TACO BELL INVESTOR DAY - corporate-ir. · PDF fileYum! Profits Driven By China, YRI, and U.S....

64

TACO BELL INVESTOR DAY Tim Jerzyk SVP, Investor Relations

Transcript of TACO BELL INVESTOR DAY - corporate-ir. · PDF fileYum! Profits Driven By China, YRI, and U.S....

TACO BELL INVESTOR DAY

Tim Jerzyk

SVP, Investor Relations

Information herein is as of 2/17/11

This presentation will include forward-looking statements

that reflect management’s expectations based on currently

available data. However, actual results are subject to

future events and uncertainties. The information in the

presentation related to projections or other forward-looking

statements which may cause actual results to differ

materially are subject to the safe harbor statement posted

on our Web site: www.yum.com.

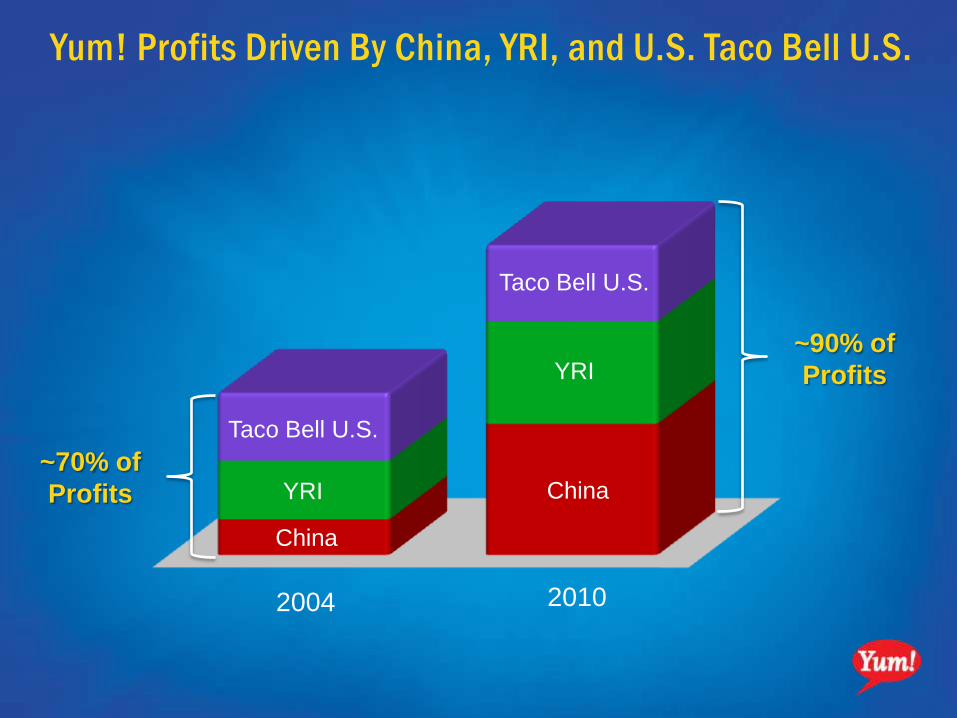

Yum! Profits Driven By China, YRI, and U.S. Taco Bell U.S.

Taco Bell U.S.

Taco Bell U.S.

