0.0

+4%

2016

10.3

+10%

+3%

8.3

GW

2009 2012

6.2

2013

9.9

2007

6.8

9.69.9

2010 2014

9.0

2015

Note: Misalignments between ID1 – ID22 and ID23 are identified

Source: GECOL data collection ID1, GECOL data collection ID22, GECOL data collection ID23, KEPCO, Strategy& analysis

Post-2011Pre-2011

Nameplate capacity evolution

1 Decreasing effective installed capacity | Nameplate capacity evolution

25

Up-dates available in

Task A&C Final Reports

Prepared for The World BankStrategy& | PwC

9.69.9

10.39.9

6.86.2

8.3

9.0

11.0

4.0

2.0

8.0

10.0

6.0

0.0

3.0

5.0

9.0

7.0

1.0

GW

+10%

7.77.68.0

2009

6.47.1

7.9

2010

6.1

2014201320122007

-6% +2%

2016

7.5

2015

… But with increasingly suspended units the effective installed capacity decreased to 7.5GW (vs. 8GW in 2010)

1) The installed capacity includes all nameplate capacity of generating units available in that year, including the small Diesel and Gas turbine (most of them out of life time) and

excludes the generating units suspended in that year (over-time / long-term maintenance, cannibalized units)

Source: GECOL data collection ID1, GECOL data collection ID22, GECOL data collection ID23, KEPCO, Strategy& analysis

Post-2011Pre-2011

Effective installed capacity evolution

1 Decreasing effective installed capacity | Effective installed capacity evolution

Suspended units1 (e.g. long-term

maintenance, cannibalized units)

Effective installed capacity

26

Up-dates available in

Task A&C Final Reports

Prepared for The World BankStrategy& | PwC

Installed capacity density and growth is concentrated in Tripoli and the Middle regions …

Effective installed capacity overview – Breakdown by region1

1) Breakdown does not include installed capacity of small and rented gas / diesel plants;

2) [Regional installed capacity (GW)] / [Total installed capacity (GW)]; 3) [Regional installed capacity growth (GW)] / [Total installed capacity growth (GW)];

Source: General Information Authority of Libya, GECOL data collection ID22, Strategy& analysis

Algeria

Niger Chad

Tunisia

Sudan

Egypt

Tripoli Benghazi

West Middle Green Mountain

South

38%

-35%

17%

-42%

22%

-51%

8%

+60%

12%

+66%

1%

-42%

10.0

6.0

2.0

4.0

0.0

8.0

Effective installedcapacity(GW)

7.5

2014 2016

-0.5(GW)

8.0

2012

7.1

2010

7.6

Legend

x%

y%

Distribution of installed capacity by region (2016, GW) 2

Participation to the growth of

total installed capacity (2010-16, GW) 3

1 Decreasing effective installed capacity | Effective installed capacity evolution

27

Prepared for The World BankStrategy& | PwC

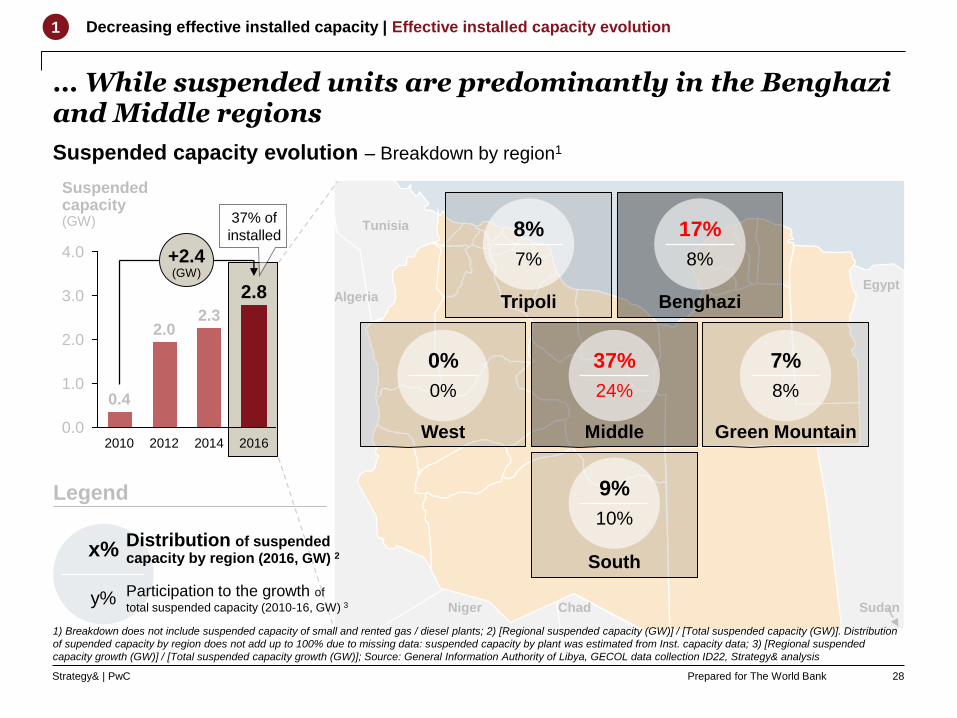

… While suspended units are predominantly in the Benghazi and Middle regions

Suspended capacity evolution – Breakdown by region1

Algeria

Niger Chad

Tunisia

Sudan

Egypt

Tripoli Benghazi

West Middle Green Mountain

South

8%

7%

17%

8%

37%

24%

9%

10%

0%

0%

7%

8%

4.0

0.0

1.0

3.0

2.0

Suspendedcapacity(GW)

2.8

2010

0.4

+2.4(GW)

20162014

2.3

2012

2.0

Legend

x%

y%

Distribution of suspended capacity by region (2016, GW) 2

Participation to the growth of

total suspended capacity (2010-16, GW) 3

37% of

installed

1 Decreasing effective installed capacity | Effective installed capacity evolution

28

1) Breakdown does not include suspended capacity of small and rented gas / diesel plants; 2) [Regional suspended capacity (GW)] / [Total suspended capacity (GW)]. Distribution

of supended capacity by region does not add up to 100% due to missing data: suspended capacity by plant was estimated from Inst. capacity data; 3) [Regional suspended

capacity growth (GW)] / [Total suspended capacity growth (GW)]; Source: General Information Authority of Libya, GECOL data collection ID22, Strategy& analysis

Prepared for The World BankStrategy& | PwC

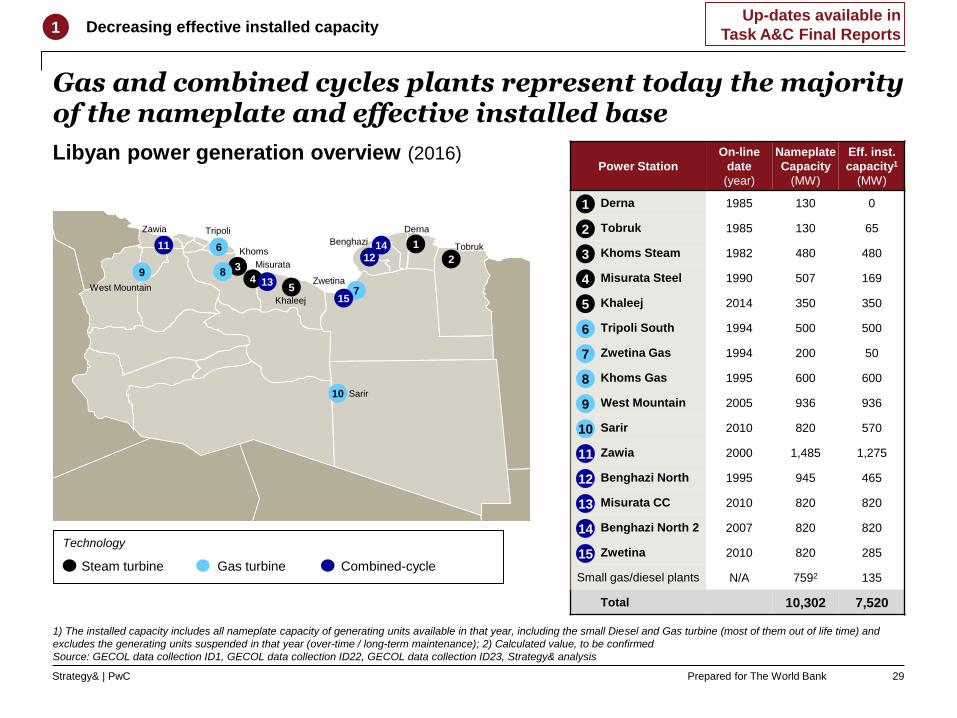

Gas and combined cycles plants represent today the majority of the nameplate and effective installed base

Power Station

On-line

date

(year)

Nameplate

Capacity

(MW)

Eff. inst.

capacity1

(MW)

Derna 1985 130 0

Tobruk 1985 130 65

Khoms Steam 1982 480 480

Misurata Steel 1990 507 169

Khaleej 2014 350 350

Tripoli South 1994 500 500

Zwetina Gas 1994 200 50

Khoms Gas 1995 600 600

West Mountain 2005 936 936

Sarir 2010 820 570

Zawia 2000 1,485 1,275

Benghazi North 1995 945 465

Misurata CC 2010 820 820

Benghazi North 2 2007 820 820

Zwetina 2010 820 285

Small gas/diesel plants N/A 7592 135

Total 10,302 7,520

1

2

3

4

5

6

7

8

9

10

11

12

13

14

Libyan power generation overview (2016)

1) The installed capacity includes all nameplate capacity of generating units available in that year, including the small Diesel and Gas turbine (most of them out of life time) and

excludes the generating units suspended in that year (over-time / long-term maintenance); 2) Calculated value, to be confirmed

Source: GECOL data collection ID1, GECOL data collection ID22, GECOL data collection ID23, Strategy& analysis