YRI

YRI

China

China

2004 2010

~90% of

Profits

~70% of

Profits

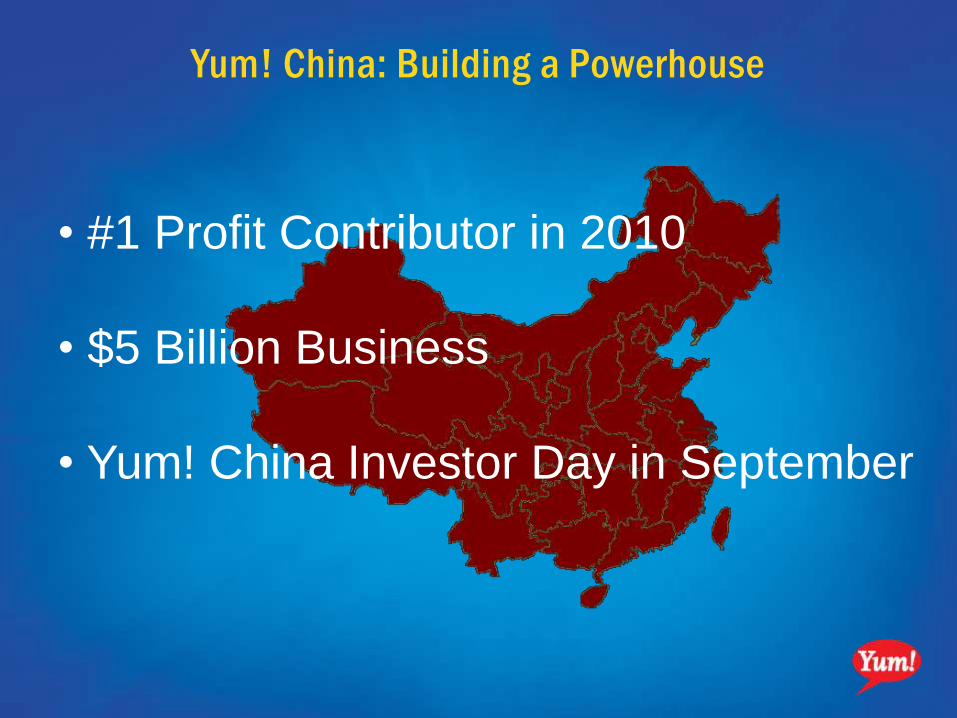

Yum! China: Building a Powerhouse

• #1 Profit Contributor in 2010

• $5 Billion Business

• Yum! China Investor Day in September

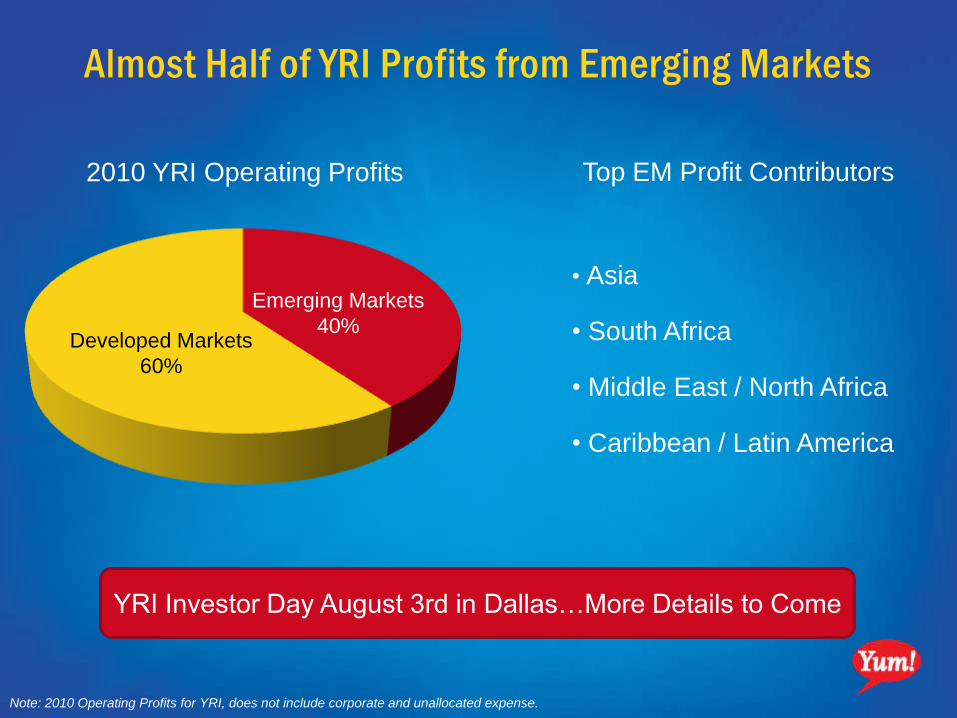

Almost Half of YRI Profits from Emerging Markets

Developed Markets

60%

Emerging Markets

40%

Note: 2010 Operating Profits for YRI, does not include corporate and unallocated expense.

2010 YRI Operating Profits Top EM Profit Contributors

• Asia

• South Africa

• Middle East / North Africa

• Caribbean / Latin America

YRI Investor Day August 3rd in Dallas…More Details to Come

Refranchising Has Transformed U.S. Division

25% 24% 24%

21%

8% 7%

18%

16%

5%

2007 2010 2011 & Beyond

% of Company Ownership by Brand

2011 Focus on KFC

13.3%

0.5%

0.5%

(0.5%)

14.2%

Refranchising Improved U.S. Restaurant Margins

2008 201020092007

U.S. Rest. Margin

2010

U.S. Rest.

Margin

0.4%

Other

Impact of Refranchising

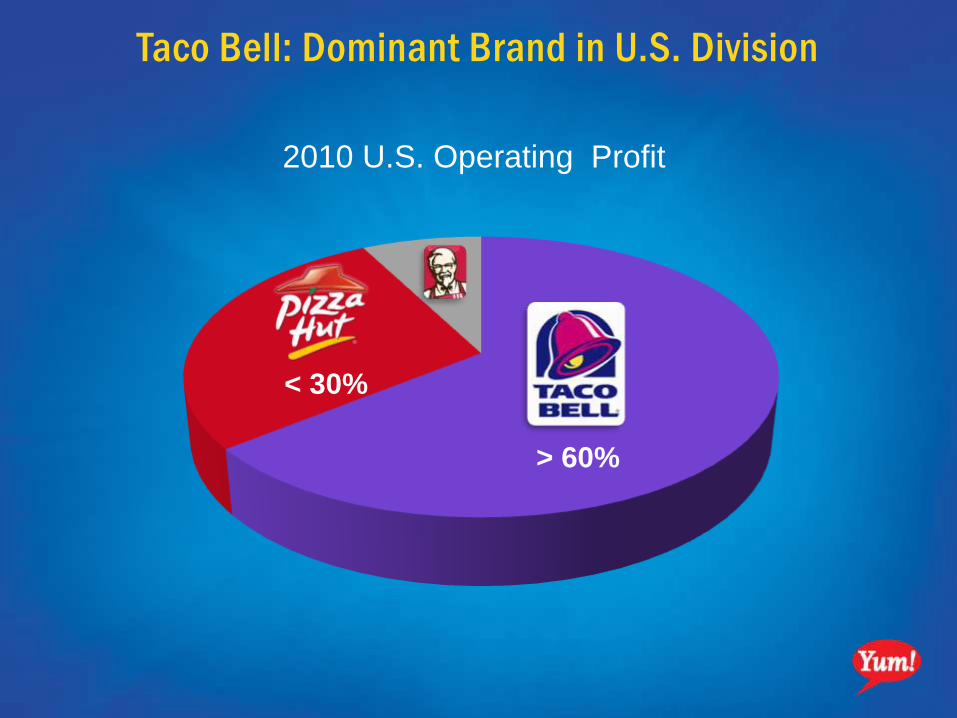

2010 U.S. Operating Profit

Taco Bell: Dominant Brand in U.S. Division

> 60%

< 30%

9:00 a.m. Yum! Welcome Tim Jerzyk SVP, IR

9:10 a.m. Brand Strategy Greg Creed CEO, Taco Bell

9:25 a.m. Marketing Overview David Ovens CMO, Taco Bell

10:00 a.m. Operations Overview Rob Savage COO, Taco Bell

10:35 a.m. Break

10:50 a.m. Development Overview Melissa Lora CFO, Taco Bell

11:30 a.m. Food Showing Liz Matthews Dir., Product Dev.

12:45 p.m. Closing Remarks Greg Creed CEO, Taco Bell

1:15 p.m. Q&A Taco Bell ET

1:30 p.m. Meeting Adjourns

Taco Bell Investor Day Agenda

BRAND OVERVIEWFebruary 17, 2011

GREGCREEDPresident & Chief Executive Officer

5,200+ Restaurants 5,600+ Points of Distribution

+$2B in Company/$5B in Franchise & License Sales

•#5 Market Share Brand

•2nd Most Profitable QSR Brand

1.5+ Billion Tacos and 1 Billion Burritos Every Year!