Decreasing effective installed capacity1

15Steam turbine Gas turbine Combined-cycle

Technology

29

Zawia Tripoli

Khoms

Misurata

Benghazi

Derna

Sarir

ZwetinaWest Mountain

Khaleej

Tobruk1

23

4

6

7

89

10

1112

13

14

155

Up-dates available in

Task A&C Final Reports

Prepared for The World BankStrategy& | PwC

9.0

9.99.6

6.2

9.910.3

8.3

6.8

4.0

1.0

10.0

6.0

9.0

2.0

0.0

8.0

7.0

3.0

11.0

5.0

5.5

GW

2014

5.6

+5%

2016

5.8

2012

-1% 0%

20152013

6.1

2010

5.7

2009

5.64.9

2007

4.8

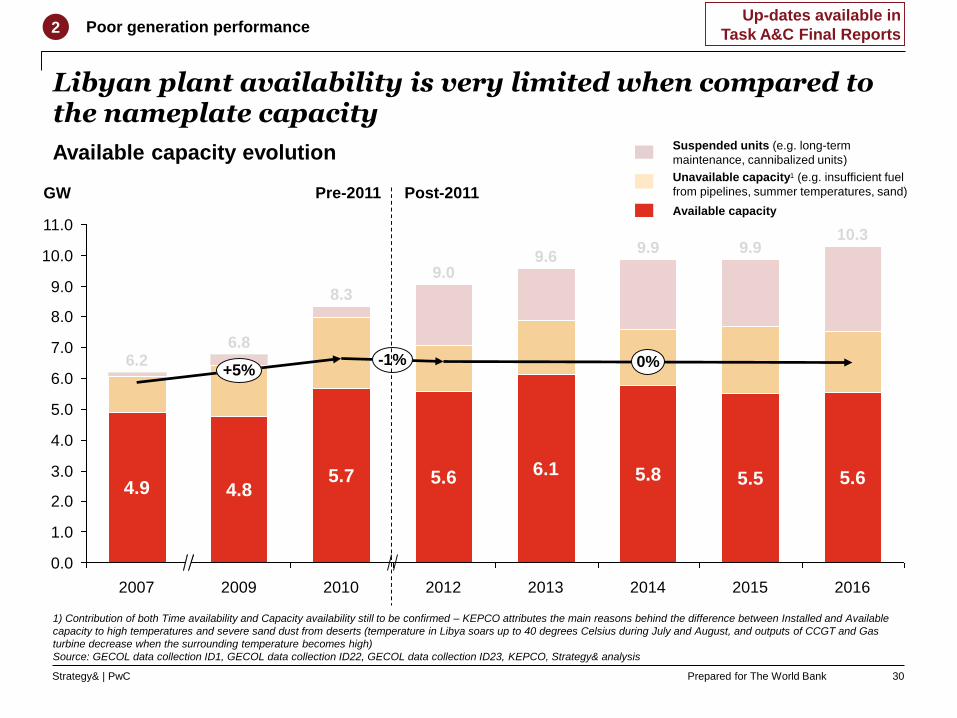

Libyan plant availability is very limited when compared to the nameplate capacity

1) Contribution of both Time availability and Capacity availability still to be confirmed – KEPCO attributes the main reasons behind the difference between Installed and Available

capacity to high temperatures and severe sand dust from deserts (temperature in Libya soars up to 40 degrees Celsius during July and August, and outputs of CCGT and Gas

turbine decrease when the surrounding temperature becomes high)

Source: GECOL data collection ID1, GECOL data collection ID22, GECOL data collection ID23, KEPCO, Strategy& analysis

Post-2011Pre-2011

Available capacity evolution

Poor generation performance2

Suspended units (e.g. long-term

maintenance, cannibalized units)

Unavailable capacity1 (e.g. insufficient fuel

from pipelines, summer temperatures, sand)

Available capacity

30

Up-dates available in

Task A&C Final Reports

Prepared for The World BankStrategy& | PwC

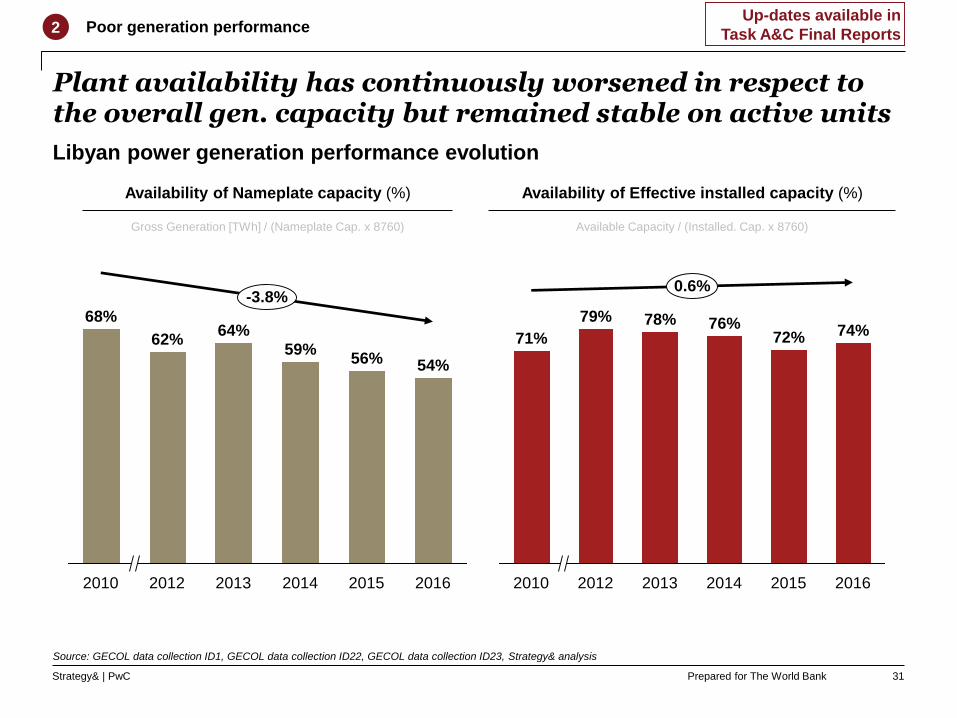

Plant availability has continuously worsened in respect to the overall gen. capacity but remained stable on active units

Availability of Nameplate capacity (%)

Source: GECOL data collection ID1, GECOL data collection ID22, GECOL data collection ID23, Strategy& analysis

-3.8%

56%

2014 2015

59%

2013 2016

54%

62%

2010

68%64%

2012

Gross Generation [TWh] / (Nameplate Cap. x 8760)

Poor generation performance2

Libyan power generation performance evolution

2010 2013 2014

71%

2012

0.6%

74%76%78%

2015 2016

79%

72%

Availability of Effective installed capacity (%)

Available Capacity / (Installed. Cap. x 8760)

31

Up-dates available in

Task A&C Final Reports

Prepared for The World BankStrategy& | PwC

Overall electricity generation has remained mostly stable since 2012, ranging between 36 and 38 TWh

10

5

20

40

35

30

25

15

0

TWh

2000 2015

37.7

2010

32.5

2013

37.9

15.3

2012

36.234.0

2005

36.4

22.4

-1%

20162014

Source: GECOL data collection ID24, Strategy& analysis

Slowly growing electricity generation3

Electricity generated

Electricity Generated (ID24)

Electricity generated (ID 37) 36.8 35.431.0 34.431.5 N/A

32

Prepared for The World BankStrategy& | PwC

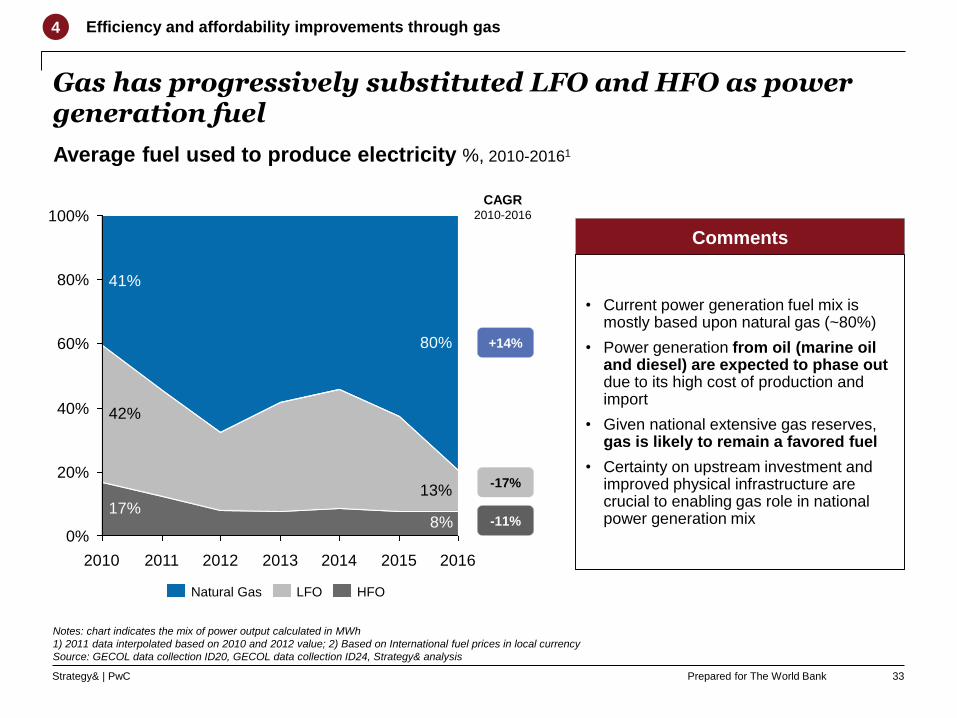

Gas has progressively substituted LFO and HFO as power generation fuel

+14%

-11%

CAGR2010-2016

Notes: chart indicates the mix of power output calculated in MWh

1) 2011 data interpolated based on 2010 and 2012 value; 2) Based on International fuel prices in local currency

Source: GECOL data collection ID20, GECOL data collection ID24, Strategy& analysis

-17%

Average fuel used to produce electricity %, 2010-20161

Efficiency and affordability improvements through gas4

8%17%

13%

42%

80%

41%80%

40%

20%

0%

60%

100%

2012 20132010 2011 201620152014

HFONatural Gas LFO

• Current power generation fuel mix is mostly based upon natural gas (~80%)

• Power generation from oil (marine oil and diesel) are expected to phase out due to its high cost of production and import

• Given national extensive gas reserves, gas is likely to remain a favored fuel

• Certainty on upstream investment and improved physical infrastructure are crucial to enabling gas role in national power generation mix

Comments

33

Prepared for The World BankStrategy& | PwC

18.436.0

18.418.418.4

2009-162006 2007 20082002-05

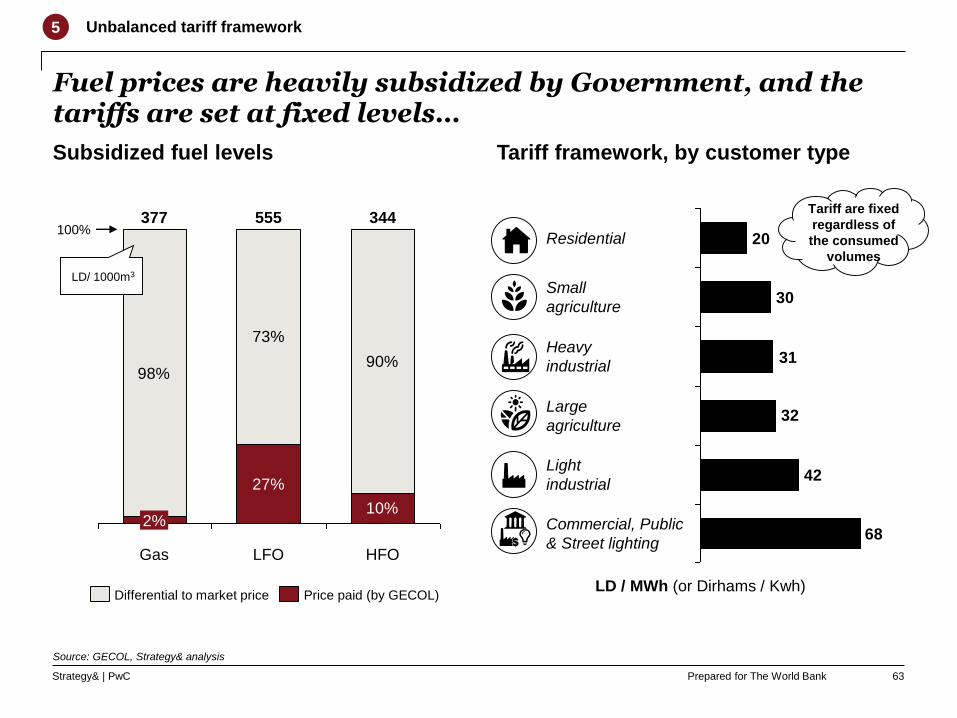

Fuels have remained at fixed prices well below market (but also officially-set?) levels

1) International fuel price in local currency; 2) In 2008, a Governement decree officially set a gas price increase which, however, was never implemented

Source: GECOL data collection ID20, Strategy& analysis

27%

10%

98%

73%

90%

100%

HFOLFOGas

2%

344555377

Price paid (by GECOL)Differential to international

fuel price in local currency

GECOL prices paid vs. market levels1

(2015, % and LD / m3 and LD/1000m3 for gas)

Fuel price evolution (GECOL price paid 2002-2016, market levels 2015)

8.48.48.4 8.4 20.0

NG

LD/ 1000m3

HFO

LD/ m3

LFO

LD/ m3

NOC has continued to

invoice GECOL the previous2

rate of 8.4 LD/ 1000m3

Market

price1

377.1

344.2

554.8

Efficiency and affordability improvements through gas4

LD/ 1000m3

34

150.0

56.036.066.0 86.0

Prepared for The World BankStrategy& | PwC

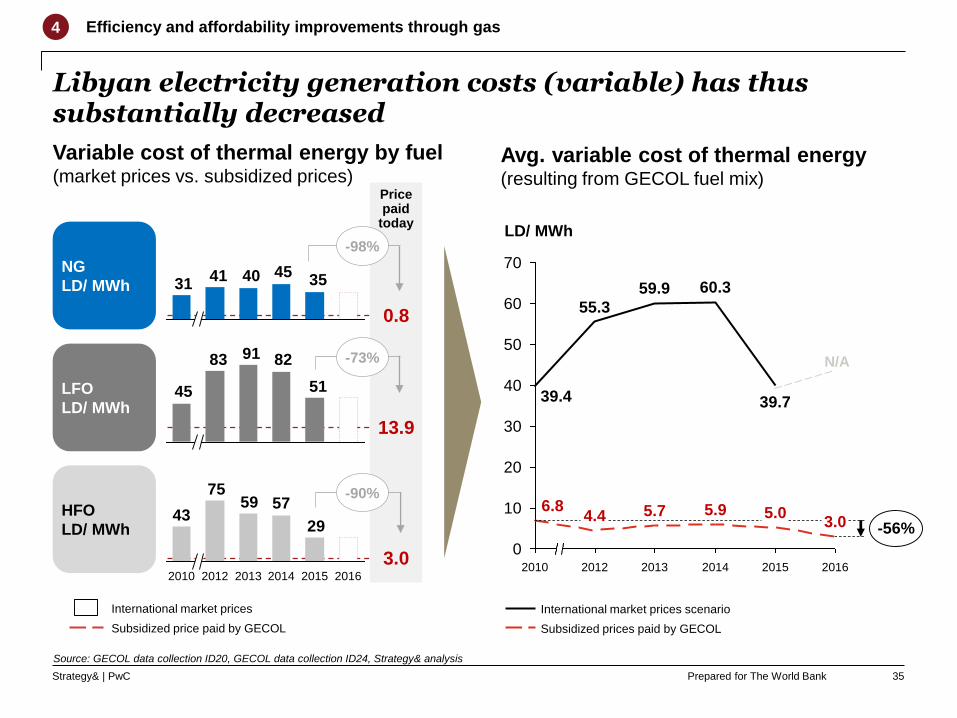

Libyan electricity generation costs (variable) has thus substantially decreased

35

Efficiency and affordability improvements through gas4

NG

LD/ MWh

HFO

LD/ MWh

LFO

LD/ MWh

Variable cost of thermal energy by fuel(market prices vs. subsidized prices)

0.8

13.9

3.0

35454041

31

29

575975

43

2010 2013 2014 201620152012

51

829183

45

Avg. variable cost of thermal energy(resulting from GECOL fuel mix)

Subsidized prices paid by GECOL

International market prices scenario

Source: GECOL data collection ID20, GECOL data collection ID24, Strategy& analysis

0

10

20

30

40

50

60

70

2012 20132010 2015 20162014

LD/ MWh

55.3

60.3

-56%5.0

39.7

4.4

59.9

3.05.95.76.8

39.4

N/A

-98%

-73%

-90%

International market prices

Subsidized price paid by GECOL

Price paid

today

Prepared for The World BankStrategy& | PwC

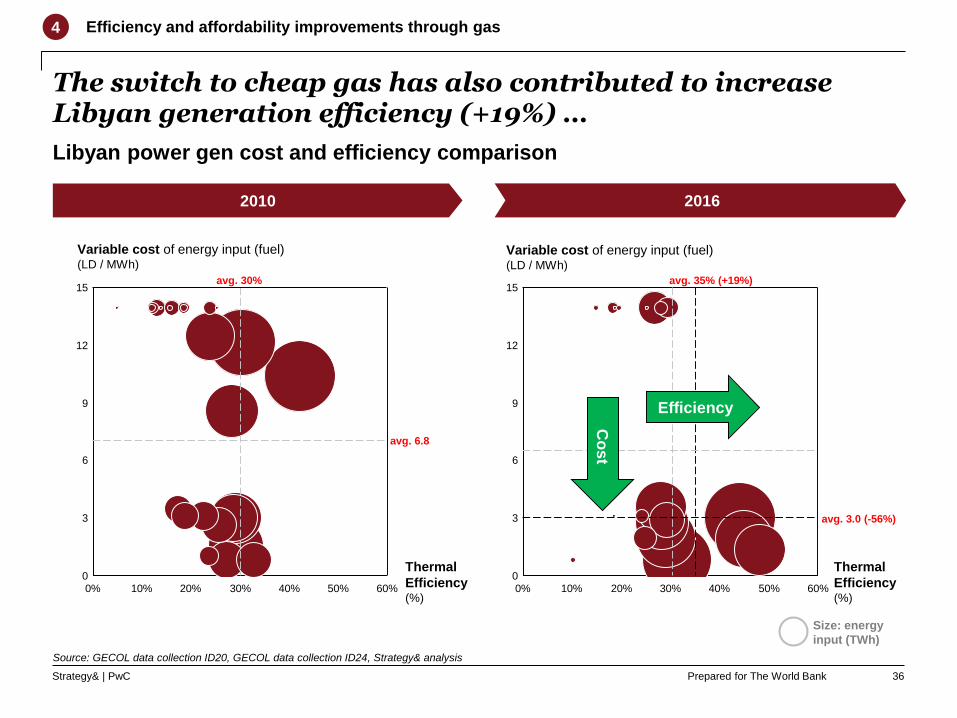

The switch to cheap gas has also contributed to increase Libyan generation efficiency (+19%) …

40%

15

12

6

9

3

060%30% 50%20%10%0% 60%

12

040%

15

6

3

30% 50%0%

9

20%10%

avg. 30% avg. 35% (+19%)

avg. 3.0 (-56%)

Variable cost of energy input (fuel)(LD / MWh)

Variable cost of energy input (fuel)(LD / MWh)

Thermal

Efficiency (%)

Thermal

Efficiency (%)

2010 2016

Co

st

Libyan power gen cost and efficiency comparison

Efficiency and affordability improvements through gas4

Source: GECOL data collection ID20, GECOL data collection ID24, Strategy& analysis

Efficiency

36

Size: energy

input (TWh)

avg. 6.8

Prepared for The World BankStrategy& | PwC

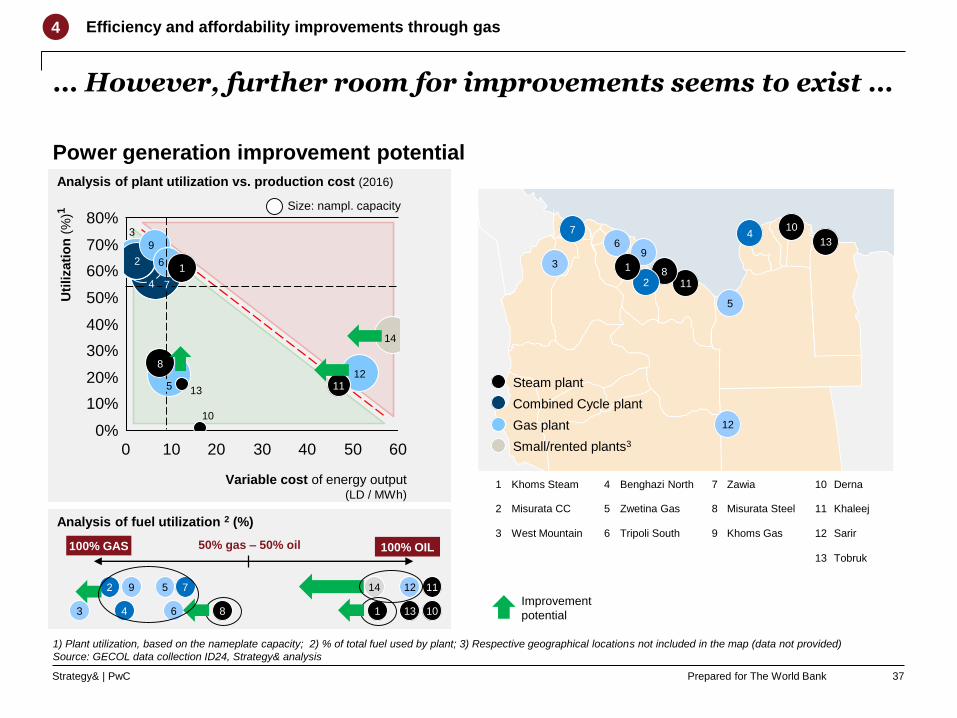

Analysis of plant utilization vs. production cost (2016)