WHO WE ARE

OUR OPPORTUNITY8,000 Restaurants

#2 QSR Market Share

• Increased Restaurant Penetration

•Daypart Expansion—Breakfast

$10B in System Sales

BRAND STRATEGY HAS REMAINED CONSISTENT

Enablers: People & HWWT 2

Operations

World Class Ops

Assets

New Builds & Asset Remodels

Assets

BYA & New Sales Layers

Technology/Infrastructure

KEYS TO SUCCESSCompelling Product Innovation and

Capitalizing on Daypart Opportunities

Run Great Restaurants—Deliver a Great Experience Matching the Great Food

Seize the Development Opportunity and Refresh the Entire Asset Portfolio

DELIVER THE BRAND PROMISE!

Also Appeared In:San Francisco Chronicle • Montgomery Advertiser • Mobile Press

Anniston Star • San Diego Tribune • Birmingham News • Hoy (Chicago) La Opinion (Los Angeles) • El Diario La Prensa (New York)

DAVID OVENSChief Marketing Officer

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

-5%

0%

5%

10%

15%

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

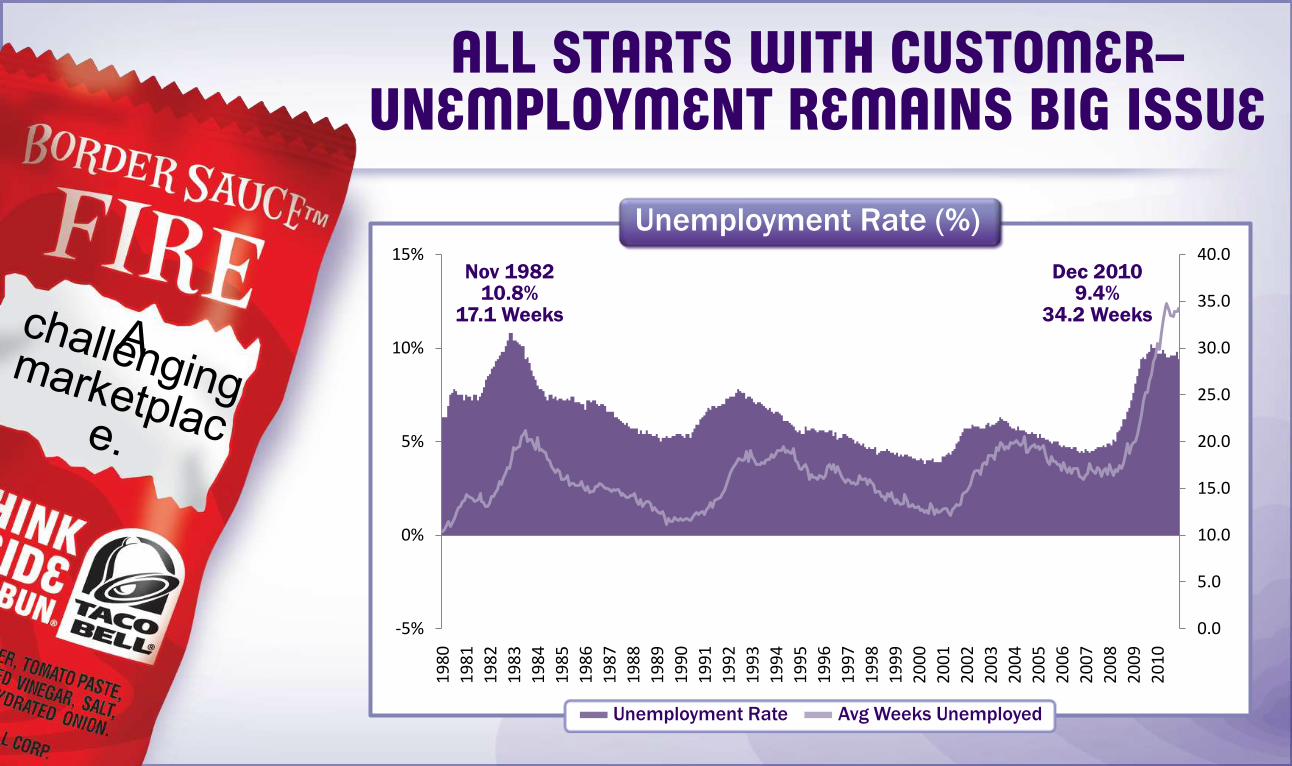

Nov 198210.8%

17.1 Weeks

ALL STARTS WITH CUSTOMER–UNEMPLOYMENT REMAINS BIG ISSUE

Unemployment Rate (%)

Unemployment Rate Avg Weeks Unemployed

Dec 20109.4%

34.2 Weeks

FINANCIAL CRISIS FORCED CONSUMERS TO RE-EVALUATE WHAT’S IMPORTANT

Went from “I Want It All”

To “What‟s Most Important to Me?”

Trading Up

Exuberance

Bullish

Accumulation

Responsibility

Vigilance

Resourceful

Prioritization

QSR TRAFFIC RECOVERINGQSR Traffic

(% Change vs. Year Ago)

-1.1%

1.0%

-2.4%

-1.7%

-0.6%

-2.7%

-0.2%

2.2%

0.8%

-3.7%

0.8%0.3%

1.5%

0.1%0.7%

Q2 ’10

Q1 ’07

Q2 ’07

Q3 ’07

Q4 ’07

Q1 ’08

Q2 ’08

Q3 ’08

Q4 ’08

Q1 ’09

Q2 ’09

Q4 ’09

Q1 ’10

Q3 ’09

Q3 ’10

DRIVING TRAFFIC WITH WHY PAY MORE! & PRODUCT INNOVATION

2008/09 20112010

TB Traffic Growth vs. QSR (2008–2010)

-1.1%

-2.4%

-1.7%

-0.6%

-2.7%

-0.2%

-3.7%

0.8%0.3%

1.5%

0.7%

TB TRAFFIC GROWTH OUTPACING QSRQSR

TB

Q2 ’10

Q2 ’08

Q3 ’08

Q4 ’08

Q1 ’09

Q2 ’09

Q4 ’09

Q1 ’10

Q3 ’09

Q3 ’10

Q4 ’10

Q1 ’08

VALUE LEADERSHIP STRENGTH

6.0

6.5

7.0

7.5

8.0

Q4'08 Q1'09 Q2'09 Q3'09 Q4'09 Q1'10 Q2'10 Q3'10

Value for Money

5.0

5.5

6.0

6.5

7.0

7.5

8.0

Q4'08 Q1'09 Q2'09 Q3'09 Q4'09 Q1'10 Q2'10 Q3'10

Low Prices

CHANGED VALUE MEAL PARADIGM &BUILT NEW CHECK OPPORTUNITY

6.0

6.5

7.0

7.5

8.0

Q4'08 Q1'09 Q2'09 Q3'09 Q4'09 Q1'10 Q2'10 Q3'10

Value for Money

VFM COMPLEMENTED BY ABUNDANCEAmount of

Food for Money

6.0

6.5

7.0

7.5

8.0

EXECUTION OF HIGH/LOW STRATEGY ENABLING BALANCED SALES GROWTH

Total SSS Growth (2010)

5%

4%

3%

2%

1%

0%

-1%

-2%

-3%

-4%

Q2 ’10 Q3 ’10 Q4 ’10

Trans

Check

Q1 ’10

-4%

2%

-1% 0%

3%2%

3%

1%

CORE BRAND GROWTH DRIVEN BY CAPABILITY IN INNOVATION & VALUE

Mexican Inspired, Forms, Flavors and Proteins

Not Just Low Prices,Priced to Make Value Matter

Proprietary, One-of-a-Kind Products

CraveableTastes

PioneeringValue

ProductInnovation

DRIVE PIPELINE INNOVATION ACROSS BIGGEST NEEDS!