Analysis of fuel utilization 2 (%)

… However, further room for improvements seems to exist …

1) Plant utilization, based on the nameplate capacity; 2) % of total fuel used by plant; 3) Respective geographical locations not included in the map (data not provided)

Source: GECOL data collection ID24, Strategy& analysis

Efficiency and affordability improvements through gas4

13

12

11

10

9

8

7

6

5

4

3

2

1

1

2

3

4

5

Khoms Steam

Misurata CC

West Mountain

Benghazi North

Zwetina Gas

6

7

8

9

10

Tripoli South

Zawia

Misurata Steel

Khoms Gas

Derna

11

12

13

Khaleej

Sarir

Tobruk

60

80%

30%

10%

0 10

20%

30

40%

0%

50%

60%

70%

504020

13

Uti

lizati

on

(%

)1

Variable cost of energy output(LD / MWh)

14

1

1211

7

5

3

9

8

4

2

10

6

Small/rented plants3

Combined Cycle plant

Gas plant

Steam plant

100% GAS 100% OIL

5

43 6 8

92 7 14 11

1 1013

12

50% gas – 50% oil

Power generation improvement potential

Size: nampl. capacity

Improvement

potential

37

Prepared for The World BankStrategy& | PwC

Khoms Steam 61%

Misurata CC 63%

Western Mountain 64%

Benghazi North 63%

Zwetina Gas 20%

Tripoli South 63%

Zawia 59%

Misurata Steel 25%

Khoms Gas 69%

Sarir 16%

Small/rented plants 35%

Derna 0.2%

Khaleej 21%

Tobruk 17%

… In 2016 for example, 18% of production was still generated by plants fueled with oil (possible gas supply constraints?)

38

2

120

503

403

1,052

223

1,144

299

395

194

304

177

0

2,484

Fuel type by plant (2016)

0

15

3,340

0

2,370

0

1,197

4,933

330

0

6,491

5,264

4,428

79

GAS-based production (MWh) OIL-based production (MWh)

6.6 TWh18% of total

production(2016)

13

12

11

10

9

8

7

6

5

4

3

2

1

14

Possible

constraints on

gas supply?

Utilization1

1) Plant utilization, based on the nameplate capacity

Source: GECOL data collection ID24, Strategy& analysis

Efficiency and affordability improvements through gas4

224 Mn LYD

Theoretical savings (2016). Scenario based on:

• CC plants 100% fueled with gas, at 85% utilization

• Sarir plant 100% fueled with gas, at 2016 utilization Gas plant

Small/rented plants

Steam plant

CC plant

Prepared for The World BankStrategy& | PwC

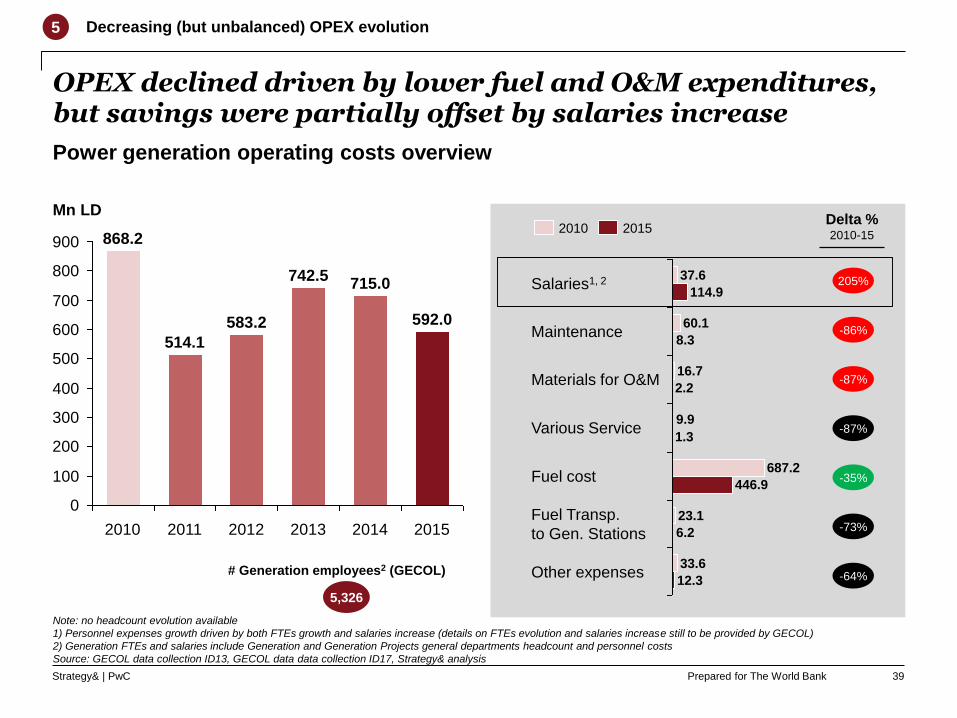

OPEX declined driven by lower fuel and O&M expenditures, but savings were partially offset by salaries increase

600

400

200

0

800

700

900

500

100

300

514.1

2010

868.2

2015

715.0

Mn LD

20142013

742.5

592.0

2012

583.2

2011

Power generation operating costs overview

33.6

687.2Fuel cost

23.1

16.7

6.2

Materials for O&M

Other expenses

Fuel Transp.

to Gen. Stations

446.9

Various Service

12.3

1.3

9.9

2.2

Maintenance8.3

37.6

60.1

Salaries1, 2114.9

20152010

5,326

# Generation employees2 (GECOL)

Delta %2010-15

205%

-86%

-35%

-73%

-87%

-87%

-64%

Note: no headcount evolution available

1) Personnel expenses growth driven by both FTEs growth and salaries increase (details on FTEs evolution and salaries increase still to be provided by GECOL)

2) Generation FTEs and salaries include Generation and Generation Projects general departments headcount and personnel costs

Source: GECOL data collection ID13, GECOL data data collection ID17, Strategy& analysis

Decreasing (but unbalanced) OPEX evolution5

39

Prepared for The World BankStrategy& | PwC

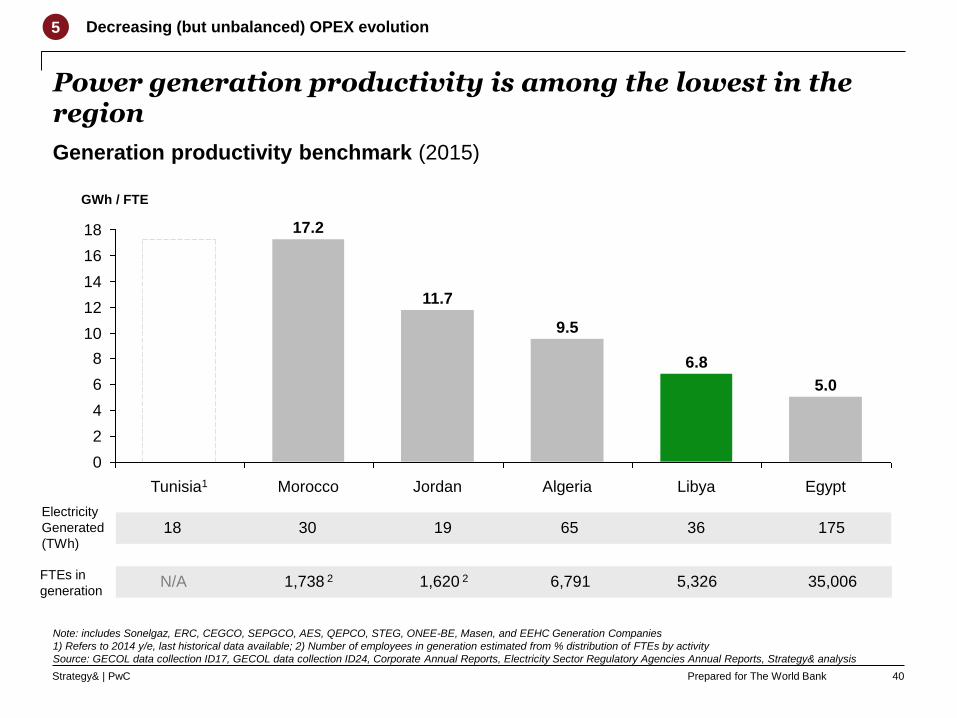

Power generation productivity is among the lowest in the region

Generation productivity benchmark (2015)

Note: includes Sonelgaz, ERC, CEGCO, SEPGCO, AES, QEPCO, STEG, ONEE-BE, Masen, and EEHC Generation Companies

1) Refers to 2014 y/e, last historical data available; 2) Number of employees in generation estimated from % distribution of FTEs by activity

Source: GECOL data collection ID17, GECOL data collection ID24, Corporate Annual Reports, Electricity Sector Regulatory Agencies Annual Reports, Strategy& analysis

18 30 19 65 17536Electricity

Generated

(TWh)

N/A 1,738 2 1,620 2 6,791 5,326 35,006FTEs in

generation

0

2

4

6

8

10

12

14

16

18

Tunisia1

6.8

Libya

17.2

Jordan

9.5

Algeria

11.7

Morocco

GWh / FTE

Egypt

5.0

Decreasing (but unbalanced) OPEX evolution5

40

Prepared for The World BankStrategy& | PwC

Projects execution lagged behind plan, with only 23% of the planned investments for 2010-2016 being actually realized