CraveableTastes

Product Innovation

AfternoonSnack

DinnerLunchAM SnackBk’fst

1.5

3.53.8

0.30.1

2.8

EveningSnack

BUILD NEW REASONS TO VISIT TACO BELL

TB Share of All Restaurant Meals by Daypart

All Meals

2.7

Beverages & Desserts

Expanded Dayparts

Balanced Options

Beverages

Branded Value & New Proteins

NEW SALES LAYERS WILL ACCELERATE GROWTH

FutureBackVision

BREAKFAST COMPETITIVE LANDSCAPE HAS CHANGED DRAMATICALLY

NOWQ2 2009

Breakfast Category Media Spend:

$41MMBreakfast %

of QSR Spend:

5%

Q1 2010

Breakfast Category Media Spend:

$54MMBreakfast %

of QSR Spend:

6%

Q2 2010

Breakfast Category Media Spend:

$100MMBreakfast %

of QSR Spend:

12%

FIRSTMEAL APPROACH SIMILAR TO LATE NIGHT

BUILD NEW REASONS TO VISIT TACO BELL

AfternoonSnack

DinnerLunchAM SnackBk’fst

1.5

3.53.8

0.30.1

2.8

EveningSnack

TB Share of All Restaurant Meals by Daypart

All Meals

2.7

OASIS: THE BEVERAGE &SNACKING STRATEGY

Refresh Refuel Reconnect

“All I get is a soda.”

“Lunch, Dinner or Late Night.”

“I’d rather eat in my car.”

FR

OM

TO

“It’s a Beverage

Destination.”

“Satisfying snacks for my

clocklesslifestyle.”

“I come to Taco Bell

as much for the

experience as the food.”

PRODUCTS ARE DELICIOUS...

Beverages Desserts

EXPERIENCE CHANGES PERCEPTIONS!

“I’d rather eat in my car”

Sit & Stay

Modular Furniture

Seating Options

Quality Lighting

SUMMARY Value leadership great in

current economy

Product innovation culture a strategic advantage to get beyond low prices

New sales layers are hard, but when done correctly, payoff will be huge

ROB SAVAGEChief Operating Officer

ACHIEVING STEP-CHANGE IN CUSTOMER RESULTS...