Planned capacity expansions (nameplate) vs. realized GW, 2010-2016

2

94

5

Under

Construction

& Contracted

2010-2016

77%

Actually

realized

2010-20164

Total Planned,

contracted

and under

construction

2010-2016

Planned

Projects

2010-2016

PlannedGeneration

typeMW1,2 On-line

date

Misurata II Combined

Cycle

750 2014

Militah 1400 2015

Bumba Gulf - 1,500 2015

Tripoli East Steam 350 2018

Under construction

and contracted

Generation

typeMW1,2 On-line

date

Sarir

Gas

285 2011

Ubari 750 2012

Misurata I

Combined

Cycle

250 2011

Benghazi North II 250 2011

Zwetina I 250 2013

Khaleej (or Gulf)

Steam

1,400 2013

Tripoli West II 1,400 2014

1) Nameplate capacity breakdown by plant still to be provided (data to be confirmed)

2) Considering the entry into force at full capacity;

3) Plant extension has been fully commissioned but due to technical or operational problems some unit

Are either suspended, out of service or not operational; full operation is thus estimated in 2017

4) Data inconsistency about nameplate capacity to be resolved (possibly includes also additional plants)

Source: GECOL data collection ID1, GECOL presentation (2010), Strategy& analysis

Old plan

Delays in project execution6

Projects planned in 2010, fully finalized in 2016

Projects planned in 2010, partially finalized in 2016

Projects planned in 2010, still not operative in 2016

3

3

41

Up-dates available in

Task A&C Final Reports

Prepared for The World BankStrategy& | PwC

Since 2012, Government did not always approve the

CAPEX actually expensed by GECOL

CAPEX slowed down substantially, and despite this the expenditures were not always fully ratified by Government

Generation CAPEX evolution1

Note: In accordance with Libyan subsidized tariff framework, to date all investment in electricity infrastructure (incl. generation capacity) has been made by Gov’t, either directly or

indirectly; CAPEX is normally compensated to GECOL ex-post, with Ministry of planning approving the proposed CAPEX budget, and Ministry of Finance allocating such funding

Sources: GECOL data collection ID15, Strategy& analysis

0

1,000

500

2,000

1,500

2010 2011

502

1,936

137

1,191

2012

485

2013

704

2015

-36%

1,223

20162014

Mn LD

CAPEX (effectively expensed by sector opreator) CAPEX approved by Government

Delays in project execution6

42

Prepared for The World BankStrategy& | PwC

Going forward, GECOL relies upon a significant capacity increase plan (name-plate) …

Source: GECOL data collection ID1, GECOL data collection ID23, GECOL presentation (2010 ), Strategy& analysis

PlannedGeneration

typeMW

On-line

date

Tripoli East

Steam

1,400 2021

Tobruk 700 2021

Derna 700 2022

Benghazi West 1,400 2026

SabhaGas

855 2021

Tripoli South II 855 2023

Misurata II

Combined

Cycle

750 2021

Militah 1,640 2021

Zwetina II 820 2021

Tubrok 820 2022

AbouKammash 820 2025

Under construction

and commissioning

Generation

typeMW

On-line

date

KhaleejSteam

1,050 2019

Tripoli West II 1,400 2020

Ubari

Gas

470 2018

Ubari 154 2017

Alhoms II 524 2017

Tripoli South I 141 2017

Zahra 94 2017

Nameplate capacity planned expansion GW, 2017-2030

Significant but outdated investments plans towards 20307

8

-2

12

4

2

6

10

0

14

1614.6

0.9

2030

2027

2029

2028

2026

0.7

2025

13.9

0.6

2024

3.3

2022

-0.2

0.6

2023

-0.2

12.413.0

10.3

11.8

1.5

2020

0.9

2021

0.9

-1.3-0.6

1.1

-0.3

1.8

2018

0.8

2019

2017

0.4

2.0

7.0

4.6

1.7

Divestments

Under constr. & contr.

Planned

New capacity (nameplate, cumulated)

43

Up-dates available in

Task A&C Final Reports

Prepared for The World BankStrategy& | PwC

Demand

Generation

Transmission

Distribution and supply

Supply / demand balance

Governance and sector structure

References for analysis update

44

Prepared for The World BankStrategy& | PwC

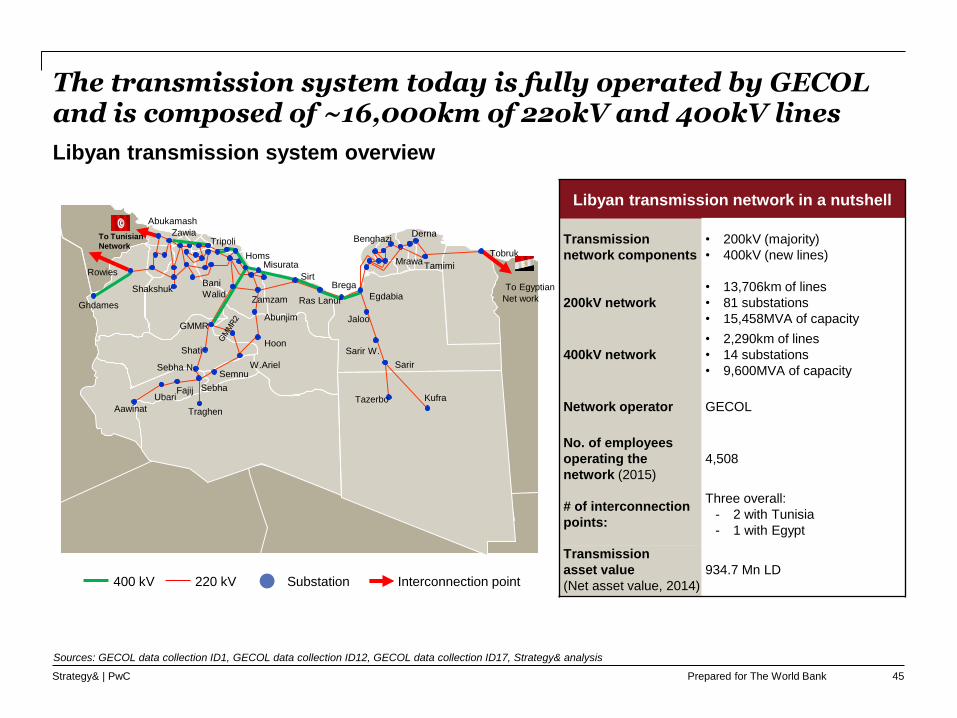

The transmission system today is fully operated by GECOL and is composed of ~16,000km of 22okV and 400kV lines

Libyan transmission network in a nutshell

Transmission

network components

• 200kV (majority)

• 400kV (new lines)

200kV network

• 13,706km of lines

• 81 substations

• 15,458MVA of capacity

400kV network

• 2,290km of lines

• 14 substations

• 9,600MVA of capacity

Network operator GECOL

No. of employees

operating the

network (2015)

4,508

# of interconnection

points:

Three overall:

- 2 with Tunisia

- 1 with Egypt

Transmission

asset value

(Net asset value, 2014)

934.7 Mn LD

Libyan transmission system overview

400 kV 220 kV Interconnection pointSubstation

Sources: GECOL data collection ID1, GECOL data collection ID12, GECOL data collection ID17, Strategy& analysis

Kufra

Sarir W.

Benghazi

Egdabia

Sirt

Hoon

GMMR

Homs

TripoliZawia

Tobruk

Sebha

To Tunisian

Network

Tazerbo

Sarir

Jaloo

Brega

Ras LanufZamzam

Abunjim

W.Ariel

Traghen

Semnu

Shati

FajijUbari

Aawinat

Bani

Walid

TamimiMrawa

Derna

Misurata

Abukamash

Shakshuk

Rowies

Sebha N.

Ghdames

To Egyptian

Net work

45

Prepared for The World BankStrategy& | PwC

• Network has suffered from substantial damages in the past years, which caused inefficiencies to

the grid operation & management

• Libyan transmission losses have remained constant at pre-2011 levels at ~1.8%

• Technical performance is in line with regional peers

• Transmission OPEX are continuously increasing, driven by salaries

The results of the rapid assessment of the Libyan transmission sector can be summarized in 4 key areas

Summary of rapid assessment of transmission sector

Stable technical

performance

Continuous cost

increase

Structurally weak /

damaged network

• CAPEX in transmission have substantially decreased

• Government has not always approved CAPEX actually expended by the sector operator

• GECOL is pursuing plans to reinforce the transmission system with 400kV lines, but the status of

implementation is uncertain and seems to lag behind

Decreasing

investments and

unclear new

projects status

1

3

4

2

46

Up-dates available in

Task A&C Final Reports

Prepared for The World BankStrategy& | PwC

In the last years the transmission system has suffered from damages, evidencing structural weaknesses

Structural network weaknesses

Structurally weak / damaged network1

Sources: GECOL data collection ID2, GECOL data collection ID22, Strategy& analysis

Issues / damages occurred in the period 2011-2016

Damages / issues overview

• Since 2011 the Libyan transmission system

suffered many incidence of damage due to:

– Military clashes between factions

– Acts of vandalism and theft

• Overall lines, sub-stations & cables were affected

• Incidents led to isolation of complete regions until

GECOL was able to repair or replace the

damaged infrastructure (in some cases repairs

took several months or even years)

• Most severe and longest lasting cases are

damages in the south and west of Benghazi city in

2014/2015 (yellow circle in the map), which led to:

– Separation of network into an Eastern and

Western section

– Load shedding in Benghazi

– Shortages in generation in the Western

network and consequent load shedding

• Other damages to the transmission have led to

prolonged outages in the south western and south

eastern regions, with consequent isolation of

power plants or reduction in supplies

• In almost every case GECOL has been able to

eventually repair, replace or compensate for the

damaged parts of the network

400 kV 220 kV Interconnection pointSubstation

Kufra

Sarir W.

Benghazi

Egdabia

Sirt

Hoon

GMMR

Homs

TripoliZawia

Tobruk

Sebha

To Tunisian

Network

Tazerbo

Sarir

Jaloo

Brega

Ras LanufZamzam

Abunjim

W.Ariel

Traghen

Semnu

Shati

FajijUbari

Aawinat

Bani

Walid

TamimiMrawa

Derna

Misurata

Abukamash

Shakshuk

Rowies

Sebha N.