2008

91.93%

2009 2010

91.8%

89.0%

National CBCC RAF

2008

.12

2009 2010

.13

.17

PRC Overall Complaint Contact/1K Trans

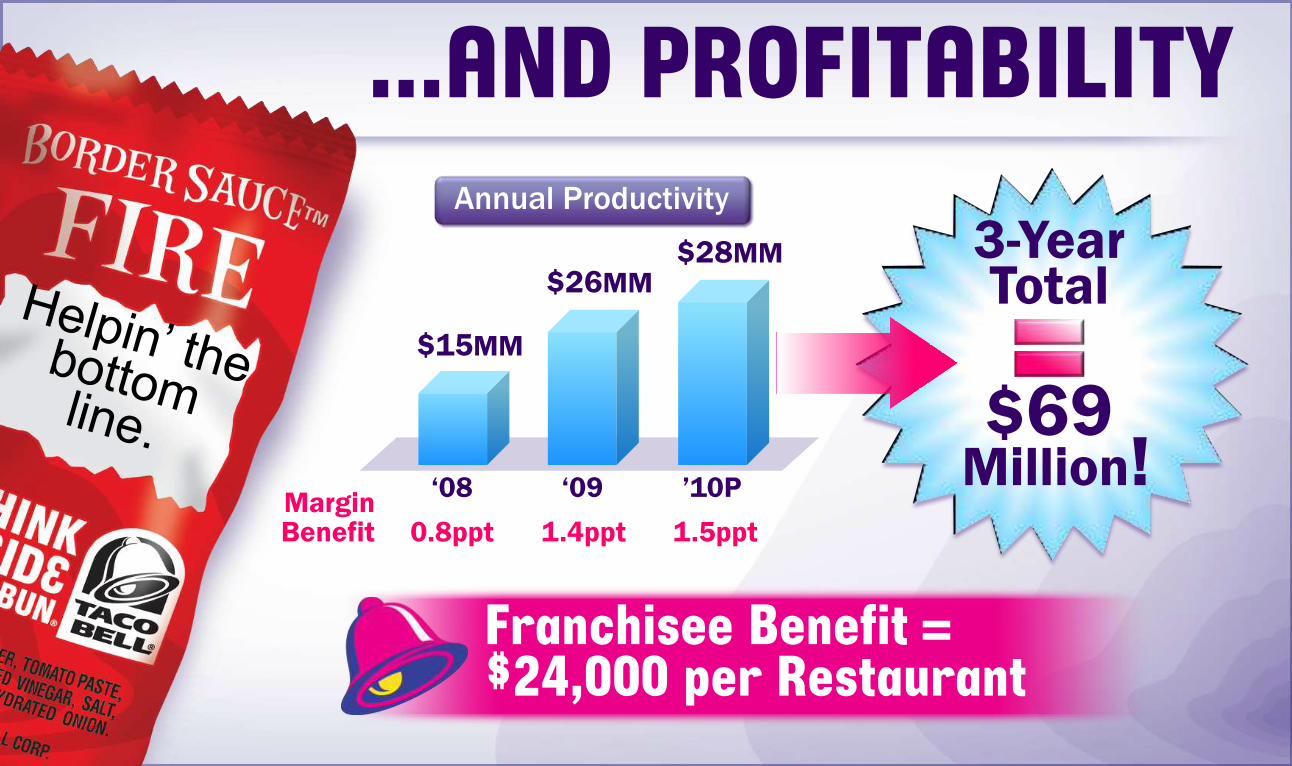

3-Year Total

$69Million!

...AND PROFITABILITY

„08

$28MM

„09 ‟10P

$26MM

$15MM

Annual Productivity

MarginBenefit 0.8ppt 1.4ppt 1.5ppt

Franchisee Benefit =$24,000 per Restaurant

Our Opportunity is to Go from Good to GREAT!

COMMITMENT TO BE THE BEST

Work Eat OwnFamilies/High

Performance TeamsReliable/

Best on BlockReturns/

Growth Mindset

BEST PLACE TO WORK

Processes Infrastructure/Technology

Improved Rest-Level TrainingGreater EE/Mgr Capability

Behavior-Based Evaluation Tools“How” and “What”=

Consistency & Culture

Bring Brand to LifeLive Purple

Implementation of E-Learning“Learning Zone”