Ghdames

To Egyptian

Net work

47

Prepared for The World BankStrategy& | PwC

Technical performances remained constant, with losses generally maintained at pre-2011 levels

Stable technical performance2

1.0%

2.5%

1.5%

0.0%

0.5%

2.0%

3.0%

1.8% 1.7%

2.5%

2014

1.7%

1.8%

1.8%

201520132012

2.5%

(%)2

1.6%

2011

2.4%

1.7%

1.7%

2010

25

10

5

30

40

20

35

15

0

TWh and %

Electricity

generated

(ID37)

34.81.8%35.4

Electricity

entered the

distribution

network

98.2%

-0.6

Transmission

Losses

100%

1) Transmission losses are assumed by GECOL based on the load flow studies (further investigations ongoing); 2) Transmission losses: (net electricity generated – electricity

entered the distribution network) / (net electricity generated); 3) Additional transmission losses if generation data from ID24 is considered (delta ID24 vs. ID37 is proportionally

distributed between transmission and Distribution losses of ID37); Source: GECOL data collection ID24, GECOL data collection ID37, Strategy& analysis

Evolution of transmission losses1 Electricity entering distribution system (2015)

Transmission Losses incidence on Generation (ID37)

Inconsistency vs. Generation (ID24)3

36.2 TWh

(ID 24)

48

PRELIMINARY

Prepared for The World BankStrategy& | PwC

Performances showed are in line with regional peers

0%

5%

10%

15%

20%

25%

30%

35%

40%

500200 4001000 300

Total Length of the T&D System (‘000 km)

Transmission grid length (%)

as % of total T&D grid length

JordanEgypt

Tunisia1

Morocco

Libya

Algeria

4%

4%

4%

2%

2%

2%

3%0% 4% 5%2%1%

Jordan

Egypt

Tunisia1

Libya

Morocco

Algeria

Note: includes Sonelgaz, NEPCO, STEG, ONEE-BE and Egyptian Electricity Transmission Company

1) Data refers to STEG annual report 2014, last available data point; 2) Indicate numbers are estimated

Sources: GECOL data collection ID1 and ID37, BMI Research Database, Corporate Annual Reports, Electricity Sector Regulatory Agencies Annual Reports, Strategy& analysis

Benchmarking sample (2015) Transmission losses benchmarking (2015) 2

Stable technical performance2

49

PRELIMINARY

Prepared for The World BankStrategy& | PwC

OPEX have continuously increased, mostly driven by salaries

140

120

100

80

60

40

20

0

92.8

Mn LD

2014

130.4

2010 2012

113.1

20152013

128.5

69.6

119.2

+6.7%

2011

Continuous cost increase3

Transmission O&M cost overview

Fuel Transp.

to Gen. Stations 0

0

Other expenses

11.4

Materials for O&M

4.1

0.3

0.4

6.2

16.0

Maintenance

Fuel cost

Salaries1

0.8

108.0

37.6

Various Service

18.6

13.9

4.0

20152010

4,508

# Transmission FTEs1 (GECOL) - 2016

Delta %2010-15

+187%

-39%

+74%

N.A.

-74%

-96%

-71%

Note: No headcount evolution available

1) Transmission FTEs and salaries include Transmission, Transmission Projects and Control general departments headcount and personnel costs

Source: GECOL data collection ID13, GECOL data collection ID17, Strategy& analysis

50

Prepared for The World BankStrategy& | PwC

Since 2012, Government did not always approve the

CAPEX actually expensed by GECOL

CAPEX in the transmission sector slowed down substantially and was not always fully approved by Government …

Transmission CAPEX evolution1

Note: In accordance with the Libyan subsidized tariff framework, CAPEX expenses are separately covered by the government through ad-hoc capital injections; CAPEX is normally

compensated to the sector operator (GECOL) ex-post, with Ministry of planning approving the proposed CAPEX budget, and Ministry of Finance allocating such funding

1) Includes both new transmission grids investments and major overhauls; data on the exact split of the two components has not been received

Sources: GECOL data collection ID15, Strategy& analysis

400

600

1,000

1,200

800

0

200

1,100

300

500

900

100

700

Mn LD

20162015

-35%

86

191

20112010

484

2012 2013

305

163

1,174

2014

446

CAPEX approved by GovernmentCAPEX (effectively expensed by sector opreator)

Decreasing investments and unclear new projects status4

51

Prepared for The World BankStrategy& | PwC

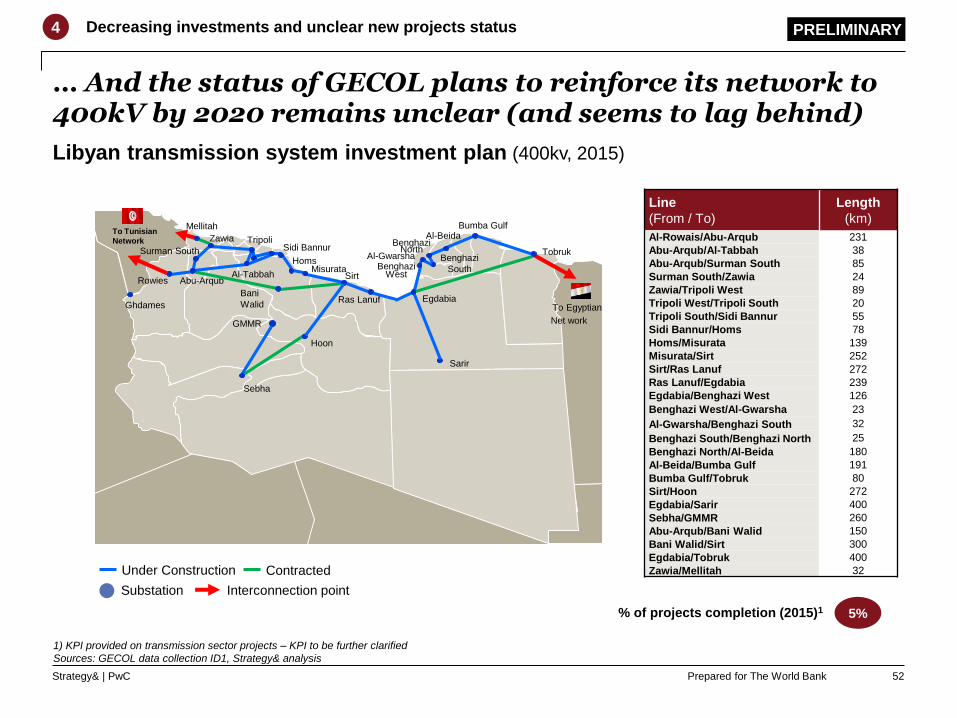

… And the status of GECOL plans to reinforce its network to 400kV by 2020 remains unclear (and seems to lag behind)

Libyan transmission system investment plan (400kv, 2015)

Under Construction Contracted

Interconnection pointSubstation

Line

(From / To)

Length

(km)

Al-Rowais/Abu-Arqub 231

Abu-Arqub/Al-Tabbah 38

Abu-Arqub/Surman South 85

Surman South/Zawia 24

Zawia/Tripoli West 89

Tripoli West/Tripoli South 20

Tripoli South/Sidi Bannur 55

Sidi Bannur/Homs 78

Homs/Misurata 139

Misurata/Sirt 252

Sirt/Ras Lanuf 272

Ras Lanuf/Egdabia 239

Egdabia/Benghazi West 126

Benghazi West/Al-Gwarsha 23

Al-Gwarsha/Benghazi South 32

Benghazi South/Benghazi North 25

Benghazi North/Al-Beida 180

Al-Beida/Bumba Gulf 191

Bumba Gulf/Tobruk 80

Sirt/Hoon 272

Egdabia/Sarir 400

Sebha/GMMR 260

Abu-Arqub/Bani Walid 150

Bani Walid/Sirt 300

Egdabia/Tobruk 400

Zawia/Mellitah 32

PRELIMINARY

1) KPI provided on transmission sector projects – KPI to be further clarified

Sources: GECOL data collection ID1, Strategy& analysis

Decreasing investments and unclear new projects status4

5%% of projects completion (2015)1

BenghaziNorth

Egdabia

Sirt

Hoon

Homs

TripoliZawia

Tobruk

Sebha

To Egyptian

Net work

Sarir

Ras LanufBani

Walid

Misurata

Surman South

Abu-ArqubRowies

Ghdames

Sidi Bannur

BenghaziWest

Al-Gwarsha Benghazi

South

Al-BeidaBumba GulfMellitah

To Tunisian

Network

Al-Tabbah

GMMR

52

Prepared for The World BankStrategy& | PwC

Demand

Generation

Transmission

Distribution and supply

Supply / demand balance

Governance and sector structure

References for analysis update

53

Prepared for The World BankStrategy& | PwC

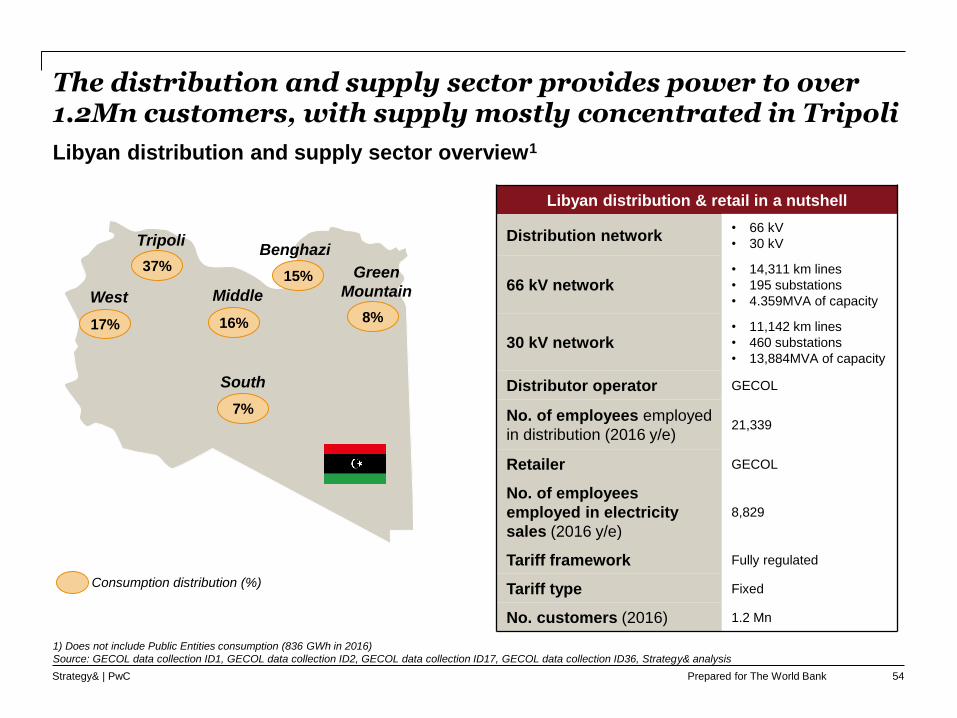

The distribution and supply sector provides power to over 1.2Mn customers, with supply mostly concentrated in Tripoli

Libyan distribution & retail in a nutshell

Distribution network• 66 kV

• 30 kV

66 kV network• 14,311 km lines

• 195 substations

• 4.359MVA of capacity

30 kV network• 11,142 km lines

• 460 substations

• 13,884MVA of capacity

Distributor operator GECOL

No. of employees employed

in distribution (2016 y/e)21,339

Retailer GECOL

No. of employees

employed in electricity

sales (2016 y/e)

8,829

Tariff framework Fully regulated

Tariff type Fixed

No. customers (2016) 1.2 Mn

Libyan distribution and supply sector overview1

Consumption distribution (%)

17%

West

8%

Green

Mountain

37%

Tripoli

16%

Middle

7%

South

Benghazi

15%

1) Does not include Public Entities consumption (836 GWh in 2016)

Source: GECOL data collection ID1, GECOL data collection ID2, GECOL data collection ID17, GECOL data collection ID36, Strategy& analysis

54

Prepared for The World BankStrategy& | PwC

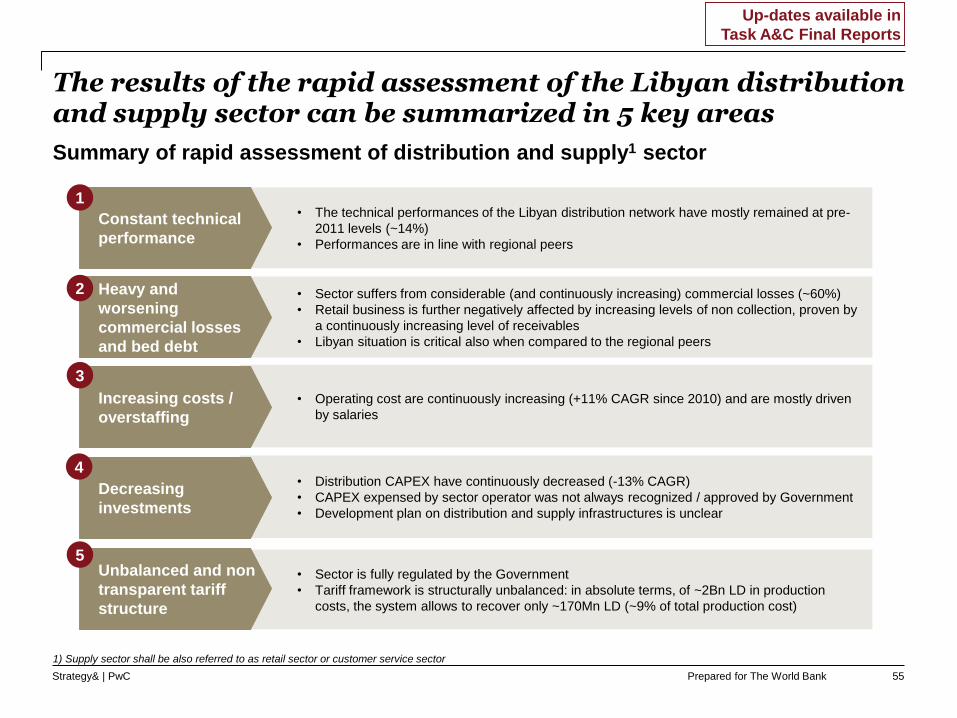

• Sector suffers from considerable (and continuously increasing) commercial losses (~60%)

• Retail business is further negatively affected by increasing levels of non collection, proven by

a continuously increasing level of receivables

• Libyan situation is critical also when compared to the regional peers

• Operating cost are continuously increasing (+11% CAGR since 2010) and are mostly driven

by salaries

• Sector is fully regulated by the Government

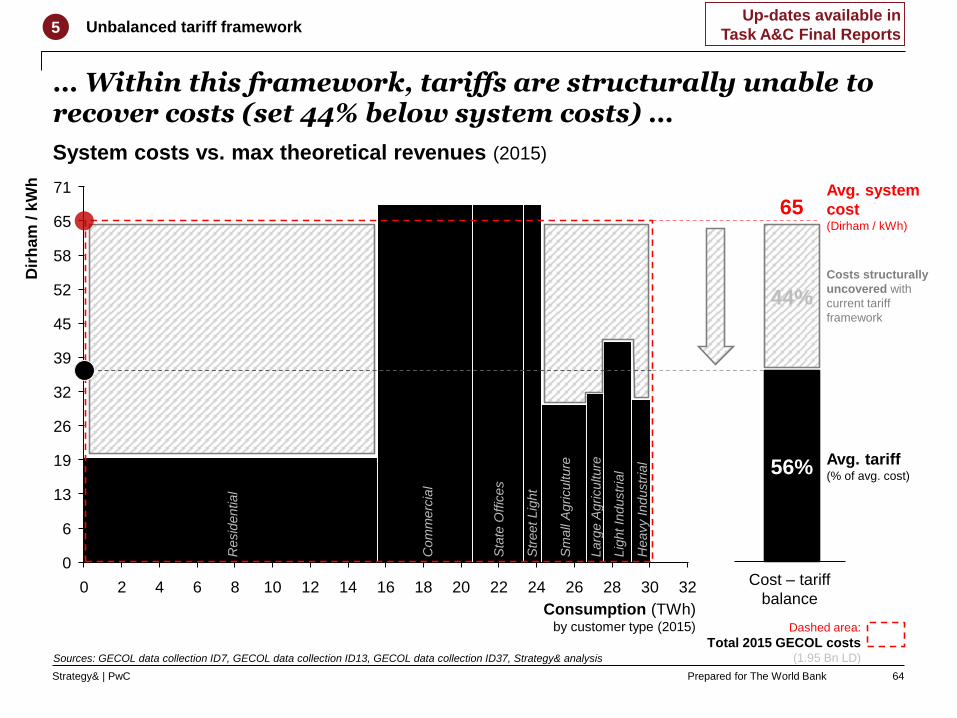

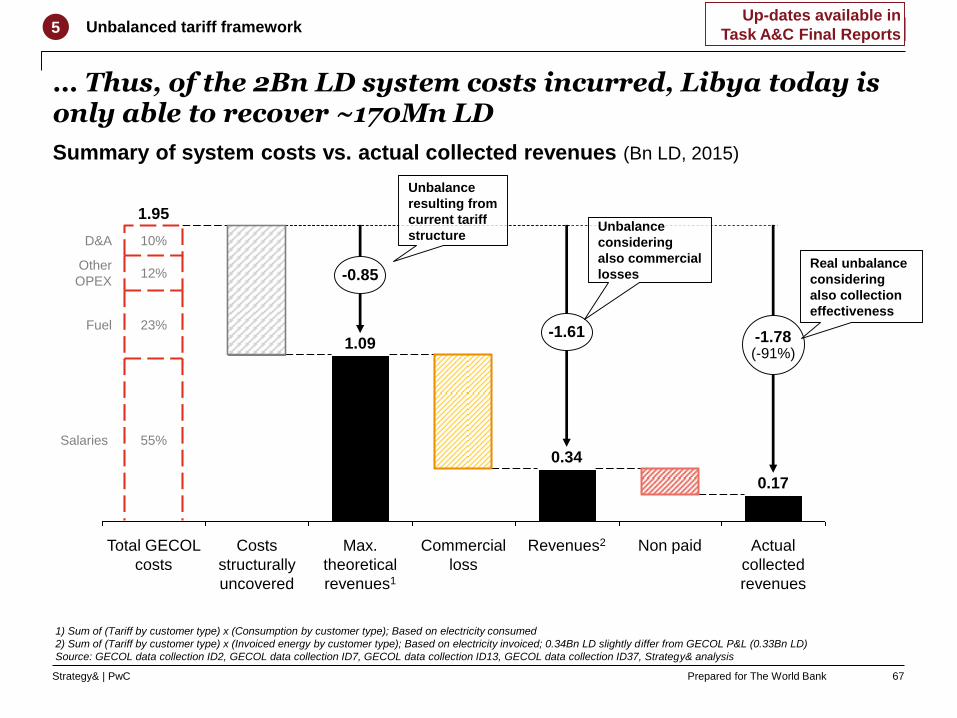

• Tariff framework is structurally unbalanced: in absolute terms, of ~2Bn LD in production

costs, the system allows to recover only ~170Mn LD (~9% of total production cost)

The results of the rapid assessment of the Libyan distribution and supply sector can be summarized in 5 key areas

Summary of rapid assessment of distribution and supply1 sector

Increasing costs /

overstaffing

Unbalanced and non

transparent tariff

structure

Heavy and

worsening

commercial losses

and bed debt

• The technical performances of the Libyan distribution network have mostly remained at pre-

2011 levels (~14%)

• Performances are in line with regional peers

Constant technical

performance

• Distribution CAPEX have continuously decreased (-13% CAGR)

• CAPEX expensed by sector operator was not always recognized / approved by Government

• Development plan on distribution and supply infrastructures is unclear

Decreasing

investments

2

3

5

1

4

1) Supply sector shall be also referred to as retail sector or customer service sector

55

Up-dates available in

Task A&C Final Reports

Prepared for The World BankStrategy& | PwC

The technical performance of the distribution network have remained at pre-2011 levels …

0%

5%

10%

15%

20%

12.3%13.4%12.9%13.7%12.8%

19.3%

13.8%

2014 2015

12.9%

2010 2012

18.5%

13.1%

2011

18.9%

(%)2

2013

10

5

35

0

25

30

40

20

15

-4.7

13.4%

TWh and %

1.8%

Transmission

Losses

35.4

Electricity

generated

(ID37)

-0.6

100%84.8%

Distribution

Losses

30.1

Electricity

consumed

1) Distribution losses assumed with measurements made by GECOL (further investigations ongoing); 2) Distribution losses: (electricity consumed – net electricity generated) / (net

electricity generated); 3) Additional distribution losses if generation data from ID24 is considered (delta ID24 vs. ID37 is proportionally distributed between transmission and

distribution losses of ID37); Source: GECOL data collection ID2, ID24, ID37, Strategy& analysis