Internet-Based PortalsReal-Time Communication

Dashboards for Daily PerformancePerformance Tracking

Internal Maintenance TeamOperators Focus on the Customer

Certified Best PracticesService Improvement Guide

Menu OptimizationEliminate “One-Offs”/

Drives Consistency

Improved AccuracyProduct Delivery System

Improved SpeedBottleneck Management

Processes Infrastructure/Technology

BEST PLACE TO EAT

Processes Infrastructure/Technology

Enhanced RSC SupportDedicated Ops & Financial

Stewardship

Ongoing Productivity InitiativesTarget .5% Annually

Insight-Based ReportingDrive Sales/Profit

Inventory ManagementReduced Time/Optimized Capacity

Daily Business SummaryFinger-tip Performance Analysis

Internal Maintenance TeamReduced Repair Costs/

Longer Life-Cycle

BEST PLACE TO OWN

World-Class Ops

WORLD-CLASS OPERATIONS AS A CATALYST

MELISSA LORAChiefFinancialOfficer

Build More Upgrade Existing Portfolio

ASSET STRATEGY IS SIMPLE

STEADY NEW UNIT DEVELOPMENT

System New Units

2009

102

115–125

88

2010 2011

Net New % 0.8% 0.6% 1.2%

2 PRIMARY TACTICS TO ACCELERATE GROWTH

FlexibilityFocus

8,000 8,000

FOCUS ON QUALITY TRADE AREAS & SMART MARKET PLANNING

Quality Number

A

B

C

D

220

693

927

483

An Excellent Site/Big Box Retail/Daily Consumer Needs

Strong Area/Major Generator Moving In/ Other Retailers Present

Fewer Generators/Growth Anticipated

No Opportunity for Next Five Years

913

INLINE DESIGN WILL PROVIDE FLEXIBILITY

Quality Opportunity

Rural 1,100Less Populated Areas

More Brand Design Less Design Flexibility

REFRESH/REMODEL ACCELERATING

2007

316

2008 2009

194126

390371

2010 2011

System AssetUpgrades

Asset Strategy–YE 2008

Bold27%

AllOther

Asset Strategy–YE 2011

Bold54%

AllOther

OPTIONS ENABLE ACCELERATION

Full Replacement

Next 2 Ten

Baby Bold

Flex 2 Five

OPTIONS ENABLE ACCELERATION

Flex 2 Five

OPTIONS ENABLE ACCELERATION

Next 2 Ten

OPTIONS ENABLE ACCELERATION

Baby Bold

OPTIONS ENABLE ACCELERATION

Full Replacement

OPTIONS ENABLE ACCELERATION

OLD NEW

Refresh

REFRESH BRINGS CONTINUITY TO LOOK & FOUNDATION FOR BRAND

OCB

Menuboards

POS

Certified Broadband

PaintSignage

SUMMARYDoubling Net

New Unit Growth• Free Standing and Inline

520 Total Asset Actions• Remodels = 398

Refresh Look and Foundation for Ops by June 2013

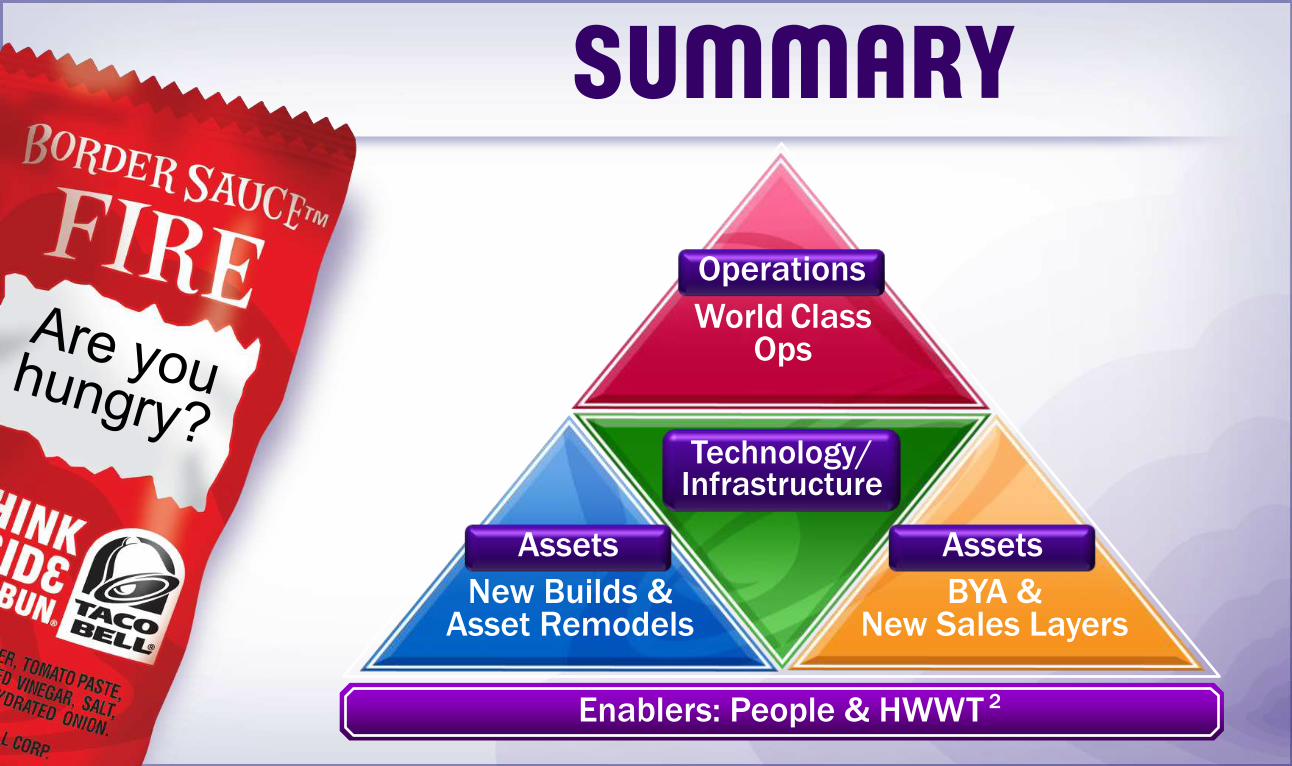

SUMMARY

Enablers: People & HWWT 2

Operations

World Class Ops

Assets

New Builds & Asset Remodels

Assets

BYA & New Sales Layers

Technology/Infrastructure

BRAND OVERVIEWFebruary 17, 2011