Distribution Losses incidence on Generation (ID37)

Inconsistency vs. Generation (ID24) 3

Evolution of Libyan distribution losses1 Electricity consumed vs. generated (2015)

Constant technical performance1

36.2 TWh

(ID 24)

56

Prepared for The World BankStrategy& | PwC

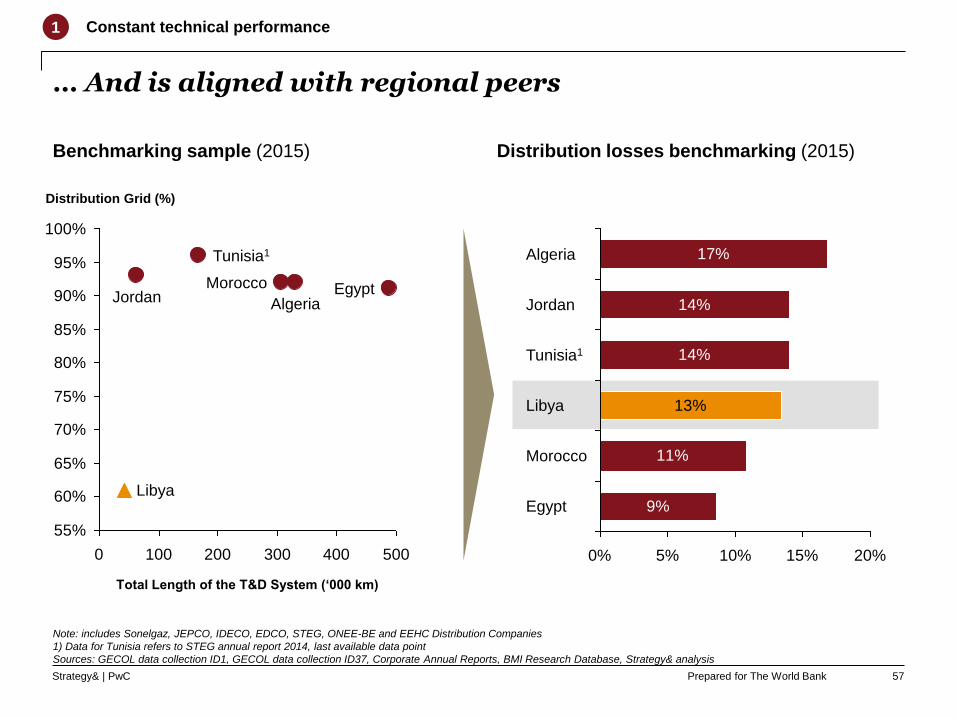

… And is aligned with regional peers

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

5004003002001000

Distribution Grid (%)

Total Length of the T&D System (‘000 km)

Morocco Egypt

Tunisia1

Libya

AlgeriaJordan

17%

14%

14%

11%

9%

13%

5%0% 10% 15% 20%

Tunisia1

Jordan

Algeria

Egypt

Libya

Morocco

Note: includes Sonelgaz, JEPCO, IDECO, EDCO, STEG, ONEE-BE and EEHC Distribution Companies

1) Data for Tunisia refers to STEG annual report 2014, last available data point

Sources: GECOL data collection ID1, GECOL data collection ID37, Corporate Annual Reports, BMI Research Database, Strategy& analysis

Benchmarking sample (2015) Distribution losses benchmarking (2015)

1 Constant technical performance

57

Prepared for The World BankStrategy& | PwC

The distribution and supply business is affected by huge commercial losses …

0%

10%

20%

30%

40%

50%

60%

70%

2014

47%

2010 2015

60%

2012

41%

65%

24%

20132011

20%

(%)1

1) Commercial losses: (electricity consumed – electricity invoiced) / (net electricity generated);

2) Different from Commercial losses incidence (%) calaculated in ID37, which are based only on a part of Total energy generated (i.e. excluding energy generated at 34-66kV)

Source: GECOL data collection ID37, Strategy& analysis

Commercial Losses incidence on Generation (ID37)

Heavy and worsening commercial losses and bed debt2

Evolution of Libyan commercial losses Electricity generated vs. invoiced (2015)

0

30

10

15

40

35

20

25

5

Commercial

Losses2

8.9

60%100%

25%

35.4

15%

Technical

Losses

Electricity

generated

(ID37)

-5.4

-21.1

Electricity

invoiced

TWh and %

36.2 TWh

(ID 24)

58

Prepared for The World BankStrategy& | PwC

… Further aggravated by increasing bed debt

2

Electricity collected vs. generated (e2015)

1) Non paid (%): (electricity invoiced – electricity collected) / (net generation);

2) Estimation based on revenues collected (only partial breakdown by sector available) and current tariff structure

Source: GECOL data collection ID7, GECOL data collection ID12, GECOL data collection ID21, GECOL data collection ID37, Strategy& analysis

15

35

20

40

25

30

10

0

5

100%

-21.1

Comm.

Losses

Electricity

generated

(ID37)

Non paid1

5.62

Techn.

Losses

Electricity

collected

TWh & %

15%

-3.4 15%

10%2

35.4

-5.4

60%

36.2 TWh

(ID 24)

Heavy and worsening commercial losses and bed debt

2,400

0

800

600

200

400

1,000

1,200

1,400

1,600

1,800

2,000

2,200

1,320

1,928

2010

1,611

2011

15%

1,971

2013

2,269

2014 2015

Mn LD

2012

Evolution of GECOL receivables

N/AReceivables

59

Prepared for The World BankStrategy& | PwC

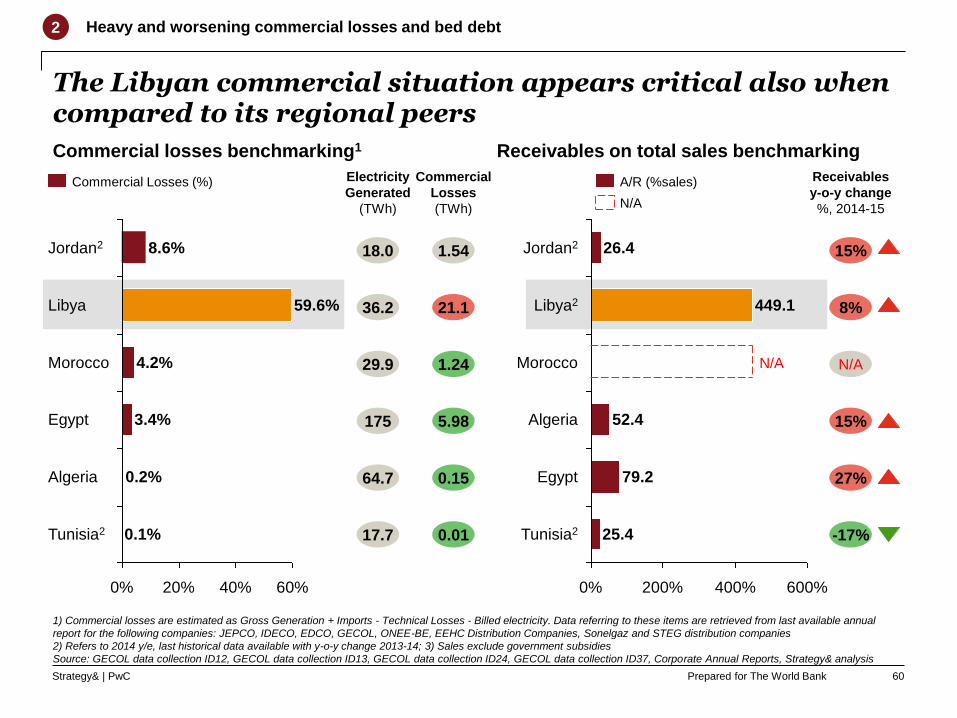

The Libyan commercial situation appears critical also when compared to its regional peers

Commercial losses benchmarking1 Receivables on total sales benchmarking

60%40%20%0%

Tunisia2 0.1%

Jordan2

4.2%

Libya

Algeria 0.2%

3.4%Egypt

Morocco

59.6%

8.6%

1) Commercial losses are estimated as Gross Generation + Imports - Technical Losses - Billed electricity. Data referring to these items are retrieved from last available annual

report for the following companies: JEPCO, IDECO, EDCO, GECOL, ONEE-BE, EEHC Distribution Companies, Sonelgaz and STEG distribution companies

2) Refers to 2014 y/e, last historical data available with y-o-y change 2013-14; 3) Sales exclude government subsidies

Source: GECOL data collection ID12, GECOL data collection ID13, GECOL data collection ID24, GECOL data collection ID37, Corporate Annual Reports, Strategy& analysis

Electricity

Generated

(TWh)

Commercial

Losses

(TWh)

0% 400% 600%200%

Egypt

Libya2

Tunisia2

Algeria

Morocco

Jordan2

79.2

N/A

26.4

25.4

52.4

449.1

15%

8%

N/A

15%

27%

-17%

Receivables

y-o-y change

%, 2014-15N/A

A/R (%sales)

18.0

36.2

29.9

175

64.7

17.7

1.54

21.1

1.24

5.98

0.15

0.01

Commercial Losses (%)

2 Heavy and worsening commercial losses and bed debt

60

Prepared for The World BankStrategy& | PwC

Operating costs have continuously increased, mostly driven by salaries

100

800

700

500

600

0

200

400

300

245

711

466

369

100

423482

2011

269

2010

110

2012

312

177 173

687

514

174

2013

548

2014

658

2015

722

11%Mn LD

Distribution & supply operating costs evolution

21,339# sector employees1

(GECOL)

3

8,829

Distribution

Supply

Increasing costs / overstaffing

634Salaries1

Fuel cost1

23

Fuel Transp.

to Gen. Stations

Other expenses23

246

00

43

Materials for O&M

Various Service10

1

Maintenance5325

284

2010 2015Delta %2010-15

+157%

+113%

+8%

N/A

-77%

-98%

-2%

1) Distribution FTEs and salaries include Distribution, Distribution Projects and Medium Voltage general departments headcount and personnel costs

Source: GECOL data collection ID13, GECOL data collection ID17, Strategy& analysis

61

Prepared for The World BankStrategy& | PwC

Since 2012, Government did not always approve the

CAPEX actually spent by GECOL

Distribution sector CAPEX have slowed down since 2010, and was not always fully approved by Government

Decreasing investments and unclear development plan4